IPSAS WORKSHOP. Key Provisions of the PFM Act 2012 and Mwongozo Code of Governance. Mountain Breeze Hotel - EMBU, 15 th -16 th June 2017

|

|

|

- Piers Howard

- 5 years ago

- Views:

Transcription

1 IPSAS WORKSHOP Key Provisions of the PFM Act 2012 and Mwongozo Code of Governance Mountain Breeze Hotel - EMBU, 15 th -16 th June 2017 Uphold. Public. Interest

2 Session Objectives The aims of the Session: To outline the significance of PFM 2012 Act, Regulations 2015 and NT circulars To discuss the Implementation Challenges Explore options towards compliance with PFM 2012 Act & Regulations 2015

3 Our understanding of PFM PFM is an essential part of the national development process. PFM includes all phases of the budget cycle, including planning, the preparation of the budget, budget execution, internal control and audit, procurement, monitoring and reporting arrangements, and external audit.

4 Our understanding of PFM The PFM reforms witnessed is meant to increase transparency and accountability in the way public finances are managed In the legal overview - the Constitution provides the framework for the PFM reforms Since introduction, there have been gains as well as challenges - the future also has opportunities

Roles,")

5 Core Areas of Good PFM System Macro-Fiscal Policy making Budget Execution, Accounting & Reporting (Audit) Roles, Responsibilities & Powers Budgeting and Budgetary Process Treasury Management

6 The Public Financial Management Process Oversight (Parliament, Constitutional and Independent Institutions & Publics) Revenue Collection Operational efficiency Increased scope Preparation and Planning Budgeting Medium Term Planning Public Expenditure Execution Accounting Control Reporting Service delivery Monitoring Macro-economic framework Evaluation Constitutional and legal framework International benchmarks

7 Legal Framework - Planning, Budgeting, Recording, Accounting and Reporting There are four main components in government Planning, Budgeting, Recording, Accounting and Reporting framework: 1. The Constitution highest in the legal hierarchy. The Constitution clarifies: relative powers of the executive & legislative branches with respect to public finance; Definition of the financial relations between national & sub-national(county) levels of government; Principles of public finance- article 201; 2. Public Finance Management Act, 2012 and Regulations main vehicle for establishing principles of public financial management. Provides the basis for budget preparation, approval, execution, control, accounting & auditing; 3. Public Audit 2015 and guidelines 2016: Underlines the public audit process and detailed instructions on public audit arrangements 4. Public Procurement and Asset Disposal Act 2015 and Regulations

8 Understanding - Planning, Budgeting, Recording, Accounting and Reporting To understand Planning, Budgeting, Recording, Accounting and Reporting, it is important to: i. Assess the basic soundness by judging the Planning, Budgeting, Recording, Accounting and Reporting system against international accepted standards and principles ; ii. iii. Know the rules governing the accounting and reporting preparation process; Who is responsible for what elements of the process; The soundness of the systems can be judged by; i. Comprehensiveness:-is the coverage of the entity operations complete? ii. iii. iv. Transparency:-how useful and clear is the reporting? Does it meet international standards? Realism:- is the system based on a realistic framework? Are the financing provisions realistic? Is there a clear separation between present and new policies? Relevant:- Timeliness?

9 Extent of IPSAS application in Government - Africa

10

11 PFM Act and Regulations Expected Gains Openness, accountability, and public participation in PFM; Equitable sharing of revenues; Equitable sharing of burdens and benefits of public borrowing ; and Observation of fiscal discipline. Social Economic development & Prosperity Accelerated & Sustained Economic growth Enhanced Debt Financing Management

12 PFM Regulations 2015 The PFM Act 2012 is to be read in conjunction with the PFM regulations, 2015, which give the guidelines on how to apply the Act. The Opportunities and Challenges lie both in the interpretation and application of the law or lack of it.

13 PFM ACT 2012 The PFM Act 2012 shall prevail in the case of any Inconsistency between it and any other legislation on the following matters: a) Preparation and submission of budget estimates, including the time for doing so; b) Preparation and submission of accounts for audit, including the time for doing so; c) Borrowing, lending and loan guarantees; d) Raising of revenue and making of expenditures; e) Banking arrangements, including opening of bank accounts and investment of moneys; f) Establishment and management of public funds; g) Establishment and dissolution of state corporations.

14 Corporate Management..is the process and structure used to direct and manage business affairs of the national/county government entities towards enhancing prosperity and good governance with the ultimate objective of realizing national long-term value while taking into account the interest of all stakeholders; Opportunities Enhanced Corporate governance (Mwongozo?) Standing committees (PFM R 18) Accounting Officers/AIE holders

15 Areas of focus for the Code Chapter One - The Board of Directors Chapter Two Transparency and Disclosure Chapter Three - Accountability, Risk Management and Internal Control Chapter Four - Ethical Leadership and Corporate Citizenship Chapter Five - Shareholder Rights and Obligations

16 Areas of Focus for the Code Chapter Six - Stakeholder Relationships Chapter Seven - Sustainability and Performance Management Chapter Eight - Compliance with Laws and Regulations Appendices - Sample Board charter & Sample Code of conduct and ethics

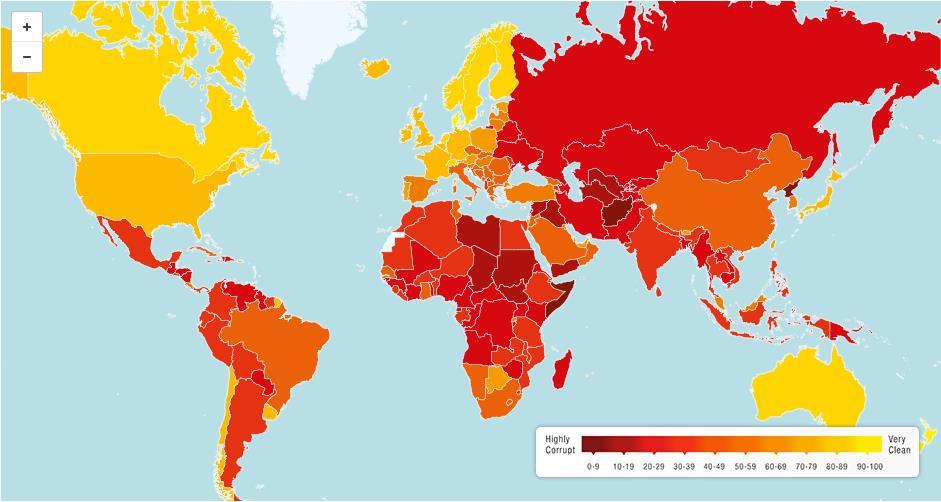

17 Potential Benefits of Mwongozo Enhance competitiveness Provide critical infrastructure, financial, commercial & social services in cost efficient manner Reduce fiscal burden/risks Improve SCs access to external sources of finance Strengthen transparency & accountability (reduce corruption) Improve economic growth

18 Potential Benefits of Mwongozo Improves the GoK ownership role Improves performance monitoring system for accountability Enhances financial & fiscal discipline Rationalizes SC Boards Enhances transparency & disclosure Ensures stakeholders protection Builds support & capacity for implementation

19 Fiscal Strategy and Macroeconomic Framework Fiscal responsibility principles. Budget Policy Statement. Macroeconomic framework. Contents of a fiscal framework. Revisions to a fiscal framework

20 Budget Preparation PFMA Opportunities: Budget preparation process. Budget guidelines Budget estimates, Appropriation Bills, Vote on Account, Approval by National Assembly

21 The Budget Process National Government Budget circular issued by National Treasury by 30 th August Budget Review and Outlook Paper (BROP) is prepared and approved by Cabinet by 30 th September. Submit BROP to Parliament 7 days upon approval by Cabinet. 6 months before the commencement of the financial year or at a later date agreed between CRA and Cabinet Secretary (finance), CRA shall submit recommendations on vertical and horizontal division of revenue. National Treasury prepares and submits the BPS to Parliament by 15 th February. Division of Revenue Bill (DoRB) and County Allocation of Revenue Bill (CARB) are submitted together with the BPS. County Government Budget Circular issued by County Treasuries by 30 th August. Budget Review and Outlook Paper (BROP) is prepared and approved by County Executive Committee (CEC) by 30 th September Submit BROP to county assembly 7 days upon approval by CEC. County Executive Committee member (planning) to submit a development plan to the county assembly for approval by 1 st September. Urban areas and cities shall prepare a strategic plan consistent with the County Fiscal Strategy Paper. County Treasury prepares and submit the County Fiscal Strategy Paper to county assembly by 15 th February.

22 The Budget Process cont d National Government Parliament to approve the annual DoRB and CARB not later than 30 days after they are submitted (Art 218). Budget Estimates and other Bills (except Finance Bill) submitted to National Assembly by 30 th April Cabinet Secretary (finance) to submit to NA comments on budget estimates of Parliament and Judiciary by 15 th May. The National Assembly approves the budget estimates and passes an Appropriation Bill and the President assents to the Bill by 30 th June. County Government Budget Estimates and other Bills (except Finance Bill) submitted to County Assembly by 30 th April County assembly approves the budget estimates and passes a county Appropriation Bill by 30 th June.

23 The Budget Process cont d National Government County Government Cabinet Secretary (finance) to make public pronouncement of budget policy highlights and revenue raising measures on a date agreed with the other EAC governments. National Assembly to approve Finance Bill not later than 90 days after the passing of the Appropriation Bill. Submit Debt Management Strategy to Parliament by 15 th February. County Executive Committee member (finance) to make a public pronouncement of revenue raising measures on the date the County Finance Bill is submitted to Parliament. County Assembly to approve Finance Bill not later than 90 days after the passing of the Appropriation Bill. Submit Debt Management Strategy to county assembly by 28 th February.

24 Budget Execution PFMA Opportunities: Budgetary control, variation, reallocations Release of Funds/Quarterly requests Commitment control Quarterly reporting

25 Management Revenues/ Receipts PFMA Opportunities Classification of revenues A.I.A and applications, Collectors and receivers, Quarterly reporting

26 Management of Grants and Donations PFMA Opportunities Definitions and administration, Accounting and reporting, Project accounts, Project selection Responsibilities of NGOs

27 Treasury and Cash management PFMA Opportunities: The Consolidated Fund, Cash and banking arrangements, Cheques & EFT, Cash Management Advisory Committee, Bank Reconciliation Imprest Management Treasury Single Account

28 Accounting and Reporting PFMA Opportunities: Form & Structure provided, Books of Account defined, Automation (IFMIS), Public Sector Accounting Standards Board (PSASB)

29 ACCOUNTING AND REPORTING: National Government National Treasury shall prepare a consolidated annual financial statement of NG and submit to the Auditor-General with copies to the CoB and CRA not later than 4 months after end of financial year. Accounting officer to prepare an annual financial statement of NG entity and submit to the Auditor-General with copies to CoB, CRA and NT not later than 3 months after the end of the financial year. Not later than 15 days after the end of each quarter, accounting officer for a NG entity will prepare a quarterly report and submit to the Cabinet Secretary for that entity with copies to CS (finance) and CoB. County Government County Treasury shall prepare a consolidated annual financial statement of CG and submit to the Auditor-General with copies to the CoB, CRA and NT not later than 4 months after end of financial year. Accounting officer to prepare an annual financial statement of CG entity and submit to the Auditor-General with copies to CoB, CRA and CT not later than 3 months after the end of the financial year. Not later than 15 days after the end of each quarter, accounting officer for a CG entity will prepare a quarterly report and submit to the County Treasury.

30 ACCOUNTING AND REPORTING: cont d National Government National Treasury will consolidate the quarterly reports of NG entities and submit the consolidated report to the National Assembly, with copies to CoB, Auditor- General and CRA not later than 45 days after end of each quarter. Not later than 3 months after the end of the financial year, a receiver of revenue shall submit a annual report of revenue received and collected in that financial year and submit to the Auditor-General with copies to NT, CoB and CRA. Not later than 3 months after the end of each financial year, each Receiver of Revenue shall submit to the Auditor- General a report of waivers and variations in taxes, fees and charges. County Government County Treasury will consolidate the quarterly reports of CG entities and submit the consolidated report to the county assembly, with copies to the CoB, CRA and NT not later than 1 month after that end of each quarter. Not later than 3 months after the end of the financial year, a receiver of revenue shall submit a annual report of revenue received and collected in that financial year and submit to the Auditor-General with copies to NT, CT, CoB and CRA. Not later than 2 months after the end of each financial year, Receiver of Revenue shall submit to the county assembly a report of waivers and variations in taxes, fees and charges.

31 ACCOUNTING AND REPORTING: cont d National Government Not later than 3 months after the end of a financial year, an administrator of a national public fund shall prepare an annual financial statement of the public fund and submit it to the Auditor- General with a copy to the Cabinet Secretary responsible for the fund. Administrator of a public fund to prepare a quarterly report of a national public fund in a form prescribed by the Public Sector Accounting Standards Board. Separate reporting by State Corporations (sections 88 and 89) Pre-election report not earlier than 4 months before polling day. Post-election report not later than 4 months after the polling day. County Government Not later than 3 months after the end of a financial year, an administrator of a county public fund shall prepare an annual financial statement of the public fund and submit it to the Auditor-General with a copy to the County Executive Committee member responsible for the fund. Administrator of a public fund to prepare a quarterly report of the county public fund not later than 15 days after the end of the each quarter and submit the report to the CT with a copy to the CoB. Separate reporting by County Corporations (sections 184 and 185)

32 Scope and Authority of IPSASs IPSAS are designed to guide the preparation and presentation of general purpose financial statements of public sector entities. Public sector entities include national (central), regional and local governments, and their component entities such as departments, agencies, boards, commissions et cetera. IPSAS do not apply to Government Business Enterprises (GBE) or also known as Commercial Public Sector Entities

33 Government Business Enterprises (GBEs) GBEs use IFRS and not IPSAS. A GBE is an entity that has meets the following criteria, a) Is an entity with the power to contract in its own name; b) Has been assigned the financial and operational authority to carry on a business; c) Sells goods and services, in the normal course of its business, to other entities at a profit or full cost recovery; d) Is not reliant on continuing government funding to be a going concern (other than purchases of outputs at arm s length); and e) Is controlled by a public sector entity.

34 General purpose financial statements General purpose financial statements are those intended to meet the needs of users who are not in a position to demand reports tailored to meet their specific information needs, e.g taxpayers and ratepayers, members of the legislature, creditors, suppliers, the media, and employees. Such reports provide information about an entity s assets, liabilities, changes in net assets/equity, revenue, expenses, and cash flows and may be presented separately or within another public document such as an annual report.

35 Objectives of general purpose financial statements To provide information that is useful for decision-making and to demonstrate the accountability of the entity for the resources entrusted to it by providing information: (a) About the sources, allocation and uses of financial resources entrusted to it; (b) On how the entity financed its activities and met its cash requirements; (c) That is useful in evaluating the entity s ability to finance its activities and to meet its liabilities and commitments; (d) About the financial condition of the entity and changes in it (e) Useful in evaluating the entity s performance in terms of service costs, efficiency and accomplishments.

36 Objectives of general purpose financial statements (cont.) General purpose financial statements also have a predictive or prospective role. They provide information useful in predicting the level of resources required for continued operations, the resources that may be generated by continued operations, and the associated risks and uncertainties. Financial reporting may also provide users with information indicating whether resources were obtained and used (a) in line with the legally adopted budget; and (b) in accordance with legal and contractual requirements, including financial limits established by appropriate legislative authorities

37 Responsibility for Financial Statements The responsibility for the preparation and presentation of financial statements varies within and across jurisdictions with some drawing a distinction between the responsibility for preparing and responsibility for approving or presenting the financial statements. Consider examples of people / positions responsible for the preparation and for the approval and presentation of financial statements of individual public entities. These may be the heads or chief executives for the individual entities and the finance minister or the head of the central finance agency (e.g., controller or accountant-general) for the government as a whole.

38 Components of Financial Statements A complete set of financial statements comprises: (a) A statement of financial position; (b) A statement of financial performance; (c) A statement of changes in net assets/equity; (d) A cash flow statement; (e) When the entity makes publicly available its approved budget, a comparison of budget and actual amounts either as a separate additional financial statement or as a budget column in the financial statements; and (f) Notes, comprising a summary of significant accounting policies and other explanatory notes.

39 Expenditure Management and Control PFMA Opportunities: Consolidated Fund Services, Accountable Documents, Procurement Plans Challenge: Compliance? What controls are there then?

40 Monitoring and Reporting PFMA Opportunities: Responsibility for monitoring, evaluation and reporting Special National Government public Funds, State Corporations additional reporting

41 Asset Management PFMA Opportunities: Inventories of Assets, Transfer of assets, Register of Assets, Losses and Write-offs Opportunities for the entities to develop and maintain assets

42 INTERNAL AUDIT AND AUDIT COMMITTEES PFMA Opportunities: Mandate of internal auditors. Compliance with professional standards and code of ethics. Independence of the internal auditor. New dawn for audit function (audit committee Guidelines issued June 2016)

43 Public Debt Management Country borrowing strategy - domestically, foreign debts vs Interest rates The country s external debt has increased from Sh billion in May 2003 to Sh1.8 trillion as at June this year. In total, the country s public debt stands at around Sh3.2 trillion. PFM required levels?

44 Intergovernmental fiscal relations Financial autonomy supported by Articles 6 and 189 of the Constitution: Art. 6 (2) The governments at the national and county levels are distinct and inter-dependent and shall conduct their mutual relations on the basis of consultation and cooperation. Art. 189 (1)(a): Government at either level shall perform its functions, and exercise its powers, in a manner that respects the functional and institutional integrity of government at the other level, and respects the constitutional status and institutions of government at the other level. Role of institutions and fiscal responsibility principles

45 Way Forward No easy answers in addressing the challenges and seizing the opportunities. Government needs to have more and better regard for the Constitution- and PFM reforms Corruption and impunity have undermined the gains expected of the reforms in the PFM Act. The functions of the Auditor General, Controller of budget should not be undermined. Fiscal reforms should be targeted at propping the economy Government should check its spending spree Government should communicate better Only then, might we start seeing the fruits of the reforms.

46 Way Forward - Questions Can Counties bring more prosperity to the people? Can public participation be made more effective? Can devolution take resources closer to the people? Can Government cut waste in spending? Can we prioritize spending on projects with catalytic value? Can we maintain macro-economic stability with low inflation, low fiscal deficit and fiscal space?

47 Conclusion Discussion Questions?

FINANCIAL MANAGEMENT FOR HIGHER EDUCATION SECTOR WORKSHOP

FINANCIAL MANAGEMENT FOR HIGHER EDUCATION SECTOR WORKSHOP Public Financial Management Systems and Guidelines HILTON HOTEL, NAIROBI, 20 th -21 st APRIL 2017 Uphold. Public. Interest Session Outline The

FINANCIAL MANAGEMENT FOR HIGHER EDUCATION SECTOR WORKSHOP Public Financial Management Systems and Guidelines HILTON HOTEL, NAIROBI, 20 th -21 st APRIL 2017 Uphold. Public. Interest Session Outline The

PUBLIC FINANCE MANAGEMENT SEMINAR. Overview of the PFM Regulations

PUBLIC FINANCE MANAGEMENT SEMINAR Overview of the PFM Regulations Mountain Breeze Hotel Embu, 28 th - 29 th September 2017 Uphold. Public. Interest Session Focus By the end of the session you will cover

PUBLIC FINANCE MANAGEMENT SEMINAR Overview of the PFM Regulations Mountain Breeze Hotel Embu, 28 th - 29 th September 2017 Uphold. Public. Interest Session Focus By the end of the session you will cover

Budget Cycle and Key Budget Documents under PFM

Budget Cycle and Key Budget Documents under PFM Stipulations of the PFM Act and Regulations (2015) on Budget Preparation, Presentation and Accountability Feedback from the Office of Controller of Budget

Budget Cycle and Key Budget Documents under PFM Stipulations of the PFM Act and Regulations (2015) on Budget Preparation, Presentation and Accountability Feedback from the Office of Controller of Budget

PUBLIC SECTOR ACCOUNTING DEVELOPMENTS. Credibility. Professionalism. AccountAbility

PUBLIC SECTOR ACCOUNTING DEVELOPMENTS Credibility. Professionalism. AccountAbility Session Objectives Legal framework of public sector accounting standards PSASB (K) and ICPAK PSASB s strategic direction

PUBLIC SECTOR ACCOUNTING DEVELOPMENTS Credibility. Professionalism. AccountAbility Session Objectives Legal framework of public sector accounting standards PSASB (K) and ICPAK PSASB s strategic direction

PREPARATION AND PRESENTATION OF PUBLIC SECTOR FINANCIAL STATEMENTS

PREPARATION AND PRESENTATION OF PUBLIC SECTOR FINANCIAL STATEMENTS APPLICATION OF IPSAS (CASH/ACCRUAL) CPA MUMO Credibility. Professionalism. AccountAbility Presentation Outline Legal foundation Constitution

PREPARATION AND PRESENTATION OF PUBLIC SECTOR FINANCIAL STATEMENTS APPLICATION OF IPSAS (CASH/ACCRUAL) CPA MUMO Credibility. Professionalism. AccountAbility Presentation Outline Legal foundation Constitution

PUBLIC FINANCE MANAGEMENT ACT

LAWS OF KENYA PUBLIC FINANCE MANAGEMENT ACT NO. 18 OF 2012 Revised Edition 2016 [2013] Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org [Rev.

LAWS OF KENYA PUBLIC FINANCE MANAGEMENT ACT NO. 18 OF 2012 Revised Edition 2016 [2013] Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org [Rev.

PUBLIC FINANCE MANAGEMENT ACT

LAWS OF KENYA PUBLIC FINANCE MANAGEMENT ACT CHAPTER 412C Revised Edition 2012 Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org [Issue 1]

LAWS OF KENYA PUBLIC FINANCE MANAGEMENT ACT CHAPTER 412C Revised Edition 2012 Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org [Issue 1]

Introduction. Accounting Standards for the Public Sector

Introduction Accounting Standards for the Public Sector The International Public Sector Accounting Standards Board (the IPSASB) of the International Federation of Accountants (IFAC) develops accounting

Introduction Accounting Standards for the Public Sector The International Public Sector Accounting Standards Board (the IPSASB) of the International Federation of Accountants (IFAC) develops accounting

The Public Financial Management Bill, 2012 THE PUBLIC FINANCIAL MANAGEMENT BILL, 2012 ARRANGEMENT OF CLAUSES PART I PRELIMINARY

Clause THE PUBLIC FINANCIAL MANAGEMENT BILL, 2012 1 Short title and commencement. 2 Interpretation. 3 Object of this Act. ARRANGEMENT OF CLAUSES PART I PRELIMINARY 4 Declaration of entities as National

Clause THE PUBLIC FINANCIAL MANAGEMENT BILL, 2012 1 Short title and commencement. 2 Interpretation. 3 Object of this Act. ARRANGEMENT OF CLAUSES PART I PRELIMINARY 4 Declaration of entities as National

IPSAS WORKSHOP Preparation of Financial Statements Under various IPSAS Mountain Breeze Hotel - EMBU, 15th -16th June 2017

IPSAS WORKSHOP Preparation of Financial Statements Under various IPSAS Mountain Breeze Hotel - EMBU, 15 th -16 th June 2017 Uphold. Public. Interest PRESENTATION OF BUDGET INFORMATION () Uphold. Public.

IPSAS WORKSHOP Preparation of Financial Statements Under various IPSAS Mountain Breeze Hotel - EMBU, 15 th -16 th June 2017 Uphold. Public. Interest PRESENTATION OF BUDGET INFORMATION () Uphold. Public.

Government Budgeting Cycle; Lessons & Opportunities for Participation by Accountants. CPA Andrew Rori

THE 4 th PUBLIC SECTOR ACCOUNTANTS CONFERENCE Government Budgeting Cycle; Lessons & Opportunities for Participation by Accountants CPA Andrew Rori Sarova Whitesands & Beach Hotel, Mombasa County, Kenya:

THE 4 th PUBLIC SECTOR ACCOUNTANTS CONFERENCE Government Budgeting Cycle; Lessons & Opportunities for Participation by Accountants CPA Andrew Rori Sarova Whitesands & Beach Hotel, Mombasa County, Kenya:

BUDGET PREPARATION MODULE

Public Financial Management BUDGET PREPARATION MODULE P A R T I C I P ANT BOOK October 2014 REPUBLIC OF KENYA NATIONAL TREASURY KENYA SCHOOL OF GOVERNMENT REPUBLIC OF KENYA MINISTRY OF DEVOLUTION AND PLANNING

Public Financial Management BUDGET PREPARATION MODULE P A R T I C I P ANT BOOK October 2014 REPUBLIC OF KENYA NATIONAL TREASURY KENYA SCHOOL OF GOVERNMENT REPUBLIC OF KENYA MINISTRY OF DEVOLUTION AND PLANNING

Financial Reporting Under the Cash Basis of Accounting

IFAC Public Sector Committee Cash Basis IPSAS Issued January 2003 Updated 2006 International Public Sector Accounting Standard Financial Reporting Under the Cash Basis of Accounting International Public

IFAC Public Sector Committee Cash Basis IPSAS Issued January 2003 Updated 2006 International Public Sector Accounting Standard Financial Reporting Under the Cash Basis of Accounting International Public

PUBLIC FINANCE MANAGEMENT WORKSHOP

PUBLIC FINANCE MANAGEMENT WORKSHOP NYANZA BRANCH IFMIS AN ENABLER OR INHIBITOR 28 th 29 th August 2018 Presented by : Hillary Onami, Manager, Devolution & Branches Public Policy and Research, ICPAK @ Nyakoe

PUBLIC FINANCE MANAGEMENT WORKSHOP NYANZA BRANCH IFMIS AN ENABLER OR INHIBITOR 28 th 29 th August 2018 Presented by : Hillary Onami, Manager, Devolution & Branches Public Policy and Research, ICPAK @ Nyakoe

The Judiciary. Finance Policy and Procedures Manual

Finance Policy and Procedures Manual Foreword I am pleased to present the Finance Policy and Procedure Manual of the Judiciary. This manual is expected to be a key reference guide for the practices, policies

Finance Policy and Procedures Manual Foreword I am pleased to present the Finance Policy and Procedure Manual of the Judiciary. This manual is expected to be a key reference guide for the practices, policies

Public Expenditure and Financial Accountability Baseline Report. Central Provincial Government

Public Expenditure and Financial Accountability Baseline Report Central Provincial Government 1 Table of Contents Summary Assessment... 4 (i) Integrated assessment of PFM performance... 4 (ii) Assessment

Public Expenditure and Financial Accountability Baseline Report Central Provincial Government 1 Table of Contents Summary Assessment... 4 (i) Integrated assessment of PFM performance... 4 (ii) Assessment

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE PRESENTATION OF FINANCIAL STATEMENTS (GRAP 1) Issued by the Accounting Standards Board February 2010 Acknowledgement The

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE PRESENTATION OF FINANCIAL STATEMENTS (GRAP 1) Issued by the Accounting Standards Board February 2010 Acknowledgement The

Keeping you on the know Implementation of International Public Sector Accounting Standards (IPSAS) in Kenya

in Kenya") Keeping you on the know Implementation of International Public Sector Accounting Standards (IPSAS) in Kenya 25 April 2018 - Presented by CPA Samuel Kirenge CPA. Samuel Kirenge Senior Manager, Deloitte,

Keeping you on the know Implementation of International Public Sector Accounting Standards (IPSAS) in Kenya 25 April 2018 - Presented by CPA Samuel Kirenge CPA. Samuel Kirenge Senior Manager, Deloitte,

2017 FIRE AWARDS FEEDBACK FOR PUBLIC SECTOR ENTITIES. IPSAS Workshop April 2018

2017 FIRE AWARDS FEEDBACK FOR PUBLIC SECTOR ENTITIES IPSAS Workshop April 2018 Overview of the Presentation Introduction Scoring Criteria (weighting) Evaluation Findings o o o IPSAS Cash IPSAS Accrual

2017 FIRE AWARDS FEEDBACK FOR PUBLIC SECTOR ENTITIES IPSAS Workshop April 2018 Overview of the Presentation Introduction Scoring Criteria (weighting) Evaluation Findings o o o IPSAS Cash IPSAS Accrual

Public Finance Management Workshop

Public Finance Management Workshop INTEGRATED FINANCIAL MANAGEMENT INFORMATION SYSTEM (IFMIS CPA Andrew Rori City Blue Hotel & Suites, Mombasa 9th 10th August, 2018 Uphold. Public. Interest Session Outline

Public Finance Management Workshop INTEGRATED FINANCIAL MANAGEMENT INFORMATION SYSTEM (IFMIS CPA Andrew Rori City Blue Hotel & Suites, Mombasa 9th 10th August, 2018 Uphold. Public. Interest Session Outline

Governance for Improved Service Delivery Region. Program-for-Results Program ID. Republic of Kenya Implementing Agency

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM-FOR-RESULTS INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.:PIDC0091373 (The

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM-FOR-RESULTS INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.:PIDC0091373 (The

THE REPUBLIC OF KENYA CONSOLIDATED FINANCIAL STATEMENTS MINISTRIES, DEPARTMENTS AND AGENCIES FOR THE FINANCIAL YEAR ENDED 30 TH JUNE 2016

THE REPUBLIC OF KENYA CONSOLIDATED FINANCIAL STATEMENTS MINISTRIES, DEPARTMENTS AND AGENCIES FOR THE FINANCIAL YEAR ENDED 30 TH JUNE 2016 Unaudited revised March 2017 TABLE OF CONTENTS PAGE 1. COMMENTARY

THE REPUBLIC OF KENYA CONSOLIDATED FINANCIAL STATEMENTS MINISTRIES, DEPARTMENTS AND AGENCIES FOR THE FINANCIAL YEAR ENDED 30 TH JUNE 2016 Unaudited revised March 2017 TABLE OF CONTENTS PAGE 1. COMMENTARY

PUBLIC FINANCE MANAGEMENT SEMINAR

PUBLIC FINANCE MANAGEMENT SEMINAR Linking Public Sector Planning to Budgeting Mountain Breeze Hotel Embu, 28 th - 29 th September 2017 Uphold. Public. Interest Session Content Linking Public Sector Planning

PUBLIC FINANCE MANAGEMENT SEMINAR Linking Public Sector Planning to Budgeting Mountain Breeze Hotel Embu, 28 th - 29 th September 2017 Uphold. Public. Interest Session Content Linking Public Sector Planning

PARLIAMENTARY SERVICE COMMISSION. Parliamentary Budget Office. Overall Analysis of the 2013/14 Budget

PARLIAMENTARY SERVICE COMMISSION Parliamentary Budget Office Overall Analysis of the 2013/14 Budget Disclaimer The Parliamentary Budget Office (PBO) is a non-partisan professional office of the Parliament

PARLIAMENTARY SERVICE COMMISSION Parliamentary Budget Office Overall Analysis of the 2013/14 Budget Disclaimer The Parliamentary Budget Office (PBO) is a non-partisan professional office of the Parliament

COUNTY GOVERNMENTS PUBLIC FINANCE MANAGEMENT Transition ACT

LAWS OF KENYA COUNTY GOVERNMENTS PUBLIC FINANCE MANAGEMENT Transition ACT Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org County Governments

LAWS OF KENYA COUNTY GOVERNMENTS PUBLIC FINANCE MANAGEMENT Transition ACT Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org County Governments

TOPIC: Transparency and Comparability in Financial Reporting by Public Sector Entities in Kenya

PUBLIC FINANCIAL MANAGEMENT CONFERENCE 2016 TOPIC: Transparency and Comparability in Financial Reporting by Public Sector Entities in Kenya Wednesday, 6 th April 2016 Credibility. Professionalism. AccountAbility

PUBLIC FINANCIAL MANAGEMENT CONFERENCE 2016 TOPIC: Transparency and Comparability in Financial Reporting by Public Sector Entities in Kenya Wednesday, 6 th April 2016 Credibility. Professionalism. AccountAbility

Strengthening Medium Term Budget Frameworks

Strengthening Medium Term Budget Frameworks International Consortium on Governmental Financial Management Washington DC, 6 December, 2016 Taz Chaponda, Fiscal Affairs Department Outline Definitions Medium-Term

Strengthening Medium Term Budget Frameworks International Consortium on Governmental Financial Management Washington DC, 6 December, 2016 Taz Chaponda, Fiscal Affairs Department Outline Definitions Medium-Term

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) Issued September 2014 and incorporates amendments to 31 May 2017 other than consequential

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) Issued September 2014 and incorporates amendments to 31 May 2017 other than consequential

BUDGET LAW. (Revised edition) CHAPTER ONE. General provision. Article 1. Purpose of the Law

CHAPTER ONE. General provision. Article 1. Purpose of the Law") BUDGET LAW (Revised edition) CHAPTER ONE General provision Article 1. Purpose of the Law 1.1. The purpose of this Law is to establish principles, systems, composition and classification of the budget,

BUDGET LAW (Revised edition) CHAPTER ONE General provision Article 1. Purpose of the Law 1.1. The purpose of this Law is to establish principles, systems, composition and classification of the budget,

GOVERNMENT OF KENYA STATE CORPORATIONS, SEMI AUTONOMOUS GOVERNMENT AGENCIES AND PUBLIC FUNDS CONSOLIDATED FINANCIAL STATEMENTS

GOVERNMENT OF KENYA STATE CORPORATIONS, SEMI AUTONOMOUS GOVERNMENT AGENCIES AND PUBLIC FUNDS CONSOLIDATED FINANCIAL STATEMENTS FOR THE FINANCIAL YEAR ENDED 30 th JUNE 2016 Unaudited- revised March 2017

GOVERNMENT OF KENYA STATE CORPORATIONS, SEMI AUTONOMOUS GOVERNMENT AGENCIES AND PUBLIC FUNDS CONSOLIDATED FINANCIAL STATEMENTS FOR THE FINANCIAL YEAR ENDED 30 th JUNE 2016 Unaudited- revised March 2017

Public Sector Audit Accounting for Government Expenditure and Value for Money

Public Sector Audit Accounting for Government Expenditure and Value for Money Presentation by: CPA Sylvester Kiini Deputy Auditor General Office of the Auditor-General, Kenya Uphold public interest Quote

Public Sector Audit Accounting for Government Expenditure and Value for Money Presentation by: CPA Sylvester Kiini Deputy Auditor General Office of the Auditor-General, Kenya Uphold public interest Quote

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures Presentation by: By Mr. Abdullatif Essajee Wednesday, 18 th October 2017 Uphold public interest IPSAS 1: Presentation

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures Presentation by: By Mr. Abdullatif Essajee Wednesday, 18 th October 2017 Uphold public interest IPSAS 1: Presentation

Kingdom of Swaziland. Public Finance Management Bill

Kingdom of Swaziland Public Finance Management Bill CHAPTER ONE: INTERPRETATION, OBJECT, APPLICATION AND AMENDMENT OF THIS ACT 1 Short title This Act may be cited as the Public Finance Management Act 2010.

Kingdom of Swaziland Public Finance Management Bill CHAPTER ONE: INTERPRETATION, OBJECT, APPLICATION AND AMENDMENT OF THIS ACT 1 Short title This Act may be cited as the Public Finance Management Act 2010.

PUBLIC FINANCE MANAGEMENT CONFERENCE FOR AFRICA

PUBLIC FINANCE MANAGEMENT CONFERENCE FOR AFRICA Public Financial Management and Accountability Reforms - The Kenyan Scenario PRIDE INN PARADISE HOTEL, MOMBASA, 19 th -21 st APRIL 2017 Uphold. Public. Interest

PUBLIC FINANCE MANAGEMENT CONFERENCE FOR AFRICA Public Financial Management and Accountability Reforms - The Kenyan Scenario PRIDE INN PARADISE HOTEL, MOMBASA, 19 th -21 st APRIL 2017 Uphold. Public. Interest

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

IPSAS WORKSHOP. The benefits, Challenges and way forward of IFMIS in Kenya. Golf Hotel - Kakamega, 18 th -19 th July Uphold. Public.

IPSAS WORKSHOP The benefits, Challenges and way forward of IFMIS in Kenya Golf Hotel - Kakamega, 18 th -19 th July 2017 Uphold. Public. Interest Outline of Presentation Introduction to PFMS - definitions

IPSAS WORKSHOP The benefits, Challenges and way forward of IFMIS in Kenya Golf Hotel - Kakamega, 18 th -19 th July 2017 Uphold. Public. Interest Outline of Presentation Introduction to PFMS - definitions

Treasury Board of Canada Secretariat

Treasury Board of Canada Secretariat 2007 08 A Report on Plans and Priorities The Honourable Vic Toews President of the Treasury Board Table of Contents Section I: Overview... 1 Minister s Message...

Treasury Board of Canada Secretariat 2007 08 A Report on Plans and Priorities The Honourable Vic Toews President of the Treasury Board Table of Contents Section I: Overview... 1 Minister s Message...

Status update on IFRSs, IPSASs and Integrated Reporting in Kenya

Status update on IFRSs, IPSASs and Integrated Reporting in Kenya Presentation by:- CPA Hesbon Omollo Financial Reporting Workshop Uphold public interest IFRS Overview Why IFRSs? The International Accounting

Status update on IFRSs, IPSASs and Integrated Reporting in Kenya Presentation by:- CPA Hesbon Omollo Financial Reporting Workshop Uphold public interest IFRS Overview Why IFRSs? The International Accounting

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

KENYA GAZETTE SUPPLEMENT

SPECIAL ISSUE Kenya Gazette Supplement No. 15 (Acts No. 8) REPUBLIC OF KENYA KENYA GAZETTE SUPPLEMENT ACTS, 2013 NAIROBI, 25th January, 2013 CONTENT Act PAGE The County Governments Public Finance Management

SPECIAL ISSUE Kenya Gazette Supplement No. 15 (Acts No. 8) REPUBLIC OF KENYA KENYA GAZETTE SUPPLEMENT ACTS, 2013 NAIROBI, 25th January, 2013 CONTENT Act PAGE The County Governments Public Finance Management

Submission on Draft Money Bills Amendment Procedures and Related Matters Bill

Financial and Fiscal Commission Submission on Draft Money Bills Amendment Procedures and Related Matters Bill 2008 For an Equitable Sharing of National Revenue 1. Introduction 1.0.1 The Financial and Fiscal

Financial and Fiscal Commission Submission on Draft Money Bills Amendment Procedures and Related Matters Bill 2008 For an Equitable Sharing of National Revenue 1. Introduction 1.0.1 The Financial and Fiscal

IPSAS WORKSHOP. Preparation of Financial Statements Under various IPSAS Presentation of Budget Information (IPSAS 24)

") IPSAS WORKSHOP Preparation of Financial Statements Under various IPSAS Presentation of Budget Information () MERICA HOTEL NAKURU 27 th 28 th June 2017 Uphold. Public. Interest Presentation of Budget Information

IPSAS WORKSHOP Preparation of Financial Statements Under various IPSAS Presentation of Budget Information () MERICA HOTEL NAKURU 27 th 28 th June 2017 Uphold. Public. Interest Presentation of Budget Information

Fundamental Principles of Financial Auditing

ISSAI 200 Endorsement Version ISSAI 200 Fundamental Principles of Financial Auditing The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme

ISSAI 200 Endorsement Version ISSAI 200 Fundamental Principles of Financial Auditing The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme

Public Financial Management

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

THE BUDGET ACT, 2014 ARRANGEMENT OF SECTIONS PART I PRELIMINARY PROVISIONS PART II MACROECONOMIC AND FISCAL FRAMEWORK

THE UNITED REPUBLIC OF TANZANIA ISSN 0856-35X BILL SUPPLEMENT No. 13 31 st October, 2014 to the Gazette of the United Republic of Tanzania No. 44. Vol. 95 dated 31 st October, 2014 Printed by the Government

THE UNITED REPUBLIC OF TANZANIA ISSN 0856-35X BILL SUPPLEMENT No. 13 31 st October, 2014 to the Gazette of the United Republic of Tanzania No. 44. Vol. 95 dated 31 st October, 2014 Printed by the Government

Kenya School of Government Centre for Devolution Studies Working Paper Series WORKING PAPER 2

Kenya School of Government Centre for Devolution Studies Working Paper Series KENYA DEVOLUTION WORKING PAPER 2 FEBRUARY 2015 Basic Requirements for Public Participation in Kenya s Legal Framework OBJECTIVE:

Kenya School of Government Centre for Devolution Studies Working Paper Series KENYA DEVOLUTION WORKING PAPER 2 FEBRUARY 2015 Basic Requirements for Public Participation in Kenya s Legal Framework OBJECTIVE:

FINANCIAL MANAGEMENT OF PARLIAMENT BILL

REPUBLIC OF SOUTH AFRICA FINANCIAL MANAGEMENT OF PARLIAMENT BILL (As amended by the Select Committee on Financial National Council of Provinces) (The English text is the offıcial text of the Bill) (SELECT

REPUBLIC OF SOUTH AFRICA FINANCIAL MANAGEMENT OF PARLIAMENT BILL (As amended by the Select Committee on Financial National Council of Provinces) (The English text is the offıcial text of the Bill) (SELECT

Module 2 Planning and Budgeting Processes

Module 2 Planning and Budgeting Processes 7 HOURS By the end of this module, the participants will have: LEARNING OUTCOMES discussed the process of budget decision-making in Kenya, focusing on public participation;

Module 2 Planning and Budgeting Processes 7 HOURS By the end of this module, the participants will have: LEARNING OUTCOMES discussed the process of budget decision-making in Kenya, focusing on public participation;

IMPROVING BUDGET TRANSPARENCY IN SOUTH AFRICA

IMPROVING BUDGET TRANSPARENCY IN SOUTH AFRICA FISCAL TRANSPARENCY AND ACCOUNTABILITY MEETING - MOSCOW, RUSSIA Presented by: Dr Kay Brown Chief Director, Expenditure Planning 29 May 2014 Presentation outline

IMPROVING BUDGET TRANSPARENCY IN SOUTH AFRICA FISCAL TRANSPARENCY AND ACCOUNTABILITY MEETING - MOSCOW, RUSSIA Presented by: Dr Kay Brown Chief Director, Expenditure Planning 29 May 2014 Presentation outline

FINANCE DEPARTMENT S ANNUAL REPORT

FINANCE DEPARTMENT S ANNUAL REPORT FRAMING OUR FINANCIAL FUTURE This report focuses on how the City of Guelph s Finance Department plays an integral role in Framing Our Financial Future. It will discuss

FINANCE DEPARTMENT S ANNUAL REPORT FRAMING OUR FINANCIAL FUTURE This report focuses on how the City of Guelph s Finance Department plays an integral role in Framing Our Financial Future. It will discuss

EUROPEAN UNION ACCOUNTING RULE 16 PRESENTATION OF BUDGET INFORMATION IN ANNUAL ACCOUNTS

EUROPEAN UNION ACCOUNTING RULE 16 PRESENTATION OF BUDGET INFORMATION Page 2 of 9 I N D E X 1. Introduction... 3 1.1 Reasons for issuing this accounting rule... 3 1.2 Applicability... 3 1.3 Disclosure...

EUROPEAN UNION ACCOUNTING RULE 16 PRESENTATION OF BUDGET INFORMATION Page 2 of 9 I N D E X 1. Introduction... 3 1.1 Reasons for issuing this accounting rule... 3 1.2 Applicability... 3 1.3 Disclosure...

COMMENTS ON STANDARDS OF GENERALLY ACCEPTED MUNICIPAL ACCOUNTING PRACTICE (GAMAP)

") COMMENTS ON STANDARDS OF GENERALLY ACCEPTED MUNICIPAL ACCOUNTING PRACTICE (GAMAP) Introduction The Accounting Standards Board (Board) approved the exposure of the Standards of GAMAP, at the Board meeting

COMMENTS ON STANDARDS OF GENERALLY ACCEPTED MUNICIPAL ACCOUNTING PRACTICE (GAMAP) Introduction The Accounting Standards Board (Board) approved the exposure of the Standards of GAMAP, at the Board meeting

Service Performance Reporting

Service Performance Reporting Issued November 2017 This Standard was issued on 9 November 2017 by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section 12 of the

Service Performance Reporting Issued November 2017 This Standard was issued on 9 November 2017 by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section 12 of the

Government Gazette REPUBLIC OF SOUTH AFRICA. Vol. 478 Cape Town 1 April 2005 No

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 478 Cape Town 1 April 2005 No. 27443 THE PRESIDENCY No. 291 1 April 2005 It is hereby notified that the President has assented to the following Act, which

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 478 Cape Town 1 April 2005 No. 27443 THE PRESIDENCY No. 291 1 April 2005 It is hereby notified that the President has assented to the following Act, which

Government accountability

Government accountability Main points... 364 Introduction... 365 Key elements of sound accountability... 365 Accountability of Saskatchewan Government... 367 Background... 367 Need plan and performance

Government accountability Main points... 364 Introduction... 365 Key elements of sound accountability... 365 Accountability of Saskatchewan Government... 367 Background... 367 Need plan and performance

The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities

IFAC Board Final Pronouncement Exposure Draft October 2014 October 2011 Comments due: February 29, 2012 The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities This document

IFAC Board Final Pronouncement Exposure Draft October 2014 October 2011 Comments due: February 29, 2012 The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities This document

FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS

42 FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS. FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS BACKGROUND.1 This Chapter describes the results of our government-wide

42 FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS. FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS BACKGROUND.1 This Chapter describes the results of our government-wide

4/7/2015. Group. Governance and Legislation

Group 3 Governance and Legislation DIPLOMA IN PUBLIC ACCOUNTABILITY MINIMUM MUNICIPAL COMPETENCY PROGRAMME Karel van der Molen Module 2 Intergovernmental Fiscal Relations, Legislation and Policies affecting

Group 3 Governance and Legislation DIPLOMA IN PUBLIC ACCOUNTABILITY MINIMUM MUNICIPAL COMPETENCY PROGRAMME Karel van der Molen Module 2 Intergovernmental Fiscal Relations, Legislation and Policies affecting

The Applicability of IPSASs

Exposure Draft 56 July 2015 Comments due: November 30, 2015 Proposed International Public Sector Accounting Standard and Recommended Practice Guideline The Applicability of IPSASs This document was developed

Exposure Draft 56 July 2015 Comments due: November 30, 2015 Proposed International Public Sector Accounting Standard and Recommended Practice Guideline The Applicability of IPSASs This document was developed

Linking Public Sector Planning to Budgeting

Linking Public Sector Planning to Budgeting PFM Seminar, ICPAK Central Rift Branch By Fred Riaga Chief Manager - Public Policy & Research Division - ICPAK THURSDAY, 21 ST SEPTEMBER 2017 PLANNING BUDGETING

Linking Public Sector Planning to Budgeting PFM Seminar, ICPAK Central Rift Branch By Fred Riaga Chief Manager - Public Policy & Research Division - ICPAK THURSDAY, 21 ST SEPTEMBER 2017 PLANNING BUDGETING

Unit Standard : Apply the principles of budgeting within a municipality. Karel van der Molen

Unit Standard 116345: Apply the principles of budgeting within a municipality Karel van der Molen Group The full programme 1. Strategic Management; Budgeting Implementation & Performance Management 2.

Unit Standard 116345: Apply the principles of budgeting within a municipality Karel van der Molen Group The full programme 1. Strategic Management; Budgeting Implementation & Performance Management 2.

Examination I: Governmental Environment

Examination I: Governmental Environment I: Organization, Structure and Authority of Government (15%) A. Demonstrate an understanding of the levels of government, including: 1. The three levels of government:

Examination I: Governmental Environment I: Organization, Structure and Authority of Government (15%) A. Demonstrate an understanding of the levels of government, including: 1. The three levels of government:

QUESTIONNAIRE ON FISCAL INSTITUTIONS [COUNTRY]

![QUESTIONNAIRE ON FISCAL INSTITUTIONS [COUNTRY]](/thumbs/95/123560242.jpg "QUESTIONNAIRE ON FISCAL INSTITUTIONS [COUNTRY]") QUESTIONNAIRE ON FISCAL INSTITUTIONS [COUNTRY] This questionnaire is designed to gather basic information on fiscal institutions and practices as a basis for review of a country's fiscal management system

QUESTIONNAIRE ON FISCAL INSTITUTIONS [COUNTRY] This questionnaire is designed to gather basic information on fiscal institutions and practices as a basis for review of a country's fiscal management system

COMMISSION ON REVENUE ALLOCATION

COMMISSION ON REVENUE ALLOCATION Promoting an equitable society RECOMMENDATION ON THE SHARING OF REVENUE RAISED NATIONALLY BETWEEN THE NATIONAL GOVERNMENT AND THE COUNTY GOVERNMENTS FOR THE FINANCIAL YEAR

COMMISSION ON REVENUE ALLOCATION Promoting an equitable society RECOMMENDATION ON THE SHARING OF REVENUE RAISED NATIONALLY BETWEEN THE NATIONAL GOVERNMENT AND THE COUNTY GOVERNMENTS FOR THE FINANCIAL YEAR

Decentralization and Public Expenditure Analysis and Management

Decentralization and Public Expenditure Analysis and Management Dana Weist Senior Public Sector Specialist, PRMPS dweist@worldbank.org 23 May 2002 Page 1 Decentralization: A World-Wide Phenomenon Underway

Decentralization and Public Expenditure Analysis and Management Dana Weist Senior Public Sector Specialist, PRMPS dweist@worldbank.org 23 May 2002 Page 1 Decentralization: A World-Wide Phenomenon Underway

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Accounting Standards Board P O Box 74219 Lynnwood Ridge 0040 Fax: +27

STAR Contribution to Indonesia PFM

State Accountability Revitalization (RRP INO 38354) STAR Contribution to Indonesia PFM Public financial management (PFM) includes all phases of the budget cycle, including the preparation of the budget,

State Accountability Revitalization (RRP INO 38354) STAR Contribution to Indonesia PFM Public financial management (PFM) includes all phases of the budget cycle, including the preparation of the budget,

CHAPTER V. DEVELOPING AN ACTION PLAN: RECOMMENDATIONS FOR ACHIEVING FISCAL SUSTAINABILITY AND IMPROVING BUDGETARY MANAGEMENT IN BELARUS.

CHAPTER V. DEVELOPING AN ACTION PLAN: RECOMMENDATIONS FOR ACHIEVING FISCAL SUSTAINABILITY AND IMPROVING BUDGETARY MANAGEMENT IN BELARUS. 5.1 The previous chapters have focused on key issues that underpin

CHAPTER V. DEVELOPING AN ACTION PLAN: RECOMMENDATIONS FOR ACHIEVING FISCAL SUSTAINABILITY AND IMPROVING BUDGETARY MANAGEMENT IN BELARUS. 5.1 The previous chapters have focused on key issues that underpin

Service Performance Reporting

Service Performance Reporting Issued [month/year] This Standard was issued on [Date] by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section 12 of the Financial

Service Performance Reporting Issued [month/year] This Standard was issued on [Date] by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section 12 of the Financial

Draft Policy Brief: Revised Indicator 9a for the Global Partnership Monitoring Framework

Draft Policy Brief: Revised Indicator 9a for the Global Partnership Monitoring Framework March 2015 This policy brief has been produced with the kind assistance of the European Union and the German Ministry

Draft Policy Brief: Revised Indicator 9a for the Global Partnership Monitoring Framework March 2015 This policy brief has been produced with the kind assistance of the European Union and the German Ministry

MUNICIPAL FISCAL POWERS AND FUNCTIONS BILL

REPUBLIC OF SOUTH AFRICA MUNICIPAL FISCAL POWERS AND FUNCTIONS BILL (As amended by the Portfolio Committee on Finance (National Assembly)) (The English text is the offıcial text of the Bill) (MINISTER

REPUBLIC OF SOUTH AFRICA MUNICIPAL FISCAL POWERS AND FUNCTIONS BILL (As amended by the Portfolio Committee on Finance (National Assembly)) (The English text is the offıcial text of the Bill) (MINISTER

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EVENTS AFTER THE REPORTING DATE () Issued by the Accounting Standards Board February 2010 Acknowledgement The Standard of

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EVENTS AFTER THE REPORTING DATE () Issued by the Accounting Standards Board February 2010 Acknowledgement The Standard of

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE CONSTRUCTION CONTRACTS (GRAP 11)

") ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE CONSTRUCTION CONTRACTS (GRAP 11) Issued by the Accounting Standards Board December 2006 Acknowledgment This Standard of Generally

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE CONSTRUCTION CONTRACTS (GRAP 11) Issued by the Accounting Standards Board December 2006 Acknowledgment This Standard of Generally

PFMA Introduction CPD Public Sector April 2018

PFMA Introduction CPD Public Sector April 2018 PFMA - INTRODUCTION 2 PFMA - OBJECTIVE Reasons for the ACT: RDP: maximise service delivery Limited resources vs. 'Unlimited' demands Satisfy constitutional

PFMA Introduction CPD Public Sector April 2018 PFMA - INTRODUCTION 2 PFMA - OBJECTIVE Reasons for the ACT: RDP: maximise service delivery Limited resources vs. 'Unlimited' demands Satisfy constitutional

I. General Provisions... 1 Article 1. Purpose... 1 Article 2. Definitions... 1

TABLE OF CONTENTS I. General Provisions... 1 Article 1. Purpose... 1 Article 2. Definitions... 1 II. Budget Content and Planning... 3 Article 3. Fiscal Year and Temporary Financing... 3 Article 4. Passage

TABLE OF CONTENTS I. General Provisions... 1 Article 1. Purpose... 1 Article 2. Definitions... 1 II. Budget Content and Planning... 3 Article 3. Fiscal Year and Temporary Financing... 3 Article 4. Passage

RELATIONSHIP BETWEEN THE BUDGET AND THE IDP 28 FEBRUARY 2017

RELATIONSHIP BETWEEN THE BUDGET AND THE IDP 28 FEBRUARY 2017 1 Contents Introduction Legislative Requirements Inc. MSCOA Why MSCOA Local Government Accountability Cycle Budget Process and linkage to IDP

RELATIONSHIP BETWEEN THE BUDGET AND THE IDP 28 FEBRUARY 2017 1 Contents Introduction Legislative Requirements Inc. MSCOA Why MSCOA Local Government Accountability Cycle Budget Process and linkage to IDP

Pre-Proposal Conference on Web-based RMS:

Pre-Proposal Conference on Web-based RMS: Presentation on KRB-F Work Planning, Reporting Procedures; & Proposed Web-based RMS Presented on 4 th January 2019 by: Planning & Programming Dept. of KRB OUTLINE

Pre-Proposal Conference on Web-based RMS: Presentation on KRB-F Work Planning, Reporting Procedures; & Proposed Web-based RMS Presented on 4 th January 2019 by: Planning & Programming Dept. of KRB OUTLINE

ACCOUNTING STANDARDS BOARD

ACCOUNTING STANDARDS BOARD THE CONCEPTUAL FRAMEWORK FOR GENERAL PURPOSE FINANCIAL REPORTING Issued by the Accounting Standards Board Acknowledgement The Conceptual Framework for General Purpose Financial

ACCOUNTING STANDARDS BOARD THE CONCEPTUAL FRAMEWORK FOR GENERAL PURPOSE FINANCIAL REPORTING Issued by the Accounting Standards Board Acknowledgement The Conceptual Framework for General Purpose Financial

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE REVENUE FROM NON-EXCHANGE TRANSACTIONS (TAXES AND TRANSFERS) (GRAP 23)

(GRAP 23)") ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE REVENUE FROM NON-EXCHANGE TRANSACTIONS (TAXES AND TRANSFERS) (GRAP 23) Issued by the Accounting Standards Board February

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE REVENUE FROM NON-EXCHANGE TRANSACTIONS (TAXES AND TRANSFERS) (GRAP 23) Issued by the Accounting Standards Board February

The Effects of Changes in Foreign Exchange Rates

International Public Sector Accounting Standards Board IPSAS 4 Issued January 2007 International Public Sector Accounting Standard The Effects of Changes in Foreign Exchange Rates International Public

International Public Sector Accounting Standards Board IPSAS 4 Issued January 2007 International Public Sector Accounting Standard The Effects of Changes in Foreign Exchange Rates International Public

PUBLIC FINANCE MANAGEMENT CONFERENCE FOR AFRICA

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA PUBLIC FINANCE MANAGEMENT CONFERENCE FOR AFRICA Demystifying Budget Implementation & Monitoring Presented by : Naomi Rono Senior Policy Analyst ICPAK

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA PUBLIC FINANCE MANAGEMENT CONFERENCE FOR AFRICA Demystifying Budget Implementation & Monitoring Presented by : Naomi Rono Senior Policy Analyst ICPAK

NATIONAL TREASURY STRATEGIC PLAN 2013/17 PRESENTATION TO PARLIAMENTARY FINANCE COMMITTEES

NATIONAL TREASURY STRATEGIC PLAN 2013/17 PRESENTATION TO PARLIAMENTARY FINANCE COMMITTEES 14 May 2013 TREASURY AIMS AND OBJECTIVES Chapter 13 of the Constitution of the Republic of South Africa. According

NATIONAL TREASURY STRATEGIC PLAN 2013/17 PRESENTATION TO PARLIAMENTARY FINANCE COMMITTEES 14 May 2013 TREASURY AIMS AND OBJECTIVES Chapter 13 of the Constitution of the Republic of South Africa. According

A Background Brief on Kenya s Devolution1

Public Disclosure Authorized Public Disclosure Authorized A Background Brief on Kenya s Devolution1 World Bank Public Disclosure Authorized Public Disclosure Authorized Contents 1. Overview and key points...

Public Disclosure Authorized Public Disclosure Authorized A Background Brief on Kenya s Devolution1 World Bank Public Disclosure Authorized Public Disclosure Authorized Contents 1. Overview and key points...

Legal Provisions in Procurement PUBLIC PROCUREMENT AND ASSET DISPOSAL ACT, 2015

Legal Provisions in Procurement PUBLIC PROCUREMENT AND ASSET DISPOSAL ACT, 2015 By: QS Maureen Njeri kinyanjuimnjeri@gmail.com 13 th June, 2017 Bomas of Kenya, Nairobi. OUTLINE Introduction Guiding principles

Legal Provisions in Procurement PUBLIC PROCUREMENT AND ASSET DISPOSAL ACT, 2015 By: QS Maureen Njeri kinyanjuimnjeri@gmail.com 13 th June, 2017 Bomas of Kenya, Nairobi. OUTLINE Introduction Guiding principles

The Applicability of IPSASs to Government Business Enterprises and Other Public Sector Entities

IFAC Board Consultation Paper August 2014 Comments due: December 31, 2014 The Applicability of IPSASs to Government Business Enterprises and Other Public Sector Entities TREASURY:2765382V1 This Consultation

IFAC Board Consultation Paper August 2014 Comments due: December 31, 2014 The Applicability of IPSASs to Government Business Enterprises and Other Public Sector Entities TREASURY:2765382V1 This Consultation

REPUBLIC OF KENYA THE NATIONAL TREASURY

REPUBLIC OF KENYA THE NATIONAL TREASURY PRESS RELEASE SOVEREIGN BOND (EUROBOND): QUESTIONS AND ANSWERS There has been several concerns raised through the media relating to the issuance of the Sovereign

REPUBLIC OF KENYA THE NATIONAL TREASURY PRESS RELEASE SOVEREIGN BOND (EUROBOND): QUESTIONS AND ANSWERS There has been several concerns raised through the media relating to the issuance of the Sovereign

State of the Accountancy Profession in Uganda

REPUBLIC OF UGANDA MINISTRY OF FINANCE, PLANNING & ECONOMIC DEVELOPMENT State of the Accountancy Profession in Uganda By: Lawrence Semakula Accountant General 31 st Annual ICGFM Annual International Training

REPUBLIC OF UGANDA MINISTRY OF FINANCE, PLANNING & ECONOMIC DEVELOPMENT State of the Accountancy Profession in Uganda By: Lawrence Semakula Accountant General 31 st Annual ICGFM Annual International Training

Performance Budgeting in Australia

ISSN 1608-7143 OECD Journal on Budgeting Volume 7 No. 3 OECD 2007 Chapter 1 Performance Budgeting in Australia by Lewis Hawke* This article describes how the principles of management for results have worked

ISSN 1608-7143 OECD Journal on Budgeting Volume 7 No. 3 OECD 2007 Chapter 1 Performance Budgeting in Australia by Lewis Hawke* This article describes how the principles of management for results have worked

Multi-Donor Trust Fund for the Malawi Public Finance and Economic Management Reform Program Grant Agreement

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized MDTF GRANT NUMBER TF013825 Multi-Donor Trust Fund for the Malawi Public Finance and Economic Management Reform Program

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized MDTF GRANT NUMBER TF013825 Multi-Donor Trust Fund for the Malawi Public Finance and Economic Management Reform Program

2017 BUDGET REVIEW AND OUTLOOK PAPER

REPUBLIC OF KENYA THE NATIONAL TREASURY 2017 BUDGET REVIEW AND OUTLOOK PAPER SEPTEMBER 2017 September 22, 2017 Draft 2017 Budget Review and Outlook Paper (BROP) To obtain copies of the document, please

REPUBLIC OF KENYA THE NATIONAL TREASURY 2017 BUDGET REVIEW AND OUTLOOK PAPER SEPTEMBER 2017 September 22, 2017 Draft 2017 Budget Review and Outlook Paper (BROP) To obtain copies of the document, please

2013 Workshop: Standing Committee on Appropriations Role of National Treasury in determining appropriations and in-year shift of funds

2013 Workshop: Standing Committee on Appropriations Role of National Treasury in determining appropriations and in-year shift of funds Presented by: Andrew Donaldson 30 January 2013 Chapter 4 of the PFMA

2013 Workshop: Standing Committee on Appropriations Role of National Treasury in determining appropriations and in-year shift of funds Presented by: Andrew Donaldson 30 January 2013 Chapter 4 of the PFMA

Recommendation of the Council on Good Practices for Public Environmental Expenditure Management

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS - INTRODUCTION

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS - INTRODUCTION IPSAS OBJECTIVES Comparability with other international organisations and national governments Enhanced governance and internal financial

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS - INTRODUCTION IPSAS OBJECTIVES Comparability with other international organisations and national governments Enhanced governance and internal financial

Australian Hotels Association Northern Territory Branch Inc.

Australian Hotels Association Northern Territory Branch Inc. General Purpose Financial Report for the year ended 30 June 2016 Contents Independent Auditor Report 1 Certificate by Prescribed Designated

Australian Hotels Association Northern Territory Branch Inc. General Purpose Financial Report for the year ended 30 June 2016 Contents Independent Auditor Report 1 Certificate by Prescribed Designated

RECOMMENDATIONS ON SHARING OF REVENUE RAISED NATIONALLY BETWEEN THE NATIONAL AND COUNTY GOVERNMENTS FOR THE FINANCIAL YEAR 2014/2015

RECOMMENDATIONS ON SHARING OF REVENUE RAISED NATIONALLY BETWEEN THE NATIONAL AND COUNTY GOVERNMENTS FOR THE FINANCIAL YEAR 2014/2015 Media Briefing January 29 th 2014 PRESENTATION OUTLINE 1. LEGAL FRAMEWORK

RECOMMENDATIONS ON SHARING OF REVENUE RAISED NATIONALLY BETWEEN THE NATIONAL AND COUNTY GOVERNMENTS FOR THE FINANCIAL YEAR 2014/2015 Media Briefing January 29 th 2014 PRESENTATION OUTLINE 1. LEGAL FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Copyright 2017 by the Accounting Standards Board All rights reserved.

ACCOUNTING STANDARDS BOARD DIRECTIVE 5 DETERMINING THE GRAP REPORTING FRAMEWORK Issued by the Accounting Standards Board March 2009 Copyright 2017 by the Accounting Standards Board All rights reserved.

PROJECT HISTORY. Contact: Stephenie Fox December 2014

PROJECT HISTORY Contact: Stephenie Fox (stepheniefox@ipsasb.org) December 2014 The IPSASB had agreed at its September 2014 meeting that the proposed IPSAS on First-time Adoption of Accrual Basis International

PROJECT HISTORY Contact: Stephenie Fox (stepheniefox@ipsasb.org) December 2014 The IPSASB had agreed at its September 2014 meeting that the proposed IPSAS on First-time Adoption of Accrual Basis International

THE BUDGET ACT, 2014 ARRANGEMENT OF SECTIONS PART I PRELIMINARY PROVISIONS PART II MACROECONOMIC AND FISCAL FRAMEWORK

THE UNITED REPUBLIC OF TANZANIA ISSN 0856-35X BILL SUPPLEMENT No. 13 31 st October, 2014 to the Gazette of the United Republic of Tanzania No. 44. Vol. 95 dated 31 st October, 2014 Printed by the Government

THE UNITED REPUBLIC OF TANZANIA ISSN 0856-35X BILL SUPPLEMENT No. 13 31 st October, 2014 to the Gazette of the United Republic of Tanzania No. 44. Vol. 95 dated 31 st October, 2014 Printed by the Government

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5 INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: (212) 286-9344 New York, New York 10017 Fax: (212) 286-9570

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5 INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: (212) 286-9344 New York, New York 10017 Fax: (212) 286-9570