Low down payment option; qualify with as little as 3.5% down

|

|

|

- Jemima Miller

- 5 years ago

- Views:

Transcription

1

Renovation Loan combines the cost of buying the home with the cost of making repairs. It is ideal for qualified buyers interested in purchasing a home that needs repairs or updating.")

2 Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the cost of buying the home with the cost of making repairs. It is ideal for qualified buyers interested in purchasing a home that needs repairs or updating. The notable advantages include: Low down payment option; qualify with as little as 3.5% down Increased home choices for purchase Ability to personalize home enhancements Financing of mortgage, repairs & upgrades in a single loan, based on the As-Improved value of the home

3 Advantages for an FHA 203(k) Renovation Loan: FHA 203(k) Renovation Loan allows you to complete major or minor renovation projects including broad scope renovation, both structural and cosmetic Why Choose the 203(k)? Allows for repairs and improvements to be completed after closing for purchases and refinances via the establishment of an interest bearing escrow account Can borrow against the property value after improvements Avoid construction loans Increases property value and builds equity Combines the cost of the home and renovation into one low cost mortgage

4 The Full Consultant option is used for more complicated projects. Eligible repairs include: Major structural alterations and additions Major landscaping and site improvements Repair swimming pool (up to $1,500) Remodeling of rooms, including kitchens & bathrooms Relocation of load bearing walls Construction or rehab of detached garage Converting multi-unit to a single unit or a single unit to a multi-unit Basement finishing or waterproofing Appliances Energy conservation improvements

5 Purpose Max LTV Max CLTV Loan Amount Minimum FICO Purchase 96.50% % FHA Limit 620 Rate/Term 97.75% % FHA Limit 620 Cash-Out N/A N/A N/A N/A Quick Facts: 1 4 Owner Occupied only Conforming and High Balance loan amounts Fixed 30 and 15 year term Credit/Ratio/Reserve requirements follow HomeBridge FHA guidelines HomeBridge will require Approve/Eligible AUS Findings Manual underwriting not permitted on 203(k)

6 Example of 203(k) Sales Price $150,000 Renovation Costs $65,000 Contingency Reserve $6,500 Soft Costs (inspections, permits, fees, plans, etc.) $1,500 Total Acquisition Cost 223,000 Down Payment $7,805 Base Loan Amount $215,195

7 HUD Consultant Role: Approved HUD Consultant required on Full Consultant transactions Consultant fee ranges depending on cost of work HUD Consultant manages the entire project Works directly with Borrowers & contractors Provides initial Work Write-Up or Specification of Repairs report Provides draw schedule Performs draw inspections to approve disbursements to General Contractor Provides Contingency Reserve amount to be established HUD Approved Consultant Search: Find a HUD Consultant

8 Requires an FHA HUD Consultant For complicated projects and cosmetic updates Minimum cost of repairs $5,000; no max repair amount Contingency Reserve 10-20% (determined by HUD Consultant) Work to start within 30 days of closing Work must be completed within 5 months of closing Max 5 draws permitted One (1) General Contractor allowed: Subcontractors permitted under General Contractor Additional specialized contractor(s) allowed for technical items Can finance up to 6 months PITI if home deemed uninhabitable by HUD Consultant

9 Details of HUD Consultant s Work Write- Up Report, AKA Specification of Repairs Report: Signed by Consultant, Borrower and Contractor Original plan/specifications for project Describes quantity/quality of materials required Lists market costs of materials, labor, overhead, profit Includes adequacy of existing structural, heating, plumbing, electrical and roofing Must demonstrate that property will meet HUD s minimum property standards, after repairs Contractor(s) can reference the Write-Up to prepare bid(s) Provides required Contingency Reserve amount

10

11

12

13

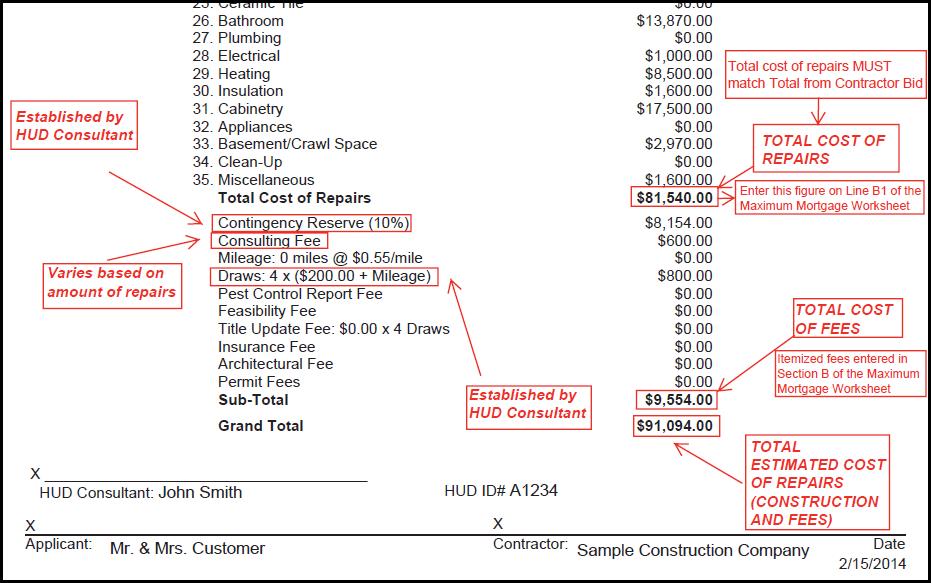

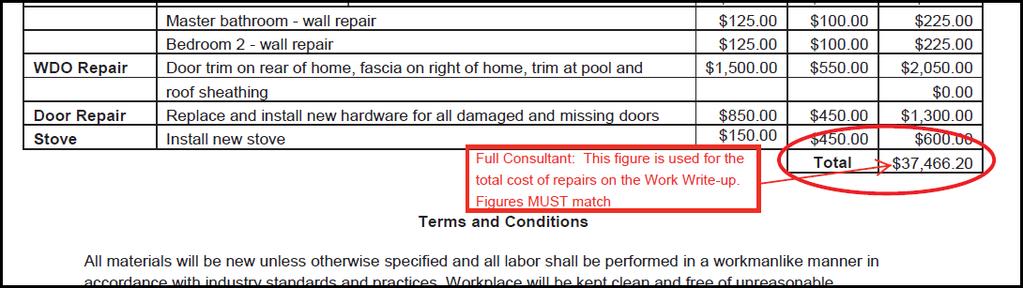

14 The Consultant Work Write-Up and Contractor Bid(s) should match on a Full Consultant loan: In the event of discrepancy: IF Contractor bid is MORE than Consultant Write-Up IF Contractor bid is LESS than Consultant Write-Up THEN Maximum Mortgage is determined by the Consultant Write-Up; Could result in additional cash to close for Borrower THEN Consultant must comment on discrepancy & validate that Contractor bid is reasonable. If the bid is unreasonable, Maximum Mortgage is determined by Consultant s Write-Up

15 Full Consultant - What is Included in Rehabilitation Costs: Total cost of rehabilitation (labor and materials) HUD Consultant Fee Contingency Reserve Established by HUD Consultant Inspection Fees Permit Fees Architectural/Engineering Fees (as applicable) Final Title Update Fee Up to 6 months PITI if property uninhabitable with HUD Consultant approval Discount Points (only the percentage attributed to renovation portion)

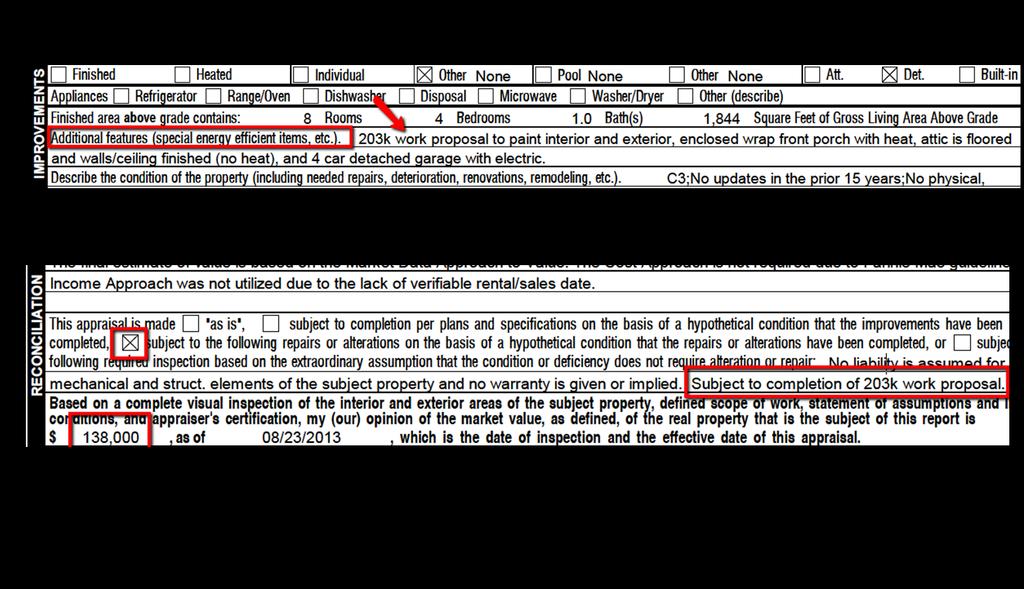

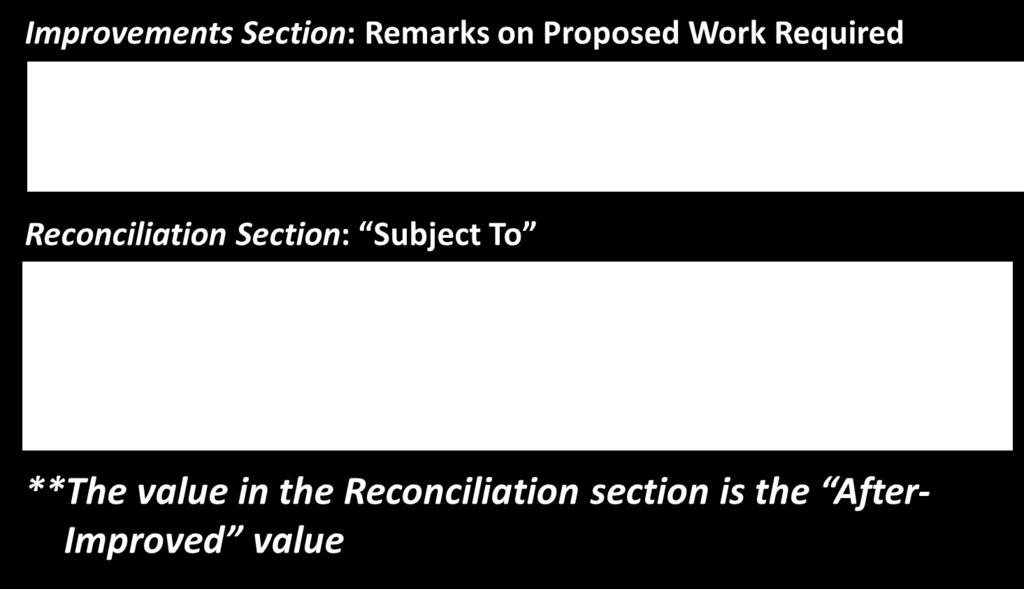

16 Appraisal Requirements: Appraisals must include the following four items unique to a 203(k) appraisal: Remarks regarding the scope of work being completed Located in Improvements Section of Report Be completed subject to in Reconciliation Section of Report Include Copies of Bid(s) and Work Write-Up in Report Full Consultant: Bid(s) and/or Write-Up required; cost of repairs must match Required values differ; see following slides for details

17 Purchase Transactions: One Required Value: An After-Improved value aka As-Completed value is always required This value is indicated in the Reconciliation section of the appraisal report The After-Improved value is the only value required by HUD on 203(k) loans The Purchase Price is used as the As-Is value: HUD does not require an As-Is value; HUD assumes the purchase price is the As-Is value

18 Refinance Transactions: Two values required An After-Improved value aka As-Completed is required This value is indicated in the Reconciliation section of the appraisal report An As-Is value is required Commonly completed as an addendum to the appraisal report

19

20 For Full Consultant loans where a property is being converted from SFR to multi-units or from multi-units to SFR, the appraisal will be completed on the form for what the property will be after renovations (not the current property type)

21 Where required by the Appraiser, the following inspections, reports and clearances may be needed: Termite Well or septic cert HVAC or other system certifications Architectural exhibits as required Full Consultant: all inspections Consultant and/or Appraiser require must be completed

22 AUS: An Approved/Eligible finding is required Manual Underwriting is not allowed Cash Out: Not Allowed

23 Condo Eligibility: Project must be approved by HUD at time of case number assignment Work limited to interior of unit Lesser of 5 units per HOA, or 25% of total number of units, can be undergoing rehabilitation at any time Max mortgage cannot exceed 100% of the After- Improved value Rehabilitation limited to subject unit in buildings with 1-4 total units See next slide for additional details

24 Condo Building/Structure Eligibility: Subject unit must be in a building/structure that has a maximum of 4 units The Condo project may have multiple buildings with no limit to the total number of units Eligible Building/Structure Scenario Project consists of 10 buildings, each with 4 units, for a total of 40 units Ineligible Building/Structure Scenario Project consists of 10 buildings, each with 6 units, for a total of 60 units This property is ineligible because it is in a building/structure with more than 4 units More than 4 units in a building allowed when the renovation reduces the number of units in the building to 4 or less Ex: Borrower purchases 2 units and converts to 1 unit

25 A Contingency Reserve is held from the loan proceeds to cover health, safety and unplanned costs that arise during construction: Ranges from 10 20% of the rehab cost as established by HUD Consultant 15% required if utilities not on or are not in good working order Deposited to an escrow account Typically only soft costs are released within 2-3 business days of receipt of final signed document package (i.e. Consultant, permit fees) Invoices are required Up to 50% of custom ordered material costs can be released Requires consultant authorization Disbursed to the manufacturer directly No funds are disbursed to Contractor or Borrower at closing

26 Contingency Reserve Options: The contingency reserve may be financed or funded by the Borrower from their own funds: Financed Contingency Reserve: any funds remaining at the end of the renovation process must be applied as a principal reduction Borrower Funded Contingency Reserve: any funds remaining at the end of the renovation process are returned to the Borrower

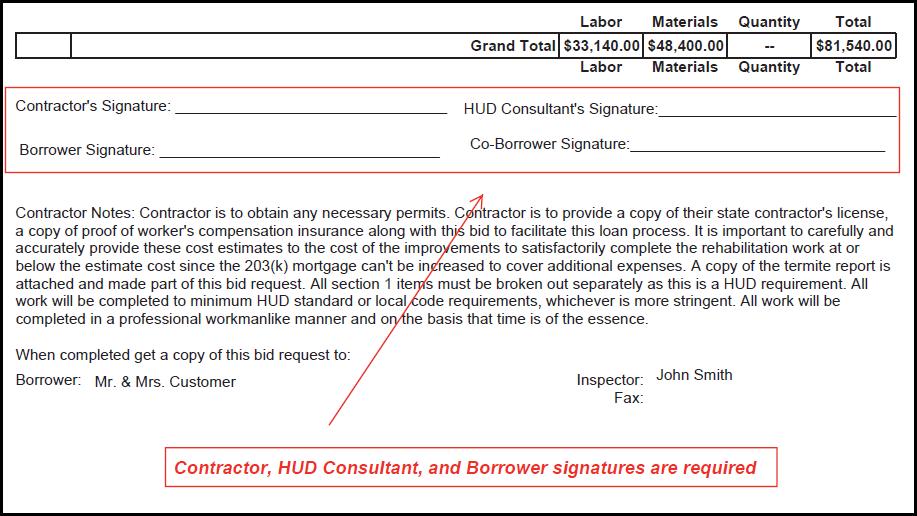

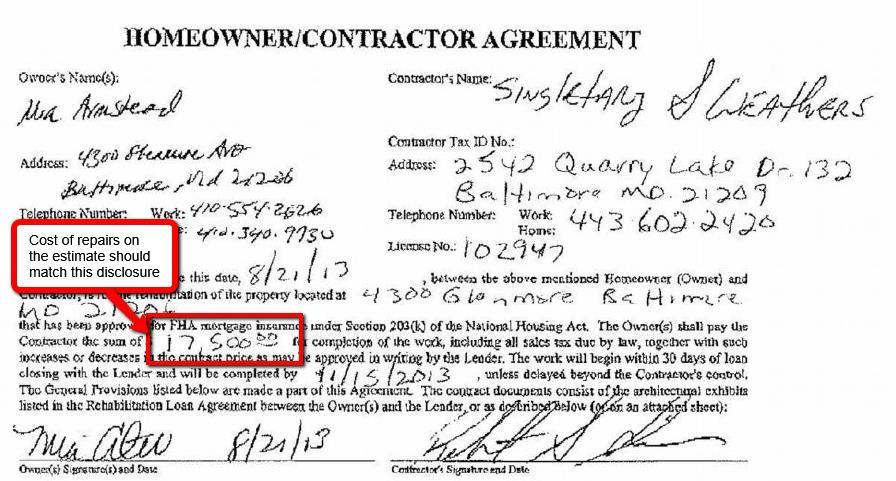

27 Contractor Requirements: Completed Contractor Profile Applicable licenses and proof of insurance as required by the local, state, county and city jurisdiction Completed Federal W 9 Signed bid(s) Homeowner/Contractor Agreement Contractor Acknowledgment If license/insurance is expired, proof of current documentation is required.

28 Contractor Insurance Requirements: If insurance includes Workman Compensation in General Liability a separate policy is typically not required Builder Risk required only if Master insurance does not cover construction Often seen in 203(k) Full Consultant transactions Builder Risk can be paid by the homeowner or contractor

number (not")

29 Contractor W-9 Completion Tips: If Limited Liability Corporation selected, W-9 must indicate classification of corporation Taxpayer Identification Number must be completed correctly Must enter SS # or EIN # (Employee Identification Number) number (not both)

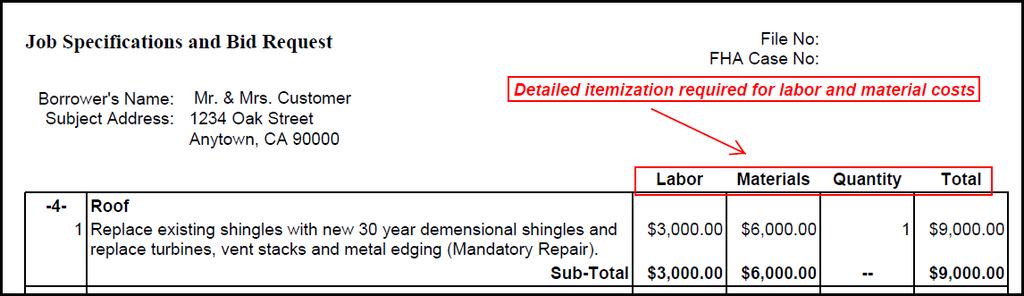

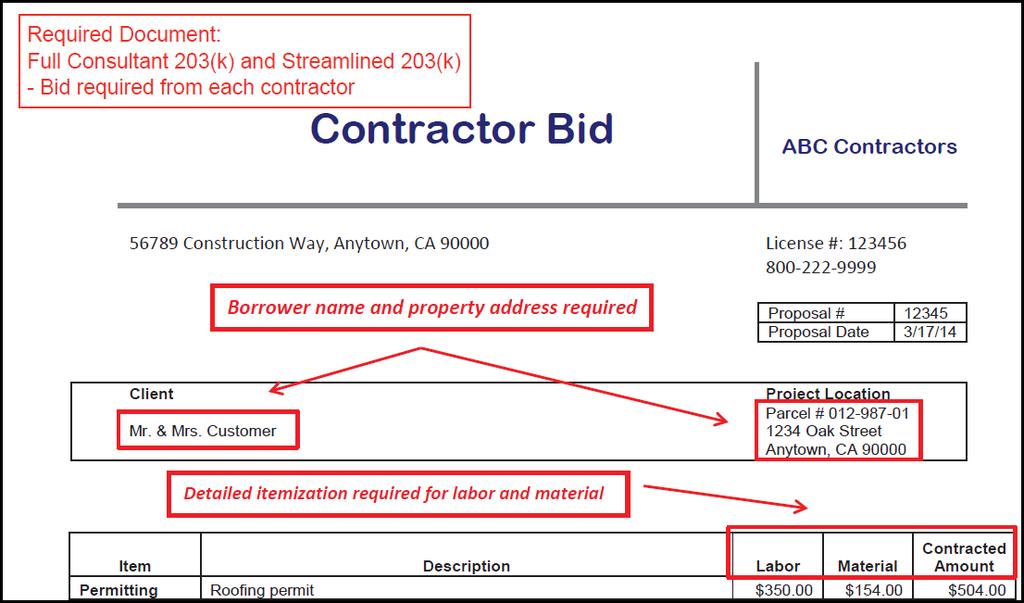

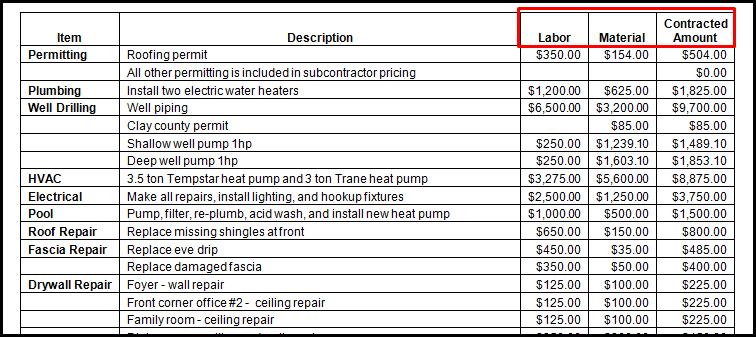

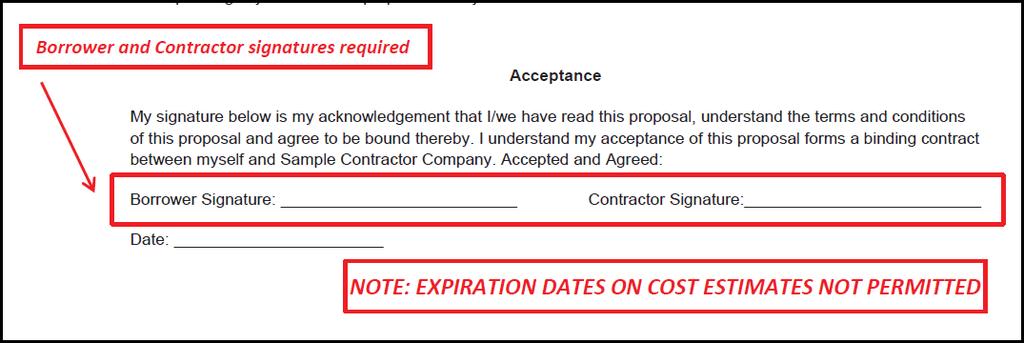

30 Contractor Bid Tips: All Contractor Bids must include: Borrower(s) name and property address Borrower(s) and Contractor signatures Clearly state the nature of the repair/renovation Cost for completion of each work item performed Expiration dates on cost estimates not permitted Detail itemization required for: Material costs of each item Labor costs of each item Make/model and description of material item used Borrower cannot supply or pay for materials If permits required should be noted on bid

31

32

33

34

35 Disbursement Process: Seller has the option to issue 1 st draw Borrower will be contacted by HomeBridge Renovation Concierge Service Department to manage the renovation process from time loan is purchased by HomeBridge until completed As repairs/renovation work is completed and draws are requested: 10% holdback is withheld from each draw Draws released when acceptable Consultant inspection(s) received Note: Soft costs and/or release of funds to manufacturers for custom made materials is not considered a draw

36 Disbursement Process (continued): Once final repairs/renovation work is complete: HomeBridge Renovation Concierge Department to be notified by the HUD Consultant Final Title Update performed to evidence no liens Final draw is released to Borrower and Contractor All checks are two party Checks are sent via 2 nd day UPS Holdback funds are released after issuance of the Final Release Notice Unused funds remaining in the escrow account will be applied to the remaining loan balance HomeBridge will notify seller of final disbursement and provide tracking information

37 Escrow/Impounds: Required on all loans. No exceptions. Feasibility Study: A Feasibility Analysis (AKA Feasibility Study or Feasibility Site Report) serves to help Borrowers make a quick decision regarding the cost involved to renovate a property to meet HUD minimum property standards Completed at discretion of Borrower on a Full Consultant 203(k) loan Not required; obtained at Borrower discretion Typical fee $ Reviews property for compliance for Minimum Property Standards (MPS) per HUD Used to determine if Full Consultant should be utilized If Full Consultant, cost of study typically credited towards Consultant Fee Often used for purchase transactions and/or determine scope of repairs

38 Sample Feasibility Study

39 Sample Feasibility Study (Continued)

40 Sample Feasibility Study (Continued)

41 Sample Feasibility Study (Continued)

42 Sample Feasibility Study (Continued)

43 Forms: 203(k) Forms and Documents 203(k) Maximum Mortgage Worksheet (HUD Form 92700) 203(k) Borrower s Acknowledgment (HUD Form A). Borrower must complete the Loan Requirements section of the Acknowledgment form indicating how the interest earned on the Rehabilitation Escrow Account is to be applied after the Final Release Notice is issued. Borrower/Contractor Identity of Interest/Conflict of Interest Certification Consultant Identity of Interest Certification Homeowner/Contractor Agreement Full Consultant (HUD Form 2420) Homeowner/Contractor 203(k) Certification Contractor Acknowledgment Full Consultant 203(k) Program W-9 Contractor Profile (Fannie Mae Form 1202) Work Write-Up aka Specification of Repairs report Contractor bid(s) Feasibility Site Report, aka Feasibility Study (not required)

44 Gift Funds Allowed: Follow HomeBridge Funding 203(k) Renovation Guidelines Identity of Interest: There can be no identity-of-interest issues between any parties participating in the 203(k) transaction Borrower must certify there is not a conflict of interest with any party to the transaction by executing an Identity of Interest Certification. The certification verifies no conflict of interest including, but not limited to, any of the following: Seller Appraiser Realtor Lender Contractor Consultant Inspector Closing Agent Title Company

45 Identity of Interest Disclosures are required to confirm there is no relationship with any parties to the transaction as follows: Full Consultant: Borrower Identity of Interest Certification and Consultant Identity of Interest Certification

46 Loan terms: 15 and 30 year fixed rate term only Maximum mortgage amounts: Maximum mortgage amounts vary by loan purpose Purchase: 96.50% Refinance: 97.75% The maximum mortgage (total loan amount) cannot exceed FHA county limits Important reminder: Condos and Super Storm Sandy cannot exceed 100% of After-Improved Value. Condos and Super Storm Sandy still use the same max mortgage calculations for purchase and refinance transactions

47 What is included in Maximum Mortgage Calculation: INCLUDED IN TOTAL REHABILITATION COSTS Repairs Contingency Reserve Inspection Fee(s) Final Title Update Fee Escrowed Mortgage Payments Architectural/Engineering Fees (as required) Consultant Fees Permit Fees (If Applicable) Discount Points Full Consultant Materials and Labor 10-20% of Rehab Cost; 15% If utilities are not on or not in good working order Established by HUD Consultant Up to 5 Inspection Fees Allowed Per Draw Completed by HUD Consultant Refer to Work Write-Up 1 Final Title Update Fee Refer to Final Title Update Fees by State Matrix Up to 6 months PITI if property is uninhabitable and approved by HUD Consultant Included Included Included Calculated from Repair Costs and Fees

48 Maximum Mortgage Amount: Purchase Calculations: Step 1: Identify the lesser of the below calculations: Purchase Price + Renovation Costs OR 110% of After-Improved Value* OR As-is Value + Renovation Costs** * For Condos and Super Storm Sandy use 100% of After-Improved Value **HUD does not require an As-Is value; HUD assumes the purchase price is the As-Is value Step 2: Multiply the lesser calculation by 96.5% to obtain Base Loan Amount: 96.5% of the lesser above calculation = Base Loan Amount Step 3: Add UFMIP to Base Loan Amount to obtain Total Loan Amount: Base Loan Amount + UFMIP = Total Loan Amount

49 Maximum Mortgage Amount: Full Consultant Purchase Examples: Full Consultant 203(k) Purchase Purchase Price and Renovation Costs Dollar Amount Purchase Price $120,000 Total Cost of Repairs (labor & materials) $24,500 Contingency Reserve (15%) $3,675 Allowable Fees/Costs $1,500 Total Purchase Price and Renovation Costs $149, % of After-Improved Value After-Improved Value (Located in Reconciliation section of Appraisal) $176,000 Maximum Base Loan Amount $144,436 UFMIP $2,528 Total Loan Amount $146,964 LTV Calculation Step 1: Identify the lesser of the below calculations - Purchase Price + Renovation Costs - As-is Value + Renovation Costs (HUD does not require an As-Is value; HUD assumes the purchase price is the As-Is value) - 110% of After-Improved Value Step 2: Multiply the lesser calculation by 96.5% to obtain Base Loan Amount Step 3: Add UFMIP to Base Loan Amount to obtain Total Loan Amount In this example the Purchase Price plus Renovation Costs is less than 110% of After-Improved Value. Therefore, $149,675 is used to calculate the base loan amount.

4.")

50 Maximum Mortgage Worksheet Examples: Full Consultant 203(k), Purchase: Section A 1. Purchase Price 2. HUD does not require an As-Is value; HUD assumes the purchase price is the As-Is value 3. After-Improved Value from Appraisal (Reconciliation section) % of After-Improved Value 5. N/A - only applicable for refinances 6. N/A HomeBridge does not offer EEM s

3.")

51 Maximum Mortgage Worksheet Examples: Full Consultant 203(k), Purchase: Section B, Lines Cost of Repairs (labor & material) 2. Cost of Repairs X Contingency Reserve % (10-20% of Rehab Cost; 15% If utilities are not on OR not in good working order; Established by HUD Consultant) 3. Inspections Fee(s) (Number of inspections determined by HUD Consultant) + Title Update Fee (Refer to Final Title Update Fees by State Matrix) 4. Up to 6 Months PITI (If property is uninhabitable and approved by HUD Consultant) 5. Subtotal of B1-B4

9. Other Fees (describe in Remarks Section on Page 2) 10. Subtotal of Lines B5-B9 11. N/A HomeBridge does not charge Supplemental Origination Fee 12.")

52 Maximum Mortgage Worksheet Examples: Full Consultant 203(k), Purchase: Section B, Lines Architectural and Engineering Fees (if applicable) 7. HUD Consultant Fee (from Work Write-Up) 8. Permits (if applicable) 9. Other Fees (describe in Remarks Section on Page 2) 10. Subtotal of Lines B5-B9 11. N/A HomeBridge does not charge Supplemental Origination Fee 12. Discount Points (Discount % x Line B10 = Discount on Repair Costs and Fees) 13. Lines B6-B9 + B11 (N/A) + B Total Rehabilitation Cost (must be at least $5,000, with no maximum)

4. 96.")

53 Maximum Mortgage Worksheet Examples: Full Consultant 203(k), Purchase: Section C 1. Purchase Price 2. Total Rehabilitation Cost (Line B14) 3. Lesser of Line C1 + Line C2 OR 110% of the After-Improved Value (Line A4) % of Line C3 Sales Price: $120,000 As Is Value: $120,000 Rehab Cost: $29,675 After-Improved Value: $160,000 Line C1 + C2: $149, % of After-Improved Value: $176,000 Lesser Of: $149, % of $149,675 = $144,436 Base Ln Amt

54 Purchase Max Mortgage Calculation Reminders: HUD requires the lower of the following to be used when determining Max Mortgage Amount: Purchase Price + Renovation Costs, or 110% of After Improved Value, or As-Is Value + Renovation Costs* *HUD does not require an As-Is value; HUD assumes the purchase price is the As-Is Value

55 Purchase Examples: Why Not Requiring an As-Is Value is a Benefit: Example #1: Purchase Price + Renovation Costs Purchase Price is $150,000 Total Renovation cost is $50,000 Appraisal does not show an As-Is Value only a $225,000 After-Improved Value Max Base Loan Amount is $193,000 ($150,000 +$50,000=$200,000 X 96.5%) Example #2: 110% Of Value Purchase Price is $150,000 Total Renovation cost is $50,000 Appraisal does not show an As-Is Value only a $180,000 After-Improved Value 110% of $180,000 is $198,000 Max Base Loan Amount is $191,070 ($198,000 X 96.5%) Example #3: As-Is Value + Renovation Costs Purchase Price is $150,000 Total Renovation cost is $50,000 Appraisal shows an As-Is Value of $140,000 and an After-Improved Value of $225,000 Max Base Loan Amount is $188,350 ($140,000 + $50,000=$190,000 X 96.5%)

56 Maximum Mortgage Amount: Refinance Calculations: Step 1: Identify the lesser of the below calculations: Existing Debt + Renovation Costs + Closing Costs & Prepaids OR (As-is Value + Renovation Costs) X 97.75% OR (110% of After- Improved Value) X 97.75%* * For Condos and Super Storm Sandy use 100% of After-Improved Value Step 2: The lesser of the above calculations equals the Base Loan Amount: Lesser of the above calculations = Base Loan Amount Step 3: Add UFMIP to Base Loan Amount to obtain Total Loan Amount: Base Loan Amount + UFMIP = Total Loan Amount

57 Maximum Mortgage Amount: Consultant Refinance Example: Full Consultant 203(k) Refinance Existing Debt, Renovation, Closing Costs, and Prepaids Dollar Amount Existing Debt $120,000 Total Cost of Repairs (labor and material) $40,000 Contingency Reserve (15%) $6,000 Allowable Fees/Costs $1,600 Closing Costs/Prepaids $3,500 Total Existing Debt, Renovation, Closing Costs, and Prepaids $171,100 As-is Value + Renovations Costs As-Is Value from Appraisal (Typically noted within Addendum to report) 110% of After-Improved Value After-Improved Value (Located in Reconciliation section of Appraisal) $177,600 $176,000 Maximum Base Loan Amount $171,100 UFMIP $2,994 Total Loan Amount $174,094 LTV Calculation Step 1: Identify the lesser of the below calculations - Existing Debt + Renovation Costs + Closing Costs and Prepaid - (As-is Value + Renovation Costs) X 97.75% - (110% of After-Improved Value) X 97.75% Step 2: The lesser of the above calculations equals the Base Loan Amount Step 3: Add UFMIP to Base Loan Amount to obtain Total Loan Amount In this example the Existing Debt + Renovation Costs + Closing Costs & Prepaids is the lesser calculation. Therefore, $171,100 is the base loan amount.

2. As-Is Value (Typically noted within addendum to report) 3.")

58 Maximum Mortgage Worksheet Example: Full Consultant 203(k), Refinance: Section A 1. Existing Debt-Principal and Interest (If subject owned for less than 12 months, use lesser of existing debt or original purchase price) 2. As-Is Value (Typically noted within addendum to report) 3. After-Improved Value from Appraisal (Reconciliation section) % of After-Improved Value 5. Closing Costs and Prepaids 6. N/A HomeBridge does not offer EEM s

59 Maximum Mortgage Worksheet Example: Full Consultant 203(k), Refinance: Section B, Lines Cost of Repairs (labor & material) 2. Cost of Repairs X Contingency Reserve % (10-20% of rehab cost;15% if utilities are not on OR not in good working order; Established by HUD Consultant) 3. Inspection Fee(s) (Number of inspections determined by HUD Consultant) + Title Update Fee (Refer to Final Title Update Fees by State Matrix) 4. Up to 6 months PITI (If property is uninhabitable and approved by HUD Consultant) 5. Sub-total B1 thru B4

60 Maximum Mortgage Worksheet Example: Full Consultant 203(k), Refinance: Section B, Lines Architectural and Engineering Fees (if applicable) 7. Consultant Fee (from Work Write-Up) 8. Permit(s) (if applicable) 9. Other Fees (describe in Remarks Section on Page 2) 10. Sub-total B5 thru B9 11. N/A HomeBridge does not charge Supplemental Origination Fee 12. Discount Points (Discount % x Line B10 = Discount on Repair Costs and Fees) 13. Lines B6-B9, B11 (N/A) + B Total Rehabilitation Cost (must be at least $5,000, with no maximum)

61 Maximum Mortgage Worksheet Example: Full Consultant 203(k), Refinance: Section D 1. Existing Debt + Renovation Costs + Closing Costs & Prepaids 2. Lesser of: As-Is Value + Renovation Costs OR 110% of After-Improved Value 3. Line D2 x 97.75% 4. Base Mortgage Amount is lesser of Lines D1 and D3

62 Property Eligibility: *Full Consultant Reminders: Conversion of single family to multi-units and vice versa is acceptable See matrix for restrictions on multi-units in IL, NJ & NY ** Condo Restriction: Property Type Full Consultant Primary Residence Yes SFR Yes 2-4 Units Yes* PUD Yes Condo** Yes New Construction No Mixed Use No Co-operatives No Manufactured Housing No Max Mortgage cannot exceed 100% of the After -Improved value

63 Property Eligibility (continued): Applies to Full Consultant options: New construction not eligible Properties must be considered existing and completed for at least 1 year (CO required for 1 year) Demolished homes or homes that will be torn down during the rehab process are eligible provided a portion of the original foundation is in place All health and safety issues must be addressed through the renovation loan

64 Property Eligibility: REOs are eligible Qualifying Ratios: Per AUS findings Reserves: Per AUS findings Self Help: Self Help, or work completed by the Borrower, is not eligible under any circumstances Also known as DIY

65 Seller Contributions: Allowed up to 6% of the sales price Super Storm Sandy: Specific requirements for property identified in declared disaster area impacted by Sandy: See matrix for specifics Eligible on Full Consultant only Additional requirements vary and include but are not limited to: Flood Elevation Certificate, Structural Engineer Report, HUD Consultant Feasibility Study Effective for case numbers 9/27/13-3/27/15 Restriction: max base loan amount cannot exceed 100% of After- Improved Value of property See ML for additional details

66 Taxes and Insurance Qualification: Taxes for qualification purposes for purchases and refinances: Calculate off of current property taxes, regardless of property state location Insurance for qualification purposes for purchases and refinances: Calculate off of After-Improved value

67 Utilities Not In Good Working Order: If utility inspection reveals utilities are not in good working order, Contractor Bid(s) must specify required repairs Full Consultant only: Work Write-Up utility repair must match Contractor Bid(s) Utility Requirements: Utilities must be inspected to ensure they are in good working order If utilities are not on or are not in good working order, a 15% Contingency Reserve will be required for Full Consultant This includes winterized properties This includes REO s with winterized utilities Utilities On At Time Of Inspection and In Good Working Condition: Appraiser or other licensed professional* must confirm in writing the following: Utilities visually inspected Utilities appear to be in good working order *Acceptable licensed professionals: Consultant, Inspector, Contractor, Plumber or Electrician

68 Utilities Not On At Time Of Inspection: Utilities not on at time of inspection and Work-Write Up does not require repairs, the following alternative documentation to validate condition of utilities may be provided: Winterized Property: winterization certification Certification from acceptable licensed professional * confirming utilities in good working order REO properties home inspection from listing report * Acceptable licensed professionals: Consultant, Inspector, Contractor, Plumber or Electrician

69 Utility Guidance REO Property: REO s typically have winterized utilities since the property is vacant Proof of winterization required via: Winterization certification OR Home inspection from listing report Winterized properties always require a 15% Contingency Reserve

70

HomeStyle Renovation Product Offering 8/29/14

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

FHA 203(k) Product Offering 8/12/14

Product Offering 8/12/14") FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

Benefits to Borrower - Why Renovation?

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

FHA 203(k) Rehabilitation Mortgage REMN Wholesale Product Description

Rehabilitation Mortgage REMN Wholesale Product Description") PROGRAM OVERVIEW STANDARD... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 LIMITED... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 Footnotes...

PROGRAM OVERVIEW STANDARD... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 LIMITED... 3 Primary Residence 1-4 Unit... 3 Purchase... 3 Rate/Term... 3 Cash-Out... 3 Footnotes...

FHA 203(k) Standard Product Guide

Standard Product Guide") FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

Limited FHA 203K. Village Mortgage NMLS Intended for Mortgage Professionals Only 1

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

FNMA Homestyle Steps to Success

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

Products. Loan Amount

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

FHA 203(K) PROGRAM. General Description. Overlays. Available Options

PROGRAM. General Description. Overlays. Available Options") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

Renovating and Rebuilding America - One Home at a Time. FHA 203(K) Renovation Lending Product Information

Renovation Lending Product Information") FHA 203(K) Product Information 1 Program Summary The FHA 203(k) The FHA 203(k) loan allows a borrower to purchase or refinance and repair or renovate a property all in one loan. The borrower closes with

FHA 203(K) Product Information 1 Program Summary The FHA 203(k) The FHA 203(k) loan allows a borrower to purchase or refinance and repair or renovate a property all in one loan. The borrower closes with

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

This saves borrowers thousands of dollars out of pocket.

A 203(k) loan is a loan that allows the borrower to purchase or refinance a home and include in the loan the costs to do repairs, upgrades and remodeling of the home. This saves borrowers thousands of

A 203(k) loan is a loan that allows the borrower to purchase or refinance a home and include in the loan the costs to do repairs, upgrades and remodeling of the home. This saves borrowers thousands of

FHA 203(k) () streamline mortgage Program. make improvements all with a single loan

() streamline mortgage Program. make improvements all with a single loan") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

Revised 4/6/18. FHA 203K Renovation

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

203(k) Program Full and Streamline

Program Full and Streamline") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

FHA 203(k) () streamline mortgage Program

() streamline mortgage Program") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

Understanding The FHA 203(k) Rehab Streamline Loan Program

Rehab Streamline Loan Program") Understanding The FHA 203(k) Rehab Streamline Loan Program FHA s 203K Streamline Rehab Program The FHA 203(k) program is HUD s primary program for the rehabilitation and repair of residential properties

Understanding The FHA 203(k) Rehab Streamline Loan Program FHA s 203K Streamline Rehab Program The FHA 203(k) program is HUD s primary program for the rehabilitation and repair of residential properties

Revised 04/30/18. FHA Standard 203K

Revised 04/30/18 FHA Standard 203K FHA Standard 203K Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official

Revised 04/30/18 FHA Standard 203K FHA Standard 203K Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official

FHA Renovation Loan Program, or 203K

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

203k Quick Reference Guide

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

Renovate your Real Estate Business

Renovate your Real Estate Business Shawn Barsness NMLS ID #67292 Renovation Lending This class is to help real estate agents better serve their clients by understanding how renovation loans work to solve

Renovate your Real Estate Business Shawn Barsness NMLS ID #67292 Renovation Lending This class is to help real estate agents better serve their clients by understanding how renovation loans work to solve

Subject Property Not in Perfect Condition? Know All the Renovation Financing Options! 9/7/2016. Back in the old days

Subject Property Not in Perfect Condition? Know All the Renovation Financing Options! Back in the old days Homebuyers had difficulty finding workable financing options for home repairs, renovations and

Subject Property Not in Perfect Condition? Know All the Renovation Financing Options! Back in the old days Homebuyers had difficulty finding workable financing options for home repairs, renovations and

FHA 203K MATRIX. Second Appraisal Requirements

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

WCDA LOAN PRODUCT MATRIX

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

Conventional and Government Program Overlays

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Under Construction. Construction and Rehab Loan Programs

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

203K Steps to Success

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

Good for 120 days. Minimum Required Investment Little to NO reserves ARMS allowed Manual Underwriting is Allowed

FHA PURCHASE Credit Score 620+ Score required ----------- 580-619 -with 2 month PITI reserves -NO gift funds -Max base loan $417,000 Max LTV 1/1/5 3/1/5 5/2/6 ARMs Appraisal 96.5% Allowed Yes Good for

FHA PURCHASE Credit Score 620+ Score required ----------- 580-619 -with 2 month PITI reserves -NO gift funds -Max base loan $417,000 Max LTV 1/1/5 3/1/5 5/2/6 ARMs Appraisal 96.5% Allowed Yes Good for

Properties listed with the following two logos are eligible: and

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate FNMA only Eligible properties must be owned by Fannie Mae (as a result of foreclosure or other similar action such as deed-in-lieu of foreclosure), sold by

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate FNMA only Eligible properties must be owned by Fannie Mae (as a result of foreclosure or other similar action such as deed-in-lieu of foreclosure), sold by

PURCHASE. Max Ratios MINIMUM FICO 550 MINIMUM FICO 580 MINIMUM FICO 620. Regardless of AUS Maximum 45%/49.99%

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 550 90.00% 96.50% MINIMUM FICO 580 MINIMUM FICO 620 43% 0 X 30 Past 12 Months 43%* 0 X 30 Past 12 Months 96.50% Regardless

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 550 90.00% 96.50% MINIMUM FICO 580 MINIMUM FICO 620 43% 0 X 30 Past 12 Months 43%* 0 X 30 Past 12 Months 96.50% Regardless

Assistance Program: Miami Dade County PHCD Affordable Housing First Time Homebuyer Program Code: DFLMIAMCY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

PRODUCT GUIDELINES FHA 203K STREAMLINE PROGRAM CODES: F30F203K, H30F203K

90.00%* 96.5%* 96.5%*...... PURCHASE MINIMUM FICO 580 ** *The maximum on a Purchase transaction is 96.5% of the LESSER of 110%** of the after improved value or the sum of the 'as is' appraised value or

90.00%* 96.5%* 96.5%*...... PURCHASE MINIMUM FICO 580 ** *The maximum on a Purchase transaction is 96.5% of the LESSER of 110%** of the after improved value or the sum of the 'as is' appraised value or

Fannie Mae Conforming and High Balance

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

FNMA Jumbo Conforming Fixed & ARM (HIGH BALANCE LOANS) T300J 30 Year Fixed & T301J 15 Year Fixed A341J 5/1 ARM & A342J 7/1 ARM 30 Year Adjustable

T300J 30 Year Fixed & T301J 15 Year Fixed A341J 5/1 ARM & A342J 7/1 ARM 30 Year Adjustable") High Balance loan limits (including 2013) are posted on E Fannie Mae website. Link: https://www.efanniemae.com/sf/refmaterials/loanlimits/xls/loanlimref.xls The following link can also be used for specific

High Balance loan limits (including 2013) are posted on E Fannie Mae website. Link: https://www.efanniemae.com/sf/refmaterials/loanlimits/xls/loanlimref.xls The following link can also be used for specific

FHA 203(k) Standard and Limited

Standard and Limited") In order to participate in Impac s 203(k) program, a relationship must be established between Seller and either Trinity Real Estate Solutions, Inc. or National Capital Funding regarding construction management

In order to participate in Impac s 203(k) program, a relationship must be established between Seller and either Trinity Real Estate Solutions, Inc. or National Capital Funding regarding construction management

Plaza s VA Renovation

Click here to add a longer headline about the slide Plaza s VA Renovation July 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial

Click here to add a longer headline about the slide Plaza s VA Renovation July 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial

***UPDATED 9/5/18*** TPO Fannie Mae HomeStyle Renovation Product

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

Renovation Lending Suite

Renovation Lending Suite M A R C H, 2 0 1 9 4/10/2019 1 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why

Renovation Lending Suite M A R C H, 2 0 1 9 4/10/2019 1 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why

Federal Housing Administration (FHA) Product Matrix

Product Matrix") APPRAISAL All FHA appraisals are valid for 120 days including New Construction and HUD REO s. FHA approved lenders are prohibited from accepting appraisals prepared by appraisers who are selected, retained

APPRAISAL All FHA appraisals are valid for 120 days including New Construction and HUD REO s. FHA approved lenders are prohibited from accepting appraisals prepared by appraisers who are selected, retained

PURCHASE. Max Ratios MINIMUM FICO 550 MINIMUM FICO 580 MINIMUM FICO 620. Regardless of AUS Maximum 45%/49.99%

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 550 90.00% 96.50% MINIMUM FICO 580 MINIMUM FICO 620 43% 0 X 30 Past 12 Months 43%* 0 X 30 Past 12 Months 96.50% * DTI

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 550 90.00% 96.50% MINIMUM FICO 580 MINIMUM FICO 620 43% 0 X 30 Past 12 Months 43%* 0 X 30 Past 12 Months 96.50% * DTI

Buy a home, plus make improvements, with just one loan

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

Non-Agency Jumbo 5/1 LIBOR ARM PRODUCT CODE A512

Product Overview: This is a variable rate mortgage product, without negative amortization, whereby the interest rate and payment is adjusted in accordance with the specified index. Index: The index used

Product Overview: This is a variable rate mortgage product, without negative amortization, whereby the interest rate and payment is adjusted in accordance with the specified index. Index: The index used

Rehab Financing The FHA Streamline 203(k) Program

Program") The FHA Streamline 203(k) Program A Guide to Financing Your Home Improvement Project The Program: This is a new 1 st mortgage program sponsored by the FHA and designed to provide homeowners with low-cost

The FHA Streamline 203(k) Program A Guide to Financing Your Home Improvement Project The Program: This is a new 1 st mortgage program sponsored by the FHA and designed to provide homeowners with low-cost

HomeStyle Renovation & Energy Mortgages. Finance renovation or energy efficient costs into a single-close home purchase or refinance loan

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

Multiple Financed Properties Program Fannie Mae/Freddie Mac. Table of Contents

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

FHA FIXED PROGRAM HIGHLIGHTS

Product Summary These guidelines represent the companies underwriting requirements for FHA fixed rate and ARM mortgages, and are to be utilized in conjunction with the following FHA Handbooks: 4155.1 for

Product Summary These guidelines represent the companies underwriting requirements for FHA fixed rate and ARM mortgages, and are to be utilized in conjunction with the following FHA Handbooks: 4155.1 for

ENERGY EFFICIENT HOMES DELEGATED CLIENTS ONLY

ENERGY EFFICIENT HOMES DELEGATED CLIENTS ONLY These programs enable the borrower to cover the cost of making energy efficiency improvements to an existing property at the time of purchase or refinance

ENERGY EFFICIENT HOMES DELEGATED CLIENTS ONLY These programs enable the borrower to cover the cost of making energy efficiency improvements to an existing property at the time of purchase or refinance

PURCHASE. Max Ratios MINIMUM FICO 550 MINIMUM FICO 580 MINIMUM FICO 620. Regardless of AUS Maximum 45%/49.99%

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 550 90.00% 96.50% 96.50% * DTI may exceed 43% with compensating factors documented in the file and manual underwrite.

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 550 90.00% 96.50% 96.50% * DTI may exceed 43% with compensating factors documented in the file and manual underwrite.

Fannie Mae High Balance Matrix

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

Holidays; DU Version 9.2; Reminders and USDA

Holidays; DU Version 9.2; Reminders and USDA Purpose This announcement includes the following topics: Holiday Schedule. DU Version 9.2. Updates and Corrections Made. Reminder: FHA/VA ARM Look Back Period

Holidays; DU Version 9.2; Reminders and USDA Purpose This announcement includes the following topics: Holiday Schedule. DU Version 9.2. Updates and Corrections Made. Reminder: FHA/VA ARM Look Back Period

Your Home Should Be YOUR WAY. That s the FAIR WAY! A Renovation Guide Made Simple

Your Home Should Be YOUR WAY That s the FAIR WAY! A Renovation Guide Made Simple Table of Contents The Renovation Loan: A Solution to a Problem... 3 Options for Renovation... 4 10 FHA 203k Standard FHA

Your Home Should Be YOUR WAY That s the FAIR WAY! A Renovation Guide Made Simple Table of Contents The Renovation Loan: A Solution to a Problem... 3 Options for Renovation... 4 10 FHA 203k Standard FHA

FHA 203(k) Standard and Limited

Standard and Limited") In order to participate in Impac s 203(k) program, a relationship must be established between Seller and Trinity Real Estate Solutions, Inc. regarding construction management for pre- and post-closing

In order to participate in Impac s 203(k) program, a relationship must be established between Seller and Trinity Real Estate Solutions, Inc. regarding construction management for pre- and post-closing

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

One-Close Construction

RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction

RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

ONE TIME CLOSE RENOVATION TO PERM OPTION III

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

One loan to renovate. Your homebuyer guide to renovation

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

Know Your Products. Marc Kaplan, Sr. VP Retail Sales

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 500 MINIMUM FICO 580

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 500 90.00% 1-4 UNITS. PER FHA MAX COUNTY LIMITS FOR STANDARD PROGRAM. Manual: 43% 0 X 30 Past 12 Months MINIMUM FICO

PURCHASE Maximum LTV Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 500 90.00% 1-4 UNITS. PER FHA MAX COUNTY LIMITS FOR STANDARD PROGRAM. Manual: 43% 0 X 30 Past 12 Months MINIMUM FICO

Correspondent Lending FHA Fixed Rate & ARM Product Profile

Government Occupancy Correspondent Lending ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM High Balance 15 & 30 YR Fixed Rates Primary Residence Purchase Property

Government Occupancy Correspondent Lending ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM High Balance 15 & 30 YR Fixed Rates Primary Residence Purchase Property

Maximum LTV/FICO Requirements. No Cash-out Refinance

PennyMac Correspondent Group FHA 203(k) Product Profile Overlays to FHA are underlined Lenders must be approved by PennyMac prior to delivering 203(k) loans. 09.23.2015 Maximum LTV/FICO Requirements Purchase

PennyMac Correspondent Group FHA 203(k) Product Profile Overlays to FHA are underlined Lenders must be approved by PennyMac prior to delivering 203(k) loans. 09.23.2015 Maximum LTV/FICO Requirements Purchase

FNMA HomeStyle Steps to Success

WHOLESALE EDITION - Nov 2013 FNMA HomeStyle Steps to Success Step One- Program Education Register for classes at M&T University Review Program Product Pages and M&T Agency Underwriting and Eligibility

WHOLESALE EDITION - Nov 2013 FNMA HomeStyle Steps to Success Step One- Program Education Register for classes at M&T University Review Program Product Pages and M&T Agency Underwriting and Eligibility

Search Tip: Use the CTRL+F Key to find words within this document.

Table of Contents TABLE OF CONTENTS... 1 1. PROGRAM BASICS... 5 1.1. Overview... 5 1.2. Product Codes... 5 1.3. Occupancy Types... 5 1.4. Eligible States... 5 1.5. LTV/CLTV... 5 1.5.1. Rehabilitation Loan

Table of Contents TABLE OF CONTENTS... 1 1. PROGRAM BASICS... 5 1.1. Overview... 5 1.2. Product Codes... 5 1.3. Occupancy Types... 5 1.4. Eligible States... 5 1.5. LTV/CLTV... 5 1.5.1. Rehabilitation Loan

Assistance Program: Hernando County SHIP Down Payment Assistance Program Code: DFLHCSHIP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

FULL DOC. PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO. Owner Occupied (O/O) 1 unit 80% 80% unit (see MI section below) 95% 95% 700

1 unit 80% 80% unit (see MI section below) 95% 95% 700") FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

INSURING QUALITY ASSURANCE CHECKLIST

Borrower: Loan #: Late Endorsement Letter Yes No N/A 1. Present in the file if endorsed 60 days or more after disbursement date: a. If PR applied on loan, payment history reflects PR amount as well as

Borrower: Loan #: Late Endorsement Letter Yes No N/A 1. Present in the file if endorsed 60 days or more after disbursement date: a. If PR applied on loan, payment history reflects PR amount as well as

PRODUCT GUIDELINES FHA 203K LIMITED PROGRAM CODES: F30F203K, H30F203K

Maximum LTV 90.00%* 96.5%* 96.5%* **DTI may exceed 31%/43% with compensating factors documented in the file and manual underwrite. Refer to Manual Underwrite section for additional information. ***Refer

Maximum LTV 90.00%* 96.5%* 96.5%* **DTI may exceed 31%/43% with compensating factors documented in the file and manual underwrite. Refer to Manual Underwrite section for additional information. ***Refer

VERY IMPORTANT THE LOAN WILL BE RUN THROUGH DU PRIOR TO START OF CONSTRUCTION AND MUST REFLECT APPROVE ELIGIBLE.

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

HomeStyle Renovation Program Conforming & High Balance Loan Amounts Fixed Rate Only. Applies to loans submitted to DU 10.1

Conforming & High Balance Loan Amounts Fixed Rate Only Applies to loans submitted to DU 10.1 Owner-Occupied Primary Residence Transaction Type Units LTV 1 CLTV Loan Amount 2 Credit Score Purchase/ Limited

Conforming & High Balance Loan Amounts Fixed Rate Only Applies to loans submitted to DU 10.1 Owner-Occupied Primary Residence Transaction Type Units LTV 1 CLTV Loan Amount 2 Credit Score Purchase/ Limited

Annoucement Correspondent Lending

Superior Performance Our Commit ment New VP Correspondent Lending Turn Times New Correspondent Team Members Update Guidelines Annoucement 2011 10-25 Correspondent Lending IN THIS ANNCOUNCEMENT 203Ks Updated

Superior Performance Our Commit ment New VP Correspondent Lending Turn Times New Correspondent Team Members Update Guidelines Annoucement 2011 10-25 Correspondent Lending IN THIS ANNCOUNCEMENT 203Ks Updated

Document Checklist for 203k Loans

Document Checklist for 203k Loans HUD-92700: 203(k) and Streamlined (k) Maximum Mortgage Worksheet HUD-92700a: 203(k) Borrower's Acknowledgment Appraisal with all improvements listed on Repairs & Updates

Document Checklist for 203k Loans HUD-92700: 203(k) and Streamlined (k) Maximum Mortgage Worksheet HUD-92700a: 203(k) Borrower's Acknowledgment Appraisal with all improvements listed on Repairs & Updates

Fannie Mae has specific requirements for multiple financed properties:

Fannie Mae has specific requirements for multiple financed properties: If subject loan is owner occupied, Fannie Mae has no limit on number of properties financed If subject is second home or investment

Fannie Mae has specific requirements for multiple financed properties: If subject loan is owner occupied, Fannie Mae has no limit on number of properties financed If subject is second home or investment

WINTRUST (WM) CONFORMING FIXED LP

CONFORMING FIXED LP") LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPLICATION:... 3 APPRAISAL REQUIREMENTS:...

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPLICATION:... 3 APPRAISAL REQUIREMENTS:...

AFR JUMBO OVERVIEW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

Conforming Loans as of October 24, 2007

Conforming Loans Fixed Rate, Fixed Period ARMs, and Standard ARMs (Full/Alt Documentation) (Standard Amortization) Cash Out Refinances Occupancy 1 1 1 1 1 1 1-Unit Properties 95/95% 95/95% 85/85% 2-Unit

Conforming Loans Fixed Rate, Fixed Period ARMs, and Standard ARMs (Full/Alt Documentation) (Standard Amortization) Cash Out Refinances Occupancy 1 1 1 1 1 1 1-Unit Properties 95/95% 95/95% 85/85% 2-Unit

CHOOSING THE RIGHT MORTGAGE PARTNER

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

FHA Fixed Rate/Adjustable Rate FHA Streamline Refinances. Underwriting Guidelines GFF3000/GFF2000/GFF1500 GAF3115/GAF5115

FHA Fixed Rate/Adjustable Rate FHA Streamline Refinances Underwriting Guidelines GFF3000/GFF2000/GFF1500 GAF3115/GAF5115 BSM Direct FHA guidelines have been created to provide guidance and consistency

FHA Fixed Rate/Adjustable Rate FHA Streamline Refinances Underwriting Guidelines GFF3000/GFF2000/GFF1500 GAF3115/GAF5115 BSM Direct FHA guidelines have been created to provide guidance and consistency

Congratulations, you have made the big decision to buy a home. Now what? There are many questions you will need to ask yourself before moving ahead:

Buyers Congratulations, you have made the big decision to buy a home. Now what? There are many questions you will need to ask yourself before moving ahead: BEFORE YOU BUY 1. Decide where you want to live.

Buyers Congratulations, you have made the big decision to buy a home. Now what? There are many questions you will need to ask yourself before moving ahead: BEFORE YOU BUY 1. Decide where you want to live.

Correspondent Guidelines Matrix

Correspondent Guidelines Matrix October 8, 2013 Version 1.2 For any questions, please call your Account Executive at 1 855 OK SUNWEST. FHA: STANDARD AND JUMBO/HIGH BALANCE Loan Purpose FICO Maximum LTV

Correspondent Guidelines Matrix October 8, 2013 Version 1.2 For any questions, please call your Account Executive at 1 855 OK SUNWEST. FHA: STANDARD AND JUMBO/HIGH BALANCE Loan Purpose FICO Maximum LTV

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

WesLend Advantage Non-QM ITIN

SECTION 1: MATRIX: Highlight: Uses the borrowers Individual Taxpayer Identification Number, (ITIN) in lieu of a Social Security number Credit Scores NOT Required Credit Report is pulled with every ITIN

SECTION 1: MATRIX: Highlight: Uses the borrowers Individual Taxpayer Identification Number, (ITIN) in lieu of a Social Security number Credit Scores NOT Required Credit Report is pulled with every ITIN

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

PURCHASE Maximum LTV* Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 500 MINIMUM FICO 580 MINIMUM FICO 620

PURCHASE Maximum LTV* Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 500 90.00%* 96.5%* MINIMUM FICO 580 MINIMUM FICO 620 43% 0 X 30 Past 12 Months 43%** Evaluated by AUS*** 96.5%* Regardless

PURCHASE Maximum LTV* Max Loan Amount Max Ratios Mortgage/Rental History MINIMUM FICO 500 90.00%* 96.5%* MINIMUM FICO 580 MINIMUM FICO 620 43% 0 X 30 Past 12 Months 43%** Evaluated by AUS*** 96.5%* Regardless

Fannie Mae (DU) Conventional Loan Matrix

Conventional Loan Matrix") PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

FHA Standard Fixed T year Fixed and T year Fixed T100 HC- 30 year Fixed High Balance loans

This product guide provides Product High Lights Only. Please refer to applicable HUD Handbooks, Mortgagee Letters, Federal Register Updates and HUD Notices for specific criteria. In addition, your local

This product guide provides Product High Lights Only. Please refer to applicable HUD Handbooks, Mortgagee Letters, Federal Register Updates and HUD Notices for specific criteria. In addition, your local

FHA CREDIT QUALIFYING STREAMLINE REFINANCE

Table of Contents 1. Eligible Mortgage Product-Existing Loan... 2 2. FICO... 2 3. Eligible Mortgage Product-New Loan... 2 4. Maximium Loan Amount... 2 5. Maximium LTV/CLTV... 2 6. MIP Requirements..2-4

Table of Contents 1. Eligible Mortgage Product-Existing Loan... 2 2. FICO... 2 3. Eligible Mortgage Product-New Loan... 2 4. Maximium Loan Amount... 2 5. Maximium LTV/CLTV... 2 6. MIP Requirements..2-4

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions Fixed Rate

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions Fixed Rate

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

CONTRACTOR'S GUIDE 203(K) STANDARD

STANDARD") CONTRACTOR'S GUIDE 203(K) STANDARD CONTRACTOR'S CHECKLIST Contractor Profile W-9 Contractor's License(s) General Liability (Certificate of Insurance) Workman's Comp (Certificate of Insurance) Disclosures

CONTRACTOR'S GUIDE 203(K) STANDARD CONTRACTOR'S CHECKLIST Contractor Profile W-9 Contractor's License(s) General Liability (Certificate of Insurance) Workman's Comp (Certificate of Insurance) Disclosures

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs Red indicates changes from previous matrix Overlays to Investor guidelines are underlined and in italics Owner Occupied

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs Red indicates changes from previous matrix Overlays to Investor guidelines are underlined and in italics Owner Occupied

All-in-One Custom Construction

Wholesale Lending All-in-One Custom Construction This is a true one-time-close loan program designed to finance the construction or major remodel of a primary residence or second home. This loan includes

Wholesale Lending All-in-One Custom Construction This is a true one-time-close loan program designed to finance the construction or major remodel of a primary residence or second home. This loan includes

Assistance Program: City of Los Angeles Low Income Purchase Assistance Program (LIPA) Zero Interest Code: DCALIPADP

Zero Interest Code: DCALIPADP") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

PRODUCT GUIDELINES CONVENTIONAL CONFORMING HIGH BALANCE PROGRAM (DU ONLY)

") PURCHASE, RATE &TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount LTV CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves 90%* 90%* 620 75.0% 75.0% 75.0% 75.0% 620 620

PURCHASE, RATE &TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount LTV CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves 90%* 90%* 620 75.0% 75.0% 75.0% 75.0% 620 620