Community and Renewable Energy Scheme Project Development Project Toolkit Project Finance Module

|

|

|

- Ellen Rogers

- 6 years ago

- Views:

Transcription

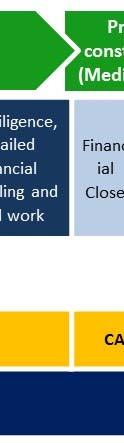

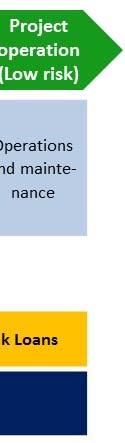

1 Community and Renewable Energy Scheme Project Development Project Toolkit Module Structure In the past, it was the case that the high costs involved with setting up loan finance for energy projects tended to favour large ( million plus) schemes, but there are now a number of different sources of finance aimed at smaller projects. However, whatever the scale, the basics of project finance will remain the same. This module is organised into the following sections 1. Overview: funding each stage of development 2. Steps to Obtaining Project Finance: i. Early stage finance ii. Assessing Financial Viability iii. Project Finance Options iv. Financial Close Obtaining Project Finance 3. The Basics of Finance 4. Further Information For each stage, different sources of finance are available. Overview: funding each stage of development The appropriate source of funding will depend on where your project is in the development process. CARES Sources of Finance module can provide guidance on the appropriate source of funding. Figure 1 shows the development risk and sources of funding that are available at each stage of the project development cycle. Sources are split into grants, debt and equity. This includes where CARES grants, loans and REIF funding may be applicable. Information on these is available in the Further Information Section. Developed by Ricardo AEA Version 5 1

2 Figure 1 Risks and financing options at each stage of the project development cycle Developed by Ricardo AEA Version 5 2

3 The main kinds of funding by project stage are: I. Project Development Grant funding: for example, CARES Start up grant Debt funding: for example CARES Pre planning loan Equity provided by project owners II. Project Construction Debt: CARES Renewable Energy Investment Fund (REIF) or Bank Loans Equity provided by project owners: for example through a community share offer III. Project Operation Revenue from the project should be sufficient to cover operating costs and loan repayments. Early stage finance This section presents the steps to follow during the preliminary stages, helping community groups to select and access the appropriate finance method. Step 1 Selecting an appropriate financing method Once your group has Developed the Vision for their community energy project (See step 1 of the technology specific CARES Toolkit Technology Modules), they should consider the best way of financing the project. Figure 1 on the next page provides a useful guide for new community groups or community businesses on the best finance arrangements for their project. This includes set up options, and whether debt or equity should be used. The CARES Establishing a Community Group module outlines the available sources of finance available to different types of community groups. Step 2 Consider applying for CARES community grants CARES provides start up grant funding to help towards the costs of feasibility studies, community consultation and other preparatory costs. Up to 10,000 is available for community groups to fund non capital aspects of a project. These should be early stage activities, without which the installations would not be able to go ahead. Before applying for CARES funding, it is recommended that you review your ideas with the CARES team and also look to other sources of funding for early stage community capacity building activity. Information on applying to CARES and progressing community projects see Further Information. Developed by Ricardo AEA Version 5 3

Developed by Ricardo AEA Version 5")

4 Figure 2: Potential funding arrangements for your project (Source: based on a diagram developed by The Carbon Trust) Developed by Ricardo AEA Version 5 4

5 Assessing Financial Viability The action and tools for assessing the community project s financial viability are presented here. Step 3 Using the CARES Project Finance Model The CARES Toolkit contains a financial model that is based on inflation adjusted cash flows, profit and loss (with depreciation), and provides balance sheets for the life of the project. The CARES Project Finance model is easy to use and incorporates all the elements that a lender will expect to see: Project schedules, income and operating costs; Pre planning costs and construction costs at the appropriate periods of the project; Cash flow and balance sheet calculations; and Project IRR, Equity IRR, Project NPV, Debt Service Cover Ratio and more. Any lender will want to see a completed finance model for the project from development through construction to operations. It is important to begin populating and using this model at an early stage. However, it must be recognised that finance providers will have their own approach to project appraisal, so this generic model should be used for indicative purposes only. By populating the financial model with all the costs associated with project development, construction, operation and maintenance, you will have collected a lot of the information that a bank will require to see before considering the offer of a loan. Coupled with the CARES Investment Ready Tool, you will be in a strong position when entering discussions with lenders. Step 4 Measuring the project s financial performance There are a number of ways in which the financial performance of a project can be measured. Different finance providers may prefer different measures. Simple payback Net present value (NPV) Internal Rate of return (IRRs) Both IRR and NPV can be calculated for your project using the CARES Project Finance Model. As a minimum you would want to know the indicative equity IRR of your project in your first financial viability assessment. For further information see The Basics of Finance section below. Financial covenants To provide the security required by the finance provider a number of financial covenants must be provided. Debt service cover ratio (DSCR). Debt service reserve account (DSRA). Loan life cover ratio (LLCR). Maintenance reserve account. The CARES Project Finance Model calculates DSCR and DSRA, for further information see The Basics of Finance section. Developed by Ricardo AEA Version 5 5

6 CARES Project Finance Model The CARES Project Finance Model allows for more than 30 different inputs. The following table outlines the minimum inputs that are required to be entered to evaluate the potential financial performance. Model Input Description Input data 2 Development Phase Start Date The model assumes the development phase starts on the last day of a month to avoid interest costs in that month. Enter the date in the MM/YYYY format and the actual end month date is automatically calculated 3 Financial Close Date The model assumes Financial Close (i.e. the date the project documents all get signed and banks offer loans on the main project) occurs on the last day of a month to avoid interest costs in that month. Enter the date in the MM/YYYY format and the actual end month date is automatically calculated. 4 Construction End Date 6 Rated power of renewable energy device (kw) 7 Maximum electricity generated assuming no downtime (kwh per year) 11 Support tariff (p/kwh) at date of operations commencement The date that the construction of the project ends and all commissioning is completed which assumed to occur at the end of a month. Enter the date in the MM/YYYY format and the actual end month date is automatically calculated. The next day, operations starts. The capacity of the renewable energy device in kw Total energy generated assuming no downtime (maintenance and repairs). This value will be found in the Technical Advisers report, e.g. the P50 value. Support tariff (e.g. FiT rate (p/kwh) at the date of operations commencement. PLEASE NOTE: if the project is expected to be commissioned and start generating support revenues in one year's time then the support price (p/kwh) needs to be estimated to account for inflationary increases in support prices. Account also needs to be taken for any FiT degression for projects supported by FiTs. 16 Development Costs The development costs need to be inserted into the light green cells in worksheet 'Development Costs', splitting between costs that will be financed with a combination of a CARES loan and equity (in the proportion of cell [23]), other junior loans (e.g. Renewable Energy Infrastructure Fund (REIF) loans) and equity (in the proportion of cell [23]), and any development phase grants. Some explanations (column B) have been put in, but the user is free to amend the headings as they see fit. The user should enter the expected monthly costs for each sub component in the number cells. PLEASE NOTE: this worksheet automatically updates dates from development phase start to the date of financial close. Please ensure that no numbers appear outside the green box. This will mean that if the date of the Development Phase start [2] or Financial Close [3] changes in a scenario this worksheet will need to be updated 18 Construction Costs The construction costs need to be inserted into the light green cells in worksheet 'Construction phase'. Some explanations (column B) have been put in, but the User is free to amend the headings as they see fit. The User should enter the expected monthly costs for each sub component in the number cells. PLEASE NOTE: this Developed by Ricardo AEA Version 5 6

7 worksheet automatically updates dates from financial close to the end of the construction phase. Please ensure that no numbers appear outside the green box. This will mean that if the date of Financial Close [3] changes in a scenario this worksheet will need to be updated 20 Operating Costs Constant annual operating costs that only rise by inflation should be inserted. The User is free to adjust the headings. It may be the case that the landowner receives a fixed rental on the site, in which case the rental should be included here. However, it is also possible the landowner may receive a land rental related to the electricity sold (plus the support tariffs and LECs), in which case the percentage can be included in [21]. PLEASE NOTE: this worksheet automatically updates dates from financial close to the end of the construction phase. Please ensure that no numbers appear outside the green box Developed by Ricardo AEA Version 5 7

8 Step 5 Applying for CARES pre-planning loan If the initial feasibility study determines there is a potential financially viable project and no show stoppers were identified, a group may wish to consider applying for a pre planning loan. The preplanning loan provides support to community applicants taking forward plans for renewable energy generation schemes on land they own or could lease from a land owner. You can access an Expression of Interest Form and a CARES local development officers will support you throughout (see Further Information). Applications are competitive and will be taken until funds are fully allocated. This loan will cover up to 95% of pre planning costs such as EIAs and technical feasibility studies. The maximum loan per entity is 150,000. Applicants must contribute a minimum of 5% (equity finance). Step 6 Securing equity finance As a condition for most debt finance, project owners must be prepared to contribute as much as 30% of the total project finance. Finance provided by project owners is known as equity. Potential sources of equity finance include: Stakeholders, in return for some kind of share of the benefits from the operating project this can take the form of money or the donation of effort as part of the development process (socalled sweat equity ); Private sector sources ( venture capital providers) usually in return for a large stake in the operating project; Local share offers supported by organisations such as Energy4All, Community Shares Scotland, Microgenius. While it may only require sweat equity to take a project to the point where it is demonstrated to be potentially viable, money will be required from that point on. Project Finance Options Project financing will cover the construction and part of the operational phase of your project. Step 7 Choosing a source of debt funding There are several difference types of Loan to choose from, detailed below. Visit the Local Energy Scotland website for further information on the grants and loans available from CARES. Renewable Energy Investment Fund (REIF) loans Community renewable energy projects that have successfully gained planning permission can apply for support from the Renewable Energy Investment Fund (REIF). REIF is delivered by the Scottish Investment Bank, on behalf of the Scottish Government, and is designed to build on the early stage support provided through the CARES scheme. Developed by Ricardo AEA Version 5 8

9 REIF offers a flexible lending service that can be tailored to individual community projects that have advanced to the delivery stage, but still have challenging funding gaps. REIF loans can be used to bridge funding gaps prior to financial close (e.g. for turbine deposits or grid connection deposits). The majority of the investment opportunities are expected to arise from community led renewables projects, but REIF can also consider larger and more bespoke deals involving the funding of community investments into projects led by private developers or utilities. Further details on the eligibility criteria for REIF funding can be accessed from the Scottish Enterprise website. CARES can guide communities through the REIF application procedures, providing advice and support for you to develop your project to a stage that is application ready. For more information about CARES loans, please contact your local CARES development officer Further examples of sources of funding can be seen in the Further Information Section. Fund and Bank loans In addition, funds and banks loan money directly to developers of renewable energy projects. Some, such as Triodos, have specialist renewable energy funds. Barclays and Close Brothers supports Cleantech investments. Other high street banks such as The Royal Bank of Scotland and Santander have also provided finance to viable renewable energy projects. In general, the value of the loan sought will dictate if your application will be dealt with at branch level or by specialist teams in the bank. It is worth noting however that these types of commercial lenders are often looking to fund projects with over 1million in capital costs, and the cost of the due diligence process is usually high. It is likely that your group will have had to negotiate banking facilities to operate. In this case, your banking services provider may be worth talking to about providing a loan for the project as well. Before approaching any lender, it is important to ensure that you have collected all the information that a bank will require, enabling them to make an informed decision regarding the level of risk associated with your project. A high level checklist of these requirements is outlined in the Cares Investment Ready Tool. A CARES development officer will be able to work with you to outline how to collect this information. Other Sources of debt funding Other sources of funding specific to community schemes include, but are not limited to: Abundance Generation Big Issue Invest The Charity Bank The Co operative Bank The Community Generation Fund Social Investment Buisness Social Investment Scotland Developed by Ricardo AEA Version 5 9

10 Trillion Fund In addition, there are a growing number of examples where the communities themselves fund projects by selling shares in the scheme. The CARES Sources of Finance document has more information on these and additional sources of funding. Financial Close There are a number of potential sources of funding for community based energy schemes in Scotland. CARES has specifically tailored schemes designed to support the high risk stages of project development to get a project to the point where it can be financed. These milestones are required for securing finance: Grid connection; Required options and leases Planning consent; and Turbine deposits. Without all four in place, the project does not have a significant market value. However, once these are in place, the project will be in a position to begin discussions with major lenders with a view of securing indicative offers, identifying any funding gaps and obtaining a payment. Step 8 CARES Investment Ready Tool For a lender to consider providing finance for a project, there are a significant number of factors they will consider over and above whether or not the project is profitable. Each of these factors has a risk associated with it and the overall level of risk associated with a project, in addition to whether or not a project is profitable, will influence whether they will consider financing a project. The CARES Investment Ready Tool has been developed to capture the majority of information that lenders will want to see when making their investment decision. Before releasing any funds, the lender will expect the CARES Investment Ready Tool, or something similar, to be completed. If it has not been completed, the lender will expect to see a clear action plan to completing the tool. Step 9 Preparing for Lender Due diligence Any finance provider will want to scrutinise every aspect of your project and your organisation to confirm the things that you are telling them and to identify areas of risk. These may be things that you had not even considered. They will complete this assessment at your expense. The CARES Investment Ready Tool has been developed to assist you in collating all the information that will be required by a lender when completing its due diligence. Having this information quickly and easily to hand simplifies the process, will potentially reduce any delays and costs, and will show to the lender that the project is being well managed. Listed below are some of the key studies, contracts and documents that you would normally want to have in place to assist the due diligence process. Developed by Ricardo AEA Version 5 10

11 Financial due diligence A professionally indemnified assessment of proposed capital and operating costs and associated project lifecycle cash flows, debt service cover ratio analysis and sensitivity analysis on the main financial variables (e.g. capital cost, operating costs, revenue rates and any variable interest rates). Completing the CARES Project Finance Model is a good starting point for this. The CARES Toolkit Project Finance Model is an indicative early stage financial model to help communities understand the potential profitability of renewable projects, before deciding whether it is worth undertaking further technical and financial due diligence to develop the idea further. Disclaimer The model is copyright of the Scottish Government and all rights are reserved. The model has been developed as part of the Scottish Government s CARES programme which is delivered by Local Energy Scotland. The model has been prepared for Local Energy Scotland by its consultant Ricardo AEA and is an indicative early stage financial model to help community groups understand the potential profitability of community renewable investments. Any information and results derived from the use of the model are subject to the accuracy of data inputs supplied by the User. All results should be checked and challenged before any reliance, publication or use. This model has not been subject to any external independent audit. The Scottish Government, Local Energy Scotland and Ricardo AEA hold no liability for any subsequent adjustment or amendments made to the model or any loss or damage arising from any reliance on or use of the information generated by this model by any community group, lender, investor or other interested parties. Financial due diligence also requires a comprehensive understanding of the assumptions underlying the project to support the performance of a sensitivity analysis to define an agreed financial base case. This includes quantification of a range of project specific uncertainties and exceedance probabilities. Where this process shows that the annual energy yield prediction has a 50% probability of reaching a higher or lower annual energy production than predicted, it is called P50. In a similar way, a result of P75 from this process indicates that the probability of the annual energy production being reached is 75%. The risk that the annual energy production of P90 is not reached is 10%. These then become measures of the required energy output not being met. P50 and P90 values over a 10 year period are commonly used by financiers. Technical due diligence These are technology specific activities that relate to key technical areas of risk. Examples are shown below: Resource assessments with a clear indication of the forecast resource and resulting annual energy yield over the life of the project Geotechnical reports for any foundations (e.g. for wind turbines), hard standings for biomass fuel storage, and other construction and access improvement works Design plans that are compliant with the Construction Design and Management Regulations 2007 and site specific method statements for the construction of all generator and associated infrastructure installations, any new and altered road, and amenity and sea access works necessary to commission the installation Transport route assessment report and sign off from the relevant competent authorities for any use of public highways and marine facilities, etc., and additional marine transport method statements for any proposed novel/non standard marine transport proposals Legal due diligence Developed by Ricardo AEA Version 5 11

12 These are technology specific activities that relate to key legal areas of risk. Examples are shown below: Evidence of unfettered title to land and/or to conduct all necessary activities on the land Evidence of unfettered access to all necessary lands and resources, including lay down and oversail rights, and a resource protection assurance for wind, hydroelectric and solar resources Evidence of adequate legally binding contractual commitments with suppliers, contractors and sub contractors in place, and suitable provisions and bonds secured to guarantee performance and/or mitigate default against contractual terms Evidence that full insurance cover is in place to cover all delays and project failure risks not covered elsewhere by performance bonds and professional indemnity covers in place This makes it important for you to be as rigorous as possible during the development of your project, and to identify and deal with all areas of uncertainty or risk. A record of each of the studies and contracts should be included in your CARES Investment Ready Tool with a summary of each for reference. You must also be clear on cash flows during and after the development and construction of the project, and ensure that you have enough cash available to complete the project. For instance, as a newly established legal entity, suppliers or contractors may require a down payment and, as the developer, you will also need to provide construction insurance. This may require you to borrow more money. The CARES Project Finance Model allows you to schedule all your payments and provides you with a detailed cash flow during project development, construction and operation. It enables you to determine the impact of shifting a payment from one month to the next and how this will affect interest payments on loans. It is standard practice in project financing to negotiate changes in payment schedules for deposits to optimise the cash flow balance of the project. A financially viable project with a grid connection, a lease and planning consent has value. At this stage you are in a position to approach lenders for funding, which covers the construction and operational stages of the project. Step 10 Making debt and equity repayments When the project is operational, revenues will be earned through the sale of electricity. This is the main source of funding at this stage. Revenues will cover the operational costs of the project. They will also serve to repay the debt financers, through project loans and interest payments. In addition, equity financers will also be repaid, through dividend payments for shareholders. Developed by Ricardo AEA Version 5 12

13 The Basics of Finance This section reviews basic and key concepts in project finance. Further definitions can also be found in the CARES Toolkit Finance Glossary. Equity Typically projects are funded by a mixture of debt and equity. Equity finance is funding that comes from project owners. Debt finance is funding that comes from third parties, for example a bank. Until a project has secured a site and all consents, it is not debt financeable because there is nothing of substance to finance. Therefore, equity finance is used to cover the costs involved in taking a project from concept to the point where it becomes potentially able to draw down debt finance against the demonstrated value of the project. As there is no guarantee that a project will progress from concept to operation, equity finance is always provided at risk of gaining no return. Debt A lender will need the following before making any money available for a project: Due diligence assessments of risk; The payment of fees to arrange any loan (usually); Security they want to be the last to lose their money if a project fails; and Financial covenants (linked to the above). Types of loan Loans can be differentiated by seniority. If a project has more than one loan, the loan seniority determines the order in which these loans are repaid, after operating costs and taxes have been paid. 1. Senior Loans are the first to be repaid. Loans offered by banks are commonly called senior loans. 2. Junior loans are second to be repaid i.e. in each period they are only repaid if the operating costs, taxes and senior loan providers have been paid. Junior loans can also been known as subordinated debt or sometimes mezzanine finance. If there are three levels of loans, then a common terminology is senior loans, junior loans and then subordinated debt as the third most risky level. In addition to seniority, loans can further be differentiated by two recourse types. Project finance or non-recourse finance This loan is secured on the asset of the project alone. In this case, the project debt and equity used to finance the project are paid back from the income generated by the project. This requires far higher levels of due diligence to be undertaken and stricter financial controls to be applied. The lenders need to have complete confidence that the project is viable and the income generated by the project will be sufficient to finance the loan provided. Equity is also invested at the Developed by Ricardo AEA Version 5 13

14 point of construction, with the potential that grants can form part of the equity invested by a community. The greater the amount of equity in a project, the less finance that is required. Secured finance or recourse finance This loan requires some other form of asset to secure the loan, usually in the form of property. As a result, more legal documentation is required and property valuations must be undertaken. It is important to note that some form of equity is also likely to be required, even in a project finance scenario. This is because funders want to be sure that the project developers have a good incentive to make the project a success. Terms of loan This will include: Loan length. Depending on the lending institution, they may offer a variety of loan structures and lengths. They may have breakpoints built in where refinancing could be appropriate Fees. The loan provider will likely charge a fee which can be around 0.5% of the loan. On top of this will be legal fees and the cost of undertaking the due diligence exercise Interest rate. The rate of interest is built up from the interest rate banks can lend between themselves (called the London Interbank Offered Rate (LIBOR)) and a margin to cover the risk inherent in a project. For senior loans banks commonly lend at about 6% or 7%, but the rate varies depending on the length of the loan, the technology, riskiness of the project and other factors. Project Financial performance measures This section details methods for calculating the financial performance of your project. Simple payback As the name implies, this simply compares the total cost of project development with the income after all operating costs, to calculate the point at which the income pays back the development cost. A payback can be calculated for all finance provided or a payback just on the equity invested. While this gives a good rule of thumb as to viability, it is almost never used by finance providers. On the other hand, community business or community groups that are self financing a project can use this approach as one of a number of metrics to decide if they want to invest their own money into a project. Net present value Net present value (NPV) compares the value of a pound today to the value of that same pound in the future, taking inflation and returns into account. This future return required (%) is typically expressed as a discount rate. NPVs are commonly calculated for a project as a whole. This means the period on period cash flows of the initial investment and then the subsequent cash flow available for finance (revenues, less operating costs and taxation) are discounted by a single discount rate. If the NPV of a prospective project is positive then it makes more that the target return. If a project is financed 100% by equity then the discount rate would be the target return equity investors require. Developed by Ricardo AEA Version 5 14

15 If a project is financed with a blend of debt and equity then the discount rate is the weighted average cost of capital. The NPV can be calculated for your project using the CARES Project Finance Model. Since NPV takes into consideration the future value of money, financiers sometimes use it as a measure of project attractiveness. Examples of how NPVs are calculated can be found at: present value explained in simple words/ Internal rate of return The internal rate of return (IRR) is the discount rate that makes the NPV of all cash flows from a particular project equal to zero. This is another measure of project desirability as, generally speaking, the higher a project's IRR, the more profitable it will be. The IRR can be calculated for your project using the CARES Project Finance Model. Two main types of IRR are commonly calculated for a project. These are the: Project IRR this is simply the discount rate that makes the NPV of the period on period cash flows of the initial investment and then the subsequent cash flow available for finance (revenues, less operating costs and taxation) equal to zero. So if a project s IRR is calculated at 12%, but the weighted average cost of finance (the blended return required by debt and equity providers) is 8% the project can be viewed as profitable Equity IRR this is the discount rate that makes the NPV of the initial equity injection and then all the subsequent dividend repayments and repayment of equity equal to zero. So if equity investors have a target return of 12% and the equity IRR is 15% the project could be viewed by equity investors as attractive. Because the IRR is a rate quantity, it is an indicator of the yield from an investment. This is in contrast with the NPV, which is an indicator of the value or magnitude of an investment.. This can be calculated for your project using the CARES Project Finance Model. As a minimum you would calculate the project IRR in your first financial viability assessment. Examples of how the IRR is calculated can be found at: budgeting/irr rate return.html Financial covenants To provide the security required by the finance provider, it is usual that a number of financial covenants must be provided. Developed by Ricardo AEA Version 5 15

16 Debt to equity ratio. Also known as loan: value ratio. Usually, senior debt providers will provide only 70% (or 75%) of the debt and require the remainder to come from equity or from junior loans/ subordinated debt/ mezzanine finance. Debt service cover ratio. The debt service cover ratio (DSCR) can also be known as debt cover ratio (DCR) is the ratio of cash available for debt service divided by the interest and principal repayments in that period. Typically, most commercial banks require the ratio of between 1.15 and The CARES Project Finance Model can be used to calculate the DSCR for your project Loan life cover ratio. This is the ratio of operating cash flow to debt payments over the entire term of the loan. Usually, a ratio of 1.50 is required to ensure that the project is profitable and the loan covered Debt service reserve account. Banks are likely to require that enough cash is held in reserve to cover debt payments for items over and above loan repayments. In the case of project finance, at least six months cover may be required, but less for secured finance loans Maintenance service reserve. For assets that require periodic refurbishments, or upgrades (e.g. solar panels require the inverters to be replaced after 7 years or so) banks often require a reserve account to be built up in the 12 or 18 months running up to the replacement to ensure there is sufficient cash flow to pay for the maintenance. Refinancing. Once a project has been financed through the construction and early phases of operation, some finance providers provide an option to refinance the project at this stage Developed by Ricardo AEA Version 5 16

17 Further Information Module Structure CARES Finance Glossary: CARES Community Investor Module: Overview: funding each stage of development CARES Sources of Finance Module: Early stage finance Step 1 - Selecting an appropriate financing method CARES Toolkit Technology Modules: resources/resources advice/cares toolkit/technology/ Cares Toolkit Establishing a Community Group Module resources/resources advice/cares toolkit/projectdevelopment/establishing a community group/ Step 2- Consider applying for CARES community grants Applying for CARES funding advice/applying to cares/ For further information about progressing community projects your own electricity/ Assessing Financial Viability Step 3- Using the CARES Project Finance Model CARES Project Finance model Step 4 - Measuring the project s financial Refer to CARES Project Finance model above. Step 5- Applying for CARES pre-planning loan Expression of Interest Form and contact CARES local development officers us/regional contacts/ Developed by Ricardo AEA Version 5 17

18 Step 6- Securing equity finance Energy4All, Community Shares Scotland, Microgenius., Project Finance Step 7- Choosing Local Energy Scotland website advice/applying to cares/ Renewable Energy Investment Fund (REIF) loans Scottish Enterprise website enterprise.com/services/attract investment/renewable energy investmentfund/overview Funding and Fund and Bank loans Triodos, Renewable Energy Funds Barclays Cleantech Investments mediatelecoms/cleantech.html?gclid=co3o1qndibocfu_htaodckuavw Close Brothers Royal Bank of Scotland society/energyfinancing.html Santander ity/santander and sustainability/financing renewable energy projects.html Other Sources of debt funding CARES Sources of Finance. Abundance Generation Big Issue Invest The Charity Bank: The Co operative Bank operativebank.co.uk/corporate The Community Generation Fund impactfunding/community generation fund Social Investment Business Social Investment Scotland (SIS) Trillion Fund Developed by Ricardo AEA Version 5 18

19 Financial Close Step 8- CARES Investment Ready Tool CARES Investment Ready Tool Step 9- Preparing for Lender Due diligence Refer to CARES Project Finance model and CARES Investment Ready Tool above. Commissioned by the Scottish Government and Energy Saving Trust. Produced by Ricardo AEA Ltd Queen s Printer for Scotland 2009, 2010, 2011, 2012 This document was last updated April 2015 Developed by Ricardo AEA Version 5 19

Community and Renewable Energy Scheme Project Development Toolkit

Community and Renewable Energy Scheme Project Development Toolkit Shared Ownership Module This module has been developed for Local Energy Scotland to provide support to community groups looking to invest

Community and Renewable Energy Scheme Project Development Toolkit Shared Ownership Module This module has been developed for Local Energy Scotland to provide support to community groups looking to invest

Ventus 2 VCT plc. Strategy Note Executive Summary

1 Executive Summary This note summarises the outcome of a strategy review undertaken by the Board of Ventus 2 VCT plc (the Company ) over the past year during the period when the last of the Company s

1 Executive Summary This note summarises the outcome of a strategy review undertaken by the Board of Ventus 2 VCT plc (the Company ) over the past year during the period when the last of the Company s

ACCA. Paper F9. Financial Management June Revision Mock Answers

ACCA Paper F9 Financial Management June 2013 Revision Mock Answers To gain maximum benefit, do not refer to these answers until you have completed the revision mock questions and submitted them for marking.

ACCA Paper F9 Financial Management June 2013 Revision Mock Answers To gain maximum benefit, do not refer to these answers until you have completed the revision mock questions and submitted them for marking.

Introduction to the Toolkit Financial Models

World Bank & Brazilian Ministry of Transport Workshop on the Toolkit for PPP in Roads and Highways Introduction to the Toolkit Financial Models Cesar Queiroz World Bank Brasilia, Brazil, June 8-9, 2010

World Bank & Brazilian Ministry of Transport Workshop on the Toolkit for PPP in Roads and Highways Introduction to the Toolkit Financial Models Cesar Queiroz World Bank Brasilia, Brazil, June 8-9, 2010

Growth Finance Expertise. Mergers & Acquisitions. Business Banking

Growth Finance Expertise Mergers & Acquisitions 1 Introduction Irish businesses, such as Version 1 in technology and Glanbia in agrifoods, have shown that a well-executed Mergers and Acquisitions (M&A)

Growth Finance Expertise Mergers & Acquisitions 1 Introduction Irish businesses, such as Version 1 in technology and Glanbia in agrifoods, have shown that a well-executed Mergers and Acquisitions (M&A)

UK Solar Investment. 8% return per annum. Defined exit strategy at the end of year 3 with option to extend. Pension Compatible.

UK Solar Investment 8% return per annum. Defined exit strategy at the end of year 3 with option to extend. Pension Compatible. Sovereign backed income. All investments presently generating projected real

UK Solar Investment 8% return per annum. Defined exit strategy at the end of year 3 with option to extend. Pension Compatible. Sovereign backed income. All investments presently generating projected real

Financing Terms. Guide to using Term Sheets Social Investment Toolkit Module 7. Version 1.0

Financing Terms Guide to using Term Sheets Social Investment Toolkit Module 7 Version 1.0 Content Overview 3 What is a Term Sheet? 4 How do you prepare a Term Sheet? 5 What is the format of a Term Sheet?

Financing Terms Guide to using Term Sheets Social Investment Toolkit Module 7 Version 1.0 Content Overview 3 What is a Term Sheet? 4 How do you prepare a Term Sheet? 5 What is the format of a Term Sheet?

Behind the Meter Solar PV Funding Guidebook

Behind the Meter Solar PV Funding Guidebook DISCLAIMER Subject to the below, the copyright in this Guidebook belongs to Frontier Impact Group and this document must not be copied or reproduced in any other

Behind the Meter Solar PV Funding Guidebook DISCLAIMER Subject to the below, the copyright in this Guidebook belongs to Frontier Impact Group and this document must not be copied or reproduced in any other

Project Finance Modelling

Project Finance Modelling A 3 Day Programme This course is presented in London on: 28 February 2 March 2018, 10-12 September 2018 The Banking and Corporate Finance Training Specialist Course Objectives

Project Finance Modelling A 3 Day Programme This course is presented in London on: 28 February 2 March 2018, 10-12 September 2018 The Banking and Corporate Finance Training Specialist Course Objectives

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

INFORMATION FOR MORTGAGE CUSTOMERS.

INFORMATION FOR MORTGAGE CUSTOMERS. WELCOME TO YOUR GUIDE TO HALIFAX MORTGAGES. Fold back this page for a brief summary of key mortgage features. YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP

INFORMATION FOR MORTGAGE CUSTOMERS. WELCOME TO YOUR GUIDE TO HALIFAX MORTGAGES. Fold back this page for a brief summary of key mortgage features. YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP

SCOTTISH FUNDING COUNCIL CAPITAL PROJECTS DECISION POINT PROCESS

SCOTTISH FUNDING COUNCIL CAPITAL PROJECTS DECISION POINT PROCESS Incorporating amendments by Scottish Futures Trust (Proposals for Decision Points 2 5 Only) Executive summary... 1 Section 1: Introduction

SCOTTISH FUNDING COUNCIL CAPITAL PROJECTS DECISION POINT PROCESS Incorporating amendments by Scottish Futures Trust (Proposals for Decision Points 2 5 Only) Executive summary... 1 Section 1: Introduction

Research. Bridging the Gap: Mezzanine Financing PREI. Executive Summary

PREI Bridging the Gap: Mezzanine Financing March 2009 Research Peter Hayes, PhD Director of Research, Europe London Office Tel +44 (0) 20 7766 2435 Fax +44 (0) 20 7766 2449 peter.hayes@pramericarei.com

PREI Bridging the Gap: Mezzanine Financing March 2009 Research Peter Hayes, PhD Director of Research, Europe London Office Tel +44 (0) 20 7766 2435 Fax +44 (0) 20 7766 2449 peter.hayes@pramericarei.com

The Economics and Financing of Distributed Generation Investment. Budapest, Hungary November 17, 2016

The Economics and Financing of Distributed Generation Investment Budapest, Hungary November 17, 2016 Topics to Cover How to Finance Distributed Generation Investments 1 Importance of financial aspects

The Economics and Financing of Distributed Generation Investment Budapest, Hungary November 17, 2016 Topics to Cover How to Finance Distributed Generation Investments 1 Importance of financial aspects

Aripaev conference. Crowd Funding/ Energy Coop s. KPMG Baltics SIA Energy and Utilities Advisory services. November 2013

Aripaev conference Crowd Funding/ Energy Coop s KPMG Baltics SIA Energy and Utilities Advisory services November 2013 Finland specific Energy coop examples Kontiolahti, Lehmo Area, Vaskela Area Wood chip

Aripaev conference Crowd Funding/ Energy Coop s KPMG Baltics SIA Energy and Utilities Advisory services November 2013 Finland specific Energy coop examples Kontiolahti, Lehmo Area, Vaskela Area Wood chip

ScotWind leasing - new offshore wind leasing for Scotland

November 2018 ScotWind leasing - new offshore wind leasing for Scotland Summary of Discussion Document responses and update on leasing design In May 2018 we published a Discussion Document setting out

November 2018 ScotWind leasing - new offshore wind leasing for Scotland Summary of Discussion Document responses and update on leasing design In May 2018 we published a Discussion Document setting out

Sustainable Energy Handbook

Sustainable Energy Handbook Module 6.1 Simplified Financial Models Published in February 2016 1 Introduction to simplified financial models The simplified financial model is a tool that enables to understand

Sustainable Energy Handbook Module 6.1 Simplified Financial Models Published in February 2016 1 Introduction to simplified financial models The simplified financial model is a tool that enables to understand

Certified Expert in Climate & Renewable Energy Finance. Module 7: Renewable Energy Finance and the Role of Project Finance

Certified Expert in Climate & Renewable Energy Finance Module 7: Renewable Energy Finance and the Role of Project Finance 2014 Frankfurt School of Finance & Management The content of this LinkEd e-learning

Certified Expert in Climate & Renewable Energy Finance Module 7: Renewable Energy Finance and the Role of Project Finance 2014 Frankfurt School of Finance & Management The content of this LinkEd e-learning

Information for mortgage customers. Mortgages

Information for mortgage customers. Mortgages Hello. This is your guide to TSB mortgages. This guide provides lots of information about our mortgages. Some of it is relevant to everyone but some of it

Information for mortgage customers. Mortgages Hello. This is your guide to TSB mortgages. This guide provides lots of information about our mortgages. Some of it is relevant to everyone but some of it

Financing the renewable energy supply chain. Steve Lewis Ernst & Young Orenda Corporate Finance Inc 4 May 2011

Financing the renewable energy supply chain Steve Lewis Ernst & Young Orenda Corporate Finance Inc 4 May 2011 Agenda Section 1 Section 2 Section 3 Section 4 Section 5 Appendix 1 Introduction to the team

Financing the renewable energy supply chain Steve Lewis Ernst & Young Orenda Corporate Finance Inc 4 May 2011 Agenda Section 1 Section 2 Section 3 Section 4 Section 5 Appendix 1 Introduction to the team

The Complete Guide to Bridging Loans

Bridging Loans Hotline Call 0117 313 6058 The Complete Guide to Bridging Loans Need to move fast? Mortgage chain issues? Buying an auction property? Seeking development finance? READ HERE Contact Us Tel:

Bridging Loans Hotline Call 0117 313 6058 The Complete Guide to Bridging Loans Need to move fast? Mortgage chain issues? Buying an auction property? Seeking development finance? READ HERE Contact Us Tel:

Business Protection. Adviser guide. Why a business needs protecting 3. Key person protection 5. Business loan protection 9. Shareholder protection 11

Business Protection Adviser guide Click the orange buttons below to jump to page Why a business needs protecting 3 Key person protection 5 Business loan protection 9 Shareholder protection 11 Partnership

Business Protection Adviser guide Click the orange buttons below to jump to page Why a business needs protecting 3 Key person protection 5 Business loan protection 9 Shareholder protection 11 Partnership

Mr. D.K.Goswami Choice International Limited 12 November 2011

Long-term financing of Projects Debt Mr. D.K.Goswami Choice International Limited 12 November 2011 1 Flow of Presentation Meaning of the word Project and its types Cost of Project Setting-up of a Project

Long-term financing of Projects Debt Mr. D.K.Goswami Choice International Limited 12 November 2011 1 Flow of Presentation Meaning of the word Project and its types Cost of Project Setting-up of a Project

Fact Sheets for Selected Financial Schemes

Fact Sheets for Selected Schemes United Kingdom PV Financing Project Deliverable 3.2 This project has received funding from the European Union s Horizon 2020 research and innovation programme under grant

Fact Sheets for Selected Schemes United Kingdom PV Financing Project Deliverable 3.2 This project has received funding from the European Union s Horizon 2020 research and innovation programme under grant

ARTICLE ON PROJECT FINANCING

ARTICLE ON PROJECT FINANCING 1. INTRODUCTION Project financing means arranging funds for implementing a new project or undertaking expansion, diversification, modernization or rehabilitation of existing

ARTICLE ON PROJECT FINANCING 1. INTRODUCTION Project financing means arranging funds for implementing a new project or undertaking expansion, diversification, modernization or rehabilitation of existing

A review of DECC s Impact Assessment of Feed-in-Tariff rates for small-scale renewables

A review of DECC s Impact Assessment of Feed-in-Tariff rates for small-scale renewables A report for the British Photovoltaic Association 22 October 2015 Cambridge Econometrics Covent Garden Cambridge

A review of DECC s Impact Assessment of Feed-in-Tariff rates for small-scale renewables A report for the British Photovoltaic Association 22 October 2015 Cambridge Econometrics Covent Garden Cambridge

Financial Modelling for Project Finance

Financial Modelling for Project Finance Financial Modelling for Project Finance Penelope Lynch Euromoney Books Contents 1 Introduction 1.1. The need for the model 1.2. Purpose and uses of the model 1.2.1

Financial Modelling for Project Finance Financial Modelling for Project Finance Penelope Lynch Euromoney Books Contents 1 Introduction 1.1. The need for the model 1.2. Purpose and uses of the model 1.2.1

Guidelines for Implementing Total Management Planning. Financial Management. USER MANUAL Advanced Financial Model

Guidelines for Implementing Total Management Planning Financial Management USER MANUAL Advanced Financial Model 2 Financial Management: User Manual, Advanced Financial Model TABLE OF CONTENTS Page No.

Guidelines for Implementing Total Management Planning Financial Management USER MANUAL Advanced Financial Model 2 Financial Management: User Manual, Advanced Financial Model TABLE OF CONTENTS Page No.

Guide to the house buying process

Guide to the house buying process www.caesar howie.co.uk For more information or to speak to one of our trained advisers please telephone our Senior Issues team on 0800 005 1755. The Caesar& Howie Group

Guide to the house buying process www.caesar howie.co.uk For more information or to speak to one of our trained advisers please telephone our Senior Issues team on 0800 005 1755. The Caesar& Howie Group

IFRS Foundation: Training Material for the IFRS for SMEs. Module 22 Liabilities and Equity

2009 IFRS Foundation: Training Material for the IFRS for SMEs Module 22 Liabilities and Equity IFRS Foundation: Training Material for the IFRS for SMEs including the full text of Section 22 Liabilities

2009 IFRS Foundation: Training Material for the IFRS for SMEs Module 22 Liabilities and Equity IFRS Foundation: Training Material for the IFRS for SMEs including the full text of Section 22 Liabilities

PROCEDURES MANUAL. for. The technical and financial Due Diligence assessment under the NER 300 process

EUROPEAN COMMISSION PROCEDURES MANUAL for The technical and financial Due Diligence assessment under the NER 300 process Disclaimer This Manual has been developed by the Commission in consultation with

EUROPEAN COMMISSION PROCEDURES MANUAL for The technical and financial Due Diligence assessment under the NER 300 process Disclaimer This Manual has been developed by the Commission in consultation with

Basic Financial Modelling in Excel

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: 14-15 May 2018 This course can also be presented in-house for your company or via live on-line webinar The

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: 14-15 May 2018 This course can also be presented in-house for your company or via live on-line webinar The

SCOTTISH WIDOWS BANK MORTGAGE CONDITIONS 2017

SCOTTISH WIDOWS BANK MORTGAGE CONDITIONS 2017 PLEASE READ WE KNOW THAT HAVING TO READ A LEGAL CONTRACT CAN BE OFF PUTTING, SO WE HAVE DECIDED TO DO THINGS DIFFERENTLY. THIS BOOKLET CONTAINS: A brief explanation

SCOTTISH WIDOWS BANK MORTGAGE CONDITIONS 2017 PLEASE READ WE KNOW THAT HAVING TO READ A LEGAL CONTRACT CAN BE OFF PUTTING, SO WE HAVE DECIDED TO DO THINGS DIFFERENTLY. THIS BOOKLET CONTAINS: A brief explanation

Project Finance. This course can be presented in-house for you on a date of your choosing. The Banking and Corporate Finance Training Specialist

Project Finance This course can be presented in-house for you on a date of your choosing The Banking and Corporate Finance Training Specialist Course Objectives Participants Will: Develop your understanding

Project Finance This course can be presented in-house for you on a date of your choosing The Banking and Corporate Finance Training Specialist Course Objectives Participants Will: Develop your understanding

Renewable Generation (Category 1-20 kw and less):

:") Renewable Generation (Category 1-20 kw and less): Net Metering Program Interconnection Program Application Parallel Operating Agreement Net Metering Program What is net metering? Net metering is a tool

Renewable Generation (Category 1-20 kw and less): Net Metering Program Interconnection Program Application Parallel Operating Agreement Net Metering Program What is net metering? Net metering is a tool

Steps to Success. Energy Efficiency Loans in Wales Applicant Supporting Information. Updated May 2018

Steps to Success Energy Efficiency Loans in Wales Applicant Supporting Information Updated May 2018 Energy Efficiency Loans in Wales Congratulations! You re taking the first step towards saving your business

Steps to Success Energy Efficiency Loans in Wales Applicant Supporting Information Updated May 2018 Energy Efficiency Loans in Wales Congratulations! You re taking the first step towards saving your business

Renewable Generation (Category 1 20 kw and less):

:") Renewable Generation (Category 1 20 kw and less): Net Metering Program Interconnection Program Application Parallel Operating Agreement Net Metering Program What is net metering? Net metering is a tool

Renewable Generation (Category 1 20 kw and less): Net Metering Program Interconnection Program Application Parallel Operating Agreement Net Metering Program What is net metering? Net metering is a tool

Wairakei Ring Investment Proposal. Project Reference: CTNI_TRAN-DEV-01. Attachment A GIT Results

Wairakei Ring Investment Proposal Project Reference: CTNI_TRAN-DEV-01 Attachment A GIT Results December 2008 Document Revision Control Document Number/Version 001/Rev A Description Wairakei Ring Investment

Wairakei Ring Investment Proposal Project Reference: CTNI_TRAN-DEV-01 Attachment A GIT Results December 2008 Document Revision Control Document Number/Version 001/Rev A Description Wairakei Ring Investment

Social Investment Jargon Buster

Social Investment Jargon Buster A Asset something valuable that an organisation owns, benefits from, or has use of that is recorded on its balance sheet. Tangible assets could include property, vehicles,

Social Investment Jargon Buster A Asset something valuable that an organisation owns, benefits from, or has use of that is recorded on its balance sheet. Tangible assets could include property, vehicles,

Accruals accounts. How to prepare accruals accounts and the trustees annual report

Accruals accounts How to prepare accruals accounts and the trustees annual report CCNI ARR04 consultation document 1 December 2015 The Charity Commission for Northern Ireland The Charity Commission for

Accruals accounts How to prepare accruals accounts and the trustees annual report CCNI ARR04 consultation document 1 December 2015 The Charity Commission for Northern Ireland The Charity Commission for

NPD Model Explanatory Note

NPD Model Explanatory Note March 2015 FOREWORD In recent years a number of public authorities in Scotland have procured privately financed infrastructure projects using the non-profit distributing or NPD

NPD Model Explanatory Note March 2015 FOREWORD In recent years a number of public authorities in Scotland have procured privately financed infrastructure projects using the non-profit distributing or NPD

The Examiner's Answers Specimen Paper F3 - Financial Strategy

The Examiner's Answers Specimen Paper F3 - Financial Strategy SECTION A Answer to Question One Requirement (a) Appendix A 1. Assume constant exchange rate Project years 1 3 4 5 5 to 24 6 to 25 Calendar

The Examiner's Answers Specimen Paper F3 - Financial Strategy SECTION A Answer to Question One Requirement (a) Appendix A 1. Assume constant exchange rate Project years 1 3 4 5 5 to 24 6 to 25 Calendar

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L3 Project Financing www.mba638.wordpress.com Objectives To understand what project financing is and what steps are involved in securing and managing

MBF1223 Financial Management Prepared by Dr Khairul Anuar L3 Project Financing www.mba638.wordpress.com Objectives To understand what project financing is and what steps are involved in securing and managing

Planned and Cyclical Maintenance Policy

M3 Planned and Cyclical Maintenance Policy Date of Approval Review Date August 2016 August 2019 Planned and Cyclical Maintenance 1. Policy Context The introduction of this new comprehensive policy on Planned

M3 Planned and Cyclical Maintenance Policy Date of Approval Review Date August 2016 August 2019 Planned and Cyclical Maintenance 1. Policy Context The introduction of this new comprehensive policy on Planned

PRINCE2. Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version:

PRINCE2 Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version: 1.0 Exam M QUESTION 1 Identify the missing word(s) from the following sentence. A project is a temporary organization that is

PRINCE2 Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version: 1.0 Exam M QUESTION 1 Identify the missing word(s) from the following sentence. A project is a temporary organization that is

Risk management for the renewable energy sector

Aon Risk Solutions Power Renewable Energy Risk management for the renewable energy sector Plug into protection that s as innovative as your technologies. Risk. Reinsurance. Human Resources. Your projects

Aon Risk Solutions Power Renewable Energy Risk management for the renewable energy sector Plug into protection that s as innovative as your technologies. Risk. Reinsurance. Human Resources. Your projects

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Basic Financial Modelling in Excel

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: DATES TBD This course can also be presented in-house for your company or via live on-line webinar The Banking

Basic Financial Modelling in Excel A Two Day Programme This course is presented in London on: DATES TBD This course can also be presented in-house for your company or via live on-line webinar The Banking

World Bank Group - LED Streetlight Financing Tool: User s Manual

World Bank Group - LED Streetlight Financing Tool: User s Manual The World Bank Group developed the CityLED Streetlight Financing Tool to allow cities to evaluate the financial implications, as well as

World Bank Group - LED Streetlight Financing Tool: User s Manual The World Bank Group developed the CityLED Streetlight Financing Tool to allow cities to evaluate the financial implications, as well as

POLICY IN CONFIDENCE

DRAFT FOR DISCUSSION 13 June 2002 POLICY IN CONFIDENCE The NHS as an Innovative Organisation: A Framework and Guidance on the Management of Intellectual Property in the NHS Executive Summary 1. This Framework

DRAFT FOR DISCUSSION 13 June 2002 POLICY IN CONFIDENCE The NHS as an Innovative Organisation: A Framework and Guidance on the Management of Intellectual Property in the NHS Executive Summary 1. This Framework

RAISING FINANCE. Key Contracts. Commercial Contracts. Contractual JV. Collaboration. Design. Protecting IP. Key IP Rights. Development & Production

RAISING FINANCE Key Terms of Occupation Lease Key Protections Rent & Other Charges Joint Ventures JV Commercial CC Business Premises BP Corporate JV Contractual JV Employees E Managing Risk Accounting

RAISING FINANCE Key Terms of Occupation Lease Key Protections Rent & Other Charges Joint Ventures JV Commercial CC Business Premises BP Corporate JV Contractual JV Employees E Managing Risk Accounting

A Glossary of Loan Terms

A Glossary of Loan Terms Link to Online Glossary of Loan Terms: http://www.gdrc.org/icm/loan-glossary.html Assets Anything of value. Any interest in real or personal property which can be appropriated

A Glossary of Loan Terms Link to Online Glossary of Loan Terms: http://www.gdrc.org/icm/loan-glossary.html Assets Anything of value. Any interest in real or personal property which can be appropriated

Mergers and closures. Guidance for charities on merging or closing their charity

Mergers and closures Guidance for charities on merging or closing their charity The Charity Commission for Northern Ireland The Charity Commission for Northern Ireland is the regulator of charities in

Mergers and closures Guidance for charities on merging or closing their charity The Charity Commission for Northern Ireland The Charity Commission for Northern Ireland is the regulator of charities in

You have your idea, your business plan and an office to work from but in order to get your business off the ground you need money.

RF CORPORATE JV CONTRACTUAL JV COLLABO You have your idea, your business plan and an office to work from but in order to get your business off the ground you need money. In the early stages of a business

RF CORPORATE JV CONTRACTUAL JV COLLABO You have your idea, your business plan and an office to work from but in order to get your business off the ground you need money. In the early stages of a business

Development finance. A best practice guide to lending. Constructing Excellence South West A

Development finance A best practice guide to lending Constructing Excellence South West A Contents This guide has been produced by Constructing Excellence South West s Lean Forum led by their drafting

Development finance A best practice guide to lending Constructing Excellence South West A Contents This guide has been produced by Constructing Excellence South West s Lean Forum led by their drafting

INFORMATION ABOUT YOUR MORTGAGE: A GUIDE TO MORTGAGES ON PROPERTIES TO BE LET

INFORMATION ABOUT YOUR MORTGAGE: A GUIDE TO MORTGAGES ON PROPERTIES TO BE LET INTRODUCTION This guide gives details of our mortgages and is split into two parts: The first part is useful for customers

INFORMATION ABOUT YOUR MORTGAGE: A GUIDE TO MORTGAGES ON PROPERTIES TO BE LET INTRODUCTION This guide gives details of our mortgages and is split into two parts: The first part is useful for customers

Fiscal Policy and Financial Support Schemes for Clean Energy Mini Grids (CEMG)

") Fiscal Policy and Financial Support Schemes for Clean Energy Mini Grids (CEMG) page 1 page 2 Summary of the presentation Introduction 1. Fiscal Policy and Regulation (B1) 2. Grants and Subsidies (E1) 3.

Fiscal Policy and Financial Support Schemes for Clean Energy Mini Grids (CEMG) page 1 page 2 Summary of the presentation Introduction 1. Fiscal Policy and Regulation (B1) 2. Grants and Subsidies (E1) 3.

Solar is a Bright Investment

Solar is a Bright Investment Investing in a solar system seems like a great idea, but what are the financial implications? How much will it cost and what is the payback? These are common questions that

Solar is a Bright Investment Investing in a solar system seems like a great idea, but what are the financial implications? How much will it cost and what is the payback? These are common questions that

ACCOUNTING STANDARDS BOARD EXPOSURE DRAFT OF A PROPOSED GUIDELINE ON THE APPLICATION OF MATERIALITY TO FINANCIAL STATEMENTS (ED 168)

") Comments due by 7 December 2018 ACCOUNTING STANDARDS BOARD EXPOSURE DRAFT OF A PROPOSED GUIDELINE ON THE APPLICATION OF MATERIALITY TO FINANCIAL STATEMENTS (ED 168) Issued by the Accounting Standards Board

Comments due by 7 December 2018 ACCOUNTING STANDARDS BOARD EXPOSURE DRAFT OF A PROPOSED GUIDELINE ON THE APPLICATION OF MATERIALITY TO FINANCIAL STATEMENTS (ED 168) Issued by the Accounting Standards Board

BUSINESS IN THE UK A ROUTE MAP

1 BUSINESS IN THE UK A ROUTE MAP 18 chapter 02 Anyone wishing to set up business operations in the UK for the first time has a number of options for structuring those operations. There are a number of

1 BUSINESS IN THE UK A ROUTE MAP 18 chapter 02 Anyone wishing to set up business operations in the UK for the first time has a number of options for structuring those operations. There are a number of

TREASURY MANAGEMENT POLICY The Association s Treasury Management Policy will be operated by the following principles:

1.0 STATEMENT OF PRINCIPLES TREASURY MANAGEMENT POLICY 2017 The Association s Treasury Management Policy will be operated by the following principles: (i) (ii) (iii) The Association regards the successful

1.0 STATEMENT OF PRINCIPLES TREASURY MANAGEMENT POLICY 2017 The Association s Treasury Management Policy will be operated by the following principles: (i) (ii) (iii) The Association regards the successful

Checklist for PV Installations Feb 2012

Checklist for PV Installations Feb 2012 Installation of Solar Photovoltaic systems (PV) can generate an income in the form of the Feed In Tariff, which is paid for every kwh generated, plus a separate

Checklist for PV Installations Feb 2012 Installation of Solar Photovoltaic systems (PV) can generate an income in the form of the Feed In Tariff, which is paid for every kwh generated, plus a separate

Chapter 8: Lifecycle Planning

Chapter 8: Lifecycle Planning Objectives of lifecycle planning Identify long-term investment for highway infrastructure assets and develop an appropriate maintenance strategy Predict future performance

Chapter 8: Lifecycle Planning Objectives of lifecycle planning Identify long-term investment for highway infrastructure assets and develop an appropriate maintenance strategy Predict future performance

Hightown Housing Association Limited 4 per cent. Bonds due 31 October 2027 (including Retained Bonds)

") PROSPECTUS DATED 10 OCTOBER 2017 Hightown Hightown Housing Association Limited 4 per cent. Bonds due 31 October 2027 (including Retained Bonds) Issued by Retail Charity Bonds PLC secured on a loan to Hightown

PROSPECTUS DATED 10 OCTOBER 2017 Hightown Hightown Housing Association Limited 4 per cent. Bonds due 31 October 2027 (including Retained Bonds) Issued by Retail Charity Bonds PLC secured on a loan to Hightown

Overview of cogeneration project development

Overview of cogeneration project development 2004 Cogeneration Week in Thailand 23-25 March 2004 Miracle Grand Convention Hotel, Bangkok Romel M. Carlos Financial Advisor Project Development Process Commissioning

Overview of cogeneration project development 2004 Cogeneration Week in Thailand 23-25 March 2004 Miracle Grand Convention Hotel, Bangkok Romel M. Carlos Financial Advisor Project Development Process Commissioning

Use your property to your advantage. A guide to our Buy-to-Let products

Use your property to your advantage A guide to our Buy-to-Let products Introducing Retirement Advantage 2 A guide to our Buy-to-Let products Retirement Advantage is a wellestablished company that can trace

Use your property to your advantage A guide to our Buy-to-Let products Introducing Retirement Advantage 2 A guide to our Buy-to-Let products Retirement Advantage is a wellestablished company that can trace

RICS preferred UK PI Broker

RICS preferred UK PI Broker PROFESSIONAL INDEMNITY INSURANCE FOR START-UP SURVEYING FIRMS PROPOSAL FORM Guidance Notes 1. Please provide CVs for all the Partner(s) / Director(s) / Principal(s) of the Firm.

RICS preferred UK PI Broker PROFESSIONAL INDEMNITY INSURANCE FOR START-UP SURVEYING FIRMS PROPOSAL FORM Guidance Notes 1. Please provide CVs for all the Partner(s) / Director(s) / Principal(s) of the Firm.

1 SOURCES OF FINANCE

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

Private Sector Facility: Working with Local Private Entities, Including Small and Medium-Sized Enterprises

Private Sector Facility: Working with Local Private Entities, Including Small and Medium-Sized Enterprises GCF/B.09/12 5 March 2015 Meeting of the Board 24-26 March 2015 Songdo, Republic of Korea Agenda

Private Sector Facility: Working with Local Private Entities, Including Small and Medium-Sized Enterprises GCF/B.09/12 5 March 2015 Meeting of the Board 24-26 March 2015 Songdo, Republic of Korea Agenda

Creating a planet run by the sun

28 th Annual ROTH Conference March 14, 2016 Creating a planet run by the sun 1 Safe Harbor & Forward Looking Statements This presentation contains forward-looking statements within the meaning of Section

28 th Annual ROTH Conference March 14, 2016 Creating a planet run by the sun 1 Safe Harbor & Forward Looking Statements This presentation contains forward-looking statements within the meaning of Section

The Essential Guide to Successful Refinancing The 4 industry secrets vital to refinance and save

The Essential Guide to Successful Refinancing The 4 industry secrets vital to refinance and save R.E.F.I Reason-Explore-Formalise-Implement Being an award winning financial services business requires a

The Essential Guide to Successful Refinancing The 4 industry secrets vital to refinance and save R.E.F.I Reason-Explore-Formalise-Implement Being an award winning financial services business requires a

Obtaining Project Financing. Chapter 7. Contents: 7-1. Financing: What Lenders/Investors Look For 1

Contents: 7-1. Financing: What Lenders/Investors Look For 1 7-2. Financing Approaches 1 7-2.1 Looking for Low Interest Loans or Cost Share Funding... 4 7-2.2 Debt Financing... 4 Lender s Requirements...4

Contents: 7-1. Financing: What Lenders/Investors Look For 1 7-2. Financing Approaches 1 7-2.1 Looking for Low Interest Loans or Cost Share Funding... 4 7-2.2 Debt Financing... 4 Lender s Requirements...4

HOW TO GUIDE. The FINANCE module

HOW TO GUIDE The FINANCE module Copyright and publisher: EMD International A/S Niels Jernes vej 10 9220 Aalborg Ø Denmark Phone: +45 9635 44444 e-mail: emd@emd.dk web: www.emd.dk About energypro energypro

HOW TO GUIDE The FINANCE module Copyright and publisher: EMD International A/S Niels Jernes vej 10 9220 Aalborg Ø Denmark Phone: +45 9635 44444 e-mail: emd@emd.dk web: www.emd.dk About energypro energypro

Growth Finance Expertise. Transfer of Family Business. Business Banking

Growth Finance Expertise Transfer of Family Business Business Banking 1 Business Banking Family businesses are the keystone of the Irish economy, notable family firms include the Musgrave Group, in family

Growth Finance Expertise Transfer of Family Business Business Banking 1 Business Banking Family businesses are the keystone of the Irish economy, notable family firms include the Musgrave Group, in family

ASIC RG46 Disclosure. AusFunds Fractional Property Investment Platform ARSN

AusFunds Fractional Property Investment Platform ARSN 623 862 662 ASIC RG46 Disclosure 5 November 2018 Vasco Investment Managers Limited ABN 71 138 715 009 AFSL 344486 ASIC Regulatory Guide 46 Disclosure

AusFunds Fractional Property Investment Platform ARSN 623 862 662 ASIC RG46 Disclosure 5 November 2018 Vasco Investment Managers Limited ABN 71 138 715 009 AFSL 344486 ASIC Regulatory Guide 46 Disclosure

Project Finance An Overview

Project Finance An Overview KAMAL TAK ICAI, Navi Mumbai Chapter December 16, 2012 1 Project Finance An Overview What is Project Financing? How is it different? How are Projects developed? Various Project

Project Finance An Overview KAMAL TAK ICAI, Navi Mumbai Chapter December 16, 2012 1 Project Finance An Overview What is Project Financing? How is it different? How are Projects developed? Various Project

Project Finance Modelling For Renewable Energy

Project Finance Modelling For Renewable Energy A 3-Day Programme This course can be presented in-house for you on a date of your choosing The Banking and Corporate Finance Training Specialist Course Objectives

Project Finance Modelling For Renewable Energy A 3-Day Programme This course can be presented in-house for you on a date of your choosing The Banking and Corporate Finance Training Specialist Course Objectives

Financing DESCOs : A framework of financing working capital for Distributed Energy Services Companies. Chris Aidun and Dirk Muench March 2015

Financing DESCOs : A framework of financing working capital for Distributed Energy Services Companies Chris Aidun and Dirk Muench March 2015 INTRODUCTION... 3 WHAT IS WORKING CAPITAL?... 4 TOTAL CAPITAL

Financing DESCOs : A framework of financing working capital for Distributed Energy Services Companies Chris Aidun and Dirk Muench March 2015 INTRODUCTION... 3 WHAT IS WORKING CAPITAL?... 4 TOTAL CAPITAL

PSE&G Solar Loan III Program General Q&A

PSE&G Solar Loan III Program General Q&A Note: The following are common questions that PSE&G has received regarding the Solar Loan III Program. This document is for informational purposes only. See your

PSE&G Solar Loan III Program General Q&A Note: The following are common questions that PSE&G has received regarding the Solar Loan III Program. This document is for informational purposes only. See your

TIME:CTC. Corporate Trading Companies. Information Memorandum

Corporate Trading Companies Information Memorandum Corporate Trading Companies This document is for Authorised Financial Advisers only and for existing Shareholders for information only. Issued in the

Corporate Trading Companies Information Memorandum Corporate Trading Companies This document is for Authorised Financial Advisers only and for existing Shareholders for information only. Issued in the

2.6 STEP SIX: Assess Risks and Adjust for Optimism Bias

2.6 STEP SIX: Assess Risks and Adjust for Optimism Bias 2.6.1 In appraisals, there is always likely to be some difference between what is expected and what eventually happens, because of biases unwittingly

2.6 STEP SIX: Assess Risks and Adjust for Optimism Bias 2.6.1 In appraisals, there is always likely to be some difference between what is expected and what eventually happens, because of biases unwittingly

Invitation to Tender

Invitation to Tender November 2016 BRIEF FOR CONSULTANT TO CARRY OUT A NETWORK ANALYSIS OF THE WESTERN ISLES GRID, A REVIEW OF BUDGET ESTIMATES RECEIVED AND A STUDY ON FUTURE INNOVATIVE CONNECTION OPTIONS

Invitation to Tender November 2016 BRIEF FOR CONSULTANT TO CARRY OUT A NETWORK ANALYSIS OF THE WESTERN ISLES GRID, A REVIEW OF BUDGET ESTIMATES RECEIVED AND A STUDY ON FUTURE INNOVATIVE CONNECTION OPTIONS

Guidance for providers about the financial information required for registration

Guidance for providers about the financial information required for registration Introduction 1. This regulatory advice sets out guidance about the financial data and information you need to submit with

Guidance for providers about the financial information required for registration Introduction 1. This regulatory advice sets out guidance about the financial data and information you need to submit with

Model Concession Agreement for Highways: An Overview

Model Concession Agreement for Highways: An Overview - Gajendra Haldea The highways sector in India is witnessing significant interest from both domestic as well as foreign investors following the policy

Model Concession Agreement for Highways: An Overview - Gajendra Haldea The highways sector in India is witnessing significant interest from both domestic as well as foreign investors following the policy

Renewable energy project finance A product that FITs? Chris Rodgers 19 Mar 2014

Renewable energy project finance A product that FITs? Chris Rodgers 19 Mar 2014 Agenda Renewable Energy Finance 1. Introduction to Close Brothers & our Energy Team 2. The current 1-15m renewable energy

Renewable energy project finance A product that FITs? Chris Rodgers 19 Mar 2014 Agenda Renewable Energy Finance 1. Introduction to Close Brothers & our Energy Team 2. The current 1-15m renewable energy

DIRECTION ISSUE CHANGE RATIONALE PART 1. Wording added: These Directions are given to the Local Health Boards. some definitions:

GP Premises- Revised Directions Detailed amendments and stated rationale DIRECTION ISSUE CHANGE RATIONALE PART 1 General 1 Citation, Commencement and application 2 Interpretation Additional Definitions

GP Premises- Revised Directions Detailed amendments and stated rationale DIRECTION ISSUE CHANGE RATIONALE PART 1 General 1 Citation, Commencement and application 2 Interpretation Additional Definitions

ASX interim guidance: Reporting scoping studies

ASX interim guidance: Reporting scoping studies NOVEMBER 2016 ASX interim guidance: Reporting scoping studies Introduction ASX is working with ASIC, JORC and industry to develop an appropriate and robust

ASX interim guidance: Reporting scoping studies NOVEMBER 2016 ASX interim guidance: Reporting scoping studies Introduction ASX is working with ASIC, JORC and industry to develop an appropriate and robust

Kaplan analysis of May 2013 strategic pre-seen material

Kaplan analysis of May 2013 strategic pre-seen material Kaplan s three Content Specialists for the CIMA Strategic Level papers Christine Bligh, Ben Dickson-Green and Andrew Howarth present their Top 10

Kaplan analysis of May 2013 strategic pre-seen material Kaplan s three Content Specialists for the CIMA Strategic Level papers Christine Bligh, Ben Dickson-Green and Andrew Howarth present their Top 10

The Mortgage Works (UK) plc