Budgetary review and recommendations report Briefing to Portfolio Committee on Basic Education Add subtitle here. XX Month XXXX

|

|

|

- Moses Nathaniel Hodges

- 5 years ago

- Views:

Transcription

1 Budgetary review and recommendations report Briefing to Portfolio Committee on Basic Education Add subtitle here XX Month XXXX 1

2 Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the supreme audit institution (SAI) of South Africa, exists to strengthen our country s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building public confidence. 2

.")

3 Role of the AGSA in the reporting process Our role as the AGSA is to reflect on the audit work performed to assist the portfolio committee in its oversight role of assessing the performance of the entities taking into consideration the objective of the committee to produce a Budgetary Review and Recommendations Report (BRRR). 3

4 1 Our focus 4

5 Our annual audit examines three areas 1FAIR PRESENTATION AND RELIABILITY OF FINANCIAL STATEMENTS 2 RELIABLE AND CREDIBLE PERFORMANCE INFORMATION FOR PREDETERMINED OBJECTIVES 3 COMPLIANCE WITH KEY LEGISLATION ON FINANCIAL AND PERFORMANCE MANAGEMENT 5

6 The AGSA expresses the following different audit opinions Unqualified opinion with no findings (clean audit) Financially unqualified opinion with findings Qualified opinion Adverse opinion Disclaimed opinion Auditee: produced credible and reliable financial statements that are free of material misstatements reported in a useful and reliable manner on performance as measured against predetermined objectives in the annual performance plan (APP) complied with key legislation in conducting their day-to-day operations to achieve their mandate Auditee produced financial statements without material misstatements or could correct the material misstatements, but struggled in one or more area to: align performance reports to the predetermined objectives they committed to in APPs set clear performance indicators and targets to measure their performance against their predetermined objectives report reliably on whether they achieved their performance targets Auditee: had the same challenges as those with unqualified opinions with findings but, in addition, they could not produce credible and reliable financial statements had material misstatements on specific areas in their financial statements, which could not be corrected before the financial statements were published. Auditee: had the same challenges as those with qualified opinions but, in addition, they had so many material misstatements in their financial statements that we disagreed with almost all the amounts and disclosures in the financial statements Auditee: had the same challenges as those with qualified opinions but, in addition, they could not provide us with evidence for most of the amounts and disclosures reported in the financial statements, and we were unable to conclude or express an opinion on the credibility of their financial statements determine the legislation that they should comply with and implement the required policies, procedures and controls to ensure compliance 6

7 The percentages in this presentation are calculated based on the completed audits of 3 auditees, unless indicated otherwise The overall audit outcomes are indicated as follows: Unqualified with no findings Unqualified with findings Qualified with findings Adverse with findings Disclaimed with findings Audits outstanding DBE Department of Basic Education UMALUSI Council for Quality Assurance in General and Further Education and Training SACE South African Council of Educators Movement over the previous year is depicted as follows: Improved Unchanged Movement of 5% or less: slight improvement slight regression Regressed 7

8 2 The audit outcomes 8

9 ACCOUNTABILITY = PLAN + DO + CHECK + ACT PLAN DO ACT CHECK 9

10 Audit outcomes of portfolio over five years 67% (2) SACE UMALUSI 100% (3) DBE SACE UMALUSI 100% (3) DBE SACE UMALUSI 100% (3) DBE SACE UMALUSI 100% (3) DBE SACE UMALUSI 33% (1) DBE auditees 3 auditees 3 auditees 3 auditees 3 auditees 10

Quality performance reports: 66%")

Irregular expenditure: R268 Million")

11 Portfolio snapshot ( ) Clean audits: 0% ( : 0%) Quality financial statements: 0% ( : 0%) Quality performance reports: 66% (SACE, UMALUSI) ( : 33% SACE) No findings on compliance with legislation: 0% ( : 0%) Irregular expenditure: R268 Million ( : R622 Million) 11

12 3 Management and delivery of key programmes 12

13 School Infrastructure (ASIDI) Budget vs spending Financial management (AFS) Compliance Pre-determined objectives Programme Number of new schools built and completed through ASIDI Number of schools provided with sanitation facilities through ASIDI Number of schools provided with water through ASIDI Number of schools provided with electricity through ASIDI Budget Allocation: 2 billion Project budget was revised from 2 Billion to 1.6 Billion as per adjusted budget Actual expenditure to date R 1.6 Billion Processes are not in place to ensure that accruals are complete and fairly stated. Processes are not in place to ensure that assets capitalised upon receipt of practical completion certificates are capitalised at the correct value. This is evident by expenses being captured 2 years after completion certificates are received. Processes are not in place to ensure that all completed projects are correctly accounted for on the immovable asset register. (Including the prefer class or mobile classrooms) Large commitment balances remain if AFS for schools even though the schools have been completed and are in-use for a number of years. Is the commitment register overstated. Procurement and contract management Findings including the following: Irregular expenditure as a result of non-compliance by implementing agents. Expenditure incurred exceeded the contract values for which variation orders had to be applied for. The variation orders approved in this regard exceeded 20% of the contract values and were approved by the accounting officer (or acting accounting officer) at the time of approval and not by National Treasury as required. Lack of contract management on these projects, irregularities were identified. Material adjustments were noted in the infrastructure indicators (water, sanitation and electricity that have reached practical completion). The following criteria were affected: Validity Completeness Actual achievement 0 of the 4 target were achieved for 2017/18 Value add In some instance, there were significant delays in submission of documentation for audit, for example: payment certificates, extension of time approvals, and/or variation order approvals. In some instances, findings that were raised in the prior year had either not been addressed or was in the process of being addressed by the department. In all eleven of the selected projects, delays were experienced in the implementation of the projects which resulted in projects not achieving contractual timelines. Delays were ranging from 8 to 35 months. In certain projects, delays resulted in an increase in cost on projects with an average of approximately 21% over the original contract price. Six out of the 11 projects had replacement contractors. The department and implementing agents did not conduct a proper site assessment to determine the amount of work needed to be done by the replacement contractors. Therefore, the project budget was increased via variation orders. Furthermore, variation orders as a result of poor planning were approved on certain projects. The water reticulation system was not standardized. Some schools had a system where water purification was present; whilst others had a system of access to water directly from the water tanks not purified. Instances of poor quality of work were identified on nine projects, as a result of inadequate project management. Some of the schools were not handed over to the provincial department. As a result, there was no accountability with regards to maintenance of completed schools. The department allowed Adopt-A-School to conduct construction on their property without prior engagements and approval of the scope of works and designs. As a result, variation orders were approved for remedial works that were due to non-compliance of the department s norms and standards. Material findings / concerns noted No material findings / concerns noted 13

14 4 Financial Management 14

15 Unauthorised, irregular as well as fruitless and wasteful expenditure decrease over 5 years Definition DBE Expenditure not in accordance with the budget vote/ overspending of budget or programme Expenditure incurred in vain and could have been avoided if reasonable steps had been taken. No value for money! Expenditure incurred in contravention of key legislation; goods delivered but prescribed processes not followed Unauthorised expenditure Fruitless and wasteful expenditure Irregular expenditure R6 million R0,5 million R11 million R2 million R 268 million Unauthorised expenditure The balance of unauthorised expenditure is made up of amounts that were identified in the 2014/15 financial year that are still under investigation. Fruitless and wasteful expenditure The department incurred costs for work that should have been performed internally and payment made to the fraudulent tutors of Kha Ri Gude volunteers. Contributor DBE: 0,5 Million Irregular expenditure 100% of irregular expenditure incurred in the current financial year was as a result of contravention of SCM legislation Contributors DBE: R 257,4 Million Umalusi: R11 Million R 622 million R 599 million R 728 million R 771 million

16 Irregular expenditure and supply chain management Irregular expenditure decreased from R622 million to R268.4 million (57,% Decrease) R268.4 million R154 million 38% (R103 million) of the irregular expenditure was payments/ expenses in previous years only uncovered and disclosed for the first time in % (R165 million) of the irregular expenditure includes payments made on contracts irregularly awarded in a previous years - if the noncompliance is not investigated and condoned, the payments on multi-year contracts continue to be viewed and disclosed as irregular expenditure, however as the contract come to an end, it decreases the irregular expenditure R0 million R103 million % (SACE, UMALUSI) 33% (SACE) 67% (DBE, UMALUSI) 33% (DBE) With no findings With findings With material findings 16

17 Most common findings on supply chain management Limitations awards selected but could not be tested 33% (DBE) Three written qoutations not invited 33% (UMALUSI) Inadequate contract performance measures and monitoring 33% (SACE) 17

18 Fraud and consequence management No auditees had findings on non-compliance with legislation on consequence management Allegations of financial and/or fraud and SCM misconduct (2 auditees) Allegations not investigated 00 Investigations took longer than three months 67% (DBE; UMALUSI) Allegations not properly investigated 0 18

19 Supply chain management findings reported to management for investigation Other SCM findings reported for investigation during the audit process (1 auditees) Supplier(s) submitted false declaration of interest 33% (DBE) 1 instance Employee(s) failed to disclose interest in supplier 0% 33% (DBE) Other SCM findings 1 instance reported for investigation 19

20 Root causes Slow response to improving key controls and addressing risk areas Daily, Monthly internal control are not effective Inadequate consequences for poor performance and transgressions 20

21 Management and utilisation of Conditional Grant We identified the following capital expenditure payments made on projects that were not budgeted for in the U-AMP for the 2017/18 financial year. (FS) Through inspection of the invoice attached to the payment voucher of the item below, the service related to installation of computer desks (incl: Material, labour and transport) at Tjhebelopele School, therefore not within the purpose of the Education Infrastructure Grant as stated above. (FS) Through inspection of note 15 to the financial statements, the department has a bank overdraft of R There is therefore not available cash in the bank to back the unspent portion and to surrender the unspent conditional grants to Treasury using the 2017/18 allocation. (FS) The department overspent on one EIG grant project which relates to the Koster Primary School. The overspending amounts to R as the approved amount of the project was R and expenditure to date is R (NW) 21

22 5 Control Environment 22

33% (SACE) 33% (DBE) Accounting officer/authority 67% (UMALUSI; SACE) 33% (DBE) Executive authority")

------------------------------------------------------------------------------------------------ Provides assurance Provides some")

23 Third level Second level First level Assurance provided Assurance Senior management 33% (UMALUSI) 33% (SACE) 33% (DBE) Accounting officer/authority 67% (UMALUSI; SACE) 33% (DBE) Executive authority Internal audit unit 67% (UMALUSI; DBE) 33% (SACE) Audit committee Portfolio committee 100% (DBE; SACE; UMALUSI) Provides assurance Provides some assurance Provides limited/ no assurance Not established 23

24 Status of internal control Leadership 33% (SACE) 33% (UMALUSI) 33% (DBE) Financial and performance management 66% (UMALUSI, SACE) 33% (DBE) Governance (DBE; SACE, UMALUSI) Good Of concern Intervention required 24

25 Little improvement in plan-do-check-act cycle PLAN Status of audit action plans unchanged Usefulness of performance indicators and targets regressed DO Overall internal controls slightly regressed Basic financial and performance management controls regressed ICT controls unchanged Vacancies in CFO positions Unchanged CHECK Assurance provided by: Senior management and accounting officer/ authority slightly regressed Executive authority remained unchanged (provides some assurance) Internal audit units and audit committees improved (provides assurance) Portfolio committee remained improved (provides assurance) ACT Compliance with consequence management legislation improved Investigation of previous year UIFW improved (closing balance of UIFW not dealt with is R1.560 million) Investigations into SCM findings we reported in previous year unchanged 25

26 Recommendations Responsive action plans should be implemented and monitored regularly to ensure improved internal environment, the oversight over financial and performance reporting should be strengthen Daily management disciplines Getting the daily disciplines of management right is critical for an improved audit outcome. Effective coordination between the various implementing agent and the department is also critical for an improvement of the audit outcome. Monitoring and evaluation processes The monitoring and evaluation of all information received internally and externally must be thoroughly reviewed, monitored and evaluated to ensure it is credible and reliable. 26

27 27

28 6 Sector outcome 28

29 Sector outcomes 29

30 Sector audit focus areas Usage, verifications of SA-SAMS data and LURITS interface School Infrastructure School management and governance Early Childhood Development Grade R Curriculum coverage Textbook retention and retrieval 30

31 6.1 Usage, verifications of SA-SAMS data and LURITS interface 31

32 SA-SAMS and LURITS 32

33 Deficiencies identified on SA-SAMS The majority of schools were using SA-SAMS and the following key deficiencies were identified: IT security management, user access management and IT service continuity controls were not adequately designed and implemented regarding policies and procedures, users access management on the system, and how backups should be performed and stored; IT capacity remains a challenge at most of the provinces with SA-SAMS as current IT technicians cannot adequately support the provincial and school s; The link specification documentation was not used when finalising the data integrity in some of the provinces. Furthermore, data quality was not performed at three provinces (GP, KZN and EC) due to resource constraints. Learner numbers and enrolment could be open to inflation and could result in planning, budgeting and spending on salaries, infrastructure and learner materials being based on inaccurate data. Some learners were identified without a national tracking number and an identification number on the SA-SAMS application due to the fact the learner national tracking number and the identification number fields were not compulsory. This resulted in the information uploaded on the LURITS system being invalid, incomplete and inaccurate. The learner database file created at school level was not appropriately secured. Information on the learner database can be easily altered and the data can be compromised. It was found that 9.37% of the schools (1955) are on version and older versions which was not the latest version (18.1.0). There were also, instances identified where 8.13% of the schools (1694) did not disclose the version number. 33

34 6.2 Education Infrastructure 34

35 Education Infrastructure Grant Sector Findings Delays in completion of the committed school infrastructure projects. (all 9 provinces had findings) School facilities needing maintenance but not included in the maintenance project list. (7 provinces had findings except EC and WC) Quality deficiencies identified from the school infrastructure projects Schools completed were not occupied as per the plan. (8 provinces had findings except WC) School infrastructure projects incurred additional cost from the contractual agreement. (all 9 provinces had findings) 35

36 Quality deficiencies 36

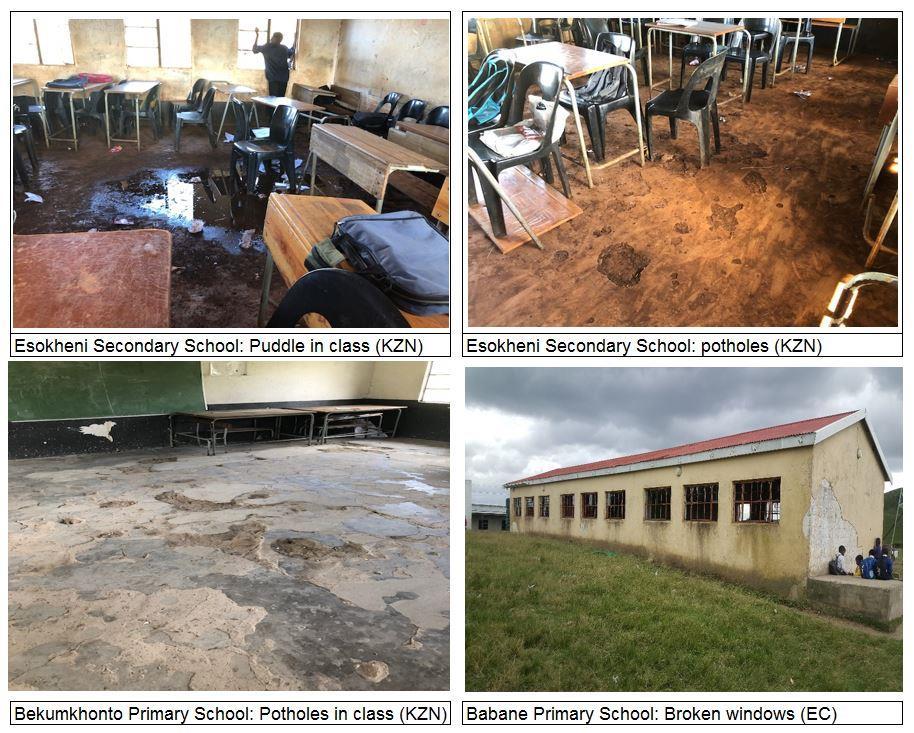

37 Maintenance issues 37

38 6.3 Curriculum coverage 38

39 Education Sector Audit objectives and scope Objective To determine whether the departments of education effectively and adequately implemented management measures to ensure that the standards of education provision, delivery and performance are monitored and reported. The scope of the audit The sector audit covered the following: The school management and governance and Early Childhood Development were audited in with follow-up in Textbook retention and retrieval and curriculum coverage were audited in schools, 21 education districts and 9 provincial education departments (PED) and also the role of DBE in developing and communicating policies. The audit specifically focussed on Mathematics and English First Additional Language (EFAL) for grades 3, 6, 9 and 11. The site visits for selected schools were conducted in the 4th term / quarter before the schools closes in December High performing and low performing secondary schools according to National Senior Certificate results and feeder primary schools. In provinces with more than 10 districts, we selected 3 districts and 12 schools In provinces with less that 10 districts, we selected 2 districts and 10 schools 39

40 Criteria for curriculum coverage at schools The School Management Teams (SMT) are expected to monitor and report curriculum coverage by educators as outlined in Personnel Administrative Measures (PAM). This is through: Heads of Department (HoD) at schools to: Ensure that all educators under their supervision use Curriculum Assessment Policy Statement (CAPS) and Annual Teaching Plan (ATP) as policy instruments to monitor curriculum coverage. Monitor whether educators have covered topics according to the CAPS and ATP timelines. Identify deficiencies on curriculum coverage and agree on corrective measures with educators under their supervision. Report on the status and progress of curriculum coverage for educators under their supervision. The principal of the school consolidate curriculum coverage by HoDs for submission to education districts (NSLA/AAPR) 40

41 Curriculum Coverage Schools Findings and Root Causes Not all educators at schools visited timely covered topics outlined in the ATP and CAPS and some schools HoDs did not compile curriculum coverage reports (all nine provinces had findings) Some principals did not report on the state of curriculum coverage at the end of every school term. (7 provinces except GP and WC had findings) Some schools did not monitor and implement corrective measures where curriculum coverage deficiencies were identified. (7 provinces except FS and WC had findings) Some schools did not establish and implement systems and processes to monitor curriculum coverage. (8 provinces except FS had findings) Root causes for deficiencies Awareness, knowledge and understanding by newly appointed and acting schools officials. Lack of consequences for non-compliance Inadequate monitoring and support by education district officials Absence of annual directive to School Management Teams (SMT) to monitor and report on curriculum coverage Curriculum coverage challenges not identified and captured in the school improvement plans 41

42 Curriculum Coverage Districts Findings and Root Causes Criteria Education district should support schools through assisting principals and educators to improve the quality of teaching and learning through school visits, classroom observation, consultation, cluster meetings, suitable feedback reports and other means. Deficiencies Some education districts did not communicate directives to ensure monitoring of curriculum coverage. (5 provinces had findings (EC, FS, LP, MP, NW) Some education districts did not report on curriculum coverage at all levels. (4 provinces had findings (KZN, LP, NC, WC) Some education districts did not monitor and implement corrective measures where deficiencies identified. (all nine provinces had findings) Root causes Uncoordinated education districts monitoring, support and reporting which results in deficiencies not identified and adequately addressed. (units working n silos) 42

43 Sector Audit findings of the Provincial Education Department on Curriculum Coverage Criteria The PED is responsible for communicating policy directive to education districts and schools in order to create awareness, provide guidance and support district and school officials to implement new changes in policy or any other policy requirement. Deficiencies PED did not ensure that education districts submit consolidated report on curriculum coverage. (3 provinces, FS, KZN, LP) had findings PED did not conduct monitoring of education districts responsibility for curriculum coverage. (7 PEDs) Root causes Ineffective oversight, monitoring and reporting by the PEDs to ensure that standards of education are implemented. 43

44 6.4 Textbook retention and retrieval 44

45 Textbook Retention and Retrieval - DBE Audit Criteria Key Findings Root Causes National policy development on textbook retention and retrieval. Monitoring and support for PEDs on textbook retention systems by PEDs. Analysis of provincial reports on textbook retrieval and retention to identify common challenges and provide guidance and support as remedial action. Policy: The national policy for the provision and management of learning and teaching support material, drafted in 2015, was never finalised and approved. Monitoring and support: DBE did not monitor PEDs to ensure that textbook retention and retrieval deficiencies are identified and support is provided for effective policy implementation. The DBE did not conduct an analysis of provincial reports received from provinces in particular the universal coverage that identify gaps and corrective actions Public comment phase not finalized. In a process of incorporating LTSM management into financial management guidelines for schools. Reports on the monitoring of provinces, education districts and schools does not articulate retention and retrieval deficiencies and remedial actions. Due to poor recordkeeping and reporting at schools, inaccuracies in textbook retention and retrieval not identified in the NSLA and universal coverage reporting. 45

46 Textbook Retention and Retrieval - PED Audit Criteria Findings Root Causes Establish LTSM policies and systems for the provincial environment. Effectively monitor and accurately report on textbook retention and retrieval. Seven of the nine PEDs did not establish policies and/or implement coordinated systems which require schools to implement and accurately report on retention processes, management of textbook shortages and retrieval of textbooks at yearend. Five of the nine PEDs did not effectively monitor and accurately report on the retrieval of textbooks by schools at year end. Uncoordinated processes and systems for textbook retention and retrieval (electronic and/or manual retention and retrieval system at schools). Inadequate staffing in the provincial LTSM line function and the provincial LTSM Committees to effectively monitor and support the functioning of retention and retrieval processes and systems at districts and schools. 46

47 Textbook Retrieval and Retention Education Districts Audit Criteria Findings Root Causes Guidance, monitoring and supporting schools on textbook retention and retrieval. Development of a consolidated report of schools performance regarding textbook retention and retrieval within the education district. In six of the nine PEDs, education districts did not roll-out policies and guidance to schools to ensure textbook management systems In all nine PEDs, education districts did not effectively monitor and evaluate the effectiveness of the textbook management systems at schools. In eight of the nine PEDs, education districts did not implement corrective measures where inadequate textbook management systems existed at schools. In seven of the nine PEDs, education districts did not monitor the availability and adequacy of textbook procurement where textbook shortages existed. In seven of the nine PEDs, education districts did not monitor and report on the retrieval of textbooks at schools at year end. In six of the nine PEDs, education districts did not implement corrective measures to address deficiencies regarding the retrieval of textbooks. Inadequate and ineffective functioning of the LTSM committees at circuit and district level to establish, advocate and monitor the schools textbook retention and retrieval. Circuit Managers and curriculum officials at the selected districts are not capacitated (knowledge and tools) to appropriately evaluate the effectiveness of LTSM management at schools. 47

48 Textbook Retention and Retrieval - Schools Audit Criteria Findings Root Causes Implementation and monitoring of policy textbook retention and retrieval in terms of LTSM Policy, committee establishment, conducting audits, reporting Instances where some schools in: all nine PE Ds had no policy to manage and guide the retention and retrieval of textbooks. seven of the nine PEDs did not conduct an annual LTSM audit and update textboo kinventory registers to reflect the availability of textbooks. eight of the nine PEDs did not order sufficient textboo ks for each learner. eight of the nine PE Ds did not formally impose responsibility on learners and parents whereby they undertake to replace lost or damaged textbooks. eight of the nine PE Ds did not perform quarterly inventory chec ks to identify missing or worn-out textbooks. eight of the nine PEDs did not retrieve textboo ks in a coordinated manner at year end to ensure a 100% retrieval rate eight of the nine PE Ds did not report to districts on textboo k retrievals, reasons for non-return of textboo ks and plans to improve textbook retention. Comprehensive, standardised LTSM policies not adopted at all schools. LT SM challenges such as textboo k retention and retrieval are not included in the school processes such as SMT and SGB oversight records. Inadequate and ineffective functioning of the LTSM committees at schools in establishing and monitoring textbook retention and retrieval. Record keeping not uniform across all grades, subjects and education districts to ensure effective implementation of retention and retrieval processes and systems at schools. 48

49 Pictures depicting the AGSA observation at schools 49

50 6.5 Early Childhood Development Grade R 50

51 Early Childhood Development findings Workbooks for Grade R learners were not available in some schools visited The PED did not ensure that Grade R infrastructure including (overcrowding) and facilities complied with minimum norms and standards The grade R learners ins some of schools visited was above the norm of 1:30 Some schools employed Grade R practitioners without the NQF level 6 qualifications 51

52 ECD Grade R Sector Audit follow-up further assessment During , further assessments for ECD Grade R were made at school level to determine whether the findings identified during have been addressed. The assessment focused on the following areas: Infrastructure classroom size, appropriate and safe playground and ablution facilities Educators - teacher to learner ratio and qualifications Learner and teacher support materials (LTSM) availability of workbooks Deficiencies and root cause The assessment revealed that deficiencies identified pertaining to the areas above, were still prevalent except for LTSM. The provincial departments indicated that certain deficiencies identified require the phasing in of long-term interventions up to Recommendations National Department of basic education should finalise policy framework to guide and monitor the establishment of Grade R at all schools. Provincial departments should adhere to the prescribed Grade R funding requirements and fast track the professionalisation of Grade R teachers. 52

53 6.6 School management and governance 53

54 Deficiencies for School Management and Governance Deficiencies identified Some schools did not submit annual academic performance improvement reports and quarterly performance reports. (8 provinces had findings except WC) Some principals in some schools did not effectively coordinate the functioning of the SGBs. (4 provinces had findings; EC, FS, LP and NW) Some principals did not ensure proper recording and follow-up of learner discipline cases. (6 provinces had findings except GP, NC and WC) Some education districts did not provide guidance and support to principals to: Adhere to annual management processes, Facilitate the SGB functionality in terms of arranging meetings, keeping records of minutes and record on school plans and reports, Managing learner discipline through record keeping and implementing corrective actions 54

55 Overall root causes for deficiencies identified School improvement plans do not reflect realistic challenges of schools and measures to address such challenges. The alignment of school improvement plans with the annual academic performance report. Limited knowledge, understanding and awareness of the roles and responsibilities by newly appointed officials at schools (SMT) and officials appointed in an acting capacity. Lack of consequence management for schools officials not complying with set requirements. Uncoordinated education districts monitoring, support and reporting which results in deficiencies not identified and adequately addressed. Inadequate oversight, monitoring and reporting by the PEDs to ensure that standards of education are implemented. Absence of analysis by DBE of data reported by PEDs to identify deficiencies that makes the policy implementation ineffective. 55

56 Overall recommendations 1. The DBE should conduct an analysis of quarterly and annual reports submitted by PEDs to identify deficiencies or gaps in the policy implementations curriculum coverage, LTSM, ECD and school management and governance.. 2. The DBE should strengthen the monitoring of policy implementations to schools in order to identify deficiencies in the curriculum coverage, LTSM, ECD and school management and governance. 3. The PEDs should strengthen their oversight, guidance and support to education districts to ensure that education districts planning, monitoring and reporting processes and systems capture the state of curriculum coverage, textbook retrieval and retention, adherence to school management and governance, early childhood development and infrastructure maintenance and project management. 4. The education districts monitoring and support processes and systems should focus on the school planning, monitoring and reporting to ensure that it reflects accurate state of curriculum coverage, textbook retention and retrieval, adherence to annual management processes, adequate resourcing of early childhood management and infrastructure maintenance and proper project management. 5. The School Management Teams and School Governing Bodies should ensure that processes and systems identify deficiencies which should be captured in the improvement plans, monitored and reported on quarterly basis. 56

57 School Management and Administration Systems Value- proposition for improving basic education sector School planning processes Self diagnostic assessment Whole School Evaluation School Improvement Plan School performance management School management team (SMT) School committees DSG, LTSM, Learner Discipline. Facilities School performance monitoring and oversight School Governing Body oversight Education districts National and provincial monitoring School Reporting Systems - Monthly reports - Quarterly reports - Annual School Performance Report

58 Stay in touch with the AGSA 58

Budgetary review and recommendations report

Budgetary review and recommendations report Department of Basic Education 03 October 2017 1 Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the supreme

Budgetary review and recommendations report Department of Basic Education 03 October 2017 1 Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the supreme

PFMA. Briefing to the Portfolio Committee: Home Affairs Audit outcomes of the portfolio for the financial year

Briefing to the Portfolio Committee: Home Affairs Audit outcomes of the portfolio for the financial year 2014-15 MFMA 1 1 The AGSA s promise and focus 2 Reputation promise The Auditor-General of South

Briefing to the Portfolio Committee: Home Affairs Audit outcomes of the portfolio for the financial year 2014-15 MFMA 1 1 The AGSA s promise and focus 2 Reputation promise The Auditor-General of South

PFMA. The AGSA s promise, focus and message

2015-16 Briefing to the Portfolio Committee: Public Service Administration and Planning Monitoring and Evaluation Audit outcomes of the PME portfolio for the 2015-16 financial year 2015-16 1 1 The AGSA

2015-16 Briefing to the Portfolio Committee: Public Service Administration and Planning Monitoring and Evaluation Audit outcomes of the PME portfolio for the 2015-16 financial year 2015-16 1 1 The AGSA

Budgetary review and recommendations report

Budgetary review and recommendations report Environmental Affairs Portfolio 03 October 2017 1 Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the supreme

Budgetary review and recommendations report Environmental Affairs Portfolio 03 October 2017 1 Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the supreme

SECTION 9: AUDIT OUTCOMES OF INDIVIDUAL PORTFOLIOS. Consolidated general report on national and provincial audit outcomes for

SECTION 9: AUDIT OUTCOMES OF INDIVIDUAL PORTFOLIOS 6 Consolidated general report on national and provincial audit outcomes for 0- Vote : The Presidency Overall improvement in audit outcomes Financial statements

SECTION 9: AUDIT OUTCOMES OF INDIVIDUAL PORTFOLIOS 6 Consolidated general report on national and provincial audit outcomes for 0- Vote : The Presidency Overall improvement in audit outcomes Financial statements

Taking accountability to improve audit outcomes

Taking accountability to improve audit outcomes INTEGRATED DEVELOPMENT PLAN (IDP) Plan-Do-Check-Act Cycle, also the Deming cycle, courtesy of the International Organization for Standardization 3 4 5 6

Taking accountability to improve audit outcomes INTEGRATED DEVELOPMENT PLAN (IDP) Plan-Do-Check-Act Cycle, also the Deming cycle, courtesy of the International Organization for Standardization 3 4 5 6

Briefing to the Portfolio Committee: Arts and culture Audit outcomes of the portfolio for the financial year.

Briefing to the Portfolio Committee: Arts and culture Audit outcomes of the portfolio for the financial year 11 October 2016 1 1 The AGSA s promise and focus 2 Reputation promise The Auditor-General of

Briefing to the Portfolio Committee: Arts and culture Audit outcomes of the portfolio for the financial year 11 October 2016 1 1 The AGSA s promise and focus 2 Reputation promise The Auditor-General of

PFMA Audit Outcomes of the Telecommunications and Postal Services Portfolio National D October 2014

2013-2014 Audit Outcomes of the Telecommunications and Postal Services Portfolio National D October 2014 Our reputation promise/mission The Auditor-General of South Africa (AGSA) has a constitutional mandate

2013-2014 Audit Outcomes of the Telecommunications and Postal Services Portfolio National D October 2014 Our reputation promise/mission The Auditor-General of South Africa (AGSA) has a constitutional mandate

Briefing to the Portfolio Committee on Transport Audit outcomes of the Transport portfolio for the financial year

Briefing to the Portfolio Committee on Transport Audit outcomes of the Transport portfolio for the financial year 13 October 2015 Reputation promise/mission The Auditor-General of South Africa has a constitutional

Briefing to the Portfolio Committee on Transport Audit outcomes of the Transport portfolio for the financial year 13 October 2015 Reputation promise/mission The Auditor-General of South Africa has a constitutional

Accountability for government spending: From the plan to the people

Accountability for government spending: From the plan to the people 1 Plan-Do-Check-Act Cycle, also the Deming cycle, courtesy of the International Organization for Standardization 2 PLAN DO ACT CHECK

Accountability for government spending: From the plan to the people 1 Plan-Do-Check-Act Cycle, also the Deming cycle, courtesy of the International Organization for Standardization 2 PLAN DO ACT CHECK

MFMA. Audit outcomes of municipalities

0- Audit outcomes of municipalities 0- Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, it exists

0- Audit outcomes of municipalities 0- Reputation promise The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, it exists

General report on the audit outcomes of local government WESTERN CAPE

2011-12 General report on the audit outcomes of local government WESTERN CAPE Our reputation promise The Auditor-General has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South

2011-12 General report on the audit outcomes of local government WESTERN CAPE Our reputation promise The Auditor-General has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South

PFMA Accountability and remedies to address transgressions and poor performance

PFMA 2011-12 Accountability and remedies to address transgressions and poor performance CONSOLIDATED GENERAL REPORT on NATIONAL and PROVINCIAL audit outcomes Our reputation promise/mission The Auditor-General

PFMA 2011-12 Accountability and remedies to address transgressions and poor performance CONSOLIDATED GENERAL REPORT on NATIONAL and PROVINCIAL audit outcomes Our reputation promise/mission The Auditor-General

Briefing to the standing committee on appropriation. Audit outcomes for the financial year Water portfolio

Briefing to the standing committee on appropriation Audit outcomes for the 2014-15 financial year Water portfolio 14 April 2016 Reputation promise/mission The Auditor-General of South Africa has a constitutional

Briefing to the standing committee on appropriation Audit outcomes for the 2014-15 financial year Water portfolio 14 April 2016 Reputation promise/mission The Auditor-General of South Africa has a constitutional

MPUMALANGA EDUCATION

WHEN THE SUN RISES WE WORK HARD TO DELIVER MPUMALANGA EDUCATION PROVINCIAL STRATEGIC IMPERATIVES AND PERSONNEL ALLOCATION, AND ITS IMPACT ON THE NUMBER OF EDUCATOR POSTS FOR A 3 YEAR PERIOD BEGINNING 2017

WHEN THE SUN RISES WE WORK HARD TO DELIVER MPUMALANGA EDUCATION PROVINCIAL STRATEGIC IMPERATIVES AND PERSONNEL ALLOCATION, AND ITS IMPACT ON THE NUMBER OF EDUCATOR POSTS FOR A 3 YEAR PERIOD BEGINNING 2017

PART FOUR: HIGHLIGHTS OF PROVINCIAL AUDIT OUTCOMES FOREWORD

PART FOUR: HIGHLIGHTS OF PROVINCIAL AUDIT OUTCOMES FOREWORD part 4: highlights of provincial audit outcomes 469 PART 4 Highlights of provincial audit outcomes This section of the general report is a high-level

PART FOUR: HIGHLIGHTS OF PROVINCIAL AUDIT OUTCOMES FOREWORD part 4: highlights of provincial audit outcomes 469 PART 4 Highlights of provincial audit outcomes This section of the general report is a high-level

Status of financial management

4 Status of financial management 33 4. Status of financial management The effect of poor internal controls on financial management is reflected and demonstrated in this section. 4.1 Financial statements

4 Status of financial management 33 4. Status of financial management The effect of poor internal controls on financial management is reflected and demonstrated in this section. 4.1 Financial statements

Auditor-General tables three performance audit reports dealing with the pharmaceuticals, water infrastructure and urban renewal projects

1 P a g e 30 November 2016 Auditor-General tables three performance audit reports dealing with the pharmaceuticals, water infrastructure and urban renewal projects PRETORIA Government leadership needs

1 P a g e 30 November 2016 Auditor-General tables three performance audit reports dealing with the pharmaceuticals, water infrastructure and urban renewal projects PRETORIA Government leadership needs

GENERAL REPORT ON THE AUDIT OUTCOMES OF THE FREE STATE LOCAL GOVERNMENT

GENERAL REPORT ON THE AUDIT OUTCOMES OF THE FREE STATE LOCAL GOVERNMENT 2010-11 PR: 188/2012 ISBN: 978-0-621-41075-4 The information and insights presented in this flagship publication of my office are

GENERAL REPORT ON THE AUDIT OUTCOMES OF THE FREE STATE LOCAL GOVERNMENT 2010-11 PR: 188/2012 ISBN: 978-0-621-41075-4 The information and insights presented in this flagship publication of my office are

NATIONAL YOUTH DEVELOPMENT AGENCY ANNUAL REPORT PRESENTATION TO THE STANDING COMMITTEE ON APPROPRIATIONS DATE: 16 October 2013

NATIONAL YOUTH DEVELOPMENT AGENCY ANNUAL REPORT 2012-2013 PRESENTATION TO THE STANDING COMMITTEE ON APPROPRIATIONS DATE: 16 October 2013 PRESENTATION OUTLINE A OVERVIEW OF NYDA 2012/2013 PERFORMANCE B

NATIONAL YOUTH DEVELOPMENT AGENCY ANNUAL REPORT 2012-2013 PRESENTATION TO THE STANDING COMMITTEE ON APPROPRIATIONS DATE: 16 October 2013 PRESENTATION OUTLINE A OVERVIEW OF NYDA 2012/2013 PERFORMANCE B

Eastern Cape General report

Eastern Cape General report on the audit outcomes of local government MFMA 2012-13 Eastern Cape MFMA 2012-13 Our reputation promise/mission The Auditor-General of South Africa has a constitutional mandate

Eastern Cape General report on the audit outcomes of local government MFMA 2012-13 Eastern Cape MFMA 2012-13 Our reputation promise/mission The Auditor-General of South Africa has a constitutional mandate

March Implementation of Broad Based Black Economic Empowerment (B-BBEE) Challenges faced by organs of state

Challenges faced by organs of state") March 2018 Implementation of Broad Based Black Economic Empowerment (B-BBEE) Challenges faced by organs of state Reputation promise of AGSA The Auditor-General of South Africa has a constitutional mandate

March 2018 Implementation of Broad Based Black Economic Empowerment (B-BBEE) Challenges faced by organs of state Reputation promise of AGSA The Auditor-General of South Africa has a constitutional mandate

PFMA Introduction CPD Public Sector April 2018

PFMA Introduction CPD Public Sector April 2018 PFMA - INTRODUCTION 2 PFMA - OBJECTIVE Reasons for the ACT: RDP: maximise service delivery Limited resources vs. 'Unlimited' demands Satisfy constitutional

PFMA Introduction CPD Public Sector April 2018 PFMA - INTRODUCTION 2 PFMA - OBJECTIVE Reasons for the ACT: RDP: maximise service delivery Limited resources vs. 'Unlimited' demands Satisfy constitutional

Fraud and consequence management

9.3 Fraud and consequence management 111 9.3 Fraud and consequence management Accountability for government spending can be improved through acting in a consistent and deliberate manner against those officials

9.3 Fraud and consequence management 111 9.3 Fraud and consequence management Accountability for government spending can be improved through acting in a consistent and deliberate manner against those officials

Table of Content 11/7/2016 2

Mr. Abbey Chikane Executive Chairman Briefing by NHBRC to deal with Irregular Expenditure Portfolio Committee of Human Settlements, Old Assembly 08 November 2016 11/7/2016 1 Table of Content 1. Organogram

Mr. Abbey Chikane Executive Chairman Briefing by NHBRC to deal with Irregular Expenditure Portfolio Committee of Human Settlements, Old Assembly 08 November 2016 11/7/2016 1 Table of Content 1. Organogram

free state Kimi Makwetu Auditor-General

free state MFMA 2013-14 The information and insights presented in this flagship publication are aimed at empowering oversight structures and local and provincial government leaders to focus on those issues

free state MFMA 2013-14 The information and insights presented in this flagship publication are aimed at empowering oversight structures and local and provincial government leaders to focus on those issues

SECTION 2: OVERVIEW OF AUDIT OUTCOMES. Consolidated general report on national and provincial audit outcomes for

SECTION 2: OVERVIEW OF AUDIT OUTCOMES 45 Consolidated general report on national and provincial audit outcomes for 204-5 Figure : Slight improvement in audit outcomes (all auditees) 7% (76) 28% (3) 26%

SECTION 2: OVERVIEW OF AUDIT OUTCOMES 45 Consolidated general report on national and provincial audit outcomes for 204-5 Figure : Slight improvement in audit outcomes (all auditees) 7% (76) 28% (3) 26%

FINANCIAL MANAGEMENT OF PARLIAMENT BILL

REPUBLIC OF SOUTH AFRICA FINANCIAL MANAGEMENT OF PARLIAMENT BILL (As amended by the Select Committee on Financial National Council of Provinces) (The English text is the offıcial text of the Bill) (SELECT

REPUBLIC OF SOUTH AFRICA FINANCIAL MANAGEMENT OF PARLIAMENT BILL (As amended by the Select Committee on Financial National Council of Provinces) (The English text is the offıcial text of the Bill) (SELECT

SABC Presentation to Standarding Committee on Public Accounts

SABC Presentation to Standarding Committee on Public Accounts INTRODUCTION The SABC acknowledges the request from SCOPA to provide specific information relating to the details of irregular, fruitless and

SABC Presentation to Standarding Committee on Public Accounts INTRODUCTION The SABC acknowledges the request from SCOPA to provide specific information relating to the details of irregular, fruitless and

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS

FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS") TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

I Public Works I CGO I Pretoria

I Public Works I CGO I Pretoria 1 Purpose Purpose of the Presentation by the Department of Public Works - To reflect on the 2013/14 Non-Financial and Financial Performance of the Department of Public Works

I Public Works I CGO I Pretoria 1 Purpose Purpose of the Presentation by the Department of Public Works - To reflect on the 2013/14 Non-Financial and Financial Performance of the Department of Public Works

Audit communication and reporting

Audit communication and reporting Report of the Auditor-General to Parliament or the Provincial Legislature on the financial statements and performance information Content Report on the financial statements

Audit communication and reporting Report of the Auditor-General to Parliament or the Provincial Legislature on the financial statements and performance information Content Report on the financial statements

Audit Committee Reporting

Audit Committee Reporting The information contained in this guidance paper is provided for discussion purposes. As such, it is intended to provide the reader and the entity with general information of

Audit Committee Reporting The information contained in this guidance paper is provided for discussion purposes. As such, it is intended to provide the reader and the entity with general information of

Report of the Auditor-General

Report of the Auditor-General of South Africa to Parliament on an investigation at the Commission for Gender Equality October 2010 Published by authority RP 268/2010 ISBN 978-0-621-39781-9 Report of the

Report of the Auditor-General of South Africa to Parliament on an investigation at the Commission for Gender Equality October 2010 Published by authority RP 268/2010 ISBN 978-0-621-39781-9 Report of the

GEORGE MUNICIPALITY POLICY ON UNAUTHORISED, IRREGULAR OR FRUITLESS AND WASTEFUL EXPENDITURE. Approved by Council on 27 May 2015

GEORGE MUNICIPALITY - POLICY ON UNAUTHORISED, IRREGULAR OR FRUITLESS AND WASTEFUL EXPENDITURE Approved by Council on 27 May 2015 CONTENTS 1. BACKGROUND 3 2. OBJECTIVE 3 3. DEFINITIONS 4 4. REGULATORY FRAMEWORK

GEORGE MUNICIPALITY - POLICY ON UNAUTHORISED, IRREGULAR OR FRUITLESS AND WASTEFUL EXPENDITURE Approved by Council on 27 May 2015 CONTENTS 1. BACKGROUND 3 2. OBJECTIVE 3 3. DEFINITIONS 4 4. REGULATORY FRAMEWORK

Office of Public and Indian Housing Real Estate Assessment Center, Washington, DC

Office of Public and Indian Housing Real Estate Assessment Center, Washington, DC Physical Inspection Operations Division Office of Audit, Region 6 Fort Worth, TX Audit Report Number: 2018-FW-0003 August

Office of Public and Indian Housing Real Estate Assessment Center, Washington, DC Physical Inspection Operations Division Office of Audit, Region 6 Fort Worth, TX Audit Report Number: 2018-FW-0003 August

OFFICE OF CHIEF SCHOOL PERFORMANCE OFFICER Summary of State Board of Education Agenda Items November 12, 2014

OFFICE OF CHIEF SCHOOL PERFORMANCE OFFICER Summary of State Board of Education Agenda Items November 12, 2014 OFFICE OF ACCREDITATION 07. Approval to begin the Administrative Procedures Act process: To

OFFICE OF CHIEF SCHOOL PERFORMANCE OFFICER Summary of State Board of Education Agenda Items November 12, 2014 OFFICE OF ACCREDITATION 07. Approval to begin the Administrative Procedures Act process: To

NATIONAL TREASURY MFMA IMPLEMENTATION PLAN - TEMPLATE (Medium Capacity Municipality Only)

") NATIONAL TREASURY MFMA IMPLEMENTATION PLAN - TEMPLATE (Medium Capacity Municipality Only) Name of municipality: SIYANDA DISTRICT (eg: City of Johannesburg) Demarcation code:_dc8 (eg: GT001) Plan Action

NATIONAL TREASURY MFMA IMPLEMENTATION PLAN - TEMPLATE (Medium Capacity Municipality Only) Name of municipality: SIYANDA DISTRICT (eg: City of Johannesburg) Demarcation code:_dc8 (eg: GT001) Plan Action

Focus on Household and Economic Statistics. Insights from Stats SA publications. Nthambeleni Mukwevho Stats SA

Focus on Household and Economic Statistics Insights from Stats SA publications Nthambeleni Mukwevho Stats SA South African Population Results from CS 2016 Source: CS 2016 EC Household Results from CS 2016

Focus on Household and Economic Statistics Insights from Stats SA publications Nthambeleni Mukwevho Stats SA South African Population Results from CS 2016 Source: CS 2016 EC Household Results from CS 2016

SCOPA Review of the 2016/2017, Irregular, Fruitless and Wasteful Expenditure and Accruals for the South African Police Service

SCOPA Review of the 2016/2017, Irregular, Fruitless and Wasteful Expenditure and Accruals for the South African Police Service 29 November 2017 1 BACKGROUND Procurement of goods and services, either by

SCOPA Review of the 2016/2017, Irregular, Fruitless and Wasteful Expenditure and Accruals for the South African Police Service 29 November 2017 1 BACKGROUND Procurement of goods and services, either by

Kingdom of Swaziland. Public Finance Management Bill

Kingdom of Swaziland Public Finance Management Bill CHAPTER ONE: INTERPRETATION, OBJECT, APPLICATION AND AMENDMENT OF THIS ACT 1 Short title This Act may be cited as the Public Finance Management Act 2010.

Kingdom of Swaziland Public Finance Management Bill CHAPTER ONE: INTERPRETATION, OBJECT, APPLICATION AND AMENDMENT OF THIS ACT 1 Short title This Act may be cited as the Public Finance Management Act 2010.

Evaluation of Health Service Delivery Challenges in the EC

Evaluation of Health Service Delivery Challenges in the EC 12 April 2013 ECPC Quality Healthcare Workshop Jay Kruuse Head: Monitoring and Advocacy Public Service Accountability Monitor Rhodes University

Evaluation of Health Service Delivery Challenges in the EC 12 April 2013 ECPC Quality Healthcare Workshop Jay Kruuse Head: Monitoring and Advocacy Public Service Accountability Monitor Rhodes University

REPORT 2015/115 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

Performance reports. General report on the national and provincial audit outcomes for

8 Performance reports 83 8. Performance reports Performance reports are a key accountability mechanism. In the performance reports, auditees report on whether they achieved the objectives that had been

8 Performance reports 83 8. Performance reports Performance reports are a key accountability mechanism. In the performance reports, auditees report on whether they achieved the objectives that had been

Terms of Reference and Annual Planner for National and Provincial Government Audit Committees

Terms of Reference and Annual Planner for National and Provincial Government Audit Committees The information contained in this guidance paper is intended to provide the reader or his/her entity with general

Terms of Reference and Annual Planner for National and Provincial Government Audit Committees The information contained in this guidance paper is intended to provide the reader or his/her entity with general

The status of performance management. Consolidated general report on the national and provincial audit outcomes

4 The status of performance management 57 4. Annual performance reports Figure 1 provides an overview of audit outcomes on the APRs, the APRs submitted with no material misstatements (red line) and the

4 The status of performance management 57 4. Annual performance reports Figure 1 provides an overview of audit outcomes on the APRs, the APRs submitted with no material misstatements (red line) and the

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF BUYENDE DISTRICT LOCAL GOVERNMENT FOR THE YEAR ENDED 30 TH JUNE 2015 REPORT OF THE AUDITOR

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF BUYENDE DISTRICT LOCAL GOVERNMENT FOR THE YEAR ENDED 30 TH JUNE 2015 REPORT OF THE AUDITOR

Provincial Budgeting and Financial Management

Provincial Budgeting and Financial Management Presentation to Select Committee on Appropriations Presenter: Edgar Sishi National Treasury 15 July 2014 INTRODUCTION Provincial functions are assigned by

Provincial Budgeting and Financial Management Presentation to Select Committee on Appropriations Presenter: Edgar Sishi National Treasury 15 July 2014 INTRODUCTION Provincial functions are assigned by

Buffalo City Metropolitan Municipality Presentation to the Select Committee on Finance

Buffalo City Metropolitan Municipality Presentation to the Select Committee on Finance 11 September 2018 Metros financial position at year-ending June 2017 30 June 2015/16 30 June 2016/17 Municipality

Buffalo City Metropolitan Municipality Presentation to the Select Committee on Finance 11 September 2018 Metros financial position at year-ending June 2017 30 June 2015/16 30 June 2016/17 Municipality

Short Learning Programmes

Accountancy@UJ Short Learning Programmes INTERNAL AUDITING AND FINANCIAL CONTROL The purpose of the SLP in Internal Auditing and Financial Control is to provide Chief Financial Officers and accountants

Accountancy@UJ Short Learning Programmes INTERNAL AUDITING AND FINANCIAL CONTROL The purpose of the SLP in Internal Auditing and Financial Control is to provide Chief Financial Officers and accountants

STEP Academy Trust Finance Policy

STEP Academy Trust Finance Policy Date of Policy: SEPTEMBER 2015 CONTENTS 1 Introduction 1 2 Organisation of Responsibility and Accountability 1 3 Financial planning and Budget Monitoring 3 4 Personnel

STEP Academy Trust Finance Policy Date of Policy: SEPTEMBER 2015 CONTENTS 1 Introduction 1 2 Organisation of Responsibility and Accountability 1 3 Financial planning and Budget Monitoring 3 4 Personnel

FINANCIALS South African Broadcasting Corporation [SOC] Ltd SABC Annual Report

![FINANCIALS South African Broadcasting Corporation [SOC] Ltd SABC Annual Report](/thumbs/93/114271806.jpg "FINANCIALS South African Broadcasting Corporation [SOC] Ltd SABC Annual Report") 84 FINANCIALS South African Broadcasting Corporation [SOC] Ltd SABC Annual Report 2014 2015 85 ANNUAL FINANCIAL STATEMENTS STATEMENT OF RESPONSIBILITY AND CONFIRMATION OF ACCURACY OF PERFORMANCE INFORMATION

84 FINANCIALS South African Broadcasting Corporation [SOC] Ltd SABC Annual Report 2014 2015 85 ANNUAL FINANCIAL STATEMENTS STATEMENT OF RESPONSIBILITY AND CONFIRMATION OF ACCURACY OF PERFORMANCE INFORMATION

AGSA Strategic plan and budget SCoAG engagement 17 November 2017

AGSA Strategic plan and budget 2018-2021 SCoAG engagement 17 November 2017 Reputation promise The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI)

AGSA Strategic plan and budget 2018-2021 SCoAG engagement 17 November 2017 Reputation promise The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI)

NOTICE 125 OF Internal control, as indicated by the reference to financial management in sections 4(1) and (3) of the PAA 4

and (3) of the PAA 4") STAATSKOERANT, 11 FEBRUARIE 2015 No. 38464 3 GENERAL NOTICE NOTICE 125 OF 2015 DIRECTIVE ISSUED IN TERMS OF THE PUBLIC AUDIT ACT, 2004 Under the powers vested in me by section 2, read with section 13(3)

STAATSKOERANT, 11 FEBRUARIE 2015 No. 38464 3 GENERAL NOTICE NOTICE 125 OF 2015 DIRECTIVE ISSUED IN TERMS OF THE PUBLIC AUDIT ACT, 2004 Under the powers vested in me by section 2, read with section 13(3)

Municipal Infrastructure Grant Baseline Study

Municipal Infrastructure Grant Baseline Study August 2008 Published July 2009 Disclaimer This Research Report for the Municipal Infrastructure Grant (MIG) Baseline Study has been prepared using information

Municipal Infrastructure Grant Baseline Study August 2008 Published July 2009 Disclaimer This Research Report for the Municipal Infrastructure Grant (MIG) Baseline Study has been prepared using information

FINANCIAL REGULATIONS AUGUST 2012 EFFECTIVE DATE 1 APRIL 2013

FINANCIAL REGULATIONS AUGUST 2012 EFFECTIVE DATE 1 APRIL 2013 CONTENTS PAGE PREAMBLE... 4 PRINCIPLES OF SOUND FINANCIAL MANAGEMENT... 4 CHAPTER 1 FINANCIAL REGULATIONS... 6 PART I - PURPOSE AND SCOPE...

FINANCIAL REGULATIONS AUGUST 2012 EFFECTIVE DATE 1 APRIL 2013 CONTENTS PAGE PREAMBLE... 4 PRINCIPLES OF SOUND FINANCIAL MANAGEMENT... 4 CHAPTER 1 FINANCIAL REGULATIONS... 6 PART I - PURPOSE AND SCOPE...

REPORT OF THE SELECT COMMITTEE ON FINANCE ON THE PROVINCIAL TREASURIES EXPENDITURE REVIEW FOR THE 2014/15 FINANCIAL YEAR, DATED 14 OCTOBER 2015

REPORT OF THE SELECT COMMITTEE ON FINANCE ON THE PROVINCIAL TREASURIES EXPENDITURE REVIEW FOR THE 2014/15 FINANCIAL YEAR, DATED 14 OCTOBER 2015 1. Introduction and Background The Select Committee on Finance

REPORT OF THE SELECT COMMITTEE ON FINANCE ON THE PROVINCIAL TREASURIES EXPENDITURE REVIEW FOR THE 2014/15 FINANCIAL YEAR, DATED 14 OCTOBER 2015 1. Introduction and Background The Select Committee on Finance

The Presidency Department of Performance Monitoring and Evaluation

The Presidency Department of Performance Monitoring and Evaluation Briefing to the Standing Committee on Appropriations on the Strategic Plan and Annual Performance Plan for the 2012/13 financial year

The Presidency Department of Performance Monitoring and Evaluation Briefing to the Standing Committee on Appropriations on the Strategic Plan and Annual Performance Plan for the 2012/13 financial year

AUDITOR-GENERAL OF SOUTH AFRICA NO MAY 2016

Auditor-General of South Africa/ Ouditeur-Generaal van Suid-Afrika 574 Public Audit Act (25/2004): Directive issued in terms of the Public Audit Act 40021 STAATSKOERANT, 27 MEI 2016 No. 40021 33 AUDITOR-GENERAL

Auditor-General of South Africa/ Ouditeur-Generaal van Suid-Afrika 574 Public Audit Act (25/2004): Directive issued in terms of the Public Audit Act 40021 STAATSKOERANT, 27 MEI 2016 No. 40021 33 AUDITOR-GENERAL

Government Gazette REPUBLIC OF SOUTH AFRICA. AIDS HELPLINE: Prevention is the cure

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

I n t r o d u c t i o n

T he District Health Systems (DHS) across South Africa are the decentralised building blocks of the National Health System. The aim of the DHS is to have decisions made locally about services and resources.

T he District Health Systems (DHS) across South Africa are the decentralised building blocks of the National Health System. The aim of the DHS is to have decisions made locally about services and resources.

TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

Performance Monitoring Report

Eastern Cape Department of Health Performance Monitoring Report 2006/07 November 2007 Lesley Odendal Monitoring and Research Programme, Public Service Accountability Monitor For more information contact

Eastern Cape Department of Health Performance Monitoring Report 2006/07 November 2007 Lesley Odendal Monitoring and Research Programme, Public Service Accountability Monitor For more information contact

Children and South Africa s Budget

Children and South Africa s Budget Children and South Africa s Budget 1. Macro context 2. Health 3. Education 4. Social Development 1. MACRO CONTEXT South Africa Key message 1 The nearly 20 million children

Children and South Africa s Budget Children and South Africa s Budget 1. Macro context 2. Health 3. Education 4. Social Development 1. MACRO CONTEXT South Africa Key message 1 The nearly 20 million children

External Audit. April 2012

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

Unit Standard : Apply the principles of budgeting within a municipality. Karel van der Molen

Unit Standard 116345: Apply the principles of budgeting within a municipality Karel van der Molen Group The full programme 1. Strategic Management; Budgeting Implementation & Performance Management 2.

Unit Standard 116345: Apply the principles of budgeting within a municipality Karel van der Molen Group The full programme 1. Strategic Management; Budgeting Implementation & Performance Management 2.

Swellendam Municipality 2015/16 Combined Assurance Plan SWELLENDAM MUNICIPALITY 2015/2016 COMBINED ASSURANCE PLAN

SWELLENDAM MUNICIPALITY 2015/2016 COMBINED ASSURANCE PLAN APPROVED BY COUNCIL PER ITEM C20 ON 30 SEPTEMBER 2015 i Contents 1 Introduction 3 2 Objectives 3 3 Approach 3 4 Roles and Responsibilties 3 4.1

SWELLENDAM MUNICIPALITY 2015/2016 COMBINED ASSURANCE PLAN APPROVED BY COUNCIL PER ITEM C20 ON 30 SEPTEMBER 2015 i Contents 1 Introduction 3 2 Objectives 3 3 Approach 3 4 Roles and Responsibilties 3 4.1

FRUITLESS AND WASTEFUL EXPENDITURE

FRUITLESS AND WASTEFUL EXPENDITURE BRIEFING TO SCOPA Presenter: Lindy Bodewig Chief Director: Technical Support Services 19 August 2014 Discovery of unwanted expenditures Accounting officer to record details

FRUITLESS AND WASTEFUL EXPENDITURE BRIEFING TO SCOPA Presenter: Lindy Bodewig Chief Director: Technical Support Services 19 August 2014 Discovery of unwanted expenditures Accounting officer to record details

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

Annual governance report

Annual governance report University Hospitals of Morecambe Bay NHS Foundation Trust Audit 2011/12 Audit Commission Annual governance report 1 Contents Key messages... 3 Before I give my opinion... 4 Financial

Annual governance report University Hospitals of Morecambe Bay NHS Foundation Trust Audit 2011/12 Audit Commission Annual governance report 1 Contents Key messages... 3 Before I give my opinion... 4 Financial

Annual Financial Statements 2018

Annual Financial Statements 2018 A A www.transnet.net U D Annual Financial Statements 2018 TRANSNET Annual Financial Statements 2018 1 1 Contents 2 4 12 14 128 129 34 Performance highlights 1 Approval

Annual Financial Statements 2018 A A www.transnet.net U D Annual Financial Statements 2018 TRANSNET Annual Financial Statements 2018 1 1 Contents 2 4 12 14 128 129 34 Performance highlights 1 Approval

Initiative of National Department of Health to accelerate Health Infrastructure Service Delivery

Initiative of National Department of Health to accelerate Health Infrastructure Service Delivery To manage the mentioned challenges, in 2010/11, Financial year, the National Department of Health (NDOH)

Initiative of National Department of Health to accelerate Health Infrastructure Service Delivery To manage the mentioned challenges, in 2010/11, Financial year, the National Department of Health (NDOH)

Our reputation promise/mission. General report on the national and provincial audit outcomes for

The information and insights presented in this flagship publication of my office are aimed at empowering oversight structures and executive leaders to focus on those issues that will result in reliable

The information and insights presented in this flagship publication of my office are aimed at empowering oversight structures and executive leaders to focus on those issues that will result in reliable

Internal Audit Report

Internal Audit Report MENORAH HIGH SCHOOL FOR GIRLS 13 July 2017 To: Copied to: Chair of Governors Headteacher Education and Skills Director Commissioning Director (Children and Young People) School Finance

Internal Audit Report MENORAH HIGH SCHOOL FOR GIRLS 13 July 2017 To: Copied to: Chair of Governors Headteacher Education and Skills Director Commissioning Director (Children and Young People) School Finance

CHAPTER 7 CONTEXTUALIZATION OF CRITICAL PUBLIC FINANCE MANAGEMENT ISSUES

CHAPTER 7 CONTEXTUALIZATION OF CRITICAL PUBLIC FINANCE MANAGEMENT ISSUES 7.1 INTRODUCTION: During the study, research reveals that public finance management system has evolved in the Public Service. It

CHAPTER 7 CONTEXTUALIZATION OF CRITICAL PUBLIC FINANCE MANAGEMENT ISSUES 7.1 INTRODUCTION: During the study, research reveals that public finance management system has evolved in the Public Service. It

REPORT THE AUDITOR-GENERAL THE FINANCIAL OPERATIONS BUSIA COUNTY ASSEMBLY

REPUBLIC OF KENYA REPORT OF THE AUDITOR-GENERAL ON THE FINANCIAL OPERATIONS OF BUSIA COUNTY ASSEMBLY FOR THE PERIOD 1 JULY 2013 TO 30 JUNE 2014 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 Introduction...

REPUBLIC OF KENYA REPORT OF THE AUDITOR-GENERAL ON THE FINANCIAL OPERATIONS OF BUSIA COUNTY ASSEMBLY FOR THE PERIOD 1 JULY 2013 TO 30 JUNE 2014 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 Introduction...

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

Briefing to the Parliamentary Portfolio

Briefing to the Parliamentary Portfolio Committee on Communications 2016 17 FY Annual Report Contents Organisational Mandate Strategic Fit - Government s Priority Outcomes Strategic Outcome Oriented Goals:

Briefing to the Parliamentary Portfolio Committee on Communications 2016 17 FY Annual Report Contents Organisational Mandate Strategic Fit - Government s Priority Outcomes Strategic Outcome Oriented Goals:

INTERNAL AUDIT DIVISION REPORT 2016/155. Audit of the United Nations Human Settlements Programme project management process

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

Materiality and Significance Framework applicable to the Financial Year

APPENDICES APPENDIX 1 Materiality and Significance Framework applicable to the 2007-08 Financial Year Index 1. Background 72 2. Broad Framework for Robben Island Museum 73 3. RIM General Approach to Qualitative

APPENDICES APPENDIX 1 Materiality and Significance Framework applicable to the 2007-08 Financial Year Index 1. Background 72 2. Broad Framework for Robben Island Museum 73 3. RIM General Approach to Qualitative

DEPARTMENT OF BASIC EDUCATION. No August SOUTH AFRICAN SCHOOLS ACT, 1996 (ACT NO 84 of 1996)

") STAATSKOERANT, 27 AUGUSTUS 2012 No. 35617 3 GOVERNMENT NOTICE DEPARTMENT OF BASIC EDUCATION No. 646 27 August 2012 SOUTH AFRICAN SCHOOLS ACT, 1996 (ACT NO 84 of 1996) AMENDED NATIONAL NORMS AND STANDARDS

STAATSKOERANT, 27 AUGUSTUS 2012 No. 35617 3 GOVERNMENT NOTICE DEPARTMENT OF BASIC EDUCATION No. 646 27 August 2012 SOUTH AFRICAN SCHOOLS ACT, 1996 (ACT NO 84 of 1996) AMENDED NATIONAL NORMS AND STANDARDS

Inform Practice Note #19

Inform Practice Note #19 June 2009 (Version 1 - June 2009) Streamlining Payment Processes cidb s Inform Practice notes provide guidance and clarity in achieving client objectives in construction procurement

Inform Practice Note #19 June 2009 (Version 1 - June 2009) Streamlining Payment Processes cidb s Inform Practice notes provide guidance and clarity in achieving client objectives in construction procurement

2) Budgetary Comparison Schedule - General Fund and All Major Special Revenue Funds

Budgetary Comparison Schedule - General Fund and All Major Special Revenue Funds") Herbein + Company, Inc. 2763 Century Boulevard Reading, PA 19610 P: 610.378.1175 F: 610.378.0999 www.herbein.com March 22, 2018 Board of Directors Oley Valley School District 17 Jefferson Street Oley,

Herbein + Company, Inc. 2763 Century Boulevard Reading, PA 19610 P: 610.378.1175 F: 610.378.0999 www.herbein.com March 22, 2018 Board of Directors Oley Valley School District 17 Jefferson Street Oley,

Internal, Operational, and Compliance Auditing

CHAPTER 21 Internal, Operational, and Compliance Auditing Review Questions 21 1 Internal auditing may be defined as an independent, objective assurance and consulting activity designed to add value and

CHAPTER 21 Internal, Operational, and Compliance Auditing Review Questions 21 1 Internal auditing may be defined as an independent, objective assurance and consulting activity designed to add value and

COJ: MAYORAL COMMITTEE GROUP AUDIT COMMITTEE

REPORT OF THE GROUP AUDIT COMMITTEE OF THE CITY OF JOHANNESBURG METROPOLITAN MUNICIPALITY ON THE PROGRESS TO DATE IN THE EVALUATION OF THE DRAFT ANNUAL FINANCIAL STATEMENTS FOR THE FINANCIAL YEAR ENDED

REPORT OF THE GROUP AUDIT COMMITTEE OF THE CITY OF JOHANNESBURG METROPOLITAN MUNICIPALITY ON THE PROGRESS TO DATE IN THE EVALUATION OF THE DRAFT ANNUAL FINANCIAL STATEMENTS FOR THE FINANCIAL YEAR ENDED

REPORT OF INDEPENDENT AUDITORS AND SINGLE AUDIT REPORTS SOUTHERN CALIFORNIA REGIONAL RAIL AUTHORITY

REPORT OF INDEPENDENT AUDITORS AND SINGLE AUDIT REPORTS SOUTHERN CALIFORNIA REGIONAL RAIL AUTHORITY June 30, 2017 Table of Contents Report of Independent Auditors on the Financial Statements for the Year

REPORT OF INDEPENDENT AUDITORS AND SINGLE AUDIT REPORTS SOUTHERN CALIFORNIA REGIONAL RAIL AUTHORITY June 30, 2017 Table of Contents Report of Independent Auditors on the Financial Statements for the Year

REPORT 2016/054 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

SCOPA REVIEW OF IRREGULAR, FRUITLESS AND WASTEFUL EXPENDITURE OF THE DEPARTMENT OF MILITARY VETERANS DATED 15 NOVEMBER 2016

SCOPA REVIEW OF 2015 2016 IRREGULAR, FRUITLESS AND WASTEFUL EXPENDITURE OF THE DEPARTMENT OF MILITARY VETERANS DATED 15 NOVEMBER 2016 PRESENTED BY ACTING DIRECTOR-GENERAL: MAX OZINSKY 1 PRESENTATION OUTLOOK

SCOPA REVIEW OF 2015 2016 IRREGULAR, FRUITLESS AND WASTEFUL EXPENDITURE OF THE DEPARTMENT OF MILITARY VETERANS DATED 15 NOVEMBER 2016 PRESENTED BY ACTING DIRECTOR-GENERAL: MAX OZINSKY 1 PRESENTATION OUTLOOK

Financial Governance Audits

Internal Audit Report s 2013/14 Issued to: Simon Newland Assistant Director (Education Provision and Access) Waqaas Munir Finance Manager - Education & Early Years Report Status: Final for Information

Internal Audit Report s 2013/14 Issued to: Simon Newland Assistant Director (Education Provision and Access) Waqaas Munir Finance Manager - Education & Early Years Report Status: Final for Information

PROGRESS WITH THE NATIONAL INFRASTRUCTURE MAINTENANCE STRATEGY

PROGRESS WITH THE NATIONAL INFRASTRUCTURE MAINTENANCE STRATEGY Kevin Wall CSIR, P.O. Box 395, Pretoria, 0001; Cell: 082-4593618, Email: kwall@csir.co.za ABSTRACT The National Infrastructure Maintenance

PROGRESS WITH THE NATIONAL INFRASTRUCTURE MAINTENANCE STRATEGY Kevin Wall CSIR, P.O. Box 395, Pretoria, 0001; Cell: 082-4593618, Email: kwall@csir.co.za ABSTRACT The National Infrastructure Maintenance

PRESENTATION TO THE STANDING COMMITTEE ON APPROPRIATIONS BRIEFING ON THE 2015 APPROPRIATION BILL 19 MAY 2015

PRESENTATION TO THE STANDING COMMITTEE ON APPROPRIATIONS BRIEFING ON THE 2015 APPROPRIATION BILL 19 MAY 2015 Introduction The PSC is established in terms of Chapter 10 of the Constitution. It derives its

PRESENTATION TO THE STANDING COMMITTEE ON APPROPRIATIONS BRIEFING ON THE 2015 APPROPRIATION BILL 19 MAY 2015 Introduction The PSC is established in terms of Chapter 10 of the Constitution. It derives its

Pelican Educational Foundation, Inc. A Nonprofit Organization