Data-Driven Financial Conduct Regulation: the FCA s remit, datasets and research, and opportunities for collaboration

|

|

|

- Hugh Pearson

- 5 years ago

- Views:

Transcription

1 Data-Driven Financial Conduct Regulation: the FCA s remit, datasets and research, and opportunities for collaboration Dr Stefan Hunt Head of Behavioural Economics and Data Science Big Data Analytics for Financial Services, UCL 7 th January

2 Remit of the FCA We regulate most of the UK financial markets. Retail: - Savings and investments - Consumer credit - Mortgages - Insurance - and wholesale: - Investment banking - Fund management - 2 Number correct as at 6 January Does not include consumer credit firms with interim permissions. Other firms are mainly consumer credit

3 Objectives and powers Strategic objective Ensure that financial markets function well Operational objectives Market integrity Consumer Protection Promoting effective competition The FCA intervenes in markets through: Authorising firms and people to operate Policy-making: creating laws Supervision: check compliance Enforcement: prosecution and punishment increasingly using competition analysis

4 Key FCA data sets Wholesale: 1. Financial transactions / Zen 2. EMIR (interest rates, OTC derivatives) 3. AIFMD (hedge funds) Retail: 4. Payday lending 5. Credit card statements (~ all statements for last five years) 6. Credit bureau files 7. Personal current account micro data 8. Data from large field experiments (e.g. savings, insurance), matched with surveys 9. Product sales data (retail products, mortgages good quality) Firms and employees: 10.Firms regulatory submissions, consumer complaints etc. 11.Employees authorisations and records

5 The data ecosystem Firm regular & ad-hoc submissions Complaints & supervisory data Supervision, Enforcement etc. Credit bureaus Surveys ONS Other Social media Data Audit and ingest Elastic high-performance cloud storage Machine learning & statistical models Visualisation

6 Payday lending price cap Parliament created duty to impose cap on high-cost shortterm credit. Structure and level decided by FCA Questions: 1 What happens to firms and firms lending decisions? 2 What options are there for consumers without access to loans? Are they better or worse off?

7 Data 7 Requested data using formal legal powers Data on payday loans in : top 37 lenders, ~99% market For 11 lenders, ~90% market, all applications, denied and accepted, including lender credit score and revenues and costs Match applicants across firms and to credit bureau files using unique identifier. 6 years of data including loan applications, holding and balances, credit events, defaults and credit bureau credit scores Dataset of vast majority of first-time loan applications, ~1.9million applicants (observe 4.6 million people, ~10% of adult population)

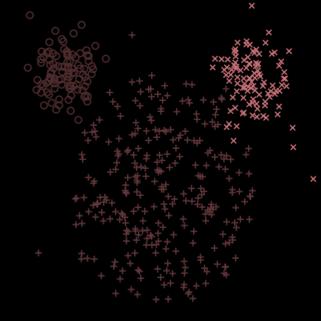

8 Recreating lending decisions: credit scores Good credit score ROC = Receiver Operating Characteristic 45 o credit score has no explanatory power 8

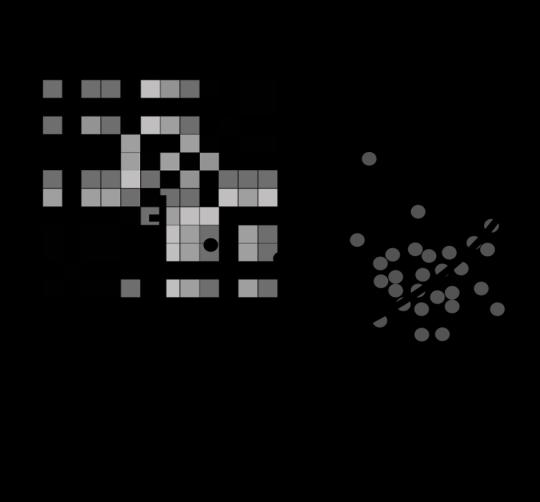

9 Example: Impact on customer profitability Expected Customer Lifetime Profitability Before Cap After Cap Credit score 9

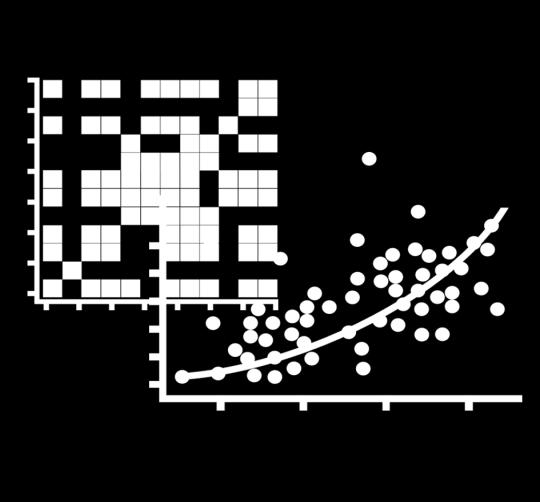

10 Use regression discontinuity design to estimate causal effect of payday loans Probability of getting payday loan 1 st Stage: 2 nd Stage: Probability of missing a nonpayday payment 80% 40% 80% 60% 5.9% causal impact of payday on missing payments 0% % Internal Credit Score 10

11 Causal impact of payday loan use on consumers Change in likelihood of exceeding overdraft limit 95% confidence interval Evidence suggests payday use worsens financial outcomes Use behavioural models to assess welfare impacts Months relative to first loan application Next step: identify heterogeneous treatment effects, who is gaining and losing, using data science methods (Athey and Imbens, 2015)

12 More practical examples of using research Retail: 1. Impact of annual summaries, mobile banking and SMS alerts in personal current accounts 2. Field experiments on information disclosures in savings and car and home insurance Wholesale: 3. Impact of high-frequency trading on institutional investors 12

13 Data Science Roadmap Machine-driven compliance Text Analytics Mis-selling or failure propensity Clustering Data Harmonisation Data collection & audit Feature Engineering Predictive Analytics Proactive Regulation Visualisation

14 Summary DATA: FCA collects rich transaction data + legal powers to gather more data METHODS: Undertaken rigorous, ground-breaking empirical research to inform policies. Starting to use range of data science methods PEOPLE: Empirical economists + data scientists OPEN: Open to new ideas for research + collaboration. Regularly work with world-leading academics + aim to publish in top journals ACCESSIBLE: Creating high-specification secure cloud environment facilitating off-site access 14 REAL-WORLD RELEVANT: Research has to be immediately usable to inform policymakers

15 > print( Thank you )

Data Sharing in Regulation Experiences from the UK

Data Sharing in Regulation Experiences from the UK Sebastian de-ramon Prudential Policy Directorate 5th October 2017 Disclaimer The views expressed in this paper are those of the author, and not necessarily

Data Sharing in Regulation Experiences from the UK Sebastian de-ramon Prudential Policy Directorate 5th October 2017 Disclaimer The views expressed in this paper are those of the author, and not necessarily

Comments on: How do Payday Loans Affect Consumer Finances? by John Gathergood, Ben Guttman-Kenney and Stefan Hunt

Comments on: How do Payday Loans Affect Consumer Finances? by John Gathergood, Ben Guttman-Kenney and Stefan Hunt Justin Wolfers University of Michigan also Brookings, CEPR, CESifo, IZA, PIIE and NBER

Comments on: How do Payday Loans Affect Consumer Finances? by John Gathergood, Ben Guttman-Kenney and Stefan Hunt Justin Wolfers University of Michigan also Brookings, CEPR, CESifo, IZA, PIIE and NBER

Data Analytics and Unstructured Data Actuaries 2.0

Data Analytics and Unstructured Data Actuaries 2.0 David Brown, KPMG Gary Richardson, KPMG 13 June 2014 Empowering Underwriters to listen to the whole data conversation High volume, velocity, variety New

Data Analytics and Unstructured Data Actuaries 2.0 David Brown, KPMG Gary Richardson, KPMG 13 June 2014 Empowering Underwriters to listen to the whole data conversation High volume, velocity, variety New

Risk Management and Credit Scoring

Study Unit 5 Risk Management and Credit Scoring ANL 309 Business Analytics Applications Introduction Importance of risk management in CRM Credit Risk Management Cycle (CRMC) Credit scoring Simple credit

Study Unit 5 Risk Management and Credit Scoring ANL 309 Business Analytics Applications Introduction Importance of risk management in CRM Credit Risk Management Cycle (CRMC) Credit scoring Simple credit

Policy Evaluation: Methods for Testing Household Programs & Interventions

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Transfer of consumer credit to the Financial Conduct Authority. Sam Stoakes

Transfer of consumer credit to the Financial Conduct Authority. Sam Stoakes 1 1 April 2014 Financial Conduct Authority takes over consumer credit regulation from the Office of Fair Trading This creates

Transfer of consumer credit to the Financial Conduct Authority. Sam Stoakes 1 1 April 2014 Financial Conduct Authority takes over consumer credit regulation from the Office of Fair Trading This creates

The FCA s response to the CMA s consultation on its provisional decision to refer personal current accounts and SME banking

Financial Conduct Authority The FCA s response to the CMA s consultation on its provisional decision to refer personal current accounts and SME banking September 2014 Contents 1 Executive summary 2 2

Financial Conduct Authority The FCA s response to the CMA s consultation on its provisional decision to refer personal current accounts and SME banking September 2014 Contents 1 Executive summary 2 2

ESMA Risk Assessment Work Programme 2019

ESMA Risk Assessment Work Programme 2019 7 February 2019 ESMA50-157-1588 Table of Contents 1 Summary... 3 2 Introduction... 4 2.1 Objectives of ESMA Risk Assessment... 4 2.2 Coverage... 4 2.2.1 Risk monitoring

ESMA Risk Assessment Work Programme 2019 7 February 2019 ESMA50-157-1588 Table of Contents 1 Summary... 3 2 Introduction... 4 2.1 Objectives of ESMA Risk Assessment... 4 2.2 Coverage... 4 2.2.1 Risk monitoring

2018 Report. July 2018

2018 Report July 2018 Foreword This year the FCA and FCA Practitioner Panel have, for the second time, carried out a joint survey of regulated firms to monitor the industry s perception of the FCA and

2018 Report July 2018 Foreword This year the FCA and FCA Practitioner Panel have, for the second time, carried out a joint survey of regulated firms to monitor the industry s perception of the FCA and

Data Bulletin May 2017

Data Bulletin May 2017 In focus: The retail intermediary sector Latest trends in activities and revenues Issue 9 1 Introduction Financial Conduct Authority Introduction from the editor Jo Hill Director

Data Bulletin May 2017 In focus: The retail intermediary sector Latest trends in activities and revenues Issue 9 1 Introduction Financial Conduct Authority Introduction from the editor Jo Hill Director

THE APPLICATION OF AI IN ENTERPRISE FOR IMPROVED PERFORMANCE, INNOVATION & CUSTOMER EXPERIENCE.

1 THE APPLICATION OF AI IN ENTERPRISE FOR IMPROVED PERFORMANCE, INNOVATION & CUSTOMER EXPERIENCE F E B R UA RY 2 0 1 8 2 Company overview. 3 is living the Megatrends right here in Africa. MyBucks Technology.

1 THE APPLICATION OF AI IN ENTERPRISE FOR IMPROVED PERFORMANCE, INNOVATION & CUSTOMER EXPERIENCE F E B R UA RY 2 0 1 8 2 Company overview. 3 is living the Megatrends right here in Africa. MyBucks Technology.

Executive Summary of the Payday, Vehicle Title, and Certain High-Cost Installment Loans Rule

1700 G Street NW, Washington, DC 20552 October 5, 2017 Executive Summary of the Payday, Vehicle Title, and Certain High-Cost Installment Loans Rule The Consumer Financial Protection Bureau (Bureau) has

1700 G Street NW, Washington, DC 20552 October 5, 2017 Executive Summary of the Payday, Vehicle Title, and Certain High-Cost Installment Loans Rule The Consumer Financial Protection Bureau (Bureau) has

Application Form for Alternative Mortgage Repayments

Application Form for Alternative Mortgage Repayments Documents checklist Borrower 1 Borrower 2 A property valuation must be carried out prior to the assessment of all Voluntary Sale cases. Your Intermediary

Application Form for Alternative Mortgage Repayments Documents checklist Borrower 1 Borrower 2 A property valuation must be carried out prior to the assessment of all Voluntary Sale cases. Your Intermediary

High-cost credit Including review of the high-cost short-term credit price cap

Including review of the high-cost short-term credit price cap Feedback Statement FS17/2 July 2017 FS17/2 This relates to Contents In this Feedback Statement we report on the main issues arising from Call

Including review of the high-cost short-term credit price cap Feedback Statement FS17/2 July 2017 FS17/2 This relates to Contents In this Feedback Statement we report on the main issues arising from Call

Question 1: Do you have evidence of misleading or unfair advertising or marketing practices with regard to mortgage and consumer credit?

Responsible Lending and Borrowing The Financial Regulator welcomes the Commission s undertaking, following this consultation, to come forward with measures at EU level on responsible lending and borrowing.

Responsible Lending and Borrowing The Financial Regulator welcomes the Commission s undertaking, following this consultation, to come forward with measures at EU level on responsible lending and borrowing.

TRANSUNION ADFUEL Audience Buying Guide

TRANSUNION ADFUEL Audience Buying Guide TU AdfuelSM Make the Right Impressionsm The Financial Services and Insurance Industries trusted source for consumer finance and small business audiences Q2, 2016

TRANSUNION ADFUEL Audience Buying Guide TU AdfuelSM Make the Right Impressionsm The Financial Services and Insurance Industries trusted source for consumer finance and small business audiences Q2, 2016

David Malcolm Strategy & Competition Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 08 February 2017

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk David Malcolm Strategy & Competition Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 08 February 2017 Dear David, Call

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk David Malcolm Strategy & Competition Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 08 February 2017 Dear David, Call

Special Alert: CFPB Issues Rule Regarding Payday, Title, Deposit Advance, and Certain Other Installment Loans

Special Alert: CFPB Issues Rule Regarding Payday, Title, Deposit Advance, and Certain Other Installment Loans On October 5, 2017, the CFPB published its final rule (the Rule ) addressing payday loans,

Special Alert: CFPB Issues Rule Regarding Payday, Title, Deposit Advance, and Certain Other Installment Loans On October 5, 2017, the CFPB published its final rule (the Rule ) addressing payday loans,

Financial Conduct Authority Proposals for a price cap on high cost short term credit

Financial Conduct Authority Consultation Paper CP14/10*** Proposals for a price cap on high cost short term credit July 2014 Contents Abbreviations used in this document 3 1 Executive summary 5 2 Overview

Financial Conduct Authority Consultation Paper CP14/10*** Proposals for a price cap on high cost short term credit July 2014 Contents Abbreviations used in this document 3 1 Executive summary 5 2 Overview

Reduced Repayment Application Form For Alternative Mortgage Repayments

Reduced Repayment Application Form For Alternative Mortgage Repayments How to complete the form 1 Please use a BLACK pen 2 Mark boxes like this If you make a mistake, do this and mark the correct box 3

Reduced Repayment Application Form For Alternative Mortgage Repayments How to complete the form 1 Please use a BLACK pen 2 Mark boxes like this If you make a mistake, do this and mark the correct box 3

This helpful resource translates some commonly used financial terms into plain English.

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

The Effects of Supervision on Bank Performance: Evidence from Discontinuous Examination Frequencies

The Effects of Supervision on Bank Performance: Evidence from Discontinuous Examination Frequencies Marcelo Rezende and Jason Wu 1 Federal Reserve Board 1 The views expressed herein are my own and do not

The Effects of Supervision on Bank Performance: Evidence from Discontinuous Examination Frequencies Marcelo Rezende and Jason Wu 1 Federal Reserve Board 1 The views expressed herein are my own and do not

Moneylending Review of the Consumer Protection Code for Licensed Moneylenders. Consultation Paper CP 118

Moneylending Review of the Consumer Protection Code for Licensed Moneylenders Consultation Paper CP 118 March 2018 [Type here] Review of the Consumer Protection Code for Licensed Moneylenders 1 Contents

Moneylending Review of the Consumer Protection Code for Licensed Moneylenders Consultation Paper CP 118 March 2018 [Type here] Review of the Consumer Protection Code for Licensed Moneylenders 1 Contents

Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay.

Fixed Fee Account Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay. Choose the account plan that best suits your

Fixed Fee Account Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay. Choose the account plan that best suits your

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau. April 4, Dear Mr.

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau April 4, 2014 Dear Mr. Silberman, The Assets & Opportunity Network (the Network) is grateful for

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau April 4, 2014 Dear Mr. Silberman, The Assets & Opportunity Network (the Network) is grateful for

Pecuniary Mistakes? Payday Borrowing by Credit Union Members

Chapter 8 Pecuniary Mistakes? Payday Borrowing by Credit Union Members Susan P. Carter, Paige M. Skiba, and Jeremy Tobacman This chapter examines how households choose between financial products. We build

Chapter 8 Pecuniary Mistakes? Payday Borrowing by Credit Union Members Susan P. Carter, Paige M. Skiba, and Jeremy Tobacman This chapter examines how households choose between financial products. We build

Payday Futures: Sub-Prime Credit Markets In Transition?

Payday Futures: Sub-Prime Credit Markets In Transition? Carl Packman, Research and Good Practice Manager, Toynbee Hall Dr Lindsey Appleyard, Research Fellow, Centre for Business in Society (CBiS) Partnership

Payday Futures: Sub-Prime Credit Markets In Transition? Carl Packman, Research and Good Practice Manager, Toynbee Hall Dr Lindsey Appleyard, Research Fellow, Centre for Business in Society (CBiS) Partnership

Welcome to the FinCoNet newsletter

Issue 1 March 2019 201420140142014 CONTENTS Welcome 1 In focus 2 Current issues forum 4 Microfinance: new caps for marginal debt value and daily interest rate Conduct of Business Returns for the South

Issue 1 March 2019 201420140142014 CONTENTS Welcome 1 In focus 2 Current issues forum 4 Microfinance: new caps for marginal debt value and daily interest rate Conduct of Business Returns for the South

1. Use a plan to manage spending and achieve financial goals. Unit 1, Ch. 1, 2, 3

Washington STATE STANDARD OR BENCHMARK: CORRELATES WITH: Spending and Saving 9.SS Financial Education Grade 9 Develop a plan for spending and saving. 1. Use a plan to manage spending and achieve financial

Washington STATE STANDARD OR BENCHMARK: CORRELATES WITH: Spending and Saving 9.SS Financial Education Grade 9 Develop a plan for spending and saving. 1. Use a plan to manage spending and achieve financial

Machine Learning Applications in Insurance

General Public Release Machine Learning Applications in Insurance Nitin Nayak, Ph.D. Digital & Smart Analytics Swiss Re General Public Release Machine learning is.. Giving computers the ability to learn

General Public Release Machine Learning Applications in Insurance Nitin Nayak, Ph.D. Digital & Smart Analytics Swiss Re General Public Release Machine learning is.. Giving computers the ability to learn

REDUCING DEFAULT RATES OF REVERSE MORTGAGES

July 2016, Number 16-11 RETIREMENT RESEARCH REDUCING DEFAULT RATES OF REVERSE MORTGAGES By Stephanie Moulton, Donald R. Haurin, and Wei Shi* Introduction For many U.S. households, Social Security benefits

July 2016, Number 16-11 RETIREMENT RESEARCH REDUCING DEFAULT RATES OF REVERSE MORTGAGES By Stephanie Moulton, Donald R. Haurin, and Wei Shi* Introduction For many U.S. households, Social Security benefits

Dan Waters, FSA Director of Retail Policy and Themes. and Sector Leader, Asset Management. 8 April Testimony to the European Parliament

Dan Waters, FSA Director of Retail Policy and Themes and Sector Leader, Asset Management 8 April Testimony to the European Parliament ECON: Economic and Monetary Affairs Committee Public Hearing on Hedge

Dan Waters, FSA Director of Retail Policy and Themes and Sector Leader, Asset Management 8 April Testimony to the European Parliament ECON: Economic and Monetary Affairs Committee Public Hearing on Hedge

GET SOCIAL WITH US. #vision2016. Tweet, follow, share throughout the session.

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

AN APPROACH TO RISK-BASED MARKET CONDUCT REGULATION

CCIR Canadian Council of Insurance Regulators AN APPROACH TO RISK-BASED MARKET CONDUCT REGULATION Conseil canadien des responsables de la réglementation d assurance A report prepared by the Canadian Council

CCIR Canadian Council of Insurance Regulators AN APPROACH TO RISK-BASED MARKET CONDUCT REGULATION Conseil canadien des responsables de la réglementation d assurance A report prepared by the Canadian Council

ESMA Risk Assessment Work Programme 2018

ESMA Risk Assessment Work Programme 2018 9 February 2018 ESMA20-95-839 Table of Contents 1 Summary... 3 2 Introduction... 4 2.1 Objectives of ESMA Risk Assessment... 4 2.2 Coverage... 4 2.2.1 Risk monitoring

ESMA Risk Assessment Work Programme 2018 9 February 2018 ESMA20-95-839 Table of Contents 1 Summary... 3 2 Introduction... 4 2.1 Objectives of ESMA Risk Assessment... 4 2.2 Coverage... 4 2.2.1 Risk monitoring

Citizens Advice Scotland Scottish Association of Citizens Advice Bureaux

Citizens Advice Scotland Scottish Association of Citizens Advice Bureaux www.cas.org.uk Financial Conduct Authority Detailed proposals for the FCA regime for consumer credit Response from Citizens Advice

Citizens Advice Scotland Scottish Association of Citizens Advice Bureaux www.cas.org.uk Financial Conduct Authority Detailed proposals for the FCA regime for consumer credit Response from Citizens Advice

CONSUMER CREDIT (CREDIT BROKING) INSTRUMENT 2014

INSTRUMENT 2014") CONSUMER CREDIT (CREDIT BROKING) INSTRUMENT 2014 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the following powers and related provisions in the Financial

CONSUMER CREDIT (CREDIT BROKING) INSTRUMENT 2014 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the following powers and related provisions in the Financial

Investor Presentation. November 2015

Investor Presentation November 2015 Safe Harbor Statement Cautionary Statement Regarding Risks and Uncertainties That May Affect Future Results This presentation contains forward-looking statements within

Investor Presentation November 2015 Safe Harbor Statement Cautionary Statement Regarding Risks and Uncertainties That May Affect Future Results This presentation contains forward-looking statements within

Report on Impact of CFPB Proposals Under Consideration on the State of South Carolina Consumer Lending Market September 28, 2015

Report on Impact of CFPB Proposals Under Consideration on the State of South Carolina Consumer Lending Market September 28, 2015 Prepared for the State of South Carolina Board of Financial Institutions

Report on Impact of CFPB Proposals Under Consideration on the State of South Carolina Consumer Lending Market September 28, 2015 Prepared for the State of South Carolina Board of Financial Institutions

Agreement terms M&S CREDIT CARD. Key terms

M&S CREDIT CARD Agreement terms Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key terms How much can you borrow?

M&S CREDIT CARD Agreement terms Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key terms How much can you borrow?

DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA

October 2014 DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA Report Prepared for the Oklahoma Assets Network by Haydar Kurban Adji Fatou Diagne 0 This report was prepared for the Oklahoma Assets Network by

October 2014 DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA Report Prepared for the Oklahoma Assets Network by Haydar Kurban Adji Fatou Diagne 0 This report was prepared for the Oklahoma Assets Network by

Unsecured business loans Intermediary enquiry form

Unsecured business loans Intermediary enquiry form 01202 850 830 Intermediary details Contact name: Phone: Company: Email: Intermediary address and postcode: Intermediary fees Do you wish to add these

Unsecured business loans Intermediary enquiry form 01202 850 830 Intermediary details Contact name: Phone: Company: Email: Intermediary address and postcode: Intermediary fees Do you wish to add these

THE FCA PRACTITIONER PANEL S. Response to HM Treasury s Review of the Balance of Competences:

THE FCA PRACTITIONER PANEL S Response to HM Treasury s Review of the Balance of Competences: Single Market: Financial Services and the Free Movement of Capital - call for evidence 17 January 2014 1 1.

THE FCA PRACTITIONER PANEL S Response to HM Treasury s Review of the Balance of Competences: Single Market: Financial Services and the Free Movement of Capital - call for evidence 17 January 2014 1 1.

The Financial Services Consumer Panel welcomes the opportunity to respond to the FCA s consultation on High-cost Credit Review: Overdrafts.

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk Neil Marshall Financial Conduct Authority 12 Endeavour Square London E20 1JN 31 August 2018 By email: cp18-13@fca.org.uk Dear Neil, CP18/13 High-cost

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk Neil Marshall Financial Conduct Authority 12 Endeavour Square London E20 1JN 31 August 2018 By email: cp18-13@fca.org.uk Dear Neil, CP18/13 High-cost

CMA Market investigation into payday lending notice of possible remedies

CMA Market investigation into payday lending notice of Response by the Money Advice Trust Date: JULY 2014 Contents Page 2 Page 3 Page 4 Page 5 Contents Introduction / About the Money Advice Trust Introductory

CMA Market investigation into payday lending notice of Response by the Money Advice Trust Date: JULY 2014 Contents Page 2 Page 3 Page 4 Page 5 Contents Introduction / About the Money Advice Trust Introductory

LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT

45 LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT Edward M. Gramlich Member, Board of Governors of the Federal Reserve System Introduction I am pleased to be here today to kick off the conference

45 LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT Edward M. Gramlich Member, Board of Governors of the Federal Reserve System Introduction I am pleased to be here today to kick off the conference

Committee on Development and Intellectual Property (CDIP)

") E CDIP/14/7 ORIGINAL: ENGLISH DATE: SEPTEMBER 22, 2014 Committee on Development and Intellectual Property (CDIP) Fourteenth Session Geneva, November 10 to 14, 2014 PROJECT ON INTELLECTUAL PROPERTY (IP)

E CDIP/14/7 ORIGINAL: ENGLISH DATE: SEPTEMBER 22, 2014 Committee on Development and Intellectual Property (CDIP) Fourteenth Session Geneva, November 10 to 14, 2014 PROJECT ON INTELLECTUAL PROPERTY (IP)

Secured and Unsecured (1)

") LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia)

BERHAD (Incorporated in Malaysia)") UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS FOR THE FINANCIAL HALF YEAR ENDED 30 JUNE 2018 UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2018 ASSETS

UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS FOR THE FINANCIAL HALF YEAR ENDED 30 JUNE 2018 UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2018 ASSETS

ESMA Risk Assessment Work Programme 2017

ESMA Risk Assessment Work Programme 2017 ESMA50-1121423017-286 Table of Contents 1 Summary... 3 2 Introduction... 4 2.1 Objectives of ESMA Risk Assessment... 4 2.2 Coverage... 4 2.2.1 Risk monitoring and

ESMA Risk Assessment Work Programme 2017 ESMA50-1121423017-286 Table of Contents 1 Summary... 3 2 Introduction... 4 2.1 Objectives of ESMA Risk Assessment... 4 2.2 Coverage... 4 2.2.1 Risk monitoring and

Details of FCA Consumer Credit Regime (13/29) 14 October 2013

14 October 2013") CPA Audit LLP, Talbot House, 8-9 Talbot Court, London EC3V 0BP Telephone: 020 7621 9010 Facsimile: 020 7621 9011 email: info@cpaaudit.co.uk web: www.cpaaudit.co.uk Details of FCA Consumer Credit Regime

CPA Audit LLP, Talbot House, 8-9 Talbot Court, London EC3V 0BP Telephone: 020 7621 9010 Facsimile: 020 7621 9011 email: info@cpaaudit.co.uk web: www.cpaaudit.co.uk Details of FCA Consumer Credit Regime

Modification By Consent for a Hybrid Lifetime Mortgage

Modification By Consent for a Hybrid Lifetime Mortgage To: [ ] (the firm") Ref: [ ] Of: [ ] Date: [ ] Handbook Version as in force at the date of this Direction Power 1. This direction is given by the

Modification By Consent for a Hybrid Lifetime Mortgage To: [ ] (the firm") Ref: [ ] Of: [ ] Date: [ ] Handbook Version as in force at the date of this Direction Power 1. This direction is given by the

first direct Credit Card Terms

first direct Credit Card Terms Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key Terms How much can you borrow? You

first direct Credit Card Terms Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key Terms How much can you borrow? You

A guide to joining the CFA

A guide to joining the CFA Working for your business There are many excellent reasons to join the CFA. By becoming a member you won t just get information about all the latest developments in the industry,

A guide to joining the CFA Working for your business There are many excellent reasons to join the CFA. By becoming a member you won t just get information about all the latest developments in the industry,

Outline. Consumers generate Big Data. Big Data and Economic Modeling. Economic Modeling with Big Data: Understanding Consumer Overdrafting at Banks

Economic Modeling with Big Data: Understanding Consumer Overdrafting at Banks Xiao Liu, Alan L. Montgomery and Kannan Srinivasan Tepper School of Business Carnegie Mellon University Outline Big Data and

Economic Modeling with Big Data: Understanding Consumer Overdrafting at Banks Xiao Liu, Alan L. Montgomery and Kannan Srinivasan Tepper School of Business Carnegie Mellon University Outline Big Data and

While real incomes in the lower and middle portions of the U.S. income distribution have

CONSUMPTION CONTAGION: DOES THE CONSUMPTION OF THE RICH DRIVE THE CONSUMPTION OF THE LESS RICH? BY MARIANNE BERTRAND AND ADAIR MORSE (CHICAGO BOOTH) Overview While real incomes in the lower and middle

CONSUMPTION CONTAGION: DOES THE CONSUMPTION OF THE RICH DRIVE THE CONSUMPTION OF THE LESS RICH? BY MARIANNE BERTRAND AND ADAIR MORSE (CHICAGO BOOTH) Overview While real incomes in the lower and middle

Report 9. Evaluating CFPB Simulations of the Impact of Proposed Rules on Storefront Payday Lending BY RICK HACKETT

Report 9 n o n P r i m e 1 0 1 W H I T E P A P E R Evaluating CFPB Simulations of the Impact of Proposed Rules on Storefront Payday Lending BY RICK HACKETT E V A L U A T I N G C F P B S I M U L A T I O

Report 9 n o n P r i m e 1 0 1 W H I T E P A P E R Evaluating CFPB Simulations of the Impact of Proposed Rules on Storefront Payday Lending BY RICK HACKETT E V A L U A T I N G C F P B S I M U L A T I O

Broad and Deep: The Extensive Learning Agenda in YouthSave

Broad and Deep: The Extensive Learning Agenda in YouthSave Center for Social Development August 17, 2011 Campus Box 1196 One Brookings Drive St. Louis, MO 63130-9906 (314) 935.7433 www.gwbweb.wustl.edu/csd

Broad and Deep: The Extensive Learning Agenda in YouthSave Center for Social Development August 17, 2011 Campus Box 1196 One Brookings Drive St. Louis, MO 63130-9906 (314) 935.7433 www.gwbweb.wustl.edu/csd

Executive Order on Investor Protection in connection with Securities Trading 1)

") While this translation was carried out by a professional translation agency, the text is to be regarded as an unofficial translation based on the latest official Executive Order no. 964 of 30 September

While this translation was carried out by a professional translation agency, the text is to be regarded as an unofficial translation based on the latest official Executive Order no. 964 of 30 September

Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters

A brief from Feb 2015 Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters Overview According to an analysis of banks account data published by the Consumer

A brief from Feb 2015 Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters Overview According to an analysis of banks account data published by the Consumer

BCAP Payday Loans Consultation Evaluation of responses

BCAP Payday Loans Consultation Evaluation of responses 1 1. Introduction The Broadcast Committee of Advertising Practice (BCAP) has decided not to introduce scheduling restrictions on the television advertising

BCAP Payday Loans Consultation Evaluation of responses 1 1. Introduction The Broadcast Committee of Advertising Practice (BCAP) has decided not to introduce scheduling restrictions on the television advertising

FREQUENTLY ASKED QUESTIONS THE CENTRAL CREDIT REGISTER

FREQUENTLY ASKED QUESTIONS THE CENTRAL CREDIT REGISTER Q 1: What is The Central Credit Register (the CCR )? A: The CCR is a new secure system set-up by the Central Bank of Ireland (the Bank ) for the collection

FREQUENTLY ASKED QUESTIONS THE CENTRAL CREDIT REGISTER Q 1: What is The Central Credit Register (the CCR )? A: The CCR is a new secure system set-up by the Central Bank of Ireland (the Bank ) for the collection

Statement regarding IOSCO Principles

Statement regarding IOSCO Principles Introduction The "Principles for Financial Benchmarks" ("Principles") were published by the International Organization of Securities Commissions ( IOSCO ) on 17 July

Statement regarding IOSCO Principles Introduction The "Principles for Financial Benchmarks" ("Principles") were published by the International Organization of Securities Commissions ( IOSCO ) on 17 July

Financial Conduct Authority. Call for Input: High-cost credit Including review of the high-cost short-term credit price cap

Call for Input: High-cost credit Including review of the high-cost short-term credit price cap November 2016 Contents Abbreviations used in this document 3 1. Overview 5 Section 1: High-cost credit 2.

Call for Input: High-cost credit Including review of the high-cost short-term credit price cap November 2016 Contents Abbreviations used in this document 3 1. Overview 5 Section 1: High-cost credit 2.

The Roadmap. The Evolution of Irish Loan-Level Data. Central Credit Register 201X. 2013: A better Loan Level Database. 2011: A Loan Level database

The Evolution of Irish Loan-Level Data Workshop on Integrated Management of Micro-databases 20 June 2013 Rory McElligott, Central Bank of Ireland The Roadmap 2011: A Loan Level database 2013: A better

The Evolution of Irish Loan-Level Data Workshop on Integrated Management of Micro-databases 20 June 2013 Rory McElligott, Central Bank of Ireland The Roadmap 2011: A Loan Level database 2013: A better

Expert Analysis Understanding the Evolving Legal And Regulatory Landscape for Consumer Marketplace Lending

Westlaw Journal bank & Lender Liability Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 21, issue 19 / february 8, 2016 Expert Analysis Understanding the Evolving Legal And

Westlaw Journal bank & Lender Liability Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 21, issue 19 / february 8, 2016 Expert Analysis Understanding the Evolving Legal And

The importance of regulating in the FinTech s world for the protection of consumers

The importance of regulating in the FinTech s world for the protection of consumers Călin Rangu Business Conduct Director, Authority of Financial Supervision Vice-president InsurTech Task Force, EIOPA-European

The importance of regulating in the FinTech s world for the protection of consumers Călin Rangu Business Conduct Director, Authority of Financial Supervision Vice-president InsurTech Task Force, EIOPA-European

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Investor Presentation. February 2015

Investor Presentation February 2015 Safe Harbor Statement Cautionary Statement Regarding Risks and Uncertainties That May Affect Future Results This presentation may contain forward-looking statements

Investor Presentation February 2015 Safe Harbor Statement Cautionary Statement Regarding Risks and Uncertainties That May Affect Future Results This presentation may contain forward-looking statements

NOTES FOR COMPLETION OF THE DATA ITEMS RELATING TO CONSUMER CREDIT ACTIVITIES

16 Annex 38BG NOTES FOR COMPLETION OF THE DATA ITEMS RELATING TO CONSUMER CREDIT ACTIVITIES Contents Introduction CCR001: CCR002: CCR003: CCR004: CCR005: CCR006: CCR007: General notes on the data items

16 Annex 38BG NOTES FOR COMPLETION OF THE DATA ITEMS RELATING TO CONSUMER CREDIT ACTIVITIES Contents Introduction CCR001: CCR002: CCR003: CCR004: CCR005: CCR006: CCR007: General notes on the data items

Real-time Driver Profiling & Risk Assessment for Usage-based Insurance with StreamAnalytix

Real-time Driver Profiling & Risk Assessment for Usage-based Insurance with StreamAnalytix The auto insurance industry is rising up to meet consumer expectations of personalization and flexibility in all

Real-time Driver Profiling & Risk Assessment for Usage-based Insurance with StreamAnalytix The auto insurance industry is rising up to meet consumer expectations of personalization and flexibility in all

Report on Retail OTC Leveraged Products. Consultation Report

Report on Retail OTC Leveraged Products Consultation Report The Board OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS CR01/2018 FEBRUARY 2018 This paper is for public consultation purposes

Report on Retail OTC Leveraged Products Consultation Report The Board OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS CR01/2018 FEBRUARY 2018 This paper is for public consultation purposes

Reporting Annex IV transparency information under the Alternative Investment Fund Managers Directive

Reporting Annex IV transparency information under the Alternative Investment Fund Managers Directive December 2017 Page 1 of 19 As a full-scope UK AIFM (Alternative Investment Fund Manager AIFM ), small

Reporting Annex IV transparency information under the Alternative Investment Fund Managers Directive December 2017 Page 1 of 19 As a full-scope UK AIFM (Alternative Investment Fund Manager AIFM ), small

Potential drivers of insurers equity investments

Potential drivers of insurers equity investments Petr Jakubik and Eveline Turturescu 67 Abstract As a consequence of the ongoing low-yield environment, insurers are changing their business models and looking

Potential drivers of insurers equity investments Petr Jakubik and Eveline Turturescu 67 Abstract As a consequence of the ongoing low-yield environment, insurers are changing their business models and looking

Know the score: how positive data could impact your next credit application

1 Know the score: how positive data could impact your next credit application Credit applications and your data When you apply for credit in Australia, the credit provider will usually ask for your permission

1 Know the score: how positive data could impact your next credit application Credit applications and your data When you apply for credit in Australia, the credit provider will usually ask for your permission

HSBC Premier Credit Card. Terms and conditions

HSBC Premier Credit Card Terms and conditions 2 Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key Terms How much

HSBC Premier Credit Card Terms and conditions 2 Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key Terms How much

FCA Business Plan 2017/18

FCA Business Plan 2017/18 17 May 2017 www.moorestephens.co.uk PRECISE. PROVEN. PERFORMANCE. Andrew Jacobs Agenda Introduction Andrew Jacobs Main themes of 2017/18 Business Plan Giovanni Giro Governance

FCA Business Plan 2017/18 17 May 2017 www.moorestephens.co.uk PRECISE. PROVEN. PERFORMANCE. Andrew Jacobs Agenda Introduction Andrew Jacobs Main themes of 2017/18 Business Plan Giovanni Giro Governance

What is the micro-elasticity of mortgage demand to interest rates?

What is the micro-elasticity of mortgage demand to interest rates? Stephanie Lo 1 December 2, 2016 1 Part of this work has been performed at the Federal Reserve Bank of Boston. The views expressed in this

What is the micro-elasticity of mortgage demand to interest rates? Stephanie Lo 1 December 2, 2016 1 Part of this work has been performed at the Federal Reserve Bank of Boston. The views expressed in this

HOW DOES COMPREHENSIVE CREDIT REPORTING AFFECT ME?

HOW DOES COMPREHENSIVE CREDIT REPORTING AFFECT ME? www.creditsimple.com.au INTRODUCTION Most Australians apply for credit at some point in their lives. Whether you re buying a mobile phone, a car or even

HOW DOES COMPREHENSIVE CREDIT REPORTING AFFECT ME? www.creditsimple.com.au INTRODUCTION Most Australians apply for credit at some point in their lives. Whether you re buying a mobile phone, a car or even

Tackling problem debt

A picture of the National Audit Office logo Report by the Comptroller and Auditor General Cross-government, HM Treasury Tackling problem debt HC 1499 SESSION 2017 2019 6 SEPTEMBER 2018 Our vision is to

A picture of the National Audit Office logo Report by the Comptroller and Auditor General Cross-government, HM Treasury Tackling problem debt HC 1499 SESSION 2017 2019 6 SEPTEMBER 2018 Our vision is to

PRODUCT GOVERNANCE POLICY V X Spot Markets (EU) Ltd.

Ltd.") PRODUCT GOVERNANCE POLICY V1.0 2018 X Spot Markets (EU) Ltd. Table of Contents A. Introduction & Purpose... 3 B. Legal Framework... 3 C. Definitions... 3 D. Requirements and procedures for manufacturers...

PRODUCT GOVERNANCE POLICY V1.0 2018 X Spot Markets (EU) Ltd. Table of Contents A. Introduction & Purpose... 3 B. Legal Framework... 3 C. Definitions... 3 D. Requirements and procedures for manufacturers...

Unemployment Benefits, Unemployment Duration, and Post-Unemployment Jobs: A Regression Discontinuity Approach

Unemployment Benefits, Unemployment Duration, and Post-Unemployment Jobs: A Regression Discontinuity Approach By Rafael Lalive* Structural unemployment appears to be strongly correlated with the potential

Unemployment Benefits, Unemployment Duration, and Post-Unemployment Jobs: A Regression Discontinuity Approach By Rafael Lalive* Structural unemployment appears to be strongly correlated with the potential

Empirical Household Finance. Theresa Kuchler (NYU Stern)

") Empirical Household Finance Theresa Kuchler (NYU Stern) Overview Three classes: 1. Questions and topics on household finance 2. Recent work: Online data sources 3. Recent work: Administrative data sources

Empirical Household Finance Theresa Kuchler (NYU Stern) Overview Three classes: 1. Questions and topics on household finance 2. Recent work: Online data sources 3. Recent work: Administrative data sources

COMMISSION DELEGATED REGULATION (EU) No /.. of

No /.. of") EUROPEAN COMMISSION Brussels, 17.12.2013 C(2013) 9098 final COMMISSION DELEGATED REGULATION (EU) No /.. of 17.12.2013 supplementing Directive 2011/61/EU of the European Parliament and of the Council with

EUROPEAN COMMISSION Brussels, 17.12.2013 C(2013) 9098 final COMMISSION DELEGATED REGULATION (EU) No /.. of 17.12.2013 supplementing Directive 2011/61/EU of the European Parliament and of the Council with

A Call to Action Enabling Open Standards Data Flow

A Call to Action Enabling Open Standards Data Flow Mapping the Construction Technology Ecosystem Financial Markets Bank Insurance Surety https://www.mckinsey.com/industries/capi tal-projects-and-infrastructure/ourinsights/seizing-opportunity-in-todaysconstruction-technology-ecosystem

A Call to Action Enabling Open Standards Data Flow Mapping the Construction Technology Ecosystem Financial Markets Bank Insurance Surety https://www.mckinsey.com/industries/capi tal-projects-and-infrastructure/ourinsights/seizing-opportunity-in-todaysconstruction-technology-ecosystem

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013 Consultation Paper 13/10: Detailed Proposals for the FCA regime for Consumer Credit In early October

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013 Consultation Paper 13/10: Detailed Proposals for the FCA regime for Consumer Credit In early October

NEPAL MONETARY POLICY 2018 Highlights

NEPAL MONETARY POLICY 2018 Highlights www.nbsm.com.np NBSM & Associates Chartered Accountants NBSM Consulting Table of Content Economic Outlook 3 Monitory Management 4 Debt Management 5 Regulations 6 Financial

NEPAL MONETARY POLICY 2018 Highlights www.nbsm.com.np NBSM & Associates Chartered Accountants NBSM Consulting Table of Content Economic Outlook 3 Monitory Management 4 Debt Management 5 Regulations 6 Financial

AIFMD. Fundamental considerations to be addressed at a strategic level for marketing in the EU:

AIFMD Are you ready? The Alternative Investment Fund Managers Directive ( AIFMD or the Directive ) came into force on July 22, 2013 with certain activities or requirements being governed by transitional

AIFMD Are you ready? The Alternative Investment Fund Managers Directive ( AIFMD or the Directive ) came into force on July 22, 2013 with certain activities or requirements being governed by transitional

REPORTING ANNEX IV TRANSPARENCY INFORMATION UNDER THE ALTERNATIVE INVESTMENT FUND MANAGERS DIRECTIVE

REPORTING ANNEX IV TRANSPARENCY INFORMATION UNDER THE ALTERNATIVE INVESTMENT FUND MANAGERS DIRECTIVE For SMALL NON-EEA AIFMs and ABOVE-THRESHOLD NON-EEA AIFMs marketing in the UK under the UK National

REPORTING ANNEX IV TRANSPARENCY INFORMATION UNDER THE ALTERNATIVE INVESTMENT FUND MANAGERS DIRECTIVE For SMALL NON-EEA AIFMs and ABOVE-THRESHOLD NON-EEA AIFMs marketing in the UK under the UK National

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia)

BERHAD (Incorporated in Malaysia)") UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS FOR THE FINANCIAL QUARTER ENDED 31 MARCH 2018 UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2018 ASSETS

UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS FOR THE FINANCIAL QUARTER ENDED 31 MARCH 2018 UNAUDITED CONDENSED INTERIM FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2018 ASSETS

Consumer lending. terms and conditions

Consumer lending terms and conditions 1 Important information Who we are Teachers Mutual Bank Limited ABN 30 087 650 459 AFSL/Australian Credit Licence 238981. In this document, the Bank, we, us and our

Consumer lending terms and conditions 1 Important information Who we are Teachers Mutual Bank Limited ABN 30 087 650 459 AFSL/Australian Credit Licence 238981. In this document, the Bank, we, us and our

AN APPROACH TO RISK-BASED MARKET CONDUCT REGULATION

CCIR Canadian Council of Insurance Regulators AN APPROACH TO RISK-BASED MARKET CONDUCT REGULATION Conseil canadien des responsables de la réglementation d assurance A report prepared by the Canadian Council

CCIR Canadian Council of Insurance Regulators AN APPROACH TO RISK-BASED MARKET CONDUCT REGULATION Conseil canadien des responsables de la réglementation d assurance A report prepared by the Canadian Council

Ministry of Health, Labour and Welfare Statistics and Information Department

Special Report on the Longitudinal Survey of Newborns in the 21st Century and the Longitudinal Survey of Adults in the 21st Century: Ten-Year Follow-up, 2001 2011 Ministry of Health, Labour and Welfare

Special Report on the Longitudinal Survey of Newborns in the 21st Century and the Longitudinal Survey of Adults in the 21st Century: Ten-Year Follow-up, 2001 2011 Ministry of Health, Labour and Welfare

Conducting Equity Release Business

Conducting Equity Release Business 1 1. Introduction The term Equity Release refers to both Lifetime Mortgages and Home Reversion Plans. Conducting Equity Release business includes all activities relating

Conducting Equity Release Business 1 1. Introduction The term Equity Release refers to both Lifetime Mortgages and Home Reversion Plans. Conducting Equity Release business includes all activities relating

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Data Bulletin September 2017

Data Bulletin September 2017 In focus: Latest trends in the retirement income market Highlights from the FCA and Practitioner Panel Survey 2017 Issue 10 Introduction Introduction from the editor Jo Hill

Data Bulletin September 2017 In focus: Latest trends in the retirement income market Highlights from the FCA and Practitioner Panel Survey 2017 Issue 10 Introduction Introduction from the editor Jo Hill

The CFPB s Priorities in Rulemaking, Supervision, and Enforcement

The CFPB s Priorities in Rulemaking, Supervision, and Enforcement July 21, 2016 Scott M. Pearson Ballard Spahr LLP 424.204.4323 pearsons@ballardspahr.com John D. Socknat Ballard Spahr LLP 202.661.2253

The CFPB s Priorities in Rulemaking, Supervision, and Enforcement July 21, 2016 Scott M. Pearson Ballard Spahr LLP 424.204.4323 pearsons@ballardspahr.com John D. Socknat Ballard Spahr LLP 202.661.2253

European Long Term Investment Funds - ELTIFs

European Long Term Investment Funds - ELTIFs Updated May 2015 The publication of the Regulation for ELTIFs on 19 May 2015 in the EU Official Journal will result in ELTIFs being introduced under the AIFMD

European Long Term Investment Funds - ELTIFs Updated May 2015 The publication of the Regulation for ELTIFs on 19 May 2015 in the EU Official Journal will result in ELTIFs being introduced under the AIFMD

After FSA the new regulatory landscape

After FSA the new regulatory landscape Simon Morris Partner - CMS Cameron McKenna LLP 15 th April 2011 What is proposed? Financial Policy Committee create the focus for macro-prudential regulation that

After FSA the new regulatory landscape Simon Morris Partner - CMS Cameron McKenna LLP 15 th April 2011 What is proposed? Financial Policy Committee create the focus for macro-prudential regulation that

Reporting transparency information to the FCA. Questions and answers

Reporting transparency information to the FCA Questions and answers December 2017 Introduction... 3 Section 1 - Introduction to AIFMD Reporting Requirements... 4 Section 2 - AIFMD Submission through Gabriel...

Reporting transparency information to the FCA Questions and answers December 2017 Introduction... 3 Section 1 - Introduction to AIFMD Reporting Requirements... 4 Section 2 - AIFMD Submission through Gabriel...