The Marginal Propensity to Consume Out of Credit: Deniz Aydın

|

|

|

- Dominick Barton

- 6 years ago

- Views:

Transcription

1 The Marginal Propensity to Consume Out of Credit: Evidence from Random Assignment of 54,522 Credit Lines Deniz Aydın WUSTL

2 Marginal Propensity to Consume /Credit Question: By how much does household expenditure increase, if credit lines are increased by 1$?

3 Marginal Propensity to Consume /Credit Question: By how much does household expenditure increase, if credit lines are increased by 1$? Answer distinguishes competing intertemporal models, ranging from the permanent income hypothesis to rule-of-thumb.

4 Marginal Propensity to Consume /Credit Question: By how much does household expenditure increase, if credit lines are increased by 1$? Answer distinguishes competing intertemporal models, ranging from the permanent income hypothesis to rule-of-thumb. Answer matters for understanding macroeconomic fluctuations through financial sector linkages, and formulating monetary, fiscal, macroprudential policy to offset them.

5 Marginal Propensity to Consume /Credit Question: By how much does household expenditure increase, if credit lines are increased by 1$? Answer distinguishes competing intertemporal models, ranging from the permanent income hypothesis to rule-of-thumb. Answer matters for understanding macroeconomic fluctuations through financial sector linkages, and formulating monetary, fiscal, macroprudential policy to offset them. Proven difficult to identify, due to lack of comprehensive micro data on households variables, and a pervasive orthogonalization problem of credit supply.

6 1. Measure the magnitude, heterogeneity and composition of the marginal propensity to consume out of credit i.e. the spending response to a 1$ increase in credit availability.

7 1. Measure the magnitude, heterogeneity and composition of the marginal propensity to consume out of credit i.e. the spending response to a 1$ increase in credit availability. Design a field experiment of unique size (N = 54, 522) and randomized nature, where credit lines are varied.

8 Event Study Note. Figure plots average interest bearing credit card debt at bank, D t. Levels normalized by pre-intervention values, D 1.

9 1. Measure the magnitude, heterogeneity and composition of the marginal propensity to consume out of credit i.e. the spending response to a 1$ increase in credit availability. Design a field experiment of unique size (N = 54, 522) and randomized nature, where credit lines are varied. Use in conjunction with comprehensive administrative data on income, spending, balance sheets and untapped credit.

10 1. Measure the magnitude, heterogeneity and composition of the marginal propensity to consume out of credit i.e. the spending response to a 1$ increase in credit availability. Design a field experiment of unique size (N = 54, 522) and randomized nature, where credit lines are varied. Use in conjunction with comprehensive administrative data on income, spending, balance sheets and untapped credit. Complement literature on consumption response to income shocks Cochrane (1991) Johnson et al. (2006) Blundell et al. (2008) Baker (2013) This paper: Large sample + RCT! Precise/robust estimates Improve literature on borrowing response to credit shocks Gross and Souleles (2002) Agarwal et al. (2015) This paper: Balance sheet correlates, spending patterns

11 2. Use the empirical findings to test competing predictions of models of intertemporal behavior. Friedman (1957) Bewley (1977) Campbell and Mankiw (1989) Deaton (1991) Carroll (1997) Laibson (1997) Gourinchas and Parker (2002) Kaplan and Violante (2014)

12 2. Use the empirical findings to test competing predictions of models of intertemporal behavior. Friedman (1957) Bewley (1977) Campbell and Mankiw (1989) Deaton (1991) Carroll (1997) Laibson (1997) Gourinchas and Parker (2002) Kaplan and Violante (2014) & a buffer-stock model with illiquid durables and one-sided adjustment costs is consistent many aspects of the MPC quantitatively.

13 2. Use the empirical findings to test competing predictions of models of intertemporal behavior. Friedman (1957) Bewley (1977) Campbell and Mankiw (1989) Deaton (1991) Carroll (1997) Laibson (1997) Gourinchas and Parker (2002) Kaplan and Violante (2014) & a buffer-stock model with illiquid durables and one-sided adjustment costs is consistent many aspects of the MPC quantitatively. 3. Discuss implications for Consumption booms and household leveraging Hall (2011) Eggertsson and Krugman (2012) Guerrieri and Lorenzoni (2015) Fiscal, monetary and macroprudential policy Jappelli and Pistaferri (2014) Auclert (2015) Korinek and Simsek (2015) Welfare in credit markets Kaboski and Townsend (2011)

14 Data I European retail bank I I I I I I Credit card variables Categorized expenditures Balance sheet: Liquid assets and debt Credit bureau information Labor income Demographics I Sample size: 10+ million I Unit of analysis is an individual and frequency is monthly. See Credit card market See Installment contract

15 The Randomized Trial I Experiment participants (N=54,522) Pre-existing cardholders approved for a credit line increase See Sampling

16 Credit supply function I How the experiment participants are selected. # Type Variable Range Cutoff (1) Profitability Expected value added (-, ) 0 (2) CRM Months since limit increase [0, ) > 6 (3) Months card open [0, ) > 2 (4) Risk Behavior score [100, 800] < 180 (5) Customer score [100, 800] < 180 (6) Credit card score [100, 800] < 180 (7) Non-performing loans [0, ) = 0 (8) Late pay days [0, ) = 0 (9) RCT Control group {0, 1} = 0 (10) Regulatory Total limit to income [0, ) <4

17 The Randomized Trial I Experiment participants (N=54,522) Pre-existing cardholders approved for a credit line increase I Control group (N C =13,438) Determined by a random number generator Withheld from additional credit lines for T = 9 months. See Sampling

18 The Randomized Trial I Experiment participants (N=54,522) Pre-existing cardholders approved for a credit line increase I Control group (N C =13,438) Determined by a random number generator Withheld from additional credit lines for T = 9 months. I Treatment group (N T =41,084) Limits extended by a median 120% of monthly income. See Sampling

19 The Randomized Trial I Experiment participants (N=54,522) Pre-existing cardholders approved for a credit line increase I Control group (N C =13,438) Determined by a random number generator Withheld from additional credit lines for T = 9 months. I Treatment group (N T =41,084) Limits extended by a median 120% of monthly income. I Initiated by issuer and unannounced prior to intervention. I No effect on interest rate or other features of contract. See Sampling

20 Summary Statistics Group Count Age Income Limit Debt Credit score Risk score All cardholders >5m ,488 8,664 2,261 1, Participants 54, ,785 5,452 1,236 1, P( P = All ) < 0.01 < 0.01 < 0.01 < 0.01 < 0.01 < 0.01 Treatment 41, ,870 5,887 1,208 1, Treatment - US 27, ,047 6,704 1,044 1, Treatment 13, ,434 4,203 1,548 1, Control 13, ,494 4,121 1,523 1, P( T + US = C ) < 0.01 < 0.01 < 0.01 < 0.01 < 0.01 < 0.01 P( T = C ) Note. Table entries are group means unless otherwise noted. Row (1) based on a 50,000 random sample of all credit card holders in August Row (2) is based on 54,522 experiment participants in August Income, credit limit and credit card debt variables expressed in local currency. Labor income information for the subset of customers with direct deposit. Risk score represents the sum of three proprietary credit scores. See Robustness: Sampling

21 Event Study Note. Figure plots average interest bearing credit card debt at bank, D t. Levels normalized by pre-intervention values, D 1.

22 MPC out of Credit I Distributed lag DD it = T  f j DL it j=0 j + # it I MPC is the cumulative response after t months. MPC(t) = t  f j j=0 I Because the magnitude of the limit change is not random, instrument using I {DL it > 0}

23 Magnitude I Markets are incomplete and borrowing limit tighter than the natural limit. See Balance shifting See Robustness: Magnitude

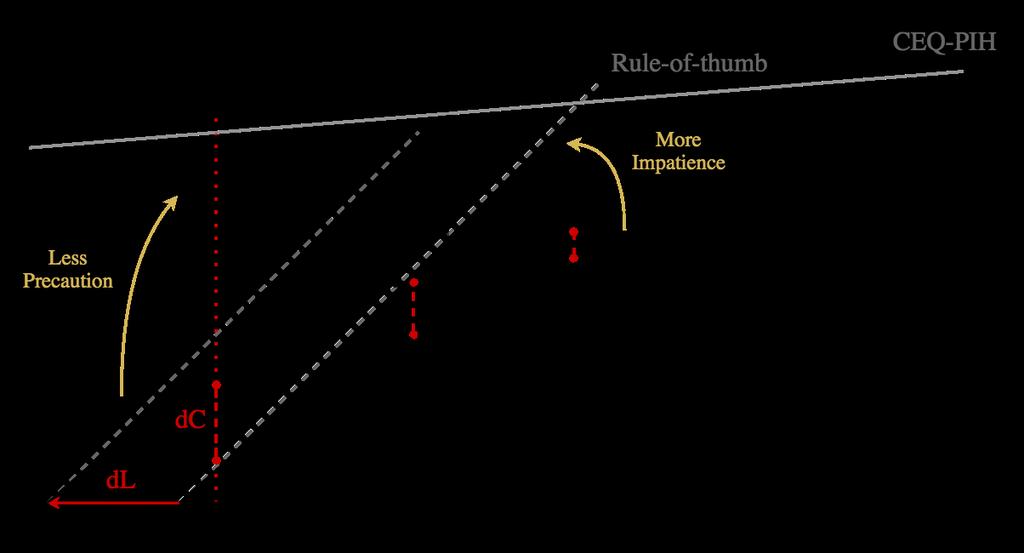

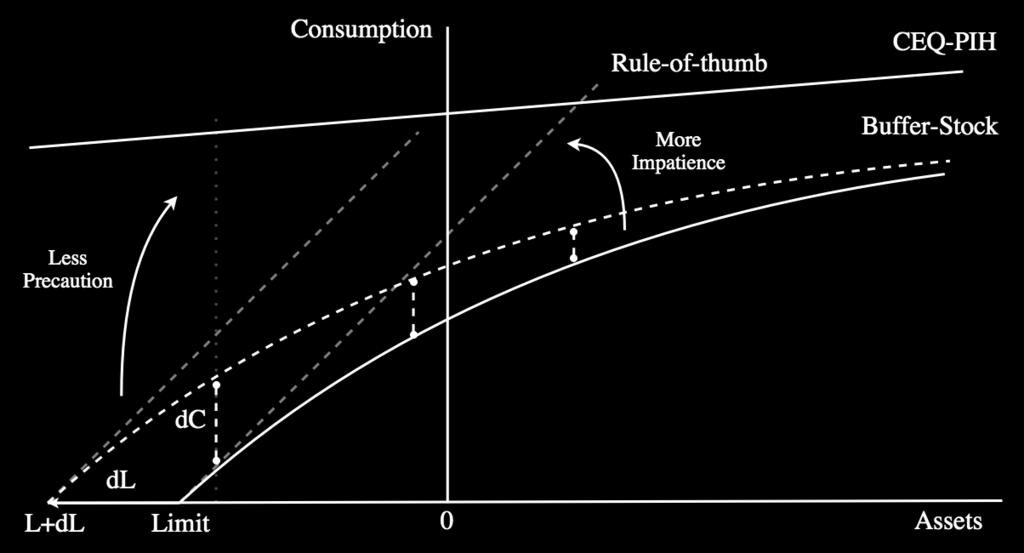

24 Heterogeneity I Response not driven by a small fraction of credit constrained or rule-of-thumb consumers. See Heterogeneity by Age, Education, Gender, Marital Status See Heterogeneity by Income, Assets, Cash-on-hand, URE

25 Composition I Installments used to invest in durables and services. I Revolving debt used for self-insurance. DDebt = DInstallments + DRevolving

26 Spending patterns Note. Figure displays the share of each category in the additional credit card spending done by the treatment group. Some spending above is crowded out from cash transactions, or transactions outside the bank. See Spending patterns: Installments

27 Utilization Dynamics Note. Figure plots average debt/limit of consumers binned at t=0. Consumers in the top bin have debt/limit in excess of 0.9 at t=0, and so on. Figure uses data from the universe of all cardholders. See Robustness: Universe of cardholders

28 Utilization Dynamics: Percentiles Note. Figure plots percentiles of debt/limit of consumers constrained at t=0. Figure uses data from the universe of all cardholders. See Dynamics: Percentiles, unconstrained

29 Credit in a Simple Intertemporal Model Discrete time, infinite horizon consumption/savings problem (1) Budget constraint: No credit card puzzle. (2) Uninsurable idiosyncratic income shocks: Realistic persistence r and unemployment risk. (3) Credit constraint: Ad-hoc limit L, tighter than the natural limit. Ṽ(A 0, Y 0 ; L) = max C t, A t+1 E 0 Â t=0 b t C1 t g 1 g s.t. C t + DA t apple Y t (1) Y t+1 P(Y t ) (2) D t+1 apple L (3) See Calibration

30 Conceptual framework

31 Nested Intertemporal Models: MPCL and Testable Implications 0 MPC out of Credit 1! Buffer-stock CEQ-PIH Buffer-stock w/durables Myopia Rule-of-thumb See Quantitative model

32 Nested Intertemporal Models: MPCL and Testable Implications 0 MPC out of Credit 1! Buffer-stock CEQ-PIH Buffer-stock w/durables Myopia Rule-of-thumb Credit affects behavior? N X X X X See Quantitative model

33 Nested Intertemporal Models: MPCL and Testable Implications 0 MPC out of Credit 1! Buffer-stock CEQ-PIH Buffer-stock w/durables Myopia Rule-of-thumb Credit affects behavior? Unconstrained respond? N X X X X N X X X N See Quantitative model

34 Nested Intertemporal Models: MPCL and Testable Implications 0 MPC out of Credit 1! Buffer-stock CEQ-PIH Buffer-stock w/durables Myopia Rule-of-thumb Credit affects behavior? Unconstrained respond? Deliver magnitude quantitatively? N X X X X N X X X N N N X X N See Quantitative model

35 Nested Intertemporal Models: MPCL and Testable Implications 0 MPC out of Credit 1! Buffer-stock CEQ-PIH Buffer-stock w/durables Myopia Rule-of-thumb Unconstrained respond? Deliver magnitude quantitatively? mean- Utilization reverting? Credit affects behavior? N X X X X N X X X N N N X X N N X X N N See Quantitative model

36 Nested Intertemporal Models: MPCL and Testable Implications 0 MPC out of Credit 1! Buffer-stock CEQ-PIH Buffer-stock w/durables Myopia Rule-of-thumb Unconstrained respond? Deliver magnitude quantitatively? mean- Utilization reverting? Credit affects behavior? N X X X X N X X X N N N X X N N X X N N See Quantitative model

37 Credit in a Simple Intertemporal Model Discrete time, infinite horizon consumption/savings problem (1) Budget constraint: No credit card puzzle. (2) Uninsurable idiosyncratic income shocks: Realistic persistence r and unemployment risk. (3) Credit constraint: Ad-hoc limit L, tighter than the natural limit. (+) Illiquid durables: Depreciation d, liquidation cost z, no adjustment cost upwards. (+) Borrowing/lending rate spread. Ṽ(A 0, Y 0 ; L) = max C t, A t+1,k t E 0 Â t=0 b t (C a t K1 a t ) 1 g 1 g s.t. C t + DA t apple Y t + DD t L(K t+1, K t ) (1) Y t+1 P(Y t ) (2) D t+1 apple L (3) See Calibration

38 Thank you!

Under revision. For conference submission only. The Marginal Propensity to Consume out of Credit:

Under revision. For conference submission only. The Marginal Propensity to Consume out of Credit: Evidence from Random Assignment of 54,522 Credit Lines Deniz Aydın May 2017 Abstract This paper investigates

Under revision. For conference submission only. The Marginal Propensity to Consume out of Credit: Evidence from Random Assignment of 54,522 Credit Lines Deniz Aydın May 2017 Abstract This paper investigates

The Marginal Propensity to Consume Out of Liquidity:

The Marginal Propensity to Consume Out of Liquidity: Evidence from Random Assignment of 54,522 Credit Lines Deniz Aydın Stanford University Job Market Paper December 22, 2015 [Latest Version] Abstract

The Marginal Propensity to Consume Out of Liquidity: Evidence from Random Assignment of 54,522 Credit Lines Deniz Aydın Stanford University Job Market Paper December 22, 2015 [Latest Version] Abstract

Preview of results The marginal propensity to consume out of liquidity: Evidence from a randomized controlled trial

Preview of results The marginal propensity to consume out of liquidity: Evidence from a randomized controlled trial [PRELIMINARY AND INCOMPLETE] [DO NOT CITE OR CIRCULATE] Deniz Aydın Stanford University

Preview of results The marginal propensity to consume out of liquidity: Evidence from a randomized controlled trial [PRELIMINARY AND INCOMPLETE] [DO NOT CITE OR CIRCULATE] Deniz Aydın Stanford University

A Model of the Consumption Response to Fiscal Stimulus Payments

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan University of Pennsylvania Gianluca Violante New York University Federal Reserve Board May 31, 2012 1/47 Fiscal stimulus payments

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan University of Pennsylvania Gianluca Violante New York University Federal Reserve Board May 31, 2012 1/47 Fiscal stimulus payments

The Marginal Propensity to Consume Out of Credit. Lorenz Kueng

Discussion of Aydin (2017) The Marginal Propensity to Consume Out of Credit Lorenz Kueng Northwestern University and NBER Very interesting paper! Lots to think about. I applaud Deniz - for getting access

Discussion of Aydin (2017) The Marginal Propensity to Consume Out of Credit Lorenz Kueng Northwestern University and NBER Very interesting paper! Lots to think about. I applaud Deniz - for getting access

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Fiscal Policy and MPC Heterogeneity

Fiscal Policy and MPC Heterogeneity by Tullio Jappelli and Luigi Pistaferri Discussion by: Fabrizio Perri Bocconi, Minneapolis Fed, IGIER & NBER Macroeconomic Dynamics with Heterogeneous Agents, June 2013

Fiscal Policy and MPC Heterogeneity by Tullio Jappelli and Luigi Pistaferri Discussion by: Fabrizio Perri Bocconi, Minneapolis Fed, IGIER & NBER Macroeconomic Dynamics with Heterogeneous Agents, June 2013

A Model of the Consumption Response to Fiscal Stimulus Payments

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan 1 Gianluca Violante 2 1 Princeton University 2 New York University Presented by Francisco Javier Rodríguez (Universidad Carlos

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan 1 Gianluca Violante 2 1 Princeton University 2 New York University Presented by Francisco Javier Rodríguez (Universidad Carlos

The Micro of Macro: Lessons from our research to help understand severe economic downturns

The Micro of Macro: Lessons from our research to help understand severe economic downturns Amir Sufi University of Chicago Booth School of Business NBER Giving Macroeconomics a Bad Name? During the crisis,

The Micro of Macro: Lessons from our research to help understand severe economic downturns Amir Sufi University of Chicago Booth School of Business NBER Giving Macroeconomics a Bad Name? During the crisis,

The Marginal Propensity to Consume for Different Income Groups

The Marginal Propensity to Consume for Different Income Groups Zara Afraie and Charles Grant June 2018 Brunel University London Key Idea Permanent Income Hypothesis(PIH), Milton Friedman(1957) people plan

The Marginal Propensity to Consume for Different Income Groups Zara Afraie and Charles Grant June 2018 Brunel University London Key Idea Permanent Income Hypothesis(PIH), Milton Friedman(1957) people plan

Microeconomic Heterogeneity and Macroeconomic Shocks

Microeconomic Heterogeneity and Macroeconomic Shocks Greg Kaplan University of Chicago Gianluca Violante Princeton University BdF/ECB Conference on HFC In preparation for the Special Issue of JEP on The

Microeconomic Heterogeneity and Macroeconomic Shocks Greg Kaplan University of Chicago Gianluca Violante Princeton University BdF/ECB Conference on HFC In preparation for the Special Issue of JEP on The

insignificant, but orthogonality restriction rejected for stock market prices There was no evidence of excess sensitivity

Supplemental Table 1 Summary of literature findings Reference Data Experiment Findings Anticipated income changes Hall (1978) 1948 1977 U.S. macro series Used quadratic preferences Coefficient on lagged

Supplemental Table 1 Summary of literature findings Reference Data Experiment Findings Anticipated income changes Hall (1978) 1948 1977 U.S. macro series Used quadratic preferences Coefficient on lagged

Lecture 2. (1) Permanent Income Hypothesis. (2) Precautionary Savings. Erick Sager. September 21, 2015

Permanent Income Hypothesis. (2) Precautionary Savings. Erick Sager. September 21, 2015") Lecture 2 (1) Permanent Income Hypothesis (2) Precautionary Savings Erick Sager September 21, 2015 Econ 605: Adv. Topics in Macroeconomics Johns Hopkins University, Fall 2015 Erick Sager Lecture 2 (9/21/15)

Lecture 2 (1) Permanent Income Hypothesis (2) Precautionary Savings Erick Sager September 21, 2015 Econ 605: Adv. Topics in Macroeconomics Johns Hopkins University, Fall 2015 Erick Sager Lecture 2 (9/21/15)

How Much Insurance in Bewley Models?

How Much Insurance in Bewley Models? Greg Kaplan New York University Gianluca Violante New York University, CEPR, IFS and NBER Boston University Macroeconomics Seminar Lunch Kaplan-Violante, Insurance

How Much Insurance in Bewley Models? Greg Kaplan New York University Gianluca Violante New York University, CEPR, IFS and NBER Boston University Macroeconomics Seminar Lunch Kaplan-Violante, Insurance

Consumer Response to Changes in Credit Supply: Evidence from Credit Card Data

Financial Institutions Center Consumer Response to Changes in Credit Supply: Evidence from Credit Card Data by David B. Gross Nicholas S. Souleles 00-04-B The Wharton Financial Institutions Center The

Financial Institutions Center Consumer Response to Changes in Credit Supply: Evidence from Credit Card Data by David B. Gross Nicholas S. Souleles 00-04-B The Wharton Financial Institutions Center The

Relating Income to Consumption Part 1

Part 1 Extract from Earnings, Consumption and Lifecycle Choices by Costas Meghir and Luigi Pistaferri. Handbook of Labor Economics, Vol. 4b, Ch. 9. (2011). James J. Heckman University of Chicago AEA Continuing

Part 1 Extract from Earnings, Consumption and Lifecycle Choices by Costas Meghir and Luigi Pistaferri. Handbook of Labor Economics, Vol. 4b, Ch. 9. (2011). James J. Heckman University of Chicago AEA Continuing

The Marginal Propensity to Consume Over the Business Cycle *

The Marginal Propensity to Consume Over the Business Cycle * August, 216 Tal Gross Matthew J. Notowidigdo Jialan Wang Abstract This paper estimates how the marginal propensity to consume (MPC) varies over

The Marginal Propensity to Consume Over the Business Cycle * August, 216 Tal Gross Matthew J. Notowidigdo Jialan Wang Abstract This paper estimates how the marginal propensity to consume (MPC) varies over

The Costs of Financial Mistakes: Evidence from U.S. Consumers

The Costs of Financial Mistakes: Evidence from U.S. Consumers Adam T. Jørring Click here for most recent version November 13, 2017 Abstract This paper investigates the relationship between financial mistakes

The Costs of Financial Mistakes: Evidence from U.S. Consumers Adam T. Jørring Click here for most recent version November 13, 2017 Abstract This paper investigates the relationship between financial mistakes

Identifying Household Income Processes Using a Life Cycle Model of Consumption

Identifying Household Income Processes Using a Life Cycle Model of Consumption Dmytro Hryshko University of Alberta Abstract In the literature, econometricians typically assume that household income is

Identifying Household Income Processes Using a Life Cycle Model of Consumption Dmytro Hryshko University of Alberta Abstract In the literature, econometricians typically assume that household income is

Asymmetric consumption effects of transitory income shocks

No. 551 / March 2017 Asymmetric consumption effects of transitory income shocks Dimitris Christelis, Dimitris Georgarakos, Tullio Jappelli, Luigi Pistaferri and Maarten van Rooij Asymmetric consumption

No. 551 / March 2017 Asymmetric consumption effects of transitory income shocks Dimitris Christelis, Dimitris Georgarakos, Tullio Jappelli, Luigi Pistaferri and Maarten van Rooij Asymmetric consumption

Discussion of Capital Injection to Banks versus Debt Relief to Households

Discussion of Capital Injection to Banks versus Debt Relief to Households Atif Mian Princeton University and NBER Jinhyuk Yoo asks an important and interesting question in this paper: if policymakers have

Discussion of Capital Injection to Banks versus Debt Relief to Households Atif Mian Princeton University and NBER Jinhyuk Yoo asks an important and interesting question in this paper: if policymakers have

Idiosyncratic risk and the dynamics of aggregate consumption: a likelihood-based perspective

Idiosyncratic risk and the dynamics of aggregate consumption: a likelihood-based perspective Alisdair McKay Boston University March 2013 Idiosyncratic risk and the business cycle How much and what types

Idiosyncratic risk and the dynamics of aggregate consumption: a likelihood-based perspective Alisdair McKay Boston University March 2013 Idiosyncratic risk and the business cycle How much and what types

Overpersistence Bias in Individual Income Expectations and its Aggregate Implications

Overpersistence Bias in Individual Income Expectations and its Aggregate Implications Filip Rozsypal Kathrin Schlafmann August 16, 2017 Abstract Using micro level data, we document a systematic, income-related

Overpersistence Bias in Individual Income Expectations and its Aggregate Implications Filip Rozsypal Kathrin Schlafmann August 16, 2017 Abstract Using micro level data, we document a systematic, income-related

The Intertemporal Keynesian Cross. Auclert-Rognlie-Straub

The Intertemporal Keynesian Cross Auclert-Rognlie-Straub Discussion Gianluca Violante Princeton University Outline of my discussion 1. Background, insight, and contribution 2. Empirics of the IMPC 3. The

The Intertemporal Keynesian Cross Auclert-Rognlie-Straub Discussion Gianluca Violante Princeton University Outline of my discussion 1. Background, insight, and contribution 2. Empirics of the IMPC 3. The

A Tale of Two Stimulus Payments: 2001 vs 2008

A Tale of Two Stimulus Payments: 2001 vs 2008 Greg Kaplan Princeton University & NBER Gianluca Violante New York University, CEPR & NBER American Economic Associa-on Annual Mee-ng January 5, 2013 Fiscal

A Tale of Two Stimulus Payments: 2001 vs 2008 Greg Kaplan Princeton University & NBER Gianluca Violante New York University, CEPR & NBER American Economic Associa-on Annual Mee-ng January 5, 2013 Fiscal

11/6/2013. Chapter 17: Consumption. Early empirical successes: Results from early studies. Keynes s conjectures. The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

Day 4. Redistributive and macro effects of fiscal stimulus policies

Day 4 Redistributive and macro effects of fiscal stimulus policies Gianluca Violante New York University Mini-Course on Policy in Models with Heterogeneous Agents Bank of Portugal, June 15-19, 2105 p.

Day 4 Redistributive and macro effects of fiscal stimulus policies Gianluca Violante New York University Mini-Course on Policy in Models with Heterogeneous Agents Bank of Portugal, June 15-19, 2105 p.

Excess Smoothness of Consumption in an Estimated Life Cycle Model

Excess Smoothness of Consumption in an Estimated Life Cycle Model Dmytro Hryshko University of Alberta Abstract In the literature, econometricians typically assume that household income is the sum of a

Excess Smoothness of Consumption in an Estimated Life Cycle Model Dmytro Hryshko University of Alberta Abstract In the literature, econometricians typically assume that household income is the sum of a

The Idea. Friedman (1957): Permanent Income Hypothesis. Use the Benchmark KS model with Modifications. Income Process. Progress since then

: Permanent Income Hypothesis. Use the Benchmark KS model with Modifications. Income Process. Progress since then") Wealth Heterogeneity and Marginal Propensity to Consume Buffer Stock Saving in a Krusell Smith World Christopher Carroll 1 Jiri Slacalek 2 Kiichi Tokuoka 3 1 Johns Hopkins University and NBER ccarroll@jhu.edu

Wealth Heterogeneity and Marginal Propensity to Consume Buffer Stock Saving in a Krusell Smith World Christopher Carroll 1 Jiri Slacalek 2 Kiichi Tokuoka 3 1 Johns Hopkins University and NBER ccarroll@jhu.edu

House Prices and Consumer Spending

House Prices and Consumer Spending David Berger Northwestern University Guido Lorenzoni Northwestern University Veronica Guerrieri University of Chicago Joseph Vavra University of Chicago November 21,

House Prices and Consumer Spending David Berger Northwestern University Guido Lorenzoni Northwestern University Veronica Guerrieri University of Chicago Joseph Vavra University of Chicago November 21,

House Price Gains and U.S. Household Spending from 2002 to 2006

House Price Gains and U.S. Household Spending from 2002 to 2006 Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business and NBER May 2014 Abstract We examine the

House Price Gains and U.S. Household Spending from 2002 to 2006 Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business and NBER May 2014 Abstract We examine the

A Model of the Consumption Response to Fiscal Stimulus Payments *

A Model of the Consumption Response to Fiscal Stimulus Payments * Greg Kaplan University of Pennsylvania and IFS gkaplan@sas.upenn.edu Giovanni L. Violante New York University, CEPR, IFS and NBER glv2@nyu.edu

A Model of the Consumption Response to Fiscal Stimulus Payments * Greg Kaplan University of Pennsylvania and IFS gkaplan@sas.upenn.edu Giovanni L. Violante New York University, CEPR, IFS and NBER glv2@nyu.edu

What Would You Do with $500? Spending Responses to Gains, Losses, News, and Loans

Federal Reserve Bank of New York Staff Reports What Would You Do with $500? Spending Responses to Gains, Losses, News, and Loans Andreas Fuster Greg Kaplan Basit Zafar Staff Report No. 843 March 2018 This

Federal Reserve Bank of New York Staff Reports What Would You Do with $500? Spending Responses to Gains, Losses, News, and Loans Andreas Fuster Greg Kaplan Basit Zafar Staff Report No. 843 March 2018 This

Credit Cards and Consumption

Credit Cards and Consumption Scott L. Fulford and Scott Schuh June 2018 Abstract Using credit bureau data, we show that the revolving credit available to consumers fluctuates substantially over the business

Credit Cards and Consumption Scott L. Fulford and Scott Schuh June 2018 Abstract Using credit bureau data, we show that the revolving credit available to consumers fluctuates substantially over the business

Micro foundations, part 1. Modern theories of consumption

Micro foundations, part 1. Modern theories of consumption Joanna Siwińska-Gorzelak Faculty of Economic Sciences, Warsaw University Lecture overview This lecture focuses on the most prominent work on consumption.

Micro foundations, part 1. Modern theories of consumption Joanna Siwińska-Gorzelak Faculty of Economic Sciences, Warsaw University Lecture overview This lecture focuses on the most prominent work on consumption.

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment Owen Zidar Chicago Booth and NBER December 1, 2014 Owen Zidar (Chicago Booth) Tax Cuts for Whom? December 1, 2014

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment Owen Zidar Chicago Booth and NBER December 1, 2014 Owen Zidar (Chicago Booth) Tax Cuts for Whom? December 1, 2014

DO LIQUIDITY CONSTRAINTS AND INTEREST RATES MATTER FOR CONSUMER BEHAVIOR? EVIDENCE FROM CREDIT CARD DATA*

DO LIQUIDITY CONSTRAINTS AND INTEREST RATES MATTER FOR CONSUMER BEHAVIOR? EVIDENCE FROM CREDIT CARD DATA* DAVID B. GROSS AND NICHOLAS S. SOULELES This paper utilizes a unique data set of credit card accounts

DO LIQUIDITY CONSTRAINTS AND INTEREST RATES MATTER FOR CONSUMER BEHAVIOR? EVIDENCE FROM CREDIT CARD DATA* DAVID B. GROSS AND NICHOLAS S. SOULELES This paper utilizes a unique data set of credit card accounts

The marginal propensity to consume out of a tax rebate: the case of Italy

The marginal propensity to consume out of a tax rebate: the case of Italy Andrea Neri 1 Concetta Rondinelli 2 Filippo Scoccianti 3 Bank of Italy 1 Statistical Analysis Directorate 2 Economic Outlook and

The marginal propensity to consume out of a tax rebate: the case of Italy Andrea Neri 1 Concetta Rondinelli 2 Filippo Scoccianti 3 Bank of Italy 1 Statistical Analysis Directorate 2 Economic Outlook and

Excess Smoothness of Consumption in an Estimated Life Cycle Model

Excess Smoothness of Consumption in an Estimated Life Cycle Model Dmytro Hryshko University of Alberta Abstract In the literature, econometricians typically assume that household income is the sum of a

Excess Smoothness of Consumption in an Estimated Life Cycle Model Dmytro Hryshko University of Alberta Abstract In the literature, econometricians typically assume that household income is the sum of a

How do households respond to income shocks?

How do households respond to income shocks? Dirk Krueger University of Pennsylvania, CEPR and NBER Fabrizio Perri University of Minnesota, Minneapolis FED, CEPR and NBER August 2009 Abstract Commonly used

How do households respond to income shocks? Dirk Krueger University of Pennsylvania, CEPR and NBER Fabrizio Perri University of Minnesota, Minneapolis FED, CEPR and NBER August 2009 Abstract Commonly used

Consumption and Portfolio Choice under Uncertainty

Chapter 8 Consumption and Portfolio Choice under Uncertainty In this chapter we examine dynamic models of consumer choice under uncertainty. We continue, as in the Ramsey model, to take the decision of

Chapter 8 Consumption and Portfolio Choice under Uncertainty In this chapter we examine dynamic models of consumer choice under uncertainty. We continue, as in the Ramsey model, to take the decision of

Household finance in Europe 1

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Household finance in Europe 1 Miguel Ampudia, European Central

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Household finance in Europe 1 Miguel Ampudia, European Central

Household Expenditure & Property Taxes

Household Expenditure & Property Taxes Evidence from a Fiscal Consolidation Plan Paolo Surico Riccardo Trezzi London Business School and CEPR Board of Governors of the Federal Reserve System ESSIM - May

Household Expenditure & Property Taxes Evidence from a Fiscal Consolidation Plan Paolo Surico Riccardo Trezzi London Business School and CEPR Board of Governors of the Federal Reserve System ESSIM - May

Macroeconomics: Fluctuations and Growth

Macroeconomics: Fluctuations and Growth Francesco Franco 1 1 Nova School of Business and Economics Fluctuations and Growth, 2011 Francesco Franco Macroeconomics: Fluctuations and Growth 1/54 Introduction

Macroeconomics: Fluctuations and Growth Francesco Franco 1 1 Nova School of Business and Economics Fluctuations and Growth, 2011 Francesco Franco Macroeconomics: Fluctuations and Growth 1/54 Introduction

Discussion of Optimal Monetary Policy and Fiscal Policy Interaction in a Non-Ricardian Economy

Discussion of Optimal Monetary Policy and Fiscal Policy Interaction in a Non-Ricardian Economy Johannes Wieland University of California, San Diego and NBER 1. Introduction Markets are incomplete. In recent

Discussion of Optimal Monetary Policy and Fiscal Policy Interaction in a Non-Ricardian Economy Johannes Wieland University of California, San Diego and NBER 1. Introduction Markets are incomplete. In recent

Empirical Macroeconomics

Empirical Macroeconomics Francesco Franco Nova SBE April 22, 2013 Francesco Franco Empirical Macroeconomics 1/15 From Keynes to Friedman The amount of aggregate consumption mainly depends on the amount

Empirical Macroeconomics Francesco Franco Nova SBE April 22, 2013 Francesco Franco Empirical Macroeconomics 1/15 From Keynes to Friedman The amount of aggregate consumption mainly depends on the amount

ECNS 303 Ch. 16: Consumption

ECNS 303 Ch. 16: Consumption Micro foundations of Macro: Consumption Q. How do households decide how much of their income to consume today and how much to save for the future? Micro question with macro

ECNS 303 Ch. 16: Consumption Micro foundations of Macro: Consumption Q. How do households decide how much of their income to consume today and how much to save for the future? Micro question with macro

ECO209 MACROECONOMIC THEORY. Chapter 14

Prof. Gustavo Indart Department of Economics University of Toronto ECO209 MACROECONOMIC THEORY Chapter 14 CONSUMPTION AND SAVING Discussion Questions: 1. The MPC of Keynesian analysis implies that there

Prof. Gustavo Indart Department of Economics University of Toronto ECO209 MACROECONOMIC THEORY Chapter 14 CONSUMPTION AND SAVING Discussion Questions: 1. The MPC of Keynesian analysis implies that there

Informational Assumptions on Income Processes and Consumption Dynamics In the Buffer Stock Model of Savings

Informational Assumptions on Income Processes and Consumption Dynamics In the Buffer Stock Model of Savings Dmytro Hryshko University of Alberta This version: June 26, 2006 Abstract Idiosyncratic household

Informational Assumptions on Income Processes and Consumption Dynamics In the Buffer Stock Model of Savings Dmytro Hryshko University of Alberta This version: June 26, 2006 Abstract Idiosyncratic household

The Buffer-Stock Model and the Marginal Propensity to Consume. A Panel-Data Study of the U.S. States.

The Buffer-Stock Model and the Marginal Propensity to Consume. A Panel-Data Study of the U.S. States. María José Luengo-Prado Northeastern University Bent E. Sørensen University of Houston and CEPR March

The Buffer-Stock Model and the Marginal Propensity to Consume. A Panel-Data Study of the U.S. States. María José Luengo-Prado Northeastern University Bent E. Sørensen University of Houston and CEPR March

Discussion of Credit Crises, Precautionary Savings, and the Liquidity Trap by Veronica Guerrieri and Guido Lorenzoni

Discussion of Credit Crises, Precautionary Savings, and the Liquidity Trap by Veronica Guerrieri and Guido Lorenzoni Discussion by Bob Hall EF&G Research Meeting NBER Summer Institute July 16, 2011 1 Bewley

Discussion of Credit Crises, Precautionary Savings, and the Liquidity Trap by Veronica Guerrieri and Guido Lorenzoni Discussion by Bob Hall EF&G Research Meeting NBER Summer Institute July 16, 2011 1 Bewley

Kaplan, Moll and Violante: Unconventional Monetary Policy in HANK

Discussion of Kaplan, Moll and Violante: Unconventional Monetary Policy in HANK Workshop on Current Monetary Policy Challenges Jirka Slacalek European Central Bank www.slacalek.com ECB, December 2016 The

Discussion of Kaplan, Moll and Violante: Unconventional Monetary Policy in HANK Workshop on Current Monetary Policy Challenges Jirka Slacalek European Central Bank www.slacalek.com ECB, December 2016 The

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER EXPENDITURE

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER 1 Explaining the observed patterns in data on consumption and income: short-run and cross-sectional data show that MPC < APC, whilst long-run data show

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER 1 Explaining the observed patterns in data on consumption and income: short-run and cross-sectional data show that MPC < APC, whilst long-run data show

Credit Card Utilization and Consumption over the Life. Cycle and Business Cycle

Credit Card Utilization and Consumption over the Life Cycle and Business Cycle Scott L. Fulford and Scott Schuh September 2017 Abstract The revolving credit available to consumers changes substantially

Credit Card Utilization and Consumption over the Life Cycle and Business Cycle Scott L. Fulford and Scott Schuh September 2017 Abstract The revolving credit available to consumers changes substantially

Ination Expectations and Consumption Expenditure

Ination Expectations and Consumption Expenditure Francesco D'Acunto University of Maryland Daniel Hoang Karlsruhe Institute of Technology Michael Weber University of Chicago September 25, 2015 Introduction

Ination Expectations and Consumption Expenditure Francesco D'Acunto University of Maryland Daniel Hoang Karlsruhe Institute of Technology Michael Weber University of Chicago September 25, 2015 Introduction

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Fall University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Micro-foundations: Consumption. Instructor: Dmytro Hryshko

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Chapter 16 Consumption. 8 th and 9 th editions 4/29/2017. This chapter presents: Keynes s Conjectures

2 0 1 0 U P D A T E 4/29/2017 Chapter 16 Consumption 8 th and 9 th editions This chapter presents: An introduction to the most prominent work on consumption, including: John Maynard Keynes: consumption

2 0 1 0 U P D A T E 4/29/2017 Chapter 16 Consumption 8 th and 9 th editions This chapter presents: An introduction to the most prominent work on consumption, including: John Maynard Keynes: consumption

What Drives Heterogeneity in the Marginal Propensity to Consume? Temporary Shocks vs Persistent Characteristics

What Drives Heterogeneity in the Marginal Propensity to Consume? Temporary Shocks vs Persistent Characteristics Michael Gelman December 3, 2016 Click here for the most recent version Abstract Many empirical

What Drives Heterogeneity in the Marginal Propensity to Consume? Temporary Shocks vs Persistent Characteristics Michael Gelman December 3, 2016 Click here for the most recent version Abstract Many empirical

HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE

DISCUSSION OF: HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE BY MIAN, SUFI AND VERNER Emi Nakamura Columbia University December 2015 Nakamura Inflation Expectations December 2015 1 / 24 Could a credit boom

DISCUSSION OF: HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE BY MIAN, SUFI AND VERNER Emi Nakamura Columbia University December 2015 Nakamura Inflation Expectations December 2015 1 / 24 Could a credit boom

How do Households Respond to Income Shocks?

How do Households Respond to Income Shocks? Dirk Krueger University of Pennsylvania, CEPR and NBER Fabrizio Perri University of Minnesota, Minneapolis FED, CEPR and NBER October 2012 Abstract We use the

How do Households Respond to Income Shocks? Dirk Krueger University of Pennsylvania, CEPR and NBER Fabrizio Perri University of Minnesota, Minneapolis FED, CEPR and NBER October 2012 Abstract We use the

MACROECONOMICS II - CONSUMPTION

MACROECONOMICS II - CONSUMPTION Stefania MARCASSA stefania.marcassa@u-cergy.fr http://stefaniamarcassa.webstarts.com/teaching.html 2016-2017 Plan An introduction to the most prominent work on consumption,

MACROECONOMICS II - CONSUMPTION Stefania MARCASSA stefania.marcassa@u-cergy.fr http://stefaniamarcassa.webstarts.com/teaching.html 2016-2017 Plan An introduction to the most prominent work on consumption,

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

How Do House Prices Affect Consumption? Evidence from Micro Data

How Do House Prices Affect Consumption? Evidence from Micro Data The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters. Citation Published

How Do House Prices Affect Consumption? Evidence from Micro Data The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters. Citation Published

Overpersistence bias in individual income expectations and its aggregate implications

Overpersistence bias in individual income expectations and its aggregate implications Filip Rozsypal Kathrin Schlafmann April 18, 2017 Abstract We study the role of household income expectations for consumption

Overpersistence bias in individual income expectations and its aggregate implications Filip Rozsypal Kathrin Schlafmann April 18, 2017 Abstract We study the role of household income expectations for consumption

NBER WORKING PAPER SERIES DISENTANGLING FINANCIAL CONSTRAINTS, PRECAUTIONARY SAVINGS, AND MYOPIA: HOUSEHOLD BEHAVIOR SURROUNDING FEDERAL TAX RETURNS

NBER WORKING PAPER SERIES DISENTANGLING FINANCIAL CONSTRAINTS, PRECAUTIONARY SAVINGS, AND MYOPIA: HOUSEHOLD BEHAVIOR SURROUNDING FEDERAL TAX RETURNS Brian Baugh Itzhak Ben-David Hoonsuk Park Working Paper

NBER WORKING PAPER SERIES DISENTANGLING FINANCIAL CONSTRAINTS, PRECAUTIONARY SAVINGS, AND MYOPIA: HOUSEHOLD BEHAVIOR SURROUNDING FEDERAL TAX RETURNS Brian Baugh Itzhak Ben-David Hoonsuk Park Working Paper

A Theory of Macroprudential Policies in the Presence of Nominal Rigidities by Farhi and Werning

A Theory of Macroprudential Policies in the Presence of Nominal Rigidities by Farhi and Werning Discussion by Anton Korinek Johns Hopkins University SF Fed Conference March 2014 Anton Korinek (JHU) Macroprudential

A Theory of Macroprudential Policies in the Presence of Nominal Rigidities by Farhi and Werning Discussion by Anton Korinek Johns Hopkins University SF Fed Conference March 2014 Anton Korinek (JHU) Macroprudential

Can Financial Frictions Explain China s Current Account Puzzle: A Firm Level Analysis (Preliminary)

") Can Financial Frictions Explain China s Current Account Puzzle: A Firm Level Analysis (Preliminary) Yan Bai University of Rochester NBER Dan Lu University of Rochester Xu Tian University of Rochester February

Can Financial Frictions Explain China s Current Account Puzzle: A Firm Level Analysis (Preliminary) Yan Bai University of Rochester NBER Dan Lu University of Rochester Xu Tian University of Rochester February

The Consumption Response to Income Changes

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 08-52 The Consumption Response to Income Changes By Tullio Jappelli Universy

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 08-52 The Consumption Response to Income Changes By Tullio Jappelli Universy

Liquidity Constraints of the Middle Class

Liquidity Constraints of the Middle Class Jeffrey R. Campbell and Zvi Hercowitz December 28 Abstract This paper combines impatience with large recurring expenditures to replicate the observation that middle-class

Liquidity Constraints of the Middle Class Jeffrey R. Campbell and Zvi Hercowitz December 28 Abstract This paper combines impatience with large recurring expenditures to replicate the observation that middle-class

Do credit shocks matter for aggregate consumption?

Do credit shocks matter for aggregate consumption? Tomi Kortela Abstract Consumption and unsecured credit are correlated in the data. This fact has created a hypothesis which argues that the time-varying

Do credit shocks matter for aggregate consumption? Tomi Kortela Abstract Consumption and unsecured credit are correlated in the data. This fact has created a hypothesis which argues that the time-varying

Monetary Policy, Mortgages and Consumption: Evidence from Italy

Economic Policy 65th Panel Meeting Hosted by the Central Bank of Malta Valletta, 21-22 April 2017 Monetary Policy, Mortgages and Consumption: Evidence from Italy Tullio Jappelli (University of Naples Federico

Economic Policy 65th Panel Meeting Hosted by the Central Bank of Malta Valletta, 21-22 April 2017 Monetary Policy, Mortgages and Consumption: Evidence from Italy Tullio Jappelli (University of Naples Federico

Liquidity Constraints, the Extended Family, and Consumption

Working Paper WP 2015-320 Liquidity Constraints, the Extended Family, and Consumption HwaJung Choi, Kathleen McGarry, and Robert F. Schoeni Project #: UM14-04 Liquidity Constraints, the Extended Family,

Working Paper WP 2015-320 Liquidity Constraints, the Extended Family, and Consumption HwaJung Choi, Kathleen McGarry, and Robert F. Schoeni Project #: UM14-04 Liquidity Constraints, the Extended Family,

Federal Reserve Bank of Chicago

Federal Reserve Bank of Chicago Liquidity Constraints of the Middle Class Jeffrey R. Campbell and Zvi Hercowitz REVISED February 2018 WP 2009-20 Liquidity Constraints of the Middle Class Jeffrey R. Campbell

Federal Reserve Bank of Chicago Liquidity Constraints of the Middle Class Jeffrey R. Campbell and Zvi Hercowitz REVISED February 2018 WP 2009-20 Liquidity Constraints of the Middle Class Jeffrey R. Campbell

Inequality, Heterogeneity, and Consumption in the Journal of Political Economy Greg Kaplan August 2017

Inequality, Heterogeneity, and Consumption in the Journal of Political Economy Greg Kaplan August 2017 Today, inequality and heterogeneity are front-and-center in macroeconomics. Most macroeconomists agree

Inequality, Heterogeneity, and Consumption in the Journal of Political Economy Greg Kaplan August 2017 Today, inequality and heterogeneity are front-and-center in macroeconomics. Most macroeconomists agree

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1 Sumit Agarwal Georgetown University Amit Bubna Cornerstone Research Molly Lipscomb University of Virginia Abstract The within-month

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1 Sumit Agarwal Georgetown University Amit Bubna Cornerstone Research Molly Lipscomb University of Virginia Abstract The within-month

Credit Constraints and Search Frictions in Consumer Credit Markets

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

Workers Response to the 2011 Payroll Tax Cuts

Workers Response to the 2011 Payroll Tax Cuts Grant Graziani Wilbert van der Klaauw Basit Zafar 1 ABSTRACT This paper presents new survey evidence on workers response to the 2011 payroll tax cuts. While

Workers Response to the 2011 Payroll Tax Cuts Grant Graziani Wilbert van der Klaauw Basit Zafar 1 ABSTRACT This paper presents new survey evidence on workers response to the 2011 payroll tax cuts. While

On the Welfare and Distributional Implications of. Intermediation Costs

On the Welfare and Distributional Implications of Intermediation Costs Antnio Antunes Tiago Cavalcanti Anne Villamil November 2, 2006 Abstract This paper studies the distributional implications of intermediation

On the Welfare and Distributional Implications of Intermediation Costs Antnio Antunes Tiago Cavalcanti Anne Villamil November 2, 2006 Abstract This paper studies the distributional implications of intermediation

Notes for Econ202A: Consumption

Notes for Econ22A: Consumption Pierre-Olivier Gourinchas UC Berkeley Fall 215 c Pierre-Olivier Gourinchas, 215, ALL RIGHTS RESERVED. Disclaimer: These notes are riddled with inconsistencies, typos and

Notes for Econ22A: Consumption Pierre-Olivier Gourinchas UC Berkeley Fall 215 c Pierre-Olivier Gourinchas, 215, ALL RIGHTS RESERVED. Disclaimer: These notes are riddled with inconsistencies, typos and

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Rational Expectations and Consumption

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Rational Expectations and Consumption Elementary Keynesian macro theory assumes that households make consumption decisions

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Rational Expectations and Consumption Elementary Keynesian macro theory assumes that households make consumption decisions

Debt Constraints and the Labor Wedge

Debt Constraints and the Labor Wedge By Patrick Kehoe, Virgiliu Midrigan, and Elena Pastorino This paper is motivated by the strong correlation between changes in household debt and employment across regions

Debt Constraints and the Labor Wedge By Patrick Kehoe, Virgiliu Midrigan, and Elena Pastorino This paper is motivated by the strong correlation between changes in household debt and employment across regions

Overborrowing, Financial Crises and Macro-prudential Policy

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

The role of dynamic renegotiation and asymmetric information in financial contracting

The role of dynamic renegotiation and asymmetric information in financial contracting Paper Presentation Tim Martens and Christian Schmidt 1 Theory Renegotiation Parties are unable to commit to the terms

The role of dynamic renegotiation and asymmetric information in financial contracting Paper Presentation Tim Martens and Christian Schmidt 1 Theory Renegotiation Parties are unable to commit to the terms

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

The Composition Effect of Consumption around Retirement: Evidence from Singapore

The Composition Effect of Consumption around Retirement: Evidence from Singapore By SUMIT AGARWAL, JESSICA PAN AND WENLAN QIAN* * Agarwal: National University of Singapore, 15 Kent Ridge Drive, NUS Business

The Composition Effect of Consumption around Retirement: Evidence from Singapore By SUMIT AGARWAL, JESSICA PAN AND WENLAN QIAN* * Agarwal: National University of Singapore, 15 Kent Ridge Drive, NUS Business

WORKING PAPER NO THE CAUSES OF HOUSEHOLD BANKRUPTCY: THE INTERACTION OF INCOME SHOCKS AND BALANCE SHEETS

WORKING PAPER NO. 16-19 THE CAUSES OF HOUSEHOLD BANKRUPTCY: THE INTERACTION OF INCOME SHOCKS AND BALANCE SHEETS Vyacheslav Mikhed Payment Cards Center Federal Reserve Bank of Philadelphia Barry Scholnick

WORKING PAPER NO. 16-19 THE CAUSES OF HOUSEHOLD BANKRUPTCY: THE INTERACTION OF INCOME SHOCKS AND BALANCE SHEETS Vyacheslav Mikhed Payment Cards Center Federal Reserve Bank of Philadelphia Barry Scholnick

Household Heterogeneity in Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

CONSUMPTION SMOOTHING AFTER THE FINAL MORTGAGE PAYMENT: TESTING THE MAGNITUDE HYPOTHESIS

FORTHCOMING: REVIEW OF ECONOMICS AND STATISTICS NOTE CONSUMPTION SMOOTHING AFTER THE FINAL MORTGAGE PAYMENT: TESTING THE MAGNITUDE HYPOTHESIS Barry Scholnick School of Business, University of Alberta,

FORTHCOMING: REVIEW OF ECONOMICS AND STATISTICS NOTE CONSUMPTION SMOOTHING AFTER THE FINAL MORTGAGE PAYMENT: TESTING THE MAGNITUDE HYPOTHESIS Barry Scholnick School of Business, University of Alberta,

Worker Betas: Five Facts about Systematic Earnings Risk

Worker Betas: Five Facts about Systematic Earnings Risk By FATIH GUVENEN, SAM SCHULHOFER-WOHL, JAE SONG, AND MOTOHIRO YOGO How are the labor earnings of a worker tied to the fortunes of the aggregate economy,

Worker Betas: Five Facts about Systematic Earnings Risk By FATIH GUVENEN, SAM SCHULHOFER-WOHL, JAE SONG, AND MOTOHIRO YOGO How are the labor earnings of a worker tied to the fortunes of the aggregate economy,

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

Consumer Spending and the Economic Stimulus Payments of 2008 *

Consumer Spending and the Economic Stimulus Payments of 2008 * Jonathan A. Parker Northwestern University and NBER Nicholas S. Souleles University of Pennsylvania and NBER David S. Johnson U.S. Census

Consumer Spending and the Economic Stimulus Payments of 2008 * Jonathan A. Parker Northwestern University and NBER Nicholas S. Souleles University of Pennsylvania and NBER David S. Johnson U.S. Census

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

ESSAYS ON STRUCTURAL MODELS AND MICRO DATA IN CONSUMER FINANCE. Jiaxiong Yao

ESSAYS ON STRUCTURAL MODELS AND MICRO DATA IN CONSUMER FINANCE by Jiaxiong Yao A dissertation submitted to The Johns Hopkins University in conformity with the requirements for the degree of Doctor of Philosophy.

ESSAYS ON STRUCTURAL MODELS AND MICRO DATA IN CONSUMER FINANCE by Jiaxiong Yao A dissertation submitted to The Johns Hopkins University in conformity with the requirements for the degree of Doctor of Philosophy.

How Individuals Smooth Spending: Evidence from the 2013 Government Shutdown Using Account Data *

How Individuals Smooth Spending: Evidence from the 2013 Government Shutdown Using Account Data * Michael Gelman, Shachar Kariv, Matthew D. Shapiro, Dan Silverman, Steven Tadelis First Version: February

How Individuals Smooth Spending: Evidence from the 2013 Government Shutdown Using Account Data * Michael Gelman, Shachar Kariv, Matthew D. Shapiro, Dan Silverman, Steven Tadelis First Version: February

1 Business-Cycle Facts Around the World 1

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Capital markets liberalization and global imbalances

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the