Macroeconomics: Policy, 31E23000, Spring 2018

|

|

|

- Cori Holmes

- 5 years ago

- Views:

Transcription

1 Macroeconomics: Policy, 31E23000, Spring 2018 Lecture 8: Safe Asset, Government Debt Pertti University School of Business March 19, 2018

2 Today Safe Asset, basics Government debt, sustainability, fiscal policy rules GDP-linked bonds

3 Safe Asset 1 Monetary unions, especially EMU, have problems in a ZLB-situation: Standard monetary policy ineffective in dealing with unionwide problem. Fiscal policy powerful, in principle, but in the absence of union wide policy depends on the coordination of national fiscal policies. National fiscal policies should take care also of national problems. Safe asset: can ensure that standard monetary policy can be used also in ZLB-situation. Shortage of safe assets as one reason why ZLB emerges to begin with.

4 Safe Asset 2 I transfer the closed economy model in Caballero, Farhi and Gourinchas (2016) Safe Asset Scarcity and Aggregate Demand, American Economic Review, into our framework. Recall the 3-equation short-term model: y = A ar, a > 0 (IS) (1) π π 1 = α (y y e ) (PC) (2) π π T = αβ (y y e ) (MR) (3) With the safe asset the IS-curve is y = A ar 1 br s 1, a, b > 0 (4) In (4) r s is the return to the safe asset. The coefficient b is small: private sector capacity to create (issue) safe asset is limited.

5 Safe Asset 3 PC- and MR- equations are the same, but there is a market for the safe asset. With gross (flow) supply of s the equilibrium condition for the safe asset market is ϕ y y + ϕ s r s ψ (r r s ) = s, ϕ y, ϕ s > 0, ψ 0 (5) r s is now the policy rate. r is the risky market interest rate, r r s is the market risk premium. Caballero et. al. argue that ψ = 0: it measures how easy it is for the private sector to create safe assets. Here we use this assumption. With this the key point is that risk premium is determined by the IS-curve, output and the safe interest rate by the remaining part of the model.

6 Safe Asset 3 To understand the role of the safe asset supply look at the value of the natural safe interest rate when output is at its Wicksellian level y e. From (5): r s = s ϕ yy e ϕ s (6) Clearly, if the supply of the safe asset is so low that s ϕ y y e < 0 the economy is driven to the ZLB-equilibrium with r s = 0 and output at the Keynesian level y = s ϕ y. Role for Q(uantitative) E(asing)? (4) implies that the shortage of assets increases the risk premium at y = y e.

7 Safe Asset 4 Assume now that the safe asset is supplied at high enough level for the safe interest rate to be positive. To see how the economy adjusts when a shock hits assume that the shock is a temporary negative demand shock reducing current output to y 0 whereby current inflation is reduced to (from the PC-curve) to π 0 = π T α (y e y 0 ) In period 1 the inflation is π 1 = π 0 + α (y 1 y e ). This together with the MR-equation π 1 π T = αβ (y 1 y e ) determine the output level and inflation rate y 1, π 1. We know that y 1 > y e and π T > π 1 > π 0.

8 Safe Asset 5 Given the one-period lag for the change in the interest rate change to have an effect on inflation and output, the CB sets the interest rate today,r 0 s, at a level that leads the economy to y 1, π 1 next period: r0 s = s ϕ yy 1 (7) ϕ s The IS-equation can be solved for the market interest rate r 0. How does the risk premium change in period 0?

9 From short run to long run 1 Be it as it is, most also academic economists support the claim that fiscal policies should be sustainable, the public debt relative to GDP cannot grow without limits without causing troubles. How do we evaluate the sustainability of the debt? As already noted, debt should be evaluated against the resources to pay it back. As tax revenues grow with the GDP and the government has in addition right to tax citizens, the proper measure for sustainability analysis is the debt/gdp-ratio. The basic budget equation for change in public debt can be obtained from the government budget constraint and is B t = G t T t + i t B t 1 (8)

10 From short run to long run 2 Here B = government debt, denotes change, B t B t B t 1. The nominal value of GDP is P t y t To get to the development of the debt/gdp-ratio divide both sides of (8) by P t y t : B t = d t + ib t, d t G t T t P t y t P t y t d t = primary deficit/gdp and b t = debt/gdp. We are interested in the development of b t., b t B t 1 P t y t (9)

11 From short run to long run 3 Now B t B t P t+1 y t+1 = B t 1 P t y t P t+1 y t+1 P t y t P t y t (10) = b t+1 (1 + π t ) (1 + g t ) b t (11) = b t+1 b t + (π t + g t + π t g t ) b t+1 (12) Here g t is the growth rate of the real GDP. Use (12) in (9) to get b t+1 b t = d + ib t (π t + g t + π t g t ) b t+1 d + (i t π t g t ) b t (13) Here we assume that π t g t is a small number as also are the inflation and growth rates and the period to make the difference (i π t g t ) b t+1 (i π t g t ) b t small.

12 From short run to long run 4 Now we have it, after remembering that the real rate of interest is r t = i t π t The first question we can analyze is how large the primary surplus must be if one wants to stabilize the debt at its current level, immediately. The answer is d = (r g) b t (14) Here the interest rate and the growth rate are projections of long run real interest rate and growth rate. This equation is known as the Domar-equation. It shows that if r g > 0 there must be a primary surplus while if r g < 0 debt can be stabilized even by running primary deficit.

13 From short run to long run 5 Conversely, one can ask what happens if the primary deficit or surplus is fixed to some level d. Obviously, if there is primary deficit and r g > 0, the debt will explode while with a surplus the debt will either explode (surplus too small) or the public sector will become net creditor (and the credit goes to infinity), unless the surplus is exactly at the level given by the Domar-equation. I leave the case with r g < 0 for you to look at the textbook, the answer is that there is no explosion, the economy will converge either to a finite indebtedness or finite creditor position.

14 From short run to long run 6 But should we take such sudden adjustments like adjusting from current primary deficit levels to primary surpluses given by the Domar-equation? With current knowledge the answer is no. Why? Theory supports tax smoothing, tax rates should be constant or change very slowly. We follow the study by Portes and Wren-Lewis (published 2015 in Manchester School), the working paper version can be found at files/publications/dp429.pdf.

15 From short run to long run 7 The idea is easy to understand. Let τ t be the (average income tax rate). By the Harberger-triangle arguments the efficiency cost associated with this tax can be approximated by τ 2 t. Since b t = (1 + r) b t 1 + d t and by assuming that the government does not allow its debt to explode the optimal path for the tax rate is given by minimizing the total discounted costs τ1 2 2µ 1 [b 2 (1 + r) b 1 g 1 + τ 1 ] + 1 [ τ2 2 2µ 2 [b 3 (1 + r) b 2 g 2 + τ 2 ]] ρ ( ) 1 t 1 [ + τt 2 2µ t [b t+1 (1 + r) b t g t + τ t ]] ρ Here, and just for now, g = government expenditure/gdp, µ t 1 is the cost of respecting the budget constraint (Lagrange-multiplier), ρ is the social time preference.

16 From short run to long run 8 The optimality conditions with respect to the choice of the tax rate and debt are which implies that τ t = µ t (15) µ t = 1 + r 1 + ρ µ t+1 (16) τ t = 1 + r 1 + ρ τ t+1 (17) In the Permanent-Income-Hypothesis case, r = ρ the tax rate is constant, τ t = τ t+1. This is the case of perfect tax smoothing. But even with other cases the realistic values for the interest rates imply very small changes in the tax rate.

17 From short run to long run 9 Tax smoothing is thus optimal in managing public finances. This has strong implications: All shocks should be absorbed by public debt, not by changing the tax rate. There is no optimal level of debt. But obviously (?) public sector should not be allowed to become insolvent. The optimal fiscal policy rule would then set both some target level for the debt/gdp-ratio and some adjustment parameter determining how fast the target should be reached.

18 From short run to long run 10 The adjustment parameter should be small to make the adjustment slow. To see more clearly the implications of tax smoothing we can see from (13) that the debt does not increase if ( T y ) P ( G y ) P b r P g P (18) where P refers to permanent or long-run and especially ( ) P G y refers to a long-run government plan. The question is now how to fund this plan.

19 From short run to long run 11 Tax smoothing implies that ( T y The previous equation then implies that ) P is constant ( T y ) P = τ. ( ) G P τ + ( r P g P) b (19) y Since d = G y T y, (13) implies that ( ( ) ) G G P b y + [( r r P) ( g g P)] (20) y

20 From short run to long run 12 Burden of debt: Ricardian neutrality Burden of debt: taxation crowding out Burden of debt: intergenerational transfers and other functions of debt.

21 Fiscal Policy Rules 1 Optimal fiscal policy: tax smoothing, no fixed level of debt optimal, but policies must ensure solvency of the public sector. Optimal policy rule: fix the target level for debt/gdp b and adjust either public expenditure or average tax rate (or both) to reach the target in the long run: g t g = a (b t 1 b ), a > 0 (21) τ t τ = c (b t 1 b ), c > 0 (22) τ t g t = rb t 1 + f (b t 1 b ), f > 0 (23) g and τ are the expenditure and tax rate consistent with b. Tax smoothing: the adjustment parameters a, c and f must be small. Also research results: a b.

22 Fiscal Policy Rules 2 The problem with the rules like (21) is that with a small adjustment coefficient the target debt will not be achieved in typical conditions under the lifetime of a government adopting the target. Also, or the other side of the coin, is that there is no incentive for a government to fulfill the requirements given by a rule like (21), deviations do not matter. There also no incentive to implement the policy: unforeseen events can be blamed for not implementing. This is an issue of transparency also. The rules reflect partly the household fallacy : debts have to paid back?

23 Fiscal Policy Rules 3 One way around the problems is to specify the required percentage adjustment in debt implied by the optimal rules for the electoral term, given the forecasts of growth and interest rates. The problem then is that with surprise adverse changes in growth reaching the goal could imply very large changes in taxes or expenditure. This can be mitigated by specifying debt reduction targets in terms of equivalent reductions in (primary) deficits, the impact of adverse shocks would have less deflationary implications. Swiss rule: deviations from plans allowed but too rapid a return to norm required. Deficit targets: rolling targets (fixing only the date by which the target is achieved) allows debt to work as shock absorber.

24 Fiscal Policy Rules 4 Conditional targets: adjusting for cyclicality. Threat of manipulation but allows shock absorbers to work efficiently. Role for fiscal councils in reducing manipulation: independent evaluation of the adjustments needed? Treatment of public investment? Golden rule : public investment not included in deficit calculations.

25 Fiscal Policy Rules 5 EMU rules? Target for both deficit and debt, but allowing some rolling. Rationale? De facto prevented automatic stabilization to work efficiently.

26 Does public debt matter? 1 Ricardian equivalence: as long as the government is committed to servicing and paying back its debt, the debt is not net wealth: Private agents understand that the present value of future taxes equals the value of debt, in net terms changing the structure of funding of the public sector does not have any real effects, the Modigliani-Miller theorem for the public sector. Assume that there is one household in the economy, the economy exists for two periods. The public sector has a fixed expenditure plan over the economy s lifetime, G 1 and G 2. The household consumes C i, i = 1, 2, in period i and its net saving in period 1 is S.

27 Does public debt matter? 2 Assume that the household face the same interest rate r as the government. Assume also that the taxes are lump-sum taxes. Then the budget constraints of the household are C 1 + S = Y 1 T 1 (24) C 2 = Y 2 + (1 + r) S T 2 (25) Similarly, the budget constraints of the government are G 1 = B + T 1 (26) T 2 = G 2 + (1 + r) B (27) Here B = borrowing by the government. Assume capital markets are perfect: the household and the government can freely choose S and B.

28 Does public debt matter? 3 Solve S from (24) and substitute in the second household budget constraint, and solve B from (24) and substitute in the second government budget constraint (this is OK by the assumption of perfect capital markets). The resulting equations, intertemporal budget constraints, are These imply that C 1 + C r = Y 1 + Y r T 1 T r G 1 + G r = T 1 + T r (28) (29) C 1 + C r = Y 1 + Y r G 1 G 2 (30) 1 + r Thus, only the present value of government purchases matters for the household behavior, not how government purchases are financed. This is the Ricardian Equivalence (RE).

29 Does public debt matter? 4 RE needs all the assumptions made above (in bold) to hold. Given this, it is not suprising that empirics does not support its relevance. RE is also known as Debt Neutrality. This tells what exactly the issue is: If debt neutrality holds it is hard to see what burden public debt can be and how borrowing could be harmful to future generations: the present generation undoes the negative impacts of debt. Note also the implication that government expenditure just crowds out private consumption. Implications for the effectiveness of fiscal policy?

30 Burden of Public Debt Change assumptions needed for RE and debt matters for the private sector. Overlapping (finite-lifetime) generations (OLG): Without perfect altruims RE is not valid. If taxes are not lump sum but are distortionary then debt can be a burden to future generations: the taxes needed to pay back the debt reduce aggregate output. But what if the rate of interest is below the growth rate? ZLB and debt funded increase in government expenditure? Public debt crowding out private investment? Public debt need not to paid back ever, burden to future generations? Debt has to be serviced. Many, heterogeneous households: Those not holding any debt will share in paying back the debt. But, in general, current debt is taken care of by the generations currently living.

31 Interest rates and growth rates 1 The difference between the interest rate on government debt and economic growth is crucial for the sustainability of debt and the burden of debt on future generations. Jorda et. al. (2017) have collected data on government short and long term debt (in addition to other returns) and economic growth in 17 rich countries for , see e.g. Jorda-Knoll-Kuvshinov-Schularick-Taylor-The-Rate-of-Re pdf. Next figure shows the development of safe returns and economic growth, both in real terms.

32 SugarSync/Luennot/Macro2018/L8, F1.pdf L8, F1

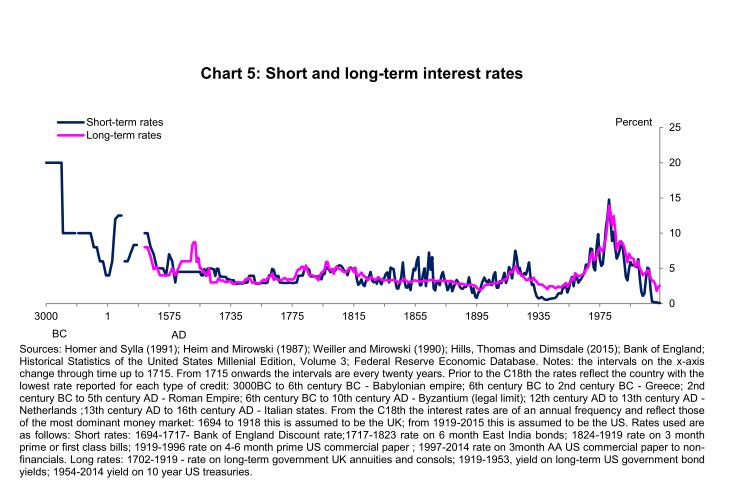

33 Interest rates and growth rates 2 To get a longer view, let us have a look at short and long term interest rates since 3000 BC. The numbers come from Andrew Haldane s speech, files/speech/2015/stuck.pdf?la=en&hash= 3247D34307D99E8E4E11E5B890837AD6C6CAEFFB:

34 SugarSync/Luennot/Macro2018/L8, F2.pdf L8, F2

35 GDP-linked government bonds Robert Shiller proposed in 1993 that governments should issue bonds with the interest rate indexed to the GDP growth rate: lower interest rate with lower growth, higher with higher growth. This would improve automatic stabilization: in booms increased pressure to contain/reduce government expenditure, in recessions maintain/increase expenditure. Benefits to governments: fiscal space (e.g. the sustainable level of government debt relative to GDP) would increase from per. Benefits to investors: lower risk of government bankruptcy, access to returns from all factors of production (e.g. human capital). How to create? Linking to GNI instead of GDP.

Macroeconomics: Policy, 31E23000, Spring 2018

Macroeconomics: Policy, 31E23000, Spring 2018 Lecture 7: Intro to Fiscal Policy, Policies in Currency Unions Pertti University School of Business March 14, 2018 Today Macropolicies in currency areas Fiscal

Macroeconomics: Policy, 31E23000, Spring 2018 Lecture 7: Intro to Fiscal Policy, Policies in Currency Unions Pertti University School of Business March 14, 2018 Today Macropolicies in currency areas Fiscal

Chapter 5 Fiscal Policy and Economic Growth

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far.

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far.

Y t )+υ t. +φ ( Y t. Y t ) Y t. α ( r t. + ρ +θ π ( π t. + ρ

+υ t. +φ ( Y t. Y t ) Y t. α ( r t. + ρ +θ π ( π t. + ρ") Macroeconomics ECON 2204 Prof. Murphy Problem Set 6 Answers Chapter 15 #1, 3, 4, 6, 7, 8, and 9 (on pages 462-63) 1. The five equations that make up the dynamic aggregate demand aggregate supply model

Macroeconomics ECON 2204 Prof. Murphy Problem Set 6 Answers Chapter 15 #1, 3, 4, 6, 7, 8, and 9 (on pages 462-63) 1. The five equations that make up the dynamic aggregate demand aggregate supply model

Final Exam Solutions

14.06 Macroeconomics Spring 2003 Final Exam Solutions Part A (True, false or uncertain) 1. Because more capital allows more output to be produced, it is always better for a country to have more capital

14.06 Macroeconomics Spring 2003 Final Exam Solutions Part A (True, false or uncertain) 1. Because more capital allows more output to be produced, it is always better for a country to have more capital

Fiscal Policy and Economic Growth

Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far. We first introduce and discuss the intertemporal budget

Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far. We first introduce and discuss the intertemporal budget

Fiscal policy: Ricardian Equivalence, the e ects of government spending, and debt dynamics

Roberto Perotti November 20, 2013 Version 02 Fiscal policy: Ricardian Equivalence, the e ects of government spending, and debt dynamics 1 The intertemporal government budget constraint Consider the usual

Roberto Perotti November 20, 2013 Version 02 Fiscal policy: Ricardian Equivalence, the e ects of government spending, and debt dynamics 1 The intertemporal government budget constraint Consider the usual

Answers to Problem Set #6 Chapter 14 problems

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Answers to Problem Set #8

Macroeconomic Theory Spring 2013 Chapter 15 Answers to Problem Set #8 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values

Macroeconomic Theory Spring 2013 Chapter 15 Answers to Problem Set #8 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values

Micro-foundations: Consumption. Instructor: Dmytro Hryshko

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Government debt. Lecture 9, ECON Tord Krogh. September 10, Tord Krogh () ECON 4310 September 10, / 55

ECON 4310 September 10, / 55") Government debt Lecture 9, ECON 4310 Tord Krogh September 10, 2013 Tord Krogh () ECON 4310 September 10, 2013 1 / 55 Today s lecture Topics: Basic concepts Tax smoothing Debt crisis Sovereign risk Tord

Government debt Lecture 9, ECON 4310 Tord Krogh September 10, 2013 Tord Krogh () ECON 4310 September 10, 2013 1 / 55 Today s lecture Topics: Basic concepts Tax smoothing Debt crisis Sovereign risk Tord

1 Ricardian Neutrality of Fiscal Policy

1 Ricardian Neutrality of Fiscal Policy For a long time, when economists thought about the effect of government debt on aggregate output, they focused on the so called crowding-out effect. To simplify

1 Ricardian Neutrality of Fiscal Policy For a long time, when economists thought about the effect of government debt on aggregate output, they focused on the so called crowding-out effect. To simplify

Eco504 Spring 2010 C. Sims MID-TERM EXAM. (1) (45 minutes) Consider a model in which a representative agent has the objective. B t 1.

(45 minutes) Consider a model in which a representative agent has the objective. B t 1.") Eco504 Spring 2010 C. Sims MID-TERM EXAM (1) (45 minutes) Consider a model in which a representative agent has the objective function max C,K,B t=0 β t C1 γ t 1 γ and faces the constraints at each period

Eco504 Spring 2010 C. Sims MID-TERM EXAM (1) (45 minutes) Consider a model in which a representative agent has the objective function max C,K,B t=0 β t C1 γ t 1 γ and faces the constraints at each period

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

A Central Bank Theory of Price Level Determination

A Central Bank Theory of Price Level Determination Pierpaolo Benigno (LUISS and EIEF) Monetary Policy in the 21st Century CIGS Conference on Macroeconomic Theory and Policy 2017 May 30, 2017 Pierpaolo

A Central Bank Theory of Price Level Determination Pierpaolo Benigno (LUISS and EIEF) Monetary Policy in the 21st Century CIGS Conference on Macroeconomic Theory and Policy 2017 May 30, 2017 Pierpaolo

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Classroom Etiquette. No reading the newspaper in class (this includes crossword puzzles). Limited talking. Attendance is NOT REQUIRED.

. Limited talking. Attendance is NOT REQUIRED.") Classroom Etiquette No reading the newspaper in class (this includes crossword puzzles). Limited talking. Attendance is NOT REQUIRED. Chari and Kehoe article: Modern Macroeconomics in Practice: How Theory

Classroom Etiquette No reading the newspaper in class (this includes crossword puzzles). Limited talking. Attendance is NOT REQUIRED. Chari and Kehoe article: Modern Macroeconomics in Practice: How Theory

Consumption-Savings Decisions and Credit Markets

Consumption-Savings Decisions and Credit Markets Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) Consumption-Savings Decisions Fall

Consumption-Savings Decisions and Credit Markets Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) Consumption-Savings Decisions Fall

Macroeconomics. Based on the textbook by Karlin and Soskice: Macroeconomics: Institutions, Instability, and the Financial System

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

Intermediate Macroeconomics, 7.5 ECTS

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

Eco504 Fall 2010 C. Sims CAPITAL TAXES

Eco504 Fall 2010 C. Sims CAPITAL TAXES 1. REVIEW: SMALL TAXES SMALL DEADWEIGHT LOSS Static analysis suggests that deadweight loss from taxation at rate τ is 0(τ 2 ) that is, that for small tax rates the

Eco504 Fall 2010 C. Sims CAPITAL TAXES 1. REVIEW: SMALL TAXES SMALL DEADWEIGHT LOSS Static analysis suggests that deadweight loss from taxation at rate τ is 0(τ 2 ) that is, that for small tax rates the

LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence. September 19, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence September 19, 2018 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence September 19, 2018 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

The Ramsey Model. Lectures 11 to 14. Topics in Macroeconomics. November 10, 11, 24 & 25, 2008

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

Ramsey s Growth Model (Solution Ex. 2.1 (f) and (g))

and (g))") Problem Set 2: Ramsey s Growth Model (Solution Ex. 2.1 (f) and (g)) Exercise 2.1: An infinite horizon problem with perfect foresight In this exercise we will study at a discrete-time version of Ramsey

Problem Set 2: Ramsey s Growth Model (Solution Ex. 2.1 (f) and (g)) Exercise 2.1: An infinite horizon problem with perfect foresight In this exercise we will study at a discrete-time version of Ramsey

Please choose the most correct answer. You can choose only ONE answer for every question.

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Options for Fiscal Consolidation in the United Kingdom

WP//8 Options for Fiscal Consolidation in the United Kingdom Dennis Botman and Keiko Honjo International Monetary Fund WP//8 IMF Working Paper European Department and Fiscal Affairs Department Options

WP//8 Options for Fiscal Consolidation in the United Kingdom Dennis Botman and Keiko Honjo International Monetary Fund WP//8 IMF Working Paper European Department and Fiscal Affairs Department Options

9. Real business cycles in a two period economy

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

Chapter 15. Government Spending and its Financing Pearson Addison-Wesley. All rights reserved

Chapter 15 Government Spending and its Financing Chapter Outline The Government Budget: Some Facts and Figures Government Spending, Taxes, and the Macroeconomy Government Deficits and Debt Deficits and

Chapter 15 Government Spending and its Financing Chapter Outline The Government Budget: Some Facts and Figures Government Spending, Taxes, and the Macroeconomy Government Deficits and Debt Deficits and

Classroom Etiquette. No reading the newspaper in class (this includes crossword puzzles). Attendance is NOT REQUIRED.

. Attendance is NOT REQUIRED.") Classroom Etiquette No reading the newspaper in class (this includes crossword puzzles). Limited talking No Texting. Attendance is NOT REQUIRED. Do NOT leave in the middle of the lecture. What is this??

Classroom Etiquette No reading the newspaper in class (this includes crossword puzzles). Limited talking No Texting. Attendance is NOT REQUIRED. Do NOT leave in the middle of the lecture. What is this??

The Goods Market and the Aggregate Expenditures Model

The Goods Market and the Aggregate Expenditures Model Chapter 8 The Historical Development of Modern Macroeconomics The Great Depression of the 1930s led to the development of macroeconomics and aggregate

The Goods Market and the Aggregate Expenditures Model Chapter 8 The Historical Development of Modern Macroeconomics The Great Depression of the 1930s led to the development of macroeconomics and aggregate

Macroeconomics and finance

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Business Cycles. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") Business Cycles (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the

Business Cycles (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the

1 Ricardian Neutrality of Fiscal Policy

1 Ricardian Neutrality of Fiscal Policy We start our analysis of fiscal policy by stating a neutrality result for fiscal policy which is due to David Ricardo (1817), and whose formal illustration is due

1 Ricardian Neutrality of Fiscal Policy We start our analysis of fiscal policy by stating a neutrality result for fiscal policy which is due to David Ricardo (1817), and whose formal illustration is due

Business Cycles II: Theories

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

Lecture Notes. Macroeconomics - ECON 510a, Fall 2010, Yale University. Fiscal Policy. Ramsey Taxation. Guillermo Ordoñez Yale University

Lecture Notes Macroeconomics - ECON 510a, Fall 2010, Yale University Fiscal Policy. Ramsey Taxation. Guillermo Ordoñez Yale University November 28, 2010 1 Fiscal Policy To study questions of taxation in

Lecture Notes Macroeconomics - ECON 510a, Fall 2010, Yale University Fiscal Policy. Ramsey Taxation. Guillermo Ordoñez Yale University November 28, 2010 1 Fiscal Policy To study questions of taxation in

Advanced Macroeconomics 4. The Zero Lower Bound and the Liquidity Trap

Advanced Macroeconomics 4. The Zero Lower Bound and the Liquidity Trap Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Zero Lower Bound Spring 2015 1 / 26 Can Interest Rates Be Negative?

Advanced Macroeconomics 4. The Zero Lower Bound and the Liquidity Trap Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Zero Lower Bound Spring 2015 1 / 26 Can Interest Rates Be Negative?

Toshihiro Ihori. Principles of Public. Finance. Springer

Toshihiro Ihori Principles of Public Finance Springer Contents 1 Public Finance and a Review of Basic Concepts 1 1 The Main Functions of the Public Sector 1 1.1 Resource Allocation 1 1.2 Redistribution

Toshihiro Ihori Principles of Public Finance Springer Contents 1 Public Finance and a Review of Basic Concepts 1 1 The Main Functions of the Public Sector 1 1.1 Resource Allocation 1 1.2 Redistribution

INTERMEDIATE MACROECONOMICS

INTERMEDIATE MACROECONOMICS LECTURE 6 Douglas Hanley, University of Pittsburgh CONSUMPTION AND SAVINGS IN THIS LECTURE How to think about consumer savings in a model Effect of changes in interest rate

INTERMEDIATE MACROECONOMICS LECTURE 6 Douglas Hanley, University of Pittsburgh CONSUMPTION AND SAVINGS IN THIS LECTURE How to think about consumer savings in a model Effect of changes in interest rate

Fiscal and Monetary Policies: Background

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

GOVERNMENT AND FISCAL POLICY IN JUNE 16, 2010 THE CONSUMPTION-SAVINGS MODEL (CONTINUED) ADYNAMIC MODEL OF THE GOVERNMENT

ADYNAMIC MODEL OF THE GOVERNMENT") GOVERNMENT AND FISCAL POLICY IN THE CONSUMPTION-SAVINGS MODEL (CONTINUED) JUNE 6, 200 A Government in the Two-Period Model ADYNAMIC MODEL OF THE GOVERNMENT So far only consumers in our two-period world

GOVERNMENT AND FISCAL POLICY IN THE CONSUMPTION-SAVINGS MODEL (CONTINUED) JUNE 6, 200 A Government in the Two-Period Model ADYNAMIC MODEL OF THE GOVERNMENT So far only consumers in our two-period world

Macroeconomics: Policy, 31E23000

Macroeconomics: Policy, 31E23000 Lecture 1 Pertti Aalto University School of Business 22.02.2016 About this course 1 Current crisis: Role of policies in creating it? Role of policies in helping to get

Macroeconomics: Policy, 31E23000 Lecture 1 Pertti Aalto University School of Business 22.02.2016 About this course 1 Current crisis: Role of policies in creating it? Role of policies in helping to get

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Week 5. Remainder of chapter 9: the complete real model Chapter 10: money Copyright 2008 Pearson Addison-Wesley. All rights reserved.

Week 5 Remainder of chapter 9: the complete real model Chapter 10: money 10-1 A Decrease in the Current Capital Stock This could arise due to a war or natural disaster. Output may rise or fall, depending

Week 5 Remainder of chapter 9: the complete real model Chapter 10: money 10-1 A Decrease in the Current Capital Stock This could arise due to a war or natural disaster. Output may rise or fall, depending

Lecture 2 General Equilibrium Models: Finite Period Economies

Lecture 2 General Equilibrium Models: Finite Period Economies Introduction In macroeconomics, we study the behavior of economy-wide aggregates e.g. GDP, savings, investment, employment and so on - and

Lecture 2 General Equilibrium Models: Finite Period Economies Introduction In macroeconomics, we study the behavior of economy-wide aggregates e.g. GDP, savings, investment, employment and so on - and

Graduate Macro Theory II: Fiscal Policy in the RBC Model

Graduate Macro Theory II: Fiscal Policy in the RBC Model Eric Sims University of otre Dame Spring 7 Introduction This set of notes studies fiscal policy in the RBC model. Fiscal policy refers to government

Graduate Macro Theory II: Fiscal Policy in the RBC Model Eric Sims University of otre Dame Spring 7 Introduction This set of notes studies fiscal policy in the RBC model. Fiscal policy refers to government

(Incomplete) summary of the course so far

summary of the course so far") (Incomplete) summary of the course so far Lecture 9a, ECON 4310 Tord Krogh September 16, 2013 Tord Krogh () ECON 4310 September 16, 2013 1 / 31 Main topics This semester we will go through: Ramsey (check)

(Incomplete) summary of the course so far Lecture 9a, ECON 4310 Tord Krogh September 16, 2013 Tord Krogh () ECON 4310 September 16, 2013 1 / 31 Main topics This semester we will go through: Ramsey (check)

EC 324: Macroeconomics (Advanced)

") EC 324: Macroeconomics (Advanced) Consumption Nicole Kuschy January 17, 2011 Course Organization Contact time: Lectures: Monday, 15:00-16:00 Friday, 10:00-11:00 Class: Thursday, 13:00-14:00 (week 17-25)

EC 324: Macroeconomics (Advanced) Consumption Nicole Kuschy January 17, 2011 Course Organization Contact time: Lectures: Monday, 15:00-16:00 Friday, 10:00-11:00 Class: Thursday, 13:00-14:00 (week 17-25)

FISCAL POLICY AND THE PRICE LEVEL CHRISTOPHER A. SIMS. C 1t + S t + B t P t = 1 (1) C 2,t+1 = R tb t P t+1 S t 0, B t 0. (3)

C 2,t+1 = R tb t P t+1 S t 0, B t 0. (3)") FISCAL POLICY AND THE PRICE LEVEL CHRISTOPHER A. SIMS These notes are missing interpretation of the results, and especially toward the end, skip some steps in the mathematics. But they should be useful

FISCAL POLICY AND THE PRICE LEVEL CHRISTOPHER A. SIMS These notes are missing interpretation of the results, and especially toward the end, skip some steps in the mathematics. But they should be useful

Intermediate Macroeconomics

Intermediate Macroeconomics Lecture 12 - A dynamic micro-founded macro model Zsófia L. Bárány Sciences Po 2014 April Overview A closed economy two-period general equilibrium macroeconomic model: households

Intermediate Macroeconomics Lecture 12 - A dynamic micro-founded macro model Zsófia L. Bárány Sciences Po 2014 April Overview A closed economy two-period general equilibrium macroeconomic model: households

Lecture Notes in Macroeconomics. Christian Groth

Lecture Notes in Macroeconomics Christian Groth July 28, 2016 ii Contents Preface xvii I THE FIELD AND BASIC CATEGORIES 1 1 Introduction 3 1.1 Macroeconomics............................ 3 1.1.1 The field............................

Lecture Notes in Macroeconomics Christian Groth July 28, 2016 ii Contents Preface xvii I THE FIELD AND BASIC CATEGORIES 1 1 Introduction 3 1.1 Macroeconomics............................ 3 1.1.1 The field............................

Carlin & Soskice: Macroeconomics

Carlin & Soskice: Macroeconomics 6 Fiscal Policy Solutions to questions set in the textbook Please email w.carlin@ucl.ac.uk with any comments about the questions and answers. We would also be pleased to

Carlin & Soskice: Macroeconomics 6 Fiscal Policy Solutions to questions set in the textbook Please email w.carlin@ucl.ac.uk with any comments about the questions and answers. We would also be pleased to

Lecture 10: Two-Period Model

Lecture 10: Two-Period Model Consumer s consumption/savings decision responses of consumer to changes in income and interest rates. Government budget deficits and the Ricardian Equivalence Theorem. Budget

Lecture 10: Two-Period Model Consumer s consumption/savings decision responses of consumer to changes in income and interest rates. Government budget deficits and the Ricardian Equivalence Theorem. Budget

1 No capital mobility

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #7 1 1 No capital mobility In the previous lecture we studied the frictionless environment

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #7 1 1 No capital mobility In the previous lecture we studied the frictionless environment

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

SDP Macroeconomics Final exam, 2014 Professor Ricardo Reis

SDP Macroeconomics Final exam, 2014 Professor Ricardo Reis Answer each question in three or four sentences and perhaps one equation or graph. Remember that the explanation determines the grade. 1. Question

SDP Macroeconomics Final exam, 2014 Professor Ricardo Reis Answer each question in three or four sentences and perhaps one equation or graph. Remember that the explanation determines the grade. 1. Question

QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS. Economics 222 A&B Macroeconomic Theory I. Final Examination 20 April 2009

Page 1 of 9 QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222 A&B Macroeconomic Theory I Final Examination 20 April 2009 Instructors: Nicolas-Guillaume Martineau (Section

Page 1 of 9 QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222 A&B Macroeconomic Theory I Final Examination 20 April 2009 Instructors: Nicolas-Guillaume Martineau (Section

Fiscal Policy. Changes in federal taxes and purchases

Fiscal Policy Changes in federal taxes and purchases Where does the government spend its money? Federal Government Spending, 2010 Fiscal Policy An Overview of Government Spending and Taxes The Federal

Fiscal Policy Changes in federal taxes and purchases Where does the government spend its money? Federal Government Spending, 2010 Fiscal Policy An Overview of Government Spending and Taxes The Federal

Open Economy Macroeconomics: Theory, methods and applications

Open Economy Macroeconomics: Theory, methods and applications Econ PhD, UC3M Lecture 9: Data and facts Hernán D. Seoane UC3M Spring, 2016 Today s lecture A look at the data Study what data says about open

Open Economy Macroeconomics: Theory, methods and applications Econ PhD, UC3M Lecture 9: Data and facts Hernán D. Seoane UC3M Spring, 2016 Today s lecture A look at the data Study what data says about open

SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM

26 SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM WHAT S NEW IN THE FOURTH EDITION: There are no substantial changes to this chapter. LEARNING OBJECTIVES: By the end of this chapter, students should understand:

26 SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM WHAT S NEW IN THE FOURTH EDITION: There are no substantial changes to this chapter. LEARNING OBJECTIVES: By the end of this chapter, students should understand:

GRA 6639 Topics in Macroeconomics

Lecture 9 Spring 2012 An Intertemporal Approach to the Current Account Drago Bergholt (Drago.Bergholt@bi.no) Department of Economics INTRODUCTION Our goals for these two lectures (9 & 11): - Establish

Lecture 9 Spring 2012 An Intertemporal Approach to the Current Account Drago Bergholt (Drago.Bergholt@bi.no) Department of Economics INTRODUCTION Our goals for these two lectures (9 & 11): - Establish

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

17.2 U.S. Government Spending and Revenue Introduction. Chapter 17 The Government and the Macroeconomy. In 2008, federal spending

Chapter 17 The Government and the Macroeconomy By Charles I. Jones Media Slides Created By Dave Brown Penn State University 17.2 U.S. Government Spending and Revenue In 2008, federal spending Was about

Chapter 17 The Government and the Macroeconomy By Charles I. Jones Media Slides Created By Dave Brown Penn State University 17.2 U.S. Government Spending and Revenue In 2008, federal spending Was about

Money in an RBC framework

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Chapter 8 A Short Run Keynesian Model of Interdependent Economies

George Alogoskoufis, International Macroeconomics, 2016 Chapter 8 A Short Run Keynesian Model of Interdependent Economies Our analysis up to now was related to small open economies, which took developments

George Alogoskoufis, International Macroeconomics, 2016 Chapter 8 A Short Run Keynesian Model of Interdependent Economies Our analysis up to now was related to small open economies, which took developments

Syllabus item: 113 Weight: 3

Macroeconomics - 2.4 Fiscal policy Syllabus item: 113 Weight: 3 113. Sources of government revenue IB Question Explain that the government earns revenue primarily from taxes (direct and indirect), as well

Macroeconomics - 2.4 Fiscal policy Syllabus item: 113 Weight: 3 113. Sources of government revenue IB Question Explain that the government earns revenue primarily from taxes (direct and indirect), as well

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Postponed exam: ECON4310 Macroeconomic Theory Date of exam: Monday, December 14, 2015 Time for exam: 09:00 a.m. 12:00 noon The problem set covers 13 pages (incl.

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Postponed exam: ECON4310 Macroeconomic Theory Date of exam: Monday, December 14, 2015 Time for exam: 09:00 a.m. 12:00 noon The problem set covers 13 pages (incl.

What we know about monetary policy

Apostolis Philippopoulos What we know about monetary policy The government may have a potentially stabilizing policy instrument in its hands. But is it effective? In other words, is the relevant policy

Apostolis Philippopoulos What we know about monetary policy The government may have a potentially stabilizing policy instrument in its hands. But is it effective? In other words, is the relevant policy

THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND. Chapter 34

1 THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND Chapter 34 Importance of economic policy Economic policy refers to the actions of the government that have a direct impact on the macroeconomic

1 THE INFLUENCE OF MONETARY AND FISCAL POLICY ON AGGREGATE DEMAND Chapter 34 Importance of economic policy Economic policy refers to the actions of the government that have a direct impact on the macroeconomic

Bernanke and Gertler [1989]

![Bernanke and Gertler [1989]](/thumbs/90/103712154.jpg "Bernanke and Gertler [1989]") Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Module 4: Applications of Supply and Demand

The following list shows a summary of the topics covered in the macroeconomics course. Module 1: Economic Thinking Understanding Economics and Scarcity The Concept of Opportunity Cost Labor, Markets, and

The following list shows a summary of the topics covered in the macroeconomics course. Module 1: Economic Thinking Understanding Economics and Scarcity The Concept of Opportunity Cost Labor, Markets, and

Financial Integration in the Arab Region: A Focus on Monetary Coordination and a Presentation of New Ideas and Developments by:

Financial Integration in the Arab Region: A Focus on Monetary Coordination and a Presentation of New Ideas and Developments by: Wassim Shahin, Professor of Business Economics, Lebanese American University

Financial Integration in the Arab Region: A Focus on Monetary Coordination and a Presentation of New Ideas and Developments by: Wassim Shahin, Professor of Business Economics, Lebanese American University

Inflation & Welfare 1

1 INFLATION & WELFARE ROBERT E. LUCAS 2 Introduction In a monetary economy, private interest is to hold not non-interest bearing cash. Individual efforts due to this incentive must cancel out, because

1 INFLATION & WELFARE ROBERT E. LUCAS 2 Introduction In a monetary economy, private interest is to hold not non-interest bearing cash. Individual efforts due to this incentive must cancel out, because

Exam #3 (Final Exam) Solution Notes Spring, 2011

Solution Notes Spring, 2011") Economics 1021, Section 1 Prof. Steve Fazzari Exam #3 (Final Exam) Solution Notes Spring, 2011 MULTIPLE CHOICE (5 points each) Write the letter of the alternative that best answers the question in the

Economics 1021, Section 1 Prof. Steve Fazzari Exam #3 (Final Exam) Solution Notes Spring, 2011 MULTIPLE CHOICE (5 points each) Write the letter of the alternative that best answers the question in the

Macroeconomics, Spring 2007, Final Exam, several versions, Early May

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Spring 2007, Final Exam, several versions, Early May Read these Instructions carefully! You must follow them exactly! I) On your Scantron card

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Spring 2007, Final Exam, several versions, Early May Read these Instructions carefully! You must follow them exactly! I) On your Scantron card

Fiscal/Monetary Coordination When the Anchor Cable Has Snapped. Christopher A. Sims Princeton University

Fiscal/Monetary Coordination When the Anchor Cable Has Snapped Christopher A. Sims Princeton University sims@princeton.edu May 22, 2009 Outline Introduction The Fed balance sheet Implications for monetary

Fiscal/Monetary Coordination When the Anchor Cable Has Snapped Christopher A. Sims Princeton University sims@princeton.edu May 22, 2009 Outline Introduction The Fed balance sheet Implications for monetary

This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON

~~EC2065 ZB d0 This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZB BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences,

~~EC2065 ZB d0 This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZB BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences,

Question 5 : Franco Modigliani's answer to Simon Kuznets's puzzle regarding long-term constancy of the average propensity to consume is that : the ave

DIVISION OF MANAGEMENT UNIVERSITY OF TORONTO AT SCARBOROUGH ECMCO6H3 L01 Topics in Macroeconomic Theory Winter 2002 April 30, 2002 FINAL EXAMINATION PART A: Answer the followinq 20 multiple choice questions.

DIVISION OF MANAGEMENT UNIVERSITY OF TORONTO AT SCARBOROUGH ECMCO6H3 L01 Topics in Macroeconomic Theory Winter 2002 April 30, 2002 FINAL EXAMINATION PART A: Answer the followinq 20 multiple choice questions.

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

Topic 2: Consumption

Topic 2: Consumption Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Topic 2: Consumption 1 / 48 Reading and Lecture Plan Reading 1 SWJ Ch. 16 and Bernheim (1987) in NBER Macro

Topic 2: Consumption Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Topic 2: Consumption 1 / 48 Reading and Lecture Plan Reading 1 SWJ Ch. 16 and Bernheim (1987) in NBER Macro

Dynamic Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does not imply

only, and the presence of them, or of links to them, on the IMF website does not imply") 7 TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 9-10, 2006 The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does

7 TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 9-10, 2006 The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does

14.02 Principles of Macroeconomics Problem Set 1 Solutions Spring 2003

14.02 Principles of Macroeconomics Problem Set 1 Solutions Spring 2003 Question 1 : Short answer (a) (b) (c) (d) (e) TRUE. Recall that in the basic model in Chapter 3, autonomous spending is given by c

14.02 Principles of Macroeconomics Problem Set 1 Solutions Spring 2003 Question 1 : Short answer (a) (b) (c) (d) (e) TRUE. Recall that in the basic model in Chapter 3, autonomous spending is given by c

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy. Julio Garín Intermediate Macroeconomics Fall 2018

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Name: Days/Times Class Meets: Today s Date:

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007, Final Exam, several versions, December Read these Instructions carefully! You must follow them exactly! I) On your Scantron card

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007, Final Exam, several versions, December Read these Instructions carefully! You must follow them exactly! I) On your Scantron card

Definition 58 POTENTIAL GDP is the economy s long run growth trend for real GDP.

III GDP and the Business Cycle We now begin our discussion of business cycles, chapter. Definition 58 POTENTIAL GDP is the economy s long run growth trend for real GDP. Definition 59 The BUSINESS CYCLE

III GDP and the Business Cycle We now begin our discussion of business cycles, chapter. Definition 58 POTENTIAL GDP is the economy s long run growth trend for real GDP. Definition 59 The BUSINESS CYCLE

Intermediate Macroeconomics

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

What Are Equilibrium Real Exchange Rates?

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

Economics 826 International Finance. Final Exam: April 2007

Economics 826 International Finance Final Exam: April 2007 Answer 3 questions from Part A and 4 questions from Part B. Part A is worth 60%. Part B is worth 40%. You may write in english or french. You

Economics 826 International Finance Final Exam: April 2007 Answer 3 questions from Part A and 4 questions from Part B. Part A is worth 60%. Part B is worth 40%. You may write in english or french. You

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

Consumption, Saving, and Investment. Chapter 4. Copyright 2009 Pearson Education Canada

Consumption, Saving, and Investment Chapter 4 Copyright 2009 Pearson Education Canada This Chapter In Chapter 3 we saw how the supply of goods is determined. In this chapter we will turn to factors that

Consumption, Saving, and Investment Chapter 4 Copyright 2009 Pearson Education Canada This Chapter In Chapter 3 we saw how the supply of goods is determined. In this chapter we will turn to factors that

Outline Conduct of Economic Policy The Implementation of Economic Policy. Macroeconomic Policy. Bilgin Bari

1 The Policy Framework The Policy Interactions 2 The Policy Framework The Policy Interactions There are two major types of macroeconomic policies are used to control aggregate demand. growth of money supply

1 The Policy Framework The Policy Interactions 2 The Policy Framework The Policy Interactions There are two major types of macroeconomic policies are used to control aggregate demand. growth of money supply

3. TFU: A zero rate of increase in the Consumer Price Index is an appropriate target for monetary policy.

Econ 304 Fall 2014 Final Exam Review Questions 1. TFU: Many Americans derive great utility from driving Japanese cars, yet imports are excluded from GDP. Thus GDP should not be used as a measure of economic

Econ 304 Fall 2014 Final Exam Review Questions 1. TFU: Many Americans derive great utility from driving Japanese cars, yet imports are excluded from GDP. Thus GDP should not be used as a measure of economic

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Consumption and Savings (Continued)

") Consumption and Savings (Continued) Lecture 9 Topics in Macroeconomics November 5, 2007 Lecture 9 1/16 Topics in Macroeconomics The Solow Model and Savings Behaviour Today: Consumption and Savings Solow

Consumption and Savings (Continued) Lecture 9 Topics in Macroeconomics November 5, 2007 Lecture 9 1/16 Topics in Macroeconomics The Solow Model and Savings Behaviour Today: Consumption and Savings Solow

Macroeconomics

Macroeconomics 978-1-63545-006-4 To learn more about all our offerings Visit Knewtonalta.com Source Author(s) (Text or Video) Title(s) Link (where applicable) OpenStax Senior Contributing Authors: Steve

Macroeconomics 978-1-63545-006-4 To learn more about all our offerings Visit Knewtonalta.com Source Author(s) (Text or Video) Title(s) Link (where applicable) OpenStax Senior Contributing Authors: Steve

QUIZ 4: Macro Winter Question 1. Would you expect a country to have a larger Deficit/GDP ratio or a Debt/GDP ratio?

Name: QUIZ 4: Macro Winter 2011 You must always show your thinking to get full credit. Question 1 Would you expect a country to have a larger Deficit/GDP ratio or a Debt/GDP ratio? You would expect the

Name: QUIZ 4: Macro Winter 2011 You must always show your thinking to get full credit. Question 1 Would you expect a country to have a larger Deficit/GDP ratio or a Debt/GDP ratio? You would expect the

Business Cycles. (c) Copyright 1999 by Douglas H. Joines 1. Module Objectives. What Are Business Cycles?

Copyright 1999 by Douglas H. Joines 1. Module Objectives. What Are Business Cycles?") Business Cycles Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the business cycle Understand the benefits and

Business Cycles Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the business cycle Understand the benefits and

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8 1 Cagan Model of Money Demand 1.1 Money Demand Demand for real money balances ( M P ) depends negatively on expected inflation In logs m d t p t =

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8 1 Cagan Model of Money Demand 1.1 Money Demand Demand for real money balances ( M P ) depends negatively on expected inflation In logs m d t p t =

ANSWER: We can find consumption and saving by solving:

Economics 154a, Spring 2005 Intermediate Macroeconomics Problem Set 4: Answer Key 1. Consider an economy that consists of a single consumer who lives for two time periods. The consumers income in the current

Economics 154a, Spring 2005 Intermediate Macroeconomics Problem Set 4: Answer Key 1. Consider an economy that consists of a single consumer who lives for two time periods. The consumers income in the current