Community Development with a Purpose. CDFI Certification: A Building Block of Community Finance

|

|

|

- Kathryn Ryan

- 6 years ago

- Views:

Transcription

1 Community Development with a Purpose CDFI Certification: A Building Block of Community Finance

2 CDFI Fund CDFI Fund established by Congress in 1994 through the efforts of Federation and others in community finance Mission of CDFI Fund Expand the capacity of financial institutions to provide credit, capital, and financial services to underserved populations and economically distressed communities in the United States Certification given by the U.S. Department of Treasury Broad bi-partisan support; appropriations stable or increasing

3 CDFI Target Markets Places (Geographic) CDFI Investment Area (Census Tracts) Low Income High Poverty High Unemployment 384 Persistent Poverty Counties Poverty rate above 20% as of 1990, 2000 and 2010 People (Demographic) Low Income Targeted Populations Other Targeted Populations

4

5

6

7

8

9 Credit Unions & CDFI Fund CUs Initially slow to embrace CDFI certification New momentum since 2010 Doubling in number of NCUA Low Income Designated CUs Increased visibility of CDFI success stories 2014 NCUA CDFI Certification Challenge Federation CDFI Certification Challenge Positive research findings on performance & impact of CDFI CUs

10 The CDFI Industry More than just credit unions Type of CDFI Unregulated CDFIs December 2013 October 2015 Number Percent Number Percent Percentage Increase Loan Funds % % +4% Venture Capital Funds 13 2% 14 1% +8% Regulated CDFIs Credit Unions % % +53% Banks and Thrifts 76 9% % +47% Depository Holding Companies 50 6% 61 6% +22% Total % %

11 Top Ten States for CDFI Credit Unions Rank State # CDFIs CDFI Certifications as of 10/31/2015 Credit Unions Loan Funds Banks & Depository Holding Companies Venture Capital Funds CU % of State CDFIs 1 Missouri % 2 Louisiana % 3 New York % 4 Texas % 5 Florida % 6 Michigan % 7 California % 8 Mississippi % 9 Illinois % 10 Washington %

12 California in CDFI Terms 46% of census tracts in state classified as Investment Areas by CDFI Fund Indicators of economic distress include low median family income, high rates of poverty, unemployment Nearly 17 million Californians live in CDFI Investment Areas 11 California credit unions are CDFI certified 34 credit unions show strong potential for certification More than 67% of branches located in CDFI Investment Areas Strong financial and operational capacity Profile of community development products and services comparable to CDFI credit unions

13 By the numbers California CDFI Credit Unions CDFI certifications as of 10/31/2015; Financial data as of 12/31/2014 Type of Credit Unions # of CUs # of Branches Total Members Total Assets CDFI Certified ,603 $ 4,061,370,839 High Potential CDFIs ,298 $ 1,896,659,823 Totals ,901 $ 5,958,030,662

14

15

16

17

18

19

20

21

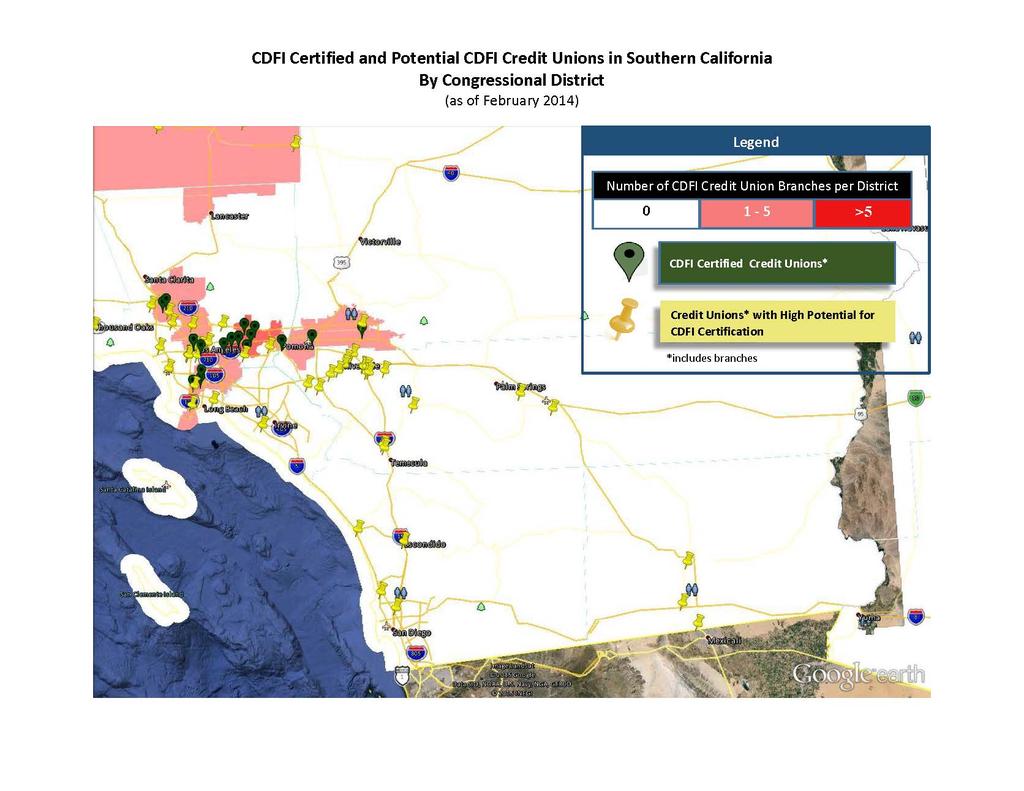

22 CDFI CUs by Congressional District All 53 Congressional Districts include census tracts that qualify as CDFI Investment Areas minimum 11 tracts in CA 45 th maximum 176 tracts in CA 11 th CDFI certified credit unions are located in 21 Districts From 1 to 8 branches, depending on District 32 Districts have no CDFI certified credit unions at this time 43 potential CDFI credit unions have branches in 13 Districts that currently have at least one CDFI credit union 25 Districts that currently have zero

23

24

25

26

27 What the Research Says

28 Positive Impact of CDFI Credit Unions CDFIs promote economic revitalization among underserved communities and populations Financial services are a critical path to financial inclusion CDFI credit unions leverage more private capital than any other type of CDFI Median Loan Fund leverage: $1.10 Median CDFI Credit Union leverage: $9.91 From , 61 credit unions that received $102.7 million in CDFI grants increased Total Assets by $2.4 billion Total Loans by $1.5 Billion Leverage rate of more than 23:1

29 Positive Performance of CDFI Credit Unions Despite serving low-income, underserved markets, when compared with mainstream peers, CDFI credit unions Deliver comparable financial results (ROI) Show no greater institutional risks Rate equal or better in operational efficiency CDFI CUs outperform their mainstream peers in Member service technologies Complex loan products Community development loan products Community development services Capacity building services

30 What Makes a CDFI? CDFI Fund has 7 requirements for certification 1. Legal entity 2. Primary mission of community development 3. Financing entity 4. Target market (more than 60% of activities) 5. Accountability to target market 6. Development services to build capacity of members 7. Non-governmental entity.

31 What Really Makes a CDFI? A matter of intent What they do, not where they live CDFI credit unions far more likely than peers to offer Community Development Loan Products credit builder, shared secured credit cards, micro business & consumer, pay da, refund anticipation anti-predatory STS loans Community Development Savings & Account Services check-cashing, international remittances, money orders, business share accounts Capacity-Building Services financial counseling, financial education, first-time home-buyers programs, bilingual services, free tax preparation services.

32 CDFI Certification Requirements & Process

33 7 Tests for CDFI Certification 1. Legal Entity 2. Primary Mission 3. Financing Entity 4. Target Market 5. Accountability 6. Development Services 7. Non-Government Entity Documents Documents Documents Documents Automatic Automatic (LICUs) Automatic Automatic Documents Automatic

34 1. Legal Entity 2. Primary Mission 3. Financing Entity 4. Target Market 5. Accountability 6. Development Services 7. Non-Government Entity What s left?

35 Test # 4: Target Market Single most critical test for credit unions At least 60% of financing activities must be targeted to eligible Target Market CDFI Target Markets: CDFI Investment Areas Low-Income Targeted Populations Other Targeted Populations May use one or more TMs to qualify

36 Investment Areas (IA) A geographic unit (county, census tract, block group, Indian/Native areas), or contiguous geographic units in the US that meets distress benchmarks for: Low median family income; High rate of poverty; and/or High rate of unemployment. Most CDCUs qualify simply on IA criteria Easiest Target Market to document Random sample of member addresses CDFI Fund mapping program Qualified Investment Area must consist of contiguous tracts Geocode member addresses to tell % that live in Investment Areas Cross check with updated ACS data

37 Low Income Targeted Pop (LITP) Population for a geographic unit is comprised of individuals whose family income is not more than 80% of the MFI. Requires more extensive analysis: Federation has developed a Random sample of borrowers addresses and income CDFI Fund mapping program Geocode member addresses to tell % that live in Investment Areas Identify area median income benchmark for each borrower Compare actual borrower income to low-income benchmark

38 Other Targeted Populations African Americans, Alaska Natives residing in Alaska, Hispanics, Native Americans, Native Hawaiians residing in Hawaii, Other ethnicities. OTP data not typically collected systematically by credit unions Must provide basis for estimating % of total activities directed towards OTP OTP credit unions can generally also qualify on basis of Investment Areas or Low-Income Targeted Populations

39 Test #5: Accountability Based on analysis of governing and advisory board members Automatic for or credit unions with Target Market defined as Low Income Targeted Population (LITP) or Investment Areas (if accounts for more than 50% activities) OTP (if accounts for more than 50% of activities) CU boards are democratically elected by the people they serve (no other types of CDFIs have such direct accountability to their TMs) Federation continues to advocate with CDFI Fund that credit unions are automatically accountable to all TMS in proportion to membership CDFIs must ensure that Boards understand and support CDFI certification

40 #6. Development Services Non transactional activities Builds capacity to manage personal finances Linked to financial products e.g., financial education, credit counseling, VITA/EITC Complete Development Services Table Provide one-page narrative Briefly describe each Development Service Clearly describe link to CU financial products If a partner organization provides your Dev Services: Describe relationship Attach a copy of the services contract/agreement

41 CDFI Certification Assistance Federation approach is based on preliminary analysis of a CU s borrowers sampling Helps determine eligibility 100% success rate for eligible certification applicants Sampling can be used for Certification, Recertification, Monitoring and CDCI Compliance

42 Questions?

CDFI Certification. A Pathway to Growth and Impact

CDFI Certification A Pathway to Growth and Impact CDFI Fund Basics Established by Congress 1994 Federation and CDCUs instrumental in founding CDFIs include regulated and unregulated institutions that meet

CDFI Certification A Pathway to Growth and Impact CDFI Fund Basics Established by Congress 1994 Federation and CDCUs instrumental in founding CDFIs include regulated and unregulated institutions that meet

Strengthening Your Capacity to Serve the Underserved

Strengthening Your Capacity to Serve the Underserved Blake Myers Consultant, National Federation of Community Development Credit Unions Teri Robinson CEO, Pacific NW Ironworkers FCU Agenda 1. The Opportunity:

Strengthening Your Capacity to Serve the Underserved Blake Myers Consultant, National Federation of Community Development Credit Unions Teri Robinson CEO, Pacific NW Ironworkers FCU Agenda 1. The Opportunity:

Low Income Designation: Leveraging Regulations to Amplify your Impact in Low Income Markets

Low Income Designation: Leveraging Regulations to Amplify your Impact in Low Income Markets System Challenges Supplemental Capital: significant pressure to comply with net worth minimum requirements and/or

Low Income Designation: Leveraging Regulations to Amplify your Impact in Low Income Markets System Challenges Supplemental Capital: significant pressure to comply with net worth minimum requirements and/or

National Case Statement

Discussion Topics Session Description Learn about the advantages your Credit Union Members can receive by obtaining low-income designation and CDFI Certification and how this translates to Member value.

Discussion Topics Session Description Learn about the advantages your Credit Union Members can receive by obtaining low-income designation and CDFI Certification and how this translates to Member value.

Credit Union Access to Capital

Credit Union Access to Capital & How the Federation Can Help! 2012 AACUC Annual Conference Charleston, SC Terri J. Fowlkes Director, Community Development Investments National Federation of Community Development

Credit Union Access to Capital & How the Federation Can Help! 2012 AACUC Annual Conference Charleston, SC Terri J. Fowlkes Director, Community Development Investments National Federation of Community Development

Asset Policy 101: Building Wealth for All Californians

Asset Policy 101: Building Wealth for All Californians California Asset Policy Working Lunch Series Hosted by the Asset Policy Initiative of California & the New America Foundation California State Capitol

Asset Policy 101: Building Wealth for All Californians California Asset Policy Working Lunch Series Hosted by the Asset Policy Initiative of California & the New America Foundation California State Capitol

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C FORM 8-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest

Lapkoff & Gobalet Demographic Research, Inc.

Lapkoff & Gobalet Demographic Research, Inc. 22361 Rolling Hills Road, Saratoga, CA 95070-6560 (408) 725-8164 Fax (408) 725-1479 2120 6 th Street #9, Berkeley, CA 94710-2204 (510) 540-6424 Fax (510) 540-6425

Lapkoff & Gobalet Demographic Research, Inc. 22361 Rolling Hills Road, Saratoga, CA 95070-6560 (408) 725-8164 Fax (408) 725-1479 2120 6 th Street #9, Berkeley, CA 94710-2204 (510) 540-6424 Fax (510) 540-6425

Community Development Financial Institutions Fund United States Department of the Treasury. Performance and Accountability Report FY 2010

Community Development Financial Institutions Fund United States Department of the Treasury Performance and Accountability Report FY 200 Table of Contents Message from the Director...3 Community Development

Community Development Financial Institutions Fund United States Department of the Treasury Performance and Accountability Report FY 200 Table of Contents Message from the Director...3 Community Development

Serving the Underserved: Building Alternative Financial Services in Low-Income Communities

Serving the Underserved: Building Alternative Financial Services in Low-Income Communities Today s Presentations About the Federation Overview of Building Blocks LID & CDFI Secondary Capital Market Opportunity

Serving the Underserved: Building Alternative Financial Services in Low-Income Communities Today s Presentations About the Federation Overview of Building Blocks LID & CDFI Secondary Capital Market Opportunity

Measuring the Recession: An Impact Index

Measuring the Recession: An Impact Index October 2009 65 Broadway, Suite 1800, New York NY 10006 (212) 248-2785 www.centerforsocialinclusion.org 1 Executive Summary Across America people have been hit

Measuring the Recession: An Impact Index October 2009 65 Broadway, Suite 1800, New York NY 10006 (212) 248-2785 www.centerforsocialinclusion.org 1 Executive Summary Across America people have been hit

Promoting Investment in Distressed Communities:

CommunityDevelopment Financial Institutions Fund Promoting Investment in Distressed Communities: The New Markets Tax Credit Program UNITED STATES DEPARTMENT OF THE TREASURY PREPARED by Financial Strategies

CommunityDevelopment Financial Institutions Fund Promoting Investment in Distressed Communities: The New Markets Tax Credit Program UNITED STATES DEPARTMENT OF THE TREASURY PREPARED by Financial Strategies

Determinants of Federal and State Community Development Spending:

Determinants of Federal and State Community Development Spending: 1981 2004 by David Cashin, Julie Gerenrot, and Anna Paulson Introduction Federal and state community development spending is an important

Determinants of Federal and State Community Development Spending: 1981 2004 by David Cashin, Julie Gerenrot, and Anna Paulson Introduction Federal and state community development spending is an important

Findings from the CDFI Fund's Impact Analysis. Michael Swack, Carsey School of Public Policy, University of New Hampshire

Understanding Impact Measurement: Findings from the CDFI Fund's Impact Analysis Michael Swack, Carsey School of Public Policy, University of New Hampshire Carsey Study s Key Findings CDFIs are concentrating

Understanding Impact Measurement: Findings from the CDFI Fund's Impact Analysis Michael Swack, Carsey School of Public Policy, University of New Hampshire Carsey Study s Key Findings CDFIs are concentrating

CDFI Credit Unions A Business Case for Community Development Finance. CDFI Institute February 28, 2017

CDFI Credit Unions A Business Case for Community Development Finance CDFI Institute February 28, 2017 What it means to be a CDFI? Community Development Key Products & Services Inclusive transaction services

CDFI Credit Unions A Business Case for Community Development Finance CDFI Institute February 28, 2017 What it means to be a CDFI? Community Development Key Products & Services Inclusive transaction services

COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND DEPARTMENT OF THE TREASURY. Fiscal Year ACCOUNTABILITY REPORT

COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND DEPARTMENT OF THE TREASURY 2003 Fiscal Year ACCOUNTABILITY REPORT TABLE OF CONTENTS Message from the Director s Office... 3 Message from the Deputy Director

COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND DEPARTMENT OF THE TREASURY 2003 Fiscal Year ACCOUNTABILITY REPORT TABLE OF CONTENTS Message from the Director s Office... 3 Message from the Deputy Director

Be a Hero. Rethinking Service to People of Modest Means: New Strategies Out of the Box Thinking and Best Practices

Be a Hero Rethinking Service to People of Modest Means: New Strategies Out of the Box Thinking and Best Practices Leveraging Our History to Develop New Strategies Credit Union Heroes Dare Greatly To Dare

Be a Hero Rethinking Service to People of Modest Means: New Strategies Out of the Box Thinking and Best Practices Leveraging Our History to Develop New Strategies Credit Union Heroes Dare Greatly To Dare

Did States Maximize Their Opportunity Zone Selections?

M E T R O P O L I T A N H O U S I N G A N D C O M M U N I T I E S P O L I C Y C E N T E R Did States Maximize Their Opportunity Zone Selections? Analysis of the Opportunity Zone Designations Brett Theodos,

M E T R O P O L I T A N H O U S I N G A N D C O M M U N I T I E S P O L I C Y C E N T E R Did States Maximize Their Opportunity Zone Selections? Analysis of the Opportunity Zone Designations Brett Theodos,

Commission District 4 Census Data Aggregation

Commission District 4 Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page

Commission District 4 Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page

Northwest Census Data Aggregation

Northwest Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5) Table

Northwest Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5) Table

Community Development Investment Program (CDIP) for CDCUs SECONDARY CAPITAL I APPLICATION

for CDCUs SECONDARY CAPITAL I APPLICATION") Community Development Investment Program (CDIP) for CDCUs SECONDARY CAPITAL I APPLICATION Date: Credit Union: Charter Number: Contact Person: Title : Telephone: ( ) Fax: ( ) E-mail Mailing Address: Secondary

Community Development Investment Program (CDIP) for CDCUs SECONDARY CAPITAL I APPLICATION Date: Credit Union: Charter Number: Contact Person: Title : Telephone: ( ) Fax: ( ) E-mail Mailing Address: Secondary

Riverview Census Data Aggregation

Riverview Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5) Table

Riverview Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5) Table

Tax Incentives for Opportunity Zones: In Brief

Sean Lowry Analyst in Public Finance Donald J. Marples Specialist in Public Finance April 5, 2018 Congressional Research Service 7-5700 www.crs.gov R45152 Contents What Census Tracts Can Be Nominated as

Sean Lowry Analyst in Public Finance Donald J. Marples Specialist in Public Finance April 5, 2018 Congressional Research Service 7-5700 www.crs.gov R45152 Contents What Census Tracts Can Be Nominated as

Zipe Code Census Data Aggregation

Zipe Code 66101 Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5)

Zipe Code 66101 Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5)

Zipe Code Census Data Aggregation

Zipe Code 66103 Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5)

Zipe Code 66103 Census Data Aggregation 2011-2015 American Community Survey Data, U.S. Census Bureau Table 1 (page 2) Table 2 (page 2) Table 3 (page 3) Table 4 (page 4) Table 5 (page 4) Table 6 (page 5)

Put in place to assist the unemployed or underemployed.

By:Erin Sollund The federal government Put in place to assist the unemployed or underemployed. Medicaid, The Women, Infants, and Children (WIC) Program, and Aid to Families with Dependent Children (AFDC)

By:Erin Sollund The federal government Put in place to assist the unemployed or underemployed. Medicaid, The Women, Infants, and Children (WIC) Program, and Aid to Families with Dependent Children (AFDC)

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE June 6, 2016 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Mizuho Bank (USA) RSSD No. 229913 1251 Avenue of the Americas New York, NY 10020 FEDERAL RESERVE BANK OF NEW YORK 33 LIBERTY

PUBLIC DISCLOSURE June 6, 2016 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Mizuho Bank (USA) RSSD No. 229913 1251 Avenue of the Americas New York, NY 10020 FEDERAL RESERVE BANK OF NEW YORK 33 LIBERTY

2018:IIIQ Nevada Unemployment Rate Demographics Report*

2018:IIIQ Nevada Unemployment Rate Demographics Report* Department of Employment, Training & Rehabilitation Research and Analysis Bureau Dr. Tiffany Tyler-Garner, Director Dennis Perea, Deputy Director

2018:IIIQ Nevada Unemployment Rate Demographics Report* Department of Employment, Training & Rehabilitation Research and Analysis Bureau Dr. Tiffany Tyler-Garner, Director Dennis Perea, Deputy Director

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE January 14, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Orange County Trust Company RSSD No. 176101 212 Dolson Avenue Middletown, NY 10940 FEDERAL RESERVE BANK OF NEW YORK

PUBLIC DISCLOSURE January 14, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Orange County Trust Company RSSD No. 176101 212 Dolson Avenue Middletown, NY 10940 FEDERAL RESERVE BANK OF NEW YORK

Commonly Collected OUTPUT and OUTCOME Indicators

Commonly Collected OUTPUT and OUTCOME Indicators Business Line Indicator Name Type Potential Uses Cross-Cutting Housing (single and multi-family) # Loans originated Output HMDA, CRA, CDFI Fund, NCIF, GIIN

Commonly Collected OUTPUT and OUTCOME Indicators Business Line Indicator Name Type Potential Uses Cross-Cutting Housing (single and multi-family) # Loans originated Output HMDA, CRA, CDFI Fund, NCIF, GIIN

Community Development Financial Institutions (CDFI) Fund

Fund") Community Development Financial Institutions (CDFI) Fund Overview April 1, 2008 National Interagency Community Reinvestment Conference How to Make Community Development Venture Capital Work Community Development

Community Development Financial Institutions (CDFI) Fund Overview April 1, 2008 National Interagency Community Reinvestment Conference How to Make Community Development Venture Capital Work Community Development

Private Equity Performance Update

Private Equity Performance Update Returns as reported through June 2015 www.pegcc.org 2 Contents Page Private Equity Performance Benchmarks 3 Private Equity Performance Public Pensions 6 Description of

Private Equity Performance Update Returns as reported through June 2015 www.pegcc.org 2 Contents Page Private Equity Performance Benchmarks 3 Private Equity Performance Public Pensions 6 Description of

The Community Development Financial

Community Development Financial Institutions Fund By Shannon Ross, Director, Government Relations, Housing Partnership Network Administering agency: U.S. Department of the Treasury (Treasury) Year program

Community Development Financial Institutions Fund By Shannon Ross, Director, Government Relations, Housing Partnership Network Administering agency: U.S. Department of the Treasury (Treasury) Year program

Nation s Uninsured Rate for Children Drops to Another Historic Low in 2016

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

An Introduction to the CDFI Fund

An Introduction to the CDFI Fund Making the New Markets Tax Credit Work in Native Communities PRESENTED ON MAY 24, 2018 COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND www.cdfifund.gov About the CDFI

An Introduction to the CDFI Fund Making the New Markets Tax Credit Work in Native Communities PRESENTED ON MAY 24, 2018 COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND www.cdfifund.gov About the CDFI

Federal Registry. NMLS Federal Registry Quarterly Report Quarter I

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Tassistance program. In fiscal year 1998, it represented 18.2 percent of all food stamp

CHARACTERISTICS OF FOOD STAMP HOUSEHOLDS: FISCAL YEAR 1998 (Advance Report) United States Department of Agriculture Office of Analysis, Nutrition, and Evaluation Food and Nutrition Service July 1999 he

CHARACTERISTICS OF FOOD STAMP HOUSEHOLDS: FISCAL YEAR 1998 (Advance Report) United States Department of Agriculture Office of Analysis, Nutrition, and Evaluation Food and Nutrition Service July 1999 he

Union Members in New York and New Jersey 2018

For Release: Friday, March 29, 2019 19-528-NEW NEW YORK NEW JERSEY INFORMATION OFFICE: New York City, N.Y. Technical information: (646) 264-3600 BLSinfoNY@bls.gov www.bls.gov/regions/new-york-new-jersey

For Release: Friday, March 29, 2019 19-528-NEW NEW YORK NEW JERSEY INFORMATION OFFICE: New York City, N.Y. Technical information: (646) 264-3600 BLSinfoNY@bls.gov www.bls.gov/regions/new-york-new-jersey

An Introduction to the American Community Survey Health Insurance Coverage Estimates

September 2009 An Introduction to the American Community Survey Health Insurance Coverage Estimates Introduction The American Community Survey (ACS) is a new source of data for health insurance coverage

September 2009 An Introduction to the American Community Survey Health Insurance Coverage Estimates Introduction The American Community Survey (ACS) is a new source of data for health insurance coverage

Creating a Sustainable Foundation for Financial Inclusion

Creating a Sustainable Foundation for Financial Inclusion Scott Butterfield, Your Credit Union Partner Sarah Marshall, North Side Community Credit Union Jamey Gill, Mendo Lake Credit Union Purpose of this

Creating a Sustainable Foundation for Financial Inclusion Scott Butterfield, Your Credit Union Partner Sarah Marshall, North Side Community Credit Union Jamey Gill, Mendo Lake Credit Union Purpose of this

Metrics and Measurements for State Pension Plans. November 17, 2016 Greg Mennis

Metrics and Measurements for State Pension Plans November 17, 2016 Greg Mennis Fiscal Sustainability Metrics Net Amortization Measures whether contributions are sufficient to reduce pension debt if plan

Metrics and Measurements for State Pension Plans November 17, 2016 Greg Mennis Fiscal Sustainability Metrics Net Amortization Measures whether contributions are sufficient to reduce pension debt if plan

Population in the U.S. Floodplains

D ATA B R I E F D E C E M B E R 2 0 1 7 Population in the U.S. Floodplains Population in the U.S. Floodplains As sea levels rise due to climate change, planners and policymakers in flood-prone areas must

D ATA B R I E F D E C E M B E R 2 0 1 7 Population in the U.S. Floodplains Population in the U.S. Floodplains As sea levels rise due to climate change, planners and policymakers in flood-prone areas must

RECOMMENDATIONS ON THE COMMUNITY REINVESTMENT ACT TO EXPAND REACH AND IMPACT. October 12, 2017

RECOMMENDATIONS ON THE COMMUNITY REINVESTMENT ACT TO EXPAND REACH AND IMPACT October 12, 2017 The National Federation of Community Development Credit Unions (the Federation ) appreciates the opportunity

RECOMMENDATIONS ON THE COMMUNITY REINVESTMENT ACT TO EXPAND REACH AND IMPACT October 12, 2017 The National Federation of Community Development Credit Unions (the Federation ) appreciates the opportunity

Utah. Demographic and Economic Profile. Metro and Nonmetro Counties in Utah

Demographic and Economic Profile Utah Updated July 2006 Metro and Nonmetro Counties in Utah Based on the most recent listing of core based statistical areas by the Office of Management and Budget (December

Demographic and Economic Profile Utah Updated July 2006 Metro and Nonmetro Counties in Utah Based on the most recent listing of core based statistical areas by the Office of Management and Budget (December

Independence, MO Data Profile 2015

, MO Data Profile 2015 5 year American Community Survey (ACS) Jackson County, Missouri Data sources: U.S. Census Bureau, American Community Survey (ACS), 2011 2015 (released December 8, 2016), compared

, MO Data Profile 2015 5 year American Community Survey (ACS) Jackson County, Missouri Data sources: U.S. Census Bureau, American Community Survey (ACS), 2011 2015 (released December 8, 2016), compared

The Office of Advocacy

The Office of Advocacy Created by Congress in 1976, the Office of Advocacy of the U.S. Small Business Administration (SBA) is an independent voice for small business within the federal government. Appointed

The Office of Advocacy Created by Congress in 1976, the Office of Advocacy of the U.S. Small Business Administration (SBA) is an independent voice for small business within the federal government. Appointed

Estimating the Number of People in Poverty for the Program Access Index: The American Community Survey vs. the Current Population Survey.

Background Estimating the Number of People in Poverty for the Program Access Index: The American Community Survey vs. the Current Population Survey August 2006 The Program Access Index (PAI) is one of

Background Estimating the Number of People in Poverty for the Program Access Index: The American Community Survey vs. the Current Population Survey August 2006 The Program Access Index (PAI) is one of

Household Income for States: 2010 and 2011

Household Income for States: 2010 and 2011 American Community Survey Briefs By Amanda Noss Issued September 2012 ACSBR/11-02 INTRODUCTION Estimates from the 2010 American Community Survey (ACS) and the

Household Income for States: 2010 and 2011 American Community Survey Briefs By Amanda Noss Issued September 2012 ACSBR/11-02 INTRODUCTION Estimates from the 2010 American Community Survey (ACS) and the

Demographic and Economic Profile. Florida. Updated May 2006

Demographic and Economic Profile Florida Updated May 2006 Metro and Nonmetro Counties in Florida Based on the most recent listing of core based statistical areas by the Office of Management and Budget

Demographic and Economic Profile Florida Updated May 2006 Metro and Nonmetro Counties in Florida Based on the most recent listing of core based statistical areas by the Office of Management and Budget

County Economic Status and Distressed Areas in the Appalachian Region

County Economic Status and Distressed Areas in the Appalachian Region Kostas Skordas, Director Regional Planning & Research Division Appalachian Regional Commission Washington, DC Appalachian Regional

County Economic Status and Distressed Areas in the Appalachian Region Kostas Skordas, Director Regional Planning & Research Division Appalachian Regional Commission Washington, DC Appalachian Regional

Community Development Financial Institutions. Fund

equality U.S. Department of the Treasury equality INVESTMENT Community Development Financial Institutions invest neighborhood Fund New Markets Tax Credits: 2003 Allocation Application CDFI Fund Mission

equality U.S. Department of the Treasury equality INVESTMENT Community Development Financial Institutions invest neighborhood Fund New Markets Tax Credits: 2003 Allocation Application CDFI Fund Mission

MEDICAID BUY-IN PROGRAMS

MEDICAID BUY-IN PROGRAMS Under federal law, states have the option of creating Medicaid buy-in programs that enable employed individuals with disabilities who make more than what is allowed under Section

MEDICAID BUY-IN PROGRAMS Under federal law, states have the option of creating Medicaid buy-in programs that enable employed individuals with disabilities who make more than what is allowed under Section

Demographic and Economic Profile. New Jersey. Updated December 2006

Demographic and Economic Profile New Jersey Updated December 2006 Metro and Nonmetro Counties in New Jersey Based on the most recent listing of core based statistical areas by the Office of Management

Demographic and Economic Profile New Jersey Updated December 2006 Metro and Nonmetro Counties in New Jersey Based on the most recent listing of core based statistical areas by the Office of Management

An introduction to the Community Reinvestment Act. John Meeks Atlanta Region FDIC Community Affairs

An introduction to the Community Reinvestment Act John Meeks Atlanta Region FDIC Community Affairs What is the CRA? CRA stands for: The Community Reinvestment Act of 1977 The regulations implementing the

An introduction to the Community Reinvestment Act John Meeks Atlanta Region FDIC Community Affairs What is the CRA? CRA stands for: The Community Reinvestment Act of 1977 The regulations implementing the

LEGISLATIVE PRIORITIES

HUD SECTION 108 The Section 108 Program allows grantees of the Community Development Block Grant (CDBG) Program to borrow Federally-guaranteed funds for community development purposes. Section 108 borrowers

HUD SECTION 108 The Section 108 Program allows grantees of the Community Development Block Grant (CDBG) Program to borrow Federally-guaranteed funds for community development purposes. Section 108 borrowers

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE February 22, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Orange County Trust Company RSSD No. 176101 212 Dolson Avenue Middletown, NY 10940 FEDERAL RESERVE BANK OF NEW YORK

PUBLIC DISCLOSURE February 22, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Orange County Trust Company RSSD No. 176101 212 Dolson Avenue Middletown, NY 10940 FEDERAL RESERVE BANK OF NEW YORK

Tassistance program. In fiscal year 1999, it 20.1 percent of all food stamp households. Over

CHARACTERISTICS OF FOOD STAMP HOUSEHOLDS: FISCAL YEAR 1999 (Advance Report) UNITED STATES DEPARTMENT OF AGRICULTURE OFFICE OF ANALYSIS, NUTRITION, AND EVALUATION FOOD AND NUTRITION SERVICE JULY 2000 he

CHARACTERISTICS OF FOOD STAMP HOUSEHOLDS: FISCAL YEAR 1999 (Advance Report) UNITED STATES DEPARTMENT OF AGRICULTURE OFFICE OF ANALYSIS, NUTRITION, AND EVALUATION FOOD AND NUTRITION SERVICE JULY 2000 he

# of Credit Unions As of March 31, 2011

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

2018 TOP POOL EXECUTIVE COMPENSATION & BENEFITS ANALYSIS REDACTED: Data provided to participating pools

2018 TOP POOL EXECUTIVE COMPENSATION & BENEFITS ANALYSIS TABLE OF CONTENTS Introduction............................. 3 Anticipated retirement of top executives............. 4 Salary findings...........................

2018 TOP POOL EXECUTIVE COMPENSATION & BENEFITS ANALYSIS TABLE OF CONTENTS Introduction............................. 3 Anticipated retirement of top executives............. 4 Salary findings...........................

Demographic and Economic Profile. North Dakota. Updated June 2006

Demographic and Economic Profile North Dakota Updated June 2006 Metro and Nonmetro Counties in North Dakota Based on the most recent listing of core based statistical areas by the Office of Management

Demographic and Economic Profile North Dakota Updated June 2006 Metro and Nonmetro Counties in North Dakota Based on the most recent listing of core based statistical areas by the Office of Management

Investing in Opportunity Zones

Investing in Opportunity Zones for the 2018 Defense Communities National Summit Gregory Clements Partner, Dover Novogradac & Company LLP gregory.clements@novoco.com Taxpayers can get capital gains tax

Investing in Opportunity Zones for the 2018 Defense Communities National Summit Gregory Clements Partner, Dover Novogradac & Company LLP gregory.clements@novoco.com Taxpayers can get capital gains tax

March Karen Cunnyngham Amang Sukasih Laura Castner

Empirical Bayes Shrinkage Estimates of State Supplemental Nutrition Assistance Program Participation Rates in 2009-2011 for All Eligible People and the Working Poor March 2014 Karen Cunnyngham Amang Sukasih

Empirical Bayes Shrinkage Estimates of State Supplemental Nutrition Assistance Program Participation Rates in 2009-2011 for All Eligible People and the Working Poor March 2014 Karen Cunnyngham Amang Sukasih

Exploring the Geography of College Opportunity

E D U C A T I O N P O L I C Y P R O G R A M Exploring the Geography of College Opportunity Data and Methodology Kristin Blagg and Victoria Rosenboom April 2018 Data Our analysis builds on the work we completed

E D U C A T I O N P O L I C Y P R O G R A M Exploring the Geography of College Opportunity Data and Methodology Kristin Blagg and Victoria Rosenboom April 2018 Data Our analysis builds on the work we completed

Community Development Financial Institutions (CDFIs)

") Community Development Financial Institutions (CDFIs) o Private financial institutions focused on serving low income communities o Combine financial & development services o Raise capital with interest

Community Development Financial Institutions (CDFIs) o Private financial institutions focused on serving low income communities o Combine financial & development services o Raise capital with interest

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING 1 FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017 GCIR PROVIDES A FORUM FOR FUNDERS TO: Learn about current issues through in-depth

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING 1 FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017 GCIR PROVIDES A FORUM FOR FUNDERS TO: Learn about current issues through in-depth

American Views on Payday Loans. Survey of 1,000 Christians in 30 states Sponsored by: Faith for Just Lending

American Views on Payday Loans Survey of 1,000 Christians in 30 states Sponsored by: Faith for Just Lending 2 Methodology The online survey of Americans in 30 states was conducted February 5-17, 2016 The

American Views on Payday Loans Survey of 1,000 Christians in 30 states Sponsored by: Faith for Just Lending 2 Methodology The online survey of Americans in 30 states was conducted February 5-17, 2016 The

Federal Employees Retirement System: Summary of Recent Trends

Federal Employees Retirement System: Summary of Recent Trends Katelin P. Isaacs Analyst in Income Security January 11, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

Federal Employees Retirement System: Summary of Recent Trends Katelin P. Isaacs Analyst in Income Security January 11, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

In Baltimore City today, 20% of households live in poverty, but more than half of the

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Unionization Trends in Ohio and the U.S.

February, 2011 Unionization Trends in Ohio and the U.S. Prepared by Felicia Bernardini, MPA,SPHR Maria L. Mone, JD, MPA The Ohio State University The John Glenn School of Public Affairs Management Development

February, 2011 Unionization Trends in Ohio and the U.S. Prepared by Felicia Bernardini, MPA,SPHR Maria L. Mone, JD, MPA The Ohio State University The John Glenn School of Public Affairs Management Development

Kentucky , ,349 55,446 95,337 91,006 2,427 1, ,349, ,306,236 5,176,360 2,867,000 1,462

TABLE B MEMBERSHIP AND BENEFIT OPERATIONS OF STATE-ADMINISTERED EMPLOYEE RETIREMENT SYSTEMS, LAST MONTH OF FISCAL YEAR: MARCH 2003 Beneficiaries receiving periodic benefit payments Periodic benefit payments

TABLE B MEMBERSHIP AND BENEFIT OPERATIONS OF STATE-ADMINISTERED EMPLOYEE RETIREMENT SYSTEMS, LAST MONTH OF FISCAL YEAR: MARCH 2003 Beneficiaries receiving periodic benefit payments Periodic benefit payments

Demographic and Economic Trends in Rural America

Demographic and Economic Trends in Rural America John Cromartie Geographer, ERS-USDA Tom Hertz Economist, ERS-USDA Lorin Kusmin Economist, ERS-USDA Presentation for HUD Rural Gateway Peer-to-Peer Call

Demographic and Economic Trends in Rural America John Cromartie Geographer, ERS-USDA Tom Hertz Economist, ERS-USDA Lorin Kusmin Economist, ERS-USDA Presentation for HUD Rural Gateway Peer-to-Peer Call

PROGRESS SUMMARY First Quarter 2018

PROGRESS SUMMARY Catalyst Corporate is pleased to report continued progress during the first quarter of 2018. Not only has Catalyst Corporate met the broad objectives of its original business plan, but

PROGRESS SUMMARY Catalyst Corporate is pleased to report continued progress during the first quarter of 2018. Not only has Catalyst Corporate met the broad objectives of its original business plan, but

ASSEMBLY BILL No. 643

AMENDED IN ASSEMBLY JANUARY, 0 AMENDED IN ASSEMBLY APRIL, 0 california legislature 0 regular session ASSEMBLY BILL No. Introduced by Assembly Member Davis February, 0 An act to amend Section. of, and to

AMENDED IN ASSEMBLY JANUARY, 0 AMENDED IN ASSEMBLY APRIL, 0 california legislature 0 regular session ASSEMBLY BILL No. Introduced by Assembly Member Davis February, 0 An act to amend Section. of, and to

State Corporate Income Tax Collections Decline Sharply

Corporate Income Tax Collections Decline Sharply Nicholas W. Jenny and Donald J. Boyd The Rockefeller Institute Fiscal News: Vol. 1, No. 3 July 26, 2001 According to a report from the Congressional Budget

Corporate Income Tax Collections Decline Sharply Nicholas W. Jenny and Donald J. Boyd The Rockefeller Institute Fiscal News: Vol. 1, No. 3 July 26, 2001 According to a report from the Congressional Budget

Health Coverage for the Black Population Today and Under the Affordable Care Act

fact sheet Health Coverage for the Black Population Today and Under the Affordable Care Act July 2013 As of 2011, 37 million individuals living in the United States identified as Black or African American.

fact sheet Health Coverage for the Black Population Today and Under the Affordable Care Act July 2013 As of 2011, 37 million individuals living in the United States identified as Black or African American.

Demographic and Economic Profile. Kentucky. Updated June 2006

Demographic and Economic Profile Kentucky Updated June 2006 Metro and Nonmetro Counties in Kentucky Based on the most recent listing of core based statistical areas by the Office of Management and Budget

Demographic and Economic Profile Kentucky Updated June 2006 Metro and Nonmetro Counties in Kentucky Based on the most recent listing of core based statistical areas by the Office of Management and Budget

# of Credit Unions As of September 30, 2011

# of Credit Unions # of Credit Unions # of Credit Unions As of September 30, 2011 8,400 8,200 8,000 7,800 7,600 7,400 7,200 8,332 8,065 7,794 7,556 7,325 7,000 6,800 9,000 8,000 7,000 6,000 5,000 4,000

# of Credit Unions # of Credit Unions # of Credit Unions As of September 30, 2011 8,400 8,200 8,000 7,800 7,600 7,400 7,200 8,332 8,065 7,794 7,556 7,325 7,000 6,800 9,000 8,000 7,000 6,000 5,000 4,000

Tyler Area Economic Overview

Tyler Area Economic Overview Demographic Profile. 2 Unemployment Rate. 4 Wage Trends. 4 Cost of Living Index...... 5 Industry Clusters. 5 Occupation Snapshot. 6 Education Levels 7 Gross Domestic Product

Tyler Area Economic Overview Demographic Profile. 2 Unemployment Rate. 4 Wage Trends. 4 Cost of Living Index...... 5 Industry Clusters. 5 Occupation Snapshot. 6 Education Levels 7 Gross Domestic Product

Demographic and Economic Profile. Delaware. Updated December 2006

Demographic and Economic Profile Delaware Updated December 2006 Metro and Nonmetro Counties in Delaware Based on the most recent listing of core based statistical areas by the Office of Management and

Demographic and Economic Profile Delaware Updated December 2006 Metro and Nonmetro Counties in Delaware Based on the most recent listing of core based statistical areas by the Office of Management and

Providing Capital Building Communities Creating Impact

Providing Capital Building Communities Creating Impact FY 2005 Data Fifth Edition Community Development Financial Institutions A Publication of the CDFI Data Project This report is a product of the CDFI

Providing Capital Building Communities Creating Impact FY 2005 Data Fifth Edition Community Development Financial Institutions A Publication of the CDFI Data Project This report is a product of the CDFI

The CDFI Banking Sector: 2011 Annual Report on Financial and Social Performance

The CDFI Banking Sector: 2011 Annual Report on Financial and Social Performance Table of Contents I. Executive Summary...1 II. Introduction...3 III. Financial Performance of CDFI Banks... 4 Balance Sheet

The CDFI Banking Sector: 2011 Annual Report on Financial and Social Performance Table of Contents I. Executive Summary...1 II. Introduction...3 III. Financial Performance of CDFI Banks... 4 Balance Sheet

Exploring the Geography of College Opportunity

E D U C A T I O N P O L I C Y P R O G R A M Exploring the Geography of College Opportunity Data and Methodology Kristin Blagg and Victoria Rosenboom April 2018 (updated May 2018) Data Our analysis builds

E D U C A T I O N P O L I C Y P R O G R A M Exploring the Geography of College Opportunity Data and Methodology Kristin Blagg and Victoria Rosenboom April 2018 (updated May 2018) Data Our analysis builds

UPDATED BRIEF WITH 2016 DATA

Substantial Increases in AI/AN Enrollment in Medicaid Expansion s and Ongoing Potential for Additional Increases in AI/AN Enrollment, Particularly in Non Medicaid Expansion s 1 UPDATED BRIEF WITH 2016

Substantial Increases in AI/AN Enrollment in Medicaid Expansion s and Ongoing Potential for Additional Increases in AI/AN Enrollment, Particularly in Non Medicaid Expansion s 1 UPDATED BRIEF WITH 2016

MINIMUM WAGE WORKERS IN HAWAII 2013

WEST INFORMATION OFFICE San Francisco, Calif. For release Wednesday, June 25, 2014 14-898-SAN Technical information: (415) 625-2282 BLSInfoSF@bls.gov www.bls.gov/ro9 Media contact: (415) 625-2270 MINIMUM

WEST INFORMATION OFFICE San Francisco, Calif. For release Wednesday, June 25, 2014 14-898-SAN Technical information: (415) 625-2282 BLSInfoSF@bls.gov www.bls.gov/ro9 Media contact: (415) 625-2270 MINIMUM

TECHNICAL REPORT NO. 11 (5 TH EDITION) THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION

THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION") TECHNICAL REPORT NO. 11 (5 TH EDITION) THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT 208903 SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION KRY/WJS/lgh 12/17/12 203905 SEWRPC Technical

TECHNICAL REPORT NO. 11 (5 TH EDITION) THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT 208903 SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION KRY/WJS/lgh 12/17/12 203905 SEWRPC Technical

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE March 10, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Tioga State Bank RSSD No. 910118 1 Main Street P.O. Box 386 Spencer, NY 14883 FEDERAL RESERVE BANK OF NEW YORK 33 LIBERTY

PUBLIC DISCLOSURE March 10, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Tioga State Bank RSSD No. 910118 1 Main Street P.O. Box 386 Spencer, NY 14883 FEDERAL RESERVE BANK OF NEW YORK 33 LIBERTY

PUBLIC DISCLOSURE. June 4, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION. Utah Independent Bank RSSD #

PUBLIC DISCLOSURE June 4, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Utah Independent RSSD # 256179 55 South State Street Salina, Utah 84654 Federal Reserve of San Francisco 101 Market Street

PUBLIC DISCLOSURE June 4, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Utah Independent RSSD # 256179 55 South State Street Salina, Utah 84654 Federal Reserve of San Francisco 101 Market Street

Key Facts: NATIONAL WOMEN S LAW CENTER FACT SHEET JAN 2018

NATIONAL WOMEN S LAW CENTER FACT SHEET JAN 2018 WORKPLACE JUSTICE PUBLIC SECTOR UNIONS PROMOTE ECONOMIC SECURITY AND EQUALITY FOR WOMEN Kayla Patrick Public sector unions are crucial to the economic security

NATIONAL WOMEN S LAW CENTER FACT SHEET JAN 2018 WORKPLACE JUSTICE PUBLIC SECTOR UNIONS PROMOTE ECONOMIC SECURITY AND EQUALITY FOR WOMEN Kayla Patrick Public sector unions are crucial to the economic security

Basic Economic Security in the United States: How Much Income Do Working Adults Need in Each State?

IWPR R590 October 2018 Basic Economic Security in the United States: How Much Income Do Working Adults Need in Each State? Economic security is a critical part of the overall health and well-being of women,

IWPR R590 October 2018 Basic Economic Security in the United States: How Much Income Do Working Adults Need in Each State? Economic security is a critical part of the overall health and well-being of women,

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation UPDATED July 2014 This chapter looks at the percentage of American workers who work for an employer who sponsors

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation UPDATED July 2014 This chapter looks at the percentage of American workers who work for an employer who sponsors

THE HOME ENERGY AFFORDABILITY GAP 2017

TOTAL US $38,597,642,593 $47,648,609,571 123.4 The Index (2 nd Series) indicates the extent to which the has increased between the base year and the current year. In the total United States this Index

TOTAL US $38,597,642,593 $47,648,609,571 123.4 The Index (2 nd Series) indicates the extent to which the has increased between the base year and the current year. In the total United States this Index

Demographic and Economic Profile. New Mexico. Updated June 2006

Demographic and Economic Profile New Mexico Updated June 2006 Metro and Nonmetro Counties in New Mexico Based on the most recent listing of core based statistical areas by the Office of Management and

Demographic and Economic Profile New Mexico Updated June 2006 Metro and Nonmetro Counties in New Mexico Based on the most recent listing of core based statistical areas by the Office of Management and

CRA TOOLKIT. Resources to use in developing and implementing a CRA strategy for your bank.

CRA TOOLKIT Resources to use in developing and implementing a CRA strategy for your bank. Outline l Supervisory agency & other regulatory resources l Assessment area and geographic data resources l Performance

CRA TOOLKIT Resources to use in developing and implementing a CRA strategy for your bank. Outline l Supervisory agency & other regulatory resources l Assessment area and geographic data resources l Performance

Access to Care and the Economic Impact of Community Health Centers

Access to Care and the Economic Impact of Community Health Centers National Congress on the Un and Underinsured Monday, December 10, 2007 3:30-4:30 The Robert Graham Center Community Health Centers What

Access to Care and the Economic Impact of Community Health Centers National Congress on the Un and Underinsured Monday, December 10, 2007 3:30-4:30 The Robert Graham Center Community Health Centers What

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE January 26, 2009 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Amboy Bank RSSD No. 9807 3590 Highway 9 Old Bridge, NJ 08859 Federal Reserve Bank of New York 33 Liberty Street New

PUBLIC DISCLOSURE January 26, 2009 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Amboy Bank RSSD No. 9807 3590 Highway 9 Old Bridge, NJ 08859 Federal Reserve Bank of New York 33 Liberty Street New

CC:PA:LPD:PR (Notice ) Room 5203 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington, DC

Room 5203 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington, DC") CC:PA:LPD:PR (Notice 2006-60) Room 5203 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington, DC 20044 August 31, 2006 To whom it may concern: Opportunity Finance Network appreciates the

CC:PA:LPD:PR (Notice 2006-60) Room 5203 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington, DC 20044 August 31, 2006 To whom it may concern: Opportunity Finance Network appreciates the

Annotated CRA CHAT Tables

SUMMARY REPORTS Median Family Income Report 2 Assessment Area Summary Report 2 Loan Type Selection Report 3 Loan Records Summary Report 4 Duplicate Loan Details Report 5 Outside Assessment Area Summary

SUMMARY REPORTS Median Family Income Report 2 Assessment Area Summary Report 2 Loan Type Selection Report 3 Loan Records Summary Report 4 Duplicate Loan Details Report 5 Outside Assessment Area Summary

Papers presented at the ICES-III, June 18-21, 2007, Montreal, Quebec, Canada

Future Developments In the Bureau of Labor Statistics Business Employment Dynamics Data By Kristin Fairman and Sheryl Konigsberg Division of Administrative Statistics and Labor Turnover Bureau of Labor

Future Developments In the Bureau of Labor Statistics Business Employment Dynamics Data By Kristin Fairman and Sheryl Konigsberg Division of Administrative Statistics and Labor Turnover Bureau of Labor

CRA History. The Community Reinvestment Act passage did two things:

CRA History The Community Reinvestment Act passage did two things: The discussion of CRA brought light to the illegal practice of redlining. Required regulated financial institutions to help meet the credit

CRA History The Community Reinvestment Act passage did two things: The discussion of CRA brought light to the illegal practice of redlining. Required regulated financial institutions to help meet the credit

Doing Well by Doing Good. Successful Business Models & Key Elements of Business Plans for CDFI Credit Unions

Doing Well by Doing Good Successful Business Models & Key Elements of Business Plans for CDFI Credit Unions Today A goal without a plan is just a wish Antoine de Saint-Exupéry Part 1: How to Succeed in

Doing Well by Doing Good Successful Business Models & Key Elements of Business Plans for CDFI Credit Unions Today A goal without a plan is just a wish Antoine de Saint-Exupéry Part 1: How to Succeed in