Additional Praise For Basic Accounting Simplified

|

|

|

- Jonathan Summers

- 6 years ago

- Views:

Transcription

1

2 Additional Praise For Basic Accounting Simplified A strongly recommended pick for anyone who is pursuing accounting as his or her career of choice. Midwest Book Review, Small Press Bookwatch, Education Shelf The author s presentation is ingenious - and very effective. Sidney Kess, CPA, JD, LLM, nationally renowned tax expert and lecturer With its fresh approach, clear language, memory aids, and visual illustrations, Basic Accounting Simplified makes the basics of accounting easy to understand. Peter Gulia, Fiduciary Guidance Counsel, Philadelphia, PA Why struggle with accounting concepts? This is the first book to explain a practical system in a readily understood manner. Lester J. Mantell, CPA, JD, LLM, New York, NY They say that one picture is worth a thousand words and this book is yet further proof of that statement. The charts and diagrams are extremely well done, and make a complicated subject easy to understand. Mac Brown, President, Doctors Financial Management Group, Orlando, FL A straightforward, step-by-step process makes difficult concepts very easy to understand. Richard Epstein, CPA, New York, NY It s nicely laid out, tightly written, and makes sense from start to finish. Gordon Burgett, author of Niche Publishing, Novato, CA A great overview. By simplifying complex concepts, like subsidiary ledgers and the general ledger, you will be able to more easily think through, understand, and master the more difficult issues that will be taught as your accounting education progresses. Sam D. Arkind, Former IRS Training Instructor, Brooklyn, NY a great supplementary teaching guide. Best used before the class begins, then looked at during class, and kept as a reference later. Bernard I. Rader, CPA, Freeport, NY Finally, there is a book on the market with an easy-to-grasp formula that can help bewildered students, confused bookkeepers, and anybody with his or her own business to understand the principles of accounting. Basic Accounting Simplified provides practical insight into the world of accounting. Bruce J. Temkin, author of The Terrible Truth About Investing

3 BASIC ACCOUNTING SIMPLIFIED Alvin L. Lesser, PA and Gary S. Lesser, JD

4 Copyright 2011 GSL Galactic Publishing. All Rights Reserved. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional services. If legal advice or other professional assistance is required, the services of a competent professional person should be sought. From a Declaration of Principles jointly adopted by a Committee of the American Bar Association and a Committee of Publishers and Associations GSL Galactic Publishing (317) No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage and retrieval system, without permission in writing from GSL Galactic Publishing. Requests for permission to reproduce content should be directed to Gary Lesser at qpsep@aol.com. Printed in the United States of America ISBN

5 About the Authors Alvin L. Lesser, PA., practiced public accounting in New York for over 35 years. He was also a licensed real estate broker and commercial property developer. After serving in the military, Alvin received his B.A. in Accounting from New York University. Before computers came into popular usage, Alvin developed a method that substantially shortened the time to complete a set of books. Gary S. Lesser, JD, is a nationally known author, educator, and speaker. He is also the technical editor and co-author of Aspen Publishers' Health Savings Account Answer Book, Roth IRA Answer Book, 457 Answer Book, and Quick Reference to IRAs. Gary is also the principal author and technical editor of The CPA's Guide to Retirement Plans for Small Businesses and other publications of the American Institute of Certified Public Accountants (AICPA). Gary graduated from New York Law School and received his B.A. in accounting from Fairleigh Dickinson University. He is admitted to the bars of the state of New York and the United States Tax Court.

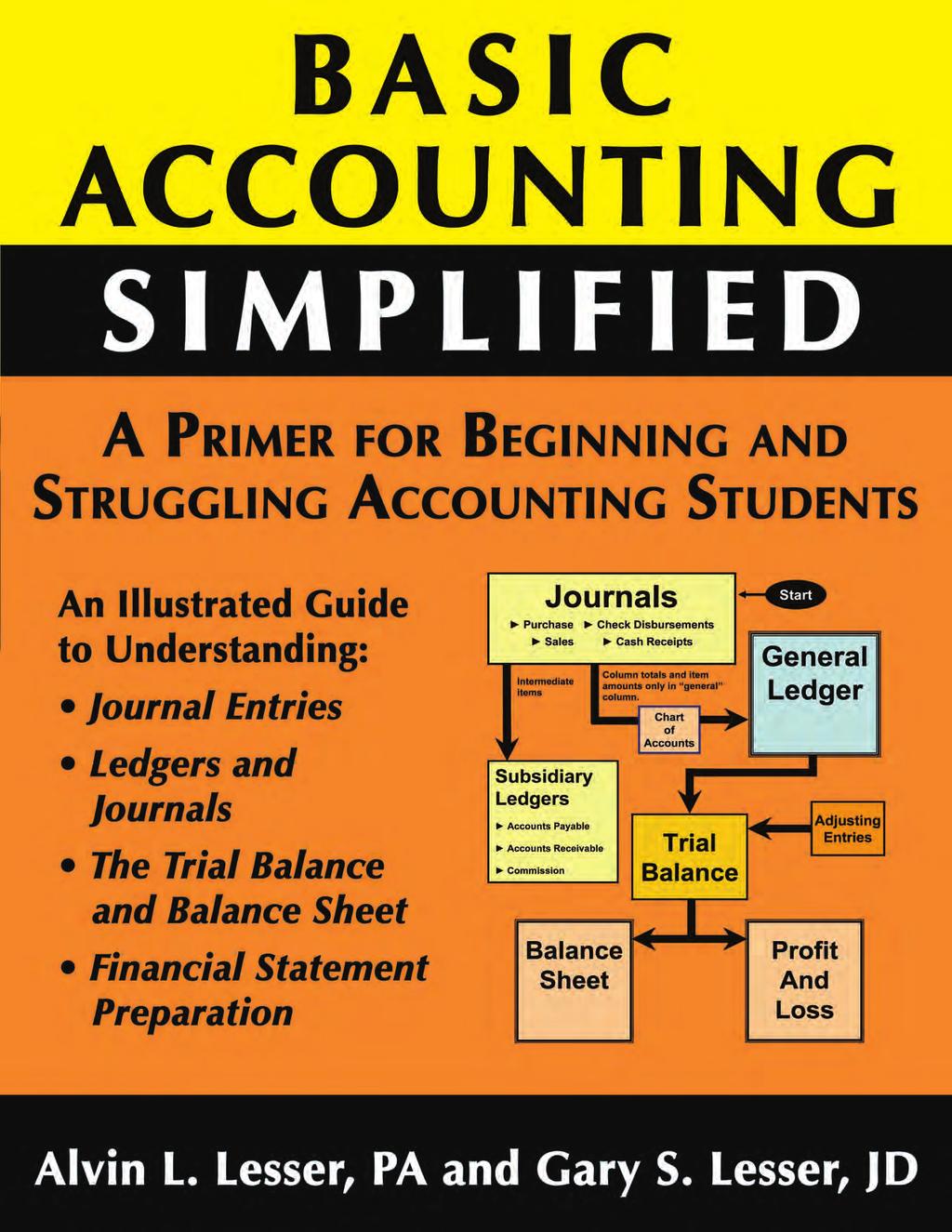

6 Introduction When the basics are understood, the more advanced aspects of accounting are easier to understand. By simplifying complex concepts, Basic Accounting Simplified helps students of accounting to think through, understand, and master the more difficult issues that will be taught as their accounting education progresses. Basic Accounting Simplified also provides a practical approach to solving problems. Straightforward instructions will guide the student through this process and will engage the student every step of the way. The objective of this book is to impart an in-depth understanding of the fundamentals of accounting to the beginning or struggling accounting student. It presents an easy-to-grasp technique that can be mastered in a short time. This book: Uses a unique teaching method that takes the stress out of learning the basics in order to make it easier to learn more complex accounting principles Explains journal entries and their relation to the trial balance Displays and explains the journals and ledgers and all postings Exhibits a full set of accounting books Covers the steps necessary to make financial statements Basic Accounting Simplified is the safety net every accounting student should have in order to be successful in this field.

7 Overview Chapter 1 The Method The basics of accounting, including the trial balance, are discussed and thoroughly explained in this chapter. Learning the basics of accounting The large scope of double-entry accounting Journal entries and how to make them Examples of journal entries Journal entries and posting to the Trial Balance A completed trial balance made by journal entry Chapter 2 Ledgers, Journals, and the Trial Balance The various books of account are discussed and explained in this chapter. The relationship between journals and ledgers and the trial balance are analyzed and examined in this chapter. The following ledgers and journals are included: The General Ledger The Subsidiary Ledgers The Check Disbursement Journal The Cash Receipts Journal The Purchase Journal and Accounts Payable Ledger The Sales Journal and Accounts Receivable Ledger The Commission Ledger and Petty Cash Book Chapter 3 Combining Journals and Ledgers The books of account will be combined and provide a thorough overview of accounting. Making postings, journals, and ledgers, are explained in this chapter. Chapter 4 Student Practice Session: Posting From Journals to Ledgers The student will complete the posting from completed journals to ledgers. The posting from the Check Disbursement Journal, the Cash Receipts Journal, the Purchase Journal, and the Sales Journal are examined in this chapter. Appendices

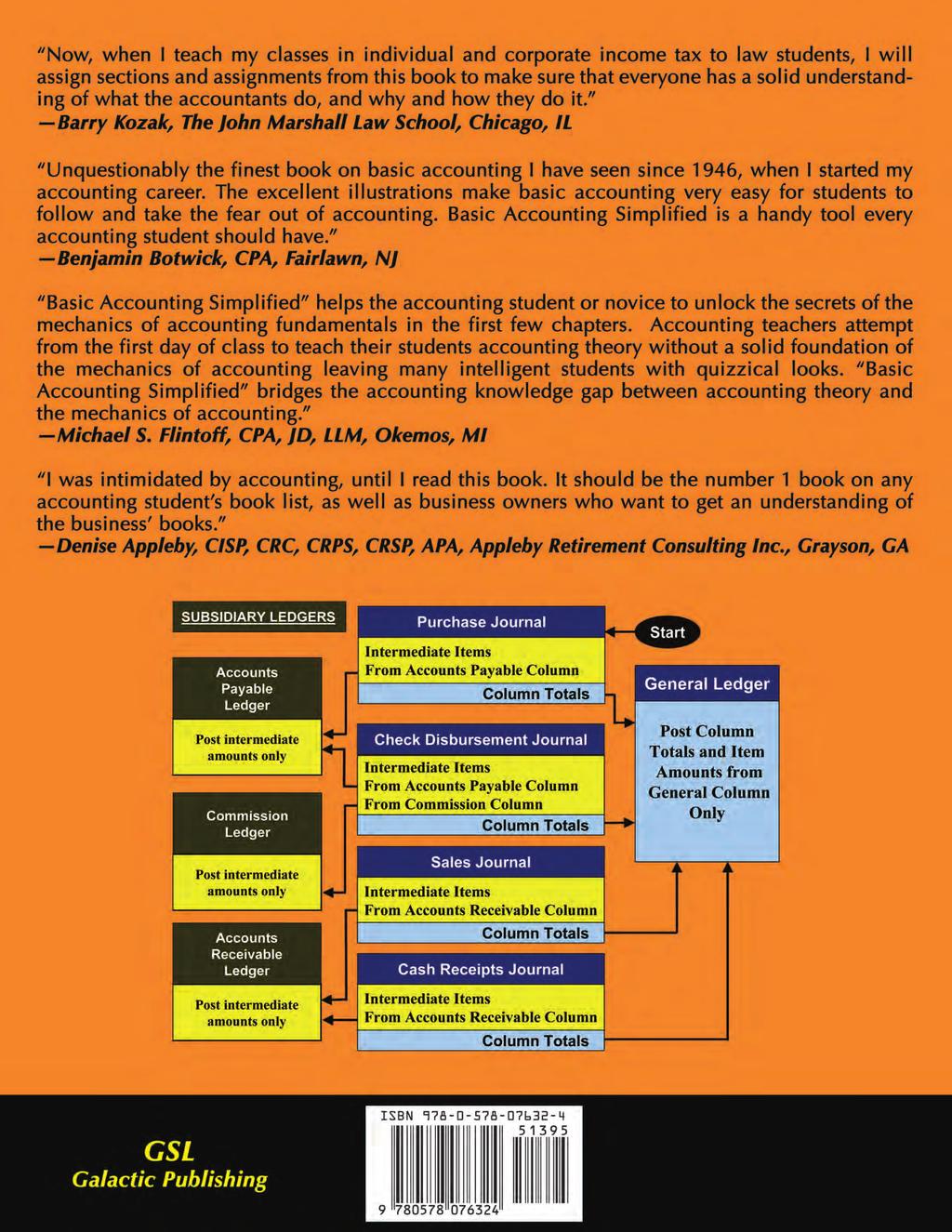

8 Chapter 1 Contents 1. Introduction Chapter Objective The Journal Entry The Trial Balance The Balance Sheet A. Assets B. Liabilities Profit and Loss Items Chart of Accounts The Wide Scope of Double-Entry Accounting Types of Journal Entries A. The Diagonal Journal Entry B. The Horizontal Journal Entry C. Section Summary Practice Questions Examples of Journal Entries and Posting to the Trial Balance Practice Journal Entries Calculating Profits or Loss Journal Entries versus Books of Accounts Chapter 2 1. Introduction A. General Ledger B. Chart of Accounts Subsidiary Ledgers A. Types of Subsidiary Ledgers B. Intermediate Items C. Location of Columns D. Accounting s Limitation E. Journal Entry Flow Chart F. Observations The Purchase Journal A. Function of the Subsidiary Ledger B. Observations The Check Disbursement Journal

9 5. Creating a Check Disbursement Journal from the Checking Account Student Exercise Bank Reconciliation Finding Errors The Cash Receipts Journal A. Summary B. Observations Purchase Journal and the Accounts Payable Ledger The Sales Journal and Accounts Receivable Ledger The Commission Ledger Establishing a Petty Cash Book Chapter 3 1. Introduction Student Practice Sessions A. The Check Disbursement Journal B. The Cash Receipts Journal C. The Purchase Journal and Accounts Payable Ledger D. The Sales Journal and Accounts Receivable Ledger Chapter 4 1. Introduction The Star Company General Ledger Preparing the Trial Balance Adjusting Entries Accrual Basis of Accounting Prepaid Expense Account Cash Basis of Accounting Deferrals Interim Financial Statements A. Balance Sheet B. Profit and Loss Statement Appendices

10 Chapter 1 The Method 1. Introduction Chapter Objective The Journal Entry The Trial Balance The Balance Sheet A. Assets B. Liabilities Profit and Loss Items Chart of Accounts The Wide Scope of Double-Entry Accounting Types of Journal Entries A. The Diagonal Journal Entry B. The Horizontal Journal Entry C. Section Summary Practice Questions Examples of Journal Entries and Posting to the Trial Balance Practice Journal Entries Calculating Profits or Loss Journal Entries versus Books of Accounts

11 The Method Introduction The practice or profession of accounting is more of a science than an art. The double-entry system of accounting provides assurance errors have not been made. Business transactions are recorded in journals in a well-defined manner. The recordation into the general ledger provides a pathway to the Trial Balance and ultimately to the Balance Sheet and Profit and Loss statement. This book employs a unique method of instruction in that it starts with the first phase of the accounting process, the journal entry, and skips to the last phase, the trial balance, completely omitting journals and ledgers. This will facilitate the understanding of journals and ledgers as they are later explained in Chapter 2. Slowly and gradually, a complete set of accounting books will be created. The steps involved in making a financial record of business transactions and in the preparation of statements concerning the Balance Sheet and income are fully discussed and explained. 2. Chapter Objective To learn the basics of accounting up to and including the trial balance. When the basics are understood, the more advanced aspects of accounting will be more easily understood. The following figure is an important illustration. It should be kept in mind now and throughout your accounting career (see also, Figure 1-3 located below in Section 5A). The following diagram is illustrative of one of the most basic concepts in accounting. Debits and credits can be good or bad for the business. Simply knowing whether an item is good or bad for the business and whether it is a balance sheet or profit and loss item can be used to determine whether the item is posted as a debit or credit. Balance Sheet Debit = Good For The Business Bad For The Business = Credit Debit = Bad For The Business Figure 1-1 Profit & Loss Good For The Business = Credit

12 Basic Accounting Simplified 1 2 The illustration shows that: A balance sheet item that is good for the business is a debit. A balance sheet item that is bad for the business is a credit. A profit and loss item that is good for the business is a credit. A profit and loss item that is bad for the business is a debit. 3. The Journal Entry A journal entry is the method used in accounting to record business transactions. The journal entry could be very simple by having just one debit and one credit. It could also have one debit and ten credits. It does not matter how many debits or credits a journal entry has, but the cardinal rule is the total of the debits must equal the total of the credits in every journal entry. All areas of accounting utilize journal entries. When information is recorded in any book of account it is done by journal entry, for example. When data is posted to the general ledger it is posted by journal entry When the numbers in the general ledger are netted, a journal entry is formed in the balance column When the netted amounts are placed on the trial balance it is a journal entry Helpful Tip. A debit is always on the left side and a credit is always on the right side. There is an r in credit and right. 4. The Trial Balance In the system of instruction ( The Method ) used in Chapter 1, all journal entries will be posted directly to the trial balance. In figure 1-2, below, in the first two columns following the Item column is an illustration of the Trial Balance to which all the journal entries that follow later in this chapter will be posted. The adjusting entries and the financial statements are made after the trial balance has been entered in those columns. Helpful Tip. As will be discussed later in this book, transactions are recorded using journal entries and the trial balance. At the end of each accounting period and after all the preparatory work has been done, the results are recorded in the general ledger. The net amounts contained in the general ledger are then recorded onto the trial balance.

13 The Method 1 3 For instructional purposes, all the journal entries in Chapter 1 will be posted directly to the trial balance. Journal entry items that affect the balance sheet are placed under the caption balance sheet items, and those that affect profit and loss are placed in that designated area on the trial balance. Since they are separated in name only, a journal entry that affects both the balance sheet and profit and loss are placed in their respective areas. Item Trial Balance Balance Sheet Items Debit Credit Adjusting Entries Debit Credit Balance Sheet Debit Credit Profit & Loss Items Profit & Loss Figure The Balance Sheet The balance sheet maintains a permanent, but ever changing record, of the financial matters that affect a business. It shows the financial position of a business at any specific moment in time. The balance sheet is comprised of assets (shown as debits) and liabilities (shown as credits). As shown in Figure 1-3, assets are represented by the word Good. All the good items a business possesses, such as money in the bank, accounts receivable, and so on, are assets and are good. The liabilities are the opposite and are represented by the word Bad. To put it simply good in the balance sheet minus bad equals the Owner s Equity which, as shown, is on the credit side, but nevertheless is shown as good. The reason it is shown as good is explained later. Examples of some of the items carried on the balance sheet are: Accounts Payable maintains a record of the total amount owed to the vendors when merchandise or services are purchased on credit. Accounts Receivable maintains a record of the total amount owed by purchasers when merchandise or services are sold on credit.

14 Basic Accounting Simplified 1 4 Inventory maintains a record of the relative value of the merchandise on hand at the beginning and at the end of the accounting period. Loans Payable maintains a record of who is owed money and how much is owed. Equipment maintains a record of trucks, cars, and other equipment owned by the Star Company. Petty Cash maintains a record of the cash available for reimbursement of miscellaneous expenditures made on behalf of the Star Company. Bank keeps a record of the amount of cash in the bank. Balance sheet items are those items that maintain a record as long as the business is in existence. The balance sheet items that exist at the end of an older accounting period also exist on the first day of the next (new) accounting period. A. Assets Assets are all the items in the possession of a business that are good for the business. Having more money in the bank, larger accounts receivable, more inventory and equipment, and so on, reflect a thriving business. All assets are debits and placed in the first quadrant of Figure 1-3. TRIAL BALANCE WITH QUADRANTS Debits Balance Sheet Credits GOOD Quadrant 1 BAD Quadrant 2 Assets Liabilities Owner s Equity Good Debits Profit & Loss Credits BAD Quadrant 3 GOOD Quadrant 4 Losses Profits Figure 1-3 B. Liabilities Liabilities are all the items in the possession of a business that are bad for the business. Being overdrawn at the bank, large accounts payable, too many loans and notes payable, etc., may be indications of a business in dire straits. Balance sheet items that are bad for the business are displayed as credits in the second quadrant of Figure 1-3.

15 The Method Profit and Loss Items Profit and loss items are the normal income and expense items associated with a business. At the end of the accounting period, the expenses are subtracted from sales and other income items and the profit or loss is determined. This profit or loss is transferred by journal entry to the owner s equity account (discussed in chapter 4). The closing entry is such that all the profit and loss items become zero at the beginning of the new accounting period. As the new accounting period progresses, the new income and expense amounts build up and, at the end of the new accounting period they are, once again, transferred to owner s equity. Thus, this process is repeated for each accounting period. Examples of items that appear in the balance sheet area or in the profit and loss area on the trial balance are shown in Table 1-1, below. Table 1-1. Balance Sheet and Profit and Loss Items Balance Sheet Items Accounts Payable Accounts Receivable Bank Deposits Equipment Furniture & Fixtures ( F&F ) Equipment Inventory Loans Payable Owner Equity Petty Cash Profit & Loss Items Advertising Auto Expense Commission Electric Food and Lodging Purchases Rent Sales Telephone Table 1-1 Note. Throughout the book there will be many references to the word account. When this word is used, reference is being made to one of the items listed in the chart of accounts shown in Section 7.

16 Basic Accounting Simplified Chart of Accounts The chart of accounts serves the same function in accounting as the table of contents found at the beginning of a book. The chart, provided by the accountant, provides the bookkeeper with the means of determining the accounts included in the general ledger and their page numbers within the general ledger. The chart of accounts for the Star Company, a small manufacturing business, is shown below. Chart of Accounts General Ledger GL # Balance Sheet Items * Accounts Payable (Control) 7 Accounts Receivable (Control) 3 Bank 1 Deposits 4 Inventory 10 Loans Payable 8 Owner s Equity 9 Equipment 5 Petty Cash 2 Reserve for Depreciation 6 Profit and Loss Items * Auto Expense 53 Commission 54 Food and Lodging 55 Depreciation 58 Profit & Loss 59 Purchases 52 Rent 56 Telephone 57 Sales 51 * The word item is used, at times, when referring to a specific item in the chart of accounts. It is primarily used when referring to the balance sheet or the profit and loss statement. For example, a balance sheet item means that it belongs in the balance sheet portion of the trial balance. Conversely, a profit and loss item means it belongs in the profit and loss portion of the trial balance.

17 The Method The Wide Scope of Double-Entry Accounting All of accounting is primarily a journal entry. A journal entry is, first and foremost, an example of double-entry accounting. It doesn t seem logical to be able to record one transaction using the same number two times. No other area in mathematics uses the same number twice. Why doesn t using the same number twice lead to duplications and erroneous answers? Why does double-entry accounting work? A journal entry consists of two parts, a debit and a credit. For example, in the case of a sale, one of the journal entry parts is entered on the balance sheet and the other half is entered on the profit and loss. The fact the same number is entered two times works in accounting because the part put on the balance sheet keeps a record of what has transpired in the profit and loss portion. The point to remember is that each half of a journal entry performs a different function. There are exceptions to this rule that will be discussed later. Example. Assume the following: A. A cash sale for $100 was made; the money is deposited into the bank. B. A $200 sale was made and the money is placed in the cash register. C. A $300 sale was made on credit. TRIAL BALANCE Debits Balance Sheet Credits (A) Bank 100 (B ) Cash 200 (C) Accounts Receivable 300 Figure 1-4 Profit & Loss (A) Sale 100 (B) Sale 200 (C) Sale 300 In the above example, the amount of sales ($100, $200, and $300) is known. But, equally important, there is a record of what was acquired as a result of the sales (bank, cash, and a receivable). As additional transactions are recorded, the principle remains the same: the items that keep a record are placed in the balance sheet and the items that describe the sales and expenses are placed in the profit and loss sections.

18 Basic Accounting Simplified 1 8 Each time part of a journal entry is placed on the balance sheet a record is being kept Each time part of a journal entry is placed in the profit and loss, income or loss is affected Helpful Tip. The double-entry accounting system serves as an error-detection system: if at any point the debits do not equal the corresponding credits, an error has occurred. 9. Types of Journal Entries A. The Diagonal Journal Entry A diagonal journal entry going from quadrant 1 to quadrant 4 is good for the business since it increases the probability of making a profit. A diagonal journal entry going from quadrant 3 to quadrant 2 is bad for the business since it increases the probability of suffering a loss, see Figure 1-5. Diagonal journal entries are the most prevalent types of journal entry; more than 95 percent of all journal entries are diagonal. For example, depositing money in the bank as a result of a sale (quadrant 1 to 4) is a common occurrence. Withdrawing money from the bank for a purchase (quadrant 3 to 2) is also a common occurrence. Figure 1-5 Trial Balance Debits Balance Sheet Credits QUADRANT 1 QUADRANT 2 GOOD BAD Debit Profit & Loss Credit QUADRANT 3 QUADRANT 4 BAD GOOD For centuries the books of account have been set up recognizing the great frequency of these types of transactions. It is the very foundation of double entry accounting. When a sale is made, profit is affected, and the bank account is increased by the extent of the sale. When a purchase is made, loss is affected, and the bank account is decreased to the extent of the purchase.

19 The Method 1 9 Items that affect income adversely are placed in quadrant 3. Many of the same expenses that an individual has in operating a household would be in quadrant 3. Items that have a negative impact on income include cleaning, rent, purchases, auto expenses, utilities, telephone, etc. If an entry is made to quadrant 3, the other half of that entry must go to quadrant 2, which keeps a record of how quadrant 2 is adversely affected (e.g., a reduction in the bank account or an increase in accounts payable). B. The Horizontal Journal Entry Horizontal journal entries go from quadrant 1 to quadrant 2 or from quadrant 3 to quadrant 4. For example, purchasing equipment (quadrant 1), with funds withdrawn from the bank (quadrant 2), is an example of a horizontal journal entry. Horizontal journal entries that go from quadrant 1(assets) to quadrant 2 (liabilities) only affect the balance sheet. Income is not affected when horizontal journal entries are placed in the balance sheet. Following are examples of horizontal type balance sheet journal entries. It should be noted the total of the assets and the liabilities remain the same after a horizontal entry is made to the balance sheet. When an error has been committed. To record an overcharge to B Co. that should have been charge to A Co. Debit Credit Accounts Receivable A Co. 10 Accounts Receivable B Co. 10 When equipment has been purchased. To record purchase of an automobile. Debit Credit Automobile 30,000 Bank 30,000 When the owner invests money in the business. To record owner s investment. Debit Credit Bank 10,000 Owner s Equity 10,000 When money is borrowed. Money is borrowed from the bank. Debit Credit Bank 5,000 Loan Payable-Smith Bank 5,000

20 Basic Accounting Simplified 1 10 Petty Cash fund is established. Establishment of a petty cash fund. Debit Credit Petty Cash Fund 30 Bank 30 Note. There are very few journals entries that go horizontally from quadrant 3 (expense) to quadrant 4 (income). Horizontal journal entries that go from quadrant 3 to quadrant 4 are used mainly to correct errors. C. Section Summary In general, there are two types of diagonal journal entries. On type goes from the asset side of the balance sheet to the income side of the profit and loss. The other type goes from the expense side of the profit and loss to the liability side of the balance sheet. There are two types of horizontal journal entries. One type goes from the asset side of the balance sheet to the liability side of the balance sheet. The other type goes from the expense side of the profit and loss to the income side of the profit and loss. Horizontal journal entries are primarily used to rectify an error, to make an adjustment, or to record the purchase of a capital asset (and have no affect on profit and loss). TRIAL BALANCE DEBITS Balance Sheet CREDITS GOOD Quadrant 1. BAD Quadrant 2. Assets Liabilities Owner s equity Good DEBITS Profit & Loss CREDITS BAD Quadrant 3. GOOD Quadrant 4. Loss Profit More than 95 percent of all journal entries are diagonal. They are either: A debit to quadrant 1 and a credit to quadrant 4 This is an entry that increases profit, or A debit to quadrant 3 and a credit to quadrant 2 This is an entry that decreases profit.

21

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

DOWNLOAD PDF GENERAL JOURNAL AND LEDGER

Chapter 1 : The General Journal and Ledger The general journal is a place to first record an entry before it gets posted to the appropriate accounts. Related Questions What is the difference between entries

Chapter 1 : The General Journal and Ledger The general journal is a place to first record an entry before it gets posted to the appropriate accounts. Related Questions What is the difference between entries

Accounting Part 1 STUDY UNIT. Accounting Part 1 STUDY UNIT

Accounting Part 1 STUDY UNIT Accounting Part 1 STUDY UNIT 06100202 Study Unit Accounting, Part 1 By John R. Cerepak, Ph.D., C.P.A. Department Chairman and Professor of Accounting and Quantitative Analysis

Accounting Part 1 STUDY UNIT Accounting Part 1 STUDY UNIT 06100202 Study Unit Accounting, Part 1 By John R. Cerepak, Ph.D., C.P.A. Department Chairman and Professor of Accounting and Quantitative Analysis

Accounting Demystified

Accounting Demystified This page intentionally left blank Accounting Demystified Jeffry R. Haber, Ph.D., CPA American Management Association New York Atlanta Brussels Chicago Mexico City San Francisco

Accounting Demystified This page intentionally left blank Accounting Demystified Jeffry R. Haber, Ph.D., CPA American Management Association New York Atlanta Brussels Chicago Mexico City San Francisco

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

CHAPTER 3. The Adjusting Process. Chapter Overview

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Bookkeeping (Explanation)

") Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Learning Accountancy: The Novel Way

Learning Accountancy: The Novel Way Learning Accountancy: The Novel Way By Zarir Suntook Learning Accountancy: The Novel Way, by Zarir Suntook This book first published 2010 Cambridge Scholars Publishing

Learning Accountancy: The Novel Way Learning Accountancy: The Novel Way By Zarir Suntook Learning Accountancy: The Novel Way, by Zarir Suntook This book first published 2010 Cambridge Scholars Publishing

DOWNLOAD PDF JOURNAL ENTRY EXAMPLES ACCOUNTING

Chapter 1 : Ledger Accounts Posting Transactions Example Analyzing transactions and recording them as journal entries is the first step in the accounting blog.quintoapp.com begins at the start of an accounting

Chapter 1 : Ledger Accounts Posting Transactions Example Analyzing transactions and recording them as journal entries is the first step in the accounting blog.quintoapp.com begins at the start of an accounting

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE 1 CONTENTS A) Bookkeeping 1) About Single Entry System and its disadvantages 2) About Bookkeeping and Accounting Process 3) About Double

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE 1 CONTENTS A) Bookkeeping 1) About Single Entry System and its disadvantages 2) About Bookkeeping and Accounting Process 3) About Double

Basic Understanding of the Accounting Industry: Basic Understanding of the Accounting Industry:

Texas University Interscholastic League Contest Event: Accounting The contest focuses on the elementary principles and practices of accounting for sole proprietorship, partnerships and corporations, and

Texas University Interscholastic League Contest Event: Accounting The contest focuses on the elementary principles and practices of accounting for sole proprietorship, partnerships and corporations, and

CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION

REVIEW QUESTIONS CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION 1. It is necessary to distinguish between business assets and liabilities and nonbusiness assets and liabilities of a single proprietor

REVIEW QUESTIONS CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION 1. It is necessary to distinguish between business assets and liabilities and nonbusiness assets and liabilities of a single proprietor

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1 Published by ICB Direct Ltd ICB Direct Ltd 2013 All rights reserved. No part of this publication may be reproduced, sorted in a retrieval system,

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1 Published by ICB Direct Ltd ICB Direct Ltd 2013 All rights reserved. No part of this publication may be reproduced, sorted in a retrieval system,

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Full file at Chapter 2: Analyzing Business Transactions

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Guide to Bookkeeping Concepts

Guide to Bookkeeping Concepts Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Guide to Bookkeeping Concepts Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Debits and Credits. (Explanation)

") s and s (Explanation) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Introduction to s and s If the

s and s (Explanation) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Introduction to s and s If the

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

Your Business Finances

ASi Simple Start tto Managing Your Business Finances A Guide to the Essentials QB_05/2005_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

ASi Simple Start tto Managing Your Business Finances A Guide to the Essentials QB_05/2005_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018 Administrative Items Re-do Seating Chart for Sections 14 and 15 Reminder of correct usage of Self-Assessments Reminder of

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018 Administrative Items Re-do Seating Chart for Sections 14 and 15 Reminder of correct usage of Self-Assessments Reminder of

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

4 Adjustments for financial reporting

4 Adjustments for financial reporting 4.1 Learning objectives Describe the basic characteristics of the cash basis and the accrual basis of accounting. Identify the reasons why adjusting entries must be

4 Adjustments for financial reporting 4.1 Learning objectives Describe the basic characteristics of the cash basis and the accrual basis of accounting. Identify the reasons why adjusting entries must be

A Simple Start to Managing Your Business Finances

A Simple Start to Managing Your Business Finances A Guide to the Essentials QB_10/2004_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

A Simple Start to Managing Your Business Finances A Guide to the Essentials QB_10/2004_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

Using other accounts in QuickBooks

LESSON 5 Using other accounts in QuickBooks 5 Lesson objectives, 134 Supporting materials, 134 Instructor preparation, 134 To start this lesson, 134 Other account types in QuickBooks, 135 Tracking credit

LESSON 5 Using other accounts in QuickBooks 5 Lesson objectives, 134 Supporting materials, 134 Instructor preparation, 134 To start this lesson, 134 Other account types in QuickBooks, 135 Tracking credit

DOWNLOAD PDF LIST OF DEBIT AND CREDIT ITEMS IN ACCOUNTING

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Fundamental Accounting Principles

Last revised: January 23, 2016. SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 15 th Canadian Edition by Larson/Jensen/Dieckmann Revised for the 15 th Edition by: Praise Ma, Kwantlen Polytechnic

Last revised: January 23, 2016. SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 15 th Canadian Edition by Larson/Jensen/Dieckmann Revised for the 15 th Edition by: Praise Ma, Kwantlen Polytechnic

Buy The Complete Version of This Book at Booklocker.com:

Accounting and bookkeeping text with student working papers and solutions. How to Do Accounting I with student working papers and solutions Buy The Complete Version of This Book at Booklocker.com: http://www.booklocker.com/p/books/4709.html?s=pdf

Accounting and bookkeeping text with student working papers and solutions. How to Do Accounting I with student working papers and solutions Buy The Complete Version of This Book at Booklocker.com: http://www.booklocker.com/p/books/4709.html?s=pdf

Debits and Credits CHAPTER

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

Example Candidate Responses

Example Candidate Responses Cambridge O Level Principles of Accounts 7110 Cambridge Secondary 2 In order to help us develop the highest quality Curriculum Support resources, we are undertaking a continuous

Example Candidate Responses Cambridge O Level Principles of Accounts 7110 Cambridge Secondary 2 In order to help us develop the highest quality Curriculum Support resources, we are undertaking a continuous

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

AAT. Accounts Preparation. Pocket notes

AAT Accounts Preparation Pocket notes Accounts Preparation British library cataloguing-in-publication data A catalogue record for this book is available from the British Library. Published by: Kaplan Publishing

AAT Accounts Preparation Pocket notes Accounts Preparation British library cataloguing-in-publication data A catalogue record for this book is available from the British Library. Published by: Kaplan Publishing

Department Budgets and Finance

International Security Training, LLC Module 4 Page 1 of 18 Department Budgets and Finance Financial management is a crucial aspect of any thriving business. Profit maximization, or stockholder wealth maximization,

International Security Training, LLC Module 4 Page 1 of 18 Department Budgets and Finance Financial management is a crucial aspect of any thriving business. Profit maximization, or stockholder wealth maximization,

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Appendices - Introduction

Appendices - Introduction For more than one reason, we have posted a printable "pdf" copy of the appendices listed below, on our website @: http://www.full-chargebookkeeping.com/ > Resources & Links page.

Appendices - Introduction For more than one reason, we have posted a printable "pdf" copy of the appendices listed below, on our website @: http://www.full-chargebookkeeping.com/ > Resources & Links page.

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions. Chapter Overview. Learning Objectives

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Accounting I Class Schedule

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

T Accounts, Debits and Credits, Trial Balance, and Financial Statements

2 T Accounts, s and s, Trial Balance, and Financial Statements TEACHING OBJECTIVES 1. To introduce the T account form 2. To introduce debit and credit 3. To introduce the function and preparation of a

2 T Accounts, s and s, Trial Balance, and Financial Statements TEACHING OBJECTIVES 1. To introduce the T account form 2. To introduce debit and credit 3. To introduce the function and preparation of a

Online Course Manual By Craig Pence. Module 7

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Chart of Accounts. Chart of Accounts

Chart of Accounts A company s Chart of Accounts is a list of all Asset, Liability, Equity, Revenue, and Expense accounts included in the company s General Ledger. The number of accounts included in the

Chart of Accounts A company s Chart of Accounts is a list of all Asset, Liability, Equity, Revenue, and Expense accounts included in the company s General Ledger. The number of accounts included in the

*Define and differentiate the accrual method and cash method of recording transactions.

Accounting 1 *Define and differentiate the terms accounting, auditing, and bookkeeping: --Accounting the process of recording, reporting and analyzing financial transactions. --Bookkeeping the process

Accounting 1 *Define and differentiate the terms accounting, auditing, and bookkeeping: --Accounting the process of recording, reporting and analyzing financial transactions. --Bookkeeping the process

Money Made Simple. The Ultimate Guide to Personal Finance

Money Made Simple The Ultimate Guide to Personal Finance Table of Contents Section 1 Back to Basics: What is Money? 5 Section 2 Clearing Out the Clutter. 17 Section 3 Where Does All My Money Go? 27 Section

Money Made Simple The Ultimate Guide to Personal Finance Table of Contents Section 1 Back to Basics: What is Money? 5 Section 2 Clearing Out the Clutter. 17 Section 3 Where Does All My Money Go? 27 Section

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

York University AP/Adms Introduction to Financial Accounting Midterm Examination Test Form B

York University AP/Adms 2500.03 Introduction to Financial Accounting Midterm Examination Test Form B Time: 3.0 hours Winter 2010 March 5 th, 2010 Questions: 50 Instructions: 1. Only the mark sense sheet

York University AP/Adms 2500.03 Introduction to Financial Accounting Midterm Examination Test Form B Time: 3.0 hours Winter 2010 March 5 th, 2010 Questions: 50 Instructions: 1. Only the mark sense sheet

A Review of the Accounting Cycle

CHAPTER 2 A Review of the Accounting Cycle LEARNING OBJECTIVES 1. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze business documents, Journalize transactions,

CHAPTER 2 A Review of the Accounting Cycle LEARNING OBJECTIVES 1. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze business documents, Journalize transactions,

MYOB Accounting 101. For Mac Users. Written by: Todd Salkovitz Macintosh Product Manager MYOB Ltd USA Edition

MYOB Accounting 101 For Mac Users Written by: Todd Salkovitz Macintosh Product Manager MYOB Ltd. 2009 USA Edition Like all small business owners, you went into business with a dream: to sell your unique

MYOB Accounting 101 For Mac Users Written by: Todd Salkovitz Macintosh Product Manager MYOB Ltd. 2009 USA Edition Like all small business owners, you went into business with a dream: to sell your unique

CHAPTER 2 ANALYZING TRANSACTIONS

CHAPTER 2 ANALYZING TRANSACTIONS EYE OPENERS 1. An account is a form designed to record changes in a particular asset, liability, owner s equity, revenue, or expense. A ledger is a group of related accounts.

CHAPTER 2 ANALYZING TRANSACTIONS EYE OPENERS 1. An account is a form designed to record changes in a particular asset, liability, owner s equity, revenue, or expense. A ledger is a group of related accounts.

Chapter 23 Audit of Cash and Financial Instruments. Copyright 2014 Pearson Education

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Seminar on Bookkeeping Basics

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

HS Accounting I 2013 Business and Technology

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Chapter 2. Ex a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit. Ex.

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

Accounting for Management: Concepts and Tools

Accounting for Management: Concepts and Tools Accounting for Management: Concepts and Tools Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by

Accounting for Management: Concepts and Tools Accounting for Management: Concepts and Tools Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Robert L. Dansby, Ph.D. Burton S. Kaliski, Ed.D. Michael D. Lawrence, MBA, CPA, CMA

Robert L. Dansby, Ph.D. Columbus Technical College Columbus, Georgia Burton S. Kaliski, Ed.D. Southern New Hampshire University Manchester, New Hampshire Michael D. Lawrence, MBA, CPA, CMA Portland Community

Robert L. Dansby, Ph.D. Columbus Technical College Columbus, Georgia Burton S. Kaliski, Ed.D. Southern New Hampshire University Manchester, New Hampshire Michael D. Lawrence, MBA, CPA, CMA Portland Community

Understanding the Mathematics of Personal Finance An Introduction to Financial Literacy Lawrence N. Dworsky A John Wiley & Sons, Inc., Publication Understanding the Mathematics of Personal Finance Understanding

Understanding the Mathematics of Personal Finance An Introduction to Financial Literacy Lawrence N. Dworsky A John Wiley & Sons, Inc., Publication Understanding the Mathematics of Personal Finance Understanding

Graded Project Ice Cream Systems

Graded Project Ice Cream Systems PROJECT GOAL 1 PROJECT INFORMATION 1 PROJECT INSTRUCTIONS 14 SUBMITTING YOUR PROJECT 26 C o n t e n t s iii Ice Cream Systems PROJECT GOAL The goal of this graded project

Graded Project Ice Cream Systems PROJECT GOAL 1 PROJECT INFORMATION 1 PROJECT INSTRUCTIONS 14 SUBMITTING YOUR PROJECT 26 C o n t e n t s iii Ice Cream Systems PROJECT GOAL The goal of this graded project

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

Account - A record of financial transactions that are similar in terms of a given frame of reference such as purpose, objective, or source.

This section includes definitions of terms used in this guide and additional terms necessary for the understanding of financial accounting procedures for internal funds. Internal funds are defined as all

This section includes definitions of terms used in this guide and additional terms necessary for the understanding of financial accounting procedures for internal funds. Internal funds are defined as all

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS PRINCIPLES OF ACCOUNTING I ACC 2110

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS PRINCIPLES OF ACCOUNTING I ACC 2110 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Fall 1999 Catalog Course Description:

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS PRINCIPLES OF ACCOUNTING I ACC 2110 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Fall 1999 Catalog Course Description:

2000 Accounting II Page 1

2000 Accounting II Page 1 1. In accounting, the two types of equity are liabilities and owner's equity. 2. When journalizing, you are advised to go from left to right. 3. Transportation charges need to

2000 Accounting II Page 1 1. In accounting, the two types of equity are liabilities and owner's equity. 2. When journalizing, you are advised to go from left to right. 3. Transportation charges need to

2. From the Desktop, click on Accounting > Operations > Account Transactions

Pre-Programmed Default General Ledger Accounts in Partner XE To Access 1. From the Desktop, click on the Accounting Icon The Daily Processing screen will come up From within Accounting click on Account

Pre-Programmed Default General Ledger Accounts in Partner XE To Access 1. From the Desktop, click on the Accounting Icon The Daily Processing screen will come up From within Accounting click on Account

Composed & Solved Hafiz Salman Majeed

FINALTERM EXAMINATION Fall 2008 MGT101- Financial Accounting (Session - 4) Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset

FINALTERM EXAMINATION Fall 2008 MGT101- Financial Accounting (Session - 4) Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset

2 GoVenture CEO LEARNING GUIDE. Learning Guide & Activity Book SAMPLE

2 GoVenture CEO GoVenture CEO Learning Guide & Activity Book This guide helps you learn the fundamental concepts of business as they are applied in the GoVenture CEO simulation. ISBN 978-1-894353-31-1

2 GoVenture CEO GoVenture CEO Learning Guide & Activity Book This guide helps you learn the fundamental concepts of business as they are applied in the GoVenture CEO simulation. ISBN 978-1-894353-31-1

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

1 st Year Examination : Summer FINANCIAL ACCOUNTING l NEW SYLLABUS. PAPER, SOLUTIONS and EXAMINERS REPORT

1 st Year Examination : Summer 2009 FINANCIAL ACCOUNTING l NEW SYLLABUS PAPER, SOLUTIONS and EXAMINERS REPORT NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

1 st Year Examination : Summer 2009 FINANCIAL ACCOUNTING l NEW SYLLABUS PAPER, SOLUTIONS and EXAMINERS REPORT NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

Chapter 3: Double-Entry Bookkeeping

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Model Paper Principals of Accounting Objective

Model Paper Principals of Accounting Objective Intermediate Part I (11 th Class) Examination Session 2012-2013 and onward Total marks: 15 Paper Code Time Allowed: 20 minutes Note:- You have four choices

Model Paper Principals of Accounting Objective Intermediate Part I (11 th Class) Examination Session 2012-2013 and onward Total marks: 15 Paper Code Time Allowed: 20 minutes Note:- You have four choices

Introduction... 4 Cash vs Accrual Components of the Balance Sheet How to Get a Snapshot View with Balance Sheet Accounts Ratios...

TABLE OF CONTENTS Introduction... 4 Cash vs Accrual... 5 Components of the Balance Sheet... 6 How to Get a Snapshot View with Balance Sheet Accounts... 7 Ratios... 8 Entrepreneurial Finance: Bonus Ratios

TABLE OF CONTENTS Introduction... 4 Cash vs Accrual... 5 Components of the Balance Sheet... 6 How to Get a Snapshot View with Balance Sheet Accounts... 7 Ratios... 8 Entrepreneurial Finance: Bonus Ratios

Student s Book. Financial

FET FIRST NATED Series Financial Accounting N4 Student s Book R. Eyssen FET FIRST NATED Series Financial Accounting Student s Book R. Eyssen, 2012 All rights reserved. No part of this publication may be

FET FIRST NATED Series Financial Accounting N4 Student s Book R. Eyssen FET FIRST NATED Series Financial Accounting Student s Book R. Eyssen, 2012 All rights reserved. No part of this publication may be

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Tax-Wise Portfolio Rebalancing the financial markets. The answer generally recommended by financial advisors is

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Tax-Wise Portfolio Rebalancing the financial markets. The answer generally recommended by financial advisors is

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Number Key Question Number Key 1 C 16 C 2 D 17 A 3 D 18 B 4 B 19 B 5 A 20 A 6 D 21 D 7 D 22 A 8 C 23 D 9 A 24 A 10 B 25 D 11 A 26 C 12 A 27

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Number Key Question Number Key 1 C 16 C 2 D 17 A 3 D 18 B 4 B 19 B 5 A 20 A 6 D 21 D 7 D 22 A 8 C 23 D 9 A 24 A 10 B 25 D 11 A 26 C 12 A 27

FUNDAMENTAL ACCOUNTING (01) Regional 2013

Regional 2013") Page 1 of 11 Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Secondary Regional 2013 Multiple Choice Account Identification Problem 1 Journalizing Problem 2 Income Statement Problem 3 Closing Entries

Page 1 of 11 Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Secondary Regional 2013 Multiple Choice Account Identification Problem 1 Journalizing Problem 2 Income Statement Problem 3 Closing Entries

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 11 Contestant Number: Time: Rank: FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2017 CONCEPT KNOWLEDGE: True/False (15 @ 2 points each) Multiple Choice (25 @ 2 points each) APPLICATION KNOWLEDGE:

Page 1 of 11 Contestant Number: Time: Rank: FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2017 CONCEPT KNOWLEDGE: True/False (15 @ 2 points each) Multiple Choice (25 @ 2 points each) APPLICATION KNOWLEDGE:

Church Accounting Icon Systems Inc.

IconCMO Church Software by Icon Systems Inc. All rights reserved. No parts of this work may be reproduced in any form or by any means - graphic, electronic, or mechanical, including photocopying, recording,

IconCMO Church Software by Icon Systems Inc. All rights reserved. No parts of this work may be reproduced in any form or by any means - graphic, electronic, or mechanical, including photocopying, recording,

Full Disclosures in Financial Reporting

Full Disclosures in Financial Reporting Full Disclosures in Financial Reporting Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any means,

Full Disclosures in Financial Reporting Full Disclosures in Financial Reporting Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any means,

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

REDISCOVER THE LOST ART OF CHART READING

REDISCOVER THE LOST ART OF CHART READING Using Volume Spread Analysis BY: Todd Krueger Most traders are aware of the two widely known approaches used to analyze a market, fundamental analysis and technical

REDISCOVER THE LOST ART OF CHART READING Using Volume Spread Analysis BY: Todd Krueger Most traders are aware of the two widely known approaches used to analyze a market, fundamental analysis and technical

Robert L. Dansby, Ph.D. Burton S. Kaliski, Ed.D. Michael D. Lawrence, MBA, CPA, CMA

Robert L. Dansby, Ph.D. Columbus Technical College Columbus, Georgia Burton S. Kaliski, Ed.D. Southern New Hampshire University Manchester, New Hampshire Michael D. Lawrence, MBA, CPA, CMA Portland Community

Robert L. Dansby, Ph.D. Columbus Technical College Columbus, Georgia Burton S. Kaliski, Ed.D. Southern New Hampshire University Manchester, New Hampshire Michael D. Lawrence, MBA, CPA, CMA Portland Community

18. Double-entry accounting means that every transaction affects and is recorded in at least two accounts. True False 19. Debits increase asset and

02 Student: 1. The first step in the accounting cycle is transaction analysis. 2. An account is a detailed record of increases and decreases in a specific asset, liability or equity item. 3. A ledger is

02 Student: 1. The first step in the accounting cycle is transaction analysis. 2. An account is a detailed record of increases and decreases in a specific asset, liability or equity item. 3. A ledger is

Principles of Financial Accounting

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Fall 2018 Principles

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Fall 2018 Principles

ISBN Copyright 2001, The National Underwriter Company P.O. Box Cincinnati, OH

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering

2018 VCE Accounting examination report

General comments The Accounting examination consisted of eight questions, with most containing several parts. One graph was presented for interpretation in. There was also one discuss question, where students

General comments The Accounting examination consisted of eight questions, with most containing several parts. One graph was presented for interpretation in. There was also one discuss question, where students

An entity s ability to maintain its short-term debt-paying ability is important to all

chapter 6 Liquidity of Short-Term Assets; Related Debt-Paying Ability An entity s ability to maintain its short-term debt-paying ability is important to all users of financial statements. If the entity

chapter 6 Liquidity of Short-Term Assets; Related Debt-Paying Ability An entity s ability to maintain its short-term debt-paying ability is important to all users of financial statements. If the entity

Chapter 4: The Simple Ledger

Chapter 4: The Simple Ledger 4.1: Ledger Accounts Pages 88 92 account a record that documents each change to items in the accounting equation. There is one account for each asset, each liability, and each

Chapter 4: The Simple Ledger 4.1: Ledger Accounts Pages 88 92 account a record that documents each change to items in the accounting equation. There is one account for each asset, each liability, and each

QUICKBOOKS ONLINE PLUS: A COMPLETE COURSE Chapter 5: General Accounting and End-of- Period Procedures

QUICKBOOKS ONLINE PLUS: A COMPLETE COURSE 2016 Chapter 5: General Accounting and End-of- Period Procedures Lecture Focus 2 Complete end-of-period procedures Record adjusting entries Record Owner s Equity

QUICKBOOKS ONLINE PLUS: A COMPLETE COURSE 2016 Chapter 5: General Accounting and End-of- Period Procedures Lecture Focus 2 Complete end-of-period procedures Record adjusting entries Record Owner s Equity

Veideretti Cabinets. Algorithmic Version. Student Manual

Veideretti Cabinets Algorithmic Version Student Manual Page 1 An Introduction to Algorithmic Veideretti Cabinets Veideretti Cabinets, Incorporated, (pronounced Vi-der-etty) is a small business corporation

Veideretti Cabinets Algorithmic Version Student Manual Page 1 An Introduction to Algorithmic Veideretti Cabinets Veideretti Cabinets, Incorporated, (pronounced Vi-der-etty) is a small business corporation

Work4Me I Accounting Simulations. Demonstration Problem

Work4Me I Accounting Simulations 3 rd Web-Based Edition Demonstration Problem Classic Accounting Services, Incorporated Page 1 Problem 1 Demonstration Problem The Work4Me problems begin with a hands-on,

Work4Me I Accounting Simulations 3 rd Web-Based Edition Demonstration Problem Classic Accounting Services, Incorporated Page 1 Problem 1 Demonstration Problem The Work4Me problems begin with a hands-on,

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

GENERAL LEDGER TABLE OF CONTENTS

GENERAL LEDGER TABLE OF CONTENTS L.A.W.S. Documentation Manual General Ledger GENERAL LEDGER 298 General Ledger Menu 298 Overview Of The General Ledger Account Number Structure 299 Profit Center Processing

GENERAL LEDGER TABLE OF CONTENTS L.A.W.S. Documentation Manual General Ledger GENERAL LEDGER 298 General Ledger Menu 298 Overview Of The General Ledger Account Number Structure 299 Profit Center Processing

Accountings Summary OUTLINE

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting