Basis Issues for Partnerships and S Corporations. Edward K. Zollars, CPA

|

|

|

- Alexandra Cummings

- 6 years ago

- Views:

Transcription

1 Basis Issues for Partnerships and S Corporations Edward K. Zollars, CPA ed@tzlcpas.com

2 Importance of Basis One of three limits on deducting a loss Required attachment to tax return for an S corporation shareholder claiming a loss Must know basis to determine if Distribution is taxable (Partnership or S corporation) Repayment of debt taxable (S corporation) Used to compute gain/loss on disposition of asset 2

3 Must Have Basis to Prepare a Return for a Holder of a Flowthrough Entity 3

4 Basis and Debt - Partnerships Basis Issues for Partnerships and S Corporations 4

5 Partnerships and Debt Partnerships get basis from any debt Note that may not get at-risk amount (which is a different issue) Debt is responsible for what is often erroneously called negative basis 5

6 Basis cannot go below zero 6

7 Basis is Not A partner s tax basis capital account A partner s 704(b) capital account ( book capital) A partner s GAAP capital account The total of the partner s share of the basis of partnership assets 7

8 Definition of a Liability Per Reg (a)(4) a liability Creates or increases basis of an asset Creates a deductible expense Creates a nondeductible expense Special contingent liability ant-abuse rule specifically blocks Son of BOSS structure 8

9 All Partnership Liabilities are Classified as Either Recourse or Nonrecourse 9

10 Allocate Recourse Debts 10

11 Presumption of Repayment All partners are presumed to meet their legal responsibilities to repay Limited exception for disregarded entities 11

12 Guarantees Don t Change This Unless Partner Gives Up Right of Reimbursement 12

13 Distribution Problem Reduction in debt allocated to a partner is deemed to be a distribution of cash [IRC 752(b)] Distributions in excess of basis trigger taxable gain to partner [IRC 731(a)(1)] 13

14 Nonrecourse Liabilities Only classified as such if no partner has economic risk of loss Note this definition is not the definition used for testing cancellation of debt Debt can be nonrecourse partnership debt Still can be recourse for COD purposes The simplest example would be accounts payable in an LLC 14

15 Allocation of Nonrecourse Debt 1st Tier 2 nd Tier 3 rd Tier Partner s share of minimum gain on assets encumbered by nonrecourse debt Partner s share of minimum gain determined under 704(c) Remainder using a reasonable method (generally profit sharing is reasonable) 15

16 At-Risk is Separate from Basis 16

17 Basics of At Risk (Outside Manual) Losses may only be deducted to extent taxpayer is at risk If amount at risk is reduced, must recapture prior losses claimed Generally not at risk for nonrecourse debt Certain real estate loans can be qualified nonrecourse debt Compute on Form

18 Key Rules Your software cannot properly handle the allocation of debt to the partners except in trivial situations Many K-1s you receive will not be prepared correctly Must track debt from year to year for partner Remember the cash distribution problem 18

19 Basis in Stock and Debt S Corporations Basis Issues for Partnerships and S Corporations 19

20 S Corporations and Basis Different from partnerships in a number of ways Have stock basis and debt basis determined under different rules Debt basis is totally unrelated to partnership debt basis rules 20

21 S Corporation Annual Basis Adjustments 21

22 Basis Can Only Be Increased if Shareholder Actually Reports Income (But Reduction for Loss Takes Effect Regardless) 22

23 Special Rules Inherited stock & IRD issues Separate share rule Duty of consistency 23

24 Debt Basis Once stock basis is exhausted move on to amounts loaned from shareholder to corporation Proportionate allocation to each debt Basis restored with income, and takes place Before repayment gain/loss calculated Before adjusting stock basis 24

25 Debts That Provide Basis Must be bona fide debts Must be from shareholder Can be borrowed from third party then lent Shareholder must be only person on debt What does not work Guarantee of debt Co-maker 25

26 Repayment of Debt If basis < face, a prorate amount of basis allocated to principal paid and taxpayer recognizes gain If no note ordinary gain If evidenced by a note capital gain 26

27 27

28 Debt can be converted tax free to stock at any time and why you might want to (or not want to) advise doing that 28

29 Carryovers and Basis Adjustments Additions first, then distributions Losses in excess of basis cannot be deducted Election to reorder basis adjustments If don t make election, must first reduce basis (but not below zero) by nondeductible items If still have nondeductible items, they disappear If elect, nondeductibles pushed to last item to be used but must be carried forward 29

30 Schedule E Instructions Require Basis Schedule When S Losses Claimed 30

31 If stock is sold, first make basis adjustments, then compute gain/loss on sale 31

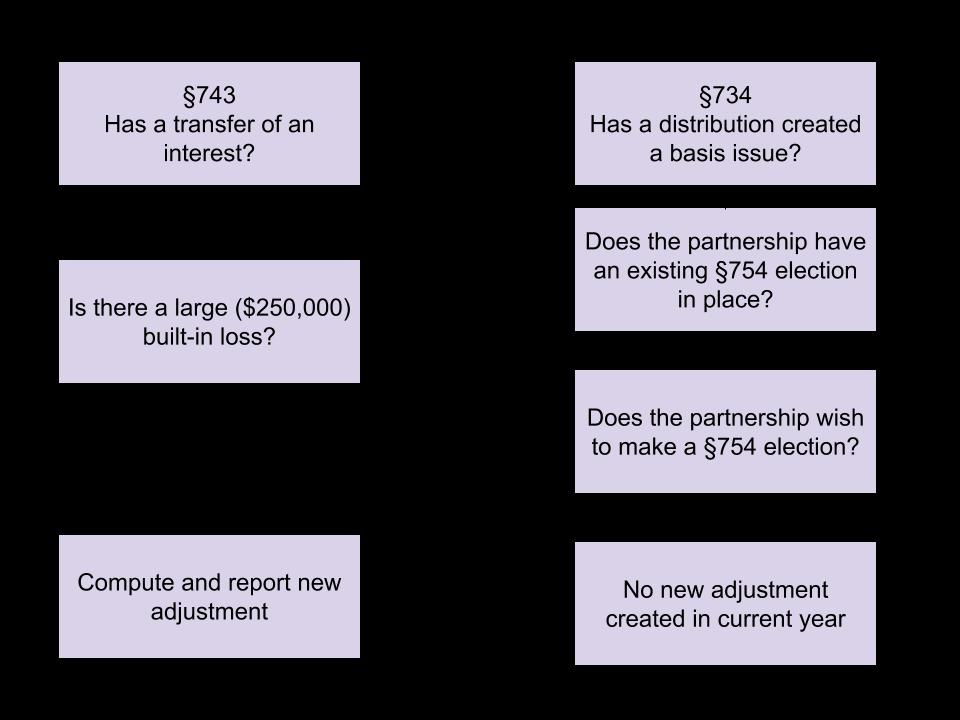

32 Partnership Basis Adjustments ( 704(c) and 754) Basis Issues for Partnerships and S Corporations 32

33 Section 704(c) Built-in gains/losses go to contributing partner Also appears when have recapitalizations (reverse 704(c) allocations) Different than S result Must be used unless de minimis rule applies Difference not more than 15% and Total difference not more than $20,000 33

34 Traditional Method Only use actual items to allocate differences May end up not solving the problem entirely due to ceiling rule 34

35 Traditional Method with Curative Allocations Can use other similar items actually on the return to fix the original differences For instance, ordinary business deductions could substitute for depreciation Much more likely to solve problem However still possible to end up with no way to solve or nothing similar exists (especially capital gain/loss issue) 35

36 Remedial Allocation Method If it does work we make it work Make correction and then create an offsetting items to return balance Or, to put it simply, plug it If use this method, for depreciation establish a new asset placed in service when asset is contributed (or there is a recapitalization) 36

37 Revaluations Required in certain situations, allowed in others if agreement provides Creates reverse 704(c) allocations 37

38 Distributions and 704(c) Can t avoid the issue by pushing asset out to another partner For seven years, distributing property out to another partner triggers gain recognition Could have been a 1031 Exchange exception Watch for disguised sales rules as well 38

39 For 737 have unique issue of worrying about fair value vs. basis for a distribution 39

40 40

41 Making the Election Required attachments Late election relief under (d) Revocation of Election 41

42 Section 732(d) Election is Very Easy to Overlook 42

43 Partnership Distributions Basis Issues for Partnerships and S Corporations 43

44 Partnership Distributions Unlike corporations, generally no trigger of deemed sale Also, gain only recognized to extent of cash received But cash includes deemed cash from reduction in debt allocated 44

45 Current Distributions Reduce basis by cash (excess would be gain) Reduce basis for inventory/accounts receivable basis Reduce basis by basis of other assets 45

46 Liquidating Distributions Reduce basis by cash (excess would be gain) Reduce basis for inventory/accounts receivable basis (if nothing else received, remaining basis is loss) Allocate basis to other assets received 46

47 Hot Assets Generally triggered if a distribution leads to a change in share of hot assets Hot assets Unrealized receivables (note broader than expected definition) Appreciated inventory 47

48 Regulations in Flux Current regulations Gross value method Deemed distribution of proportionate share of hot/non-hot assets followed by a taxable exchange to get what was actually received Can create interesting situations if don t just pay cash Proposed regulations Before and after calculation for liquidation Look at any person whose Share of hot asset income goes down or Share of hot asset loss goes up Can elect to use, but must stay with if start using them 48

49 Section 736 Distributions Retirement issue Traditional liquidation payment is Section 736(b) payment Payments in excess of capital treated as Section 736(a) payments Ordinary income to recipient as guaranteed payment Special rule can exempt payment from selfemployment tax 49

50 S Corporation Distributions Basis Issues for Partnerships and S Corporations 50

51 Taxation of a Distribution (Not a Dividend) Return of capital up to basis in the stock Capital gain for any amounts in excess of basis

52 Tax Dividends Different from state law corporate dividends Treated as taxable income and do not affect basis Generally a corporation will treat distributions as dividends up to the amount of earnings and profits But S corporations interpose a special account known as the accumulated adjustments account 52

53 Accumulated Adjustments Account Is a corporate (not shareholder) account Relevant only for Treatment of S corporation distributions when corporation has earnings and profits In the post-termination transition period Generally impacted by same items as basis except for tax exempt income and deductions related to the same 53

54 S Corporation Tiers Accumulated Adjustments Account Treated as a distributions Recovery of basis, then gain Earnings and Profits Taxable as a dividend (Form 1099DIV) No affect on basis Distributions Back to recovery of basis Gain for exess 54

55 Earnings and Profits Only created now in C corporation years Computed on year by year basis See worksheet on Form 5452 Also have AICPA Corporations and Shareholders Tax Resource Panel practice guide 55

56 Distribution Elections Bypass AAA Deemed distribution from E&P Election to bypass PTI (extremely rare nowonly comes from pre-1982 earnings with pre shareholder) 56

57 Post Termination Transition Period One year after ceases to be S corporation 120 days from end of audit that changes S item 120 days from determination S status has been terminated 57

58 Sale of Interests/ Net Investement Income Tax Basis Issues for Partnerships and S Corporations 58

59 S Corporation Dispositions and Failures Worthless security rule Bad debt deduction issue Section 1244 stock 59

60 Partnership Interest Sale or Exchange Determination of gain or loss Character of gain or loss Hot asset rules come back with required reporting Potential for split holding period Installment sale of partnership interest 60

61 Gift of a Partnership Interest Partnership interest with liabilities Assignment of income issues Family partnership issues Charitable contributions 61

62 Abandonment 1990 Revenue Ruling can only get ordinary loss if there is no debt Otherwise a capital loss Still an issue on how Section 1234A affects this Tax Court says effectively can never abandon But Fifth Circuit overturned 62

63 Net Investment Income Tax General rules for partnerships General rules for S corporations Key issue is if the entity carries on a trade or business in which equity holder participates 63

64 1411 Reporting 64

S Corporations A Complete Guide

S Corporations A Complete Guide Edward K Zollars Phoenix, Arizona S Corporations A Complete Guide PARTNERSHIPS VS S CORPORATIONS 1 Comparison Background Formation of the Entity Basis Rules Ownership Taxable

S Corporations A Complete Guide Edward K Zollars Phoenix, Arizona S Corporations A Complete Guide PARTNERSHIPS VS S CORPORATIONS 1 Comparison Background Formation of the Entity Basis Rules Ownership Taxable

Pass Through Entities: Advanced Tax Issues. Edward K Zollars, CPA

Pass Through Entities: Advanced Tax Issues Edward K Zollars, CPA ed@tzlcpas.com Edward K Zollars Thomas, Zollars & Lynch, Ltd. Nichols Patrick CPE, Inc. Bisk Education (http://www.cpeasy.com) Arizona Income

Pass Through Entities: Advanced Tax Issues Edward K Zollars, CPA ed@tzlcpas.com Edward K Zollars Thomas, Zollars & Lynch, Ltd. Nichols Patrick CPE, Inc. Bisk Education (http://www.cpeasy.com) Arizona Income

2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE

& PARTNERSHIP FEDERAL TAX UPDATE") 2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE Gregory L. Gandy, CPA Tax Partner, BiggsKofford 630 Southpointe Court, Suite 200 Colorado Springs, CO 80906 719-579-9090 ggandy@biggskofford.com

2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE Gregory L. Gandy, CPA Tax Partner, BiggsKofford 630 Southpointe Court, Suite 200 Colorado Springs, CO 80906 719-579-9090 ggandy@biggskofford.com

Staff Tax Training Partnerships & LLCs (Form 1065) Case Solutions

Case Solutions") Staff Tax Training Partnerships & LLCs (Form 1065) Case Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution, even if there may be more than one way to solve

Staff Tax Training Partnerships & LLCs (Form 1065) Case Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution, even if there may be more than one way to solve

2016 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY. CPElite T.M. In a Class By Yourself T.M.

![2016 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY. CPElite T.M. In a Class By Yourself T.M.](/thumbs/78/78016337.jpg "2016 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY. CPElite T.M. In a Class By Yourself T.M.") 2016 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY CPElite T.M. In a Class By Yourself T.M. (800) 9500-CPE P.O. BOX 1059, CLEMSON, SC 29633-1059 & P.O. BOX 721, WHITE ROCK,

2016 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY CPElite T.M. In a Class By Yourself T.M. (800) 9500-CPE P.O. BOX 1059, CLEMSON, SC 29633-1059 & P.O. BOX 721, WHITE ROCK,

Chapter Two - Formation of a Corporation

Chapter Two - Formation of a Corporation Fundamental income tax elements: 1) Transferor: 351(a) - nonrecognition treatment applicable to the asset transferor (if certain conditions are met); otherwise:

Chapter Two - Formation of a Corporation Fundamental income tax elements: 1) Transferor: 351(a) - nonrecognition treatment applicable to the asset transferor (if certain conditions are met); otherwise:

Form 1065 Schedule K-1 Analysis Basis Calculations & Distributions for Partnerships & LLCs Case Suggested Solutions

Form 1065 Schedule K-1 Analysis Basis Calculations & Distributions for Partnerships & LLCs Case Suggested Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution,

Form 1065 Schedule K-1 Analysis Basis Calculations & Distributions for Partnerships & LLCs Case Suggested Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution,

Partnerships: The Fundamentals

American Bar Association Tax Section Partnerships: The Fundamentals January 28, 2016 Moderator: Michael Hirschfeld, Dechert LLP, New York, NY Alfred Bae, KPMG, San Francisco, CA Panelists Philip Hirschfeld,

American Bar Association Tax Section Partnerships: The Fundamentals January 28, 2016 Moderator: Michael Hirschfeld, Dechert LLP, New York, NY Alfred Bae, KPMG, San Francisco, CA Panelists Philip Hirschfeld,

2014 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY. CPElite T.M. In a Class By Yourself T.M.

![2014 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY. CPElite T.M. In a Class By Yourself T.M.](/thumbs/85/92439502.jpg "2014 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY. CPElite T.M. In a Class By Yourself T.M.") 2014 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY CPElite T.M. In a Class By Yourself T.M. (800) 9500-CPE P.O. BOX 1059, CLEMSON, SC 29633-1059 & P.O. BOX 721, WHITE ROCK,

2014 S CORPORATION TAXATION PART II Recommended CPE Credit: 6 HRS [B] PREPARED BY CPElite T.M. In a Class By Yourself T.M. (800) 9500-CPE P.O. BOX 1059, CLEMSON, SC 29633-1059 & P.O. BOX 721, WHITE ROCK,

Partnership Taxation and the Preparation of Form 1065

AA. Introduction to the Federal Income Tax Issues of Partnership Taxation and the Preparation of Form 1065 Paul La Monaca, CPA, MST NSTP Director of Education Legislative Change Effective for 2016 Form

AA. Introduction to the Federal Income Tax Issues of Partnership Taxation and the Preparation of Form 1065 Paul La Monaca, CPA, MST NSTP Director of Education Legislative Change Effective for 2016 Form

Corporate Tax Segment 3 Corporate Formation

Corporate Tax Segment 3 Corporate Formation University of Leiden International Tax Center May 2007 Professor William P. Streng University of Houston Law Center 4/30/2007 (c) William P. Streng 1 Formation

Corporate Tax Segment 3 Corporate Formation University of Leiden International Tax Center May 2007 Professor William P. Streng University of Houston Law Center 4/30/2007 (c) William P. Streng 1 Formation

Basis Calculations for Pass-Through Entities: Challenges for Tax Preparers

Basis Calculations for Pass-Through Entities: Challenges for Tax Preparers Tackling Complex Calculation Issues for S Corporations, Partnerships and LLCs TUESDAY, JANUARY 8, 2013, 1:00-2:50 pm Eastern IMPORTANT

Basis Calculations for Pass-Through Entities: Challenges for Tax Preparers Tackling Complex Calculation Issues for S Corporations, Partnerships and LLCs TUESDAY, JANUARY 8, 2013, 1:00-2:50 pm Eastern IMPORTANT

STRUCTURE. Schedule K consists of Sales COGS Rent G&A Salary Charity Capital Loss Net Income

SCORP STRUCTURE Operation and Separately stated items Distributions to shareholders AAA Account Health insurance premiums S Status Termination Built in gains tax Schedule K consists of Sales COGS Rent

SCORP STRUCTURE Operation and Separately stated items Distributions to shareholders AAA Account Health insurance premiums S Status Termination Built in gains tax Schedule K consists of Sales COGS Rent

Redemptions of Partnership Interests and Divisions of Partnerships

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Redemptions of Partnership Interests and

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Redemptions of Partnership Interests and

Making sense of taxes: The ABCs of MLPs. By: Shobana Gopal, CPA and Michelle Kelly, CFA Tortoise

Making sense of taxes: The ABCs of MLPs By: Shobana Gopal, CPA and Michelle Kelly, CFA 2 Making sense of taxes & MLPs Master Limited Partnerships (MLPs) have gained in popularity during the last decade.

Making sense of taxes: The ABCs of MLPs By: Shobana Gopal, CPA and Michelle Kelly, CFA 2 Making sense of taxes & MLPs Master Limited Partnerships (MLPs) have gained in popularity during the last decade.

Choice of Entity. Danny Santucci

Choice of Entity Danny Santucci Table of Contents Chapter 1 Sole Proprietorship... 1 Learning Objectives... 1 Introduction... 1 Advantages... 1 Disadvantages... 1 Formation... 1 Start-Up Expenses... 2

Choice of Entity Danny Santucci Table of Contents Chapter 1 Sole Proprietorship... 1 Learning Objectives... 1 Introduction... 1 Advantages... 1 Disadvantages... 1 Formation... 1 Start-Up Expenses... 2

Section 3 S Corporations Entity Tax Classification

Section 3 S Corporations Entity Tax Classification Business entities classification for tax purposes Check the box regulations Taxpaying entities Flow-through entities Corporations are C corporations unless

Section 3 S Corporations Entity Tax Classification Business entities classification for tax purposes Check the box regulations Taxpaying entities Flow-through entities Corporations are C corporations unless

Business Entities GENERAL PARTNERSHIP

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

SHORT VERSION S CORPORATION INCOME TAX RETURN CHECKLIST 2008 FORM 1120S

Client Name and Number: Prepared by: Date: Reviewed by: Date: 100) GENERAL INFORMATION 101) Consider obtaining signed:.1) Engagement letter..2) Engagement letter for tax advice under the CPA-client privilege

Client Name and Number: Prepared by: Date: Reviewed by: Date: 100) GENERAL INFORMATION 101) Consider obtaining signed:.1) Engagement letter..2) Engagement letter for tax advice under the CPA-client privilege

REG (Oct. 31, 2014) -- Proposed Regulations on Partner s Treatment of U/R and Inventory with Distributions

-- Proposed Regulations on Partner s Treatment of U/R and Inventory with Distributions") generating ordinary income to Alice of $20,000 ($25,000 - $5,000). 2 The fictional distribution of inventory reduced Alice s outside basis to $70,000 ($75,000 - $5,000); therefore, the remaining $75,000

generating ordinary income to Alice of $20,000 ($25,000 - $5,000). 2 The fictional distribution of inventory reduced Alice s outside basis to $70,000 ($75,000 - $5,000); therefore, the remaining $75,000

BASIC PARTNERSHIP TAX II SALES, DISGUISED SALES & TERMINATIONS

BASIC PARTNERSHIP TAX II SALES, DISGUISED SALES & TERMINATIONS TABLE CONTENTS PART I... 1 SALES & EXCHANGEs OF PARTNERSHIP INTERESTS... 1 A. General Rules Transferor/Selling Partner... 1 B. General Rules

BASIC PARTNERSHIP TAX II SALES, DISGUISED SALES & TERMINATIONS TABLE CONTENTS PART I... 1 SALES & EXCHANGEs OF PARTNERSHIP INTERESTS... 1 A. General Rules Transferor/Selling Partner... 1 B. General Rules

ESTATE PLANNING AND ADMINISTRATION FOR S CORPORATIONS

ESTATE PLANNING AND ADMINISTRATION FOR S CORPORATIONS I. INTRODUCTION... 1 II. ALLOCATING INCOME IN THE YEAR OF DEATH... 1 III. SHAREHOLDER ELIGIBILITY... 2 A. Estates... 2 B. Certain Trusts... 3 1. Grantor

ESTATE PLANNING AND ADMINISTRATION FOR S CORPORATIONS I. INTRODUCTION... 1 II. ALLOCATING INCOME IN THE YEAR OF DEATH... 1 III. SHAREHOLDER ELIGIBILITY... 2 A. Estates... 2 B. Certain Trusts... 3 1. Grantor

Form 1120-S Corporation Issues

Michigan Society of Enrolled Agents MiSEA Presents Form 1120-S Corporation Issues at the Bavarian Inn Lodge and Conference Center One Covered Bridge Lane Frankenmuth, Michigan on November 13, 2017 Course

Michigan Society of Enrolled Agents MiSEA Presents Form 1120-S Corporation Issues at the Bavarian Inn Lodge and Conference Center One Covered Bridge Lane Frankenmuth, Michigan on November 13, 2017 Course

Business Entities GENERAL PARTNERSHIP

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

Hot Topics in Partnership Taxation

Hot Topics in Partnership Taxation New York State Bar (Tax Section) Annual Meeting James B. Sowell, Principal Washington National Tax Notice The following information is not intended to be written advice

Hot Topics in Partnership Taxation New York State Bar (Tax Section) Annual Meeting James B. Sowell, Principal Washington National Tax Notice The following information is not intended to be written advice

DISREGARDED ENTITIES AND PARTNERSHIP LIABILITY ALLOCATIONS: PROPOSED REGS CRITIQUED

DISREGARDED ENTITIES AND PARTNERSHIP LIABILITY ALLOCATIONS: PROPOSED REGS CRITIQUED By Blake D. Rubin and Andrea Macintosh Whiteway Blake D. Rubin and Andrea Macintosh Whiteway are partners with Arnold

DISREGARDED ENTITIES AND PARTNERSHIP LIABILITY ALLOCATIONS: PROPOSED REGS CRITIQUED By Blake D. Rubin and Andrea Macintosh Whiteway Blake D. Rubin and Andrea Macintosh Whiteway are partners with Arnold

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS LECTURE NOTES

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS 10.1 FORMS OF DOING BUSINESS LECTURE NOTES 1. Legal Forms. Business entities can be organized into the following principal legal forms. Sole proprietorship.

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS 10.1 FORMS OF DOING BUSINESS LECTURE NOTES 1. Legal Forms. Business entities can be organized into the following principal legal forms. Sole proprietorship.

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Structuring Contributions of Appreciated Property to Partnerships: Avoiding Tax Recognition on Built-in Gain Assets Navigating Allocation Challenges,

Presenting a live 90-minute webinar with interactive Q&A Structuring Contributions of Appreciated Property to Partnerships: Avoiding Tax Recognition on Built-in Gain Assets Navigating Allocation Challenges,

New Partnership Liability and Disguised Sale Regulations

Tax Alert October 11, 2016 Key Points Final, temporary and proposed regulations issued on October 5, 2016, address complex rules dealing with partnership disguised sales and debt allocation rules under

Tax Alert October 11, 2016 Key Points Final, temporary and proposed regulations issued on October 5, 2016, address complex rules dealing with partnership disguised sales and debt allocation rules under

Federal Taxation on Disposition of Partnership Interests

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1994 Federal Taxation on Disposition of Partnership

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1994 Federal Taxation on Disposition of Partnership

PASS THROUGH BUSINESS UPDATES

PASS THROUGH BUSINESS UPDATES A Pass Through Entity (PTE) includes the following: A partnership p as defined in the Pennsylvan nia Statue at 72 P.S. 7301(n.0): Partnership means a domestic or foreign

PASS THROUGH BUSINESS UPDATES A Pass Through Entity (PTE) includes the following: A partnership p as defined in the Pennsylvan nia Statue at 72 P.S. 7301(n.0): Partnership means a domestic or foreign

A CPA s Guide to Trusts

A CPA s Guide to Trusts Edward K. Zollars, CPA Phoenix, Arizona ed@tzlcpas.com www.cperesources.com CPA s Guide to Trusts KEY PLAYERS IN A TRUST 1 Purposes of Trusts Parties Involved in a Trust 2 Advisers

A CPA s Guide to Trusts Edward K. Zollars, CPA Phoenix, Arizona ed@tzlcpas.com www.cperesources.com CPA s Guide to Trusts KEY PLAYERS IN A TRUST 1 Purposes of Trusts Parties Involved in a Trust 2 Advisers

2016 S CORPORATION INCOME TAX RETURN CHECKLIST (form 1120S) (SHORT)

(SHORT)") Client name and number: Prepared by: Date: Reviewed by: Date: 100) GENERAL 101) Identify the authorized officer who will sign the return. 102) Obtain a signed engagement letter. 103) Confirm the taxpayer

Client name and number: Prepared by: Date: Reviewed by: Date: 100) GENERAL 101) Identify the authorized officer who will sign the return. 102) Obtain a signed engagement letter. 103) Confirm the taxpayer

Basis Calculations & Distributions for Pass-Thru Entities Case Suggested Solutions

Calculations & Distributions for Pass-Thru Entities Case Suggested Solutions Suggested Solution Disclaimer All problems, exercises, activities, etc., have at least one suggested solution, even if there

Calculations & Distributions for Pass-Thru Entities Case Suggested Solutions Suggested Solution Disclaimer All problems, exercises, activities, etc., have at least one suggested solution, even if there

26th Annual Health Sciences Tax Conference

26th Annual Health Sciences Tax Conference Partnerships and joint ventures: M&A, current developments and JVs with exempt organizations December 7, 2016 Disclaimer EY refers to the global organization,

26th Annual Health Sciences Tax Conference Partnerships and joint ventures: M&A, current developments and JVs with exempt organizations December 7, 2016 Disclaimer EY refers to the global organization,

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

Instructions for PA-20S/PA-65 Schedule NRK-1 Nonresident Schedule of Shareholder/Partner/Beneficiary Pass Through Income, Loss and Credits

Pennsylvania Department of Revenue 2012 Instructions for PA-20S/PA-65 Schedule NRK-1 Nonresident Schedule of Shareholder/Partner/Beneficiary Pass Through Income, Loss and Credits What s New PA Account

Pennsylvania Department of Revenue 2012 Instructions for PA-20S/PA-65 Schedule NRK-1 Nonresident Schedule of Shareholder/Partner/Beneficiary Pass Through Income, Loss and Credits What s New PA Account

Tax Planning and Compliance for Closely Held Businesses and Their Owners. Edward K. Zollars Phoenix, Arizona

Tax Planning and Compliance for Closely Held Businesses and Their Owners Edward K. Zollars Phoenix, Arizona ed@tzlcpas.com www.cperesources.com Edward K Zollars Email: ed@tzlcpas.com Website: www.cperesources.com

Tax Planning and Compliance for Closely Held Businesses and Their Owners Edward K. Zollars Phoenix, Arizona ed@tzlcpas.com www.cperesources.com Edward K Zollars Email: ed@tzlcpas.com Website: www.cperesources.com

Corporate Taxation Chapter Two: Corporate Formation

Presentation: Corporate Taxation Chapter Two: Corporate Formation Professors Wells January 21, 2015 Key Statutory Provision: 351, 357, 358, 362, 368(c), 1032, 1223(1), 1223(2), 1245(b)(3), 118, 195, 212(3),

Presentation: Corporate Taxation Chapter Two: Corporate Formation Professors Wells January 21, 2015 Key Statutory Provision: 351, 357, 358, 362, 368(c), 1032, 1223(1), 1223(2), 1245(b)(3), 118, 195, 212(3),

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1065 Deskbook. Twenty-seventh Edition (October 2016)

") Route To: j Partners j Managers j Staff j File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1065 Deskbook Twenty-seventh Edition (October 2016) Highlights of this Edition The following are some of the

Route To: j Partners j Managers j Staff j File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1065 Deskbook Twenty-seventh Edition (October 2016) Highlights of this Edition The following are some of the

THE UNEXPECTED CURVE THE ESTATE OF COSTANZA AND ITS IMPACT ON SELF CANCELING INSTALLMENT NOTES

THE UNEXPECTED CURVE THE ESTATE OF COSTANZA AND ITS IMPACT ON SELF CANCELING INSTALLMENT NOTES By: Richard F. Roth I. CREATIVE FINANCING A. The future of estate tax in question. B. The future of gift tax

THE UNEXPECTED CURVE THE ESTATE OF COSTANZA AND ITS IMPACT ON SELF CANCELING INSTALLMENT NOTES By: Richard F. Roth I. CREATIVE FINANCING A. The future of estate tax in question. B. The future of gift tax

CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM!

CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! REG: C-CORP ANOTHER QUALITY BOOK FROM CPA-PLANET This book is for anyone studying for the

CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! REG: C-CORP ANOTHER QUALITY BOOK FROM CPA-PLANET This book is for anyone studying for the

Tax reform and the choice of business entity

The Adviser s Guide to Financial and Estate Planning: Tax reform and the choice of business entity Presented by: Steven G. Siegel, JD, LLM About the PFP Section & PFS Credential The AICPA Personal Financial

The Adviser s Guide to Financial and Estate Planning: Tax reform and the choice of business entity Presented by: Steven G. Siegel, JD, LLM About the PFP Section & PFS Credential The AICPA Personal Financial

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Page What s New. Type Here S-Corporation Taxes at the Entity Level 1

Page 257-272 What s New Type Here 13 - S-Corporation Taxes at the Entity Level 1 The PATH Act: A. Permanently limited the recognition period for the BIG to 5 years. B. Temporarily extended the recognition

Page 257-272 What s New Type Here 13 - S-Corporation Taxes at the Entity Level 1 The PATH Act: A. Permanently limited the recognition period for the BIG to 5 years. B. Temporarily extended the recognition

2017 National Conference on Special Needs Planning. Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J.

2017 National Conference on Special Needs Planning and Special Needs Trusts Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J. Frigon Law Offices of Bradley J. Frigon 6500

2017 National Conference on Special Needs Planning and Special Needs Trusts Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J. Frigon Law Offices of Bradley J. Frigon 6500

Reforming Subchapter K

Reforming Subchapter K University of Chicago Tax Conference Stuart Rosow Eric Solomon Stephen Rose Jennifer Alexander November 7, 2015 Introduction Flexibility and Fairness Administrability The current

Reforming Subchapter K University of Chicago Tax Conference Stuart Rosow Eric Solomon Stephen Rose Jennifer Alexander November 7, 2015 Introduction Flexibility and Fairness Administrability The current

CHAPTER 22 NONLIQUIDATING DISTRIBUTIONS. Problems, page 684

204 CHAPTER 22 NONLIQUIDATING DISTRIBUTIONS Problems, page 684 22-1. X does not recognize gain on the distribution because the amount of cash distributed is less than X's outside basis immediately before

204 CHAPTER 22 NONLIQUIDATING DISTRIBUTIONS Problems, page 684 22-1. X does not recognize gain on the distribution because the amount of cash distributed is less than X's outside basis immediately before

United States Tax Alert Transition tax guidance: proposed regulations released

International Tax 10 August 2018 United States Tax Alert Transition tax guidance: proposed regulations released On August 1, 2018, Treasury and the IRS released proposed regulations (the Proposed Regulations

International Tax 10 August 2018 United States Tax Alert Transition tax guidance: proposed regulations released On August 1, 2018, Treasury and the IRS released proposed regulations (the Proposed Regulations

June 5, Mr. Daniel I. Werfel Acting Commissioner Internal Revenue Service 1111 Constitution Avenue, Room 3000 Washington, DC 20024

June 5, 2013 Mr. Daniel I. Werfel Acting Commissioner Internal Revenue Service 1111 Constitution Avenue, Room 3000 Washington, DC 20024 Re: Comments on Revenue Ruling 99-5 Dear Mr. Werfel: The American

June 5, 2013 Mr. Daniel I. Werfel Acting Commissioner Internal Revenue Service 1111 Constitution Avenue, Room 3000 Washington, DC 20024 Re: Comments on Revenue Ruling 99-5 Dear Mr. Werfel: The American

Purchase and Sale of Interests; Asset and Stock Acquisitions; Redemptions; and Terminations in Pass-Through Entities

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1994 Purchase and Sale of Interests; Asset and

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1994 Purchase and Sale of Interests; Asset and

A Look at the Final Section 2053 Regulations

A PROFESSIONAL CORPORATION ATTORNEYS AT LAW A Look at the Final Section 2053 Regulations 2009 by Jonathan G. Blattmachr & Mitchell M. Gans All Rights Reserved. Introduction As a general rule, expenses

A PROFESSIONAL CORPORATION ATTORNEYS AT LAW A Look at the Final Section 2053 Regulations 2009 by Jonathan G. Blattmachr & Mitchell M. Gans All Rights Reserved. Introduction As a general rule, expenses

Partnerships. Internal Revenue Service Market Segment Specialization Program. Audit Technique Guide (ATG)

") Internal Revenue Service Market Segment Specialization Program Partnerships Audit Technique Guide (ATG) NOTE: This guide is current through the publication date. Since changes may have occurred after the

Internal Revenue Service Market Segment Specialization Program Partnerships Audit Technique Guide (ATG) NOTE: This guide is current through the publication date. Since changes may have occurred after the

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Copyright 2015 Carolina Academic Press, LLC. All rights reserved. UNDERSTANDING TAXATION OF BUSINESS ENTITIES

UNDERSTANDING TAXATION OF BUSINESS ENTITIES LexisNexis Law School Publishing Advisory Board Bridgette Carr Clinical Professor of LawUniversity of Michigan Law School Steven I. Friedland Professor of Law

UNDERSTANDING TAXATION OF BUSINESS ENTITIES LexisNexis Law School Publishing Advisory Board Bridgette Carr Clinical Professor of LawUniversity of Michigan Law School Steven I. Friedland Professor of Law

Tax Strategies for Real Estate LLC and LP Agreements: Capital Commitments, Tax Allocations and Distributions, and More

Presenting a live 90-minute webinar with interactive Q&A Tax Strategies for Real Estate LLC and LP Agreements: Capital Commitments, Tax Allocations and Distributions, and More TUESDAY, APRIL 3, 2018 1pm

Presenting a live 90-minute webinar with interactive Q&A Tax Strategies for Real Estate LLC and LP Agreements: Capital Commitments, Tax Allocations and Distributions, and More TUESDAY, APRIL 3, 2018 1pm

Tax Management. Real Estate Journal

Tax Management Real Estate Journal Reproduced with permission from, Vol. 32, 2, p. 31, 02/03/2016. Copyright 2016 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Partnership Property

Tax Management Real Estate Journal Reproduced with permission from, Vol. 32, 2, p. 31, 02/03/2016. Copyright 2016 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Partnership Property

2017 Deloitte Renewable Energy Seminar Innovating for tomorrow November 13-15, 2017

2017 Deloitte Renewable Energy Seminar Innovating for tomorrow November 13-15, 2017 Michael Kohler, Managing Director, Deloitte Tax LLP Tom Stevens, Partner, Deloitte Tax LLP Partnership flip structure:

2017 Deloitte Renewable Energy Seminar Innovating for tomorrow November 13-15, 2017 Michael Kohler, Managing Director, Deloitte Tax LLP Tom Stevens, Partner, Deloitte Tax LLP Partnership flip structure:

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

capital gains and dividend income

capital gains and dividend income Managing capital gains and losses can help you save taxes, defer taxes and obtain the highest after-tax yield on your assets. This planning is very critical when considering

capital gains and dividend income Managing capital gains and losses can help you save taxes, defer taxes and obtain the highest after-tax yield on your assets. This planning is very critical when considering

Choice of Entity. 69 th Annual Program of the West Virginia Tax Institute October 28-30, 2018 Marriott Morgantown Morgantown, West Virginia

Choice of Entity 69 th Annual Program of the West Virginia Tax Institute October 28-30, 2018 Marriott Morgantown Morgantown, West Virginia John F. Allevato Spilman Thomas & Battle, PLLC 300 Kanawha Boulevard,

Choice of Entity 69 th Annual Program of the West Virginia Tax Institute October 28-30, 2018 Marriott Morgantown Morgantown, West Virginia John F. Allevato Spilman Thomas & Battle, PLLC 300 Kanawha Boulevard,

Partnership Flip Structuring Tax Perspectives. Tom Stevens Bill O Shea Deloitte Tax LLP

Partnership Flip Structuring Tax Perspectives Tom Stevens tstevens@deloitte.com Bill O Shea woshea@deloitte.com Deloitte Tax LLP September 29, 2015 Tax Incentives are Integral to Project Economics What

Partnership Flip Structuring Tax Perspectives Tom Stevens tstevens@deloitte.com Bill O Shea woshea@deloitte.com Deloitte Tax LLP September 29, 2015 Tax Incentives are Integral to Project Economics What

Income Tax Update for Community Banks

Income Tax Update for Community Banks Tuesday December 9, 2014 Beverly Seier Shareholder, Elliott Davis 2013 Elliott Davis, PLLC 2013 Elliott Davis, LLC This material was used by Elliott Davis during an

Income Tax Update for Community Banks Tuesday December 9, 2014 Beverly Seier Shareholder, Elliott Davis 2013 Elliott Davis, PLLC 2013 Elliott Davis, LLC This material was used by Elliott Davis during an

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING. Jenny Coates Law, PLLC, International Tax Lawyer

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance

Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance") Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Reverse 704(c) Allocations: Partnership Revaluations, Triggering Events, and Recent IRS Guidance FOR LIVE PROGRAM ONLY WEDNESDAY, JANUARY 10, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

THE REGULATIONS GOVERNING INTERCOMPANY TRANSACTIONS WITHIN CONSOLIDATED GROUPS. August Mark J. Silverman Steptoe & Johnson LLP Washington, D.C.

PRACTISING LAW INSTITUTE TAX STRATEGIES FOR CORPORATE ACQUISITIONS, DISPOSITIONS, SPIN-OFFS, JOINT VENTURES FINANCINGS, REORGANIZATIONS AND RESTRUCTURINGS 2001 THE REGULATIONS GOVERNING INTERCOMPANY TRANSACTIONS

PRACTISING LAW INSTITUTE TAX STRATEGIES FOR CORPORATE ACQUISITIONS, DISPOSITIONS, SPIN-OFFS, JOINT VENTURES FINANCINGS, REORGANIZATIONS AND RESTRUCTURINGS 2001 THE REGULATIONS GOVERNING INTERCOMPANY TRANSACTIONS

Corporate Formations and Capital Structure

Learning Objectives Chapter C:2 Corporate Formations and Capital Structure After studying this chapter, the student should be able to: 1. Explain the tax advantages and disadvantages of using each of the

Learning Objectives Chapter C:2 Corporate Formations and Capital Structure After studying this chapter, the student should be able to: 1. Explain the tax advantages and disadvantages of using each of the

Partnership Issues in International Tax Planning Tax Executives Institute February 16, 2015

www.pwc.com Partnership Issues in International Tax Planning Tax Executives Institute Instructors Craig Gerson WNTS Principal Craig Gerson recently rejoined as a Principal in the Mergers and Acquisitions

www.pwc.com Partnership Issues in International Tax Planning Tax Executives Institute Instructors Craig Gerson WNTS Principal Craig Gerson recently rejoined as a Principal in the Mergers and Acquisitions

Re: Comments on Notice , Section 704(c) Layers relating to Partnership Mergers, Divisions and Tiered Partnerships

Layers relating to Partnership Mergers, Divisions and Tiered Partnerships") April 30, 2010 The Honorable William J. Wilkins IRS Chief Counsel Internal Revenue Service 1111 Constitution Avenue, Room Washington, DC 20224 VIA E-MAIL: Notice.comments@irscounsel.treas.gov Re: Comments

April 30, 2010 The Honorable William J. Wilkins IRS Chief Counsel Internal Revenue Service 1111 Constitution Avenue, Room Washington, DC 20224 VIA E-MAIL: Notice.comments@irscounsel.treas.gov Re: Comments

I Want Out Tax Considerations In Exiting a Partnership

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2013 I Want Out Tax Considerations In Exiting

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2013 I Want Out Tax Considerations In Exiting

PROSHARES SAMPLE TAX PACKAGE 7501 WISCONSIN AVE SUITE 1000 BETHESDA, MD PROSHARES. K-1 Account Number:

PROSHARES 750 WISCONSIN AVE SUITE 000 BETHESDA, MD 2084 PROSHARES K- Account Number: 207 SCHEDULE K- SUPPLEMENTAL INFORMATION % of the amount of interest income included on your Schedule K- is from US

PROSHARES 750 WISCONSIN AVE SUITE 000 BETHESDA, MD 2084 PROSHARES K- Account Number: 207 SCHEDULE K- SUPPLEMENTAL INFORMATION % of the amount of interest income included on your Schedule K- is from US

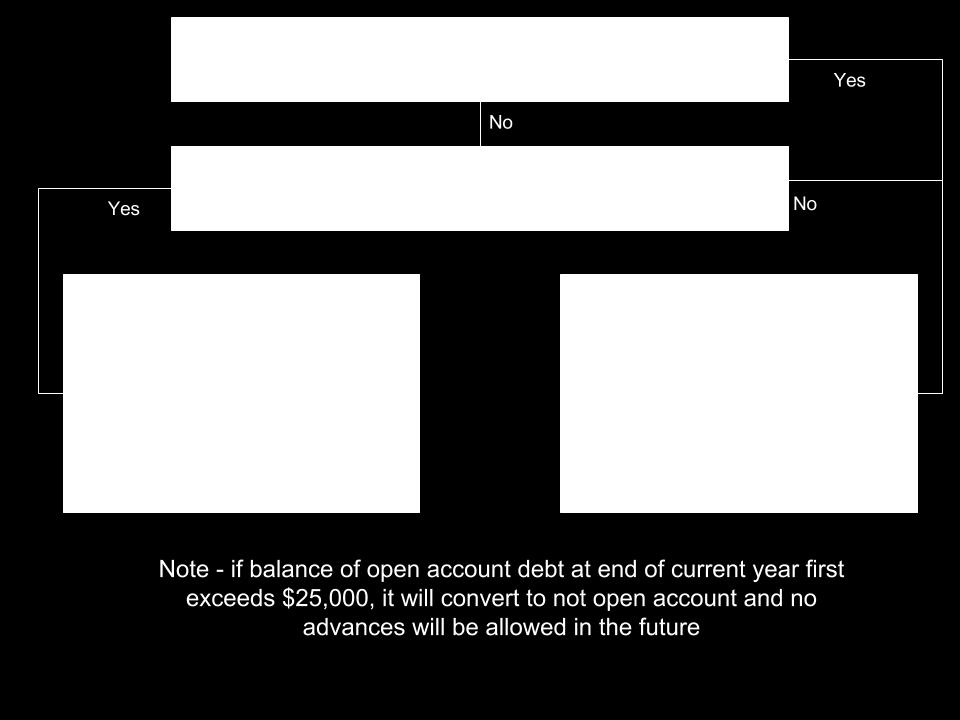

Section. 754 Election. With Distributions

Section 754 Election With Distributions 76 1 754 Election Activates Sec. 743 Sales, Exchanges, Deaths Sec. 734 Distributions 2 Two Upward Adjustment Triggers in Sec. 734 3 1) Distributee recognizes sec.

Section 754 Election With Distributions 76 1 754 Election Activates Sec. 743 Sales, Exchanges, Deaths Sec. 734 Distributions 2 Two Upward Adjustment Triggers in Sec. 734 3 1) Distributee recognizes sec.

S Corporation Shareholder Basis. Losses Claimed in Excess of Basis

S Corporation Shareholder Basis Losses Claimed in Excess of Basis Campaign Description S corporation shareholders must track adjustments to their basis in S corporation stock and debt to avoid improperly

S Corporation Shareholder Basis Losses Claimed in Excess of Basis Campaign Description S corporation shareholders must track adjustments to their basis in S corporation stock and debt to avoid improperly

TAX ASPECTS OF DEBT RESTRUCTURING, WORKOUTS & FORECLOSURE May 2004

TAX ASPECTS OF DEBT RESTRUCTURING, WORKOUTS & FORECLOSURE May 2004 WENDI L. KOTZEN BALLARD SPAHR ANDREWS & INGERSOLL, LLP 1735 Market Street, 51 st Floor Philadelphia, PA 19103-7599 kotzenw@ballardspahr.com

TAX ASPECTS OF DEBT RESTRUCTURING, WORKOUTS & FORECLOSURE May 2004 WENDI L. KOTZEN BALLARD SPAHR ANDREWS & INGERSOLL, LLP 1735 Market Street, 51 st Floor Philadelphia, PA 19103-7599 kotzenw@ballardspahr.com

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law

, CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law") EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

General Rule Capital Gain or Loss. Sec Example 12-1 Sale. General rule: a sale by a partner generates capital gain or loss.

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

October 31, Summary of Opportunity Zone Proposed Regulations. Table of Contents

Schuyler M. Moore D: 310.201.7559 F: 310.201.4444 SMoore@ggfirm.com October 31, 2018 To Colleagues, Friends, and Clients: Re: Summary of Opportunity Zone Proposed Regulations This letter provides a summary

Schuyler M. Moore D: 310.201.7559 F: 310.201.4444 SMoore@ggfirm.com October 31, 2018 To Colleagues, Friends, and Clients: Re: Summary of Opportunity Zone Proposed Regulations This letter provides a summary

Business Interests: Planning Considerations

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Capital Gain or Loss. Pub 4012 Tab D Pub 4491 Lesson 11

Capital Gain or Loss Pub 4012 Tab D Pub 4491 Lesson 11 Introduction Ordinary income tax rates range from 10% to 37% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very

Capital Gain or Loss Pub 4012 Tab D Pub 4491 Lesson 11 Introduction Ordinary income tax rates range from 10% to 37% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very

Tax Considerations in Buying or Selling a Business

Tax Considerations in Buying or Selling a Business By Charles A. Wry, Jr. @MorseBarnes Boston, MA Cambridge, MA Waltham, MA mbbp.com This article is not intended to constitute legal or tax advice and cannot

Tax Considerations in Buying or Selling a Business By Charles A. Wry, Jr. @MorseBarnes Boston, MA Cambridge, MA Waltham, MA mbbp.com This article is not intended to constitute legal or tax advice and cannot

FILING DEADLINES EXTENDED

IRS Depa r t ment s Tax Relief Provisions for Disaster Losses Shirley Dennis-Escoffier Weather-related casualty losses have been on the increase with Hurricanes Harvey, Irma, and Maria recently leaving

IRS Depa r t ment s Tax Relief Provisions for Disaster Losses Shirley Dennis-Escoffier Weather-related casualty losses have been on the increase with Hurricanes Harvey, Irma, and Maria recently leaving

IRS issues regulations on disguised sales of property and allocations of partnership liabilities

Partnerships & Joint Ventures IRS issues regulations on disguised sales of property and allocations of partnership liabilities The IRS has issued final (TD 9787), final and temporary (TD 9788), and proposed

Partnerships & Joint Ventures IRS issues regulations on disguised sales of property and allocations of partnership liabilities The IRS has issued final (TD 9787), final and temporary (TD 9788), and proposed

MLP Tax Technical Seminar

www.pwc.com MLP Tax Technical Seminar Back to the Basics: MLP Fundamentals April 19-20, 2017 Agenda Session 1 Introduction & Overview 2 Economic Effect and Substantiality 3 Partner s Interest in the Partnership

www.pwc.com MLP Tax Technical Seminar Back to the Basics: MLP Fundamentals April 19-20, 2017 Agenda Session 1 Introduction & Overview 2 Economic Effect and Substantiality 3 Partner s Interest in the Partnership

By Deborah Fields, Holly Belanger and Eric Lee*

May 2010 Triangles in a World of Squares: A Primer on Significant U.S. Federal Income Tax Issues for Natural Resources Publicly Traded Partnerships (Part III Bringing in the Public and Management and Partnership

May 2010 Triangles in a World of Squares: A Primer on Significant U.S. Federal Income Tax Issues for Natural Resources Publicly Traded Partnerships (Part III Bringing in the Public and Management and Partnership

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

IAS 16 Property, Plant and Equipment

IAS 16 Property, Plant and Equipment How do we recognise them on initial recognition? At cost! So, what is cost? Cost includes: purchase price import duties and non-refundable purchase taxes LESS: trade

IAS 16 Property, Plant and Equipment How do we recognise them on initial recognition? At cost! So, what is cost? Cost includes: purchase price import duties and non-refundable purchase taxes LESS: trade

Partnership Workouts Hot Topics Addendum

Partnership Workouts Hot Topics Addendum A. Section 108(e)(8) Application to Partnerships 1. In General. Code Section 108(e)(8) was expanded in 2004 to include discharges of partnership indebtedness. [Prior

Partnership Workouts Hot Topics Addendum A. Section 108(e)(8) Application to Partnerships 1. In General. Code Section 108(e)(8) was expanded in 2004 to include discharges of partnership indebtedness. [Prior

University of Akron MTax Direct Melanie McCoskey, Ph.D., CPA Module 1 Corporate Formation

University of Akron MTax Direct Melanie McCoskey, Ph.D., CPA mmccoskey@uakron.edu 330.972.6930 Module 1 Corporate Formation May 4, 2015 2 Overview of Chapter Corporate Formation Effect on corp» Gain/loss

University of Akron MTax Direct Melanie McCoskey, Ph.D., CPA mmccoskey@uakron.edu 330.972.6930 Module 1 Corporate Formation May 4, 2015 2 Overview of Chapter Corporate Formation Effect on corp» Gain/loss

Listed Transactions. Basket Option Contracts

Listed Transactions Basket Option Contracts These are transactions designed to defer or change the character of income recognition. They typically involve a taxpayer entering into an option contract to

Listed Transactions Basket Option Contracts These are transactions designed to defer or change the character of income recognition. They typically involve a taxpayer entering into an option contract to

January 29, RE: Request for Immediate Guidance Regarding Pub. L. No Dear Messrs. Kautter and Paul:

January 29, 2018 The Honorable David J. Kautter Assistant Secretary for Tax Policy Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Mr. William M. Paul Principal Deputy Chief

January 29, 2018 The Honorable David J. Kautter Assistant Secretary for Tax Policy Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Mr. William M. Paul Principal Deputy Chief

Capital Gain or Loss. Form 1040 Line 13 Pub 4012 Tab D Pages Pub 4491 Part 3 Lesson 11

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Practising Law Institute

Practising Law Institute Tax Planning For Domestic & Foreign Partnerships, LLCs, Joint Ventures & Other Strategic Alliances 2016 International Joint Venture Issues Paul Oosterhuis Skadden, Arps, Slate,

Practising Law Institute Tax Planning For Domestic & Foreign Partnerships, LLCs, Joint Ventures & Other Strategic Alliances 2016 International Joint Venture Issues Paul Oosterhuis Skadden, Arps, Slate,

Partnership Basis and Distributions: Navigating Sections , 751(b) and 755

and 755") Presenting a live 110-minute teleconference with interactive Q&A Partnership Basis and Distributions: Navigating Sections 731-737, 751(b) and 755 WEDNESDAY, JULY 17, 2013 1pm Eastern 12pm Central 11am

Presenting a live 110-minute teleconference with interactive Q&A Partnership Basis and Distributions: Navigating Sections 731-737, 751(b) and 755 WEDNESDAY, JULY 17, 2013 1pm Eastern 12pm Central 11am

Charitable Remainder Unitrust. Planned Charitable Giving Using a Split-Interest Trust

Charitable Remainder Unitrust Planned Charitable Giving Using a Split-Interest Trust CRUT Overview Lifetime transfer of cash or property in trust in exchange for unitrust interest payable over (a) Fixed

Charitable Remainder Unitrust Planned Charitable Giving Using a Split-Interest Trust CRUT Overview Lifetime transfer of cash or property in trust in exchange for unitrust interest payable over (a) Fixed

Tax Considerations in Buying or Selling a Business

Tax Considerations in Buying or Selling a Business By Charles A. Wry, Jr. mbbp.com Corporate IP Licensing & Strategic Alliances Employment & Immigration Taxation 781-622-5930 CityPoint 230 Third Avenue,

Tax Considerations in Buying or Selling a Business By Charles A. Wry, Jr. mbbp.com Corporate IP Licensing & Strategic Alliances Employment & Immigration Taxation 781-622-5930 CityPoint 230 Third Avenue,

Chapter 15 Taxation of S Corporations

Chapter 15 Taxation of S Corporations "Tax Option" corporations/subchapter S. Fundamental inquiry: Should the corporation (as an entity) be subject to any federal income tax? Alternatively, should the

Chapter 15 Taxation of S Corporations "Tax Option" corporations/subchapter S. Fundamental inquiry: Should the corporation (as an entity) be subject to any federal income tax? Alternatively, should the

Corporate Taxation Chapter Eight: Taxable Acquisitions

Presentation: Corporate Taxation Chapter Eight: Taxable Acquisitions Professors Wells March 9, 2015 Chapter 8 Taxable Corporate Acquisitions/Dispositions Corporate ownership disposition options: 1) Sale

Presentation: Corporate Taxation Chapter Eight: Taxable Acquisitions Professors Wells March 9, 2015 Chapter 8 Taxable Corporate Acquisitions/Dispositions Corporate ownership disposition options: 1) Sale