Microfinance Credit Reporting. Colin Raymond - IFC CB Regional Specialist - Asia Rabat September, 2014 Session 11

|

|

|

- Shonda Bradley

- 6 years ago

- Views:

Transcription

1 Microfinance Credit Reporting Colin Raymond - IFC CB Regional Specialist - Asia Rabat September, 2014 Session 11

2 Case Study of MicroMicro Read description of the case study provided Discuss the following questions: What are some of the expected obstacles and what recommended solutions can you propose? How do you build the confidence of the rest of the industry to share their customer data? What can the bureaus do on their part, to encourage the submission of data by as many of the industry participants as possible? What resistance (if any) should we expect from staff/personnel within MM? Any other critical issues to consider? Prepare 4-5 key recommendations You have 15 minutes to complete this exercise 2

3 MFI Credit Bureau Initiative - India HKN Raghavan - COO Equitas Rabat September, 2014 Session 11 bis

4 Seeds of Credit Bureau Managing Director of Equitas Micro Finance within 2 months of inception strongly felt that there was a need to have better control on the clients leverage. Dec 2008, on the sidelines of the CGAP workshop it was decided to set up an informal data sharing amongst all the MFI s to know the default and over leveraged clients. MFIs had to seek the services of the credit bureaus approved by the Central Bank. Dec 2009, an association of the NBFCs (Non Banking Financial Institutions) MFI s formed an association under the name MFIN (Micro Finance Institutions Network). Highmark, Equifax, Experian were awarded licenses to set up in India. MFIN decided to work with Highmark for credit bureau initiative and also invested in Highmark as a signal to work closely with them. Vijay Mahajan, a father figure for the Micro Finance industry galvanized the entire NBFC MFI s to support this initiative. IFC provided the technical support. Omidyar funded the project, while MFIN did the ground work. IFC did the coordinating all these activities Dec, the credit bureau got established. 4

5 Challenges Many MFIs did not have data captured in the system, different hardware & software, different architecture. All these were a major issue. Many MFIs expressed doubt over misuse of the data for competitive purpose. Some of them were quite skeptical about the output in the absence of common KYC norms. IFC hired a technical consultant who worked with each individual MFI and studied the various software and platform on which the MFIs were working. They developed a software which can sit on any type of architecture and software and extract a common data format (CDF) which can be uploaded by the credit bureau. MFIN on the other hand had a detailed discussion with all the MFI s to alley the fear on any breach of data confidentiality. Regulator came out with guidelines of max 2 MFI exposure for the client made the MFI s to fall in line. April 2011, Equitas and Ujjivan, 2 MFI s started accessing the credit reports. 5

6 Operational Challenges There were discipline issues of submitting the data consistently with quality every month. By the time the data got uploaded the lag would have been 45 days. In this gap the client could avail loans from other MFIs. Other challenge was if MFIs are using the Credit Bureau report before taking any decision on lending. MFIN set up a credit bureau committee consisting the members who drew road map for weekly data submission, also to know if MFIs were using the CB report for credit decision. This follow up yielded a significant result where the data submission became more uniform and disciplined. 6

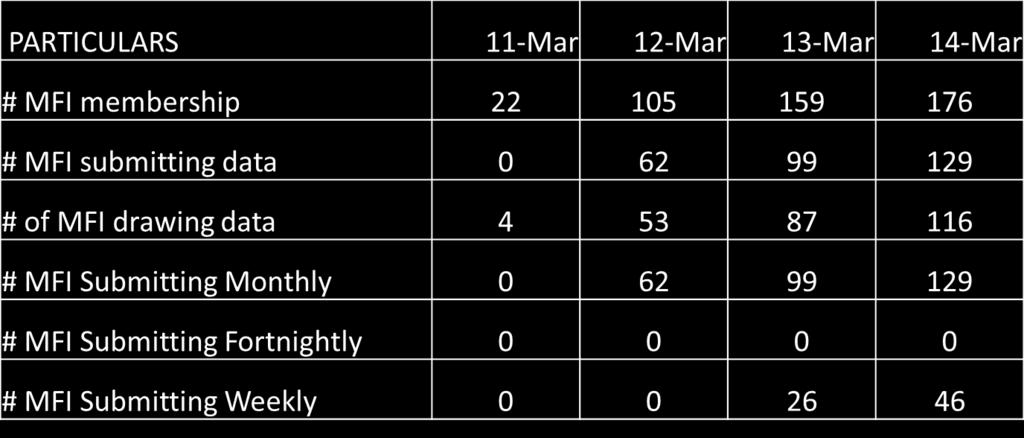

7 Progress on data 7

8 Clients Portfolio Analysis 8

9 Next set of challenges 96% accuracy has been achieved thanks to MFI fraternity and the work done by the credit bureaus. We further need to plug the gap. IFC funded the next round of initiative with technology partner which is under way working on further fine tuning the quality of the data. With the recommendations given we should be able to achieve close to 100% accuracy of the data output. MFIN is working with the central bank on getting the similar data on Self Help Groups to the bureau so that we will have complete exposure otherwise this is limited to the MFI borrowing only. We would say this has been fantastic journey where something impossible has been achieved at such a short time. 9

10 Q & A Discussion 10

11 2014 Exercise Session 11 - Rabat training Credit bureaus and microfinance: The case of MicroMicro Shall MFIs use Credit bureaus in order to better control their portfolio? Colin Raymond and HKN Raghavan 23 September, 2014

12 CREDIT REPORTING EXERCISE SESSION 11 - RABAT TRAINING Shall MFIs use Credit bureaus in order to better control their portfolio 23 September, 2014 DRAFT WORKSHOP CASE STUDY MicroMicro (MM) is a specialized microfinance institution offering flexible micro- credit, micro- savings and micro- insurance products countrywide. MM is currently active in 12 districts, encompassing both rural and urban areas of the country, and has successfully implemented development projects involving wide- ranging development aims: from disaster risk reduction to the provision of non- formal education to working children. In particular, MM is at the forefront of efforts to improve the lives of poor and extreme poor people. MM has been engaged in (i) empowering target groups through institution building, (ii) women s development, (iii) environmental development through awareness raising, plantation and sanitation programs, (iv) emergency disaster response and service delivery, (v) the provision of health services to women, children, adolescent and older people (vi) formal and non- formal education to underprivileged children, (vii) income generation through micro- credit operations, (viii) employment development training for the poor, (ix) natural disaster preparedness and risk reduction programs, (x) empowerment of older people, (xi) agriculture development and food security and (xii) urban governance. Target clients: Very poor, poor, micro- entrepreneurs, small and marginal farmers Mission: To be an independent, sustainable, cost- effective microfinance institution that provides diverse, appropriate and market responsive quality financial and business development services at competitive prices along with other social development programs to very poor, poor and non- poor customers. Products: The microcredit products on offer consist of both, group- based microcredit (urban and rural), as well as individual microenterprise loans. Moreover, existing clients are eligible for short- term additional loans such as seasonal input loans, educational loans and disaster relief loans. Installments have to be made on a weekly, bi- weekly or monthly basis, depending on the loan category. For regular loans, the term is fixed at 12 months, interest rate ranging from 25 to 35%, repayments are scheduled over 45 weeks only. Different types of loans are given to meet specific needs of customers. The loans include rural/urban, micro- enterprise, disaster, seasonal, educational, ultra- poor, emergency, festival, family and housing loans. Despite significant competition (at least half a dozen other MFIs operate in the same geographical districts) and the recent financial crisis, MM has managed to remain profitable in its microcredit operations. Loan repayments are maintained on healthy levels, while the customer base will need to be broadened steeply over the next 2-3 years. Operational strategy: Formation of village organization (kendra) with poor women. Weekly meeting for participatory decision making, Provide social awareness training and then provide small credit based on their need and proposal. International Finance Corporation Advisory Services The World Bank Group IFC Advisory Services Page 2

13 CREDIT REPORTING EXERCISE SESSION 11 - RABAT TRAINING Shall MFIs use Credit bureaus in order to better control their portfolio 23 September, 2014 Credit Bureaus: Around 12 months ago, the regulating authority issued operating licenses to 4 private credit bureaus, two of whom have started operations and are actively recruiting new members. They are both making the claim as to having the largest database and the best coverage of MFI loans in the country. Both bureaus are keen for MM s patronage and appear to be willing to be very price competitive. As previously mentioned, there are a number of other MFIs operating in the same geography. Some of whom are regulated, while there are a large number non- regulated, they have no obligation to share their credit information, nor to consult with credit bureaus the credit history of their prospective customers. There is a mistrust of credit bureaus, they believe that if they share their credit information, customers will be easily stolen by other financial institutions. There are other issues like internet service not being available everywhere and poor IT capabilities in most institutions. MM is determined to change this situation in order to develop a robust market, with lower rates of non- performing loans and lesser risk of over- indebtedness. Your Assignment (should you decide to accept it!) You are a consultant engaged by MM who has been charged to assess the situation and recommend whether they should use credit bureau services in order to have a better control of their loan portfolio, as well to screen customers more carefully. Focus on the WHAT & HOW of what MM will need to do as actionable activities to incorporate the use of credit bureau services into their risk assessment practices. What are some of the expected obstacles and what recommended solutions can you propose? How do you build the confidence of the rest of the industry to share their customer data? What can the bureaus do on their part, to encourage the submission of data by as many of the industry participants as possible? What resistance (if any) should we expect from staff/personnel within MM? Any other critical issues to consider? Discuss this question with your group and prepare a brief presentation (4-5 bullets with your recommendations). You have 1 International Finance Corporation Advisory Services The World Bank Group IFC Advisory Services Page 3

14 CREDIT REPORTING EXERCISE SESSION 11 - RABAT TRAINING Shall MFIs use Credit bureaus in order to better control their portfolio 23 September, 2014 International Finance Corporation Advisory Services The World Bank Group IFC Advisory Services Page 4

MICROFINANCE INSTITUTIONS/RURAL CREDIT REPORTING. Colin Raymond / Mauricio Zambrana Kuala Lumpur November, Session 9

MICROFINANCE INSTITUTIONS/RURAL CREDIT REPORTING Colin Raymond / Mauricio Zambrana Kuala Lumpur - 5-9 November, 2012 - Session 9 Presentation contents Background to Microfinance Case Study (MicroMicro)

MICROFINANCE INSTITUTIONS/RURAL CREDIT REPORTING Colin Raymond / Mauricio Zambrana Kuala Lumpur - 5-9 November, 2012 - Session 9 Presentation contents Background to Microfinance Case Study (MicroMicro)

Questions/Concerns regarding PAT CDP through Microcredit proposal

Questions/Concerns regarding PAT CDP through Microcredit proposal 1) In the proposal, it says - almost all our 35000 target members in Ariyalur, Trichy and Tanjore Districts in TamilNadu... What kind of

Questions/Concerns regarding PAT CDP through Microcredit proposal 1) In the proposal, it says - almost all our 35000 target members in Ariyalur, Trichy and Tanjore Districts in TamilNadu... What kind of

GUIDELINES OF INDIA MICROFINANCE EQUITY FUND

GUIDELINES OF INDIA MICROFINANCE EQUITY FUND 1 CONTENTS 1. Objective - Page 3 2. Principal features - Page 3 3. Purpose - Page 3 4. Types of instruments - Page 3 5. Eligibility criteria - Page 4 6. Sanction

GUIDELINES OF INDIA MICROFINANCE EQUITY FUND 1 CONTENTS 1. Objective - Page 3 2. Principal features - Page 3 3. Purpose - Page 3 4. Types of instruments - Page 3 5. Eligibility criteria - Page 4 6. Sanction

Case module 10 (a): Building Trust and Assets After the Khmer Rouge CARE Community Savings Microfinance in Cambodia

: Building Trust and Assets After the Khmer Rouge CARE Community Savings Microfinance in Cambodia") Case module 10 (a): Building Trust and Assets After the Khmer Rouge CARE Community Savings Microfinance in Cambodia Decades of war have taken their toll on Cambodia s human and economic development. High

Case module 10 (a): Building Trust and Assets After the Khmer Rouge CARE Community Savings Microfinance in Cambodia Decades of war have taken their toll on Cambodia s human and economic development. High

SAMRUDHI Micro Fin Society (SMS) Brief Profile

Brief Profile") SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

Micro Finance in the World and in India: Status, Problems and Prospects

Micro Finance in the World and in India: Status, Problems and Prospects By Vijay Mahajan Chair, CGAP ExCom Founder and CEO, BASIX Social Enterprise Group, India President, MFIN (MFI Network of India) March

Micro Finance in the World and in India: Status, Problems and Prospects By Vijay Mahajan Chair, CGAP ExCom Founder and CEO, BASIX Social Enterprise Group, India President, MFIN (MFI Network of India) March

Mysterious ways of Impact Investing

Murder on the Orient Express? Mysterious ways of Impact Investing Raghavan Narayanan World Bank Group Outline 1. What is the media saying and Who are the suspects? (A View of the Impact Investor Universe)

Murder on the Orient Express? Mysterious ways of Impact Investing Raghavan Narayanan World Bank Group Outline 1. What is the media saying and Who are the suspects? (A View of the Impact Investor Universe)

Mongolia: Development of State Audit Capacity

Technical Assistance Report Project Number: 47198-001 Capacity Development Technical Assistance (CDTA) November 2013 Mongolia: Development of State Audit Capacity The views expressed herein are those of

Technical Assistance Report Project Number: 47198-001 Capacity Development Technical Assistance (CDTA) November 2013 Mongolia: Development of State Audit Capacity The views expressed herein are those of

Blended finance in Myanmar. TCX s role in realizing financial inclusion through innovative partnerships in Myanmar

Blended finance in Myanmar TCX s role in realizing financial inclusion through innovative partnerships in Myanmar Table of Contents FOREWORD 4 TCX AT WORK 5 How local currency finance benefits Myanmar

Blended finance in Myanmar TCX s role in realizing financial inclusion through innovative partnerships in Myanmar Table of Contents FOREWORD 4 TCX AT WORK 5 How local currency finance benefits Myanmar

REPORT 2015/174 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

M2i s Experience in Microfinance

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

Chapter-VII Data Analysis and Interpretation

Chapter-VII Data Analysis and Interpretation 16 CHAPTER-VII DATA ANALYSIS AND INTERPRETATION In order to arrive at a logical and constructive analysis of micro financing by commercial banks in Rajasthan

Chapter-VII Data Analysis and Interpretation 16 CHAPTER-VII DATA ANALYSIS AND INTERPRETATION In order to arrive at a logical and constructive analysis of micro financing by commercial banks in Rajasthan

IFC Supported Program

IFC Supported Program Microfinance Institutions are a good medium to save money for micro entrepreneurs, although there have been differences of opinion. IFC s supported project on microfinance has created

IFC Supported Program Microfinance Institutions are a good medium to save money for micro entrepreneurs, although there have been differences of opinion. IFC s supported project on microfinance has created

CODE OF CONDUCT FOR MICROFINANCE INSTITUTIONS IN INDIA

CODE OF CONDUCT FOR MICROFINANCE INSTITUTIONS IN INDIA PREAMBLE Microfinance Institutions (MFIs), irrespective of legal forms, seek to create social benefits and promote financial inclusion by providing

CODE OF CONDUCT FOR MICROFINANCE INSTITUTIONS IN INDIA PREAMBLE Microfinance Institutions (MFIs), irrespective of legal forms, seek to create social benefits and promote financial inclusion by providing

GRAMEEN FINANCIAL SERVICES PVT. LTD. S CODE OF CONDUCT E-LEARNING MODULE

GRAMEEN FINANCIAL SERVICES PVT. LTD. S CODE OF CONDUCT E-LEARNING MODULE Meet Grameen Financial Services Pvt. Ltd. Grameen Financial Services Pvt. Ltd. (GFSL) is an Indian Non Banking Financial Company

GRAMEEN FINANCIAL SERVICES PVT. LTD. S CODE OF CONDUCT E-LEARNING MODULE Meet Grameen Financial Services Pvt. Ltd. Grameen Financial Services Pvt. Ltd. (GFSL) is an Indian Non Banking Financial Company

Madura Micro Finance Limited. Corporate Social Responsibility Policy 2015

Madura Micro Finance Limited (CIN: U65929TN2005PLC057390) Corporate Social Responsibility Policy 2015 Brief Background In terms of Section 135 of Companies Act, 2013, effective 1 st April 2014, every Company

Madura Micro Finance Limited (CIN: U65929TN2005PLC057390) Corporate Social Responsibility Policy 2015 Brief Background In terms of Section 135 of Companies Act, 2013, effective 1 st April 2014, every Company

1BSUOFST GPS %FWFMPQNFOU T "QQSPBDI UP.JDSPöOBODF

1BSUOFST GPS %FWFMPQNFOU T "QQSPBDI UP.JDSPöOBODF %FDFNCFS Partners for Development gggͷ`trͷ_bv Table of Contents Introduction... 2 Why PfD Supports Microcredit... 2 How PfD Supports Microcredit... 2 Partner

1BSUOFST GPS %FWFMPQNFOU T "QQSPBDI UP.JDSPöOBODF %FDFNCFS Partners for Development gggͷ`trͷ_bv Table of Contents Introduction... 2 Why PfD Supports Microcredit... 2 How PfD Supports Microcredit... 2 Partner

BFIL s lowest interest rate benefits 55 lakh women in 1 lakh villages

BFIL UPDATE Sab se Sastha loan BFIL s lowest interest rate benefits 55 lakh women in 1 lakh villages MAR 2017 BHARAT FINANCIAL INCLUSION LIMITED (Formerly known as SKS Microfinance Limited ) BSE: 533228

BFIL UPDATE Sab se Sastha loan BFIL s lowest interest rate benefits 55 lakh women in 1 lakh villages MAR 2017 BHARAT FINANCIAL INCLUSION LIMITED (Formerly known as SKS Microfinance Limited ) BSE: 533228

TANMEYAH MICRO ENTERPRISE SERVICES. Microinsurance Learning Sessions in Egypt Innovative ways of Micro insurance Distribution

TANMEYAH MICRO ENTERPRISE SERVICES Microinsurance Learning Sessions in Egypt Innovative ways of Micro insurance Distribution Contents About Us I. Tanmeyah: The First and Last Resort for Microenterprises

TANMEYAH MICRO ENTERPRISE SERVICES Microinsurance Learning Sessions in Egypt Innovative ways of Micro insurance Distribution Contents About Us I. Tanmeyah: The First and Last Resort for Microenterprises

Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012

Bill, 2012") Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012 The Bill was introduced in the Lok Sabha by the Minister of Finance on May 22, 2012. The Bill was referred to the

Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012 The Bill was introduced in the Lok Sabha by the Minister of Finance on May 22, 2012. The Bill was referred to the

PNPM SUPPORT FACILITY (PSF) Project Proposal

Project Proposal") PNPM SUPPORT FACILITY (PSF) Project Proposal Project Title: Objective: Executing Agency: Estimated Duration: Estimated Budget: Geographic Coverage: Implementation Arrangements: PNPM Mandiri Revolving Loan

PNPM SUPPORT FACILITY (PSF) Project Proposal Project Title: Objective: Executing Agency: Estimated Duration: Estimated Budget: Geographic Coverage: Implementation Arrangements: PNPM Mandiri Revolving Loan

UTILIZATION OF CREDIT REPORTING DATA FOR THE FINANCIAL AND BANKING SECTOR, AND BANKING SUPERVISION JAVIER VACA- RFD ECUADOR

UTILIZATION OF CREDIT REPORTING DATA FOR THE FINANCIAL AND BANKING SECTOR, AND BANKING SUPERVISION JAVIER VACA- RFD ECUADOR TABLE OF CONTENTS 1.Background: Ecuador status (2000) 2.Problem of credit reporting

UTILIZATION OF CREDIT REPORTING DATA FOR THE FINANCIAL AND BANKING SECTOR, AND BANKING SUPERVISION JAVIER VACA- RFD ECUADOR TABLE OF CONTENTS 1.Background: Ecuador status (2000) 2.Problem of credit reporting

ANSWER KEY C F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C Indian Financial System

(CHOICE BASE) SEMESTER - I / C Indian Financial System") ANSWER KEY-00135 C0921 - F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C0584 - Indian Financial System Q1) a) Answer whether the below statements are True or False: (Attempt any 8) (8

ANSWER KEY-00135 C0921 - F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C0584 - Indian Financial System Q1) a) Answer whether the below statements are True or False: (Attempt any 8) (8

LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT

45 LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT Edward M. Gramlich Member, Board of Governors of the Federal Reserve System Introduction I am pleased to be here today to kick off the conference

45 LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT Edward M. Gramlich Member, Board of Governors of the Federal Reserve System Introduction I am pleased to be here today to kick off the conference

Evaluation Approach Project Performance Evaluation Report for Loan 2167 and Grant 0006-SRI: Tsunami-Affected Areas Rebuilding Project September 2015

Asian Development Bank 6 ADB Avenue, Mandaluyong City, 1550 Metro Manila, Philippines Tel +63 2 632 4444; Fax +63 2 636 2163; evaluation@adb.org www.adb.org/evaluation Evaluation Approach Project Performance

Asian Development Bank 6 ADB Avenue, Mandaluyong City, 1550 Metro Manila, Philippines Tel +63 2 632 4444; Fax +63 2 636 2163; evaluation@adb.org www.adb.org/evaluation Evaluation Approach Project Performance

IFMR CAPITAL CONNECTING MICROFINANCE INSTITUTIONS TO CAPITAL MARKETS

Introduction to Securitisation for MFIs IFMR CAPITAL CONNECTING MICROFINANCE INSTITUTIONS TO CAPITAL MARKETS About IFMR Capital IFMR Capital is a non-banking finance company based in Chennai, whose mission

Introduction to Securitisation for MFIs IFMR CAPITAL CONNECTING MICROFINANCE INSTITUTIONS TO CAPITAL MARKETS About IFMR Capital IFMR Capital is a non-banking finance company based in Chennai, whose mission

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN Non-Bank Microfinance Guide NIC Building, 63 Jinnah Avenue, Islamabad, Pakistan Tel: 051-9207091-4, UAN: 111 117 327 Fax: 051-9204915 Website: www.secp.gov.pk

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN Non-Bank Microfinance Guide NIC Building, 63 Jinnah Avenue, Islamabad, Pakistan Tel: 051-9207091-4, UAN: 111 117 327 Fax: 051-9204915 Website: www.secp.gov.pk

Understanding Rural Finance Issues and the Macro and Micro Operating Environment. Module 2 Rural Finance & Microfinance Actors and approaches

Understanding Rural Finance Issues and the Macro and Micro Operating Environment Module 2 Rural Finance & Microfinance Actors and approaches Rural and Agricultural Finance Module 2 Agenda Block 1 Introductions

Understanding Rural Finance Issues and the Macro and Micro Operating Environment Module 2 Rural Finance & Microfinance Actors and approaches Rural and Agricultural Finance Module 2 Agenda Block 1 Introductions

Regulation of Microfinance Institutions in India

Regulation of Microfinance Institutions in India Santadarshan Sadhu, Kenny Kline, Justin Oliver CMF-IFMR 20 th April 2011 Study Outline Microfinance sector - overview Analysis of the existing regulatory

Regulation of Microfinance Institutions in India Santadarshan Sadhu, Kenny Kline, Justin Oliver CMF-IFMR 20 th April 2011 Study Outline Microfinance sector - overview Analysis of the existing regulatory

CSR POLICY OF MAX LIFE INSURANCE COMPANY LTD.

CSR POLICY OF MAX LIFE INSURANCE COMPANY LTD. I. PREAMBLE 1.1 Corporate Social Responsibility has been an area of focus or the Max Group and Max Life Insurance Company Limited, ( Max Life or the Company

CSR POLICY OF MAX LIFE INSURANCE COMPANY LTD. I. PREAMBLE 1.1 Corporate Social Responsibility has been an area of focus or the Max Group and Max Life Insurance Company Limited, ( Max Life or the Company

WTO: The Question of Microfinance in LEDCs Cambridge Model United Nations 2018

Study Guide: The Question of Microfinance in LEDCs Committee: World Trade Organisation Topic: The Question of Microfinance in LEDC s Introduction: Micro financing has been used as a way of helping those

Study Guide: The Question of Microfinance in LEDCs Committee: World Trade Organisation Topic: The Question of Microfinance in LEDC s Introduction: Micro financing has been used as a way of helping those

RBI/ /49 DNBS.(PD)CC.No. 347 / / July 1, 2013

CC.No. 347 / / July 1, 2013") RBI/2013-14/49 DNBS.(PD)CC.No. 347 /03.10.38/2013-14 July 1, 2013 To, All NBFCs(excluding RNBCs) Dear Sirs, Master Circular- Introduction of New Category of NBFCs - Non Banking Financial Company-Micro

RBI/2013-14/49 DNBS.(PD)CC.No. 347 /03.10.38/2013-14 July 1, 2013 To, All NBFCs(excluding RNBCs) Dear Sirs, Master Circular- Introduction of New Category of NBFCs - Non Banking Financial Company-Micro

Reviewing the Role of Namibia Post Savings Bank (NSB) in Broadening Access to Financial Services to the Poor. Problem Statement Background...

in Broadening Access to Financial Services to the Poor. Problem Statement Background...") Reviewing the Role of Namibia Post Savings Bank (NSB) in Broadening Access to Financial Services to the Poor Table of Contents Problem Statement... 3 Background... 3 Analysis... 4 The Status Quo of Nampost

Reviewing the Role of Namibia Post Savings Bank (NSB) in Broadening Access to Financial Services to the Poor Table of Contents Problem Statement... 3 Background... 3 Analysis... 4 The Status Quo of Nampost

Credit for Water and Sanitation Improvements: a Case Study of Women s Self-Help Groups in Tamil Nadu, India

Credit for Water and Sanitation Improvements: a Case Study of Women s Self-Help Groups in Tamil Nadu, India Executive summary In 2003, WaterPartners initiated a program which utilized micro-finance to

Credit for Water and Sanitation Improvements: a Case Study of Women s Self-Help Groups in Tamil Nadu, India Executive summary In 2003, WaterPartners initiated a program which utilized micro-finance to

Peter Graves Senior Vice President, Technical Services World Council of Credit Unions

Expanding Access to Finance to the Bottom Billion Critical Factors Presentation to UN Preparatory Process/3 rd International Conference on Financing for Development 14 November 2014 Peter Graves Senior

Expanding Access to Finance to the Bottom Billion Critical Factors Presentation to UN Preparatory Process/3 rd International Conference on Financing for Development 14 November 2014 Peter Graves Senior

Gender Issues in SME Finance: Philippines

2011/GFPN/WKSP/023 Session 7 Gender Issues in SME Finance: Philippines Submitted by: Philippines Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011 Gender Issues in SME Finance: Philippines

2011/GFPN/WKSP/023 Session 7 Gender Issues in SME Finance: Philippines Submitted by: Philippines Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011 Gender Issues in SME Finance: Philippines

1. Key development issues and rationale for Bank involvement

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized DRAFT PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB5278 Project Name

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized DRAFT PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB5278 Project Name

Supply of and Demand for Financial Products

Chapter 2 Supply of and Demand for Financial Products 2.1 Payment and Transaction Products Payment and transaction products play key roles in smoothing retail banking and settling payment obligations in

Chapter 2 Supply of and Demand for Financial Products 2.1 Payment and Transaction Products Payment and transaction products play key roles in smoothing retail banking and settling payment obligations in

A Billion to Gain? Microfinance clients are not cut from the same cloth

A Billion to Gain? Microfinance clients are not cut from the same cloth Introduction Exploring differences in microfinance impact Problems with the impact for an average client and the need for heterogeneous

A Billion to Gain? Microfinance clients are not cut from the same cloth Introduction Exploring differences in microfinance impact Problems with the impact for an average client and the need for heterogeneous

Labelled Loans, Credit Constraints and Sanitation Investments -- Evidence from an RCT on sanitation loans in rural India

Labelled Loans, Credit Constraints and Sanitation Investments -- Evidence from an RCT on sanitation loans in rural India Strategic Impact Evaluation Fund Institute for Fiscal Studies Britta Augsburg, Bet

Labelled Loans, Credit Constraints and Sanitation Investments -- Evidence from an RCT on sanitation loans in rural India Strategic Impact Evaluation Fund Institute for Fiscal Studies Britta Augsburg, Bet

CSR Policy of Delta Corp Limited. 1. Corporate Social Responsibility (CSR) Policy of Delta Corp Limited ( Company )

Policy of Delta Corp Limited ( Company )") CSR Policy of Delta Corp Limited 1. Corporate Social Responsibility (CSR) Policy of Delta Corp Limited ( Company ) Corporate Social Responsibility is strongly connected with the principles of Sustainability;

CSR Policy of Delta Corp Limited 1. Corporate Social Responsibility (CSR) Policy of Delta Corp Limited ( Company ) Corporate Social Responsibility is strongly connected with the principles of Sustainability;

New Zealand Clearing Limited. Clearing and Settlement Procedures

New Zealand Clearing Limited Clearing and Settlement Procedures 6 May 2016 Contents Section A: Interpretation and Construction 7 Section 1: Introduction and General Provisions 8 Amendment Procedure 8 1.1

New Zealand Clearing Limited Clearing and Settlement Procedures 6 May 2016 Contents Section A: Interpretation and Construction 7 Section 1: Introduction and General Provisions 8 Amendment Procedure 8 1.1

Clearing and Settlement Procedures. New Zealand Clearing Limited. Clearing and Settlement Procedures

Clearing and Settlement Procedures New Zealand Clearing Limited Clearing and Settlement Procedures 3 August 2010 Contents Section A: Interpretation and Construction 6 Section 1: Introduction and General

Clearing and Settlement Procedures New Zealand Clearing Limited Clearing and Settlement Procedures 3 August 2010 Contents Section A: Interpretation and Construction 6 Section 1: Introduction and General

FSDZ Multi Sector GIS Mapping Project Final Report 17th September 23 rd December 2015

FSDZ Multi Sector GIS Mapping Project Final Report 17th September 23 rd December 2015 Geo-Spatial Analysis: 3 Components 1). Access point data collection 3). Mapping Software 2). Add Poverty and other

FSDZ Multi Sector GIS Mapping Project Final Report 17th September 23 rd December 2015 Geo-Spatial Analysis: 3 Components 1). Access point data collection 3). Mapping Software 2). Add Poverty and other

September. EMN POLICY NOTE on the EMN Overview of the Microcredit Sector in the European Union

September 2014 EMN POLICY NOTE on the EMN Overview of the Microcredit Sector in the European Union 2012-13 EMN POLICY NOTE Steady growth of microcredit provision in value and number of microloans surveyed

September 2014 EMN POLICY NOTE on the EMN Overview of the Microcredit Sector in the European Union 2012-13 EMN POLICY NOTE Steady growth of microcredit provision in value and number of microloans surveyed

Mikrofin CARE Microfinance Case Study Banja Luka, Bosnia and Herzegovina (BH) September, 2001

September, 2001") Mikrofin CARE Microfinance Case Study Banja Luka, Bosnia and Herzegovina (BH) September, 2001 1 Program context and regional operating environment Mikrofin s microcredit program was originally started

Mikrofin CARE Microfinance Case Study Banja Luka, Bosnia and Herzegovina (BH) September, 2001 1 Program context and regional operating environment Mikrofin s microcredit program was originally started

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble MBA - I, Finance What is Microfinance? Microfinance is the supply of loans, savings, and other basic financial services to the

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble MBA - I, Finance What is Microfinance? Microfinance is the supply of loans, savings, and other basic financial services to the

OPPORTUNITY S MICROFINANCE IMPACT IN INDIA: Growth, Innovation, and Client Impact

OPPORTUNITY S MICROFINANCE IMPACT IN INDIA: Growth, Innovation, and Client Impact SUMMARY In India, Opportunity and its subsidiary Dia Vikas Capital partner with Indian microfinance institutions to provide

OPPORTUNITY S MICROFINANCE IMPACT IN INDIA: Growth, Innovation, and Client Impact SUMMARY In India, Opportunity and its subsidiary Dia Vikas Capital partner with Indian microfinance institutions to provide

Credit Information Sharing. Recent Developments: Credit Reporting Standards G20 SME Finance Initiative. Hong Kong, 24 th March 2011

Credit Information Sharing Recent Developments: Credit Reporting Standards G20 SME Finance Initiative Hong Kong, 24 th March 2011 Tony Lythgoe Head, Financial Infrastructure, Global Credit Bureau Program

Credit Information Sharing Recent Developments: Credit Reporting Standards G20 SME Finance Initiative Hong Kong, 24 th March 2011 Tony Lythgoe Head, Financial Infrastructure, Global Credit Bureau Program

Reserve Bank of India. Draft Guidelines for Licensing of New Banks in the Private Sector

Reserve Bank of India Draft Guidelines for Licensing of New Banks in the Private Sector August 29, 2011 Over the last two decades, the Reserve Bank licensed twelve banks in the private sector. This happened

Reserve Bank of India Draft Guidelines for Licensing of New Banks in the Private Sector August 29, 2011 Over the last two decades, the Reserve Bank licensed twelve banks in the private sector. This happened

Report and Recommendation of the President to the Board of Directors

Report and Recommendation of the President to the Board of Directors Project Number: 49207-001 November 2015 Proposed Equity Investment and Loan RBL Bank Supporting Financial Inclusion Project (India)

Report and Recommendation of the President to the Board of Directors Project Number: 49207-001 November 2015 Proposed Equity Investment and Loan RBL Bank Supporting Financial Inclusion Project (India)

Welcome to my Presentation

Welcome to my Presentation 12 November, 2010 Comparative synthesis of GB, BRAC and ASA microfinance approaches in Bangladesh Presented by- M. Wakilur Rahman Intern IPRCC, China PhD Research Student NWSUAF,

Welcome to my Presentation 12 November, 2010 Comparative synthesis of GB, BRAC and ASA microfinance approaches in Bangladesh Presented by- M. Wakilur Rahman Intern IPRCC, China PhD Research Student NWSUAF,

The Microfinance Law (The Pyidaungsu Hluttaw Law No.13) The 5 th Waxing Day of Nadaw, 1373 M.E. (30 th, November, 2011)

The 5 th Waxing Day of Nadaw, 1373 M.E. (30 th, November, 2011)") The Microfinance Law (The Pyidaungsu Hluttaw Law No.13) The 5 th Waxing Day of Nadaw, 1373 M.E. (30 th, November, 2011) The Pyidaungsu Hluttaw hereby enacts the following Law: Chapter I Title and Definition

The Microfinance Law (The Pyidaungsu Hluttaw Law No.13) The 5 th Waxing Day of Nadaw, 1373 M.E. (30 th, November, 2011) The Pyidaungsu Hluttaw hereby enacts the following Law: Chapter I Title and Definition

Internal Audit of NBFCs

Internal Audit of NBFCs Introduction to NBFC Meaning of NBFC A company registered under the Companies Act, 2013 engaged in: the business of loans and advances, acquisition of shares/stocks/bonds/debentures/securities

Internal Audit of NBFCs Introduction to NBFC Meaning of NBFC A company registered under the Companies Act, 2013 engaged in: the business of loans and advances, acquisition of shares/stocks/bonds/debentures/securities

FINAL EVALUATION VIE/033. Climate Adapted Local Development and Innovation Project

FINAL EVALUATION VIE/033 Climate Adapted Local Development and Innovation Project PROJECT SUMMARY DATA Country Long project title Short project title LuxDev Code Vietnam Climate Adapted Local Development

FINAL EVALUATION VIE/033 Climate Adapted Local Development and Innovation Project PROJECT SUMMARY DATA Country Long project title Short project title LuxDev Code Vietnam Climate Adapted Local Development

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro and Small Enterprise Finance Financial Institutions

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro and Small Enterprise Finance Financial Institutions

Banking and Finance Indian Microfinance Sector: Entering a phase of moderate credit risk, three years post AP crisis

Indian Microfinance Sector: Entering a phase of moderate credit risk, three years post AP crisis March 7, 214 Summary Microfinance sector in India has gone through 3 broad risk phases in the past high

Indian Microfinance Sector: Entering a phase of moderate credit risk, three years post AP crisis March 7, 214 Summary Microfinance sector in India has gone through 3 broad risk phases in the past high

Impact Investments in India

Introduction: Impact investments, which aim to generate financial returns while creating measurable social and environmental benefits to address some of the world s most pressing challenges, have attained

Introduction: Impact investments, which aim to generate financial returns while creating measurable social and environmental benefits to address some of the world s most pressing challenges, have attained

SAMRUDHI Micro Fin Society

SAMRUDHI Micro Fin Society Update & Renewal for Asha fellowship SAMRUDHI is a responsible civil society to work with the rural & urban poor women to reinforce their efforts to rise, remain, above the poverty

SAMRUDHI Micro Fin Society Update & Renewal for Asha fellowship SAMRUDHI is a responsible civil society to work with the rural & urban poor women to reinforce their efforts to rise, remain, above the poverty

WALL STREET MEETS MICROFINANCE

NOVEMBER 3, 2003 WWB/FWA LENORE ALBOM LECTURE SERIES WALL STREET MEETS MICROFINANCE STANLEY FISCHER 1 CITIGROUP I must confess that I started out as a skeptic on microfinance even after I had heard about

NOVEMBER 3, 2003 WWB/FWA LENORE ALBOM LECTURE SERIES WALL STREET MEETS MICROFINANCE STANLEY FISCHER 1 CITIGROUP I must confess that I started out as a skeptic on microfinance even after I had heard about

Session 1: SME financing in Asia and the Pacific and Latin America An overview. SME financing in Asia and the Pacific An introduction to the workshop

Session 1: SME financing in Asia and the Pacific and Latin America An overview SME financing in Asia and the Pacific An introduction to the workshop A presentation by Alberto Isgut, Financing for Development

Session 1: SME financing in Asia and the Pacific and Latin America An overview SME financing in Asia and the Pacific An introduction to the workshop A presentation by Alberto Isgut, Financing for Development

Key Findings. Financing Water and Sanitation for the Poor PROBLEM STATEMENT

WATER AND SANITATION PROGRAM: LEARNING NOTE Financing Water and Sanitation for the Poor The role of microfinance institutions in addressing the water and sanitation gap November 2015 PROBLEM STATEMENT

WATER AND SANITATION PROGRAM: LEARNING NOTE Financing Water and Sanitation for the Poor The role of microfinance institutions in addressing the water and sanitation gap November 2015 PROBLEM STATEMENT

Al-Amal Microfinance Bank

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

Recent Crisis in India and Other Parts and Lessons for Commercial Microfinance

2011/GFPN/WKSP/006 Session 1 Recent Crisis in India and Other Parts and Lessons for Commercial Microfinance Submitted by: BASIX Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011 Recent

2011/GFPN/WKSP/006 Session 1 Recent Crisis in India and Other Parts and Lessons for Commercial Microfinance Submitted by: BASIX Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011 Recent

People s Republic of China: Promotion of a Legal Framework for Financial Consumer Protection

Technical Assistance Report Project Number: 47042-001 Policy and Advisory Technical Assistance (PATA) October 2013 People s Republic of China: Promotion of a Legal Framework for Financial Consumer Protection

Technical Assistance Report Project Number: 47042-001 Policy and Advisory Technical Assistance (PATA) October 2013 People s Republic of China: Promotion of a Legal Framework for Financial Consumer Protection

Terms of Reference (ToR) Business Potential survey in Doti District

Business Potential survey in Doti District") Terms of Reference (ToR) Business Potential survey in Doti District 1. Background Good Neighbors International (GNI) is an international humanitarian and development NGO in general consultative status

Terms of Reference (ToR) Business Potential survey in Doti District 1. Background Good Neighbors International (GNI) is an international humanitarian and development NGO in general consultative status

A STUDY ON FINANCIAL INCLUSION AWARENESS AMONG SELECTED WORKING WOMEN OF SATNA (M.P.)

") A STUDY ON FINANCIAL INCLUSION AWARENESS AMONG SELECTED WORKING WOMEN OF SATNA (M.P.) SHWETA SINGH Research scholar at MGCGV Chitrakoot, Satna (M.P.) ABSTRACT This research work is based on the awareness

A STUDY ON FINANCIAL INCLUSION AWARENESS AMONG SELECTED WORKING WOMEN OF SATNA (M.P.) SHWETA SINGH Research scholar at MGCGV Chitrakoot, Satna (M.P.) ABSTRACT This research work is based on the awareness

EFSE Annual Meeting 2009 Structure and Performance of EFSE

EFSE Annual Meeting 2009 Structure and Performance of EFSE Arial EFSE 24and the Financial Crisis Responsible Finance NOVI SAD, SERBIA 27 MAY 2009 A Unique Blend of Commercial and Social Values EFSE - A

EFSE Annual Meeting 2009 Structure and Performance of EFSE Arial EFSE 24and the Financial Crisis Responsible Finance NOVI SAD, SERBIA 27 MAY 2009 A Unique Blend of Commercial and Social Values EFSE - A

Job creation: Progress Microfinance implementation report frequently asked questions

EUROPEAN COMMISSION MEMO Brussels, 17 July 2012 Job creation: Progress Microfinance implementation report 2011 - frequently asked questions The European Progress Microfinance Facility (Progress Microfinance)

EUROPEAN COMMISSION MEMO Brussels, 17 July 2012 Job creation: Progress Microfinance implementation report 2011 - frequently asked questions The European Progress Microfinance Facility (Progress Microfinance)

Asha for Education Fellowship Application Form

Asha for Education Fellowship Application Form SECTION I: Personal Contact Information Name : Sanju Kumar Address : H.No.144, 2 nd Cross, Behind Bus Stand C.I.B Colony, Gulbarga-585104 Karnataka State,

Asha for Education Fellowship Application Form SECTION I: Personal Contact Information Name : Sanju Kumar Address : H.No.144, 2 nd Cross, Behind Bus Stand C.I.B Colony, Gulbarga-585104 Karnataka State,

HOUSING FINANCE FROM A MICROFINANCE PERSPECTIVE

Organized by HOUSING FINANCE FROM A MICROFINANCE PERSPECTIVE HOUSING FINANCE: OPENING FRONTIERS THROUGH MICROFINANCE September 12, 2017 Micro Housing-an effective vehicle for financial inclusion Housing

Organized by HOUSING FINANCE FROM A MICROFINANCE PERSPECTIVE HOUSING FINANCE: OPENING FRONTIERS THROUGH MICROFINANCE September 12, 2017 Micro Housing-an effective vehicle for financial inclusion Housing

Potency and The Role of Credit Union in Poverty Alleviation Through Perspective Rural Economic Development

Potency and The Role of Credit Union in Poverty Alleviation Through Perspective Rural Economic Development Izzati Amperaningrum Faculty of Economic Gunadarma University izzati@staff.gunadarma.ac.id Mohammad

Potency and The Role of Credit Union in Poverty Alleviation Through Perspective Rural Economic Development Izzati Amperaningrum Faculty of Economic Gunadarma University izzati@staff.gunadarma.ac.id Mohammad

Ex Post-Evaluation Brief INDIA: Microfinance Facility

Ex Post-Evaluation Brief INDIA: Microfinance Facility Source: www.mapsofindia.com, Copyright 2010 Sector 2404000 Informal and semi-formal financial intermediaries Programme/Client Microfinance facility

Ex Post-Evaluation Brief INDIA: Microfinance Facility Source: www.mapsofindia.com, Copyright 2010 Sector 2404000 Informal and semi-formal financial intermediaries Programme/Client Microfinance facility

Financial Products to Promote Climate Change Resilience in Bolivia

Financial Products to Promote Climate Change Resilience in Bolivia Country / Region: Bolivia Project Id: PPCRBO602A Fund Name: PPCR Comment Type Commenter Name Commenter Profile Comment Date Comment 1

Financial Products to Promote Climate Change Resilience in Bolivia Country / Region: Bolivia Project Id: PPCRBO602A Fund Name: PPCR Comment Type Commenter Name Commenter Profile Comment Date Comment 1

Agenda item 12: Consideration of accreditation proposals

Page 5 (h) (j) (k) (l) (m) (n) Also requests the Appointment Committee to provide additional recommendations on the salary levels for consideration by the Board at its eleventh meeting; Decides that the

Page 5 (h) (j) (k) (l) (m) (n) Also requests the Appointment Committee to provide additional recommendations on the salary levels for consideration by the Board at its eleventh meeting; Decides that the

Reaching the poorest. Stuart Rutherford IDPM Manchester & SafeSave Bangladesh

Reaching the poorest Stuart Rutherford IDPM Manchester & SafeSave Bangladesh www.safesave.org The views expressed in this presentation are the views of the author and do not necessarily reflect the views

Reaching the poorest Stuart Rutherford IDPM Manchester & SafeSave Bangladesh www.safesave.org The views expressed in this presentation are the views of the author and do not necessarily reflect the views

Analysis of Potential Blockchain Use Cases Deloitte Consulting, September 2016

Analysis of Potential Blockchain Use Cases Deloitte Consulting, September 20 A look into KYC in a blockchain world August, 20 Investor KYC Utility Use Case Investor KYC Utility Introduction Current-state

Analysis of Potential Blockchain Use Cases Deloitte Consulting, September 20 A look into KYC in a blockchain world August, 20 Investor KYC Utility Use Case Investor KYC Utility Introduction Current-state

Pricing Micro-insurance Products

Pricing Micro-insurance Products By: Denis Garand & John J. Wipf Microinsurance (MI) has been developing rapidly since the early 1990 s in many countries and is being recognized as an important service

Pricing Micro-insurance Products By: Denis Garand & John J. Wipf Microinsurance (MI) has been developing rapidly since the early 1990 s in many countries and is being recognized as an important service

2018/SMEWG/DIA/008 National Financial Inclusion Strategy

2018/SMEWG/DIA/008 National Financial Inclusion Strategy 2016-2020 Submitted by: Centre for Excellence in Financial Inclusion Policy Dialogue on Micro, Small and Medium Enterprises Internationalization

2018/SMEWG/DIA/008 National Financial Inclusion Strategy 2016-2020 Submitted by: Centre for Excellence in Financial Inclusion Policy Dialogue on Micro, Small and Medium Enterprises Internationalization

SUPPLEMENTARY DOCUMENT 3: THE PROPOSED NATIONAL COMMUNITY-DRIVEN DEVELOPMENT PROGRAM 1

KALAHI CIDSS National Community-Driven Development Project (RRP PHI 46420) SUPPLEMENTARY DOCUMENT 3: THE PROPOSED NATIONAL COMMUNITY-DRIVEN DEVELOPMENT PROGRAM 1 A. Program Objective and Outcomes 1. The

KALAHI CIDSS National Community-Driven Development Project (RRP PHI 46420) SUPPLEMENTARY DOCUMENT 3: THE PROPOSED NATIONAL COMMUNITY-DRIVEN DEVELOPMENT PROGRAM 1 A. Program Objective and Outcomes 1. The

Title: Rabobank in developing countries Toon Bullens Number: 22

Title: Rabobank in developing countries Toon Bullens Number: 22 Rabobank was founded in the Netherlands more than a hundred years ago as a co-operative bank providing access to financial services for small

Title: Rabobank in developing countries Toon Bullens Number: 22 Rabobank was founded in the Netherlands more than a hundred years ago as a co-operative bank providing access to financial services for small

Underwriting Guidelines For Microfinance Group Loans

Underwriting Guidelines For Microfinance Group Loans Definition of Group Loans For the purpose of these underwriting guidelines, Group Loans are defined as loans that are made based on the following criteria:

Underwriting Guidelines For Microfinance Group Loans Definition of Group Loans For the purpose of these underwriting guidelines, Group Loans are defined as loans that are made based on the following criteria:

Terms of Reference (ToR) Earthquake Hazard Assessment and Mapping Specialist

Earthquake Hazard Assessment and Mapping Specialist") Terms of Reference (ToR) Earthquake Hazard Assessment and Mapping Specialist I. Introduction With the support of UNDP, the Single Project Implementation Unit (SPIU) of the Ministry of Disaster Management

Terms of Reference (ToR) Earthquake Hazard Assessment and Mapping Specialist I. Introduction With the support of UNDP, the Single Project Implementation Unit (SPIU) of the Ministry of Disaster Management

Public Disclosure Authorized. Public Disclosure Authorized. Public Disclosure Authorized. Public Disclosure Authorized

69052 Tajikistan Agriculture Sector: Policy Note 3 Demand and Supply for Rural Finance Improving Access to Rural Finance The Asian Development Bank has conservatively estimated the capital investment needs

69052 Tajikistan Agriculture Sector: Policy Note 3 Demand and Supply for Rural Finance Improving Access to Rural Finance The Asian Development Bank has conservatively estimated the capital investment needs

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE Nancy Lee General Manager MULTILATERAL INVESTMENT FUND Multilateral Investment Fund Member of the IDB Group Microfinance Trends

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE Nancy Lee General Manager MULTILATERAL INVESTMENT FUND Multilateral Investment Fund Member of the IDB Group Microfinance Trends

Microfinance Institutions Ratings

Microfinance Institutions Ratings INTRODUCTION Micro Finance Institutions (MFIs) have reversed conventional banking practice by removing the need for collateral and created a banking system based on mutual

Microfinance Institutions Ratings INTRODUCTION Micro Finance Institutions (MFIs) have reversed conventional banking practice by removing the need for collateral and created a banking system based on mutual

VANUATU NATIONAL INFRASTRUCTURE MASTERPLAN. Terms of Reference for Consultants

VANUATU NATIONAL INFRASTRUCTURE MASTERPLAN Terms of Reference for Consultants 1. BACKGROUND INFORMATION Government of Vanuatu has requested TA support in the formulation and preparation of a national infrastructure

VANUATU NATIONAL INFRASTRUCTURE MASTERPLAN Terms of Reference for Consultants 1. BACKGROUND INFORMATION Government of Vanuatu has requested TA support in the formulation and preparation of a national infrastructure

ASIAN DEVELOPMENT BANK

ASIAN DEVELOPMENT BANK TAR:INO 34147 TECHNICAL ASSISTANCE (Cofinanced by the Government of the United Kingdom) TO THE REPUBLIC OF INDONESIA FOR INTEGRATION OF POVERTY CONSIDERATIONS IN DECENTRALIZED EDUCATION

ASIAN DEVELOPMENT BANK TAR:INO 34147 TECHNICAL ASSISTANCE (Cofinanced by the Government of the United Kingdom) TO THE REPUBLIC OF INDONESIA FOR INTEGRATION OF POVERTY CONSIDERATIONS IN DECENTRALIZED EDUCATION

18th Year of Publication. A monthly publication from South Indian Bank.

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 18th Year of Publication Experience

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 18th Year of Publication Experience

Ex post evaluation India

Ex post evaluation India Sector: Financial sector (CRS Code 2404000) Project: Capitalisation programme for microcredits BMZ No.1998 66 872* Programme-/Project executing agency: Indian cooperative bank

Ex post evaluation India Sector: Financial sector (CRS Code 2404000) Project: Capitalisation programme for microcredits BMZ No.1998 66 872* Programme-/Project executing agency: Indian cooperative bank

Environment Friendly Enterprise Development Project Implementing Guidelines

SAMPLE FORMAT Page 1 of 5 I. RATIONALE Environment Friendly Enterprise Development Project Implementing Guidelines Economic condition of the coastal communities is highly affected by the illegal fishing

SAMPLE FORMAT Page 1 of 5 I. RATIONALE Environment Friendly Enterprise Development Project Implementing Guidelines Economic condition of the coastal communities is highly affected by the illegal fishing

OUR MicroLending. Changes in US & Cuba: The impact on Florida. Opening doors to your future. The Microcredit Impact October 13, 2011

OUR MicroLending Opening doors to your future Changes in US & Cuba: The impact on Florida The Microcredit Impact October 13, 2011 The Question: What People know about Microcredit? That somewhere near India

OUR MicroLending Opening doors to your future Changes in US & Cuba: The impact on Florida The Microcredit Impact October 13, 2011 The Question: What People know about Microcredit? That somewhere near India

Community Managed Revolving Fund (Sustainable mechanism of microfinance practices to disadvantaged community)

") Community Managed Revolving Fund (Sustainable mechanism of microfinance practices to disadvantaged community) A paper presented in Micro Finance Summit 2008 New departure in expanding the outreach of Micro-finance

Community Managed Revolving Fund (Sustainable mechanism of microfinance practices to disadvantaged community) A paper presented in Micro Finance Summit 2008 New departure in expanding the outreach of Micro-finance

Southern Punjab Poverty Alleviation Project (SPPAP)

") Southern Punjab Poverty Alleviation Project (SPPAP) Initial Impact of Community Revolving Funds for Agriculture Input Supply (CRFAIS) ~A Pilot Activity of SPPAP National Rural Support Programme (NRSP)

Southern Punjab Poverty Alleviation Project (SPPAP) Initial Impact of Community Revolving Funds for Agriculture Input Supply (CRFAIS) ~A Pilot Activity of SPPAP National Rural Support Programme (NRSP)

WOMEN EMPOWERMENT THROUGH SELF HELP GROUPS : A STUDY IN COIMBATORE DISTRICT

Available online at : http://euroasiapub.org/current.php?title=ijrfm, pp. 36~43 Thomson Reuters Researcher ID: L-5236-2015 WOMEN EMPOWERMENT THROUGH SELF HELP GROUPS : A STUDY IN COIMBATORE DISTRICT Dr.

Available online at : http://euroasiapub.org/current.php?title=ijrfm, pp. 36~43 Thomson Reuters Researcher ID: L-5236-2015 WOMEN EMPOWERMENT THROUGH SELF HELP GROUPS : A STUDY IN COIMBATORE DISTRICT Dr.

Recommendations on Draft Guidelines for Licensing of Small Banks in the Private Sector

Recommendations on Draft Guidelines for Licensing of Small Banks in the Private Sector Submitted to the Reserve Bank of India under Poorest States Inclusive Growth (PSIG) Programme Date: 14 th August 2014

Recommendations on Draft Guidelines for Licensing of Small Banks in the Private Sector Submitted to the Reserve Bank of India under Poorest States Inclusive Growth (PSIG) Programme Date: 14 th August 2014

A BRIEF NOTE ON THE IMPLEMENTATION OF NATIONAL RURAL EMPLOYMENT GUARANTEE SCHEME IN HIMACHAL PRADESH

A BRIEF NOTE ON THE IMPLEMENTATION OF NATIONAL RURAL EMPLOYMENT GUARANTEE SCHEME IN HIMACHAL PRADESH NATIONAL RURAL EMPLOYMENT GUARANTEE SCHEME The National Rural Employment Guarantee Act was notified

A BRIEF NOTE ON THE IMPLEMENTATION OF NATIONAL RURAL EMPLOYMENT GUARANTEE SCHEME IN HIMACHAL PRADESH NATIONAL RURAL EMPLOYMENT GUARANTEE SCHEME The National Rural Employment Guarantee Act was notified

Compulsory Group Training Tool

Compulsory Group Training Tool www.smartcampaign.org November 2012, New Delhi, India Introduction The majority of microfinance institutions (MFI) in Asia adopt a Grameen-style lending methodology. Prior

Compulsory Group Training Tool www.smartcampaign.org November 2012, New Delhi, India Introduction The majority of microfinance institutions (MFI) in Asia adopt a Grameen-style lending methodology. Prior

Disaster Management The

Disaster Management The UKRAINIAN Agricultural AGRICULTURAL Dimension WEATHER Global Facility for RISK Disaster MANAGEMENT Recovery and Reduction Seminar Series February 20, 2007 WORLD BANK COMMODITY RISK

Disaster Management The UKRAINIAN Agricultural AGRICULTURAL Dimension WEATHER Global Facility for RISK Disaster MANAGEMENT Recovery and Reduction Seminar Series February 20, 2007 WORLD BANK COMMODITY RISK

MICROFINANCE IN ACTION: A BUSINESS PROCESS ANALYSIS OF AN OPERATION IN NICARAGUA

MICROFINANCE IN ACTION: A BUSINESS PROCESS ANALYSIS OF AN OPERATION IN NICARAGUA Julio Martinez, Fairfield University,07_jmartinez3@stagweb.fairfield.edu Winston Tellis, Fairfield University, Winston@mail.fairfield.edu

MICROFINANCE IN ACTION: A BUSINESS PROCESS ANALYSIS OF AN OPERATION IN NICARAGUA Julio Martinez, Fairfield University,07_jmartinez3@stagweb.fairfield.edu Winston Tellis, Fairfield University, Winston@mail.fairfield.edu