On behalf of the Resource Allocation Task Force (RATF), I am pleased to forward you our final report. Your charge to the RATF was:

|

|

|

- Randolph Pearson

- 6 years ago

- Views:

Transcription

, I am pleased to")

1 To: Dr. Rodolfo Arévalo, President From: Rex Fuller, Dean and Task Force Chair Date: May 21, 2008 Re: Resource Allocation Task Force On behalf of the Resource Allocation Task Force (RATF), I am pleased to forward you our final report. Your charge to the RATF was: to assess and develop a zero-based or modified zero-based resource allocation model to determine a process by which Eastern s resources will be allocated. The RATF spent the bulk of fall and winter quarter reviewing budget models and from those deliberations developed a modified zero-based approach. The RATF has held campus-wide meetings and vetted its work in coming to this final report. The Task Force recommends that Business and Finance develop templates to support the budgeting process. A noted in the report, we are also recommending that the RATF reconvene at a future date to review the implementation of the model if it is adopted by the campus. The RATF is unanimous in recommending the final report to you for final consideration. However, if you have questions, the Task Force is more than willing to meet with you. We look forward to seeing this recommendation implemented. College of Business and Public Administration Office of the Dean N. 668 Riverpoint Blvd., Suite A, Room 310 Spokane, WA fax: Eastern Washington University is committed to equal opportunity and affirmative action in employment.

2 Resource Allocation Task Force Final Report May 21, 2008 Barbara Alvin Jane Button Bob Campbell Rex Fuller (Chair) Ann Le Bar Trudy Miller Annette Skaer Mary Jo Van Bemmel Mary Voves, Ex Officio Bob Zinke

3 Introduction The budgeting process at EWU is designed to give the University the ability to meet changing institutional needs, while supporting its historical mission. The budget should be strongly linked to the University s Strategic Plan. In the past EWU s budget process has been largely incremental with some limited funding tied to strategic initiatives and enrollment. While this approach may have served the University well in times of increasing enrollments, it does not allow for sufficient flexibility in times of stable or declining enrollments. The University will be facing increased competition for enrollment in the coming years. In such an environment, the campus must develop a resource allocation process that enables it to reallocate funds to support expanded and new initiatives. Resource Allocation Task Force In this environment, President Arévalo appointed the Resource Allocation Task Force to develop an allocation model that will assist EWU in managing its financial resources in an increasingly competitive higher education environment. Specifically, President Arévalo charged the task force as follows: The charge of the Resource Allocation Task Force is to assess and develop a zero-based or modified zero-based resource allocation model to determine a process by which Eastern s resources will be allocated. As its initial step the Resource Allocation Task Force (RATF) reviewed selected articles that addressed varying approaches to the budgeting process. In addition, the Presidents Executive Committee was also considering these issues. After review and consideration of the various approaches, the RATF determined that a modified zero-based model would best serve the University. The principal advantages of this approach are: 1) it allows for reallocation of funding to support key initiatives, both new and continuing, 2) it curbs mission creep by re-evaluating past budgeting commitments and requires justification of spending in accord with the University Strategic Plan, and 3) finally it is responsive to changing circumstances. Most important, the approach allows for a direct link between budgeting and the Strategic Plan. The modified ZBB provides for campus and community input by: Reviewing University Strategic Plan and key initiatives with campus community Identify funding priorities for policy based funding Establishing and communicating timelines for budget process Providing a consistent approach for making budgeting proposals Establishing budget priorities that can be vetted by the University Budget Committee, Cabinet and Board of Trustees University Budget Committee The University Budget Committee is an advisory group consisting of representation from faculty, classified staff, exempt staff, students and administrators. This body is advisory to the President and all members shall be appointed by the President based on recommendations from appropriate constituencies. The UBC shall work with the President to establish priority funding recommendations based on the University s Strategic Plan. The Budget Committee will review new budget proposals. 1

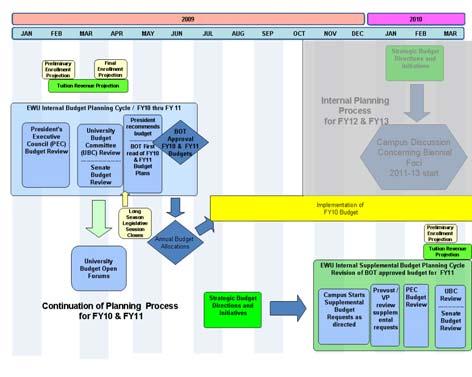

4 In time of budget reversions the committee will review budget reduction plans. In addition, the committee will participate in the development of the University funding initiatives which are submitted biennially to Olympia. Committee members are expected to represent their constituencies while applying a university wide perspective to the budget deliberations and recommendations. The committee will be chaired by the VP for Business who will have no voting rights. The Budget office will staff the committee and maintain minutes and official records of actions. The Budget Committee will meet once monthly throughout the year. Voting members of the UBC will serve two year terms. They will be rotating terms: one half of the committee membership rotates each year to allow for experience and continuity. Voting membership: Three faculty members nominated by the faculty senate One classified staff member One student representative One dean One representative from the exempt staff One representative from each of the VP areas One representative from Athletics The committee is chaired by the VP for Business who will have no voting rights. Each dean or division head prepares the necessary planning forms to submit to the VP of the appropriate division for consideration through the divisional budget process. Budget proposals are then forwarded to the University Budget Committee. The UBC holds hearings in which the units may justify their proposals. These hearings are open to the campus community. The UBC makes a preliminary recommendation to the President. Budget Process Eastern s external state budget process is a two year (biennial) process. Eastern will submit its biennial operating budget request (for FY10 & FY11) to Olympia in September This budget request is used by the Office of Financial Management to prepare the Governor s budget proposal to be released in December The Legislature will prepare a final budget during the 2009 legislative session. The final legislative budget will be signed by the Governor about mid-april Basic Process for Resource Allocation Eastern s internal strategic budget planning process coincides with the external biennial budget cycle. For example, the internal strategic budget planning process for biennium (i.e., FY10 and FY 11) began in January The internal budget planning calendar for FY10 and FY11 follows: January thru May 2008 University strategic budget directions and initiatives are discussed campus-wide to determine foci for planning FY10 and FY11. 2

5 June 2008 University budget priorities are discussed with the Board of Trustees (BOT) at the June retreat. Clear written funding priorities and goals for FY10 & FY11 are established by the President after the BOT retreat. July and August 2008 University funding goals established and shared, discussed, applied and clarified with university leadership at the Cabinet retreat. September and October 2008 Divisional budget development process. Each division holds meetings to discuss and plan FY10 and FY11 budget proposals. Divisional budget development processes may vary from simple to complex depending on the needs of the unit. Steps: Based on the Strategic Plan, funding goals and priorities and specific budget instructions for the biennium are normally distributed to the campus community no later than September. Each unit prepares two budget proposals: Stable Funding includes funding level costs for core functions, and Either Enhanced Funding includes funding level costs for basic services, and additions for enhanced services/programs to constituents. Or Decreased Funding includes funding level costs for reduced core services. (See, Appendix B for a description of stable, enhanced and decreased levels) Each budget proposal for each unit should include: a brief narrative description and justification for the budget proposals how the budget proposals support the University Strategic Plan goals the impact of no or partial funding the tie to key performance indicators and University accountability measures a proposed assessment plan Budget proposals are submitted to the appropriate VP no later than November. All divisional budget proposals must include a brief narrative description and justification, a tie to the University Strategic Plan, the impact of no or partial funding, and a proposed assessment plan. November and December 2008 Provost and Vice Presidential budget development process. Each executive level holds meetings to discuss and plan FY10 and FY11 budget proposals. Executive budget development processes may vary from simple to complex depending on the needs of the unit. All executive budget proposals must include a brief narrative description and justification, a tie to the University Strategic Plan, the impact of no or partial funding, and a proposed assessment plan. Steps: The Provost or VP reviews budget proposals within their unit and schedules forums within their unit to share and discuss the budget proposals. The Provost or VP prepares separate executive budget proposals: Each unit prepares two budget proposals Stable Funding includes funding level costs for core functions, and Either Enhanced Funding includes funding level costs for basic services, and additions for enhanced services/programs to constituents. Or Decreased Funding includes funding level costs for reduced core services. 3

6 Budget proposals for each unit should include: a brief narrative description and justification for the budget proposals how the budget proposals support the University Strategic Plan the impact of no or partial funding the tie to key performance indicators and University accountability measures a proposed assessment plan The Provost or VP communicates final executive budget proposal with all units. Budget proposals are submitted to the budget office in early January. January thru March 2009 President s Executive Council (PEC) review of executive budget proposals for FY10 and FY11. Preliminary tuition revenue projections for FY10 and FY11 (based on enrollment projections provided by Student Affairs) are provided by Business & Finance after Winter Quarter 10 th day. March and April 2009 The University Budget Committee (UBC) reviews and comments on executive level budget proposals. Late April The President, in consultation with the UBC and executive staff, makes budget allocation decisions for FY10 and FY11 using university strategic goals and priorities. Final tuition revenue projections for FY10 and FY11 (based on enrollment projections provided by Student Affairs) are provided by Business & Finance after Spring Quarter 10 th day. May 2009 First read of FY10 and FY11 budgets to Board of Trustees June 2009 Second read of FY10 and FY11 budgets and Board of Trustee approval biennial budgets are authorized and appropriated. July 2009 Strategic budget plans are implemented for FY10. Budgets are distributed to units and the new fiscal year begins. August 2009 Beginning of FY11 supplemental budget process. Priorities for supplemental budget proposals are discussed at Cabinet retreat November and December 2009 Campus begins preparation of FY11 supplemental budget revision proposals as directed by the president. January 2010 Provost and Vice Presidents review of FY11 supplemental proposals. Preliminary adjustment to tuition revenue budget for FY11 (based on enrollment projections provided by Student Affairs) are provided by Business & Finance after Winter Quarter 10 th day. Strategic budget planning cycle for begins February 2010 President s Executive Council review of FY11 supplemental proposals. March 2010 University Budget Committee review of FY11 supplemental proposals. 4

7 April The President, in consultation with the University Budget Committee and executive team, makes FY11 supplemental budget allocation decisions using university strategic goals and priorities. Final adjusted tuition revenue budget for FY11 (based on enrollment projections provided by Student Affairs) are provided by Business & Finance after Spring Quarter 10 th day. May 2010 First read of supplemental FY11 budget to Board of Trustees June 2010 Second read of supplemental FY11 budget and Board of Trustee approval. July 2010 Budgets are implemented for FY11. Budgets are distributed to units and the new fiscal year begins. August 2011 Biennial budget outcome assessment reports are submitted to the University Budget Committee and the President by the Provost and VPs comparing funding allocation with actual spending, outcome and assessment measures and executive level progress on Strategic Plan goals. Final reports will be posted to the university website and made widely available to the campus community. This accountability step is in accord with the intent of new legislation concerning accountability in higher education, which established a performance agreement for public higher education institutions. As noted in the legislation: Summary The goals and outcomes identified in a performance agreement shall be linked to the role, mission, and strategic plan of the institution of higher education and aligned with the statewide strategic master plan for higher education. (EHB 2641, Higher Education Performance Agreements, p. 3) The new allocation process described above differs in one fundamental way from the University s earlier model. The prior model did not address base budgets and assumed that base budgets would continue. The focus of the model was on meeting new enrollment demand (i.e., increased FTES over a rolling 3-year average), identification of policy dollars, and a University reserve. Such a model can be considered as a blend of formula driven budgeting and incremental budgeting. This approach worked well in periods of relatively predictable enrollment growth. However, in periods of steady enrollment, declining enrollment, and/or enrollment variations by program, a different approach is needed to allow for resources to move to the highest and best use for the University. The zero-based budget approach described above is designed to enable the University to align its funding decisions with its Strategic Plan s goals. By engaging a two-year process, reallocation decisions can be made in a manner that enables units to plan accordingly. Moreover, this approach will provide greater opportunities to enhance selected activities. The earlier model noted that a portion of the budget will be committed to fostering strategic initiatives, innovations and entrepreneurial activities that are directly related to the Strategic Plan of the University. Zero-based-budgeting affords the University more opportunity to accomplish this objective. The Task Force held as series of meetings with the campus concerning this proposal. These included: Cabinet, BOT Finance Committee, Senate Rules Committee, Senate, and three open 5

8 forums. At these meetings, the proposal was generally met with favorable comments; however, several open issues were identified. One matter concerned the need to utilize the work of the campus in identifying key performance indicators. The Task Force recommends that the earlier work be used as a foundation in establishing the performance indicators that should be used in the model. More importantly, the Task Force wants to stress the need to create a stronger linkage between the strategic planning process and budgeting. It is evident that the linkage will be crucial in determining the model s success. In conclusion, the success of the model will depend, to a large degree, on the degree to which the budgeting process allows for campus-wide dialog and participation. For this reason, the Task Force strongly recommends that the President, faculty leadership and staff leadership encourage participation in the process. In addition, the Task Force recommends that it reconvene to review the model after its first year of implementation. We recognize the complex nature of budgeting and understand that we may need to adapt the model as we engage in the process. 6

9 Appendix A Summary of zero-based budgeting as described by the Chartered Institute of Public Finance and Accounting, Zero Based Budgeting, zero-based budgeting (ZBB) consists of several steps or stages: Stage 1 Defining the Scope of ZBB Decide which parts of the organization are to be assessed using ZBB. For complex, multifunction organizations, it may be helpful to pilot the approach in a few areas where activities are closely aligned to organizational structure. It is essential that the activities to be assessed have clearly defined objectives, and wherever possible, measurable outputs and outcomes. Stage 2 Identify the resources This stage falls into 2 parts: The identification of the schedule of input resources that will be required in order to deliver the outputs The identification of the individuals who will take responsibility for assessing the various options. Stage 3 Objective matching stage It is possible that objectives may be deliverable at different service levels, and in these cases, the review should identify, as a minimum: Basic level of service (usually, in a public sector context, that which is required to meet statutory duties) Current level of service Any step changes in service Options for delivering each level may differ and will need to be identified. Clearly, it is essential to be able to analyze costs between fixed and variable elements. The outcome of these stages is a set of competing proposals that needs to be refined into the final decision items. This refining process involves evaluating the proposals and establishing priorities. Ranking the Decision Packages The decision packages should be evaluated and ranked in order of importance. Performance measurement tools including cost/benefit analysis are clearly a very important component, but it is also appropriate to apply a level of subjectivity. This is because few activities are capable of reduction to a manageable number of measures, while some ideal measures may not be practical because of difficulties in real world application, or simply because of the costs of data collection. For example, managers may believe that there would be a feelgood factor in taking a particular course of action. This could never be accurately quantified. Allocating resources The ranking list then results in a priority order for the allocation of resources. The most important activities are funded, whether they are existing ones, or new. The final budget will be made up of the decision packages that have been approved for funding, reallocated into the appropriate operational units. 7

10 Appendix B Stable Budget Proposal 1. Description and justification for the proposal. 2. How does this proposal support the University Strategic Plan s goals? Does the benefit warrant the program expenditures? Can the benefits be measured? If so, how? 3. What would happen if this was not funded? Who would be impacted? What would happen if this program were expanded? 4. How does this proposal contribute to improvement of the key performance indicators and university accountability measures? 5. What is the assessment plan for this proposal? What will be measured and how will that measure indicate success? Enhanced Budget Proposal 1. Description and justification for the proposal. 2. How does this proposal support the University Strategic Plan s goals? Does the benefit warrant the program expenditures? Can the benefits be measured? If so, how? 3. What would happen if this proposal was not funded? Who would be impacted? What would happen if this program were expanded? 4. How does this proposal contribute to improvement of the key performance indicators and university accountability measures? 5. What is the assessment plan for this proposal? What will be measured and how will that measure indicate success? Decreased Budget Proposal 1. Description of impact of decreased funding. 2. How will this impact achieving the University Strategic Plan s goals? Will the decreased funding yield meaningful financial gains? 3. How will this impact achievement of key performance indicators and university accountability measures? 8

11 Appendix C Glossary Budget Proposals: Stable a proposal that utilizes existing budget authority to achieve a unit s goals Decreased a proposal that utilizes less budget authority Enhanced a proposal that utilizes greater budget authority to enhance services and/or develop new initiatives Fiscal Years: FY10 refers to fiscal year , which begins July 1, 2009 and ends June 30, Supplemental Budget: refers to the second year budget of each biennium and the legislative process. For example, the Supplemental Budget for the biennium is the budget for The supplemental budget allows changes to funds allocated in the original capital, operating, or transportation budgets. 9

12 Appendix D The University Budget Committee The University Budget Committee is an advisory group consisting of representation from faculty, classified staff, exempt staff, students and administrators. This body is advisory to the President and all members shall be appointed by the President based on recommendations from appropriate constituencies. The UBC shall work with the President to establish priority funding recommendations based on the university s strategic plan. The Budget Committee will review new budget proposals. In time of budget reversions the committee will review budget reduction plans. In addition, the committee will participate in the development of the University funding initiatives which are submitted biennially to Olympia. Committee members are expected to represent their constituencies while applying a university wide perspective to the budget deliberations and recommendations. The committee will be chaired by the VP for Business who will have no voting rights. The Budget office will staff the committee and maintain minutes and official records of actions. The Budget Committee will meet once monthly throughout the year. Voting members of the UBC will serve two year terms. They will be rotating terms: one half of the committee membership rotates each year to allow for experience and continuity. Voting membership: Three faculty members nominated by the faculty senate One classified staff member One student representative One dean One representative from the exempt staff One representative from each of the VP areas One representative from Athletics Each dean or division head prepares the necessary planning forms to submit to the VP of the appropriate division for consideration through the divisional budget process. Budget proposals are then forwarded to the University Budget Committee. The UBC holds hearings in which the units may justify their proposals. These hearings are open to the campus community. The UBC makes a preliminary recommendation to the President. Final allocations are made after consultation with the BOT. 10

13 Frequently Asked Questions: o What are the university divisions? President (including Athletics) Academic Affairs Business and Finance Student Affairs Advancement Information Resources Appendix E RATF Campus Budget Forums Notes o o o What funding sources does the proposed budget model include? Initially Ledger 1 only (state appropriations and tuition revenues); however, it is the goal to include all funding sources in the future What is the difference between basic and core funding levels? They are the same. The task force used them interchangeably while drafting the proposal. It is the minimum funding level required by a department or unit to fulfill its mission. Is there a web site for feedback and/or additional questions? Contact Rex Fuller at rfuller@mail.ewu.edu or any of the committee members. Noteworthy Points During all Presentations: o The RATF proposal is a budgeting framework and not a rigid model. The framework will be tested, evaluated, and refined as we use it. o The Delaware Study will be used as a starting point in Academic Affairs to get a sense of where departments are in terms of enrollment. Declines in enrollment don t necessarily indicate that funding should be reduced; they may indicate that additional funding is needed. May 5, :00-2:30 Cheney: o Attendance: 18 (excluding executives (Dr. Arevalo and Dr. Mason attended) and RATF committee members) Questions and Responses: o From a faculty member in Engineering and Design: Can you give us examples of core functions? Rex Fuller: These are the absolute needs we must have to meet our missions. The enhanced service level is beyond the core function level. o o From a faculty member: What is the impact of reduced funding? Rex Fuller: Which of all of our functions could we give up? It involves discussions with those closest to the functions. From a faculty member: How can overlap between funding sources be accommodated? Rex Fuller: It is up to the individual units to determine the best use of all funding sources. 11

14 o From a faculty member in Music: She was interested in the enrollment and revenue projections and if departmental funding would be available for recruitment and retention. Rex Fuller: There has been funding this year for recruitment and retention. Dr. Mason: The Delaware Study will provide Eastern with comparative peer data on enrollment and funding levels by department. This will be a starting point for Academic Affairs discussions. The workload adjustment is a starting point; a decline in enrollment might signal the need for additional funding in a unit rather than reduced funding based upon the old RAM model. Rex Fuller: The old RAM model didn t tie back to national norms. Bob Zinke: The proposed budgeting framework is more systematic. May 6, :00-2:30 Cheney: o Attendance: 31 (excluding RATF members) Questions and Responses: o From Julie Thayer: What is different about the proposed model from the old model? Rex Fuller: The new model includes a complete review of budget authority in the biennial year and is modified zero based. It is not entirely enrollment driven as was the RAM model. The new model allows for balancing inequities and re-basing if necessary. The new model works in an environment without enrollment growth and allows for base reauthorization. o o From a faculty member: What would the narrative (stable, enhanced, decreased) look like? Rex Fuller: Everything should come forward with a unified look. From the same faculty member: What is the focus of the assessment? Rex Fuller: It will be different for each unit; there are imposed goal/assessments from the state, and KPIs will be incorporated. From Judd Case: How do we deal with growth? Rex Fuller: The Delaware Study will be a tool that helps to identify norms for comparative analysis. The model doesn t automatically redirect funding to units that are growing; however, it could redirect funding to growing units. The model allows flexibility for value based funding. The old RAM model didn t use norm comparison and automatically redirected funding to growing units and away from declining units. May 6, :30-5:00 Riverpoint: o Attendance: 6 (excluding RATF members) Questions and Responses: o From a staff member: What are the changes that we anticipating? Which data is used for the enrollment projections? Rex Fuller: We are using state and national demographic data that indicates that college enrollments will most likely continue to decline. We are past the growth stages that occurred during the last decade, and we have to strategically position the university for changes in enrollment and in the economy. o From Don Fuller of the Communications Disorders department: How will the model impact accreditation? Rex Fuller: The model will help to determine the desired cost for programs, and decisions will have to be made. Don: If a program is stable but not growing, would it be able to receive increased funding? (The Communications Disorders department is not growing due to the fact that they are unable to place additional students into practicums because the Spokane market is saturated). Rex Fuller: Programs should not grow just for growths sake. A program can remain stable and still receive additional 12

15 funding. Enrollment is just one piece of the review. It s difficult to move significant funding from one unit to another; however, the model systematically addresses this issue. o o Bob Zinke: In the current system, everything is invisible. The proposed process has decision points that are open. Transparency is very important because when the process is more open to the public, the legislature, and other constituencies they can see the affects of reduced funding to the institution. Rex Fuller: Budget alignment will make EWU budget presentations more competitive. The return on the investment of public dollars will be more apparent for dollars appropriated to Eastern than for other institutions that haven t strategically aligned their budget requests. 13

16 Eastern Washington University Proposed Biennial Budgeting Process for Fiscal Years 2010 and

17 Resource Allocation Task Force Members Barbara Alvin Faculty Jane Button Business & Finance Bob Campbell Student Affairs Rex Fuller (Chair) Ann Le Bar Faculty Trudy Miller Advancement Annette Skaer Academic Affairs Mary Jo Van Bemmel Classified Staff Mary Voves (Ex Officio) Bob Zinke Faculty 2

18 Resource Allocation Task Force Charge The charge of the Resource Allocation Task Force is to assess and develop a zero-based or modified zero-based resource allocation model to determine a process by which Eastern s resources will be allocated. 3

19 Recommended Biennial Budgeting Process Modified zero based strategic budgeting Designed to meet changing needs Linked to University Strategic Plan Enables reallocation to support expanded and new initiatives 4

20 Budgeting Principles Transparent Flexible Accountable Responsive Systematic 5

21 Biennial Budgeting Process Overview Proposed internal budget planning for FY10 and FY11: Budget planning process begins in early 2008 to allow for complete participation from all constituent groups Board of Trustee approval of biennial budgets in June 2009 Implementation of approved budgets from July 2009 through June 2011 The budgeting process ends with outcome assessment reports completed in August

22 7 Biennial & Annual Budget Timeline

23 8 Overview of Two Year Cycle

24 Budgeting Timeline Detail Planning January thru May 2008 University strategic budget directions and initiatives are discussed campuswide to determine foci for planning FY10 and FY11. 9

25 Budgeting Timeline Detail Priorities and Goals June 2008 University budget priorities are discussed with the Board of Trustees (BOT) at the June retreat. Clear written funding priorities and goals for FY10 & FY11 are established by the President after the BOT retreat. 10

26 Budgeting Timeline Detail Priorities and Goals July and August 2008 University funding goals established and shared, discussed, applied and clarified with university leadership at the Cabinet retreat. 11

27 12 DIVISIONAL BUDGET PROCESS

28 Divisional Budget Development September and October 2008 Divisional budget development process. Each division holds forums to discuss and plan FY10 and FY11 budget proposals. Divisional budget development processes may vary from simple to complex depending on the needs of the unit. 13

29 Divisional Budget Development All divisional budget proposals must include a brief narrative description and justification, a tie to the University Strategic Plan s goals, the impact of no or partial funding, and a proposed assessment plan. 14

30 Divisional Budget Development Steps: Based on the Strategic Plan, funding goals and priorities for the following biennium are distributed to the campus community no later than early September. Specific budget instructions for the following biennium are distributed to all units in early September. Budget instructions may require budget reductions. Each unit prepares two budget proposals: Stable Funding includes funding level costs for core functions, and Either Enhanced Funding includes funding level costs for core services, and additions for enhanced services/programs to constituents. Or Decreased Funding includes funding level costs for reduced core services. 15

31 Divisional Budget Development Budget proposals for each unit should include: a brief narrative description and justification for the proposals how the budget proposals support the University Strategic Plan s goals the impact of no or partial funding the tie to key performance indicators and University accountability measures a proposed assessment plan Budget proposals are submitted by early November. 16

32 17 EXECUTIVE LEVEL BUDGET PROCESS

33 Executive Level Budget Development November and December 2008 Provost and Vice Presidential budget development process. Each executive level holds forums to discuss and plan FY10 and FY11 budget proposals. Executive budget development processes may vary from simple to complex depending on the needs of the unit. 18

34 Executive Level Budget Development All executive budget proposals must include a brief narrative description and justification, a tie to the University s Strategic Plan s goals, the impact of no or partial funding, and a proposed assessment plan. 19

35 Executive Level Budget Development Steps: The Provost or VP reviews budget proposals within their unit and schedules forums within their unit to share and discuss the proposals. The Provost or VP prepares two budget proposals: Stable Funding includes funding level costs for core functions, and Either Enhanced Funding includes funding level costs for core services, and additions for enhanced services/programs to constituents. Or Decreased Funding includes funding level costs for reduced core services. 20

36 Executive Level Budget Development Budget proposals for each unit should include: a brief narrative description and justification for the proposal how the budget proposals support the University s Strategic Plan s goals the impact of no or partial funding the tie to key performance indicators and University accountability measures a proposed assessment plan The Provost or VP communicates final executive budget proposals with all units. Budget proposals are submitted to the budget office in early January. 21

37 Executive Review January thru March 2009 President s Executive Council (PEC) reviews executive budget proposals for FY10 and FY11. Preliminary tuition revenue projections for FY10 and FY11 22

38 University Budget Committee & Campus Review March and April 2009 The University Budget Committee (UBC) reviews and comments on executive level budget proposals. UBC presents to Faculty Senate and holds open campus forums. 23

39 University Budget Committee The University Budget Committee is an advisory group consisting of representation from faculty, classified staff, exempt staff, students and administrators. This body is advisory to the President and all members shall be appointed by the President based on recommendations from appropriate constituencies. The UBC shall work with the President to establish priority funding recommendations based on the University s Strategic Plan. 24

40 University Budget Committee Voting membership: Three faculty members nominated by the faculty senate One classified staff member One student representative One dean One representative from the exempt staff One representative from each of the VP areas One representative from Athletics The committee will be chaired by the VP for Business (ex officio) 25

41 Budgeting Timeline Detail Final Budget Recommendations Late April The President, in consultation with the University Budget Committee and executive staff, makes budget allocation decisions for FY10 and FY11 using university strategic goals and priorities. Final tuition revenue projections for FY10 and FY11. 26

42 Budgeting Timeline Detail Board of Trustees Approval May2009 First read of FY10 and FY11 budgets to Board of Trustees June 2009 Second read of FY10 and FY11 budgets and Board of Trustee approval. Budgets are authorized and appropriated. 27

43 28 Supplemental Budget

44 Budgeting Timeline Detail Implementation for FY10 and Supplemental Process July 2009 Strategic budget plans are implemented for FY10. August 2009 Beginning of FY11 supplemental budget process. Priorities for supplemental budget proposals are discussed at Cabinet retreat. 29

45 Budgeting Timeline Detail Campus Supplemental Budget Request November and December 2009 Campus begins preparation of FY11 supplemental budget revision proposals as directed by the President. 30

46 Budgeting Timeline Detail Supplemental Executive Review January 2010 Provost and Vice Presidents review divisional FY11 supplemental proposals. Preliminary adjustment to tuition revenue budget for FY11 Note: Strategic budget planning cycle for FY12 & FY13 begins 31

47 Budgeting Timeline Detail Supplemental Executive Review February 2010 President s Executive Council review of FY11 supplemental proposals. 32

48 Budgeting Timeline Detail Supplemental UBC & Campus Review March 2010 University Budget Committee review of FY11 supplemental proposals. University Budget Committee presents to Faculty Senate and holds campus forums. 33

49 Budgeting Timeline Detail Final Supplemental Budget Recommendations April 2010 The President in consultation with the University Budget Committee and executive staff makes FY11 supplemental budget allocation decisions using university strategic goals and priorities. Final adjusted tuition revenue budget for FY11. 34

50 Budgeting Timeline Detail BOT Supplemental Budget Approval May 2010 First read of supplemental FY11 budget to Board of Trustees June 2010 Second read of supplemental FY11 budget and Board of Trustee approval. 35

51 Budgeting Timeline Detail Implementation of FY11 Budgets July 2010 Budgets are implemented for FY11. 36

52 37 OUTCOMES ASSESSMENT

53 Budgeting Timeline Detail Outcomes Assessment August 2011 Biennial budget outcome reports are submitted to the University Budget Committee and the President by the Provost and VPs comparing funding allocation with actual spending, outcome and assessment measures and executive level progress on the University s Strategic Plan s goals. Final reports are posted to the website and made widely available to the campus community. Official end to the FY10 & FY11 biennial budgeting cycle 38

54 Changes in Budget Model and Process The new budget allocation process differs in one fundamental way from the University s earlier budget model. The prior model did not address base budgets and assumed that base budgets would continue. In periods of steady enrollment, declining enrollment, and/or enrollment variations by program, a different approach is needed to allow for resources to move to the highest and best use for the University. 39

55 Summary The modified zero based strategic budgeting approach uses a transparent and participatory process to align university funding decisions with strategic plan goals. 40

56 41 Questions or Comments?

57

Open Budget Forum January Biennium

Open Budget Forum January 2009 2009 2011 Biennium Table of Contents Eastern Washington University Open Budget Forum January 2009 Agenda...1 Governor s Budget Proposal Overview A-1 A-4 Governor s Budget

Open Budget Forum January 2009 2009 2011 Biennium Table of Contents Eastern Washington University Open Budget Forum January 2009 Agenda...1 Governor s Budget Proposal Overview A-1 A-4 Governor s Budget

Biennium Open Budget Forum April 2009

2009-11 Biennium Open Budget Forum April 2009 Table of Contents Eastern Washington University Open Budget Forum April 2009 Comparison of Governor, House, & Senate Proposals.. A-1 A-4 Biennial Budget Proposals

2009-11 Biennium Open Budget Forum April 2009 Table of Contents Eastern Washington University Open Budget Forum April 2009 Comparison of Governor, House, & Senate Proposals.. A-1 A-4 Biennial Budget Proposals

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER STATE BIENNIAL BUDGET CYCLE OFM issues budget instructions EVEN YEARS JUN EWU BIENNIAL BUDGET CYCLE ONGOING Agency Strategic Planning Agencies submit budget

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER STATE BIENNIAL BUDGET CYCLE OFM issues budget instructions EVEN YEARS JUN EWU BIENNIAL BUDGET CYCLE ONGOING Agency Strategic Planning Agencies submit budget

New Mexico Highlands University Annual Operating Budget Process. approved Fall 2016

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

New Campus Budget Model

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW Ralph C. Wilcox, Ph.D. Provost & Senior Vice President for Academic Affairs January 21, 2009 Purpose Prepare balanced budget and legislative

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW Ralph C. Wilcox, Ph.D. Provost & Senior Vice President for Academic Affairs January 21, 2009 Purpose Prepare balanced budget and legislative

UW-Platteville Pioneer Budget Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

UNTHSC. Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

Sequoias Community College District RESOURCE

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

IDENTIFICATION AR II /15/06 THE PLANNING, BUDGETING, AND ASSESSMENT CYCLE. Part 1. THE PLANNING, BUDGETING, AND ASSESSMENT CYCLE

UNIVERSITY OF KENTUCKY ADMINISTRATIVE REGULATIONS IDENTIFICATION AR II-1.0-6 DATE EFFECTIVE PAGE 1 SUPERSEDES REGULATIONS DATED II-1.5-1 (1/01/01); II-1.5-2 (1/01/01); II-1.0-6 (8/23/93) THE PLANNING,

UNIVERSITY OF KENTUCKY ADMINISTRATIVE REGULATIONS IDENTIFICATION AR II-1.0-6 DATE EFFECTIVE PAGE 1 SUPERSEDES REGULATIONS DATED II-1.5-1 (1/01/01); II-1.5-2 (1/01/01); II-1.0-6 (8/23/93) THE PLANNING,

UW-STOUT Annual Operating Budget Process

UW-STOUT Annual Operating Budget Process An institution s budget process is shaped by institutional character; institutional size; administrative sophistication; faculty governance structures and processes;

UW-STOUT Annual Operating Budget Process An institution s budget process is shaped by institutional character; institutional size; administrative sophistication; faculty governance structures and processes;

Adopting a Different Approach to University Budgeting February 10, 2016

Adopting a Different Approach to University Budgeting February 10, 2016 1. Purpose. This document captures the analytical process and decision to change the Northwestern State University budgeting model

Adopting a Different Approach to University Budgeting February 10, 2016 1. Purpose. This document captures the analytical process and decision to change the Northwestern State University budgeting model

I. INTRODUCTION II. ROLES & RESPONSIBILITIES

Page 1 I. INTRODUCTION The District implements a broad-based comprehensive and integrated planning system that is a foundation for strategic directions and resource allocation decisions. The Superintendent/President

Page 1 I. INTRODUCTION The District implements a broad-based comprehensive and integrated planning system that is a foundation for strategic directions and resource allocation decisions. The Superintendent/President

Eastern Kentucky University

Eastern Kentucky University Budget Advisory Committee January 2018 Advisory Committee Charge: This committee was charged with developing recommendations to the President's Council that will address financial

Eastern Kentucky University Budget Advisory Committee January 2018 Advisory Committee Charge: This committee was charged with developing recommendations to the President's Council that will address financial

The Institutional Effectiveness Process at SJU: From Unit Assessment to Institutional Decision Making. Wenjun Chi Shawn Krahmer

The Institutional Effectiveness Process at SJU: From Unit Assessment to Institutional Decision Making Wenjun Chi Shawn Krahmer Resources in Higher ED Source: Sean McKitrick 2015 Workshop Group Activity

The Institutional Effectiveness Process at SJU: From Unit Assessment to Institutional Decision Making Wenjun Chi Shawn Krahmer Resources in Higher ED Source: Sean McKitrick 2015 Workshop Group Activity

A 10 STANDING COMMITTEES. A. Academic and Student Affairs Committee. Activity Based Budgeting Update. For information only.

A 10 VII. STANDING COMMITTEES A. Academic and Student Affairs Committee Activity Based Budgeting Update For information only. Attachments Initial Charge to Working Group, June 24, 2009 Working Group Report,

A 10 VII. STANDING COMMITTEES A. Academic and Student Affairs Committee Activity Based Budgeting Update For information only. Attachments Initial Charge to Working Group, June 24, 2009 Working Group Report,

THE COLLEGE OF NEW JERSEY STRATEGIC BUDGET PLANNING FISCAL YEAR 2015

THE COLLEGE OF NEW JERSEY STRATEGIC BUDGET PLANNING FISCAL YEAR 2015 Committee on Strategic Planning and Priorities (CSPP) Budget Decision-Making Principles and Process Approved by the Board of Trustees

THE COLLEGE OF NEW JERSEY STRATEGIC BUDGET PLANNING FISCAL YEAR 2015 Committee on Strategic Planning and Priorities (CSPP) Budget Decision-Making Principles and Process Approved by the Board of Trustees

Vernon College Annual Planning Calendar Academic Year

August, 2016 Evaluation of 16-17 Annual Action Plan (ongoing) and Institutional Plans Annual 16-17committee reports posted on website for College Committee review Responsibility: Committee Chairs and Director

August, 2016 Evaluation of 16-17 Annual Action Plan (ongoing) and Institutional Plans Annual 16-17committee reports posted on website for College Committee review Responsibility: Committee Chairs and Director

ASL Budget Forum. May 8, 2017

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

Evaluation of Annual Action Plan (ongoing) and Institutional Effectiveness Plans Responsibility: Component Leadership

and Institutional Effectiveness Plans Responsibility: Component Leadership") August, 2016 Evaluation of 15-16 Annual Action Plan (ongoing) and Institutional Plans Annual 15-16 committee reports posted on website for College review Responsibility: Committee Chairs and Director of

August, 2016 Evaluation of 15-16 Annual Action Plan (ongoing) and Institutional Plans Annual 15-16 committee reports posted on website for College review Responsibility: Committee Chairs and Director of

Budget Allocation Subcommittee: Report and Recommendations

RESOURCES PLANNING TASK FORCE Budget Allocation Subcommittee: Report and Recommendations I. Preamble The Committee was asked to determine how KPU should move forward in a budget environment that needs

RESOURCES PLANNING TASK FORCE Budget Allocation Subcommittee: Report and Recommendations I. Preamble The Committee was asked to determine how KPU should move forward in a budget environment that needs

BUSINESS AND FINANCIAL AFFAIRS DIVISION BUDGET OFFICE

Six-Year Planning: Initiative Summary Title: Implement More Effective and Efficient Budget Tools Initiative description, including statement of purpose and anticipated outcomes: The purpose of this initiative

Six-Year Planning: Initiative Summary Title: Implement More Effective and Efficient Budget Tools Initiative description, including statement of purpose and anticipated outcomes: The purpose of this initiative

Office of the Academic Senate One Washington Square San Jose, California Fax:

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 At its meeting of February 25, 2002, the Academic

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 At its meeting of February 25, 2002, the Academic

RESOURCE. Sequoias Community College District. College of the Sequoias

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

Evaluation of Annual Action Plan (ongoing) and Institutional Effectiveness Plans Responsibility: Component Leadership

and Institutional Effectiveness Plans Responsibility: Component Leadership") August, 2018 Evaluation of 17-18 Annual Action Plan (ongoing) and Institutional Plans Annual 17-18 committee reports posted on website for College Committee review Responsibility: Committee Chairs and

August, 2018 Evaluation of 17-18 Annual Action Plan (ongoing) and Institutional Plans Annual 17-18 committee reports posted on website for College Committee review Responsibility: Committee Chairs and

Strategic Budgeting Initiative

Strategic Budgeting Initiative Senate Presentation November 5, 2013 Financial Challenges Sharply reduced state support Increased risk from tuition dependency At Auburn, dependency rose from 44% to 63%

Strategic Budgeting Initiative Senate Presentation November 5, 2013 Financial Challenges Sharply reduced state support Increased risk from tuition dependency At Auburn, dependency rose from 44% to 63%

University Budget Advisory Committee Composition

University Budget Advisory Composition The University Budget (UBAC) is established by the President to provide input and recommendations to the President regarding the University s General Operating Fund

University Budget Advisory Composition The University Budget (UBAC) is established by the President to provide input and recommendations to the President regarding the University s General Operating Fund

Central Connecticut State University Integrated Budget Model. Pilot Department Overview and Training Session

Central Connecticut State University Integrated Budget Model Pilot Department Overview and Training Session Welcome and Introductions CCSU Budget Current As Is Process Zero-Based Budgeting in Practice

Central Connecticut State University Integrated Budget Model Pilot Department Overview and Training Session Welcome and Introductions CCSU Budget Current As Is Process Zero-Based Budgeting in Practice

POLICY RECOMMENDATION THE PLANNING AND BUDGET PROCESS AT SJSU

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 S05-10 At its meeting of May 9, 2005, the

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 S05-10 At its meeting of May 9, 2005, the

COLLEGE OF THE DESERT COLLEGE PLANNING COUNCIL MEETING

COLLEGE OF THE DESERT COLLEGE PLANNING COUNCIL MEETING Friday, February 6, 2015 10:00 a.m. to 12:00 p.m. PSA Room 19A Minutes Members: A. Bynum, A. Davies, A. Nery, A. Sawa, ASCOD President J. Zepeda,

COLLEGE OF THE DESERT COLLEGE PLANNING COUNCIL MEETING Friday, February 6, 2015 10:00 a.m. to 12:00 p.m. PSA Room 19A Minutes Members: A. Bynum, A. Davies, A. Nery, A. Sawa, ASCOD President J. Zepeda,

USF System Annual Strategic Budget Planning Process

USF System Annual Strategic Budget Planning Process University budget strategy, planning and development should be led by the Provost to assure that the budget reflects USF s strategic priorities The President

USF System Annual Strategic Budget Planning Process University budget strategy, planning and development should be led by the Provost to assure that the budget reflects USF s strategic priorities The President

Campus Budget Open Forum. October 5, 2017

Campus Budget Open Forum October 5, 2017 2 Agenda WSCUC Accreditation Area of Inquiry URPC membership and role Budget update Public facing budget dashboards Achieved budget savings (Spring 2017 - Phase

Campus Budget Open Forum October 5, 2017 2 Agenda WSCUC Accreditation Area of Inquiry URPC membership and role Budget update Public facing budget dashboards Achieved budget savings (Spring 2017 - Phase

California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

NORTHWESTERN STATE UNIVERSITY Budget Development. Budget Model

VII-2 Budget Development NORTHWESTERN STATE UNIVERSITY Budget Development Budget Model The Planning, Programming, and Budget Execution (PPBE) model best fits the University s Budget Development. This model

VII-2 Budget Development NORTHWESTERN STATE UNIVERSITY Budget Development Budget Model The Planning, Programming, and Budget Execution (PPBE) model best fits the University s Budget Development. This model

North Orange County Community College District Integrated. Planning Manual March 2014 Update

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

Frequently Asked Questions (FAQs) about NKU s New Budget Model

about NKU s New Budget Model") Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

TYLER JUNIOR COLLEGE PROCEDURAL CALENDAR PROGRAM ASSESSMENT, PLANNING, BUDGETING, AND EVALUATION SYSTEM

Looking Over the Horizon To Plan for the Future TYLER JUNIOR COLLEGE 2009-10 PROCEDURAL CALENDAR PROGRAM ASSESSMENT, PLANNING, BUDGETING, AND EVALUATION SYSTEM AREAS: Academic Affairs Advancement and External

Looking Over the Horizon To Plan for the Future TYLER JUNIOR COLLEGE 2009-10 PROCEDURAL CALENDAR PROGRAM ASSESSMENT, PLANNING, BUDGETING, AND EVALUATION SYSTEM AREAS: Academic Affairs Advancement and External

Budget Process from State Appropriations to University Disbursements

Budget Process from State Appropriations to University Disbursements Dennis Jones, Norfolk State University Patricia McDermott, Christopher Newport University Deborah Swiecinski, Old Dominion University

Budget Process from State Appropriations to University Disbursements Dennis Jones, Norfolk State University Patricia McDermott, Christopher Newport University Deborah Swiecinski, Old Dominion University

Budget Reform Update. Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

STATE CENTER COMMUNITY COLLEGE DISTRICT

STATE CENTER COMMUNITY COLLEGE DISTRICT Districtwide Resource Allocation Model General Fund Unrestricted Budget Fresno Reedley Madera Oakhurst Willow International Table of Contents Background... 3 Elements

STATE CENTER COMMUNITY COLLEGE DISTRICT Districtwide Resource Allocation Model General Fund Unrestricted Budget Fresno Reedley Madera Oakhurst Willow International Table of Contents Background... 3 Elements

BUDGET TRANSPARENCY REPORT

Academic Senate Strategic Issues Committee San Francisco State University Academic Year 16/17 BUDGET TRANSPARENCY REPORT 2016/2017 Recommendations laying the foundation for future budget focus TABLE OF

Academic Senate Strategic Issues Committee San Francisco State University Academic Year 16/17 BUDGET TRANSPARENCY REPORT 2016/2017 Recommendations laying the foundation for future budget focus TABLE OF

FAQs Finance and Budget Modeling Initiative

FAQs Finance and Budget Modeling Initiative Why do we need to create a new budget model? o To improve transparency, to ensure that data drives decision making, and to make strategic decisions based on

FAQs Finance and Budget Modeling Initiative Why do we need to create a new budget model? o To improve transparency, to ensure that data drives decision making, and to make strategic decisions based on

Version 2.0- Project. Q: What is the current status of your project? A: Completed

Baker College, MI Project: Develop an institutional quality assurance framework to measure institutional effectiveness and drive continuous quality improvement efforts Version 2.0- Project What is the

Baker College, MI Project: Develop an institutional quality assurance framework to measure institutional effectiveness and drive continuous quality improvement efforts Version 2.0- Project What is the

California Community Colleges/Districts Funding Model Proposal Submitted to Chancellor Oakley December 20, 2017

NOTE as of January 29, 2018: The CCC Funding Model Proposal recommendations by the Advisory Workgroup on Fiscal Affairs was provided to Chancellor Oakley prior to the release of the Governor s 2018-19

NOTE as of January 29, 2018: The CCC Funding Model Proposal recommendations by the Advisory Workgroup on Fiscal Affairs was provided to Chancellor Oakley prior to the release of the Governor s 2018-19

Resource Allocation, Management, and Planning Steering Committee #7

Resource Allocation, Management, and Planning Steering #7 August 28, 2018 1 Agenda Huron is pleased to partner with WKU on this resource allocation, management, and planning ( RAMP ) initiative. Our goals

Resource Allocation, Management, and Planning Steering #7 August 28, 2018 1 Agenda Huron is pleased to partner with WKU on this resource allocation, management, and planning ( RAMP ) initiative. Our goals

Guidelines for Fiscal 2019 Budget Submissions Priority-Based Budgeting

Guidelines for Fiscal 2019 Budget Submissions Priority-Based Budgeting Executive Summary Incremental funding available to Georgia Tech, has not been sufficient to cover the research, instructional, public

Guidelines for Fiscal 2019 Budget Submissions Priority-Based Budgeting Executive Summary Incremental funding available to Georgia Tech, has not been sufficient to cover the research, instructional, public

FY19 Budget Development

January 1 Holiday - New Year's Day (First 2018 Holiday) January 4 Commission on Higher Education Meeting January 8 Budget Staff Meeting January 8 FY19 Governor's Proposed Budget Released - estimated January

January 1 Holiday - New Year's Day (First 2018 Holiday) January 4 Commission on Higher Education Meeting January 8 Budget Staff Meeting January 8 FY19 Governor's Proposed Budget Released - estimated January

University Budget Committee. April 13, 2018

University Budget Committee April 13, 2018 1 Agenda I. Welcome II. Review and Approve Minutes from March 23, 2018 III. IV. UBC Feedback on Academic Senate Resolution on Increasing Faculty Involvement in

University Budget Committee April 13, 2018 1 Agenda I. Welcome II. Review and Approve Minutes from March 23, 2018 III. IV. UBC Feedback on Academic Senate Resolution on Increasing Faculty Involvement in

University Cabinet Outline of Budget Reduction Decisions February 22, 2018

Priorities in Budget Planning Student success Equity and diversity Fiscal stability and good stewardship of resources Shared responsibility and accountability Values (These are summarized from the Values

Priorities in Budget Planning Student success Equity and diversity Fiscal stability and good stewardship of resources Shared responsibility and accountability Values (These are summarized from the Values

Budget Planning and Development Workshop

Budget Planning and Development Workshop Presented By: Administration and Finance Student Life Information Technology Services Workshop Agenda Resource Allocation Overview All Funds Budget Model Budget

Budget Planning and Development Workshop Presented By: Administration and Finance Student Life Information Technology Services Workshop Agenda Resource Allocation Overview All Funds Budget Model Budget

Planning and Budgeting Integration (PBI) Model

Model") Peralta Community College District Planning and Budgeting Integration (PBI) Model OVERVIEW Introduction This document describes the central principles and features of Peralta s Planning and Budgeting Integration

Peralta Community College District Planning and Budgeting Integration (PBI) Model OVERVIEW Introduction This document describes the central principles and features of Peralta s Planning and Budgeting Integration

SHEPHERD UNIVERSITY BUDGET PACKAGE FOR ANNUAL OPERATING AND CAPITAL BUDGET FISCAL YEAR 2011

ATTACHMENT BB: SHEPHERD UNIVERSITY BUDGET PACKAGE FOR ANNUAL OPERATING AND CAPITAL BUDGET FISCAL YEAR 2011 BACKGROUND Contents The budget package for this year includes the following: 1. Detailed instructions

ATTACHMENT BB: SHEPHERD UNIVERSITY BUDGET PACKAGE FOR ANNUAL OPERATING AND CAPITAL BUDGET FISCAL YEAR 2011 BACKGROUND Contents The budget package for this year includes the following: 1. Detailed instructions

BUDGET MESSAGE FISCAL YEAR Presented May 13, 2015

BUDGET MESSAGE FISCAL YEAR 2015-16 Presented May 13, 2015 The fiscal year 2015-16 budget reflects a year-long process of analysis, review, and application of our budget development principles, criteria

BUDGET MESSAGE FISCAL YEAR 2015-16 Presented May 13, 2015 The fiscal year 2015-16 budget reflects a year-long process of analysis, review, and application of our budget development principles, criteria

Financial Management Guidelines and Procedures

The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the

The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the

We produced the Strategic Planning Process (SPP) using the following design principles:

using the following design principles:") I. Introduction The strategic planning process guides the district in integrating planning, budgeting and evaluation processes that result in the district achieving its goals as set forth in the vision

I. Introduction The strategic planning process guides the district in integrating planning, budgeting and evaluation processes that result in the district achieving its goals as set forth in the vision

STRATEGIES ASSESSMENT

DRAFT MONTANA STATE UNIVERSITY - BOZEMAN Annual Planning & Budgeting Cycle STRATEGIES PLANNING MISSION and VISION BUDGETING ASSESSMENT c:pba plan 02.20.01 Planning & Budgeting Committee Organization President

DRAFT MONTANA STATE UNIVERSITY - BOZEMAN Annual Planning & Budgeting Cycle STRATEGIES PLANNING MISSION and VISION BUDGETING ASSESSMENT c:pba plan 02.20.01 Planning & Budgeting Committee Organization President

Eastern Washington University

FY18 SUPPLEMENTAL OPERATING BUDGET REQUEST 2017-2019 BIENNIUM Eastern Washington University EASTERN WASHINGTON UNIVERSITY OPERATING BUDGET REQUEST FY18 Supplemental 370 EASTERN WASHINGTON UNIVERSITY FY18

FY18 SUPPLEMENTAL OPERATING BUDGET REQUEST 2017-2019 BIENNIUM Eastern Washington University EASTERN WASHINGTON UNIVERSITY OPERATING BUDGET REQUEST FY18 Supplemental 370 EASTERN WASHINGTON UNIVERSITY FY18

UMass Lowell A Strategic Plan for the Next Decade. Committee on Financial Planning & Budget Review Organizational Meeting

UMass Lowell 2020 A Strategic Plan for the Next Decade Committee on Financial Planning & Budget Review Organizational Meeting March 6, 2009 Agenda Summary of Committee Charge Budget Planning Context Overview

UMass Lowell 2020 A Strategic Plan for the Next Decade Committee on Financial Planning & Budget Review Organizational Meeting March 6, 2009 Agenda Summary of Committee Charge Budget Planning Context Overview

Peralta Planning and Budgeting Integration (PBI) Model. OVERVIEW (August 6, 2009)

Model. OVERVIEW (August 6, 2009)") Peralta Planning and Budgeting Integration (PBI) Model OVERVIEW (August 6, 2009) On August 3, 2009, Chancellor Harris issued Administrative Procedure 2.20 to implement the Planning and Budgeting Integration

Peralta Planning and Budgeting Integration (PBI) Model OVERVIEW (August 6, 2009) On August 3, 2009, Chancellor Harris issued Administrative Procedure 2.20 to implement the Planning and Budgeting Integration

Strategic Plan Design, Execution & Assessment to Meet Governing Board Priorities

Strategic Plan Design, Execution & Assessment to Meet Governing Board Priorities Dr. Brian Lofman, Dean, Planning & Effectiveness Dr. Willard Lewallen, Superintendent/President Patricia Donohue, Vice President,

Strategic Plan Design, Execution & Assessment to Meet Governing Board Priorities Dr. Brian Lofman, Dean, Planning & Effectiveness Dr. Willard Lewallen, Superintendent/President Patricia Donohue, Vice President,

Welcome to the Spring 2018 Budget Forum! Hosted by the President s Budget Advisory Committee

Welcome to the Spring 2018 Budget Forum! Hosted by the President s Budget Advisory Committee Campus Budget Spring 2018 Budget Forum Sonoma State University March 13, 2018 Budget Basics About My Unit Laura

Welcome to the Spring 2018 Budget Forum! Hosted by the President s Budget Advisory Committee Campus Budget Spring 2018 Budget Forum Sonoma State University March 13, 2018 Budget Basics About My Unit Laura

The University of Rhode Island Kingston, Rhode Island. Fall 2010 Report to:

The University of Rhode Island Kingston, Rhode Island Fall 2010 Report to: The Commission on Institutions of Higher Education of the New England Association of Schools and Colleges September 10, 2010 This

The University of Rhode Island Kingston, Rhode Island Fall 2010 Report to: The Commission on Institutions of Higher Education of the New England Association of Schools and Colleges September 10, 2010 This

Accreditation Action Plan for Removal of Probation presented to the LACCD Board of Trustees. Aug. 22, 2012 Los Angeles Harbor College

Accreditation Action for Removal of Probation presented to the LACCD Board of Trustees Aug. 22, 2012 Los Angeles Harbor College Rolled up our sleeves and got to work Focused on our students success Affirmed

Accreditation Action for Removal of Probation presented to the LACCD Board of Trustees Aug. 22, 2012 Los Angeles Harbor College Rolled up our sleeves and got to work Focused on our students success Affirmed

Focus for the Future: A retrospective outsider view. John Wiencek

Focus for the Future: A retrospective outsider view John Wiencek 1 Genesis: Zero Based Budgeting May 2013 Memo from SBOE staff indicates that the Governor s mandate that all state agencies undergo a zero

Focus for the Future: A retrospective outsider view John Wiencek 1 Genesis: Zero Based Budgeting May 2013 Memo from SBOE staff indicates that the Governor s mandate that all state agencies undergo a zero

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2015

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2015 Purpose: The principal purpose of the budget planning process is to provide Georgia Tech s senior leadership the essential

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2015 Purpose: The principal purpose of the budget planning process is to provide Georgia Tech s senior leadership the essential

BUDGET ALLOCATION PROCESS University Administrators Forum February 6, 2013

DIVISION OF BUSINESS AND FINANCE BUDGET ALLOCATION PROCESS University Administrators Forum February 6, 2013 North Carolina Agricultural and Technical State University Presentation Outline Budget Overview

DIVISION OF BUSINESS AND FINANCE BUDGET ALLOCATION PROCESS University Administrators Forum February 6, 2013 North Carolina Agricultural and Technical State University Presentation Outline Budget Overview

Budget Model Refinement Discussion. October 2018

Budget Model Refinement Discussion October 2018 1 Agenda 1. Budget Model Refinement Schedule 2. Opportunities for Refinement Significant Financial Challenges/Issues Overall Policy Issues Budget Model Formula

Budget Model Refinement Discussion October 2018 1 Agenda 1. Budget Model Refinement Schedule 2. Opportunities for Refinement Significant Financial Challenges/Issues Overall Policy Issues Budget Model Formula

Finance and Budget Modeling Town Hall. March 27 & 28, 2018

Finance and Budget Modeling Town Hall March 27 & 28, 2018 FINANCE AND BUDGET MODELING TASK FORCE Charge The Finance and Budget Modeling Task Force will create a new budget model that is transparent, data-driven,

Finance and Budget Modeling Town Hall March 27 & 28, 2018 FINANCE AND BUDGET MODELING TASK FORCE Charge The Finance and Budget Modeling Task Force will create a new budget model that is transparent, data-driven,

Saddleback College Strategic Planning Process. Recommended by the Consultation Council, 6/16/09 Approved by the President, 6/23/09 Revised, 8/6/09

Saddleback College Strategic Planning Process Recommended by the Consultation Council, 6/16/09 Approved by the President, 6/23/09 Revised, 8/6/09 Table of Contents Purpose... 3 Planning Bodies... 4 Consultation

Saddleback College Strategic Planning Process Recommended by the Consultation Council, 6/16/09 Approved by the President, 6/23/09 Revised, 8/6/09 Table of Contents Purpose... 3 Planning Bodies... 4 Consultation

University Planning Phase 1. Organizational and Process Enhancements

University Planning Phase 1 Organizational and Process Enhancements October 31, 2008 Today s Agenda Background, Vision, Goals Guiding Principles University Planning Proposed Organizational Structure Operating

University Planning Phase 1 Organizational and Process Enhancements October 31, 2008 Today s Agenda Background, Vision, Goals Guiding Principles University Planning Proposed Organizational Structure Operating

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2016

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2016 Purpose: The principal purpose of the budget planning process is to provide Georgia Tech s senior leadership the essential

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2016 Purpose: The principal purpose of the budget planning process is to provide Georgia Tech s senior leadership the essential

FY 2019 UNIVERSITY BUDGET CALENDAR

FY 2019 UNIVERSITY BUDGET CALENDAR FY2019 UNIVERSITY BUDGET CALENDAR PLANNING: July, 2017 Office of Budget Management distributes the following to all Vice Presidents, Provost Office, and Business Representatives

FY 2019 UNIVERSITY BUDGET CALENDAR FY2019 UNIVERSITY BUDGET CALENDAR PLANNING: July, 2017 Office of Budget Management distributes the following to all Vice Presidents, Provost Office, and Business Representatives

Fourth Report of the Budget Model Development Committee

INTRODUCTION This (BMDC) has resulted from over a year of investigating models of budget development and resource management in higher education. The goal of this study is to propose a new approach to

INTRODUCTION This (BMDC) has resulted from over a year of investigating models of budget development and resource management in higher education. The goal of this study is to propose a new approach to

Wing-Kit Chung, Vice President of Administrative Services Jim Langstraat, Associate VP of Financial Services

Wing-Kit Chung, Vice President of Administrative Services Jim Langstraat, Associate VP of Financial Services 1 Agenda 1. State Funding Level 2. PERS Reminder 3. Enrollment Target 4. Tuition Environment

Wing-Kit Chung, Vice President of Administrative Services Jim Langstraat, Associate VP of Financial Services 1 Agenda 1. State Funding Level 2. PERS Reminder 3. Enrollment Target 4. Tuition Environment

Financial Operating. & Capital Plan Reviews FY Budget Forum. February 14, FY 2014 Budget Forum - February

Financial Operating & Capital Plan Reviews FY 2014 Budget Forum February 14, 2013 FY 2014 Budget Forum - February 2013 0 University Budget Council (UBC) Bob Warren, Chair VP Administration & Finance Dennis

Financial Operating & Capital Plan Reviews FY 2014 Budget Forum February 14, 2013 FY 2014 Budget Forum - February 2013 0 University Budget Council (UBC) Bob Warren, Chair VP Administration & Finance Dennis

A G E N D A Revised WORKSHOP BUDGET MEETING OF THE PARK RIDGE CITY COUNCIL CITY HALL COUNCIL CHAMBERS 505 BUTLER PLACE PARK RIDGE, IL

CITY OF PARK RIDGE 505 BUTLER PLACE PARK RIDGE, IL 60068 TEL: 847/ 318-5200 FAX: 847/ 318-5300 TDD: 847/ 318-5252 URL: http://www.parkridge.us A G E N D A Revised WORKSHOP BUDGET MEETING OF THE PARK RIDGE

CITY OF PARK RIDGE 505 BUTLER PLACE PARK RIDGE, IL 60068 TEL: 847/ 318-5200 FAX: 847/ 318-5300 TDD: 847/ 318-5252 URL: http://www.parkridge.us A G E N D A Revised WORKSHOP BUDGET MEETING OF THE PARK RIDGE

Administrative Procedures Integrated Planning and Budgeting (IPB) Model

Model") Administrative Procedures Integrated Planning and Budgeting (IPB) Model Team: Dr. Rosemary Delia and Dr. Dettie C. Del Rosario EXPECTED OUTCOME: Institutional excellence is the primary expected outcome

Administrative Procedures Integrated Planning and Budgeting (IPB) Model Team: Dr. Rosemary Delia and Dr. Dettie C. Del Rosario EXPECTED OUTCOME: Institutional excellence is the primary expected outcome

San Francisco State University. We Make Great Things Happen. University Budget Committee September 12, 2017

San Francisco State University We Make Great Things Happen University Budget Committee September 12, 2017 Welcome to the new Academic 2017-2018 Year! Today s Agenda Welcome and Announcements (President

San Francisco State University We Make Great Things Happen University Budget Committee September 12, 2017 Welcome to the new Academic 2017-2018 Year! Today s Agenda Welcome and Announcements (President

Office of the Provost University of Illinois at Urbana-Champaign. 3 February 2016

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself