If you have trouble making your payments, contact your creditors as quickly as possible and ask for more time. MY PART ONE: WHAT DOES ZERO MEAN?

|

|

|

- Patricia Harrison

- 5 years ago

- Views:

Transcription

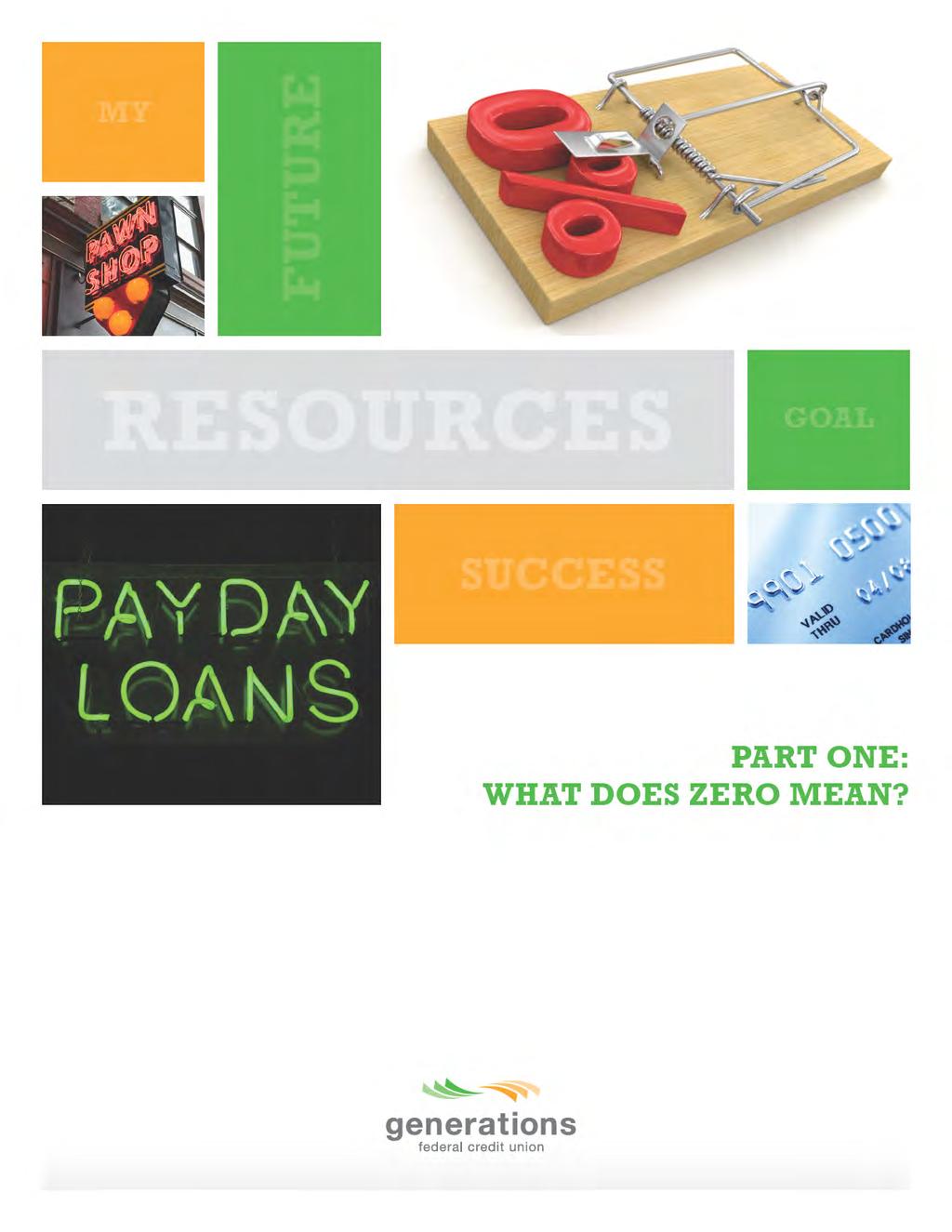

1

2 HOW CAN NOTHING BE SOMETHING? On the surface it may defy logic, but no number carries more weight than zero. It can be the cause for a joyous occasion, such as the number of days until your retirement or the amount owed on your mortgage. Or, it can be a cause for great concern, such as your latest exam score or the balance in your checking account. In the days leading up to the creation of the number zero, philosophers pondered the question, How can nothing be something? This question is just as relevant now as it was then when considering zero s most popular use, err, abuse in perpetrating an unlimited number of sins of omission through grand promises such as zero percent interest, zero financing and zero payments, to name a few. But what does zero really mean? This first part of a two-part series seeks to uncover the truth behind the promise of zero as it pertains to credit cards, payday loans and pawnbrokers. The second part in the series covers the topics of the rent-to-own industry, refund anticipation loans and car loans. CREDIT CARDS Credit cards have their pros and cons, for instance: pro - access to funds in emergencies; con - increased exposure to identity theft. But the credit card s greatest pro or con depending on which side of the transaction you stand is the impulse buy. Businesses long ago realized the benefit of the impulse buy and, accordingly, push hard for the use of retail credit cards. How many times have you seen that big ticket item and decided to purchase it simply because of a zero percent financing store credit card offer for 12-to-18 months? But did you read the fine print? Within it, you ll usually find zero percent is not as clear cut as advertised. In most cases, to get zero percent you must make minimum monthly payments equal to a set percentage of your balance which sometimes is never stated or nearly impossible to find and pay off the balance within a set time period. If you have trouble making your payments, contact your creditors as quickly as possible and ask for more time. Miss one regular payment, or fail to completely repay the total purchase price within the time allotted, and you are faced with paying the interest that has incurred from the original date of purchase, compounded monthly at an astronomical percentage rate usually in the percentage arena. Consumers were given more protections against such unfair or deceptive credit card practices with the passage of the Credit Card Accountability, Responsibility, and Disclosure (CARD) Act of However, these protections do 1

3 CONSUMER VS. BUSINESS Here are some key protection differences between business and consumer credit cards, as noted by the Pew Safe Credit Cards Project: Consumer Terms cannot change during the first year; after this period, 45 days notice is required and consumers generally may opt out. Existing balances are protected from arbitrary increases. Business Issuers may change any term at any time with little or no notice, including raising rates on existing balances. Consumer Penalty fees must be reasonable and proportional, generally $25 for the first infraction and $35 for additional violations within six months. Fees must not exceed the violation (e.g., the penalty for a $4 over-the-limit transaction must be $4 or less). Over-the-limit fees cannot apply unless the cardholder has opted in. Business Penalty fees are virtually unrestricted. Consumer Any payment amount above the minimum payment due each month must be applied to the highest-rate balance first, thereby reducing interest charges to cardholders. Business Issuers can direct payments first to low-rate balances, such as balance transfers, while interest accrues on higher-rate balances. not apply for business or commercial credit cards. Don t be misled by these cards names, consumers are still at risk with these cards because they can be marketed to nearly everyone regardless of whether the account holder is a large corporation, a small business or an employee. Because they are unregulated, commercial credit cards can have unpredictable pricing structures, hair-trigger penalty interest rates and require individuals to be personally liable for all charges under a business account. According to the Pew Safe Credit Cards Project, one-in-ten credit card offers consumers receive in the mail are for business credit cards. This adds up to more than 10 million offers every month. PAYDAY LOANS If you ve ever been in a money crunch, the prospect of a payday loan can look pretty appealing, especially when you are inundated with endless payday loan promotions, such as: Zero money upfront! Get instant cash to hold you over until your next payday! However, this instant cash can translate into high transaction and interest fees. Those fees are there to hedge bets that you will be unable to pay back the loan on time. By being in your current predicament, payday lenders feel the odds are in their favor you will fall into a money crunch again and be unable to repay to loan when it is due. So, you choose to roll over the loan and are subjected to the payday lender s high fees. Take for instance this example from the Federal Trade Commission (FTC): You go to a payday lender because you need to borrow $100 for two weeks. You write a personal check for $115, with $15 as the fee to borrow the money. The payday lender agrees to hold your check until your next payday. If you budgeted appropriately, when that day comes around, either the lender deposits the check or you redeem it by paying the $115 in cash. But if you find yourself unable to payback the loan, you choose to roll over the loan and are charged $15 more to extend the financing for another 14 days. If you roll over the loan three times, the finance charge would climb to $60 to borrow $100! This translates into an annual percentage rate of 391 percent. 2

4 There are more affordable options out there. Consider these payday loan alternatives: Seek a small loan from your local credit union or a community-based organization Often, credit unions and community-based organizations will offer short-term loans for small amounts at competitive rates, including small business loans. If you are having trouble making your payments, contact your creditors or loan servicer as quickly as possible and ask for more time Many creditors may be willing to work with you if they see you are acting in good faith. They may offer an extension on your bills, but make sure to find out what the charges would be for that service, such as a late charge, an additional finance charge or a higher interest rate. Make a realistic budget, including your monthly and daily expenditures, and plan, plan, plan Try to avoid unnecessary purchases. The costs of small, everyday items like a cup of coffee add up. At the same time, try to build some savings: small deposits do help. A savings plan, however modest, can help you avoid borrowing for emergencies. Saving the fee on a $300 payday loan for six months, for example, can help you create a buffer against financial emergencies. Borrow only as much as you can pay with your next paycheck and still have enough to make it to the payday that follows. Contact your local consumer credit counseling service if you need help developing a budget or working out a debt repayment plan with creditors Non-profit groups in every state offer credit guidance to consumers for little-to-no costs. You may want to check with your employer, credit union or housing authority for a list of reputable counseling programs. The bottom line on payday loans: try to find an alternative. Whenever you borrow money, try to limit the amount. Borrow only as much as you can afford to pay with your next paycheck and still have enough to make it to the payday that follows. PAWN BROKERS The precursor to the payday loan, pawn shops set the stage for high interest financing rates on small loans. Typically, the average size of a pawn loan is $75-$100. Fees charged can vary from as low as 12 percent to as high as 300 percent annually. Depending on which state you reside in, there are different laws that set the maximum amount of interest charged on a pawn loan; however, most states allow pawnbrokers to charge an additional monthly service fee as high as 20 percent. 3

5 The terms of the loan are usually longer (approximately 15-to-30 days). After the loan period has passed, most pawn brokers will implement a 30-to-60 day grace period where customers can still regain their valuables provided they pay back the loan amount plus exorbitant fees and interest tacked on. Because the valuables being held hostage can have high sentimental value, many customers blindly pay those fees to recover their items. YOUR RIGHTS If you find yourself a victim to these zero offers and are unable to climb out, there is always an alternative solution to digging yourself deeper in debt. Work within your rights to come up with a debt collection agreement with your debtors. FTC enforces the Fair Debt Collection Practices Act (FDCPA), which prohibits debt collectors from using abusive, unfair or deceptive practices to collect from you. FDCPA covers personal, family and household debts, including money you owe on a personal credit card account, an auto loan, a medical bill and your mortgage. For more information on your rights, visit FTC s online Debt Collection FAQs page at Be sure to read Part Two: What Does Zero Mean?, which seeks to uncover the truth behind the promise of zero as it pertains to the rent-to-own industry, refund anticipation loans and car loans. 4

6

c» BALANCE c» Financially Empowering You Credit Matters Podcast

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Taking Control of Your Money. Using Credit Wisely

Taking Control of Your Money Using Credit Wisely Session 4: Using Credit Wisely To help you stay financially healthy you need to understand credit. Credit is access to money that belongs to lenders (e.g.

Taking Control of Your Money Using Credit Wisely Session 4: Using Credit Wisely To help you stay financially healthy you need to understand credit. Credit is access to money that belongs to lenders (e.g.

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Secured and Unsecured (1)

") LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

Volume 2 Your Credit Report and Your Rights

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

WHAT HAPPENS IF I DON T PAY

LESSON 7 WHAT HAPPENS IF I DON T PAY THE LESSON IN A NUTSHELL Not paying your bills has consequences. Even when you re late, pay as soon as you can. Overview...2 Activity #1: You ve Been Pre-Approved!...

LESSON 7 WHAT HAPPENS IF I DON T PAY THE LESSON IN A NUTSHELL Not paying your bills has consequences. Even when you re late, pay as soon as you can. Overview...2 Activity #1: You ve Been Pre-Approved!...

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

What is Buying on Credit? What Kinds of Things Are Usually Bought on Credit? What is the Difference Between Open-End Credit and Closed-End Credit?

buying on credit What is Buying on Credit? When you buy on credit, you pay extra for the privilege of spreading your payments out over a period of time. What Kinds of Things Are Usually Bought on Credit?

buying on credit What is Buying on Credit? When you buy on credit, you pay extra for the privilege of spreading your payments out over a period of time. What Kinds of Things Are Usually Bought on Credit?

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

YOU work hard to earn your money. Make it work for YOU!

YOU work hard to earn your money. Make it work for YOU! I raised my credit score by 100 points and saved on my car loan. We paid off our high-interest payday loan and started an emergency fund. I used

YOU work hard to earn your money. Make it work for YOU! I raised my credit score by 100 points and saved on my car loan. We paid off our high-interest payday loan and started an emergency fund. I used

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

Teens. lesson seven. about credit

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

yourmoney a guide to managing your credit and debt Volume 6 Life After Debt

yourmoney a guide to managing your credit and debt Volume 6 Life After Debt Call InCharge Debt Solutions today at 1-877-544-9126 or contact us at www.incharge.org Life After Debt You can do it. A life

yourmoney a guide to managing your credit and debt Volume 6 Life After Debt Call InCharge Debt Solutions today at 1-877-544-9126 or contact us at www.incharge.org Life After Debt You can do it. A life

Workbook 3. Borrowing Money

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

CREDIT BASICS. Advanced Level

CREDIT BASICS Advanced Level YOUR PRESENT SELF IMPACTS YOUR FUTURE SELF You receive goods or services today With the promise to pay back the determined amount of money (usually in small increments plus

CREDIT BASICS Advanced Level YOUR PRESENT SELF IMPACTS YOUR FUTURE SELF You receive goods or services today With the promise to pay back the determined amount of money (usually in small increments plus

20 Steps to Financial Health:

20 Steps to Financial Health: Achieving Lifelong Financial Fitness American Consumer Credit Counseling 130 Rumford Avenue Auburndale, MA 02466 1.800.769.3571 ConsumerCredit.com On behalf of American Consumer

20 Steps to Financial Health: Achieving Lifelong Financial Fitness American Consumer Credit Counseling 130 Rumford Avenue Auburndale, MA 02466 1.800.769.3571 ConsumerCredit.com On behalf of American Consumer

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

PERSONAL FINANCE FINAL EXAM REVIEW. Click here to begin

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

Peace be unto you, Sincerely, O'Rell Muhammad

Peace be unto you, We all know how valuable and vital having a good credit rating can be. Without a good credit rating, your financial, occupational, and personal goals are at risk of being severely limited.

Peace be unto you, We all know how valuable and vital having a good credit rating can be. Without a good credit rating, your financial, occupational, and personal goals are at risk of being severely limited.

Drive Away Happy: Car Buying Decisions

Drive Away Happy: Car Buying Decisions Buy new, buy used, or lease? These are just a few of the many decisions you ll need to make before happily driving away with a vehicle. While shopping for a car or

Drive Away Happy: Car Buying Decisions Buy new, buy used, or lease? These are just a few of the many decisions you ll need to make before happily driving away with a vehicle. While shopping for a car or

First Timer s Guide: Credit Cards. Used the right way, your credit card can be your new financial BFF.

First Timer s Guide: Credit Cards Used the right way, your credit card can be your new financial BFF. Like most things, with great power comes great responsibility. And credit cards are no different. Used

First Timer s Guide: Credit Cards Used the right way, your credit card can be your new financial BFF. Like most things, with great power comes great responsibility. And credit cards are no different. Used

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Beware of skip-a-month payment offers. Remember, you still pay interest on your outstanding debt, and your total interest costs continue to rise.

Managing Debt: Are You In Over Your Head Last week we began the conversation on credit and using it wisely. Maybe you do not have lots of debt issues or are spending within a comfortable range. Knowing

Managing Debt: Are You In Over Your Head Last week we began the conversation on credit and using it wisely. Maybe you do not have lots of debt issues or are spending within a comfortable range. Knowing

HOW TO BUY A CAR WITH BAD CREDIT

Your credit score is not the only way to prove your credit worthiness. It does do a good job of indicating what type of credit customer you might be; however, today the credit system is being used to exploit

Your credit score is not the only way to prove your credit worthiness. It does do a good job of indicating what type of credit customer you might be; however, today the credit system is being used to exploit

Predatory LENDING BROUGHT TO YOU BY

Predatory LENDING BROUGHT TO YOU BY YOUR GUIDE TO Identifying Abusive or Unfair Lending Practices Predatory Lending COMES IN MANY FORMS PREPAID DEBIT PAWNBROKERS Individuals or businesses that offer secured

Predatory LENDING BROUGHT TO YOU BY YOUR GUIDE TO Identifying Abusive or Unfair Lending Practices Predatory Lending COMES IN MANY FORMS PREPAID DEBIT PAWNBROKERS Individuals or businesses that offer secured

Personal Finance Unit 2 Chapter Glencoe/McGraw-Hill

0 Chapter 6 Consumer Credit What You ll Learn Section 6.1 Explain the meaning of consumer credit. Differentiate between closed-end credit and openend credit. Section 6.2 Name the five C s of credit. Identify

0 Chapter 6 Consumer Credit What You ll Learn Section 6.1 Explain the meaning of consumer credit. Differentiate between closed-end credit and openend credit. Section 6.2 Name the five C s of credit. Identify

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

CONSUMER LEGAL ADVISORS

CONSUMER LEGAL ADVISORS A CONSUMER PROTECTION LAW FIRM PROTECTING AMERICA S CONSUMERS ONE CONTRACT AT A TIME 1 IMPORTANT CONTACT INFORMATION We are here for you! Contact us with ANY questions, comments

CONSUMER LEGAL ADVISORS A CONSUMER PROTECTION LAW FIRM PROTECTING AMERICA S CONSUMERS ONE CONTRACT AT A TIME 1 IMPORTANT CONTACT INFORMATION We are here for you! Contact us with ANY questions, comments

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

An interactive game designed to familiarize students with the personal finance management issues they are beginning to face as young adults Features

An interactive game designed to familiarize students with the personal finance management issues they are beginning to face as young adults Features financial questions throughout the game Like football,

An interactive game designed to familiarize students with the personal finance management issues they are beginning to face as young adults Features financial questions throughout the game Like football,

Toolkit 2 Borrowing Wisely

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

c» BALANCE C:» Financially Empowering You Financial First Aid Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You Financial First Aid Podcast [Music plays] Nikki:](/thumbs/83/88246744.jpg "c» BALANCE C:» Financially Empowering You Financial First Aid Podcast [Music plays] Nikki:") Financial First Aid Podcast [Music plays] Nikki: You re listening to Financial first aid. Hi. I m Nicky, your host for today s podcast. Many circumstances in life can derail even the best plans and leave

Financial First Aid Podcast [Music plays] Nikki: You re listening to Financial first aid. Hi. I m Nicky, your host for today s podcast. Many circumstances in life can derail even the best plans and leave

usfinancialcapability.org U.S. Survey Data at a Glance

usfinancialcapability.org Survey Data at a Glance Making ends meet 212 Spending vs Saving % Spent More Than Income 41% 36% 19% 19% 2% Spend less Break even Spend more 212 29 Individuals who report spending

usfinancialcapability.org Survey Data at a Glance Making ends meet 212 Spending vs Saving % Spent More Than Income 41% 36% 19% 19% 2% Spend less Break even Spend more 212 29 Individuals who report spending

First Time Home Buying Steps

Buying a home is one of the biggest emotional and financial decisions you'll ever make in your life time. The differences between renting and buying a home are huge, and there are numbers of pros and cons

Buying a home is one of the biggest emotional and financial decisions you'll ever make in your life time. The differences between renting and buying a home are huge, and there are numbers of pros and cons

The answer s yes your indispensable guide to securing a mortgage

The answer s yes your indispensable guide to securing a mortgage Hello from HOOCHT These days, life moves faster than ever. To keep pace with it, we re used to doing everything at lightning speed, with

The answer s yes your indispensable guide to securing a mortgage Hello from HOOCHT These days, life moves faster than ever. To keep pace with it, we re used to doing everything at lightning speed, with

Using Credit Wisely: Curves Ahead

Using Credit Wisely: Curves Ahead What we will cover Types of credit Ownership of credit accounts Credit terms Guidelines for using credit Using credit means greater cost Establishing credit What we will

Using Credit Wisely: Curves Ahead What we will cover Types of credit Ownership of credit accounts Credit terms Guidelines for using credit Using credit means greater cost Establishing credit What we will

Credit Cards. The Language of Credit. Student Loans. Installment Loans 12/14/2016

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Presentation Slides. Lesson Nine. Cars and Loans 04/09

Presentation Slides $ Lesson Nine Cars and Loans 04/09 costs of owning and operating a motor vehicle ownership (fixed) costs: Depreciation (based on purchase price) Interest on loan (if buying on credit)

Presentation Slides $ Lesson Nine Cars and Loans 04/09 costs of owning and operating a motor vehicle ownership (fixed) costs: Depreciation (based on purchase price) Interest on loan (if buying on credit)

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU?

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

Chapter 4 Debt. Section Credit misdirection

Chapter 4 Debt Section 2 2.1 Credit misdirection Credit Misdirection Lending money to friends or family members is a bad idea. It will strain relationships and in some cases ruin friendships. If you have

Chapter 4 Debt Section 2 2.1 Credit misdirection Credit Misdirection Lending money to friends or family members is a bad idea. It will strain relationships and in some cases ruin friendships. If you have

Fresh Start. Living DebtFree. By Douglas Hoyes. BA, CA, CIRP, CBV, Licensed Insolvency Trustee. Co-Founder of

Fresh Start A Concise Guide to Living DebtFree By Douglas Hoyes BA, CA, CIRP, CBV, Licensed Insolvency Trustee Co-Founder of Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP,

Fresh Start A Concise Guide to Living DebtFree By Douglas Hoyes BA, CA, CIRP, CBV, Licensed Insolvency Trustee Co-Founder of Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP,

10 Errors to Avoid When Refinancing

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

MODULE 7: Borrowing Basics PARTICIPANT GUIDE

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Chapter 07. Sources of Consumer Credit. Chapter 7 Learning Objectives. Choosing a Source of Credit: The of Credit Alternatives

Chapter 07 Choosing a Source of Credit: The of Credit Alternatives McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 7-1 Chapter 7 Learning Objectives 1. Analyze

Chapter 07 Choosing a Source of Credit: The of Credit Alternatives McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 7-1 Chapter 7 Learning Objectives 1. Analyze

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

Credit Choosing a credit card: Read the fine print How to tell if you have a credit emergency Protecting yourself against identity theft

MoTax Human Environmental Sciences Personal Financial Planning missourifamilies.org/money/ Missouri Taxpayer Education Credit Choosing a credit card: Read the fine print How to tell if you have a credit

MoTax Human Environmental Sciences Personal Financial Planning missourifamilies.org/money/ Missouri Taxpayer Education Credit Choosing a credit card: Read the fine print How to tell if you have a credit

BANKING & FINANCE (145)

") Page 1 of 9 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2018 Multiple Choice: (30 @ 2 points each) Financial Word Problems: (4 @ 3 points each) Parts of a Check: (6 @ 3 points each)

Page 1 of 9 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2018 Multiple Choice: (30 @ 2 points each) Financial Word Problems: (4 @ 3 points each) Parts of a Check: (6 @ 3 points each)

FINANCIAL AVENUE LEARNING OBJECTIVES PSYCHOLOGY OF MONEY FOUNDATIONS OF MONEY LEARNING OBJECTIVES LEARNING OBJECTIVES

FINANCIAL AVENUE PSYCHOLOGY OF MONEY We ve all made poor spending choices, even when we sometimes know better; it s what makes us human. With that in mind, students will explore their financial personality

FINANCIAL AVENUE PSYCHOLOGY OF MONEY We ve all made poor spending choices, even when we sometimes know better; it s what makes us human. With that in mind, students will explore their financial personality

years INTEREST ONLY MORTGAGES

HOMEBUYER S GUIDE Buying a new home can be a potentially daunting process so we ve prepared this step-by-step guide to help you. It outlines the buying process and gives a guide to the different types

HOMEBUYER S GUIDE Buying a new home can be a potentially daunting process so we ve prepared this step-by-step guide to help you. It outlines the buying process and gives a guide to the different types

Top Things To Know KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT ECONOMICS - PERSONAL FINANCE WORKSHOPS # 4 - CONTROLLING DEBT

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT ECONOMICS - PERSONAL FINANCE WORKSHOPS # 4 - CONTROLLING DEBT Vocabulary Keys : Words that are in bold = are terms that appear in one of the chapters, Words

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT ECONOMICS - PERSONAL FINANCE WORKSHOPS # 4 - CONTROLLING DEBT Vocabulary Keys : Words that are in bold = are terms that appear in one of the chapters, Words

CEE National Standards for Financial Literacy

Episode 101 What Is a Biz Kid? Episode 102 What Is Money? Episode 103 How Do You Get Money? Episode 104 What Can You Do with Money? Episode 105 Money Moves Episode 106 Taking Charge of Your Financial Future

Episode 101 What Is a Biz Kid? Episode 102 What Is Money? Episode 103 How Do You Get Money? Episode 104 What Can You Do with Money? Episode 105 Money Moves Episode 106 Taking Charge of Your Financial Future

IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT

IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT This disclosure contains important information about our Home Equity Line(s) of Credit (Plan). You should read it carefully and keep a copy for your records.

IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT This disclosure contains important information about our Home Equity Line(s) of Credit (Plan). You should read it carefully and keep a copy for your records.

What you need to know about getting, using and keeping credit. A Guide to Credit* American Financial Services Association Education Foundation

A Guide to Credit* What you need to know about getting, American Financial Services Association Education Foundation www.afsaef.org www.gmacfs.com using and keeping credit *If you would like to receive

A Guide to Credit* What you need to know about getting, American Financial Services Association Education Foundation www.afsaef.org www.gmacfs.com using and keeping credit *If you would like to receive

Quick Credit Repair Guide

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

Credit Card Basics.

Credit Card Basics http://www.nbc.com/saturday-night-live/video/dont-buystuff/n12020 Silly seems obvious! In reality, it is EASY to get caught up with credit card debt Seems like it s free money and it

Credit Card Basics http://www.nbc.com/saturday-night-live/video/dont-buystuff/n12020 Silly seems obvious! In reality, it is EASY to get caught up with credit card debt Seems like it s free money and it

You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast.

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

SEVEN LIFE-DEFINING FINANCIAL DECISIONS

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

Consolidate credit card debt with bank of america

Home Consolidate credit card debt with bank of america This quarterly newsletter includes market reports on various key industries highlighting recent transaction and market data as well as key industry

Home Consolidate credit card debt with bank of america This quarterly newsletter includes market reports on various key industries highlighting recent transaction and market data as well as key industry

How to Find and Qualify for the Best Loan for Your Business

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

SAFETY COUNTS. Cashfloat s guide to online safety

SAFETY COUNTS Cashfloat s guide to online safety Eleven Ways to Stay Safe When Taking Out Loans Online When you take a loan, you enter into a binding agreement with the lending institution. This is a legal

SAFETY COUNTS Cashfloat s guide to online safety Eleven Ways to Stay Safe When Taking Out Loans Online When you take a loan, you enter into a binding agreement with the lending institution. This is a legal

lesson nine in trouble overheads

lesson nine in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson nine in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

Financial Literacy Course. East High School Module 9

Financial Literacy Course East High School Module 9 What will you learn about? Identity Theft and Consumer Fraud Protecting Against and Identity Theft and Consumer Fraud Fair Debt Collection Practices

Financial Literacy Course East High School Module 9 What will you learn about? Identity Theft and Consumer Fraud Protecting Against and Identity Theft and Consumer Fraud Fair Debt Collection Practices

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Credit Guide. An introduction to credit and how it s used in your financial plan. Educators Credit Union. Shopper. Buyer. Planner. Spender.

Educators Credit Union Credit Guide An introduction to credit and how it s used in your financial plan. Shopper. Buyer. Planner. Spender. For the teacher in you. 262.886.5900 ecu.com Table of contents

Educators Credit Union Credit Guide An introduction to credit and how it s used in your financial plan. Shopper. Buyer. Planner. Spender. For the teacher in you. 262.886.5900 ecu.com Table of contents

Take Charge: Wise Use of Credit Cards. Brought to you by ALEC

Take Charge: Wise Use of Credit Cards Brought to you by ALEC Seminar Objectives LEARN: Advantages/pitfalls of credit cards How CARD Act affects you How to build solid credit foundation Warning signs: too

Take Charge: Wise Use of Credit Cards Brought to you by ALEC Seminar Objectives LEARN: Advantages/pitfalls of credit cards How CARD Act affects you How to build solid credit foundation Warning signs: too

By JW Warr

By JW Warr 1 WWW@AmericanNoteWarehouse.com JW@JWarr.com 512-308-3869 Have you ever found out something you already knew? For instance; what color is a YIELD sign? Most people will answer yellow. Well,

By JW Warr 1 WWW@AmericanNoteWarehouse.com JW@JWarr.com 512-308-3869 Have you ever found out something you already knew? For instance; what color is a YIELD sign? Most people will answer yellow. Well,

DEBT REPAYMENT OPTIONS OPTIONS FOR THE REPAYMENT OF YOUR UNSECURED DEBT

DEBT REPAYMENT OPTIONS OPTIONS FOR THE REPAYMENT OF YOUR UNSECURED DEBT EDUCATIONAL SERIES / MARCH 2012 1 DEBT REPAYMENT OPTIONS OPTIONS FOR THE REPAYMENT OF YOUR UNSECURED DEBT Published by Debt Management

DEBT REPAYMENT OPTIONS OPTIONS FOR THE REPAYMENT OF YOUR UNSECURED DEBT EDUCATIONAL SERIES / MARCH 2012 1 DEBT REPAYMENT OPTIONS OPTIONS FOR THE REPAYMENT OF YOUR UNSECURED DEBT Published by Debt Management

Credit Education Program

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Chapter 27. Your Credit and the Law pp

Your Credit and the Law pp. 434-447 Learning Objectives After completing this chapter, you ll be able to: 1. Explain how government protects credit rights. 2. Name federal laws that protect consumers.

Your Credit and the Law pp. 434-447 Learning Objectives After completing this chapter, you ll be able to: 1. Explain how government protects credit rights. 2. Name federal laws that protect consumers.

Chapter 17. Managing Personal Finances

Chapter 17 Managing Personal Finances Section 17-1 Using Financial Services Objectives Describe various services offered by financial institutions. Write and endorse checks correctly. Balance a checkbook.

Chapter 17 Managing Personal Finances Section 17-1 Using Financial Services Objectives Describe various services offered by financial institutions. Write and endorse checks correctly. Balance a checkbook.

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Being a Guarantor. This booklet will help you understand all that is involved in being a Guarantor.

is a big responsibility and can have serious consequences. It is important to understand exactly what you are getting yourself into and what the impact of signing the agreement may be. can be a helpful

is a big responsibility and can have serious consequences. It is important to understand exactly what you are getting yourself into and what the impact of signing the agreement may be. can be a helpful

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

Budgeting Essentials

Budgeting Essentials One of the greatest satisfactions in life is having a sense of control over your finances. Through careful planning and use of money management techniques that anyone can learn, you

Budgeting Essentials One of the greatest satisfactions in life is having a sense of control over your finances. Through careful planning and use of money management techniques that anyone can learn, you

2. To earn as much interest as possible, you should open a savings account that earns () interest Hide answers

interest Hide answers") 1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

Teacher's Guide. Lesson Nine. In Trouble 04/09

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Lesson 5: Credit and Debt

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

Peace be unto you, Sincerely, O'Rell Muhammad

Peace be unto you, We all know how valuable and vital having a good credit rating can be. Without a good credit rating, your financial, occupational, and personal goals are at risk of being severely limited.

Peace be unto you, We all know how valuable and vital having a good credit rating can be. Without a good credit rating, your financial, occupational, and personal goals are at risk of being severely limited.

HOMEOWNER S APPLICATION KIT Home Equity Line of Credit (HELOC)

") HOMEOWNER S APPLICATION KIT Home Equity Line of Credit (HELOC) Mahalo for your interest in the Hawaii Schools Federal Credit Union Home Equity Line of Credit program. This Homeowner s Application Kit has

HOMEOWNER S APPLICATION KIT Home Equity Line of Credit (HELOC) Mahalo for your interest in the Hawaii Schools Federal Credit Union Home Equity Line of Credit program. This Homeowner s Application Kit has

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 Credit is a valuable commodity. Having the ability to borrow funds enables us to obtain things we would otherwise have to save years to afford: homes, cars, a college

Federal Reserve Bank of Philadelphia 1 Credit is a valuable commodity. Having the ability to borrow funds enables us to obtain things we would otherwise have to save years to afford: homes, cars, a college

A Guide to Buying Your Own Home

A Guide to Buying Your Own Home banking on people Getting started Getting on the property ladder can be a big step for anyone to take. With this handy guide, you ll find helpful tips for planning ahead,

A Guide to Buying Your Own Home banking on people Getting started Getting on the property ladder can be a big step for anyone to take. With this handy guide, you ll find helpful tips for planning ahead,

Teacher's Guide. Lesson Thirteen. In Trouble 04/09

Teacher's Guide $ Lesson Thirteen In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Teacher's Guide $ Lesson Thirteen In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

CREDIT CARD MAKEOVER ACTION PLAN. First. Ask yourself, why are you carrying a balance? Be honest!

CREDIT CARD MAKEOVER ACTION PLAN First. Ask yourself, why are you carrying a balance? Be honest! Was it a one time emergency, divorce, medical expense, or other life event? OR Is it on-going overspending?

CREDIT CARD MAKEOVER ACTION PLAN First. Ask yourself, why are you carrying a balance? Be honest! Was it a one time emergency, divorce, medical expense, or other life event? OR Is it on-going overspending?

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

Home Equity Lines of Credit

The Federal Reserve Board What you should know about Home Equity Lines of Credit Board of Governors of the Federal Reserve System www.federalreserve.gov 0708 i What You Should Know about Home Equity Lines

The Federal Reserve Board What you should know about Home Equity Lines of Credit Board of Governors of the Federal Reserve System www.federalreserve.gov 0708 i What You Should Know about Home Equity Lines

PFIN 7: Buying Decisions 45

PFIN 7: Buying Decisions 45 7-1 Buying Plans OBJECTIVES Explain the advantages of using a buying plan. List the steps of a buying plan. Set criteria for selecting one item over another to buy. Explain

PFIN 7: Buying Decisions 45 7-1 Buying Plans OBJECTIVES Explain the advantages of using a buying plan. List the steps of a buying plan. Set criteria for selecting one item over another to buy. Explain

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Amber Mahaffey

Predatory Lending June 2004 Amber Mahaffey amber@goodvaluation.com About the Author: Amber Mahaffey is the director of research for Good Valuation, Inc. She has conducted many studies that concern common

Predatory Lending June 2004 Amber Mahaffey amber@goodvaluation.com About the Author: Amber Mahaffey is the director of research for Good Valuation, Inc. She has conducted many studies that concern common

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

Money Math for Teens. Before You Choose a Credit Card

Money Math for Teens Before You Choose a Credit Card This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Money Math for Teens Before You Choose a Credit Card This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Essential Facts for Students Carol A. Carolan, Ph.D.

The ABCs of Credit Card Finance Essential Facts for Students Carol A. Carolan, Ph.D. HOW LONG AND HOW MUCH DO I HAVE TO PAY? By using the following chart you can find out your total payoff time and total

The ABCs of Credit Card Finance Essential Facts for Students Carol A. Carolan, Ph.D. HOW LONG AND HOW MUCH DO I HAVE TO PAY? By using the following chart you can find out your total payoff time and total

HOME EQUITY EARLY DISCLOSURE

REAL ESTATE LENDING POWERED BY CUNA MUTUAL GROUP HOME EQUITY EARLY DISCLOSURE IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT PLAN This disclosure contains important information about our Home Equity

REAL ESTATE LENDING POWERED BY CUNA MUTUAL GROUP HOME EQUITY EARLY DISCLOSURE IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT PLAN This disclosure contains important information about our Home Equity

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Module Four: Building Financial Foundations Homes, Loans and Automobiles

Financial Empowerment Curriculum Moving Ahead Through Financial Management Module Four: Building Financial Foundations Homes, Loans and Automobiles 1 Financial Empowerment Curriculum Module Five: Creating

Financial Empowerment Curriculum Moving Ahead Through Financial Management Module Four: Building Financial Foundations Homes, Loans and Automobiles 1 Financial Empowerment Curriculum Module Five: Creating

Theme 8 Review - Answer Key

Theme 8 Review - Answer Key. Due to technology, the financial world is becoming each year. less complex X more complex simpler less important. The term for the act of purchasing goods and services by paying

Theme 8 Review - Answer Key. Due to technology, the financial world is becoming each year. less complex X more complex simpler less important. The term for the act of purchasing goods and services by paying