4/25/2017. Sample Agenda ~ Spring Meeting DEVELOPING A TRAINING PROGRAM FOR NEW LOCAL SCHOOL BOOKKEEPERS MAY 3, 2017

|

|

|

- Quentin Wright

- 5 years ago

- Views:

Transcription

April May (Budget Preparation and End of School Checklist) Summer Conference")

1 DEVELOPING A TRAINING PROGRAM FOR NEW LOCAL SCHOOL BOOKKEEPERS MAY 3, 2017 AASBO Annual Conference Karen O Bannon, CSFO Madison County Schools kobannon@mcssk12.org Training Program for Local School Bookkeepers Professional Development: Four Times Per Year (Time Lines) April May (Budget Preparation and End of School Checklist) Summer Conference (Payroll/Accounting Manual Topics and Updates/Special Guests) September (Fiscal Year End Checklist) December (Calendar Year End) All Bookkeepers (Networking) Local Support (On Site Training and Job Shadowing) Financial Procedures Manual Sample Agenda ~ Spring Meeting Introductions (New Bookkeepers) Computer Services Budgets Extended Day/Daycare Rates Physical Inventory End of School Checklist May Calendar Deadlines Local School Accounting Bookkeeper s Meeting April 19, :00 AM Central Office Auditorium **Important Date** Summer Workshop June 20 & June 21 Career Technical Center Auditorium 1

2 Sample Agenda ~ Summer Conference FINANCE MATTERS Summer Workshop June 20 and June 21 Wednesday, June 20 th 7:30 a.m. Sign In 7:45 8:00 a.m. Welcome by Superintendent 8:00 10:00 a.m. Alabama State Department Dennis Heard Followed by Questions and Answers from Audience 10:00 10:15 a.m. BREAK 10:15 12:00 p.m. State Examiners Office Kathy Wren Followed by Questions and Answers from Audience 12:00 12:15 p.m. BREAK 12:15 1:00 p.m. LUNCH Presentation Karen O Bannon 2015 Audit Findings Our Weaknesses Our Strengths Auditor Recommendations for Improvement 1:00 2:45 p.m. Madison County Board of Education Financial Policy Breaking it all Down Principal and Bookkeeper Responsibilities Additional Information: Financial Reports Internal Auditing Ethics Policy Karen O Bannon, Chief Financial Officer Gena Groce, Accounting Supervisor Janet Elliott, Local School Accounting Supervisor 2:45 3:00 p.m. BREAK 3:00 4:00 p.m. Jim Owens Motivational Speaker Thriving on Changes Sample Agenda ~ Summer Conference Thursday, June 21 st 7:45 a.m. Sign In 8:00 9:30 a.m. General Meeting Back to School Janet Elliott Review and Feedback from Wednesday Your Thoughts? Auditor Review Recommendations 9:30 9:45 a.m. BREAK 9:45 10:30 a.m. Payroll Issues Payroll Manager 10:30 11:30 a.m. Round Table Discussion 11:30 1:00 p.m. LUNCH 1:00 2:00 p.m. Workshop (Laptop brought from school) Setting up Allocation Tracking (Will need listing of teacher names) Sample Checklist ~ September 2

3 Sample Agenda ~ December Meeting Christmas Breakfast (Potluck) ARI Funds Calendar Year Close/1099 Vendors Coding Issues Payroll Issues Accounts Payable Issues Receipting Issues Miscellaneous Accounting Items Contracts VS Personnel Actions Tickets Ticket Reconciliations EZ Tickets Absences AESOP Purchasing Cards My School Fees Deadlines Local School Accounting Bookkeeper s Meeting December 8, :30 AM Central Office Auditorium Mission of Budget Process The mission of the budget process is to help decision makers make informed choices about the services and needs of a particular activity or local school function. Elements of the Budget Process Develop a Budget Consistent with Goals Develop a process for preparing and adopting a budget/communication Evaluate financial resources and prioritize needs Prepare budget based on decisions from team Evaluate Performance Monitor, measure, evaluate, and report Adjust or amend if necessary 3

4 Budgeting for Activity Funds Budgeting is the process of planning resources and prioritizing needs of an organization. In most cases, for a governmental entity the budget represents the legal authority to spend money. The budget also provides an important tool for the control and evaluation of resources and the uses of those resources. It is a tool to evaluate financial performance by comparing budgeted and actual operations. Bottom line, the budget is linked to financial accountability. Budget Responsibilities Delegate responsibilities for the budget (Teamwork) The educational decisions and the expenditure of approved budget funds must be controlled by the appropriate sponsor. The local school office (administrators and bookkeepers) responsibility is to assist with the organization and administration of the budget, to monitor and track spending within established guidelines. BUDGETING CLASSROOM INSTRUCTIONAL SUPPORT (CIS) FUNDS 4

5 Student Materials Elements of CIS Technology Library Enhancement Professional Development Common Purchases Classroom Instructional Support Funds PERMISSIBLE EXPENDITURES. Monies allocated for classroom instructional support may be spent for classroom instructional support purposes only, to be used either by classroom teachers or students in each teacher s respective classes. It shall be permissible to expend these monies on instructional equipment and electrical equipment which is actually utilized with students in the teacher s classroom. UNSPENT FUNDS. Any funds appropriated for classroom instructional support but not expended according to this section by the end of each fiscal year shall revert to the Education Trust Fund. TRANSFER WITH TEACHER DISALLOWED. Classroom instructional support monies are to be expended on behalf of students at a specific school and are not transportable with the teacher if the teacher is transferred to another school. ANNUAL AUDIT. All expenditures for classroom instructional support and related documents by each county and city board of education shall be subject to audit by the Examiners of Public Accounts/Private CPA Firm. It s the Law Not the CSFO Ala. Code 1975, Student Materials (Teacher Fee) allocations may not be used to supplement common purchases (Ala. Code 1975, (13)) note: $200 per unit for common purchases was appropriated in These funds have not been allocated since that time. Student Materials (Teacher Fee) allocations are not subject to a vote by the budget committee. 5

4 Teachers Elected Annually Voting by Secret Balllot Majority Vote Budget Committee The committee should elect:")

6 Budget Committee Each school must have a budget committee. The budget committee should be comprised of 5 members Principal (or designee) 4 Teachers Elected Annually Voting by Secret Balllot Majority Vote Budget Committee The committee should elect: chairperson secretary responsible for keeping minutes and actions taken to approve the budgets during the secret balloting process. The committee may form advisory committees. The committee must propose a budget for CIS, excluding student materials/teacher fee. Budgets for Library Enhancement funds are to be developed in consultation with the school s media specialist. Professional Development and Technology budgets should be consistent with the system s PD and Technology Plans Approval of Budgets Proposed budgets should be submitted to teachers at a called meeting. Teachers must be given at least two workdays to review the proposed budget prior to taking a vote. Voting must be by secret ballot. Budget must be approved by majority vote. 6

7 Local School Funds Lines of Authority Board of Education. The Board of Education adopts policies to govern the establishment and operation of all activity funds. The district s auditors reviews these policies for sound accounting and reporting principles. The Board approves the budget and financial statements as recommended by the Superintendent. Superintendent. The Superintendent is directly responsible to the Board of Education for administering all Board policies and recommends the budget and financial statements to the Board for approval. Chief School Financial Officer. The Chief School Financial Officer has the overall responsibility for accounting for and reporting all funds, including district and student activity funds, to the Board. The Chief School Financial Officer is also responsible for implementing and enforcing appropriate internal control procedures as well as monitoring and managing the financial resources. Principal. The Principal at each school is the activity fund supervisor and has overall responsibility for the operation of all activity funds, including collecting and depositing activity fund monies; approving disbursements of student activity fund monies; and adequately supervising all bookkeeping responsibilities. The activity fund supervisor should be a signatory to all disbursements, including checks drawn on the activity fund. Fiduciary Responsibility of the Principal Ultimately it is the Principal s responsibility to ensure that funds are collected and disbursed in accordance with local board policies. The Principal should be familiar with the Financial Procedures for the School District to have a basic understanding of the accounting regulations for schools. (mcssk12.org/departments/finance/financial Procedures) The Principal should work with the bookkeeper and staff when preparing the local school annual budgets. (April May) 7

sources /appropriations for the general operations of the local school under the control and direction of the Principal.")

8 Local School Activity Funds Activity funds are established to direct and account for monies available and used at the local school level. Activity funds are unique to school districts. The distinction is based on the purpose of the funds, that is, the programs and activities supported by the funds. The classifications which are commonly recognized are: district activity funds student activity funds parent support or school related organization funds Public Local School Funds Funds received from public (tax) sources /appropriations for the general operations of the local school under the control and direction of the Principal. Public funds are restricted to the same legal requirements as system funds at the district level. Funds are generally classified as public when the following criteria are met: A) Money generated school-wide B) Money used for all students instead of individual group C) Money controlled by the Principal or a school employee Public Funds - Revenue Admissions Appropriations Concessions Commission Dues & Fees Required Fines & Penalties Fund Raisers* Grants Sales Donations* *In specific situations, these may be considered Non-Public 8

, and are not under the direct control of the Principal, although he/she has the authority to")

Money generated by a")

9 Non-Public Local School Funds Funds received by an organization s or club s sponsor or officer not usually used for the general operations of the school. Non-Public funds are restricted to the intent and authorization of various organizations (their officers and members), and are not under the direct control of the Principal, although he/she has the authority to prohibit inappropriate expenditures. Funds are generally classified as non-public when the following criteria are met: A) Money generated by a particular group B) Money used for that particular group C) Money controlled by the students and/or a parental organization Non-Public Funds - Revenue Dues & Fees Self imposed by clubs or classes Fund Raisers* Donations* Accommodations* Other* *In specific situations, these may be considered public funds School Related Organizations 9

10 Non-Public Activity Funds Parent Support Organization Funds (School Related Organizations) School districts and student groups are also increasingly benefited by affiliated organizations that support curricular, co curricular, and extracurricular activities. Affiliated organizations include groups such as Parent-Teacher Associations (PTAs), Parent-Teacher Organizations (PTOs), school foundations, and athletic booster clubs. Contributions by these groups often include supplies, materials, equipment, and even school facilities, such as weight training rooms. Financial records may be included in the school books and classified as non-public funds or may be maintained outside the school records depending on the board s policy. Additional procedures should be in place for those records maintained outside the school books. (Only PTA/PTO Funds for MCBOE) Specific Requirements Parent organizations such as PTAs and PTOs that maintain their own financial records must provide: Proof of employer identification number Annual audit report Financial records to the school s auditors and authorized school employees upon request Required financial reports Fidelity Bond for Treasurer Again, a school employee may not hold a leadership role in a parent organization, i.e., President or Treasurer, if the funds are to remain non-public. Standardized Account Codes LEA Manual 10

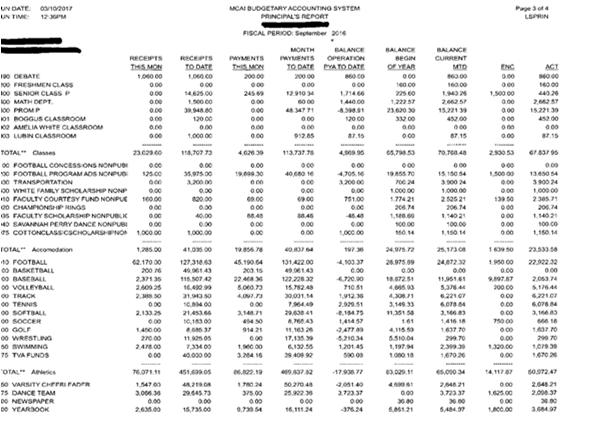

11 Principal s Activity Report HIGH SCHOOL 11

12 12

13 MIDDLE SCHOOL ELEMENTARY SCHOOL Questions & Answers 13

2/29/2016. Budget Preparation for Local Schools/School Districts. Talking Points. Budgeting for Activity Funds. What is a budget? Why we budget?

Budget Preparation for Local Schools/School Districts ALABAMA ASSOCIATION OF SCHOOL BUSINESS OFFICIALS (AASBO) LOCAL SCHOOL FINANCIAL MANAGEMENT CERTIFICATION PROGRAM MARCH 8, 2016 Talking Points What

Budget Preparation for Local Schools/School Districts ALABAMA ASSOCIATION OF SCHOOL BUSINESS OFFICIALS (AASBO) LOCAL SCHOOL FINANCIAL MANAGEMENT CERTIFICATION PROGRAM MARCH 8, 2016 Talking Points What

4/30/2015 FINANCIAL PROCEDURES FOR LOCAL SCHOOLS. Accounting for Extra-Curricular Activities. Student Organizations

Accounting for Extra-Curricular Activities Sonja Peaspanen Alabama Department of Education May 5, 2015 FINANCIAL PROCEDURES FOR LOCAL SCHOOLS APPROVED June 10, 2010 www.alsde.edu Department Offices LEA

Accounting for Extra-Curricular Activities Sonja Peaspanen Alabama Department of Education May 5, 2015 FINANCIAL PROCEDURES FOR LOCAL SCHOOLS APPROVED June 10, 2010 www.alsde.edu Department Offices LEA

Booster and Support Organization Guidelines

Booster and Support Organization Guidelines July 2016 Parent Support Organizations provide an invaluable service to our schools. Many of our programs and activities could not exist without your volunteer

Booster and Support Organization Guidelines July 2016 Parent Support Organizations provide an invaluable service to our schools. Many of our programs and activities could not exist without your volunteer

Accounting Procedures for Student and Parent Organizations

Accounting Procedures for Student and Parent Organizations AASBO LSFM Program May 2015 David Smith, Executive Director Alabama Association of School Business Officials 1 Accounting Procedures for Student

Accounting Procedures for Student and Parent Organizations AASBO LSFM Program May 2015 David Smith, Executive Director Alabama Association of School Business Officials 1 Accounting Procedures for Student

Autauga County Schools. Parent Support Organizations Guidelines and Procedures

Autauga County Schools Parent Support Organizations Guidelines and Procedures Revised 6/27/2017 TABLE OF CONTENTS GENERAL INFORMATION. I. ORGANIZATION FORMATION OF ORGANIZATION BYLAWS OFFICERS AND DIRECTORS

Autauga County Schools Parent Support Organizations Guidelines and Procedures Revised 6/27/2017 TABLE OF CONTENTS GENERAL INFORMATION. I. ORGANIZATION FORMATION OF ORGANIZATION BYLAWS OFFICERS AND DIRECTORS

Communication and Public Information

School Fund Raising Guidelines Introduction Student Activity accounts are those funds which are owned, operated, and managed by organizations, clubs, or groups within the student body under the guidance

School Fund Raising Guidelines Introduction Student Activity accounts are those funds which are owned, operated, and managed by organizations, clubs, or groups within the student body under the guidance

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY TABLE OF CONTENTS Section Page Number Guidelines 1-3 Annual Checklist 4 Forms and Instructions 5-9 Technical Assistance 10-12 (Non Authoritative/Best

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY TABLE OF CONTENTS Section Page Number Guidelines 1-3 Annual Checklist 4 Forms and Instructions 5-9 Technical Assistance 10-12 (Non Authoritative/Best

FUND RAISERS. Procedures for Fundraising and Other Revenue Programs at the Local School

Procedures for Fundraising and Other Revenue Programs at the Local School Accounting Issues Related to Fundraisers, Cash Receipts, Go Fund Me, and Similar Programs AASBO LSFM CERTIFICATION PROGRAM SONJA

Procedures for Fundraising and Other Revenue Programs at the Local School Accounting Issues Related to Fundraisers, Cash Receipts, Go Fund Me, and Similar Programs AASBO LSFM CERTIFICATION PROGRAM SONJA

FISCAL ACCOUNTABILITY FOR LOCAL SCHOOL BOARDS

FISCAL ACCOUNTABILITY FOR LOCAL SCHOOL BOARDS Dennis Heard Governmental Accounting and Auditing Forum December 6, 2012 SCHOOL FISCAL ACCOUNTABILITY ACT Act No. 2006-196 created a new chapter in Title 16

FISCAL ACCOUNTABILITY FOR LOCAL SCHOOL BOARDS Dennis Heard Governmental Accounting and Auditing Forum December 6, 2012 SCHOOL FISCAL ACCOUNTABILITY ACT Act No. 2006-196 created a new chapter in Title 16

JOHNSTON COUNTY PUBLIC SCHOOLS INTERNAL AUDIT DEPARTMENT PTA, PTO AND BOOSTER CLUB HANDBOOK

JOHNSTON COUNTY PUBLIC SCHOOLS INTERNAL AUDIT DEPARTMENT 2017-2018 PTA, PTO AND BOOSTER CLUB HANDBOOK Table of Contents Organization Guidelines 3 Financial Guidelines 3 Fundraiser Guidelines 4 Treasurer

JOHNSTON COUNTY PUBLIC SCHOOLS INTERNAL AUDIT DEPARTMENT 2017-2018 PTA, PTO AND BOOSTER CLUB HANDBOOK Table of Contents Organization Guidelines 3 Financial Guidelines 3 Fundraiser Guidelines 4 Treasurer

Fiscal Management. 3.1 Chief School Financial Officer

3.1 Chief School Financial Officer III. The Board will appoint a Chief School Financial Officer (CSFO) to oversee the financial operations of the Board and to perform the duties of the position that are

3.1 Chief School Financial Officer III. The Board will appoint a Chief School Financial Officer (CSFO) to oversee the financial operations of the Board and to perform the duties of the position that are

District Business Office Staff YES NO N/A Comments

Internal Controls Checklist by Job Responsibility A No response to any of the following questions may indicate an internal control weakness. The district should perform a self-evaluation and investigate

Internal Controls Checklist by Job Responsibility A No response to any of the following questions may indicate an internal control weakness. The district should perform a self-evaluation and investigate

GRANITE SCHOOL DISTRICT. Fiscal Policy Manual DEVELOPED BY THE BUSINESS SERVICES DIVISION

GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 This manual

GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 This manual

School Support Organizations & Groups. Rutherford County Schools Boardroom 6:30 PM, Monday, Aug. 20, 2018

School Support Organizations & Groups Rutherford County Schools Boardroom 6:30 PM, Monday, Aug. 20, 2018 SSG - School Support Group SSG can be either Booster Club or a PTO SSG semi-independent group that

School Support Organizations & Groups Rutherford County Schools Boardroom 6:30 PM, Monday, Aug. 20, 2018 SSG - School Support Group SSG can be either Booster Club or a PTO SSG semi-independent group that

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL INTRODUCTION In view of the large amount of monies received from and expended for student/campus activities, the demand has developed for efficient,

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL INTRODUCTION In view of the large amount of monies received from and expended for student/campus activities, the demand has developed for efficient,

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS The principal shall be responsible to the county board of education for financial management of his school. He shall authorize

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS The principal shall be responsible to the county board of education for financial management of his school. He shall authorize

BRYANT SCHOOL DISTRICT. GUIDELINES for AFFILIATED SUPPORT ORGANIZATIONS

BRYANT SCHOOL DISTRICT GUIDELINES for AFFILIATED SUPPORT ORGANIZATIONS Adopted by School Board March 1, 2010 Booster Clubs and Support Organizations Policy The Bryant Public School District recognizes

BRYANT SCHOOL DISTRICT GUIDELINES for AFFILIATED SUPPORT ORGANIZATIONS Adopted by School Board March 1, 2010 Booster Clubs and Support Organizations Policy The Bryant Public School District recognizes

K-0481 KBE-R RELATIONS WITH PARENT ORGANIZATIONS

K-0481 KBE-R Parent/Citizen Group Guidelines RELATIONS WITH PARENT ORGANIZATIONS In order for a parent/citizen group to be approved by the school and the District, the following guidelines must be observed.

K-0481 KBE-R Parent/Citizen Group Guidelines RELATIONS WITH PARENT ORGANIZATIONS In order for a parent/citizen group to be approved by the school and the District, the following guidelines must be observed.

Discovery Middle School Madison, Alabama

Discovery Middle School COMPONENT UNIT FINANCIAL STATEMENTS September 30, 2015 Page - 1 - Discovery Middle School Table of Contents September 30, 2015 Independent Auditors' Report 1 Component Unit Balance

Discovery Middle School COMPONENT UNIT FINANCIAL STATEMENTS September 30, 2015 Page - 1 - Discovery Middle School Table of Contents September 30, 2015 Independent Auditors' Report 1 Component Unit Balance

BOOSTER CLUBS, AND PARENT ORGANIZATIONS. August 2016

BOOSTER CLUBS, AND PARENT ORGANIZATIONS August 2016 OVERVIEW GASB 39- (Why we require information) Parent Organizations Booster Clubs Community Organizations WHY--- GOVERNMENTAL ACCOUNTING STANDARDS BOARD

BOOSTER CLUBS, AND PARENT ORGANIZATIONS August 2016 OVERVIEW GASB 39- (Why we require information) Parent Organizations Booster Clubs Community Organizations WHY--- GOVERNMENTAL ACCOUNTING STANDARDS BOARD

Brownfield ISD Business Office Procedures Manual

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

New York City Department of Education

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Michelangelo Middle School: Management of General School Funds New York City Department of

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Michelangelo Middle School: Management of General School Funds New York City Department of

SCHOOL INTERNAL ACCOUNTS TRAINING. Presented by Yvonne Clayborne, Partner

SCHOOL INTERNAL ACCOUNTS TRAINING Presented by Yvonne Clayborne, Partner 1 Today s Presentation Review various phases of this year s audit Review common audit findings noted Preparing for next year s audit

SCHOOL INTERNAL ACCOUNTS TRAINING Presented by Yvonne Clayborne, Partner 1 Today s Presentation Review various phases of this year s audit Review common audit findings noted Preparing for next year s audit

Business Operating Procedures

Business Operating Procedures 2016-2017 Learning Today. Leading Tomorrow. Accounting Procedures The Business Manager is responsible for all accounting functions in the district. It is important that he/she

Business Operating Procedures 2016-2017 Learning Today. Leading Tomorrow. Accounting Procedures The Business Manager is responsible for all accounting functions in the district. It is important that he/she

PTA and Booster Club Training Presented by Financial Services, Athletics, and Internal Audit Services

PTA and Booster Club Training 2017 Presented by Financial Services, Athletics, and Internal Audit Services Presented By Mary Russell, Executive Director of Financial Services Greg Priest, Athletic Director

PTA and Booster Club Training 2017 Presented by Financial Services, Athletics, and Internal Audit Services Presented By Mary Russell, Executive Director of Financial Services Greg Priest, Athletic Director

Documentation OTHER MATTERS State Sales Tax Ticket Sales Taxable Earnings Paid to Individuals Fund Raisers...

TABLE OF CONTENTS INTRODUCTION AND BACKGROUND INFORMATION... 1 General Provisions... 1 Basic Principles of School Activity Funds... 1 Accounting Systems...2 Internal Control... 2 Classification of Accounts...

TABLE OF CONTENTS INTRODUCTION AND BACKGROUND INFORMATION... 1 General Provisions... 1 Basic Principles of School Activity Funds... 1 Accounting Systems...2 Internal Control... 2 Classification of Accounts...

Student Activity Account Guidelines For Burlington Public Schools

Student Activity Account Guidelines For Burlington Public Schools * Information and text in this document was adapted for the Burlington Public Schools by the Finance Manager from the Student Activity

Student Activity Account Guidelines For Burlington Public Schools * Information and text in this document was adapted for the Burlington Public Schools by the Finance Manager from the Student Activity

Crook County School District School District #1970 Prineville, Oregon. Student Activity Accounting Procedures

Crook County School District School District #1970 Prineville, Oregon Student Activity Accounting Procedures January 9, 2009 Revised January 9, 2015 3 rd Revision August 10, 2017 Student Activity Accounting

Crook County School District School District #1970 Prineville, Oregon Student Activity Accounting Procedures January 9, 2009 Revised January 9, 2015 3 rd Revision August 10, 2017 Student Activity Accounting

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

STUDENT ACTIVITY FUND GUIDANCE

STUDENT ACTIVITY FUND GUIDANCE OVERVIEW Student activities require the participation of students. Student activity funds are monies generated by students participation, authorized to be spent by students,

STUDENT ACTIVITY FUND GUIDANCE OVERVIEW Student activities require the participation of students. Student activity funds are monies generated by students participation, authorized to be spent by students,

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

Administrative Assistant and Athletic Assistant Training. February 10, 2017

Administrative Assistant and Athletic Assistant Training February 10, 2017 Welcome and Introductions Who s Who? Topics for today: Uniform System of Financial Records (USFR) Questionnaire Fees and Waivers

Administrative Assistant and Athletic Assistant Training February 10, 2017 Welcome and Introductions Who s Who? Topics for today: Uniform System of Financial Records (USFR) Questionnaire Fees and Waivers

Massachusetts Department of Elementary and

Massachusetts Department of Elementary and Secondary Education Index INFORMATION CONTACT: Massachusetts Department of Elementary and Secondary Education (ESE) Contact: Jay Sullivan Phone Numbers: (781)

Massachusetts Department of Elementary and Secondary Education Index INFORMATION CONTACT: Massachusetts Department of Elementary and Secondary Education (ESE) Contact: Jay Sullivan Phone Numbers: (781)

ACTIVITY ACCOUNTING AND ACCOUNT CODING FOR LOCAL SCHOOLS

ACTIVITY ACCOUNTING AND ACCOUNT CODING FOR LOCAL SCHOOLS Sonja Peaspanen State of Alabama Department of Education Chart of Accounts/Coding Update accounting manual annually Available online: www.alsde.edu

ACTIVITY ACCOUNTING AND ACCOUNT CODING FOR LOCAL SCHOOLS Sonja Peaspanen State of Alabama Department of Education Chart of Accounts/Coding Update accounting manual annually Available online: www.alsde.edu

Booster Clubs and School Related Organizations Guidelines

Booster Clubs and School Related Organizations Guidelines 1 FOWARD This manual is designed to assist Booster Club officers, School Support Organizations ( club(s) and/or organization(s) ) and members by

Booster Clubs and School Related Organizations Guidelines 1 FOWARD This manual is designed to assist Booster Club officers, School Support Organizations ( club(s) and/or organization(s) ) and members by

Fiscal Policy Manual

GRANITE SCHOOL DISTRICT Fiscal Policy Manual DEVELOPED BY THE BUSINESS SERVICES DIVISION 2015 Adopted September, 2013 Revised May, 2015 This manual was developed in accordance with Board Policy, Article

GRANITE SCHOOL DISTRICT Fiscal Policy Manual DEVELOPED BY THE BUSINESS SERVICES DIVISION 2015 Adopted September, 2013 Revised May, 2015 This manual was developed in accordance with Board Policy, Article

Student Activity Fund (SAF) Training/Policy Guide

Training/Policy Guide") Student Activity Fund (SAF) Training/Policy Guide Contents Office of the Controller Student Activity Fund (SAF) Staff Directory 3 Student Activity Fund Policies 4 What is an ACTIVITY FUND? 4 ACTIVITY TYPE

Student Activity Fund (SAF) Training/Policy Guide Contents Office of the Controller Student Activity Fund (SAF) Staff Directory 3 Student Activity Fund Policies 4 What is an ACTIVITY FUND? 4 ACTIVITY TYPE

Update on Local School Issues June Presented by: Mike Scroggins Director, County Audit Division Examiners of Public Accounts

Update on Local School Issues June 2010 Presented by: Mike Scroggins Director, County Audit Division Examiners of Public Accounts Common Problems at Local Schools Receipts Receipts are to be deposited

Update on Local School Issues June 2010 Presented by: Mike Scroggins Director, County Audit Division Examiners of Public Accounts Common Problems at Local Schools Receipts Receipts are to be deposited

The title "School Finance Officer" shall be used herein to designate the position responsible for handling the School Activity Funds.

The Regulations of the State Board of Education define school activity funds as all funds received from extracurricular school activities, such as entertainment, athletic contests, club dues, school fund-raising,

The Regulations of the State Board of Education define school activity funds as all funds received from extracurricular school activities, such as entertainment, athletic contests, club dues, school fund-raising,

Budget Development for Budget Forums May 23 and 24, 2011

Budget Development for 2011-2012 Budget Forums May 23 and 24, 2011 as of May 23, 2011 Agenda Welcome and introductions Meeting format Budget presentation Input Context for Budget Development Unprecedented

Budget Development for 2011-2012 Budget Forums May 23 and 24, 2011 as of May 23, 2011 Agenda Welcome and introductions Meeting format Budget presentation Input Context for Budget Development Unprecedented

3/11/2016. Student Activity Funds. Basic Facts about Student Activity Funds

Student Activity Funds Presented by: Natalie Rew, CPA Basic Facts about Student Activity Funds WI Stats, s. 120.16(2) authorizes a school district treasurer to receive money raised in extra-curricular

Student Activity Funds Presented by: Natalie Rew, CPA Basic Facts about Student Activity Funds WI Stats, s. 120.16(2) authorizes a school district treasurer to receive money raised in extra-curricular

STUDENT ACTIVITY PROCEDURE MANUAL

SCHOOL DISTRICT OF RIVERVIEW GARDENS STUDENT ACTIVITY PROCEDURE MANUAL This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Riverview

SCHOOL DISTRICT OF RIVERVIEW GARDENS STUDENT ACTIVITY PROCEDURE MANUAL This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Riverview

Booster Clubs and PTA/PTO Groups. also available at wfisd.net

Booster Clubs and PTA/PTO Groups also available at wfisd.net Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer Identification Number (EIN) Becoming

Booster Clubs and PTA/PTO Groups also available at wfisd.net Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer Identification Number (EIN) Becoming

ESCAMBIA COUNTY DISTRICT SCHOOL BOARD SCHOOL INTERNAL ACCOUNTS

OFFICE OF INTERNAL AUDITING SCHOOL INTERNAL ACCOUNTS STATEMENTS OF CASH RECEIPTS, DISBURSEMENTS & TRANSFERS FOR THE YEAR ENDED JUNE 30, 2009 September 4, 2009 INTERNAL AUDITOR S REPORT SCHOOL INTERNAL

OFFICE OF INTERNAL AUDITING SCHOOL INTERNAL ACCOUNTS STATEMENTS OF CASH RECEIPTS, DISBURSEMENTS & TRANSFERS FOR THE YEAR ENDED JUNE 30, 2009 September 4, 2009 INTERNAL AUDITOR S REPORT SCHOOL INTERNAL

PARK HILL SCHOOL DISTRICT EXECUTIVE SUMMARY

EXECUTIVE SUMMARY The Executive Summary is the first major section of the school budget document. It highlights important information contained in the budget. Users may rely on this section for an overview

EXECUTIVE SUMMARY The Executive Summary is the first major section of the school budget document. It highlights important information contained in the budget. Users may rely on this section for an overview

Board Approved 9/20/16 OUTSIDE SUPPORT ORGANIZATION MANUAL

OUTSIDE SUPPORT ORGANIZATION MANUAL 1 2 Board Approved 9/20/16 Outside Support Organizations The School District encourages citizens to form Outside Support Organizations (OSO). These organizations support

OUTSIDE SUPPORT ORGANIZATION MANUAL 1 2 Board Approved 9/20/16 Outside Support Organizations The School District encourages citizens to form Outside Support Organizations (OSO). These organizations support

FISCAL YEAR-END PROCEDURES AASBO MENTOR MEETING SEPTEMBER 18, Karen O Bannon, CSFO Madison County Schools

FISCAL YEAR-END PROCEDURES AASBO MENTOR MEETING SEPTEMBER 18, 2014 Karen O Bannon, CSFO Madison County Schools kobannon@madison.k12.al.us Fiscal Year-End Recording revenues and expenditures in the correct

FISCAL YEAR-END PROCEDURES AASBO MENTOR MEETING SEPTEMBER 18, 2014 Karen O Bannon, CSFO Madison County Schools kobannon@madison.k12.al.us Fiscal Year-End Recording revenues and expenditures in the correct

III. Fiscal Management

3.1 Chief School Financial Officer III. Fiscal Management The Board will appoint a Chief School Financial Officer to oversee the financial operations of the Board and to perform the duties of the position

3.1 Chief School Financial Officer III. Fiscal Management The Board will appoint a Chief School Financial Officer to oversee the financial operations of the Board and to perform the duties of the position

Parent Organization Handbook. Lake Travis Independent School District

Parent Organization Handbook Lake Travis Independent School District FORWARD This manual is designed to assist parent organization officers and members by providing organizational and financial guidance.

Parent Organization Handbook Lake Travis Independent School District FORWARD This manual is designed to assist parent organization officers and members by providing organizational and financial guidance.

SCOTT MARUNIAK, TREASURER

BASIC FINANCIAL STATEMENTS (AUDITED) FOR THE FISCAL YEAR ENDED JUNE 30, 2016 SCOTT MARUNIAK, TREASURER TABLE OF CONTENTS Independent Auditor s Report... 1-2 Management s Discussion and Analysis... 3-11

BASIC FINANCIAL STATEMENTS (AUDITED) FOR THE FISCAL YEAR ENDED JUNE 30, 2016 SCOTT MARUNIAK, TREASURER TABLE OF CONTENTS Independent Auditor s Report... 1-2 Management s Discussion and Analysis... 3-11

Fiscal Accounting & Reporting. Crook County School District #1. Activity Funds. Procedures Manual

Fiscal Accounting & Reporting DI-R Crook County School District #1 Activity Funds Procedures Manual CROOK COUNTY SCHOOL DISTRICT #1 ACTIVITY FUNDS PROCEDURES MANUAL This procedures manual is designed to

Fiscal Accounting & Reporting DI-R Crook County School District #1 Activity Funds Procedures Manual CROOK COUNTY SCHOOL DISTRICT #1 ACTIVITY FUNDS PROCEDURES MANUAL This procedures manual is designed to

BEREA CITY SCHOOL DISTRICT

BEREA CITY SCHOOL DISTRICT STUDENT ACTIVITIES HANDBOOK Berea City School District 390 Fair Street Berea OH 44017 www.berea.k12.oh.us 216.898.8300 Page 0 Board Approved September 21, 2015 BEREA CITY SCHOOL

BEREA CITY SCHOOL DISTRICT STUDENT ACTIVITIES HANDBOOK Berea City School District 390 Fair Street Berea OH 44017 www.berea.k12.oh.us 216.898.8300 Page 0 Board Approved September 21, 2015 BEREA CITY SCHOOL

STUDENT ACTIVITY ACCOUNTS PROCEDURES FOR OPERATIONS SEEKONK PUBLIC SCHOOLS

STUDENT ACTIVITY ACCOUNTS PROCEDURES FOR OPERATIONS SEEKONK PUBLIC SCHOOLS PREFACE The following procedures will govern how student activity accounts in the Seekonk Public Schools are managed and operated.

STUDENT ACTIVITY ACCOUNTS PROCEDURES FOR OPERATIONS SEEKONK PUBLIC SCHOOLS PREFACE The following procedures will govern how student activity accounts in the Seekonk Public Schools are managed and operated.

THE SCHOOL DISTRICT OF GREENVILLE COUNTY

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

FRISCO INDEPENDENT SCHOOL DISTRICT

FRISCO INDEPENDENT SCHOOL DISTRICT STUDENT SERVICES BOOSTER CLUB REQUIREMENTS AND OPERATIONAL GUIDELINES 2017-2018 FOREWORD Frisco Independent School District recognizes the importance of parent and community

FRISCO INDEPENDENT SCHOOL DISTRICT STUDENT SERVICES BOOSTER CLUB REQUIREMENTS AND OPERATIONAL GUIDELINES 2017-2018 FOREWORD Frisco Independent School District recognizes the importance of parent and community

and (Revised )

") 2016-2017 and 2017-2018 (Revised 04.27.17) Athletics 5% Overall Budget Cut $33,355 Services $4,620 $1,320 $2,975 Total Cut $42,270 16/17 Cut $42,270 Additional Budget Cut $45,000 Decreased Budget by $16,000

2016-2017 and 2017-2018 (Revised 04.27.17) Athletics 5% Overall Budget Cut $33,355 Services $4,620 $1,320 $2,975 Total Cut $42,270 16/17 Cut $42,270 Additional Budget Cut $45,000 Decreased Budget by $16,000

FACILITIES RENTAL INFORMATION

FACILITIES RENTAL INFORMATION Georgetown ISD Administration 603 Lakeway Drive Georgetown, Texas 78628 (512) 943-5000 Fax (512) 759-4797 Statement of Purpose The primary purpose or function of public school

FACILITIES RENTAL INFORMATION Georgetown ISD Administration 603 Lakeway Drive Georgetown, Texas 78628 (512) 943-5000 Fax (512) 759-4797 Statement of Purpose The primary purpose or function of public school

IMPORTANT NOTICE TO PROSPECTIVE FACILITY USERS, INCLUDING SCHOOL-RELATED USERS

EBH (July 2004) HINDS COUNTY SCHOOL FACILITY RENTAL I. PURPOSE To establish reasonable regulations for the short-term use of certain school facilities for school related activities and by the community

EBH (July 2004) HINDS COUNTY SCHOOL FACILITY RENTAL I. PURPOSE To establish reasonable regulations for the short-term use of certain school facilities for school related activities and by the community

I n t r o d u c t i o n

I n t r o d u c t i o n Booster Clubs are organized to help promote, support, and improve the extra curricular activities of the schools in Wasatch County School District. Each administrator is responsible

I n t r o d u c t i o n Booster Clubs are organized to help promote, support, and improve the extra curricular activities of the schools in Wasatch County School District. Each administrator is responsible

ASB Operations Manual

To Table of Contents Bellevue School District ASB Operations Manual Effective: September 1, 2011 Staff: Simone Sangster, Ed.D. Assistant Superintendant of Finance and Operations Marie Telecky Director

To Table of Contents Bellevue School District ASB Operations Manual Effective: September 1, 2011 Staff: Simone Sangster, Ed.D. Assistant Superintendant of Finance and Operations Marie Telecky Director

BUDGET ADVISORY MEETING #2 March 6, 2018 HIGH SCHOOL LIBRARY 7:30 PM 8:00 PM

BUDGET ADVISORY MEETING #2 HIGH SCHOOL LIBRARY 7:30 PM 8:00 PM Overview Budget Priorities Elementary Secondary Rollover Budget Budget Components 1000 General Support, Operations & Maintenance, Utilities

BUDGET ADVISORY MEETING #2 HIGH SCHOOL LIBRARY 7:30 PM 8:00 PM Overview Budget Priorities Elementary Secondary Rollover Budget Budget Components 1000 General Support, Operations & Maintenance, Utilities

TECUMSEH LOCAL SCHOOL DISTRICT

TECUMSEH LOCAL SCHOOL DISTRICT ACTIVITIES HANDBOOK Student Activity Accounts Principal Fund Accounts Athletic Accounts Tecumseh Local School District 9760 West National Road, New Carlisle, Ohio 45344 www.tecumseh.k12.oh.us

TECUMSEH LOCAL SCHOOL DISTRICT ACTIVITIES HANDBOOK Student Activity Accounts Principal Fund Accounts Athletic Accounts Tecumseh Local School District 9760 West National Road, New Carlisle, Ohio 45344 www.tecumseh.k12.oh.us

STATE PUBLIC SCHOOL FUND (LOCAL EDUCATION AGENCIES - LEAS)

") APRIL 2015 STATE PUBLIC SCHOOL FUND (LOCAL EDUCATION AGENCIES - LEAS) State Authorization: North Carolina General Statutes Chapter 115C, Articles 1 31 Federal Authorization: American Recovery and Reinvestment

APRIL 2015 STATE PUBLIC SCHOOL FUND (LOCAL EDUCATION AGENCIES - LEAS) State Authorization: North Carolina General Statutes Chapter 115C, Articles 1 31 Federal Authorization: American Recovery and Reinvestment

WICHITA FALLS INDEPENDENT SCHOOL DISTRICT GUIDELINES FOR OPERATIONS. BOOSTER CLUBS and PTA/PTO GROUPS

WICHITA FALLS INDEPENDENT SCHOOL DISTRICT GUIDELINES FOR OPERATIONS BOOSTER CLUBS and PTA/PTO GROUPS Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer

WICHITA FALLS INDEPENDENT SCHOOL DISTRICT GUIDELINES FOR OPERATIONS BOOSTER CLUBS and PTA/PTO GROUPS Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer

Accounting and Purchasing Manual. A manual provided for schools to guide them in appropriate cash handling and procurement procedures

Accounting and Purchasing Manual A manual provided for schools to guide them in appropriate cash handling and procurement procedures June, 2009 **IMPORTANT REMINDERS** Applies to all cash received at schools

Accounting and Purchasing Manual A manual provided for schools to guide them in appropriate cash handling and procurement procedures June, 2009 **IMPORTANT REMINDERS** Applies to all cash received at schools

Dollars and Sense. The Role of the Treasurer

Dollars and Sense The Role of the Treasurer 2014-15 What do I need to know? Your PTA s tax number, formally called the Employer Identification Number (EIN). Your PTA s bank and bank account number. The

Dollars and Sense The Role of the Treasurer 2014-15 What do I need to know? Your PTA s tax number, formally called the Employer Identification Number (EIN). Your PTA s bank and bank account number. The

THE SCHOOL DISTRICT OF ESCAMBIA COUNTY OUTSIDE SUPPORT ORGANIZATIONS

THE SCHOOL DISTRICT OF ESCAMBIA COUNTY OUTSIDE SUPPORT ORGANIZATIONS Guidelines Manual APPROVED ESCAMBIA COUNTY SCHOOL BOARD OCT 1 8 2016 MALCOLM TH0' 1/'.S, SUPCR!MTE ldent VERIFIED BY RECORDING SECRETARY

THE SCHOOL DISTRICT OF ESCAMBIA COUNTY OUTSIDE SUPPORT ORGANIZATIONS Guidelines Manual APPROVED ESCAMBIA COUNTY SCHOOL BOARD OCT 1 8 2016 MALCOLM TH0' 1/'.S, SUPCR!MTE ldent VERIFIED BY RECORDING SECRETARY

James Clemens High School Madison, Alabama

STUDENT ACTIVITY FUND FINANCIAL STATEMENTS September 30, 2017 1 Table of Contents September 30, 2017 REPORT Page Independent Auditors Report 1 Balance Sheet 3 Statement of Revenues, Expenditures and Changes

STUDENT ACTIVITY FUND FINANCIAL STATEMENTS September 30, 2017 1 Table of Contents September 30, 2017 REPORT Page Independent Auditors Report 1 Balance Sheet 3 Statement of Revenues, Expenditures and Changes

Leon County Schools. School Internal Accounts Procedures Manual. Page 1 of 57

Leon County Schools School Internal Accounts Procedures Manual Page 1 of 57 TABLE OF CONTENTS CHAPTER 1 GENERAL OVERVIEW... 7 A. DEFINITION INTERNAL ACCOUNTS... 7 B. INTRODUCTION... 7 C. BASIC PRINCIPLES...

Leon County Schools School Internal Accounts Procedures Manual Page 1 of 57 TABLE OF CONTENTS CHAPTER 1 GENERAL OVERVIEW... 7 A. DEFINITION INTERNAL ACCOUNTS... 7 B. INTRODUCTION... 7 C. BASIC PRINCIPLES...

Chapter 8. School Internal Funds

Chapter 8 School Internal Funds SECTION I PRINCIPLES 1. The district school board shall be responsible for the administration and control of internal funds of the district school system, and in connection

Chapter 8 School Internal Funds SECTION I PRINCIPLES 1. The district school board shall be responsible for the administration and control of internal funds of the district school system, and in connection

New York City Department of Education

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

Lyford CISD. Travel Manual

Lyford CISD Travel Manual Lyford CISD Travel Manual Table of Contents I. Employee Travel A. Legal Requirements for Travel B. Travel Authorization C. Funds Availability D. Purchase Orders & Check Availability

Lyford CISD Travel Manual Lyford CISD Travel Manual Table of Contents I. Employee Travel A. Legal Requirements for Travel B. Travel Authorization C. Funds Availability D. Purchase Orders & Check Availability

SCOTT MARUNIAK, TREASURER

CASH BASIS FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 SCOTT MARUNIAK, TREASURER CASH BASIS FINANCIAL STATEMENTS TABLE OF CONTENTS Table of Contents... 1 Accountant s Compilation Report...

CASH BASIS FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 SCOTT MARUNIAK, TREASURER CASH BASIS FINANCIAL STATEMENTS TABLE OF CONTENTS Table of Contents... 1 Accountant s Compilation Report...

James Clemens High School Madison, Alabama

STUDENT ACTIVITY FUND FINANCIAL STATEMENTS September 30, 2016-1 - Table of Contents September 30, 2016 REPORT Page Independent Auditors Report 1 Balance Sheet 3 Statement of Revenues, Expenditures and

STUDENT ACTIVITY FUND FINANCIAL STATEMENTS September 30, 2016-1 - Table of Contents September 30, 2016 REPORT Page Independent Auditors Report 1 Balance Sheet 3 Statement of Revenues, Expenditures and

BOOSTER CLUB HANDBOOK

BOOSTER CLUB HANDBOOK Pikeville Junior High/High School 120 Championship Drive Pikeville, KY 41501 (606) 432-0185 Message From the School Dear Stakeholders, On behalf of the students, faculty, and administration

BOOSTER CLUB HANDBOOK Pikeville Junior High/High School 120 Championship Drive Pikeville, KY 41501 (606) 432-0185 Message From the School Dear Stakeholders, On behalf of the students, faculty, and administration

CITY OF PEMBROKE PINES, FLORIDA FLORIDA STATE UNIVERSITY CHARTER ELEMENTARY SCHOOL

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES a. Reporting Entity On February 3, 2003, the City of Pembroke Pines ( the City ) and Florida State University ( FSU ) signed an agreement ( Charter Agreement

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES a. Reporting Entity On February 3, 2003, the City of Pembroke Pines ( the City ) and Florida State University ( FSU ) signed an agreement ( Charter Agreement

CLASS AGENDA ACTIVITY FUND ACCOUNTING

CLASS AGENDA ACTIVITY FUND ACCOUNTING FOR LOCAL SCHOOL PERSONNEL DR. KEREN H. DEAL, CPA, CGFM PROFESSOR OF ACCOUNTING AUBURN UNIVERSITY MONTGOMERY Review of the Accounting Cycle Fund Accounting Internal

CLASS AGENDA ACTIVITY FUND ACCOUNTING FOR LOCAL SCHOOL PERSONNEL DR. KEREN H. DEAL, CPA, CGFM PROFESSOR OF ACCOUNTING AUBURN UNIVERSITY MONTGOMERY Review of the Accounting Cycle Fund Accounting Internal

JACKSON COUNTY BOARD OF EDUCATION

JACKSON COUNTY BOARD OF EDUCATION Jackson County School System FINANCIAL GUIDELINES FOR SCHOOL ACTIVITY FUNDS AND SCHOOL SYSTEM ACCOUNTS Updated: October 2004 2 JACKSON COUNTY BOARD OF EDUCATION FINANCIAL

JACKSON COUNTY BOARD OF EDUCATION Jackson County School System FINANCIAL GUIDELINES FOR SCHOOL ACTIVITY FUNDS AND SCHOOL SYSTEM ACCOUNTS Updated: October 2004 2 JACKSON COUNTY BOARD OF EDUCATION FINANCIAL

CITY OF PEMBROKE PINES, FLORIDA CHARTER SCHOOLS

CITY OF PEMBROKE PINES, FLORIDA CHARTER SCHOOLS FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2008 (With Independent Auditors Reports Thereon) CITY OF PEMBROKE PINES, FLORIDA CHARTER SCHOOLS

CITY OF PEMBROKE PINES, FLORIDA CHARTER SCHOOLS FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2008 (With Independent Auditors Reports Thereon) CITY OF PEMBROKE PINES, FLORIDA CHARTER SCHOOLS

ADMINISTRATIVE TRAVEL GUIDELINES

Donna Independent School District ADMINISTRATIVE TRAVEL GUIDELINES FOR DONNA I.S.D. EMPLOYEES Effective Date: January 1, 2014 Travel Policy for In-District and Out-of-District/Valley Travel Principals

Donna Independent School District ADMINISTRATIVE TRAVEL GUIDELINES FOR DONNA I.S.D. EMPLOYEES Effective Date: January 1, 2014 Travel Policy for In-District and Out-of-District/Valley Travel Principals

for FISCAL REPORTING to the DISTRICT for ORGANIZATIONS USING the DISTRICT S EIN and NOT FOR PROFIT STATUS

GUIDELINES and PROCEDURES for FISCAL REPORTING to the DISTRICT for ORGANIZATIONS USING the DISTRICT S EIN and NOT FOR PROFIT STATUS November 2015 The Beaver Dam Unified School District does not discriminate

GUIDELINES and PROCEDURES for FISCAL REPORTING to the DISTRICT for ORGANIZATIONS USING the DISTRICT S EIN and NOT FOR PROFIT STATUS November 2015 The Beaver Dam Unified School District does not discriminate

COMMUNITY UNIT SCHOOL DISTRICT NO. 1 COLES-CUMBERLAND COUNTIES. FINANCIAL STATEMENTS For the Year Ended June 30, 2018

COLES-CUMBERLAND COUNTIES FINANCIAL STATEMENTS For the Year Ended June 30, 2018 TABLE OF CONTENTS Page No. Independent Auditor s Report... 1 Independent Auditor s Report on Internal Control over Financial

COLES-CUMBERLAND COUNTIES FINANCIAL STATEMENTS For the Year Ended June 30, 2018 TABLE OF CONTENTS Page No. Independent Auditor s Report... 1 Independent Auditor s Report on Internal Control over Financial

Corona-Norco Unified School District. Booster Club Manual

Corona-Norco Unified School District Booster Club Manual TABLE OF CONTENTS I. Operating Requirements a. Booster Club Basic Requirements II. General Guidelines and Information a. Purpose of a Booster Club

Corona-Norco Unified School District Booster Club Manual TABLE OF CONTENTS I. Operating Requirements a. Booster Club Basic Requirements II. General Guidelines and Information a. Purpose of a Booster Club

STATE OF NEW MEXICO ARTESIA PUBLIC SCHOOLS. ANNUAL FINANCIAL REPORT June 30, 2010

ANNUAL FINANCIAL REPORT June 30, 2010 De'Aun Willoughby CPA, PC Certified Public Accountant Melrose, New Mexico Table of Contents Official Roster 6 Independent Auditor's Report. 7-8 Basic Financial Statements

ANNUAL FINANCIAL REPORT June 30, 2010 De'Aun Willoughby CPA, PC Certified Public Accountant Melrose, New Mexico Table of Contents Official Roster 6 Independent Auditor's Report. 7-8 Basic Financial Statements

Allen ISD Booster Club Guidelines

Allen ISD Booster Club Guidelines Revised: February 5, 2013 FOREWORD The Booster Club Guidelines were prepared to assist booster clubs by providing organizational and financial guidance. It also aims to

Allen ISD Booster Club Guidelines Revised: February 5, 2013 FOREWORD The Booster Club Guidelines were prepared to assist booster clubs by providing organizational and financial guidance. It also aims to

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

Lewisville Independent School District BOOSTER CLUB GUIDELINES. Debate

Lewisville Independent School District BOOSTER CLUB GUIDELINES Debate Booster Clubs A school district approved club formed by parents and other interested non-student adults to work for the best interest

Lewisville Independent School District BOOSTER CLUB GUIDELINES Debate Booster Clubs A school district approved club formed by parents and other interested non-student adults to work for the best interest

Corona Norco Uni ied School District BOOSTER CLUB MANUAL. Suppor ng the students of CNUSD

Corona Norco Uni ied School District BOOSTER CLUB MANUAL Suppor ng the students of CNUSD TABLE OF CONTENTS I. Operating Requirements A. Booster Club Basic Requirements... Page 1 II. General Guidelines

Corona Norco Uni ied School District BOOSTER CLUB MANUAL Suppor ng the students of CNUSD TABLE OF CONTENTS I. Operating Requirements A. Booster Club Basic Requirements... Page 1 II. General Guidelines

MOUNTAIN BROOK CITY BOARD OF EDUCATION

MOUNTAIN BROOK CITY BOARD OF EDUCATION BASIC FINANCIAL STATEMENTS TOGETHER WITH INDEPENDENT AUDITOR S REPORT YEAR ENDED SEPTEMBER 30, 2017 MOUNTAIN BROOK CITY BOARD OF EDUCATION MOUNTAIN BROOK, ALABAMA

MOUNTAIN BROOK CITY BOARD OF EDUCATION BASIC FINANCIAL STATEMENTS TOGETHER WITH INDEPENDENT AUDITOR S REPORT YEAR ENDED SEPTEMBER 30, 2017 MOUNTAIN BROOK CITY BOARD OF EDUCATION MOUNTAIN BROOK, ALABAMA

Parent Support Organizations Mandatory Training August 18, 2018

Parent Support Organizations Mandatory Training August 18, 2018 Vnet & GPS Finance TRAINING AGENDA I. Purpose of Training II. Definition and Role of the Parent Support Organization (PSO) A. Types B. Role

Parent Support Organizations Mandatory Training August 18, 2018 Vnet & GPS Finance TRAINING AGENDA I. Purpose of Training II. Definition and Role of the Parent Support Organization (PSO) A. Types B. Role

AUBURN UNION SCHOOL DISTRICT Auburn, California. FINANCIAL STATEMENTS June 30, 2014

Auburn, California FINANCIAL STATEMENTS June 30, 2014 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2014 TABLE OF CONTENTS Page Independent Auditor's Report 1 Management's

Auburn, California FINANCIAL STATEMENTS June 30, 2014 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2014 TABLE OF CONTENTS Page Independent Auditor's Report 1 Management's

PTO / BOOSTER CLUB GUIDELINES

PTO / BOOSTER CLUB GUIDELINES 2017-2018 1 Dear Parents: On behalf of the Granbury Independent School District s Board of Trustees, I want to express my sincere appreciation for the time and energy you

PTO / BOOSTER CLUB GUIDELINES 2017-2018 1 Dear Parents: On behalf of the Granbury Independent School District s Board of Trustees, I want to express my sincere appreciation for the time and energy you

Cafeteria Parking Lot Library Kitchen/Preparing* Auditorium Stadium (No Lights) Kitchen/Serving* Gymnasium Stadium (Lights)

Kitchen/Serving* Gymnasium Stadium (Lights)") PANTHER VALLEY SCHOOL DISTRICT 1 Panther Way, Lansford, PA 18232 Phone: (570) 645-4248 Fax: (570) 645-6232 USE OF FACILITIES AGREEMENT (Please return to Athletic & Activities Director) (File at least two

PANTHER VALLEY SCHOOL DISTRICT 1 Panther Way, Lansford, PA 18232 Phone: (570) 645-4248 Fax: (570) 645-6232 USE OF FACILITIES AGREEMENT (Please return to Athletic & Activities Director) (File at least two

The information in this manual supersedes all prior publications concerning school accounting procedures.

Accounting Manual August 2013 INTRODUCTION This manual was prepared to provide standardized accounting procedures for all schools and departments in the Salt Lake City School District. School principals,

Accounting Manual August 2013 INTRODUCTION This manual was prepared to provide standardized accounting procedures for all schools and departments in the Salt Lake City School District. School principals,

Montclair Elementary School Audit of School Internal Accounts For the Year Ended June 30, 2016

Audit of School Internal Accounts For the Year Ended June 30, 2016 Office of Internal Auditing October 2016 David J. Bryant, CPA, CIA, CFE, CGFM, CRMA Director Internal Auditing Audit Team: Brad Mostert,

Audit of School Internal Accounts For the Year Ended June 30, 2016 Office of Internal Auditing October 2016 David J. Bryant, CPA, CIA, CFE, CGFM, CRMA Director Internal Auditing Audit Team: Brad Mostert,

The purpose of this session is to give the user a high-level overview of the process flow for managing an Activity Fund Account.

The purpose of this session is to give the user a high-level overview of the process flow for managing an Activity Fund Account. The user is responsible to read the GPISD Business Operations Manual to

The purpose of this session is to give the user a high-level overview of the process flow for managing an Activity Fund Account. The user is responsible to read the GPISD Business Operations Manual to

Elgin ISD Cash Management Procedures

Purpose: The District receives cash and checks from many sources. These procedures are designed to ensure that all cash and checks received by the District and its employees are deposited and tracked for

Purpose: The District receives cash and checks from many sources. These procedures are designed to ensure that all cash and checks received by the District and its employees are deposited and tracked for

Facility Rental Guidelines

Facility Rental Guidelines Cape Coral Charter School Authority Cape Coral, Florida PURPOSE The purpose of this procedure is to establish the rules, conditions, and fees under which Cape Coral Charter School

Facility Rental Guidelines Cape Coral Charter School Authority Cape Coral, Florida PURPOSE The purpose of this procedure is to establish the rules, conditions, and fees under which Cape Coral Charter School

Ernest Ward Middle School Audit of School Internal Accounts For the Year Ended June 30, 2017

For the Year Ended June 30, 2017 Office of Internal Auditing September 2017 David J. Bryant, CPA, CIA, CFE, CGFM, CRMA Director Internal Auditing Audit Team: Jeremy Williams, CFE Audit Administration Specialist

For the Year Ended June 30, 2017 Office of Internal Auditing September 2017 David J. Bryant, CPA, CIA, CFE, CGFM, CRMA Director Internal Auditing Audit Team: Jeremy Williams, CFE Audit Administration Specialist

Burlington County Special Services School District Burlington County Institute of Technology. STUDENT ACTIVITY FUNDS Standard Operating Procedure

I. Purpose: Student Activity Funds are operated and managed by the club/athletic advisor under the guidance and direction of the building principal for educational related purposes. The building principal

I. Purpose: Student Activity Funds are operated and managed by the club/athletic advisor under the guidance and direction of the building principal for educational related purposes. The building principal