BUSINESS STUDIES REVISION GUIDE

|

|

|

- Edward Welch

- 5 years ago

- Views:

Transcription

1 BUSINESS STUDIES REVISION GUIDE Answer booklet Name: 1

2 Contents This answer booklet is designed to help you mark your own work. Don t use it to cheat! That would be silly and ultimately pointless because you will learn nothing! 2

3 Contents Topic 1: Financial Documents used in a transaction Page 4 Topic 2: Computerised Accounting Systems Page 13 Topic 3: Business Costs Page 16 Topic 4: Payment Methods Page 20 Topic 5: Understanding Profit and Loss Accounts Page 26 Topic 6: Understanding Balance Sheets Page 35 3

4 Topic 7: Solvency Ratios Page 40 Topic 8: Profitability Ratios Page 46 Topic 9: Importance of Financial Documents to Stakeholders Page 52 4

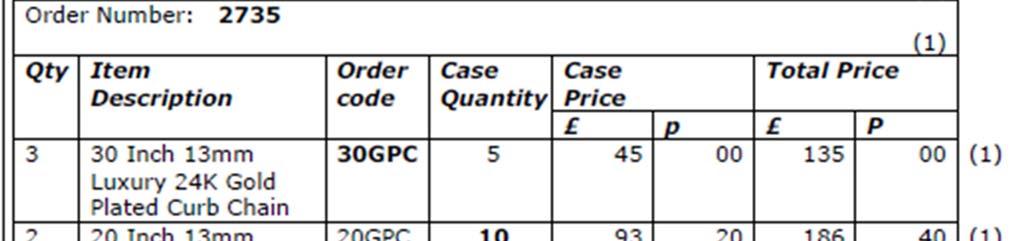

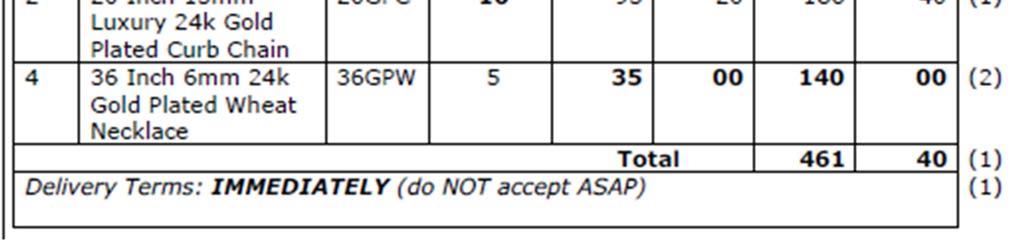

5 1) Financial Documents C Good Received Note Order Form Receipt Credit note Statement Sales Invoice Delivery Note Remittance Advice Slip Cheque 5

6 6

7 Leather Belts Silky Scarves Pairs of gloves SSM 342 SWL 517 DE 87 Today This mistake could lead to Trendy having inaccurate records of stock which in turn could mean the business accepts an order that they cannot fulfil. This will leave the customer dissatisfied and unlikely to order again. 7

8 8

9 24 th May nd June % Problem 1: The wrong amount could be paid which would lead to inaccurate records and potentially lost money. Problem 2: Customers are likely to avoid using the company again in the future as they would perceive the business as being unreliable. 9

10 10

11 11

12 12

13 Purchase Order Invoice Cheque 13

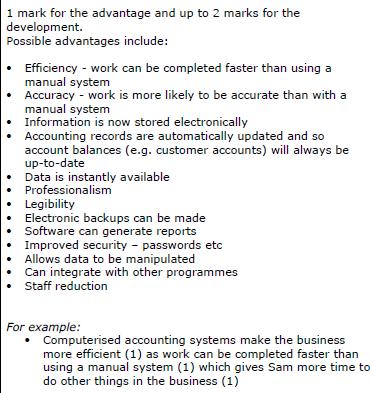

14 2) Computerised Accounting Systems Billy-Bob Brannan has been told by his friend Jimmy-John Jingle that he would benefit from introducing a computerised accounting system to help him complete his financial documents. Billy-Bob isn t sure what a computerised accounting system is or what it does. Help Billy-Bob out by explaining what a computerised accounting system is and how it might help him with his business selling Banjo s. A Computerised accounting system is an automated system used to create financial documents and manage business accounts. Billy Bob would benefit from using a computerised accounting system as it would reduce the amount of human input needed in creating the documents and organising the company s account. This saves both time and money that can be used elsewhere. 14

15 Billy-Bob likes the sound of introducing a computerised accounting system but just as he was looking to invest, Jimmy-John explains that a computerised accounting system could potentially lead to a drop in profits. Billy-Bob is confused again. Help him out again by explaining why a computerised accounting system could lead to a drop in profits Computerised accounting systems are not always guaranteed to be a success. Computerised accounting systems are very expensive to install and maintain. If Billy Bob doesn t get regular orders he might struggle to afford the new system. There are also costs if the system goes wrong which could be so expensive that Billy Bob cannot afford to maintain the system. If Billy Bob s costs increase then this will reduce the amount of profit his business is making. 15

16 16

17 17

18 3) Business Costs State two examples of running costs and explain how you know they are running costs Suitable 1)... running costs can include:... Utility... Bills... Staff Wages... Rent... Equipment... Maintenance Stock... purchases / Supplier deliverys These are all running costs because they are ongoing payments that are made on a consistent basis. 2) Running or start-up? Cost Start-up cost Running cost Rent Computer equipment Utility bills Staff wages New factory building Equipment Maintenance Initial advertising Annual staff training Delivery Vehicle 18

19 Macy is the owner of Grandio Supermarkets. She has been told that she can reduce costs by using ICT. She has money to invest but is unsure of what to buy. Advise Macy on what she could buy and explain how this will benefit the company. Macy could invest in: Computerised accounting systems to speed up the process of creating financial documents This would mean time and money would be saved to be used in other areas of the business. Barcode scanners This would allow Macy to keep a close check on stock as it is all done automatically. This again saves time rather than having to count all stock manually. It could also save the cost of paying people to do stock checks. 19

20 20

21 21

22 4) Payment Methods Create your own payment methods cheat sheet 22

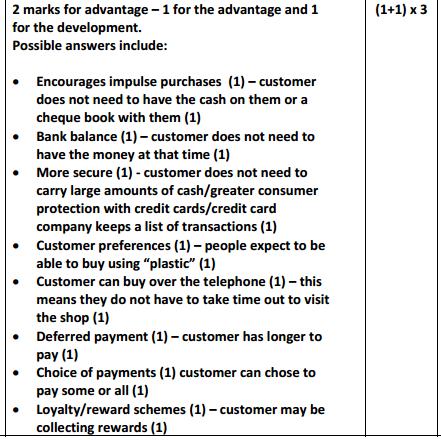

23 Practice MOP questions Explain one advantage and one disadvantage to Sharpe s world of knives of allowing customers to pay using cash. (4) Advantage Advantages can include: Quick cash received immediately and can then be re spent in other areas of the business No need for expensive machinery (chip and pin) No processing fees Disadvantages can include: Disadvantage Could result in human error counting it all up Is not very secure having lots of cash on the premises, plus it has to be transported to the bank. The wonderful world of Wilson have recently conducted some market research and found that most of their customers prefer to pay by debit card rather than cash. Explain why some customers may prefer debit cards rather than cash (3) Reasons could include: Do not have to carry lots of cash; this could be insecure or lost. Debit cards are also useful to use online. Outline one advantage to customers of allowing them to pay by cheque when purchasing sports cars from Carr s cars. (2) The customer would get to keep the money in their account for another three days. Purchasing a car is likely to be expensive and involve a lot of money. Paying by cheque is much more secure than carrying large volumes of cash. Outline one disadvantage to Cooper s clothes of allowing customers to pay by credit card. (2) Coopers Clothes would have to pay commission each time they process a card payment. This will _ reduce their profits. 23

24 Outline one advantage to Richard s Reem Refrigerators of allowing their customers to pay by debit card (2) This could increase customers as debit cards are a preferred payment method for a lot of customers. Customers feel more secure in making payments rather than having to carry large amounts of cash. Transfer of cash is relatively quick 24

25 25

26 26

27 27

28 5) Profit & Loss Accounts Profit and Loss account activities Fill in the blanks to show the order of a profit and loss account: Sales Cost of Sales Gross Profit Other Expenses Net Profit Complete the following profit and loss account: Sales 35,000 Cost of Sales 12,000 Gross Profit 23,000 Other Expenses 6,000 Net Profit 17,000 28

29 Katy has asked you to help her construct a profit and loss account using the figures below Sales Revenue 50,000 Electricity - 2,000 Phone Bill - 1,000 Rent - 12,000 Cost of sales 21,000 50,000 Cost of Sales 21,000 29,000 Electricity Phone Bill Rent 2,000 1,000 12,000 15,000 Net Profit 14,000 29

30 Will is a farmer who sells cow s milk to supermarkets and vegetables in his farm shop. He needs help constructing a profit and loss account for He has provided the following figures: Sales of milk - 138,000 Electricity - 23,000 Revenue from farm shop 24,000 Both income so add them both together to work out total sales Rent - 12,000 Equipment - 15,000 Cost of sales 81, ,000 Cost of Sales 81,000 81,000 Electricity Equipment 23,000 15,000 Rent 12,000 50,000 Net Profit 31,000 30

31 If Will the farmer wanted to increase his Net Profit what would you recommend he does? Will could try and increase his Net Profit by: Making more sales Increases the price of his products and hope that customers still buy them Reduce his costs 31

32 Issac creates wooden garden furniture and sells them on his online store; He has asked for your help creating a profit and loss account for the previous 6 months: Here are his figures: (This one is tough take your time) Online Sales - 86,000 Raw materials - 37,000 Rent - 12,000 Website maintenance - 4,000 Cost of sales are the costs directly associated with creating the product. Raw materials are therefore the cost of sales Equipment - 25,000 Petrol - 1,500 86,000 Cost of Sales 37,000 49,000 Equipment Website Maintenance Rent 25,000 4,000 12,000 Petrol 1,500 42,500 Net Profit 6,500 32

33 33 A business

34 34

35 Complete the profit and loss account for The Kimberley Hotel for year ending

36 Final challenge! Create a profit and loss account using the figures below: Online Sales - 186,000 In Store Sales 195,000 Rent - 87,000 Equipment - 55,000 Utility Bills - 11,500 Wages - 169,000 Cost of Sales - 81,000 Total Sales 381,000 Cost Of Sales 81,000 Gross Profit 300,000 Other Expenses Rent 87,000 Equipment 55,000 Utility Bills 11,500 Wages 169,000 Total Expenses 322,500 Net Profit ( 22,500) Remember minus numbers are written in brackets! 36

37 6) Balance Sheets Business belongings that are expected to be kept for over 12 months Business belongings that are expected to be kept for under 12 months Debts that the business has to pay People who you owe money to They have given you credit People who owe you money They in debt to you 37

38 Look at the information below and in the end column decide if the item is an asset or liability: Item Amount Asset or liability? Cash in the till 565 Asset Suppliers awaiting payment 1,000 Liability Delivery van 5,000 Asset Money in the bank 8,000 Asset Stock 6,500 Asset Warehouse building 120,000 Asset Utility Bill 6,000 Liability What is the total value of current assets for this business? , ,500 = 15,065 What is the value of current liabilities for this business? 1, ,000 = 7,000 What is the working capital for this business? Current assets Current Liabilities 15,065-7,000 = 8,065 Work out the following for Ice Snax LTD 38

39 , = 2, = 900 2, = 1,200 Cash in the bank Cash in the till Stock in the store room Business Van Shelving in the shop Tools used by the business Office Furniture Customers who owe the business money Overdraft to be paid Advertising bill to be paid Bank Loan Mortgage Business Rates Tax to be paid 39

40 Complete the shaded cells in the following balance sheet: (Use your notes if you need to) Balance sheet for Harriet s Hardware Store Fixed Assets Property 220,000 Equipment 40, ,000 Current Assets Stock 35,000 Cash in the bank 8,000 43,000 Current Liabilities Utility Bills 7,000 Supplier Bill 24,000 Working Capital 12,000 Net Total Assets 272,000 Financed by: Capital 200,000 Profit 72, ,000 40

41 CJG Photography offer photo shoots as well as selling camera equipment and accessories in their store. This one is tough because it s easy to mistake this for camera equipment they are selling. However if they are selling the object it is normally labelled stock. Therefore this would have said stock of camera equipment Working Capital 41

Net Total Assets 125,000 Financed by: Capital 112,000 Profit 13,000 125,000 (1) (1)")

42 Complete the shaded boxes to help Sarena complete her balance sheet Balance sheet for Sarena s Sugary Snacks 2013 Fixed Assets Property 120,000 Vehicle 8, ,000 (1) Current Assets Stock 15,000 Cash in the bank 3,000 18,000 Current Liabilities Utility Bills 7,000 Supplier Bill 14,000 Working Capital ( 3000) Net Total Assets 125,000 Financed by: Capital 112,000 Profit 13, ,000 (1) (1) 42

43 7) Solvency Ratios Use the following information to calculate the current and acid test ratios: Current assets 12,000 Current liabilities 14,000 Stock 2,000 The Current Ratio: Current assets Current Liabilities What does this show? 12,000 14,000 = 0.8;1 This shows that the business has a below ideal value and may struggle to pay back debts as they do not have enough assets to pay for their liabilities. The Acid Test Ratio: Current assets - Stock Current Liabilities 12,000-2,000 14,000 = 0.7;1 What does this show? This further confirms that this business would struggle to pay back debts as they do not have the assets to pay for their liabilities. Is this business solvent? No, this business is not solvent as it does not have ideal values for the current ratio or the acid test ratio. 43

44 Current assets 18,000 Current liabilities 10,000 Stock 4,000 Have another go: The Current Ratio: Current assets Current Liabilities 18,000 10,000 = 1.8;1 What does this show? This shows that the business has 1.8 worth of assets to every liability. This is a positive figure and shows they are able to pay back their debt. The Acid Test Ratio: Current assets - Stock Current Liabilities 18,000-4,000 10,000 = 1.4;1 What does this show? This shows the business has enough assets to pay back debts regardless of how much of its stock it sells. This acid test ratio is an ideal value. 44

45 Is this business solvent? Yes this business is solvent as both values are within the ideal value range. It shows they have enough assets to pay off their liabilities. It also shows they would be able to pay off their liabilities even if they were unable to sell their stock. Ok one more: The Current Ratio: Current assets Current Liabilities 75,000 60,000 = 1..25;1 What does this show? This shows that the business does have more current assets than liabilities but it is just short of the ideal value. The business might struggle to pay off debts The Acid Test Ratio: Current assets - Stock Current Liabilities 75,000-20,000 60,000 = 0.9;1 What does this show? This shows the business would not be able to pay debts if they were unable to sell all of their stock. They would only have 0.9 worth of assets to every 1 debt. This would mean they are unable to pay. Is this business solvent? The business does not have ideal values for either ratio and therefore would not be considered to be a solvent business. They need to sell more stock and turn this in to cash which would in turn increase their current assets. They would then be able to be considered solvent. 45

46 If a business has a current ratio of 2.3 what does this mean? It means the business has 2.3 worth of assets to every 1 debt. This is positive because it means they have enough current assets to pay current liabilities. However, it is slightly above the ideal range. This might mean they have current assets that are not be fully utilised. This could be unsold stock or money in the bank that isn t being used. They should consider using these assets in order to generate more income for the business. David is concerned as his Acid-Test ratio is under the ideal value. He is unsure of how to improve the ratio. Advise David on how this can be done. David would need to increase his acid test ratio by increasing his current assets or by decreasing his current liabilities. David needs to be aware that stock will not count towards current assets in the acid test ratio and therefore producing more stock will not correct the problem. David needs to turn sell his current stock and turn this in to profit that be used to pay off liabilities or be re-invested. 46

47 Jenny is considering expanding her business but is unsure if she can afford to do so. Using the solvency ratios advise Jenny on is expand 47

48 Mohammed is unsure of what his businesses ratios actually mean. He asked his finance department to calculate the ratios and send them to you. Explain to Mohammed what the ratios show about the solvency of his business. (6) 48

49 8) Profitability Ratios Ok your turn: Work out the profitability ratios for this company: Sales 100,000 Gross profit 75,000 Net profit 11,000 Capital 5,000 Remember to show your working and give your answer to two decimal places! Calculation Answer Gross Profit Margin 75, ,000 x100 75% Net Profit Margin 11, ,000 x100 11% Return on Capital 11,000 5,000 x % Employed What does this show about the business? It shows us that the business is profitable. It is difficult to compare it s performance as we cannot see previous year s figures but we can see that the business is making money. It is also clear that the owner has made a good return on the original investment he has put in to the company. 49

50 Ok try this one: Blane the owner invested 45,000 to start the business. Work out the profitability ratios for both years 2012 Calculation Answer Gross Profit Margin 34,500 56,000 x % Net Profit Margin 22,000 56,000 x % Return on Capital Employed 22,000 45,000 x % 2013 Calculation Answer Gross Profit Margin 48,000 64,500 x % Net Profit Margin 25,450 64,500 x % Return on Capital Employed 25,450 45,000 x % Blane (the owner of the business) has asked you to explain to him what the profitability ratios show. The ratios show that Blane s business is making a profit in both 2012 and It has also shown sign of improvement from 2012 to 2013 as all percentages are higher. Sales are also higher from 2012 to 2013 so it shows that the business is selling more of its products. It does show that although Gross profit has increased sharply from 2012 to 2013 the net profit hasn t risen quite as much. This could mean cost of sales has decreased or Blane needs to look further at other expenses as Net Profit has increased in the same way as Gross Profit. It shows that Blane in 2013 has returned 56.55% of his original investment. Overall this is a healthy business that is making profit and showing signs of improvement. 50

51 51

52 The past two years Sam s accountant worked out that the businesses Gross Profit Margin. There were as follows: % 71% This year however Sam s account has said he can t be arsed and therefore Sam has asked Sales 175,000 Gross profit 136,000 Net profit 95,000 Capital 125,000 you to help out. Using the following figures work out the Gross Profit Margin for , ,000 X 100 = 77.71% (2) The business has shown an upward trend in the gross profit margin as it has climbed from 69% in 2009 to 71% in 2010 and 77.71% in This is a positive sign for the business and shows they are either making more sales or reducing the cost of sales. An increase in Gross Profit will also allow the business to cover the costs of their other expenses and increase their net profit. 52

53 If they are feeling particularly evil the examiners can test you on both ratios together in one question. Try this one: 53

54 54 Contiuned from previous question:

55 9) Importance of financial documents to stakeholders 55

56 Mark scheme continues on the next page 56

57 57

58 58

Name of Document PURCHASE ORDER DELIVERY NOTE. Shows a list of transactions and the amount owed at the end of the month The Customer

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

with the support of Everyday Banking An easy read guide March 2018

with the support of Everyday Banking An easy read guide March 2018 Who is this guide for? This guide has been designed to help anyone who might need more information about everyday banking. We will cover

with the support of Everyday Banking An easy read guide March 2018 Who is this guide for? This guide has been designed to help anyone who might need more information about everyday banking. We will cover

Revision Guide for Finance Exam

Revision Guide for Finance Exam Financial Documents Financial Document Purchase Order (what is to be ordered) Delivery Notes (sent with goods - check you have received the correct goods) Goods received

Revision Guide for Finance Exam Financial Documents Financial Document Purchase Order (what is to be ordered) Delivery Notes (sent with goods - check you have received the correct goods) Goods received

Economic and Management Sciences Grade 7 - Term 2. FINANCIAL LITERACY Topic 5: Accounting Concepts

1 Economic and Management Sciences Grade 7 - Term 2 FINANCIAL LITERACY Topic 5: Accounting Concepts There are certain basic accounting concepts that are used throughout the business world. It is important

1 Economic and Management Sciences Grade 7 - Term 2 FINANCIAL LITERACY Topic 5: Accounting Concepts There are certain basic accounting concepts that are used throughout the business world. It is important

The figures in the left (debit) column are all either ASSETS or EXPENSES.

column are all either ASSETS or EXPENSES.") Correction of Errors & Suspense Accounts. 2008 Question 7. Correction of Errors & Suspense Accounts is pretty much the only topic in Leaving Cert Accounting that requires some knowledge of how T Accounts

Correction of Errors & Suspense Accounts. 2008 Question 7. Correction of Errors & Suspense Accounts is pretty much the only topic in Leaving Cert Accounting that requires some knowledge of how T Accounts

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2009 MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. Accounting 2 DoE/Feb. March 2009 INSTRUCTIONS AND INFORMATION Read

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2009 MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. Accounting 2 DoE/Feb. March 2009 INSTRUCTIONS AND INFORMATION Read

Osborne Books sample material

2 AS Accounting for AQA AS ACCOUNTING UNIT 1: Introduction to Financial Accounting ADDITIONAL QUESTIONS CHAPTERS 1-6: DOUBLE-ENTRY PROCEDURES; BUSINESS DOCUMENTS The questions in this section deal with

2 AS Accounting for AQA AS ACCOUNTING UNIT 1: Introduction to Financial Accounting ADDITIONAL QUESTIONS CHAPTERS 1-6: DOUBLE-ENTRY PROCEDURES; BUSINESS DOCUMENTS The questions in this section deal with

Accounting Fundamentals July 2012

Accounting Fundamentals July 2012 Suggested answers and examiner s comments Important notice When reading these suggested answers, please note that the answers are intended as an indication of what is

Accounting Fundamentals July 2012 Suggested answers and examiner s comments Important notice When reading these suggested answers, please note that the answers are intended as an indication of what is

TRADING, PROFIT & LOSS ACCOUNT (INCOME STATEMENT) FOR THE YEAR ENDED 31 AUGUST 20*7

FOR THE YEAR ENDED 31 AUGUST 20*7") GCSE Revision- Unit 2 Finance 1. What are the advantages and disadvantages of a large business using the following sources of finance: (5 marks) Retained profits: these are profits that the owners put

GCSE Revision- Unit 2 Finance 1. What are the advantages and disadvantages of a large business using the following sources of finance: (5 marks) Retained profits: these are profits that the owners put

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2012 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 1 Key Messages This question paper contained a mixture of multiple-choice, short-answer and structured

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 1 Key Messages This question paper contained a mixture of multiple-choice, short-answer and structured

Spending Money. Chapter 6

Spending Money Chapter 6 The Banking module is very useful in MYOB. Many businesses use the Banking module for all their financial transactions, without ever using the Sales or Purchases area. Businesses

Spending Money Chapter 6 The Banking module is very useful in MYOB. Many businesses use the Banking module for all their financial transactions, without ever using the Sales or Purchases area. Businesses

Cambridge International Examinations Cambridge International General Certificate of Secondary Education

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *7579080582* ACCOUNTING 0452/22 Paper 2 May/June 2018 1 hour 45 minutes Candidates answer on the

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *7579080582* ACCOUNTING 0452/22 Paper 2 May/June 2018 1 hour 45 minutes Candidates answer on the

How to calculate your taxable profits

Helpsheet 222 Tax year 6 April 2013 to 5 April 2014 How to calculate your taxable profits A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200 3310 the

Helpsheet 222 Tax year 6 April 2013 to 5 April 2014 How to calculate your taxable profits A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200 3310 the

Accounting Question Booklet. Examination information. Questions 1 to 4 Answer all questions Write your answers in this question booklet

South Australian Certificate of Education Accounting 2017 Question Booklet Questions 1 to 4 Answer all questions Write your answers in this question booklet Examination information Materials Question Booklet

South Australian Certificate of Education Accounting 2017 Question Booklet Questions 1 to 4 Answer all questions Write your answers in this question booklet Examination information Materials Question Booklet

15-16 Tax Workshop. for. By Julie Pocock MAAT

15-16 Tax Workshop for By Julie Pocock MAAT What are the deadlines for the 15-16 Tax Year? The 15-16 Tax Year begins on 6 th April 2015 and ends on 5 th April 2016. If you submit a paper tax return, HMRC

15-16 Tax Workshop for By Julie Pocock MAAT What are the deadlines for the 15-16 Tax Year? The 15-16 Tax Year begins on 6 th April 2015 and ends on 5 th April 2016. If you submit a paper tax return, HMRC

2016 ACCOUNTING ATTACH SACE REGISTRATION NUMBER LABEL TO THIS BOX

External Examination 2016 2016 ACCOUNTING FOR OFFICE USE ONLY SUPERVISOR CHECK ATTACH SACE REGISTRATION NUMBER LABEL TO THIS BOX RE-MARKED Tuesday 15 November: 1.30 pm Time: 2 hours Pages: 33 Questions:

External Examination 2016 2016 ACCOUNTING FOR OFFICE USE ONLY SUPERVISOR CHECK ATTACH SACE REGISTRATION NUMBER LABEL TO THIS BOX RE-MARKED Tuesday 15 November: 1.30 pm Time: 2 hours Pages: 33 Questions:

Adding & Subtracting Percents

Ch. 5 PERCENTS Percents can be defined in terms of a ratio or in terms of a fraction. Percent as a fraction a percent is a special fraction whose denominator is. Percent as a ratio a comparison between

Ch. 5 PERCENTS Percents can be defined in terms of a ratio or in terms of a fraction. Percent as a fraction a percent is a special fraction whose denominator is. Percent as a ratio a comparison between

Using a Credit Card. Name Date

Unit 4 Using a Credit Card Name Date Objective In this lesson, you will learn to explain and provide examples of the benefits and disadvantages of using a credit card. This lesson will also discuss the

Unit 4 Using a Credit Card Name Date Objective In this lesson, you will learn to explain and provide examples of the benefits and disadvantages of using a credit card. This lesson will also discuss the

ENGIE Prepayment. A Guide to your prepayment meter

ENGIE Prepayment A Guide to your prepayment meter 1 An introduction to prepayment Welcome to prepayment from all of us here at ENGIE. This guide is here to give you lots of information about prepayment

ENGIE Prepayment A Guide to your prepayment meter 1 An introduction to prepayment Welcome to prepayment from all of us here at ENGIE. This guide is here to give you lots of information about prepayment

A short simple integrated approach to bookkeeping.

A short simple integrated approach to bookkeeping. Electrical Shop You have decided to set up your Business, an Electrical Shop. You will now be self employed (this means working for your self) Decide

A short simple integrated approach to bookkeeping. Electrical Shop You have decided to set up your Business, an Electrical Shop. You will now be self employed (this means working for your self) Decide

Math 5.1: Mathematical process standards

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

E X A M I N A T I O N S C O U N C I L

C A R I B B E A N E X A M I N A T I O N S C O U N C I L CARIBBEAN SECONDARY EDUCATION CERTIFICATE EXAMINATION * Barcode Area * Front Page Bar Code FILL IN ALL THE INFORMATION REQUESTED CLEARLY IN CAPITAL

C A R I B B E A N E X A M I N A T I O N S C O U N C I L CARIBBEAN SECONDARY EDUCATION CERTIFICATE EXAMINATION * Barcode Area * Front Page Bar Code FILL IN ALL THE INFORMATION REQUESTED CLEARLY IN CAPITAL

Managing your money and paying your rent

Managing your money and paying your rent How to make the most of your Universal Credit payments This guide can help you Get the right bank account Draw up a budget Pay your rent Deal with rent arrears

Managing your money and paying your rent How to make the most of your Universal Credit payments This guide can help you Get the right bank account Draw up a budget Pay your rent Deal with rent arrears

Topic 5 Sources of Finance. N5 Business Management

Topic 5 Sources of Finance N5 Business Management 1 Learning Intentions / Success Criteria Learning Intentions Sources of finance Success Criteria By end of this topic you will be able to describe: sources

Topic 5 Sources of Finance N5 Business Management 1 Learning Intentions / Success Criteria Learning Intentions Sources of finance Success Criteria By end of this topic you will be able to describe: sources

1. Introduction Why Budget? The budgeted profit and loss Sales Other income Gross profit 7 3.

1. Introduction 3 2. Why Budget? 4 3. The budgeted profit and loss 6 3.1 Sales 6 3.2 Other income 6 3.3 Gross profit 7 3.4 Overheads 7 4. Budgeted cash flow 9 5. Interpreting your budgets 10 6. Monitoring

1. Introduction 3 2. Why Budget? 4 3. The budgeted profit and loss 6 3.1 Sales 6 3.2 Other income 6 3.3 Gross profit 7 3.4 Overheads 7 4. Budgeted cash flow 9 5. Interpreting your budgets 10 6. Monitoring

VAT guide for small businesses. VAT guide

VAT guide 1 Contents... What is VAT? Contents What is VAT? VAT or, Value Added Tax, is a tax that is charged on most goods and services that VAT registered businesses provide in the UK. Introduction to

VAT guide 1 Contents... What is VAT? Contents What is VAT? VAT or, Value Added Tax, is a tax that is charged on most goods and services that VAT registered businesses provide in the UK. Introduction to

Topic 2: Compare different types of payment card

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

Topic 2: Compare different types of payment card

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

VAT for small businesses

VAT for small businesses What is VAT? VAT, or Value Added Tax, is a tax that is charged on most goods and services that VAT registered businesses provide in the UK. Unlike other taxes, VAT is collected

VAT for small businesses What is VAT? VAT, or Value Added Tax, is a tax that is charged on most goods and services that VAT registered businesses provide in the UK. Unlike other taxes, VAT is collected

Accounting Fundamentals

Subject no. 50A Certificate in Offshore Finance and Administration Accounting Fundamentals July 2012 Tuesday morning 10 July 2012 Time allowed: 2 hours Do not open this examination paper until the presiding

Subject no. 50A Certificate in Offshore Finance and Administration Accounting Fundamentals July 2012 Tuesday morning 10 July 2012 Time allowed: 2 hours Do not open this examination paper until the presiding

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education

*2076080738* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/21 Paper 2 October/November 2012 Candidates answer on the Question

*2076080738* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/21 Paper 2 October/November 2012 Candidates answer on the Question

Unit 2 Finance for Business

Pupil Name: Learner name: Teacher name: Unit 2 Finance for Business External Assessment Unit introduction All businesses have to spend money before they can make a profit, and when they spend money, they

Pupil Name: Learner name: Teacher name: Unit 2 Finance for Business External Assessment Unit introduction All businesses have to spend money before they can make a profit, and when they spend money, they

Northeast Power. Sixty and. James P. Smith. Electric Bill /22/2003 $ 60.00

R esponsibly managing a checking account is simple once you get into the practice of accurately keeping track of all the money that is deposited and withdrawn. You just need to remember the most important

R esponsibly managing a checking account is simple once you get into the practice of accurately keeping track of all the money that is deposited and withdrawn. You just need to remember the most important

Level 2 Accounting, 2013

91176 911760 2SUPERVISOR S Level 2 Accounting, 2013 91176 Prepare financial information for an entity that operates accounting subsystems 9.30 am Friday 29 November 2013 Credits: Five Achievement Achievement

91176 911760 2SUPERVISOR S Level 2 Accounting, 2013 91176 Prepare financial information for an entity that operates accounting subsystems 9.30 am Friday 29 November 2013 Credits: Five Achievement Achievement

ACCOUNTING: PAPER II MARKING GUIDELINES

NATIONAL SENIOR CERTIFICATE EXAMINATION NOVEMBER 2016 ACCOUNTING: PAPER II MARKING GUIDELINES Time: 2 hours 100 marks These marking guidelines are prepared for use by examiners and sub-examiners, all of

NATIONAL SENIOR CERTIFICATE EXAMINATION NOVEMBER 2016 ACCOUNTING: PAPER II MARKING GUIDELINES Time: 2 hours 100 marks These marking guidelines are prepared for use by examiners and sub-examiners, all of

Making the Most of Your Money

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

SENIOR CERTIFICATE EXAMINATIONS

SENIOR CERTIFICATE EXAMINATIONS ACCOUNTING 2016 MARKS: 300 TIME: 3 hours This question paper consists of 21 pages and an answer book of 20 pages. Accounting 2 DBE/2016 INSTRUCTIONS AND INFORMATION Read

SENIOR CERTIFICATE EXAMINATIONS ACCOUNTING 2016 MARKS: 300 TIME: 3 hours This question paper consists of 21 pages and an answer book of 20 pages. Accounting 2 DBE/2016 INSTRUCTIONS AND INFORMATION Read

GRAAD 12 NATIONAL SENIOR CERTIFICATE GRADE 12

GRAAD 12 NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING NOVEMBER 2011 MARKS: 300 TIME: 3 hours This question paper consists of 19 pages and an 18-page answer book. Accounting 2 DBE/November 2011 INSTRUCTIONS

GRAAD 12 NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING NOVEMBER 2011 MARKS: 300 TIME: 3 hours This question paper consists of 19 pages and an 18-page answer book. Accounting 2 DBE/November 2011 INSTRUCTIONS

Loans: Banks or credit unions can loan you money. You pay the money back a little at a time. They charge you interest for the loan.

Basic Banking Services and Checking Accounts Intermediate MATERIALS What Can a Bank Do for You? Lesson 1: Introduction to Banking Services Worksheet 1-1 page 1 Beginner & Low- What Can a Bank Do for You?

Basic Banking Services and Checking Accounts Intermediate MATERIALS What Can a Bank Do for You? Lesson 1: Introduction to Banking Services Worksheet 1-1 page 1 Beginner & Low- What Can a Bank Do for You?

Welcome to this Contact a Family Webinar. If there is a technical hitch, please do bear with us

Welcome to this Contact a Family Webinar If there is a technical hitch, please do bear with us Those of you joining by pc, laptop, tablet or smart phone should now be able to see this introduction slide

Welcome to this Contact a Family Webinar If there is a technical hitch, please do bear with us Those of you joining by pc, laptop, tablet or smart phone should now be able to see this introduction slide

The Fundamental Finance Function

The Fundamental Finance Function Have you ever thought about starting your own business? If so, you ve probably considered the goods or services you ll sell, where you ll open your store, and how you ll

The Fundamental Finance Function Have you ever thought about starting your own business? If so, you ve probably considered the goods or services you ll sell, where you ll open your store, and how you ll

Expenses ACCOUNTING FEES EXPENSE ADVERTISING EXPENSE AUTOMOBILE EXPENSE

Expenses The majority of Consultants will be using the Quick Method of paying HST/GST, so expenses should be entered into the manual including HST/GST. If you are using the Long Method for remitting HST/GST,

Expenses The majority of Consultants will be using the Quick Method of paying HST/GST, so expenses should be entered into the manual including HST/GST. If you are using the Long Method for remitting HST/GST,

Continuing Cookie Chronicle

1 CCC1 Natalie Koebel spent much of her childhood learning the art of cookiemaking from her grandmother. They spent many happy hours mastering every type of cookie imaginable and later devised new recipes

1 CCC1 Natalie Koebel spent much of her childhood learning the art of cookiemaking from her grandmother. They spent many happy hours mastering every type of cookie imaginable and later devised new recipes

Credit sales = Payments from debtors + Debtors 31/12 Debtors 1/1. Cash sales = Total of cash payments + Cash 31/12 Cash 1/1 + Cash drawings

Incomplete Records (A) SALES. Credit sales = Payments from debtors + Debtors 31/12 Debtors 1/1 Cash sales = Total of cash payments + Cash 31/12 Cash 1/1 + Cash drawings PURCHASES. Credit purchases = Payments

Incomplete Records (A) SALES. Credit sales = Payments from debtors + Debtors 31/12 Debtors 1/1 Cash sales = Total of cash payments + Cash 31/12 Cash 1/1 + Cash drawings PURCHASES. Credit purchases = Payments

Name Form. AO1. Recall, select and communicate their knowledge and understanding of concepts, issues and terminology.

Name Form Skills to be developed and how you will be assessed throughout the course and in the exam AO1. Recall, select and communicate their knowledge and understanding of concepts, issues and terminology.

Name Form Skills to be developed and how you will be assessed throughout the course and in the exam AO1. Recall, select and communicate their knowledge and understanding of concepts, issues and terminology.

ACCOUNTING GRADE 12 SEPTEMBER 2015

Metro East Education District ACCOUNTING GRADE 12 SEPTEMBER 2015 MARKS: 300 TIME: 3 hours This question paper consists of 20 pages and an answer book of 19 pages. Accounting 2 MEED September 2015 INSTRUCTIONS

Metro East Education District ACCOUNTING GRADE 12 SEPTEMBER 2015 MARKS: 300 TIME: 3 hours This question paper consists of 20 pages and an answer book of 19 pages. Accounting 2 MEED September 2015 INSTRUCTIONS

TABLE OF CONTENTS. Introduction 3. General Guidelines for Successful Account Management 3. Managing Your Checking Account. 1.

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

About. Direct Payments

About Direct Payments March 2017 2 About Direct Payments 3 The purpose of this booklet is to offer advice and information to anyone receiving a direct payment or for people considering taking a direct

About Direct Payments March 2017 2 About Direct Payments 3 The purpose of this booklet is to offer advice and information to anyone receiving a direct payment or for people considering taking a direct

2018 DollarWise Summer Youth Contest Study Guide

2018 DollarWise Summer Youth Contest Study Guide The DollarWise Summer Youth Contest Final Exam questions are designed to test your full knowledge of the information provided in the contest. During the

2018 DollarWise Summer Youth Contest Study Guide The DollarWise Summer Youth Contest Final Exam questions are designed to test your full knowledge of the information provided in the contest. During the

A warrant of control will only help if the defendant (debtor) has:

has:") EX322 Warrant of control How do I ask for a warrant of control? What should I do? Read the leaflet called EX321 I have a judgment but the defendant hasn t paid What can I do?, which is available online

EX322 Warrant of control How do I ask for a warrant of control? What should I do? Read the leaflet called EX321 I have a judgment but the defendant hasn t paid What can I do?, which is available online

TO UNDERSTANDING ACCIDENT & CRITICAL ILLNESS INSURANCE

3 STEPS TO UNDERSTANDING ACCIDENT & CRITICAL ILLNESS INSURANCE What s Inside Step 1: What What are accident and critical illness insurance products? 4 Step 2: How How do accident and critical illness insurance

3 STEPS TO UNDERSTANDING ACCIDENT & CRITICAL ILLNESS INSURANCE What s Inside Step 1: What What are accident and critical illness insurance products? 4 Step 2: How How do accident and critical illness insurance

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Question Key Number Number Key 1 D 16 C 2 C 17 A 3 C 18 C 4 B 19 C 5 D 20 D 6 A 21 C 7 A 22 A 8 D 23 D 9 C 24 B 10 C 25 B 11 A 26 A 12 B 27

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Question Key Number Number Key 1 D 16 C 2 C 17 A 3 C 18 C 4 B 19 C 5 D 20 D 6 A 21 C 7 A 22 A 8 D 23 D 9 C 24 B 10 C 25 B 11 A 26 A 12 B 27

Club Accounts - David Wilson Question 6.

Club Accounts - David Wilson. 2011 Question 6. Anyone familiar with Farm Accounts or Service Firms (notes for both topics are back on the webpage you found this on), will have no trouble with Club Accounts.

Club Accounts - David Wilson. 2011 Question 6. Anyone familiar with Farm Accounts or Service Firms (notes for both topics are back on the webpage you found this on), will have no trouble with Club Accounts.

BUSINESS, ACCOUNTING AND FINANCIAL STUDIES PAPER 1

FANLING LUTHERAN SECONDARY SCHOOL 2017-2018 S6 MOCK EXAMINATION BUSINESS, ACCOUNTING AND FINANCIAL STUDIES PAPER 1 Date: 31st January, 2018 Time allowed: 8:30 am - 9:45 am (1 hour 15 minutes) This paper

FANLING LUTHERAN SECONDARY SCHOOL 2017-2018 S6 MOCK EXAMINATION BUSINESS, ACCOUNTING AND FINANCIAL STUDIES PAPER 1 Date: 31st January, 2018 Time allowed: 8:30 am - 9:45 am (1 hour 15 minutes) This paper

The Role of the Bookkeeper Types of Businesses The concepts of Business Entity and Historic Cost Setting up the Bank Account The Analysed Cash Book

Paper B1 - Level 2 Unit 1 The Role of the Bookkeeper Types of Businesses The concepts of Business Entity and Historic Cost Setting up the Bank Account The Analysed Cash Book 1. Introduction You have probably

Paper B1 - Level 2 Unit 1 The Role of the Bookkeeper Types of Businesses The concepts of Business Entity and Historic Cost Setting up the Bank Account The Analysed Cash Book 1. Introduction You have probably

Learning about. Checking. Accounts WHAT YOU NEED TO KNOW Deluxe Corp. All Right Reserved.

Learning about Checking Accounts WHAT YOU NEED TO KNOW 2010 Deluxe Corp. All Right Reserved. Contents Learn About Checking Accounts................................3 Write a Check....................................................4

Learning about Checking Accounts WHAT YOU NEED TO KNOW 2010 Deluxe Corp. All Right Reserved. Contents Learn About Checking Accounts................................3 Write a Check....................................................4

In comparison, borrowing from a bank or building society is a business transaction with clearly defined rules to follow.

Teacher s notes money from friends/family People can borrow money from a friend or family member, in which case the arrangements for paying the money back are entirely up to the individuals. Although friends

Teacher s notes money from friends/family People can borrow money from a friend or family member, in which case the arrangements for paying the money back are entirely up to the individuals. Although friends

The Good Bookkeeping Guide

The Good Bookkeeping Guide The Friendly Accountants Chartered Accountants Chartered Tax Advisers Partners: Lesley Ward BSc FCA Richard Baldwyn ATT CTA Arena Business Centre Holyrood Close Poole Dorset

The Good Bookkeeping Guide The Friendly Accountants Chartered Accountants Chartered Tax Advisers Partners: Lesley Ward BSc FCA Richard Baldwyn ATT CTA Arena Business Centre Holyrood Close Poole Dorset

ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

GRADE 11 NOVEMBER 2013 ACCOUNTING

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER 2013 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. 2 ACCOUNTING (NOVEMBER 2013) INSTRUCTIONS AND INFORMATION 1. This question

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER 2013 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. 2 ACCOUNTING (NOVEMBER 2013) INSTRUCTIONS AND INFORMATION 1. This question

Name: Class: Instructions to Candidates. Mark Awarded. Year 9 ACCOUNTING Time: 1:30min. The use of calculators is allowed.

Year 9 ACCOUNTING Time: 1:30min Name: Class: Instructions to Candidates The use of calculators is allowed. All questions must be attempted. All workings must be shown. Mark Awarded Page 1 of 8 1. Tick

Year 9 ACCOUNTING Time: 1:30min Name: Class: Instructions to Candidates The use of calculators is allowed. All questions must be attempted. All workings must be shown. Mark Awarded Page 1 of 8 1. Tick

BOOKKEEPERS IRELAND BOOKKEEPING STANDARDS IN IRELAND. In this issue WAGES VAT OFFICE ADMINISTRATION PAYE/PRSI INCOME LEVY FEEDBACK BOOKKEEPING PODCAST

BOOKKEEPERS IRELAND THE MAGAZINE DEDICATED TO BOOKKEEPING IN IRELAND JUNE 2010 BOOKKEEPING STANDARDS IN IRELAND OR RATHER THE LACK OF THEM Anyone can call themselves an accountant in Ireland, but only

BOOKKEEPERS IRELAND THE MAGAZINE DEDICATED TO BOOKKEEPING IN IRELAND JUNE 2010 BOOKKEEPING STANDARDS IN IRELAND OR RATHER THE LACK OF THEM Anyone can call themselves an accountant in Ireland, but only

Paying for care and support

Paying for care and support Adult Social Care Hull City Council This handbook is all about paying for social care services in Hull. It tells you about the financial assessment process and explains what

Paying for care and support Adult Social Care Hull City Council This handbook is all about paying for social care services in Hull. It tells you about the financial assessment process and explains what

Debit & Credit Cards Extension Activity for Money & Payment Options Presentation

Debit & Credit Cards Extension Activity for Money & Payment Options Presentation Grade Level: Grade 5 Learning Objective: This extension activity, along with the Money & Payment Options presentation should

Debit & Credit Cards Extension Activity for Money & Payment Options Presentation Grade Level: Grade 5 Learning Objective: This extension activity, along with the Money & Payment Options presentation should

ACCOUNTING ACC1 Unit 1 Financial Accounting: The Accounting Information System You will need no other materials. Instructions all Information ACC1

Surname Other Names For Examiner s Use Centre Number Candidate Number Candidate Signature General Certifi cate of Education June 2008 Advanced Subsidiary Examination ACCOUNTING ACC1 Unit 1 Financial Accounting:

Surname Other Names For Examiner s Use Centre Number Candidate Number Candidate Signature General Certifi cate of Education June 2008 Advanced Subsidiary Examination ACCOUNTING ACC1 Unit 1 Financial Accounting:

GRADE 12 SEPTEMBER 2012 ACCOUNTING

Province of the EASTERN CAPE EDUCATION NATIONAL SENIOR CERTIFICATE GRADE 12 SEPTEMBER 2012 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 17 pages. 2 ACCOUNTING (SEPTEMBER 2012) INSTRUCTIONS

Province of the EASTERN CAPE EDUCATION NATIONAL SENIOR CERTIFICATE GRADE 12 SEPTEMBER 2012 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 17 pages. 2 ACCOUNTING (SEPTEMBER 2012) INSTRUCTIONS

GATHER THE INFO STEP 1 - UNDERSTAND WHAT YOU EARN

Brought to you by Take Charge of Your Money GATHER THE INFO This workbook relates to Lessons 4 & 5 (the practical bits of creating a budget) but I would really encourage you to watch the videos in Lessons

Brought to you by Take Charge of Your Money GATHER THE INFO This workbook relates to Lessons 4 & 5 (the practical bits of creating a budget) but I would really encourage you to watch the videos in Lessons

Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay.

Fixed Fee Account Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay. Choose the account plan that best suits your

Fixed Fee Account Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay. Choose the account plan that best suits your

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/02

Centre Number Candidate Number Name UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/02 Paper 2 Candidates answer on the Question

Centre Number Candidate Number Name UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education ACCOUNTING 0452/02 Paper 2 Candidates answer on the Question

Your money goals. Choosing a goal

Choosing a goal 01 Your money goals Next, think about a money goal that you most want to pursue towards that dream. Write down some ideas on how you could start working towards them. My money goal is:

Choosing a goal 01 Your money goals Next, think about a money goal that you most want to pursue towards that dream. Write down some ideas on how you could start working towards them. My money goal is:

A.1 Answer Sheet 1: Understand the Costs Involved in Business Complete the revision sheet then use the answer sheet to self-assess your answers

Finance Revision Worksheet A.1 Answer Sheet 1: Understand the Costs Involved in Business Complete the revision sheet then use the answer sheet to self-assess your answers No Question Your answer Score

Finance Revision Worksheet A.1 Answer Sheet 1: Understand the Costs Involved in Business Complete the revision sheet then use the answer sheet to self-assess your answers No Question Your answer Score

Completing your first self assessment David Hinshelwood

Completing your first self assessment David Hinshelwood Understand AIMS AND OBJECTIVES Understand HMRC requirements What should be included in the records What records should be kept and for how long How

Completing your first self assessment David Hinshelwood Understand AIMS AND OBJECTIVES Understand HMRC requirements What should be included in the records What records should be kept and for how long How

Finance. Contents. Page. 1 Introduction 3. 2 Bookkeeping Systems 5. 3 Profit & Loss Account Balance Sheet Sources of Finance 29

Finance Contents Page 1 Introduction 3 2 Bookkeeping Systems 5 3 Profit & Loss Account 16 4 Balance Sheet 24 5 Sources of Finance 29 6 Glossary of Terms 37 1 2 Finance 1 Introduction Good financial management

Finance Contents Page 1 Introduction 3 2 Bookkeeping Systems 5 3 Profit & Loss Account 16 4 Balance Sheet 24 5 Sources of Finance 29 6 Glossary of Terms 37 1 2 Finance 1 Introduction Good financial management

lesson eight credit cards overheads

lesson eight credit cards overheads shopping for a credit card costs: Annual Percentage Rate (APR) or Finance (Interest) Charges Grace period Annual fees Transaction fees Balancing computation method for

lesson eight credit cards overheads shopping for a credit card costs: Annual Percentage Rate (APR) or Finance (Interest) Charges Grace period Annual fees Transaction fees Balancing computation method for

Switching accounts is easy.

Switching accounts is easy. Discover the local banking difference. At TSB, we re here to look after you. We don t get distracted by things like big corporate finance or investment banking. We use the savings

Switching accounts is easy. Discover the local banking difference. At TSB, we re here to look after you. We don t get distracted by things like big corporate finance or investment banking. We use the savings

Investing 101. Jaspreet Singh Minority Mindset.

Investing 101 Jaspreet Singh Minority Mindset www.theminoritymindset.com Table of Contents i WHO AM I & WHAT IS THE MINORITY MINDSET? ii FOLLOW US iii DISCLAIMER 01 HOW DO YOU MAKE MONEY WITHOUT WORKING?

Investing 101 Jaspreet Singh Minority Mindset www.theminoritymindset.com Table of Contents i WHO AM I & WHAT IS THE MINORITY MINDSET? ii FOLLOW US iii DISCLAIMER 01 HOW DO YOU MAKE MONEY WITHOUT WORKING?

LEARNING TASKS. These tasks match pages 3-21 in Student Guide 5.

STUDENT LEARNING PLAN Lesson 5-1: Checking Accounts OVERVIEW Nothing beats the feel of a crisp new $20 bill in your hand. But as you move toward the real world after high school, you ll run into situations

STUDENT LEARNING PLAN Lesson 5-1: Checking Accounts OVERVIEW Nothing beats the feel of a crisp new $20 bill in your hand. But as you move toward the real world after high school, you ll run into situations

How Do You Calculate Cash Flow in Real Life for a Real Company?

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

Teacher's Guide. Lesson Seven. Credit 04/09

Teacher's Guide $ Lesson Seven Credit 04/09 credit websites Consumers may use credit frequently, but many struggle to manage it wisely. To optimize credit and make sound financial decisions, students need

Teacher's Guide $ Lesson Seven Credit 04/09 credit websites Consumers may use credit frequently, but many struggle to manage it wisely. To optimize credit and make sound financial decisions, students need

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2011 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education www.xtremepapers.com Paper 0452/11 Paper 11 Key messages This question paper contained a mixture of multiple-choice, short

ACCOUNTING Cambridge International General Certificate of Secondary Education www.xtremepapers.com Paper 0452/11 Paper 11 Key messages This question paper contained a mixture of multiple-choice, short

CHAPTER 2 Financial Statements: A Window on an Entity EXERCISES E2-1. Assets = Liabilities + Owners Equity Situation 1 $425,000 $236,000 $189,000

CHAPTER 2 Financial Statements: A Window on an Entity EXERCISES E2-1. Assets = Liabilities + Owners Equity Situation 1 $425,000 $236,000 $189,000 Situation 2 1,350,000 730,000 620,000 Situation 3 200,000

CHAPTER 2 Financial Statements: A Window on an Entity EXERCISES E2-1. Assets = Liabilities + Owners Equity Situation 1 $425,000 $236,000 $189,000 Situation 2 1,350,000 730,000 620,000 Situation 3 200,000

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 3

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 3 DEVELOP YOUR UNDERSTANDING Question 3.1 1. Abi s capital account balance at 1 September 2017 Remember that assets liabilities = capital (equity) Assets Inventory

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 3 DEVELOP YOUR UNDERSTANDING Question 3.1 1. Abi s capital account balance at 1 September 2017 Remember that assets liabilities = capital (equity) Assets Inventory

Introduction 7 WORKSHEET 1 9 The History Of Money 11 WORKSHEET 2 13 History Of Banking 15 WORKSHEET 3 17 Budgeting 21 WORKSHEET 4 23 WORKSHEET 5

Introduction 7 WORKSHEET 1 9 The History Of Money 11 WORKSHEET 2 13 History Of Banking 15 WORKSHEET 3 17 Budgeting 21 WORKSHEET 4 23 WORKSHEET 5 27 WORKSHEET 6 29 Increasing Your Income 33 WORKSHEET 7

Introduction 7 WORKSHEET 1 9 The History Of Money 11 WORKSHEET 2 13 History Of Banking 15 WORKSHEET 3 17 Budgeting 21 WORKSHEET 4 23 WORKSHEET 5 27 WORKSHEET 6 29 Increasing Your Income 33 WORKSHEET 7

Notes. The American Center for Credit Education. Promotional Copy. CheckWise by the American Center for Credit Education

The American Center for Credit Education CheckWise by the American Center for Credit Education 2007 by Rushmore Consumer Credit Resource Center (RCCRC) Published by the American Center for Credit Education

The American Center for Credit Education CheckWise by the American Center for Credit Education 2007 by Rushmore Consumer Credit Resource Center (RCCRC) Published by the American Center for Credit Education

100 Accounting Interview Questions and Answers

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

KEY GUIDE. Business succession planning

KEY GUIDE Business succession planning When disaster strikes What happens to a business if its owner or co-owner dies or falls seriously ill? Much will depend on the type of business sole trader, partnership

KEY GUIDE Business succession planning When disaster strikes What happens to a business if its owner or co-owner dies or falls seriously ill? Much will depend on the type of business sole trader, partnership

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

1. Jake s credit application has been declined because of his negative credit history. Which statement is most likely to be true?

Student Name: Teacher: Date: District: Cabarrus Assessment: 9_12 Shared Courses BF05 - Personal Finance Quiz 1 Description: Exam Review Quiz 5 Form: 501 1. Jake s credit application has been declined because

Student Name: Teacher: Date: District: Cabarrus Assessment: 9_12 Shared Courses BF05 - Personal Finance Quiz 1 Description: Exam Review Quiz 5 Form: 501 1. Jake s credit application has been declined because

Managing your monthly charges

MONTHLY PRICEPLAN Managing your monthly charges To put your business in greater control we d like to fully explain your business banking fees With our Monthly PricePlan you can choose a PricePlan that

MONTHLY PRICEPLAN Managing your monthly charges To put your business in greater control we d like to fully explain your business banking fees With our Monthly PricePlan you can choose a PricePlan that

Partnership Tax Return 2018 for the year ended 5 April 2018 ( )

") Partnership Tax Return 2018 for the year ended 5 April 2018 (2017 18) Tax reference Date Issue address HM Revenue and Customs office address Telephone For Reference This notice requires you by law to send

Partnership Tax Return 2018 for the year ended 5 April 2018 (2017 18) Tax reference Date Issue address HM Revenue and Customs office address Telephone For Reference This notice requires you by law to send

Cambridge International Examinations Cambridge International General Certificate of Secondary Education

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *0963224435* ACCOUNTING 0452/22 Paper 2 October/November 2018 1 hour 45 minutes Candidates answer

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *0963224435* ACCOUNTING 0452/22 Paper 2 October/November 2018 1 hour 45 minutes Candidates answer

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by: How to Prepare

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by: How to Prepare

National Quali cations SPECIMEN ONLY

N5 S800/75/11 National Quali cations SPECIMEN ONLY Accounting Date Not applicable Duration 2 hours Total marks 130 Section 1 70 marks Attempt BOTH questions. Section 2 60 marks Attempt ALL questions. Write

N5 S800/75/11 National Quali cations SPECIMEN ONLY Accounting Date Not applicable Duration 2 hours Total marks 130 Section 1 70 marks Attempt BOTH questions. Section 2 60 marks Attempt ALL questions. Write

ACCN2 (JUN09ACCN201) General Certificate of Education Advanced Subsidiary Examination June Financial and Management Accounting TOTAL

General Certificate of Education Advanced Subsidiary Examination June Financial and Management Accounting TOTAL") Centre Number Surname Candidate Number For Examiner s Use Other Names Candidate Signature Examiner s Initials Accounting General Certificate of Education Advanced Subsidiary Examination June 2009 ACCN2

Centre Number Surname Candidate Number For Examiner s Use Other Names Candidate Signature Examiner s Initials Accounting General Certificate of Education Advanced Subsidiary Examination June 2009 ACCN2

Year 10 GENERAL MATHEMATICS

Year 10 GENERAL MATHEMATICS UNIT 2, TOPIC 3 - Part 1 Percentages and Ratios A lot of financial transaction use percentages and/or ratios to calculate the amount owed. When you borrow money for a certain

Year 10 GENERAL MATHEMATICS UNIT 2, TOPIC 3 - Part 1 Percentages and Ratios A lot of financial transaction use percentages and/or ratios to calculate the amount owed. When you borrow money for a certain

General Motors of Canada Dealer s Standard Accounting System Manual

General Motors of Canada Dealer s Standard Accounting System Manual 2003 General Motors Corporation This manual cannot be reproduced in whole or in part without the expressed written permission of General

General Motors of Canada Dealer s Standard Accounting System Manual 2003 General Motors Corporation This manual cannot be reproduced in whole or in part without the expressed written permission of General

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2014 MARKS: 300 TIME: 3 hours This question paper consists of 24 pages and an 18-page answer book. Accounting 2 DBE/Feb. Mar. 2014 INSTRUCTIONS

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2014 MARKS: 300 TIME: 3 hours This question paper consists of 24 pages and an 18-page answer book. Accounting 2 DBE/Feb. Mar. 2014 INSTRUCTIONS

Cambridge International Examinations Cambridge International General Certificate of Secondary Education

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *3733931195* ACCOUNTING 0452/11 Paper 1 October/November 2018 1 hour 45 minutes Candidates answer

Cambridge International Examinations Cambridge International General Certificate of Secondary Education *3733931195* ACCOUNTING 0452/11 Paper 1 October/November 2018 1 hour 45 minutes Candidates answer

Unit 4 More Banking: Checks, Savings and ATMs

Unit 4 More Banking: Checks, Savings and ATMs Banking: Vocabulary Review Directions: Draw a line to match the word with its meaning. 1. bank 2. credit 3. ATM 4. minimum 5. maximum 6. teller 7. balance

Unit 4 More Banking: Checks, Savings and ATMs Banking: Vocabulary Review Directions: Draw a line to match the word with its meaning. 1. bank 2. credit 3. ATM 4. minimum 5. maximum 6. teller 7. balance

London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary Unit 1: The Accounting System and Costing

Advanced Subsidiary Unit 1: The Accounting System and Costing") Centre No. Candidate No. Surname Signature Paper Reference(s) 6001/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary Unit 1: The Accounting System and Costing Wednesday 15 May

Centre No. Candidate No. Surname Signature Paper Reference(s) 6001/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary Unit 1: The Accounting System and Costing Wednesday 15 May