REPAYE guide The Revised Pay As You Earn program explained $ $

|

|

|

- Moses Fitzgerald

- 5 years ago

- Views:

Transcription

1 REPAYE guide The Revised Pay As You Earn program explained

, and you re trying to figure out")

2 WHAT IS REPAYE? You look a little lost maybe you ve heard that the federal government just introduced a new incomebased loan repayment plan, called Revised Pay As You Earn (REPAYE), and you re trying to figure out what it is? We re with you there. Having to figure out how to repay your student loans can be stressful enough, without having to figure out the fine print of all the various loan repayment programs out there. But that s what Credible is here for! This is a guide created just for you, a resource you can keep coming back to, that will explain what income-driven repayment plans are, the different income-driven plans available, and all the details you could ever need about the newest income-driven repayment plan REPAYE. Cool. So, uh, what is REPAYE? The Revised Pay As You Earn (REPAYE) plan is the newest income-driven loan repayment plan and, as the name implies, is a revised version of the Pay As You Earn (PAYE) plan. REPAYE officially launched on Dec. 17, Like other income-driven repayment plans before it, REPAYE ties the size of your loan payments to your income. Under REPAYE, your monthly payments are equal to 10 percent of your discretionary income. So while your payments will increase as you earn more, they shouldn t become unmanageable. If you re not earning enough to pay off undergraduate student loan debt in REPAYE after 20 years, it s forgiven. It takes longer 25 years to qualify for forgiveness of graduate school debt under REPAYE. Those extra five years can be a big deal, adding tens of thousands of dollars in total costs when repaying high-balance grad school debt, as we ll see below. The reason REPAYE is being greeted with such excitement, though, is that it removes previous barriers to eligibility, opening up the option of an income-based repayment plan to an additional 5 million people. But REPAYE isn t perfect. Like other income-driven repayment plans, REPAYE comes with certain qualifiers. Hold on, I m new to this. Let s back up what exactly is an income-driven repayment plan and how does it work? How is it different from the 10-year Standard Repayment Plan? 2

3 Income Driven Repayment Plan versus 10-year Standard Repayment Plan Income-driven plans are meant to be more fexible than Standard Repayment, and are individualized for each borrower s current financial situation. So instead of a fixed monthly payment over the course of 10 years which is how the Standard Repayment Plan typically works income-driven plans take into account factors like how much money you make and the size of your family. Essentially, incom-based plans can help you lower your monthly payments by capping them at 10 percent of your discretionary monthly income.* *IBR plans for borrowers who had Direct Loans or FFELP loans on or before July 1, 2014 cap monthly payments at 15 percent of discretionary income. Income-driven repayment plans include the Income-Based Repayment (IBR) plan, Income- Contingent Repayment (ICR) plan, Pay As You Earn (PAYE), and now REPAYE. 3

4 Diving deeper into income-driven plans Do income-driven plans save me money? How REPAYE stacks up in the long-run Income-driven plans sounds great to borrowers because they limit how much you have to pay each month, but they re not all roses. In fact, unless you are consolidating several loans, you might actually end up paying more money overall under an income-driven plan than you would under the Standard Repayment Plan. Say what? I thought income-driven plans were based on my income and were supposed to save me money. The key thing to remember is that income-driven plans like REPAYE might save you money, but it largely depends on factors like how much debt you have and how much you re paying off each month. Unlike refinancing, consolidating loans into an income-driven plan doesn t actually reduce your interest rate it simply limits your monthly payments to a percentage of your income, so that, in theory at least, you re never paying more than you can afford. One way you might save money using REPAYE is if you are consolidating a large amount of debt, and a good chunk of it ends up being forgiven. But here s the catch: When that debt is forgiven, you could be faced with a fat tax bill. That s because, under current tax laws, any unpaid interest and principal that s forgiven is considered income. The good news is that REPAYE provides a new interest subsidy, and only half of your unpaid interest will be counted as forgiven at the end of the loan. When does REPAYE make sense? The way income-driven repayment plans typically work is by extending the term of your loan, minimizing the monthly payment. These plans are geared towards borrowers who are just beginning to pay back large balances that, if paid back in just 10 years, would require sizeable monthly payments that might be unaffordable or impossible to make. Making the lowest possible monthly payment sounds great, but there s sometimes a price to pay. Incomedriven plans might make your monthly payments more manageable, but the longer you take to repay the loan, the more you ll pay back in the long run in interest. 4

5 Generally speaking, stretching out the term of a loan from 10 years to 20 years, for example can reduce your monthly payments, but result in higher total interest payments over the life of the loan. Standard Repayment Plans for most government loans are 10 years. If you can afford to make the monthly payments on a Standard Repayment Plan, they can save you money. But if you are combining multiple loans into a single Direct Consolidation Loan or FFELP Consolidation Loan, the Standard Repayment plan works a little differently. Instead of being fixed at 10 years, the term of a Standard Repayment Plan for consolidation loans depends on the loan balance. Your term could be stretched out up to 30 years and you ll never qualify for forgiveness. Keep in mind though, that borrowers with FFELP loans only have access to one income-driven repayment plan: IBR. But combining FFELP loans into a Direct Consolidation Loan gives borrowers access to the REPAYE, PAYE, and ICR plans. Standard Repayment Plan for a Direct Consolidation Loan or FFELP Consolidation Loans Balance (lower bound) Balance (upper bound) Loan term 0 7, years 7,500 10, years 10,000 20, years 20,000 40, years 40,000 60, years 60, years The Department of Education has updated its student loan calculator to help you understand the pros and cons of different repayment plans for borrowers. Which plan is best for you will depend on your income, type of student loan debt, and level of debt. To give you an idea of how repayment plans can differ, we ve run the numbers for a hypothetical borrower with 50,000 in adjusted gross income (AGI) carrying different levels of debt ranging from 10,000 to 150,000. We ll assume that the hypothetical borrower has combined all of their loans into a direct, unsubsidized consolidation loan at 6.4 percent interest. As you can see from the charts below, for this particular borrower, PAYE and REPAYE beat the Standard Repayment Plan for all loan balances. 5

6 Standard repayment plan (for direct consolidation loans) Debt Monthly payment Total paid (principal & interest) Total forgiven 10, (x180) 15, , (x240) 53, , (x300) 100, , (x360) 225, , (x360) 337,773 0 PAYE income-driven plan (20-year maximum) Debt Monthly payment Total paid (principal & interest) Total forgiven* 10, (x39) 11, , (x131) 42, , (x202) 88, , (x240) 121, , , (x240) 121, ,955 REPAYE income-driven plan (25-year maximum) Debt Monthly payment Total paid (principal & interest) *Forgiven debt is considered taxable income by the Internal Revenue Service. Total forgiven* 10, (x39) 11, , (x117) 41, , (x197) 87, , ,086 (x300) 179,599 64, , ,086 (x300) 179, ,780 At modest levels of student loan debt, monthly payments under the Standard Repayment Plan are less than what you might comfortably afford. PAYE and REPAYE, which set monthly payments according to what you can afford, allow you pay off a 10,000 loan in just over 3 years, instead of the 15-year term for the Standard Repayment Plan. In these low-balance scenarios, it s the Standard Payment Plan that stretches out smaller monthly payments over a longer term, which costs you more in total interest payments. In high-balance scenarios, PAYE and REPAYE not only protect you from monthly payments that might strain your budget at the outset, but offer loan forgiveness that can save you tens of thousands of dollars. Those savings could be partially offset by taxes, as we ll see below. 6

7 What are the differences between PAYE and REPAYE? PAYE and REPAYE are very similar if you re tackling a reasonable amount of debt that you can comfortably pay off before you qualify for forgiveness. The differences between the programs become more apparent when your debt burden is high enough that you won t be able to pay it off before you qualify for forgiveness after 20 years in the PAYE program, or 25 years for grad school debt paid back under REPAYE. One of the biggest differences between PAYE and REPAYE is the fact that graduate school debt doesn t qualify for forgiveness until you ve made 25 years of payments. Forgiveness for all loans in PAYE is available after 20 years. So total interest and principal payments on 100,000 in consolidated debt at 6.4 percent interest will be 121,045 over 20 years in PAYE, compared to 179,599 in REPAYE a difference of nearly 60,000. One more thing to keep in mind is that, outside of special programs for some public servants, forgiven student loan debt is considered taxable income by the IRS. One helpful feature of REPAYE though, is an interest subsidy only half of the unpaid interest you rack up is counted as forgiven debt. So in the scenario above, the interest subsidy, plus 5 years of additional payments, reduces the total amount forgiven under REPAYE and the tax bill you ll get hit with at the end of your loan. Our hypothetical borrower paying back 100,000 under PAYE will have 106,955 in debt forgiven, while the REPAYE borrower will have just 64,076 forgiven. Assuming that forgiven debt is taxed as income at 25 percent, the PAYE borrower will be starting a 26,700 tax bill in the face at the end of their loan, compared to about 16,000 under REPAYE. Once you factor taxes in, some of the savings advantages of the PAYE program can evaporate. Our borrower s total cost to pay back a 100,000 loan in PAYE ends up being about 147,700, compared to around 195,600 under REPAYE. That s a difference of about 48,000 between the two programs, compared to 60,000 before taxes are factored in. The tax implications of forgiven debt are even more significant on a 150,000 loan. Our borrower could be looking at a 55,200 tax bill under PAYE, bringing the total cost of repaying the loan to about 176,300. REPAYE will set her back 223,300 after 43,700 in taxes are factored in. While Congress could someday decide not to tax forgiven student loan debt as income, the charts we ve run illustrate a potential problem that could arise. When payments are income-based and part of a loan ends up in forgiveness, it doesn t cost the borrower a thing to take on even more debt, if forgiveness isn t taxed. Under REPAYE, for example, the total the borrower pays back on a 100,000 loan 179,599 is exactly what they pay back for a 150,000 loan. So once borrowers reach a certain level of indebtedness, there s no penalty for taking out more unless there are tax implications. 7

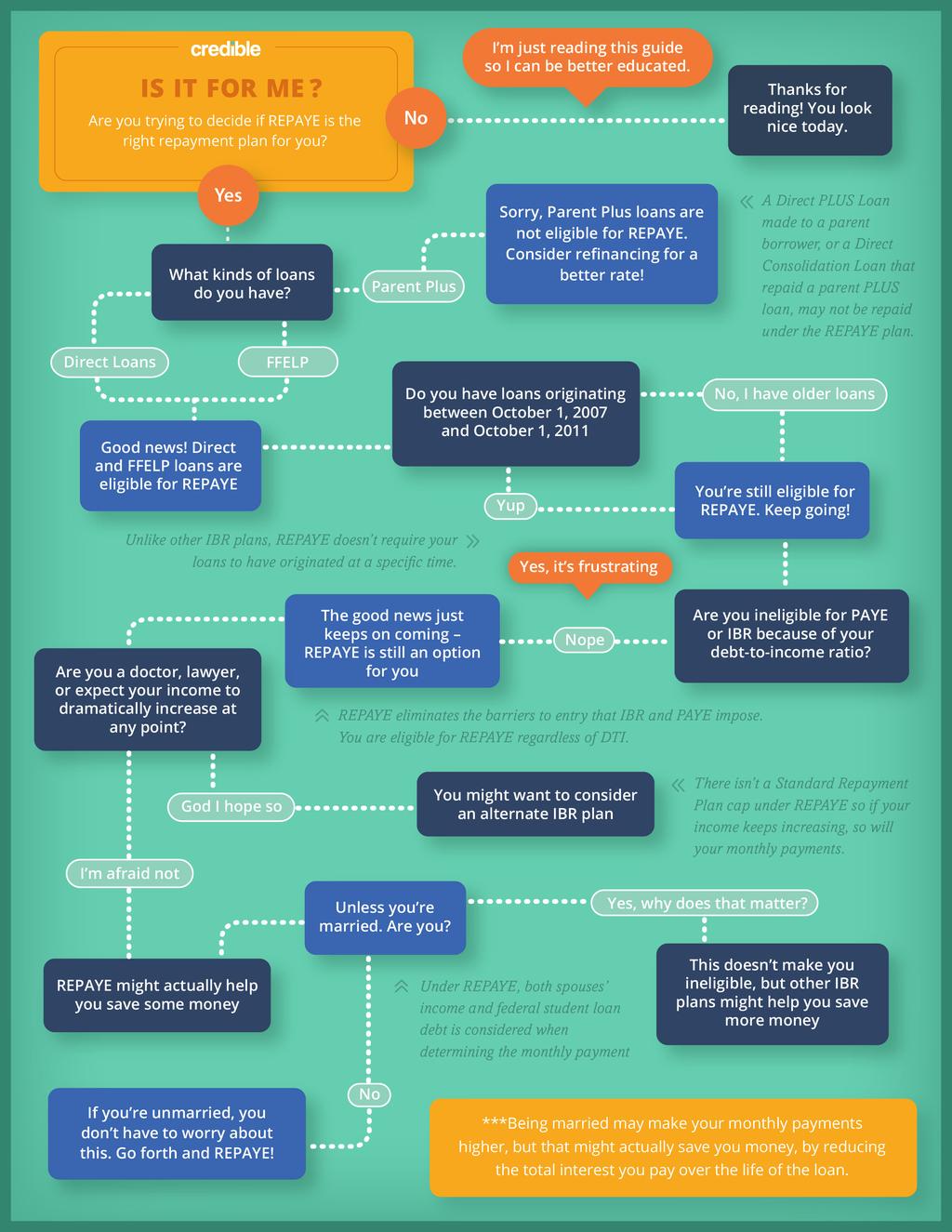

8 REPAYE: PROS AND CONS Okay, so REPAYE could save me money, but if I have a lot of debt, I could end up paying more? Why would I opt for REPAYE? PROS CONS No time-based or debt-toincome based eligibility requirements Loan forgiveness after 20 years for undergraduate loans, and 25 years for graduate or professional loans Note: Student loan debt forgiven at the end of an income-driven repayment plan, including unpaid interest, is currently treated by the IRS as taxable income. Available only for those who have Direct Loans. Parent PLUS loans are not eligible No Standard Repayment cap on how much monthly payments can increase For married borrowers, both partners income is considered when calculating the minimum monthly payment Okay, got it. Income-based plans can be helpful, as long as you keep in mind all the various criteria. How do I know if I m eligible for REPAYE or if it s the right repayment plan for me? It can get a little bit complicated, so we put together a handy flowchart to quickly help you figure out if REPAYE might be a good option for you. 8

9

10 THANK YOU! We d love to hear from you! Credible is here to help you with all your student loans needs. See how much you can save by refinancing your student loans with Credible at If you have any questions about refinancing, or you just want to chat about what options are available to you, please contact us directly at or us at support@credible.com. We look forward to hearing from you! The Credible Team About Credible Credible s founding principle is to provide borrowers the level of transparency they deserve. As a multi-lender marketplace that allows borrowers to receive competitive loan offers from its vetted lenders, Credible empowers consumers to take control of their student loans. Borrowers can fill out one form, then receive and compare personalized offers from numerous lenders and choose which best serves their individual needs. Credible is fiercely independent, committed to delivering fair and unbiased solutions in student /crediblelabs +crediblelabs

What is an income-driven repayment plan?

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Federal Student Loan Repayment

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

Student Loan Ombudsman Caucus

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

STUDENT LOAN REPAYMENT. Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

Student loans: there s more than one way to repay

Student loans: there s more than one way to repay Repayment options 1 Consolidation If you have multiple federal student loans, you may be interested in a Direct Consolidation Loan to simplify loan repayment.

Student loans: there s more than one way to repay Repayment options 1 Consolidation If you have multiple federal student loans, you may be interested in a Direct Consolidation Loan to simplify loan repayment.

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service programs 4. Rights and Responsibilities, resources,

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service programs 4. Rights and Responsibilities, resources,

College Numbers Planning

College Numbers Planning Today s Plan What s new in financial aid and student borrowing What s the deal with student loan interest rates How to use consolidation (and how not to) Comparing repayment options

College Numbers Planning Today s Plan What s new in financial aid and student borrowing What s the deal with student loan interest rates How to use consolidation (and how not to) Comparing repayment options

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed Latest Report Class of 2015 average student loan debt $30,100 44% of college grads in their 20s are employed in low-wage jobs Many

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed Latest Report Class of 2015 average student loan debt $30,100 44% of college grads in their 20s are employed in low-wage jobs Many

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

THE ROAD TO ZERO. A Strategic Approach to Student Loan Repayment. Financial education resources from a nonprofit you can trust. AccessLex.

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

Should Physicians REPAYE?

Should Physicians REPAYE? [Editor s Note: This is a guest post from blog advertiser and student loan expert Jan Miller, President of Student Loan Consultant. He offers fee-only advice about your student

Should Physicians REPAYE? [Editor s Note: This is a guest post from blog advertiser and student loan expert Jan Miller, President of Student Loan Consultant. He offers fee-only advice about your student

ATSU-KCOM SENIOR LOAN EXIT INTERVIEW CLASS OF 2015

ATSU-KCOM SENIOR LOAN EXIT INTERVIEW CLASS OF 2015 Special Thanks to Paul S. Garrard of PGPresents, LLC, who shared these slides with Osteo Financial Aid Directors! SUMMARY AND TO-DO LIST Self assessment

ATSU-KCOM SENIOR LOAN EXIT INTERVIEW CLASS OF 2015 Special Thanks to Paul S. Garrard of PGPresents, LLC, who shared these slides with Osteo Financial Aid Directors! SUMMARY AND TO-DO LIST Self assessment

Ten Things You Should Know About Student Loans

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014.

1 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014. Our research indicates

1 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014. Our research indicates

Income-Driven Repayment Plans

Income-Driven Repayment Plans Agenda Income-Driven Repayment Plans Overview Income-Based Repayment Plan (IBR) Income-Contingent Repayment Plan (ICR) Pay As You Earn Plan (PAYE) Revised Pay As You Earn

Income-Driven Repayment Plans Agenda Income-Driven Repayment Plans Overview Income-Based Repayment Plan (IBR) Income-Contingent Repayment Plan (ICR) Pay As You Earn Plan (PAYE) Revised Pay As You Earn

SUNY Downstate. Medical Students guide to student loans. The Financial Aid Office 2017

SUNY Downstate Medical Students guide to student loans The Financial Aid Office 2017 Quick thoughts about repayment 1) Be organized and pay attention to the details of your loans. 2) Set a monthly budget

SUNY Downstate Medical Students guide to student loans The Financial Aid Office 2017 Quick thoughts about repayment 1) Be organized and pay attention to the details of your loans. 2) Set a monthly budget

A Guide to Student Loan Refinancing. Practical repayment information for everyone (with special tips for medical professionals)

") A Guide to Student Loan Refinancing Practical repayment information for everyone (with special tips for medical professionals) For years student loan borrowers have felt stuck, with limited options to

A Guide to Student Loan Refinancing Practical repayment information for everyone (with special tips for medical professionals) For years student loan borrowers have felt stuck, with limited options to

TAKE CHARGE OF LOAN REPAYMENT!

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2013 Jeffrey Hanson Education Services University of San Diego School of Law Your Action Plan 4 Steps 2 1. Take stock

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2013 Jeffrey Hanson Education Services University of San Diego School of Law Your Action Plan 4 Steps 2 1. Take stock

Repayment Plans. October Kim Wells U.S. Department of Education 1. Agenda. Standard Plan. Default repayment plan Loans eligible for inclusion

Repayment Plans U.S. Department of Education Agenda Standard Plan Extended Plan Graduated Plan Income-Driven Plans Resources 2 Standard Plan Default repayment plan Loans eligible for inclusion Direct Subsidized

Repayment Plans U.S. Department of Education Agenda Standard Plan Extended Plan Graduated Plan Income-Driven Plans Resources 2 Standard Plan Default repayment plan Loans eligible for inclusion Direct Subsidized

IBR and ICR Options to help borrowers manage repayment

IBR and ICR Options to help borrowers manage repayment Course outline Similarities of IBR and ICR plans Overview of IBR plan Overview of ICR plan Summary Upcoming changes Resources 1 Staggering growth

IBR and ICR Options to help borrowers manage repayment Course outline Similarities of IBR and ICR plans Overview of IBR plan Overview of ICR plan Summary Upcoming changes Resources 1 Staggering growth

9/19/2013 BORROWERS HAVE MORE OPTIONS OBJECTIVES COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

TICAS Proposal to Create One Improved Income-Driven Repayment Plan

TICAS Proposal to Create One Improved Income-Driven Repayment Plan All federal student loan borrowers should be able to choose the assurance of manageable payments and forgiveness after 20 years of payments.

TICAS Proposal to Create One Improved Income-Driven Repayment Plan All federal student loan borrowers should be able to choose the assurance of manageable payments and forgiveness after 20 years of payments.

That means the average cost for just one four-year degree will be $132,000

With the cost of tuition constantly going up these days, it is a rarity that I speak to a recent graduate who is not in student loan debt of some kind. In fact, the most recent statistics show that over

With the cost of tuition constantly going up these days, it is a rarity that I speak to a recent graduate who is not in student loan debt of some kind. In fact, the most recent statistics show that over

Meet The Speakers. Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

The Price of Success: Managing Student Loan Repayment. American College of Foot and Ankle Surgeons Webinar August 30, 2018

The Price of Success: Managing Student Loan Repayment American College of Foot and Ankle Surgeons Webinar August 30, 2018 Presenters Todd Woodlee, Vice President igrad Nicholas Smith, DPM, FACFAS Columbus

The Price of Success: Managing Student Loan Repayment American College of Foot and Ankle Surgeons Webinar August 30, 2018 Presenters Todd Woodlee, Vice President igrad Nicholas Smith, DPM, FACFAS Columbus

Class of 2014 Loan Repayment Information Session

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

ATSU-SOMA SENIOR LOAN EXIT INTERVIEW CLASS OF 2017

ATSU-SOMA SENIOR LOAN EXIT INTERVIEW CLASS OF 2017 Presented by ATSU Financial Aid Federal Stafford* Federal Grad PLUS* Federal Perkins* *Reported on NSLDS at www.nslds.ed.gov FEDERAL STAFFORD LOANS Unsubsidized

ATSU-SOMA SENIOR LOAN EXIT INTERVIEW CLASS OF 2017 Presented by ATSU Financial Aid Federal Stafford* Federal Grad PLUS* Federal Perkins* *Reported on NSLDS at www.nslds.ed.gov FEDERAL STAFFORD LOANS Unsubsidized

TAKE CHARGE OF LOAN REPAYMENT!

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2014 Jeffrey Hanson Education Services University of Wisconsin Law School Federal student loans are unique 2 q Flexible

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2014 Jeffrey Hanson Education Services University of Wisconsin Law School Federal student loans are unique 2 q Flexible

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

Federal Student Loan Repayment Do s & Don ts

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

2/22/2015 SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Dental school graduates have great track record for repayment Multiple ways

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Dental school graduates have great track record for repayment Multiple ways

How to Find and Qualify for the Best Loan for Your Business

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

The Truth About Student Loans JumpStart Conference May Copyright 2016 Finance Authority of Maine

The Truth About Student Loans JumpStart Conference May 2016 Copyright 2016 Finance Authority of Maine Loans TYPES William D Ford Federal Direct Loan Program (Direct) o Direct Subsidized and Direct Unsubsidized

The Truth About Student Loans JumpStart Conference May 2016 Copyright 2016 Finance Authority of Maine Loans TYPES William D Ford Federal Direct Loan Program (Direct) o Direct Subsidized and Direct Unsubsidized

COLLEGE COST REDUCTION AND ACCESS ACT OF Short Title: CCRAA

COLLEGE COST REDUCTION AND ACCESS ACT OF 2007 Short Title: CCRAA College Cost Reduction and Access Act of 2007 (CCRAA) In part, Congress s response to the problem of high monthly repayment obligations

COLLEGE COST REDUCTION AND ACCESS ACT OF 2007 Short Title: CCRAA College Cost Reduction and Access Act of 2007 (CCRAA) In part, Congress s response to the problem of high monthly repayment obligations

Please Check In and Pick Up Your Folder. Exit Counseling Folder

Exit Counseling Please Check In and Pick Up Your Folder Exit Counseling Folder Personalized federal student loan balances Letter from our office and bookmark Loan Servicer information Loan Tips and Resources

Exit Counseling Please Check In and Pick Up Your Folder Exit Counseling Folder Personalized federal student loan balances Letter from our office and bookmark Loan Servicer information Loan Tips and Resources

10/17/2016. Haverford HS College Financial Aid Programs. Paying for College 10/10 Loans & Repayment 10/17 Saving For College 10/24

Presented By Fred Amrein Haverford HS College Financial Aid Programs Paying for College 10/10 Loans & Repayment 10/17 Saving For College 10/24 Amrein Financial is an independent, fee only Registered Investment

Presented By Fred Amrein Haverford HS College Financial Aid Programs Paying for College 10/10 Loans & Repayment 10/17 Saving For College 10/24 Amrein Financial is an independent, fee only Registered Investment

2/26/2015 SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Multiple ways to effectively handle your student loan debt Constantly evaluate

SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Multiple ways to effectively handle your student loan debt Constantly evaluate

PUBLIC SERVICE LOAN FORGIVENESS

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

LOAN REPAYMENT STRATEGIES

LOAN REPAYMENT STRATEGIES Be Ready! Develop a Plan! Fall 2017 Jeffrey Hanson Education Services Boston University School of Law You have CHOICES Decisions to be made 2 Should you pay the interest on your

LOAN REPAYMENT STRATEGIES Be Ready! Develop a Plan! Fall 2017 Jeffrey Hanson Education Services Boston University School of Law You have CHOICES Decisions to be made 2 Should you pay the interest on your

Student Loan Best Practices for Transitioning to Practice

Student Loan Best Practices for Transitioning to Practice Stanford Hospital November 16 th, 2015 By Jason DiLorenzo & Marti Trujillo Questions from Housestaff If I m in IBR, is it possible that some or

Student Loan Best Practices for Transitioning to Practice Stanford Hospital November 16 th, 2015 By Jason DiLorenzo & Marti Trujillo Questions from Housestaff If I m in IBR, is it possible that some or

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Objectives. Objectives. Loans 101. Purpose and types of Federal loans. Life cycle of a Federal loan. Repayment options. Delinquency and default

Loans 101 Becky Davis and Debbie Murphy Ascendium Education Solutions Objectives 1 2 3 Purpose and types of Federal loans Life cycle of a Federal loan Repayment options 2019 ILASFAA Annual Conference 2

Loans 101 Becky Davis and Debbie Murphy Ascendium Education Solutions Objectives 1 2 3 Purpose and types of Federal loans Life cycle of a Federal loan Repayment options 2019 ILASFAA Annual Conference 2

Repaying your federal student loans

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Drowning in Debt? How to Take Control of Your Future and Manage Your Educational Debt

Drowning in Debt? How to Take Control of Your Future and Manage Your Educational Debt Today s Agenda Resources for managing educational debt Know Your Loans Entering Repayment Broad Federal Relief Programs

Drowning in Debt? How to Take Control of Your Future and Manage Your Educational Debt Today s Agenda Resources for managing educational debt Know Your Loans Entering Repayment Broad Federal Relief Programs

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

Follow the below directions to print and mail your application and income documentation:

IDR Request Servicer Mailing Information Follow the below directions to print and mail your application and income documentation: 1. View your completed application (below). Note: Responses to all applicable

IDR Request Servicer Mailing Information Follow the below directions to print and mail your application and income documentation: 1. View your completed application (below). Note: Responses to all applicable

Federal Student Aid. Direct Loan. Entrance Counseling Guide

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

ATSU-ATHLETIC TRAINING SENIOR LOAN EXIT INTERVIEW CLASS OF 2017

ATSU-ATHLETIC TRAINING SENIOR LOAN EXIT INTERVIEW CLASS OF 2017 Presented by ATSU Financial Aid Federal Stafford* Federal Grad PLUS* Federal Perkins* *Reported on NSLDS at www.nslds.ed.gov FEDERAL STAFFORD

ATSU-ATHLETIC TRAINING SENIOR LOAN EXIT INTERVIEW CLASS OF 2017 Presented by ATSU Financial Aid Federal Stafford* Federal Grad PLUS* Federal Perkins* *Reported on NSLDS at www.nslds.ed.gov FEDERAL STAFFORD

This form is for use by Vermont Student Assistance Corporation customers only. If your loans are not serviced by VSAC please contact your servicer

This form is for use by Vermont Student Assistance Corporation customers only. If your loans are not serviced by VSAC please contact your servicer directly for the appropriate application. This page intentionally

This form is for use by Vermont Student Assistance Corporation customers only. If your loans are not serviced by VSAC please contact your servicer directly for the appropriate application. This page intentionally

Student Loan Repayment. Health Sciences Financial Aid Office May 17 th, 2018

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING ADVISING CLIENTS WITH STUDENT LOANS Financial planners today have more clients dealing with student loans than ever before. Outstanding student

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING ADVISING CLIENTS WITH STUDENT LOANS Financial planners today have more clients dealing with student loans than ever before. Outstanding student

The power of borrowing like a boss

The power of borrowing like a boss Borrowing can help you do some pretty wonderful things. Like getting that home that s right for you and your family (or family to be!). The place where you ll make memories

The power of borrowing like a boss Borrowing can help you do some pretty wonderful things. Like getting that home that s right for you and your family (or family to be!). The place where you ll make memories

Student Loan REFINANCING GUIDE THE BIGLAW INVESTOR

Student Loan REFINANCING GUIDE THE BIGLAW INVESTOR How to Refinance Your Student Loans (for lawyers, doctors and anyone who wants to save money!) SO YOU WANT TO GET RID OF THOSE LAW SCHOOL LOANS? This

Student Loan REFINANCING GUIDE THE BIGLAW INVESTOR How to Refinance Your Student Loans (for lawyers, doctors and anyone who wants to save money!) SO YOU WANT TO GET RID OF THOSE LAW SCHOOL LOANS? This

Repayment Strategies Title Lorem Ipsum. Quillen College of Medicine

Repayment Strategies Title Lorem Ipsum Subhead duis tincidunt lectus Quillen College of Medicine Authors Julie Gilbert Sr. Education Debt Management Specialist April 10, 2018 Agenda aamc.org/nextsteps

Repayment Strategies Title Lorem Ipsum Subhead duis tincidunt lectus Quillen College of Medicine Authors Julie Gilbert Sr. Education Debt Management Specialist April 10, 2018 Agenda aamc.org/nextsteps

PUBLIC SERVICE LOAN REPAYMENT STRATEGIES

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

PUBLIC SERVICE LOAN REPAYMENT STRATEGIES

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

Moonlighting vs IBR, PAYE, and PSLF: A Student Loan Showdown

Moonlighting vs IBR, PAYE, and PSLF: A Student Loan Showdown [Editor s Note: This is a guest blog post written by Ramsey Tate, MD. She is currently a fellow and shares tools on personal finance and productivity

Moonlighting vs IBR, PAYE, and PSLF: A Student Loan Showdown [Editor s Note: This is a guest blog post written by Ramsey Tate, MD. She is currently a fellow and shares tools on personal finance and productivity

Republican Policy Committee Millennial Task Force on College Completion, Flexibility, and Affordability for an Emerging Generation

Testimony of Jack Remondi President & CEO Navient Republican Policy Committee Millennial Task Force on College Completion, Flexibility, and Affordability for an Emerging Generation April 12, 2016 Testimony

Testimony of Jack Remondi President & CEO Navient Republican Policy Committee Millennial Task Force on College Completion, Flexibility, and Affordability for an Emerging Generation April 12, 2016 Testimony

Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2016 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have a great track record for repayment Multiple ways

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2016 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have a great track record for repayment Multiple ways

A+ Debt Management Strategies for Federal Student Loan Borrowers

A+ Debt Management Strategies for by, JD, CLU ABSTRACT Federal Student Loan Repayment could be an upper-level course at all institutions of higher education. Unfortunately, for borrowers, it is not. Many

A+ Debt Management Strategies for by, JD, CLU ABSTRACT Federal Student Loan Repayment could be an upper-level course at all institutions of higher education. Unfortunately, for borrowers, it is not. Many

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2014 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have great track record for repayment Multiple ways to

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2014 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have great track record for repayment Multiple ways to

Warm-Up 2/12/16. If you make $8.25/hour, work an average of 25 hours per week, and lose 20% to taxes, what is your annual NET pay?

Warm-Up 2/12/16 If you make $8.25/hour, work an average of 25 hours per week, and lose 20% to taxes, what is your annual NET pay? If you are paid a salary of $40,900 and lose 20% to taxes, what is your

Warm-Up 2/12/16 If you make $8.25/hour, work an average of 25 hours per week, and lose 20% to taxes, what is your annual NET pay? If you are paid a salary of $40,900 and lose 20% to taxes, what is your

Partial Financial Hardship 8/11/2014. Disadvantages of income-driven plans. Interest and capitalization benefits accompany the income-driven plans

Income-Driven Plan Payment Amount Comprehensive Student Loan Training Series Income-Contingent The lesser of: 20 percent of discretionary income, or what borrower would pay on a fixed payment over the

Income-Driven Plan Payment Amount Comprehensive Student Loan Training Series Income-Contingent The lesser of: 20 percent of discretionary income, or what borrower would pay on a fixed payment over the

DEBT MANAGEMENT FOR JUILLIARD GRADUATES. Presented by the Office of Financial Aid

DEBT MANAGEMENT FOR JUILLIARD GRADUATES Presented by the Office of Financial Aid Broad Strokes Terms and Legislation Explained TERMS TO KNOW Servicer An organization that monitors loans while borrowers

DEBT MANAGEMENT FOR JUILLIARD GRADUATES Presented by the Office of Financial Aid Broad Strokes Terms and Legislation Explained TERMS TO KNOW Servicer An organization that monitors loans while borrowers

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Student Loan Repayment Workshop. Amanda Seitz Direct Loan Coordinator - Student Financial Services

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Balancing Act: Budgeting for Law Students

Balancing Act: Budgeting for Law Students Kris Henderson, Associate Dean for Student Services and Administration David Curtis, Assistant Director, Office of Financial Aid September 12, 2016 Business Finance

Balancing Act: Budgeting for Law Students Kris Henderson, Associate Dean for Student Services and Administration David Curtis, Assistant Director, Office of Financial Aid September 12, 2016 Business Finance

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF GOT A LITTLE BIT OF A MATHEMATICAL CALCULATION TO GO THROUGH HERE. THESE

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF GOT A LITTLE BIT OF A MATHEMATICAL CALCULATION TO GO THROUGH HERE. THESE

Navigating Your Student Loan Repayment. Spring, 2016

Navigating Your Student Loan Repayment Spring, 2016 Overview Determining Your Loan Portfolio Understanding Loan Types Debt Management Considerations Repayment Plans Strategies for Repayment Other Resources

Navigating Your Student Loan Repayment Spring, 2016 Overview Determining Your Loan Portfolio Understanding Loan Types Debt Management Considerations Repayment Plans Strategies for Repayment Other Resources

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

The Mortgage Guide. Helping you find the right mortgage for you. Brought to you by. V a

The Mortgage Guide Helping you find the right mortgage for you Brought to you by V0050713a Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us

The Mortgage Guide Helping you find the right mortgage for you Brought to you by V0050713a Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us

Growing your business with affordable financing

Spot Small Business Growing your business with affordable financing An affordable business loan, designed exclusively for small businesses like yours fundingcircle.com support@fundingcircle.com 855.385.5356

Spot Small Business Growing your business with affordable financing An affordable business loan, designed exclusively for small businesses like yours fundingcircle.com support@fundingcircle.com 855.385.5356

Take control of your future. The time is. now

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Class of 2018! Congratulations! University of Louisville School of Medicine. From the SOM Financial Aid Office. aamc.org/first

From the SOM Financial Aid Office Congratulations! University of Louisville School of Medicine Class of 2018! 1 Student Loans and Repayment Strategies Prepared for the Graduating Class of 2018 Leslie R.

From the SOM Financial Aid Office Congratulations! University of Louisville School of Medicine Class of 2018! 1 Student Loans and Repayment Strategies Prepared for the Graduating Class of 2018 Leslie R.

Understanding and Managing your Student Loans and Repayment

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Office of Student Financial Management. Kasia Palm, Director of Student Financial Management

Office of Student Financial Management Kasia Palm, Director of Student Financial Management We advise prospective, current, and former Denver Law students on: General financial aid questions We do not

Office of Student Financial Management Kasia Palm, Director of Student Financial Management We advise prospective, current, and former Denver Law students on: General financial aid questions We do not

How to buy a home EDINBURGH THE LOTHIANS FIFE

How to buy a home EDINBURGH THE LOTHIANS FIFE Feel at home with ESPC Buying a home is exciting, satisfying and also pretty daunting. There s a lot to get your head around, but if you break it into bite-size

How to buy a home EDINBURGH THE LOTHIANS FIFE Feel at home with ESPC Buying a home is exciting, satisfying and also pretty daunting. There s a lot to get your head around, but if you break it into bite-size

Are You Receiving 8-10% Interest on your Investments?

Are You Receiving 8-10% Interest on your Investments? If your answer to the above questions is no, you will want to pay very special attention. The following information could significantly increase the

Are You Receiving 8-10% Interest on your Investments? If your answer to the above questions is no, you will want to pay very special attention. The following information could significantly increase the

Shared Dollar Life Insurance: An inter-generational approach to retirement planning

Shared Dollar Life Insurance: An inter-generational approach to retirement planning What will retirement look like for our children? If you are like most working people, from time to time you think about

Shared Dollar Life Insurance: An inter-generational approach to retirement planning What will retirement look like for our children? If you are like most working people, from time to time you think about

Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security and what can we expect.

Wi$e Up Webinar Catching On to Retirement September 28, 2007 Speaker 2 Diana Varela Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security

Wi$e Up Webinar Catching On to Retirement September 28, 2007 Speaker 2 Diana Varela Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security

Repayment Strategies for Dental School Graduates

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2018 Repayment Strategies for Dental School Graduates Considerations Dental school graduates have a great track record for repayment Use free resources

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2018 Repayment Strategies for Dental School Graduates Considerations Dental school graduates have a great track record for repayment Use free resources

paying off student loans

paying off student loans PAYING OFF STUDENT LOANS Student loans are a national crisis impacting millions of people. The class of 2016 borrowed an average of $37,172 in student loans.* Total student loan

paying off student loans PAYING OFF STUDENT LOANS Student loans are a national crisis impacting millions of people. The class of 2016 borrowed an average of $37,172 in student loans.* Total student loan

Student Loans and Repayment Strategies

Student Loans and Repayment Strategies Prepared for the Graduating Class of 2019 Presenter s name:gloria Salinas Presenter s title: Assistant Director, Financial Aid, UT Health San Antonio Spring 2019

Student Loans and Repayment Strategies Prepared for the Graduating Class of 2019 Presenter s name:gloria Salinas Presenter s title: Assistant Director, Financial Aid, UT Health San Antonio Spring 2019

[01:02] [02:07]

![[01:02] [02:07]](/thumbs/95/125833488.jpg "[01:02] [02:07]") Real State Financial Modeling Introduction and Overview: 90-Minute Industrial Development Modeling Test, Part 3 Waterfall Returns and Case Study Answers Welcome to the final part of this 90-minute industrial

Real State Financial Modeling Introduction and Overview: 90-Minute Industrial Development Modeling Test, Part 3 Waterfall Returns and Case Study Answers Welcome to the final part of this 90-minute industrial

Title IV Loans: Understanding The Basics

Title IV Loans: Understanding The Basics Objectives Review Title IV loans and their basic terms Review some changes to Title IV loans RMASFAA Conference 2012, Omaha, NE Just the Basics: entrance/exit counseling,

Title IV Loans: Understanding The Basics Objectives Review Title IV loans and their basic terms Review some changes to Title IV loans RMASFAA Conference 2012, Omaha, NE Just the Basics: entrance/exit counseling,

MANAGING YOUR LOAN DEBT: BEST PRACTICES FOR 2018 SGU VETERINARY GRADUATES. Presented by Jason DiLorenzo Founder & Executive Director

MANAGING YOUR LOAN DEBT: BEST PRACTICES FOR 2018 SGU VETERINARY GRADUATES Presented by Jason DiLorenzo Founder & Executive Director Agenda Veterinary Graduate Economics Overview of Repayment options Maximizing

MANAGING YOUR LOAN DEBT: BEST PRACTICES FOR 2018 SGU VETERINARY GRADUATES Presented by Jason DiLorenzo Founder & Executive Director Agenda Veterinary Graduate Economics Overview of Repayment options Maximizing

YOU ARE NOT ALONE Hello, my name is <name> and I m <title>.

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

Looking to buy your first home? What to consider when it comes to getting the right loan.

Looking to buy your first home? What to consider when it comes to getting the right loan. Here are the most important things to know before you borrow. If you re looking to buy your first home, chances

Looking to buy your first home? What to consider when it comes to getting the right loan. Here are the most important things to know before you borrow. If you re looking to buy your first home, chances

Credit Cards Are Not For Credit!

Starting At Zero Writing this website, responding to comments and emails, and participating in internet forums makes me a bit insulated to what s really going on out there sometimes. That s one reason

Starting At Zero Writing this website, responding to comments and emails, and participating in internet forums makes me a bit insulated to what s really going on out there sometimes. That s one reason

Drowning in Debt? How government and nonprofit employees can earn public service loan forgiveness

Drowning in Debt? How government and nonprofit employees can earn public service loan forgiveness Isaac Bowers ibowers@equaljusticeworks.org www.equaljusticeworks.org Today s Agenda Resources for Managing

Drowning in Debt? How government and nonprofit employees can earn public service loan forgiveness Isaac Bowers ibowers@equaljusticeworks.org www.equaljusticeworks.org Today s Agenda Resources for Managing

The Mortgage Guide Helping you find the right mortgage for you

The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make. And it can be stressful.

The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make. And it can be stressful.

Your Guide to Finding the Right 401k Plan

Your Guide to Finding the Right 401k Plan Find everything you need to know to make the right decision for your business An Introduction to 401k plans Saving for retirement isn t just for big businesses

Your Guide to Finding the Right 401k Plan Find everything you need to know to make the right decision for your business An Introduction to 401k plans Saving for retirement isn t just for big businesses

Avoid Annuity Traps Page 1

Avoid Annuity Traps Page 1 Thinking About Purchasing An Annuity? Are you thinking about purchasing an annuity? Or maybe you already own one and are considering surrendering it? If so, then before you do

Avoid Annuity Traps Page 1 Thinking About Purchasing An Annuity? Are you thinking about purchasing an annuity? Or maybe you already own one and are considering surrendering it? If so, then before you do

Understanding Loan Repayment Plans and Alternative Repayment

Understanding Loan Repayment Plans and Alternative Repayment Session Outline Grace Periods Direct Loan and FFEL Repayment Plans Emphasis on Income Driven Plans Other Repayment Strategies Default Management

Understanding Loan Repayment Plans and Alternative Repayment Session Outline Grace Periods Direct Loan and FFEL Repayment Plans Emphasis on Income Driven Plans Other Repayment Strategies Default Management

LIVE RICHER ACADEMY LIVE FINANCIAL AID STRATEGY SESSION

LIVE RICHER ACADEMY LIVE FINANCIAL AID STRATEGY SESSION featuring, Financial Aid Expert, ANGELA HOWZE I Angela Howze, Financial Aid Strategist make every effort to ensure an accurate representation of

LIVE RICHER ACADEMY LIVE FINANCIAL AID STRATEGY SESSION featuring, Financial Aid Expert, ANGELA HOWZE I Angela Howze, Financial Aid Strategist make every effort to ensure an accurate representation of

10 Errors to Avoid When Refinancing

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

How to Get Ahead of Your Student Debt

Client Conversations How to Get Ahead of Your Student Debt WHEN COLLEGE ENDS, YOU RE LEFT WITH A DIPLOMA AND A SENSE OF ACCOMPLISHMENT but you re also probably left with some pretty hefty debt and subsequent

Client Conversations How to Get Ahead of Your Student Debt WHEN COLLEGE ENDS, YOU RE LEFT WITH A DIPLOMA AND A SENSE OF ACCOMPLISHMENT but you re also probably left with some pretty hefty debt and subsequent

Income Driven Repayment Plans

Income Driven Repayment Plans Adapted from FSA Presentation Income-Driven Plans - Overview Three main plans Income-Contingent Repayment Plan (ICR) 1994 Direct Loan Program only More information available

Income Driven Repayment Plans Adapted from FSA Presentation Income-Driven Plans - Overview Three main plans Income-Contingent Repayment Plan (ICR) 1994 Direct Loan Program only More information available

Indexed Annuities. Annuity Product Guides

Annuity Product Guides Indexed Annuities An annuity that claims to offer longevity protection along with liquidity and upside potential but doesn t do any of it well Modernizing retirement security through

Annuity Product Guides Indexed Annuities An annuity that claims to offer longevity protection along with liquidity and upside potential but doesn t do any of it well Modernizing retirement security through