Module 3: Debt Lesson Part 1

|

|

|

- Madeleine McGee

- 5 years ago

- Views:

Transcription

1

2 Module 3: Debt Lesson Part 1

3 Module 3: Debt Lesson Part 1 The Debt Stuff No One is Talking About

4 The Lesson Blueprint What is Debt? Type of Debt Credit Scores

5 What is Debt? Debt is ANYTHING you owe to Someone Else Credit Cards Student Loans Car Payments Medical Bills IRS Payday Loans Family Member Collections

6 Secured Debt? Utilizes a Form of Collateral Your Car Your Boat Your RV Your House Your Dog? Think REPO Man

7 Unsecured Debt? Does NOT have Collateral Stuff you bought on your Credit Card Student Loans Income Taxes Telephone/Utility Bills Personal Loans Most Debt falls under Unsecured Debt

8 Fixed Rate Debt? Same Interest Rate for Life of Loan Your Mortgage (15 year FIXED) Car Loans Federally Backed Student Loans Some Privately Held Student Loans

9 Variable Rate Debt? The Interest Can Change or is Scheduled to Change Adjusts as Market Rates Change Credit Cards Variable Rate Mortgages (ARMs) Some Privately Held Student Loans Usually Starts off with an Introductory Offer to tease you!

10 Fixed vs Variable Terms When the Loan is Scheduled to be Paid Off Fixed The Loan Pay Off Date is Already Determined Mortgage Car Loan Auto Lease Student Loan Variable The Payment Term is left Open (No End Date) Forever Debt Credit Cards

11 Credit Card Debt Unsecured Debt END of you Budget These can be negotiated

12 Credit Card Debt You Need a Credit Card to. Rent a Car Purchase Online Travel This is Just Plain Wrong

13 Credit Card Debt Debit Cards Just Aren t Safe

14 Credit Card Points The Credit Card Company is Smarter than You Nothing is Ever Free Who s Building is Bigger? If you Carry Credit Card Debt, Cut Up the Cards If you Don t Carry Credit Card Debt, Cut Up the Cards

15 Medical Debt Unsecured Debt END of you Budget These can be negotiated

16 Student Loans You HAVE to Pay These Don t Go Away After Bankruptcy Exceptions to the Rule Brunner Test Difficult Disability

17 Predatory Lenders Cash Advance Payday Lenders Title Loans Rent to Own

18 Predatory Lenders Predominantly Found in Lower Income Areas of Town Average Payday Lender Charges 400% Interest - Centers for Responsible Lending Illegal in Some States Interest Rate Caps In Some States Bottom Line: Stay Far Away

19 Zero Percent Interest There is no such thing Why Would a Bank want to Lend you Money for Free? They Don t Want to and They Never Do

20 Car Debt New Cars Leased Cars

21 New Cars New Cars lose 60% - 70% in the first 4 years! Most of it in the Very First Year Average Car Payment is $503 over 68 Months USA TODAY 2016 Average New Car Sold in 2016 = $33,560 Four Years Later. $12,000

22 New Cars Average Profit for Car Sold: $111 new cars are essentially a loss leader for dealers, who make most of their money by fixing your car, selling you a warranty when you buy a new car, financing car loans, and used car sales -Huffington Post

23 Leased Cars The Most Expensive Way to Operate a Vehicle You are Covering the Depreciation of the Vehicle Example: You Lease a Brand New $30,000 Car You turn it in after 36 Months & Car is Worth Only $14,000

24 Leased Cars You Covered the Depreciation for the Dealer at $444/month You Provided the Profit with Down Payment and the $0.10/mile that you went over

25 Leased Cars But I get to write off my Lease You are creating an unnecessary business expense just for the write off

26 Leased Cars If you paid $444/month ($5,328/yr) for the Lease, you could write off that amount off to save $1,332 You paid the Dealership $5,333 to avoid sending $1,332 to the Government And Your Car Dropped in Value Like a Rock

27 Credit Score

28

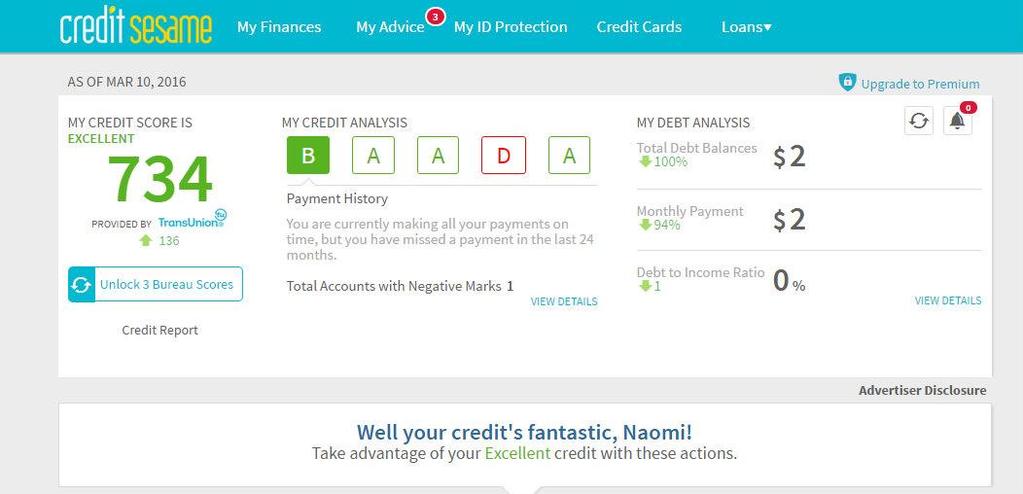

29 awesomemoneycourse.com/creditsesame

30 But First Good to know Credit Score? YES!!! Better to have ZERO Debt than High Credit Score? YES!!! Checking you Credit Report? (Module 4)

31 Rookie Mistakes You Continue to Believe the Lies about Debt Your Broke Friend Tells You What You Want to Hear You Make Yourself the Exception

32 Wrapping Up Debt is Everywhere Arm Yourself with Knowledge We are Changing Our Behavior You Can Live Without Debt and Survive

33 In the Next Module The Steps to Paying Off Debt I Don t Have the Money to Pay Them Getting out of your Car Payment Collection Bullies

34

Module 4: Debt Lesson Part 2

Module 4: Debt Lesson Part 2 Module 4: Debt Lesson Part 2 Getting Rid of Your Debt Forever The Lesson Blueprint Where do I Start First? What Tools Can I Use? Rookie Mistakes Where Do I Start? Debt Snowball

Module 4: Debt Lesson Part 2 Module 4: Debt Lesson Part 2 Getting Rid of Your Debt Forever The Lesson Blueprint Where do I Start First? What Tools Can I Use? Rookie Mistakes Where Do I Start? Debt Snowball

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

Chapter 4 Debt. Section Credit misdirection

Chapter 4 Debt Section 2 2.1 Credit misdirection Credit Misdirection Lending money to friends or family members is a bad idea. It will strain relationships and in some cases ruin friendships. If you have

Chapter 4 Debt Section 2 2.1 Credit misdirection Credit Misdirection Lending money to friends or family members is a bad idea. It will strain relationships and in some cases ruin friendships. If you have

What is your credit score? A community empowerment program brought to you by MasterCard

What is your credit score? A community empowerment program brought to you by MasterCard Understand what a credit score is so you can make sure you re making smart decisions right from the start. 2 Master

What is your credit score? A community empowerment program brought to you by MasterCard Understand what a credit score is so you can make sure you re making smart decisions right from the start. 2 Master

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Work with a partner. All these words are connected to getting a mortgage. Do you know their meaning?

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

PERSONAL FINANCE FINAL EXAM REVIEW. Click here to begin

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Money Smart - A Financial Education Program

Money Smart - A Financial Education Program The Money Smart Training Program Money Smart for Youth Modules Bank On It By the end of this course, participants will understand Available banking services

Money Smart - A Financial Education Program The Money Smart Training Program Money Smart for Youth Modules Bank On It By the end of this course, participants will understand Available banking services

Student Loans And Credit: An Overview Tanya Tanaro, Manager Higher Education Partnerships, ASA

Student Loans And Credit: An Overview 12.14.15 Tanya Tanaro, Manager Higher Education Partnerships, ASA Agenda 2 Borrowing realities Credit reports and scores Student loan and credit card impact Conversation

Student Loans And Credit: An Overview 12.14.15 Tanya Tanaro, Manager Higher Education Partnerships, ASA Agenda 2 Borrowing realities Credit reports and scores Student loan and credit card impact Conversation

Chapter 27. Your Credit and the Law pp

Your Credit and the Law pp. 434-447 Learning Objectives After completing this chapter, you ll be able to: 1. Explain how government protects credit rights. 2. Name federal laws that protect consumers.

Your Credit and the Law pp. 434-447 Learning Objectives After completing this chapter, you ll be able to: 1. Explain how government protects credit rights. 2. Name federal laws that protect consumers.

Borrowing. Evaluating the Benefits and Costs of Credit

Unit 9 Borrowing Lesson 9B: Evaluating the Benefits and Costs of Credit Rule 9: Pay on time and in full. While borrowing has both benefits and costs, at times it is an indication that something has gone

Unit 9 Borrowing Lesson 9B: Evaluating the Benefits and Costs of Credit Rule 9: Pay on time and in full. While borrowing has both benefits and costs, at times it is an indication that something has gone

Credit and Going into Debt A. What is credit?

Lesson 4 standards E.6.1 Explain the basic functions of money. E.6.2 Identify the composition of the money supply of the United States. E.6.3 Explain the roles of financial institutions. E.6.6 Explain

Lesson 4 standards E.6.1 Explain the basic functions of money. E.6.2 Identify the composition of the money supply of the United States. E.6.3 Explain the roles of financial institutions. E.6.6 Explain

Credit Guide. An introduction to credit and how it s used in your financial plan. Educators Credit Union. Shopper. Buyer. Planner. Spender.

Educators Credit Union Credit Guide An introduction to credit and how it s used in your financial plan. Shopper. Buyer. Planner. Spender. For the teacher in you. 262.886.5900 ecu.com Table of contents

Educators Credit Union Credit Guide An introduction to credit and how it s used in your financial plan. Shopper. Buyer. Planner. Spender. For the teacher in you. 262.886.5900 ecu.com Table of contents

Understanding Debt Problems & Solutions

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

The Easy Picture Guide to Insurance for People Living Independently. Your Money Your Insurance

for People Living Independently Your Money Your Insurance 2 This guide is all about insurance. Insurance is something you buy to make sure if something goes wrong, you will get money to put things right.

for People Living Independently Your Money Your Insurance 2 This guide is all about insurance. Insurance is something you buy to make sure if something goes wrong, you will get money to put things right.

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Lending with a Purpose

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

What is credit and why does it matter to me?

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Charge It Right 2

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Building a strong credit history. A public education campaign brought to you by MasterCard

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Justine PETERSEN Building Assets. Changing Lives. Credit Report Basics and Definitions Justine PETERSEN Credit Building Training

Justine PETERSEN Building Assets. Changing Lives Credit Report Basics and Definitions Justine PETERSEN Credit Building Training Included Topics Who reports to the credit bureaus Statute of Limitations

Justine PETERSEN Building Assets. Changing Lives Credit Report Basics and Definitions Justine PETERSEN Credit Building Training Included Topics Who reports to the credit bureaus Statute of Limitations

Making cards work for you. A public education campaign brought to you by MasterCard

Making cards work for you A public education campaign brought to you by MasterCard At school or work paying bills, renting an apartment or shopping for a new car, you need to know how cards save you money

Making cards work for you A public education campaign brought to you by MasterCard At school or work paying bills, renting an apartment or shopping for a new car, you need to know how cards save you money

By JW Warr

By JW Warr 1 WWW@AmericanNoteWarehouse.com JW@JWarr.com 512-308-3869 Have you ever found out something you already knew? For instance; what color is a YIELD sign? Most people will answer yellow. Well,

By JW Warr 1 WWW@AmericanNoteWarehouse.com JW@JWarr.com 512-308-3869 Have you ever found out something you already knew? For instance; what color is a YIELD sign? Most people will answer yellow. Well,

HOW TO BUY A CAR WITH BAD CREDIT

Your credit score is not the only way to prove your credit worthiness. It does do a good job of indicating what type of credit customer you might be; however, today the credit system is being used to exploit

Your credit score is not the only way to prove your credit worthiness. It does do a good job of indicating what type of credit customer you might be; however, today the credit system is being used to exploit

What you need to know about getting, using and keeping credit. A Guide to Credit* American Financial Services Association Education Foundation

A Guide to Credit* What you need to know about getting, American Financial Services Association Education Foundation www.afsaef.org www.gmacfs.com using and keeping credit *If you would like to receive

A Guide to Credit* What you need to know about getting, American Financial Services Association Education Foundation www.afsaef.org www.gmacfs.com using and keeping credit *If you would like to receive

Being a Guarantor. This booklet will help you understand all that is involved in being a Guarantor.

is a big responsibility and can have serious consequences. It is important to understand exactly what you are getting yourself into and what the impact of signing the agreement may be. can be a helpful

is a big responsibility and can have serious consequences. It is important to understand exactly what you are getting yourself into and what the impact of signing the agreement may be. can be a helpful

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

DEBTS AND DISPUTES. Understanding Debt. What to do?

DEBTS AND DISPUTES If you ve ever been owed money, you know it s a frustrating situation to be in. Even when it s a small sum, debts not only leave a bad taste, but they can really affect your financial

DEBTS AND DISPUTES If you ve ever been owed money, you know it s a frustrating situation to be in. Even when it s a small sum, debts not only leave a bad taste, but they can really affect your financial

Managing Your Finances

1 Presentation Notes: Part 1 Slide 1 Part I Planning for Financial Stability A seven step plan for a secure future Financial stability does not just happen. It takes a plan. We all want to have money when

1 Presentation Notes: Part 1 Slide 1 Part I Planning for Financial Stability A seven step plan for a secure future Financial stability does not just happen. It takes a plan. We all want to have money when

III MoneyWise Workshop Financial Freedom: Living Beneath Your Means

Personal Finance Essentials: 8 Financial Priorities III MoneyWise Workshop Financial Freedom: Living Beneath Your Means Module 2 Discussion Topics 1. Perspectives: Behavior versus money 2. Income: Maximize

Personal Finance Essentials: 8 Financial Priorities III MoneyWise Workshop Financial Freedom: Living Beneath Your Means Module 2 Discussion Topics 1. Perspectives: Behavior versus money 2. Income: Maximize

with the support of Everyday Banking An easy read guide March 2018

with the support of Everyday Banking An easy read guide March 2018 Who is this guide for? This guide has been designed to help anyone who might need more information about everyday banking. We will cover

with the support of Everyday Banking An easy read guide March 2018 Who is this guide for? This guide has been designed to help anyone who might need more information about everyday banking. We will cover

Keeping Score: Why Credit Matters

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Managing Financial Risks

Managing Financial Risks Standard 5 The student will analyze the costs and benefits of saving and investing. Lesson Objectives Discuss the role of risk when saving and investing Personal Financial Literacy

Managing Financial Risks Standard 5 The student will analyze the costs and benefits of saving and investing. Lesson Objectives Discuss the role of risk when saving and investing Personal Financial Literacy

12 Steps to Improved Credit Steven K. Shapiro

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

Banking Basics. Banks and Credit Unions. Warm-Up Activity. Why should you put your money in a bank?

Account Management Account Management You will be introduced to the banking process. You will learn how to locate a bank or credit union with which you want to do business, what accounts you should have

Account Management Account Management You will be introduced to the banking process. You will learn how to locate a bank or credit union with which you want to do business, what accounts you should have

Secured and Unsecured (1)

") LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

Debt Literacy, Financial Experiences and Overindebtedness

Presentation to the World Bank Conference on Measurement, Promotion and Impact of Access to Financial Services Debt Literacy, Financial Experiences and Overindebtedness March 12, 2009 Annamaria Lusardi

Presentation to the World Bank Conference on Measurement, Promotion and Impact of Access to Financial Services Debt Literacy, Financial Experiences and Overindebtedness March 12, 2009 Annamaria Lusardi

Product Guide. What is the Platinum Discount Network? FIVE STAR PASS. TheCreditPros Services. Advantages: Selling Platinum Discount Network

Product Guide What is the Platinum Discount Network? The Platinum Discount Network is an exclusive member s only savings program that offers discounts on travel, retail, dining, personal services, free

Product Guide What is the Platinum Discount Network? The Platinum Discount Network is an exclusive member s only savings program that offers discounts on travel, retail, dining, personal services, free

Name Period. Finance charge Loan term Grace period Late fee Cash Advance Fee Prepayment Penalty Origination Fee Amortization Collateral Capital

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

2. To earn as much interest as possible, you should open a savings account that earns () interest Hide answers

interest Hide answers") 1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

MODULE 7: Borrowing Basics PARTICIPANT GUIDE

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

How to be Successful With Higher-Risk Auto Lending

How to be Successful With Higher-Risk Auto Lending Heartland Credit Union Association Annual Convention Overland Park, KS October 6, 2017 By Brett Christensen, Owner CU Lending Advice, LLC brett@culendingadvice.com

How to be Successful With Higher-Risk Auto Lending Heartland Credit Union Association Annual Convention Overland Park, KS October 6, 2017 By Brett Christensen, Owner CU Lending Advice, LLC brett@culendingadvice.com

Homebuyer Education TEST

To obtain the required Homebuyer Education Certificate through the Ohio Housing Finance Agency (OHFA), you will need to complete this test and related budget form. Once your loan is reserved, you may upload

To obtain the required Homebuyer Education Certificate through the Ohio Housing Finance Agency (OHFA), you will need to complete this test and related budget form. Once your loan is reserved, you may upload

Lesson 5: Credit and Debt

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

MODULE 7: Borrowing Basics INSTRUCTOR GUIDE. MONEY SMART for Adults

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

Fannie Mae National Housing Survey. July - September 2010 Quarterly Wave

Fannie Mae National Housing Survey July - ember 2010 Quarterly Wave Copyright 2010 by Fannie Mae Release Date: November 23, 2010 Consumer attitudes: measure current and track change Attitudinal Questions

Fannie Mae National Housing Survey July - ember 2010 Quarterly Wave Copyright 2010 by Fannie Mae Release Date: November 23, 2010 Consumer attitudes: measure current and track change Attitudinal Questions

Workbook 3. Borrowing Money

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Money Management Curriculum

Module 2: Loans and Credit Cards Money Management Curriculum Module 2: Loans and Credit Cards Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension,

Module 2: Loans and Credit Cards Money Management Curriculum Module 2: Loans and Credit Cards Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension,

Toolkit 2 Borrowing Wisely

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Students will: Explain the importance of financial literacy. Explain the importance of taking responsibility for personal financial decisions.

Cars, Cards and Currency Lesson 1: Keep the Currency Lesson Description Students participate in a discussion of the general features of a $1 bill. They learn that although currency is valued, people often

Cars, Cards and Currency Lesson 1: Keep the Currency Lesson Description Students participate in a discussion of the general features of a $1 bill. They learn that although currency is valued, people often

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+ MODULE 4 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+ MODULE 4 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management

CARDMEMBER AGREEMENT RATES AND FEES TABLE INTEREST RATES AND INTEREST CHARGES FEES

Purchase Annual Percentage Rate (APR) Balance Transfer APR Cash Advance APR Paying Interest Minimum Interest Charge Credit Card Tips from the Consumer Financial Protection Bureau CARDMEMBER AGREEMENT RATES

Purchase Annual Percentage Rate (APR) Balance Transfer APR Cash Advance APR Paying Interest Minimum Interest Charge Credit Card Tips from the Consumer Financial Protection Bureau CARDMEMBER AGREEMENT RATES

FINANCIAL FOUNDATIONS

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Module Four: Building Financial Foundations Homes, Loans and Automobiles

Financial Empowerment Curriculum Moving Ahead Through Financial Management Module Four: Building Financial Foundations Homes, Loans and Automobiles 1 Financial Empowerment Curriculum Module Five: Creating

Financial Empowerment Curriculum Moving Ahead Through Financial Management Module Four: Building Financial Foundations Homes, Loans and Automobiles 1 Financial Empowerment Curriculum Module Five: Creating

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Unit 8 - Math Review. Section 8: Real Estate Math Review. Reading Assignments (please note which version of the text you are using)

") Unit 8 - Math Review Unit Outline Using a Simple Calculator Math Refresher Fractions, Decimals, and Percentages Percentage Problems Commission Problems Loan Problems Straight-Line Appreciation/Depreciation

Unit 8 - Math Review Unit Outline Using a Simple Calculator Math Refresher Fractions, Decimals, and Percentages Percentage Problems Commission Problems Loan Problems Straight-Line Appreciation/Depreciation

Math 5.1: Mathematical process standards

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

3. How to Use Credit

3. How to Use Credit Did you know? Wealth and Income Wealth is what you own minus your debts (financial assets minus liabilities). It is the money you have saved and the property you own (for example,

3. How to Use Credit Did you know? Wealth and Income Wealth is what you own minus your debts (financial assets minus liabilities). It is the money you have saved and the property you own (for example,

2017 BUSINESS & TAX CONSULTANTS, INC.

2017 BUSINESS & TAX CONSULTANTS, INC. Questionnaire 2017 Please check the appropriate box and include all necessary details When in doubt, please check the Not Sure box so that we can discuss the issue

2017 BUSINESS & TAX CONSULTANTS, INC. Questionnaire 2017 Please check the appropriate box and include all necessary details When in doubt, please check the Not Sure box so that we can discuss the issue

PROTECTING YOUR ASSETS

PROTECTING YOUR ASSETS Always encourage your students to take notes. Also, remember to leave yourself 5 minutes before the end of class to go over the post-test and collect them! Making a connection to

PROTECTING YOUR ASSETS Always encourage your students to take notes. Also, remember to leave yourself 5 minutes before the end of class to go over the post-test and collect them! Making a connection to

Standard 5: The student will analyze the costs and benefits of saving and investing.

STUDENT MODULE 5.2 SAVING AND INVESTING PAGE 1 Standard 5: The student will analyze the costs and benefits of saving and investing. The Rule of 72 Micah bought his car, and is now saving for a new speaker

STUDENT MODULE 5.2 SAVING AND INVESTING PAGE 1 Standard 5: The student will analyze the costs and benefits of saving and investing. The Rule of 72 Micah bought his car, and is now saving for a new speaker

Borrowing Basics. FDIC Money Smart for Young Adults. Building: Knowledge, Security, Confidence

Borrowing Basics FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Define credit Explain why credit is important Identify three types of loans Identify the costs associated

Borrowing Basics FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Define credit Explain why credit is important Identify three types of loans Identify the costs associated

OECD-Brazilian International Conference on Financial Education

OECD-Brazilian International Conference on Financial Education Debt Literacy, Financial Experiences and Overindebtedness December 15-16, 2009 Annamaria Lusardi Dartmouth College & NBER (Joint work with

OECD-Brazilian International Conference on Financial Education Debt Literacy, Financial Experiences and Overindebtedness December 15-16, 2009 Annamaria Lusardi Dartmouth College & NBER (Joint work with

Financial Matters. Optional Extension Tips: Optional Extension Tips: Below Level Differentiation. Above Level Differentiation

Below Level Differentiation Reading and Discussion Tips: When discussing the explanations to the test questions, provide students with the pre-test answer key so they can follow along. Students may use

Below Level Differentiation Reading and Discussion Tips: When discussing the explanations to the test questions, provide students with the pre-test answer key so they can follow along. Students may use

Teens. lesson seven. about credit

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

Consumer Debt for 2012

Borrower Beware 1 Why Borrow? 2 Consumer Debt for 2012 Averages per US Household: O Average credit card debt: $15,204 O Average mortgage debt: $148,818 O Average student loan debt: $33,005 Total American

Borrower Beware 1 Why Borrow? 2 Consumer Debt for 2012 Averages per US Household: O Average credit card debt: $15,204 O Average mortgage debt: $148,818 O Average student loan debt: $33,005 Total American

The Common Sense Guide: HECM

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet

The CFSI Underbanked Consumer Study - Fact Sheet June 8, 28 The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet Released: June 8, 28 Introduction The purpose

The CFSI Underbanked Consumer Study - Fact Sheet June 8, 28 The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet Released: June 8, 28 Introduction The purpose

new homebuyers guide PERSONAL FINANCE

new homebuyers guide PERSONAL FINANCE NEW Buying a home will be one of the biggest financial decisions of your lifetime. People say this all the time, but most people don t understand what buying a home

new homebuyers guide PERSONAL FINANCE NEW Buying a home will be one of the biggest financial decisions of your lifetime. People say this all the time, but most people don t understand what buying a home

What is a SHORT SALE?

Frequently Asked Questions What is a SHORT SALE? What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property.

Frequently Asked Questions What is a SHORT SALE? What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property.

Smart Debt Management: Six Tips for Keeping Your Debt in Check

Smart Debt Management: Six Tips for Keeping Your Debt in Check By Tim Steffen, CPA/PFS, CFP, CPWA, Director of Advanced Planning Debt is a subject about which most people feel conflicted. While debt makes

Smart Debt Management: Six Tips for Keeping Your Debt in Check By Tim Steffen, CPA/PFS, CFP, CPWA, Director of Advanced Planning Debt is a subject about which most people feel conflicted. While debt makes

Tell Your Story. Week 4 How would it feel to be 100% debt-free now and forever? date

Tell Your Story Week 4 How would it feel to be 100% debt-free now and forever? date dumping debt breaking the chains of debt Debt is the most successfully, aggressively marketed product in history. What?

Tell Your Story Week 4 How would it feel to be 100% debt-free now and forever? date dumping debt breaking the chains of debt Debt is the most successfully, aggressively marketed product in history. What?

Keeping Finances Under Control. How to Manage Debt so it Doesn t Manage You

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

Your Guide to Cars, Insurance and Identity Theft

Ignition Your Guide to Cars, Insurance and Identity Theft Each step toward independence comes with questions about finances that may affect your future. We ve got you covered; this booklet can answer some

Ignition Your Guide to Cars, Insurance and Identity Theft Each step toward independence comes with questions about finances that may affect your future. We ve got you covered; this booklet can answer some

Your Money, Your Goals too. Financial empowerment toolkit

Your Money, Your Goals too Financial empowerment toolkit DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It does not constitute

Your Money, Your Goals too Financial empowerment toolkit DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It does not constitute

Surviving Debt { INSIDE } A Quick Answer Guide to Debt Relief. Introduction 1 Debt Getting Help 4-6 About CareOne Credit 7

Surviving Debt A Quick Answer Guide to Debt Relief { INSIDE } Introduction 1 Debt 101 2-3 Getting Help 4-6 About CareOne Credit 7 Introduction. Please know that you are not alone. There are a lot of us

Surviving Debt A Quick Answer Guide to Debt Relief { INSIDE } Introduction 1 Debt 101 2-3 Getting Help 4-6 About CareOne Credit 7 Introduction. Please know that you are not alone. There are a lot of us

Understanding Consumer and Mortgage Loans

Personal Finance: Another Perspective Understanding Consumer and Mortgage Loans Updated 2017-02-07 Note: Graphs on this presentation are from http://www.bankrate.com/funnel/graph/default.aspx? Copied on

Personal Finance: Another Perspective Understanding Consumer and Mortgage Loans Updated 2017-02-07 Note: Graphs on this presentation are from http://www.bankrate.com/funnel/graph/default.aspx? Copied on

Credit & Money Management

Credit & Money Management Certification Program TABLE OF CONTENTS SECTION 1 Understanding Money Chapter 1 Organizing Your Financial Life... 4 Chapter 2 Building Budgeting Skills... 8 Chapter 3 Basics of

Credit & Money Management Certification Program TABLE OF CONTENTS SECTION 1 Understanding Money Chapter 1 Organizing Your Financial Life... 4 Chapter 2 Building Budgeting Skills... 8 Chapter 3 Basics of

MONEY-MIND 101 FINANCIAL MANAGEMENT TRAINING FOR YOUNG ADULTS Early Intervention to Avoid Learning Financial Lessons the Hard Way

MONEY-MIND 101 FINANCIAL MANAGEMENT TRAINING FOR YOUNG ADULTS Early Intervention to Avoid Learning Financial Lessons the Hard Way A PRIMER BY PSYCHOLOGIST CHRISTOPHER BAYER, PH.D. Introductions & Expectations

MONEY-MIND 101 FINANCIAL MANAGEMENT TRAINING FOR YOUNG ADULTS Early Intervention to Avoid Learning Financial Lessons the Hard Way A PRIMER BY PSYCHOLOGIST CHRISTOPHER BAYER, PH.D. Introductions & Expectations

Profiles in Credit is designed to be flexible and meet the needs of learners in different educational settings. Examples include:

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Presentation Slides. Lesson Four. Credit 04/09

Presentation Slides $ Lesson Four Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

Presentation Slides $ Lesson Four Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU?

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+ MODULE 4 // FINANCIAL SOCCER PROGRAM Financial Soccer is an educational video game designed to help students learn more about the fundamentals

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+ MODULE 4 // FINANCIAL SOCCER PROGRAM Financial Soccer is an educational video game designed to help students learn more about the fundamentals

credit crunch lesson 6: student outcomes Chapter 30 from Reality Check time relationship to national standards assessment materials

Chapter 30 from Reality Check time 50 minutes relationship to national standards FCS National Standards: 2.1.2, 2.6.2, 3.3.3 JumpStart Financial Literacy Standards PMM3, CD 1 assessment Do I Have to Have

Chapter 30 from Reality Check time 50 minutes relationship to national standards FCS National Standards: 2.1.2, 2.6.2, 3.3.3 JumpStart Financial Literacy Standards PMM3, CD 1 assessment Do I Have to Have

EverFi Financial Literacy Cumulative Exam

EverFi Financial Literacy Cumulative Exam Module 1: Savings 1. Use the Rule of 72 to calculate how long it will take for your money to double if it s earning 6% in interest: a. 12yrs b. 16yrs c. 36yrs

EverFi Financial Literacy Cumulative Exam Module 1: Savings 1. Use the Rule of 72 to calculate how long it will take for your money to double if it s earning 6% in interest: a. 12yrs b. 16yrs c. 36yrs

YOU work hard to earn your money. Make it work for YOU!

YOU work hard to earn your money. Make it work for YOU! I raised my credit score by 100 points and saved on my car loan. We paid off our high-interest payday loan and started an emergency fund. I used

YOU work hard to earn your money. Make it work for YOU! I raised my credit score by 100 points and saved on my car loan. We paid off our high-interest payday loan and started an emergency fund. I used

Your Money, Your Goals Spotlight Series. Dealing with debt: A closer look

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

SURVEY OF CONSUMER EXPECTATIONS. Housing Survey 2016

SURVEY OF CONSUMER EXPECTATIONS Housing Survey 2016 Federal Reserve Bank of New York Andreas Fuster and Basit Zafar with Kevin Morris une 2, 2016 SCE ederal Housing Reserve Survey 2016 Bank of New York

SURVEY OF CONSUMER EXPECTATIONS Housing Survey 2016 Federal Reserve Bank of New York Andreas Fuster and Basit Zafar with Kevin Morris une 2, 2016 SCE ederal Housing Reserve Survey 2016 Bank of New York

YOU ARE NOT ALONE Hello, my name is <name> and I m <title>.

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

INS and OUTs of insurance

INS and OUTs of insurance What do other high school students know about insurance? We asked high school students about what they think about insurance. Insurance is something that will pay for medical

INS and OUTs of insurance What do other high school students know about insurance? We asked high school students about what they think about insurance. Insurance is something that will pay for medical

DRIVING MY FINANCIAL FUTURE

STUDENT ACTIVITY 2 Write all of the things you d like to have or do that cost money, you can make the list as long as you want. Review the items you have listed and group them into the 3 category boxes

STUDENT ACTIVITY 2 Write all of the things you d like to have or do that cost money, you can make the list as long as you want. Review the items you have listed and group them into the 3 category boxes

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

Detailed Results 9TH ANNUAL PARENTS, KIDS & MONEY SURVEY

Detailed Results 9TH ANNUAL PARENTS, KIDS & MONEY SURVEY Contents Household Finances..3 Household Debt 19 Savings..28 Emergency Fund..32 Retirement Savings..36 Parental Knowledge, Attitudes and Behavior.....42

Detailed Results 9TH ANNUAL PARENTS, KIDS & MONEY SURVEY Contents Household Finances..3 Household Debt 19 Savings..28 Emergency Fund..32 Retirement Savings..36 Parental Knowledge, Attitudes and Behavior.....42