For personal use only

|

|

|

- Lesley Casey

- 5 years ago

- Views:

Transcription

1

2

3

4 4

5 5

6 6

7

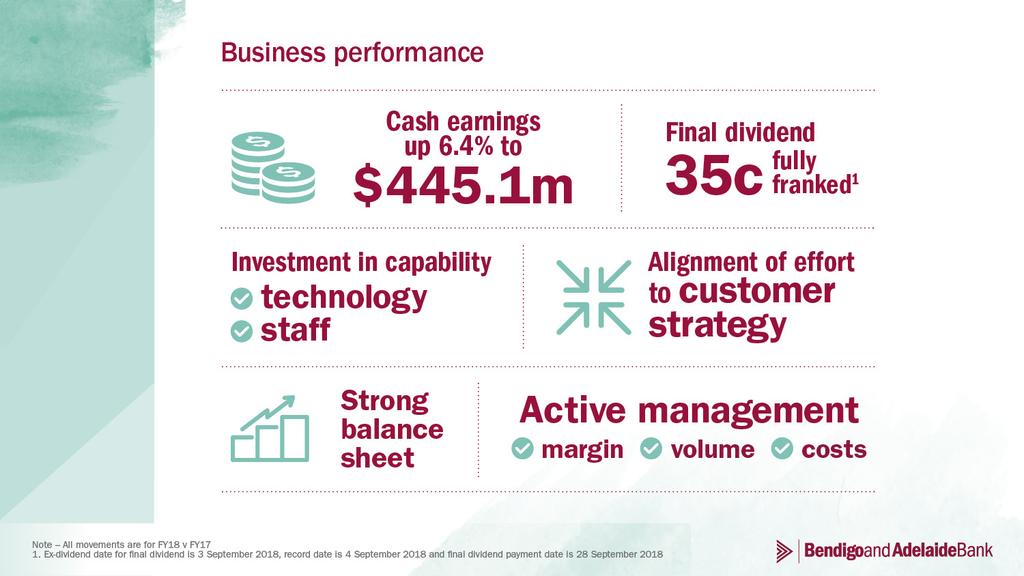

8 Financial performance Statutory earnings ($m) +1.1% Cash earnings ($m) +6.4% Cash earnings per share ( ) +4.1% FY16 FY17 FY18 FY16 FY17 FY18 FY16 FY17 FY18 Return on equity 1 (%) +13 bps Return on tangible equity 1 (%) -9 bps Cost to income ratio (%) -50 bps FY16 FY17 FY18 FY16 FY17 FY18 FY16 FY17 FY18 1. Cash earnings basis 8

9 Balance sheet and capital Total gross loans ($b) +1.4% Retail deposit funding (%) Jun-16 Jun-17 Jun-18 Jun-16 Jun-17 Jun-18 Common Equity Tier 1 (%) +35 bps Total capital (%) +39 bps Jun-16 Jun-17 Jun-18 Jun-16 Jun-17 Jun-18 9

10 2H18 growth outcomes Total lending growth Housing loan growth Major 5.5% Major 5.8% System 4.8% System 5.1% Regional 4.5% Major 4.8% Major 4.3% BEN 4.7% BEN 4.2% Major 3.4% Major 3.8% Regional 3.0% Regional 3.6% Regional 2.9% Major 2.3% Major 2.6% Total deposit growth Business lending growth Major 4.4% Rural Bank 11.3% Major 3.7% Regional 9.7% System Regional BEN Regional Major Major -2.6% -2.2% -1.9% 1.2% 0.9% 2.0% Regional Major Major BEN 1 System Major Major -1.5% 5.5% 5.1% 4.7% 4.7% 4.3% 7.3% Source: APRA Monthly Banking Statistics June 2018 Note - Data is an annualised growth rate based on a 6 month period (30/06/17 30/06/18) for BEN and Rural Bank 1. Represents total business lending growth including Rural Bank 10

11 Residential mortgage growth $2000m Retail - settlements breakdown 1 $2000m Third Party - settlements breakdown 2 $1500m $1500m $1000m $1000m $500m $500m $m OO PI OO IO INV PI INV IO $m OO PI OO IO INV PI INV IO 2H16 1H17 2H17 1H18 2H18 2H16 1H17 2H17 1H18 2H18 Investor credit growth 10% Investor growth limit Interest only flows 30% Interest Only flows limit 10% 30.0% 8% 6% 4% 25.0% 20.0% 15.0% 10.0% 2% 5.0% 0% Jun-17 Sep-17 Dec-17 Mar-18 Jun % Jun-17 Sep-17 Dec-17 Mar-18 Jun Loan settlements for Bendigo Bank retail banking excluding Delphi Bank and line of credits 2. Loan settlements for Adelaide Bank excluding Alliance Bank and line of credits 11

12 Cash earnings growth Cash earnings up 6.4% FY18 ($m) FY17 ($m) FY18 v FY17 2H18 v 2H17 Strong annual margin performance +14bps Significantly lower trading book income 2H18 cost increase as expected Improved credit costs in 2H18 leading to lower annual BDD Net interest income $1,323.6 $1, % +4.5% Other income $281.2 $309.7 (9.2%) (8.5%) Homesafe 1 $11.3 $ % +2.0% Cash earnings ($m) Operating expenses $900.9 $ % +4.4% Credit $70.6 $71.8 (1.7%) (24.1%) Cash earnings (after tax) $445.1 $ % +2.3% 2H16 1H17 2H17 1H18 2H18 1. Homesafe net realised income after tax 12

13 Net interest margin Historical NIM +14bps Active management of margin / volume balance for both lending and deposits June 2018 exit margin of 2.35% Mortgage repricing in late July 2018 to offset higher funding costs Front book discounts will continue to challenge margin 1H17 2H17 1H18 2H18 FY17 BEN Community Bank & Alliance Bank share FY18 NIM impacts 1H18 2H18 Front book/back book repricing (4bps) (4bps) Variable mortgage repricing 5bps - Hedging costs 2bps 1bp Treasury liquids - 1bp Retail deposit repricing 4bps 7bps Wholesale deposit repricing 1bp (4bps) Funding mix 1bp 1bp Equity contribution 1bp (1bp) Total 10bps 1bp NIM monthly movement Monthly NIM 3 Month rolling NIM Jun 16 Dec 16 Jun 17 Dec 17 Jun 18 13

14 Other income Lower ATM and transaction fees Commission 2H18 stronger with flows into superannuation and managed funds Trading book income lower given the stable interest rate environment in the first half, second half impacted by elevated cash/bills spread Continued erosion of other income is evident across the industry FY18 ($m) FY17 ($m) FY18 v FY17 2H18 v 1H18 Fee income $167.9 $172.2 (2.5%) (1.8%) Commissions $71.7 $72.7 (1.4%) +3.7% Foreign exchange income $18.8 $ % +4.3% Other income ($m) Trading book income $0.8 $19.8 (96.0%) (175.0%) Other $22.0 $27.0 (18.5%) (19.7%) Total other income $281.2 $309.7 (9.2%) (5.4%) 2H16 1H17 2H17 1H18 2H18 14

15 Cost to income 50bp improvement over FY18 in challenging environment Cost to income ratio (%) Increased cost of compliance and regulation 58.1 Staff costs up 3.5% for FY18 due to annual salary increases and reduction in project capitalisation -50bps Software amortisation up $7m on prior year Continue to actively manage costs 2H18 negative jaws outcome driven by lower revenue FY16 FY17 FY18 Operating expense (cash $m) CAGR = 2.1% Jaws momentum (%) 4.0% 4.1% % 0.4% 3.2% % FY16 FY17 FY18 1H17 2H17 1H18 2H18 Income growth Expense growth 15

16 Bad and doubtful debts BDD charge 11bps of gross loans, 10bps excluding Great Southern in line with four year average Bad and doubtful debts composition ($m) 46.3 New impaired loans in 2H18 are being actively managed and provisions are based on recent valuations Collective provision reduced as Great Southern portfolio runs off and reduction in higher risk lending portfolios Provision coverage of 92% Agribusiness provisions continue to remain low All core portfolios remain well secured, with low LVRs (0.6) 2H17 1H18 2H18 Local Connection Partner Connection Agribusiness Great Southern 2.7 Provisions for doubtful debts ($m) BDD / loans 1.00% % % % Jun 16 Dec 16 Jun 17 Dec 17 Jun 18 General Collective Specific 0.20% 0.00% FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 BEN Major Banks Regional peers 16

17 Arrears remain benign 1.6% Residential Loan Arrears 3.0% Business Loan Arrears 1.2% 0.8% 0.4% 2.0% 1.0% 0.0% Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Res 90d+ 0.0% Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Bus 90d+ Consumer Loan Arrears Home Loans 90+ days past due - by state 1 3.0% 2.0% 1.0% 0.0% Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 PL 90d+ CC 90d+ 2.0% 1.5% 1.0% 0.5% 0.0% VIC NSW/ACT QLD SA WA Portfolio Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Note - Data excludes commercial arrangement loans 1. Keystart included from Jun-17 17

200.7 57.5 (1.1) Local Connection ($m) (13.5) (16.9) (6.0) 213.5 213.5 Managed funds up 9.")

18 Business segment performance (cash earnings) All lending markets remain highly competitive Significant margin improvement in Local and Partner Connection businesses Extreme price competition in agribusiness lending Full year impact of Agri FMD 100% offset product (c$1.5m) (1.1) Local Connection ($m) (13.5) (16.9) (6.0) Managed funds up 9.6% 1, including Bendigo SmartStart Super up 21% 2 Reduced credit expenses in Partner Connection (Great Southern) and Agribusiness FY17 Net interest income Other income Operating Expenses Credit expenses Tax FY18 Partner Connection ($m) Agribusiness ($m) ( 12.8 ) 16.7 ( 11.9 ) (1.7) 0.4 (1.5) FY17 Net interest income Other income 3 Homesafe Operating expenses Credit expenses Tax FY18 FY17 Net interest income Other income Operating expenses Credit expenses Tax FY18 1. Growth is based on 12 month figures (Jun-17 to Jun-18) 2. Growth is based on 12 month figures (Jun-17 to Jun-18) 3. Homesafe net realised income after tax 18

19 Continued CET1 strength Historical CET1 35bp increase in CET1 since June well positioned to meet unquestionably strong CET1 requirement Organic capital growth reflects strong profitability, stable balance sheet and move to lower risk exposures 8.27 CET1 maintained in 2H18 following stronger asset growth Last RMBS transaction in August 2017 for $750m The new APRA proposals regarding credit risk weights are being evaluated and the Bank has made an individual submission on the proposals Progress towards Advanced Accreditation is continuing positively with greater clarity expected post finalisation of the new standards Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 CET1 movement - 12 months 1.10 (0.04) ( 0.66 ) (0.05) Jun-17 1 Retained Earnings RWA Dividend (net of DRP) 2 Other Jun Unrealised Homesafe revaluation revenue excluded from increases in retained earnings was 5bps 2. Other includes movement in capitalised expenses, deferred tax assets and intangibles 19

20 Industry leading funding position Funding mix continues to be a strength providing flexibility to fund asset growth and manage margin Historical funding mix Retail call deposit portfolio continues to increase with customer demand for revised product range Increased BBSW spreads impacting cost of wholesale and securitisation funding Industry TD rates trending higher in Q4 23.8% 11.3% 64.9% 6.3% 6.6% 5.7% 13.5% 13.8% 14.1% 80.2% 79.6% 80.2% LCR of 125.6%, NSFR ~109% at 30 June 2018 $500m 5-year senior unsecured deal completed in January 2018 at +105bps Retail deposit composition Jun-09 Jun-17 Dec-17 Jun-18 Retail Wholesale Securitisation Retail call deposit interest rate mix Retail call deposits 24% 26% 0.01% Retail term deposits 53.3% Jun % 51.4% Jun % 6% > 0.01% % > 0.25% % > 1.50% 44% 20

21 AASB 9 $112.8m increase in collective provision due to expected loss model rather than incurred loss model $m AASB 9 Impact on Collective Provision and General Reserve for Credit Losses Increase taken through retained earnings as at 1 July Individually assessed specific provisions process is unchanged Underlying portfolio credit quality unchanged 100 CET1 ratio will decrease by 8bps on 1 July AASB139 AASB9 25 Provision coverage % 0.47% 0 AASB139 AASB9 Collective Provision General Reserve for Credit Losses 1. Provision coverage is collective provision divided by credit risk weighted assets 21

22

23 23

24 24

25 25

26 26

27

28

29 29

30 30

31 31

32 32

33 Future proofing technology Improving customer choice and convenience Creating safe and secure online presence Ensuring we remain relevant Implemented agile way of working Focusing on simplification and innovation Continuing investment in cloud Maintaining a strong information security program Capitalised software ($m) ( 20.6 ) ( 28.0 ) Jun-16 Jun-17 Jun-18 Additions Amortisation 33

34 Tic:Toc The world s first instant home loan TM $600 Application Pipeline ($m) $500 $400 $300 Significant growth since July 2017 launch: $1.36b value of submitted applications $170m loan portfolio Successfully validated, approved and provided home loan documentation for customers in as little as 1 hour A more responsible way to lend: $200 $100 $ Jul-17 Sep-17 Nov-17 Jan-18 Mar-18 May-18 Jul-18 Settled Awaiting settlement Approved Awaiting info 35.0% 30.0% Comparative borrower Debt to Income Automated credit decisioning and exception based underwriting is not only more efficient, but more responsible Digital validation ensures more accurate verification of financials 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% 0x 1x 2x 3x 4x 5x 6x 7x 8x 9x 10x Tic:Toc Data provided to BRC by a major bank 1 1. BRC refers to the Banking Royal Commission Tic:Toc.com.au 34

35 Up Super powered banking Australia s first fully licenced and all-in-app mobile banking platform Testing began in Oct % up-time Public beta live in Aug customers Public launch planned for Oct 2018 Up brings a more human-focused technology solution to market, as a mobile-first banking platform helping digital natives gain financial independence and enrich their financial life up.com.au 35

36 36

37 Funding Retail deposit balances ($bn) $m 1,400 1,200 Term funding maturity profile 1, Jun-16 Dec-16 Jun-17 Dec-17 Jun Retail call deposits Retail term deposits Term senior debt Sub-debt EMTN 100% Retail term deposit retention rate 1 Wholesale funding composition 2 90% 2% 9% 80% 70% 42% Jun-18 46% 60% 1% 50% Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 ST domestic ST offshore LT domestic LT offshore Sub-Debt Note Reclassification of some middle market deposits from Retail to Whole has reduced the retail deposit ratios: Dec-16 by 2.7% and June-16 by 2.4% 1.Company data 2.Wholesale funding composition excludes financial markets NCD s 37

38 Key capital ratios 1H17 2H17 1H18 2H18 Common Equity Tier % 8.27% 8.61% 8.62% Additional Tier % 2.22% 2.37% 2.34% Tier % 10.49% 10.98% 10.96% Tier % 1.97% 2.00% 1.89% Total capital 12.20% 12.46% 12.98% 12.85% Total Risk weighted assets $38.3b $38.1b $37.7b $38.3b Group Economic Capital 1 ($b) Group Standardised Regulatory Capital ($b) S&P RAC Ratio % % 9.1% 8.9% 7.9% Credit Risk Op Risk Other Market Risk Business Risk Credit Risk Market Risk Op Risk BEN Major 1 Major 2 Major 3 Major 4 1. Calculated using a combination of internal models and standardised measures 2. S&P RAC ratio, Major 2, 3 & 4 as at 30 Sept 2017, BEN & Major 1 as at 30 June

39 Stress testing scenarios The Bank has a comprehensive stress testing framework in place which has been operational since 2010 and is managed by a dedicated stress testing team within Group Risk Stress testing is undertaken annually at the Group level (across all risk types) and quarterly at the credit portfolio level Impact of stress is assessed against capital, liquidity and other key ratios Key Assumptions Annual enterprise wide stress test GDP negative growth 2-3 qtrs Key Assumptions Quarterly portfolio stress test Retail Portfolios default rates increased 4x (peak to trough) Unemployment >10% over the term of the scenario Retail Portfolios -national residential property prices fall 30% Cash rate falls (0.1% at last test) National residential property prices fall 30% (greater in certain states) Stressed PDs for residential investor are assumed to be 10% higher than owner occupier Stress test period is 5 years LMI payouts assumed at 70% (from >95%) Non-retail portfolios - default rates increased by a factor of 1 to 8x (peak to trough) Non-retail portfolios security values discounted by up to 50% Margin lending portfolio single stock failure scenario Margin lending portfolio severe market shock (25% & 35% single day decline) Rural Portfolios default rates by a factor of 1 to 8x (peak to trough) Collateral value for construction falls 50% Rural portfolios security values discounted by up to 50% Wholesale funding markets (incl securitisation) are shut in early years of scenario Rural Portfolios adhoc stress tests are periodically undertaken based on agri outlook (commodity price, climatic conditions) 39

40 Liquidity Liquidity coverage ratio 3 month average ($b) Sep-17 Dec-17 Mar-18 Jun-18 High quality liquid assets Committed liquidity facility $b Net stable funding ratio (NSFR) 109.2% as at 30 June 2018 $49.7b Wholesale funding & other $45.5b 40 Total LCR liquid assets Other loans Customer deposits Wholesale funding Retail & SME deposits 20 Other flows Residential mortgages <35% Net cash outflows LCR 127% 124% 131% 123% 5 0 Capital Available stable funding Liquids & other assets Required stable funding 40

1H17 2H17 1H18 2H18 Offset account portfolio ($b) 40.0 2.6 2.6 39.0 2.3 2.4 38.0 37.")

41 Residential lending Total residential loan approval ($m) Settlements 2 ($b) 9.1 8,711 5,419 5,881 5, H17 2H17 1H18 2H18 Residential portfolio balance 1 ($b) 1H17 2H17 1H18 2H18 Offset account portfolio ($b) Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 1H17 2H17 1H18 2H18 Source: Company data, APRA statistics June Based on APRA statistics (loans to households : owner occupied & investment and housing loans securitised) 2. Settlements include LaTrobe and business lending 41

42 Residential LVR breakdown at origination Proportion of portfolio with LVR 80% is 77% Residential LVR breakdown Average LVR has reduced to 59% (based on property value at origination) Dynamic LVR reflects an even lower portfolio average LVR 0% - 60% 31% 60%-80% 46% 80%-90% 16% 16% 7% Jun-18 31% 90%+ 7% 46% 40.0% 20.0% 0.0% Residential loan-to-value profile 77% of portfolio with LVR 80% 0% - 60% 60%-80% 80%-90% 90%+ Jun-16 Dec-16 Jun-17 Dec-17 Jun % 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% Residential Mortgage - portfolio and flow 1 VIC NSW / ACT SA / NT QLD WA TAS OVERSEAS Portfolio Flow Note - Breakdown of LVRs for by residential mortgages at 30 June 2018 by origination 1. Contains all Local Connection and Partner Connection residential mortgage lending. Overseas removed from graph due to small percentage (Portfolio 0.5%, flow 0.5%) 42

43 Secure and low risk loan portfolios BEN loan composition 1 Residential mortgages Commercial mortgages 71.4% Listed securities & managed funds Unsecured Other 23.7% 2.7% 1.6% 0.5% 2% 3% 3% 4% 8% 11% 27% Commercial breakdown Agri, forestry & fishing Rental, hiring & real estate Construction 43% Health Care & Social assist Retail trade Finance & insurance Accom & food services Other 98.4% secured 97.9% secured by mortgages and listed securities Residential mortgages average LVR 59% 63% owner occupied Margin Lending 78% of portfolios hold 4 stocks Average LVR 35% Residential Mortgages 2,3 Jun-18 Dec-17 Retail mortgages 59% 58% Third Party mortgages 41% 42% Lo Doc 2% 2% Owner occupied 63% 63% Owner occupied P&I 82% 79% Owner occupied I/O 18% 21% Investment 37% 37% Investment P&I 42% 38% Investment I/O 58% 62% Residential Mortgages 2,3 Jun-18 Dec-17 Mortgages with LMI 23% 27% Average LVR 59% 61% Average loan balance $231k $225k 90+ days past due - exc arrangements 0.5% 0.5% Impaired loans 0.11% 0.13% Specific provisions 0.03% 0.03% Loss rate 0.02% 0.01% Variable 74% 72% Fixed 26% 28% 1. Loan data represented by security as per page 23 in the 4E 2. Loan data represented by purpose 3. Excludes Delphi Bank & Keystart data 43

44 Commercial Loan book portfolio Portfolio Jun-18 Jun-17 VIC Melbourne 33% 34% VIC other 14% 13% NSW Sydney 6% 6% NSW other 4% 3% QLD Brisbane 4% 4% QLD other 6% 6% QLD - Gold Coast 2% 1% 1.40% 1.20% 1.00% 0.80% 0.60% 0.40% 0.20% 0.00% Business arrears by state ACT NSW QLD SA/NT TAS VIC WA SA 17% 17% WA 10% 10% Other 1 3% 4% 1. Other includes NT, Tasmania and ACT 44

45 Specific provisions Specific provision balance ($m) Specific provisions breakdown Represented by Local Connection residential mortgages Consumer Business lending Partner Connection residential mortgages Delphi Bank Great Southern Agribusiness Alliance Partners Jun-18 Jun-17 Dec-17 Jun-18 Provision as % of each portfolio s gross loans Local Connection residential mortgages Consumer Business Lending Partner Connection residential mortgages Delphi Bank Great Southern Agribusiness Alliance Partners BEN total June % 0.53% 0.98% 0.06% 0.08% 11.62% 0.20% 0.05% 0.19% June % 0.58% 0.49% 0.06% 0.22% 9.42% 0.22% 0.06% 0.15% Portfolio as % of gross loans 39.6% 1.8% 11.6% 33.1% 3.0% 0.1% 9.5% 1.3% 100% 45

46 Great Southern paying down Great Southern portfolio has paid down significantly and adequately provisioned Past due 90 days of $50.5m 1, down 36% from 30 June 2017 Specific provision of $9.9m 1, down 17% from 30 June 2017 Collective provision of $13.5m 1, reduced by $3m in line with reduction in portfolio $m Great Southern portfolio # Great Southern BDD ($m) Dec-09 Jun-16 Dec-16 Jun-17 Dec-17 Jun Balance (LHS) Borrowers (RHS) 1H17 2H17 1H18 2H Data as at 30 June

47 Agribusiness Lending customer management Agribusiness loan arrears 4.0% 3.0% 49% Jun-18 51% 2.0% 1.0% Elders Rural Bank 0.0% Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Agri 90d+ Agri exposure by industry Agri exposure by state Grain/Sheep/Beef 28.4% VIC 37.2% Grain Sheep/Beef 14.3% 15.6% WA 19.2% Beef 14.2% NSW 15.9% Dairy 10.2% SA/NT 14.9% Sheep Other 7.8% 5.4% QLD 9.8% Hort./Vit. 4.2% TAS 2.9% 47

48 Homesafe investment property portfolio Proceeds on completed contracts continue to exceed pre-overlay values Overlay reflects an assumed 3% increase in property prices for the next 18 months before returning to a long term growth rate of 6% Average annual return on completed contracts since inception is 9.9%, pre funding costs H15 2H15 1H16 2H16 1H17 2H17 1H18 2H18 Homesafe portfolio distribution Homesafe portfolio and funding balance ($m) % Sydney Melbourne -2.33% 1 Jun-18 61% +6.55% Jun 07 Jun 08 Jun 09 Jun 10 Jun 11 Jun 12 Jun 13 Jun 14 Jun 15 Jun 16 Jun 17 Jun 18 Realised - income vs funding costs ($m) Realised income Realised funding costs Portfolio Balance Funding Balance months movement reflects Residex movement between 1 June 2017 and 31 May

49 Homesafe investment property portfolio (statutory earnings) Portfolio overlay ($m) H17 ($m) 2H17 ($m) 1H18 ($m) 2H18 ($m) Profit on sale $1.4 $0.3 $1.0 $ H17 2H17 1H18 2H18 Discount $9.0 $9.4 $10.4 $10.1 Change Total balance Homesafe statutory income contribution ($m) Property revaluations $38.5 $36.4 $30.1 $ Portfolio overlay -$2.5 -$2.1 -$1.9 -$ Total income contribution $46.4 $44.0 $39.6 $15.8 FY15 FY16 FY17 FY18 49

50 Homesafe accounting treatment illustrative example Start of Year 1 End of Year 1 Year 2 Year 3 Year 4 Total Day 1 funding 100,000 Property value 110, , ,000 Homesafe Income 10,000 20,000 (10,000) 5,000 Unrealised funding costs (5,000) (5,000) (5,000) (5,000) Property sold 125,000 Realised profit 25,000 Realised funding costs (20,000) Profit and Loss Unrealised funding costs (NII) (5,000) (5,000) (5,000) (5,000) (20,000) Homesafe revaluation income 10,000 20,000 (10,000) 5,000 25,000 Total statutory earnings before tax 5,000 15,000 (15,000) 0 5,000 Cash earnings adjustments Unrealised funding costs 5,000 5,000 5,000 5,000 20,000 Homesafe revaluation income (10,000) (20,000) 10,000 (5,000) (25,000) Realised income ,000 25,000 Realised funding costs (20,000) (20,000) Total before tax (5,000) (15,000) 15,000 5,000 0 Net cash earnings before tax ,000 5,000 Note for illustrative purposes only 50

2 Significant matched funding leveraged")

51 The Community Bank model 20 th anniversary Over $200m in community contributions 1 since inception enabling tangible economic and social benefits for the communities and our business Community Bank footings ($bn) 2 Significant matched funding leveraged by community partners for major local infrastructure initiatives 321 Community Bank branches, of which over 20% are the last financial institution in the town or suburb Proven, reliable and cost effective distribution strategy Up to 80% of Community Bank profit (after tax) distributed to the community FY15 FY16 FY17 FY18 Loans Deposits 1. Includes total sponsorships, donations and grants 2. Community Bank footing includes Private Franchises (4 branches in total) 51

52 Alliance Bank growth Nova Alliance Bank added in May 2018 Nova included $71m in total loans and deposits and 1,500 new members Alliance Bank delivered 13.6% lending growth in FY18 Alliance Bank loan portfolio balance Alliance Bank deposit portfolio balance Jun-16 Dec-16 Jun-17 Dec-17 Jun Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Total Loans Nova Total Deposits Nova 52

53 Statutory earnings to cash earnings - reconciliation FY18 ($m) FY17 ($m) Statutory Profit after tax $434.5 $429.6 Fair value adjustments $0.8 $1.8 Homesafe unrealised adjustments ($26.8) ($52.2) Hedging/income (costs) ($1.2) $5.6 (Profit)/Loss on sale of business $1.2 ($2.7) Integration costs $5.3 $9.2 Impairment charge/(reversal) $0.4 ($0.9) Operating expenses, includes legal, litigation and compensation costs $13.8 $4.4 Amortisation of intangibles $5.8 $12.4 Cash earnings after tax (sub total) 1 $433.8 $407.2 Homesafe net realised income after tax $11.3 $11.1 Cash earnings after tax $445.1 $ Cash earnings subtotal is equal to cash earnings before Homesafe realised income 53

54

55

Bendigo and Adelaide Bank 2013 half year results

Bendigo and Adelaide Bank 2013 half year results February 18, 2013 1 This document is a presentation of general background information about the Group s activities current at the date of the presentation.

Bendigo and Adelaide Bank 2013 half year results February 18, 2013 1 This document is a presentation of general background information about the Group s activities current at the date of the presentation.

Overview Financial performance Summary & Outlook Appendices. Agenda 3

This document is a presentation of general background information about the Group s activities current at the date of the presentation. It is information in a summary form and no representation or warranty

This document is a presentation of general background information about the Group s activities current at the date of the presentation. It is information in a summary form and no representation or warranty

Investor presentation

FY17 INVESTOR PRESENTATION 1 18 August 2017 Investor presentation FY17 Agenda FY17 INVESTOR PRESENTATION 1. Overview & strategic landscape Melos Sulicich CEO & Managing Director 2. Financial results David

FY17 INVESTOR PRESENTATION 1 18 August 2017 Investor presentation FY17 Agenda FY17 INVESTOR PRESENTATION 1. Overview & strategic landscape Melos Sulicich CEO & Managing Director 2. Financial results David

For personal use only

Appendix 4E Full Year Results For the year ended 30 June 2017 Released 14 August 2017 ABN 11 068 049 178 This report comprises information given to the ASX under listing rule 4.3A THIS PAGE HAS BEEN LEFT

Appendix 4E Full Year Results For the year ended 30 June 2017 Released 14 August 2017 ABN 11 068 049 178 This report comprises information given to the ASX under listing rule 4.3A THIS PAGE HAS BEEN LEFT

FOR THE HALF-YEAR ENDED 28 FEBRUARY Bank of Queensland Limited ABN AFSL No

FOR THE HALF-YEAR ENDED 28 FEBRUARY 2017 Bank of Queensland Limited ABN 32 009 656 740. AFSL No 244616. JON SUTTON Managing Director & CEO ANTHONY ROSE Chief Financial Officer JON SUTTON Managing Director

FOR THE HALF-YEAR ENDED 28 FEBRUARY 2017 Bank of Queensland Limited ABN 32 009 656 740. AFSL No 244616. JON SUTTON Managing Director & CEO ANTHONY ROSE Chief Financial Officer JON SUTTON Managing Director

INVESTOR PRESENTATION

INVESTOR PRESENTATION FULL YEAR FY2018 17 August 2018 AGENDA FY18 INVESTOR PRESENTATION 1. Highlights & strategy Melos Sulicich Managing Director & CEO 2. Financial results David Harradine Chief Financial

INVESTOR PRESENTATION FULL YEAR FY2018 17 August 2018 AGENDA FY18 INVESTOR PRESENTATION 1. Highlights & strategy Melos Sulicich Managing Director & CEO 2. Financial results David Harradine Chief Financial

1Q18 Capital, Funding and Asset Quality Update

200 years proudly supporting Australia 1Q18 Capital, Funding and Asset Quality Update 5 February 2018 This document should be read in conjunction with Westpac s Pillar 3 Report December 2017, incorporating

200 years proudly supporting Australia 1Q18 Capital, Funding and Asset Quality Update 5 February 2018 This document should be read in conjunction with Westpac s Pillar 3 Report December 2017, incorporating

Bendigo and Adelaide Bank

Bendigo and Adelaide Bank FY 2009 Results August 10, 2009 This document is a presentation of general background information about the Group s activities current at the date of the presentation. It is information

Bendigo and Adelaide Bank FY 2009 Results August 10, 2009 This document is a presentation of general background information about the Group s activities current at the date of the presentation. It is information

1H19 RESULTS PRESENTATION

1H19 RESULTS PRESENTATION 11 APRIL 2019 Half year ended 28 February 2019 Anthony Rose Interim CEO Matt Baxby Chief Financial Officer Anthony Rose Interim CEO 2 Niche growth, asset quality and capital remain

1H19 RESULTS PRESENTATION 11 APRIL 2019 Half year ended 28 February 2019 Anthony Rose Interim CEO Matt Baxby Chief Financial Officer Anthony Rose Interim CEO 2 Niche growth, asset quality and capital remain

Bank of Queensland. Full Year Results 31 August 2008

Bank of Queensland Full Year Results 31 August 2008 Agenda Result highlights David Liddy Managing Director & CEO Financial result in detail Ram Kangatharan Group Executive & CFO BOQ Portfolio Ram Kangatharan

Bank of Queensland Full Year Results 31 August 2008 Agenda Result highlights David Liddy Managing Director & CEO Financial result in detail Ram Kangatharan Group Executive & CFO BOQ Portfolio Ram Kangatharan

Bank of Queensland Full year results 31 August Bank of Queensland Limited ABN AFSL No

Bank of Queensland Full year results 31 August 2013 Bank of Queensland Limited ABN 32 009 656 740. AFSL No 244616. Agenda Result overview Stuart Grimshaw Managing Director and CEO Financial detail Anthony

Bank of Queensland Full year results 31 August 2013 Bank of Queensland Limited ABN 32 009 656 740. AFSL No 244616. Agenda Result overview Stuart Grimshaw Managing Director and CEO Financial detail Anthony

ASX Release MONDAY 18 FEBRUARY 2019 WESTPAC 1Q19 UPDATE AND PILLAR 3 REPORT

ASX Release MONDAY 18 FEBRUARY 2019 WESTPAC 1Q19 UPDATE AND PILLAR 3 REPORT Westpac Banking Corporation has today released its Pillar 3 report for December 2018, along with slides providing further detail

ASX Release MONDAY 18 FEBRUARY 2019 WESTPAC 1Q19 UPDATE AND PILLAR 3 REPORT Westpac Banking Corporation has today released its Pillar 3 report for December 2018, along with slides providing further detail

3Q17 Capital, Funding and Asset Quality Update

3Q17 Capital, Funding and Asset Quality Update 21 August 2017 This document should be read in conjunction with Westpac s Pillar 3 Report June 2017, incorporating the requirements of APS330. All comparisons

3Q17 Capital, Funding and Asset Quality Update 21 August 2017 This document should be read in conjunction with Westpac s Pillar 3 Report June 2017, incorporating the requirements of APS330. All comparisons

For personal use only

1Q17 Capital, Funding & Asset Quality Update 21 February 2017 This document should be read in conjunction with Westpac s Pillar 3 Report December 2016, incorporating the requirements of APS330. All comparisons

1Q17 Capital, Funding & Asset Quality Update 21 February 2017 This document should be read in conjunction with Westpac s Pillar 3 Report December 2016, incorporating the requirements of APS330. All comparisons

For personal use only

Appendix 4D Half Year Results For the period ended 31 December 2015 Released 15 February 2016 ABN 11 068 049 178 This report comprises information given to the ASX under listing rule 4.2A. Information

Appendix 4D Half Year Results For the period ended 31 December 2015 Released 15 February 2016 ABN 11 068 049 178 This report comprises information given to the ASX under listing rule 4.2A. Information

3Q16 Capital, Funding & Asset Quality Update (Pillar 3) August Westpac Banking Corporation ABN

August Westpac Banking Corporation ABN") 3Q16 Capital, Funding & Asset Quality Update (Pillar 3) August 2016 Westpac Banking Corporation ABN 33 007 457 141. This document should be read in conjunction with Westpac s Pillar 3 Report June 2016,

3Q16 Capital, Funding & Asset Quality Update (Pillar 3) August 2016 Westpac Banking Corporation ABN 33 007 457 141. This document should be read in conjunction with Westpac s Pillar 3 Report June 2016,

1Q16 Capital & Asset Quality Update (Pillar 3) February 2016

February 2016") 1Q16 Capital & Asset Quality Update (Pillar 3) February 2016 Westpac Banking Corporation ABN 33 007 457 141. This document should be read in conjunction with Westpac s Pillar 3 report for December 2015,

1Q16 Capital & Asset Quality Update (Pillar 3) February 2016 Westpac Banking Corporation ABN 33 007 457 141. This document should be read in conjunction with Westpac s Pillar 3 report for December 2015,

Westpac FY16 Fixed Income Investor Update November 2016

Westpac FY16 Fixed Income Investor Update November 2016 Disclaimer The material contained in this presentation is intended to be general background information on Westpac Banking Corporation ( Westpac

Westpac FY16 Fixed Income Investor Update November 2016 Disclaimer The material contained in this presentation is intended to be general background information on Westpac Banking Corporation ( Westpac

Financial Results for the half year ended 31 December Create a better today DATA PACK RELEASE DATE 14 FEBRUARY 2019

Financial Results for the half year ended 31 December 2018 Create a better today DATA PACK RELEASE DATE 14 FEBRUARY 2019 SUNCORP GROUP LIMITED ABN 66 145 290 124 Michael Cameron CEO & Managing Director

Financial Results for the half year ended 31 December 2018 Create a better today DATA PACK RELEASE DATE 14 FEBRUARY 2019 SUNCORP GROUP LIMITED ABN 66 145 290 124 Michael Cameron CEO & Managing Director

Bendigo and Adelaide Bank Limited ABN

Bendigo and Adelaide Bank Limited For the year ended 30 June 2011 Released 8 August 2011 This report comprises information given to the ASX under listing rule 4.3A CONTENTS 1. APPENDIX 4E: PRELIMINARY

Bendigo and Adelaide Bank Limited For the year ended 30 June 2011 Released 8 August 2011 This report comprises information given to the ASX under listing rule 4.3A CONTENTS 1. APPENDIX 4E: PRELIMINARY

Westpac Banking Corporation

Westpac Banking Corporation David Morgan Chief Executive Officer March 2007 Westpac Banking Corporation at a glance Australia s first bank est. 1817 Top 50 bank globally 1 Consistent earnings growth Strong

Westpac Banking Corporation David Morgan Chief Executive Officer March 2007 Westpac Banking Corporation at a glance Australia s first bank est. 1817 Top 50 bank globally 1 Consistent earnings growth Strong

Suncorp Bank. Debt Investor Presentation. Suncorp Group Limited. November 2015

Suncorp Bank Debt Investor Presentation 1 Suncorp Investor Update Agenda Suncorp Group Group Financial Results & Capital Suncorp Bank APS330 Funding & Liquidity Australian Mortgages 3 5 19 29 34 2 Suncorp

Suncorp Bank Debt Investor Presentation 1 Suncorp Investor Update Agenda Suncorp Group Group Financial Results & Capital Suncorp Bank APS330 Funding & Liquidity Australian Mortgages 3 5 19 29 34 2 Suncorp

Bendigo and Adelaide Bank Limited ABN

Bendigo and Adelaide Bank Limited Appendix 4D Half Year Report Half Year Announcement Half Year Financial Report For the period ending 31 December 2011 Released 20 February 2012 This report comprises information

Bendigo and Adelaide Bank Limited Appendix 4D Half Year Report Half Year Announcement Half Year Financial Report For the period ending 31 December 2011 Released 20 February 2012 This report comprises information

Bank of Ireland Presentation October As at 1 Oct 2014

Bank of Ireland Presentation October 2014 As at 1 Oct 2014 1 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

Bank of Ireland Presentation October 2014 As at 1 Oct 2014 1 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

Bendigo and Adelaide Bank Limited (Bendigo Bank)

") (Bendigo Bank) Executive summary (Bendigo Bank) is a regional bank that specialises in retail banking with a focus on rural communities. It also owns Rural Bank and Delphi Bank and operates the margin

(Bendigo Bank) Executive summary (Bendigo Bank) is a regional bank that specialises in retail banking with a focus on rural communities. It also owns Rural Bank and Delphi Bank and operates the margin

Bank of Queensland. Half-Year Results 29 February FY08 Half-Year Results

Bank of Queensland Half-Year Results 29 February 2008 1 Agenda Result highlights Financial result in detail BOQ Portfolio Strategy and outlook David Liddy Managing Director & CEO Ram Kangatharan Group

Bank of Queensland Half-Year Results 29 February 2008 1 Agenda Result highlights Financial result in detail BOQ Portfolio Strategy and outlook David Liddy Managing Director & CEO Ram Kangatharan Group

Debt Investor Update FY16

SUNCORP GROUP LIMITED ABN 66 145 290 124 Debt Investor Update FY16 CREATE A BETTER TODAY Suncorp Debt Investor Update Agenda Suncorp Group Group Financial Results Capital Suncorp Bank Funding & Liquidity

SUNCORP GROUP LIMITED ABN 66 145 290 124 Debt Investor Update FY16 CREATE A BETTER TODAY Suncorp Debt Investor Update Agenda Suncorp Group Group Financial Results Capital Suncorp Bank Funding & Liquidity

JP Morgan Australasian Conference Edinburgh

JP Morgan Australasian Conference Edinburgh Ralph Norris CHIEF EXECUTIVE OFFICER 18 September 2008 Commonwealth Bank of Australia ACN 123 123 124 Disclaimer The material that follows is a presentation

JP Morgan Australasian Conference Edinburgh Ralph Norris CHIEF EXECUTIVE OFFICER 18 September 2008 Commonwealth Bank of Australia ACN 123 123 124 Disclaimer The material that follows is a presentation

HALF YEAR RESULTS 2017

HALF YEAR RESULTS Incorporating the requirements of Appendix 4D The half year results announcement incorporates the half year report given to the Australian Securities Exchange (ASX) under Listing Rule

HALF YEAR RESULTS Incorporating the requirements of Appendix 4D The half year results announcement incorporates the half year report given to the Australian Securities Exchange (ASX) under Listing Rule

Incorporating the requirements of APS 330 Half Year Update as at 31 March 2018

Incorporating the requirements of APS 330 Half Year Update as at 31 March "My patients weren't liking the shoes out there. That's when I decided to design my own range." Caroline McCulloch FRANKiE4 Footwear

Incorporating the requirements of APS 330 Half Year Update as at 31 March "My patients weren't liking the shoes out there. That's when I decided to design my own range." Caroline McCulloch FRANKiE4 Footwear

OVERVIEW ANDREW THORBURN

OVERVIEW ANDREW THORBURN Group Chief Executive Officer This presentation is general background information about NAB. It is intended to be used by a professional analyst audience and is not intended to

OVERVIEW ANDREW THORBURN Group Chief Executive Officer This presentation is general background information about NAB. It is intended to be used by a professional analyst audience and is not intended to

Suncorp Group Limited ABN Suncorp Bank APS330 for the quarter ended 30 September 2014

Suncorp Group Limited ABN 66 145 290 124 Suncorp Bank APS330 for the quarter ended 30 September 2014 Release date: 10 November 2014 Suncorp Bank APS330 Basis of preparation This document has been prepared

Suncorp Group Limited ABN 66 145 290 124 Suncorp Bank APS330 for the quarter ended 30 September 2014 Release date: 10 November 2014 Suncorp Bank APS330 Basis of preparation This document has been prepared

Bank of Queensland. Half year results 28 February 2010

Bank of Queensland Half year results 28 February 2010 Agenda Result highlights David Liddy Managing Director & CEO Financial result in detail Ram Kangatharan Chief Operating Officer BOQ portfolio Strategy

Bank of Queensland Half year results 28 February 2010 Agenda Result highlights David Liddy Managing Director & CEO Financial result in detail Ram Kangatharan Chief Operating Officer BOQ portfolio Strategy

G R O W I N G TO G E T H E R

2 MAY 2018 1Q18 FINANCIAL RESULTS PRESENTATION G R O W I N G TO G E T H E R 2018 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains general information

2 MAY 2018 1Q18 FINANCIAL RESULTS PRESENTATION G R O W I N G TO G E T H E R 2018 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains general information

It is therefore pleasing to report that this evolution of BOQ has continued throughout this financial year.

1 2 Good morning everyone. I will start with the highlights of the results. The strategy we have been implementing in the past few years has transformed BOQ into a resilient, multi-channel business that

1 2 Good morning everyone. I will start with the highlights of the results. The strategy we have been implementing in the past few years has transformed BOQ into a resilient, multi-channel business that

Suncorp Bank APS330 Update

ASX announcement APS330 Update 3 May 2016 today provided its quarterly update on Bank assets, credit quality and capital as at 31 March 2016, as required under Australian Prudential Standard 330. s lending

ASX announcement APS330 Update 3 May 2016 today provided its quarterly update on Bank assets, credit quality and capital as at 31 March 2016, as required under Australian Prudential Standard 330. s lending

Paragon Banking Group PLC. Financial Results for twelve months ended 30 September 2018

Paragon Banking Group PLC Financial Results for twelve months ended 3 September 218 218 results highlights 2 Strong financial performance and further strategic progress Strong operational performance New

Paragon Banking Group PLC Financial Results for twelve months ended 3 September 218 218 results highlights 2 Strong financial performance and further strategic progress Strong operational performance New

Suncorp Group Limited. Suncorp Bank. Debt Investor Presentation. Suncorp Group Limited August 2015

Suncorp Bank Debt Investor Presentation 1 Suncorp Investor Update Agenda Suncorp Group Group Financial Results & Capital Suncorp Bank Funding & Liquidity Australian Mortgages 3 5 16 25 31 2 Suncorp Group

Suncorp Bank Debt Investor Presentation 1 Suncorp Investor Update Agenda Suncorp Group Group Financial Results & Capital Suncorp Bank Funding & Liquidity Australian Mortgages 3 5 16 25 31 2 Suncorp Group

Financial Results for the full year ended 30 June 2017

Financial Results for the full year ended 30 June 2017 Create a better today DATA PACK RELEASE DATE 3 AUGUST 2017 SUNCORP GROUP LIMITED ABN 66 145 290 124 Results Group Net Profit After Tax of $1,075m

Financial Results for the full year ended 30 June 2017 Create a better today DATA PACK RELEASE DATE 3 AUGUST 2017 SUNCORP GROUP LIMITED ABN 66 145 290 124 Results Group Net Profit After Tax of $1,075m

PILLAR 3 DISCLOSURE APS 330: PUBLIC DISCLOSURE

2017 BASEL III PILLAR 3 DISCLOSURE AS AT 31 DECEMBER 2017 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet its

2017 BASEL III PILLAR 3 DISCLOSURE AS AT 31 DECEMBER 2017 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet its

Profit Announcement For the full year ended 30 June 2013

Profit Announcement For the full year ended 30 June 2013 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 14 AUGUST 2013 FIND OUT MORE VIA OUR APP ASX Appendix 4E Results for announcement to the market (1)

Profit Announcement For the full year ended 30 June 2013 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 14 AUGUST 2013 FIND OUT MORE VIA OUR APP ASX Appendix 4E Results for announcement to the market (1)

Suncorp-Metway Limited. Recent Developments

May 3, 2016 Suncorp-Metway Limited Recent Developments The information set forth below is not complete and should be read in conjunction with the information contained on the US Rule 144A Programme Investors

May 3, 2016 Suncorp-Metway Limited Recent Developments The information set forth below is not complete and should be read in conjunction with the information contained on the US Rule 144A Programme Investors

For personal use only

Media Release CBA FY17 Results For the full year ended 30 June 2017¹ Reported 9 August 2017 Commonwealth Bank delivers for Australia CEO Comment: Ian Narev Commonwealth Bank s performance this year has

Media Release CBA FY17 Results For the full year ended 30 June 2017¹ Reported 9 August 2017 Commonwealth Bank delivers for Australia CEO Comment: Ian Narev Commonwealth Bank s performance this year has

Suncorp Group Limited

Suncorp Group Limited Financial results for the half year ended 31 December 2013 1 Suncorp results presentation Agenda Results & operational highlights Patrick Snowball CFO report Steve Johnston Outlook

Suncorp Group Limited Financial results for the half year ended 31 December 2013 1 Suncorp results presentation Agenda Results & operational highlights Patrick Snowball CFO report Steve Johnston Outlook

Genworth Mortgage Insurance Australia

Genworth Mortgage Insurance Australia Full Year 2016 Financial Results Presentation 8 February 2017 2017 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation

Genworth Mortgage Insurance Australia Full Year 2016 Financial Results Presentation 8 February 2017 2017 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation

Bank of Ireland Presentation November As at 3 Nov 2014

Bank of Ireland Presentation November 2014 As at 3 Nov 2014 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

Bank of Ireland Presentation November 2014 As at 3 Nov 2014 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

FY2015 Annual Results August Brett McKeon - CEO David Bailey - CFO

FY2015 Annual Results August 27 2015 Brett McKeon - CEO David Bailey - CFO FY2015 Financial Results Highlights Delivery on FY15 Prospectus forecasts Pro forma NPAT $19.3 million up 8.4% against IPO forecast

FY2015 Annual Results August 27 2015 Brett McKeon - CEO David Bailey - CFO FY2015 Financial Results Highlights Delivery on FY15 Prospectus forecasts Pro forma NPAT $19.3 million up 8.4% against IPO forecast

Standard Bank Group : J' :ź? WN ī 5' :Tź :TJ' ī ' 'T 55i : 5 ':T J T ': : ' 5 N?5WT'?:N HJ?b' J Ąā 1W: ăāăĉ

Standard Bank Group OVERVIEW OF STANDARD BANK GROUP AFRICA IS OUR HOME, WE DRIVE HER GROWTH ON-THE-GROUND PRESENCE IN 2 SUB-SAHARAN COUNTRIES OFFICES IN SIX KEY CENTRES 1 216 Branches 9 173 ATMs South

Standard Bank Group OVERVIEW OF STANDARD BANK GROUP AFRICA IS OUR HOME, WE DRIVE HER GROWTH ON-THE-GROUND PRESENCE IN 2 SUB-SAHARAN COUNTRIES OFFICES IN SIX KEY CENTRES 1 216 Branches 9 173 ATMs South

For personal use only

For personal use only Left to right: Antonio Tricoli, Westpac Scholar; Westpac Rescue Helicopter; and Bob Mac Smith, fifth generation farmer and Westpac customer. 206 Financial Results Incorporating the

For personal use only Left to right: Antonio Tricoli, Westpac Scholar; Westpac Rescue Helicopter; and Bob Mac Smith, fifth generation farmer and Westpac customer. 206 Financial Results Incorporating the

BASEL III PILLAR 3 DISCLOSURE

BASEL III PILLAR 3 DISCLOSURE AS AT 30 JUNE 20 JUNE 20 PILLAR 3 / 20 THIRD QUARTER CHART PACK AUSTRALIA AND NEW Z EALAND BANKING GROUP LIMITED 14 AUGUST 20 To be read in conjunction with ANZ 20 Basel III

BASEL III PILLAR 3 DISCLOSURE AS AT 30 JUNE 20 JUNE 20 PILLAR 3 / 20 THIRD QUARTER CHART PACK AUSTRALIA AND NEW Z EALAND BANKING GROUP LIMITED 14 AUGUST 20 To be read in conjunction with ANZ 20 Basel III

Australian Banks. The chicken or the egg AUSTRALIA. Growth under threat... but undeniable valuation support. Inside

AUSTRALIA Inside The chicken or the egg 2 Earnings/price target changes 4 Margins outlook upside overstated Deteriorating credit quality outlook 17 Attractive valuations... but need to be brave 26 Returns

AUSTRALIA Inside The chicken or the egg 2 Earnings/price target changes 4 Margins outlook upside overstated Deteriorating credit quality outlook 17 Attractive valuations... but need to be brave 26 Returns

2017 Results. 27 February 2018

2017 Results 27 February 2018 FY17 Financial Performance 37.8p EPS 1 +29% 192.1m Stat profit 2 +37% RoTE of 14% up from 12.4% in FY16 13.8% CET1 Ratio 6.0p Total dividend +18% 297p TNAV +9% Note: (1) Basic

2017 Results 27 February 2018 FY17 Financial Performance 37.8p EPS 1 +29% 192.1m Stat profit 2 +37% RoTE of 14% up from 12.4% in FY16 13.8% CET1 Ratio 6.0p Total dividend +18% 297p TNAV +9% Note: (1) Basic

WESTPAC RELEASES DECEMBER 2014 PILLAR 3 REPORT AND ADVISES OF AN ACCOUNTING CHANGE THAT WILL BE MADE IN ITS 1H15 RESULT

ASX Release 20 February 2015 WESTPAC RELEASES DECEMBER 2014 PILLAR 3 REPORT AND ADVISES OF AN ACCOUNTING CHANGE THAT WILL BE MADE IN ITS 1H15 RESULT Westpac Group today released its December 2014 Pillar

ASX Release 20 February 2015 WESTPAC RELEASES DECEMBER 2014 PILLAR 3 REPORT AND ADVISES OF AN ACCOUNTING CHANGE THAT WILL BE MADE IN ITS 1H15 RESULT Westpac Group today released its December 2014 Pillar

Yapı Kredi 2017 Earnings Presentation

Yapı Kredi 2017 Earnings Presentation 6 February 2018 Strong results leading to above guidance performance 3.6 bln TL Net Income +33% y/y 1 Ongoing strategy supporting net profit 13.6% ROATE 2 +170 bps

Yapı Kredi 2017 Earnings Presentation 6 February 2018 Strong results leading to above guidance performance 3.6 bln TL Net Income +33% y/y 1 Ongoing strategy supporting net profit 13.6% ROATE 2 +170 bps

2018 INVESTOR INFORMATION

2018 INVESTOR INFORMATION Year ended 31 August 2018 Investor Information 2018 1 ASX APPENDIX 4E FOR THE YEAR ENDED 31 AUGUST 2018 RESULTS FOR ANNOUNCEMENT TO THE MARKET (1) $m Revenues from ordinary activities

2018 INVESTOR INFORMATION Year ended 31 August 2018 Investor Information 2018 1 ASX APPENDIX 4E FOR THE YEAR ENDED 31 AUGUST 2018 RESULTS FOR ANNOUNCEMENT TO THE MARKET (1) $m Revenues from ordinary activities

ASX Release. 24 April 2018

ASX Release 24 April 2018 Westpac 2018 Interim Financial Results Template The Westpac has today released the template for its 2018 Interim Financial Results. It outlines the changes that will be made in

ASX Release 24 April 2018 Westpac 2018 Interim Financial Results Template The Westpac has today released the template for its 2018 Interim Financial Results. It outlines the changes that will be made in

Bank of Queensland. Macquarie Connections Australia Conference 7 May 2009

Bank of Queensland 7 May 2009 Difficult environment... Our response The Environment... Going forward Economic growth slowing Unemployment rising towards 7-8%... Plan for economy to bottom in late 2010

Bank of Queensland 7 May 2009 Difficult environment... Our response The Environment... Going forward Economic growth slowing Unemployment rising towards 7-8%... Plan for economy to bottom in late 2010

SUNCORP GROUP LIMITED ABN SUNCORP BANK APS 330. for the quarter ended 31 MARCH 2018

SUNCORP GROUP LIMITED ABN 66 145 290 124 SUNCORP BANK APS 330 for the quarter ended 31 MARCH 2018 RELEASE DATE: 1 MAY 2018 Basis of preparation This document has been prepared by Suncorp Bank to meet the

SUNCORP GROUP LIMITED ABN 66 145 290 124 SUNCORP BANK APS 330 for the quarter ended 31 MARCH 2018 RELEASE DATE: 1 MAY 2018 Basis of preparation This document has been prepared by Suncorp Bank to meet the

Profit Announcement (U.S. Version) Half Year ended 31 December 2008

Half Year ended 31 December 2008") Profit Announcement (U.S. Version) Half Year ended 31 December 2008 ASX Appendix 4D Results for announcement to the market (1) Report for the half year ended 31 December 2008 $M Revenue from ordinary activities

Profit Announcement (U.S. Version) Half Year ended 31 December 2008 ASX Appendix 4D Results for announcement to the market (1) Report for the half year ended 31 December 2008 $M Revenue from ordinary activities

This document comprises the Westpac Group full year results and is provided to the Australian Securities Exchange under Listing Rule 4.3A.

RESULTS ANNOUNCEMENT TO THE MARKET ASX APPENDIX 4E RESULTS FOR ANNOUNCEMENT TO THE MARKET 1 REPORT FOR THE FULL YEAR ENDED 30 SEPTEMBER 2013 2 Revenue from ordinary activities 3,4 () up 4% to $18,639 Profit

RESULTS ANNOUNCEMENT TO THE MARKET ASX APPENDIX 4E RESULTS FOR ANNOUNCEMENT TO THE MARKET 1 REPORT FOR THE FULL YEAR ENDED 30 SEPTEMBER 2013 2 Revenue from ordinary activities 3,4 () up 4% to $18,639 Profit

For personal use only. Pepper Group Limited. Full year results as at 31 December 2016 Investor presentation. 24 February Copyright 2017 Pepper.

Pepper Group Limited Full year results as at 31 December 2016 Investor presentation 24 February 2016 Pepper s strategy is delivering strong earnings growth Record originations via multiple channels and

Pepper Group Limited Full year results as at 31 December 2016 Investor presentation 24 February 2016 Pepper s strategy is delivering strong earnings growth Record originations via multiple channels and

Profit Announcement. For the full year ended 30 June 2017

Profit Announcement For the full year ended 30 June 2017 Commonwealth Bank of Australia ACN 123 123 124 9 August 2017 ASX Appendix 4E Results for announcement to the market (1) Report for the year ended

Profit Announcement For the full year ended 30 June 2017 Commonwealth Bank of Australia ACN 123 123 124 9 August 2017 ASX Appendix 4E Results for announcement to the market (1) Report for the year ended

Swedbank year-end results 2018

Swedbank year-end results 218 Birgitte Bonnesen (CEO), Anders Karlsson (CFO), Helo Meigas (CRO) Strong financial result in 218 delivered on strategic priorities SELECTED 218 DELIVERIES Continued digitisation

Swedbank year-end results 218 Birgitte Bonnesen (CEO), Anders Karlsson (CFO), Helo Meigas (CRO) Strong financial result in 218 delivered on strategic priorities SELECTED 218 DELIVERIES Continued digitisation

This page has been left blank intentionally. Full Year Results

This page has been left blank intentionally. Results for announcement to the market Results for announcement to the market Report for the full year ended 30 September 30 September $m Revenue from ordinary

This page has been left blank intentionally. Results for announcement to the market Results for announcement to the market Report for the full year ended 30 September 30 September $m Revenue from ordinary

UBS Financial Services Conference

UBS Financial Services Conference Expanding our Leadership Position in Business Banking 25 June 2009 Joseph Healy Group Executive, Business Banking National Australia Bank Limited ABN 12 004 044 937 Business

UBS Financial Services Conference Expanding our Leadership Position in Business Banking 25 June 2009 Joseph Healy Group Executive, Business Banking National Australia Bank Limited ABN 12 004 044 937 Business

Performance and Outlook. December 2015

Performance and Outlook December 2015 Agenda Macro Picture Performance Highlights Q&A 2 Agenda Macro Picture Performance Highlights Fundamentals (IIP) Output conditions Inflation Rates Credit and Deposit

Performance and Outlook December 2015 Agenda Macro Picture Performance Highlights Q&A 2 Agenda Macro Picture Performance Highlights Fundamentals (IIP) Output conditions Inflation Rates Credit and Deposit

For personal use only Genworth Mortgage Insurance Australia

Genworth Mortgage Insurance Australia 3Q 2016 Financial Results Presentation 4 November 2016 2016 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains

Genworth Mortgage Insurance Australia 3Q 2016 Financial Results Presentation 4 November 2016 2016 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains

2002 Interim Results. David Morgan, Chief Executive Officer Philip Chronican, Chief Financial Officer. 2 May 2002

David Morgan, Chief Executive Officer Philip Chronican, Chief Financial Officer 2 May 2002 Another record result $m 1,100 900 700 500 701 Net Profit After Tax & EPS CAGR 755 1H99 1H02 EPS 14% NPAT 13%

David Morgan, Chief Executive Officer Philip Chronican, Chief Financial Officer 2 May 2002 Another record result $m 1,100 900 700 500 701 Net Profit After Tax & EPS CAGR 755 1H99 1H02 EPS 14% NPAT 13%

QUARTER ENDING DECEMBER Incorporating the requirements of Australian Prudential Standard 330. MyState Limited APS330

Incorporating the requirements of Australian Prudential Standard 330 QUARTER ENDING DECEMBER 2016 1 EXECUTIVE SUMMARY MYSTATE This document has been prepared by MyState Limited to meet the disclosure obligations

Incorporating the requirements of Australian Prudential Standard 330 QUARTER ENDING DECEMBER 2016 1 EXECUTIVE SUMMARY MYSTATE This document has been prepared by MyState Limited to meet the disclosure obligations

Westpac 2009 Full Year Results

Westpac 2009 Full Year Results Gail Kelly Chief Executive Officer Westpac Banking Corporation ABN 33 007 457 141 Key areas of focus in 2009 Position the Group strongly through the GFC and economic downturn

Westpac 2009 Full Year Results Gail Kelly Chief Executive Officer Westpac Banking Corporation ABN 33 007 457 141 Key areas of focus in 2009 Position the Group strongly through the GFC and economic downturn

2018 BASEL III PILLAR 3 DISCLOSURE

2018 BASEL III PILLAR 3 DISCLOSURE AS AT 31 MARCH 2018 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet its disclosure

2018 BASEL III PILLAR 3 DISCLOSURE AS AT 31 MARCH 2018 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet its disclosure

Economic and housing outlook for New South Wales. Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017

Economic and housing outlook for New South Wales Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017 Risks to residential building moving from global to local World

Economic and housing outlook for New South Wales Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017 Risks to residential building moving from global to local World

Presentation of Half Year Results 13 February

Presentation of Half Year Results 13 February 2001 www.commbank.com.au Disclaimer The material that follows is a presentation of general background information about the Bank s activities current at the

Presentation of Half Year Results 13 February 2001 www.commbank.com.au Disclaimer The material that follows is a presentation of general background information about the Bank s activities current at the

Ralph Norris CHIEF EXECUTIVE OFFICER

Ralph Norris CHIEF EXECUTIVE OFFICER 27 September 2007 Commonwealth Bank of Australia ACN 123 123 124 JP MORGAN ASIA PACIFIC AUSTRALASIAN CONFERENCE 2007 EDINBURGH Disclaimer The material that follows

Ralph Norris CHIEF EXECUTIVE OFFICER 27 September 2007 Commonwealth Bank of Australia ACN 123 123 124 JP MORGAN ASIA PACIFIC AUSTRALASIAN CONFERENCE 2007 EDINBURGH Disclaimer The material that follows

Equity story. December 2017

Equity story December 2017 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E Operating in a robust Norwegian economy Positive GDP growth and low unemployment rates Norwegian GDP

Equity story December 2017 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E Operating in a robust Norwegian economy Positive GDP growth and low unemployment rates Norwegian GDP

Media Release CBA 1H17 Results

Media Release CBA 1H17 Results For the half year ended 31 December 2016¹ Reported 15 February 2017 Summary Statutory net profit after tax (NPAT) of $4,895 million, up 6%. 2 Cash NPAT of $4,907 million,

Media Release CBA 1H17 Results For the half year ended 31 December 2016¹ Reported 15 February 2017 Summary Statutory net profit after tax (NPAT) of $4,895 million, up 6%. 2 Cash NPAT of $4,907 million,

BASEL III PILLAR 3 DISCLOSURE

BASEL III PILLAR 3 DISCLOSURE AS AT 31 DECEMBER 20 DECEMBER 20 PILLAR 3 / 2018 FIRST QUARTER CHART PACK AUSTRALIA AND NEW Z EALAND BANKING GROUP LIMITED 20 FEBRUARY 2018 To be read in conjunction with

BASEL III PILLAR 3 DISCLOSURE AS AT 31 DECEMBER 20 DECEMBER 20 PILLAR 3 / 2018 FIRST QUARTER CHART PACK AUSTRALIA AND NEW Z EALAND BANKING GROUP LIMITED 20 FEBRUARY 2018 To be read in conjunction with

Westpac Banking Corporation

Westpac Banking Corporation Philip Chronican Group Executive Westpac Institutional Bank March 7 Westpac Banking Corporation at a glance Australia s first bank est. 87 Top bank globally Consistent earnings

Westpac Banking Corporation Philip Chronican Group Executive Westpac Institutional Bank March 7 Westpac Banking Corporation at a glance Australia s first bank est. 87 Top bank globally Consistent earnings

Basel III Pillar 3. Capital Adequacy and Risks Disclosures as at 31 December 2016

Basel III Pillar 3 Capital Adequacy and Risks Disclosures as at 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 15 FEBRUARY 2017 This page has been intentionally left blank Table of Contents

Basel III Pillar 3 Capital Adequacy and Risks Disclosures as at 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 15 FEBRUARY 2017 This page has been intentionally left blank Table of Contents

SUNCORP GROUP LIMITED ABN RELEASE DATE 4 AUGUST Debt Investor Update FY16. Covered Bond CREATE A BETTER TODAY

SUNCORP GROUP LIMITED ABN 66 145 290 124 RELEASE DATE 4 AUGUST 2016 Debt Investor Update FY16 Covered Bond CREATE A BETTER TODAY Suncorp Debt Investor Update Agenda Suncorp Group Group Financial Results

SUNCORP GROUP LIMITED ABN 66 145 290 124 RELEASE DATE 4 AUGUST 2016 Debt Investor Update FY16 Covered Bond CREATE A BETTER TODAY Suncorp Debt Investor Update Agenda Suncorp Group Group Financial Results

Egg plc. Preliminary Results 24 February 2003

Egg plc Preliminary Results 24 February 2003 agenda Introduction Paul Gratton (CEO) Operational Review - Paul Gratton Financial Results - Stacey Cartwright (CFO) Outlook & Summary - Paul Gratton 1 highlights

Egg plc Preliminary Results 24 February 2003 agenda Introduction Paul Gratton (CEO) Operational Review - Paul Gratton Financial Results - Stacey Cartwright (CFO) Outlook & Summary - Paul Gratton 1 highlights

Investor Discussion Pack

Investor Discussion Pack David Morgan, Chief Executive Officer May 2002 Disclaimer The material contained in the following presentation is intended to be general background information on Westpac Banking

Investor Discussion Pack David Morgan, Chief Executive Officer May 2002 Disclaimer The material contained in the following presentation is intended to be general background information on Westpac Banking

Investor Presentation

Investor Presentation 16 th and 17 th November, 2010 Who we are ASB New Zealand s Best Bank Established in 1847 CBA acquired 75% in 1989 Wholly owned by CBA since 2000 Total Assets NZ$63.56bn as at June

Investor Presentation 16 th and 17 th November, 2010 Who we are ASB New Zealand s Best Bank Established in 1847 CBA acquired 75% in 1989 Wholly owned by CBA since 2000 Total Assets NZ$63.56bn as at June

For personal use only

CBA 3Q18 Trading Update For the quarter ended 31 March 2018 1. Reported 9 May 2018. All comparisons are to the average of the two quarters of the first half of FY18 unless noted otherwise. Summary Unaudited

CBA 3Q18 Trading Update For the quarter ended 31 March 2018 1. Reported 9 May 2018. All comparisons are to the average of the two quarters of the first half of FY18 unless noted otherwise. Summary Unaudited

2007 Final Results. David Morgan Chief Executive Officer. A strong, high quality result

27 Final Results David Morgan Chief Executive Officer 1 November 27 A strong, high quality result Strong earnings growth and a higher return on equity High quality revenue led performance Enhanced franchise

27 Final Results David Morgan Chief Executive Officer 1 November 27 A strong, high quality result Strong earnings growth and a higher return on equity High quality revenue led performance Enhanced franchise

The Outlook for the Housing Industry in Western Australia

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2012 Europe muddles while China rebalances China is looking to rebalance

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2012 Europe muddles while China rebalances China is looking to rebalance

For personal use only

For personal use only Profit Announcement FOR THE FULL YEAR ENDED 30 JUNE 2014 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 13 AUGUST 2014 ASX Appendix 4E Results for announcement to the market (1) Report

For personal use only Profit Announcement FOR THE FULL YEAR ENDED 30 JUNE 2014 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 13 AUGUST 2014 ASX Appendix 4E Results for announcement to the market (1) Report

Results Presentation & Investor Discussion Pack

Results Presentation & Investor Discussion Pack Index Full Year Result Overview CEO Presentation 3 CFO Presentation 13 Additional Financial Information Adjustments between Statutory Profit and Cash Profit

Results Presentation & Investor Discussion Pack Index Full Year Result Overview CEO Presentation 3 CFO Presentation 13 Additional Financial Information Adjustments between Statutory Profit and Cash Profit

For personal use only

17 February 2017 The Manager Company Announcements Australian Securities Exchange 20 Bridge Street Sydney NSW 2000 MyState Limited Correction to Investor Presentation Please be advised that an amendment

17 February 2017 The Manager Company Announcements Australian Securities Exchange 20 Bridge Street Sydney NSW 2000 MyState Limited Correction to Investor Presentation Please be advised that an amendment

ANZ Investor Day Auckland, New Zealand

ANZ Investor Day Auckland, New Zealand AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED Thursday, 4 June 2015 New Zealand Update Antonia Watson CHIEF FINANCIAL OFFICER, NEW ZEALAND Delivering stable low-risk

ANZ Investor Day Auckland, New Zealand AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED Thursday, 4 June 2015 New Zealand Update Antonia Watson CHIEF FINANCIAL OFFICER, NEW ZEALAND Delivering stable low-risk

Consolidated financial results for 2Q 2017

Citi Handlowy Strategy and Investor Relations Department Consolidated financial results for 2Q 2017 August 22 nd, 2017 2Q 2017 summary Consistent growth of customer business: Loan volume growth in institutional

Citi Handlowy Strategy and Investor Relations Department Consolidated financial results for 2Q 2017 August 22 nd, 2017 2Q 2017 summary Consistent growth of customer business: Loan volume growth in institutional

NATIONAL RMBS TRUST

The Manager confirms NAB s continued retention of an amount equal to at least 5% of the aggregate principal balance of securitised exposures Transaction Details as at 20 March 2013 Issuance Date 13-Dec-12

The Manager confirms NAB s continued retention of an amount equal to at least 5% of the aggregate principal balance of securitised exposures Transaction Details as at 20 March 2013 Issuance Date 13-Dec-12

Bendigo and Adelaide Bank Convertible Preference Shares 2 Offer and SPS Reinvestment Offer

Bendigo and Adelaide Bank Convertible Preference Shares 2 Offer and SPS Reinvestment Offer 3 September 2014 2 This presentation has been prepared by Bendigo and Adelaide Bank Limited (ABN 11 068 049 178,

Bendigo and Adelaide Bank Convertible Preference Shares 2 Offer and SPS Reinvestment Offer 3 September 2014 2 This presentation has been prepared by Bendigo and Adelaide Bank Limited (ABN 11 068 049 178,

Genworth Mortgage Insurance Australia

Genworth Mortgage Insurance Australia 1Q 2016 Financial results presentation 29 April 2016 2016 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains

Genworth Mortgage Insurance Australia 1Q 2016 Financial results presentation 29 April 2016 2016 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains

AUSTRALIAN SECURITISATION FORUM Australian Market Review and Outlook. Ken Hanton May 2018

AUSTRALIAN SECURITISATION FORUM Australian Market Review and Outlook Ken Hanton May 2018 Australian Bond Market Source: Australian Fixed Income Securities in a Low Rate World. Christopher Kent, RBA, Assistant

AUSTRALIAN SECURITISATION FORUM Australian Market Review and Outlook Ken Hanton May 2018 Australian Bond Market Source: Australian Fixed Income Securities in a Low Rate World. Christopher Kent, RBA, Assistant

Westpac Group 2014 Full Year Results Announcement Template

ASX RELEASE 30 October 2014 Group 2014 Results Announcement Template The Group has today released the template for its 2014 Results Announcement. This release provides: Details of additional cash earnings

ASX RELEASE 30 October 2014 Group 2014 Results Announcement Template The Group has today released the template for its 2014 Results Announcement. This release provides: Details of additional cash earnings

Bank of Ireland Presentation

Bank of Ireland Presentation October 2013 (as at 1 Oct 2013) 1 Forward looking statement 2 Irish Economy Overview 3 Government finances ahead of target Public finances continue towards sustainability The

Bank of Ireland Presentation October 2013 (as at 1 Oct 2013) 1 Forward looking statement 2 Irish Economy Overview 3 Government finances ahead of target Public finances continue towards sustainability The

CYBG PLC INTERIM FINANCIAL RESULTS

CYBG PLC INTERIM FINANCIAL RESULTS Strategic progress David Duffy Chief Executive Officer S T R O N G P R O G R E S S I N D E L I V E R I N G O U R S T R AT E G Y Building a bank fit for the Sustainable

CYBG PLC INTERIM FINANCIAL RESULTS Strategic progress David Duffy Chief Executive Officer S T R O N G P R O G R E S S I N D E L I V E R I N G O U R S T R AT E G Y Building a bank fit for the Sustainable

PILLAR 3 DISCLOSURE APS 330: PUBLIC DISCLOSURE

2015 BASEL III PILLAR 3 DISCLOSURE AS AT 31 MARCH 2015 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet its disclosure

2015 BASEL III PILLAR 3 DISCLOSURE AS AT 31 MARCH 2015 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet its disclosure

Genworth Mortgage Insurance Australia

Genworth Mortgage Insurance Australia 1H 2015 Financial results presentation 5 August 2015 2015 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains

Genworth Mortgage Insurance Australia 1H 2015 Financial results presentation 5 August 2015 2015 Genworth Mortgage Insurance Australia Limited. All rights reserved. Disclaimer This presentation contains