Loan Modifications: Determining What Programs are Available. Joseph Rebella Senior Staff Attorney MFY Legal Services, Inc.

|

|

|

- Myra Curtis

- 6 years ago

- Views:

Transcription

1 Loan Modifications: Determining What Programs are Available Joseph Rebella Senior Staff Attorney MFY Legal Services, Inc.

an FHA-insured loan, (2) held by Fannie Mae or Freddie Mac, (3) serviced by a company")

2 Different Loan Modification Programs The availability of loan modification programs depends on the insurer, investor and servicer. To determine what workout programs are available, the counselor should determine whether or not the loan is (1) an FHA-insured loan, (2) held by Fannie Mae or Freddie Mac, (3) serviced by a company that participates in Making Home Affordable (MHA) or (4) none of the above.

3 3

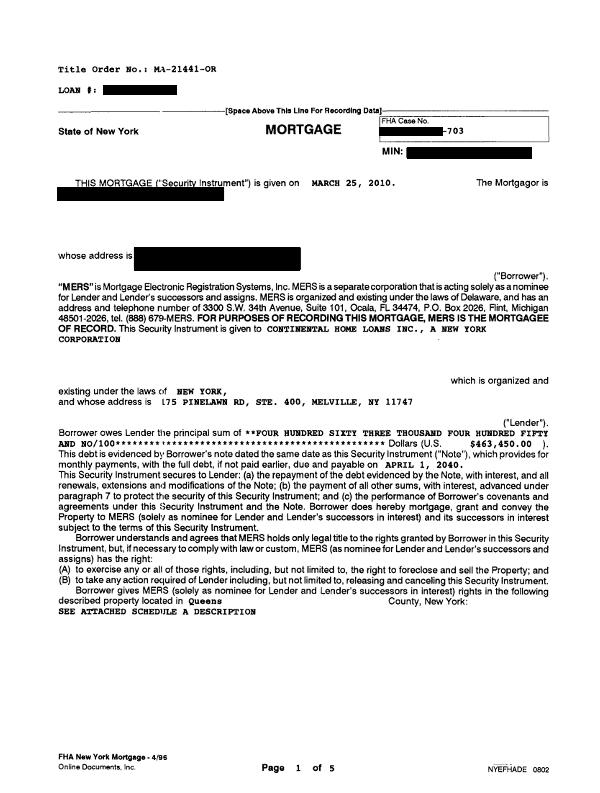

4 FHA Loans FHA is the Federal Housing Administration, which is a branch of HUD. Loans insured by FHA are serviced according to FHA s loss mitigation rules - which are described in the resource guide and in the FHA User s Guide on MFY s website. You can tell that a loan is an FHA loan by looking at the mortgage, which will have an FHA Case Number on the first page. Also, if the mortgage statement includes a charge for MIP or FHA Insurance.

5

6 Fannie Mae/Freddie Mac Loans Fannie Mae and Freddie Mac are both Government Sponsored Entities (GSEs) that own and insure mortgage loans. GSE loans must be serviced according to detailed guides set forth by the relevant GSE. Determine whether the loan is a Fannie or Freddie loan by using the GSEs websites to look up the mortgage. Freddie Mac s and Fannie Mae s lookup tools are available at and respectively. Both loan lookup tools require the borrower s name, address and the last four digits of his or her Social Security Number. The online lookup tools are not always accurate. GSE Loans are eligible for HAMP and Standard Modifications.

7 MHA Servicers Certain companies have agreed to participate in HAMP even for non-gse loans. A list of companies that have agreed to participate is available here: Loans serviced by participating servicers are eligible for HAMP and HAMP Tier 2. Notable exceptions to MHA participation include HSBC and Caliber. If the loan doesn t meet any of these criteria i.e. not FHA, not GSE, not MHA then the servicer may still have an inhouse modification program.

8 Non-Economic Criteria For Modifications Each program has both economic and non-economic criteria. The economic criteria are more complex and change more often the economic criteria for each program are described in the resource guide. The non-economic criteria are easier to determine. In this presentation, we ll discuss: Origination Date Owner Occupancy Prior Modification Prior Trial Plan Default Additionally, every program is limited to 1-4 unit residential properties.

9 Origination Date Restrictions The origination date is the date that the loan was made. It refers to the original date of the mortgage (including a consolidation if the mortgage arose from a consolidation). It does not refer to a modification date, if there was a prior modification. Origination date requirements: HAMP on or before January 1, 2009 HAMP Tier 2 on or before January 1, 2009 GSE Standard Modifications at least 12 months prior to evaluation FHA at least 12 months prior to evaluation, and borrower must have made at least 4 payments.

10 Owner Occupancy Restrictions HAMP must be owner occupied (unless displacement due to military service). HAMP Tier 2 may be owner occupied, family occupied, or a rental (may be vacant if available for rent); may not be a vacation home, second home or abandoned. GSE Standard Modifications any property that is not abandoned or condemned. FHA must be owner occupied.

11 Prior Modification Restrictions Re-defaults on prior modifications are becoming increasingly common Effect of a prior modification: FHA-HAMP: must have been at least 24 months since the last modification. HAMP: cannot have had a prior HAMP or a prior HAMP Tier 2 prior GSE Standard Modification is fine. Cannot have had a prior HAMP on any other property, as well (even if the borrower has moved). HAMP Tier 2: cannot have had a prior HAMP Tier 2 modification prior HAMP modification is fine. GSE Standard Modification: maximum of two previous modifications of any sort.

12 Prior Trial Plan Default Restrictions Default on a trial plan (TPP) may affect rights to future modification. A borrower does not default on a trial plan if the borrower (1) makes all the trial plan payments, but does not receive a permanent modification, (2) makes all the trial plan payments, but does not accept the permanent modification, or (3) doesn t make any of the trial plan payments. Effect of a prior trial plan: FHA-HAMP: must show a change in circumstances. HAMP: cannot have had a TPP default under HAMP or HAMP Tier 2 prior GSE Standard Modification TPP default is ok. HAMP Tier 2: cannot have had a prior HAMP Tier 2 TPP default. GSE Standard Modification: must not have failed a GSE Standard Modification TPP in the last 12 months.

HAMP. The Hamp Program. Avoid Foreclosure. More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages

The Program Works to Help Homeowners Avoid Foreclosure Avoid Foreclosure HAMP More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages What is HAMP? Home Affordable Modification

The Program Works to Help Homeowners Avoid Foreclosure Avoid Foreclosure HAMP More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages What is HAMP? Home Affordable Modification

Supplemental Directive January 29, 2015

Supplemental Directive 15-01 January 29, 2015 Making Home Affordable Program MHA Program Updates In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program to stabilize

Supplemental Directive 15-01 January 29, 2015 Making Home Affordable Program MHA Program Updates In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program to stabilize

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams Exam structure and tips: Structure: the exam is composed of 20-25 questions divided into two parts

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams Exam structure and tips: Structure: the exam is composed of 20-25 questions divided into two parts

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015

Compensation Last Updated: April 30, 2015") Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015 Program Name Frequency and Timing Payee/Beneficiary Amount Accrual and Notes Servicer Incentive One time Servicer/Servicer Non-GSE

Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015 Program Name Frequency and Timing Payee/Beneficiary Amount Accrual and Notes Servicer Incentive One time Servicer/Servicer Non-GSE

MHA Reason Codes and Descriptions

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012

LOAN MODIFICATION UPDATE July 17, 2012") HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012 Diane Thompson, NCLC, Moderator Jeff Gentes, Connecticut Fair Housing Center Lisa Sitkin, Housing and Economic Rights Advocates 0 The World of

HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012 Diane Thompson, NCLC, Moderator Jeff Gentes, Connecticut Fair Housing Center Lisa Sitkin, Housing and Economic Rights Advocates 0 The World of

First Lien Modification Program Home Affordable Modification Program. Phase 1 Engagement

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet

Eligibility Worksheet") Loan Look Up Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet HAFA: A Making Home Affordable (MHA) Initiative Determine the type of first lien (Fannie Mae, Freddie Mac or Treasury)

Loan Look Up Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet HAFA: A Making Home Affordable (MHA) Initiative Determine the type of first lien (Fannie Mae, Freddie Mac or Treasury)

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers

Model (v5.02) Training Module for Servicers") Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 9 HAMP Eligibility Criteria Base NPV Model Overview Standard and Alternative Modification

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 9 HAMP Eligibility Criteria Base NPV Model Overview Standard and Alternative Modification

HAMP Trusted Advisor 1

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Standard and Alternative Waterfalls 1

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

HAMP Home Affordable Modification Program UPDATE

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017 1 Diane Cipollone, Esq. Consultant to National Fair Housing Alliance Former Director

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017 1 Diane Cipollone, Esq. Consultant to National Fair Housing Alliance Former Director

Supplemental Directive December 10, 2013

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive October 18, 2013

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix

Home Affordable Foreclosure Alternative (HAFA) Matrix") Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Servicing Alignment Initiative Overview for Freddie Mac Servicers

Servicing Alignment Initiative Overview for Freddie Mac Servicers Consistent requirements and processes for servicing delinquent mortgages Working at the direction of, and in concert with, the Federal

Servicing Alignment Initiative Overview for Freddie Mac Servicers Consistent requirements and processes for servicing delinquent mortgages Working at the direction of, and in concert with, the Federal

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Year over Year Q2-211 to H1 212 Q2-211 Q3-211 Q4-211 Q1-212 Q2-212 Apr-212 May-212 Jun-212 Q2-212 Total Completed Modifications 251,424 255,667 24,523 23,463 182,6 56,922 61,489 63,594-28% 385,468 HAMP

Year over Year Q2-211 to H1 212 Q2-211 Q3-211 Q4-211 Q1-212 Q2-212 Apr-212 May-212 Jun-212 Q2-212 Total Completed Modifications 251,424 255,667 24,523 23,463 182,6 56,922 61,489 63,594-28% 385,468 HAMP

Supplemental Directive November 3, Home Affordable Modification Program Borrower Notices

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

SUBJECT: NEIGHBORHOOD STABILIZATION INITIATIVE MYCITY MODIFICATION FOR THE CITY OF DETROIT, MICHIGAN

TO: Freddie Mac Servicers June 18, 2014 2014-11 SUBJECT: NEIGHBORHOOD STABILIZATION INITIATIVE MYCITY MODIFICATION FOR THE CITY OF DETROIT, MICHIGAN This Single-Family Seller/Servicer Guide ( Guide ) Bulletin

TO: Freddie Mac Servicers June 18, 2014 2014-11 SUBJECT: NEIGHBORHOOD STABILIZATION INITIATIVE MYCITY MODIFICATION FOR THE CITY OF DETROIT, MICHIGAN This Single-Family Seller/Servicer Guide ( Guide ) Bulletin

Supplemental Directive September 30, 2014

Supplemental Directive 14-03 September 30, 2014 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 14-03 September 30, 2014 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive August 30, 2013

Supplemental Directive 13-06 August 30, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-06 August 30, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive March 1, 2013

Supplemental Directive 13-01 March 1, 2013 Making Home Affordable Program Making Home Affordable Outreach and Borrower Intake Project In February 2009, the Obama Administration introduced the Making Home

Supplemental Directive 13-01 March 1, 2013 Making Home Affordable Program Making Home Affordable Outreach and Borrower Intake Project In February 2009, the Obama Administration introduced the Making Home

Supplemental Directive November 30, 2012

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Making Home Affordable

Making Home Affordable Today s Topics: MHA Resources MHA Refinance (HARP) MHA Loan Modifications (HAMP) Other Programs for Borrowers 2 What is Making Home Affordable? Part of President Obama s Homeowner

Making Home Affordable Today s Topics: MHA Resources MHA Refinance (HARP) MHA Loan Modifications (HAMP) Other Programs for Borrowers 2 What is Making Home Affordable? Part of President Obama s Homeowner

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu *

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu * Description & Purpose Contents As a condition to receiving the incentive payments offered through the Home Affordable

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu * Description & Purpose Contents As a condition to receiving the incentive payments offered through the Home Affordable

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

Understanding the Terms of a HAMP Modification: Interest Rate Increase, Impact, and Resources. Training Presentation for Trusted Advisors

Understanding the Terms of a HAMP Modification: Interest Rate Increase, Impact, and Resources Training Presentation for Trusted Advisors Making Making Home Making Home Affordable Home Affordable Affordable

Understanding the Terms of a HAMP Modification: Interest Rate Increase, Impact, and Resources Training Presentation for Trusted Advisors Making Making Home Making Home Affordable Home Affordable Affordable

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q2-215 Q3-215 Q4-215 Q1-216 Q2-216 Jun-16 Jul-16 Aug-16 Total Completed Modifications 119,658 97,773 84,798 86,167 1,198 41,872 34,815 36,6

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q2-215 Q3-215 Q4-215 Q1-216 Q2-216 Jun-16 Jul-16 Aug-16 Total Completed Modifications 119,658 97,773 84,798 86,167 1,198 41,872 34,815 36,6

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) Keeping families in their homes is a top priority for REALTORS. Unfortunately, it is not always

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) Keeping families in their homes is a top priority for REALTORS. Unfortunately, it is not always

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness Edward DeMarco, Acting Director Federal Housing Finance Agency The Brookings Institution April 10, 2012 My goal today is to answer

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness Edward DeMarco, Acting Director Federal Housing Finance Agency The Brookings Institution April 10, 2012 My goal today is to answer

Version 2.0 As of September 22, 2010

Version 2.0 As of September 22, 2010 MHA Handbook v2.0 1 FOREWORD... 6 OVERVIEW... 7 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 11 1 SERVICER PARTICIPATION IN MHA... 12 1.1 SERVICER PARTICIPATION

Version 2.0 As of September 22, 2010 MHA Handbook v2.0 1 FOREWORD... 6 OVERVIEW... 7 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 11 1 SERVICER PARTICIPATION IN MHA... 12 1.1 SERVICER PARTICIPATION

Supplemental Directive December 21, 2017

Supplemental Directive 17-02 December 21, 2017 Making Home Affordable Program Handbook for Servicers Version 5.2 and Administrative Clarifications In February 2009, the Federal Government introduced the

Supplemental Directive 17-02 December 21, 2017 Making Home Affordable Program Handbook for Servicers Version 5.2 and Administrative Clarifications In February 2009, the Federal Government introduced the

Loan Modifications 101 Tara Twomey National Consumer Law Center

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Supplemental Directive December 10, Making Home Affordable Program Program End Date and Administrative Clarifications

Supplemental Directive 18-01 December 10, 2018 Making Home Affordable Program Program End Date and Administrative Clarifications In February 2009, the Making Home Affordable (MHA) Program was introduced

Supplemental Directive 18-01 December 10, 2018 Making Home Affordable Program Program End Date and Administrative Clarifications In February 2009, the Making Home Affordable (MHA) Program was introduced

UNIFORM BORROWER ASSISTANCE FORM

If you are experiencing a temporary or long term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

If you are experiencing a temporary or long term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

Navigating the Loan Modification Process Part III. Presented by: Empire Justice Center Kevin Purcell, Esq.

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Loss Mitigation Trends and Tips OCTOBER 3, 2017

Loss Mitigation Trends and Tips OCTOBER 3, 2017 Current Trends Modifications are now a mixed bag Depends on the type of loan and investor In general, the trend seems to be: 30 or 40-year term Market interest

Loss Mitigation Trends and Tips OCTOBER 3, 2017 Current Trends Modifications are now a mixed bag Depends on the type of loan and investor In general, the trend seems to be: 30 or 40-year term Market interest

Announcement SVC September 21, 2010

Announcement SVC-2010-15 September 21, 2010 Updates to Fannie Mae's Forbearance, Income Eligibility, and Home Affordable Modification Program Requirements. Introduction In this Announcement, Fannie Mae

Announcement SVC-2010-15 September 21, 2010 Updates to Fannie Mae's Forbearance, Income Eligibility, and Home Affordable Modification Program Requirements. Introduction In this Announcement, Fannie Mae

CheckMyNPV.com Overview for Trusted Advisors

Overview CheckMyNPV.com Overview for Trusted Advisors Agenda 1 2 3 4 5 6 MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 2 MHA

Overview CheckMyNPV.com Overview for Trusted Advisors Agenda 1 2 3 4 5 6 MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 2 MHA

Streamline HAMP Modification Process. Training for Servicers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Loss Mitigation Application

Loss Mitigation Application If you are experiencing a financial hardship and need help, please complete this form. In order to recommend you for a loss mitigation program, we must receive the following

Loss Mitigation Application If you are experiencing a financial hardship and need help, please complete this form. In order to recommend you for a loss mitigation program, we must receive the following

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

Foreclosure Diversion Program Information Session. Understanding and Preparing for Mediation

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Fannie Mae Flex Modification. 1. Welcome Intro. 1.1 Welcome. 1.2 Objectives. Notes: Notes: Published by Articulate Storyline

Fannie Mae Flex Modification 1. Welcome Intro 1.1 Welcome Notes: Welcome, and thank you for taking time to view the Fannie Mae Flex Modification course. 1.2 Objectives Notes: Published by Articulate Storyline

Fannie Mae Flex Modification 1. Welcome Intro 1.1 Welcome Notes: Welcome, and thank you for taking time to view the Fannie Mae Flex Modification course. 1.2 Objectives Notes: Published by Articulate Storyline

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

National Foreclosure Mitigation Counseling Program Funding Announcement for Round 9 Funds

National Foreclosure Mitigation Counseling Program Funding Announcement for Round 9 Funds Revised January 22, 2015 National Foreclosure Mitigation Counseling Program Round 9 Funding Announcement October

National Foreclosure Mitigation Counseling Program Funding Announcement for Round 9 Funds Revised January 22, 2015 National Foreclosure Mitigation Counseling Program Round 9 Funding Announcement October

If you need assistance, contact us immediately at: Dear PNC Mortgage Customer: Take the First Step

We are here to help Dear : We know how challenging it can be when you re experiencing difficulty in keeping your mortgage payments current. Whether your situation is temporary or long-term, PNC Mortgage

We are here to help Dear : We know how challenging it can be when you re experiencing difficulty in keeping your mortgage payments current. Whether your situation is temporary or long-term, PNC Mortgage

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

THE FHA WATERFALL WORKSHEET

THE FHA WATERFALL WORKSHEET Joseph Rebella MFY Legal Services, Inc. Funded through the New York State Attorney General Homeownership Protection Program MFY LEGAL SERVICES, INC., 299 Broadway, New York,

THE FHA WATERFALL WORKSHEET Joseph Rebella MFY Legal Services, Inc. Funded through the New York State Attorney General Homeownership Protection Program MFY LEGAL SERVICES, INC., 299 Broadway, New York,

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q4-2016 Q1-2017 Q2-2017 Q3-2017 Q4-2017 Oct-17 Nov-17 Dec-17 Total Completed Modifications 85,357 89,213 78,302 54,318 56,355 19,400 18,819

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q4-2016 Q1-2017 Q2-2017 Q3-2017 Q4-2017 Oct-17 Nov-17 Dec-17 Total Completed Modifications 85,357 89,213 78,302 54,318 56,355 19,400 18,819

Conventional 97% LTV Options updated 12/5/2018 Freddie Mac HomeOne Mortgage 97% LTV

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Mortgage Assistance Application

Loan number: Mortgage Assistance Application If you are having mortgage payment challenges, please complete and submit this application, along with the required documentation, to ServiSolutions via mail:

Loan number: Mortgage Assistance Application If you are having mortgage payment challenges, please complete and submit this application, along with the required documentation, to ServiSolutions via mail:

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING FEDERAL HOUSING COMMISSIONER Date: August 24, 2016 To: All FHA Approved Mortgagees All Direct

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING FEDERAL HOUSING COMMISSIONER Date: August 24, 2016 To: All FHA Approved Mortgagees All Direct

Supplemental Directive May 11, Home Affordable Unemployment Program. Help for Unemployed Borrowers. Background

Supplemental Directive 10-04 May 11, 2010 Home Affordable Unemployment Program Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility, underwriting and

Supplemental Directive 10-04 May 11, 2010 Home Affordable Unemployment Program Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility, underwriting and

Retrieving and Interpreting the NPV Test Results

Retrieving and Interpreting the NPV Test Results When determining whether a borrower is eligible for a modification under the Home Affordable Modification Program SM (HAMP ), the loan must be evaluated

Retrieving and Interpreting the NPV Test Results When determining whether a borrower is eligible for a modification under the Home Affordable Modification Program SM (HAMP ), the loan must be evaluated

Foreclosure Process in Minnesota

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

IMMINENT DEFAULT EVALUATION AND PROCESS FOR MORTGAGE MODIFICATIONS

TO: Freddie Mac Servicers October 11, 2017 2017-22 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Imminent default evaluation and process for mortgage modifications New imminent default evaluation

TO: Freddie Mac Servicers October 11, 2017 2017-22 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Imminent default evaluation and process for mortgage modifications New imminent default evaluation

Servicemember Financial Protection

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Ability-to-Repay and Qualified Mortgage Rule (ATR/QM Rule)- Effective 1/10/14

- Effective 1/10/14") Ability-to-Repay and Qualified Mortgage Rule (ATR/QM Rule)- Effective 1/10/14 1) Dodd Frank requires that lenders make a reasonable, good-faith determination that the loan applicant has a reasonable ability

Ability-to-Repay and Qualified Mortgage Rule (ATR/QM Rule)- Effective 1/10/14 1) Dodd Frank requires that lenders make a reasonable, good-faith determination that the loan applicant has a reasonable ability

Supplemental Directive August 9, Home Affordable Foreclosure Alternatives Program Policy Update

Supplemental Directive 11-08 August 9, 2011 Home Affordable Foreclosure Alternatives Program Policy Update In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 11-08 August 9, 2011 Home Affordable Foreclosure Alternatives Program Policy Update In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Property Information. Address:

Member Number: Account Number: If you are having mortgage payment challenges, please complete and submit this application, along with the required documentation, to General Electric Credit Union via mail:

Member Number: Account Number: If you are having mortgage payment challenges, please complete and submit this application, along with the required documentation, to General Electric Credit Union via mail:

Servicing and Loss Mitigation. Jennifer Schultz, Esq. Community Legal Services, Inc W. Erie Ave. Philadelphia, PA

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Quick Guide - Preparing to Refinance WORK FOR YOU

Quick Guide - Preparing to Refinance COOPERATIVE FINANCING MODELS THAT MAY WORK FOR YOU Cooperative Financing Mortgage programs for Cooperatives Reasons to seek new financing What Lender s look at How

Quick Guide - Preparing to Refinance COOPERATIVE FINANCING MODELS THAT MAY WORK FOR YOU Cooperative Financing Mortgage programs for Cooperatives Reasons to seek new financing What Lender s look at How

National Foreclosure Mitigation Counseling Program FINAL Funding Announcement for Round 5 Funds. December 1, 2010

National Foreclosure Mitigation Counseling Program FINAL Funding Announcement for Round 5 Funds December 1, 2010 P a g e National Foreclosure Mitigation Counseling Program Funding Announcement National

National Foreclosure Mitigation Counseling Program FINAL Funding Announcement for Round 5 Funds December 1, 2010 P a g e National Foreclosure Mitigation Counseling Program Funding Announcement National

1. It s All About Income

1. It s All About Income Loan modification programs are based on one thing, income. The biggest misconception out there is that the bank cares about the type of hardship you have. This myth couldn t be

1. It s All About Income Loan modification programs are based on one thing, income. The biggest misconception out there is that the bank cares about the type of hardship you have. This myth couldn t be

Loan Workout Hierarchy for Fannie Mae Conventional Loans

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL TELEPHONE (352) FAX (352)

FAX (352)") NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL 32601 TELEPHONE (352)380-9119 FAX (352)380-9170 WWW.GNHDC.ORG Dear Homeowner, We re so glad you took that tough first step

NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL 32601 TELEPHONE (352)380-9119 FAX (352)380-9170 WWW.GNHDC.ORG Dear Homeowner, We re so glad you took that tough first step

[Space Above This Line For Recording Data] CONSOLIDATION, EXTENSION, AND MODIFICATION AGREEMENT

![[Space Above This Line For Recording Data] CONSOLIDATION, EXTENSION, AND MODIFICATION AGREEMENT](/thumbs/75/72356163.jpg "[Space Above This Line For Recording Data] CONSOLIDATION, EXTENSION, AND MODIFICATION AGREEMENT") [Space Above This Line For Recording Data] CONSOLIDATION, EXTENSION, AND MODIFICATION AGREEMENT WORDS USED OFTEN IN THIS DOCUMENT (A) Agreement. This document, which is dated,, and exhibits and riders

[Space Above This Line For Recording Data] CONSOLIDATION, EXTENSION, AND MODIFICATION AGREEMENT WORDS USED OFTEN IN THIS DOCUMENT (A) Agreement. This document, which is dated,, and exhibits and riders

STANDARD MODIFICATION

Bulletin NUMBER: 2011-16 TO: Freddie Mac Servicers September 12, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are announcing complete requirements related to the Freddie

Bulletin NUMBER: 2011-16 TO: Freddie Mac Servicers September 12, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are announcing complete requirements related to the Freddie

Supplemental Directive June 3, Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative

Supplemental Directive 10-05 June 3, 2010 Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive 10-05 June 3, 2010 Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative Background In Supplemental Directive 09-01, the Treasury Department

Legal Basics: Foreclosure Prevention. March 21, 2017 Odette Williamson National Consumer Law Center

Legal Basics: Foreclosure Prevention March 21, 2017 Odette Williamson National Consumer Law Center National Consumer Law Center 2013 National Consumer Law Center Advocate on behalf of low-income consumers

Legal Basics: Foreclosure Prevention March 21, 2017 Odette Williamson National Consumer Law Center National Consumer Law Center 2013 National Consumer Law Center Advocate on behalf of low-income consumers

Niche Loan Programs. Featured Loan. Zero Down Loan

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Making Home Affordable Program Performance Report Third Quarter 2015

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Affordability: Modifications should provide affordable payments and terms. Sustainability: Modifications should produce long term performance.

November 3, 2016 Ms. Maria Fernandez Mr. Prasant Sar Ms. Mary Baehr Mr. Luis Saucedo Federal Housing Finance Agency Constitution Center 400 7 th Street, S.W. Washington, DC 20219 Dear Ms. Fernandez, Mr.

November 3, 2016 Ms. Maria Fernandez Mr. Prasant Sar Ms. Mary Baehr Mr. Luis Saucedo Federal Housing Finance Agency Constitution Center 400 7 th Street, S.W. Washington, DC 20219 Dear Ms. Fernandez, Mr.

Making Home Affordable Program Dodd-Frank Certification, Internal Quality Assurance and Verification of Income Update

Supplemental Directive 11-01 February 17, 2011 Making Home Affordable Program Dodd-Frank Certification, Internal Quality Assurance and Verification of Income Update In February 2009, the Obama Administration

Supplemental Directive 11-01 February 17, 2011 Making Home Affordable Program Dodd-Frank Certification, Internal Quality Assurance and Verification of Income Update In February 2009, the Obama Administration

[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale

![[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale](/thumbs/90/103076486.jpg "[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale") [Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

[Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

Fannie Mae Mortgage Help Center Jacksonville Homeowner Packet

7077 Bonneval Road, Suite 450 Jacksonville, FL 32216 (866) 442-8578 phone (866) 442-6293 fax Fannie Mae Mortgage Help Center Jacksonville Homeowner Packet 7077 Bonneval Road, Suite 450 Jacksonville, FL

7077 Bonneval Road, Suite 450 Jacksonville, FL 32216 (866) 442-8578 phone (866) 442-6293 fax Fannie Mae Mortgage Help Center Jacksonville Homeowner Packet 7077 Bonneval Road, Suite 450 Jacksonville, FL

Loan Number: Co-Borrower s Name. Social Security Number. with area code. Cell or work number with area code. Address

Section A BORROWER CO-BORROWER Borrower s Name Co-Borrower s Name Social Security Number of Birth Social Security Number of Birth Home phone number with area code Home phone number with area code Cell

Section A BORROWER CO-BORROWER Borrower s Name Co-Borrower s Name Social Security Number of Birth Social Security Number of Birth Home phone number with area code Home phone number with area code Cell

Please complete the attached application and submit to KeyBank using any of the following delivery methods below:

KEYBANK REQUEST FOR ASSISTANCE FORM COVER LETTER Please complete the attached application and submit to KeyBank using any of the following delivery methods below: FAX: 216-370-5819 EMAIL: Loss_Mitigation@keybank.com

KEYBANK REQUEST FOR ASSISTANCE FORM COVER LETTER Please complete the attached application and submit to KeyBank using any of the following delivery methods below: FAX: 216-370-5819 EMAIL: Loss_Mitigation@keybank.com

All of the changes announced in this Bulletin are effective immediately unless otherwise noted.

TO: Freddie Mac Servicers June 13, 2018 2018-9 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Forbearance plan requirements Consolidation and restructuring of our requirements for short-term,

TO: Freddie Mac Servicers June 13, 2018 2018-9 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Forbearance plan requirements Consolidation and restructuring of our requirements for short-term,

Workout Hierarchy for Fannie Mae Conventional Loans NOTE: Refer to the Fannie Mae Servicing Guide

Workout Hierarchy for Fannie Mae Conventional Loans The following table is a summary of Fannie Mae workout options available to assist borrowers experiencing financial hardship. The servicer must first

Workout Hierarchy for Fannie Mae Conventional Loans The following table is a summary of Fannie Mae workout options available to assist borrowers experiencing financial hardship. The servicer must first

Assistance Program: City of Tuscaloosa Home Purchase Assistance Program Code: DALTUSHPP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Home Affordable Modification Program Policies and Procedures Manual

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

FREDDIE MAC REPORTS FIRST QUARTER 2010 FINANCIAL RESULTS

FOR IMMEDIATE RELEASE MEDIA CONTACT: Michael Cosgrove 703-903-2123 INVESTOR CONTACT: Linda Eddy 703-903-3883 FREDDIE MAC REPORTS FIRST QUARTER 2010 FINANCIAL RESULTS Company Continues to Provide Critical

FOR IMMEDIATE RELEASE MEDIA CONTACT: Michael Cosgrove 703-903-2123 INVESTOR CONTACT: Linda Eddy 703-903-3883 FREDDIE MAC REPORTS FIRST QUARTER 2010 FINANCIAL RESULTS Company Continues to Provide Critical

Bulletin. TO: All Freddie Mac Servicers December 12, 2008

Bulletin TO: All Freddie Mac Servicers December 12, 2008 SUBJECTS Servicing requirements are provided in this Single-Family Seller/Servicer Guide (Guide) Bulletin. With this Bulletin we are: Providing

Bulletin TO: All Freddie Mac Servicers December 12, 2008 SUBJECTS Servicing requirements are provided in this Single-Family Seller/Servicer Guide (Guide) Bulletin. With this Bulletin we are: Providing

HomeReady vs. Home Possible Comparison

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Supplemental Directive January 28, Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications

Supplemental Directive 10-01 January 28, 2010 Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive 10-01 January 28, 2010 Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications Background In Supplemental Directive 09-01, the Treasury Department

Request for Mortgage Assistance (RMA) Loan Number:

Loan Number:") Request for Mortgage Assistance (RMA) Loan Number: If you are experiencing a financial hardship and need help, you must complete and submit this form along with other required documentation to be considered

Request for Mortgage Assistance (RMA) Loan Number: If you are experiencing a financial hardship and need help, you must complete and submit this form along with other required documentation to be considered

HOPE NOW Alliance. Statement for the Record. Committee on Oversight and Government Reform. U.S. House of Representatives. Hearing

HOPE NOW Alliance Statement for the Record Committee on Oversight and Government Reform U.S. House of Representatives Hearing Foreclosure Prevention Part II: Are Loan Servicers Honoring Their Commitments

HOPE NOW Alliance Statement for the Record Committee on Oversight and Government Reform U.S. House of Representatives Hearing Foreclosure Prevention Part II: Are Loan Servicers Honoring Their Commitments

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

UNIFORM BORROWER ASSISTANCE FORM

If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department