(50 Marks) Proposed Policy I (40 days) A. Expected Profit: (4 marks) (a) Credit Sales 4,20,000 4,41,000 4,72,500 4,83,000

|

|

|

- Vincent Banks

- 6 years ago

- Views:

Transcription

Note: All questions are compulsory.")

1 INTER CA MAY 2018 Sub: Financial Management Topics Capital Structure, Cost of Capital, Capital Budgeting, estimation of working capital, receivables management. Test Code M25 Branch: MULTIPLE Date: (50 Marks) Note: All questions are compulsory. Question 1 (8 marks) Statement showing the Evaluation of Debtors Policies (Total Approach) Particulars Present Policy (30 days) Proposed Policy I (40 days) Proposed Policy II (60 days) Proposed Policy III (75 days) (`) (`) (`) (`) A. Expected Profit: (4 marks) (a) Credit Sales 4,20,000 4,41,000 4,72,500 4,83,000 (b) Total Cost (other than Bad Debts) (i) Variable Costs [Sales x ` 2/` 3] 2,80,000 2,94,000 3,15,000 3,22,000 (ii) Fixed Costs (W.N. 1) Total Cost (Variable Cost+ Fixed Cost) 35,000 35,000 35,000 35,000 3,15,000 3,29,000 3,50,000 3,57,000 (c) Bad Debts 4,200 6,615 14,175 19,320 (1% of (1.5% of (3% of (4% of (d) Expected Profit [(a) (b) (c)] 4,20,000) 4,41,000) 4,72,500) 4,83,000) 1,00,800 1,05,385 1,08,325 1,06,680 B. Opportunity Cost of Investments in Receivables * (2 marks) 5,250 7, ,66 14,875 (315000*30/100*20/360) (329000*40/360*20/100) (350000*60/100*20/360) (357000*75/360*20/100) C. Net Benefits (A B)(1mark) 95,550 98,074 96,658 91,805 Recommendation: The Proposed Policy I (i.e. increase in collection period by 10 days or total 40 days) should be adopted since the net benefits under this policy are higher as compared to other policies. (1 mark) Working Note- 1: (i) Calculation of Fixed Cost = [Average Cost per unit Variable Cost per unit] No. of Units sold = [(2.25 2) (` 4, 20,000/3)] = ` 35,000 1 Page

2 *Calculation of Opportunity Cost of Average Investments Opportunity Cost = Total Cost x Collection period x rate of return 360 days 100 Question 2 (8 Marks) Particulars Lakhs 1. Present Capital Employed = Equity + Debt = ( ) + ( ) 900,00 [or] = Fixed Assets + NWC= ( ) Note: Bank Borrowings are also included in the computation of capital Employed (1 mark) 2. Additional Capital reqd to meet extra sales = Capital Employed x % of sales Increase = ` Lakhs x 20% (1 mark) 3. Internal Cash Accruals = Sales x Net Profit Ratio x After Dividend, i.e. Retention Rate = (` 600 Lakhs x 12%) x 4% NP Ratio x 50% post dividend (1 mark) External Funds required = Total Additional Funds required (Less) Internal Cash Accruals = ( ) (1 mark) 5. Constrains for raising External Funds of ` Lakhs (2 marks) (a) Current Ratio = = ( ) % = () %. ( ) % On Substitution, = 1.33 ( ) % So, Short Term Bank Borrowings =. = Lakhs.. Since existing Short Term Bank Borrowings = Additional Borrowings = (b) % = 1.5 times. So, Long Term Loans = = Lakhs. Since existing Long Term Loans = , Additional Long Term Loans = Manner of raising additional capital: (Required = ` 180,000 Lakhs) (a) Internal Cash Accruals (WN 3) (b) Short Term Bank Borrowings (WN 5a) (c) Long Term Loans (WN 5b) (d) Equity Capital (balancing figure, on comparing with ` 180 Lakhs) (1 mark) Total Additional Funds Employed Confirmation of Long Term Debt to Equity Ratio: Long Term Debt to Equity Ratio = Question 3 (6 Marks) (.... ) = 1.05 times. (1 mark) 1. Computation if Interest Cost on delayed collections (5 marks) Amt Due (1) Pymt Recd (2) Balance Due (1-2) Period of Due Interest Cost per quarter ` 5,00,000 (` 20,00,000 4 quarters) Initial = Nil ` 5,00, days ` 5,00,000 x x 25%=`6,849 ` 5,00,000 15% = ` 75,000 ` 4,25,000 (45 20) = 25 days ` 4,25,000 x x 25%=`7,277 Amt Due (1) Pymt Recd (2) Balance Due (1-2) Period of Due Interest Cost per quarter ` 4,25,000 30% = ` ` 2,75,000 (90 45) = 45 days 1,50,000 ` 2,75,000 x x 25%= ` 8,476 ` 2,75,000 25% = ` ` 1,50,000 (100 90) = 10 1,25,000 days ` 1,50,000 x x 25%=` 1,027 ` 1,50,000 28% = ` ` 10,000 Bad Debt Fully lost, so ignored here. 1,40,000 Total ` 23,629 So, Interest Cost per annum = ` 23,629 x 4 quarters = ` 94, Page

(`) Annual Income before Tax and Depreciation 3,45,000 4,55,000 Less : Depreciation Machine I: 10,00,000 /5 2,00,000 - Machine II: 15,00,000 / 6-2,50,000 Income before Tax 1,45,000 2,05,000 Less:")

3 2. Cost Benefits Analysis (3 marks) Particulars Computation ` Profit from Sales ` 20,00,000 x ` ` 3,00,000 Less: Costs thereon: Annual Fixed Costs Bad Debts Interest on Average Debtors Given ` 20,00,000 x 2% As per computation above 35,000 40,000 94,516 Net Benefit 1,30,484 Note: Since there is a Net Benefit, the proposal is worthwhile. Question 4 (8 Marks) (b) Computation of Discounted Payback Period, Net Present Value (NPV) and Internal Rate of Return (IRR) for Two Machines Calculation of Cash Inflows (1 mark) Machine I Machine II (`) (`) Annual Income before Tax and Depreciation 3,45,000 4,55,000 Less : Depreciation Machine I: 10,00,000 /5 2,00,000 - Machine II: 15,00,000 / 6-2,50,000 Income before Tax 1,45,000 2,05,000 Less: 30 % 43,500 61,500 Income after Tax 1,01,500 1,43,500 Add: Depreciation 2,00,000 2,50,000 Annual Cash Inflows 3,01,500 3,93,500 3 Page

4 2 marks 2 marks 2 marks 4 Page

Year Cash inflow(rs.) PV Factor@12% (Rs.) 1 2,00,000 0.")

5 1 mark Question 5 (8 marks) (Rs.in lakhs) Equipment Cost 150 Working Capital Calculation of Cash Inflows: (3 Marks) Years Sales in units 80,000 1,20,00 3,00,000 2,00,000 (Rs.) (Rs.) (Rs.) (Rs.) Contribution@Rs.60 p.u 48,00,000 72,00,000 1,80,00,000 1,20,00,00 Fixed cost 16,00,000 16,00,000 16,00,000 16,00,000 Advertisement 30,00,000 15,00,000 10,00,000 4,00,000 Depreciation 15,00,000 15,00,000 16,50,000 16,50,000 Profit/(loss) 13,00,000 26,00,000 1,37,50,000 83,50,000 NIL 13,00,000 68,75,000 41,75,000 Profit/(loss)after tax (13,00,000) 13,00,000 68,75,000 41,75,000 Add: Depreciation 15,00,000 15,00,000 16,50,000 16,50,000 Cash inflow 2,00,000 28,00,000 85,25,000 58,25,000 Computation of PV of Cash Inflow(4 Marks) Year Cash inflow(rs.) PV Factor@12% (Rs.) 1 2,00, ,78, ,00, ,31, ,25, ,69, ,25, ,21,900 5 Page

6 5 85,25, ,33, ,25, ,53, ,25, ,32, ,25, ,53,300 Working Capital 15,00, ,400 (A) 2,73,21,450 Cash Outflow: Initial Cash Outlay 1,75,00, ,75,00,000 Additional Investment 10,00, ,97,000 (B) 1,82,97,000 Net Present Value(NPV) (A-B) 90,24,450 Recommendation :Accept the project in view of positive NPV.(1 mark) Question 6 (8 Marks) Working Notes: 1. Capital employed before expansion plan: (Rs.) Equity shares (Rs.10 x80,000 shares) 8,00,000 Debenture {(Rs.1,20,000/12) x100} 10,00,000 Retained earnings 18,00,000 Total capital employed 36,00,000 (1/2 mark) 2.Earnings before the payment of interest and tax(ebit): (Rs.) Profit(EBT) 6,00,000 Add: Interest 1,20,000 EBIT 7,20,00 (1/2 mark) 3.Return on Capital Employed (ROCE): EBIT Rs. 7,20,000 Roce= 100 = 100 = 20% Capital employed Rs. 36,00,000 (1 mark) 4.Earnings before interest and tax (EBIT) after expansion scheme: (1 mark) After expansion, capital employed =Rs.36,00,000+Rs.8,00,000 =Rs.44,00,000 Desired EBIT =20% x Rs.44,00,000=Rs.8,80,000 (i) Computation or Earnings per Share (EPS) under the following options: (4 Marks) Present Expansion scheme Additional funds raised as Debt Equity (Rs.) (Rs.) (Rs.) Earnings before Interest and 7,20,000 8,80,000 8,80,000 Tax(EBIT) Less: Interest Old capital 1,20,000 1,20,000 1,20,000 6 Page

7 -New capital - 96,000 - (Rs.8,00,000 x12%) Earnings before Tax(EBT) 6,00,000 6,64,000 7,60,000 Less: Tax(50%of EBT) 3,00,000 3,32,000 3,80,000 PAT 3,00,000 3,32,000 3,80,000 No. of shares outstanding 80,000 80,000 1,60,000 Earnings per share(eps) Rs. 3,00,000 80,000 Rs. 3,32,000 80,000 Rs. 3,80, ,000 (ii) Advise to the Company :When the expansion scheme is financed by additional debt, the EPS is higher.hence, the company should finance the expansion scheme by raising debt.(1 Mark) Question 7 (4 Marks) Major considerations in capital structure planning There are three major considerations, i.e. risk, cost of capital and control, which help the finance manager in determining the proportion in which he can raise funds from various sources. Although, three factors, i.e., risk, cost and control determine the capital structure of a particular business undertaking at a given point of time. (1 mark) Risk: The finance manager attempts to design the capital structure in such a manner, so that risk and cost are the least and the control of the existing management is diluted to the least extent. However, there are also subsidiary factors also like marketability of the issue, manoeuvrability and flexibility of the capital structure, timing of raising the funds. Risk is of two kinds, i.e., Financial risk and Business risk. Here, we are concerned primarily with the financial risk. Financial risk also is of two types: Risk of cash insolvency Risk of variation in the expected earnings available to equity share-holders (1 mark) Cost of Capital: Cost is an important consideration in capital structure decisions. It is obvious that a business should be at least capable of earning enough revenue to meet its cost of capital and finance its growth. Hence, along with a risk as a factor, the finance manager has to consider the cost aspect carefully while determining the capital structure. (1 mark) Control: Along with cost and risk factors, the control aspect is also an important consideration in planning the capital structure. When a company issues further equity shares, it automatically dilutes the controlling interest of the present owners. Similarly, preference shareholders can have voting rights and thereby affect the composition of the Board of Directors, in case dividends on such shares are not paid for two consecutive years. Financial institutions normally stipulate that they shall have one or more directors on the Boards. Hence, when the management agrees to raise loans from financial institutions, by implication it agrees to forego a part of its control over the company. It is obvious, therefore, that decisions concerning capital structure are taken after keeping the control factor in mind. (1 mark) ************ 7 Page

INTER CA MAY Note: All questions are compulsory. Question 1 (6 marks) Question 2 (8 Marks)

Question 2 (8 Marks)") (50 Marks) Note: All questions are compulsory. INTER CA MAY 2018 Sub: Financial Management Topics Capital Structure, Cost of Capital, Capital Budgeting, estimation of working capital, receivables management,

(50 Marks) Note: All questions are compulsory. INTER CA MAY 2018 Sub: Financial Management Topics Capital Structure, Cost of Capital, Capital Budgeting, estimation of working capital, receivables management,

(50 Marks) Note: The cost of equity can be calculated without taking the effect of growth on dividend.

Note: The cost of equity can be calculated without taking the effect of growth on dividend.") IPCC November 2017 FINANCIAL MANAGEMENT Test Code 8012 Branch (MULTIPLE) (Date : 11.06.2017) (50 Marks) Note: All questions are compulsory. Question 1(6 Marks) (i) Cost of Equity Capital(K e ): (2 marks)

IPCC November 2017 FINANCIAL MANAGEMENT Test Code 8012 Branch (MULTIPLE) (Date : 11.06.2017) (50 Marks) Note: All questions are compulsory. Question 1(6 Marks) (i) Cost of Equity Capital(K e ): (2 marks)

INTER CA MAY Note: All questions are compulsory. Question 1 (6 marks)

") Note: All questions are compulsory. INTER CA MAY 2018 Sub: Accountancy & FM Topics: Hire purchase & Instalment selling, Branch Accounts, Estimation of Working Capital, Cash Budget, Cash Flow Statement.

Note: All questions are compulsory. INTER CA MAY 2018 Sub: Accountancy & FM Topics: Hire purchase & Instalment selling, Branch Accounts, Estimation of Working Capital, Cash Budget, Cash Flow Statement.

INTER CA NOVEMBER 2018

INTER CA NOVEMBER 2018 Sub: FINANCIAL MANAGEMENT Topics Estimation of Working Capital, Receivables Management, Accounting Ratio, Leverages, Capital Structure. Test Code N16 Branch: Multiple Date: (50 Marks)

INTER CA NOVEMBER 2018 Sub: FINANCIAL MANAGEMENT Topics Estimation of Working Capital, Receivables Management, Accounting Ratio, Leverages, Capital Structure. Test Code N16 Branch: Multiple Date: (50 Marks)

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8. CA. Anurag Singal

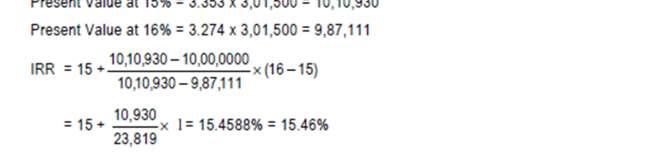

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8 CA. Anurag Singal Internal Rate of Return Miscellaneous Sums Internal Rate of Return (IRR) is the rate at which NPV = 0 XYZ Ltd., an

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8 CA. Anurag Singal Internal Rate of Return Miscellaneous Sums Internal Rate of Return (IRR) is the rate at which NPV = 0 XYZ Ltd., an

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

SOLUTIONS TO ASSIGNMENT PROBLEMS. Problem No.1 10,000 5,000 15,000 20,000. Problem No.2. Problem No.3

MASTER MINDS No. for CA/CWA & MEC/CEC. CAPITAL BUDGETING SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. Calculation of ARR for machine A and B: Machine A Step : Average Profit After Tax 5,, 5,, 5, Total

MASTER MINDS No. for CA/CWA & MEC/CEC. CAPITAL BUDGETING SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. Calculation of ARR for machine A and B: Machine A Step : Average Profit After Tax 5,, 5,, 5, Total

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM. Test Code CIM 8109

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT - FM Test Code CIM 8109 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT - FM Test Code CIM 8109 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM. Test Code CIN 5001

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM FM Test Code CIN 5001 BRANCH- MULTIPLE (Date : 08.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM FM Test Code CIN 5001 BRANCH- MULTIPLE (Date : 08.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Gurukripa s Guideline Answers to Nov 2015 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management

Cost Accounting & Financial Management") Gurukripa s Guideline Answers to Nov 2015 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Question No.1 is compulsory (4 5 = 20 Marks). Answer any five questions from the remaining

Gurukripa s Guideline Answers to Nov 2015 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Question No.1 is compulsory (4 5 = 20 Marks). Answer any five questions from the remaining

MTP_Intermediate_Syl2016_June2017_Set 1 Paper 10- Cost & Management Accounting and Financial Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM SUBJECT- F.M. Test Code CIN 5021 (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e ANSWER-1

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM SUBJECT- F.M. Test Code CIN 5021 (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e ANSWER-1

Gurukripa s Guideline Answers to Nov 2010 IPCC Exam Questions

Gurukripa s Guideline Answers to Nov 2010 IPCC Exam Questions Question No.1 is compulsory (4 X 5 20 Marks). Answer any five questions from the remaining six questions (16 X 5 80 Marks). Question 1(a):

Gurukripa s Guideline Answers to Nov 2010 IPCC Exam Questions Question No.1 is compulsory (4 X 5 20 Marks). Answer any five questions from the remaining six questions (16 X 5 80 Marks). Question 1(a):

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

(All Batches) DATE: MAXIMUM MARKS: 100 TIMING: 3¼ Hours

DATE: MAXIMUM MARKS: 100 TIMING: 3¼ Hours") (All Batches) DATE: 16.04.2018 MAXIMUM MARKS: 100 TIMING: 3¼ Hours FINANCIAL MANAGEMENT & ECONOMICS FOR FINANCE SECTION A Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made

(All Batches) DATE: 16.04.2018 MAXIMUM MARKS: 100 TIMING: 3¼ Hours FINANCIAL MANAGEMENT & ECONOMICS FOR FINANCE SECTION A Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made

Gurukripa s Guideline Answers to May 2012 Exam Questions IPCC Cost Accounting and Financial Management

Gurukripa s Guideline Answers to May 2012 Exam Questions IPCC Cost Accounting and Financial Management Question No.1 is compulsory (4 5 20 Marks). Answer any five questions from the remaining six questions

Gurukripa s Guideline Answers to May 2012 Exam Questions IPCC Cost Accounting and Financial Management Question No.1 is compulsory (4 5 20 Marks). Answer any five questions from the remaining six questions

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT 1 Test Series: March, 2017 Answers are to be given only in English except in the case of the candidates who

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT 1 Test Series: March, 2017 Answers are to be given only in English except in the case of the candidates who

CA - IPCC. Quality Education beyond your imagination...! Solutions to Assignment Problems in Financial Management_31e

CA - IPCC COURSE MATERIAL Quality Education beyond your imagination...! Solutions to Assignment Problems in Financial Management_31e Visit us @ www.gntmasterminds.com, Mail : mastermindsinfo@ymail.com

CA - IPCC COURSE MATERIAL Quality Education beyond your imagination...! Solutions to Assignment Problems in Financial Management_31e Visit us @ www.gntmasterminds.com, Mail : mastermindsinfo@ymail.com

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

Important questions prepared by Mirza Rafathulla Baig. For B.com & MBA Important questions visit

Financial Management -MBA-II SEM 1. Charm plc, a software company, has developed a new game, Fingo, which it plans to launch in the near future. Sales of the new game are expected to be very strong, following

Financial Management -MBA-II SEM 1. Charm plc, a software company, has developed a new game, Fingo, which it plans to launch in the near future. Sales of the new game are expected to be very strong, following

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE

MANAGEMENT ACCOUNTING AND FINANCE") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks, 1.

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks, 1.

Capital Budgeting. Questions 4, 5, 8, 9, 12, 15, 16, 19, 22, 23, 24, 25, 27, 45, 61, 62, 63, 64, 65, 66

Financial Management 1 Capital Budgeting LIST OF IMPORTANT QUESTIONS MUST TO REVISE Questions 4, 5, 8, 9, 12, 15, 16, 19, 22, 23, 24, 25, 27, 45, 61, 62, 63, 64, 65, 66 Rest also to be done but list of

Financial Management 1 Capital Budgeting LIST OF IMPORTANT QUESTIONS MUST TO REVISE Questions 4, 5, 8, 9, 12, 15, 16, 19, 22, 23, 24, 25, 27, 45, 61, 62, 63, 64, 65, 66 Rest also to be done but list of

Question 1. (i) Standard output per day. Actual output = 37 units. Efficiency percentage 100

Standard output per day. Actual output = 37 units. Efficiency percentage 100") Question 1 PAPER 4 : COST ACCOUNTING AND FINANCIAL MANAGEMENT All questions are compulsory. Working notes should form part of the answer wherever appropriate, suitable assumptions should be made. Answer

Question 1 PAPER 4 : COST ACCOUNTING AND FINANCIAL MANAGEMENT All questions are compulsory. Working notes should form part of the answer wherever appropriate, suitable assumptions should be made. Answer

Suggested Answer_Syl2012_Jun2014_Paper_20 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

Answer to MTP_Intermediate_Syllabus 2012_Jun2017_Set 1 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM. Test Code - CIM 8059

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT - FM Test Code - CIM 8059 BRANCH - () (Date : 09/09/2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT - FM Test Code - CIM 8059 BRANCH - () (Date : 09/09/2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

Gurukripa s Guideline Answers to Nov 2016 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Working Notes should form part of the answers. Question No.1 is compulsory (4 5 20 Marks).

Gurukripa s Guideline Answers to Nov 2016 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Working Notes should form part of the answers. Question No.1 is compulsory (4 5 20 Marks).

FINAL CA May 2018 Strategic Financial Management. Test Code F3 Branch: DADAR Date: (50 Marks) All questions are. compulsory.

All questions are. compulsory.") FINAL CA May 2018 Strategic Financial Management Test Code F3 Branch: DADAR Date: 03.12.2017 compulsory. Note: (50 Marks) All questions are Question 1 (10 marks) (i) E Ltd. H Ltd. (ii) (iii) Market capitalisation

FINAL CA May 2018 Strategic Financial Management Test Code F3 Branch: DADAR Date: 03.12.2017 compulsory. Note: (50 Marks) All questions are Question 1 (10 marks) (i) E Ltd. H Ltd. (ii) (iii) Market capitalisation

Chapter -9 Financial Management

Chapter -9 Financial Management Business Studies (VKS) Definition Financial management is concerned with efficient acquisition and allocation of funds. In other words, financial management means estimating

Chapter -9 Financial Management Business Studies (VKS) Definition Financial management is concerned with efficient acquisition and allocation of funds. In other words, financial management means estimating

MTP_Intermediate_Syllabus 2012_Jun2017_Set 1 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 7 Total number of printed pages : 7

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 7 Total number of printed pages : 7 NOTE : 1. Answer FIVE questions including Question No.1 which is compulsory. All

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 7 Total number of printed pages : 7 NOTE : 1. Answer FIVE questions including Question No.1 which is compulsory. All

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

The Institute of Chartered Accountants of India

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Working notes should form part of the answer Question 1 (a) Human

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Working notes should form part of the answer Question 1 (a) Human

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

BATCH : All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours COST ACCOUNTING AND FINANCIAL MANAGEMENT. = 1.5 kg. 250 units = 450 kg.

MITTAL COMMERCE CLASSES IPCC MOCK TEST BATCH : All Batches DATE: 20.09.2016 MAXIMUM MARKS: 100 TIMING: 3 Hours COST ACCOUNTING AND FINANCIAL MANAGEMENT Answer 1(a) Actual production of P 250 units Standard

MITTAL COMMERCE CLASSES IPCC MOCK TEST BATCH : All Batches DATE: 20.09.2016 MAXIMUM MARKS: 100 TIMING: 3 Hours COST ACCOUNTING AND FINANCIAL MANAGEMENT Answer 1(a) Actual production of P 250 units Standard

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

DFM-01,02,03,04. January (Diploma In Financial Management) :-DFM. Dr. Babasaheb Ambedkar Open University

:-DFM. Dr. Babasaheb Ambedkar Open University") Dr. Babasaheb Ambedkar Open University 'Jyotirmay' Parisar, Opp. Balaji Temple, Sarkhej-Gandhinagar Highway, Chharodi, Ahmedabad-382 481 E-mail: feedback@baou.edu.in Website : www.baou.edu.in January -2016

Dr. Babasaheb Ambedkar Open University 'Jyotirmay' Parisar, Opp. Balaji Temple, Sarkhej-Gandhinagar Highway, Chharodi, Ahmedabad-382 481 E-mail: feedback@baou.edu.in Website : www.baou.edu.in January -2016

SAMVIT ACADEMY IPCC MOCK EXAM

SUGGESTED ANSWERS - Group 1 Costing (Code FUN) Disclaimer (Read carefully) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

SUGGESTED ANSWERS - Group 1 Costing (Code FUN) Disclaimer (Read carefully) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

9706 ACCOUNTING. 9706/01 Paper 1 (Multiple Choice), maximum raw mark /02 Paper 2 (Structured Questions), maximum raw mark 90

, maximum raw mark /02 Paper 2 (Structured Questions), maximum raw mark 90") UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary and Advanced Level MARK SCHEME for the June 2004 question papers 9706 ACCOUNTING 9706/01 Paper 1 (Multiple Choice), maximum raw

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary and Advanced Level MARK SCHEME for the June 2004 question papers 9706 ACCOUNTING 9706/01 Paper 1 (Multiple Choice), maximum raw

Sree Lalitha Academy s Key for CA IPC Costing & FM- Nov 2013

1. a. Question No.1 is compulsory Answer any 5 questions from the remaining 6 questions (Key Covers only Problems does not include theory) i. Annual Demand 60,000 Units Cost Rs. 10 Per unit Cost of Placing

1. a. Question No.1 is compulsory Answer any 5 questions from the remaining 6 questions (Key Covers only Problems does not include theory) i. Annual Demand 60,000 Units Cost Rs. 10 Per unit Cost of Placing

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT. FCA, CFA L3 Candidate

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

Financial Management - Important questions for IPCC November 2017

Financial Management - Important questions for IPCC November 2017 BASICS OF FINANCIAL MANAGEMENT 1. Discuss conflict in profit versus wealth maximization objective Conflict in Profit versus Wealth Maximization

Financial Management - Important questions for IPCC November 2017 BASICS OF FINANCIAL MANAGEMENT 1. Discuss conflict in profit versus wealth maximization objective Conflict in Profit versus Wealth Maximization

WEEK 7 Investment Appraisal -1

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

UNIT 2 FINANCING DECISION

UNIT 2 FINANCING DECISION Capital structure Capital structure is the permanent long term financing that is represented by long term debt, preference share capital, equity share capital and retained earnings.

UNIT 2 FINANCING DECISION Capital structure Capital structure is the permanent long term financing that is represented by long term debt, preference share capital, equity share capital and retained earnings.

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

Downloaded From visit: for more updates & files...

Downloaded From http://www.cacracker.com, visit: http://www.cacracker.com for more updates & files... 1 PP FTFM December 2011 PROFESSIONAL PROGRAMME EXAMINATION DECEMBER 2011 FINANCIAL, TREASURY AND FOREX

Downloaded From http://www.cacracker.com, visit: http://www.cacracker.com for more updates & files... 1 PP FTFM December 2011 PROFESSIONAL PROGRAMME EXAMINATION DECEMBER 2011 FINANCIAL, TREASURY AND FOREX

Copyright -The Institute of Chartered Accountants of India. The forward contract is sold before its due date, hence considered as speculative.

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

SOLUTIONS TO ASSIGNMENT PROBLEMS. Problem No.1

W.N.-1: Calculation of depreciation per annum Depreciation p.a. = SOLUTIONS TO ASSIGNMENT PROBLEMS Cost -Scrap Value Life W.N.-2: Calculation of PAT p.a. Problem No.1 80,000 5 10,000 = Rs.14,000 p.a. 2.

W.N.-1: Calculation of depreciation per annum Depreciation p.a. = SOLUTIONS TO ASSIGNMENT PROBLEMS Cost -Scrap Value Life W.N.-2: Calculation of PAT p.a. Problem No.1 80,000 5 10,000 = Rs.14,000 p.a. 2.

Suggested Answer_Syl12_Dec2014_Paper_8 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-8: COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-8: COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

The Institute of Chartered Accountants of India

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I: COST ACCOUNTING QUESTIONS Material 1. Arnav Udyog, a small scale manufacturer, produces a product X by using two raw materials A and B in the ratio

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I: COST ACCOUNTING QUESTIONS Material 1. Arnav Udyog, a small scale manufacturer, produces a product X by using two raw materials A and B in the ratio

Suggested Answer_Syl2012_Dec2014_Paper_20 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

Answer to MTP_Intermediate_Syl2016_June2017_Set 2 Paper 10- Cost & Management Accounting and Financial Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Answer to MTP_Intermediate_Syl2016_June2017_Set 1 Paper 10- Cost & Management Accounting and Financial Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

The nature of investment decision

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

Capital investment decisions: 1

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Answer to MTP_Final_Syllabus 2012_Dec 2014_Set 2

Paper 20: Financial Analysis & Business Valuation Time Allowed: 3 hours Full Marks: 100 This paper contains 4 questions, representing two separate sections as prescribed under syllabus 2012. All questions

Paper 20: Financial Analysis & Business Valuation Time Allowed: 3 hours Full Marks: 100 This paper contains 4 questions, representing two separate sections as prescribed under syllabus 2012. All questions

No. of Pages: 7 Total Marks: 100

LG No. of Pages: 7 Total Marks: 100 No of Questions: 7 Time Allowed: 3 Hrs Question No. 1 is compulsory Answer any five questions from the remaining six questions. Wherever necessary, suitable assumption(s)

LG No. of Pages: 7 Total Marks: 100 No of Questions: 7 Time Allowed: 3 Hrs Question No. 1 is compulsory Answer any five questions from the remaining six questions. Wherever necessary, suitable assumption(s)

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS") 1. (a) Working notes: MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I Test Series: October, 2015 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS 1. (i) Number of units sold at

1. (a) Working notes: MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I Test Series: October, 2015 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS/ HINTS 1. (i) Number of units sold at

DISCLAIMER.

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Class 12 Accountancy NCERT Solutions Cash Flow Statement

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

CS 413 Software Project Management LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

First Edition : May 2018 Published By : Directorate of Studies The Institute of Cost Accountants of India

First Edition : May 2018 Published By : Directorate of Studies The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata 700 016 www.icmai.in Copyright of these study notes is reserved

First Edition : May 2018 Published By : Directorate of Studies The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata 700 016 www.icmai.in Copyright of these study notes is reserved

Rupees Product RAX (552,000 x Rs.360) 198,720,

198,720,") Question No. 2 (a) Break-even Sales Revenue: SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 8 Calculation of total contribution: Product RAX (552,000 x Rs.216) 119,232,000 0.5 Product MAX (1,200,000

Question No. 2 (a) Break-even Sales Revenue: SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 8 Calculation of total contribution: Product RAX (552,000 x Rs.216) 119,232,000 0.5 Product MAX (1,200,000

Scanner Appendix. IPCC Gr. I (Solution of May ) Paper - 3 : Cost Accounting and Financial Management. Paper - 3A : Cost Accounting

Paper - 3 : Cost Accounting and Financial Management. Paper - 3A : Cost Accounting") Solved Scanner Appendix IPCC Gr. I (Solution of May - 2016) Paper - 3 : Cost Accounting and Financial Management Paper - 3A : Cost Accounting Chapter - 1 : Basic Concepts 2016 - May [5] (a) Basis of Cost

Solved Scanner Appendix IPCC Gr. I (Solution of May - 2016) Paper - 3 : Cost Accounting and Financial Management Paper - 3A : Cost Accounting Chapter - 1 : Basic Concepts 2016 - May [5] (a) Basis of Cost

1 INVESTMENT DECISIONS,

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

Rs. 75,00,000 Rs. 1,00,00,000

Test Series: April 2018 MOCK TEST PAPER II INTERMEDIATE (IPC): GROUP II PAPER 8: FINANCIAL MANAGEMENT& ECONOMICS FOR FINANCE 1. (a) Firm A Ltd. (pure equity): unlevered firm: EAT = EBIT (1 t) PAPER 8A

Test Series: April 2018 MOCK TEST PAPER II INTERMEDIATE (IPC): GROUP II PAPER 8: FINANCIAL MANAGEMENT& ECONOMICS FOR FINANCE 1. (a) Firm A Ltd. (pure equity): unlevered firm: EAT = EBIT (1 t) PAPER 8A

MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I

: GROUP I") MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I Test Series: September, 2015 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Answers are to be given only in English except in the case of the candidates

MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I Test Series: September, 2015 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Answers are to be given only in English except in the case of the candidates

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

Answer to MTP_Final_ Syllabus 2012_December 2016_Set 2. Paper 20: Financial Analysis and Business Valuation

Paper 20: Financial Analysis and Business Valuation Page 1 of 21 Paper 20- Financial Analysis and Business Valuation Full Marks: 100 Time allowed: 3 Hours Question No. 1 which is compulsory and carries

Paper 20: Financial Analysis and Business Valuation Page 1 of 21 Paper 20- Financial Analysis and Business Valuation Full Marks: 100 Time allowed: 3 Hours Question No. 1 which is compulsory and carries

INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS

CHAPTER8 INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS PROBABILISTIC APPROACH Question 1: A project under consideration is likely to cost `5 lakh by way of fixed assets and requires

CHAPTER8 INTRODUCTION TO RISK ANALYSIS IN CAPITAL BUDGETING PRACTICAL PROBLEMS PROBABILISTIC APPROACH Question 1: A project under consideration is likely to cost `5 lakh by way of fixed assets and requires

Before discussing capital expenditure decision methods, we may understand following three points:

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 7 Capital Budgeting (Capital Expenditure decisions) Chapter Index Method Based on Accounting

KE2 MCQ Questions. Identify the feasible projects Alpha can select to invest.

KE2 MCQ Questions Question 01 You are required to choose the most appropriate answer. 1.1 Company Alpha is considering following four independent projects for investment. The initial cash outflow required

KE2 MCQ Questions Question 01 You are required to choose the most appropriate answer. 1.1 Company Alpha is considering following four independent projects for investment. The initial cash outflow required

Answer to MTP_Intermediate_Syllabus 2012_Dec2013_Set 1

Paper 8 Cost Accounting & Financial Management Section A Cost Accounting Prime Costs & Overheads (Full Marks : 60) Answer Question no.1 which is compulsory and any three from the rest in this section.

Paper 8 Cost Accounting & Financial Management Section A Cost Accounting Prime Costs & Overheads (Full Marks : 60) Answer Question no.1 which is compulsory and any three from the rest in this section.

Suggested Answer_Syl12_Dec2017_Paper 14 FINAL EXAMINATION

FINAL EXAMINATION GROUP III (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 14: ADVANCED FINANCIAL MANAGEMENT Time Allowed: 3 Hours Full Marks: 100 The figures on the right margin indicate

FINAL EXAMINATION GROUP III (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 14: ADVANCED FINANCIAL MANAGEMENT Time Allowed: 3 Hours Full Marks: 100 The figures on the right margin indicate

Solved Answer COST & F.M. CA IPCC Nov

Solved Answer COST & F.M. CA IPCC Nov. 2009 1 1. Answer any five of the following : [5x2=10 marks] (i) Define the following : (a) Imputed cost (b) Capitalised cost. (ii) Calculate efficiency, and activity

Solved Answer COST & F.M. CA IPCC Nov. 2009 1 1. Answer any five of the following : [5x2=10 marks] (i) Define the following : (a) Imputed cost (b) Capitalised cost. (ii) Calculate efficiency, and activity

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING Question 1 is compulsory (4 5 = 20 Marks) Answer any five questions from the remaining six questions (16 5 = 80 Marks).

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING Question 1 is compulsory (4 5 = 20 Marks) Answer any five questions from the remaining six questions (16 5 = 80 Marks).

MG 177 Third Year B. B. A. Examination April / May 2003 Advanced Financial Management

MG 177 Third Year B. B. A. Examination April / May 2003 Advanced Financial Management Seat No. Time : 3 Hours] [Total Marks : 70 Instructions : (1) All the calculations-work sheet should be a part of your

MG 177 Third Year B. B. A. Examination April / May 2003 Advanced Financial Management Seat No. Time : 3 Hours] [Total Marks : 70 Instructions : (1) All the calculations-work sheet should be a part of your

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

Ratio Analysis. CA Past Years Exam Question

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Appendix. IPCC Gr. I (Solution of May ) Paper - 3A : Cost Accounting

Paper - 3A : Cost Accounting") Solved Scanner Appendix IPCC Gr. I (Solution of May - 2015 ) Paper - 3A : Cost Accounting Chapter - 1: Basic Concepts 2015 - May [5] (a) Sunk Cost: Sunk costs are historical costs incurred in the past

Solved Scanner Appendix IPCC Gr. I (Solution of May - 2015 ) Paper - 3A : Cost Accounting Chapter - 1: Basic Concepts 2015 - May [5] (a) Sunk Cost: Sunk costs are historical costs incurred in the past

What is it? Measure of from project. The Investment Rule: Accept projects with NPV and accept highest NPV first

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F9 Branch : Borivali Date: 17.12.2017 (50 Marks) compulsory. Note: All questions are Question 1 (9 marks) Following information is provided in respect of

FINAL CA May 2018 Financial Reporting Test Code F9 Branch : Borivali Date: 17.12.2017 (50 Marks) compulsory. Note: All questions are Question 1 (9 marks) Following information is provided in respect of

Financial Management Questions

Financial Management Questions Question 1. What Is The Financial Management Reform? The Financial Management Reform is the new policy framework that had been adopted by the Fiji Government to improve performance

Financial Management Questions Question 1. What Is The Financial Management Reform? The Financial Management Reform is the new policy framework that had been adopted by the Fiji Government to improve performance

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA32) MANAGEMENT ACCOUNTING AND FINANCE

MANAGEMENT ACCOUNTING AND FINANCE") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks,

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks,

Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions.

Question 1 (i) (ii) PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions. What is Cost accounting? Enumerate its important objectives. Distinguish between Fixed

Question 1 (i) (ii) PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions. What is Cost accounting? Enumerate its important objectives. Distinguish between Fixed