Section 11.5 Buying a House with a Mortgage

|

|

|

- Pierce Winfred Holt

- 5 years ago

- Views:

Transcription

1 Section 11.5 Buying a House with a Mortgage A mortgage is a long term loan in which the property is pledged as security for payment of the difference between the down payment and the sale price. The down payment is the amount of cash the buyer must pay to the seller before the bank will grant the mortgage. The down payment varies depending on the lender. It can be as low as 5% when money is loose or easy to borrow, or as high as 25% when money is tight or difficult to borrow. Once the borrower meets the criteria for the mortgage the bank prepares a written agreement called the mortgage. The agreement states: a) repayment schedule b) duration of the loan c) whether the loan can be assumed by another party d) penalty if payments are late e) 50 more pages of mumbo jumbo

2 Two most popular types of mortgage loans: 1. Conventional Loan The interest rate is fixed for the duration of the loan. Advantage lower interest rates same payment for life of loan Disadvantage higher interest rate (rates could drop) 20% down payment 2. Adjustable Rate Loan (Variable Rate) The interest rate may change every period (1 5 years) Advantage/Disadvantage Lower rates than conventional loanrate but can be raised as much as 2% per year with a cap of 10% increase Short term buy

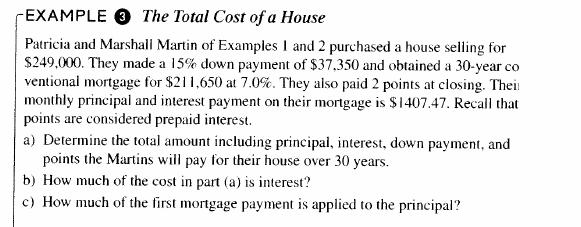

3 Down payments less than 20% requires the borrower to purchase Private Mortgage Insurance (PMI) until they have 20% equity in the house. The cost of PMI is usually 0.5% to 1% of the loan amount annually. Example: Loan of $100,000 Pay Points at closing (the final step in the buying process) a) 1 point = 1% of the loan(not the price of the house) prepaid interest and also lowers the interest rate. b) Reduces the monthly payment. c) If you don't pay Points, then the interest rate will be higher. d) You should only pay points if you plan on staying in the home for a long time. Closing Cost loans/mortgage purchase/closing costcalculator.go

4 Page 694

5 John Boy wishes to purchase a house selling for $425,000. He plans to obtain a loan from his mortgage company. The company requires a 20% down payment, payable to the seller, and a payment of 1.5 points, payable to the bank, at the time of closing. a) Determine John Boy's down payment. b) Determine the amount of John Boy's mortgage. c) Determine the cost of the 1.5 points paid by John Boy on his mortgage.

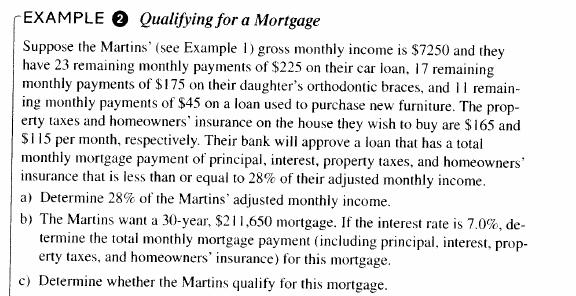

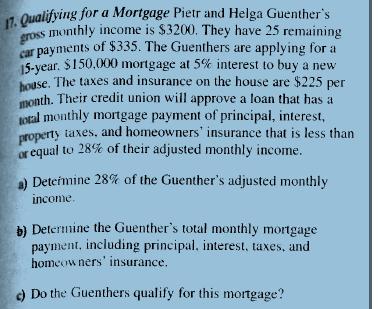

6 The banks uses a formula to determine the maximum monthly payment a purchaser can afford. Gross monthly income is the amount of money you make in a month before any taxes, social security, and retirement money is taken from you check. 1. Adjusted monthly income = gross monthly income minus any fixed monthly payments with more than 10 months remaining from your income. 2. Adjusted monthly income X 28% This amount must cover principal, interest, property tax, and insurance. Taxes and insurance are not necessarily paid by the bank.

7

8

9

10

11

12 Determine monthly payments calculator.aspx

13

14

15

16

17 Adjustable Rate Mortgages Generally, the ARM monthly payments remain the same for 1, 2, or 5 year period eve though the interest rate my change every 3 or 6 months. The interest rate is based on index that is determined by the Federal Home Loan Ban Association or on the Federal Treasury bill. The interest rate is determined by adding 3% to 3.5%, called the add on rate, to the rate of the Treasury bill.

18

19

20

21 FHA Mortgage (Federal Housing Authority) smaller down payment, as low as 3% loan is obtained through a bank, mortgage broker, or credit union but the FHA guarantees the loan against default by the borrower. this guarantee and small down payment makes it possible for some people who might not qualify for a conventional mortgage. allow buyer to have slightly higher monthly payments 29% of buyer's adjusted monthly income instead of 28% the money paid at the closing can be added on the amount of money being borrowed.

Section Buying a House with a Mortgage. Copyright 2013, 2010, 2007, Pearson, Education, Inc.

Section 11.5 Buying a House with a Mortgage What You Will Learn Homeowner s Mortgage Conventional Loans Adjustable-Rate Mortgages 2 Homeowner s Mortgage A homeowner s mortgage is a longterm loan in which

Section 11.5 Buying a House with a Mortgage What You Will Learn Homeowner s Mortgage Conventional Loans Adjustable-Rate Mortgages 2 Homeowner s Mortgage A homeowner s mortgage is a longterm loan in which

12-Step Home Mortgage Steps

1 You should review your credit report for any errors before submitting your mortgage application. Your credit report is used by banks and other lending institutions to determine your creditworthiness.

1 You should review your credit report for any errors before submitting your mortgage application. Your credit report is used by banks and other lending institutions to determine your creditworthiness.

MORTGAGE Sage By B & I Computer Consultants, Inc. ( 1

MORTGAGE Sage (Rent versus Buy Calculator) B & I Computer Consultants, Inc. www.bandisoftware.com (301) 537 4754 INTRODUCTION: Many people have asked whether they should buy a home or continue to rent?

MORTGAGE Sage (Rent versus Buy Calculator) B & I Computer Consultants, Inc. www.bandisoftware.com (301) 537 4754 INTRODUCTION: Many people have asked whether they should buy a home or continue to rent?

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

White Paper Choosing a Mortgage

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 Introduction...

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 Introduction...

Interest (monthly) = Principal x Rate x Time

= Principal x Rate x Time") Lesson 3: Mortgages In this lesson you will take a look at mortgages and the monthly payments they require. More detailed calculations will be examined in Lesson 4. While home ownership can be a rewarding

Lesson 3: Mortgages In this lesson you will take a look at mortgages and the monthly payments they require. More detailed calculations will be examined in Lesson 4. While home ownership can be a rewarding

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Chapter 15: Government Involvement in Real Estate Financing

Modern Real Estate Practice, 19 th Edition Chapter 15: Government Involvement in Real Estate Financing 1. Kahlid has been making periodic payments of principal and interest on a loan, but the final payment

Modern Real Estate Practice, 19 th Edition Chapter 15: Government Involvement in Real Estate Financing 1. Kahlid has been making periodic payments of principal and interest on a loan, but the final payment

document with your Loan Estimate. Transaction Information X Property Taxes NO X Homeowner's Insurance NO Other: details.

Closing Disclosure document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement Agent File # Property Sale Price BLANKTRID Transaction Information Borrower

Closing Disclosure document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement Agent File # Property Sale Price BLANKTRID Transaction Information Borrower

This chapter will describe the different classifications and types of loans, and the types of mortgages.

Principles of Real Estate Chapter 11-Loan Classifications This chapter will describe the different classifications and types of loans, and the types of mortgages. Overview Objectives At the end of this

Principles of Real Estate Chapter 11-Loan Classifications This chapter will describe the different classifications and types of loans, and the types of mortgages. Overview Objectives At the end of this

Sample Mortgage Banker

Sample Mortgage Banker What s included in Five Steps to Your New Home.............................. iii A review of the five worksheets provided for you to estimate your mortgage and home purchase eligibility

Sample Mortgage Banker What s included in Five Steps to Your New Home.............................. iii A review of the five worksheets provided for you to estimate your mortgage and home purchase eligibility

Section 2.02 The ARM Alternative

Section 2.02 The ARM Alternative In This Product Description This product description contains the following topics. Overview... 2 Product Summary... 2 Related Bulletins... 3 Features... 4 Options... 4

Section 2.02 The ARM Alternative In This Product Description This product description contains the following topics. Overview... 2 Product Summary... 2 Related Bulletins... 3 Features... 4 Options... 4

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1 SLIDE 1 COVER PAGE SLIDE 2 TOPICS In this section we will cover the following topics: I. Conventional mortgages II. III.

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1 SLIDE 1 COVER PAGE SLIDE 2 TOPICS In this section we will cover the following topics: I. Conventional mortgages II. III.

Mortgages. Amount of Mortgage: difference between sale price and the down payment.

Mortgages Mortgage: a long-term installment loan for the purpose of buying a home. If payments are not made on the loan, the lender may take possession of the property. Down Payment: A percentage of the

Mortgages Mortgage: a long-term installment loan for the purpose of buying a home. If payments are not made on the loan, the lender may take possession of the property. Down Payment: A percentage of the

REAL ESTATE DICTIONARY

Adjustable-rate mortgage (ARM) -- Home loan in which the interest rate is changed periodically based on a standard financial index. Most ARMs have caps on how much an interest rate may increase. Amortization

Adjustable-rate mortgage (ARM) -- Home loan in which the interest rate is changed periodically based on a standard financial index. Most ARMs have caps on how much an interest rate may increase. Amortization

Conventional loans are the most popular type of mortgages. They re not backed by the government and are ideal for buyers with good credit.

M O R T G A G E Buying your home is exciting. Whether you re purchasing or refinancing a home, Broadway Bank can help you find the loan that s right for you. Let our mortgage experts guide you through

M O R T G A G E Buying your home is exciting. Whether you re purchasing or refinancing a home, Broadway Bank can help you find the loan that s right for you. Let our mortgage experts guide you through

Overview of Types of Mortgages Available

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Broker. Financing Real Estate. Chapter 12. Copyright Gold Coast Schools 1

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

Loan Estimates. with the following requirements: Estimate SMF SMF SMF

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Closing Disclosure $ % $ $ $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Chapter 13 Multiple Choice Questions

Chapter 13 Multiple Choice Questions / Page 1 Chapter 13 Multiple Choice Questions 1. The primary difference between a secured and unsecured loan is a. whether or not the lender charges interest on the

Chapter 13 Multiple Choice Questions / Page 1 Chapter 13 Multiple Choice Questions 1. The primary difference between a secured and unsecured loan is a. whether or not the lender charges interest on the

UMB Mortgage Solutions. Home Buying 101

UMB Mortgage Solutions Home Buying 101 1 Agenda Are You Ready to Buy a Home? Selecting a Lender Mortgage Loans Getting Started Home Checklist Purchase Contract Questions 2 Home buying Terms Mortgage Lender

UMB Mortgage Solutions Home Buying 101 1 Agenda Are You Ready to Buy a Home? Selecting a Lender Mortgage Loans Getting Started Home Checklist Purchase Contract Questions 2 Home buying Terms Mortgage Lender

Home Buyer s Dictionary

ARM? GPM? PITI? You d have to be a cryptologist to figure out some of the terms you might encounter during the home buying process. Doing research on how to buy a house before beginning the process can

ARM? GPM? PITI? You d have to be a cryptologist to figure out some of the terms you might encounter during the home buying process. Doing research on how to buy a house before beginning the process can

Financing Residential Real Estate. Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

Printable Lesson Materials

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Loan Originator Compensation Guide

Loan Originator Compensation Guide Overview The Federal Reserve Board is implementing new rules on 4/6/2011 under Regulation Z of the Truth in Lending Act which governs compensation paid to loan originators

Loan Originator Compensation Guide Overview The Federal Reserve Board is implementing new rules on 4/6/2011 under Regulation Z of the Truth in Lending Act which governs compensation paid to loan originators

Sales Associate Course

Sales Associate Course Chapter Thirteen Types of Mortgages & Sources of Finance Copyright Gold Coast Schools 1 Types of Mortgages FHA - Federal Housing Administration VA - Veterans Administration Conventional

Sales Associate Course Chapter Thirteen Types of Mortgages & Sources of Finance Copyright Gold Coast Schools 1 Types of Mortgages FHA - Federal Housing Administration VA - Veterans Administration Conventional

Closing Disclosure. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

HOME BUYING MADE EASY. Know what you need to get it right.

HOME BUYING MADE EASY Know what you need to get it right. HOME BUYING MADE EASY PNC, PNC HomeHQ, PNC Home Insight and Home Insight are registered service marks of The PNC Financial Services Group, Inc.

HOME BUYING MADE EASY Know what you need to get it right. HOME BUYING MADE EASY PNC, PNC HomeHQ, PNC Home Insight and Home Insight are registered service marks of The PNC Financial Services Group, Inc.

Loan Comparison Report. Sample

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

A Place to Rent. 1/3 of people in the United States Single people, young married couples, and older adults Mobile lifestyles

Obtaining Housing A Place to Rent 1/3 of people in the United States Single people, young married couples, and older adults Mobile lifestyles Security Deposit A payment that ensures the owner against financial

Obtaining Housing A Place to Rent 1/3 of people in the United States Single people, young married couples, and older adults Mobile lifestyles Security Deposit A payment that ensures the owner against financial

Deseret First Credit Union Mortgage Team NMLS#

Deseret First Credit Union Mortgage Team NMLS# 403075 What we ll cover: The Process & Key People Finding the Right Property Your Budget Your Credit Pre-approval Your Mortgage Questions Finding your Home

Deseret First Credit Union Mortgage Team NMLS# 403075 What we ll cover: The Process & Key People Finding the Right Property Your Budget Your Credit Pre-approval Your Mortgage Questions Finding your Home

Closing Information Transaction Information Loan Information. VA Property Loan ID # Lender MIC # Sale Price $

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

REAL ESTATE TERMS Acceleration: Adjustable-Rate Mortgage (ARM): Adjusted Basis: Adjustment Date: Adjustment Interval: Adjustment Period:

: Adjusted Basis: Adjustment Date: Adjustment Interval: Adjustment Period:") REAL ESTATE TERMS A Acceleration: The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgager (borrower), or by using the right

REAL ESTATE TERMS A Acceleration: The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgager (borrower), or by using the right

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

HOME BUYING MADE EASY

HOME BUYING MADE EASY Know what you need to get it right. Brought to you by: PNC Mortgage Loan Officer NMLS# HOME BUYING MADE EASY PNC, PNC HomeHQ, PNC Home Insight

HOME BUYING MADE EASY Know what you need to get it right. Brought to you by: PNC Mortgage Loan Officer NMLS# HOME BUYING MADE EASY PNC, PNC HomeHQ, PNC Home Insight

Chapter Objectives. Chapter 8. Housing. How much housing can you afford? What are the rental prices in your area?

Chapter Objectives Chapter 8. Housing To determine how much you can afford to spend on housing To compare whether it is financially more attractive to buy or rent To explain the real estate transaction

Chapter Objectives Chapter 8. Housing To determine how much you can afford to spend on housing To compare whether it is financially more attractive to buy or rent To explain the real estate transaction

1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application.

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

Buyer s Packet. Prepared by John & Tracy Ingles The Ingles/Company Realtors

Buyer s Packet Prepared by John & Tracy Ingles The Ingles/Company Realtors 6711 Academy NE #B Albuquerque, NM 87109 Office # 828-1366 Cell # 269-3027/269-9903 1-800-766-2055 Dear Prospective Buyer: Attached

Buyer s Packet Prepared by John & Tracy Ingles The Ingles/Company Realtors 6711 Academy NE #B Albuquerque, NM 87109 Office # 828-1366 Cell # 269-3027/269-9903 1-800-766-2055 Dear Prospective Buyer: Attached

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

PPDocs, Inc. Compliance Certificate

PPDocs, Inc. Lender: Peirson & Patterson Borrower(s): Webinar Demo, a single man Property: 2310 W Interstate 20, Arlington, TX 76017 Loan Type: First Lien Fixed Rate Conventional Loan Loan Purpose: Purchase

PPDocs, Inc. Lender: Peirson & Patterson Borrower(s): Webinar Demo, a single man Property: 2310 W Interstate 20, Arlington, TX 76017 Loan Type: First Lien Fixed Rate Conventional Loan Loan Purpose: Purchase

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Printable Lesson Materials

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

CHAPTER TWO FINANCING

CHAPTER TWO FINANCING TABLE OF CONTENTS 1) NOTE MORTGAGE/TRUST DEED PAGE 2 2) ANALYSIS OF A NOTE PAGE 8 3) INTEREST/PAYMENT PLANS PAGE 10 4) PROVISIONS OF A MORTAGE/TRUST DEED PAGE 22 5) TYPES OF MORTGAGES/TRUST

CHAPTER TWO FINANCING TABLE OF CONTENTS 1) NOTE MORTGAGE/TRUST DEED PAGE 2 2) ANALYSIS OF A NOTE PAGE 8 3) INTEREST/PAYMENT PLANS PAGE 10 4) PROVISIONS OF A MORTAGE/TRUST DEED PAGE 22 5) TYPES OF MORTGAGES/TRUST

Dodd-Frank Rules Frequently Asked Questions Wholesale

Dodd-Frank Rules Frequently Asked Questions Wholesale Question 1. What is the effective date of the new requirements on the 3% 2. If the QM points and fees limit is 3%, then why is FCM capping broker compensation

Dodd-Frank Rules Frequently Asked Questions Wholesale Question 1. What is the effective date of the new requirements on the 3% 2. If the QM points and fees limit is 3%, then why is FCM capping broker compensation

Understanding Mortgages

Part 1: Your Loan s Interest Rate and APR Part 2: Your Decision to Pay or Not Pay Points Part 3: Your Loan s Prepayment Penalty A loan s interest rate and its APR (annual percentage rate) are not the same.

Part 1: Your Loan s Interest Rate and APR Part 2: Your Decision to Pay or Not Pay Points Part 3: Your Loan s Prepayment Penalty A loan s interest rate and its APR (annual percentage rate) are not the same.

Home Buying Workshop. Today s Workshop 2/22/2017. **Cash Rebate. Outline the services offered through the Real Estate Advantage Program

Home Buying Workshop Today s Workshop Outline the services offered through the Real Estate Advantage Program Step you through the home financing process Highlight key considerations in your decision to

Home Buying Workshop Today s Workshop Outline the services offered through the Real Estate Advantage Program Step you through the home financing process Highlight key considerations in your decision to

Practical Application. Pre-qualified - Buyer supplied information to the lender which is not verified and results in a rough estimate of price range.

Finance 1 Practical Application Pre-qualified - Buyer supplied information to the lender which is not verified and results in a rough estimate of price range. 2 Pre-approval - Includes an application and

Finance 1 Practical Application Pre-qualified - Buyer supplied information to the lender which is not verified and results in a rough estimate of price range. 2 Pre-approval - Includes an application and

CURRENT 30 YEAR FIXED MORTGAGE RATES - CHART AND TABLE

30 YEARS MORTGAGE RATE PDF CURRENT 30 YEAR FIXED MORTGAGE RATES - CHART AND TABLE 30-YEAR FIXED-RATE MORTGAGES SINCE 1971 - FREDDIE MAC 1 / 5 2 / 5 3 / 5 30 years mortgage rate pdf View and compare?urrent

30 YEARS MORTGAGE RATE PDF CURRENT 30 YEAR FIXED MORTGAGE RATES - CHART AND TABLE 30-YEAR FIXED-RATE MORTGAGES SINCE 1971 - FREDDIE MAC 1 / 5 2 / 5 3 / 5 30 years mortgage rate pdf View and compare?urrent

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Lending Practices. Loans. Early Payoff 6/18/2014. P & I per Year on the Amortizing Loan. Repaying a 6-year, $1,000 Loan

Loans Chapter 10 Lending Practices Term loan interest payments only until due Also called bullet loan or interest only loan. Amortized loan regular equal payments for life of loan including both principal

Loans Chapter 10 Lending Practices Term loan interest payments only until due Also called bullet loan or interest only loan. Amortized loan regular equal payments for life of loan including both principal

8 Bag of tricks? What s in a Loan officer s. Money talks but credit has an echo. -Bob Thaves

What s in a Loan officer s 8 Bag of tricks? chapter In the world of mortgage lending, there are many different types of loans and loan terms. How can you decide which loan best fits your financial circumstances?

What s in a Loan officer s 8 Bag of tricks? chapter In the world of mortgage lending, there are many different types of loans and loan terms. How can you decide which loan best fits your financial circumstances?

Manual Mortgage Payment Calculator With Taxes And Pmi And Insurance And Down

Manual Mortgage Payment Calculator With Taxes And Pmi And Insurance And Down Mortgage calculator with graphs, amortization tables, extra payments and PMI. FICO 760+, PMI FICO 720 759, PMI FICO 680 719,

Manual Mortgage Payment Calculator With Taxes And Pmi And Insurance And Down Mortgage calculator with graphs, amortization tables, extra payments and PMI. FICO 760+, PMI FICO 720 759, PMI FICO 680 719,

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

refinancing web page discussion.notebook January 14, 2016 Mortgage Options REFINANCING

Mortgage Options REFINANCING Define Refinancing Paying off one loan by obtaining another Generally done to secure better loan terms (Like a lower interest rate) Should You Refinance? Whether or not to

Mortgage Options REFINANCING Define Refinancing Paying off one loan by obtaining another Generally done to secure better loan terms (Like a lower interest rate) Should You Refinance? Whether or not to

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS. Mortgage Planner Marketing

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS Mortgage Planner Marketing Qualified & Formal Approval Becoming qualified is the first step. This means having your debt ratios and credit report

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS Mortgage Planner Marketing Qualified & Formal Approval Becoming qualified is the first step. This means having your debt ratios and credit report

Today s Rates Looking for the best mortgage loan rate

Today s Rates Looking for the best mortgage loan rate by Natalie Danielson www.clockhours.com A Washington State Approved Real Estate School under R.C.W. 18.85. Sponsor S 1353 Today's Rates Looking for

Today s Rates Looking for the best mortgage loan rate by Natalie Danielson www.clockhours.com A Washington State Approved Real Estate School under R.C.W. 18.85. Sponsor S 1353 Today's Rates Looking for

LESSON 8 -- BUYING A HOME

LESSON 8 -- BUYING A HOME LESSON DESCRIPTION AND BACKGROUND This lesson uses the Better Money Habits video Is Buying a Home Right for You? (www.bettermoneyhabits.com) to help students compare the costs

LESSON 8 -- BUYING A HOME LESSON DESCRIPTION AND BACKGROUND This lesson uses the Better Money Habits video Is Buying a Home Right for You? (www.bettermoneyhabits.com) to help students compare the costs

PERSONALIZED SERVICE. EXPERT GUIDANCE.

PERSONALIZED SERVICE. EXPERT GUIDANCE. BANK OF AMERICA HOME FINANCING SOLUTIONS Financing a home can impact you personally as much as it does financially. Building roots, supporting family, or securing

PERSONALIZED SERVICE. EXPERT GUIDANCE. BANK OF AMERICA HOME FINANCING SOLUTIONS Financing a home can impact you personally as much as it does financially. Building roots, supporting family, or securing

Congratulations, you have made the big decision to buy a home. Now what? There are many questions you will need to ask yourself before moving ahead:

Buyers Congratulations, you have made the big decision to buy a home. Now what? There are many questions you will need to ask yourself before moving ahead: BEFORE YOU BUY 1. Decide where you want to live.

Buyers Congratulations, you have made the big decision to buy a home. Now what? There are many questions you will need to ask yourself before moving ahead: BEFORE YOU BUY 1. Decide where you want to live.

* PFC = Prepaid Finance Charge Total Loan Amount $ 175,000 Interest Rate: % Term/Due In: 360 / 360 mths

GOOD FAITH ESTIMATE Applicants: John / Jane Application No: borrowerj Property Addr: 1234 TBD Street, Price, UT 84501 Date Prepared: 09/25/2009 Prepared By: Republic Mortgage Home Loans, LLC Ph. 801-426-5500

GOOD FAITH ESTIMATE Applicants: John / Jane Application No: borrowerj Property Addr: 1234 TBD Street, Price, UT 84501 Date Prepared: 09/25/2009 Prepared By: Republic Mortgage Home Loans, LLC Ph. 801-426-5500

Glossary of Real Estate Terms

Glossary of Real Estate Terms Abstract of Title: A summary of the public records relating to the ownership of a particular piece of land. It represents a short legal history of an individual piece of property

Glossary of Real Estate Terms Abstract of Title: A summary of the public records relating to the ownership of a particular piece of land. It represents a short legal history of an individual piece of property

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage Buying your first home is both exhilarating and overwhelming. Stay on top of it all with this step-by-step guide on what to expect

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage Buying your first home is both exhilarating and overwhelming. Stay on top of it all with this step-by-step guide on what to expect

arrears credit debit level payment plan

Section 14 Part 1 SLIDE 1 Real Estate Computations and Closing (Cover Page) SLIDE 2 TOPICS In this section we will cover the following topics: I. Basic Real Estate Computations II. III. IV. Preliminary

Section 14 Part 1 SLIDE 1 Real Estate Computations and Closing (Cover Page) SLIDE 2 TOPICS In this section we will cover the following topics: I. Basic Real Estate Computations II. III. IV. Preliminary

2019 HOME BUYER'S HOW TO PREPARE FOR THE HOME OF YOUR DREAMS AMIT DARJI NJ REALTOR LONG AND FOSTER REAL ESTATE

2019 HOME BUYER'S BIGGEST FEARS HOW TO PREPARE FOR THE HOME OF YOUR DREAMS AMIT DARJI NJ REALTOR LONG AND FOSTER REAL ESTATE Table of Contents Introduction...Page 3 What Can You Really Afford? - Budget...Page

2019 HOME BUYER'S BIGGEST FEARS HOW TO PREPARE FOR THE HOME OF YOUR DREAMS AMIT DARJI NJ REALTOR LONG AND FOSTER REAL ESTATE Table of Contents Introduction...Page 3 What Can You Really Afford? - Budget...Page

FINANCING THE LOAN/MORTGAGE SEQUENCE

THE LOAN/MORTGAGE SEQUENCE FINANCING 1. Buyer applies to lender - Savings Associations, Mutual Savings Banks, Cooperative Banks, Commercial Banks (the Thrifts); Mortgage Companies, Credit Unions, Life

THE LOAN/MORTGAGE SEQUENCE FINANCING 1. Buyer applies to lender - Savings Associations, Mutual Savings Banks, Cooperative Banks, Commercial Banks (the Thrifts); Mortgage Companies, Credit Unions, Life

Loan Originator Compensation and Steering Prohibitions. Branch Originations March 2011

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

CALIFORNIA INTERACTIVE STUDY GROUP UNIT 5: BOBRA TAHAN HOWARD HARRIS FINANCING

CALIFORNIA INTERACTIVE STUDY GROUP 1 UNIT 5: BOBRA TAHAN HOWARD HARRIS FINANCING Study Group Information 2 Information regarding the Study Group may be found at: www.kapre.com/caisg At this location you

CALIFORNIA INTERACTIVE STUDY GROUP 1 UNIT 5: BOBRA TAHAN HOWARD HARRIS FINANCING Study Group Information 2 Information regarding the Study Group may be found at: www.kapre.com/caisg At this location you

TILA RESPA Integrated Disclosure (TRID) Closing Disclosure Instructions Page 1 LHFSCorrespondent.com (972)

Closing Disclosure Instructions Page 1 LHFSCorrespondent.com (972)") Page 1 The date this disclosure is delivered to the consumer. The date of consummation. The date when the loan amount will be paid, either to the consumer and seller for purchase loans, or to the consumer

Page 1 The date this disclosure is delivered to the consumer. The date of consummation. The date when the loan amount will be paid, either to the consumer and seller for purchase loans, or to the consumer

Legal Description of Subject Property (attach description if necessary) (a) Present Value of Lot

(a) Present Value of Lot") This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY Mortgage Credit Certificate Program (HFA: 328) Table of Contents

Table of Contents") NEW HAMPSHIRE HOUSING FINANCE AUTHORITY Mortgage Credit Certificate Program () Table of Contents PART ONE: Overview, Purpose and Applicability 328.01 - Overview and Purpose 328.02 - Applicability and Additional

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY Mortgage Credit Certificate Program () Table of Contents PART ONE: Overview, Purpose and Applicability 328.01 - Overview and Purpose 328.02 - Applicability and Additional

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

20 Hour SAFE Comprehensive: Financing Residential Real Estate

20 Hour SAFE Comprehensive: Financing Residential Real Estate COURSE MANUAL Days 1-4 Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director 9/16 NMLS Rules of Conduct for Students (ROC) Day 1 Real

20 Hour SAFE Comprehensive: Financing Residential Real Estate COURSE MANUAL Days 1-4 Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director 9/16 NMLS Rules of Conduct for Students (ROC) Day 1 Real

PLACER TITLE RATE QUOTE+ USER MANUAL

PLACER TITLE RATE QUOTE+ USER MANUAL Congratulations on downloading the Placer Title Rate Quote + app. Please take a few moments to review the User Manual that will be useful in registering, setting up

PLACER TITLE RATE QUOTE+ USER MANUAL Congratulations on downloading the Placer Title Rate Quote + app. Please take a few moments to review the User Manual that will be useful in registering, setting up

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Mortgage. A Beginner s. Rates. Guide

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Transaction Information. Tennessee Housing Development Agency

Tennessee Housing Development Agency Second Mortgage Loan This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Disclosure Closing Information

Tennessee Housing Development Agency Second Mortgage Loan This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Disclosure Closing Information

ICON 1003 Loan Application

ICON 1003 Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

ICON 1003 Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

Chapter 4 Summary Real Estate Financing Principles: Real Estate Finance 1

The money to finance loans comes from a number of sources. The primary mortgage market is made up of lenders who originate loans. They make the money available directly to borrowers. The primary mortgage

The money to finance loans comes from a number of sources. The primary mortgage market is made up of lenders who originate loans. They make the money available directly to borrowers. The primary mortgage

Understanding Consumer and Mortgage Loans

Personal Finance: Another Perspective Understanding Consumer and Mortgage Loans Updated 2017-02-07 Note: Graphs on this presentation are from http://www.bankrate.com/funnel/graph/default.aspx? Copied on

Personal Finance: Another Perspective Understanding Consumer and Mortgage Loans Updated 2017-02-07 Note: Graphs on this presentation are from http://www.bankrate.com/funnel/graph/default.aspx? Copied on

2017 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.

Real Estate... getting involved 2017 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License. Nominal Justification..

Real Estate... getting involved 2017 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License. Nominal Justification..

Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Mortgage terminology.

Mortgage terminology. Adjustable Rate Mortgage (ARM). A mortgage on which the interest rate, after an initial period, can be changed by the lender. While ARMs in many countries abroad allow rate changes

Mortgage terminology. Adjustable Rate Mortgage (ARM). A mortgage on which the interest rate, after an initial period, can be changed by the lender. While ARMs in many countries abroad allow rate changes

COBB COUNTY HOME PROGRAM RESALE/RECAPTURE PROVISIONS Revised 12/15/2015

I. BACKGROUND COBB COUNTY HOME PROGRAM RESALE/RECAPTURE PROVISIONS Revised 12/15/2015 Section 215 of the HOME statute establishes specific requirements that all HOME-assisted homebuyer housing must meet

I. BACKGROUND COBB COUNTY HOME PROGRAM RESALE/RECAPTURE PROVISIONS Revised 12/15/2015 Section 215 of the HOME statute establishes specific requirements that all HOME-assisted homebuyer housing must meet

Loan Estimate $ NO. Loan Terms. Loan Amount $ NO. Interest Rate 1.75% NO

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Uniform Residential Loan Application

First Name: Mortgage Pre-Qualification Application Last Name: Mortgage Pre Qual Application NMLS# 799643 Privacy Policy: Our privacy policy protects the privacy of your personal-identifying information

First Name: Mortgage Pre-Qualification Application Last Name: Mortgage Pre Qual Application NMLS# 799643 Privacy Policy: Our privacy policy protects the privacy of your personal-identifying information

Niche Loan Programs. Featured Loan. Zero Down Loan

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Teacher's Guide. Lesson Five. Buying a Home 04/09

Teacher's Guide $ Lesson Five Buying a Home 04/09 buying a home websites Buying a Home is a major life milestone that requires some thoughtful planning and know-how. Students need to understand all aspects

Teacher's Guide $ Lesson Five Buying a Home 04/09 buying a home websites Buying a Home is a major life milestone that requires some thoughtful planning and know-how. Students need to understand all aspects

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Closing Disclosure $0 NO. $0 a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Mortgage Glossary. Common terms used in the mortgage process

Adjustable-Rate Mortgage (ARM): Interest rates on adjustable rate mortgages can go up or down causing your mortgage payment to adjust accordingly. The interest rate is usually set for a specific period

Adjustable-Rate Mortgage (ARM): Interest rates on adjustable rate mortgages can go up or down causing your mortgage payment to adjust accordingly. The interest rate is usually set for a specific period

Lifetime Mortgage. Advantages You benefit from any future house price inflation.

Lifetime Mortgage What is it? Lifetime mortgages are one of the two main types of equity release. The other is a home reversion plan. A lifetime mortgage is a long term loan where you borrow money secured

Lifetime Mortgage What is it? Lifetime mortgages are one of the two main types of equity release. The other is a home reversion plan. A lifetime mortgage is a long term loan where you borrow money secured

A Complete Guide to Help You Buy, Build or Refinance Your Home myhonorbank.com

Homebuyer s Guide A Complete Guide to Help You Buy, Build or Refinance Your Home myhonorbank.com 877.325.8031 Mortgage Programs With every season, there is a time to reflect on your stage in life and your

Homebuyer s Guide A Complete Guide to Help You Buy, Build or Refinance Your Home myhonorbank.com 877.325.8031 Mortgage Programs With every season, there is a time to reflect on your stage in life and your

Closing Disclosure. This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate.

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information must also be provided (and

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information must also be provided (and