Expanding Homeownership Responsibly National Federation of Community Development Credit Unions. Sandra Heidinger September 2017

|

|

|

- Hugo Miles

- 5 years ago

- Views:

Transcription

1 Expanding Homeownership Responsibly National Federation of Community Development Credit Unions Sandra Heidinger September 2017

2 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability and affordability of mortgage markets For customers...competing to earn their business For taxpayers...reducing their exposure to mortgage risks

3 Advancing Affordable Lending Offering financing solutions to help qualified borrowers become homeowners» For low- and moderate-income households» For first-time homebuyers Supporting underserved markets» Rural housing» Manufactured housing Working with housing finance agencies Forming alliances across the industry to create ownership opportunities Conducting education and outreach Providing resources, training, and tools

4 Freddie Mac Products & Offerings to Help with Your Purchase Business

5 Home Possible Features and Benefits High LTV mortgage for qualified first-time homebuyers, low- and moderate-income borrowers and move up buyers Borrower Profile First-time homebuyers Repeat homebuyers Families in underserved areas Multi-cultural buyers Empty Nesters Very low and low- to moderateincome borrowers Key Features Maximum LTV/TLTV: Home Possible Advantage - 97% LTV / 105% TLTV Home Possible 95% LTV / 95% TLTV Eligible annual income of up to 100% of Area Median Income (higher in high cost areas) No income limit in Underserved Areas Homebuyer education only required for one borrower when all borrowers are First-Time Homebuyers Loan Product Advisor or Manual Underwrite Borrower Benefits Low down payment No minimum borrower contribution from personal funds for 1-unit residences Flexible down payment and closing cost funding options Reduced mortgage insurance coverage levels (25% coverage when LTV > 90%) No reserves required on 1 unit owner-occupied properties (2 months reserves on 2-4 units) Homebuyer education available at no cost to the borrower

6 Home Possible Mortgages Eligibility Criteria* Eligibility Criteria Eligible Mortgages Home Possible (95% LTV / 95% TLTV) Purchase and no cash out refinance 15-, 20- and 30-year fixed 5/1, 7/1 and 10/1 CMT- and LIBOR-indexed ARMS Construction Conversion and Renovation Mortgages Home Possible Advantage (97% LTV / 105% TLTV) Purchase and no cash out refinance 15-, 20- and 30-year fixed Construction Conversion and Renovation Mortgages Occupancy Primary residence Same Property Type - 1- to 4- units: Single-family, Condos, PUDs - Manufactured Housing (1-unit primary residences only) - 1-unit: Single-family, Condo, PUD Underwriting Method Loan Product Advisor or Manual Same Other Income Boarder income (1-unit properties only) up to 30% of qualifying income from this source allowed if 12 months documentation of recent rent payments and continued rental arrangement included Same Fund Sources for Down Payment & Closing Costs Gifts, grants, Affordable Seconds Same No Credit Score Borrowers Borrowers with no credit score can be evaluated through Loan Product Advisor Not Available * See Freddie Mac Single-Family Seller/Servicer Guide for details.

7 General Requirements: Home Possible Income and Property Eligibility The Borrower s eligible annual income* % AMI Can be up to 100% of the Area Median Income (AMI) AMI Limit: The maximum allowed qualifying income based on the median income for the area in which the mortgaged premises is located or High Cost Area Can be higher based on the higher income limit in high cost areas (Refer to Guide Section ) or Underserved Area Can exceed the AMI as the AMI requirements do not apply *Borrower income: The Seller must attempt to verify all income reported on the Form 65, Uniform Residential Loan Application, in accordance with Chapters 5302 through All income reported on the Form 65 that has been verified and that meets the criteria for stable monthly income as described in Topic 5300 must be used to qualify the Borrower and submitted to Loan Product Advisor for Loan Product Advisor Mortgages. Any discrepancies, including underreported income, must be corrected before submitting the Mortgage to Loan Product Advisor. Guide Chapter 4501

8 What is an Underserved area? An Underserved Area is defined as any of the following:» Low income tract: Census tracts or block numbering areas in which median income does not exceed 80% of the AMI.» Disaster area designation: Disaster areas are designated at the county level by FEMA. A county will be treated as a designated disaster area for three years, beginning January 1 after the FEMA designation.» Minority census tracts: Census tracts that have a minority population of at least 30%. When a property is located in a designated Underserved Area, AMI requirements do not apply.

9 Home Possible Income & Property Eligibility Tool

10 Home Possible Income & Property Eligibility Tool St. Louis, MO

11 Key Features and Benefits Loan Product Advisor Feedback Certificate The loan meets Home Possible income limits based on the property location for address entered Employment & Income Section: Feedback message returned when either Home Possible or Home Possible Advantage Offering Identifier has been selected

12 Flexible Down-payment & Closing-cost Sources Flexible Sources of Funds* Financing Concessions» 3% LTV/TLTV ratio > 90%» 6% LTV/TLTV ratio > 75% < 90%» 9% LTV/TLTV ratio < 75% * Closing costs Lender Credit Unsecured Loan: Originating Lender (Refer to Guide Section ) Borrower Personal Funds* (Minimum borrower contribution, if applicable) Depository accounts Sale of Borrower Asset Cash on hand Trust disbursement Pooled funds Loan secured by Financial Assets Securities Government bonds Retirement accounts Individual Development Account (IDA): include matching funds only if not subject to recapture tax Community Savings deposited by the Borrower Trade equity Rent Credits Cash value of life insurance Borrower s real estate commission Credit card charges, cash advances or unsecured line of credit: to pay fees associated with the mortgage application process Other Eligible Sources Gifts/Wedding Gift Funds/Gift of Equity Gift/Grant: Agency Secondary Financing Affordable Seconds Employer-Assisted Homeownership Benefit IDA: matching funds subject to recapture tax Unsecured loan: Agency/Related Person, or Community Savings Systems (funds in excess of Borrower s contribution) Sweat equity (once 5% downpayment from personal funds has been met)

13 Why choose Home Possible over FHA? Home Possible Mortgage Insurance vs. FHA Ends when LTV < 80% Stays for the life of the loan Conventional MI: monthly OR single premiums Only required if the LTV is 80% or higher Down payment funds applied to principal FHA: Upfront AND monthly premiums Required regardless of the LTV Down payment funds applied to principal AND upfront PMI WHAT THIS MEANS: With more funds applied toward the principal upfront, a Home Possible mortgage with PMI lets the borrower build equity faster.

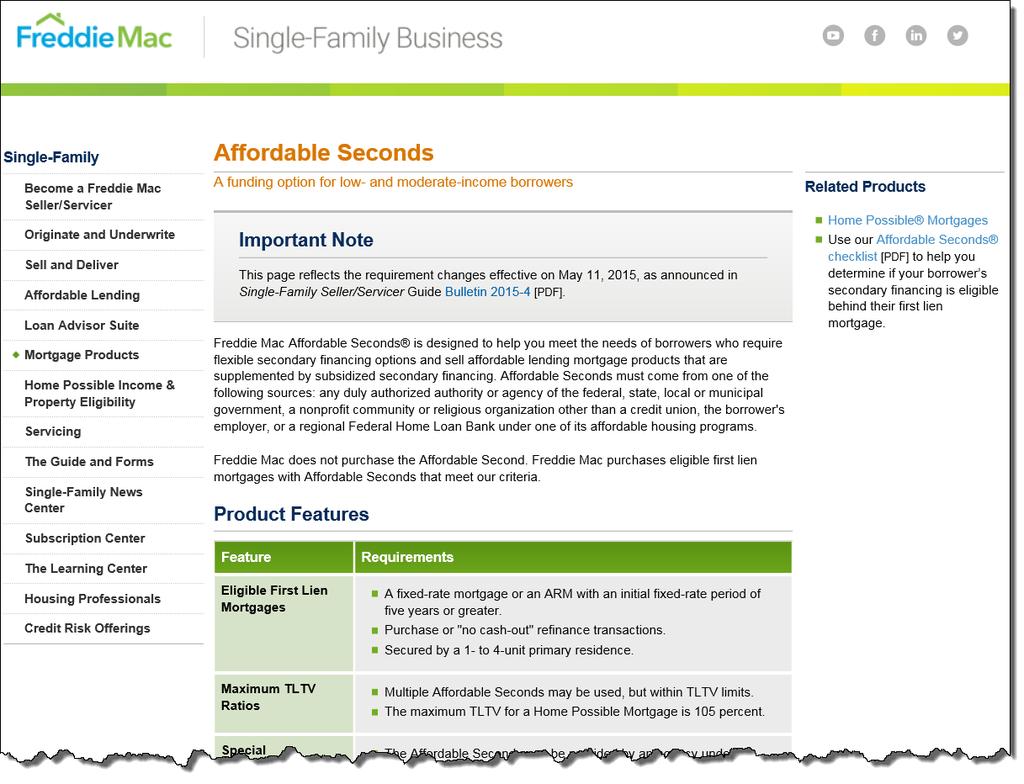

14 Affordable Seconds

15 Down Payment Resource Website Down Payment Resource Website* - Helps connect borrowers with homeownership programs that can help with down payment. DownPaymentResource.com/are-you-eligible/ * Available on FreddieMac.com

16 Homeownership Education Purchase Transactions Required: When all borrowers are first-time homebuyers, at least one qualifying borrower must participate in a homeownership education program before the Note Date*» A copy of a Homeownership Education Certification, or another document with comparable information, to be retained in the mortgage file 2- to 4-unit primary residence (Home Possible only): At least one qualifying Borrower must participate in a landlord education program before the Note Date*» A copy of a certificate evidencing successful completion of the landlord education program must be retained in the Mortgage file *NOTE: Must not be provided by an interested party to the transaction, the originating lender or Seller This requirement stresses the importance of utilizing a curriculum that contains the minimum core content specified by the National Industry Standards for Homeownership Education and Counseling. These standards help ensure quality education and counseling is delivered with fairness and respect to homebuyers and homeowners *or the Effective Date of Permanent Financing for Construction Conversion and Renovation Mortgages Guide Chapter 4501

17 Supporting the Duty to Serve Program Proposing ways to help address some of society s most persistent housing challenges What - Support 3 underserved markets» Rural housing» Manufactured housing» Affordable housing preservation Why» Support very low-, low-, and moderateincome households nationwide» Address communities needs in sustainable ways that over time will benefit our country for generations to come

18 Duty to Serve - Single Family Core Activities HERA established a duty for the GSEs to serve three historically underserved markets: Manufactured Housing Rural Housing Affordable Housing Preservation Specifically, the GSEs are to increase the liquidity of mortgage investments and improve the distribution of investment capital available for mortgage financing for very low-, low-, and moderate-income families in these underserved markets Housing in Rural Areas Core Activities Manufactured Housing Activities that Serve High Needs Rural Regions (areas of persistent poverty) Middle Appalachia, Lower Mississippi Delta, Colonia A tract located in a persistent poverty county Activities that Serve High-Needs Rural Populations: Members of a federally recognized Native American tribe located in an Indian area Agricultural workers Financing by small financial institutions of owner-occupied housing Real estate-financed units Chattel-financed units (including both pilot and ongoing initiatives) Energy Efficiency Improvements on First-lien Properties Projections that improvements financed will reduce energy or water consumption by the homeowner or tenant by at least 15 percent; and The utility savings generated over an improvement s expected life must exceed the cost of installation Affordable Housing Preservation Distressed Properties Purchase or rehab of certain distressed properties Homes eligible for short sale, foreclosure sale, REO Shared Equity Homeownership Programs with long-term affordability administered by community land trusts, other non-profits or state/local governments or instrumentalities Preservation of Housing Stock via: Deed-Restricted Programs, or Ground Leases, or Shared Appreciation Loans

19 Resources to Support Your Business Tools for You and Your Client

20 Home Possible Information FreddieMac.com/homepossible FreddieMac.com/learn/mp/homepossible.html

21 Purchase Market Resource Center

22 Community Lender Resource Center

23 Freddie Mac s Duty to Serve Web Page Duty to Serve Web Link:

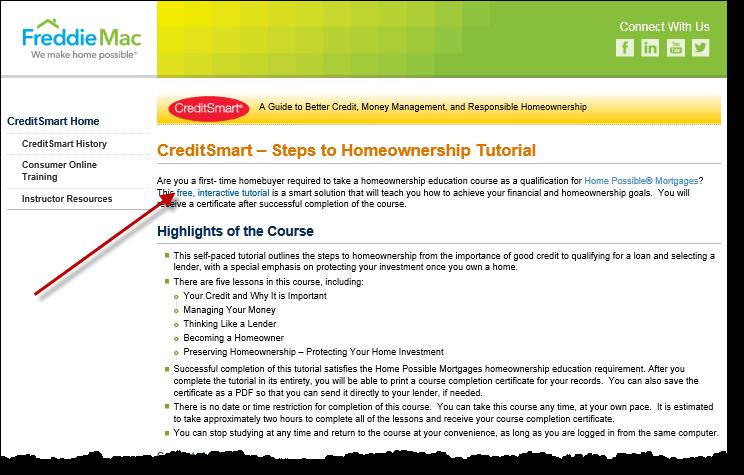

24 CreditSmart FreddieMac.com/creditsmart/tutorial.html FREE

25 Freddie Mac Borrower Help Centers and National Network Borrower Help Centers and Network Work with trusted national nonprofit intermediaries Support Freddie Mac s ongoing commitment of: preparing prospective buyers for responsible homeownership helping struggling borrowers with Freddie Mac-owned mortgages avoid foreclosure HUD-Approved Agencies 14 locations across the country Work with Lenders in minority and underserved communities FreddieMac.com/singlefamily/housingpros/help_centers.html

26 My Home by Freddie Mac SM Consumer Website What will the borrower find on My Home? A wealth of information to help the borrower decide whether to rent or buy, understand the mortgage process and who to contact for help if they are struggling to pay their mortgage. All of this, plus: Tutorials Meet the Experts video series Calculators Quizzes Worksheets Brochures Infographics What home means to me photo essay myhome.freddiemac.com

27 YOU are the critical link YOU are the critical link to helping well-qualified homebuyers achieve their homeownership objectives:» Provide access to credit; originate loans to the full extent of Freddie Mac s credit box» Utilize your mortgage finance expertise» Explain the process and dispel the 20% down payment myth» Identify and match available financial resources in your area (government, nonprofit, private sources) with a sustainable mortgage solution» Take advantage of Freddie Mac training and resources for both you and your borrower First-time homebuyer dream realized and more business for you if you know your market and where to find those affordability gap solutions Freddie Mac is here to help

28 QA &

Expanding Homeownership Responsibly with Freddie Mac Home Possible. February 2017

Expanding Homeownership Responsibly with Freddie Mac Home Possible February 2017 Presenter Dennis J. Smith Joined Freddie Mac in September 2015 as Affordable Lending Manager Works with lenders, nonprofits

Expanding Homeownership Responsibly with Freddie Mac Home Possible February 2017 Presenter Dennis J. Smith Joined Freddie Mac in September 2015 as Affordable Lending Manager Works with lenders, nonprofits

Expanding Homeownership Responsibly with Freddie Mac Home Possible

Expanding Homeownership Responsibly with Freddie Mac Home Possible March 23, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability

Expanding Homeownership Responsibly with Freddie Mac Home Possible March 23, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability

Expanding Homeownership Responsibly with Freddie Mac Home Possible. Nadja Vital MBA Central FL, Nov.8, 2017

Expanding Homeownership Responsibly with Freddie Mac Home Possible Nadja Vital MBA Central FL, Nov.8, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve

Expanding Homeownership Responsibly with Freddie Mac Home Possible Nadja Vital MBA Central FL, Nov.8, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve

Expanding Homeownership Responsibly with Freddie Mac. March 2, 2017

Expanding Homeownership Responsibly with Freddie Mac March 2, 2017 A Better Freddie Mac and a better housing finance system For homebuyers...innovating to improve the liquidity, stability and affordability

Expanding Homeownership Responsibly with Freddie Mac March 2, 2017 A Better Freddie Mac and a better housing finance system For homebuyers...innovating to improve the liquidity, stability and affordability

Home Possible and Home Possible Advantage

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Grow Your Business with Freddie Mac Home Possible Mortgages. Jenneese Worley, Account Executive, Nadja Vital, Affordable Manager

Grow Your Business with Freddie Mac Home Possible Mortgages Jenneese Worley, Account Executive, Nadja Vital, Affordable Manager June 9, 2016 Single-Family 2016 priorities 1. Look for better ways to provide

Grow Your Business with Freddie Mac Home Possible Mortgages Jenneese Worley, Account Executive, Nadja Vital, Affordable Manager June 9, 2016 Single-Family 2016 priorities 1. Look for better ways to provide

Freddie Mac s HFA Advantage Mortgage Master Servicer: US Bank

HFA Advantage Mortgage: Maximum 97% LTV / 105% TLTV HFA income limits All delivery fees waived Charter-level mortgage insurance available available exclusively through participating State or Local Housing

HFA Advantage Mortgage: Maximum 97% LTV / 105% TLTV HFA income limits All delivery fees waived Charter-level mortgage insurance available available exclusively through participating State or Local Housing

GMFS LA CAFA. Home Possible Advantage for HFA. Freddie Conforming CAFA

GMFS LA CAFA Home Possible Advantage for HFA Freddie Conforming CAFA Familiarize you with the benefits, key features and requirements for GMFS LA CAFA s low down payment mortgage offering: Home Possible

GMFS LA CAFA Home Possible Advantage for HFA Freddie Conforming CAFA Familiarize you with the benefits, key features and requirements for GMFS LA CAFA s low down payment mortgage offering: Home Possible

LPA HOME POSSIBLE. Home Possible

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

Duty to Serve. Single Family Affordable Lending and Access to Credit May 2018

Duty to Serve Single Family Affordable Lending and Access to Credit May 2018 Freddie Mac s Mission A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity,

Duty to Serve Single Family Affordable Lending and Access to Credit May 2018 Freddie Mac s Mission A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity,

State of the Housing Market

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

HomeStyle Renovation & Energy Mortgages. Finance renovation or energy efficient costs into a single-close home purchase or refinance loan

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

Conventional 97% LTV Options updated 12/5/2018 Freddie Mac HomeOne Mortgage 97% LTV

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

1-Unit properties, including condominiums and units in Planned Unit Developments o No Manufactured Homes

OVERVIEW HomeOne mortgage, a new conventional (non-fha) 3% down payment option for qualified first-time homebuyers. HomeOne mortgage broadly serves borrowers without geographic or income restrictions.

OVERVIEW HomeOne mortgage, a new conventional (non-fha) 3% down payment option for qualified first-time homebuyers. HomeOne mortgage broadly serves borrowers without geographic or income restrictions.

HomeReady vs. Home Possible Comparison

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Doing More for Underserved Housing Markets

Doing More for Underserved Housing Markets Overview of the Duty To Serve Rule 2018 Fannie Mae. Trademarks of of Fannie Mae. 1 Agenda What is the Duty To Serve Rule? Why is the Duty To Serve important?

Doing More for Underserved Housing Markets Overview of the Duty To Serve Rule 2018 Fannie Mae. Trademarks of of Fannie Mae. 1 Agenda What is the Duty To Serve Rule? Why is the Duty To Serve important?

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

HomeReady. Eligibility 1 UNIT 2 TO 4 UNITS. Purchase or Limited Cash-Out Refinance. Loan Purpose. Occupancy and Property Type Borrower Income Limits

HomeReady 1 UNIT 2 TO 4 UNITS Loan Purpose Purchase or Limited Cash-Out Refinance Eligibility Occupancy and Property Type Borrower Income Limits Minimum Borrower Contribution Acceptable Sources of Funds

HomeReady 1 UNIT 2 TO 4 UNITS Loan Purpose Purchase or Limited Cash-Out Refinance Eligibility Occupancy and Property Type Borrower Income Limits Minimum Borrower Contribution Acceptable Sources of Funds

FHLMC PROGRAM LINEUP`

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FNMA s HomeReady Program

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

HOMEREADY. Table of Contents

Table of Contents 1. Table of Contents... 1 2. Overview... 2 3. Product Codes... 2 4. Accessory Unit Income... 2 5. Boarder Income... 2 6. Borrower Income Limits and Calculations... 3 7. DU Loan Case Files:

Table of Contents 1. Table of Contents... 1 2. Overview... 2 3. Product Codes... 2 4. Accessory Unit Income... 2 5. Boarder Income... 2 6. Borrower Income Limits and Calculations... 3 7. DU Loan Case Files:

HomeReady Mortgage. Overview for Loan Officers May Fannie Mae. Trademarks of Fannie Mae. 1

HomeReady Mortgage Overview for Loan Officers May 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 An Important note about the seminar content While every effort has been made to ensure the reliability

HomeReady Mortgage Overview for Loan Officers May 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 An Important note about the seminar content While every effort has been made to ensure the reliability

Close More Loans with HomeReady Mortgage

Close More Loans with HomeReady Mortgage Overview for Loan Officers May 2, 2017, 2 3:30 p.m. ET Dial-in number: 800-779-8492 Participant passcode: 4344988 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Seminar

Close More Loans with HomeReady Mortgage Overview for Loan Officers May 2, 2017, 2 3:30 p.m. ET Dial-in number: 800-779-8492 Participant passcode: 4344988 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Seminar

Accessing Credit: Permanent Mortgage

U.S. Department of Housing and Urban Development HUD NSP Webinar Accessing Credit: Permanent Mortgage Financing Thursday, February 24, 2011 Community Planning and Development Presenters: Host: Kent Buhl

U.S. Department of Housing and Urban Development HUD NSP Webinar Accessing Credit: Permanent Mortgage Financing Thursday, February 24, 2011 Community Planning and Development Presenters: Host: Kent Buhl

GSFA PLATINUM PROGRAM CONVENTIONAL GUIDELINES SUMMARY

OVERVIEW The GSFA Conventional Down Payment Assistance Program (DAP) is a competitively priced Conventional loan program that does not require a minimum down payment from the homebuyer(s). GSFA provides

OVERVIEW The GSFA Conventional Down Payment Assistance Program (DAP) is a competitively priced Conventional loan program that does not require a minimum down payment from the homebuyer(s). GSFA provides

Native American Indian Housing Council 2018 Annual Conference. San Diego, CA May 30, Collaborating with Fannie Mae to Expand Affordable Housing

Native American Indian Housing Council 2018 Annual Conference San Diego, CA May 30, 2018 Collaborating with Fannie Mae to Expand Affordable Housing 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Agenda Who

Native American Indian Housing Council 2018 Annual Conference San Diego, CA May 30, 2018 Collaborating with Fannie Mae to Expand Affordable Housing 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Agenda Who

HomeReady Conforming Fixed Program Summary

HomeReady Conforming Fixed Program Summary HomeReady Matrix with Mortgage Insurance Guideline Overlays: PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO/Score LTV/CLTV/HCLTV Primary Residence 1 620

HomeReady Conforming Fixed Program Summary HomeReady Matrix with Mortgage Insurance Guideline Overlays: PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO/Score LTV/CLTV/HCLTV Primary Residence 1 620

How to Originate and Deliver HomeReady Mortgages

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

Deep Dive with Freddie Mac 2019 NCSHA HFA Institute. Erin Quinn and Simone Beaty Single Family Affordable Lending and Access to Credit

Deep Dive with Freddie Mac 2019 NCSHA HFA Institute Erin Quinn and Simone Beaty Single Family Affordable Lending and Access to Credit January 17, 2019 A Better Freddie Mac and a better housing finance

Deep Dive with Freddie Mac 2019 NCSHA HFA Institute Erin Quinn and Simone Beaty Single Family Affordable Lending and Access to Credit January 17, 2019 A Better Freddie Mac and a better housing finance

Close More Loans with HomeReady Mortgage An Overview for Loan Officers. Dial- in for audio:

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-866-845-1266 Seminar guidelines Please do not place the call on hold at any time. Please place your phone on

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-866-845-1266 Seminar guidelines Please do not place the call on hold at any time. Please place your phone on

PennyMac Correspondent Group Freddie Mac Home Possible Overlays to Freddie Mac are underlined

PennyMac Correspondent Group Freddie Mac Home Possible 01.18.18 Overlays to Freddie Mac are underlined Home Possible Freddie Mac - LPA Accept Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Freddie Mac Home Possible 01.18.18 Overlays to Freddie Mac are underlined Home Possible Freddie Mac - LPA Accept Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

Opportunities for HFA and GSE Collaboration. Moderator: Maria Day-Marshall Panelists: Erin Quinn, Shaun Smith, Mark Spates, and Tabaré Borbón

Opportunities for HFA and GSE Collaboration Moderator: Maria Day-Marshall Panelists: Erin Quinn, Shaun Smith, Mark Spates, and Tabaré Borbón Opportunities for HFA and GSE Collaboration NALHFA Annual Conference

Opportunities for HFA and GSE Collaboration Moderator: Maria Day-Marshall Panelists: Erin Quinn, Shaun Smith, Mark Spates, and Tabaré Borbón Opportunities for HFA and GSE Collaboration NALHFA Annual Conference

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Home Possible Conforming Fixed

Home Possible Conforming Fixed Home Possible Matrix with Mortgage Insurance Guideline Overlays: PURCHASE & RATE TERM REFINANCE Occupancy Units FICO/Score LP LTV/CLTV Primary Residence 1 620 97/97 Primary

Home Possible Conforming Fixed Home Possible Matrix with Mortgage Insurance Guideline Overlays: PURCHASE & RATE TERM REFINANCE Occupancy Units FICO/Score LP LTV/CLTV Primary Residence 1 620 97/97 Primary

Close More Loans with HomeReady Mortgage An Overview for Loan Officers. Dial- in for audio: Attendee passcode:

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-800-779-8492 Attendee passcode: 4344988 Seminar guidelines Please do not place the call on hold at any time.

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-800-779-8492 Attendee passcode: 4344988 Seminar guidelines Please do not place the call on hold at any time.

Freddie Mac Duty to Serve Underserved Markets Plan. For

Freddie Mac Duty to Serve Underserved Markets Plan For 2018-2020 DUTY TO SERVE Underserved Markets Plan 3-Year Activities and Objectives (By Evaluation Area and Year) Manufactured Housing Activities and

Freddie Mac Duty to Serve Underserved Markets Plan For 2018-2020 DUTY TO SERVE Underserved Markets Plan 3-Year Activities and Objectives (By Evaluation Area and Year) Manufactured Housing Activities and

SUBJECT: SELLING UPDATES

TO: Freddie Mac Sellers August 29, 2018 2018-13 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Home Possible Enhanced credit flexibilities and simplified Home Possible Mortgage requirements through

TO: Freddie Mac Sellers August 29, 2018 2018-13 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Home Possible Enhanced credit flexibilities and simplified Home Possible Mortgage requirements through

(Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac) (collectively, the Enterprises) to serve three specified underserved markets

and the Federal Home Loan Mortgage Corporation (Freddie Mac) (collectively, the Enterprises) to serve three specified underserved markets") BILLING CODE: 8070-01-P FEDERAL HOUSING FINANCE AGENCY 12 CFR Part 1282 RIN 2590-AA27 Enterprise Duty to Serve Underserved Markets AGENCY: Federal Housing Finance Agency. ACTION: Final rule. SUMMARY: The

BILLING CODE: 8070-01-P FEDERAL HOUSING FINANCE AGENCY 12 CFR Part 1282 RIN 2590-AA27 Enterprise Duty to Serve Underserved Markets AGENCY: Federal Housing Finance Agency. ACTION: Final rule. SUMMARY: The

EverBank Wholesale Lending

EverBank Wholesale Lending LOAN PROGRAM CODE PRODUCT OVERVIEW LOAN TYPE LOAN TERMS ELIGIBLE PROPERTY TYPES INELIGIBLE PROPERTY TYPES OCCUPANCY 30 Year - 30FNMC 15 Year - 15FNMC The FNMA MyCommunity products

EverBank Wholesale Lending LOAN PROGRAM CODE PRODUCT OVERVIEW LOAN TYPE LOAN TERMS ELIGIBLE PROPERTY TYPES INELIGIBLE PROPERTY TYPES OCCUPANCY 30 Year - 30FNMC 15 Year - 15FNMC The FNMA MyCommunity products

May 17, Housing Sector Overview

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

FNMA HomeReady & Loan Programs 97%

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

Instructions for Completing the Uniform Residential Loan Application

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Attention All Correspondent Lending Sellers: April 20, 2018 CA Announcing Freddie Mac Home Possible and Home Possible Advantage

Attention All Correspondent Lending Sellers: April 20, 2018 CA 18-037 Announcing Freddie Mac Home Possible and Home Possible Advantage Subject Summary Effective Date Home Possible Advantage Mortgage Maximum

Attention All Correspondent Lending Sellers: April 20, 2018 CA 18-037 Announcing Freddie Mac Home Possible and Home Possible Advantage Subject Summary Effective Date Home Possible Advantage Mortgage Maximum

ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

SONYMA Conventional Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Bulletin. TO: All Freddie Mac Sellers and Servicers April 22, 2008

Bulletin TO: All Freddie Mac Sellers and Servicers April 22, 2008 SUBJECTS With this Single-Family Seller/Servicer Guide (Guide) Bulletin, we are making the following changes to our selling requirements:

Bulletin TO: All Freddie Mac Sellers and Servicers April 22, 2008 SUBJECTS With this Single-Family Seller/Servicer Guide (Guide) Bulletin, we are making the following changes to our selling requirements:

Minnesota Housing: A Path to Successful Homeownership. A Path to Homeownership & Family Self-Sufficiency (REP)

") Minnesota Housing: A Path to Successful Homeownership Minnesota Housing: Real Estate Program A Path to Homeownership & Family Self-Sufficiency (REP) Today s conversation Who we are Why we re here Increasing

Minnesota Housing: A Path to Successful Homeownership Minnesota Housing: Real Estate Program A Path to Homeownership & Family Self-Sufficiency (REP) Today s conversation Who we are Why we re here Increasing

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile Overlays to Fannie Mae are underlined

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

The Chase Guaranteed Rural Housing Purchase Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18 Jerry Flach (973) 305-8800 x 4252 gflach@valleynationalbank.com Sofi Cordero (973) 305-8800 x 8884 scordero@valleynationalbank.com

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18 Jerry Flach (973) 305-8800 x 4252 gflach@valleynationalbank.com Sofi Cordero (973) 305-8800 x 8884 scordero@valleynationalbank.com

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Energy Efficiency Proposals in Fannie Mae and Freddie Mac s Draft Underserved Markets Plans

Energy Efficiency Proposals in Fannie Mae and Freddie Mac s Draft Underserved Markets Plans Prepared May 17, 2017 by the National Association of State Energy Officials (NASEO) Contact: Sandy Fazeli (sfazeli@naseo.org)

Energy Efficiency Proposals in Fannie Mae and Freddie Mac s Draft Underserved Markets Plans Prepared May 17, 2017 by the National Association of State Energy Officials (NASEO) Contact: Sandy Fazeli (sfazeli@naseo.org)

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Unders

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Understanding Credit Programs Impact of TRID (TILA Respa

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Understanding Credit Programs Impact of TRID (TILA Respa

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile Overlays to Freddie Mac are underlined

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 01.01.18 Overlays to Freddie Mac are underlined Agency Finance Type Occupancy Term Freddie Mac - LPA Accept Purchase

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 01.01.18 Overlays to Freddie Mac are underlined Agency Finance Type Occupancy Term Freddie Mac - LPA Accept Purchase

Wholesale Overlay Matrix

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Oklahoma s Affordable Housing Resources

Oklahoma s Affordable Housing Resources The Regional Housing Forums 2017 - Ardmore - Enid - Midwest City - Tulsa - Economic Inclusion Ladder 1. Support quality and innovation in programs to build financial

Oklahoma s Affordable Housing Resources The Regional Housing Forums 2017 - Ardmore - Enid - Midwest City - Tulsa - Economic Inclusion Ladder 1. Support quality and innovation in programs to build financial

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile

Agency Finance Type Occupancy Term PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 05.10.18 Freddie Mac - LPA Accept Purchase and Rate/Term Refinances Owner Occupied

Agency Finance Type Occupancy Term PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 05.10.18 Freddie Mac - LPA Accept Purchase and Rate/Term Refinances Owner Occupied

Federal Home Loan Banks Affordable Housing Program. April 17, 2018

Federal Home Loan Banks Affordable Housing Program April 17, 2018 1 Key Dates: Deadlines to Submit Comments Weigh in on OFN s letter Due by April 25, 2018 Email comments to dwilliams@ofn.org Submit comments

Federal Home Loan Banks Affordable Housing Program April 17, 2018 1 Key Dates: Deadlines to Submit Comments Weigh in on OFN s letter Due by April 25, 2018 Email comments to dwilliams@ofn.org Submit comments

Section Agency Loan Programs

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

Section 2.23 Veterans Administration (VA) Loan Program

Loan Program") Section 2.23 Veterans Administration (VA) Loan Program In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Correspondent Lenders with

Section 2.23 Veterans Administration (VA) Loan Program In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Correspondent Lenders with

Freddie Mac Duty to Serve Underserved Markets Plan. For

Freddie Mac Duty to Serve Underserved Markets Plan For 2018-2020 Rural Housing Disclaimer: Implementation of the activities and objectives in Freddie Mac s Duty to Serve Underserved Markets Plan may be

Freddie Mac Duty to Serve Underserved Markets Plan For 2018-2020 Rural Housing Disclaimer: Implementation of the activities and objectives in Freddie Mac s Duty to Serve Underserved Markets Plan may be

Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America. Sara Morgan Fahe / #OFNCONF #CDFIsINVEST

Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America Sara Morgan Fahe / 09-28-2017 Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and

Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America Sara Morgan Fahe / 09-28-2017 Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and

Freddie Mac LP Open Access (Relief Refinance Mortgages) (CF30OAFR & CF15OAFR)

(CF30OAFR & CF15OAFR)") Table of Contents 1. Eligible Transactions...2 2. Ineligible Transactions...2 3. Eligible Borrowers...3 4. Borrower Benefit...3 5. Underwriting Method...3 6. Credit (Derogatory)...4 7. LTV/TLTV...4 8.

Table of Contents 1. Eligible Transactions...2 2. Ineligible Transactions...2 3. Eligible Borrowers...3 4. Borrower Benefit...3 5. Underwriting Method...3 6. Credit (Derogatory)...4 7. LTV/TLTV...4 8.

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Stockton Mortgage Funding HomeReady Fixed Rate Mortgage Product

1. PRODUCT DESCRIPTION Conventional C onforming fixed rate m ortgage DU Version 9.3 10, 15, 20, or 30 year terms for product 30 year term only for product Fully amortizing Qualified Mortgage (QM) Safe

1. PRODUCT DESCRIPTION Conventional C onforming fixed rate m ortgage DU Version 9.3 10, 15, 20, or 30 year terms for product 30 year term only for product Fully amortizing Qualified Mortgage (QM) Safe

FNMA Home Affordable Refinance Program (HARP) Transaction Type Number of Units Fixed Rate Max LTV/CLTV

Transaction Type Number of Units Fixed Rate Max LTV/CLTV") FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

Exhibit B: Guide Chapter K33 Mortgages for Newly Constructed Homes

Exhibit B: Guide Chapter K33 for Newly Constructed Homes K33.1: Overview This chapter details the requirements for the three types of for Newly Constructed Homes: Newly Built Home Conversion Renovation

Exhibit B: Guide Chapter K33 for Newly Constructed Homes K33.1: Overview This chapter details the requirements for the three types of for Newly Constructed Homes: Newly Built Home Conversion Renovation

<logo> Offered through 21 st Century Home Loans WHOLESALE DIVISION

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

FANNIE MAE MATRICES & GUIDELINES

FANNIE MAE MATRICES & GUIDELINES LSMG Fannie Mae Matrices & Guidelines Page 1 of 37 Revised 06/17/2016 Fannie Mae Matrices & Guidelines... 1 LSMG Fannie Mae Purchase Matrix and Guidelines... 5 Qualifying

FANNIE MAE MATRICES & GUIDELINES LSMG Fannie Mae Matrices & Guidelines Page 1 of 37 Revised 06/17/2016 Fannie Mae Matrices & Guidelines... 1 LSMG Fannie Mae Purchase Matrix and Guidelines... 5 Qualifying

8:1 CONFORMING FIXED RATE

8:1 CONFORMING FIXED RATE LOAN PRODUCT CODES LOAN PRODUCT LOAN TERM/AMORTIZATION* 101 30 Year Fixed Rate 241-360 months 104 20 Year Fixed Rate 181-240 months 102 15 Year Fixed Rate 121-180 months 110 10

8:1 CONFORMING FIXED RATE LOAN PRODUCT CODES LOAN PRODUCT LOAN TERM/AMORTIZATION* 101 30 Year Fixed Rate 241-360 months 104 20 Year Fixed Rate 181-240 months 102 15 Year Fixed Rate 121-180 months 110 10

AHP 2018 Implementation Plan Native American Homeownership Initiative (NAHI) Program Guidelines

Program Guidelines") I. (NAHI) Program Guidelines 1. Program Summary In 2018 the Bank will make $1,000,000 available on a first-come first-served basis to eligible members that have executed a Down Payment Subsidy Agreement.

I. (NAHI) Program Guidelines 1. Program Summary In 2018 the Bank will make $1,000,000 available on a first-come first-served basis to eligible members that have executed a Down Payment Subsidy Agreement.

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES

DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES") THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

CHFA-Approved Lenders Mortgage Program Training. Rev 5/10/18

CHFA-Approved Lenders Mortgage Program Training Rev 5/10/18 Our Mission To alleviate the shortage of housing for low-to-moderate income families and persons in this State and, when appropriate, to promote

CHFA-Approved Lenders Mortgage Program Training Rev 5/10/18 Our Mission To alleviate the shortage of housing for low-to-moderate income families and persons in this State and, when appropriate, to promote

Niche Loan Programs. Featured Loan. Zero Down Loan

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

ARLINGTON COUNTY, VIRGINIA. County Board Agenda Item Meeting of April 21, 2012

ARLINGTON COUNTY, VIRGINIA County Board Agenda Item Meeting of April 21, 2012 DATE: April 13, 2012 SUBJECT: Funding for the Moderate Income Purchase Assistance Program (MIPAP) to Assist Qualifying Vested

ARLINGTON COUNTY, VIRGINIA County Board Agenda Item Meeting of April 21, 2012 DATE: April 13, 2012 SUBJECT: Funding for the Moderate Income Purchase Assistance Program (MIPAP) to Assist Qualifying Vested

ditech BUSINESS LENDING FREDDIE MAC HOME POSSIBLE LPMI FIXED RATE MORTGAGE PRODUCT

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING FREDDIE MAC HOME POSSIBLE LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage Servicing retained 10-30 year term in annual increments

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING FREDDIE MAC HOME POSSIBLE LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage Servicing retained 10-30 year term in annual increments

Craig Nickerson, National Community Stabilization Trust (NCST) Rob Grossinger, Enterprise Community Partners (Enterprise)

Rob Grossinger, Enterprise Community Partners (Enterprise)") Presenters Host: National Development Council Moderator: TBD Presenters: Craig Nickerson, National Community Stabilization Trust (NCST) Rob Grossinger, Enterprise Community Partners (Enterprise) 2 NSP

Presenters Host: National Development Council Moderator: TBD Presenters: Craig Nickerson, National Community Stabilization Trust (NCST) Rob Grossinger, Enterprise Community Partners (Enterprise) 2 NSP

Freddie Mac Conforming and Super Conforming Fixed Rate

NOTE: Freddie Mac s new Income (Bulletin 2016-19) and Asset (Bulletin 2016-23) requirements are available now and may be used immediately. Loans using prior guidance must be disbursed by LSM on or before

NOTE: Freddie Mac s new Income (Bulletin 2016-19) and Asset (Bulletin 2016-23) requirements are available now and may be used immediately. Loans using prior guidance must be disbursed by LSM on or before

Fixed-rate, fully amortizing with level payments for life of loan. This program is for conventional conforming loan amounts.

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Chapter 23: Maximum Loan Amounts and LTV, TLTV and HTLTV Ratios

May 2, 2008 Guide Bulletin Chapter 23: Maximum Loan Amounts and LTV, TLTV and HTLTV Ratios 23.5: Maximum financing (05/02/08) Financing to the maximum loan-to value (LTV) ratio, as set forth in Section

May 2, 2008 Guide Bulletin Chapter 23: Maximum Loan Amounts and LTV, TLTV and HTLTV Ratios 23.5: Maximum financing (05/02/08) Financing to the maximum loan-to value (LTV) ratio, as set forth in Section

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

Correspondent Lending FHA Fixed Rate

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Participating Lender Training

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

WELCOME. Introductions. Housekeeping items. Breaks. Getting Started

Training on CHFA WELCOME Introductions Getting Started Housekeeping items Breaks AGENDA Website www.chfa.org About CHFA-Mission/History Homebuyer Programs Reserving CHFA Funds Homebuyer Program Guidelines

Training on CHFA WELCOME Introductions Getting Started Housekeeping items Breaks AGENDA Website www.chfa.org About CHFA-Mission/History Homebuyer Programs Reserving CHFA Funds Homebuyer Program Guidelines

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

Glossary. An item of value that you own.

Term A adjustable-rate mortgage (ARM) amortization amortized annual percentage rate (APR) appraisal appreciation assessment fees asset association fees Definition A mortgage loan with an interest rate

Term A adjustable-rate mortgage (ARM) amortization amortized annual percentage rate (APR) appraisal appreciation assessment fees asset association fees Definition A mortgage loan with an interest rate

Exhibit 19 Credit Fees in Price

Exhibit 19 Credit Fees in Price 1. Credit Fees in Price for Mortgages with Special Attributes This Credit Fee in Price Matrix sets forth the Credit Fee in Price amounts and/or Credit Fee in Price rates

Exhibit 19 Credit Fees in Price 1. Credit Fees in Price for Mortgages with Special Attributes This Credit Fee in Price Matrix sets forth the Credit Fee in Price amounts and/or Credit Fee in Price rates

Rural Development. Connecting the Dots to Homeownership on Indian Reservations

Rural Development Connecting the Dots to Homeownership on Indian Reservations Business Programs Guaranteed Business and Industry Loans Loans/Grants for small businesses and value added products Community

Rural Development Connecting the Dots to Homeownership on Indian Reservations Business Programs Guaranteed Business and Industry Loans Loans/Grants for small businesses and value added products Community

NIFA Lender Workshop. North Platte, NE April 24, 2018 LaVista, NE April 25, 2018

NIFA Lender Workshop North Platte, NE April 24, 2018 LaVista, NE April 25, 2018 An important note about the seminar content While every effort has been made to ensure the reliability of the session content,

NIFA Lender Workshop North Platte, NE April 24, 2018 LaVista, NE April 25, 2018 An important note about the seminar content While every effort has been made to ensure the reliability of the session content,

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

DU 9.1 Revisions and Other Agency Enhancements

Bankruptcies Products (non AUS & DU) If a public record does not indicate a bankruptcy, but an individual tradeline does, the borrower must meet these bankruptcy guidelines. Generally, bankruptcies (except

Bankruptcies Products (non AUS & DU) If a public record does not indicate a bankruptcy, but an individual tradeline does, the borrower must meet these bankruptcy guidelines. Generally, bankruptcies (except

Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s

, this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s") Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s explorations into manufactured home mortgage data. This

Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s explorations into manufactured home mortgage data. This

Bulletin NUMBER: TO: Freddie Mac Sellers November 15, 2011

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Summary of Senate Banking Committee Leaders Bipartisan Housing Finance Reform Draft

Summary of Senate Banking Committee Leaders Bipartisan Housing Finance Reform Draft The housing market accounts for nearly 20 percent of the American economy, so it is critical that we have a strong and

Summary of Senate Banking Committee Leaders Bipartisan Housing Finance Reform Draft The housing market accounts for nearly 20 percent of the American economy, so it is critical that we have a strong and