2017 Beginning Farmer Loan and Tax Credit Programs

|

|

|

- Wendy Maxwell

- 6 years ago

- Views:

Transcription

1 2017 Beginning Farmer Loan and Tax Credit Programs

2 Iowa Agricultural Development Division Staff Steve Ferguson Tax Credit Program Specialist wa.gov Tammy Nebola Loan Program Specialist a.gov

3 Iowa Agricultural Development Division Formerly Iowa Agricultural Development Authority Became a Division of the Iowa Finance Authority in July, 2013 Administers loan and tax credit programs to benefit Beginning Farmers in Iowa.

Loan Participation Program (LPP) Beginning Farmer Tax")

DNR Lease to Beginning Farmer Program* * Administered")

4 Iowa Agricultural Development Division Programs Beginning Farmer Loan Program (BFLP) Loan Participation Program (LPP) Beginning Farmer Tax Credit Program (BFTC) Beginning Farmer Custom Farming Tax Credit Program (BFCF) DNR Lease to Beginning Farmer Program* * Administered by DNR

5 Who is a Beginning Farmer? Same for ALL Programs 2017 maximum net worth less than $645,284 This amount changes every year At least 18 years old (No upper age limit) Resident of Iowa Must be owner/operator of the farm Cannot lease to someone else or hire someone else to do the work Must have sufficient education, training and experience for the anticipated farm operation But not the same as FSA requirement of >3 years and <10 years Must have access to adequate working capital, farm machinery, livestock and/or agricultural land

6 Approval Procedures All applications are due the by 1 st of month Reviewed by IADD board Usually the 4 th Wednesday of the month Recommendation made to the IFA board Usually meets 1 st Wednesday of the following month After Board meeting Approval letter sent or Letter detailing additional requirements needed before application can be approved

7 Application Packets For all IADD Programs Program Application Financial Statement less than 30 days old Signed by Beginning Farmer and spouse Witnessed by financial professional that helped prepare statement Background letter explaining Education, training and experience for the anticipated farm operation Access to working capital, farm machinery, livestock and/or agricultural land Explain agreement for machinery use (rental or trading labor for use) Application Fee Other documentation specific to each program

8 Beginning Farmer Loan Program

9 Beginning Farmer Loan Program Low-interest loan through a lender or contract seller Financed through a tax-exempt bond issued by IFA Interest earned is exempt from federal income taxes For contract sellers, interest is both federal and state tax-exempt income Because the interest earned is tax-exempt, lenders and contract sellers can charge the beginning farmer a lower interest rate Typically the beginning farmer will see about a 25% interest rate reduction using the Beginning Farmer Loan Program (BFLP)

10 Beginning Farmer Loan Uses Purchase Agricultural land Depreciable machinery or equipment Breeding livestock-not feeders Make improvements Existing buildings New farm improvements Cannot finance Operating expenses Refinance previous purchases

11 Financing or Constructing a Facility If financing a feeding facility, per federal regulations the feeding contract must be on a per head/per day basis This restriction can cause complications, but most integrators are willing to change the contract when they know it is a requirement of the financing The per head/per day contract format must be maintained for the life of the loan The program cannot be used for any type of rental, so the federal restriction on the feeding contract is to distinguish between Rental agreement (per pig space) Not eligible Service agreement (per head/per day) Eligible

12 Maximum Bond Amounts Maximum bond amount - adjusts annually on January 1 st $524,200 for real estate $250,000 for existing buildings or farm improvements and new depreciable agricultural property $ 62,500 for used depreciable agricultural property Federal legislation has been introduced to increase all maximums to the maximum bond amount H.R Restrictions Dwelling may not exceed 5% of bond proceeds CRP ground may not exceed 25% of bond proceeds Combination of the above can be used up to maximum bond

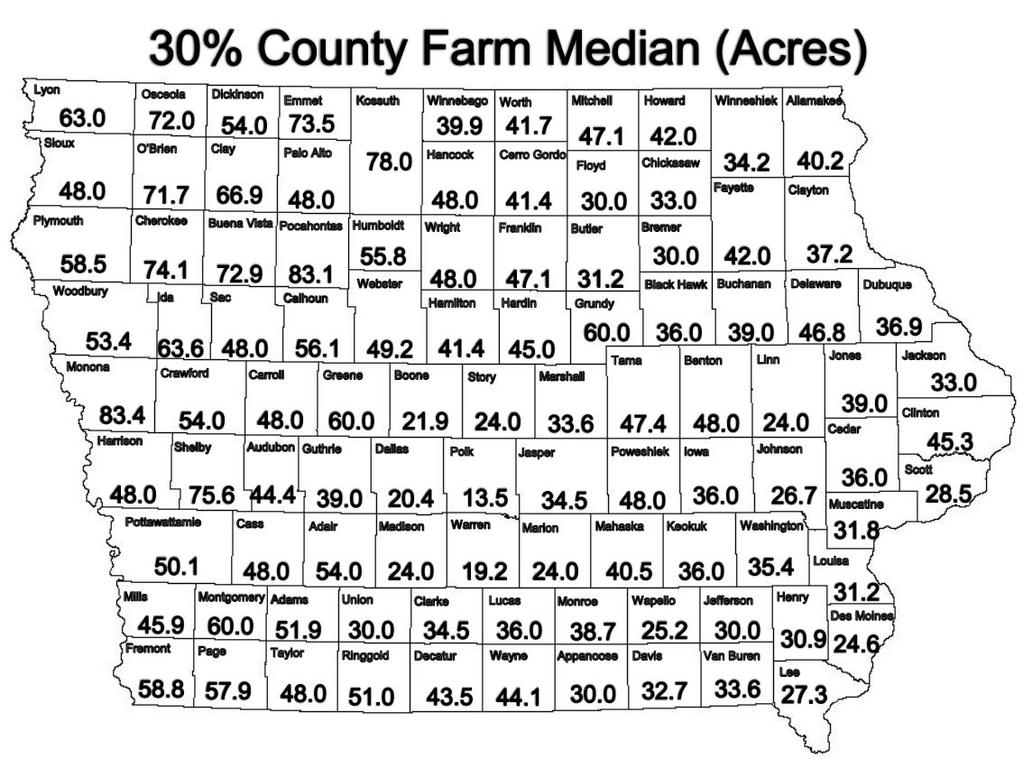

13 Additional Eligibility requirement Other BFLP Factors If beginning farmer does now or has in the past owned land it must be less than 30% of the county median The federal legislation introduced would also change the maximum land ownership from 30% of the county median to 30% of the county average. Purchases from closely related family members (parents, grandparents or siblings) are permitted but: they must be financed through a 3 rd party lender (no contract sale) Must be sold for at least the appraised value Contract sale allowed if not immediate family So can be with aunts, uncles, cousins, etc.

14

loan (5/45/50 program) IADD Loan Participation Program (LPP) loan Only when financed through a")

15 Other BFLP Factors May reapply and benefit from the program until the maximum bond amount has been used or land owned exceeds the limit Beginning farmer negotiates down payment and loan terms with bank or contract seller If eligible, down payment assistance may be used with: Farm Service Agency (FSA) loan (5/45/50 program) IADD Loan Participation Program (LPP) loan Only when financed through a bank

16 Using the BFLP and FSA 5/45/50 Together % of Project Funding Source Total Interest Rate 5% of project Down payment $ 43,158 1 st year Interest 45% of project FSA Loan $300, % $4,500 50% of project BFLP Aggie Bond $520, % $20,800 $863,158 $25,300 % of Project Funding Source Total Interest Rate 1 st year Interest 100% of project Traditional Loan $863, % $46,006 $20,706 Interest Savings in the 1 st year

17 Example of Savings Using the Beginning Farmer Loan Program 5.33% Interest Loan Amortization Schedule 4.00% Interest Loan Amortization Schedule 5.33% Interest 4.00% Interest TotalSavings using BFLP Loan Amount $520,000 $520,000 Total Interest $533,293 $382,150 $151,143 Annual P&I Payments $35,110 $30,072 $5,038 Total P&I Payments $1,053,293 $902,150 $151,143

18 Other Provisions and Fees Applications can be approved if bank loan or contract transaction completed: BUT must be approved by IADD-IFA board within 60 days of any financing Non-refundable $50 application fee Closing fee 1.50% of Bond up to $250, % of Bond amount over $250,000 $300 minimum Closing fee is paid when loan closes

19 How to get started! Talk to your lender and let them know you would like to use the IADD Beginning Farmer Loan Program (BFLP) Lender will underwrite your loan to determine if they are willing to finance the project Once bank approval has been decided: Loan term and tax exempt interest rate will be negotiated Lender and beginning farmer jointly fill out application Applications, program summaries and additional information is available our website at: IowaFinanceAuthority.gov/IADD

20 How to get started! Submit application and all attachments to IADD by the 1 st of the month Application is reviewed/approved by IADD-IFA Boards process typically takes about six weeks interim financing allowed After approval, IADD sends loan closing packet to lender Loan is assigned to lender or contract seller at closing All payments are made directly to the lender or contract seller

21 Questions on the Beginning Farmer Loan Program?

22 Loan Participation Program

23 Loan Participation Program The Loan Participation Program (LPP): Established in 1996 Supplements a beginning farmer s down payment to purchase agricultural assets The program can be used for the same purposes as the Beginning Farmer Loan Program (BFLP) Can be used in conjunction with the Beginning Farmer Loan Program (BFLP)

24 Maximum and Loan Terms IADD s LPP reduces the lender s risk: LPP is Last-in/last-out Allows lender to finance more of the beginning farmer s project Maximum loan participation is 30% of project up to $150,000 Current interest rate is 2.50% Fixed for 5 years then adjusted 1.00% above FSA Direct Farm Ownership Down Payment Loan Program 10 year balloon (amortized over 20 years for land and 12 years for facilities) There are no restrictions on related party transactions

25 LPP Underwriting criteria Current assets to current liabilities > 1.1 at time of application Farm debt-to-asset ratio < 80% at closing Aggregate amount of participated loan (total amount financed) < 3 times the borrower s net worth Debt repayment ratio > 120% Off-farm income < 50% of projected gross income Loan-to-value < 100% of appraised value Collateral appraisals by qualified 3 rd party appraiser Property not eligible if house value > 50% of appraisal

26 Other Provisions and Fees Applications can be approved if bank loan has been completed: BUT must be approved by IADD-IFA board within 60 days of any financing Non-refundable application fee $100 Closing fee 1.25% of IADD participation loan $300 minimum Closing fee is paid when loan closes

27 Using the LPP and BFLP Together for Hog Facility Construction % of Project Funding Source Total Interest Rate 1 st year Interest 30% of project LPP Loan $150, % $3,750 F.I. Limit BFLP Aggie Bond $250, % $10,000 Remaining Traditional Loan $300, % $15, year amort. $700,000 $29,740 % of Project Funding Source Total Interest Rate 1 st year Interest 100% of project Traditional Loan $700, % $37,310 $7,570 Interest Savings in the 1 st year

28 Example of Savings Using the Loan Participation Program 5.33% Interest Loan Amortization Schedule Loan Amount $150,000 Number of Payments 12 Annual Interest Rate 5.33% Total Payments $206, Term of Loan in Years 12 Total Interest $56, Annual Payment $17, Balloon Payment None 2.50% Interest Loan Amortization Schedule Loan Amount $150,000 Number of Payments 10 Annual Interest Rate 2.50% Total Payments $174, Term of Loan in Years 12 Total Interest $24, Annual Payment $14, Balloon Payment $42, % Interest 2.50% Interest TotalSavings using LPP Loan Amount $150,000 $150,000 Total Interest $56,883 $24,416 $32,467 Annual P&I Payments $17,240 $14,623 $2,617 Total P&I Payments $206,883 $174,416 $32,467

29 How to get started! Talk to your lender and let them know you would like to use the IADD Loan Participation Program (LPP) Lender will underwrite your loan to determine if they are willing to participate in financing the project Once bank approval has been determined, fill out the application with your lender Applications, programs summaries and additional information is available at: IowaFinanceAuthority.gov/IADD Submit application and attachments to IADD by the 1 st of the month Pro-forma financial statement Cash flow analysis 3 Years of Federal Tax Returns

30 How to get started! IADD will review and underwrite the application Application is reviewed by IADD Board Credit Committee Application is approved by IADD-IFA Board process which typically takes 5-6 weeks interim financing is allowed IADD works with bank on closing documents At closing, funds are sent to bank via ACH All loan payments are made directly to the bank Bank sends IADD its payment amount

31 Questions on the Loan Participation Program?

Financial Resources Available to Beginning Farmers. Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension

Financial Resources Available to Beginning Farmers Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension Financial Resources There are several sources of financial resources

Financial Resources Available to Beginning Farmers Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension Financial Resources There are several sources of financial resources

BEGINNING FARMER BOND

PROGRAM SUMMARY Contact: For additional information, contact: Lorrie Karcher (618) 244-2424 ext. 1500 lkarcher@il-fa.com LOAN NUMBER An application form may be downloaded from the IFA web site: www.il-fa.com

PROGRAM SUMMARY Contact: For additional information, contact: Lorrie Karcher (618) 244-2424 ext. 1500 lkarcher@il-fa.com LOAN NUMBER An application form may be downloaded from the IFA web site: www.il-fa.com

NET WORTH STATEMENT - FARMERS AND RANCHERS Name: Date of Statement: Valuation Method: Market Cost

NET WORTH STATEMENT - FARMERS AND RANCHERS Name: Address: Phone: Date of Statement: Valuation Method: Cost Note: This net worth statement should be filled in as a single entity. If you are able to separate

NET WORTH STATEMENT - FARMERS AND RANCHERS Name: Address: Phone: Date of Statement: Valuation Method: Cost Note: This net worth statement should be filled in as a single entity. If you are able to separate

HOW CAN WE HELP YOU TODAY?

Nebraska USDA Farm Service Agency HOW CAN WE HELP YOU TODAY? USDA FARM LOAN PROGRAMS AND PROCESS DENISE M. LICKTEIG, FARM LOAN MANAGER NEMAHA COUNTY FARM SERVICE AGENCY WHO IS THE NEBRASKA FSA? 1 WE HAVE

Nebraska USDA Farm Service Agency HOW CAN WE HELP YOU TODAY? USDA FARM LOAN PROGRAMS AND PROCESS DENISE M. LICKTEIG, FARM LOAN MANAGER NEMAHA COUNTY FARM SERVICE AGENCY WHO IS THE NEBRASKA FSA? 1 WE HAVE

Mark Rickels Relationship Manager, Johnston, Ia.,

Michael Juergens Chief Underwriter, Johnston, Ia., 866-452-2617 Michael_Juergens@farmermac.com Mark Rickels Relationship Manager, Johnston, Ia., 202-872-6611 Mark_Rickels@farmermac.com 2 1 10 important

Michael Juergens Chief Underwriter, Johnston, Ia., 866-452-2617 Michael_Juergens@farmermac.com Mark Rickels Relationship Manager, Johnston, Ia., 202-872-6611 Mark_Rickels@farmermac.com 2 1 10 important

PROGRAM SUMMARY. For additional information, contact:

PROGRAM SUMMARY Contact: For additional information, contact: Patrick Evans (618) 244-2424 ext. 1501 pevans@il-fa.com Lorrie Karcher (618) 244-2424 ext. 1500 lkarcher@il-fa.com An application form may

PROGRAM SUMMARY Contact: For additional information, contact: Patrick Evans (618) 244-2424 ext. 1501 pevans@il-fa.com Lorrie Karcher (618) 244-2424 ext. 1500 lkarcher@il-fa.com An application form may

Agribusiness Lending Internal Control Questionnaire

Agribusiness Lending Internal Control Questionnaire Completed by: Date Completed: 1. Has the institution established policies that are appropriate for the complexity and scope of the agricultural lending

Agribusiness Lending Internal Control Questionnaire Completed by: Date Completed: 1. Has the institution established policies that are appropriate for the complexity and scope of the agricultural lending

Application Form The application form needs to be complete, signed and dated.

Dairy Farmers of Ontario New Entrant Quota Assistance Program (NEQAP) Application Deadline: October 31, 2018 Introduction The P5 (Ontario, Quebec, Prince Edward Island, New Brunswick and Nova Scotia) New

Dairy Farmers of Ontario New Entrant Quota Assistance Program (NEQAP) Application Deadline: October 31, 2018 Introduction The P5 (Ontario, Quebec, Prince Edward Island, New Brunswick and Nova Scotia) New

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP)

Mortgage Assistance Program (MAP)") Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

Housing Trust Silicon Valley ( HTSV ) Closing Cost Assistance (CCAP) Program

Closing Cost Assistance (CCAP) Program") Housing Trust Silicon Valley ( HTSV ) Closing Cost Assistance (CCAP) Program Program Description: The Housing Trust Silicon Valley s Closing Cost Assistance Program may be used for down payment and/or

Housing Trust Silicon Valley ( HTSV ) Closing Cost Assistance (CCAP) Program Program Description: The Housing Trust Silicon Valley s Closing Cost Assistance Program may be used for down payment and/or

By providing access to credit, FSA s Farm Loan Programs offer opportunities to:

By providing access to credit, FSA s Farm Loan Programs offer opportunities to: Start, improve, expand, transition, market, and strengthen family farming and ranching operations. Provide viable farming

By providing access to credit, FSA s Farm Loan Programs offer opportunities to: Start, improve, expand, transition, market, and strengthen family farming and ranching operations. Provide viable farming

NORTH DAKOTA VARIABLE RATE HELOC DISCLOSURE

NORTH DAKOTA VARIABLE RATE HELOC DISCLOSURE ND HELOC Disclosure 1/1/2018 Page 1 IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT Lender: Bank Forward This disclosure contains important information about

NORTH DAKOTA VARIABLE RATE HELOC DISCLOSURE ND HELOC Disclosure 1/1/2018 Page 1 IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT Lender: Bank Forward This disclosure contains important information about

PA Ag Lending Programs

Growing Business, Growing Smart Its People PA Ag Lending Programs Gary Smith President and CEO Chester County Economic Development Council Places Investing in the Economic Health of Chester County & Prosperity

Growing Business, Growing Smart Its People PA Ag Lending Programs Gary Smith President and CEO Chester County Economic Development Council Places Investing in the Economic Health of Chester County & Prosperity

lenders may contact their local County Office or State Office to telephone at

UNITED STATES DEPARTMENT OF AGRICULTURE Farm Service Agency Washington, DC 20250 For: State and County Offices 2-FLP Notice FLP-745 Guaranteed Loan Narrative Q&A s Approved by: Deputy Administrator, Farm

UNITED STATES DEPARTMENT OF AGRICULTURE Farm Service Agency Washington, DC 20250 For: State and County Offices 2-FLP Notice FLP-745 Guaranteed Loan Narrative Q&A s Approved by: Deputy Administrator, Farm

NORTH CAROLINA AGRICULTURAL FINANCE AUTHORITY

NORTH CAROLINA AGRICULTURAL FINANCE AUTHORITY Mission Statement The North Carolina Agricultural Finance Authority (NCAFA) was established by the North Carolina General Assembly to provide credit to agriculture

NORTH CAROLINA AGRICULTURAL FINANCE AUTHORITY Mission Statement The North Carolina Agricultural Finance Authority (NCAFA) was established by the North Carolina General Assembly to provide credit to agriculture

TRADING AS A FARMING COMPANY

TRADING AS A FARMING COMPANY Kevin Connolly Financial Management Specialist Teagasc Rural Economy and Development Programme (REDP) Teagasc Pig Farmers Conference 2014 Cavan Crystal Hotel 22 nd October

TRADING AS A FARMING COMPANY Kevin Connolly Financial Management Specialist Teagasc Rural Economy and Development Programme (REDP) Teagasc Pig Farmers Conference 2014 Cavan Crystal Hotel 22 nd October

Farming Through A Company

Farming Through A Company Kevin Connolly Financial Management Specialist kevin.connolly@teagasc.ie [Updated January 2018] A company is.. A separate legal entity The company becomes the famer Business profits

Farming Through A Company Kevin Connolly Financial Management Specialist kevin.connolly@teagasc.ie [Updated January 2018] A company is.. A separate legal entity The company becomes the famer Business profits

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656 Farm Business Planning Building a Farm Business Plan Lenders Perspective Financing Options How to Build

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656 Farm Business Planning Building a Farm Business Plan Lenders Perspective Financing Options How to Build

HomeTown: Portsmouth s First Time Homebuyer Program Information Packet

Revised 5/18/08 HomeTown: Portsmouth s First Time Homebuyer Program Information Packet The HomeTown Program is a partnership of the City of Portsmouth, New Hampshire Housing Finance Authority and Citizens

Revised 5/18/08 HomeTown: Portsmouth s First Time Homebuyer Program Information Packet The HomeTown Program is a partnership of the City of Portsmouth, New Hampshire Housing Finance Authority and Citizens

Profitability is the primary goal of all business

Understanding Profitability File C3-24 December 2009 www.extension.iastate.edu/agdm Profitability is the primary goal of all business ventures. Without profitability the business will not survive in the

Understanding Profitability File C3-24 December 2009 www.extension.iastate.edu/agdm Profitability is the primary goal of all business ventures. Without profitability the business will not survive in the

Welcome again to our Farm Management and Finance educational series. Borrowing money is something that is a necessary aspect of running a farm or

Welcome again to our Farm Management and Finance educational series. Borrowing money is something that is a necessary aspect of running a farm or ranch business for most of us, at least at some point in

Welcome again to our Farm Management and Finance educational series. Borrowing money is something that is a necessary aspect of running a farm or ranch business for most of us, at least at some point in

FINANCING YOUR BUYER FOR THE IMPORT OF U.S. CAPITAL GOODS.

FINANCING YOUR BUYER FOR THE IMPORT OF U.S. CAPITAL GOODS. FINANCING YOUR BUYER FOR THE IMPORT OF U.S. CAPITAL GOODS. International sales of high-value capital goods usually require medium- or long-term

FINANCING YOUR BUYER FOR THE IMPORT OF U.S. CAPITAL GOODS. FINANCING YOUR BUYER FOR THE IMPORT OF U.S. CAPITAL GOODS. International sales of high-value capital goods usually require medium- or long-term

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Monday, June 19, 2017 Ag Law Rooms: Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m.

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

Module 4 Preparing Agricultural Financial Statements: The Balance Sheet. Module Outline

Module 4 Preparing Agricultural Financial Statements: The Balance Sheet Introduction Roadside Chat #1 Balance Sheet Considerations Timing Balance Sheet Assets Liabilities Owner Equity Road Test #1 Assets

Module 4 Preparing Agricultural Financial Statements: The Balance Sheet Introduction Roadside Chat #1 Balance Sheet Considerations Timing Balance Sheet Assets Liabilities Owner Equity Road Test #1 Assets

Home Equity Disclosure Booklet

Home Equity Disclosure Booklet People s United Bank peoples.com Effective June 2017 L0014 6/17 00 1 Home Equity Disclosure TITLE PRODUCT* PAGE SECTION I. When Your Home is on the Line HELOC 2 SECTION II.

Home Equity Disclosure Booklet People s United Bank peoples.com Effective June 2017 L0014 6/17 00 1 Home Equity Disclosure TITLE PRODUCT* PAGE SECTION I. When Your Home is on the Line HELOC 2 SECTION II.

THE CANANDAIGUA NATIONAL BANK AND TRUST COMPANY (CNB) PREAPPLICATION DISCLOSURE. IMPORTANT TERMS of our FLEXEQUITY MASTER LINE OF CREDIT (MORTGAGE)

PREAPPLICATION DISCLOSURE. IMPORTANT TERMS of our FLEXEQUITY MASTER LINE OF CREDIT (MORTGAGE)") THE CANANDAIGUA NATIONAL BANK AND TRUST COMPANY (CNB) PREAPPLICATION DISCLOSURE IMPORTANT TERMS of our FLEXEQUITY MASTER LINE OF CREDIT (MORTGAGE) For applications received on or after January 1, 2011

THE CANANDAIGUA NATIONAL BANK AND TRUST COMPANY (CNB) PREAPPLICATION DISCLOSURE IMPORTANT TERMS of our FLEXEQUITY MASTER LINE OF CREDIT (MORTGAGE) For applications received on or after January 1, 2011

Promoting Innovation in Maryland Agricultural and Resource-Based Business. * Now includes financing for tree fruit orchards and hopyards *

Promoting Innovation in Maryland Agricultural and Resource-Based Business Application for the Maryland Vineyard Planting Loan Fund * Now includes financing for tree fruit orchards and hopyards * Program

Promoting Innovation in Maryland Agricultural and Resource-Based Business Application for the Maryland Vineyard Planting Loan Fund * Now includes financing for tree fruit orchards and hopyards * Program

HomeTown: Portsmouth s First Time Homebuyer Program Information & Guidelines

HomeTown: Portsmouth s First Time Homebuyer Program Information & Guidelines The HomeTown Program is a partnership of the City of Portsmouth and Citizens Bank, N.A. Overview The HomeTown Program provides

HomeTown: Portsmouth s First Time Homebuyer Program Information & Guidelines The HomeTown Program is a partnership of the City of Portsmouth and Citizens Bank, N.A. Overview The HomeTown Program provides

Additional Information

Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Summary Social Security Wage Base Entity Comparison

Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Summary Social Security Wage Base Entity Comparison

Financing Residential Real Estate. FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, graduated payment mortgages, FHA insurance premiums, sales concessions such

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, graduated payment mortgages, FHA insurance premiums, sales concessions such

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

FHA Underwriting Updates Before-and-After Matrix Effective for FHA Case Numbers Assigned on and after April 1, 2012

Self Employed Borrowers Generally, standard FHA guidelines apply with some exceptions on documentation requirements. If Approve/Eligible, the borrower must provide two (2) years of individual federal tax

Self Employed Borrowers Generally, standard FHA guidelines apply with some exceptions on documentation requirements. If Approve/Eligible, the borrower must provide two (2) years of individual federal tax

3:45 p.m. - 4:30 p.m.

2016 Commercial & Bankruptcy Law Seminar Pending Doom: Another Ag Crisis 3:45 p.m. - 4:30 p.m. Presented by Larry Eide Pappajohn Shriver, Eide & Nielsen, PC 103 E State St. Ste. 800 Mason City, IA 50402

2016 Commercial & Bankruptcy Law Seminar Pending Doom: Another Ag Crisis 3:45 p.m. - 4:30 p.m. Presented by Larry Eide Pappajohn Shriver, Eide & Nielsen, PC 103 E State St. Ste. 800 Mason City, IA 50402

CROP LOAN GUARANTEE PROGRAM

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS Hardest Hit Funding Round 2 opened Monday August 1 st, 2016 Please click on one of the following links below to go to the section you are most interested in. Introduction to

FREQUENTLY ASKED QUESTIONS Hardest Hit Funding Round 2 opened Monday August 1 st, 2016 Please click on one of the following links below to go to the section you are most interested in. Introduction to

There are multiple avenues of credit available to agricultural producers. Let s begin by identifying who can provide financing for your agricultural

1 There are multiple avenues of credit available to agricultural producers. Let s begin by identifying who can provide financing for your agricultural venture. Local commercial banks and credit unions

1 There are multiple avenues of credit available to agricultural producers. Let s begin by identifying who can provide financing for your agricultural venture. Local commercial banks and credit unions

Participant Handbook Risk Management Program. RMP for livestock Cattle Hogs Sheep Veal

Participant Handbook Risk Management Program RMP for livestock Cattle Hogs Sheep Veal Risk Management Program (RMP) for livestock includes the following four plans: RMP: Cattle RMP: Hogs RMP: Sheep RMP:

Participant Handbook Risk Management Program RMP for livestock Cattle Hogs Sheep Veal Risk Management Program (RMP) for livestock includes the following four plans: RMP: Cattle RMP: Hogs RMP: Sheep RMP:

HOME EQUITY EARLY DISCLOSURE

REAL ESTATE LENDING POWERED BY CUNA MUTUAL GROUP HOME EQUITY EARLY DISCLOSURE IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT PLAN This disclosure contains important information about our Home Equity

REAL ESTATE LENDING POWERED BY CUNA MUTUAL GROUP HOME EQUITY EARLY DISCLOSURE IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT PLAN This disclosure contains important information about our Home Equity

AGRICULTURAL RESTRUCTURING DEBT GUARANTEE APPLICATION $300 application fee For Loans Made by Lending Institutions (Please print or type)

") (IFA USE ONLY) Loan Number Application Fee Received AGRICULTURAL RESTRUCTURING DEBT GUARANTEE APPLICATION $300 application fee For Loans Made by Lending Institutions (Please print or type) Part I - REPRESENTATION

(IFA USE ONLY) Loan Number Application Fee Received AGRICULTURAL RESTRUCTURING DEBT GUARANTEE APPLICATION $300 application fee For Loans Made by Lending Institutions (Please print or type) Part I - REPRESENTATION

THE RICHLAND ELECTRIC COOPERATIVE REVOLVING LOAN FUND MANUAL

THE RICHLAND ELECTRIC COOPERATIVE REVOLVING LOAN FUND MANUAL The Rural Business Enterprise Grant (RBEG) Program, administered by the Wisconsin USDA Rural Development, provided the Richland Electric Cooperative

THE RICHLAND ELECTRIC COOPERATIVE REVOLVING LOAN FUND MANUAL The Rural Business Enterprise Grant (RBEG) Program, administered by the Wisconsin USDA Rural Development, provided the Richland Electric Cooperative

Forward the original and two copies of the completed application to:

PROCEDURES Application Form A request for a loan will not be considered until the attached application form is completed and all required exhibits are submitted. The application form should be completed

PROCEDURES Application Form A request for a loan will not be considered until the attached application form is completed and all required exhibits are submitted. The application form should be completed

Session 2: Business Planning and Farm Finance Introduction. UVM Farmer Training Program. Mark Cannella. Farm Business Management Specialist

Session 2: Business Planning and Farm Finance Introduction UVM Farmer Training Program Mark Cannella Farm Business Management Specialist Mark.Cannella@uvm.edu 802-223-2389 UVM Extension Farm Viability

Session 2: Business Planning and Farm Finance Introduction UVM Farmer Training Program Mark Cannella Farm Business Management Specialist Mark.Cannella@uvm.edu 802-223-2389 UVM Extension Farm Viability

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02 NF Net Worth Statement Instructions The Samuel Roberts Noble Foundation Introduction: Good financial management is very important to being

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02 NF Net Worth Statement Instructions The Samuel Roberts Noble Foundation Introduction: Good financial management is very important to being

OFFICE OF STATE LANDS AND INVESTMENTS STATE LOAN AND INVESTMENT BOARD 122 WEST 25TH STREET CHEYENNE, WYOMING 82002

OFFICE OF STATE LANDS AND INVESTMENTS STATE LOAN AND INVESTMENT BOARD 122 WEST 25TH STREET CHEYENNE, WYOMING 82002 REGULAR FARM LOAN / BEGINNING AGRICULTURAL PRODUCERS / SMALL WATER DEVELOPMENT PROJECT

OFFICE OF STATE LANDS AND INVESTMENTS STATE LOAN AND INVESTMENT BOARD 122 WEST 25TH STREET CHEYENNE, WYOMING 82002 REGULAR FARM LOAN / BEGINNING AGRICULTURAL PRODUCERS / SMALL WATER DEVELOPMENT PROJECT

Important Terms of Our Equity Account

Introductory Rate Current Promotion Mortgage Loan Originator # Interviewer UMB Bank, n.a. 1010 Grand Blvd Kansas City, MO 64106 Important Terms of Our Equity Account This disclosure contains important

Introductory Rate Current Promotion Mortgage Loan Originator # Interviewer UMB Bank, n.a. 1010 Grand Blvd Kansas City, MO 64106 Important Terms of Our Equity Account This disclosure contains important

AG-AMERICA COMMERCIAL FARM AND RANCH LOAN APPROVAL GUIDE

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents CHAPTER 301 LOAN APPROVAL OVERVIEW... 1 301.1 Preliminary Loan Approval... 1 Credit Standards... 1 302.2 Preliminary Loan Approval... 1 1. Loan Application...

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents CHAPTER 301 LOAN APPROVAL OVERVIEW... 1 301.1 Preliminary Loan Approval... 1 Credit Standards... 1 302.2 Preliminary Loan Approval... 1 1. Loan Application...

HOME EQUITY LINE OF CREDIT

Four Corners Community Bank 500 West Main Street, Suite 101 Farmington, NM 87401 Telephone: 505.327.3222 Fax number: 505.327.3230 Lender Interest Only San Juan County, New Mexico Borrower HOME EQUITY LINE

Four Corners Community Bank 500 West Main Street, Suite 101 Farmington, NM 87401 Telephone: 505.327.3222 Fax number: 505.327.3230 Lender Interest Only San Juan County, New Mexico Borrower HOME EQUITY LINE

Contract Hog Production: Contract hog production

1 MF-1070 Hog enterprise management Contract Hog Production: Contract hog production involves an agreement between a contractor and a grower. The contractor owns and provides feeder pigs for feeder pig

1 MF-1070 Hog enterprise management Contract Hog Production: Contract hog production involves an agreement between a contractor and a grower. The contractor owns and provides feeder pigs for feeder pig

PERSONAL TAX INFORMATION WORKSHEET

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

THE FOLLOWING RESOLUTIONS ARE RECOMMENDED FOR ADOPTION:

Building Rural America National Association of Credit Specialists of the USDA Farm Service Agency Farm Loan Program Committee THE FARM LOAN PROGRAM COMMITTEE MET AT THE CROWNE PLAZA HOTEL IN ROSEMONT,

Building Rural America National Association of Credit Specialists of the USDA Farm Service Agency Farm Loan Program Committee THE FARM LOAN PROGRAM COMMITTEE MET AT THE CROWNE PLAZA HOTEL IN ROSEMONT,

Closed End Loan Disclosure Statement

Closed End Loan Disclosure Statement FIED RATE VARIABLE RATE NAME AND ADDRESS LOAN DATE BORROWER 1 LOAN NUMBER ACCOUNT NUMBER GROUP POLICY NUMBER BORROWER 2 NAME (AND ADDRESS IF DIFFERENT FROM BORROWER

Closed End Loan Disclosure Statement FIED RATE VARIABLE RATE NAME AND ADDRESS LOAN DATE BORROWER 1 LOAN NUMBER ACCOUNT NUMBER GROUP POLICY NUMBER BORROWER 2 NAME (AND ADDRESS IF DIFFERENT FROM BORROWER

Dairy Business Analysis Project: 2007 Financial Summary 1

AN23 Dairy Business Analysis Project: 2007 Financial Summary A. De Vries, R. Giesy, M. Sowerby, and L. Ely 2 Introduction The Dairy Business Analysis Project (DBAP) was initiated in 996 by the University

AN23 Dairy Business Analysis Project: 2007 Financial Summary A. De Vries, R. Giesy, M. Sowerby, and L. Ely 2 Introduction The Dairy Business Analysis Project (DBAP) was initiated in 996 by the University

A. Scott Colby, PC Tax Organizer

A. Scott Colby, PC Tax Organizer ***YOU MUST DOWNLOAD THIS ORGANIZER TO YOUR COMPUTER AND OPEN IT IN ADOBE SOFTWARE BEFORE FILLING OUT ANY INFORMATION OR ELSE YOUR INFORMATION WILL NOT BE SAVED.*** ***DO

A. Scott Colby, PC Tax Organizer ***YOU MUST DOWNLOAD THIS ORGANIZER TO YOUR COMPUTER AND OPEN IT IN ADOBE SOFTWARE BEFORE FILLING OUT ANY INFORMATION OR ELSE YOUR INFORMATION WILL NOT BE SAVED.*** ***DO

Introducing The Income Statement 1

Circular 645 Introducing The Statement 1 P.J. van Blokland 2 Background This publication is one in a series outlining the four basic financial statements used in business today. These statements are the

Circular 645 Introducing The Statement 1 P.J. van Blokland 2 Background This publication is one in a series outlining the four basic financial statements used in business today. These statements are the

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

Refresh Webinar Series: 2018 Road Show Rundown

Refresh Webinar Series: 2018 Road Show Rundown Today s Presenters Larry Jones, Senior Relationship Manager Washington, D.C. Headquarters Phone: 202-872-6604 Scott Steveson, Assistant Manager Credit and

Refresh Webinar Series: 2018 Road Show Rundown Today s Presenters Larry Jones, Senior Relationship Manager Washington, D.C. Headquarters Phone: 202-872-6604 Scott Steveson, Assistant Manager Credit and

The Cash Flow Statement

The Cash Flow Statement This statement is also known as the Statement of Changes in Financial Position Statement of Changes in Financial Position A statement of changes in financial position reports the

The Cash Flow Statement This statement is also known as the Statement of Changes in Financial Position Statement of Changes in Financial Position A statement of changes in financial position reports the

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

AGRICULTURAL BALANCE SHEET

AGRICULTURAL BALANCE SHEET 240 W. 4th St. P.O. 797 Colby, KS 67701 (785) 460-3321 (785) 460-9727 Fax Name(s): SSN or Tax ID No. Date: Residence Address: GENERAL INFORMATION Ownership of Assets/Liabilities

AGRICULTURAL BALANCE SHEET 240 W. 4th St. P.O. 797 Colby, KS 67701 (785) 460-3321 (785) 460-9727 Fax Name(s): SSN or Tax ID No. Date: Residence Address: GENERAL INFORMATION Ownership of Assets/Liabilities

Guide to Home Loans: Finding the Right One 7 DIFFERENT LOAN TYPES

Guide to Home Loans: Finding the Right One 7 DIFFERENT LOAN TYPES ?? There are a lot of loan choices so how do you figure out which is best? If you re looking to buy your first home, refinance or cash

Guide to Home Loans: Finding the Right One 7 DIFFERENT LOAN TYPES ?? There are a lot of loan choices so how do you figure out which is best? If you re looking to buy your first home, refinance or cash

Nurturing Agricultural Businesses ESLC Conference, November 2014 Stephen McHenry, Executive Director

Nurturing Agricultural Businesses ESLC Conference, November 2014 Stephen McHenry, Executive Director www.marbidco.org Is an Ag Development Financial Intermediary Organization Serving All of Maryland With

Nurturing Agricultural Businesses ESLC Conference, November 2014 Stephen McHenry, Executive Director www.marbidco.org Is an Ag Development Financial Intermediary Organization Serving All of Maryland With

Farm Income Statement 2015 Moorhead Farm Business Management Annual Report (Farms Sorted By Net Farm Income) Number of farms

Number of farms") Farm Income Statement Cash Farm Income Barley 5,929 2,010 - - 12,581 14,753 Beans, Black Turtle 350 - - - - 1,723 Beans, Navy 3,627 13,512 - - 5,385 - Corn 168,160 172,777 84,655 79,253 289,902 214,568

Farm Income Statement Cash Farm Income Barley 5,929 2,010 - - 12,581 14,753 Beans, Black Turtle 350 - - - - 1,723 Beans, Navy 3,627 13,512 - - 5,385 - Corn 168,160 172,777 84,655 79,253 289,902 214,568

Allen L. Kockler Company 2018 Tax Organizer

Client Information: Returning Client New Client If a new client, please bring a copy of your 2017 tax return 2017 Preparer Allen Kockler Jon Augustus Mark Moore Taxpayer Name Spouse Name Taxpayer DOB Spouse

Client Information: Returning Client New Client If a new client, please bring a copy of your 2017 tax return 2017 Preparer Allen Kockler Jon Augustus Mark Moore Taxpayer Name Spouse Name Taxpayer DOB Spouse

FSA Direct Loans Loan Making

FSA Direct Loans Loan Making CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can

FSA Direct Loans Loan Making CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P.

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

Conterra Ag Capital. Providing industry leading agricultural loan servicing and wholesale lending to lending partners nationwide

Conterra Ag Capital Conterra supports American Agriculture through creative financial solutions. Providing industry leading agricultural loan servicing and wholesale lending to lending partners nationwide

Conterra Ag Capital Conterra supports American Agriculture through creative financial solutions. Providing industry leading agricultural loan servicing and wholesale lending to lending partners nationwide

IR252 January Dairy farming. A guide to the GST and PAYE obligations of dairy farmers

IR252 January 2018 Dairy farming A guide to the GST and PAYE obligations of dairy farmers www.ird.govt.nz 3 Dairy farming This guide answers some of the common questions dairy farmers ask about GST and

IR252 January 2018 Dairy farming A guide to the GST and PAYE obligations of dairy farmers www.ird.govt.nz 3 Dairy farming This guide answers some of the common questions dairy farmers ask about GST and

Estate Planning What Do We Need to Know Now? Stacy Hambelton Agriculture Business Specialist Gainesville, MO

Estate Planning What Do We Need to Know Now? Stacy Hambelton Agriculture Business Specialist Gainesville, MO Retirement and Estate Planning Issues Men (farmers in particular) don t plan for their retirement

Estate Planning What Do We Need to Know Now? Stacy Hambelton Agriculture Business Specialist Gainesville, MO Retirement and Estate Planning Issues Men (farmers in particular) don t plan for their retirement

FAIRM. Economic Development Authority. Revolving Loan Fund Guidelines

Revolving Loan Fund Guidelines The Fairmont 's Revolving Loan Fund is available within the City Limits of Fairmont, Minnesota. The program works in partnership with local lending institutions to help 'fill

Revolving Loan Fund Guidelines The Fairmont 's Revolving Loan Fund is available within the City Limits of Fairmont, Minnesota. The program works in partnership with local lending institutions to help 'fill

504 Repair Loan Pre Qualification Worksheet

504 Repair Loan Pre Qualification Worksheet Please complete the following information and have each person over the age of 18 sign a separate Form 3550 1 Authorization to Release Information and in house

504 Repair Loan Pre Qualification Worksheet Please complete the following information and have each person over the age of 18 sign a separate Form 3550 1 Authorization to Release Information and in house

City of Carpinteria. Workforce Homebuyer. Down Payment Loan Program. Program Guide and Disclosure. City of Carpinteria

Housing Trust Fund of Santa Barbara County City of Carpinteria Workforce Homebuyer Down Payment Loan Program Program Guide and Disclosure 2017 City of Carpinteria 5775 Carpinteria Avenue Carpinteria, CA

Housing Trust Fund of Santa Barbara County City of Carpinteria Workforce Homebuyer Down Payment Loan Program Program Guide and Disclosure 2017 City of Carpinteria 5775 Carpinteria Avenue Carpinteria, CA

APPLICATION FOR LOAN PARTICIPATION

Rural Finance Authority Minnesota Department of Agriculture 625 Robert Street North St. Paul, Minnesota 55155-2538 651-201-6004 FOR RFA USE ONLY: Application No.: Date Received: APPLICATION FOR LOAN PARTICIPATION

Rural Finance Authority Minnesota Department of Agriculture 625 Robert Street North St. Paul, Minnesota 55155-2538 651-201-6004 FOR RFA USE ONLY: Application No.: Date Received: APPLICATION FOR LOAN PARTICIPATION

Next Generation Farmer Loan Program

Next Generation Farmer Loan Program Program Guidelines June 2016 Commonwealth of Pennsylvania Tom Wolf, Governor Department of Agriculture Department of Community & Economic Development dced.pa.gov Commonwealth

Next Generation Farmer Loan Program Program Guidelines June 2016 Commonwealth of Pennsylvania Tom Wolf, Governor Department of Agriculture Department of Community & Economic Development dced.pa.gov Commonwealth

Instructions for Completing the Uniform Residential Loan Application

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Net farm income is an important

File C3-26 September 2016 www.extension.iastate.edu/agdm Converting Cash to Accrual Net Farm Income Net farm income is an important measure of the financial success of a farm business in a given year.

File C3-26 September 2016 www.extension.iastate.edu/agdm Converting Cash to Accrual Net Farm Income Net farm income is an important measure of the financial success of a farm business in a given year.

Adjustable Rate Mortgages (ARMs) Farm and Ranch Loans

Farm and Ranch Loans") Adjustable Rate Mortgages (ARMs) Farm and Ranch Loans 1-Month, 1-Year, 3-Year, 5-Year, 7/1, 10/1 ARMs. All ARMs have 15-year maturities and amortizations of either 15 or 25 years. The initial interest

Adjustable Rate Mortgages (ARMs) Farm and Ranch Loans 1-Month, 1-Year, 3-Year, 5-Year, 7/1, 10/1 ARMs. All ARMs have 15-year maturities and amortizations of either 15 or 25 years. The initial interest

ROLAND & DIELEMAN 2018 TAX WORKSHEET

ROLAND & DIELEMAN 2018 TAX WORKSHEET FARM 808 4 TH Ave. Grinnell, IA 50112 (641) 236-6558 126 West 3 rd Street Tama, IA 52339 (641) 484-2970 (Grinnell) (641) 484-5622 (Mon./Sat.) 612 4 th St. Sully, IA

ROLAND & DIELEMAN 2018 TAX WORKSHEET FARM 808 4 TH Ave. Grinnell, IA 50112 (641) 236-6558 126 West 3 rd Street Tama, IA 52339 (641) 484-2970 (Grinnell) (641) 484-5622 (Mon./Sat.) 612 4 th St. Sully, IA

Dairy Business Analysis Project: 2006 Financial Summary 1

AN96 Dairy Business Analysis Project: 2006 Financial Summary A. De Vries, R. Giesy, L. Ely, M. Sowerby, B. Broaddus, C. Vann 2 Introduction The Dairy Business Analysis Project (DBAP) was initiated in 996

AN96 Dairy Business Analysis Project: 2006 Financial Summary A. De Vries, R. Giesy, L. Ely, M. Sowerby, B. Broaddus, C. Vann 2 Introduction The Dairy Business Analysis Project (DBAP) was initiated in 996

The Agricultural Extension Service maintains a county farm agent in each of North Carolina s 100 counties and a home agent in 94 counties. They are as

4 meal JAN UARY, 1943 WAR SERIES EXTENSION BULLETIN, \/ HE - FARMER S INCOME TAX 1- NORTH CAROLINA STATE COLLEGE OF AGRICULTURE AND ENGINEERING OF THE UNIVERSITY OF NORTH CAROLINA AND U. 5. DEPARTMENT

4 meal JAN UARY, 1943 WAR SERIES EXTENSION BULLETIN, \/ HE - FARMER S INCOME TAX 1- NORTH CAROLINA STATE COLLEGE OF AGRICULTURE AND ENGINEERING OF THE UNIVERSITY OF NORTH CAROLINA AND U. 5. DEPARTMENT

When Your Home is on The Line:

When Your Home is on The Line: What You Should Know About Home Equity Lines of Credit. If you are in the market for credit, a home equity plan is one of several options that might be right for you. Before

When Your Home is on The Line: What You Should Know About Home Equity Lines of Credit. If you are in the market for credit, a home equity plan is one of several options that might be right for you. Before

Welcome to a brief discussion of balance sheets. The balance sheet is a summary of the things owned and owed by a business. You may choose whether it

Welcome to a brief discussion of balance sheets. The balance sheet is a summary of the things owned and owed by a business. You may choose whether it focuses on the business only or is a combined personal

Welcome to a brief discussion of balance sheets. The balance sheet is a summary of the things owned and owed by a business. You may choose whether it focuses on the business only or is a combined personal

Balance Sheets- step one for your 2018 farm analysis

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Subsidy Layering Review Guidelines & Application

Subsidy Layering Review Guidelines & Application In 2010, HUD granted the Ohio Housing Finance Agency (OHFA) the authority to complete Subsidy Layering Reviews (SLR). Public Housing Authorities (PHA) SLR

Subsidy Layering Review Guidelines & Application In 2010, HUD granted the Ohio Housing Finance Agency (OHFA) the authority to complete Subsidy Layering Reviews (SLR). Public Housing Authorities (PHA) SLR

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Consolidated Financial Statements. Mace Security International, Inc. September 30, 2017 and 2016

Consolidated Financial Statements Mace Security International, Inc. Contents Page Consolidated Balance Sheets 2-3 Consolidated Statements of Operations 4-5 Consolidated Statements of Comprehensive Income

Consolidated Financial Statements Mace Security International, Inc. Contents Page Consolidated Balance Sheets 2-3 Consolidated Statements of Operations 4-5 Consolidated Statements of Comprehensive Income

The Enhanced Cattle Feeder Associations Loan Guarantee Regulations

1 ASSOCIATIONS LOAN GUARANTEE F-8.001 REG 22 The Enhanced Cattle Feeder Associations Loan Guarantee Regulations being Chapter F-8.001 Reg 22 (effective May 14, 2003) as amended by Saskatchewan Regulations

1 ASSOCIATIONS LOAN GUARANTEE F-8.001 REG 22 The Enhanced Cattle Feeder Associations Loan Guarantee Regulations being Chapter F-8.001 Reg 22 (effective May 14, 2003) as amended by Saskatchewan Regulations

Understanding Taxes. and understanding your paycheck!

Understanding Taxes and understanding your paycheck! Summarize the purpose of paying taxes. Recognize the parts of a paystub. Differentiate between net and gross income. Explain what W-2 and W-4 forms

Understanding Taxes and understanding your paycheck! Summarize the purpose of paying taxes. Recognize the parts of a paystub. Differentiate between net and gross income. Explain what W-2 and W-4 forms

Machinery & Equipment Loan Fund (MELF) Program Guidelines Table of Contents

Program Guidelines Table of Contents") Table of Contents Section I General...........................................................1 A. Introduction............................................................1 B. Eligibility..............................................................1

Table of Contents Section I General...........................................................1 A. Introduction............................................................1 B. Eligibility..............................................................1

PAWTUCKET HOUSING AUTHORITY HCV HOMEOWNERSHIP PROGRAM

PAWTUCKET HOUSING AUTHORITY HCV HOMEOWNERSHIP PROGRAM GENERAL OVERVIEW PHA is not required to administer a Homeownership Program; It is voluntary; The PHA has made a commitment to educating, enhancing

PAWTUCKET HOUSING AUTHORITY HCV HOMEOWNERSHIP PROGRAM GENERAL OVERVIEW PHA is not required to administer a Homeownership Program; It is voluntary; The PHA has made a commitment to educating, enhancing

Refresh Webinar Road Show November 19, 2015

Refresh Webinar Road Show 2015 November 19, 2015 Welcome and Introductions Today s Presenters Patrick Kerrigan Director - Business Development Washington, DC pkerrigan@farmermac.com Jim Soppe Assistant

Refresh Webinar Road Show 2015 November 19, 2015 Welcome and Introductions Today s Presenters Patrick Kerrigan Director - Business Development Washington, DC pkerrigan@farmermac.com Jim Soppe Assistant

Livestock Loan Guarantee Program

Livestock Loan Guarantee Program Policy and Procedure Manual Cattle Bison Advance Payment Program January 2014 Saskatchewan.ca Saskatchewan.ca 35684 GSK LLGP_maual title page.indd 1 2014-01-28 12:56 PM

Livestock Loan Guarantee Program Policy and Procedure Manual Cattle Bison Advance Payment Program January 2014 Saskatchewan.ca Saskatchewan.ca 35684 GSK LLGP_maual title page.indd 1 2014-01-28 12:56 PM

Osceola County Purchase Assistance Program Guidelines

Osceola County Purchase Assistance Program Guidelines Purchase Assistance Program Objective The Osceola County Down payment Assistance Program (DPA) is made available through the State Housing Initiatives

Osceola County Purchase Assistance Program Guidelines Purchase Assistance Program Objective The Osceola County Down payment Assistance Program (DPA) is made available through the State Housing Initiatives

Financial Risk: The Importance of Lender Relationship

Financial Risk: The Importance of Lender Relationship Kevin Ferguson Extension Area Specialist Farm Management University of Tennessee Extension kferguson@utk.edu 615-898-7710 (office) Value of Cattle

Financial Risk: The Importance of Lender Relationship Kevin Ferguson Extension Area Specialist Farm Management University of Tennessee Extension kferguson@utk.edu 615-898-7710 (office) Value of Cattle

Table of Contents. Introduction

Table of Contents Option Terminology 2 The Concept of Options 4 How Do I Incorporate Options into My Marketing Plan? 7 Establishing a Minimum Sale Price for Your Livestock Buying Put Options 11 Establishing

Table of Contents Option Terminology 2 The Concept of Options 4 How Do I Incorporate Options into My Marketing Plan? 7 Establishing a Minimum Sale Price for Your Livestock Buying Put Options 11 Establishing

Department of Economics. Financial Intermediation in Agriculture Chapter 15, 16 & 17

Financial Intermediation in Agriculture Chapter 15, 16 & 17 Who has worked for a financial institution? What did you do? For whom? Functions of a financial intermediaries 1. Origination Create the financial

Financial Intermediation in Agriculture Chapter 15, 16 & 17 Who has worked for a financial institution? What did you do? For whom? Functions of a financial intermediaries 1. Origination Create the financial

FSA Guaranteed Loans

FSA Guaranteed Loans CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can change

FSA Guaranteed Loans CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can change

Evaluating the Financial Viability of the Business

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

1997 ISU Swine Business Record Program

1997 ISU Swine Business Record Program Tom J. Baas, assistant professor, Department of Animal Science ASL-R1579 Summary and Implications High-profit producers in the ISU Swine Business Record Program achieve

1997 ISU Swine Business Record Program Tom J. Baas, assistant professor, Department of Animal Science ASL-R1579 Summary and Implications High-profit producers in the ISU Swine Business Record Program achieve

IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT

IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT This disclosure contains important information about our Home Equity Line(s) of Credit (Plan). You should read it carefully and keep a copy for your records.

IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT This disclosure contains important information about our Home Equity Line(s) of Credit (Plan). You should read it carefully and keep a copy for your records.