Budget Planning Council Meeting Agenda September 20, :00am 1:00 pm Baker Center ~ Room 230

|

|

|

- Abel Garrison

- 5 years ago

- Views:

Transcription

1 Budget Planning Council Meeting Agenda September 20, :00am 1:00 pm Baker Center ~ Room 230 Meeting Objectives Provide members with an overview of the following: o FY20 Budget Timeline o OHIO Budget Model Review and discuss a Graduate Program Fee Request 1. FY20 Budget Timeline 2. OHIO Budget Model (PPT Presentation) 3. Graduate Program Fee Request John Day 4. Next Meeting: October 4, 2018 ~ Baker Center, Room 230 Topics: Fall Enrollment Update & Vote on Graduate Program Fee Request

2 FY2020 Preliminary Budget Timeline 1

3 1 FY19 Budget Planning Council OHIO Budget Model September 20, 2018

4 2 Agenda OHIO Budget Model Historical Budget Model OBM Revenue Model: Allocations SSI Undergraduate Tuition Student Financial Aid Contribution Margin Capital Cost Allocation Model (CCAM)

5 3 OHIO Budget Model FY20 Transition Between FY14 and FY19 Ohio University utilized the Responsibility Center Management (RCM) budget methodology for adopted under the following principles: Ensure the sustained strength of the University by aligning resources with University priorities to support academic excellence Support strong academic governance that promotes collaboration across units and builds on the strengths of the University Present a holistic view of the University Budget that provides a clear connection between performance and incentives Empower unit-level decision making authority to promote academic excellence and institutional efficiency that is balanced by responsibility and accountability Create a simple and transparent budget process driven by the goals of financial predictability and stability Effective FY20, University Leadership have replaced the RCM model with the OHIO Budget Model (OBM). The new model will: Preserve the academic colleges decision-making authority to budget according to their specific plans Leverage the tools and business intelligence gained with the implementation of RCM Simplify how central costs are collected by the University s revenue centers

6 4 Historical Budget Model - RCM College Subvention Pool 12.5% Tax Distribution RCM Revenues SSI UG Tuition Student Financial Aid Allocated Responsibility Centers Direct Revenues Graduate Tuition Grants & Contracts F&A Gifts Endowment Distributions Investment Other External Sales Responsibility Centers Colleges Arts & Sciences Business Communication Education Engineering Fine Arts Health Sciences Honors OGAIS University College Voinovich HCOM RHE Allocated RCM Expenses Administrative Costs Allocations (ACM) Capital Cost Allocations (CCAM) Direct Expenses Salaries, Wages & Other Payroll Benefits Supplies & Service Capitalized Costs Auxiliaries* Athletics Culinary Services Housing & Resident Life Pringin Parking & Transportation

7 5 OHIO Budget Model - OBM UG Revenue Model SSI UG Tuition Student Financial Aid Allocated Capital Costs Capital Cost Allocations (CCAM) Allocated Revenue Centers Negotiated Direct Revenues Graduate Tuition Grants & Contracts F&A Gifts Endowment Distributions Investment Other External Sales OBM Contribution Margin Operating margin that supports administrative planning units (control total units) Direct Expenses Salaries, Wages & Other Payroll Benefits Supplies & Service Capitalized Costs Revenue Centers Colleges Arts & Sciences Business Communication Education Engineering Fine Arts Health Sciences Honors OGAIS University College Voinovich HCOM* RHE* Auxiliaries* Athletics Culinary Services Housing & Resident Life Pringin Parking & Transportation *Contribution Margin: Based on $ or % of Revenue

8 6 Resource Allocation Decisions: Central, Planning Unit, & Dept. Central Decisions Raise Pool Benefits Debt Strategy Institutional Investments /SOR UG Enrollment State Support Tuition Rates Planning Unit* Decisions Graduate / Online Enrollment Allocation of Raise Pools Staffing/Replacements/Hiring Support Pathways/Priorities Capital Project Prioritization Program Priorities/Reallocations Dept/Division Responsibility Recruiting/Yield Efforts Faculty/Staff Workload Curriculum delivery Academic outcomes Student Success/Service Efficiency/Service level Compliance/Accreditation * Planning Units are defined as colleges (led by Deans) or administrative/support units (led by Executive staff)

9 7 Revenue Model: SSI Allocations to each University calculated by the Department of Higher Education funding formula primarily driven by: course completions degree completions weighting factors based on subject field of courses and degrees weighting factors associated with student demographics contributing to risk in course and degree completion The OBM Model allocates 98% of the state SSI funding, based on the following instructional categories: Undergraduate Athens RHE Master s and Doctoral Medical The remaining 2% of the SSI allocation funds the Strategic Opportunity Reserve (SOR) Medical Set-aside 8% Doctoral Setaside 12% Statewide SSI Model Degree Attainment 50% Course Completions 30%

10 8 Revenue Model: FY19 SSI Allocations RHE, $22,432,188 Arts & Sciences, $35,888,181 HCOM, $22,386,376 Voinovich, $2,015,095 Business, $14,378,524 University College, $1,912,082 OGAIS, $903,565 Honors, $46,493 Communication, $8,155,609 Education, $10,525,276 Health Sciences, $30,012,515 Fine Arts, $7,368,214 Engineering, $8,595,653

11 9 Revenue Model: FY 19 Undergraduate Tuition 2% of the annual UG tuition is used to fund SOR Program allocations are directly allocated to colleges to support travel programs and the Ohio Program for Intensive English (OPIE) The remaining UG tuition revenues for Athens are distributed to the Colleges using an RCM allocation, based on proportional shares of SCH production (85%) and headcount majors (15%). Program Allocations, $4,150,000 Hold Back (< 2% in FY19), $2,846,464 UG College Allocations (85/15), $222,212,244

12 10 Revenue Model: FY19 UG Tuition = $222.2M Honors, $164,656 OGAIS, $565,307 Regional Higher Ed, $581,280 University College, $6,764,421 Voinovich, $117,135 Health Sciences, $22,760,491 Fine Arts, $14,250,487 Arts & Sciences, $91,424,796 Engineering, $15,330,347 Education, $15,265,635 Communication, $20,851,365 Business, $34,136,324

13 11 Revenue Model: Undergraduate Net Tuition Since gross UG tuition revenues are recognized in OU s revenue model, UG Student Financial Aid is budgeted and allocated to colleges to accurately reflect net tuition revenue. Similar to the UG tuition, UG financial aid is allocated to colleges based on proportional shares of SCH production (85%) and headcount majors (15%). Fine Arts, $11,627,087 Honors, $134,344 Health Sciences, $18,570,467 Engineering, $12,508,153 Education, $12,455,354 OGAIS, $461,239 Regional Higher Ed, $474,271 University College, $5,519,145 Voinovich, $95,571 Arts & Sciences, $74,594,225 FY19 SFA =$40.9M FY19 Net UG Tuition =$181.3M Communication, $17,012,796 Business, $27,852,101

14 12 Control Total Funded Planning Units Administrative and Central Operations Effective FY20, Revenue Centers (Colleges, Auxiliaries and Central Revenues) will be supporting the control total funded planning units through contribution margins established by the OHIO Budget Model. Prior to FY20, OU s RCM model utilized the Allocated Cost Model (ACM) to support administrative and central operations. FY20 is the third year of the Administrative Unit s 7% Budget Savings Initiative. Central Planning Assumptions for FY20 include: Topic Item FALL FY20 - Planning Assumption 29 Compliance: $500K Central Costs 30 Utilities: $0.6M 31 Plant Operation & Maintenance: $0.2M 32 Base Admin Control Totals: -$2.0M

The CCAM methodology utilizes space data and depreciation to allocate costs at the planning unit level.")

15 13 Capital Cost Allocation Model (CCAM) The Capital Cost Allocation Model (CCAM) is the methodology utilized to allocate the central debt service charges to colleges and administrative planning units. CCAM does not include the debt service paid directly by planning units (e.g. Housing & Residence Life) The CCAM methodology utilizes space data and depreciation to allocate costs at the planning unit level. As new capital projects occur in the buildings occupied by a unit, the depreciation charge will increase. The University s 6-Year Capital Improvement Plan (CIP) is the basis of the future year CCAM charges. Link: FY19-24 Six Year Capital Improvement Plan OHIO UNIVERSITY CAPITAL IMPROVEMENT PLAN: DEBT ISSUANCE FY FY 2024 ($, in millions) Fiscal Year Total CIP Debt Issuance $ $ $ - $ 125 $ - $ $ 575 (in millions) FY15 Actuals FY16 Actuals FY17 Actuals FY18 Budget FY18 Forecast FY19 Budget Operating Results Internal Loan - Principal & Interest $ 27.4 $ 38.0 $ 58.2 $ 51.1 $ 49.0 $ 54.1 Consolidated Results External Debt Service - Interest $ 18.6 $ 24.3 $ 26.8 $ 28.4 $ 28.5 $ 28.0 $1.3M growth for Century Bond Deferred Maintenance FY19 $2.4M growth in Internal Loans that were delayed $1.3M growth in FY19 CIP Internal Loans

16 Questions? 14

17

18

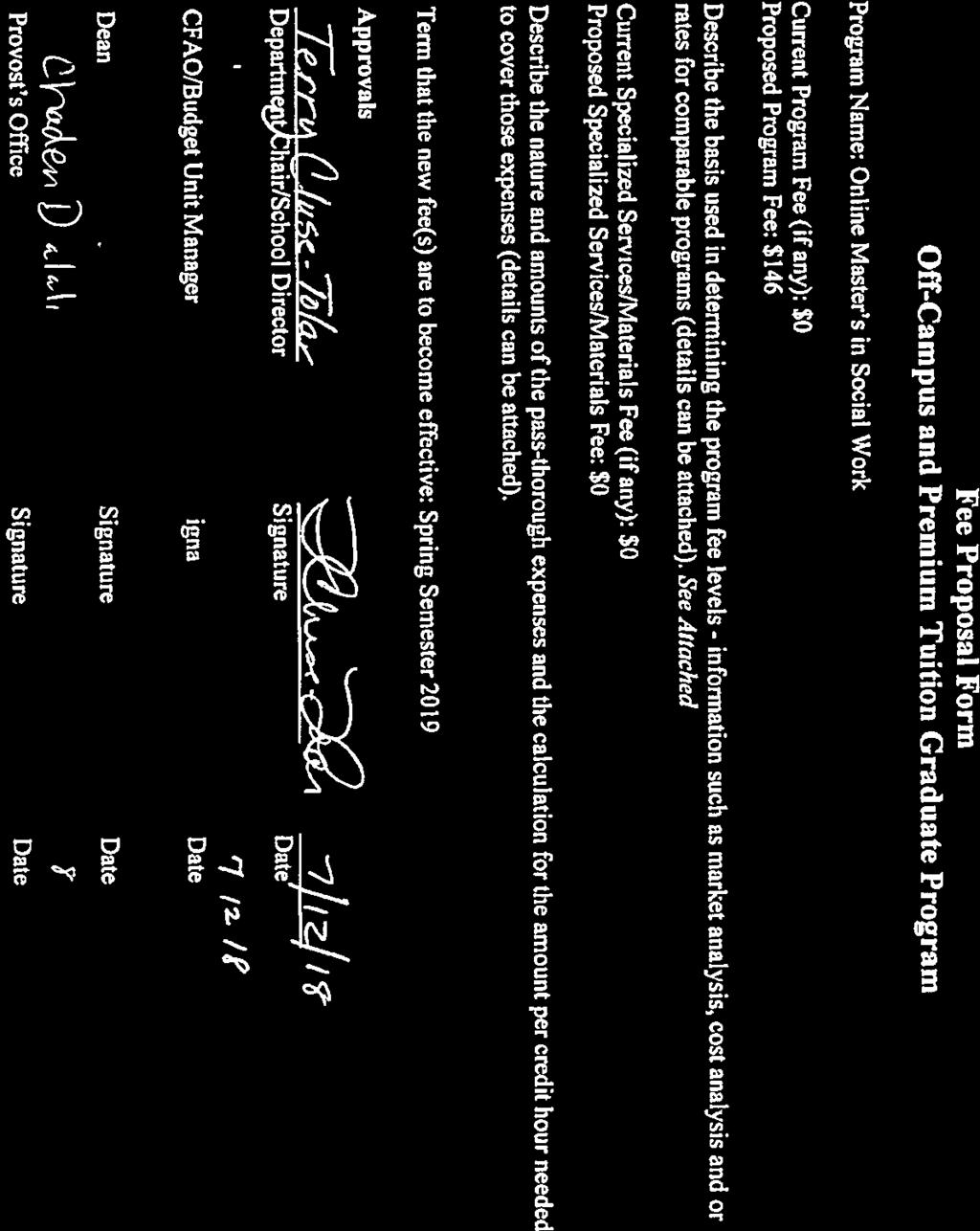

19 Fall BPC Request: Graduate Program Fee Approval PROPOSED Instructional Fee General Fee Program Fee Special Services / Materials Fee Ohio Resident Total Non Resident Fee Out of State Resident Total Online Masters in Social Work

20 Budget Planning Council Meeting Notes September 20, 2018, 11:00 AM 1:00 PM Baker Center Room 230 BPC Members In Attendance: Deb Shaffer, Chaden Djalali, Joe Shields, Madison Sloat, Joe McLaughlin, Sarah Helfrich, Susan Williams, Faith Voinovich, Jason Pina, Tim Epley, Maria Modayil, Hans Meyer, Matthew Shaftel, Dale Masel BPC Members Absent: Randy Leite, Amanda Graham Non voting Members: Katie Hensel, John Day, Dawn Weiser, Kayla Righter, Jennifer Cox, Jim Sabin, Jen Kirksey, Craig Cornell, Austin McClain, Chad Mitchell FY20 Budget Timeline o Katie reviewed the timing for various planning assumptions to be provided to units before winter break, spring financial reviews and delivery of a budget to the Board of Trustees during the June meeting OHIO Budget Model o RCM model was used previously for budget years ; the model is being changed but does retain some of the previous model characteristics o In August, 2017, President Nellis charged a Budget Model Committee to develop recommendations for a new Budget Model see attached Committee Recommendations o In January, 2018, the Committee recommendation was to retain certain RCM principles which align resources with activities, to empower decision making to units and provide stability and predictability for colleges, and to provide for a simple and transparent allocation of central costs. These recommendations have been accepted and are being built in to the FY20 budget process. o The new OHIO budget model (OBM) is being implemented: o Central revenues (SSI, tuition net of aid) and expenses will continue to be allocated based on existing methods see below. o the RCM model redirected revenues via a tax for creation of a subvention pool that then was used to redistribute funds to balance resources across colleges; the new model will allow University Leadership to establish contribution margins for each college to support the University operations, inclusive of administrative units, academic support units, and college level support HCOM, RHE and Auxiliaries may have a contribution based on a percent of revenue or flat amount o Budget assumptions are refined throughout the planning period and built into unit budgeting; colleges will have individual, targeted contribution margins, which may get to provide a balanced budget o Negotiating the colleges contribution margins is an iterative process and will be informed by the strategic decision making choices of leadership in order to balance the budget the success and importance of initiatives which support the President s Strategic Pathways and priorities will inform contribution margin decisions o Central revenue allocations the allocation methodology will not change o SSI 2% is allocated to the Strategic Opportunity Reserve (SOR) and 98% is allocated to colleges allocation from the state is based on course and degree completions primarily SSI attributed to RHE and HCOM flow directly to those units as allocated by the state o Tuition (similar to SSI) 2% to SOR with the balance to the colleges excluding small set asides to the Study Abroad and OPIE programs o UG financial aid is netted against UG tuitions and then the net revenue is allocated based on Student Credit Hour (SCH) production (85%) and headcount majors (15%)

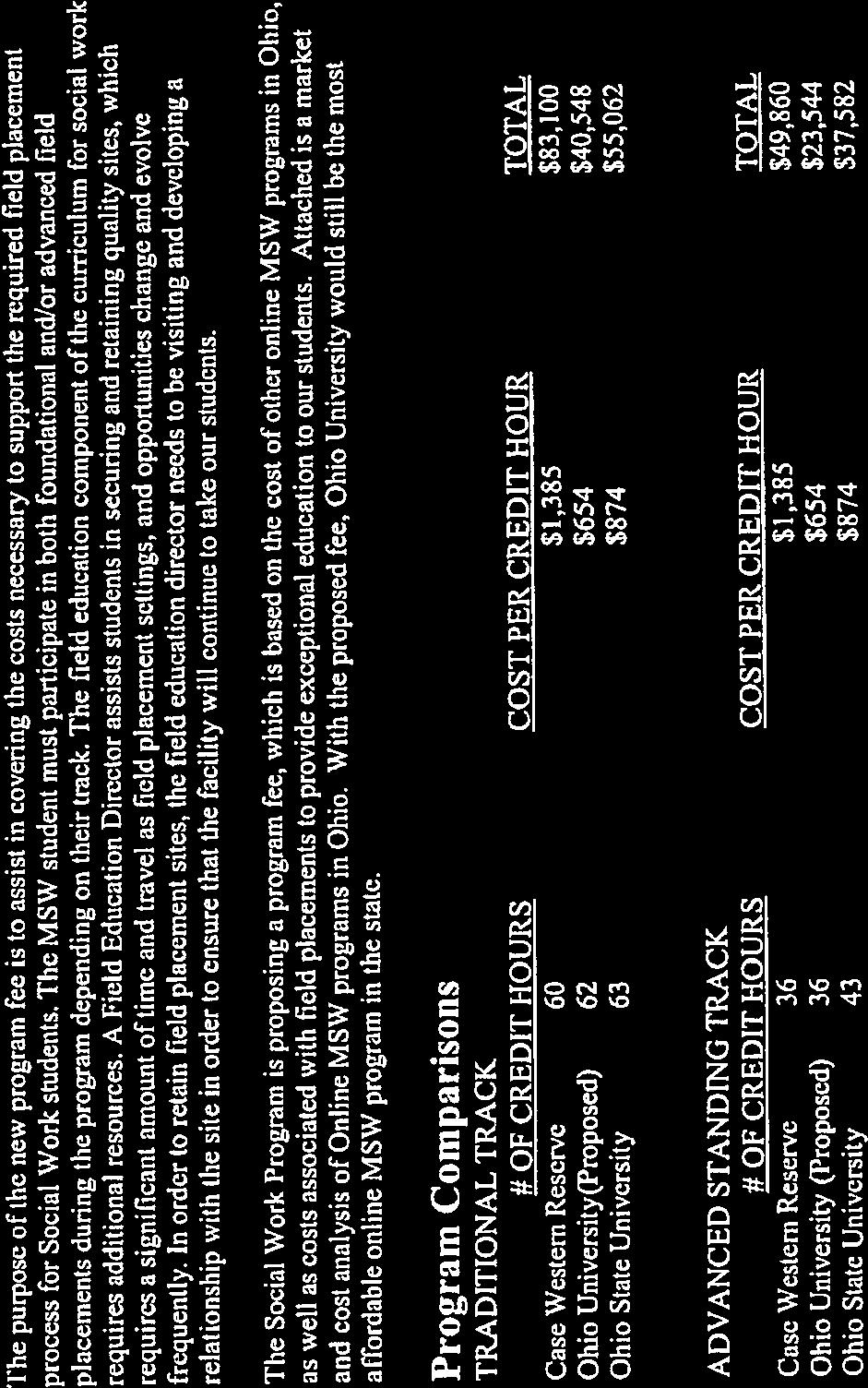

21 o o o o Administrative and Central Operations o FY20 control totals are based on the FY19 budgets for those units, layering in the initial FY20 planning assumptions for expense growth (University raise pools, debt costs, energy costs and facility square footage charges) less FY20 targeted unit reductions which represent the final year of the 7% reductions established in FY18 Capital Cost allocations continue as before and distribute central debt service charges to units for shared costs of deferred maintenance investments through depreciation Prior RCM line items (subvention lines) have been collapsed into the contribution margin under the new budget model Joe McLaughlin discussed that there is a belief among some faculty that course enrollments drive the largest portion of SSI distribution when in fact it has moved to degree completions, which account for 50% of SSI received (courses completions drive 30%) Joe suggested some beefed up communication to faculty o getting enrollments is vitally important but the state performance based funding approach is intended to incent the retention of students and ultimately graduation in order to pay for the course delivery efforts o awarding of degree SSI is not tied to the time taken to graduate. Whenever the graduation occurs, the SSI is awarded, but clearly, efficiently moving students through to graduation aligns cash receipts from the state with University expenditures supporting their instruction. Graduate Program Fee Request John Day o Online Masters in Social Work $146 program fee to be effective with a new program which will start in January Spring semester 2019 o market pricing by colleges for graduate/professional programs is achieved through the program fees o Case Western and OSU were used for program comparisons for the online MSW Next Meeting Thursday, October 4, 2018 Baker Center, Room 230

22 Budget Model Committee Charge Budget Model Committee Recommendations This committee was established at the beginning of the Fall 2017 Semester and is advisory to the President. The Budget Model Committee was charged with developing recommendations on implementation of a University budget model (revenue and cost allocations) that will be the basis for development and management of the institution s multi-year budget. The Committee was asked to consider all that we have learned from past budget models (strengths, opportunities, challenges, and goals) while also considering and evaluating models utilized by other institutions. Recommendations must be evaluated within the context of the Scope and Principles/Goals identified below: Scope Consider all Budget Models does not have to be an incremental version to the current RCM model Include all revenue sources in assessments of all models, inclusive of sponsored research, graduate and undergraduate tuition, gifts/endowment, and state support Consider how accumulated reserves should be allocated to support planning recommendations Scope does NOT include: o Macro planning assumptions (raise pools, benefit increases, capital planning, etc.) o Unit budgets (other than in the context of growth related to overall university operations/revenues) o Specific staffing/productivity decisions Principles and Goals The Budget Model and Budget Process should: Recognize and support the breadth and diversity of academic disciplines and learning environments Align resources to unit and institutional priorities Support and promote research and academic excellence Incentivize efficiency, innovation, and revenue enhancement Support research and academic excellence while being respectful of funding decisions (and various funding sources) within each college Provide incentives for efficiency, innovation, smart growth and revenue enhancement Be designed to be sustainable over time Be resilient and flexible enough to respond to changes Support multi-year, balanced budget planning Promote transparency, predictability, and common understanding 1

23 Provide a clear presentation of ALL central funding allocations and associated methodology Promote localized decision making and accountability Include a governance process with clear roles and responsibilities Recognize the internal and external restrictions on certain funds Include guidance for the role of the model in the budget process and how it is and is not used in strategic decision making Be clearly communicated and emphasize academic terminology over financial Membership Co-Chairs: John Day, Deb Shaffer David Descutner, Interim EVPP Deans/VPs/Provost : Renee Middleton, Bob Frank, Randy Leite, Dennis Irwin, Elizabeth Sayrs, Joe Shields, Brad Cohen CFAOs: Rosanna Howard, Shelley Ruff, Heather Krugman Faculty: Susan Williams, Joe McLaughlin Students: Zachary Woods, Maria Moyadil Staff Support: Laura Myers, Katie Hensel Committee Findings, Observations and Recommendations The committee collected feedback and discussed issues with the current RCM implementation. Issues centered around two areas: model-related and processrelated. A primary observation is that most issues had less to do with the details of the model calculations and more to do with the way the information from that model has been used in the budget process. There are many possible models that could be used as long the use of that information within the broader budgeting process was considered fair and transparent. Budget Context To reinforce this important distinction between a model and the budget process, the committee makes the following observations with respect to the overall context within which the budget process exits: At its core, budgeting is simply the allocation of resources in a constrained environment The primary resources that units need are people and space Both of these resources need funding to exist Therefore budgets are simply funding distributions driven by resource allocation decisions. Resource allocation decisions should be based on strategic priorities Financial information informs but should not drive resource allocation decisions Strategy should drive resource allocation 2

24 Given this broader and more strategically focused context, the committee offers the following recommendations about the budget process: Move away from the idea that a budget model is at the center of resource allocation decisions Modeling financial activity is important to understanding resource availability but is simply one piece of information used in resource allocation decisions No financial modeling can determine what the level of resource allocation should be for an academic or administrative unit Resource allocation decisions may or may not be based on financial modeling Recommendations: Drop the idea that there is budget model at the center of the process and focus on the idea that the budget is actually a series of strategic resource allocation choices and decisions. Drop the RCM label since it does not capture the broader nature of strategic resource allocation Basis for Resource Allocation Decisions As we move towards a budget process that is focused on strategic resource allocation and away from equating the budget process with a financial budget model, we will need to broaden the information that is used to information resource allocation choices and decisions. The committee offers the following observations and recommendations related to this issue: Resource allocation decisions need to be informed by a wide range of information (financial and non-financial) Strategic priorities and unit-level priorities should be quantified Resource allocation should consider unit performance relative to performance on all metrics that apply to them (both financial and nonfinancial) Recommendation: Explicitly incorporate non-financial metrics when setting and changing resource allocations for academic units Academic productivity metrics (e.g. Retention, degrees, studentfaculty ratios, etc.) Academic quality metrics (e.g. Rankings, accreditation, selectivity, faculty quality, etc.) Research productivity metrics (e.g. Research funding, publication rates, etc.) Other Each unit should have unique metrics and some metrics should be used in all colleges. 3

25 Participation in Resource Allocation Decision Making Resource allocation decisions are made at every level of the University. At the highest level, decisions about resource levels across planning units are made by the leadership of the University. Within each College/Administrative Unit, decisions are made about resource levels available to each department/school/division. At the Department/School/Division level decisions about allocation of personnel workload/effort, space utilization and other resource allocations must be made. At the University level, the distribution of resources across colleges and administrative units will be a strategic decision made by leadership. This has led to a tension between resources allocated to academic versus administrative units. There will always need to be resources allocated to administrative functions but appropriate level of central costs will always require a strategic tradeoff between functions needed and funding needed. To promote a resource allocation environment that is transparent, the committee makes the following recommendation Deans and VPs should provide input into resource allocation priorities across units and be involved as choices and tradeoffs are considered. Discussions should occur in an integrated context as opposed to sequential isolated issues. Develop an approach to open up dialogue between colleges and central support units about service levels, benchmarking costs, and efficiency Financial Modeling While recognizing that the budget process should focus on strategic resource allocation decisions, some sort of financial modeling will always be need to understand how funding is obtained and how that funding is distributed and used across units. As requested, the committee is making recommendations about how financial activity should be represented across academic units. As we do that, we would like to reinforce the following points: Short-sighted maximization of funding incents maximization of efficiency (the production of credits and degrees as cheaply as possible by using contingent faculty, large sections, low admission standards, etc.). In contrast, academic quality (accredited and highly ranked programs, tenured faculty, high admission standards) can create demand and support long-term success. Resource allocation must strike a balance between efficiency (bringing sufficient resources) and quality (distribution of resources that may not maximize funding). The same balance between quality level and efficiency must be considered in administrative units as well. 4

26 Financial modeling is needed to ensure that we understand how academic activity results in levels of funding to support resource allocation but such modeling needs to be simple and transparent. Financial Modeling Recommendations The attribution of revenues to colleges is viewed as valuable and provides transparency and a basis for understanding the financial results of academic activity as opposed to being hidden under incremental budgeting. Recommendation 1 - financial modeling should continue the current practice of showing revenues attributable to academic units as follows: Funding supporting resources within academic units that currently flows directly to the academic unit (either through external restrictions or past practice) should continue. These flows are as follows: Externally Restricted to an Academic Unit Grant Revenue Gift/Endowment External Sales Funding flowing to academic units by Past Practice ECAM Tuition Course Fees Graduate SSI Graduate Tuition and Wavers Funding that is estimated based on prior year levels of credit hours (85%) and majors (15%) SSI for all Undergraduate Activity Tuition net of Financial Aid for Athens Undergraduate Activity Recommendation 2 - Consider creating incentive funding pools to promote cooperation over competition This could be similar to the Strategic Opportunity Reserve and could be created over time by holding a percentage of revenues outside allocations to colleges Funds might be used to compensate colleges that engage in activities that run counter to results of financial modeling (e.g. interdisciplinary efforts, sharing faculty resources, honors programs, etc.) Recommendation 3 - Do not distribute central costs through an allocated cost approach as part of financial modeling The allocation of funding to central administrative units is also a strategic resource allocation decision 5

27 Treating the costs of administrative functions as attributable to the activity within colleges is not effective since colleges cannot control their use of most services, cannot opt out of services and cannot obtain services outside the university. Therefore representing resources allocated to administrative units as cost allocations to college as part of the financial modeling used in resource allocation process should be discontinued Removal of central cost allocations would also eliminates a representation of a bottom line derived from an exchange between a subvention tax and subvention pool allocation which are confusing and not well understood. Instead, represents the revenues attributable to the academic activity of the colleges and the direct expenses within the colleges to support that activity. Colleges are then able to focus on the areas that they can influence the revenue resulting from their academic activity and the direct costs supporting that activity Each college would end up with a margin and those funds are used to fund central administrative costs. When the total of margins across colleges is not sufficient to cover central administrative costs, this structural deficit must be solved collectively by all units through resource allocation decisions (same as it is now when there is a structural imbalance) This change will also remove RHE and HCOM from the allocated cost calculation. Financial modeling should still include a flow from these units to support central administrative costs. This flow could return to a simple tax allocation to support administrative costs as they were prior to RCM. They are essentially treated this way currently through the use of subvention to counterbalance central costs. This explicitly returns the setting of their contribution to a resource allocation decision 6

Budget Planning Council Meeting Agenda August 30, :00am 1:00 pm Baker Center ~ Multicultural Center Room 219

Budget Planning Council Meeting Agenda August 30, 2018 11:00am 1:00 pm Baker Center ~ Multicultural Center Room 219 Meeting Objectives Provide members with an overview of the: o Role of BPC in the Ohio

Budget Planning Council Meeting Agenda August 30, 2018 11:00am 1:00 pm Baker Center ~ Multicultural Center Room 219 Meeting Objectives Provide members with an overview of the: o Role of BPC in the Ohio

Breakfast for Progress. Ensuring a Sustainable Financial Future at Ohio University

1 Breakfast for Progress Ensuring a Sustainable Financial Future at Ohio University 1-31-18 2 Decision-making Structure What is the role of shared governance in OHIO s budget process? Board of Trustees

1 Breakfast for Progress Ensuring a Sustainable Financial Future at Ohio University 1-31-18 2 Decision-making Structure What is the role of shared governance in OHIO s budget process? Board of Trustees

1 Executive Summary 2 FY19 Budget 3 State Appropriations 4 Tuition & Educational Fees

Budget Book 2018-2019 Table of Contents 1 Executive Summary... 5 2 FY19 Budget... 11 2.1 Consolidated University Budget (All Funds)... 11 2.2 Budget Columns (All Funds)... 12 2.3 Summary of Revenue Sources...

Budget Book 2018-2019 Table of Contents 1 Executive Summary... 5 2 FY19 Budget... 11 2.1 Consolidated University Budget (All Funds)... 11 2.2 Budget Columns (All Funds)... 12 2.3 Summary of Revenue Sources...

A New Academic Business Model for UMass Dartmouth

Resourcing the Mission A New Academic Business Model for UMass Dartmouth Budgetary Planning Council 2016 Public Higher Ed in the 21 st C The situation The social compact has been compromised Resulting

Resourcing the Mission A New Academic Business Model for UMass Dartmouth Budgetary Planning Council 2016 Public Higher Ed in the 21 st C The situation The social compact has been compromised Resulting

Budget Book

Budget Book 2017-2018 Table of Contents 1 Executive Summary... 5 2 FY18 Budget... 15 Consolidated University Budget (All Funds)... 15 Budget Columns (All Funds)... 16 Summary of Revenue Sources... 19

Budget Book 2017-2018 Table of Contents 1 Executive Summary... 5 2 FY18 Budget... 15 Consolidated University Budget (All Funds)... 15 Budget Columns (All Funds)... 16 Summary of Revenue Sources... 19

What is Responsibility Centered Management?

Jim Florian Associate Vice President, Institutional Analysis Office of the Provost What is Responsibility Centered Management? Budget model that links budgets to activity Allocates revenues based on activity

Jim Florian Associate Vice President, Institutional Analysis Office of the Provost What is Responsibility Centered Management? Budget model that links budgets to activity Allocates revenues based on activity

DRAFT August 2, Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus

Budget Model Academic Colleges Focus") Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus OSU-Corvallis is implementing a new budget model with the FY18 E&G budget. The model was used to

Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus OSU-Corvallis is implementing a new budget model with the FY18 E&G budget. The model was used to

UW-Platteville Pioneer Budget Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

Finance & Administration Committee. June 6, 2018

Finance & Administration Committee June 6, 2018 1 Agenda Call to Order/Roll/Declaration of Quorum Consent Agenda Vice President s Report Third Quarter Financial Report Tuition Policy Revision - HB 4141

Finance & Administration Committee June 6, 2018 1 Agenda Call to Order/Roll/Declaration of Quorum Consent Agenda Vice President s Report Third Quarter Financial Report Tuition Policy Revision - HB 4141

Dean s RCM Workshops January 2015

Dean s RCM Workshops January 2015 Agenda General overview of RCM Overview of the model and college budget composition Education s view of RCM Engineering s view of RCM Group Activity: Scenarios 2 General

Dean s RCM Workshops January 2015 Agenda General overview of RCM Overview of the model and college budget composition Education s view of RCM Engineering s view of RCM Group Activity: Scenarios 2 General

Overview of Responsibility Centered Management (RCM) Budget Model Aug 2017

Budget Model Aug 2017") Overview of Responsibility Centered Management (RCM) Budget Model Aug 2017 The Responsibility Centered Management Budget Model was designed with the input of the University community to 1) encourage revenue

Overview of Responsibility Centered Management (RCM) Budget Model Aug 2017 The Responsibility Centered Management Budget Model was designed with the input of the University community to 1) encourage revenue

Frequently Asked Questions (FAQs) about NKU s New Budget Model

about NKU s New Budget Model") Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

Finance Reform. Speaker Series March

Finance Reform A new metrics-informed financial model designed to improve transparency, align incentives with campus goals, and simplify our planning and management environment http://budget.berkeley.edu/financereform

Finance Reform A new metrics-informed financial model designed to improve transparency, align incentives with campus goals, and simplify our planning and management environment http://budget.berkeley.edu/financereform

2/22/2019. Understanding the University Budget Kelley Westhoff Executive Director for Budget, Planning, & Analysis. Agenda

Understanding the University Budget Kelley Westhoff Executive Director for Budget, Planning, & Analysis March 6, 2019 Agenda $ The Washington State Budget & Higher Education Sector $ Budget Models $ The

Understanding the University Budget Kelley Westhoff Executive Director for Budget, Planning, & Analysis March 6, 2019 Agenda $ The Washington State Budget & Higher Education Sector $ Budget Models $ The

Refinements to Budget Procedures

Refinements to Procedures February 2016 Summarized Report of the Procedures Steering Committee Background - BPSC During the fall of 2015, an ad hoc Procedures Steering Committee was appointed by the President

Refinements to Procedures February 2016 Summarized Report of the Procedures Steering Committee Background - BPSC During the fall of 2015, an ad hoc Procedures Steering Committee was appointed by the President

The Florida International University Budget Town Hall Discussion. March 9, 2009

The Florida International University Budget Town Hall Discussion March 9, 2009 1 FLORIDA INTERNATIONAL UNIVERSITY AGENDA Direction What is the University s strategic direction? What are the state revenue

The Florida International University Budget Town Hall Discussion March 9, 2009 1 FLORIDA INTERNATIONAL UNIVERSITY AGENDA Direction What is the University s strategic direction? What are the state revenue

Budget Model Initiative (Phase 1)

") Budget Model Initiative (Phase 1) March 2017 Higher Purpose. Greater Good. 1 The Budget Model initiative is divided into two phases Phase 1: Transparency (Fall 2016 / Winter 2017) Phase 2: Redesign (Q2

Budget Model Initiative (Phase 1) March 2017 Higher Purpose. Greater Good. 1 The Budget Model initiative is divided into two phases Phase 1: Transparency (Fall 2016 / Winter 2017) Phase 2: Redesign (Q2

RCM Review. Responsibility Centered Management Review September Budget Planning & Resource Analysis

RCM Review Responsibility Centered Management Review September 2011 Budget Planning & Resource Analysis What is RCM and RCB? RCM is Responsibility Centered Management RCB is Responsibility Centered Budgeting

RCM Review Responsibility Centered Management Review September 2011 Budget Planning & Resource Analysis What is RCM and RCB? RCM is Responsibility Centered Management RCB is Responsibility Centered Budgeting

Five-year Financial Plan Orientation

Five-year Financial Plan Orientation Agenda Budget Overview Five-year Financial Plan Initiative Budget Overview Financing the Future The Financial Challenge Ahead Operating budget history Projects for

Five-year Financial Plan Orientation Agenda Budget Overview Five-year Financial Plan Initiative Budget Overview Financing the Future The Financial Challenge Ahead Operating budget history Projects for

Strategic Budgeting: 10 Critical Policy Decisions

Strategic Budgeting: 10 Critical Policy Decisions Facilitator Andrew Laws Managing Director Huron Consulting Group Panelists Melissa Johnson Director of Budget and Fiscal Planning Purdue University Chad

Strategic Budgeting: 10 Critical Policy Decisions Facilitator Andrew Laws Managing Director Huron Consulting Group Panelists Melissa Johnson Director of Budget and Fiscal Planning Purdue University Chad

Financial Operating. & Capital Plan Reviews FY Budget Forum. February 14, FY 2014 Budget Forum - February

Financial Operating & Capital Plan Reviews FY 2014 Budget Forum February 14, 2013 FY 2014 Budget Forum - February 2013 0 University Budget Council (UBC) Bob Warren, Chair VP Administration & Finance Dennis

Financial Operating & Capital Plan Reviews FY 2014 Budget Forum February 14, 2013 FY 2014 Budget Forum - February 2013 0 University Budget Council (UBC) Bob Warren, Chair VP Administration & Finance Dennis

In fiscal year (FY) , the general fund base budgets by department were as follows:

, the general fund base budgets by department were as follows:") 1.6 Fiscal Resources. The school shall have financial resources adequate to fulfill its stated mission and goals, and its instructional, research and service objectives. a. Description of the budgetary

1.6 Fiscal Resources. The school shall have financial resources adequate to fulfill its stated mission and goals, and its instructional, research and service objectives. a. Description of the budgetary

University Budget Process Fiscal Year 2018

University Budget Process Fiscal Year 2018 University Council Three Takeaways from Today 1. We have a two-part budget process. 1. University Budget Process 1. High level basic assumptions to build overall

University Budget Process Fiscal Year 2018 University Council Three Takeaways from Today 1. We have a two-part budget process. 1. University Budget Process 1. High level basic assumptions to build overall

DEANS, VICE CHANCELLORS, UNIVERSITY LIBRARIAN, ATHLETIC DIRECTOR AND CHIEF INFORMATION OFFICER

DEANS, VICE CHANCELLORS, UNIVERSITY LIBRARIAN, ATHLETIC DIRECTOR AND CHIEF INFORMATION OFFICER Re: Dear Colleagues, The budget planning process for 2019-20 marks a point of inflection for our financial

DEANS, VICE CHANCELLORS, UNIVERSITY LIBRARIAN, ATHLETIC DIRECTOR AND CHIEF INFORMATION OFFICER Re: Dear Colleagues, The budget planning process for 2019-20 marks a point of inflection for our financial

New Mexico Highlands University Annual Operating Budget Process. approved Fall 2016

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

Responsibility Center Management (RCM) University of Pennsylvania Office of Budget & Management Analysis Fall 2017

University of Pennsylvania Office of Budget & Management Analysis Fall 2017") Responsibility Center Management (RCM) University of Pennsylvania Office of Budget & Management Analysis Fall 2017 Responsibility Center Management (RCM) Management & Reporting at PENN Internal: RCM is

Responsibility Center Management (RCM) University of Pennsylvania Office of Budget & Management Analysis Fall 2017 Responsibility Center Management (RCM) Management & Reporting at PENN Internal: RCM is

University of Florida 5 Year Budget Review

University of Florida 5 Year Budget Review 1 Steering Committee Role and Responsibility Defined the scope of the review process, project goals and guiding principles. Ensured that the resulting project

University of Florida 5 Year Budget Review 1 Steering Committee Role and Responsibility Defined the scope of the review process, project goals and guiding principles. Ensured that the resulting project

DRAFT for Campus Discussion August 10, 2017

Technical Notes for the Draft Shared Responsibility Budget Model FY16, FY17, FY18 versions for Oregon State University, Corvallis Campus, Education and General Budget Author Note Principal changes from

Technical Notes for the Draft Shared Responsibility Budget Model FY16, FY17, FY18 versions for Oregon State University, Corvallis Campus, Education and General Budget Author Note Principal changes from

Technical Notes for the Shared Responsibility Budget Model, ver for Oregon State University, Corvallis Campus Education and General Budget

Technical Notes for the Shared Responsibility Budget Model, ver. 19.8 for Oregon State University, Corvallis Campus Education and General Budget August 8, 2018 Overview The goals of this shared responsibility

Technical Notes for the Shared Responsibility Budget Model, ver. 19.8 for Oregon State University, Corvallis Campus Education and General Budget August 8, 2018 Overview The goals of this shared responsibility

Presented to the Board of Trustees

Presented to the Board of Trustees 0 July 5, 2016 CSPP Budget Decision-Making Principles & Process The budget planning and development will be guided by the following Board of Trustees approved resource

Presented to the Board of Trustees 0 July 5, 2016 CSPP Budget Decision-Making Principles & Process The budget planning and development will be guided by the following Board of Trustees approved resource

Budget Model Assessment

Budget Model Assessment An Update on the Activities of the Joint Task Force on Resource Allocation Co-chairs: Elizabeth Chilton and Tim Anderson January 30 th, 2014 JTFRA Charge The Joint Task Force on

Budget Model Assessment An Update on the Activities of the Joint Task Force on Resource Allocation Co-chairs: Elizabeth Chilton and Tim Anderson January 30 th, 2014 JTFRA Charge The Joint Task Force on

UTSA FY 2018 Budget 101 Presentation Foundational

UTSA FY 2018 Budget 101 Presentation Foundational Kathryn Funk-Baxter, Vice President for www.utsa.edu/businessaffairs UTSA Budget Process Current budgeting process overview Overview of Revenue (sources)

UTSA FY 2018 Budget 101 Presentation Foundational Kathryn Funk-Baxter, Vice President for www.utsa.edu/businessaffairs UTSA Budget Process Current budgeting process overview Overview of Revenue (sources)

Resource Management: An Overview and Assessment of the Current External Environment. Melody Bianchetto

Resource Management: An Overview and Assessment of the Current External Environment Melody Bianchetto 2013 Managerial Analysis and Decision Support Salt Lake City, UT November 14 15, 2013 Agenda Resource

Resource Management: An Overview and Assessment of the Current External Environment Melody Bianchetto 2013 Managerial Analysis and Decision Support Salt Lake City, UT November 14 15, 2013 Agenda Resource

Five-Year Financial Plan (FY2019 FY 2023) 02/23/18

02/23/18") Five-Year Financial Plan (FY2019 FY 2023) 02/23/18 Renewing Our Vow to the Commonwealth Six years ago, we committed to a bold vision for UK- rebuild our campus, grow funds, support faculty and staff, and

Five-Year Financial Plan (FY2019 FY 2023) 02/23/18 Renewing Our Vow to the Commonwealth Six years ago, we committed to a bold vision for UK- rebuild our campus, grow funds, support faculty and staff, and

Budget Town Hall Meeting

Budget Town Hall Meeting FY 2018-19 Operating Budget Proposal Chancellor Steven Angle & EVC Richard Brown Factors Impacting the FY 2019 Budget UTC #1 University in CCTA Metrics for Fourth Year in a Row!

Budget Town Hall Meeting FY 2018-19 Operating Budget Proposal Chancellor Steven Angle & EVC Richard Brown Factors Impacting the FY 2019 Budget UTC #1 University in CCTA Metrics for Fourth Year in a Row!

Joseph Trubacz Senior Vice President for Finance and Administration

TO: FROM: Board of Trustees Joseph Trubacz Senior Vice President for Finance and Administration DATE: May 21, 2011 SUBJECT: FY 2013 Budget I. BACKGROUND INFORMATION Fiscal Year 2013 Operating Budget Summary

TO: FROM: Board of Trustees Joseph Trubacz Senior Vice President for Finance and Administration DATE: May 21, 2011 SUBJECT: FY 2013 Budget I. BACKGROUND INFORMATION Fiscal Year 2013 Operating Budget Summary

Budget Model Refinement Discussion. October 2018

Budget Model Refinement Discussion October 2018 1 Agenda 1. Budget Model Refinement Schedule 2. Opportunities for Refinement Significant Financial Challenges/Issues Overall Policy Issues Budget Model Formula

Budget Model Refinement Discussion October 2018 1 Agenda 1. Budget Model Refinement Schedule 2. Opportunities for Refinement Significant Financial Challenges/Issues Overall Policy Issues Budget Model Formula

How Much Does It Cost?

How Much Does It Cost? Eileen G. McLoughlin, Assistant Vice President of Finance and Budgeting, Rensselaer Polytechnic Institute Charles Tegen, Associate Vice President for Finance and Comptroller, Clemson

How Much Does It Cost? Eileen G. McLoughlin, Assistant Vice President of Finance and Budgeting, Rensselaer Polytechnic Institute Charles Tegen, Associate Vice President for Finance and Comptroller, Clemson

Budget Reform Update. Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

Staff Council President s Report Board of Trustees Committee of the Whole Friday, February 2, 2018 Karmen Swim, Staff Council President

Staff Council Staff Council President s Report Board of Trustees Committee of the Whole Friday, February 2, 2018 Karmen Swim, Staff Council President This time last year, Staff Council prepared to engage

Staff Council Staff Council President s Report Board of Trustees Committee of the Whole Friday, February 2, 2018 Karmen Swim, Staff Council President This time last year, Staff Council prepared to engage

UNTHSC. Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

2014 Planning & Budgeting Forum

2014 Planning & Budgeting Forum The Accounting of RCM September 23, 2014 Denver, CO Conference Session Speakers Name Title Contact Details Andrew L. Laws Managing Director (session facilitator) Huron Consulting

2014 Planning & Budgeting Forum The Accounting of RCM September 23, 2014 Denver, CO Conference Session Speakers Name Title Contact Details Andrew L. Laws Managing Director (session facilitator) Huron Consulting

Strategic Budgeting Initiative

Strategic Budgeting Initiative Senate Presentation November 5, 2013 Financial Challenges Sharply reduced state support Increased risk from tuition dependency At Auburn, dependency rose from 44% to 63%

Strategic Budgeting Initiative Senate Presentation November 5, 2013 Financial Challenges Sharply reduced state support Increased risk from tuition dependency At Auburn, dependency rose from 44% to 63%

ASL Budget Forum. May 8, 2017

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

Central Connecticut State University Integrated Budget Model. Pilot Department Overview and Training Session

Central Connecticut State University Integrated Budget Model Pilot Department Overview and Training Session Welcome and Introductions CCSU Budget Current As Is Process Zero-Based Budgeting in Practice

Central Connecticut State University Integrated Budget Model Pilot Department Overview and Training Session Welcome and Introductions CCSU Budget Current As Is Process Zero-Based Budgeting in Practice

An Overview: Responsibility Center Management (RCM) Treasurer s Town Hall January 15, 2015

Treasurer s Town Hall January 15, 2015") An Overview: Responsibility Center Management (RCM) Treasurer s Town Hall January 15, 2015 Common University Budget Models EVERY TUB ON ITS OWN BOTTOM INCREMENTAL FORMULA-BASED RESPONSIBILITY CENTER MANAGEMENT

An Overview: Responsibility Center Management (RCM) Treasurer s Town Hall January 15, 2015 Common University Budget Models EVERY TUB ON ITS OWN BOTTOM INCREMENTAL FORMULA-BASED RESPONSIBILITY CENTER MANAGEMENT

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW Ralph C. Wilcox, Ph.D. Provost & Senior Vice President for Academic Affairs January 21, 2009 Purpose Prepare balanced budget and legislative

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW Ralph C. Wilcox, Ph.D. Provost & Senior Vice President for Academic Affairs January 21, 2009 Purpose Prepare balanced budget and legislative

ALL FUNDS OPERATING BUDGET FY2016. Institutional Budget Document Page 1

ALL FUNDS OPERATING BUDGET FY2016 Institutional Budget Document Page 1 Table of Contents Introduction... 3 Budget Highlights... 4 General Fund Changes... 4 Tuition & Fees Rate Increase %... 4 Enrollments...

ALL FUNDS OPERATING BUDGET FY2016 Institutional Budget Document Page 1 Table of Contents Introduction... 3 Budget Highlights... 4 General Fund Changes... 4 Tuition & Fees Rate Increase %... 4 Enrollments...

January 22, Budget Model Review and Implementation Committee

Progress Report on Design and Implementation of the Resource Management Model Budget Model Review and Implementation Committee Tom Andre Tim Borich Joe Colletti Rick Dark Doug Epperson (Committee Chair)

Progress Report on Design and Implementation of the Resource Management Model Budget Model Review and Implementation Committee Tom Andre Tim Borich Joe Colletti Rick Dark Doug Epperson (Committee Chair)

LEHIGH University. Financial Planning Report With Budget

LEHIGH University Financial Planning Report With 2012-2013 Budget L E H I G H U N I V E R S I T Y 2 0 1 2-1 3 B U D G E T ------------------------- T A B L E O F C O N T E N T S PAGE I. COMMENTARY 1-9

LEHIGH University Financial Planning Report With 2012-2013 Budget L E H I G H U N I V E R S I T Y 2 0 1 2-1 3 B U D G E T ------------------------- T A B L E O F C O N T E N T S PAGE I. COMMENTARY 1-9

Transition to a New Budget Model at the University of Toronto. CAUBO June 17, 2008

Transition to a New Budget Model at the University of Toronto CAUBO June 17, 2008 Sally Garner Senior Manager Long Range Budget Planning CAUBO 17June08 Overview U of T Facts and Figures Transition Timeline

Transition to a New Budget Model at the University of Toronto CAUBO June 17, 2008 Sally Garner Senior Manager Long Range Budget Planning CAUBO 17June08 Overview U of T Facts and Figures Transition Timeline

Cleveland State University (a component unit of the State of Ohio) Financial Report Including Supplemental Information June 30, 2017

Financial Report Including Supplemental Information June 30, 2017") Cleveland State University (a component unit of the State of Ohio) Financial Report Including Supplemental Information June 30, 2017 Contents Report of Independent Auditors 1-3 Management s Discussion

Cleveland State University (a component unit of the State of Ohio) Financial Report Including Supplemental Information June 30, 2017 Contents Report of Independent Auditors 1-3 Management s Discussion

Administrative Leadership Meeting. Tuesday, May 9, 2017 Chancellor Randy Woodson

Administrative Leadership Meeting Tuesday, May 9, 2017 Chancellor Randy Woodson Upcoming ALMs July 11, 2017 Global Engagement Titmus September 12, 2017 Campus Capacity Planning Titmus November 14, 2017

Administrative Leadership Meeting Tuesday, May 9, 2017 Chancellor Randy Woodson Upcoming ALMs July 11, 2017 Global Engagement Titmus September 12, 2017 Campus Capacity Planning Titmus November 14, 2017

Informational Session for Fiscal Year Budget

Informational Session for Fiscal Year 2016-2017 Budget PRESENTED BY Angela M. Poole, CPA Acting Vice President for Finance and Administration Florida Agricultural and Mechanical University Budget and Finance

Informational Session for Fiscal Year 2016-2017 Budget PRESENTED BY Angela M. Poole, CPA Acting Vice President for Finance and Administration Florida Agricultural and Mechanical University Budget and Finance

Cleveland State University (a component unit of the State of Ohio) Financial Report Including Supplemental Information June 30, 2015

Financial Report Including Supplemental Information June 30, 2015") Cleveland State University (a component unit of the State of Ohio) Financial Report Including Supplemental Information June 30, 2015 Contents Report of Independent Auditors 1-3 Management s Discussion

Cleveland State University (a component unit of the State of Ohio) Financial Report Including Supplemental Information June 30, 2015 Contents Report of Independent Auditors 1-3 Management s Discussion

Responsibility Accounting. Profitability Analysis- Revenue and Expense by Division/Department

Responsibility Accounting Profitability Analysis- Revenue and Expense by Division/Department August 11, 2006 Overview- Definition Financial model to match all revenues and expenses associated with an Academic

Responsibility Accounting Profitability Analysis- Revenue and Expense by Division/Department August 11, 2006 Overview- Definition Financial model to match all revenues and expenses associated with an Academic

California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

ALL FUNDS OPERATING BUDGET FY2017. Institutional Budget Document Page 1

ALL FUNDS OPERATING BUDGET FY2017 Institutional Budget Document Page 1 Table of Contents Introduction... 3 Budget Highlights... 4 General Fund Changes... 4 Tuition & Fees Rate Increase %... 4 Enrollments...

ALL FUNDS OPERATING BUDGET FY2017 Institutional Budget Document Page 1 Table of Contents Introduction... 3 Budget Highlights... 4 General Fund Changes... 4 Tuition & Fees Rate Increase %... 4 Enrollments...

University Cabinet Outline of Budget Reduction Decisions February 22, 2018

Priorities in Budget Planning Student success Equity and diversity Fiscal stability and good stewardship of resources Shared responsibility and accountability Values (These are summarized from the Values

Priorities in Budget Planning Student success Equity and diversity Fiscal stability and good stewardship of resources Shared responsibility and accountability Values (These are summarized from the Values

Budget Allocation Subcommittee: Report and Recommendations

RESOURCES PLANNING TASK FORCE Budget Allocation Subcommittee: Report and Recommendations I. Preamble The Committee was asked to determine how KPU should move forward in a budget environment that needs

RESOURCES PLANNING TASK FORCE Budget Allocation Subcommittee: Report and Recommendations I. Preamble The Committee was asked to determine how KPU should move forward in a budget environment that needs

Planning and Budget Process

Planning and Budget Process The University s planning framework, The Highest Order of Excellence II, is the framework for strategic planning at all levels of the institution. Oversight for the strategic

Planning and Budget Process The University s planning framework, The Highest Order of Excellence II, is the framework for strategic planning at all levels of the institution. Oversight for the strategic

USF System Annual Strategic Budget Planning Process

USF System Annual Strategic Budget Planning Process University budget strategy, planning and development should be led by the Provost to assure that the budget reflects USF s strategic priorities The President

USF System Annual Strategic Budget Planning Process University budget strategy, planning and development should be led by the Provost to assure that the budget reflects USF s strategic priorities The President

Introduction to the UND s New Budget Model

Introduction to the UND s New Budget Model Existing Budget Model? UND s budget approach has been historical and incremental Meaning: The next year s budget for a unit would be what units got this year

Introduction to the UND s New Budget Model Existing Budget Model? UND s budget approach has been historical and incremental Meaning: The next year s budget for a unit would be what units got this year

FY2018 Operating Budget

FY2018 Operating Budget SUMMARY OF PROPOSAL The Board of Trustees is charged with reviewing and approving the university s annual operating budget. The budget supports the educational, research, and outreach

FY2018 Operating Budget SUMMARY OF PROPOSAL The Board of Trustees is charged with reviewing and approving the university s annual operating budget. The budget supports the educational, research, and outreach

Cleveland State University (a component unit of the State of Ohio) Financial Report with Supplemental Information June 30, 2018

Financial Report with Supplemental Information June 30, 2018") Cleveland State University (a component unit of the State of Ohio) Financial Report with Supplemental Information June 30, 2018 Contents Independent Auditor s Report 1-3 Management s Discussion and Analysis

Cleveland State University (a component unit of the State of Ohio) Financial Report with Supplemental Information June 30, 2018 Contents Independent Auditor s Report 1-3 Management s Discussion and Analysis

Fiscal Year 2019 Consolidated Operating Budget

Fiscal Year 2019 Consolidated Operating Budget Presented by: Paige Smith, UNTS, Associate Vice Chancellor for Budget & Planning August 9-10, 2018 Corrections made on 08.08.18 noted in orange. Page 1 of

Fiscal Year 2019 Consolidated Operating Budget Presented by: Paige Smith, UNTS, Associate Vice Chancellor for Budget & Planning August 9-10, 2018 Corrections made on 08.08.18 noted in orange. Page 1 of

Budgeting and Planning Process as of FY17

Budgeting and Planning Process as of FY17 Summary The budget is an important annual planning document for the university and reflects choices, priorities and tactics set forth as the result of intensive

Budgeting and Planning Process as of FY17 Summary The budget is an important annual planning document for the university and reflects choices, priorities and tactics set forth as the result of intensive

Prepared by the Office of the Treasurer

Prepared by the Office of the Treasurer CSPP Budget Decision-Making Principles & Process The following principles, in order of importance and approved by the Board of Trustees, will guide budget decision

Prepared by the Office of the Treasurer CSPP Budget Decision-Making Principles & Process The following principles, in order of importance and approved by the Board of Trustees, will guide budget decision

Sequoias Community College District RESOURCE

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

An Overview of University at Buffalo Governance, Funding Sources and Financial Reporting

An Overview of University at Buffalo Governance, Funding Sources and Financial Reporting Monday, February 22, 2016 Presented by: Laura J. Barnum, Associate Vice President for Resource Planning Beth A.

An Overview of University at Buffalo Governance, Funding Sources and Financial Reporting Monday, February 22, 2016 Presented by: Laura J. Barnum, Associate Vice President for Resource Planning Beth A.

WKU Budget Restructuring Plan: Recommendations to President Caboni. WKU Budget Council. February 20, 2018

WKU Budget Restructuring Plan: Recommendations to President Caboni WKU Budget Council February 20, 2018 Executive Summary In the fall of 2017, WKU President Timothy Caboni redefined the responsibilities

WKU Budget Restructuring Plan: Recommendations to President Caboni WKU Budget Council February 20, 2018 Executive Summary In the fall of 2017, WKU President Timothy Caboni redefined the responsibilities

University of Houston-Clear Lake Appendix A - Allocation of New FY 2014 Resources

Appendix A - Allocation of New FY 2014 Resources Revenue Changes A Reallocations/Reductions B Appropriations Bill 1 Reallocations $ (920,892) 1 General Revenue $ 1,310,875 2 Reductions (985,000) 2 State

Appendix A - Allocation of New FY 2014 Resources Revenue Changes A Reallocations/Reductions B Appropriations Bill 1 Reallocations $ (920,892) 1 General Revenue $ 1,310,875 2 Reductions (985,000) 2 State

New Campus Budget Model

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

THE COLLEGE OF NEW JERSEY STRATEGIC BUDGET PLANNING FISCAL YEAR 2015

THE COLLEGE OF NEW JERSEY STRATEGIC BUDGET PLANNING FISCAL YEAR 2015 Committee on Strategic Planning and Priorities (CSPP) Budget Decision-Making Principles and Process Approved by the Board of Trustees

THE COLLEGE OF NEW JERSEY STRATEGIC BUDGET PLANNING FISCAL YEAR 2015 Committee on Strategic Planning and Priorities (CSPP) Budget Decision-Making Principles and Process Approved by the Board of Trustees

FINANCIAL SYSTEM ENHANCEMENTS ACCOUNTING WITH THE NEW COA

FINANCIAL SYSTEM ENHANCEMENTS ACCOUNTING WITH THE NEW COA 1 AGENDA Foundation & Endowment Accounting Accounting for Revenue Revenue and Expense Allocations Student Orgs Funding & Accounting How to charge

FINANCIAL SYSTEM ENHANCEMENTS ACCOUNTING WITH THE NEW COA 1 AGENDA Foundation & Endowment Accounting Accounting for Revenue Revenue and Expense Allocations Student Orgs Funding & Accounting How to charge

Resource Allocation, Management, and Planning Steering Committee #7

Resource Allocation, Management, and Planning Steering #7 August 28, 2018 1 Agenda Huron is pleased to partner with WKU on this resource allocation, management, and planning ( RAMP ) initiative. Our goals

Resource Allocation, Management, and Planning Steering #7 August 28, 2018 1 Agenda Huron is pleased to partner with WKU on this resource allocation, management, and planning ( RAMP ) initiative. Our goals

After participating LEARNING OUTCOME MOVING TO A RESPONSIBILITY- CENTERED BUDGET MODEL

#AIwebcast MOVING TO A RESPONSIBILITY- CENTERED BUDGET MODEL PRINCIPLES OF RESPONSIBILITY-CENTER MANAGEMENT Larry Goldstein Campus Strategies, LLC Larry.Goldstein@Campus-Strategies.com 1 LEARNING OUTCOME

#AIwebcast MOVING TO A RESPONSIBILITY- CENTERED BUDGET MODEL PRINCIPLES OF RESPONSIBILITY-CENTER MANAGEMENT Larry Goldstein Campus Strategies, LLC Larry.Goldstein@Campus-Strategies.com 1 LEARNING OUTCOME

Strategic Budgeting Workgroup

Strategic Budgeting Workgroup November 14, 2006 David Maddox Purpose 1. Evaluate alternatives to move away from incremental budgeting and equip UCSC to fund its most strategically important needs 2. Make

Strategic Budgeting Workgroup November 14, 2006 David Maddox Purpose 1. Evaluate alternatives to move away from incremental budgeting and equip UCSC to fund its most strategically important needs 2. Make

Presentation to the UH Faculty Senate. University of Houston FY 2016 Budget For current information see

Presentation to the UH Faculty Senate University of Houston FY 2016 Budget For current information see http://www.uh.edu/af/budget/index.htm 1 Contents Background and Process Slides 3-12 Budget Topic:

Presentation to the UH Faculty Senate University of Houston FY 2016 Budget For current information see http://www.uh.edu/af/budget/index.htm 1 Contents Background and Process Slides 3-12 Budget Topic:

EAST TENNESSEE STATE UNIVERSITY BOARD OF TRUSTEES FINANCE AND ADMINISTRATION COMMITTEE MARCH 2018 SPECIAL CALLED MEETING AGENDA

EAST TENNESSEE STATE UNIVERSITY BOARD OF TRUSTEES FINANCE AND ADMINISTRATION COMMITTEE MARCH 2018 SPECIAL CALLED MEETING 3:00-4:00pm EDT Thursday March 29, 2018 President s Conference Room Burgin Dossett

EAST TENNESSEE STATE UNIVERSITY BOARD OF TRUSTEES FINANCE AND ADMINISTRATION COMMITTEE MARCH 2018 SPECIAL CALLED MEETING 3:00-4:00pm EDT Thursday March 29, 2018 President s Conference Room Burgin Dossett

UH-Clear Lake Budget

FY2016 Total Budget $ Millions Operating Budget $ 131.5 Capital Facilities 23.1 Total $ 154.6 Operating Budget Source of Funds Other Operating, $2.0M 2% Tuition & Fees $71.1M 54% Contracts & Grants *,

FY2016 Total Budget $ Millions Operating Budget $ 131.5 Capital Facilities 23.1 Total $ 154.6 Operating Budget Source of Funds Other Operating, $2.0M 2% Tuition & Fees $71.1M 54% Contracts & Grants *,

UMass Lowell A Strategic Plan for the Next Decade. Committee on Financial Planning & Budget Review Organizational Meeting

UMass Lowell 2020 A Strategic Plan for the Next Decade Committee on Financial Planning & Budget Review Organizational Meeting March 6, 2009 Agenda Summary of Committee Charge Budget Planning Context Overview

UMass Lowell 2020 A Strategic Plan for the Next Decade Committee on Financial Planning & Budget Review Organizational Meeting March 6, 2009 Agenda Summary of Committee Charge Budget Planning Context Overview

CONSOLIDATED FINANCIAL REPORT J U N E 30, 2016

U N I V E R S I T Y O F D AY T O N CONSOLIDATED FINANCIAL REPORT J U N E 30, 2016 COMPARATIVE SUMMARY INFORMATION (All Dollars In Thousands) 2011-12 2012-13 2013-14 2014-15 2015-16 Endowment - Market 397,794

U N I V E R S I T Y O F D AY T O N CONSOLIDATED FINANCIAL REPORT J U N E 30, 2016 COMPARATIVE SUMMARY INFORMATION (All Dollars In Thousands) 2011-12 2012-13 2013-14 2014-15 2015-16 Endowment - Market 397,794

Budget Forum. May 22, 2012

Budget Forum May 22, 2012 Current Status of the RCM Model The model is an approxima?on of the underlying economics of our academic ac?vity The primary goal is to provide incen?ves for growth and fairly

Budget Forum May 22, 2012 Current Status of the RCM Model The model is an approxima?on of the underlying economics of our academic ac?vity The primary goal is to provide incen?ves for growth and fairly

The Art and Science of Multi-Year Planning

The Art and Science of Multi-Year Planning Bethany Pugh Managing Director PFM Financial Advisors LLC www.pfm.com Kevin Kuhar Senior Solutions Consultant PFM Solutions LLC www.whitebrichsoftware.com 1/31

The Art and Science of Multi-Year Planning Bethany Pugh Managing Director PFM Financial Advisors LLC www.pfm.com Kevin Kuhar Senior Solutions Consultant PFM Solutions LLC www.whitebrichsoftware.com 1/31

Fourth Report of the Budget Model Development Committee

INTRODUCTION This (BMDC) has resulted from over a year of investigating models of budget development and resource management in higher education. The goal of this study is to propose a new approach to

INTRODUCTION This (BMDC) has resulted from over a year of investigating models of budget development and resource management in higher education. The goal of this study is to propose a new approach to

I. Background. Budget Advisory Council

Office of the Vice President for Finance & Business Operations 330.941.1331 Fax 330.941.1380 University Budget Process Updated 1/17/18 I. Background Youngstown State University s annual operating budget

Office of the Vice President for Finance & Business Operations 330.941.1331 Fax 330.941.1380 University Budget Process Updated 1/17/18 I. Background Youngstown State University s annual operating budget

Office of the Provost University of Illinois at Urbana-Champaign. 3 February 2016

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

University of Houston Student Leadership Forum Budget and Legislative Processes

University of Houston Student Leadership Forum Budget and Legislative Processes June 13, 2012 Overview of the Planning and Budget Process 2 Multiple Cycles January 2012 February 2012 March 2012 April 2012

University of Houston Student Leadership Forum Budget and Legislative Processes June 13, 2012 Overview of the Planning and Budget Process 2 Multiple Cycles January 2012 February 2012 March 2012 April 2012

Financial Review FISCAL YEAR 2013

Financial Review FISCAL YEAR 2013 AGENDA Overview Resource Sufficiency & Flexibility Operating Results Financial Asset Performance Debt Management Financial Outlook 2 Achieving the Goals of the EWU Board

Financial Review FISCAL YEAR 2013 AGENDA Overview Resource Sufficiency & Flexibility Operating Results Financial Asset Performance Debt Management Financial Outlook 2 Achieving the Goals of the EWU Board

Research Council November 11, 2015

Research Council November 11, 2015 A G E N D A Financial Framework and New Financial Model First Phase of Budget Model / Educational & General Fund Mason s Ten Year Strategic Plan Research Initiatives:

Research Council November 11, 2015 A G E N D A Financial Framework and New Financial Model First Phase of Budget Model / Educational & General Fund Mason s Ten Year Strategic Plan Research Initiatives:

The Stanford University Budget Plan

i The Stanford University Budget Plan 2000/01 Submitted for Action to the Board of Trustees June 8-9, 2000 This publication can also be found on the World Wide Web at: http://www.stanford.edu/dept/pres-provost/budget/plans/plan01.html

i The Stanford University Budget Plan 2000/01 Submitted for Action to the Board of Trustees June 8-9, 2000 This publication can also be found on the World Wide Web at: http://www.stanford.edu/dept/pres-provost/budget/plans/plan01.html

Food Services Advisory Committee. UH Planning and Budgeting

Food Services Advisory Committee UH Planning and Budgeting November 12, 2010 Food Services Advisory Committee UH Planning and Budgeting Budgeting Process 2 Overview of the Planning and Budget Process Internal

Food Services Advisory Committee UH Planning and Budgeting November 12, 2010 Food Services Advisory Committee UH Planning and Budgeting Budgeting Process 2 Overview of the Planning and Budget Process Internal

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER STATE BIENNIAL BUDGET CYCLE OFM issues budget instructions EVEN YEARS JUN EWU BIENNIAL BUDGET CYCLE ONGOING Agency Strategic Planning Agencies submit budget

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER STATE BIENNIAL BUDGET CYCLE OFM issues budget instructions EVEN YEARS JUN EWU BIENNIAL BUDGET CYCLE ONGOING Agency Strategic Planning Agencies submit budget

Budget Forum Fiscal Year March 2, 2017

Budget Forum Fiscal Year 2017-2018 March 2, 2017 Vision that Reflects Pacific s Values Discovery is an integral and essential component of the education process. The highest quality programs are delivered

Budget Forum Fiscal Year 2017-2018 March 2, 2017 Vision that Reflects Pacific s Values Discovery is an integral and essential component of the education process. The highest quality programs are delivered

Operating & Capital Budget Plan May 2017

2017-2018 Operating & Capital Budget Plan May 2017 Operating and Capital Budget Plan FY 2018 Operating Budget - Highlights Table 1: Composite Operating Budget 4 Table 2: Composite Operating Budget - by

2017-2018 Operating & Capital Budget Plan May 2017 Operating and Capital Budget Plan FY 2018 Operating Budget - Highlights Table 1: Composite Operating Budget 4 Table 2: Composite Operating Budget - by

Resource Allocation Charter Document

Resource Allocation Charter Document v8 Updated: September 12, 2012 Team Name Resource Allocation Executive Sponsors Business Process Owner(s) Governance Objectives - Chancellor - Provost - Vice Chancellor

Resource Allocation Charter Document v8 Updated: September 12, 2012 Team Name Resource Allocation Executive Sponsors Business Process Owner(s) Governance Objectives - Chancellor - Provost - Vice Chancellor

This budget is the first to incorporate our university community s shared goals as expressed in our new strategic plan, Building on Excellence.

Office of the President San Diego State University 5500 Campanile Drive San Diego, CA 92182 8000 Tel: 619 594 5201 Fax: 619 594 8894 September 30, 2014 Members of the university community: San Diego State

Office of the President San Diego State University 5500 Campanile Drive San Diego, CA 92182 8000 Tel: 619 594 5201 Fax: 619 594 8894 September 30, 2014 Members of the university community: San Diego State

Budget Flint Campus

2016-2017 Budget Flint Campus This page left blank intentionally. Table of Contents The University of Michigan - Flint Section One - Summary of Budgeted Revenues and Expenditures Schedule A: Summary by

2016-2017 Budget Flint Campus This page left blank intentionally. Table of Contents The University of Michigan - Flint Section One - Summary of Budgeted Revenues and Expenditures Schedule A: Summary by

FY 2019 UNIVERSITY BUDGET CALENDAR

FY 2019 UNIVERSITY BUDGET CALENDAR FY2019 UNIVERSITY BUDGET CALENDAR PLANNING: July, 2017 Office of Budget Management distributes the following to all Vice Presidents, Provost Office, and Business Representatives

FY 2019 UNIVERSITY BUDGET CALENDAR FY2019 UNIVERSITY BUDGET CALENDAR PLANNING: July, 2017 Office of Budget Management distributes the following to all Vice Presidents, Provost Office, and Business Representatives