Accounting 303 Exam 3, Chapters 7-8 Fall 2014

|

|

|

- Benedict Austin

- 5 years ago

- Views:

Transcription

1 Accounting 303 Exam 3, Chapters 7-8 Fall 2014 Name Row I. Multiple Choice Questions. (2 points each, 20 points in total) Read each question carefully and indicate your answer by circling the letter preceding the one best answer. 1. Which of the following is an appropriate reconciling item to the balance per bank in a bank reconciliation? a. Bank service charge. b. Deposit in transit. c. Bank collection of note with interest. d. Chargeback for NSF check. 2. What is the preferable presentation of accounts receivable from officers, employees, or affiliated companies on a balance sheet? a. As offsets to capital. b. By means of footnotes only. c. As assets but separately from other receivables. d. As trade notes and accounts receivable if they otherwise qualify as current assets. 3. What is the normal journal entry when writing-off an account as uncollectible under the allowance method? a. Debit Allowance for Doubtful Accounts, credit Accounts Receivable. b. Debit Allowance for Doubtful Accounts, credit Bad Debt Expense. c. Debit Bad Debt Expense, credit Allowance for Doubtful Accounts. d. Debit Accounts Receivable, credit Allowance for Doubtful Accounts. 4. Which of the following is true when accounts receivable are factored without recourse? a. The transaction may be accounted for either as a secured borrowing or as a sale, depending upon the substance of the transaction. b. The receivables are used as collateral for a promissory note issued to the factor by the owner of the receivables. c. The factor assumes the risk of collectability and absorbs any credit losses in collecting the receivables. d. The financing cost (interest expense) should be recognized ratably over the collection period of the receivables. 5. Which of the following is a characteristic of a perpetual inventory system? a. Inventory purchases are debited to a Purchases account. b. Inventory records are not kept up-to-date for every item. c. Cost of goods sold is recorded with each sale. d. Cost of goods sold is determined as the amount of purchases less the change in inventory. 1

2 6. Goods in transit which are shipped f.o.b. destination should be a. included in the inventory of the seller. b. included in the inventory of the buyer. c. included in the inventory of the shipping company. d. none of these answers are correct. 7. What is the effect of a $50,000 overstatement of last year's ending inventory on current year s ending retained earning balance? a. Understated by $50,000. b. No effect. c. Overstated by $50,000. d. Need more information to determine. 8. CSK Company purchased merchandise with an invoice price of $1,400 on terms of 2/15, n/45. CSK uses the perpetual net method to record purchases. Which of the following is the correct entry they should make to record this purchase? a. Purchases 1,400 Accounts Payable 1,400 b. Purchases 1,372 Accounts Payable 1,372 c. Inventory 1,400 Accounts Payable 1,400 d. Inventory 1,372 Accounts Payable 1, Winsor Co. records purchases at net amounts. On May 5 Winsor purchased merchandise on account, $40,000, terms 2/10, n/30. Winsor returned $3,000 of the May 5 purchase and received credit on account. At May 31 the balance had not been paid. The amount to be recorded as a purchase return is a. $2,700. b. $3,060 c. $3,000. d. $2, Risers Inc. reported total assets of $3,200,000 and net income of $255,000 for the current year. Risers determined that inventory was understated by $30,000 at the end of the year. What is the corrected amount for total assets and net income at the end of the year? a. $3,230,000 and $285,000. b. $3,170,000 and $294,000. c. $3,230,000 and $216,000. d. $3,200,000 and $255,000. 2

3 II. Problems (60 points in total) Show all work where appropriate! 1. (10 points) The trial balance before adjustment of Valdamo Company shows the following balances on December 31, 2014: Dr. Cr. Accounts receivable $250,000 Allowance for doubtful accounts 4,500 Sales (all on credit) $1,850,000 Sales returns and allowances 54,000 Required: Prepare the December 31, 2014, year-end adjusting entry for Valdamo s estimated bad debts assuming that doubtful accounts are estimated to be (a) 6% of gross accounts receivable. (b) 1% of net sales. 3

4 2. (12 points) On December 31, 2014, Parma Company sold equipment and accepted as payment a promissory note with a face value of $4,000,000, a due date of December 31, 2018, and a stated interest rate of 5%, with interest to be paid at the end of each year starting December 31, The cash price of the equipment at the date of sale would have been $3,481,645. Required (a) Determine the imputed interest rate of the note. (b) Prepare the required journal entry or entries on Parma Company s books for December 31, (c) Prepare the required journal entry or entries on Parma Company s books for December 31, 2015 assuming the imputed interest rate is 10%. 4

5 3. (10 points) On May 1, Siena, Inc. factored $1,000,000 of its accounts receivable with Quick Finance on a without recourse basis. Under the arrangement, Siena was to handle disputes concerning service, and Quick Finance was to make the collections, handle the sales discounts, and absorb the credit losses. Quick Finance assessed a finance charge of 7% of the total accounts receivable factored and retained an amount equal to 4% of the total receivables to cover sales discounts and returns. Required (a) Prepare the journal entry required on Siena's books on May 1. (b) Assume Siena factored the accounts receivable with Quick Finance on a with recourse basis instead. Siena estimates the recourse provision has a fair value of $21,000. Under these assumptions, what amount of loss would Siena report as part of their May 1 entry. 5

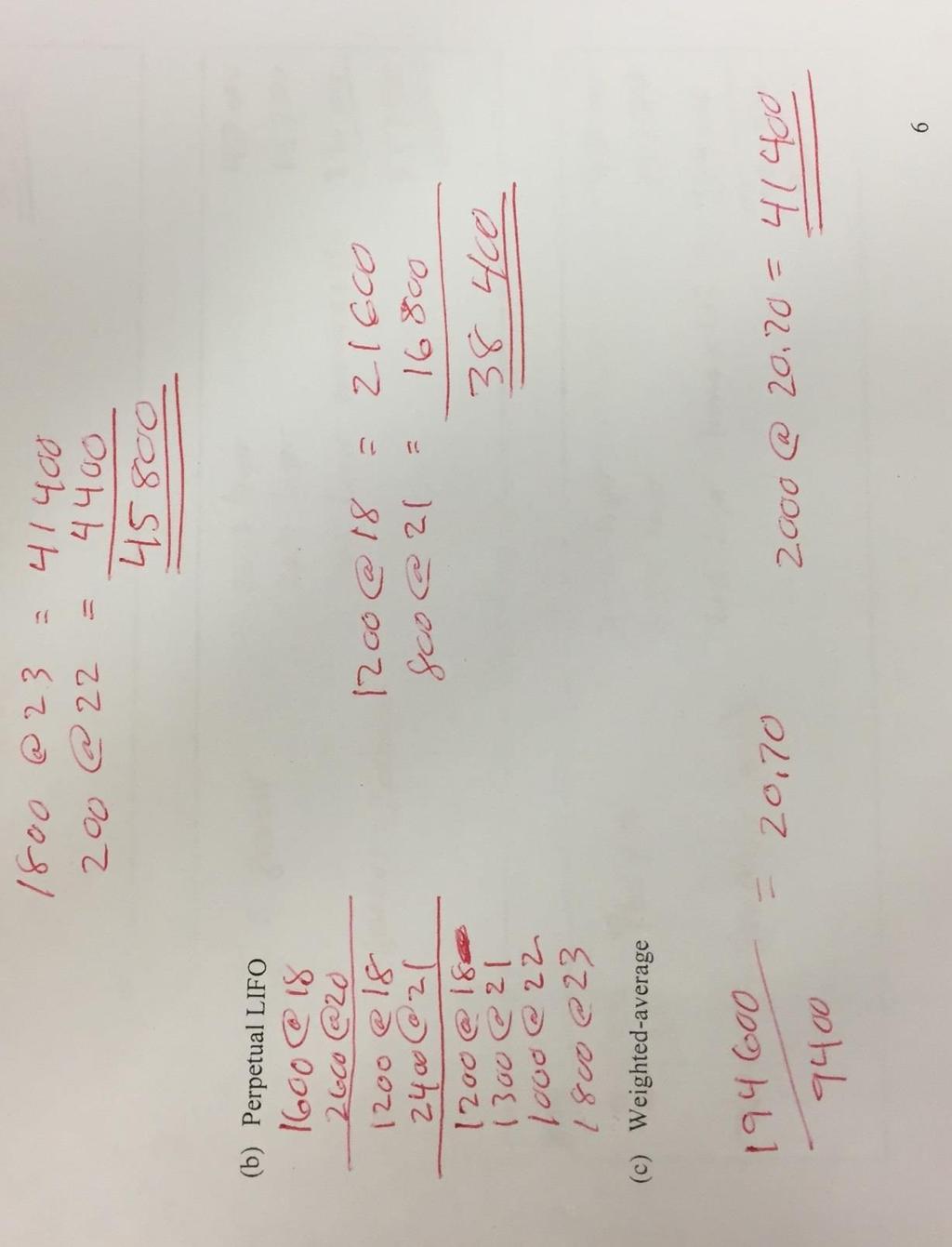

6 4. (13 points) Monterosso Company was formed on December 1, The following information is available from Monterosso's inventory records. Units Unit Amount Total January 1, 2014 (beginning inventory) 1,600 $ ,800 Purchases: January 5, 2014 Purchase 2,600 $ ,000 January 10, 2014 Sale 3,000 January 25, 2014 Purchase 2,400 $ ,400 February 1, 2014 Sale 1,100 February 16, 2014 Purchase 1,000 $ ,000 March 15, 2014 Purchase 1,800 $ ,400 March 27, 2014 Sale 3,300 9,400 7, ,600 Required: Compute the ending inventory at March 31, 2014, under each of the following inventory methods. Show supporting computations in good form. (a) Periodic FIFO (b) Perpetual LIFO (c) Weighted-average 6

7 a (15 points) Vernazza Company manufactures one product. On December 31, 2013, Vernazza adopted the dollar-value LIFO inventory method. The inventory on that date using the dollar-value LIFO inventory method was $450,000. Inventory data are as follows: Inventory at Price index Year year-end prices (base year 2013) 2014 $630, , , Required: Compute Vernazza s inventory at December 31, 2014, 2015, and 2016, using dollar-value LIFO for each year. b c

8 Solutions Multiple Choice Question Number Answer 1. b 2. c 3. a 4. c 5. c 6. a 7. b 8. d 9. d 10. a 8

9 Problem 1 (a) Bad Debt Expense... 19,500 Allowance for Doubtful Accounts... 19,500 Gross receivables $250,000 Rate 6% Total allowance needed 15,000 Present allowance 4,500 Bad debt expense $ 19,500 (b) Bad Debt Expense... 17,960 Allowance for Doubtful Accounts... 17,960 Sales $1,850,000 Sales returns and allowances (54,000) Net sales 1,796,000 Rate 1% Bad debt expense $ 17,960 9

10 2. (a) n = 4 PMT = PV = FV = CPT i = 9% (b) Notes Receivable Discount on N/R Sales (c) Cash Discount on N/R Interest Revenue (a) Cash Due from Factor ( x.04) Loss on Sale ( x.07) Acc Rec (b) Cash Due from Factor ( x.04) Loss on Sale ( x.07) Acc Rec Recourse Liability

11 4. (a) 11

12 Problem 5 12

MERCHANDISING OPERATIONS

MERCHANDISING OPERATIONS Key Topics to Know Merchandising Businesses The revenue account is Sales, not Fees Earned New expense account, Cost of Goods Sold (COGS), records the cost of merchandise inventory

MERCHANDISING OPERATIONS Key Topics to Know Merchandising Businesses The revenue account is Sales, not Fees Earned New expense account, Cost of Goods Sold (COGS), records the cost of merchandise inventory

ACCOUNTING 201. PRACTICE FINAL - (Covering Chapters 6-9)

") Problem - I Multiple Choice Circle the one best answer. ACCOUNTING 201 PRACTICE FINAL - (Covering Chapters 6-9) 1. Inventoriable costs include all of the following except the a. cost of the goods purchased.

Problem - I Multiple Choice Circle the one best answer. ACCOUNTING 201 PRACTICE FINAL - (Covering Chapters 6-9) 1. Inventoriable costs include all of the following except the a. cost of the goods purchased.

November 17, 2004 Anderson Econ 136A Midterm #2 Name

November 17, 2004 Anderson Econ 136A Midterm #2 Name Write your name, perm #, Eon 136B Midterm #2 on both your scantron and blue-book. Use your scantrons for questions 1-25. Use your blue-book for questions

November 17, 2004 Anderson Econ 136A Midterm #2 Name Write your name, perm #, Eon 136B Midterm #2 on both your scantron and blue-book. Use your scantrons for questions 1-25. Use your blue-book for questions

REPASO # 2 CONT 3105

REPASO # 2 CONT 3105 Preguntas de repaso para el Examen Coordinado Número 2 de CONT 3105, 1 de noviembre de 2013 Laboratorio CONT 3105 1. The principal reason for reconciling the cash balance per books

REPASO # 2 CONT 3105 Preguntas de repaso para el Examen Coordinado Número 2 de CONT 3105, 1 de noviembre de 2013 Laboratorio CONT 3105 1. The principal reason for reconciling the cash balance per books

February 28, 2007 Anderson ECON 136A Midterm #2 v. 1 Name

February 28, 2007 Anderson ECON 136A Midterm #2 v. 1 Name THERE IS A PROBLEM IN THIS EXAM WHICH REQUIRES THAT YOU COMPLETE IN THE SPACE PROVIDED... PLEASE BE SURE TO WRITE YOUR NAME ON THE EXAM AND TURN

February 28, 2007 Anderson ECON 136A Midterm #2 v. 1 Name THERE IS A PROBLEM IN THIS EXAM WHICH REQUIRES THAT YOU COMPLETE IN THE SPACE PROVIDED... PLEASE BE SURE TO WRITE YOUR NAME ON THE EXAM AND TURN

November 14, 2005 Anderson ECON 136A MIDTERM #2 Name

November 14, 2005 Anderson ECON 136A MIDTERM #2 Name Answer questions #1-25 (multiple choice) on your scantron and questions #26, 27 & 28 in your blue-book. ------------------------- ANSWER ON YOUR GREEN

November 14, 2005 Anderson ECON 136A MIDTERM #2 Name Answer questions #1-25 (multiple choice) on your scantron and questions #26, 27 & 28 in your blue-book. ------------------------- ANSWER ON YOUR GREEN

FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION

FINAL EXAMINATION") Canadian International Matriculation Programme Sunway College FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION Date : 6 June 2017 Time Length Lecturer : 8:30 a.m. 10:30 a.m. : 2 hours : Ms Rehnu

Canadian International Matriculation Programme Sunway College FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION Date : 6 June 2017 Time Length Lecturer : 8:30 a.m. 10:30 a.m. : 2 hours : Ms Rehnu

Financial Accounting (Corporation)

") Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

Financial Accounting (Corporation)

") Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

SU 2.1 Accounts Receivable

Part 1 Study Unit 2 SU 2.1 Accounts Receivable Overview Recording receivables, which coincides with revenue recognition, is consistent with the accrual method of accounting. Current Receivables will be

Part 1 Study Unit 2 SU 2.1 Accounts Receivable Overview Recording receivables, which coincides with revenue recognition, is consistent with the accrual method of accounting. Current Receivables will be

2013 年 会计学原理 期中考试 1 / 6

2013 年 会计学原理 期中考试 Part I True or False (0.5 mark each, 21 marks in total) 1. The primary objective of financial accounting is to provide general purpose financial statements to help external users analyze

2013 年 会计学原理 期中考试 Part I True or False (0.5 mark each, 21 marks in total) 1. The primary objective of financial accounting is to provide general purpose financial statements to help external users analyze

Financial Accounting (Sole Proprietorship)

") Financial Accounting (Sole Proprietorship) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and

Financial Accounting (Sole Proprietorship) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and

Chapter 6: Reporting and Interpreting Sales Revenue, Receivables and Cash

Chapter 6: Reporting and Interpreting Sales Revenue, Receivables and Cash A. Recognition of Revenue for Merchandising Companies FOB Shipping Point: title switch at shipping point Once you get it to a point

Chapter 6: Reporting and Interpreting Sales Revenue, Receivables and Cash A. Recognition of Revenue for Merchandising Companies FOB Shipping Point: title switch at shipping point Once you get it to a point

BUSA PRACTICAL ACCOUNTING I/II Entiat High School

BUSA 102 - PRACTICAL ACCOUNTING I/II Student Entiat High School 2010-2011 Cycle 1 1 Define and identify asset, liability, and owner s equity accounts. 1.1 2 Define a fiscal period and a fiscal year. 1.1

BUSA 102 - PRACTICAL ACCOUNTING I/II Student Entiat High School 2010-2011 Cycle 1 1 Define and identify asset, liability, and owner s equity accounts. 1.1 2 Define a fiscal period and a fiscal year. 1.1

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

ACCT-112 Final Exam Practice Solutions

ACCT-112 Final Exam Practice Solutions Question 1 Jan 1 Cash 200,000 H. Happee, Capital 200,000 Jan 2 Prepaid Insurance 10,000 Cash 10,000 Jan 15 Equipment 15,000 Cash 5,000 Notes Payable 10,000 Jan 30

ACCT-112 Final Exam Practice Solutions Question 1 Jan 1 Cash 200,000 H. Happee, Capital 200,000 Jan 2 Prepaid Insurance 10,000 Cash 10,000 Jan 15 Equipment 15,000 Cash 5,000 Notes Payable 10,000 Jan 30

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

Answer questions #1-25 on your green scantron--write YOUR VERSION # ON YOUR SCANTRON PLEASE!!!

136A fall 09 MIDTERM 2 v. 1 Name Answer questions #1-25 on your green scantron--write YOUR VERSION # ON YOUR SCANTRON PLEASE!!! Answer the remaining questions in your blue-books. 1. Which of the following

136A fall 09 MIDTERM 2 v. 1 Name Answer questions #1-25 on your green scantron--write YOUR VERSION # ON YOUR SCANTRON PLEASE!!! Answer the remaining questions in your blue-books. 1. Which of the following

Practice Multiple Choice Questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

Feb 27, 2008 Anderson ECON 136A MIDTERM 2 VERSION 1 Name

Feb 27, 2008 Anderson ECON 136A MIDTERM 2 VERSION 1 Name QUESTION NUMBER 26 HAS A FILL IN THE BLANK PORTION- BE SURE TO FILL THOSE IN AND TURN THIS EXAM IN WITH YOUR SCANTRON AND BLUE BOOK!!! WRITE YOUR

Feb 27, 2008 Anderson ECON 136A MIDTERM 2 VERSION 1 Name QUESTION NUMBER 26 HAS A FILL IN THE BLANK PORTION- BE SURE TO FILL THOSE IN AND TURN THIS EXAM IN WITH YOUR SCANTRON AND BLUE BOOK!!! WRITE YOUR

Accounting 303 Exam 3, Chapters 8-10 Fall 2015

Accounting 303 Exam 3, Chapters 8-10 Fall 2015 Name Row I. Multiple Choice Questions. (2 points each, 24 points in total) Read each question carefully and indicate your answer by circling the letter preceding

Accounting 303 Exam 3, Chapters 8-10 Fall 2015 Name Row I. Multiple Choice Questions. (2 points each, 24 points in total) Read each question carefully and indicate your answer by circling the letter preceding

Rent Revenue, Interest Revenue, Investment Income, Gains. Interest Expense, Losses

Chapter 5 Assigned Questions: 1, 4, 5, 7, 9, 11, 16, 17, 19, 20 1. The components of revenues and expenses differ as follows: Merchandising Revenue Sales Service Service Revenue, Fees Earned, Rent Revenue,

Chapter 5 Assigned Questions: 1, 4, 5, 7, 9, 11, 16, 17, 19, 20 1. The components of revenues and expenses differ as follows: Merchandising Revenue Sales Service Service Revenue, Fees Earned, Rent Revenue,

$100,000; and Medicare tax rate, 1.5% on all earnings. What is the gross pay for the employee?

Final Exam Review 1. Accumulated Depreciation a. is used to show the amount of cost expiration of intangibles b. is the same as Depreciation Expense c. is a contra asset account d. is used to show the

Final Exam Review 1. Accumulated Depreciation a. is used to show the amount of cost expiration of intangibles b. is the same as Depreciation Expense c. is a contra asset account d. is used to show the

CHAPTER 2 MEASUREMENTS, VALUATION & DISCLOSURE: INVESTMENTS & SHORT-TERM ITEMS

CHAPTER 2 MEASUREMENTS, VALUATION & DISCLOSURE: INVESTMENTS & SHORT-TERM ITEMS This chapter covers Receivables Inventory Investments A. ACCOUNTS RECEIVABLE: are the amounts owed to an entity by its customers.

CHAPTER 2 MEASUREMENTS, VALUATION & DISCLOSURE: INVESTMENTS & SHORT-TERM ITEMS This chapter covers Receivables Inventory Investments A. ACCOUNTS RECEIVABLE: are the amounts owed to an entity by its customers.

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

February 23, 2005 Anderson ECON 136A Midterm #2 Name

February 23, 2005 Anderson ECON 136A Midterm #2 Name Complete the multiple choice on green scantron and problems in your bluebook. WRITE YOUR NAME ON YOUR EXAM AND TURN IT IN WITH YOUR BLUE BOOK AND SCANTRON

February 23, 2005 Anderson ECON 136A Midterm #2 Name Complete the multiple choice on green scantron and problems in your bluebook. WRITE YOUR NAME ON YOUR EXAM AND TURN IT IN WITH YOUR BLUE BOOK AND SCANTRON

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Name: Student ID: WatIAM/Quest ID: Section (please circle): 8:30-9:50 (K. Kelly) 4:00-5:20 (R. Ducharme)

: 8:30-9:50 (K. Kelly) 4:00-5:20 (R. Ducharme)") AFM 291 Intermediate Financial Accounting I University of Waterloo Midterm Exam Friday, October 30, 2009 4:30pm-6:30pm K. Kelly (Sections 001-003) and R. Ducharme (Section 004-005) Name: Student ID: WatIAM/Quest

AFM 291 Intermediate Financial Accounting I University of Waterloo Midterm Exam Friday, October 30, 2009 4:30pm-6:30pm K. Kelly (Sections 001-003) and R. Ducharme (Section 004-005) Name: Student ID: WatIAM/Quest

Multiple choice question 51 A small neighborhood barber shop that is operated by its owner would likely be organized as a Proprietorship.

FINAL EXAM Financial accounting Multiple choice question 92 The best definition of assets is the Resources belonging to a company that have future benefit to the company. Collections of resources belonging

FINAL EXAM Financial accounting Multiple choice question 92 The best definition of assets is the Resources belonging to a company that have future benefit to the company. Collections of resources belonging

ACC 556 All Chapter Quizzes

ACC 556 All Chapter Quizzes FOR MORE CLASSES VISIT www.acc556outlet.com ACC 556 Chapter 1 Quiz (100% Score) ACC 556 Chapter 2 Quiz (100% Score) ACC 556 Chapter 3 Quiz (100% Score) ACC 556 Chapter 4 Quiz

ACC 556 All Chapter Quizzes FOR MORE CLASSES VISIT www.acc556outlet.com ACC 556 Chapter 1 Quiz (100% Score) ACC 556 Chapter 2 Quiz (100% Score) ACC 556 Chapter 3 Quiz (100% Score) ACC 556 Chapter 4 Quiz

B.COM I ACCOUNTING REGULAR/ PRIVATE. S.Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

2000 Accounting II Page 1

2000 Accounting II Page 1 1. In accounting, the two types of equity are liabilities and owner's equity. 2. When journalizing, you are advised to go from left to right. 3. Transportation charges need to

2000 Accounting II Page 1 1. In accounting, the two types of equity are liabilities and owner's equity. 2. When journalizing, you are advised to go from left to right. 3. Transportation charges need to

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Course Outline. Introduction to accounting and accounting equation Ch.2, book 1 Section A

Course Outline Course Title: Fundamentals of Accounting Course No: BS (A&F): ACC 103 Class: BS (A &F), BS (Commerce), Course No: BS (Commerce): ACC 103 B.Com (Annual system): B.Com (Annual system): Part

Course Outline Course Title: Fundamentals of Accounting Course No: BS (A&F): ACC 103 Class: BS (A &F), BS (Commerce), Course No: BS (Commerce): ACC 103 B.Com (Annual system): B.Com (Annual system): Part

York University AP/Adms Introduction to Financial Accounting Midterm Examination Test Form B

York University AP/Adms 2500.03 Introduction to Financial Accounting Midterm Examination Test Form B Time: 3.0 hours Winter 2010 March 5 th, 2010 Questions: 50 Instructions: 1. Only the mark sense sheet

York University AP/Adms 2500.03 Introduction to Financial Accounting Midterm Examination Test Form B Time: 3.0 hours Winter 2010 March 5 th, 2010 Questions: 50 Instructions: 1. Only the mark sense sheet

Zicklin School of Business, Baruch College ACC Financial Accounting 1 Fall Mid Term 2

Zicklin School of Business, Baruch College ACC 3000 -- Financial Accounting 1 Fall 2004 Mid Term 2 Instructor: Prof. Donal Byard Name: Office: VC 12-264 Phone: (646) 312-3187 Last 4 Digits of SSN: E-mail:

Zicklin School of Business, Baruch College ACC 3000 -- Financial Accounting 1 Fall 2004 Mid Term 2 Instructor: Prof. Donal Byard Name: Office: VC 12-264 Phone: (646) 312-3187 Last 4 Digits of SSN: E-mail:

Do not turn this page until the start signal is given!

UNIVERSITY INTERSCHOLASTIC LEAGUE ACCOUNTING EXAM Regional 2018-R Contestant # Do not turn this page until the start signal is given! All answers MUST be written on your answer sheet. Either upper case

UNIVERSITY INTERSCHOLASTIC LEAGUE ACCOUNTING EXAM Regional 2018-R Contestant # Do not turn this page until the start signal is given! All answers MUST be written on your answer sheet. Either upper case

Accounting Cheat Sheet

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

ACC 131 Finals Blitz

ACC 131 Finals Blitz Note: This is just an overview of some key topics to understand. This is NOT a comprehensive list. Please consult your professor and/or class syllabus for more information on what

ACC 131 Finals Blitz Note: This is just an overview of some key topics to understand. This is NOT a comprehensive list. Please consult your professor and/or class syllabus for more information on what

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Accounting 40S Exam Study Guide. Sole Proprietorship. Partnership. Corporation. Bank Reconciliation. Periodicity Concept. Business Entity Concept

Accounting 40S Exam Study Guide Sole Proprietorship Partnership Corporation Bank Reconciliation Periodicity Concept Business Entity Concept Going Concern Monetary Unit Concept Debit Credit Permanent Accounts

Accounting 40S Exam Study Guide Sole Proprietorship Partnership Corporation Bank Reconciliation Periodicity Concept Business Entity Concept Going Concern Monetary Unit Concept Debit Credit Permanent Accounts

a. True b. False a. True b. False a. True b. False a. True b. False a. True b. False a. True b. False a. True b. False a. True b.

2005 SLC Accounting II Page 1 Indicate whether the sentence or statement is True or False. Mark A if True or B if False. 1. Most companies have a code of conduct that they distribute and/or communicate

2005 SLC Accounting II Page 1 Indicate whether the sentence or statement is True or False. Mark A if True or B if False. 1. Most companies have a code of conduct that they distribute and/or communicate

Accounting 3 4. Course Outline. Board Approved: October 10, I. Course Information. A. Course Title: Accounting 3-4. B. Course Code Number: BU143

Accounting 3 4 Course Outline Board Approved: October 10, 1995 I. Course Information A. Course Title: Accounting 3-4 B. Course Code Number: BU143 C. Course Length: One Year D. Grade Level: 12 E. Units

Accounting 3 4 Course Outline Board Approved: October 10, 1995 I. Course Information A. Course Title: Accounting 3-4 B. Course Code Number: BU143 C. Course Length: One Year D. Grade Level: 12 E. Units

Accountings Summary OUTLINE

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

A U D I T I N G P R O B L E M S

2011 NATIONAL CPA MOCK BOARD EXAMINATION In partnership with the Professional Review & Training Center, Inc. and Isla Lipana & Co. A U D I T I N G P R O B L E M S INSTRUCTIONS: Select the best answer for

2011 NATIONAL CPA MOCK BOARD EXAMINATION In partnership with the Professional Review & Training Center, Inc. and Isla Lipana & Co. A U D I T I N G P R O B L E M S INSTRUCTIONS: Select the best answer for

PRINCIPLES OF ACCOUNTING b.com part I

PRINCIPLES OF ACCOUNTING b.com part I 2013 PRIVATE (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks. (3)

PRINCIPLES OF ACCOUNTING b.com part I 2013 PRIVATE (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks. (3)

3. The following information was taken from Hurlbert Company cash budget for the month June

Unit 3 (Chapters 7-9 Question Review) 1 Unit 3 Exam (Chapters 7-9 Review) 1. A $200 petty cash fund has cash of $32 and receipts of $172. The journal entry to replenish the account would include a a. debit

Unit 3 (Chapters 7-9 Question Review) 1 Unit 3 Exam (Chapters 7-9 Review) 1. A $200 petty cash fund has cash of $32 and receipts of $172. The journal entry to replenish the account would include a a. debit

Fin621 Online Quizzes & Papers GURU

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

Fin-621 Final term Solved Papers by Fahad Yusha Cell: and

FINALTERM EXAMINATION Spring 2010 FIN621 - Financial Statement Analysis Student Info StudentID: Time: 90 min Marks: 69 Center: ExamDate: Tue, Aug 10, 2010 Question No: 1 After recording the transactions

FINALTERM EXAMINATION Spring 2010 FIN621 - Financial Statement Analysis Student Info StudentID: Time: 90 min Marks: 69 Center: ExamDate: Tue, Aug 10, 2010 Question No: 1 After recording the transactions

Accounting Practice Test

Accounting Training Unlimited ~ www.atunlimited.com ~ info@atunlimited.com Page 1 Accounting Practice Test Table of Contents Accounting Practice Test... 3 Accounting Practice Test Answer Sheet... 9 Accounting

Accounting Training Unlimited ~ www.atunlimited.com ~ info@atunlimited.com Page 1 Accounting Practice Test Table of Contents Accounting Practice Test... 3 Accounting Practice Test Answer Sheet... 9 Accounting

Name: Class: Date: 1 MULTIPLE CHOICE 4-2

1 MULTIPLE CHOICE 4-2 I certify that I am taking this examination alone and am not receiving any help with it except through the use of my textbook and notes. I have not been given any of the questions

1 MULTIPLE CHOICE 4-2 I certify that I am taking this examination alone and am not receiving any help with it except through the use of my textbook and notes. I have not been given any of the questions

ADVANCED ACCOUNTING (110) Secondary

Secondary") Page 1 of 9 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2018 Multiple Choice (20 @ 2 points each) Short Answer Problem 1 Inventory Costing Problem 2 Uncollectible Accounts

Page 1 of 9 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2018 Multiple Choice (20 @ 2 points each) Short Answer Problem 1 Inventory Costing Problem 2 Uncollectible Accounts

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING Ex. 2-135 Accounting concepts identification. State the accounting assumption, principle, information characteristic, or constraint that is

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING Ex. 2-135 Accounting concepts identification. State the accounting assumption, principle, information characteristic, or constraint that is

CA CPT Account Test Combine Topic

CA CPT Account Test Combine Topic Test ID :063 Date : 14/09/2017 Time :01:55:00 Qn.1) Contingent Liabilities are shown : A. As current liability B. As Capital fund C. As footnotes to balance sheet D. As

CA CPT Account Test Combine Topic Test ID :063 Date : 14/09/2017 Time :01:55:00 Qn.1) Contingent Liabilities are shown : A. As current liability B. As Capital fund C. As footnotes to balance sheet D. As

Chapter 4 Intercompany Transactions: Topic 1, Merchandise. Student Learning Outcomes

Chapter 4 Intercompany Transactions: Topic 1, Merchandise Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Explain why transactions between members of a consolidated

Chapter 4 Intercompany Transactions: Topic 1, Merchandise Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Explain why transactions between members of a consolidated

INTERMEDIATE ACCOUNTING: RAPID REVIEW Kieso, Weygandt, Warfield, Young, Wiecek McConomy

KIESO 10th Ed._RAPID REVIEW_3rd pass_feb. 18, 2013 13-02-18 6:37 AM Page 1 INTERMEDIATE ACCOUNTING: RAPID REVIEW Kieso, Weygandt, Warfield, Young, Wiecek McConomy Tenth Canadian Edition, Volume 1: Chapters

KIESO 10th Ed._RAPID REVIEW_3rd pass_feb. 18, 2013 13-02-18 6:37 AM Page 1 INTERMEDIATE ACCOUNTING: RAPID REVIEW Kieso, Weygandt, Warfield, Young, Wiecek McConomy Tenth Canadian Edition, Volume 1: Chapters

Notes Receivable A note is a written promise to pay a specific amount at a specific future date. Includes an interest cost for the term of the note

RECEIVABLES Accounts Receivable Amounts due from customers for credit sales. Credit sales require: o Maintaining a separate account receivable for each customer. o Accounting for bad debts that result

RECEIVABLES Accounts Receivable Amounts due from customers for credit sales. Credit sales require: o Maintaining a separate account receivable for each customer. o Accounting for bad debts that result

Work Sheets for Exercises 7-3, 7-4, and 7-5 appear on the following pages. Exercise 7-6 a.

Exercise 7-1 CROCKER COMPANY Schedule of Corrected Net Income Year 2005 2006 2007 Total Exercise 7-2 Work Sheets for Exercises 7-3, 7-4, and 7-5 appear on the following pages. Exercise 7-6 a. KETTLE COMPANY

Exercise 7-1 CROCKER COMPANY Schedule of Corrected Net Income Year 2005 2006 2007 Total Exercise 7-2 Work Sheets for Exercises 7-3, 7-4, and 7-5 appear on the following pages. Exercise 7-6 a. KETTLE COMPANY

May 22, 2006 Anderson ECON 136A Midterm #2 Name

May 22, 2006 Anderson ECON 136A Midterm #2 Name Complete questions 1-15 (multiple choice) on green scantron with pencil, and the rest, #16-21 (problems/ short answers) in your blue-book. 1. Which of the

May 22, 2006 Anderson ECON 136A Midterm #2 Name Complete questions 1-15 (multiple choice) on green scantron with pencil, and the rest, #16-21 (problems/ short answers) in your blue-book. 1. Which of the

Financial Accounting. Final Exam

06169700 Financial Accounting Final Exam When you feel confident that you have mastered the material in Financial Accounting, complete the following exam by answering the questions and compiling your answers

06169700 Financial Accounting Final Exam When you feel confident that you have mastered the material in Financial Accounting, complete the following exam by answering the questions and compiling your answers

FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION

FINAL EXAMINATION") Canadian International Matriculation Programme Sunway College FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION Date : 5 December 2017 Time Length Lecturer : 8:30 a.m. 10:30 a.m. : 2 hours : Ms

Canadian International Matriculation Programme Sunway College FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION Date : 5 December 2017 Time Length Lecturer : 8:30 a.m. 10:30 a.m. : 2 hours : Ms

FINANCIAL RATIOS 2 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 3 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Accounting for Merchandising Businesses

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

Bad Debts Expense 22,000. Bad Debts Expense 22,000

Name: Date: 1. Which one of the following is not an objective of a system of internal controls? A) Safeguard company assets B) Overstate liabilities in order to be conservative C) Enhance the accuracy

Name: Date: 1. Which one of the following is not an objective of a system of internal controls? A) Safeguard company assets B) Overstate liabilities in order to be conservative C) Enhance the accuracy

EXAM #2 SAMPLE PROBLEMS

EXAM #2 SAMPLE PROBLEMS (Lessons 5-10) Use the following information to respond to problems 1-6 assuming Zee Corp. maintains their inventory records on a perpetual basis: 1/12 Zee Corp., a wholesaler of

EXAM #2 SAMPLE PROBLEMS (Lessons 5-10) Use the following information to respond to problems 1-6 assuming Zee Corp. maintains their inventory records on a perpetual basis: 1/12 Zee Corp., a wholesaler of

Chapter 5. Control Accounts. Notes to teachers

Chapter 5 Control Accounts Notes to teachers 1 Start with Chapters 3 and 4 of Frank Wood s Introduction to Accounting and briefly explain to students the basic principles of recording in the books and

Chapter 5 Control Accounts Notes to teachers 1 Start with Chapters 3 and 4 of Frank Wood s Introduction to Accounting and briefly explain to students the basic principles of recording in the books and

Grade 12 Accounting Review & Practice Questions

Grade 12 Accounting Review & Practice Questions Chapter 1 Review Questions Chapter 1 Theory: Do m/c Page 30 31 #1 10 Chapter 1 Practice: o BE1 1 o BE1 5 o BE1 6 o BE1 11 o BE1 15 Exercises o E1 4 o E1

Grade 12 Accounting Review & Practice Questions Chapter 1 Review Questions Chapter 1 Theory: Do m/c Page 30 31 #1 10 Chapter 1 Practice: o BE1 1 o BE1 5 o BE1 6 o BE1 11 o BE1 15 Exercises o E1 4 o E1

Uses of Accounting Information I (ACC 230) Final Exam Review

Final Exam Review") Uses of Accounting Information I (ACC 230) Final Exam Review Balances at the end of the first year of operations: Cash 10,000 Sales 70,000 Accounts Receivable 12,000 Accounts Payable 8,000 Cost of Goods

Uses of Accounting Information I (ACC 230) Final Exam Review Balances at the end of the first year of operations: Cash 10,000 Sales 70,000 Accounts Receivable 12,000 Accounts Payable 8,000 Cost of Goods

LITTLE NOTABLES EXCLUSIVE JOSH HAWKEY

Accounting 102: Financial Reporting Enviroment FRA Financial Reporting Act (The old way) FRB Financial Reporting Bill (The new way) IASB International Accounts Standard Board (The overseas people that

Accounting 102: Financial Reporting Enviroment FRA Financial Reporting Act (The old way) FRB Financial Reporting Bill (The new way) IASB International Accounts Standard Board (The overseas people that

PRINCIPLES OF FINANCIAL ACCOUNTING ACC-101-TE

TECEP Test Description PRINCIPLES OF FINANCIAL ACCOUNTING ACC-101-TE This TECEP is an introduction to the field of financial accounting. It covers the accounting cycle, merchandising concerns, and financial

TECEP Test Description PRINCIPLES OF FINANCIAL ACCOUNTING ACC-101-TE This TECEP is an introduction to the field of financial accounting. It covers the accounting cycle, merchandising concerns, and financial

ADVANCED ACCOUNTING (02)

") 9 Pages Contestant Number Total Work Time Rank ADVANCED ACCOUNTING (02) State 2002 Objective Portion (30 @ 2 points each) (60 pts.) Production Portion: Job 1 Depreciation (20 pts.) Job 2 Calculating Inventory

9 Pages Contestant Number Total Work Time Rank ADVANCED ACCOUNTING (02) State 2002 Objective Portion (30 @ 2 points each) (60 pts.) Production Portion: Job 1 Depreciation (20 pts.) Job 2 Calculating Inventory

Total Test Questions: 57 Levels: Grades Units of Credit:.50

DESCRIPTION Students will develop advanced skills that build upon those acquired in Accounting I. Students continue applying concepts of double-entry accounting systems related to merchandising businesses.

DESCRIPTION Students will develop advanced skills that build upon those acquired in Accounting I. Students continue applying concepts of double-entry accounting systems related to merchandising businesses.

ACCT 550 Intermediate Accounting Complete Class

ACCT 550 Intermediate Accounting Complete Class https://hwguiders.com/downloads/acct-550-intermediate-accounting-complete-class/ ACCT 550 Intermediate Accounting Complete Class ACCT 550 Week 1 Homework

ACCT 550 Intermediate Accounting Complete Class https://hwguiders.com/downloads/acct-550-intermediate-accounting-complete-class/ ACCT 550 Intermediate Accounting Complete Class ACCT 550 Week 1 Homework

Job Ready Assessment Blueprint

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

CHAPTER 11. Financial Reporting Concepts ANSWERS TO QUESTIONS

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

PANCHAKSHARI S PROFESSIONAL ACADEMY PVT. LTD. CPT Account Test: Final A/C, Inventory, Sale on Approval a) Rs. 15,300 b) Rs.

Rs. 15,300 b) Rs.") CPT Account Test: Final A/C, Inventory, Sale on Approval Marks: 60 Timing: 1hrs. Consider the following data pertaining to N Ltd for the month of March 2005: Date Purchases Issues Balance Quantity Rate

CPT Account Test: Final A/C, Inventory, Sale on Approval Marks: 60 Timing: 1hrs. Consider the following data pertaining to N Ltd for the month of March 2005: Date Purchases Issues Balance Quantity Rate

Twin Valley School District. What is the purpose and importance of accounting? Who are the users of accounting information?

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

INTRODUCTION TO FINANCIAL ACCOUNTING MGCR211 - All sections October 21 st, :00PM - 5:00PM SOLUTION. McGill ID:

October 21, 2016 Midterm Examination INTRODUCTION TO FINANCIAL ACCOUNTING MGCR211 - All sections October 21 st, 2016 3:00PM - 5:00PM SOLUTION Please pick your professor: Professor: Jorien Pruijssers Seda

October 21, 2016 Midterm Examination INTRODUCTION TO FINANCIAL ACCOUNTING MGCR211 - All sections October 21 st, 2016 3:00PM - 5:00PM SOLUTION Please pick your professor: Professor: Jorien Pruijssers Seda

Rate = 1 n RV / C Where: RV = Residual Value C = Cost n = Life of Asset Calculate the rate if: Cost = 100,000

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Accounting 2001 Midterm Exam For Review

Accounting 2001 Midterm Exam For Review PAGEl MULTIPLE CHOICE 1. Which of the following could not possibly be a closing entry? a. Debit Income Summary and credit Retained Earnings b. Debit Retained Earnings

Accounting 2001 Midterm Exam For Review PAGEl MULTIPLE CHOICE 1. Which of the following could not possibly be a closing entry? a. Debit Income Summary and credit Retained Earnings b. Debit Retained Earnings

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: MEMORIAL UNIVERSITY OF NEWFOUNDLAND FACULTY OF BUSINESS BUSINESS 6100 TERM TEST # 2 - Value - 30% of your final grade March 2016 Version 1

Name: MEMORIAL UNIVERSIY OF NEWFOUNDLAND FACULY OF BUSINESS BUSINESS 6100 ERM ES # 2 - Value - 30% of your final grade March 2016 Version 1 Question Marks Suggested ime 1 12 9 minutes 2 15 11 minutes 3

Name: MEMORIAL UNIVERSIY OF NEWFOUNDLAND FACULY OF BUSINESS BUSINESS 6100 ERM ES # 2 - Value - 30% of your final grade March 2016 Version 1 Question Marks Suggested ime 1 12 9 minutes 2 15 11 minutes 3

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Accounting I Approved 1/28/05

Accounting I introduces concepts and principles based on a double-entry system of maintaining the electronic and manual financial records for a sole proprietorship, partnership and corporation. It includes

Accounting I introduces concepts and principles based on a double-entry system of maintaining the electronic and manual financial records for a sole proprietorship, partnership and corporation. It includes

MANAGEMENT 2100Y - MIDTERM EXAM SPRING 2013

MANAGEMENT 2100Y - MIDTERM EXAM SPRING 2013 INSTRUCTOR: Steven Dyer STUDENT: INSTRUCTIONS: 1. Programmable calculators are not allowed in this exam. 2. Check that there are 15 pages (including the title

MANAGEMENT 2100Y - MIDTERM EXAM SPRING 2013 INSTRUCTOR: Steven Dyer STUDENT: INSTRUCTIONS: 1. Programmable calculators are not allowed in this exam. 2. Check that there are 15 pages (including the title

Basic Understanding of the Accounting Industry: Basic Understanding of the Accounting Industry:

Texas University Interscholastic League Contest Event: Accounting The contest focuses on the elementary principles and practices of accounting for sole proprietorship, partnerships and corporations, and

Texas University Interscholastic League Contest Event: Accounting The contest focuses on the elementary principles and practices of accounting for sole proprietorship, partnerships and corporations, and

ADVANCED ACCOUNTING (110) Secondary

Secondary") Page 1 of 9 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2018 Multiple Choice (20 @ 2 points each) Short Answer Problem 1 Inventory Costing Problem 2 Uncollectible Accounts

Page 1 of 9 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2018 Multiple Choice (20 @ 2 points each) Short Answer Problem 1 Inventory Costing Problem 2 Uncollectible Accounts

1. On Jan 1, 2003 Wilbur Retailers purchases merchandise on account for $349,000.

Name ID# Accounting 15.501/516 Spring 2004 Midterm 1 Exam Guidelines 1. Fill in your name above. Exams without names will not be graded. If you do not have an ID number, leave the corresponding space blank.

Name ID# Accounting 15.501/516 Spring 2004 Midterm 1 Exam Guidelines 1. Fill in your name above. Exams without names will not be graded. If you do not have an ID number, leave the corresponding space blank.

Zacks Bike Hut. Transactions For June Bank Reconciliation. Level II. 1 st Web-Based Edition. and the

Zacks Bike Hut Level II 1 st Web-Based Edition Transactions For June 24-30 and the Bank Reconciliation Page 1 Heads Up: In this module you will be required to (1) pay a cash dividend previously declared,

Zacks Bike Hut Level II 1 st Web-Based Edition Transactions For June 24-30 and the Bank Reconciliation Page 1 Heads Up: In this module you will be required to (1) pay a cash dividend previously declared,

Name: Class: Date: 1 MULTIPLE CHOICE 11-21

1 MULTIPLE CHOICE 11-21 I certify that I am taking this assessment alone and no help with it other than the use of my textbook and notes. I have not been given these questions in advance, and the results

1 MULTIPLE CHOICE 11-21 I certify that I am taking this assessment alone and no help with it other than the use of my textbook and notes. I have not been given these questions in advance, and the results

Advanced Accounting PRECISION EXAMS DESCRIPTION. EXAM INFORMATION Items

PRECISION EXAMS Advanced Accounting EXAM INFORMATION Items 46 Points 49 Prerequisites ACCOUNTING I AND II RECOMMENDED Grade Level 11-12 Course Length ONE SEMESTER DESCRIPTION In this college prep accounting

PRECISION EXAMS Advanced Accounting EXAM INFORMATION Items 46 Points 49 Prerequisites ACCOUNTING I AND II RECOMMENDED Grade Level 11-12 Course Length ONE SEMESTER DESCRIPTION In this college prep accounting

2. Each of the following is an example of a control procedure, except

Student Academic Resource Center Block 2 Extra Practice by Joana Marinova, Peer Tutor Page 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008.

Student Academic Resource Center Block 2 Extra Practice by Joana Marinova, Peer Tutor Page 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008.

ACCOUNTING, ADVANCED (213)

") DESCRIPTION In this college prep accounting course, students will learn traditional college-level financial accounting concepts integrated with managerial accounting concepts. Students will first gain

DESCRIPTION In this college prep accounting course, students will learn traditional college-level financial accounting concepts integrated with managerial accounting concepts. Students will first gain

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A Class: Date: Subject: Accounting Instructor: Zaheer A. Swati Time Allowed: 30 Minutes Max Marks:

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A Class: Date: Subject: Accounting Instructor: Zaheer A. Swati Time Allowed: 30 Minutes Max Marks:

Heintz & Parry. 20 th Edition. College Accounting 10-1

Heintz & Parry 20 th Edition College Accounting 10-1 Chapter 11 Accounting for Purchases and Cash Payments 1 Define merchandise purchases transactions. Merchandise acquired for resale Must be items for

Heintz & Parry 20 th Edition College Accounting 10-1 Chapter 11 Accounting for Purchases and Cash Payments 1 Define merchandise purchases transactions. Merchandise acquired for resale Must be items for

CHAPTER 22. Accounting Changes and Error Analysis

CHAPTER 22 Accounting Changes and Error Analysis OPTIONAL ASSIGNMENT CHARACTERISTICS TABLE Item BE22-1 BE22-3 BE22-6 BE22-8 Description Change in principle long-term contracts (tax effect deferred tax

CHAPTER 22 Accounting Changes and Error Analysis OPTIONAL ASSIGNMENT CHARACTERISTICS TABLE Item BE22-1 BE22-3 BE22-6 BE22-8 Description Change in principle long-term contracts (tax effect deferred tax