ISLAMIC REPUBLIC OF AFGHANISTAN

|

|

|

- Elijah Golden

- 5 years ago

- Views:

Transcription

International Monetary Fund International Development Association Afghanistan s external debt is low after extensive debt relief, but given its heavy reliance on grant financing (")

1 November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen (IDA) International Monetary Fund International Development Association Afghanistan s external debt is low after extensive debt relief, but given its heavy reliance on grant financing ( percent of GDP in, including both on and off-budget grants), public external debt is judged to remain at high risk of distress according to the IMF-World Bank framework. Under the baseline scenario, with strong reform effort and donor support, improved security and reduced uncertainty, debt is sustainable. However, under a scenario assuming a plausible grant-financing shortfall, debt burden indicators quickly become unsustainable. If security and macroeconomic conditions improve, an improvement of the risk rating could be considered in a future assessment. Accordingly, the authorities should continue their efforts to mobilize revenue, raise the efficiency of public spending through careful prioritization, and press ahead with their reform efforts, while donors should continue to provide financing in the form of grants. This DSA was prepared by IMF staff with input from World Bank, using the standard debt sustainability framework for low-income countries (LIC-DSA); see Staff Guidance Note on the Application of the Joint Bank-Fund Debt Sustainability Framework for Low-Income Countries The LIC-DSA compares the evolution over the projection period of debt-burden indicators against policy-dependent indicative thresholds, using the three-year average of the World Bank s Country Policy and Institutional Assessment (CPIA). With an average CPIA of., Afghanistan is classified as having weak performance under the LICDSF.

2 MACROECONOMIC OUTLOOK. The DSA s baseline macroeconomic scenario assumes a gradual improvement of security with continued reform and donor support during the Transformation Decade ( ). This scenario is similar to the previous DSA of April (Box ). The baseline also assumes political stability with regular election cycles and continued economic reform with governments delivering on Afghanistan s development goals and priorities that improve the business environment and governance to support privatesector-led inclusive growth. The baseline scenario also assumes continued donor support, in line with donors statements at the December London Conference, namely, their Tokyo commitment of providing $ billion through, and sustaining support, through, at or near the levels of the past decade. Going forward, donors committed to significant and continuing support that would decline. This support for Afghanistan s social and economic development priorities through the Transformation Decade is predicated on the Afghan government delivering on its commitments under the Mutual Accountability Framework. At the same time, donors expect that Afghanistan will gradually increase its contribution and, over time, assume financial costs of the security sector. Box. Macroeconomic Assumptions Comparison Table / DSA February DSA October Current vs. previous Real growth (%) Inflation (GDP, deflator, %) Nominal GDP (Billions of Afghanis) - - Revenue and grants (% GDP) Grants (% GDP) Primary expenditure (% GDP) Primary balance (% GDP) Exports of G&S (% GDP) Imports of G&S (% GDP) / Noninterest current account balance (%GDP) Sources: Afghan authorities; and IMF staff estimates and projections. / The differences between the base period exports and imports in the current and previous DSAs are explained by having new and improved data as well as new mining sector projections. / Change in imports in - between the current and previous DSAs is due to higher grant related imports.. In this scenario, growth is projected to recover and the external current account (before grants) to improve gradually. GDP growth is projected to average about percent in the In the baseline, total off budget and on budget grants are projected to decline as a share of GDP, from percent in to percent in, and percent in, with an increasing share provided to the civilian sector.

3 medium term ( ), supported by investment and production in the mining industry later in the decade, and to stabilize at about ½ percent in the long run (Table ), similar to the projection in the previous DSA. The main change relative to the previous DSA relates to lower growth rates in the near term. This lower growth is due to a slower recovery in economic confidence than projected earlier, because the political transition was longer than expected and some delays in planned implementation of mining projects as well as lower commodity prices. This lower growth is expected to be temporary, as the political transition has been completed. Growth is expected to gain steam with a recovery in confidence, increasing mining and energy related activity from onwards and the impact of continued reform, although there is downside risk that mining development could be delayed with renegotiation of several contracts and weaker commodity prices. The external current account deficit before grants is expected to improve gradually over the projection period as a whole. The initial deterioration of the external current account reflects the import of mining-related capital goods in minerals extraction. Non-mineral exports are projected to increase progressively from a low level. At the same time, imports are projected to stabilize in outer years with donor-financed imports slowing. Accordingly, the current account deficit excluding grants should narrow gradually from about percent of GDP in to about percent of GDP at the end of the projection horizon (Figure ). Figure : Current Account Balance, (In percent of GDP) Figure : Current Account Balance incl. Grants, (In percent of GDP) - Total grants to budget - Private savings Total off-budget grants - Private investments CA balance excl. grants CA balance incl. grants - - Sources: Afghan authorities; and IMF staff calculations.. Expenditures would decline marginally as a share of GDP over the coming decade. Expenditures are driven by three factors: security, development, and the civilian operating costs, including wages, pension contributions, and operating and maintenance costs of public infrastructure. Security spending will remain substantial and is projected to reach percent of GDP by, decline to percent by, and stabilize at about percent in the outer years, as security conditions improve and with some reduction in the size of security forces that will start toward the end of this decade. Non-security operating spending is expected to grow as the onbudget transfer of spending that was previously donor-managed and the associated large

4 operations and maintenance costs related to donor-funded infrastructure projects continues. Finally, public spending will also rise on account of increases in the size of the civil service, particularly in health and education, to facilitate a meaningful progress towards the Sustainable Development Goals, and a gradual rise in pensions. Given Afghanistan s large development needs, development spending, including off budget spending, is projected to be about percent of GDP, an increase of percent of GDP on budget in this decade to meet Afghanistan s human development and infrastructure needs.. Significant growth in domestic revenues is projected in the medium term, despite the VAT introduction and mining revenue coming on stream only later. Domestic revenues declined by. percentage points of GDP during, reflecting lower compliance and enforcement as well as lower import growth and economic activity due to political and security uncertainties. Furthermore, VAT implementation planned for has been postponed. Other revenue measures were introduced in, to help mitigate the revenue impact of the postponement of the VAT introduction, and are expected to mobilize revenue of around percent of GDP per year in the medium term. The impact of mining and energy projects on the medium-term revenue outlook remains substantial notwithstanding the delay compared to the DSA. The introduction of VAT by the end of decade and a sustained effort to improve compliance will also be needed. The baseline scenario assumes that: (i) the VAT introduction in will yield around percent of GDP in its initial years and above percent of GDP in the long term; (ii) the tax policy mix is improved, e.g. through the introduction of excise and property taxes, and rationalization of exemptions will yield up to percent of GDP in additional revenues after ; (iii) tax and customs administration reforms will be forcefully implemented; and (iv) revenues from mining and energy projects will start flowing in. As a result, by the ratio of domestic revenues to GDP will reach - percent of GDP, similar to the previous DSA, and percent of GDP by, a level that is typical for a lowincome country.. Given these revenue and expenditure trends, Afghanistan s total financing needs are expected to remain significant. Over the long term, the overall budget deficit (excluding grants) will remain at above percent of GDP, as in the previous DSA. A small share could be financed from external concessional loans, and there is also some limited scope for domestic financing through a sukuk projected to be introduced in mainly for market development and liquidity management purposes. This will leave a projected financing gap of over percent of GDP in and beyond. Fiscal sustainability defined as domestic revenues covering operating spending will likely only to be reached after. The recurrent operation and maintenance costs for all assets built in Afghanistan since, excluding the security sector, are estimated at about $ billion annually or more and growing as new assets are being built. Sustainment costs in the security sector are harder to estimate, but could be as high as $ billion per year. Wage restraint is assumed, with the wage growth rate indexed to inflation until and limited to percentage points over inflation until, and equal to nominal GDP growth rate after.

5 Table. Islamic Republic of Afghanistan: Medium-Term Macroeconomic Framework, Act. Projections Medium-term Long-term Averages (Annual percentage change, unless otherwise indicated) Output and prices / Real GDP Nominal GDP (in billions of U.S. dollars) Consumer prices (period average) / (In percent of GDP, unless otherwise indicated) Public finances (central government) Domestic revenues and grants Domestic revenues Grants Expenditures Operating / Development Operating balance (excluding grants) / Overall budget balance (including grants) External sector / Exports of goods (in U.S. dollars, percent change) Imports of goods (in U.S. dollars, percent change) Merchandise trade balance Current account balance, including official transfers Excluding official transfers Gross reserves (in millions of U.S. dollars) , , , , , , , , , , Public Debt Total public debt of which: Public external debt / Sources: Afghan authorities; and Fund staff estimates and projections. / Excluding the narcotics economy. / Revised with improved coverage. / Comprising mainly current spending. It is assumed that donors' recurrent expenditure off-budget is moved onto the budget by. The actual rate of transfer on-budget is uncertain. / Defined as domestic revenues minus operating expenditures. / After HIPC and MDRI debt relief, as well as debt relief beyond HIPC relief from Paris Club creditors. DEBT SUSTAINABILITY ANALYSIS. Afghanistan s public debt remains modest. Afghanistan passed the HIPC completion point and received debt relief in. External public and publicly guaranteed debt amounted to $. billion, or. percent of GDP in, mostly to multilateral creditors. It is equivalent to. This debt stock is after delivery of the already-pledged debt relief commitments and excluding some minimal amounts of non-yet-reconciled or disputed debt. Afghanistan is still following up with one Paris Club creditor on its debt relief commitments, as well as with several non-paris Club creditors on debt relief on comparable terms. In terms of debt structure and composition: apart from a small amount of legacy debt (less than percent of total), most of the external debt is owed to multilateral institutions, mainly regional and international financial institutions.

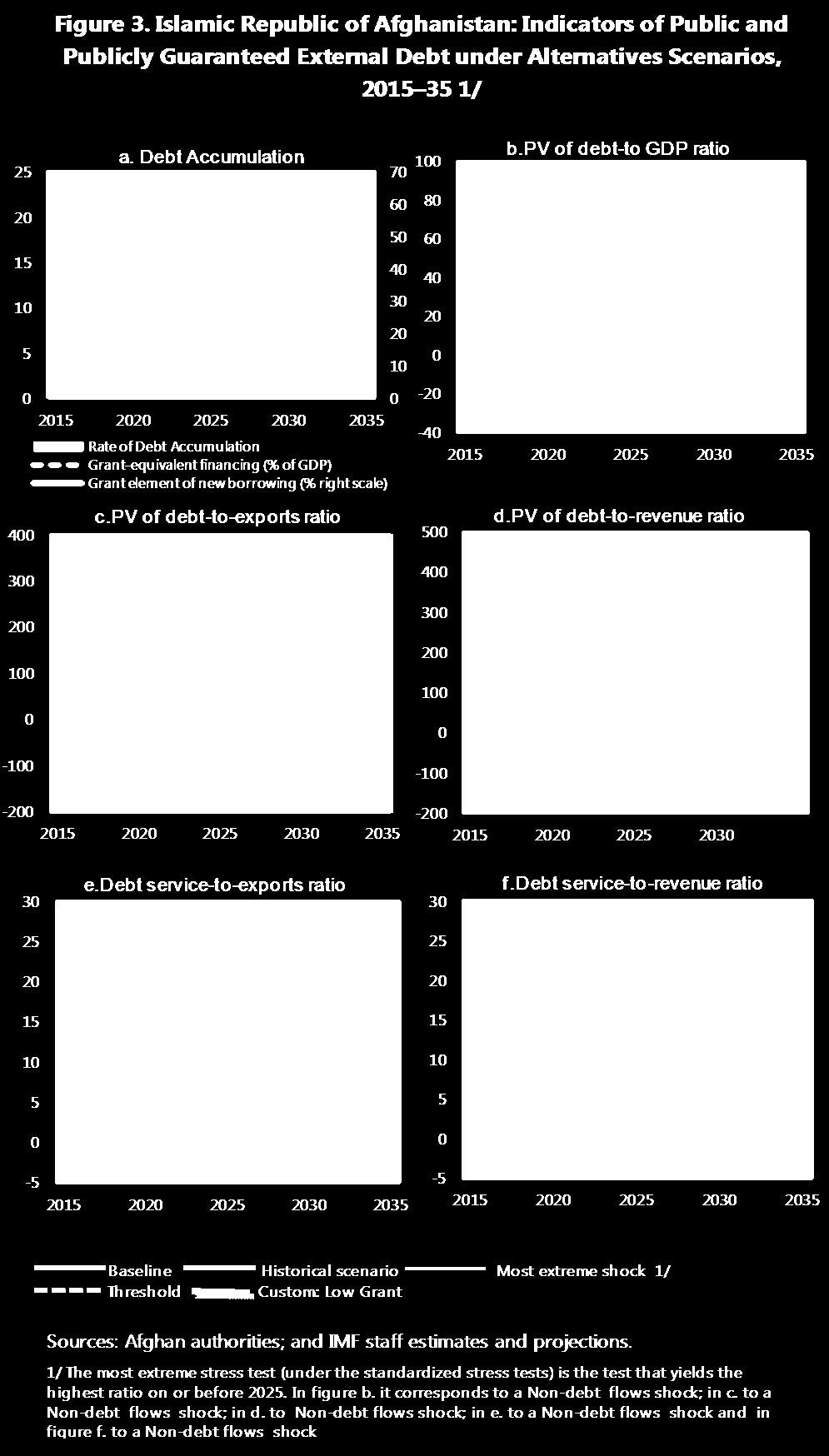

6 percent of GDP in present value (PV) terms, and to about percent of exports and percent of government revenues (Table a). Under the baseline scenario in which Afghanistan s financing gap, net of domestic financing, is entirely met by grants the present value of public external debt would be about. percent of GDP by the end of the projection period, while total public debt would be. percent of GDP, both below the indicative debt-burden threshold applicable to a country like Afghanistan.. Although the debt burden is modest, potential risks to grant financing put Afghanistan at high risk of external debt distress. Risks to this baseline include an abrupt decline in grants (an alternative scenario) combined with a shift towards debt financing, a deterioration in the security situation, which would put upward pressure on spending, or slow or reverse revenue mobilization reforms. These factors could put Afghanistan s debt burden on an unsustainable path. While donors have reconfirmed their financial support in the short to medium term at the London Conference, the longer-term prospects are less certain and will be discussed in at the Warsaw and Brussels conferences.. The standard Debt Sustainability Framework shocks result in benign outcomes. They result only in three breaches of the debt thresholds (the present value (PV) of external debt to exports and PV of external debt to revenue during this decade and PV of public debt to GDP ratio by the end of the projection period). However, the standard shocks generated by the Debt Sustainability Framework are mostly driven by the economic performance over the past ten years. While for many countries the recent past might be a useful guide for projections, this is less so in the case of Afghanistan with average annual real GDP growth of. percent and official transfers of percent of GDP. The high GDP growth represented a catch-up from a low post-conflict base, and while large grant financing has been committed for the medium term, its projected magnitude is less (as a share of GDP) than grants received over the past decade, which were exceptionally large and front-loaded to finance post-conflict rehabilitation and reconstruction. Therefore, to ensure the risks are correctly captured, a customized illustrative scenario, which examines debt sustainability with plausible downside risks that are Afghanistan-specific, is developed.. The customized illustrative scenario takes into account Afghanistan s circumstances and possible downside risks and indicates that Afghanistan faces significant risks, which if realized, would breach debt thresholds and result in a high risk of debt distress. The customized scenario focuses on the debt dynamics generated by a downward shift in the grant path. This scenario does not take into account second round effects on trade, security, interest rates, and Under the DSA framework, the external debt thresholds for countries with similar economic performance and income level as Afghanistan are: for the PV of debt percent of GDP, percent of exports, and percent of revenues; for debt service, percent of exports and percent of revenues. The PV of debt to exports and PV of debt to revenue ratio thresholds are breached when net official transfers and net FDI are one standard deviation below their historical average (Figure ). The shock is applied to two years (-) and thereafter the PV of debt to exports declines. This treatment is in line with paragraphs and of the LIC-DSF Guidance Note.

7 growth. However, on the upside, if security stabilizes, and macroeconomic conditions continue to improve, the external risk rating may be lowered in future DSAs.. The customized illustrative scenario assumes a gradual drop in grants starting in. This scenario assumes that lack of progress in reforms, donor fatigue, and/or a shift in donors priorities lead to a gradual reduction in aid beginning in and reaching a level of percent of the baseline by and beyond. At the same time, it is assumed that the nominal GDP levels are similar to the baseline, the level of public services envisaged in the baseline scenario is preserved, and additional revenue is not mobilized. percent of the resulting financing gap is covered with concessional external loans, and the remainder with domestic non-concessional borrowing. Under this scenario, debt burden indicators deteriorate rapidly, breaching virtually every threshold. The PV of external debt would reach over percent of GDP, or about percent of exports, by the end of the projection period. The PV of total public debt would reach over percent of GDP, around percent of revenues, and the debt-service-to-revenue ratio will rise to about percent (Figure ). AUTHORITIES VIEWS. The authorities broadly agreed with the conclusions of the DSA. They emphasized that continued donor financing is critical to ensure debt sustainability, while delivering on their commitments to the donor community, and that they wished to keep the debt level low. They recognized substantial risks going forward, including potential donor fatigue and underscored the importance of prudent fiscal policy. The authorities also pointed out Afghanistan s large upfront expenditure needs, particularly big infrastructure projects with potentially high rates of economic and social returns, which could support regional integration and growth, and were open to exploring options to mobilize other types of financing in addition to existing donor grants, including concessional loans. They also acknowledged the IMF s advice that contracting concessional loans would require careful project selection and an independent technical appraisal of expected returns to maintain debt sustainability, given the limited debt service capacity, and for transparent recording of its financial impact. They shared staff s view that sukuks (domestic borrowing) should be used as a liquidity management instrument and to build up the treasury s cash balance, rather than to finance projects or recurrent fiscal deficits. They underscored that further aligning donor support with Afghan priorities and channeling more funds through the budget could potentially result in expenditure savings. CONCLUSIONS. Afghanistan s debt sustainability will hinge on improved security, and continued donor grant inflows. After extensive debt relief and substantial medium-term pledges from donors, Afghanistan s debt outlook, under the baseline scenario, is benign. However, this is predicated on continued economic growth, progress in reforms, improvements in security as well as all donor assistance being provided in the form of grants. The outlook is subject to three main risks. First, an escalated and prolonged conflict would dampen or stop economic growth and would imply limited

8 economic reforms and a highly constrained ability by the central government to generate budget revenues. Second, mining revenues may be delayed, lower than hoped for, or highly volatile, leading to additional financing needs, and potentially spending cuts that would impact growth. And third, donor grants may not be forthcoming in the amounts needed, also leading to spending cuts and lower growth. Under any of these scenarios, Afghanistan would need to implement compensatory measures and, in the event of a sustained drop in grants (customized illustrative scenario), its debt burden would quickly become unsustainable and could threaten, in the extreme case, the continuity of government functions. This analysis underscores the need to redouble efforts to mobilize domestic revenue with new policy measures as well as through administrative reforms to improve compliance prioritize spending carefully, pursue expenditure rationalization, and raise the efficiency of public spending. In addition, maintaining macroeconomic stability and vigorous economic reform efforts will continue to be needed to improve economic governance, strengthen the financial sector, and spur future growth.

9

10 Figure. Islamic Republic of Afghanistan: Indicators of Public Debt Under Alternative Scenarios, / Historical scenario Fix Primary Balance Public debt benchmark Most ext Most extreme shock / Low Grant PV of Debt-to-GDP Ratio PV of Debt-to-Revenue Ratio / Debt Service-to-Revenue Ratio Sources: Afghan authorities; and IMF staff estimates and projections. / The most extreme stress test is the test that yields the highest ratio on or before. / Revenues are defined inclusive of grants.

11 Table a. Islamic Republic of Afghanistan: External Debt Sustainability Framework, Scenario, / (In percent of GDP, unless otherwise indicated) Actual External debt (nominal) / of which: public and publicly guaranteed (PPG) Change in external debt Identified net debt-creating flows Non-interest current account deficit Deficit in balance of goods and services Exports Imports Net current transfers (negative = inflow) of which: official Other current account flows (negative = net inflow) Net FDI (negative = inflow) Endogenous debt dynamics / Contribution from nominal interest rate Contribution from real GDP growth Contribution from price and exchange rate changes Residual (-) / of which: exceptional financing PV of external debt / In percent of exports PV of PPG external debt In percent of exports In percent of government revenues Debt service-to-exports ratio (in percent) PPG debt service-to-exports ratio (in percent) PPG debt service-to-revenue ratio (in percent) Total gross financing need (Billions of U.S. dollars) Non-interest current account deficit that stabilizes debt ratio Historical Average / Standard Deviation / Projections Average Average Key macroeconomic assumptions Real GDP growth (in percent) GDP deflator in US dollar terms (change in percent) Effective interest rate (percent) / Growth of exports of G&S (US dollar terms, in percent) Growth of imports of G&S (US dollar terms, in percent) Grant element of new public sector borrowing (in percent) Government revenues (excluding grants, in percent of GDP) Aid flows (in Billions of US dollars) / of which: Grants of which: Concessional loans Grant-equivalent financing (in percent of GDP) / Grant-equivalent financing (in percent of external financing) / Sources: Afghan authorities; and IMF staff estimates and projections. / Includes both public and private sector external debt. / Derived as [r g ρ(+g)]/(+g+ρ+gρ) times previous period debt ratio, with r = nominal interest rate; g = real GDP growth rate, and ρ = growth rate of GDP deflator in U.S. dollar terms. / Includes exceptional financing (i.e., changes in arrears and debt relief); changes in gross foreign assets; and valuation adjustments. For projections also includes contribution from price and exchange rate changes. / Assumes that PV of private sector debt is equivalent to its face value. / Current-year interest payments divided by previous period debt stock. / Historical averages and standard deviations are generally derived over the past years, subject to data availability. / Defined as grants, concessional loans, and debt relief. / Grant-equivalent financing includes grants provided directly to the government and through new borrowing (difference between the face value and the PV of new debt) Memorandum items: Nominal GDP (Billions of US dollars). Nominal dollar GDP growth. PV of PPG external debt (in Billions of US dollars) (PVt-PVt-)/GDPt- (in percent) Gross workers' remittances (Billions of US dollars). PV of PPG external debt (in percent of GDP + remittances) PV of PPG external debt (in percent of exports + remittances) Debt service of PPG external debt (in percent of exports + remittances.....

12 Table b. Islamic Republic of Afghanistan: Sensitivity Analysis for Key Indicators of Public and Publicly Guaranteed External Debt, (In percent) Projections PV of debt-to GDP ratio A. Alternative Scenarios A. Key variables at their historical averages in - / A. New public sector loans on less favorable terms in - Customized : Lower Grants B. Bound Tests B. B. B. B. B. B. Real GDP growth at historical average minus one standard deviation in - Export value growth at historical average minus one standard deviation in - / US dollar GDP deflator at historical average minus one standard deviation in - Net non-debt creating flows at historical average minus one standard deviation in - / Combination of B-B using one-half standard deviation shocks One-time percent nominal depreciation relative to the baseline in / PV of debt-to-exports ratio A. Alternative Scenarios A. Key variables at their historical averages in - / A. New public sector loans on less favorable terms in - Customized : Lower Grants B. Bound Tests B. B. B. B. B. B. Real GDP growth at historical average minus one standard deviation in - Export value growth at historical average minus one standard deviation in - / US dollar GDP deflator at historical average minus one standard deviation in - Net non-debt creating flows at historical average minus one standard deviation in - / Combination of B-B using one-half standard deviation shocks One-time percent nominal depreciation relative to the baseline in / PV of debt-to-revenue ratio A. Alternative Scenarios A. Key variables at their historical averages in - / A. New public sector loans on less favorable terms in - Customized : Lower Grants B. Bound Tests B. B. B. B. B. B. Real GDP growth at historical average minus one standard deviation in - Export value growth at historical average minus one standard deviation in - / US dollar GDP deflator at historical average minus one standard deviation in - Net non-debt creating flows at historical average minus one standard deviation in - / Combination of B-B using one-half standard deviation shocks One-time percent nominal depreciation relative to the baseline in /

13 Table b. Islamic Republic of Afghanistan: Sensitivity Analysis for Key Indicators of Public and Publicly Guaranteed External Debt, (concluded) (In percent) Debt service-to-exports ratio A. Alternative Scenarios A. Key variables at their historical averages in - / A. New public sector loans on less favorable terms in - Customized : Lower Grants B. Bound Tests B. B. B. B. B. B. Real GDP growth at historical average minus one standard deviation in - Export value growth at historical average minus one standard deviation in - / US dollar GDP deflator at historical average minus one standard deviation in - Net non-debt creating flows at historical average minus one standard deviation in - / Combination of B-B using one-half standard deviation shocks One-time percent nominal depreciation relative to the baseline in / Debt service-to-revenue ratio A. Alternative Scenarios A. Key variables at their historical averages in - / A. New public sector loans on less favorable terms in - Customized : Lower Grants B. Bound Tests B. B. B. B. B. B. Real GDP growth at historical average minus one standard deviation in - Export value growth at historical average minus one standard deviation in - / US dollar GDP deflator at historical average minus one standard deviation in - Net non-debt creating flows at historical average minus one standard deviation in - / Combination of B-B using one-half standard deviation shocks One-time percent nominal depreciation relative to the baseline in / Memorandum item: Grant element assumed on residual financing (i.e., financing required above baseline) / Sources: Afghan authorities; and IMF staff estimates and projections. / Variables include real GDP growth, growth of GDP deflator (in U.S. dollar terms), non-interest current account in percent of GDP, and non-debt creating flows. / Assumes that the interest rate on new borrowing is by percentage points higher than in the baseline., while grace and maturity periods are the same as in the baseline. / Exports values are assumed to remain permanently at the lower level, but the current account as a share of GDP is assumed to return to its baseline level after the shock (implicitly assuming an offsetting adjustment in import levels). / Includes official and private transfers and FDI. / Depreciation is defined as percentage decline in dollar/local currency rate, such that it never exceeds percent. / Applies to all stress scenarios except for A (less favorable financing) in which the terms on all new financing are as specified in footnote.

14 Table a. Islamic Republic of Afghanistan: Public Sector Debt Sustainability Framework, Scenario, (In percent of GDP, unless otherwise indicated) Actual Public sector debt / of which: foreign-currency denominated Change in public sector debt Identified debt-creating flows Primary deficit Revenue and grants of which: grants Primary (noninterest) expenditure Automatic debt dynamics Contribution from interest rate/growth differential of which: contribution from average real interest rate of which: contribution from real GDP growth Contribution from real exchange rate depreciation Other identified debt-creating flows Privatization receipts (negative) Recognition of implicit or contingent liabilities Debt relief (HIPC and other) Other (specify, e.g. bank recapitalization) Residual, including asset changes Estimate Average Standard Deviation / / Projections - Average - Average Other Sustainability Indicators PV of public sector debt of which: foreign-currency denominated of which: external PV of contingent liabilities (not included in public sector debt) Gross financing need / PV of public sector debt-to-revenue and grants ratio (in percent) PV of public sector debt-to-revenue ratio (in percent) of which: external / Debt service-to-revenue and grants ratio (in percent) / Debt service-to-revenue ratio (in percent) / Primary deficit that stabilizes the debt-to-gdp ratio Key macroeconomic and fiscal assumptions Real GDP growth (in percent) Average nominal interest rate on forex debt (in percent) Average real interest rate on domestic debt (in percent) Real exchange rate depreciation (in percent, + indicates depreciation) Inflation rate (GDP deflator, in percent) Growth of real primary spending (deflated by GDP deflator, in percent Grant element of new external borrowing (in percent) Sources: Afghan authorities; and IMF staff estimates and projections. / Indicate coverage of public sector, e.g., general government or nonfinancial public sector. Also whether net or gross debt is used. / Gross financing need is defined as the primary deficit plus debt service plus the stock of short-term debt at the end of the last period. / Revenues excluding grants. / Debt service is defined as the sum of interest and amortization of medium and long-term debt. / Historical averages and standard deviations are generally derived over the past years, subject to data availability.

15 Table b. Islamic Republic of Afghanistan: Sensitivity Analysis for Key Indicators of Public Debt Projections PV of Debt-to-GDP Ratio A. Alternative scenarios A. A. A. A. Real GDP growth and primary balance are at historical averages Primary balance is unchanged from Permanently lower GDP growth / Alternative Scenario : Low Grant B. Bound tests B. B. B. B. B. Real GDP growth is at historical average minus one standard deviations in - Primary balance is at historical average minus one standard deviations in - Combination of B-B using one half standard deviation shocks One-time percent real depreciation in percent of GDP increase in other debt-creating flows in PV of Debt-to-Revenue Ratio / A. Alternative scenarios A. A. A. A. Real GDP growth and primary balance are at historical averages Primary balance is unchanged from Permanently lower GDP growth / Alternative Scenario : Low Grant B. Bound tests B. B. B. B. B. Real GDP growth is at historical average minus one standard deviations in - Primary balance is at historical average minus one standard deviations in - Combination of B-B using one half standard deviation shocks One-time percent real depreciation in percent of GDP increase in other debt-creating flows in Debt Service-to-Revenue Ratio / A. Alternative scenarios A. A. A. A. Real GDP growth and primary balance are at historical averages Primary balance is unchanged from Permanently lower GDP growth / Alternative Scenario : Low Grant B. Bound tests B. B. B. B. B. Real GDP growth is at historical average minus one standard deviations in - Primary balance is at historical average minus one standard deviations in - Combination of B-B using one half standard deviation shocks One-time percent real depreciation in percent of GDP increase in other debt-creating flows in Sources: Afghan authorities; and IMF staff estimates and projections. / Assumes that real GDP growth is at baseline minus one standard deviation divided by the square root of the length of the projection period. / Revenues are defined inclusive of grants.

ISLAMIC REPUBLIC OF AFGHANISTAN

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

(January 2016). The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar

. The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar") May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

STAFF REPORT FOR THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE

January 5, 216 BANGLADESH STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Markus Rodlauer and Catherine Anne Maria Pattillo (IMF) and Satu Kahkonen (IDA)

January 5, 216 BANGLADESH STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Markus Rodlauer and Catherine Anne Maria Pattillo (IMF) and Satu Kahkonen (IDA)

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE. Joint IMF/World Bank Debt Sustainability Analysis 2010

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the

JOINT IMF/WORLD BANK DEBT SUSTAINABILITY

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BENIN JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BENIN JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Public Disclosure Authorized Prepared by the staffs of

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BENIN JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Public Disclosure Authorized Prepared by the staffs of

REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

May 18, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA)

May 18, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA)

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

KYRGYZ REPUBLIC THIRD REVIEW UNDER THE THREE-YEAR ARRANGEMENT

December, 1 THIRD REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUEST FOR MODIFICATION OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Juha Kähkönen

December, 1 THIRD REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUEST FOR MODIFICATION OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Juha Kähkönen

January 2008 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

January 28 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Niger remains at moderate risk of debt distress. Despite low debt ratios following debt relief, most recently in 26 under the MDRI, Niger

January 28 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Niger remains at moderate risk of debt distress. Despite low debt ratios following debt relief, most recently in 26 under the MDRI, Niger

PAPUA NEW GUINEA STAFF REPORT FOR THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

October 8, 215 PAPUA NEW GUINEA STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Hoe Ee Khor and Steven Barnett (IMF) Satu Kahkonen (IDA) Prepared by the staffs

October 8, 215 PAPUA NEW GUINEA STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Hoe Ee Khor and Steven Barnett (IMF) Satu Kahkonen (IDA) Prepared by the staffs

REPUBLIC OF THE MARSHALL ISLANDS

REPUBLIC OF THE MARSHALL ISLANDS December 19, 213 STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Stephan Danninger, Ranil Salgado, Jeffrey D. Lewis and Sudhir

REPUBLIC OF THE MARSHALL ISLANDS December 19, 213 STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Stephan Danninger, Ranil Salgado, Jeffrey D. Lewis and Sudhir

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 9, 218 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Markus Rodlauer and Johannes Wiegand (IMF), and John Panzer (IDA) Prepared by Staffs of the International

February 9, 218 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Markus Rodlauer and Johannes Wiegand (IMF), and John Panzer (IDA) Prepared by Staffs of the International

CENTRAL AFRICAN REPUBLIC

CENTRAL AFRICAN REPUBLIC June 29, 217 SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, FINANCING ASSURANCES REVIEW, AND REQUEST FOR AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS 6 Approved

CENTRAL AFRICAN REPUBLIC June 29, 217 SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, FINANCING ASSURANCES REVIEW, AND REQUEST FOR AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS 6 Approved

STAFF REPORT FOR THE 2014 ARTICLE IV CONSULTATION AND SECOND REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS

November 19, 214 RWANDA STAFF REPORT FOR THE 214 ARTICLE IV CONSULTATION AND SECOND REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Dan Ghura (IMF) and

November 19, 214 RWANDA STAFF REPORT FOR THE 214 ARTICLE IV CONSULTATION AND SECOND REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Dan Ghura (IMF) and

Risk of external debt distress:

November 1, 17 SEVENTH AND EIGHTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS Risk of external debt

November 1, 17 SEVENTH AND EIGHTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS Risk of external debt

Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2

May 2006 Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2 While Nicaragua s debt burden has been substantially reduced thanks to the HIPC initiative, debt levels remain elevated and subject

May 2006 Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2 While Nicaragua s debt burden has been substantially reduced thanks to the HIPC initiative, debt levels remain elevated and subject

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND ISLAMIC REPUBLIC OF MAURITANIA

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND ISLAMIC REPUBLIC

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND ISLAMIC REPUBLIC

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND MALI. Joint Bank-Fund Debt Sustainability Analysis Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND MALI Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND MALI Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL. Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

SIERRA LEONE. Approved By. June 16, 2016

SIERRA LEONE June 16, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION AND FIFTH REVIEW UNDER THE EXTENDED CREDIT FACILITY AND FINANCING ASSURANCES REVIEW AND REQUEST FOR AN EXTENSION OF THE EXTENDED

SIERRA LEONE June 16, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION AND FIFTH REVIEW UNDER THE EXTENDED CREDIT FACILITY AND FINANCING ASSURANCES REVIEW AND REQUEST FOR AN EXTENSION OF THE EXTENDED

Joint Bank-Fund Debt Sustainability Analysis Update

INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized INTERNATIONAL MONETARY FUND DOMINICA Joint Bank-Fund Debt Sustainability Analysis -218 Update Prepared by the staffs of the International

INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized INTERNATIONAL MONETARY FUND DOMINICA Joint Bank-Fund Debt Sustainability Analysis -218 Update Prepared by the staffs of the International

INTERNATIONAL MONETARY FUND ST. LUCIA. External and Public Debt Sustainability Analysis. Prepared by the Staff of the International Monetary Fund

INTERNATIONAL MONETARY FUND ST. LUCIA External and Public Debt Sustainability Analysis Prepared by the Staff of the International Monetary Fund December 23, 21 This debt sustainability analysis (DSA) assesses

INTERNATIONAL MONETARY FUND ST. LUCIA External and Public Debt Sustainability Analysis Prepared by the Staff of the International Monetary Fund December 23, 21 This debt sustainability analysis (DSA) assesses

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION DEMOCRATIC REPUBLIC OF CONGO

71 INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION DEMOCRATIC REPUBLIC OF CONGO Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the Staffs of the International Monetary

71 INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION DEMOCRATIC REPUBLIC OF CONGO Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the Staffs of the International Monetary

Risk of external debt distress: Augmented by significant risks stemming from domestic public debt?

July 5, 217 SEVENTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR EXTENSION AND AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum

July 5, 217 SEVENTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR EXTENSION AND AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum

Uganda: Joint Bank-Fund Debt Sustainability Analysis

February 26 Uganda: Joint Bank-Fund Debt Sustainability Analysis 1. Uganda s risk of debt distress is moderate. Its net present value (NPV) of debt-toexports ratio stands at 179 percent in 24/5, or below

February 26 Uganda: Joint Bank-Fund Debt Sustainability Analysis 1. Uganda s risk of debt distress is moderate. Its net present value (NPV) of debt-toexports ratio stands at 179 percent in 24/5, or below

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA August 27, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Elliott Harris (IMF) and Jeffrey

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA August 27, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Elliott Harris (IMF) and Jeffrey

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA. Joint Bank-Fund Debt Sustainability Analysis 1

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA

Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA Joint Bank-Fund Debt Sustainability Analysis for 212 Under the Debt Sustainability

Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA Joint Bank-Fund Debt Sustainability Analysis for 212 Under the Debt Sustainability

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LIBERIA

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LIBERIA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis 1 Update 1 Prepared by the

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LIBERIA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis 1 Update 1 Prepared by the

LIBERIA. Approved By. December 3, December 7, Prepared by the International Monetary Fund and International Development Association

December 3, 15 December 7, 15 FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT AND REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, MODIFICATION OF PERFORMANCE CRITERIA, AND REPHASING

December 3, 15 December 7, 15 FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT AND REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, MODIFICATION OF PERFORMANCE CRITERIA, AND REPHASING

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC Joint Bank/Fund Debt Sustainability Analysis 28 1 Prepared by the staffs of the International Development

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC Joint Bank/Fund Debt Sustainability Analysis 28 1 Prepared by the staffs of the International Development

March 2007 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1

1 November 2006 Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1 Public sector debt sustainability Since the time of the last joint DSA, the most important new signal on the likely direction of

1 November 2006 Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1 Public sector debt sustainability Since the time of the last joint DSA, the most important new signal on the likely direction of

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION

November 21, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION AND FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND FINANCING ASSURANCES REVIEW DEBT SUSTAINABILITY ANALYSIS Approved

November 21, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION AND FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND FINANCING ASSURANCES REVIEW DEBT SUSTAINABILITY ANALYSIS Approved

TOGO. Joint Bank-Fund Debt Sustainability Analysis Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND TOGO Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND TOGO Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

CÔTE D'IVOIRE ANALYSIS UPDATE. June 2, Prepared by the International Monetary Fund and the International Development Association

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1

June 8, 2016 STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Paul Cashin and Andrea Richter Hume (IMF) and Satu Kahkonen (IDA) Prepared by International Monetary

June 8, 2016 STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Paul Cashin and Andrea Richter Hume (IMF) and Satu Kahkonen (IDA) Prepared by International Monetary

Georgia: Joint Bank-Fund Debt Sustainability Analysis 1

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA Joint IMF/World Bank Debt Sustainability Analysis Under the Debt Sustainability Framework for Low-Income Countries

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA Joint IMF/World Bank Debt Sustainability Analysis Under the Debt Sustainability Framework for Low-Income Countries

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO. Joint Bank-Fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND UGANDA. Joint World Bank/IMF Debt Sustainability Analysis Update

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND UGANDA Joint World Bank/IMF Debt Sustainability Analysis Update Prepared by staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND UGANDA Joint World Bank/IMF Debt Sustainability Analysis Update Prepared by staffs of the International Development Association and

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

August 29, 213 THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS Approved By Michael Atingi-Ego and Elliott Harris (IMF) and Jeffrey

August 29, 213 THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS Approved By Michael Atingi-Ego and Elliott Harris (IMF) and Jeffrey

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI. Joint Bank Fund Debt Sustainability Analysis Update

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI Joint Bank

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI Joint Bank

DEMOCRATIC REPUBLIC OF TIMOR-LESTE

DEMOCRATIC REPUBLIC OF TIMOR-LESTE January 13, 212 STAFF REPORT FOR THE 211 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Ray Brooks and Dhaneshwar Ghura (IMF) Prepared By 1 International

DEMOCRATIC REPUBLIC OF TIMOR-LESTE January 13, 212 STAFF REPORT FOR THE 211 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Ray Brooks and Dhaneshwar Ghura (IMF) Prepared By 1 International

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN. Joint World Bank/IMF 2009 Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN Joint World Bank/IMF 29 Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN Joint World Bank/IMF 29 Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATION MONETARY FUND SOLOMON ISLANDS. Joint World bank-fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATION MONETARY FUND SOLOMON ISLANDS Public Disclosure Authorized Joint World bank-fund Debt Sustainability Analysis 213 Update Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATION MONETARY FUND SOLOMON ISLANDS Public Disclosure Authorized Joint World bank-fund Debt Sustainability Analysis 213 Update Prepared

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL. Joint Bank/Fund Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL Joint Bank/Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL Joint Bank/Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

STAFF REPORT OF THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE. Risk of external debt distress

April 7, 215 STAFF REPORT OF THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Paul Cashin and Mark Flanagan (IMF) Satu Kahkonen (IDA) Risk of external debt distress Prepared

April 7, 215 STAFF REPORT OF THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Paul Cashin and Mark Flanagan (IMF) Satu Kahkonen (IDA) Risk of external debt distress Prepared

STAFF REPORT FOR THE 2018 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 1, 218 BANGLADESH STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Kenneth Kang and Kevin Fletcher (IMF) and John Panzer (IDA) Prepared by International Monetary

May 1, 218 BANGLADESH STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Kenneth Kang and Kevin Fletcher (IMF) and John Panzer (IDA) Prepared by International Monetary

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA. Joint IMF/World Bank Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

STAFF REPORT FOR THE 2018 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS. Risk of external debt distress:

May 24, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Risk of external debt distress: Augmented by significant risks stemming from domestic public and/or private external

May 24, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Risk of external debt distress: Augmented by significant risks stemming from domestic public and/or private external

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL. Joint IMF/IDA Debt Sustainability Analysis

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERANTIONAL MONETARY FUND BURKINA FASO. Joint Bank-Fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERANTIONAL MONETARY FUND BURKINA FASO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERANTIONAL MONETARY FUND BURKINA FASO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

December 19, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Odd Per Brekk (IMF) and John Panzer (IDA) Prepared by the staff of the International Monetary

December 19, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Odd Per Brekk (IMF) and John Panzer (IDA) Prepared by the staff of the International Monetary

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND THE GAMBIA. Joint Bank-Fund Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND THE GAMBIA Joint Bank-Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND THE GAMBIA Joint Bank-Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

Joint Bank-Fund Debt Sustainability Analysis 2018 Update 1

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND DEMOCRATIC REPUBLIC OF SÃO TOMÉ AND PRÍNCIPE Public Disclosure Authorized Public Disclosure Authorized Public

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND DEMOCRATIC REPUBLIC OF SÃO TOMÉ AND PRÍNCIPE Public Disclosure Authorized Public Disclosure Authorized Public

REQUEST FOR A THREE-YEAR POLICY SUPPORT

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BURUNDI. Joint Bank/Fund Debt Sustainability Analysis 2010

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BURUNDI Joint Bank/Fund

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BURUNDI Joint Bank/Fund

FEDERATED STATES OF MICRONESIA

FEDERATED STATES OF MICRONESIA August 4, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Alison Stuart and Zuzana Murgasova (IMF), and John Panzer (IDA) Prepared

FEDERATED STATES OF MICRONESIA August 4, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Alison Stuart and Zuzana Murgasova (IMF), and John Panzer (IDA) Prepared

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA. Joint IMF/World Bank Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the World Bank Approved

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the World Bank Approved

Approved By. November 13, Prepared by the Staffs of the International Monetary Fund and the World Bank.

November 13, 215 NIGER SIXTH AND SEVENTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUEST FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, REQUEST FOR AUGMENTATION OF ACCESS, AND EXTENSION

November 13, 215 NIGER SIXTH AND SEVENTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUEST FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, REQUEST FOR AUGMENTATION OF ACCESS, AND EXTENSION

MALAWI. Approved By. December 27, Prepared by the staffs of the International Monetary Fund and the International Development Association

December 27, 213 MALAWI THIRD AND FOURTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVER OF PERFORMANCE CRITERIA, EXTENSION OF THE ARRANGEMENT, REPHASING OF DISBURSEMENTS, AND

December 27, 213 MALAWI THIRD AND FOURTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVER OF PERFORMANCE CRITERIA, EXTENSION OF THE ARRANGEMENT, REPHASING OF DISBURSEMENTS, AND

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA. Joint Bank-Fund Debt Sustainability Analysis - Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis - Update Prepared by the Staff

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis - Update Prepared by the Staff

KINGDOM OF LESOTHO SIXTH REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

August 2, 213 KINGDOM OF LESOTHO SIXTH REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde- Wolf and Chris Lane (IMF) Marcelo

August 2, 213 KINGDOM OF LESOTHO SIXTH REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde- Wolf and Chris Lane (IMF) Marcelo

LAO PEOPLE'S DEMOCRATIC REPUBLIC

LAO PEOPLE'S DEMOCRATIC REPUBLIC August 16, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS 1 Approved By David Cowen and Masato Miyazaki (IMF) Andrew D. Mason and Jeffrey

LAO PEOPLE'S DEMOCRATIC REPUBLIC August 16, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS 1 Approved By David Cowen and Masato Miyazaki (IMF) Andrew D. Mason and Jeffrey

Burkina Faso: Joint Bank-Fund Debt Sustainability Analysis

September 2005 Burkina Faso: Joint Bank-Fund Debt Sustainability Analysis 1. This document assesses the sustainability of Burkina Faso s external public debt using the Debt Sustainability Analysis (DSA)

September 2005 Burkina Faso: Joint Bank-Fund Debt Sustainability Analysis 1. This document assesses the sustainability of Burkina Faso s external public debt using the Debt Sustainability Analysis (DSA)

LAO PEOPLE'S DEMOCRATIC REPUBLIC

December 15, 2014 LAO PEOPLE'S DEMOCRATIC REPUBLIC STAFF REPORT FOR THE 2014 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer and Chris Lane (IMF) Satu Kahkonen (World

December 15, 2014 LAO PEOPLE'S DEMOCRATIC REPUBLIC STAFF REPORT FOR THE 2014 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer and Chris Lane (IMF) Satu Kahkonen (World

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Fund-Bank Debt Sustainability Analysis under the Debt Sustainability Framework for Low-Income Countries Prepared by the staffs

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Fund-Bank Debt Sustainability Analysis under the Debt Sustainability Framework for Low-Income Countries Prepared by the staffs

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND UNION OF THE COMOROS. Joint IMF/World Bank Debt Sustainability Analysis 2009

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND UNION OF THE COMOROS Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND UNION OF THE COMOROS Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the staffs of the International Development Association

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 12, 217 BANGLADESH STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Peter Allum (IMF) and John Panzer (IDA) Prepared by International Monetary Fund International

May 12, 217 BANGLADESH STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Peter Allum (IMF) and John Panzer (IDA) Prepared by International Monetary Fund International

DOCUMENT OF INTERNATIONAL MONETARY FUND AND FOR OFFICIAL USE ONLY. SM/07/347 Supplement 2

DOCUMENT OF INTERNATIONAL MONETARY FUND AND FOR OFFICIAL USE ONLY FOR AGENDA SM/7/347 Supplement 2 November 5, 27 To: From: Subject: Members of the Executive Board The Secretary Myanmar Staff Report for

DOCUMENT OF INTERNATIONAL MONETARY FUND AND FOR OFFICIAL USE ONLY FOR AGENDA SM/7/347 Supplement 2 November 5, 27 To: From: Subject: Members of the Executive Board The Secretary Myanmar Staff Report for

The Gambia: Joint Bank-Fund Debt Sustainability Analysis

1 December 26 The Gambia: Joint Bank-Fund Debt Sustainability Analysis 1. This debt sustainability analysis (DSA), prepared jointly by the staffs of the International Monetary Fund and the World Bank,

1 December 26 The Gambia: Joint Bank-Fund Debt Sustainability Analysis 1. This debt sustainability analysis (DSA), prepared jointly by the staffs of the International Monetary Fund and the World Bank,

INTERNATIONAL MONETARY FUND SOLOMON ISLANDS. Joint IMF/World Bank Debt Sustainability Analysis 1

INTERNATIONAL MONETARY FUND SOLOMON ISLANDS Joint IMF/World Bank Debt Sustainability Analysis 1 Prepared by Staffs of the International Monetary Fund and World Bank Approved by Hoe Ee Khor and Masato Miyazaki

INTERNATIONAL MONETARY FUND SOLOMON ISLANDS Joint IMF/World Bank Debt Sustainability Analysis 1 Prepared by Staffs of the International Monetary Fund and World Bank Approved by Hoe Ee Khor and Masato Miyazaki

INTERNATIONAL MONETARY FUND DOMINICA. Debt Sustainability Analysis. Prepared by the staff of the International Monetary Fund

INTERNATIONAL MONETARY FUND DOMINICA Debt Sustainability Analysis Prepared by the staff of the International Monetary Fund In consultation with World Bank Staff July 2, 27 This debt sustainability analysis

INTERNATIONAL MONETARY FUND DOMINICA Debt Sustainability Analysis Prepared by the staff of the International Monetary Fund In consultation with World Bank Staff July 2, 27 This debt sustainability analysis

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

LAO PEOPLE'S DEMOCRATIC REPUBLIC

LAO PEOPLE'S DEMOCRATIC REPUBLIC January 6, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer (IMF) John Panzer (IDA) Prepared By International

LAO PEOPLE'S DEMOCRATIC REPUBLIC January 6, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer (IMF) John Panzer (IDA) Prepared By International

International Monetary Fund Washington, D.C.

2006 International Monetary Fund December 2006 IMF Country Report No. 06/442 Honduras: Debt Sustainability Analysis 2006 This Debt Sustainability Analysis paper for Honduras was prepared jointly by a staff

2006 International Monetary Fund December 2006 IMF Country Report No. 06/442 Honduras: Debt Sustainability Analysis 2006 This Debt Sustainability Analysis paper for Honduras was prepared jointly by a staff

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA. Joint World Bank/IMF Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint World Bank/IMF Debt Sustainability Analysis Prepared by staffs of the International Development Association and International

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint World Bank/IMF Debt Sustainability Analysis Prepared by staffs of the International Development Association and International

May 2006 SIERRA LEONE: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

May 2006 SIERRA LEONE: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS This document assesses the sustainability of Sierra Leone s external and domestic public debt. The debt sustainability analysis (DSA)

May 2006 SIERRA LEONE: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS This document assesses the sustainability of Sierra Leone s external and domestic public debt. The debt sustainability analysis (DSA)

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CAMEROON Joint Bank-Fund Debt Sustainability Analysis 218 Update Public Disclosure Authorized Public Disclosure

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CAMEROON Joint Bank-Fund Debt Sustainability Analysis 218 Update Public Disclosure Authorized Public Disclosure

CAMEROON. Approved By. Prepared by the staffs of the International Monetary Fund and the International Development Association.

June 22, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION, SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA AND MODIFICATION

June 22, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION, SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA AND MODIFICATION

CÔTE D'IVOIRE. Approved By. November 23, Prepared by the International Monetary Fund and the International Development Association

CÔTE D'IVOIRE November 23, 216 REQUESTS FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Roger

CÔTE D'IVOIRE November 23, 216 REQUESTS FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Roger

REPUBLIC OF MADAGASCAR

June 14, 217 REPUBLIC OF MADAGASCAR STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION, FIRST REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUESTS FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE

June 14, 217 REPUBLIC OF MADAGASCAR STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION, FIRST REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUESTS FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE