2012 Annual Report AGRIBANK, FCB AND AFFILIATED ASSOCIATIONS

|

|

|

- Roger Robertson

- 5 years ago

- Views:

Transcription

1 AA 2012 Annual Report AGRIBANK, FCB AND AFFILIATED ASSOCIATIONS

2 TABLE OF CONTENTS AgriBank, FCB and Affiliated Associations Combined Five-Year Summary of Selected Financial Data... 1 Management's Discussion and Analysis... 2 Report of Managment Independent Auditor s Report Combined Financial Statements Notes to Combined Financial Statements Disclosure Information Required by Regulations Young, Beginning and Small Farmers and Ranchers Risk Factors Additional copies of our annual or quarterly reports may be requested free of charge by contacting AgriBank, FCB at 30 East 7 th Street, St. Paul, MN , (651) , or via to agribankmn@agribank.com. These reports are also available through AgriBank s website at To request free copies of our Annual or Quarterly Reports contact us as stated above. The Annual Report is available on our website approximately 75 days after the end of the calendar year and members are provided a copy of such report 90 days after the end of the calendar year. The Quarterly Reports are available on our website approximately 40 days after the end of each calendar quarter.

3 Combined Five-Year Summary of Selected Financial Data AgriBank, FCB and Affiliated Associations (Dollars in thousands) Combined Statement of Condition Data Loans $77,089,134 $68,349,565 $65,035,081 $60,245,483 $57,151,728 Allowance for loan losses 262, , , , ,254 Net loans 76,826,204 68,049,057 64,628,735 59,859,481 56,940,474 Investment securities and federal funds - AgriBank, FCB 11,731,861 9,988,547 10,647,108 9,575,083 9,393,119 Investment securities - Affiliated Associations 2,275,266 2,262,747 2,033,809 1,877,871 1,613,670 Other property owned 67, ,260 94,491 55,821 18,991 Other assets 2,607,512 2,723,064 2,368,284 2,456,481 2,501,265 Total assets $93,508,679 $83,136,675 $79,772,427 $73,824,737 $70,467,519 Obligations with maturities of one year or less $25,863,061 $22,700,685 $23,791,456 $22,692,372 $22,761,577 Other obligations with maturities greater than one year 52,717,155 47,002,090 43,723,027 40,289,214 38,437,214 Subordinated notes with maturities greater than one year 600, , , , Total liabilities 79,180,216 70,302,775 68,114,483 63,481,586 61,198,791 Protected borrower equity 305 2,056 2,716 3,391 4,124 At-risk borrower equity 261, , , , ,168 Allocated surplus 302, , , , ,300 Unallocated surplus 14,324,793 12,875,783 11,576,553 10,350,806 9,541,610 Accumulated other comprehensive loss (583,324) (594,096) (433,529) (480,959) (705,474) Noncontrolling interest 22,082 6, Total members' equity 14,328,463 12,833,900 11,657,944 10,343,151 9,268,728 Total liabilities and members' equity $93,508,679 $83,136,675 $79,772,427 $73,824,737 $70,467,519 Combined Statement of Income Data Net interest income $2,311,454 $2,172,337 $2,052,135 $1,828,414 $1,563,691 Provision for credit losses (33,907) (23,637) (189,913) (320,374) (126,220) Provision for income taxes (39,116) (55,726) (50,901) (29,411) (22,291) Other expenses, net (519,042) (553,180) (374,249) (579,279) (428,591) Net income $1,719,389 $1,539,794 $1,437,072 $899,350 $986,589 Combined Key Financial Ratios Return on average assets 1.98% 1.91% 1.91% 1.26% 1.52% Return on average members' equity 12.56% 12.47% 12.98% 9.16% 10.71% Net interest income as a percentage of average earning assets 2.73% 2.76% 2.79% 2.64% 2.48% Members' equity as a percentage of total assets 15.32% 15.44% 14.61% 14.01% 13.15% Net charge-offs as a percentage of average loans 0.09% 0.18% 0.28% 0.25% -- Allowance for loan losses as a percentage of loans 0.34% 0.44% 0.62% 0.64% 0.37% Debt to members' equity (:1) Permanent capital ratio (AgriBank only) 21.1% 20.9% 20.6% 18.4% 15.4% Total surplus ratio (AgriBank only) 17.4% 17.3% 16.7% 14.3% 11.5% Core surplus ratio (AgriBank only) 10.4% 10.1% 10.0% 8.2% 7.6% Net collateral ratio (AgriBank only) 106.0% 106.2% 105.8% 105.6% 104.6% Other Cash patronage paid in the current year $5,404 $428 $374 $336 $913 Cash patronage to be paid in the next fiscal year 209, , ,902 93, ,966 Total cash patronage refunds to members $214,586 $199,854 $175,276 $93,793 $107,879 Stock patronage issued in the current year $474 $361 $377 $333 $ -- Stock patronage to be issued in the next fiscal year Total stock patronage refunds to members $826 $695 $945 $675 $ -- Net surplus allocated under nonqualified patronage program $54,967 $40,015 $36,409 $27,206 $33,769 Redemption of surplus allocated under nonqualified patronage program 42,694 14,509 1,262 1,642 18,299 No dividend distributions were made during the years presented. 1

4 Management s Discussion and Analysis AgriBank, FCB and Affiliated Associations The following commentary reviews the financial condition and results of operations of AgriBank, FCB (AgriBank) and affiliated Associations (the District) and provides additional specific information. The accompanying combined financial statements and notes to the combined financial statements also contain important information about our financial condition and results of operations. The Farm Credit System The Farm Credit System (the System) is a nationwide network of borrower-owned lending institutions and specialized service organizations. Farm Credit provides more than $191 billion in loans, leases and related services to farmers, ranchers, rural homeowners, aquatic producers, timber harvesters, agribusinesses and agricultural and rural utility cooperatives. Congress established the System in 1916 to provide a reliable source of credit for the nation's farmers and ranchers. Today, the System provides more than one-third of the credit needed by those who live and work in rural America. Farmers, ranchers, agribusiness, rural homeowners and rural utilities depend on the Farm Credit System s funding and services to produce the high quality food and agricultural products enjoyed in the United States and around the globe. The Farm Credit mission is to provide a reliable source of credit for American agriculture by making loans to qualified borrowers at competitive rates and providing insurance and related services. Nearing our 100th anniversary, the System has: Assets in excess of $246 billion Nearly 500,000 member-borrowers More than 12,000 employees Coverage in every county in all 50 states plus Washington DC and Puerto Rico At December 31, 2012, the System was comprised of three Farm Credit Banks, one Agricultural Credit Bank and 82 Associations across the nation. Farm Credit System entities have specific lending authorities within their chartered territories. Farm Credit System Banks and Associations are subject to examination and regulation by an independent federal agency, the Farm Credit Administration (FCA). The Federal Farm Credit Banks Funding Corporation (the Funding Corporation) issues a variety of Federal Farm Credit Banks Consolidated Systemwide Debt Securities with broad ranges of maturities and structures on behalf of the Farm Credit System Banks. The Farm Credit System Insurance Corporation insures the timely payment of principal and interest on insured notes, bonds, and other obligations issued on behalf of Farm Credit System Banks. The Farm Credit System 2012 Annual Information Statement, issued by the Funding Corporation, includes additional information about the Farm Credit System, its funding activities and its combined financial results. You can obtain a copy of that report by contacting the Funding Corporation or visiting their website. Their contact information is located at the end of this annual report. 2

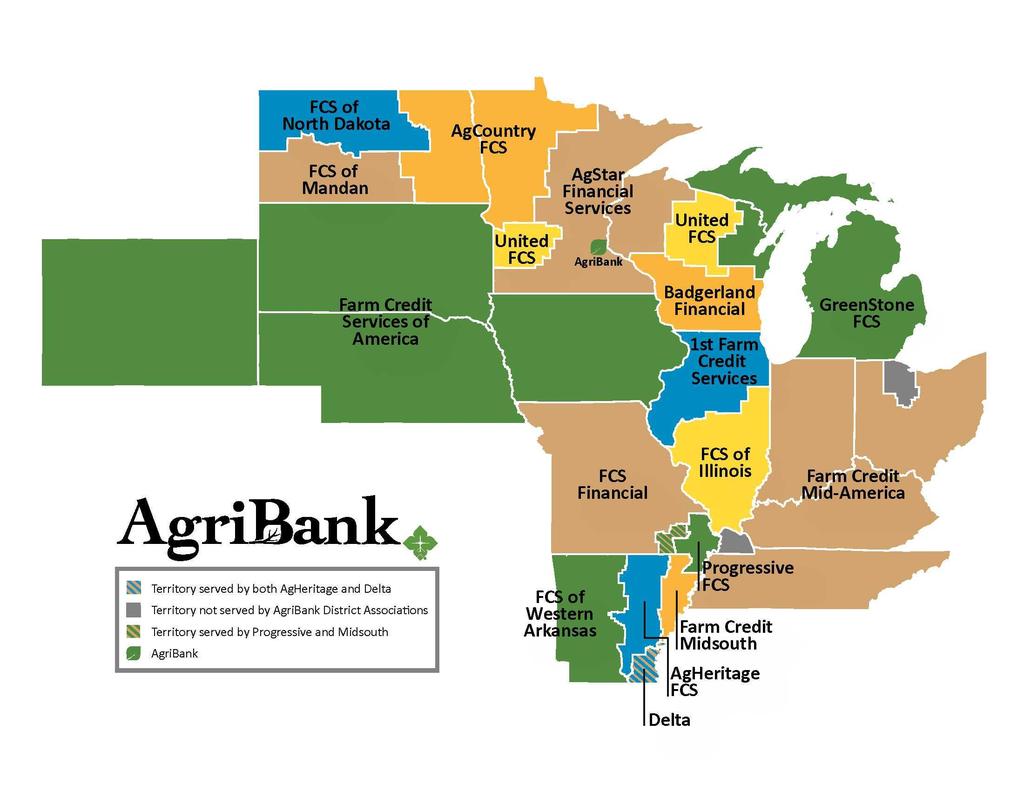

5 AgriBank and Affiliated Associations AgriBank is owned by 17 affiliated Farm Credit Associations and other financial institution (OFI) customers. AgriBank, FCB and affiliated Associations are collectively referred to as the District. AgriBank and affiliated Associations have more than $93 billion in assets. The District covers America s Midwest, a fifteen state area from Wyoming to Ohio and Minnesota to Arkansas. More than half of the nation s cropland is located within the AgriBank District. Basis of Presentation The combined financial statements and related financial information found in this Annual Report include the accounts of AgriBank and its affiliated Associations and related entities. These financial statements are presented on a combined basis due to the financial and operational interdependence of the District entities. This interdependence results, in part, from the fact that AgriBank serves as an intermediary between the financial markets and the retail lending activities of the affiliated Associations. As a result, the loans made by the Associations to the borrowers are substantially funded by Systemwide debt securities issued by AgriBank. AgriBank s ability to repay the Systemwide debt securities is dependent upon the ability of the Association borrowers to repay their loans. In the combined financial statements, the accounts of the individual District entities are combined and all significant intra-district transactions and balances are eliminated. Risk Management Risk is inherent in our business and sound risk management practices are a fundamental component of our operations. AgriBank s prudent and disciplined approach to risk management includes a formal enterprise risk management structure established to identify emerging risks and evaluate risk implications of the decisions and actions of AgriBank and others while these practices vary by entity, the overarching goals of our collective enterprise risk management practices are to: effectively assess, prioritize, monitor and report key organizational risks enhancing our ability to achieve our business objectives; embed a risk-aware culture throughout the District; identify and implement strategies to mitigate risk where appropriate; and ensure we are adequately compensated for the risks that we take. The Board of Directors of each of the entities within the District oversee risk management by adopting policies to guide the organization s risk tolerance and by monitoring performance against established risk limits. Within each Board s risk framework and limits, management establishes controls to guide the day-to-day risk management activities of the organization. Each Board, through its Audit Committee, also monitors risk management and policy compliance through the Internal Audit function. Information on some of the major types of risk inherent in our business follows: Credit risk is the risk of loss arising from a borrower or counterparty failing to perform on an obligation. Our primary sources of credit risk are our lending activities, investment portfolio and derivative contracts. We are also exposed to credit risk under our joint and several liability for Systemwide debt securities. 3

6 Interest rate risk is the risk that changes in interest rates may adversely affect operating results and financial condition. Our interest rate risk arises primarily from financing fixed rate instruments that can be prepaid, adjustable rate loans with interest rate caps and from decisions related to the investment of our equity. Substantially all of interest rate risk is managed by AgriBank. Liquidity risk is the risk of loss arising from the inability to meet obligations when they come due without incurring excessive costs. Our primary source of liquidity is access to the debt markets, which could be temporarily disrupted or available only by paying a high rate of interest. A secondary source of liquidity is provided by AgriBank s investment portfolio. Events or concerns in a particular sector could result in segments of AgriBank s investment portfolio becoming illiquid or liquid only at a severe discount to carrying value. Operational risk is the risk of loss resulting from inadequate or failed internal processes or systems, errors by employees or from external events. Reputation risk is the risk of loss resulting from events, real or perceived, that shape the image of the Farm Credit System or any of its entities. Such risks include the impact of investors perceptions about agriculture, the reliability of the Farm Credit System financial information, or the overt actions of any Farm Credit System Institution. These risks, and the methods we use to manage them, are discussed in the following sections. District Merger Activity On January 1, 2008, AgCountry Farm Credit Services, ACA and Farm Credit Services of Grand Forks, ACA consolidated to form a new Association known as AgCountry Farm Credit Services, ACA. Simultaneously, the subsidiaries of Farm Credit Services of Grand Forks, ACA merged into the subsidiaries of AgCountry Farm Credit Services, ACA. The associations had been operating under a joint management agreement since April 1, The consolidation was accounted for on a historical cost basis similar to that of a pooling of interests. Forward-Looking Information This Annual Report includes, and our representatives may from time to time make, projections concerning financial information and statements concerning future economic performance and events, plans and objectives relating to management, operations, products and services, and assumptions underlying these projections and statements. These projections and statements are not historical facts but instead represent only our belief regarding future events, many of which, by their nature, are inherently uncertain and outside our control. These projections and statements may address, among other things, business strategy, competitive strengths, goals, market and industry developments and the growth of our businesses and operations. The words anticipate, believe, estimate, expect, intend and similar expressions, as they relate to the District or its management, are intended to identify forward looking statements. Such statements reflect the current views of the District with respect to future events and are subject to certain risks, uncertainties and assumptions, including the risk factors described in this Annual Report. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein as anticipated, believed, estimated, expected or intended. 4

7 Such forward looking statements are not guarantees of future performance and involve risks and uncertainties and actual results may differ from those in the forward looking statements as a result of various factors. The information contained in this Annual Report, including without limitation, the information under Management s Discussion and Analysis identifies important factors that could cause such differences, including but not limited to a change in the U.S. agricultural economy, overall economic conditions, changes in market rates of interest and the effect of new legislation or government regulations or directives. However, actual results and developments may differ materially from our expectations and predictions due to a number of risks and uncertainties, many of which are beyond our control. These risks and uncertainties include, but are not limited to: political, legal, regulatory, financial markets and economic conditions and developments in the U.S. and abroad; economic fluctuations in the agricultural, international and farm-related business sectors; weather-related, disease and other adverse climatic or biological conditions that periodically occur that impact agricultural productivity and income; changes in U.S. government support of the agricultural industry and the Farm Credit System as a government-sponsored enterprise, as well as investor and rating agency reactions to events involving the U.S. government, other government-sponsored enterprises and other financial institutions; actions taken by the Federal Reserve System in implementing monetary policy; credit, interest rate and liquidity risk inherent in our lending activities; and changes in our assumptions for determining the allowance for loan losses, other than temporary impairment and fair value measurements. Refer to additional discussion in the Risk Factors section at the end of this report. Critical Accounting Policies Our combined financial statements are reported based on accounting principles generally accepted in the United States of America and require that significant judgment be applied to various accounting, reporting and disclosure matters. We use assumptions and estimates to apply these principles where actual measurement is not possible or practical. For a complete discussion of significant accounting policies, refer to Note 2 of the accompanying combined financial statements. The following is a summary of certain critical accounting policies: Allowance for loan losses The allowance for loan losses is our best estimate of the amount of losses on loans in our portfolio as of the date of the financial statements. We determine the allowance for loan losses based on a periodic evaluation of our loan portfolio, which considers loan loss history, probability of default, estimated loss severity, portfolio quality and current economic and environmental conditions. Refer to the Loan Portfolio Analysis of the Allowance for Loan Losses section for further discussion. Valuation methods We apply various valuation methods to assets and liabilities that often involve judgment, particularly when liquid markets do not exist for the particular items being valued. Quoted market prices are referred to when estimating fair values for certain assets, such as certain investment securities. However, for those items for which an observable active market does not exist, management utilizes significant estimates and assumptions to value such items. These valuations require the use of various assumptions, including, among others, discount rates, rates of return on assets, repayment rates, cash flows, default rates, loss severity rates, third party prices, costs of servicing and liquidation values. The use of different assumptions could produce significantly different results. 5

8 Financial Overview Our financial performance reflected strong earnings and continued loan growth for We recorded record net income of $1.7 billion in 2012, an increase of $179.6 million or 11.7% from one year ago. The most significant drivers were increases in net interest income of $139.2 million and non-interest income of $72.7 million (primarily a non-recurring distribution received from the Farm Credit System Allocated Insurance Reserve Accounts (AIRA) and mineral income) and a decrease in provision for income taxes of $16.6 million. These favorable variances were partially offset by increases in non-interest expenses and provision for credit losses of $38.6 million and $10.3 million, respectively. Refer to the Results of Operations section for further explanation of these changes. Loan Portfolio The components of loans are presented in the accompanying table: (in millions) As of December 31, Accrual loans: Real estate mortgage $43,388.4 $37,783.6 $35,110.6 $32,663.8 $31,350.4 Production and intermediate term 21, , , , ,838.8 Agribusiness 6, , , , ,053.7 Rural residential real estate 2, , , , ,005.2 Other 3, , , , ,074.6 Nonaccrual loans , Total loans $77,089.1 $68,349.6 $65,035.1 $60,245.5 $57,151.7 The other category is primarily comprised of communication and energy related loans and finance leases as well as AgriBank s loans to other financial institutions (OFIs) and loans originated under our Mission Related Investment authority. All of these categories have seen growth during The increase in total loans from December 31, 2011 was primarily in the real estate mortgage sector driven by demand for cropland. In addition, following seasonal patterns, loans increased significantly in December 2012 as borrowers increased their operating lines as they purchased 2013 production inputs primarily for tax planning strategies. The seasonal increase was magnified by increased real estate activity, which in part was spurred by uncertainty regarding potential tax law changes as of January 1, Beginning in April 2011, AgriBank began participating in the AgDirect program. The increase in the production and intermediate term sector from December 31, 2011 was primarily driven by this program. Under this program, AgriBank purchases 100% loan participation interests in retail equipment financing loans from AgDirect LLP (LLP), a Limited Liability Partnership. At December 31, 2012, the LLP was owned by five District Associations and four Associations from outside the District. Our loan portfolio exhibits some seasonality relating to the patterns of operating loans made to crop producers. Loans are normally at lowest levels during the winter months because of repayments following harvest and then increase throughout the year due to borrowings to fund operating needs, although we do see temporary increases in operating loans in December primarily due to tax planning strategies. 6

9 Loan Credit Risk Management The eligible borrowers, to whom we are authorized to make loans or participate in loans made to, are specified under the Farm Credit Act. As a result, our loan portfolio is concentrated in the agricultural industry. Earnings, loan growth and the credit quality of our loan portfolio can be affected significantly by the general state of the economy primarily as it affects agriculture and users of agricultural products. We actively manage our credit risk through various policies and standards, including our loan committees reviewing significant loan transactions. Underwriting standards include analysis of five credit factors: repayment capacity, capital position, collateral, management ability and loan terms. These standards vary by agricultural sector and are updated to reflect current market conditions. Many of the credits in our portfolio are large and complex and we do not use standardized credit scoring on these loans. Loans under $250 thousand comprise 90.8% of District customers by number and 38.5% of our loan volume. Associations generally use statistically validated scorecards to evaluate smaller credits. We use credit factors to evaluate, identify and disclose risk in our loan portfolio based on the FCA s Uniform Classification System. We assign an asset quality classification to each loan in our loan portfolio within the following categories: Acceptable assets are non-criticized assets representing the highest quality. They are expected to be fully collectible. This category is further differentiated into various probabilities of default; Other Assets Especially Mentioned (Special Mention) assets are currently collectible but exhibit some potential weakness. These assets involve increased credit risk, but not to the point of justifying a substandard classification; Substandard assets exhibit some serious weakness in repayment capacity, equity and/or collateral pledged on the loan; Doubtful assets exhibit similar weaknesses as substandard assets. However, doubtful assets have additional weaknesses in existing factors, conditions and values that make collection in full highly questionable; and Loss assets are considered uncollectible. 7

10 The following table presents the credit quality of our loan portfolio under the FCA Uniform Loan Classification System by loan type (accruing loans include accrued interest receivable): (in millions) As of December 31, 2012 Acceptable Special mention Substandard/Doubtful Total Real estate mortgage $42, % $ % $1, % $44, % Production and intermediate term 20, % % % 21, % Agribusiness 5, % % % 6, % Rural residential real estate 2, % % % 2, % Other 3, % % % 3, % Total loans $74, % $1, % $2, % $77, % (in millions) As of December 31, 2011 Acceptable Special mention Substandard/Doubtful Total Real estate mortgage $36, % $ % $1, % $38, % Production and intermediate term 18, % % % 19, % Agribusiness 5, % % % 5, % Rural residential real estate 2, % % % 2, % Other 2, % % % 2, % Total loans $64, % $1, % $2, % $69, % (in millions) As of December 31, 2010 Acceptable Special mention Substandard/Doubtful Total Real estate mortgage $33, % $1, % $1, % $36, % Production and intermediate term 17, % % % 18, % Agribusiness 5, % % % 6, % Rural residential real estate 2, % % % 2, % Other 2, % % % 2, % Total loans $60, % $2, % $2, % $65, % The credit quality of our loan portfolio remains strong at December 31, 2012 with 97.4% of our portfolio in the acceptable and special mention categories compared to 96.8% and 95.5% at December 31, 2011 and 2010, respectively. Agriculture has experienced mostly positive economic conditions over the past decade. However, agriculture is a cyclical industry and is expected to experience periodic downturns. In addition to the FCA s Uniform Classification System, we also use a two-dimensional loan rating model that incorporates a 14-point probability of default scale to identify and track the probability of borrower default and a separate 6-tier scale addressing loss given default over a period of time. Each of the probability of default rating categories carries a distinct percentage of default probability. The 14-point probability of default scale provides for granularity of the probability of default, especially in the acceptable ratings. There are 9 acceptable categories that range from a borrower of the highest quality to a borrower of minimally acceptable quality. The range of probabilities of default between 1 and 9 is very narrow and would reflect almost no default to a minimal default percentage. The probability of default increases more rapidly as a loan moves from a 9 to a 10 and increases significantly as a loan moves to an 11. A 12 or worse rating indicates that default is almost certain. The 6-tier scale for loss given default measures the expected loss severity based upon the adequacy of the collateral supporting the loan. A substantial portion of the loan portfolio is collateralized, which reduces our exposure to credit losses. Additionally, our credit policies reduce credit risk with emphasis placed on repayment capacity rather than exclusively on the underlying collateral. Although FCA regulations allow real estate 8

11 mortgage loans of up to 85% of appraised value, our underwriting standards generally allow only 65%. While underwriting exceptions on loan to appraised value are granted, they are often structured with additional principal payments in the early years. Refer to further discussion within the Land Values portion of the Agricultural Conditions section of this report. Borrower and commodity concentration lending limits have been established to manage credit exposure. The lending limit to a single borrower, as set out in the Associations General Financing Agreement (GFA) with AgriBank, is generally 15% of each Association s permanent capital. We reduce credit risk in the loan portfolio through government guarantee programs. At December 31, 2012, $1.7 billion of loans contained various levels of guarantees under such programs. One Association has reduced risk in their loan portfolios through the use of credit default swaps in connection with synthetic securitizations. The amount of loans under credit default swaps was $417.7 million at December 31, During 2012, another Association terminated its credit default swap agreement. We also manage credit risk through loan participations. We diversify our portfolio and limit our exposure to an individual borrower or commodity through buying and selling loans to other institutions within or outside of the Farm Credit System. Managing loans through participations also allows us to manage growth and capital primarily to improve geographic or commodity diversification. Portfolio Maturities The contractual maturities of loans were as follows: (in thousands) Over One One Year Through Over Five As of December 31, 2012 or Less Five Years Years Total Real estate mortgage $4,742,842 $15,931,999 $23,133,979 $43,808,820 Production and intermediate term 10,873,031 9,629, ,522 21,293,391 Agribusiness 3,124,751 2,228,075 1,049,959 6,402,785 Rural residential real estate 160, ,038 1,707,705 2,501,794 Other 1,413,630 1,000, ,288 3,082,344 Total loans $20,314,305 $29,424,376 $27,350,453 $77,089,134 Total of loans due after one year with: Fixed interest rates $25,703,320 Variable and adjustable interest rates 31,071,509 9

12 Portfolio Diversification Loan concentrations exist when amounts loaned to multiple borrowers engaged in similar activities, or within close proximity, would cause them to be similarly affected by economic or other conditions. The charts below illustrate commodity and geographic distribution of our portfolio as of December 31, 2012: Poultry, 3% Food products, 3% Ethanol, 1% Investor real estate, 5% Residential real estate, 5% District Portfolio Commodity Distribution Timber, 3% Other, 10% Dairy, 8% Cattle, 9% Pork, 5% Crops, 48% District Portfolio State Distribution Iowa 12% Illinois 10% Minnesota 9% Nebraska 8% Indiana 6% Wisconsin 6% Michigan 6% Ohio 6% Tennessee 5% South Dakota 5% Missouri 5% Kentucky 4% North Dakota 4% Arkansas 3% Wyoming 1% Other states 10% 100% While the portfolio has concentrations in crops, these crops represent staple commodities of agriculture corn, soybeans and wheat. There is diversification of these crops geographically with multiple states being significant producers of these important crops. There is further concentration in crops to some extent in the investor real estate loans. These loans are typically made for the purchase of land that is rented for crop production. Certain Associations have diversified the concentration in agricultural production through rural residential real estate and part-time farmer loans as well as agribusiness loans. Rural residential real estate, investor real estate and part-time farmer borrowers (agri-consumers) generally have significant off-farm sources of income, and therefore, are less subject to cycles in agriculture. These borrowers have been more susceptible to changes in the general economy and the condition of the general economy will influence the credit quality of these segments of the portfolio. It is important to note the counter-cyclical diversification effect of grain and livestock production. High grain prices are generally favorable to crop producers; however, livestock producers are adversely affected through higher feed costs. Conversely, low grain prices are generally negative to crop producers but tend to improve the profitability for those livestock producers who purchase most or all of their feed. Extreme volatility in commodity prices can negatively impact our District producers. The ten largest customers as of December 31, 2012 represented 2.2% of total loans (includes accrued interest receivable). Small loans (less than $250 thousand) account for 90.8% of District customers by number and 38.5% of our loan volume. Credit risk on small loans is usually reduced by non-farm income sources. Loans under $250 thousand are generally evaluated using statistically validated scorecards. The scorecards widely used by District institutions are related to operating, intermediate term (generally for farm equipment), agricultural mortgage and home mortgage loans. At December 31, 2012, we had 365 thousand scored loans, 10

13 or 62.2% by number of loans of the portfolio representing $14.7 billion, or 18.8% of total loans (includes accrued interest receivable), of which only 0.9% were delinquent. Of the ten largest customers, 98.9% of these loans were classified as acceptable, and 1.1% were classified as special mention. Within these ten largest customers there are concentrations in three significant industries: food products at 28.2%; farm machinery and equipment at 25.2%; and timber at 20.3%. Agricultural Conditions The United States Department of Agriculture (USDA) projects that U.S. net farm income will decline $5.1 billion in 2012, to $112.8 billion, when compared to the $117.9 billion for Net cash income is expected to increase by $0.9 billion, to $135.6 billion when compared to the previous record of $134.7 billion in The increase in net cash income was driven by an $11.4 billion reduction in inventory levels. The farm sector s debtto-asset ratio for 2012 is now forecasted at 10.6% which is incrementally stronger than 2011 at 10.7% net farm income is forecasted at $128.2 billion which is up 14% from The value of feed grain and oil seed crop production is forecasted to rise in 2013 as large production increases more than offset expected price declines. The 2013 forecast assumes a return to trend in crop yields and production following the 2012 U.S. drought. A 3.5% increase is forecasted in the value of livestock, dairy and poultry production production expenses are forecasted up $19.2 billion or 5.7% and continue a string of large year-over-year increases. Direct government payments to farmers, excluding the crop insurance program, are forecasted to remain steady in 2013 as compared to The farm sector s debt-to-asset ratio for 2013 is forecasted at 10.2% reflecting continued improvement. Drought Impact Extensive drought in the U.S., particularly in the Midwest, has reduced crop yields, resulting in increased crop prices. Multi-peril crop insurance (MPCI) will generally mitigate the economic impact of the drought for most crop producers. These insurance policies range in coverage levels from catastrophic and yield protection (at the lower end) to revenue protection (at the higher end). The MPCI policies are sold and serviced through private insurance companies designated by the USDA to provide insurance coverage. These companies share the risk of loss by reinsuring with large reinsurance companies. In addition, the USDA and its Federal Crop Insurance Corporation reinsures a portion of the risk along with the other private reinsurance companies. The USDA has reported that 84% of corn and soybean acres (collectively) were covered under MPCI in This is modestly lower than the 88% and 85% for corn and soybeans, respectively, covered in The majority of these policies provide for revenue protection. In addition, many crop producers have strengthened their financial positions over the past several years and are expected to withstand the financial impact of the drought. However, increased prices for corn and soybeans and other grains are placing pressure on livestock, poultry, ethanol and dairy producers who rely on these inputs. Some producers mitigated a portion of this risk by locking in prices for these inputs for However, some users of corn and soybeans in our portfolio will be unable to avoid some level of losses in Land Values Monitoring of agricultural land values is extensive within the District. The AgriBank District conducts an annual Benchmark Survey, completed by licensed real estate appraisers, of a sample of benchmark farms selected to represent the lending footprint of associations throughout the District. The District s most recent real estate market value survey indicated that District real estate values, on average, increased 15.7% over the twelvemonth period ending June 30, Qualitative surveys of lending officers compiled by the Federal Reserve Banks of Chicago, Kansas City and Minneapolis as of the end of the third quarter 2012 also indicated sharply 11

14 increasing farmland values. The Federal Reserve Banks survey cited year-over-year increase in the average value of non-irrigated farmland of 13% to 26%. Declining land values are a potential lending risk following periods of sustained, rapid land value increases. Nominal and real (inflation-adjusted) agricultural land values have increased in proportions greater than other asset classes such as stocks and urban residential and commercial land during the last decade, but District agricultural land values have, for the most part, escaped the valuation declines that other assets suffered during the recession. This is largely because the agricultural sector, particularly crop farming, has remained profitable throughout the economic crisis period, and demand for agricultural land has remained very strong. AgriBank District credit risk policies focus on loan repayment capacity in addition to conservative loan-to-value levels on the collateral that secure loans. Although FCA regulations allow real estate mortgage loans of up to 85% of appraised value, our underwriting standards generally limit lending to no more than 65% at origination. Due to very strong land values in much of our District, many Associations have implemented risk management practices that incorporate loan-to-appraised value thresholds below 65%. In addition, many District lenders impose lending caps per acre based on the land s sustainable income-producing capacity. While underwriting exceptions on loan-to-appraised-value are sometimes granted, in such cases loans are typically structured with shorter amortization schedules and/or additional principal payments in the early years to reduce risk. Specific Industry Conditions Specific conditions for our primary commodity exposures are discussed below. The commodity information was obtained from USDA National Agricultural Statistics Service publications as of December 31, Comparative amounts are the most recently published information, if revised. The commodity information for eggs was obtained from the Midwest Urner Barry report. 12/31/2012 9/30/2012 6/30/2012 3/31/ /31/2011 Crops Overall (Index) Corn ($ per bushel) Soybeans ($ per bushel) Wheat (all, $ per bushel) Cattle (all, $ per hundredweight) Hog (all, $ per hundredweight) Dairy ($ per hundredweight) Broilers ($ per pound) Eggs ($ per dozen) Rice ($ per hundredweight) Cotton ($ per pound) Crops Crops represent 48% of the District loan portfolio. Crop producers have enjoyed several years of strong income driven by favorable commodity prices. Prices have been driven by export demand for feed grains and animal protein as well as the expanded use of grains for bio-fuel production and by the impact of reduced yields from the drought in Therefore, District credit quality in this segment was strong with only 1.3% adversely classified at December 31, With dramatically lower than expected corn and soybean production due to the widespread drought, prices increased materially during the third quarter but moderated some during the fourth quarter of Further, with most producers having crop insurance protection, and a significant portion taking advantage of the revenue protection provision, we expect grain producer incomes to remain favorable. Strong liquidity and equity positions should be maintained and we expect continued favorable credit quality in this portfolio segment during the next 12 months. Domestic stocks of corn and soybeans are expected to be at 12

15 historically low levels, negatively impacting industries which use those commodities for inputs and ultimately the end user consumers. Corn: The 2012 corn crop was originally estimated to be 14.8 billion bushels by the USDA, up significantly from the 12.4 billion bushels in 2011 and However, the hot and dry weather throughout the corn belt during the 2012 growing season reduced yields substantially. While trend-line yields suggested a 166 bushel yield could be expected, adverse weather reduced yields to the current forecast of 123 bushels per acre. Planted acres for the 2012 corn crop were significantly higher than prior years with 97 million planted acres compared to 92 million planted acres in 2011 and 88 million planted acres in This is the most acres planted to corn since the 1930 s. Based on these factors, a 10.8 billion bushel corn crop is now projected for The 2011 / 2012 marketing year carryout-to-use ratio was already historically tight at 7.9%. The 2012 / 2013 marketing year projected carryout-to-use ratio of 5.6% would indicate the need for demand rationing. Feed use demand and exports are projected to bear the brunt of this rationing with a 1.0 billion bushel reduction in feed usage and a 1.0 billion bushel reduction in exports as compared to initial USDA estimates. Also, projected is a reduction of 500 million bushels for ethanol production as compared to original USDA estimates. Soybeans: Soybean production for 2012 was estimated at 3.2 billion bushels, but the hot and dry weather throughout the central U.S. has reduced yield estimates from 43.9 bushels per acre to 39.6 bushels per acre in the latest USDA World Agricultural Supply and Demand Estimates report. Therefore, soybean production estimates have fallen to 3.0 billion bushels. The drop in the production estimate was partially buffered by a 3.3 million increase in planted acres from the original estimate of 73.9 million acres to the latest USDA estimate of 77.2 million acres. Production in 2011 and 2010 measured 3.1 billion and 3.3 billion bushels, respectively. As was the case with corn, soybeans ended the 2011 / 2012 market year with extremely tight stocks reflected in an ending carryout-to-use ratio of 5.4%. Another short crop in 2012 implies rationing of available soybean supplies with an ending carryout-to-use ratio projected at 4.1%. Most of the demand rationing so far has occurred in exports, which have been reduced by 160 million bushels from the original estimate. Wheat: Estimated planted wheat acreage for 2012 is 55.7 million acres, up 2.4% from Yield per acre for 2012 is now estimated at 46.3 bushels per acre, up 0.6 bushels from the initial USDA estimate and 5.9% larger than the drought-reduced 2011 yield of 43.7 bushels per acre. Projected 2012 production is 2.3 billion bushels. The combination of a larger wheat crop, poor projected wheat crops in the former Soviet Union and Australia, and tighter corn and soybean stocks has resulted in a 219 million bushel increase in total use to 2.5 billion bushels. Ending carryout stocks for the 2012 / 2013 marketing year are projected at 28.2% which is down from a 33.3% carryout-to-use ratio for the 2011 / 2012 marketing year. Livestock Cattle: Cattle represent 9% of the District loan portfolio. This segment consists of two different and distinct risk categories: cow/calf producers and cattle feedlots. At December 31, 2012, 2.5% of the cattle portfolio was adversely classified. Cow/calf: Cow/calf producers are typically small, many of whom are supported with off-farm income. While these producers typically do not generate large profits, they generally are well capitalized and represent limited credit loss exposure. They continue to represent about 75% of the total cattle portfolio. The District has cow/calf producers in almost all 15 states, with the heaviest concentrations in Tennessee, Kentucky, Nebraska, Missouri, North Dakota and South Dakota. Cattle Feedlots: Cattle feedlot producers generally operate with higher leverage, having solvency positions of 25-40%. Feedlot operator profitability is highly variable as they are dependent upon the price 13

16 difference between feeder and slaughter prices for cattle, and the cost of weight gain which is directly tied to grain prices. The District s exposure to this sector is about 25% of the total cattle portfolio and most feedlots are concentrated in Nebraska, South Dakota and Iowa. The U.S. beef cow herd size is now the smallest it has been since the early 1970 s and has declined further throughout Projections are that the beef cow herd will continue to shrink in Both feedlot and cow/calf operations have faced higher breakeven price levels in 2012 due to the continued high price of corn, other feed stocks for cattle feedlots and high hay costs for cow/calf producers. However, cow/calf operators have received record or near record prices for feeder cattle for most of this year and for those operators that have adequate pasture or feedstock, the demand for feeder cattle should provide opportunities for solid profits for the next 2-3 years. For those operators in the areas hardest hit by this year s drought, selling calves earlier than normal and liquidating cow herds has been very common. Despite a trend of increasing exports, albeit down in 2012 compared to 2011 levels, and record or near record high fed cattle prices in much of 2011 and 2012, most feedlots operators have experienced negative operating margins (prior to any risk management strategies) due to the high costs of feeder cattle, feed stocks and energy. The feedlot segment lost money in 2012 and projects to be unprofitable into the first half of Operators will need to use strong risk management practices to remain above breakeven for Dairy: Dairy represents 8% of the District loan portfolio. At December 31, 2012, 6.4% of the dairy portfolio was adversely classified. Most Midwest dairy producers should report profitable operations in The relatively high cost of feed was offset by strong milk prices, especially in the last quarter of The ratio of milk price to feed cost was higher during the last three months of the year than for all previous months except January. The outlook for 2013 has dampened somewhat with weaker demand driving a reduction in milk price. However, the market continues to present opportunities to capture positive margins over average cost of production. No significant change in dairy portfolio credit quality, either positive or negative, is anticipated at this time. Pork: Pork represents 5% of the District loan portfolio. At December 31, 2012, 3.7% of the pork portfolio was adversely classified. A large portion of U.S. pork production is concentrated in Iowa, Minnesota, Nebraska, Indiana and Illinois. The industry was, for the most part, profitable in 2010, 2011 and 2012, allowing for substantial recovery of losses incurred in previous years ( ). Many producers have been able to build working capital levels necessary to weather the losses associated with the rapid and extreme price increases of corn and soybeans that occurred as a result of the short 2012 crop. The current outlook is that those producers with limited use of available risk management tools will likely incur losses during the first half of Robust price risk and margin management practices by some producers will partially mitigate the losses expected in the first half of the year. However extreme volatility remains in this industry. Due to the relative strength of producer balance sheets and the relatively wide use of risk management practices in the industry entering this downturn, credit quality is expected to remain fairly stable in the near term. Poultry Poultry represents 3% of the District loan portfolio. At December 31, 2012, 6.4% of the poultry portfolio was adversely classified. Broilers: Much of the District s broiler exposure is to contract growers. Over 90% of U.S. broiler production is contracted through poultry integrators (processors) represented the worst prolonged period of losses in broiler industry history due to the combination of sharply higher feed costs and oversupply of broiler meat. The industry responded to losses in 2011 with significant reductions in egg sets and chick placements in late 2011 and throughout Due to these production cutbacks and resulting lower cold storage stocks, prices improved 14

17 substantially throughout With stronger prices, easing of feed costs and record export levels, the industry achieved profitability and improved balance sheets throughout most of However, the 2012 U.S. drought has driven up feed costs again, resulting in modest losses for some in the industry in late 2012 and continuing into However, the broiler industry is in a better position today than two years ago to withstand higher feed costs due to continued management of production levels and strong broiler market pricing. Therefore, while some downgrades are likely in 2013, credit quality is expected to remain relatively stable. Turkeys: The turkey industry has enjoyed three years of profitability due to well controlled production, steady domestic demand and record export demand. Record prices continued throughout However, with an estimated 3% production increase in 2012 and the recent sharp rise in feed costs, profitability is likely to be challenged in Production is forecasted to decrease by 3% in 2013 in response to higher feed costs. Due to the balance sheet strength built up by the industry over the past three years credit quality is expected to remain relatively stable in Eggs: Egg prices improved modestly during 2012 averaging $1.23 per dozen in 2012 compared to $1.19 per dozen in Liquid egg prices were up slightly in 2012 compared to prices in 2011, at $0.64 per dozen vs. $0.62, respectively. The industry has continued to generally manage the overall flock size and supplies are generally in line with demand. However, projections for year end 2012 suggest a 1.7% increase in hen numbers year-over-year which is projected to have a modest negative impact on overall egg prices in Continued high feed costs have stressed producer margins but with overall higher 2012 egg prices, most egg producers should be marginally profitable for the year. Overall, with pricing expectations being slightly lower in 2013, and continued high costs of production, tighter margins are expected. While some downgrades are possible in 2013, credit quality is expected to remain relatively stable. Other Timber: Timber and wood products represent 3% of the District loan portfolio. At December 31, 2012, 4.8% of the timber portfolio was adversely classified. The timber and forest products industry has seen limited new loan activity in recent years due to the weak economy and the continued weak housing market. However, housing starts, although well below levels of , are showing improvement which is fostering some guarded optimism in the industry. U.S. housing starts are now projected to be at 800,000+ on a seasonally adjusted basis, well above the low point of 450,000 starts. The continued slow economic growth and high levels of unemployment continue to challenge the industry. Improvement in the housing markets is expected to be gradual over the next 2-3 years with starts projected to increase to 1,000,000 by Minimal improvement in credit quality can be expected until there is a significant housing recovery. We expect limited loan losses due to generally strong (low) and stable loan to appraised value positions for most loan exposures. Additionally, the District s timber exposure is primarily in timber production supported by land rather than timber processing. Ethanol: The District has ethanol exposure of approximately 1% of the District portfolio. At December 31, 2012, 10.8% of the ethanol portfolio was adversely classified. Margin pressure continued as a result of high priced corn, lower than expected motor fuel prices and excess ethanol inventory, resulting in losses for many producers throughout Although ethanol inventories are expected to decline, resulting in improved margins, the timing of the anticipated recovery is uncertain. While District ethanol exposure is relatively small, the impact of ethanol within the District is amplified due to ethanol s use of corn, and its relationship to corn prices. Production capacity in the industry is static, with essentially no new capacity contemplated at this time. The Renewable Fuels Standard (RFS) level for corn based ethanol in calendar year 2012 was 13.2 billion gallons and increased to 13.8 billion gallons in 2013, ultimately reaching 15 billion gallons in While there have been RFS waiver requests from various groups, these requests have not been granted. With continued 15

18 governmental support of the ethanol industry via RFS, ethanol demand is expected to recover to levels whereby producer margins will improve. We expect this portfolio to show a degree of deterioration in early 2013 and stabilize throughout the year. Other: Although not significant from a District-wide perspective, certain Associations have significant concentrations in rice, cotton and sugar beets. Competitive Conditions Competition historically is from small commercial banks, insurance companies, large banks, manufacturers/suppliers and captive finance companies. In general, community banks continue to be very competitive, and insurance companies and regional/national banks are increasingly more competitive particularly on the highest quality larger credits. Associations market shares vary greatly, with Farm Credit dominating the market in certain Association s territories, while in other territories the competition holds significant market share positions. In our traditional markets, affiliated Associations have historically been most competitive in falling interest rate environments because Farm Credit cost of funds declines more rapidly than that of our competitors. In a rising rate environment, our cost of funds tends to increase more quickly than competitors, resulting in significant competitive pressure and narrowing spreads. Many affiliated Associations have increased their spreads to enhance earnings and to reflect increased risk. Most affiliated Associations anticipate spreads will narrow in 2013 from increased competition which could be exacerbated if there was also an increase in interest rates. An increase in interest rates would create a challenging competitive environment in which the affiliated Associations may not be able, or choose not, to maintain current spreads. During 2012, retail credit spreads, measuring the difference between the rate on the retail loan and the marginal cost of debt (MCD) to fund that loan increased. The increase reflects the increased level of conversions throughout 2012 reflecting the affiliated Associations abilities to re-price borrowers loans at lower interest rates and increase spreads. During 2012, approximately $15.4 billion of retail volume converted resulting in a weighted average MCD savings of 120 basis points between AgriBank and the affiliated Associations, and a weighted average retail rate savings of 77 basis points between the affiliated Associations and the customers. The difference between the MCD the affiliated Associations paid AgriBank and the lower retail rate the affiliated Associations received from the customers was 43 basis points, which increased the retail spread at the affiliated Associations while significantly reducing farmer borrowing costs. 16

19 Analysis of Risk Assets Risk assets are comprised of nonaccrual loans, accruing restructured loans and accruing loans 90 days or more past due (risk loans) and other property owned. Comparative information regarding risk assets in the portfolio follows: (in millions) As of December 31, Nonaccrual loans $700.8 $884.9 $959.8 $1,152.8 $829.0 Accruing restructured loans Accruing loans 90 days or more past due Total risk loans , Other property owned Total risk assets $834.7 $1,033.6 $1,083.1 $1,251.0 $907.3 Risk loans as a % of total loans 0.99% 1.33% 1.50% 1.96% 1.53% Delinquencies as a % of total loans 0.65% 0.74% 0.94% 1.39% 0.95% The decrease in risk assets in 2012 was due primarily to decreases in nonaccrual loans related to repayments, net charge-offs and transfers of loans to accrual status partially offset by transfers to nonaccrual status. The decrease in other property owned was primarily due to the sale of a commercial dairy, a large tract of timber and a lumber concentration yard business at one affiliated Association. Nonaccrual loans represented 0.9% of total loans at December 31, At December 31, 2012, 61.2% of nonaccrual loans were current as to principal and interest. Total risk loans as a percentage of total loans remains within acceptable limits. The decrease in risk assets in 2011 from 2010 was due primarily to decreases in nonaccrual loans related to a customer in accrual status purchasing the assets of a large dairy customer whose loans were previously in nonaccrual status. The decrease in total risk assets in 2010 from 2009 was due to the decrease in nonaccrual loans as a few large customers loans transferred to accrual status during the fourth quarter of These customers were in the pork, dairy and ethanol industries. The increase in other property owned was primarily due to one affiliated Association acquiring a large timber operation during The increase in total risk assets in 2009 from 2008 was primarily due to the increase in nonaccrual loans as a number of accrual loans in the dairy, ethanol and pork industries transferred to nonaccrual status. Our accounting policy generally requires loans past due 90 days to be transferred into nonaccrual status. Based on management's analysis, all accruing loans 90 days or more past due were adequately secured and in the process of collection and, as such, were eligible to remain in accruing status. 17

20 The following table sets forth interest income that would have been recognized if nonaccrual and formally restructured loans had been fully performing: (in thousands) For the year ended December 31, 2012 Interest income which would have been recognized under original contract terms $87,870 Less: interest income recognized 36,503 Interest income not recognized $51,367 Cash received on nonaccrual loans is applied to reduce the recorded investment in the loan asset, except in those cases where the collection of the recorded investment is fully expected and the loan has no unrecovered prior charge-offs. Analysis of the Allowance for Loan Losses The allowance for loan losses is an estimate of losses on loans in our portfolio as of the financial statement date. We determine the appropriate level of allowance for loan losses based on the periodic evaluation of factors such as: loan loss history; probability of default; estimated loss severity; portfolio quality; and current economic and environmental conditions. Comparative allowance coverage of various loan categories is presented in the accompanying table: As of December 31, Allowance as a % of: Loans 0.34% 0.44% 0.62% 0.64% 0.37% Nonaccrual loans 37.52% 33.96% 42.34% 33.49% 25.48% Total risk loans 34.29% 32.65% 41.10% 32.30% 23.78% Net charge-offs as a % of average loans 0.09% 0.18% 0.28% 0.25% 0.00% Adverse loans as a % of risk funds* 14.03% 16.89% 24.65% 29.80% 18.00% *Risk funds includes total capital and allowance for loan losses. AgriBank and affiliated Association management teams believe the allowances are adequate in relation to the probable losses in each portfolio as of December 31, The allowance for loan losses totaled $262.9 million at December 31, 2012 a decline from $300.5 million at December 31, The decline in the allowance for loan losses was primarily driven by net charge-offs of $64.7 million partially offset by provision expense of $27.1 million during The provision for credit losses reported in the Combined Statements of Comprehensive Income includes provision expense for unfunded commitments and unfunded letters of credit of $3.0 million and $3.8 million, respectively. The reserves for unfunded commitments and letters of credit are recorded as liabilities on the Combined Statements of Condition. 18

21 A summary of the activity in the allowance for loan losses follows: (in thousands) For the year ended December 31, Balance at beginning of year $300,508 $406,346 $386,002 $211,254 $101,177 Charge-offs: Real estate mortgage (28,538) (30,938) (60,411) (49,388) (5,241) Production and intermediate term (46,079) (33,922) (84,104) (32,001) (7,180) Agribusiness (1,036) (54,701) (27,749) (63,872) (7,206) Rural residential real estate (7,038) (6,044) (8,798) (5,569) (1,611) Other (260) (16,518) (8,858) (4,422) (1,755) Total charge-offs (82,951) (142,123) (189,920) (155,252) (22,993) Recoveries: Real estate mortgage 8,477 6,306 2,991 2, Production and intermediate term 9,141 12,537 9,476 3,538 1,733 Agribusiness 368 3,399 6,753 2,612 2,970 Rural residential real estate Other ,408 Total recoveries 18,216 22,648 20,351 9,626 6,850 Net charge-offs (64,735) (119,475) (169,569) (145,626) (16,143) Provision for loan losses 27,157 13, , , ,220 Balance at end of year $262,930 $300,508 $406,346 $386,002 $211,254 We determine the amount of allowance that is required by analyzing risk loans individually and all other loans by grouping them into loan segments sharing similar risk characteristics. For loans that were not individually evaluated for impairment we use a two-dimensional loan risk rating model that incorporates a 14-point rating scale to identify and track the probability of borrower default and a separate 6-point scale addressing the loss given default. An allowance is recorded for the loan segments evaluated collectively for probable and estimable credit losses as of the financial statement date based on loss probability and loss severity appropriate for its segment. These estimated losses may be adjusted for relevant current environmental factors. These factors may vary by the different segments reflecting the risk characteristics of each segment. As loss probability, loss severity and environmental factors change, earnings are impacted. Risk loans are analyzed individually to establish specific allowances. We record a specific allowance, if appropriate, to reduce the carrying amount of the risk loan to the lower of book value or the net realizable value of collateral. The following table shows the amount of the allowance for loan losses by loan category: (in thousands) As of December 31, Amount % Amount % Amount % Amount % Amount % Real estate mortgage $94, % $107, % $170, % $115, % $72, % Production and intermediate term 91, % 124, % 145, % 131, % 60, % Agribusiness 48, % 47, % 68, % 123, % 66, % Rural residential real estate 11, % 12, % 12, % 8, % 2, % Other 16, % 8, % 8, % 8, % 9, % Total allowance $262, % $300, % $406, % $386, % $211, % 19

22 Frequency Investment Portfolio and Liquidity Liquidity Risk Management The Farm Credit System continues to have reliable access to the debt capital markets to support its mission of providing credit to farmers, ranchers and other eligible borrowers. During 2012, investor demand for Systemwide debt securities remained favorable across all products and maturities within those products. Given the continued low interest rate environment and demand for Systemwide debt securities, we refinanced callable bonds, when advantageous, in order to lower our cost of funds. AgriBank is responsible for meeting the District's funding, liquidity and asset/liability management needs. Access to funding remains the primary source of AgriBank s liquidity. AgriBank also maintains liquidity through the investment portfolio. AgriBank s liquidity policy and FCA regulations require maintaining a minimum of 90 days of liquidity on a continuous basis, assuming no access to the debt capital markets. This days of liquidity measurement refers to the number of days of maturing debt covered by liquid investments. AgriBank currently operates with a liquidity target of at least 125 days. As of December 31, 2012, AgriBank had sufficient liquidity to fund all debt maturing within 139 days. AgriBank also has a liquidity contingency plan that addresses actions AgriBank would consider in the event that there is not ready access to traditional funding sources. These potential actions include borrowing overnight via federal funds, using investment securities as collateral to borrow, using the proceeds from maturing investments and selling liquid investments. The composition of the liquidity investment portfolio is structured to provide at least 15 days of liquidity coverage in a combination of U.S. Treasury securities maturing within three years, debt to be settled and cash held in Federal Reserve Banks. As of December 31, 2012, AgriBank held U.S. Treasury securities with a book value of $3.2 billion. At December 31, 2012, AgriBank held qualifying assets in excess of that required to meet the 15 days of liquidity coverage. The following chart shows AgriBank s daily liquidity position for 2012: Frequency of Days Liquidity < Liquidity Coverage Range 20

23 Information regarding cumulative debt maturities is outlined below: (in millions) Bonds and Notes As of December 31, 2012 Amount Cumulative debt maturing in: 15 days $3, days 5, days 8, days 10,710.0 One year 24,418.7 One to five years 64,540.7 Five to ten years 73,954.7 More than ten years 77,735.9 AgriBank Investment Securities and Federal Funds AgriBank s liquid investment portfolio is comprised of mortgage-backed securities, U.S. Treasury securities, commercial paper, federal funds, asset-backed securities and U.S. Agency securities. The following table provides detail on the composition of the investment portfolio: (in millions) As of December 31, Mortgage-backed securities: Government collateralized mortgage obligations $2,453.0 $2,291.9 $2,071.6 $1,151.0 $111.6 Agency collateralized mortgage obligations 1, , , , ,729.5 Agency pass through Non-agency Total mortgage-backed securities 4, , , , ,121.6 U.S. Treasury securities 3, , , , Commercial paper and other 2, , , , ,994.6 Federal funds Asset-backed securities: Automobile Home equity Equipment Student loans Credit card receivables Total asset-backed securities U.S. Agencies Total $11,731.9 $9,988.5 $10,647.1 $9,575.1 $9,393.1 AgriBank increased its investment portfolio in 2012 in order to maintain its desired level of liquidity coverage as the loan and debt portfolios grew. With the exception of AgriBank s asset-backed and mortgage-backed securities, the majority of investments mature within one year. The expected average life is 1.6 years for asset-backed securities and 2.9 years for mortgage-backed securities at December 31, A floating rate of interest is carried by 23% of asset-backed securities and 81% of mortgage-backed securities. AgriBank has increased its asset-backed securities in the automobile and equipment segments as these segments have been targeted for growth from a strategic perspective. The characteristics of these segments (liquidity, volume, risk, spread, cash flows) complement the existing investment and loan portfolios. Targeting 21

24 these segments has changed the repricing characteristics of the asset-backed securities portfolio mix from predominately floating to predominately fixed rate. The market for investment securities is materially affected by conditions in the global financial markets and general economic conditions that may change suddenly and dramatically. Unfavorable or uncertain economic and market conditions, caused by declines in economic growth, business activity, investor confidence, limitations on the availability or increases in the cost of credit and capital and increases in inflation or interest rates may adversely affect our business and profitability. AgriBank s Asset-Liability Committee (ALCO) and Investment Credit Risk Group oversee the credit risk in their investment portfolio. AgriBank manages investment portfolio credit risk by investing only in securities that are liquid, of high quality and whose risks are well understood. At purchase all securities must meet eligibility requirements related to rating categories assigned by one or more Nationally Recognized Statistical Rating Organizations. These requirements vary by asset class but require either the highest or second highest ratings. Issues in the residential mortgage market and downgrades of certain bond insurance companies over the past four years increased the credit risk in this sector of their investment portfolio. AgriBank continually monitors the credit risk in this portfolio. 22

25 The fair value of investments by type and credit rating were: (in millions) Eligible Ineligible (2) As of December 31, 2012 AAA/Aaa A1/P1/F1 A2/P2/F2 Split Rated (1) AA/Aa A BBB BB B CCC/Caa CC/Ca C and below Total Mortgage-backed securities $ -- $ -- $ -- $3,955.1 $19.1 $28.5 $16.7 $10.4 $24.5 $64.2 $31.7 $23.4 $4,173.6 U.S. Treasury securities , ,190.6 Commercial paper and other -- 1, ,856.6 Federal funds Asset-backed securities U.S. Agencies Total $419.9 $2,268.8 $ -- $8,722.1 $21.3 $30.1 $26.1 $15.6 $40.5 $125.4 $36.8 $25.3 $11,731.9 (1) Investments that received the highest credit rating from at least one rating organization. (2) Investments that received the indicated rating as the highest rating from at least one rating organization. A substantial portion of split-rated securities are due to the 2011 downgrade of the U.S. government and any related U.S. agency or guaranteed securities. AgriBank does not believe these downgrades are reflective of deterioration in credit quality of these investment securities. At December 31, 2012, AgriBank had securities that, because the ratings were downgraded below AAA, were no longer eligible under the FCA regulations. The fair value of all ineligible investments totaled $321.1 million, including $189.1 million on which AgriBank has taken impairment charges. Of the securities ineligible under the FCA regulations, securities totaling $282.7 million have been approved by the FCA to hold beyond six months and are included in AgriBank s net collateral ratio. Securities with a fair value of $38.4 million were submitted to the FCA for approval during February Effective January 1, 2013, securities that become ineligible no longer require formal FCA approval to hold beyond six months and to include in the net collateral ratio, provided certain conditions are met, including the security having been eligible at the time it was purchased. In addition to the ineligible securities discussed above, AgriBank held split-rated non-agency mortgage-backed securities and home equity assetbacked securities with a fair value of $35.8 million that were downgraded below AAA by at least one rating agency. There are no split-rated securities on which AgriBank has taken impairment. AgriBank also held $4.0 million of home equity asset-backed securities on credit watch negative. 23

26 AgriBank continues to closely monitor its home equity asset-backed securities (ABS) and non-agency mortgage-backed securities (MBS), which are detailed in the table below: (in millions) As of December 31, 2012 As of December 31, 2011 As of December 31, 2010 Amortized Unrealized Unrealized Fair Amortized Unrealized Unrealized Fair Amortized Unrealized Unrealized Fair Cost Gains Losses Value Cost Gains Losses Value Cost Gains Losses Value First liens $117.7 $ -- $20.1 $97.6 $163.9 $ -- $51.7 $112.2 $237.9 $ -- $51.1 $186.8 Second liens Wrapped ABS Total home equity asset-backed securities $139.3 $5.1 $23.7 $120.7 $190.4 $3.7 $58.0 $136.1 $271.9 $1.8 $63.7 $210.0 Alt-A non-agency MBS - floating $12.0 $1.1 $1.5 $11.6 $16.9 $0.8 $4.2 $13.5 $22.0 $0.4 $6.6 $15.8 Alt-A non-agency MBS - fixed Alt-A non-agency MBS - ARM Jumbo non-agency MBS - floating Jumbo non-agency MBS - fixed Jumbo non-agency MBS - ARM Total non-agency mortgage-backed securities $244.8 $6.5 $10.8 $240.5 $300.9 $0.8 $47.9 $253.8 $376.9 $0.5 $63.0 $314.4 Total of above segments $384.1 $11.6 $34.5 $361.2 $491.3 $4.5 $105.9 $389.9 $648.8 $2.3 $126.7 $524.4 (in millions) As of December 31, 2009 As of December 31, 2008 Amortized Unrealized Fair Amortized Unrealized Fair Cost Losses Value Cost Losses Value First liens $334.6 $74.4 $260.2 $498.4 $83.4 $415.0 Second liens Wrapped ABS Total home equity asset-backed securities $391.0 $92.6 $298.4 $608.3 $126.9 $481.4 Alt-A non-agency MBS - floating $30.5 $8.9 $21.6 $47.4 $17.4 $30.0 Alt-A non-agency MBS - fixed Alt-A non-agency MBS - ARM Jumbo non-agency MBS - floating Jumbo non-agency MBS - fixed Jumbo non-agency MBS - ARM Total non-agency mortgage-backed securities $511.0 $129.0 $382.0 $763.1 $218.4 $544.6 Total of above segments $902.0 $221.6 $680.4 $1,371.4 $345.8 $1,

27 Beginning in mid-2007, the home equity ABS and non-agency MBS markets experienced reduced liquidity and credit issues. The liquidity in these markets has improved since AgriBank s exposure on these components of the investment portfolio has been reduced primarily by paydowns and maturities and, to a lesser extent, impairment losses. As demonstrated in the housing related asset-backed and mortgage-backed securities sectors, the liquidity of AgriBank s investment portfolio can be greatly influenced by factors such as U.S. and global economic conditions and liquidity. Accordingly, there is no guarantee our investments could be sold easily or at acceptable prices. In addition, because of the inherent uncertainty and judgment involved in estimating the fair value of investments which may not have an active market, the fair value at which we carry our investments may differ significantly from the values that would be realized if we were to sell the securities. AgriBank evaluates all investments in an unrealized loss position for other-than-temporary impairment (OTTI) on a quarterly basis. As a result of our evaluations, AgriBank recognized $25.5 million in impairment losses during 2012 representing $4.8 million on newly impaired securities and $20.7 million additional impairment on previously impaired securities. No other securities were in an other-than-temporary loss position at December 31, AgriBank has not significantly changed its methodology for identifying securities on which AgriBank performs its cash flow analysis nor has AgriBank significantly changed its methodology for determining fair value during AgriBank evaluates its assumptions used in estimating fair value and impairment and adjusts those assumptions as appropriate. The other-than-temporary impairment recorded in 2012 was similar to the amount recorded in In 2012, the impact of changes in assumptions related to reduced servicers principal and interest advances and eroding credit enhancements on selected transactions contributed to the recorded impairment. AgriBank continued to adjust selected assumptions on certain securities where the specific security information appeared inconsistent with the general assumptions used in our modeling. The following quantifies the impairment recorded: (in millions) For the year ended December 31, Impairment on non-agency MBS $11.2 $11.0 $15.8 Impairment on home-equity ABS Total impairment $25.5 $23.3 $16.0 Reflected in non-interest income in 2010 was a $7.6 million gain from the sale of previously impaired securities. AgriBank recorded $16.6 million of impairment expense in prior years on these securities. 25

28 Association Investment Securities The following table provides detail on the investment portfolios held by affiliated Associations: (in thousands) Weighted Amortized Unrealized Unrealized Fair Average As of December 31, 2012 Cost Gains Losses Value Yield Government guaranteed instruments $1,968,661 $21,922 $34,217 $1,956, % Farmer Mac mortgage-backed securities 302,650 5, , % ARC bonds % Venture capital equity investment 3,235 * * * * Total $2,275,266 $27,318 $34,329 $2,265, % Weighted Amortized Unrealized Unrealized Fair Average As of December 31, 2011 Cost Gains Losses Value Yield Government guaranteed instruments $1,915,583 $19,195 $36,578 $1,898, % Farmer Mac mortgage-backed securities 340,181 7, , % Investment notes in a trust of equipment loans 1, , % ARC bonds 3, , % Venture capital equity investment 1,885 * * * * Total $2,262,747 $26,591 $36,773 $2,250, % Weighted Amortized Unrealized Unrealized Fair Average As of December 31, 2010 Cost Gains Losses Value Yield Government guaranteed instruments $1,593,872 $19,721 $32,396 $1,581, % Farmer Mac mortgage-backed securities 386,935 7,136 1, , % Investment notes in a trust of equipment loans 38,238 1, , % ARC bonds 13, , % Venture capital equity investment 1,234 * * * * Total $2,033,809 $28,409 $34,487 $2,026, % Weighted Amortized Unrealized Unrealized Fair Average As of December 31, 2009 Cost Gains Losses Value Yield Government guaranteed instruments $1,359,322 $9,933 $22,146 $1,347, % Farmer Mac mortgage-backed securities 459,431 9,037 7, , % Investment notes in a trust of equipment loans 41, , % ARC bonds 15, , % Venture capital equity investment 503 * * * * Total $1,876,339 $20,003 $29,916 $1,865, % Weighted Amortized Unrealized Unrealized Fair Average As of December 31, 2008 Cost Gains Losses Value Yield Government guaranteed instruments $991,834 $13,067 $16,199 $988, % Farmer Mac mortgage-backed securities 542, , , % Investment notes in a trust of equipment loans 58, ,266 51, % ARC bonds 18,755 1, , % Venture capital equity investment 250 * * * * Total $1,611,350 $14,467 $45,179 $1,580, % * Not applicable due to the nature of the investment. 26

29 The investment portfolios were evaluated for OTTI. As a result of its evaluations, one affiliated Association has recognized $14 thousand and $570 thousand of impairment losses during 2012 and 2011, respectively. No securities were other-than-temporarily impaired in 2010, 2009 or Other Earning Assets Other earning assets are comprised of successor-in-interest contracts from involvement with the federal government s tobacco buy-out program by one Association. The volume was $144.2 million, $210.9 million, $272.0 million, $321.1 million and $353.3 million at December 31, 2012, 2011, 2010, 2009 and 2008, respectively. These amounts include both principal and interest income receivable. This Association has not purchased any contracts since Results of Operations We recorded record earnings of $1.7 billion in The following table illustrates profitability information: (dollars in millions) For the year ended December 31, Net income $1,719.4 $1,539.8 $1,437.1 Return on average assets 1.98% 1.91% 1.91% Return on average members' equity 12.56% 12.47% 12.98% The following table illustrates the changes in significant components of net income: (in millions) Current Year Prior Year Increase Increase (Decrease) in (Decrease) in For the year ended December 31, Net Income Net Income Net interest income $2,311.5 $2,172.3 $2,052.1 $139.2 $120.2 Provision for credit losses (33.9) (23.6) (189.9) (10.3) Non-interest income (114.0) Salaries and employee benefits (537.8) (515.0) (478.8) (22.8) (36.2) Other operating expenses (284.5) (267.2) (242.4) (17.3) (24.8) Farm Credit System insurance expense (32.2) (36.4) (29.4) 4.2 (7.0) Loss on debt extinguishment (0.8) (0.3) (10.6) (0.5) 10.3 Net impairment losses recognized in earnings (25.5) (23.3) (16.0) (2.2) (7.3) Provision for income taxes (39.1) (55.7) (50.9) 16.6 (4.8) Net income $1,719.4 $1,539.8 $1,437.1 $179.6 $