Bankruptcy How Does it Affect Form 1040?

|

|

|

- Rosamond McLaughlin

- 6 years ago

- Views:

Transcription

1 How Does it Affect Form 1040?

2 For Excel worksheets with formulas go to: User name: lisaihm Password is case sensitive: CODintheREALWORLD This text has been prepared with due diligence. However, the possibility of mechanical or human error does exist and the author accepts no responsibility or liability regarding this material and its use. This text is not intended or written by the practitioner to be used, and cannot be used by a taxpayer or a tax return preparer, for the purpose of avoiding penalties that may be imposed. The text is not intended to address every situation that may arise. Consult additional sources of information, as needed, to determine the solution to tax questions. This publication is designed to provide accurate and authoritative information on the subject of federal tax laws. It is presented with the understanding that the author is not engaged in rendering legal or accounting services Copyright 2017 by, El Cajon, CA and Lisa Ihm, EA, Coronado, CA. Reprinting any part of this text or use without the express written permission of Lisa Ihm is prohibited.

3 Table of Contents Title Chapter Misconceptions... 1 Debt that is not dischargeable... 2 Income Limitation... 2 Estate... 3 Role of the trustee... 4 Tax attributes transfer into estate... 4 Tax return filing requirement... 4 Reporting dispositions of exempt and abandoned assets... 4 Exempt Assets... 5 Exempt assets not subject to basis reduction... 5 Later foreclosure reported on debtor s individual return... 5 Exempt property s eligibility for bankruptcy exclusion... 6 Abandoned Assets... 6 Later foreclosure reported on debtor s individual return... 6 Reduction of basis usually not required... 6 Suspended passive losses... 6 Abandoned property s eligibility for bankruptcy exclusion... 6 Reaffirming debt... 6 Return of Tax Attributes... 7 Tax attributes transfer into estate... 7 Reduction of tax attributes... 7 Post-bankruptcy NOL cannot be carried back... 7 REMEMBER - No basis reduction to exempt (and usually abandoned) assets... 8 After the... 8 Debtor is left with exempt and abandoned assets... 8 Debtor s reduction of tax attributes... 8 Election to File Short-Year Return Who CANNOT make the election How to make election Should you make the short-year election? Chapter i

4 Advantages Who is eligible Role of the trustee Effect on collections Discharge Tax Impact Consider Whether Later May Be Better Deductibility of Fees to Attorney ii Comprehensive Example Worksheet Appendix... a IRS National Standards: Basic Living Allowance... a IRS National Standards: Health Care... a Local Standards: Transportation... b State Median Income Limits... c

5 Title 11 1 Be careful when reading the IRS publications regarding bankruptcy. Title 11 is the bankruptcy title. All bankruptcies come under title 11. Under that title there are different chapters, which is where we get the terms Chapter 11 or Chapter 13 Reorganization. Chapter 7 Discharge Chapter 11 Reorganization > $1 million Chapter 12 Farmers and Fishermen Chapter 13 Reorganization < $1 million Chapter 7 Misconceptions Many think you can only file Chapter 7 bankruptcy if you are low income. The truth is that even high-income people can qualify if they have large amounts of debt, especially secured debt. Many think that you lose everything in Chapter 7 bankruptcy. The truth is that most people get rid of their debt and keep their assets. Many think that the bankruptcy court sells all of the debtor s property. The truth is that the bankruptcy court abandons most property and it is returned to the debtor, and then later foreclosed. Who qualifies to file Chapter 7 bankruptcy Although an individual Chapter 7 case usually results in a discharge of debts, the right to a discharge is not absolute. Debtors must meet income limitations and some types of debts are not discharged. Moreover, a bankruptcy discharge does not extinguish a lien on property downloaded January 9, 2010

6 Debt that is not dischargeable Some of the common types of debts which are not discharged in a Chapter 7: 2 2 Debts for many taxes Returns for tax years due within 3 years of filing the bankruptcy petition Returns filed within 2 years of filing the petition Taxes assessed within 240 days of filing the petition Trust fund taxes False or fraudulent tax returns or willful attempt to evade or defeat the tax Taxes for which a required return was not filed Debts incurred to pay non-dischargeable taxes (taxes charged on credit cards) Debts that are domestic support obligations Debts for most student loans Debts for most fines, penalties, forfeitures, or criminal restitution obligations Debts for personal injuries or death caused by the debtor s operation of a motor vehicle, vessel, or aircraft while intoxicated Some debts which are not properly listed by the debtor Debts for which the debtor has given up the discharge protections by signing a reaffirmation agreement (if you keep the car you keep the car loan) Debts owed to certain retirement plans, for certain types of loans from these plans Income Limitation Income less than state median - If the debtor's "current monthly income" is less than the state median (chart in appendix), the debtor qualifies for a Chapter 7 bankruptcy. Income more than state median If the debtor s current monthly income is more than the state median, the bankruptcy code requires application of a "means test" to determine whether the debtor has the means to pay off the debt. In determining current monthly income the debtor s income is reduced by: Taxes Payments on secured debts (mortgages and cars) Minimal living expenses (rent, food), same as are allowed by the IRS when they work a collection case Involuntary deductions (union dues, uniforms) Health, disability, or term life insurance Court ordered payments (child support, alimony) Child care Health care Education for employment or disabled child Charitable contributions (if made regularly prior to bankruptcy) Care of elderly, chronically ill, or disabled Special circumstances 2 United States Court Official Form 18, 11 U.S.C. 523(a)

3 Example Ima Investor Ima Investor owns a rental property o Monthly rental income $3000 o Monthly expenses $3000 Gross wages $240,000/year Net $12,000/month House payment including taxes &")

, so he has too much income (he has the means to")

7 If the debtor has the means to pay at least part of his creditors, a Chapter 7 bankruptcy discharge will not be allowed. (He may be able to file under Chapter 13.) 3 Example Ima Investor Ima Investor owns a rental property o Monthly rental income $3000 o Monthly expenses $3000 Gross wages $240,000/year Net $12,000/month House payment including taxes & insurance - $ car payments - $1000 each Motor home payment - $1000 per month Allowable basic living expenses - $2000 per month Ima s income is $15,000 per month (rent + wages) and his allowable expenses are $13,000 per month (secured debt payments of 3,000 on rental + 5,000 on house + 2,000 cars + 1,000 motor home + living expenses of 2,000), so he has too much income (he has the means to repay the debt) and would not qualify for a Chapter 7 bankruptcy. However, if there was no tenant in the rental property, the income would drop to $12,000 and his expenses would still be $13,000 and he would qualify! Last 6 months of income and expenses - The means test is calculated based on the last 6 months of income, so a debtor may file for bankruptcy on a specific date to take advantage of a seasonally low income period. That s why we sometimes have a client call and say they are declaring bankruptcy and need their past due tax returns right away. They cannot file unless all required returns have been filed and they may need to file immediately to take advantage of a low income period and pass the means test. Estate Commencement of a Chapter 7 bankruptcy case creates a separate taxable bankruptcy estate that is overseen by a bankruptcy trustee. The estate technically controls all of the debtor's property (including tax attributes) during the duration of the estate. (No physical transfer actually happens, at least at the beginning of the process. The debtor remains in possession of his assets, including his bank accounts, investment portfolio, rental properties, etc. He continues to live in his house and life goes on as usual.)

8 Role of the trustee When a Chapter 7 petition is filed, an impartial trustee is appointed to administer the case. The trustee s duties include: 1) Determining whether the debtor qualifies for a debt discharge (including whether the debtor passes the means test), and 2) Liquidating the debtor's nonexempt assets if they are free and clear of liens, or if they are worth more than any security interest or lien attached to the property. 3 (If an asset has no equity, the trustee has no use for it.) If all the debtor's assets are exempt or subject to valid liens, the trustee will normally file a "no asset" report with the court and there will be no distribution to unsecured creditors. (Most Chapter 7 cases involving individual debtors are no asset cases.) 4 Tax attributes transfer into estate The debtor s tax attributes transfer into the estate on the 1 st day of the tax year in which the petition for bankruptcy is filed. 4 ONLY TAX ATTRIBUTES THAT EXISTED ON THE DAY OF THE BANKRUPTCY FILING WILL BE REDUCED WHEN THE BANKRUPTCY EXCLUSION IS USED. 5 Tax return filing requirement This bankruptcy estate is a new taxable entity, completely separate from the individual taxpayer. The trustee would file an income tax return on Form 1041 if the estate has gross income that meets or exceeds the amount required for filing. This amount is the total of the personal exemption amount and the basic standard deduction for a married individual filing separately. The trustee normally does NOT file a tax return, because the only income of the estate is COD that is excluded because of the bankruptcy exclusion. However, in order to use tax attributes that may transfer back to the debtor from the estate, the debtor s tax preparer needs the information that would have been on the estate s Form The preparer may need to recreate the 1041 to determine what amount of tax attributes remain. (This is discussed in detail later.) Reporting dispositions of exempt and abandoned assets Dispositions of exempt and abandoned assets are reported on the debtor s Form 1040, since they are not under the control of the bankruptcy trustee when the dispositions occur U.S.C. 701, (g) 5 IRC 108(d)(8) 6 Olson, Stanley (1990)

9 Exempt Assets An individual debtor may protect some property from the claims of creditors because it is exempt under federal bankruptcy law or under the laws of the debtor's home state. 7 In many states, the individual debtor has the option of choosing between a federal package of exemptions or the exemptions available under state law. 8 Typical exempt assets include: 5 Debtor s home (different values are excludable in different states) Cars (basic transportation) (AZ can t exceed $5000 value) Clothes Household furnishings Tools of trade (limited amounts) Limited amounts of jewelry, computers, and electronics Retirement funds including IRAs 9 (IRAs may be capped at $1M in some states 10 ) Specific state exemptions include: Texas and Florida Mansion of any value (CA exempts a max $150,000 home equity) Nevada Gun, home to $550,000, and $1000 wildcard 11 California More than $20,000 wildcard if not using homestead exemption 12 None of these exempt assets ever transfer to the estate. possession of the debtor. They remain in the Exempt assets not subject to basis reduction When doing basis reductions for COD excluded using the bankruptcy exclusion, do not reduce the basis in property that the debtor treats as exempt property. 13 This property was never a part of the bankruptcy estate, so no basis reduction will be applied to these assets. Later foreclosure reported on debtor s individual return Since the exempt property never belonged to the bankruptcy estate, the gain or loss from its sale is reported on the debtor s Form U.S.C. 522(b). 8 downloaded January 9, U.S.C. Section 522(a)(3)(C) U.S.C. 522(n) 11 Nev. Rev. Stat. Ann (z) 12 downloaded January 9, Code Sec. 1017(c)(1) 14 Olson, Stanley (1990 DC IA) affd (1991, CA8)

10 Exempt property s eligibility for bankruptcy exclusion Most exempt assets qualify for the bankruptcy exclusion, but in some cases some debts are intentionally not included in the bankruptcy. In order to use the bankruptcy exclusion, the debt had to be discharged by the bankruptcy court, and therefore had to be included in the bankruptcy. If debt that was not included in the petition is later discharged, the resulting COD is not eligible for the Exclusion, because the debt was not cancelled by the bankruptcy court. 6 Abandoned Assets The trustee may abandon any asset that has no equity, and the debt on the abandoned asset is made unenforceable by the bankruptcy court. 15 (In reality, the assets remained with the debtor the entire time and the debtor continued to use them.) Later foreclosure reported on debtor s individual return Since on abandonment the property ceases to be property of the estate, the debtors are taxable on the gain from its sale after abandonment by the trustee. 16 Reduction of basis usually not required No reduction in basis is usually required to abandoned assets because of the basis insolvency rule, which provides that basis reduction is required only to the extent that the debtor s basis exceeds his liabilities immediately after the discharge. This calculation is done by the bankruptcy estate, and since the bankruptcy estate includes all of the secured debt but not the exempt assets it will almost always be basis insolvent and basis reduction will not be required. Suspended passive losses If, before the termination of the bankruptcy estate, the estate transfers an interest in a passive activity or former passive activity to the debtor, that property s unused passive activity loss and credits also transfer back to the debtor and can be used on the debtor s individual tax return. 17 Abandoned property s eligibility for bankruptcy exclusion COD income resulting from the discharge of debt on abandoned property (that is later foreclosed or on which the loan is later modified) does qualify for the Exclusion, because the court made the debt unenforceable. Reaffirming debt If a debtor wishes to keep certain secured property (such as an automobile), he or she may decide to "reaffirm" the debt. A reaffirmation is an agreement between the debtor and the creditor that the debtor will remain liable and will pay all or a portion of the money owed, even though the debt would otherwise be discharged in the bankruptcy. In return, the creditor promises that it will not repossess or take back the automobile or other property so long as the debtor continues to pay the debt USC 554(a) 16 Olson, Stanley (1990) 17 Reg (d)(2)

11 Return of Tax Attributes Tax attributes transfer into estate The debtor s tax attributes transfer into the estate on the 1 st day of the tax year in which the petition for bankruptcy is filed No Form 1041 RECREATE IT The trustee is only required to file a Form 1041 if there is taxable income, and there is rarely any income in a Chapter 7 case since most property has no equity and is abandoned by the bankruptcy trustee. Tax attributes must be reduced, even if the trustee did not file a return. 19 If no Form 1041 was filed, one will have to be recreated in order to determine what tax attributes return to the debtor. Relax, this is much easier than you think! The Form 1041 is actually just a cover page for a Form 1040, and we all know how to do a Recreate a 1040 for the bankruptcy estate and reduce tax attributes just like you would on an individual return. Any tax attributes not required to be reduced on the Form 982 return to the debtor on the discharge date. Reduction of tax attributes Tax attributes must be reduced by the amount of COD incurred: 1) Within the bankruptcy estate (the discharge of unsecured debt, i.e. credit cards) 2) Excluded from the 1040 (debt secured by real estate) after bankruptcy exclusion ONLY ATTRIBUTES THAT EXISTED AT THE TIME OF THE BANKRUPTCY FILING ARE SUBJECT TO ATTRIBUTE REDUCTION WHEN THE BANKRUPTCY EXCLUSION IS USED. 20 If a net operating loss is created after the bankruptcy petition filing date, that NOL is NOT subject to attribute reduction when the bankruptcy exclusion is used. Post-bankruptcy NOL cannot be carried back An individual debtor cannot carry back to a tax year that preceded the tax year in which the bankruptcy case was commenced any net operating loss (NOL) or credit carryback from a tax year ending after commencement of the bankruptcy case (g) 19 Firsdon, Jack (1994) 20 IRC 108(d)(8) 21 IRC 1398(j)(2)(B); IRC 1398(j)(2)(C)(i)

12 Example Danny Debtor Has a rental property Owes $80,000 of credit card debt No NOL or other tax attributes except basis Chapter 7 bankruptcy in July $80,000 COD excluded by bankruptcy estate Rental abandoned; foreclosed December o $200,000 loss on sale o $300,000 COD (bankruptcy exclusion) o Loss creates NOL on tax return The NOL did not exist at time of bankruptcy filing, so it is not subject to reduction! Danny MUST carry NOL forward. He cannot carry back to a pre-bankruptcy year, so the NOL will carry forward even if no election to forego the carryback period is made. 8 REMEMBER - No basis reduction to exempt (and usually abandoned) assets There is no basis reduction to exempt assets (which were never a part of the estate) 22, or abandoned assets if the bankruptcy estate was basis insolvent. After the Debtor is left with exempt and abandoned assets The debtor can: 1. Continue to make payments on any secured debts on these assets and keep them, 2. Sell them, 3. Quit making payments and the lender will foreclose. Any disposal of the exempt and abandoned assets will be reported on the debtor s 1040, but the bankruptcy exclusion can generally be used to exclude the COD. Debtor s reduction of tax attributes If, after the bankruptcy, a debtor excludes COD on debt that was made unenforceable in a bankruptcy case, they must reduce tax attributes by the excluded amount, BUT ONLY TO ATTRIBUTES THAT EXISTED AT THE TIME OF THE BANKRUPTCY FILING. No basis reduction is required to exempt property, and usually not to property that was abandoned by the bankruptcy trustee (because of the basis insolvency rule), when the bankruptcy exclusion is used IRC 108(d)(8) 23 IRC 1017(c)

13 Example 1 - Simple No attributes Debtor Debbie has a house, car, furniture, and IRA accounts (all exempt) Owes $80,000 of credit card debt No tax attributes Chapter 7 bankruptcy 9 The bankruptcy estate would have $80,000 of COD income, which it would exclude using the bankruptcy exclusion. The estate is required to reduce tax attributes by the $80,000 that is excluded, but there are no tax attributes to reduce (there isn t even basis in property because all of the property was exempt so none of it is in the bankruptcy estate). There will be no impact on Debbie s personal Form Any 1099-C for the credit card discharge should be made out to the bankruptcy estate. If Debbie receives a C in her social security number, put it on line 21 and take it back off again as COD of bankruptcy estate. DO NOT put it on a Form 982. It is not her COD! Example 2 - Rental property Debbie also owns a rental property Mortgage $500,000 Worth $400,000 Suspended passive losses of $40,000 The passive losses go into the bankruptcy estate on the first day of the tax year in which Debbie files her petition. Since the property has no equity, the bankruptcy trustee will abandon it. When he abandons it, he also gives back the passive losses associated with the property. When the bankruptcy is discharged and the $80,000 of credit card debt is discharged, the bankruptcy estate will be required to reduce tax attributes, but it will no longer have the passive losses (they were returned to the taxpayer when the rental property was abandoned), so no attribute reduction will be required. On Debbie s personal Form 1040, even though the trustee had control of the rental property for a few weeks, Debbie actually retained use of the property. She collected rental income during the entire process and will report the rental of the property for the entire year on her Form Note If the passive losses are in the possession of the bankruptcy estate on the last day of the tax year, the debtor will NOT be able to use them on that year s tax return.

14 10 Example 3 filed late in the year Debbie files for bankruptcy on December 10 Her hearing date is January 15 of the next year The trustee abandons the rental on January 22 of the next year. Debbie had income from the sale of another rental property before the bankruptcy on March 3 Debbie is not in possession of the passive losses on December 31, so she cannot use them on her tax return (to offset the gain from the March sale of the other property). She will get them back when the rental property is abandoned January 22 of the next year. Example 4 Rental foreclosed later at a gain Rental later foreclosed $100,000 COD Basis $200,000 Foreclosure sale price $400,000 Debbie will report the sale of the rental on her Form The $200,000 gain ($400k sell price - $200k basis) is taxable. Her passive losses (which are freed up by the total disposition) will offset some of this income. Filing bankruptcy will NOT relieve the debtor from gain on the disposition of the asset, unless the asset is actually sold by the bankruptcy estate (which is rare). The $100k of COD will be excluded using the bankruptcy exclusion. She will have to reduce tax attributes by $100k, but will not have to reduce her passive losses because they are consumed on the tax return in the year of discharge. The reduction of tax attributes occurs on the first day of the tax year following the year of discharge. On January 1 of the next year the suspended passive losses will no longer exist. Her only tax attributes will be basis in her personal use assets, including her house, car, furniture, and IRA (which may have basis if it is a Roth IRA). These were all exempt assets in the bankruptcy, so no basis reduction is required when the bankruptcy exclusion is used.

15 Example 5 Rental foreclosed later at a loss 11 What if the foreclosure sale price was only $150,000? Filing bankruptcy will not relieve the debtor from reporting gain on disposition of an asset, but it will likewise not eliminate the deductibility of a loss on disposition. The loss of $50,000 would be deducted on Debbie s Form The $40,000 of suspended passive losses will be freed-up because of the total disposition of the activity. These two large deductions create a NOL on her return. She is required to reduce tax attributes on January 1 of the next year, but the passive losses were used and no longer exist then. The NOL will carry forward (it cannot be carried back to a pre-petition year), but because the NOL did not exist at the time of the bankruptcy filing it is not subject to attribute reduction (it was not a tax attribute transferred into the bankruptcy estate and is therefore not subject to attribute reduction when the bankruptcy exclusion is used.) Example 6 Home foreclosed in later year Home is foreclosed 5 years later COD $150,000 Sales price $350,000 Basis $100,000 The sale is reported on Debbie s Form The gain on the sale can be excluded using the 121 exclusion. The COD qualifies for the bankruptcy exclusion, even though the home was exempt, since the debt was included in the petition. Example 7 Tax attributes reduced in bankruptcy estate Danny Debtor Filed chapter 7 bankruptcy September 5 $75,000 capital loss carry forward to this year s return $80,000 of credit card debts The bankruptcy estate has $80,000 of COD income. They will use the bankruptcy exclusion to exclude the COD income and must reduce tax attributes. The only tax attribute the estate has is the $75,000 of capital loss carry forwards, so the carry forward is lost. No tax attributes return to Danny when the bankruptcy is discharged.

16 Example 8 Several types of attributes in estate 12 Danny also had a Net Operating Loss of $50,000 carrying forward to this year Tax attributes are reduced in the same order by the bankruptcy estate as they are by individuals, so the $50,000 NOL is reduced first. Danny also loses $30,000 of the capital loss carry forward, but the remaining $45,000 of capital loss carry forward is returned to Danny for use on his individual Form Election to File Short-Year Return The debtor/taxpayer can elect to end their tax year the day before the bankruptcy filing. The debtor will file two Form 1040s and the bankruptcy estate will (in theory) file a Election affects who uses tax attributes; the debtor or the estate. Election not made Attributes transfer to the bankruptcy estate on January 1, so they are not available for the debtor to use. However, any attributes created after January 1 will stay with the debtor, so if large losses or credits are incurred between January 1 and the date of filing, those attributes will stay with the debtor. Election made Attributes transfer on the day of the bankruptcy filing, after being used up by the debtor on the short-year return. If the debtor has income from January 1 to the date of filing, and tax attributes on January 1, filing a short-year return will allow him to use those attributes to offset that income before transferring the remaining attributes into the estate. Election affects who is liable for paying tax liabilities. Election not made If the election is not made, the debtor remains liable for the entire tax liability for the entire year Election made The tax liability from the first short-year return becomes a priority claim of the bankruptcy estate and will be paid first by the bankruptcy estate (if the bankruptcy estate has any assets, which it often does not). If there are not enough assets in the estate to pay the entire tax liability, it transfers back to the debtor. Who CANNOT make the election No short-year election may be made by a debtor who has no assets other than exempt property. 24 (Note that if the debtor has only abandoned property, he can still make the election.) How to make election Make the election by filing Form 1040 for the short period. This return is due on or before the 15 th day of the 4 th full month following the date of the bankruptcy filing. A 6- month extension can be filed on Form 4868, but the extension request must be made timely. Write Section 1398 Election at the top of the Form IRC Section 1398(d)(2)(C)

. If the taxpayer does not tell you about the bankruptcy until he comes in to get that year s tax return prepared, it may be too late to make the short-year election.")

17 13 If the debtor/taxpayer files for bankruptcy on February 7, the short-year return is due Example Due Date if Short-Year Election Made June 15 (4th full month is March, April, May, June, so due 15 th day of that month, June 15). If the taxpayer does not tell you about the bankruptcy until he comes in to get that year s tax return prepared, it may be too late to make the short-year election. Should you make the short-year election? Yes if: Income in the beginning of the year could be offset by attributes, or Income creates a tax balance due in the beginning of the year and there are bankruptcy assets to pay the tax. No if: An NOL, credits, and other tax attributes are created in the period from January 1 until the date of filing. Example 1 Preserve attributes available on 1-1 Danny Debtor declared bankruptcy on September 5 $75,000 capital loss carry forward to this year In May he sold stock and had an $85,000 profit Should he make a short-year election? Yes. If he makes a short year election he can use the capital loss carry forward on the short-year return to offset the $85,000 capital gain. His tax attributes will go into the bankruptcy estate on September 5 (the first day of the tax year that includes the filing date), but the capital loss will already be used up on the tax return for the period from January 1 to September 4. Example 2 No election if no attributes on 1-1 Danny has no tax attributes on January 1 Sold stock in May and had a $50,000 loss Sold more stock in October and had a $50,000 gain Should he make a short-year election? No. If he does not make the election, his tax attributes transfer into the estate on January 1. He did not have the capital loss at that time, so it does not go into the estate and he can use it on his personal tax return to offset the gain from the later stock sale. If he makes the election, the capital loss will transfer into the estate and be subject to attribute reduction.

18 Example 3 Attributes created during short-year before filing Danny has no tax attributes on January 1 Schedule C business has a $70,000 loss early this year Should he make a short-year election? 14 No. If he does not make the election, his attributes transfer into the estate on January 1. The NOL created by his business loss did not exist at that time so it will not transfer into the estate. If he makes the short-year election the attributes transfer in on September 4. The NOL created on the short-year return would then have to transfer into the bankruptcy estate. (He could carry the NOL back and file for refunds from prior years, but those expected refunds would then become assets of the bankruptcy estate.) Chapter 13 A Chapter 13 bankruptcy is often called a wage earner's plan. It enables individuals with regular income to develop a plan to repay all or part of their debts over three to five years. During this time the law forbids creditors from starting or continuing collection efforts. Advantages A particular advantage of Chapter 13 is that it provides individual debtors with an opportunity to save their homes from foreclosure by allowing them to "catch up" past due payments through a payment plan. 25 Who is eligible Any individual, even if self-employed or operating an unincorporated business, is eligible for Chapter 13 relief as long as the individual's unsecured debts are less than $394,725 and secured debts are less than $1,184, Role of the trustee When an individual files a Chapter 13 petition, an impartial trustee is appointed to administer the case. 27 The Chapter 13 trustee both evaluates the case and serves as a disbursing agent, collecting payments from the debtor and making distributions to creditors. 28 Effect on collections Individuals may use a Chapter 13 proceeding to save their home from foreclosure. The automatic stay stops the foreclosure proceeding as soon as the individual files the Chapter 13 petition. The individual may then bring the past-due payments current over a reasonable period of time. The debtor may still lose the home if he or she fails to make the regular mortgage payments that come due after the Chapter 13 filing downloaded U.S.C. 109(e) U.S.C U.S.C. 1302(b).

, debts incurred to pay nondischargeable tax obligations,")

19 15 A Chapter 13 debtor is entitled to a discharge upon completion of all payments under Discharge the Chapter 13 plan. The discharge in a Chapter 13 case is somewhat broader than in a Chapter 7 case. Debts dischargeable in a Chapter 13, but not in Chapter 7, include debts for willful and malicious injury to property (as opposed to a person), debts incurred to pay nondischargeable tax obligations, and debts arising from property settlements in divorce or separation proceedings. 29 Tax Impact When a debtor files for reorganization under Chapter 13, no separate bankruptcy estate is created. The taxpayer continues to report all transactions on their individual Form When the remaining debts are discharged at the end of the case, the COD is reported on the debtor s Form 1040 using the Exclusion, and tax attributes are reduced on the debtor s 1040 return. Example Chapter 13 discharge Wally Wageearner $80,000 credit card debt $20,000 behind on house payments $100,000 2 nd mortgage on house Filed Chapter 13 and made last payment 5 years later Discharged $80,000 of credit cards & $90,000 of 2 nd The $170,000 of COD will be reported on Wally s Form 1040 in the year he makes the last payment. (Until this time the only effect on his personal return will have been that he was not making the full payments on the 2 nd, so his mortgage interest deduction was lower than it was before he declared bankruptcy.) He will use the bankruptcy exclusion to exclude the COD income and is required to reduce tax attributes. There is no separate bankruptcy estate, so all transactions are reported on the Form Consider Whether Later May Be Better Many COD transactions result in high tax liabilities caused by both taxable COD income and gain on the disposition of property. Before the debtor rushes into bankruptcy to avoid tax on COD income, they should also estimate the tax liability on disposition of the property. It may be better to wait and declare bankruptcy 3 years later to discharge the tax on disposition. (A later bankruptcy is generally only beneficial if the debtor is not keeping any properties. If the debtor retains property, the IRS will file a tax lien on that property as soon as they realize the large amount of the liability, and a later bankruptcy will not remove the tax lien.) U.S.C. 1328(a).

20 Deductibility of Fees to Attorney 16 The debtor can deduct fees in connection with a bankruptcy if the bankruptcy is proximately caused by the failure of a business enterprise. The deductible portion is the part of the total fee which bares the same ratio to the legal fee as the claims of the business creditors bears to the claims of all the creditors. 30 Business debt x Total legal fee = Deductible legal fee Total debt 30 Pierson (1986); Cox (1981); Catalano (2000)

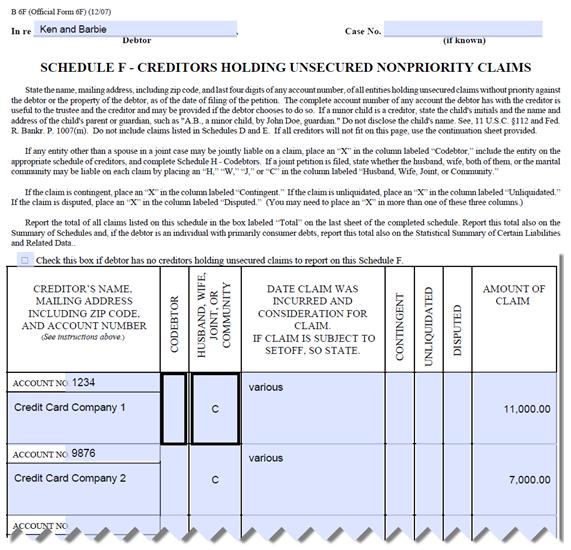

21 Comprehensive Example 17 Ken and Barbie declared bankruptcy February 1 Pertinent pages from petition follow Discharged August 1 Usedtobehome Drive mortgage modified Dec 1 of the same year Dreamhouse Lane foreclosed December 5 of the same year Boughtlongago Way foreclosed January 1 of the next year Paid attorney s fees of $3,000

22 18

23 19

24 20

25 21

26 Worksheet 22

27 Solution 23 Short-year election No short-year election was made because the taxpayer didn t tell us about the bankruptcy until after the deadline had already passed. A short-year election would have allowed us to use the NOL to offset income earned between January 1 and the bankruptcy filing date. Passive losses - The passive losses return to the debtor when the property is abandoned by the trustee. Since the property and associated passive loss was abandoned before the end of the tax year, they are back in the possession of the debtor in time to be used on his Form Net Operating Loss The California NOL is larger than the federal NOL because CA does not allow NOL carrybacks. Reduction of Tax Attributes There is $18,000 of COD in the bankruptcy estate, so tax attributes must be reduced by that amount. Attributes returned to debtor The remaining NOL is returned to the debtor on the date the bankruptcy is discharged. Since the bankruptcy was discharged before the end of the year, they are back in the possession of the debtor in time to be used on the debtor s Form (If the bankruptcy had not been discharged until the next year, the NOLs would not be available for use on the current year 1040, but could be used on the next year s return.) Attorney s fees The $3000 attorney s fees must be prorated among the debt that was discharged. Debt Description Amount % x fee Deductible Where Credit cards $ 18,000 <.5% No Dreamhouse Lane 4,000,000 70% x 3000 No Boughtlongago Way 1,250,000 22% x 3000 $660 Sch E Usedtobehome Drive 450,000 8% x 3000 No Total 5,718, % Note: Ken and Barbie moved back into Usedtobehome Drive before the bankruptcy filing, so it had reverted to personal use property.

When refinanced, $100,000 of costs added to mortgage balance Real estate taxes due $50,000 Accrued interest estimated to be $200,000 Sale price")

28 Example Continued Usedtobehome Drive loan modified December 1 Bank discharged $70,000 of accrued interest and $100,000 of principal 24 The accrued interest that is discharged does not create COD, because the interest would have been deductible if paid. Therefore, the COD is $100,000 (regardless of what the 1099-C says). Regardless of whether the loan is recourse or nonrecourse, the reduction in the principal amount by a loan modification creates COD. On Ken and Barbie s Form 1040, the COD is excluded using the bankruptcy exclusion since the debt was made unenforceable by the bankruptcy estate. They must reduce tax attributes on Jan 1 of the next year, but first we need to complete this year s return. Example Continued Dreamhouse Lane foreclosed December 5 Note the date on 1099-A (They mistakenly believed that when they filed for bankruptcy the house would be taken from them immediately, so they abandoned Dreamhouse and moved back into Usedtobehome Drive. They could have stayed in Dreamhouse for almost a whole additional year!) When refinanced, $100,000 of costs added to mortgage balance Real estate taxes due $50,000 Accrued interest estimated to be $200,000 Sale price on trustee s deed $1,500,000 Unpaid debt together with costs on trustee s deed $4,270,000 Purchased for 4,200,000 NOTE: This form was completed incorrectly. Box 2 should have been $4,000,000 (but incorrect forms are common and we need to understand how to calculate the correct numbers).

29 25

30 26 The COD is excluded using the bankruptcy exclusion rather than the Qualified Principal The loss on the sale of the residence is not deductible. Residence Exclusion (bankruptcy exclusion is mandatory). Attribute reduction is required, but we need to complete the entire return for this year before we can determine which attributes will be reduced. Example cont. After completion of the current year return, these attributes remain: NOL $35,000 ($72k returned by bankruptcy estate - $37k used) Passive loss carryover $20,900 on Boughtlongago Way

so no basis reduction is required. Ken and Barbie lose all of their NOL and passive losses.")

31 27 Basis reduction is not required in exempt assets and the bankruptcy estate was basis insolvent (debt exceeded basis immediately after discharge) so no basis reduction is required. Ken and Barbie lose all of their NOL and passive losses.

32 28 Ken and Barbie lose all of their CA NOL and passive losses.

33 29

34 FOR CALIFORNIA PURPOSES ONLY 30

35 Example Continued Boughtlongago Way foreclosed January 5 of the next year Property located in Arizona, recourse loan $400,000 sale price per trustee s deed Land basis $10,000, building basis $0 Unpaid debt together with costs from trustee s deed $900,000 Unpaid real estate taxes $3,000 Foreclosure costs $7,000 Accrued interest due $90,000 31

36 32 The gain on the sale will be reported on Ken and Barbie s Form Declaring bankruptcy will not alleviate tax on gain from the disposition of property unless the property is actually sold by the bankruptcy estate (which is extremely rare). The suspended passive loss on the property was lost to attribute reduction. (The gain on the sale is passive, so if there were any suspended passive losses on other properties, those losses would be available to offset the gain.) Planning Opportunity What if Boughtlongago Way had been foreclosed in the same year as the bankruptcy discharge? The $35,000 federal NOL and $112,000 California NOL that were lost to attribute reduction could have been used to offset the gain on the sale, as well as the $20,900 passive losses that were lost to attribute reduction. The best tax outcome will usually result if all properties are foreclosed in the same year. Planning Opportunity Should they have waited to declare bankruptcy? If they had let the properties go to foreclosure, filed the tax returns, and waited 3 years before declaring bankruptcy, the amount of tax would have been higher because the COD would not have qualified for the bankruptcy exclusion, but they could have had the entire tax discharged in the bankruptcy. The strategy works best when the debtors are not going to keep any real estate, because the IRS will file a Notice of Federal Tax Lien as soon as the balance due returns are filed. In this case, they are not keeping any real estate, so the Tax Lien would not have anything to attach to.

37 Appendix a IRS National Standards: Basic Living Allowance 31 IRS National Standards: Health Care 31 Current allowances are available at Employed/National-Standards-Food-Clothing-and-Other-Items

38 Local Standards: Transportation 32 b 32 Current allowances are available at Employed/Local-Standards-Transportation

39 State Median Income Limits 33 c 33 For cases filed after Chart changes about every 18 months

Bankruptcy 1. WHAT IS A DISCHARGE IN BANKRUPTCY?

Bankruptcy DISCLAIMER: The information contained in this fact sheet is of a general nature and is provided for your assistance. It is not intended as legal advice and is not a substitute for legal counsel.

Bankruptcy DISCLAIMER: The information contained in this fact sheet is of a general nature and is provided for your assistance. It is not intended as legal advice and is not a substitute for legal counsel.

LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA Tel.(818) Facsimile (818)

Facsimile (818)") LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214 INITIAL CONSULTATION AGREEMENT AND REQUIRED NOTICES Please Note: These documents

LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214 INITIAL CONSULTATION AGREEMENT AND REQUIRED NOTICES Please Note: These documents

BANKRUPTCY CLIENT FORM We accept the following forms of payment: cash or check. Cell Phone:

Name: Spouse s Name: Business Names: Mailing Address: Home Phone: Fax: Email: BANKRUPTCY CLIENT FORM We accept the following forms of payment: cash or check. City: Have you filed bankruptcy before? Yes

Name: Spouse s Name: Business Names: Mailing Address: Home Phone: Fax: Email: BANKRUPTCY CLIENT FORM We accept the following forms of payment: cash or check. City: Have you filed bankruptcy before? Yes

BANKRUPTCY CHAPTER 7 (aka Discharge or Liquidation )

") BANKRUPTCY CHAPTER 7 (aka Discharge or Liquidation ) ANSWERS TO THE MOST COMMONLY ASKED QUESTIONS Compliments of: Sam C. Gregory, PLLC 2742 82 nd Street Lubbock, Texas 79423 (806) 687-4357 1. What is chapter

BANKRUPTCY CHAPTER 7 (aka Discharge or Liquidation ) ANSWERS TO THE MOST COMMONLY ASKED QUESTIONS Compliments of: Sam C. Gregory, PLLC 2742 82 nd Street Lubbock, Texas 79423 (806) 687-4357 1. What is chapter

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES 1. What is a chapter 7 bankruptcy case and how does it work? A chapter 7 bankruptcy case is a proceeding under federal law

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES 1. What is a chapter 7 bankruptcy case and how does it work? A chapter 7 bankruptcy case is a proceeding under federal law

REDSTONE LEGAL BRIEF. A Preventive Law Service of The Office of the Staff Judge Advocate Redstone Arsenal, AL

REDSTONE LEGAL BRIEF A Preventive Law Service of The Office of the Staff Judge Advocate Redstone Arsenal, AL Keeping You Informed On Personal Legal Affairs Bankruptcy THIS HANDOUT is provided for general

REDSTONE LEGAL BRIEF A Preventive Law Service of The Office of the Staff Judge Advocate Redstone Arsenal, AL Keeping You Informed On Personal Legal Affairs Bankruptcy THIS HANDOUT is provided for general

Bankruptcy FAQs - Luongo Bellwoar LLP

Bankruptcy FAQs - Luongo Bellwoar LLP A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot

Bankruptcy FAQs - Luongo Bellwoar LLP A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot

Bankruptcy. Consider these questions and answers to determine whether filing for bankruptcy is in your long-term best interest.

Bankruptcy Please note that this Information Paper only provides basic information and is not intended to serve as a substitute for personal consultations with a Legal Assistance Attorney. Consider these

Bankruptcy Please note that this Information Paper only provides basic information and is not intended to serve as a substitute for personal consultations with a Legal Assistance Attorney. Consider these

CLIENT INFORMATION SHEET. PERSONAL INFORMATION spouse s ssn (last 4 only):

:") Today s date / / Please indicate below how you heard about us: CLIENT INFORMATION SHEET Your name: Spouse s name: PERSONAL INFORMATION your ssn (last 4 only): spouse s ssn (last 4 only): Physical address:

Today s date / / Please indicate below how you heard about us: CLIENT INFORMATION SHEET Your name: Spouse s name: PERSONAL INFORMATION your ssn (last 4 only): spouse s ssn (last 4 only): Physical address:

A REVIEW OF THE NEW BANKRUPTCY LAW. Wednesday, 15 February 2006

A REVIEW OF THE NEW BANKRUPTCY LAW Wednesday, 15 February 2006 I. One of the main purposes of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 is to prohibit granting relief under Chapter

A REVIEW OF THE NEW BANKRUPTCY LAW Wednesday, 15 February 2006 I. One of the main purposes of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 is to prohibit granting relief under Chapter

NEWARK-FREMONT LEGAL CENTER BANKRUPTCY WORKSHEET

NEWARK-FREMONT LEGAL CENTER BANKRUPTCY WORKSHEET Complete the form below and then call our office for an appointment. 794-LAWS Please Print Clearly! DEBTOR JOINT DEBTOR Full Name Street Address Mailing

NEWARK-FREMONT LEGAL CENTER BANKRUPTCY WORKSHEET Complete the form below and then call our office for an appointment. 794-LAWS Please Print Clearly! DEBTOR JOINT DEBTOR Full Name Street Address Mailing

Cancellation Of Debt Income. Presented by Bobby L Burns

Cancellation Of Debt Income Presented by Bobby L Burns Training Outline Lesson 1: What is COD Income? Forclosure, repossession or default. Lesson 2: IRC 108 provisions Exceptions and exclusions. Lesson

Cancellation Of Debt Income Presented by Bobby L Burns Training Outline Lesson 1: What is COD Income? Forclosure, repossession or default. Lesson 2: IRC 108 provisions Exceptions and exclusions. Lesson

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE 1. Know your case number. 2. Make your payments. Send your payments in time for the payments to reach the Trustee s office by

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE 1. Know your case number. 2. Make your payments. Send your payments in time for the payments to reach the Trustee s office by

Chapter 4. 1:05 2:05pm. The Chapter 13 Plan and Saving Your Client s Home. William F. Malaier Jr. Nagler & Malaier, P.S.

Chapter 4 1:05 2:05pm The Chapter 13 Plan and Saving Your Client s Home William F. Malaier Jr. Nagler & Malaier, P.S. PowerPoint distributed at the program and also available for download in electronic

Chapter 4 1:05 2:05pm The Chapter 13 Plan and Saving Your Client s Home William F. Malaier Jr. Nagler & Malaier, P.S. PowerPoint distributed at the program and also available for download in electronic

Chapter 15: Creditor - Debtor Relations and Bankruptcy

Chapter 15: Creditor - Debtor Relations and Bankruptcy Copyright 2009 South-Western Legal Studies in Business, a Copyright part of South-Western 2009 South-Western Cengage Legal Learning. Studies Business,

Chapter 15: Creditor - Debtor Relations and Bankruptcy Copyright 2009 South-Western Legal Studies in Business, a Copyright part of South-Western 2009 South-Western Cengage Legal Learning. Studies Business,

Correcting Depreciation Form 3115 Line-By-Line. ihmlisa

Form 3115 Line-By-Line ihmlisa This text has been prepared with due diligence. However, the possibility of mechanical or human error does exist and the author accepts no responsibility or liability regarding

Form 3115 Line-By-Line ihmlisa This text has been prepared with due diligence. However, the possibility of mechanical or human error does exist and the author accepts no responsibility or liability regarding

Traps for the Unwary Chapter 7 Bankruptcy Attorney

Traps for the Unwary Chapter 7 Bankruptcy Attorney MSBA Consumer Bankruptcy Section Presented 1/24/18 Michael G. Wolff, Esquire Chapter 7 Trustee Definition Unwary Not cautious, not aware of possible dangers

Traps for the Unwary Chapter 7 Bankruptcy Attorney MSBA Consumer Bankruptcy Section Presented 1/24/18 Michael G. Wolff, Esquire Chapter 7 Trustee Definition Unwary Not cautious, not aware of possible dangers

Bankruptcy BASICS. APRIL 2006 Revised Third Edition. Bankruptcy Judges Division. Administrative Office of the United States Courts

Bankruptcy BASICS (Applicable to Cases Filed on or After October 17, 2005) Bankruptcy Judges Division Administrative Office of the United States Courts APRIL 2006 Revised Third Edition Bankruptcy Basics

Bankruptcy BASICS (Applicable to Cases Filed on or After October 17, 2005) Bankruptcy Judges Division Administrative Office of the United States Courts APRIL 2006 Revised Third Edition Bankruptcy Basics

Analyzing benefits and risks of filing Chapter 7 bankruptcy

Analyzing benefits and risks of filing Chapter 7 bankruptcy Successful bankruptcy provides a fresh start for the honest but unfortunate debtor Chapter 7 discharge is only available once every 8 years.

Analyzing benefits and risks of filing Chapter 7 bankruptcy Successful bankruptcy provides a fresh start for the honest but unfortunate debtor Chapter 7 discharge is only available once every 8 years.

UNDERSTANDING AND PREPARING FOR BANKRUPTCY. Lewis & Jurnovoy P.A.

UNDERSTANDING AND PREPARING FOR BANKRUPTCY Lewis & Jurnovoy P.A. WARNING SIGNS If you are in financial trouble, you are not alone. At Lewis & Jurnovoy, P.A. we ve helped thousands of people just like you

UNDERSTANDING AND PREPARING FOR BANKRUPTCY Lewis & Jurnovoy P.A. WARNING SIGNS If you are in financial trouble, you are not alone. At Lewis & Jurnovoy, P.A. we ve helped thousands of people just like you

BANKRUPTCY. Freephone. FACTSHEET 10 (2018)

") What is Bankruptcy? Freephone 0800 083 8018 1 FACTSHEET 10 (2018) Bankruptcy is a way of dealing with debts that you cannot pay. Whilst you are bankrupt any assets that you have might be used to pay off

What is Bankruptcy? Freephone 0800 083 8018 1 FACTSHEET 10 (2018) Bankruptcy is a way of dealing with debts that you cannot pay. Whilst you are bankrupt any assets that you have might be used to pay off

Discharge of Unfiled Taxes under the Bankruptcy Abuse Prevention and Protection Act of 2005 (BAPCPA). No More Super Discharge?

. No More Super Discharge?") Discharge of Unfiled Taxes under the Bankruptcy Abuse Prevention and Protection Act of 2005 (BAPCPA). No More Super Discharge? Written by: Stephen B. Kass Law Offices of Stephen B. Kass, P.C.; New York

Discharge of Unfiled Taxes under the Bankruptcy Abuse Prevention and Protection Act of 2005 (BAPCPA). No More Super Discharge? Written by: Stephen B. Kass Law Offices of Stephen B. Kass, P.C.; New York

C H A P T E R O N E. Nature of Bankruptcy & Insolvency Proceedings

c01.fm Page 1 Thursday, February 16, 2006 10:45 AM C H A P T E R O N E 1 Nature of Bankruptcy & Insolvency Proceedings 1.1 OBJECTIVES 1 (a) Introduction 1 1.2 ALTERNATIVES AVAILABLE TO A FINANCIALLY TROU-

c01.fm Page 1 Thursday, February 16, 2006 10:45 AM C H A P T E R O N E 1 Nature of Bankruptcy & Insolvency Proceedings 1.1 OBJECTIVES 1 (a) Introduction 1 1.2 ALTERNATIVES AVAILABLE TO A FINANCIALLY TROU-

What Does It Mean To File For Personal Bankruptcy?

Thank you for contacting our office to ask about personal bankruptcy. The following are some answers to many of the questions people have about the process of bankruptcy. Bankruptcy is complex and the

Thank you for contacting our office to ask about personal bankruptcy. The following are some answers to many of the questions people have about the process of bankruptcy. Bankruptcy is complex and the

Welcome to today s webinar! Basic Bankruptcy Victor A. Davis February 21, 2019

Welcome to today s webinar! Basic Bankruptcy Victor A. Davis February 21, 2019 In order to obtain a CE Certificate or CLE Credit, you must listen to the webinar for a minimum of 55 minutes obtain the password

Welcome to today s webinar! Basic Bankruptcy Victor A. Davis February 21, 2019 In order to obtain a CE Certificate or CLE Credit, you must listen to the webinar for a minimum of 55 minutes obtain the password

Frequently Asked Questions for Chapter 13 Bankruptcy

Frequently Asked Questions for Chapter 13 Bankruptcy What is going to happen now that I have filed a Chapter 13 bankruptcy? Since you have just filed a Chapter 13 Bankruptcy, you probably have a lot of

Frequently Asked Questions for Chapter 13 Bankruptcy What is going to happen now that I have filed a Chapter 13 bankruptcy? Since you have just filed a Chapter 13 Bankruptcy, you probably have a lot of

UNITED STATES BANKRUPTCY COURT DISTRICT OF NEVADA CHAPTER 13 PLAN

NVB#113 (rev. 12/17) UNITED STATES BANKRUPTCY COURT DISTRICT OF NEVADA In re: BK - Debtor 1 - Chapter 13 Plan # Debtor 2 - Debtor. Confirmation Hearing Date: Confirmation Hearing Time: CHAPTER 13 PLAN

NVB#113 (rev. 12/17) UNITED STATES BANKRUPTCY COURT DISTRICT OF NEVADA In re: BK - Debtor 1 - Chapter 13 Plan # Debtor 2 - Debtor. Confirmation Hearing Date: Confirmation Hearing Time: CHAPTER 13 PLAN

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13. Name: Case Number:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 YOUR TRUSTEE S NAME, ADDRESS, AND TELEPHONE NUMBER: ADAM M. GOODMAN STANDING CHAPTER 13 TRUSTEE 260 PEACHTREE STREET N.W. SUITE 200 ATLANTA, GEORGIA 30303 Telephone:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 YOUR TRUSTEE S NAME, ADDRESS, AND TELEPHONE NUMBER: ADAM M. GOODMAN STANDING CHAPTER 13 TRUSTEE 260 PEACHTREE STREET N.W. SUITE 200 ATLANTA, GEORGIA 30303 Telephone:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 CASE

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 CASE THIS BOOKLET CONTAINS ANSWERS TO MOST OF THE QUESTIONS YOU WILL HAVE WHILE UN- DER CHAPTER 13. READ IT COMPLETELY WHEN YOU BEGIN YOUR CASE AND REFER TO IT

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 CASE THIS BOOKLET CONTAINS ANSWERS TO MOST OF THE QUESTIONS YOU WILL HAVE WHILE UN- DER CHAPTER 13. READ IT COMPLETELY WHEN YOU BEGIN YOUR CASE AND REFER TO IT

Bankruptcy Toolkit for General Practitioners SOURCES OF BANKRUPTCY LAW. 3/12/2012. March 14, 2012

Bankruptcy Toolkit for General Practitioners March 14, 2012 Gloria Z. Nagler William F. Malaier, Jr. Nagler & Associates www.naglerlaw.com SOURCES OF BANKRUPTCY LAW The Bankruptcy Code - Title 11 of the

Bankruptcy Toolkit for General Practitioners March 14, 2012 Gloria Z. Nagler William F. Malaier, Jr. Nagler & Associates www.naglerlaw.com SOURCES OF BANKRUPTCY LAW The Bankruptcy Code - Title 11 of the

Black and Buono P.C. DEBTOR S QUESTIONNAIRE

Black and Buono P.C. DEBTOR S QUESTIONNAIRE 1. Have you ever filed, or had filed against you, any type of Petition under any of the bankruptcy laws of the United States? No Yes 1A. Please complete Schedule

Black and Buono P.C. DEBTOR S QUESTIONNAIRE 1. Have you ever filed, or had filed against you, any type of Petition under any of the bankruptcy laws of the United States? No Yes 1A. Please complete Schedule

Bankruptcy BASICS (Applicable to Cases Filed on or After October 17, 2005)

") Bankruptcy BASICS (Applicable to Cases Filed on or After October 17, 2005) Leonidas Ralph Mecham, Director Administrative Office of the United States Courts Bankruptcy BASICS (Applicable to Cases Filed

Bankruptcy BASICS (Applicable to Cases Filed on or After October 17, 2005) Leonidas Ralph Mecham, Director Administrative Office of the United States Courts Bankruptcy BASICS (Applicable to Cases Filed

Bankruptcy Consultation Agreement

Bankruptcy Consultation Agreement 1. Bankruptcy Telephone Consultation Agreement (signature required) 2. Notice Pursuant to 11 USC Section 342(b) (information only) 3. Notice Pursuant to 11 USC Section

Bankruptcy Consultation Agreement 1. Bankruptcy Telephone Consultation Agreement (signature required) 2. Notice Pursuant to 11 USC Section 342(b) (information only) 3. Notice Pursuant to 11 USC Section

11/3/2011. Debt & Taxes

Debt & Taxes Elizabeth A. Maresca Clinical Associate Professor Fordham Law School, New York, NY Tax & Consumer Litigation Clinic I. General Rules: Income from discharge of indebtedness, exemptions and

Debt & Taxes Elizabeth A. Maresca Clinical Associate Professor Fordham Law School, New York, NY Tax & Consumer Litigation Clinic I. General Rules: Income from discharge of indebtedness, exemptions and

STANLEY J. KARTCHNER, CHAPTER 7 TRUSTEE

STANLEY J. KARTCHNER, CHAPTER 7 TRUSTEE EMAIL: trustee@aztrustee.com 7090 N ORACLE ROAD #178-204, TUCSON, AZ 85704 TEL (520) 742-1210 ONLINE: aztrustee.com (Date) To: (Name(s)) la version en español de

STANLEY J. KARTCHNER, CHAPTER 7 TRUSTEE EMAIL: trustee@aztrustee.com 7090 N ORACLE ROAD #178-204, TUCSON, AZ 85704 TEL (520) 742-1210 ONLINE: aztrustee.com (Date) To: (Name(s)) la version en español de

Bankruptcy. By Mrs. Lauer

Bankruptcy By Mrs. Lauer Objectives Consider the advantages of disadvantages of declaring bankruptcy. List types of debts that are discharged in bankruptcy. Distinguish between straight bankruptcy and

Bankruptcy By Mrs. Lauer Objectives Consider the advantages of disadvantages of declaring bankruptcy. List types of debts that are discharged in bankruptcy. Distinguish between straight bankruptcy and

Questions and Answers About Farm Debt

Revised October 2003 Agdex 817-14 Questions and Answers About Farm Debt This factsheet addresses some of the common, and some not-so-common, questions asked by farmers about the legal implications of debt.

Revised October 2003 Agdex 817-14 Questions and Answers About Farm Debt This factsheet addresses some of the common, and some not-so-common, questions asked by farmers about the legal implications of debt.

In Debt? Presented by: Together, we do the community justice.

In Debt? Presented by: Together, we do the community justice. HOW CAN SOMEONE COLLECT A DEBT FROM YOU? People can collect money from you only if they follow the law. The law permits people to collect a

In Debt? Presented by: Together, we do the community justice. HOW CAN SOMEONE COLLECT A DEBT FROM YOU? People can collect money from you only if they follow the law. The law permits people to collect a

Bankruptcy 101 CAPT HELEN RICKEY

Bankruptcy 101 CAPT HELEN RICKEY 21 SW/JA, PETERSON AFB, CO 27 OCTOBER 2016 UNCLASSIFIED Overview Federal Court Debtors Schedules Chapter 7 Chapter 13 Chapter 11 Creditors 1 United States Bankruptcy Court

Bankruptcy 101 CAPT HELEN RICKEY 21 SW/JA, PETERSON AFB, CO 27 OCTOBER 2016 UNCLASSIFIED Overview Federal Court Debtors Schedules Chapter 7 Chapter 13 Chapter 11 Creditors 1 United States Bankruptcy Court

RIGHTS AND RESPONSIBILITIES AGREEMENT BETWEEN CHAPTER 13 DEBTORS AND THEIR ATTORNEYS (Model Retention Agreement)

") 02/03/04 rev. UNITED STATES BANKRUPTCY COURT NORTHERN DISTRICT OF ILLINOIS In re: Case No. Judge: RIGHTS AND RESPONSIBILITIES AGREEMENT BETWEEN CHAPTER 13 DEBTORS AND THEIR ATTORNEYS (Model Retention Agreement)

02/03/04 rev. UNITED STATES BANKRUPTCY COURT NORTHERN DISTRICT OF ILLINOIS In re: Case No. Judge: RIGHTS AND RESPONSIBILITIES AGREEMENT BETWEEN CHAPTER 13 DEBTORS AND THEIR ATTORNEYS (Model Retention Agreement)

P. J. FRANKLIN ATTORNEY AT LAW

P. J. FRANKLIN ATTORNEY AT LAW 7322 S. W. FREEWAY STE. 700 HOUSTON, TX 77074 Telephone: (713) 414-3066 Fax: (713) 414-3067 E-Mail: pjf@pjfranklin.com Website:www.pjfranklin.com BANKRUPTCY QUESTIONAIRE

P. J. FRANKLIN ATTORNEY AT LAW 7322 S. W. FREEWAY STE. 700 HOUSTON, TX 77074 Telephone: (713) 414-3066 Fax: (713) 414-3067 E-Mail: pjf@pjfranklin.com Website:www.pjfranklin.com BANKRUPTCY QUESTIONAIRE

ANNOTATED VERSION of Chapter 13 Plan Form effective 2/1/2014

ANNOTATED VERSION of Chapter 13 Plan Form effective 2/1/2014 Pursuant to Local Rule 3015(a) the Chapter 13 Trustees have issued a form Chapter 13 Plan. As of 2/1/2014 a new plan is in effect. Attached

ANNOTATED VERSION of Chapter 13 Plan Form effective 2/1/2014 Pursuant to Local Rule 3015(a) the Chapter 13 Trustees have issued a form Chapter 13 Plan. As of 2/1/2014 a new plan is in effect. Attached

Tax Issues in Foreclosure Cases

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

A Bankruptcy proceeding is the procedure whereby a debtor seeks relief from creditors. There are several areas of concern relating to bankruptcy:

BANKRUPTCY A proceeding is the procedure whereby a debtor seeks relief from creditors. There are several areas of concern relating to bankruptcy: Automatic stay As soon as a bankruptcy petition is filed,

BANKRUPTCY A proceeding is the procedure whereby a debtor seeks relief from creditors. There are several areas of concern relating to bankruptcy: Automatic stay As soon as a bankruptcy petition is filed,

Information & Instructions: Demand letter opportunity to cure and intent to accelerate the note

Information & Instructions: Demand letter opportunity to cure and intent to accelerate the note 1. The demand letter in the form that follows is used to advise the debtor that he or she is delinquent in

Information & Instructions: Demand letter opportunity to cure and intent to accelerate the note 1. The demand letter in the form that follows is used to advise the debtor that he or she is delinquent in

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 CASE

A MESSAGE FROM THE CHAPTER 13 STAFF The Chapter 13 staff understands that making the decision to file bankruptcy was not easy. Some of the many factors which cause people to file bankruptcy include loss

A MESSAGE FROM THE CHAPTER 13 STAFF The Chapter 13 staff understands that making the decision to file bankruptcy was not easy. Some of the many factors which cause people to file bankruptcy include loss

lesson nine in trouble overheads

lesson nine in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson nine in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

Bankruptcy: What You Need to Know in Maryland

Bankruptcy Bankruptcy: What You Need to Know in Maryland Equal Access to Justice: Legal Aid Equal Justice for Maryland Since 1911 Legal Aid: Who We Are This brochure was prepared by the Maryland Legal

Bankruptcy Bankruptcy: What You Need to Know in Maryland Equal Access to Justice: Legal Aid Equal Justice for Maryland Since 1911 Legal Aid: Who We Are This brochure was prepared by the Maryland Legal

E. Michael Vereen, III Consultation Form Phone Fax APPLICANT INFORMATION

E. Michael Vereen, III Consultation Form Phone 770-345-9449 Fax 770-345-9425 Email mvparalegal@vereenlaw.com vereenlaw@live.com Need to file your case TODAY? Here is what you will need: 1. Paystubs for

E. Michael Vereen, III Consultation Form Phone 770-345-9449 Fax 770-345-9425 Email mvparalegal@vereenlaw.com vereenlaw@live.com Need to file your case TODAY? Here is what you will need: 1. Paystubs for

NFCC Certification Book 6 BANKRUPTCY

NFCC Certification Book 6 BANKRUPTCY This document remains the sole property of the National Foundation for Credit Counseling (NFCC). By accepting this document and participating in the NFCC Certification

NFCC Certification Book 6 BANKRUPTCY This document remains the sole property of the National Foundation for Credit Counseling (NFCC). By accepting this document and participating in the NFCC Certification

CAMPBELL LAW FIRM, P.A. CLIENT INFORMATION SHEET

CAMPBELL LAW FIRM, P.A. CLIENT INFORMATION SHEET Please provide us with the following information to help us serve you better (please print). Name: Social Security Number: Date: DOB: Address: City, State,

CAMPBELL LAW FIRM, P.A. CLIENT INFORMATION SHEET Please provide us with the following information to help us serve you better (please print). Name: Social Security Number: Date: DOB: Address: City, State,

UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION. // Filed: CHAPTER 13 PLAN

In Re: Debtor(s). UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION Case #: Chapter 13 Hon. // Filed: CHAPTER 13 PLAN ( )Original or ( )Amendment No.: ( )Pre-Confirmation

In Re: Debtor(s). UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION Case #: Chapter 13 Hon. // Filed: CHAPTER 13 PLAN ( )Original or ( )Amendment No.: ( )Pre-Confirmation

V. Bankruptcy Concepts

V. Bankruptcy Concepts Familiarity with several fundamental bankruptcy concepts and a bit of bankruptcy terminology is helpful in analyzing the bankruptcy issues that most frequently confront state courts.

V. Bankruptcy Concepts Familiarity with several fundamental bankruptcy concepts and a bit of bankruptcy terminology is helpful in analyzing the bankruptcy issues that most frequently confront state courts.

WOLFE LAW FIRM 200 Kerens Avenue Elkins, WV Phone: (304) Fax: (304)

Fax: (304)") WOLFE LAW FIRM 200 Kerens Avenue Elkins, WV 26241 Phone: (304) 637-5755 Fax: (304) 637-1001 E-mail: wolfelaw@thewolfelaw.com BANKRUPTCY QUESTIONNAIRE WE ARE A LAW FIRM PROVIDING DEBT RELIEF SERVICE TO

WOLFE LAW FIRM 200 Kerens Avenue Elkins, WV 26241 Phone: (304) 637-5755 Fax: (304) 637-1001 E-mail: wolfelaw@thewolfelaw.com BANKRUPTCY QUESTIONNAIRE WE ARE A LAW FIRM PROVIDING DEBT RELIEF SERVICE TO

FORM CHANGES EFFECTIVE 12/1/15 OUTLINE

FORM CHANGES EFFECTIVE 12/1/15 OUTLINE Prepared by Mary Viegelahn, Chapter 13 Standing Trustee, San Antonio, TX Effective 12/1/15 all but 6 official forms were replaced. A complete explanation of the changes

FORM CHANGES EFFECTIVE 12/1/15 OUTLINE Prepared by Mary Viegelahn, Chapter 13 Standing Trustee, San Antonio, TX Effective 12/1/15 all but 6 official forms were replaced. A complete explanation of the changes

10 Busted Bankruptcy Myths

10 Busted Bankruptcy Myths Malissa L. Walden MLWalden@WPLawPractice.com Cassie Pfannenstiel Rodriguez CPR@WPLawPractice.com Walden & Pfannenstiel, LLC 11900 W 87 th St Pkwy Ste 125 Lenexa, KS 66215 913-438-1112

10 Busted Bankruptcy Myths Malissa L. Walden MLWalden@WPLawPractice.com Cassie Pfannenstiel Rodriguez CPR@WPLawPractice.com Walden & Pfannenstiel, LLC 11900 W 87 th St Pkwy Ste 125 Lenexa, KS 66215 913-438-1112

Co-Debtor [Questionnaire Answers Under Oath]:

![Co-Debtor [Questionnaire Answers Under Oath]:](/thumbs/81/82962869.jpg "Co-Debtor [Questionnaire Answers Under Oath]:") 2015 Chapter 7 Trustee Debtor Questionnaire BRUCE E STRAUSS, CHAPTER 7 TRUSTEE ( Trustee@merrickbakerstrausscom) I have been appointed as your bankruptcy trustee Part of my duties as the Chapter 7 Trustee

2015 Chapter 7 Trustee Debtor Questionnaire BRUCE E STRAUSS, CHAPTER 7 TRUSTEE ( Trustee@merrickbakerstrausscom) I have been appointed as your bankruptcy trustee Part of my duties as the Chapter 7 Trustee

Basic Debtor Creditor Terminology

Basic Debtor Creditor Terminology Debtor: person who owes the money Creditor: person to whom the money is owed To qualify as a debt, it must be: Certain (i.e., not contingent on some future event) Liquidated

Basic Debtor Creditor Terminology Debtor: person who owes the money Creditor: person to whom the money is owed To qualify as a debt, it must be: Certain (i.e., not contingent on some future event) Liquidated

Wallace & Karson Law Office, PLLC

, 1618 W Second Ave, Spokane, WA 99202 (509) 326-3600 www.wallaceandkarsonlaw.com Licensed in Washington and Idaho The first step in the bankruptcy process is to fill out this packet and the creditor history

, 1618 W Second Ave, Spokane, WA 99202 (509) 326-3600 www.wallaceandkarsonlaw.com Licensed in Washington and Idaho The first step in the bankruptcy process is to fill out this packet and the creditor history

25.49%. This APR will vary with the market based on the Prime Rate.

CAPITAL ONE IMPORTANT DISCLOSURES Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 25.49%. This APR will vary with the market based on the Prime Rate. How To Avoid Paying

CAPITAL ONE IMPORTANT DISCLOSURES Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 25.49%. This APR will vary with the market based on the Prime Rate. How To Avoid Paying

An Attorney s Options for Handling Clients in Trouble with Real Estate. Aka: Forbearance to Bankruptcy and Everything in Between

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

SUMMARY PLAN DESCRIPTION FOR. Florida Tech Retirement Plan

SUMMARY PLAN DESCRIPTION FOR 1-1-2018 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

SUMMARY PLAN DESCRIPTION FOR 1-1-2018 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

CREDIT COUNSELING REQUIREMENT

CREDIT COUNSELING REQUIREMENT In order to file bankruptcy, an individual must receive from an approved nonprofit budget and credit counseling agency... an individual or group briefing... that outlines

CREDIT COUNSELING REQUIREMENT In order to file bankruptcy, an individual must receive from an approved nonprofit budget and credit counseling agency... an individual or group briefing... that outlines

SUMMARY OF BANKRUPTCY TITLE STANDARDS

TITLE STANDARDS SUMMARY OF BANKRUPTCY TITLE STANDARDS Materials By: Heather Wagner The Wagner Law Firm, LLC Roswell, Georgia Presented By: Heather D. Brown Brown Law, LLC Roswell, Georgia 169306 1 of

TITLE STANDARDS SUMMARY OF BANKRUPTCY TITLE STANDARDS Materials By: Heather Wagner The Wagner Law Firm, LLC Roswell, Georgia Presented By: Heather D. Brown Brown Law, LLC Roswell, Georgia 169306 1 of

EXCEL PARTNERS, INC. 401(k) PLAN SUMMARY PLAN DESCRIPTION

PLAN SUMMARY PLAN DESCRIPTION") EXCEL PARTNERS, INC. 401(k) PLAN SUMMARY PLAN DESCRIPTION 2015 A. General Information About the Plan TABLE OF CONTENTS B. Participation in the Plan Q & A 1 How do I become eligible to become a member of

EXCEL PARTNERS, INC. 401(k) PLAN SUMMARY PLAN DESCRIPTION 2015 A. General Information About the Plan TABLE OF CONTENTS B. Participation in the Plan Q & A 1 How do I become eligible to become a member of

Summary of Bankruptcy Reform Conference Report

Summary of Bankruptcy Reform Conference Report On the evening of Thursday, July 25, 2002, Senate and House conferees reached consensus on the final issue in disagreement between their respective versions

Summary of Bankruptcy Reform Conference Report On the evening of Thursday, July 25, 2002, Senate and House conferees reached consensus on the final issue in disagreement between their respective versions

CHAPTER 13 BANKRUPTCY IN THE EASTERN DISTRICT OF KENTUCKY

CHAPTER 13 BANKRUPTCY IN THE EASTERN DISTRICT OF KENTUCKY [PHOTO] THE DEBTOR S CHAPTER 13 HANDBOOK A Publication of the Chapter 13 Trustee for the Eastern District of Kentucky 2018 Beverly M. Burden, Trustee

CHAPTER 13 BANKRUPTCY IN THE EASTERN DISTRICT OF KENTUCKY [PHOTO] THE DEBTOR S CHAPTER 13 HANDBOOK A Publication of the Chapter 13 Trustee for the Eastern District of Kentucky 2018 Beverly M. Burden, Trustee

Loan Enforcement Improving the Odds of Recovery. By Michael A. Campbell Polsinelli Shughart PC

Loan Enforcement Improving the Odds of Recovery By Michael A. Campbell Polsinelli Shughart PC Copyright 2009 Contents 1. Good Underwriting 2. Speed and its Effect on Recoveries 3. Pre-Enforcement Asset

Loan Enforcement Improving the Odds of Recovery By Michael A. Campbell Polsinelli Shughart PC Copyright 2009 Contents 1. Good Underwriting 2. Speed and its Effect on Recoveries 3. Pre-Enforcement Asset

Florida Foreclosure Law E-Book

Florida Foreclosure Law E-Book Simple Guide to Florida Foreclosure Law by: florida Law Advisers, P.A. 1 Table Of Contents INTRODUCTION.... 3 FIGHTING THE FORECLOSURE OF YOUR HOME.... 3 PREDATORY LENDING.....

Florida Foreclosure Law E-Book Simple Guide to Florida Foreclosure Law by: florida Law Advisers, P.A. 1 Table Of Contents INTRODUCTION.... 3 FIGHTING THE FORECLOSURE OF YOUR HOME.... 3 PREDATORY LENDING.....

Early Delinquency Intervention

Early Delinquency Intervention Saving Your Home From Foreclosure There are many reasons homeowners face difficulty in making mortgage payments: unexpected expenses, loss of overtime, unemployment, overspending,

Early Delinquency Intervention Saving Your Home From Foreclosure There are many reasons homeowners face difficulty in making mortgage payments: unexpected expenses, loss of overtime, unemployment, overspending,

Personal Glossary of Terms

Annual Report Insolvency practitioners are obliged to produce regular reports detailing their actions, including an account of what money they have received from insolvent companies and individuals and

Annual Report Insolvency practitioners are obliged to produce regular reports detailing their actions, including an account of what money they have received from insolvent companies and individuals and

/ BANKRUPTCY INFORMATION FORM As non-lawyer bankruptcy petition preparers, we are not legally permitted to give you any advice or assistance in filling out these forms. We are only permitted to type the

/ BANKRUPTCY INFORMATION FORM As non-lawyer bankruptcy petition preparers, we are not legally permitted to give you any advice or assistance in filling out these forms. We are only permitted to type the

Frequently Asked Questions

Frequently Asked Questions 1. What is the difference between a professional collection service and a creditor collecting on its own behalf? Sometimes consumers confuse third-party collectors with the in-house

Frequently Asked Questions 1. What is the difference between a professional collection service and a creditor collecting on its own behalf? Sometimes consumers confuse third-party collectors with the in-house

EXHIBIT 7 1 Flow Chart for Chapter 12

EXHIBIT 7 1 Flow Chart for Chapter 12 The Filing of the Chapter 12 Petition The debtor files with the bankruptcy court clerk s office: 1. Filing fee and administrative fee 2. Voluntary petition (Official

EXHIBIT 7 1 Flow Chart for Chapter 12 The Filing of the Chapter 12 Petition The debtor files with the bankruptcy court clerk s office: 1. Filing fee and administrative fee 2. Voluntary petition (Official

2018 Publication 4012, VITA/TCE Resource Guide

2018 Publication 4012, VITA/TCE Resource Guide Publication 4012 B-4 In the second text box, in the left margin of the page, change Line 21 to: B-7A Schedule 1 Make a pen/ink change in Publication 4012.

2018 Publication 4012, VITA/TCE Resource Guide Publication 4012 B-4 In the second text box, in the left margin of the page, change Line 21 to: B-7A Schedule 1 Make a pen/ink change in Publication 4012.

Name Social Security#: Spouse: Social Security#: Address: City/State: Zip: Alternate mailing address: Home Phone: ( ) Work Phone: ( ) Cell: ( )

Work Phone: ( ) Cell: ( )") DEBTOR QUESTIONNAIRE You may print this out and bring it with you to the appointment. Please Answer these questions to the best of your information and belief. Short and general answers are sufficient.

DEBTOR QUESTIONNAIRE You may print this out and bring it with you to the appointment. Please Answer these questions to the best of your information and belief. Short and general answers are sufficient.

One-Way Buy-Sell Agreement

One Resource Group 13548 Zubrick Road Roanoke, IN 46783 888-467-6755 Life_Sales@ORGCorp.com One-Way Buy-Sell Agreement Page 1 of 8, see disclaimer on final page One-Way Buy-Sell Agreement What is it? Legal