International Journal of Academic Research ISSN: ; Vol.4, Issue-1(1), January, 2017 Impact Factor: 4.535;

|

|

|

- Gertrude Allison

- 5 years ago

- Views:

Transcription

1 Compositional changes of public expenditure in Andhra Pradesh Dr.B.Lilly Grace Eunice, Assistant Professor, Dept. of Economics, Andhra University Visakhapatnam Mr.D.Narayana Rao, Lecturer, Girraj Govt. College (A), Nizamabad Abstract: The private market economy is unable to create the needed economic infrastructure and social overhead capital in developing countries like India. The creation of economic infrastructure such as electricity, irrigation, transportation and communication and social overhead capital such as education, medical and public health and social security measures has become the main responsibility of the governments. Physical quality of life and human well-being are pivotal on the enhanced availability of these social services. These services lead to overall increase in productivity. It is in this context public expenditure assumes an important role in the process of economic development both in the developed and developing countries of the world. Hence an attempt is made to examine the changes in developmental expenditure in the State of Andhra Pradesh. It is found that there is fall in the developmental expenditure which in turn effects the development of the state of Andhra Pradesh. The compositional changes are leading to fall in the provision of social and economic infrastructure. Hence it is suggested to mobilise resources for the development of infrastructure facilities by curtailing the unnecessary expenditure on unproductive activities. Key Words: Development Expenditure, Economic Services, Social Services Introduction The credit for the recognition of the role of public expenditure in the determination and distribution of national income goes to J.M. Keynes s General Theory, which provides a theoretical base for the recent developments in the public expenditure programmes. Amartya Sen, the 1998 Nobel Laureate, emphasises that economic growth and development at a faster rate is impossible in the absence of social capital. The basic condition for economic development is the creation of infrastructure facilities and social overhead capital, which requires huge investment. The private market economy is unable to create the needed economic infrastructure and social overhead capital in developing countries like India. The creation of economic infrastructure such as electricity, irrigation, transportation and communication and social overhead capital such as education, medical and public health and social security measures has become the main responsibility of the governments. Physical quality of life and human wellbeing are pivotal on the enhanced availability of these social services. These services lead to overall increase in productivity 1. It is in this context public 03_04_05/Social_%20infra.pdf

2 expenditure assumes an important role in the process of economic development both in the developed and developing countries of the world. It is increasingly realised that the Human Development is a function of growth in Social Sector Expenditure. Development is practically impossible to achieve in a specified period of time without an adequate budgetary provision to various social sectors to provide the basic facilities, such as, education, health, roads and buildings, nutrition, rural infrastructure etc. It clearly speaks the importance of the development of Social Sectors in a country, state or region. Countries all over the world have increasingly recognised that social development is the right kind of investment. In this context it is not out of place to recall the opinion of Alfred Marshall who says that the most valuable form of capital is that invested in human beings 2. The credit for bringing special focus on human development can mainly be attributed to the noted economist Mahbub-Ul-Haq. He opines that people must be at the Centre of our development debate What really counts is how they participate in economic growth and how they benefit from it 3. The effectiveness and efficiency of government expenditure in the social sector varies between different geographical regions, and also depends Alfred Marshall (1980), Principles of Economics, Sixth Edition (1910), Mac Millan, London, p.564. Mahbub-Ul-Haq (1992), Human Development in a Changing world, Occasional Papers, Human Development Report office, New York, p.1. on the stage of development. Innovative institutional arrangements and alternative financing mechanisms are being explored in order to supplement public funds, and to improve the effectiveness of the public resources invested. For developing countries, the gains from education and its spill-over effects into other sectors will mean that the social return is likely to be more than to private return 4. Andhra Pradesh is one of the major states embarking upon planned economic development. Its development is still below its potential in spite of its endowment of natural resources 5. The expenditure policies of the State have been influenced by the policies of the Central Government. The revenue and expenditure policy of the successive governments at the State was such that by 1980s there was surplus on the revenue account. For instance, there was Rs. 103 crores, Rs. 80 crores and Rs. 133 crores surplus on the revenue account of the State during , and respectively. But the State experienced fiscal and revenue deficits during the later period. While the developmental expenditure increased due to the plan programs, the non-plan, nondevelopment expenditure shot up by 1990s for a variety of reasons. The increased revenue component of the Plan programs, interest payments and debt repayment obligations, ever-increasing 4 Banerjee, A. and E. Duflo (2004), Growth Theory through the Lens of Development Economics, mimeo, MIT. J.V.M. Sharma (2003), Fiscal Management: A Review, Economic And Political Weekly, March 22-29, p

3 government employment and establishment, large scale proliferation of populist schemes and public enterprises during the last four decades especially during 1980s have landed the State in huge fiscal and revenue deficits which reached to staggering levels by 1990s. It may be noted that the changes in the political parties in power during 1980s have influenced the expenditure policy of the State resulting in changes in the composition, pattern, direction and the growth of public expenditure. The revenue expenditure has increased phenomenally leading to substantial decline in the capital expenditure. The fiscal reforms have taken a definite shape in the State since , the expenditure policies of the government have been influenced by the economic reforms, especially the fiscal reforms, initiated by the Central government since mid In fact, Andhra Pradesh is one of the major states that responded positively to the economic reforms and has undertaken fiscal reforms. One of the main aims of the fiscal reforms is not only to compress the unabated growth of public expenditure but also to bring reprioritisation and a compositional shift in order to achieve higher economic growth by increasing the proportion of capital outlay and developmental expenditure in the total expenditure. But expenditure compression either by withdrawing or reducing developmental expenditure instead of nondevelopmental expenditure will adversely affect the growth prospects of the State. The State has initiated several measures in this direction since The state has experienced several shifts in its expenditure policies during the last two decades. Objective of the Study: With the above backdrop an attempt is made in this paper to examine structure and composition of developmental expenditure in the State of Andhra Pradesh from to (united). Data sources and methodology: The data used in this study is at current prices. Percentages are calculated to see the proportions of individual items in total developmental expenditure under different heads. In this study revenue and capital developmental expenditure is taken from the State Finances - A study of Budgets, published by Reserve Bank of India. Capital account of developmental expenditure includes expenditure on developmental purposes which are given under the head Loans and Advances by State Government. Basis of classification: A more meaningful classification and presentation of government operations in terms of functions, programmes and activities has assumed great importance 6. The State government budgets are organised along the lines of the comptroller and auditor generals four digit accounting classification with disaggregating into the traditional revenue and capital account and with additional decomposition of expenditure in to plan and non-plan categories, the later since the advent of planning in In addition, the Reserve Bank of India has been classifying budget heads into functional categories such as developmental and non-developmental Bureau of Economics and Statistics, Government of Andhra Pradesh.

4 categories of expenditure from the beginning of the early 1950s 7. All expenditure under revenue and capital account (consisting of capital outlay and loan and advances) are categorised into general services, social services and economic services. Expenditure on economic services (agriculture and rural development, industry, physical infrastructure, etc.) and social services (education, health, housing, labour welfare etc.) constitutes developmental expenditure, while those on general services comprising all services of an administrative nature including pensions as well as interest payments are covered under the category of non-developmental expenditure. The items of expenditure which have an obvious growth implication and directly related to the elevation of economic development are considered developmental or productive, whereas those which have no obvious growth implications and are not linked directly to economic growth either in the form of physical and human capital are considered as non-developmental expenditure or unproductive expenditure. The expenditure on general services, which includes spending on administration, internal and external security, judiciary and interest payments are considered non-developmental, whereas, expenditure on social, ommunity and economic services are considered developmental 8. Structure of developmental expenditure: The State governments in India have been assigned the duty to perform developmental activities to develop the economy. It refers only to a broad functional classification adopted in the budget. They are included in both revenue and capital accounts of the budget. Developmental expenditure includes items of expenditure such as education, medical care, public health, family welfare, labour employment, agricultural and animal husbandry, cooperation, rural and community development, irrigation, transport and communication, forests and other miscellaneous services. Expenditure incurred on these items both on revenue and capital accounts is grouped under developmental expenditure. The items covered under developmental expenditure mainly consist of social and economic services. The items covered under social services of revenue account are as follows: i) Education, sports, arts and culture, ii) Medical, public health and family welfare iii) Water supply and sanitation, iv) Housing, v) Urban development, vi) Welfare of scheduled castes, scheduled tribes and other backward classes, vii) Labour and labour welfare, viii) Social security and welfare ix) Nutrition, x) Relief on account of natural calamities xi) Others - which includes expenditure on information and K.S.Krishnaswamy, (1953), Finances of Part A & Part B States, Reserve Bank of India Bulletin, May. M.Jamal Khan (1993), Patterns of Public Expenditure and Financing in India, Pragati Publications, Delhi, p.19.

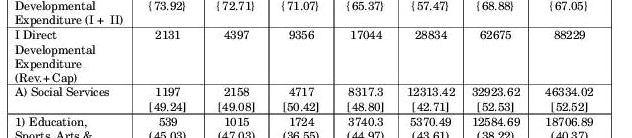

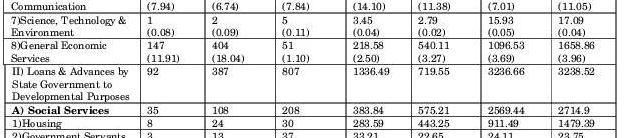

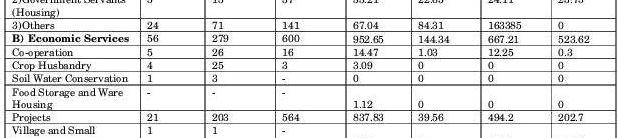

5 publicity, secretariat - social services, other social services, etc. Items covered under expenditure on economic services are as follows 1) Agriculture and Allied Activities - which includes i) Crop husbandry ii) Soil and water conservation iii) Animal husbandry iv) Dairy development v) Fisheries vi) Forestry and wild life vii) Plantation viii) Food storage and warehousing ix) Agricultural research and education x) Agricultural financial institutions xi) Co-operation and xii) Other agricultura1 programmes 2) Rural development 3) Special area programme 4) Irrigation and flood control 5) Energy - which includes power 6) Industry and minerals i) Village and small industries ii) Industries. 7) Transport and communications - which includes i) Roads and bridges ii) Others - include expenditure on port and light houses, civil aviation, road transport, inland water transport etc. 8) Science, technology and environment 9) General economic services - which includes i) Secretariat - economic services ii) Tourism iii) Civil supplies iv) Others - include expenditure on foreign trade and export promotion census, surveys and statistics other general economic services. Loans and advances by state government under capital account include developmental purposes and nondevelopmental purposes. Developmental purposes includes social services such as housing, government servants housing and others and economic services such as co-operation, crop husbandry, soil and water conservation, power projects, village and small industries, other industries, minerals and others. Loans and advances by State government indicate the schemes for which the loans are made. The institutions, organisations etc. to whom the loans are given will appear under detailed heads as - Municipalities, Panchayat Raj institutions, public sector and other undertakings, cultivators, port trusts and other parties. Loans to scholars under national loans scholarship schemes and educational loans for engineering studies are loans for education, sports, arts and culture, loans for medical and public health, loans for water supply and sanitation, loans for housing, loans for information and publicity etc. 9 Composition of developmental expenditure: Important items of developmental expenditure of Andhra Pradesh in select years during to are presented in Table 1. It may be seen from the Table that the total developmental expenditure including the loans and advances by State government for various developmental purposes has increased from Rs. 2,523 crores in to Rs crores in Developmental expenditure other than the loans and advances given by the State government has been increased from Rs. 2,131 crores in to Rs. 88,229 crores in The proportion of expenditure on Social Services in developmental expenditure is less than 50 per cent until reached to per cent in The proportion of expenditure on Economic Services is marginally higher than 50 per cent in 1980 s and reduced to the per cent in Among the social services expenditures education, sports, arts and culture, Ibid, p. 205.

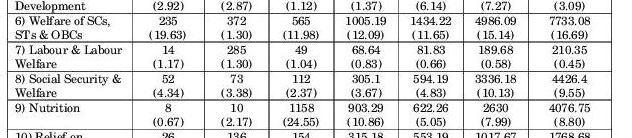

6 medical and public health and family welfare, welfare of scheduled caste, scheduled tribes and other backward classes and social security and welfare are the major components in all the select years. It may be noticed that expenditure on education, sports, arts and culture are shown under single head. Within this category of expenditure there are sub-categories, such as general education, technical education, sports and youth services and arts and culture. Again each category of expenditure consists of sub-categories such as - general education includes elementary education, secondary education, university and higher education, adult education, language development and expenditure on general items. Similarly expenditure items covered under technical education are expenditure on direction and administration, assistance to universities for technical education, assistance to non-government technical colleges and institutes, expenditure on polytechnics, scholarships etc. The expenditure items covered under sports and youth services are direction and administration, physical education, youth welfare programme for students, sports and games etc. Expenditure items covered under art and culture are direction and administration, fine arts and education, promotion of art and culture, archaeology, archives, public libraries museums etc. It may be seen in the Table that the expenditure on Education, Sports, Arts and Culture is Rs.539 crores in , which has increased to Rs.18,707 crores in Expenditure on medical and public health constitutes expenditure on urban health services, allopathic, other systems of medicine, expenditure on rural health services, medical education, expenditure on public health etc. Expenditure on family welfare covers expenditure on direction and administration, rural family welfare service, maternity and child health and compensation etc. The expenditure on medical and public health and family welfare amounted to Rs. 189 crores in and increased to Rs. 5,939 crores in The expenditure on welfare of scheduled castes, scheduled tribes and other backward classes, which includes in the budget, as a separate head from is another major component of social services has increased from Rs.235 crores in to Rs.7,733 crores in Another major component of expenditure on social services is expenditure on social security and welfare which includes welfare of handicapped, child welfare, women's welfare, welfare of aged and destitute, correctional services etc. have increased from Rs. 52 crores in to Rs.4,426 crores in Though there is an increase in the proportion of expenditure on social services during the study period, from the figure 1 and 2 remarkable change in the composition of expenditure on social services may be observed. Under social sector expenditure Educational expenditure declined from per cent in to per cent in Similarly Medical, Public Health and Family Welfare also shows declining share in expenditure on Social Services. Expenditure on Social Security and welfare and Nutrition shows an increasing trend. For instance, expenditure on social security and welfare increased from 4.34 per cent in to 9.55 per cent in The same may be seen in Figure 1 and 2.

7

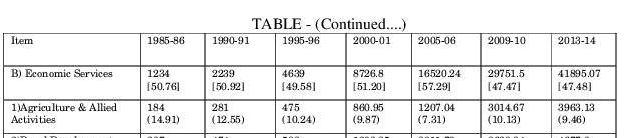

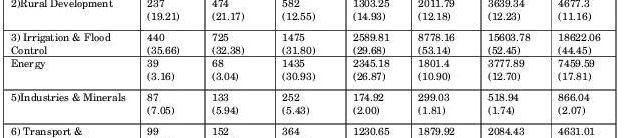

8 Among the expenditure on Economic Services - agriculture and allied activities, rural development, irrigation and flood control, energy, transport and communication are the major components. The expenditure on agriculture and allied activities amounted to Rs.184 crores in , which has increased to Rs.3,963 crores in The expenditure on rural development has been segregated only from agriculture and allied activities in and shown separately. The expenditure in rural development has increased from Rs.237 crores in to Rs.4,677 crores in The expenditure on irrigation and flood control has increased from Rs.440 crores to Rs.18,622 crores during the same period. The expenditure on energy has increased from Rs.39 crores in to Rs. 7,460 crores in The

9 expenditure on transport and communication has increased from Rs.99 crores in to Rs.4,631 crores in It may be observed from the Table that the share of expenditure on Economic Services declined during the study period from per cent in to per cent in It is clear from the Table that the share of expenditure on agriculture and allied activities, rural development, industries & minerals, science, technology and environment declined during the study period. Similarly, the share of expenditure on Irrigation & flood control, energy, transport and communication increased remarkably during the study period. The same are shown in Figure 3 and 4. Conclusion The proportion of developmental expenditure in total expenditure is declining during the study period. Hence the State of Andhra Pradesh needs to concentrate on improvement of mobilisation of resources for

10 developmental purposes. It may be observed from the composition of developmental expenditure that social services show increasing trend and economic services show decreasing trend during the select years of the study. It is also noticed that among sub sectors of social services like education, medical and public health, family welfare expenditure are declining. Those expenditure items are having significant influence on human development. Hence the State should be cautious to reduce unnecessary expenditure instead of curtailing the expenditures on human priority areas. Similarly among economic services agriculture and allied activities, rural development, industries & minerals, science, technology and environment declined during the study period. These are the expenditure items which develop economic infrastructure and play important role in the faster development of the State.

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 14,94,51,85,03, ,04,94,96,12, ,12,49,12,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF SEP/216 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF SEP/216 GENERAL STATEMENT OF ACCOUNT TAMILNADU

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 17,62,51,48,07, ,14,37,60,32, ,34,23,85,29,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF FEB/219 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF FEB/219 GENERAL STATEMENT OF ACCOUNT TAMILNADU

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 17,62,51,48,07, ,54,51,43,51, ,87,67,92,03,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF NOV/218 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF NOV/218 GENERAL STATEMENT OF ACCOUNT TAMILNADU

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT ,08,36,09,79, ,39,20,14, ,25,98,73,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF APR/216 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF APR/216 GENERAL STATEMENT OF ACCOUNT TAMILNADU

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 15,93,62,78,38, ,66,89,50,78, ,78,38,22,24,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF APR/217 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF APR/217 GENERAL STATEMENT OF ACCOUNT TAMILNADU

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 9,69,71,98,06, ,08,36,09,79, ,39,20,14,000.00

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF JUN/216 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF JUN/216 GENERAL STATEMENT OF ACCOUNT TAMILNADU

FINANCE ACCOUNTS (VOLUME I)

") FINANCE ACCOUNTS (VOLUME I) 2013-2014 GOVERNMENT OF MADHYA PRADESH Finance Accounts (VOLUME - I) 2013-14 Government of Madhya Pradesh TABLE OF CONTENTS SUBJECT PAGES VOLUME - I Table of contents i-ii Certificate

FINANCE ACCOUNTS (VOLUME I) 2013-2014 GOVERNMENT OF MADHYA PRADESH Finance Accounts (VOLUME - I) 2013-14 Government of Madhya Pradesh TABLE OF CONTENTS SUBJECT PAGES VOLUME - I Table of contents i-ii Certificate

Finance Accounts (Volume- I) Government of Haryana

Government of Haryana") Finance Accounts (Volume- I) 2015-16 Government of Haryana Subject (i) TABLE OF CONTENTS VOLUME-I Page(s) Certificate of the Comptroller and Auditor General of India (iii)-(v) Guide to Finance Accounts

Finance Accounts (Volume- I) 2015-16 Government of Haryana Subject (i) TABLE OF CONTENTS VOLUME-I Page(s) Certificate of the Comptroller and Auditor General of India (iii)-(v) Guide to Finance Accounts

Mahender Jethmalani.

12 th Five Year Plan: Concerns for the Tribal Development in Gujarat Organized by Tribal Research and Training Institute, Gujarat Vidyapith, Ahmedabad & Pathey Budget Center. 7 th October, 2011. Mahender

12 th Five Year Plan: Concerns for the Tribal Development in Gujarat Organized by Tribal Research and Training Institute, Gujarat Vidyapith, Ahmedabad & Pathey Budget Center. 7 th October, 2011. Mahender

EXPLANATORY NOTES ON DATA SOURCE AND METHODOLOGY

EXPLANATORY NOTES ON DATA SOURCE AND METHODOLOGY Data Sources The data on State Government Finances are based on the receipts and expenditure data presented in the Budget documents of the State Governments

EXPLANATORY NOTES ON DATA SOURCE AND METHODOLOGY Data Sources The data on State Government Finances are based on the receipts and expenditure data presented in the Budget documents of the State Governments

No. M-13048/35/(PY)/2009-SP-S Government of India Planning Commission (State Plans Division)

/2009-SP-S Government of India Planning Commission (State Plans Division)") / No. M-13048/35/(PY)/2009-SP-S Government of India Planning Commission (State Plans Division) Yojana Bhawan, Sansad Marg, New Delhi-II 0 001 Dated i h July,,2010 To The Chief Secretary, Government of

/ No. M-13048/35/(PY)/2009-SP-S Government of India Planning Commission (State Plans Division) Yojana Bhawan, Sansad Marg, New Delhi-II 0 001 Dated i h July,,2010 To The Chief Secretary, Government of

GOVERNMENT OF MADHYA PRADESH APPROPRIATION ACCOUNTS

1 GOVERNMENT OF MADHYA PRADESH APPROPRIATION ACCOUNTS 2004-2005 2 APPROPRIATION ACCOUNTS 2004-2005 GOVERNMENT OF MADHYA PRADESH TABLE OF CONTENTS Pages Introductory vii Summary of Appropriation Accounts

1 GOVERNMENT OF MADHYA PRADESH APPROPRIATION ACCOUNTS 2004-2005 2 APPROPRIATION ACCOUNTS 2004-2005 GOVERNMENT OF MADHYA PRADESH TABLE OF CONTENTS Pages Introductory vii Summary of Appropriation Accounts

(17 th March, 2016)

") GOVERNMENT OF MIZORAM ANNUAL FINANCIAL STATEMENT () 2016-2017 (17 th March, 2016) [The Recommendation of His Excellency the Governor required under Article 202(1) of the Constitution of India has been

GOVERNMENT OF MIZORAM ANNUAL FINANCIAL STATEMENT () 2016-2017 (17 th March, 2016) [The Recommendation of His Excellency the Governor required under Article 202(1) of the Constitution of India has been

TABLE OF CONTENTS VOLUME-I

TABLE OF CONTENTS SUBJECT PAGES VOLUME-I Table of Contents i-ii Certificate of the Comptroller and Auditor General of India iii-v Guide to Finance Accounts vii-xi 1. Statement of Financial Position 1-2

TABLE OF CONTENTS SUBJECT PAGES VOLUME-I Table of Contents i-ii Certificate of the Comptroller and Auditor General of India iii-v Guide to Finance Accounts vii-xi 1. Statement of Financial Position 1-2

UTTAR PRADESH BUDGET MANUAL CHAPTER I

UTTAR PRADESH BUDGET MANUAL CHAPTER I INTRODUCTORY This Manual contains rules framed by the Finance Department for the guidance of estimating officers and departments of the Secretariat in regard to the

UTTAR PRADESH BUDGET MANUAL CHAPTER I INTRODUCTORY This Manual contains rules framed by the Finance Department for the guidance of estimating officers and departments of the Secretariat in regard to the

FINANCE ACCOUNTS

FINANCE ACCOUNTS 2011-2012 Volume 1 GOVERNMENT OF ASSAM Placed before the State Legislative Assembly on 10 th December 2012. FINANCE ACCOUNTS 2011-2012 Volume 1 GOVERNMENT OF ASSAM TABLE OF CONTENTS Subject

FINANCE ACCOUNTS 2011-2012 Volume 1 GOVERNMENT OF ASSAM Placed before the State Legislative Assembly on 10 th December 2012. FINANCE ACCOUNTS 2011-2012 Volume 1 GOVERNMENT OF ASSAM TABLE OF CONTENTS Subject

Welcome to Presentation of Twelfth Five Year Plan and Annual Plan Proposal Madhya Pradesh. May 11, 2012

Welcome to Presentation of Twelfth Five Year Plan and Annual Plan Proposal Madhya Pradesh May 11, 2012 1 ACHIEVEMENTS OF ELEVENTH PLAN (ECONOMY) Targets and Achievement Sector Target for Growth Expected

Welcome to Presentation of Twelfth Five Year Plan and Annual Plan Proposal Madhya Pradesh May 11, 2012 1 ACHIEVEMENTS OF ELEVENTH PLAN (ECONOMY) Targets and Achievement Sector Target for Growth Expected

MINDA INDUSTRIES LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY

POLICY") MINDA INDUSTRIES LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY MINDA INDUSTRIES LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY 1. Corporate Social Responsibility Policy At UNO Minda Group,

MINDA INDUSTRIES LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY MINDA INDUSTRIES LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY 1. Corporate Social Responsibility Policy At UNO Minda Group,

GOVERNMENT OF MADHYA PRADESH

GOVERNMENT OF MADHYA PRADESH ACCOUNTANT GENERAL (ACCOUNTS AND ENTITLEMENTS) MADHYA PRADESH, GWALIOR 2 Preface The Annual Accounts of the State Government are prepared and examined under the directions

GOVERNMENT OF MADHYA PRADESH ACCOUNTANT GENERAL (ACCOUNTS AND ENTITLEMENTS) MADHYA PRADESH, GWALIOR 2 Preface The Annual Accounts of the State Government are prepared and examined under the directions

STATE FINANCES for the year ended 31 March 2015

Report of the Comptroller and Auditor General of India On STATE FINANCES for the year ended 31 March 2015 GOVERNMENT OF UTTAR PRADESH TABLE OF CONTENTS Preface Particulars Reference to Paragraph Page

Report of the Comptroller and Auditor General of India On STATE FINANCES for the year ended 31 March 2015 GOVERNMENT OF UTTAR PRADESH TABLE OF CONTENTS Preface Particulars Reference to Paragraph Page

(B) State Government Publications

State Government Publications") (B) State Government Publications 328.3657 JOINT PARLIAMENTARY COMMITTEES 1. Jammu and Kashmir. Legislative Assembly (12th). Committee on Environment 2017-2018 3rd Report. / Committee on Environment 2017-2018,

(B) State Government Publications 328.3657 JOINT PARLIAMENTARY COMMITTEES 1. Jammu and Kashmir. Legislative Assembly (12th). Committee on Environment 2017-2018 3rd Report. / Committee on Environment 2017-2018,

BUDGET: TABLE 1: BUDGET AT A GLANCE (Actuals) A. Revenue Receipts

A. Revenue Receipts") BUDGET: 2018-19 TABLE 1: BUDGET AT A GLANCE (Rs. in crore) Items 2016-17 (Actuals) (RE) 2018-19 A. Revenue Receipts 41978 58168 55307 64269 B. Revenue Expenditure 39812 48819 43882 51185 Revenue Surplus

BUDGET: 2018-19 TABLE 1: BUDGET AT A GLANCE (Rs. in crore) Items 2016-17 (Actuals) (RE) 2018-19 A. Revenue Receipts 41978 58168 55307 64269 B. Revenue Expenditure 39812 48819 43882 51185 Revenue Surplus

Analysis of State Budget Allocation of Goa, Manipur, Punjab, Uttar Pradesh and Uttarakhand

Analysis of State Budget Allocation of Goa, Manipur, Punjab, Uttar Pradesh and Uttarakhand Executive Summary The highest fiscal deficit among the 5 state is in Uttar Pradesh, amounting to an all-time high

Analysis of State Budget Allocation of Goa, Manipur, Punjab, Uttar Pradesh and Uttarakhand Executive Summary The highest fiscal deficit among the 5 state is in Uttar Pradesh, amounting to an all-time high

FINANCE ACCOUNTS VOLUME I. for the year GOVERNMENT OF TAMIL NADU

FINANCE ACCOUNTS VOLUME I for the year 201-1 GOVERNMENT OF TAMIL NADU Volume I Table of Content Subject Page No 1 2 3 4 5 6 7 8 9 10 11 12 13 Certificate of the Comptroller and Auditor General of India

FINANCE ACCOUNTS VOLUME I for the year 201-1 GOVERNMENT OF TAMIL NADU Volume I Table of Content Subject Page No 1 2 3 4 5 6 7 8 9 10 11 12 13 Certificate of the Comptroller and Auditor General of India

Budget Analysis Rajasthan Budget

Budget Analysis Rajasthan Budget 2012-13 13 Chief Minister Ashok Gehlot presented the General Budget 2012-13 to the State Assembly on 26 th of March, 2012. In his address, he commented on the fiscal performance

Budget Analysis Rajasthan Budget 2012-13 13 Chief Minister Ashok Gehlot presented the General Budget 2012-13 to the State Assembly on 26 th of March, 2012. In his address, he commented on the fiscal performance

Tata AIA Life- CSR Policy 1

Tata AIA Life- CSR Policy 1 Table of Contents I. Name... 3 II. Vision Statement... 3 III. Definitions... 3 IV. CSR Policy requirements as per the Companies Act, 2013 and notified Rules... 4 V. Tata Group

Tata AIA Life- CSR Policy 1 Table of Contents I. Name... 3 II. Vision Statement... 3 III. Definitions... 3 IV. CSR Policy requirements as per the Companies Act, 2013 and notified Rules... 4 V. Tata Group

CORPORATE SOCIAL RESPONSIBILITY POLICY (CSR POLICY)

") CORPORATE SOCIAL RESPONSIBILITY POLICY (CSR POLICY) Introduction APEPDCL, Visakhapatnam is i the leading Indian power utility spread across five districts in the southern state of Andhra Pradesh. It has

CORPORATE SOCIAL RESPONSIBILITY POLICY (CSR POLICY) Introduction APEPDCL, Visakhapatnam is i the leading Indian power utility spread across five districts in the southern state of Andhra Pradesh. It has

Legal Framework - - Services to/by Government

Legal Framework - - Services to/by Government S KHAITAN & ASSOCIATES SHUBHAM KHAITAN LEGAL FRAMEWORK - SERVICES TO/BY GOVERNMENT Relevant Definitions As per Section 2(53) of the CGST Act 2017, Government

Legal Framework - - Services to/by Government S KHAITAN & ASSOCIATES SHUBHAM KHAITAN LEGAL FRAMEWORK - SERVICES TO/BY GOVERNMENT Relevant Definitions As per Section 2(53) of the CGST Act 2017, Government

TAMILNADU STATE FINANCES

TAMILNADU STATE FINANCES Prof.K.R.Shanmugam 1 Dr.G.S.Ganesh Prasad 2 Dr. L. Venkatachalam 3 Report Submitted to The Fourteenth Finance Commission, New Delhi MADRAS INSTITUTE OF DEVELOPMENT STUDIES Chennai

TAMILNADU STATE FINANCES Prof.K.R.Shanmugam 1 Dr.G.S.Ganesh Prasad 2 Dr. L. Venkatachalam 3 Report Submitted to The Fourteenth Finance Commission, New Delhi MADRAS INSTITUTE OF DEVELOPMENT STUDIES Chennai

CONTENTS SL. NO. PARTICULARS PAGE NOS. 1 Preamble 3. 2 CSR Mission 3. 3 Objectives 3. 4 Focus Areas 4. 5 Approach to Implementation 5.

1 CONTENTS SL. NO. PARTICULARS PAGE NOS. 1 Preamble 3 2 CSR Mission 3 3 Objectives 3 4 Focus Areas 4 5 Approach to Implementation 5 6 CSR Funds 6 7 Guiding Principles for constitution of CSR Committee

1 CONTENTS SL. NO. PARTICULARS PAGE NOS. 1 Preamble 3 2 CSR Mission 3 3 Objectives 3 4 Focus Areas 4 5 Approach to Implementation 5 6 CSR Funds 6 7 Guiding Principles for constitution of CSR Committee

No.M.13048/23 (Sikkim)/2008/SP. Planning Commission (State Plans Division)

/2008/SP. Planning Commission (State Plans Division)") , ' No.M.13048/23 (Sikkim)/2008/SP. Planning Commission (State Plans Division) To The Chief Secretary, Government of Sikkim, Gangtok Yojana Bhawan, Sansad Marg, New Delhi 110001 Dated 24.8 2009 Subject:

, ' No.M.13048/23 (Sikkim)/2008/SP. Planning Commission (State Plans Division) To The Chief Secretary, Government of Sikkim, Gangtok Yojana Bhawan, Sansad Marg, New Delhi 110001 Dated 24.8 2009 Subject:

CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF KALYANI FORGE LIMITED

POLICY OF KALYANI FORGE LIMITED") CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF KALYANI FORGE LIMITED PHILOSOPY Kalyani Forge Limited has always respected contribution of the society in its growth story. We believe that business enterprises

CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF KALYANI FORGE LIMITED PHILOSOPY Kalyani Forge Limited has always respected contribution of the society in its growth story. We believe that business enterprises

` APPENDIX (Reference: Paragraph 1.1; Page 1)

") ` APPENDIX - 1.1 (Reference: Paragraph 1.1; Page 1) Part A: Structure and Form of Government Accounts Structure of Government Accounts: The accounts of the State Government are kept in three parts (i)

` APPENDIX - 1.1 (Reference: Paragraph 1.1; Page 1) Part A: Structure and Form of Government Accounts Structure of Government Accounts: The accounts of the State Government are kept in three parts (i)

Supplement to the Estimates. Fiscal Year Ending March 31, 2019

Supplement to the Estimates Fiscal Year Ending March 3, 209 Supplement to the Estimates Fiscal Year Ending March 3, 209 British Columbia Cataloguing in Publication Data British Columbia. Estimates, fiscal

Supplement to the Estimates Fiscal Year Ending March 3, 209 Supplement to the Estimates Fiscal Year Ending March 3, 209 British Columbia Cataloguing in Publication Data British Columbia. Estimates, fiscal

CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY

POLICY") THE SUPREME INDUSTRIES LIMITED Regd. Office :612, Raheja Chambers, Nariman Point, Mumbai 400021 Tel. : 022-22851656, Fax : 022-22851657, Email : sil_narimanpoint@supreme.co.in CIN : L35920MH1942PLC003554

THE SUPREME INDUSTRIES LIMITED Regd. Office :612, Raheja Chambers, Nariman Point, Mumbai 400021 Tel. : 022-22851656, Fax : 022-22851657, Email : sil_narimanpoint@supreme.co.in CIN : L35920MH1942PLC003554

FOR January, 2018

FOR 2018-19 January, 2018 MEDIUM TERM FISCAL POLICY STATEMENT & FISCAL POLICY STRATEGY STATEMENT FOR 2018 2019 Finance Department Government of West Bengal Foreword As per the statute of West Bengal Fiscal

FOR 2018-19 January, 2018 MEDIUM TERM FISCAL POLICY STATEMENT & FISCAL POLICY STRATEGY STATEMENT FOR 2018 2019 Finance Department Government of West Bengal Foreword As per the statute of West Bengal Fiscal

Gender Budgeting and women Empowerment Budget for women in Gujarat

Gender Budgeting and women Empowerment Budget for women in Gujarat A case study of Gujarat state budget by Mahender N. Jethmalani Patheya Budget Center Budgeting for Women s Essential Question: What does

Gender Budgeting and women Empowerment Budget for women in Gujarat A case study of Gujarat state budget by Mahender N. Jethmalani Patheya Budget Center Budgeting for Women s Essential Question: What does

Corporate Social Responsibility and Its Disclosure: An Analysis of Present Legal Provisions in India

7 Corporate Social Responsibility and Its Disclosure: An Analysis of Present Legal Provisions in India Debansu Das, Associate Professor, Department of Commerce, University of Kalyani, West Bengal, India

7 Corporate Social Responsibility and Its Disclosure: An Analysis of Present Legal Provisions in India Debansu Das, Associate Professor, Department of Commerce, University of Kalyani, West Bengal, India

Telangana Budget Analysis

The Finance Minister of Telangana, Mr. Eatala Rajender, presented the Budget for Telangana for financial year on March 14, 2016. Budget Highlights The Gross State Domestic Product of Telangana for is estimated

The Finance Minister of Telangana, Mr. Eatala Rajender, presented the Budget for Telangana for financial year on March 14, 2016. Budget Highlights The Gross State Domestic Product of Telangana for is estimated

Kerala Budget Analysis

2.1% 4.3% 2.9% 5.2% 5.7% 4. 7.2% 6.7% 4.3% 6.6% 7.4% Kerala Budget Analysis The Finance Minister of Kerala, Dr. T.M. Thomas Isaac, presented the Budget for financial year on February 2, 2018. Budget Highlights

2.1% 4.3% 2.9% 5.2% 5.7% 4. 7.2% 6.7% 4.3% 6.6% 7.4% Kerala Budget Analysis The Finance Minister of Kerala, Dr. T.M. Thomas Isaac, presented the Budget for financial year on February 2, 2018. Budget Highlights

Mirae Asset Global Investments (India) Pvt. Ltd. Corporate Social Responsibility (CSR) Policy

Pvt. Ltd. Corporate Social Responsibility (CSR) Policy") Mirae Asset Global Investments (India) Pvt. Ltd. Corporate Social Responsibility (CSR) Policy 1 CONTENTS I. Introduction 3 II. Background. 3 III. Our Objectives... 4 IV. Activities enumerated in Schedule

Mirae Asset Global Investments (India) Pvt. Ltd. Corporate Social Responsibility (CSR) Policy 1 CONTENTS I. Introduction 3 II. Background. 3 III. Our Objectives... 4 IV. Activities enumerated in Schedule

CSR (CORPORATE SOCIAL RESPONSIBILITY)

") CSR (CORPORATE SOCIAL RESPONSIBILITY) Policy of Spicer India Private Limited 1. INTRODUCTION 1.1 In pursuant to section 135 of the Companies Act, 2013 (the act) and the Companies (Corporate Social Responsibility

CSR (CORPORATE SOCIAL RESPONSIBILITY) Policy of Spicer India Private Limited 1. INTRODUCTION 1.1 In pursuant to section 135 of the Companies Act, 2013 (the act) and the Companies (Corporate Social Responsibility

ORDER. Subject: Constitution of a Committee for revision of the List of Major and Minor Heads of Accounts.

73 Annexure A No. T- 14018/1/2009-Codes/178-187 Government of India Ministry of Finance Department of Expenditure Controller General of Accounts Lok Nayak Bhawan, Khan Market New Delhi ORDER Subject: Constitution

73 Annexure A No. T- 14018/1/2009-Codes/178-187 Government of India Ministry of Finance Department of Expenditure Controller General of Accounts Lok Nayak Bhawan, Khan Market New Delhi ORDER Subject: Constitution

PNC INFRATECH LIMITED PNC CSR POLICY

PNC INFRATECH LIMITED PNC CSR POLICY 1 TABLE OF CONTENTS CHAPTER I CSR OVERVIEW AND ITS CONTEXT CHAPTER- II CSR FRAME WORK CHAPTER- III FUNDING FOR CSR ACTIVITIES CHAPTER- IV OPERATIONAL FRAMEWORK CHAPTER-

PNC INFRATECH LIMITED PNC CSR POLICY 1 TABLE OF CONTENTS CHAPTER I CSR OVERVIEW AND ITS CONTEXT CHAPTER- II CSR FRAME WORK CHAPTER- III FUNDING FOR CSR ACTIVITIES CHAPTER- IV OPERATIONAL FRAMEWORK CHAPTER-

POLICY FOR CORPORATE SOCIAL RESPONSIBILITY

POLICY FOR CORPORATE SOCIAL RESPONSIBILITY I. SHORT TITLE: This policy in relation to the Corporate Social Responsibility ( CSR ) of Morgan Stanley Advantage Services Private Limited is titled as the CSR

POLICY FOR CORPORATE SOCIAL RESPONSIBILITY I. SHORT TITLE: This policy in relation to the Corporate Social Responsibility ( CSR ) of Morgan Stanley Advantage Services Private Limited is titled as the CSR

(CORPORATE SOCIAL RESPONSIBIITY)

") MODEL CSR (CORPORATE SOCIAL RESPONSIBIITY) POLICY OF Haldex India Pvt.Ltd. 1. INTRODUCTION 1.1 In pursuant to section 135 of the Companies Act, 2013 (the act) and the Companies (Corporate Social Responsibility

MODEL CSR (CORPORATE SOCIAL RESPONSIBIITY) POLICY OF Haldex India Pvt.Ltd. 1. INTRODUCTION 1.1 In pursuant to section 135 of the Companies Act, 2013 (the act) and the Companies (Corporate Social Responsibility

UTI INFRASTRUCTURE AND TECHNOLOGY SERVICES LIMITED CIN: U65991MH1993GOI072051

UTI INFRASTRUCTURE AND TECHNOLOGY SERVICES LIMITED CIN: U65991MH1993GOI072051 Registered Office: Plot No. 3, Sector II, CBD Belapur, Navi Mumbai 400 614 CORPORATE SOCIAL RESPONSIBILITY POLICY WITH EFFECT

UTI INFRASTRUCTURE AND TECHNOLOGY SERVICES LIMITED CIN: U65991MH1993GOI072051 Registered Office: Plot No. 3, Sector II, CBD Belapur, Navi Mumbai 400 614 CORPORATE SOCIAL RESPONSIBILITY POLICY WITH EFFECT

SONATA FINANCE PVT LTD.- CSR POLICY. (As approved in CSR Committee meeting dated../../...) Page 1 of 8

Page 1 of 8") - SONATA FINANCE PVT LTD.- CSR POLICY (As approved in CSR Committee meeting dated../../...) Page 1 of 8 ' Contents 1.0 Introduction... 3 2.0 Preamble...... 3 3.0 Governance... 3-4 3.1 CSR Committee 3.2

- SONATA FINANCE PVT LTD.- CSR POLICY (As approved in CSR Committee meeting dated../../...) Page 1 of 8 ' Contents 1.0 Introduction... 3 2.0 Preamble...... 3 3.0 Governance... 3-4 3.1 CSR Committee 3.2

EXPENDITURE UNDER REVENUE ACCOUNT

EXPENDITURE UNDER REVENUE ACCOUNT The statement belows gives a summary of the estimate of expenditure met from revenue by broad categories.further details by heads of account regarding Actuals of 2015-2016,

EXPENDITURE UNDER REVENUE ACCOUNT The statement belows gives a summary of the estimate of expenditure met from revenue by broad categories.further details by heads of account regarding Actuals of 2015-2016,

CSR Policy of Delta Corp Limited. 1. Corporate Social Responsibility (CSR) Policy of Delta Corp Limited ( Company )

Policy of Delta Corp Limited ( Company )") CSR Policy of Delta Corp Limited 1. Corporate Social Responsibility (CSR) Policy of Delta Corp Limited ( Company ) Corporate Social Responsibility is strongly connected with the principles of Sustainability;

CSR Policy of Delta Corp Limited 1. Corporate Social Responsibility (CSR) Policy of Delta Corp Limited ( Company ) Corporate Social Responsibility is strongly connected with the principles of Sustainability;

Performance of MGNREGA in Andhra Pradesh

International Journal of Humanities and Social Science Invention ISSN (Online): 2319 7722, ISSN (Print): 2319 7714 Volume 4 Issue 4 April. 2015 PP.22-27 Performance of MGNREGA in Andhra Pradesh Dr.K.Padma

International Journal of Humanities and Social Science Invention ISSN (Online): 2319 7722, ISSN (Print): 2319 7714 Volume 4 Issue 4 April. 2015 PP.22-27 Performance of MGNREGA in Andhra Pradesh Dr.K.Padma

ACCOUNTS AT A GLANCE GOVERNMENT OF MADHYA PRADESH

ACCOUNTS AT A GLANCE 2016-2017 GOVERNMENT OF MADHYA PRADESH i ii PREFACE This is the Nineteenth issue of our annual publication "Accounts at a Glance". The Annual Accounts of the State Government are prepared

ACCOUNTS AT A GLANCE 2016-2017 GOVERNMENT OF MADHYA PRADESH i ii PREFACE This is the Nineteenth issue of our annual publication "Accounts at a Glance". The Annual Accounts of the State Government are prepared

GOVERNMENT OF MADHYA PRADESH

GOVERNMENT OF MADHYA PRADESH ACCOUNTANT GENERAL (ACCOUNTS AND ENTITLEMENTS) MADHYA PRADESH, GWALIOR 2 Preface The Annual Accounts of the State Government are prepared and examined under the directions

GOVERNMENT OF MADHYA PRADESH ACCOUNTANT GENERAL (ACCOUNTS AND ENTITLEMENTS) MADHYA PRADESH, GWALIOR 2 Preface The Annual Accounts of the State Government are prepared and examined under the directions

ENERGY LIMITED (CIN: U29224GJ1987PLC010044)

") CORPORATE SOCIAL RESPONSIBILITY POLICY ( CSR Policy ) We at John Energy Limited ( JEL or Company ) are well aware of its Corporate Social Responsibility and constantly making efforts to contribute in this

CORPORATE SOCIAL RESPONSIBILITY POLICY ( CSR Policy ) We at John Energy Limited ( JEL or Company ) are well aware of its Corporate Social Responsibility and constantly making efforts to contribute in this

Balanced Regional Development in India Issues and Policies

Balanced Regional Development in India Issues and Policies Incorporating An Introduction to Balanced Regional Development in India Plan-wise Documentation of Policies and Programmes for Balanced Regional

Balanced Regional Development in India Issues and Policies Incorporating An Introduction to Balanced Regional Development in India Plan-wise Documentation of Policies and Programmes for Balanced Regional

FINANCING EDUCATION IN UTTAR PRADESH

FINANCING EDUCATION IN UTTAR PRADESH 1. The system of education finance in India is complicated both because of general issues of fiscal federalism and the specific procedures and terminology used in the

FINANCING EDUCATION IN UTTAR PRADESH 1. The system of education finance in India is complicated both because of general issues of fiscal federalism and the specific procedures and terminology used in the

Madura Micro Finance Limited. Corporate Social Responsibility Policy 2015

Madura Micro Finance Limited (CIN: U65929TN2005PLC057390) Corporate Social Responsibility Policy 2015 Brief Background In terms of Section 135 of Companies Act, 2013, effective 1 st April 2014, every Company

Madura Micro Finance Limited (CIN: U65929TN2005PLC057390) Corporate Social Responsibility Policy 2015 Brief Background In terms of Section 135 of Companies Act, 2013, effective 1 st April 2014, every Company

ctv,d n`f"v esa Budget at a Glance

1 ctv,d n`f"v esa Budget at a Glance ¼ ` djksm+ksa esa½ (` in crore) 2013-14 2014-15 2014-15 2015-16 oklrfod ctv la'kksf/kr ctv vuqeku vuqeku vuqeku Actuals Budget Revised Budget Estimates Estimates Estimates

1 ctv,d n`f"v esa Budget at a Glance ¼ ` djksm+ksa esa½ (` in crore) 2013-14 2014-15 2014-15 2015-16 oklrfod ctv la'kksf/kr ctv vuqeku vuqeku vuqeku Actuals Budget Revised Budget Estimates Estimates Estimates

QUANTUM ASSET MANAGEMENT COMPANY PRIVATE LIMITED

1 QUANTUM ASSET MANAGEMENT COMPANY PRIVATE LIMITED 2 I. CONCEPT AND VISION The Company intends to make a positive difference to society and contribute its share towards the social cause of betterment of

1 QUANTUM ASSET MANAGEMENT COMPANY PRIVATE LIMITED 2 I. CONCEPT AND VISION The Company intends to make a positive difference to society and contribute its share towards the social cause of betterment of

GOVERNMENT OF MIZORAM

GOVERNMENT OF MIZORAM EXPLANATORY MEMORANDUM ON THE BUDGET 2012-2013 (As laid before the Legislative Assembly on 16 th July, 2012) Sl. Page Contents No. No. 1 2 3 1. Explanatory. 1-3 2. Budget Summary.

GOVERNMENT OF MIZORAM EXPLANATORY MEMORANDUM ON THE BUDGET 2012-2013 (As laid before the Legislative Assembly on 16 th July, 2012) Sl. Page Contents No. No. 1 2 3 1. Explanatory. 1-3 2. Budget Summary.

Delhi Development Report

Delhi Development Report PLANNING COMMISSION GOVERNMENT OF INDIA NEW DELHI Published by ACADEMIC FOUNDATION NEW DELHI '&.' " ': Contents o The Core Committee, including Partner Agencies and Project Team

Delhi Development Report PLANNING COMMISSION GOVERNMENT OF INDIA NEW DELHI Published by ACADEMIC FOUNDATION NEW DELHI '&.' " ': Contents o The Core Committee, including Partner Agencies and Project Team

FAMY CARE LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY

FAMY CARE LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1 1. Introduction The Companies Act 2013 (hereinafter referred to as the Act ), has introduced the idea of CSR. It mandates qualifying companies

FAMY CARE LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1 1. Introduction The Companies Act 2013 (hereinafter referred to as the Act ), has introduced the idea of CSR. It mandates qualifying companies

GOVERNMENT OF TRIPURA

GOVERNMENT OF TRIPURA ACCOUNTS AT A GLANCE SENIOR DEPUTY ACCOUNTANT GENERAL (ACCOUNTS AND ENTITLEMENT) TRIPURA, AGARTALA GOVERNMENT OF TRIPURA ACCOUNTS AT A GLANCE SENIOR DEPUTY ACCOUNTANT GENERAL (ACCOUNTS

GOVERNMENT OF TRIPURA ACCOUNTS AT A GLANCE SENIOR DEPUTY ACCOUNTANT GENERAL (ACCOUNTS AND ENTITLEMENT) TRIPURA, AGARTALA GOVERNMENT OF TRIPURA ACCOUNTS AT A GLANCE SENIOR DEPUTY ACCOUNTANT GENERAL (ACCOUNTS

Government of Bihar. Particulars

Government of Bihar Main Features-Budget 2012-13 Rs. in Cr 2009-10 2010-11 2011-12 2012-13 % 2012-13 Increase Rece./Exp. over Actuals Actuals B.E. B.E. % of Rev/ 2011-12 Cap (B.E.) 1 2 3 4 5 6 7 Particulars

Government of Bihar Main Features-Budget 2012-13 Rs. in Cr 2009-10 2010-11 2011-12 2012-13 % 2012-13 Increase Rece./Exp. over Actuals Actuals B.E. B.E. % of Rev/ 2011-12 Cap (B.E.) 1 2 3 4 5 6 7 Particulars

Corporate Social Responsibility Policy. CORDS CABLE INDUSTRIES LIMITED (Approved by Board of Director s in their meeting held on April 01, 2015)

") Corporate Social Responsibility Policy CORDS CABLE INDUSTRIES LIMITED (Approved by Board of Director s in their meeting held on April 01, 2015) Contents 1. Concept 2. CSR in India 3. Policy Objective 4.

Corporate Social Responsibility Policy CORDS CABLE INDUSTRIES LIMITED (Approved by Board of Director s in their meeting held on April 01, 2015) Contents 1. Concept 2. CSR in India 3. Policy Objective 4.

BLOSSOM INDUSTRIES LIMITED

BLOSSOM INDUSTRIES LIMITED CIN: U31200DD1989PLC003122 Address: Village Jani Vankad,Nani Daman 396 210 (U.T.) Daman And Diu Blossom Industries Limited (CIN U31200DD1989PLC003122) CORPORATE SOCIAL RESPONSIBILITY

BLOSSOM INDUSTRIES LIMITED CIN: U31200DD1989PLC003122 Address: Village Jani Vankad,Nani Daman 396 210 (U.T.) Daman And Diu Blossom Industries Limited (CIN U31200DD1989PLC003122) CORPORATE SOCIAL RESPONSIBILITY

STAR UNION DAI-ICHI LIFE INSURANCE COMPANY LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY

STAR UNION DAI-ICHI LIFE INSURANCE COMPANY LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1 Document Control Document version This Corporate Social Responsibility Policy document is version 1.5. Revision

STAR UNION DAI-ICHI LIFE INSURANCE COMPANY LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1 Document Control Document version This Corporate Social Responsibility Policy document is version 1.5. Revision

CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY BHUSHAN STEEL LIMITED

POLICY BHUSHAN STEEL LIMITED") CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF BHUSHAN STEEL LIMITED * CORPORATE SOCIAL RESPONSIBILITY POLICY (CSR) POLICY With the advent of the Companies Act, 2013 constitution of a Corporate Social

CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF BHUSHAN STEEL LIMITED * CORPORATE SOCIAL RESPONSIBILITY POLICY (CSR) POLICY With the advent of the Companies Act, 2013 constitution of a Corporate Social

Corporate Social Responsibility (CSR) Policy

Policy") KENNAMETAL INDIA LIMITED Corporate Social Responsibility (CSR) Policy (w.e.f. August 21,2015) 1 C O N T E N T S 1. Context 1.1. In the light of Companies Act, 2013 1.2. Objectives of the Policy 1.3. Definitions

KENNAMETAL INDIA LIMITED Corporate Social Responsibility (CSR) Policy (w.e.f. August 21,2015) 1 C O N T E N T S 1. Context 1.1. In the light of Companies Act, 2013 1.2. Objectives of the Policy 1.3. Definitions

HIL Limited. Corporate Social Responsibility Policy

HIL Limited Corporate Social Responsibility Policy 1. INTRODUCTION Corporate Social Responsibility ( CSR ) at HIL Limited ( Company or HIL ) portrays the deep symbiotic relationship that the Company enjoys

HIL Limited Corporate Social Responsibility Policy 1. INTRODUCTION Corporate Social Responsibility ( CSR ) at HIL Limited ( Company or HIL ) portrays the deep symbiotic relationship that the Company enjoys

HIGHLIGHTS OF KARNATAKA S BUDGET

HIGHLIGHTS OF KARNATAKA S BUDGET 2008-09 OVERVIEW OF THE BUDGET! The Budget of Government of Karnataka for 2008-09 with an outlay of Rs.56542.15 crores from the State Consolidated fund has been presented

HIGHLIGHTS OF KARNATAKA S BUDGET 2008-09 OVERVIEW OF THE BUDGET! The Budget of Government of Karnataka for 2008-09 with an outlay of Rs.56542.15 crores from the State Consolidated fund has been presented

CORPORATE SOCIAL RESPONSIBILITY CHARTER

CORPORATE SOCIAL RESPONSIBILITY CHARTER 1.0 Preamble : Heubach Colour Private Limited ( the Company ) is a Private Limited Company incorporated under the Companies Act,1956. (i) Objective : The Company

CORPORATE SOCIAL RESPONSIBILITY CHARTER 1.0 Preamble : Heubach Colour Private Limited ( the Company ) is a Private Limited Company incorporated under the Companies Act,1956. (i) Objective : The Company

IFCI Factors Limited Corporate Social Responsibility Policy

IFCI Factors Limited Corporate Social Responsibility Policy Page 1 of 11 Contents Page 2 of 11 1. INTRODUCTION The concept of Corporate Social Responsibility (CSR) has gained prominence from all avenues.

IFCI Factors Limited Corporate Social Responsibility Policy Page 1 of 11 Contents Page 2 of 11 1. INTRODUCTION The concept of Corporate Social Responsibility (CSR) has gained prominence from all avenues.

CORPORATE SOCIAL RESPONSIBILITY POLICY

T. V. Today Network Limited Registered Office: F-26, First Floor, Connaught Circus, New Delhi 110001, CIN No. L92200DL1999PLC103001, Telephone Number: 0120-4807100, Fax Number: 0120-4325028 Website: www.aajtak.intoday.in,

T. V. Today Network Limited Registered Office: F-26, First Floor, Connaught Circus, New Delhi 110001, CIN No. L92200DL1999PLC103001, Telephone Number: 0120-4807100, Fax Number: 0120-4325028 Website: www.aajtak.intoday.in,

Corporate Social Responsibility (CSR) Policy

Policy") Corporate Social Responsibility (CSR) Policy INTRODUCTION & BACKGROUND Corporate Social Responsibility is not a new concept in India, however, the Ministry of Corporate Affairs, Government of India has

Corporate Social Responsibility (CSR) Policy INTRODUCTION & BACKGROUND Corporate Social Responsibility is not a new concept in India, however, the Ministry of Corporate Affairs, Government of India has

Companies Act, 2013 Tracker II. CNK & Associates

Companies Act, 2013 Tracker II CNK & Associates Corporate Social Responsibility (CSR) Provisions As per Companies Act, 2013, CSR has become mandatory in India. The Ministry of Corporate Affairs (MCA) in

Companies Act, 2013 Tracker II CNK & Associates Corporate Social Responsibility (CSR) Provisions As per Companies Act, 2013, CSR has become mandatory in India. The Ministry of Corporate Affairs (MCA) in

Corporate Social Responsibility Policy

Corporate Social Responsibility Policy Approval Date: 1 May, 2018 Corporate Social Responsibility Policy Cerner Healthcare Solutions India Private Limited Table of Contents 1. Introduction 2. Objective

Corporate Social Responsibility Policy Approval Date: 1 May, 2018 Corporate Social Responsibility Policy Cerner Healthcare Solutions India Private Limited Table of Contents 1. Introduction 2. Objective

POLICY FOR CORPORATE SOCIAL RESPONSIBILITY

I. SHORT TITLE POLICY FOR CORPORATE SOCIAL RESPONSIBILITY This policy in relation to the Corporate Social Responsibility ( CSR ) of BPTP Limited is titled as the CSR Policy and shall include any alterations,

I. SHORT TITLE POLICY FOR CORPORATE SOCIAL RESPONSIBILITY This policy in relation to the Corporate Social Responsibility ( CSR ) of BPTP Limited is titled as the CSR Policy and shall include any alterations,

West Bengal Budget Analysis

0.3% 3. 2.3% 6.4% 5.9% 8.8% 8. 8. 11.4% 10.2% 11. 15. West Bengal Budget Analysis The Finance Minister of West Bengal, Dr. Amit Mitra presented the Budget for financial year on January 31, 2018. Budget

0.3% 3. 2.3% 6.4% 5.9% 8.8% 8. 8. 11.4% 10.2% 11. 15. West Bengal Budget Analysis The Finance Minister of West Bengal, Dr. Amit Mitra presented the Budget for financial year on January 31, 2018. Budget

TCG Lifesciences Private Limited - Corporate Social Responsibility (CSR) Policy

Policy") TCG Lifesciences Private Limited - Corporate Social Responsibility (CSR) Policy 1. Concept Corporate Social Responsibility is strongly connected with the principles of Sustainability; an organization should

TCG Lifesciences Private Limited - Corporate Social Responsibility (CSR) Policy 1. Concept Corporate Social Responsibility is strongly connected with the principles of Sustainability; an organization should

Budget Analysis for Child Protection

Budget Analysis for Child Protection Children under the age of 18 constitute 42 percent of India's population. They represent not just India's future, but are integral to securing India's present. Yet

Budget Analysis for Child Protection Children under the age of 18 constitute 42 percent of India's population. They represent not just India's future, but are integral to securing India's present. Yet

H.B. 12, 2018.] Appropriation (2019)

![H.B. 12, 2018.] Appropriation (2019)](/thumbs/94/119392137.jpg "H.B. 12, 2018.] Appropriation (2019)") H.B. 12, 2018.] I II Presented by the Minister of Finance and Economic Development BILL To apply a sum of money for the service of Zimbabwe during the year ending on the 31st December, 2019. 5 ENACTED

H.B. 12, 2018.] I II Presented by the Minister of Finance and Economic Development BILL To apply a sum of money for the service of Zimbabwe during the year ending on the 31st December, 2019. 5 ENACTED

CHAPTER III CONCEPTUAL FRAME WORK

CHAPTER III CONCEPTUAL FRAME WORK This chapter is intended primarily to provide a conceptual frame work of the study. Moreover, the important terms and concepts used in the thesis have also been explained

CHAPTER III CONCEPTUAL FRAME WORK This chapter is intended primarily to provide a conceptual frame work of the study. Moreover, the important terms and concepts used in the thesis have also been explained

CORPORATE SOCIAL RESPONSIBILITY & SUSTAINABILITY POLICY

CORPORATE SOCIAL RESPONSIBILITY & SUSTAINABILITY POLICY (w.e.f. 01.04.2014) MMTC Limited - Corporate Social Responsibility & Sustainability Policy 1. Short Title and Applicability This Policy shall be

CORPORATE SOCIAL RESPONSIBILITY & SUSTAINABILITY POLICY (w.e.f. 01.04.2014) MMTC Limited - Corporate Social Responsibility & Sustainability Policy 1. Short Title and Applicability This Policy shall be

INOX LEISURE LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY

INOX LEISURE LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1. SHORT TITLE AND APPLICABILITY 1.1 This policy, which encompasses the philosophy of Inox Leisure Limited ( Company ) for delineating its responsibility

INOX LEISURE LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1. SHORT TITLE AND APPLICABILITY 1.1 This policy, which encompasses the philosophy of Inox Leisure Limited ( Company ) for delineating its responsibility

CSR Policy. Corporate Social Responsibility Policy (CSR) of Tamilnad Mercantile Bank Limited

of Tamilnad Mercantile Bank Limited") CSR Policy Corporate Social Responsibility Policy (CSR) of Tamilnad Mercantile Bank Limited Preamble CSR is an institutionalised effort to contribute to social well being. It covers all activities through

CSR Policy Corporate Social Responsibility Policy (CSR) of Tamilnad Mercantile Bank Limited Preamble CSR is an institutionalised effort to contribute to social well being. It covers all activities through

Corporate Social Responsibility Policy

Corporate Social Responsibility Policy Corporate Social Responsibility Policy 1. Background : This document outlines the vision of Eros International Media Limited ( the Company / Eros ), India towards

Corporate Social Responsibility Policy Corporate Social Responsibility Policy 1. Background : This document outlines the vision of Eros International Media Limited ( the Company / Eros ), India towards

ADAMAWA STATE GOVERNMENT DRAFT STATEMENT OF ASSETS AND LIABILITIES Actual (JAN NOV)

") ADAMAWA STATE GOVERNMENT DRAFT STATEMENT OF ASSETS AND LIABILITIES 2015 2014 (JAN NOV) Liquid Assets =N= =N= Treasuries and Banks 18,997,723,903.29 513,515,423.64 Total 18,997,723,903.29 513,515,423.64

ADAMAWA STATE GOVERNMENT DRAFT STATEMENT OF ASSETS AND LIABILITIES 2015 2014 (JAN NOV) Liquid Assets =N= =N= Treasuries and Banks 18,997,723,903.29 513,515,423.64 Total 18,997,723,903.29 513,515,423.64

L&T METRO RAIL (HYDERABAD) LIMITED

LIMITED") L&T METRO RAIL (HYDERABAD) LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1 CORPORATE SOCIAL RESPONBILITY POLICY OF L&T METRO RAIL (HYDERABAD) LIMITED PREAMBLE: The concept of Corporate Social Responsibility

L&T METRO RAIL (HYDERABAD) LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1 CORPORATE SOCIAL RESPONBILITY POLICY OF L&T METRO RAIL (HYDERABAD) LIMITED PREAMBLE: The concept of Corporate Social Responsibility

CORPORATE SOCIAL REPONSIBILITY POLICY M/S. BEEKAYLON SYNTHETICS PRIVATE LIMITED

CORPORATE SOCIAL REPONSIBILITY POLICY OF M/S. BEEKAYLON SYNTHETICS PRIVATE LIMITED CONTENTS Sr. No Particulars Page No. 1 Preamble 3 2 Definitions 3 3 Policy Objectives 4 4 CSR Committee 4 5 Execution

CORPORATE SOCIAL REPONSIBILITY POLICY OF M/S. BEEKAYLON SYNTHETICS PRIVATE LIMITED CONTENTS Sr. No Particulars Page No. 1 Preamble 3 2 Definitions 3 3 Policy Objectives 4 4 CSR Committee 4 5 Execution

CORPORATE SOCIAL RESPONSIBILITY POLICY

CORPORATE SOCIAL RESPONSIBILITY POLICY 1. INTRODUCTION: The Board of Directors (the Board ) of Goldiam International Limited (the Company ) has adopted the following policy and procedures with regard to

CORPORATE SOCIAL RESPONSIBILITY POLICY 1. INTRODUCTION: The Board of Directors (the Board ) of Goldiam International Limited (the Company ) has adopted the following policy and procedures with regard to

NATIONAL ACCOUNTS STATISTICS FACTOR INCOMES (BASE YEAR )

") NATIONAL ACCOUNTS STATISTICS FACTOR INCOMES (BASE YEAR 1999-2000) 1980-81 1999-2000 2008 CENTRAL STATISTICAL ORGANISATION DEPARTMENT OF STATISTICS MINISTRY OF STATISTICS AND PROGRAMME IMPLEMENTATION GOVERNMENT

NATIONAL ACCOUNTS STATISTICS FACTOR INCOMES (BASE YEAR 1999-2000) 1980-81 1999-2000 2008 CENTRAL STATISTICAL ORGANISATION DEPARTMENT OF STATISTICS MINISTRY OF STATISTICS AND PROGRAMME IMPLEMENTATION GOVERNMENT

Annual Plan Planning Commission.

Annual Plan 2013 14 Planning Commission http://planningcommission.nic.in Contents Introduction... 2 Annual Plan 2013-14... 3 Budgetary Allocation: An Overview... 5 Central Plan Outlay... 6 Central Plan

Annual Plan 2013 14 Planning Commission http://planningcommission.nic.in Contents Introduction... 2 Annual Plan 2013-14... 3 Budgetary Allocation: An Overview... 5 Central Plan Outlay... 6 Central Plan

JBM AUTO LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY

POLICY") I. PREAMBLE JBM AUTO LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY The Policy outlines the Company s responsibility as a corporate citizen and lays down the guidelines and mechanism for undertaking

I. PREAMBLE JBM AUTO LIMITED CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY The Policy outlines the Company s responsibility as a corporate citizen and lays down the guidelines and mechanism for undertaking

BLUE DART AVIATION LIMITED Corporate Social Responsibility (CSR) Policy

Policy") BLUE DART AVIATION LIMITED Corporate Social Responsibility (CSR) Policy 1 TABLE OF CONTENTS I. Concept and Objectives... 3 II. CSR Budget... 3 III. CSR Activities... 4 IV. CSR Committee.... 5 V. CSR Governance

BLUE DART AVIATION LIMITED Corporate Social Responsibility (CSR) Policy 1 TABLE OF CONTENTS I. Concept and Objectives... 3 II. CSR Budget... 3 III. CSR Activities... 4 IV. CSR Committee.... 5 V. CSR Governance

CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF ASSAM POWER GENERATION CORPORATION LIMITED (APPROVED BY BOARD OF DIRECTORS)

POLICY OF ASSAM POWER GENERATION CORPORATION LIMITED (APPROVED BY BOARD OF DIRECTORS)") 1. PREAMBLE: CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF ASSAM POWER GENERATION CORPORATION LIMITED (APPROVED BY BOARD OF DIRECTORS) The concept of Corporate Social Responsibility has gained prominence

1. PREAMBLE: CORPORATE SOCIAL RESPONSIBILITY (CSR) POLICY OF ASSAM POWER GENERATION CORPORATION LIMITED (APPROVED BY BOARD OF DIRECTORS) The concept of Corporate Social Responsibility has gained prominence

WONDERLA HOLIDAYS LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY

WONDERLA HOLIDAYS LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1.0 Objective At Wonderla Holidays Ltd., (hereinafter described as the Company ) corporate social responsibility (CSR) has been the cornerstone

WONDERLA HOLIDAYS LIMITED CORPORATE SOCIAL RESPONSIBILITY POLICY 1.0 Objective At Wonderla Holidays Ltd., (hereinafter described as the Company ) corporate social responsibility (CSR) has been the cornerstone

Scholars Journal of Economics, Business and Management e-issn

Scholars Journal of Economics, Business and Management e-issn 2348-5302 Narwade SS et al.; Sch J Econ Bus Manag, 2014; 1(2):40-49 p-issn 2348-8875 SAS Publishers (Scholars Academic and Scientific Publishers)

Scholars Journal of Economics, Business and Management e-issn 2348-5302 Narwade SS et al.; Sch J Econ Bus Manag, 2014; 1(2):40-49 p-issn 2348-8875 SAS Publishers (Scholars Academic and Scientific Publishers)

Telangana Budget Analysis

-5.8% -4.9% -2.9% 3.6% 6.8% 6. 6.1% 12.9% 6.2% 11. 8.6% 12.2% 10.2% 10.1% 11.1% 10.4% Budget Analysis The Finance Minister of, Mr. Eatala Rajender, presented the Budget for financial year on March 15,

-5.8% -4.9% -2.9% 3.6% 6.8% 6. 6.1% 12.9% 6.2% 11. 8.6% 12.2% 10.2% 10.1% 11.1% 10.4% Budget Analysis The Finance Minister of, Mr. Eatala Rajender, presented the Budget for financial year on March 15,

NeoGrowth Credit Private Limited Corporate Social Responsibility Policy August 2018

NeoGrowth Credit Private Limited Corporate Social Responsibility Policy August 2018 Created Document Owner Secretarial & Legal Department The provisions of Section 135 of the Companies Act, 2013 ( the

NeoGrowth Credit Private Limited Corporate Social Responsibility Policy August 2018 Created Document Owner Secretarial & Legal Department The provisions of Section 135 of the Companies Act, 2013 ( the