AGRICULTURAL LENDING By Robin Russell CHAPTER 10

|

|

|

- Naomi Cunningham

- 5 years ago

- Views:

Transcription

1 AGRICULTURAL LENDING By Robin Russell CHAPTER 10 I. AGRICULTURAL LENDING Overview Risks Associated with Agri-Business Lending II. FARM PRODUCTS Farm Products Defined What is an Agricultural Lien Statutory Liens on Farm Products Creation of UCC Security Interests in Agricultural Collateral Perfection of the Security Interest under the UCC Fixtures Farm Products and Equipment Located on Leased Premises Crops on Mortgaged Real Property Landlord s/ Mortgagee s Subordination or Waiver Agricultural Leases Registered Animals Purchase Money Security Interests Real Property Liens Food Security Act of Crop Insurance Yield-Based Crop Coverage Crop Revenue Insurance Plans Assignment of Federal Farm Program Payments Commodity Futures Contracts Equity Interest in Agricultural Cooperatives III. WAREHOUSE RECEIPTS Overview Warehouses Warehouse Characteristics Non-Negotiable And Negotiable Receipts Terms of a Warehouse Receipt Perfection of Security Interest Inflow and Outflow of Warehouse Goods Monitoring the Stored Goods Special Bankruptcy Considerations Mediation Regulation Z i

2 IV. DOCUMENT CHECKLIST Documents Required for Farm Products Additional Documents for Warehouse Receipts V. FORMS Forms ii

3 I. AGRICULTURAL LENDING OVERVIEW: An agricultural loan may be categorized as a short-term loan, a long-term loan or carry-over debt. Short-term loans are made to finance crop and livestock production, and are typically repaid at the end of the production cycle from the proceeds of the sale of the grain or livestock produced during that cycle. Long-term loans are primarily associated with the purchase and development of capital assets, such as real estate, equipment, breeding herds and orchards, and are generally repaid from cash flows from operations. Carry-over debt refers to restructured short-term debt, such as the unpaid portion of an annual operating line of credit, because the Borrower is unable to pay off the debt as originally planned. The collateral for agricultural loans often involves a mix of collateral, including (i) real property, (ii) farm products, (iii) equipment (including equipment that may become fixtures), (iv) accounts, (v) general intangibles including payments under certain federal farm programs, and (vi) certificated motor vehicles. RISKS ASSOCIATED WITH AGRI- BUSINESS LENDING: Credit Risk. Banks financing agricultural operations and investment assume the risk of the Borrower s ability to successfully plant crops or breed animals, grow or raise the product, or harvest finished products (such as grains and livestock for slaughter). Production Risk. The Bank assumes the risk of adverse weather conditions and other natural disasters which can result in an unexpected increase in the expense of harvesting, fertilizing and transporting product as well as feed shortages. Market Volatility. Commodity prices may fluctuate because of unfavorable weather or changes in domestic and global supply and demand. Government Policies and Legal Risks. Agricultural activity may be regulated by federal, state or even local jurisdictions. Certain types of agricultural operations, such as large swine, dairy, feedlot and poultry operations are often not permitted near population centers and are subject to significant environmental regulation. An agricultural lender must keep current on the status of federal government assistance programs, since change in those programs 10-1

4 can have an effect (good and bad) on the Borrower s ability to keep its loans. For example, the Agricultural Act of 2014 eliminated direct payments to agricultural producers while continuing crop insurance options and conservation programs. Liquidity Risk. If crops losses or unfavorable market conditions result in loan payment deferrals, a Bank s liquidity could be strained. Operational Risk. Agricultural lending requires extensive documentation, inspection, control and monitoring requirements. A Bank s failure to comply with these requirements, such as improper documentation, can result in loan collection problems. Compliance Risk. A Bank must comply with applicable appraisal requirements, real estate lending standards as well as special lending limits applicable to agricultural loans. Regulation D, the lending limits promulgated by the Comptroller of the Currency and applicable to agricultural loans made by national banks and federal savings associations, is attached at the end of these materials. II. FARM PRODUCTS FARM PRODUCTS DEFINED: The UCC defines farm products as goods (things that are movable) with respect to which a debtor is engaged in farming operations and which are: 1. crops grown, growing or to be grown, including (a) crops produced on trees, vines and bushes (fruit and nuts from trees or berries from bushes) and (b) aquatic goods produced in aquacultural operations (kelp, for example) 2. livestock, born or unborn, including aquatic goods produced in aquaculture operations; 3. supplies used or produced in a farming operation; or 4. products of crops or livestock in their unmanufactured states (ginned cotton is unmanufactured as is milk that has been pasteurized or sap boiled to produce maple syrup; while the canning of farm products such as tomatoes would likely be manufacturing). [UCC 9-102(a)(34)] 10-2

5 The UCC does not define crops, livestock or supplies. Standing timber, however, is excluded from the definition of farm products. This means that the apples may be farm products, but the apple tree is not. CAUTION: If goods are farm products, they are neither equipment nor inventory. Goods that are farm products when in the possession of a Borrower engaged in farming operations will be inventory if they are in the hands of a person not engaged in farming operations The UCC defines a farming operation as raising, cultivating, propagating, fattening, grazing or any other farming, livestock, or aquacultural operation. Aquatic goods may be either livestock (e.g., catfish raised on a catfish farm) or crops (e.g., kelp). Ranching would be considered a farming operation. [UCC 9-102(a)(35)] The Uniform Commercial Code, which has been adopted, with some variation, in all 50 states is the primary method by which the Bank obtains and perfects liens in personal property, including liens on farm products. For purposes of this chapter, the term UCC refers to the Official Version of the Uniform Commercial Code. Bank Counsel should be consulted to determine variations in the UCC that are applicable in any specific state or other jurisdiction. WHAT IS AN AGRICULTURAL LIEN: An agricultural lien is defined in the UCC as an interest in farm products: that secures payment or performance of an obligation for (a) goods or services furnished in connection with a debtor s farming operation or (b) rent on real property leased by a debtor in connection with its farming operation; or that is created by statute in favor of a person that (a) in the ordinary course of its business furnished goods or services to a debtor in connection with a debtor s farming operation or (b) leased real property to a debtor in connection with the debtor s farming operation; and whose effectiveness does not depend on the lender or other creditor s possession of the personal property. [UCC-9-102(a)(5)] STATUTORY LIENS ON FARM Statutory liens vary from state to state, and may or may not be agricultural liens. If the effectiveness of a statutory lien depends 10-3

6 PRODUCTS: upon the creditor possessing the collateral, the lien is not an agricultural lien under the UCC. For example, although the following constitute some of the statutory liens in Texas, not all of them may qualify as agricultural liens for the reason noted: a chemical and seed supplier s lien on crop proceeds (agricultural lien - effectiveness doesn t require possession of collateral); a stock breeder s lien on offspring (agricultural lien - effectiveness doesn t require possession of collateral); a lien on livestock, carcasses and related products with respect to livestock sold for slaughter (not an agricultural lien because it does not secure a supplier s inputs); a cotton ginner s lien on ginned cotton (not an agricultural lien because its effectiveness depends on possession of the collateral); a feed supplier s lien on proceeds (agricultural lien); an agricultural landlord s lien (since, under Texas law, the lien persists for 30 days following harvest and thus its effectiveness is not dependent upon possession of the collateral, it is probably an agricultural lien); an agister s lien on livestock (not an agricultural lien because its effectiveness depends upon possession of the collateral); and an agricultural landlord s lien if the lien persists following harvest, therefore its effectiveness is not dependent on possession and is probably an agricultural lien). CAUTION: Local counsel should be consulted to determine the extent to which liens other than those created under the UCC may be applicable to the Bank s personal property collateral. Agricultural liens created by statute are perfected by filing a form UCC-1 in the state where the farm products are located or by possession. [UCC 9-302] CAUTION: Because agricultural liens may be on file against farm products in multiple states, the Bank must conduct a lien search in the state where the Borrower is located and in all 10-4

7 states where the Borrower has farm products. CREATION OF UCC SECURITY INTERESTS IN AGRICULTURAL COLLATERAL: Security Agreement. Under the UCC, the creation of a security interest in farm products by a Borrower is not materially different from the creation of a security interest in other personal property. As with other security interests, a security interest in farm products does not attach and become effective until all of the following have occurred: value has been given (which can be the funding of a loan or a commitment of the Bank to make a loan); the Borrower should have rights in the collateral (this could be a leasehold interest or other interest, since an ownership interest in the collateral is not required under the UCC to create a security interest); and unless the Bank has possession of the collateral (which is unusual with respect to agricultural collateral), the Borrower should sign or otherwise authenticate a security agreement in which the Borrower grants to the Bank a security interest in the described collateral. Describing the Collateral in the Security Agreement. An adequate description of the collateral in a security agreement is essential to the creation of an enforceable security interest in the collateral. If the Bank takes a security interest in farm products, the Bank also should take a security interest in inventory to protect itself in the event the Borrower ceases to qualify as person engaged in farming operations or the collateral is transferred to a person not engaged in farming operations. PERFECTION OF THE SECURITY INTEREST UNDER THE UCC: General. A Bank will rarely perfect a security interest granted by a Borrower in farm products or equipment by possession. Therefore, it is almost always necessary to file a financing statement to perfect the Bank s security interest in the farm products and equipment of a Borrower. Form of UCC-1 Financing Statement. The UCC contains forms of UCC-1 Financing Statement and UCC Financing Statement Addendum. [UCC 9-521] Many states however do not use these forms and instead use forms promulgated by the International Association of Commercial Administrators or otherwise approved by their Secretary of State. 10-5

8 CAUTION: Before you file a financing statement, always check with the filing office to be sure you are using the correct form. Describing the Collateral in the Financing Statement. While the collateral in a security agreement may be described as it is in the security agreement, the collateral in a UCC-1 Financing Statement may be described as all assets or all personal property of the Borrower. CAUTION: An all assets or all personal property description of the collateral is permitted only in the financing statement, not in a Security Agreement. Place of Filing. If the debtor is an individual, the financing statement should be filed in the Central Filing Office of the state in which the debtor has its principal residence. If, however, the debtor is a corporation, a limited liability company or a limited partnership, the financing statement should be filed in the central filing office of the state under which the debtor is organized or formed. In most states, but not all, the Central Filing Office is the Office of the Secretary of State. If the debtor is not an individual, a corporation, a limited liability company or a limited partnership, Bank Counsel should be consulted to assure that the financing statement is filed in the proper place. EXCEPTION: A Bank should be alert to the applicability of certificate of title requirements to certain equipment used in farming operations, such as trucks and farm tractors. Equipment that is subject to a certificate of title act (such as trucks) is not perfected by a UCC filing on equipment. Rather, perfection of the security in that type of equipment is by a notation on the certificate of title evidencing title to the equipment. In some states, however, farm tractors and other implements of husbandry are exempt from titling laws and should be perfected by an appropriate UCC filing. Bank Counsel should be consulted as to whether any equipment is covered by a certificate of title or is exempt from titling requirements as an implement of husbandry. FIXTURES: Even though an item used in a farming operation may fall within the above definition of equipment, it may also constitute a fixture under the UCC. 10-6

9 A fixture is an item of personal property which has become affixed to real property in such a manner that the item is viewed by the law as part of the real property. In deciding whether or not an item has become permanently affixed to the realty, courts look to the intent of the parties, as indicated by the manner in which the item is attached to the real estate, the purpose and use of the equipment, the relationship of the parties and any contractual language. The subject of fixtures can cause extensive litigation regarding the conflicting security interests of the mortgagee of real property and the Bank that finances farm equipment for a farming operation on that real property. The Bank should be aware that in financing items such as walk-in refrigeration units, and other interior furnishings, the only sure way to protect the Bank security interest is to comply with the UCC provisions governing both equipment and fixtures. If the Bank decides that a fixture filing is appropriate, the Bank should also try to get a subordination or release of the interest in the farm equipment of any mortgagee of the real property where the farm equipment is located. Bank Counsel should be consulted if the collateral includes equipment that could be a fixture. FARM PRODUCTS AND EQUIPMENT LOCATED ON LEASED PREMISES: CROPS ON MORTGAGED REAL PROPERTY: If the Borrower leases its farming premises or stores its equipment on leased premises, the Bank s security interest in the farm products and equipment may be subject to the prior interest of the landlord pursuant to state law. This landlord s lien would be in addition to any other security interests in the Borrower s farm products and equipment which a UCC search would reveal. In any such instance the Bank should seek to obtain a subordination, waiver or release of such lien from the Borrower s landlord. A security interest may be taken in crops growing or to be grown. Crops growing on real property, unless severed by actual harvesting, a prior lease or a prior security interest, may pass with the real property upon foreclosure of an existing deed of trust or mortgage on that real property. 10-7

10 The Bank should obtain an agreement with the mortgagee which will allow the Bank to harvest the crops after foreclosure if necessary. A perfected security interest in crops growing on real property has priority over a mortgagee or owner of the property if the debtor is the owner or is in possession of the real estate. [UCC 9-334(i)] LANDLORD S/ MORTGAGEE S SUBORDINATION OR WAIVER: As a practical matter, it is often difficult to obtain from a landlord or mortgagee the requested waiver, subordination or release. Often the landlord or mortgagee will seek to extract something from the Borrower (lessee) in return for such waiver, subordination or release which the Borrower (lessee) is unwilling to give. EXAMPLE: If the Borrower (lessee) has outstanding complaints against his performance under the lease, the landlord may seek a release of these complaints in return for his execution of the subordination. AGRICULTURAL LEASES: Agricultural leases may be considered a source of collateral as well as agricultural real estate and agricultural production. The Bank may wish to take an assignment of rentals due the Borrower under an existing cash lease. Under a cropshare lease, the Bank may require an assignment of the Borrower s landlord s share of all harvested crops. However, the crops taken under such an assignment may be subject to a prior security interest; (i.e., the advancement of seed money ) and the Bank should not only check for prior security interests in the crops but also should consider perfecting its own security interest as well. REGISTERED ANIMALS: Livestock which are thoroughbred animals are generally registered with a private association that maintains records of ownership of the particular type of animal (i.e., The American Quarter Horse Association). Possession of the registration is an essential element to the sale of the animal or its breeding services. The Bank taking a security interest in this type of livestock should take possession of the certificate(s) of registration but this does not alone constitute perfection. Consult Bank Counsel. 10-8

11 PURCHASE MONEY SECURITY INTERESTS: A purchase-money security interest ( PMSI ) is a security interest in goods (including livestock and equipment) securing the credit extended to enable the Borrower to acquire or use the goods. [UCC 9-103(a)(1) and (2)] It gives a super priority to the Bank that provides the financing for the Borrower to pay the purchase price of the goods. PMSI in Livestock. A perfected purchase-money security interest in livestock that are farm products has priority over a conflicting security interest in the same livestock, and in their identifiable proceeds and identifiable products in their unmanufactured states, if: the purchase-money security interest is perfected when the debtor receives possession of the livestock; the purchase-money secured party sends an authenticated notification (a writing) to the holder of the conflicting security interest; the holder of the conflicting security interest receives the notification within six months before the debtor receives possession of the livestock; and the notification states that the person sending the notification has or expects to acquire a purchase-money security interest in livestock of the debtor and describes the livestock. [UCC 9-324(d)] PMSI in Equipment and Farm Products other than Livestock. A perfected purchase money security interest in equipment and farm products (other than livestock) has priority over a conflicting security interest in the same equipment or farm products and in its identifiable proceeds if: the PMSI is perfected when the Borrower receives possession; or within 20 days after the Borrower receives possession. REAL PROPERTY LIENS: Liens on real property such as acreage and timber are created by the granting of a mortgage or a deed of trust executed by the Borrower to the Bank. Bank Counsel should be consulted as to the rules governing liens on real property to assure that a valid lien has been 10-9

12 created, and its priority over other liens, especially statutory liens. FOOD SECURITY ACT OF 1985: Congress enacted the Food Security Act of 1985 (7 U.S.C. 1631) (the FSA ). The FSA preempts the UCC and allows a buyer in the ordinary course to buy farm products from a seller/farmer free and clear of any security interest created by that seller even if the security interest is perfected and even if the buyer knows of the security interest. However, the FSA allows Banks and other secured parties to take action to prevent a buyer from buying farm products free of the security interest. The action available to the secured party depends upon whether the state involved has established a central notification system that has been certified by the U.S. Secretary of Agriculture ( CNS ). Only about 16 states have established a CNS, and Bank Counsel should be consulted to determine whether a particular state has a CNS. If the State has a CNS. If the state involved has a certified CNS system, a secured party can file an effective financing statement ( EFS ) with the Secretary of State to notify buyers of the claimed security interest. Buyers of farm products in a CNS state must subscribe to lists of filed EFS records provided on a regular basis by the secretary of state, or conduct their own searches of EFS records. If the farmer/seller appears on the published list or search of EFS records, the buyer knows it must take steps to ensure the proceeds reach the Bank or other secured party. CAUTION: An EFS is not a UCC-1 financing statement. The content requirements for an EFS record are similar but different from those for a UCC financing statement. In addition to the Borrower s name and address, an EFS must include the Borrower s social security number (or unique identifier), description and location of the farm products, and in the case of written EFS records, the Borrower s signature. Each state with a CNS system has its own EFS form, and the EFS form and the UCC-1 form are easily confused. Be careful not to confuse EFS and UCC-1 forms. If the State has no CNS. In those states that do not have a CNS, the FSA provides that a lender who does not want its security interest terminated by a sale by a farmer/seller must prenotify individual buyers of individual liens based upon information about contemplated buyers given the lender by the Borrower. A form of Verification of List of Potential Buyers is located at the end of 10-10

13 these materials. Once the lender has the list of potential buyers, the lender can notify each potential buyer of its security interest in a Borrower s farm products. A form of Notice of Security Interest is located at the end of this chapter and can be used by a lender to notify those potential buyers of farm products of the lender s security interest. Selling Off-List. If a farmer/seller sells to a buyer who was not notified of a security interest because the farmer/seller failed to give the Bank the name of the potential buyer, the farmer/seller is said to have sold off-list or made an out of trust sale. The farmer/seller is subject to a mandatory fine of at least $5000 under 7 U.S.C. 1631(h). CROP INSURANCE: If the Borrower has coverage and there is a loss the Bank may receive crop insurance proceeds directly from the government, but a special assignment in accordance with federal regulation is required. Once the proceeds are paid to the farmer/borrower, they are insurance proceeds under the UCC which are subject to the lien of a Bank that had a security interest in the underlying crops. The Risk Management Agency (RMA) of the U.S. Department of Agriculture (USDA) provides policies for more than 100 crops. Federal crop insurance policies typically consist of the Common Crop Insurance Policy, the specific crop provisions, and policy endorsements and special provisions. Farmers may select from various types of policies. Multiple-peril crop insurance (MPCI) policies are available for most insured crops. Other plans may not be available for some insured crops in some areas. Some policies listed below are not available nationwide; they are tested in pilot programs and available in selected states and counties. YIELD-BASED CROP COVERAGE: Actual Production History (APH) policies insure producers against yield losses due to natural causes such as drought, excessive moisture, hail, wind, frost, insects, and disease. The farmer selects the amount of average yield he or she wishes to insure; from percent (in some areas to 85 percent), in increments of 5 percent. The farmer also selects the percent of the predicted price he or she wants to insure; between 55 and 100 percent of the crop price established annually by RMA. If the harvest is less than the yield insured, the farmer is paid an indemnity based on the difference

14 Indemnities are calculated by multiplying this difference by the insured percentage of the established price selected when crop insurance was purchased. Group Risk Plan (GRP) policies use a county index as the basis for determining a loss. When the county yield for the insured crop, as determined by the National Agricultural Statistics Service (NASS), falls below the trigger level chosen by the farmer, an indemnity is paid. Payments are not based on the individual farmer s loss records. Yield levels are available for up to 90 percent of the expected county yield. GRP protection involves less paperwork and costs less than the farm-level coverage described above. However, individual crop losses may not be covered if the county yield does not suffer a similar level of loss. This insurance is most often selected by farmers whose crop losses typically follow the county pattern. Dollar Plan policies provide protection against declining value due to damage that causes a yield shortfall. Amount of insurance is based on the cost of growing a crop in a specific area. A loss occurs when the annual crop value is less than the amount of insurance. The maximum dollar amount of insurance is stated on the actuarial document. The insured may select a percent of the maximum dollar amount equal to CAT (catastrophic level of coverage), or purchase additional coverage levels. CROP REVENUE INSURANCE PLANS: Group Risk Income Protection (GRIP) make indemnity payments only when the average county revenue for the insured crop falls below the revenue chosen by the farmer. Adjusted Gross Revenue (AGR) policies provide protection against low revenue due to unavoidable natural disasters and market fluctuations that occur during the insurance year. AGR policies insure revenue of the entire farm rather than an individual crop by guaranteeing a percentage of average gross farm revenue, including a small amount of livestock revenue. The plan uses information from a producer s Schedule F tax forms, and current year expected farm revenue, to calculate policy revenue guarantee. Adjusted Gross Revenue Lite (AGR-L) AGR-Lite is a whole-farm revenue protection plan of insurance which protects against low revenue due to unavoidable natural disaster and market fluctuations. Most farm-raised corps, animals, and animal products are eligible

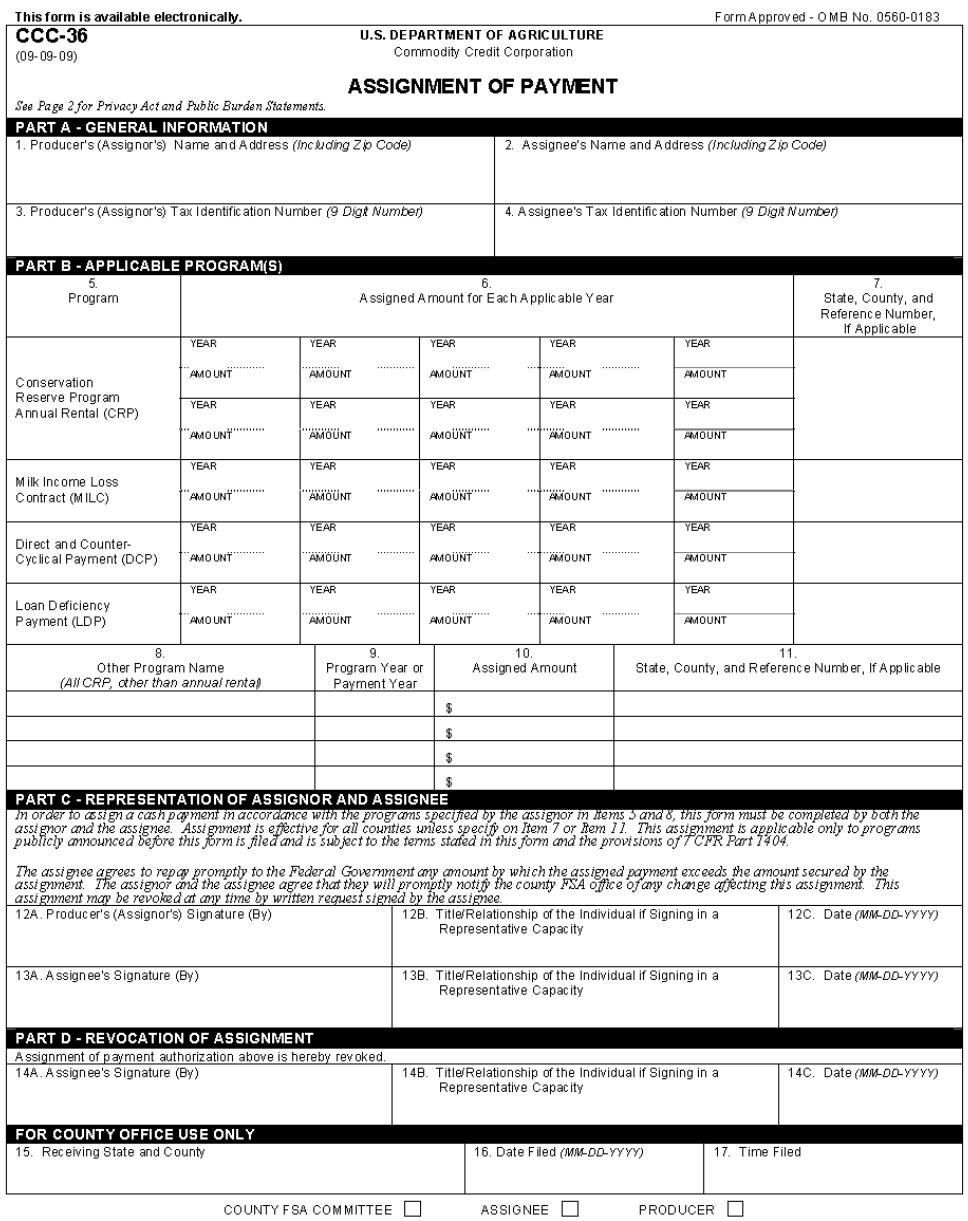

15 AGR-Lite can stand alone or be used in conjunction with other Federal crop insurance plans except Adjusted Gross Revenue (AGR). Income Protection (IP) policies protect producers against reductions in gross income when either a crop s price or yield declines from early-season expectations. To determine coverage, see the policy provisions. Revenue Assurance (RA) policies provide dollar-denominated coverage by the producer selecting a dollar amount of target revenue from a range defined by percent of expected gross revenue. For whole farm units the coverage level can be up to 85 percent of expected gross revenue. To determine coverage, see the policy provisions. Catastrophic Coverage (CAT) pays 55 percent of the established price of the commodity on crop losses in excess of 50 percent. The premium on CAT coverage is paid by the Federal Government; however, producers must pay a $100 administrative fee for each crop insured in each county. Limited-resource farmers may have this fee waived. CAT coverage is not available on all types of policies. ASSIGNMENT OF FEDERAL FARM PROGRAM PAYMENTS: The federal government makes billions of dollars of payments to agricultural producers under a wide variety of programs, the goal of which may be price support, conservation or disaster assistance. Some programs are tied to the production history of a particular tract of farm property, while other programs, relate to the tract itself, i.e. the farmer receives payment for taking the tract out of production. The same principles apply to livestock, such as removing a dairy herd from milk production. Producing a crop for market, processing livestock or completing a conservation practice can take a long time. Farmers may not always have the ready cash to pay for goods and services while the crop is being grown, the livestock fattened or the conservation practice completed. At the same time, a farmer may have money coming in from one or more programs administered by the Farm Service Agency ( Farm Service Agency ) and the Commodity Credit Corporation ( CCC ). Farmers may arrange to have all or part of their cash payments made directly to another party, such as the Bank. Such an arrangement is called an Assignment of Payment. The conservation payments are 10-13

16 general intangibles. The crops are farm products. The Bank must also have a security agreement covering the collateral and should perfect its security interest by filing a UCC-1 financing statement. Payments may be assigned for all Farm Service Agency and CCC programs that have been publicly announced, except farm loans, commodity loans, and purchase agreement proceeds. Form CCC-36, Assignment of Payment, must be used to assign all Farm Service Agency and CCC farm program payments. This form may be downloaded from payments.htm. Forms CCC-251 and CCC-252 are used to assign other CCC payments. Farmers may assign any program benefits that are applicable to Farm Service Agency or CCC farm programs. After an assignment is filed with the local Farm Service Agency office, the farmer and the Bank (assignee) should immediately notify Farm Service Agency if there is any change that could affect the assignment. CAUTION: If there is any indebtedness owed by the farmer to the Federal Government on the day a payment is being made, that amount may be subtracted from the assigned payment before it is made to the assignee according to the Special Provisions Relating to Assignments on Form CCC-36. COMMODITY FUTURES CONTRACTS: EQUITY INTEREST IN AGRICULTURAL COOPERATIVES: Farmer/Borrowers often purchase and sell commodity futures contracts through commodity brokerage firms to protect themselves against unanticipated adverse changes in the future prices of their crops, livestock and other commodities. These contracts, if held in a securities account are financial assets of the debtor. Bank Counsel should be consulted if the Bank intends to take and perfect a security interest in a farmer/borrower s rights under commodity futures contracts which are not held by a financial intermediary. See Investment Property in Chapter 6. Certificates issued to a Borrower to evidence the Borrower s equity interest in an agricultural cooperative, which, for example, processes and sells a farmer s milk or grain, are general intangibles. See General Intangibles in Chapter

17 III. WAREHOUSE RECEIPTS OVERVIEW: If a Borrower s harvested crops are stored off the farm premises in a warehouse, title to the crops may be evidenced by electronic or paper warehouse receipts. Warehouse receipts, bills of lading and other negotiable documents of title are generally defined as receipts issued by a person engaged in the business of storing, transporting or forwarding goods for hire which act as evidence of title to such goods. [UCC 9.102(a)(30)] A warehouse receipt is a document that describes goods stored in a warehouse and, generally, (i) entitles the person in possession of it to receive, hold and dispose of the document and the goods that it covers and (ii) is a commitment by the issuer to deliver the described goods to the owner of the receipt and to use reasonable care to protect the goods from damage. Bills of lading are documents of title issued by a carrier in connection with the shipment of goods. They enable a remote buyer and a remote seller to consummate a transaction with limited risk to either party. WAREHOUSES: WAREHOUSE CHARACTERISTICS: Warehouse receipt financing often is used as a hedge against supply shortages and price fluctuations. It also is used to cope with seasonal inventory buildups, especially in the agricultural industry. Warehouse receipt financing enables the borrower to avoid (i) the fixed repayment terms of many other credit arrangements and (ii) holding idle borrowed funds. A warehouse should be bonded and owned and operated by a third party that is independent of the borrower. The Bank should avoid a bonded subsidiary warehouse in which the borrower has an interest unless warehouse receipts are not the main value of the Bank s collateral. A terminal warehouse engaging in general storage for the public is the typical issuer of warehouse receipts that are taken as collateral. The inventory held in a warehouse can be finished goods with high 10-15

18 marketability, raw materials or agricultural products. The storage agreement between a borrower and a third-party warehouse should acknowledge the Bank s security interest in the stored goods, obligate the borrower to pay all warehouse charges and, if possible, waive or subordinate any statutory warehouse lien to the security interest of the Bank. As a practical matter, it is often difficult to obtain the requested waiver, subordination or release. The holder of a statutory landlord or warehousemen s lien generally is protected as to rentals or charges, and more, if notice is given to other lienholders (e.g., the Bank). If the warehouseman refuses, the Bank will have to make a judgment call as to the importance of obtaining a release, waiver or subordination. Before agreeing to accept warehouse receipts as collateral, the Bank should determine whether the issuing warehouse is acceptable. Among the matters to be investigated are: the adequacy of bonding; the adequacy of the warehouse s insurance coverage; if the warehouse is leased, the lease term must equal or exceed the duration of the contemplated secured transaction; the physical adequacy of the warehouse facility and its method of operation; the experience of the warehouse; and the financial status, credit rating and general reputation of the warehouse. NON-NEGOTIABLE AND NEGOTIABLE RECEIPTS: Warehouse receipts and bills of lading can be either non-negotiable or negotiable. A non-negotiable receipt is preferable to a negotiable receipt as collateral as there is less risk of loss. The Bank can retain possession of a non-negotiable receipt when goods are released. A non-negotiable warehouse receipt specifies the person to whom the described goods are to be delivered without adding either bearer or order, the words of negotiability. The Bank must be named by a non-negotiable receipt as the person to whom the goods are to be delivered, otherwise it is unacceptable as collateral

19 A negotiable warehouse receipt contains words of negotiability, either stating that the described goods are to be delivered to any bearer of the receipt or stating that the described goods are to be delivered to the order of a named person. A bearer receipt is negotiated by delivery of the receipt to a transferee. An order receipt is negotiated by the signature of the named person to whose order it runs, plus delivery to a transferee. In order to be acceptable as collateral, the borrower to whose order the negotiable receipt should run must endorse it with an endorsement that states that the receipt thereafter runs to the order of the Bank. The Bank should obtain the borrower s guaranty of the signatures of any unknown endorsers of negotiable receipts. TERMS OF A WAREHOUSE RECEIPT: A warehouse receipt should contain: the name and location of the warehouse; in the case of negotiable receipts, a statement that the goods are deliverable either to bearer or to a specified person or his or her order ; in the case of non-negotiable receipts, a statement that the goods will be delivered to a specified person without also using either bearer or order words; the date that the receipt is issued; the consecutive number of the receipt; either the rate of storage and handling charges of a terminal or field warehouse or a statement that a non-negotiable receipt was issued by a field warehouse; a description of the goods or of the packages contained, identifying them by weight, quantity, etc.; the signature of the issuing warehouse made by an authorized agent of the warehouse; the name and address of every person, including the issuing warehouse, with an ownership interest in the stored goods; and a statement of the advances and other liabilities for which the issuing warehouse claims a lien or a security interest. The amount of the advances or other liabilities should be specified to the extent known at the time of issue. CAUTION: Unless the Bank is knowledgeable regarding the form of negotiable receipts, Bank Counsel should be consulted to review the warehouse receipts 10-17

20 being taken as collateral. PERFECTION OF SECURITY INTEREST: If the receipt is non-negotiable, a security interest is perfected in the stored goods by the issuance of the receipt in the name of the Bank. [UCC 9.312(d)] If the receipt is negotiable, it must be endorsed to the Bank, delivered to the Bank, and retained in the Bank s possession to perfect a security interest in the stored goods. [UCC 9.312(c)] In either case, a UCC-1 Financing Statement that describes both the warehouse receipt and the stored goods by item or type as collateral should always be filed. [UCC 9.312(a) (perfection by filing)] Accompanying security agreements should also describe both the warehouse receipt and the stored goods as collateral. The Bank perfects a security interest in bills of lading in the same manner as it perfects a security interest in warehouse receipts. INFLOW AND OUTFLOW OF WAREHOUSE GOODS: All goods received by the warehouse should be formally documented at the time received, and the Bank should receive a copy of the warehouse s record of the receipt of such goods. If a warehouse receipt was issued in non-negotiable form, the warehouse receipt need not be presented to the warehouse in order to release the stored goods, but a warehouse release form should be executed by the Bank. A release form should be prepared by the borrower and presented to the Bank, together with a check for the agreed-upon percentage of the advance covering the stored goods described in the release. An effective warehouse release should contain: the name and location of the warehouse; the warehouse receipt number; a description of the type and quantity of the stored goods to be released; the agreed-upon release value of the stored goods to be released; the name of the person to whom release is authorized; and an authorized signature of the Bank. If a warehouse receipt was issued in negotiable form, the Bank must surrender the warehouse receipt to the borrower and execute a release. The borrower, however, must be required to execute a 10-18

21 MONITORING THE STORED GOODS: security agreement-trust receipt describing the negotiable receipt as collateral before the Bank surrenders the negotiable receipt. The security agreement-trust receipt serves two functions: (i) it documents the date upon which the negotiable warehouse receipt was delivered to the borrower; and (ii) it sets out the rights of the borrower and the Bank. The security agreement-trust receipt supplements the Security Agreement. Upon completion of the withdrawal, the negotiable warehouse receipt (that either has been canceled or had a partial delivery noted upon it) should be returned to the Bank by the borrower, along with payment of the agreedupon percentage of the amount advanced upon the stored goods to be released. Upon redelivery of the negotiable receipt and delivery of the payment, the Security Agreement Trust-Receipt covering the negotiable receipt is to be canceled. The Bank should closely monitor the market value and quality of the goods stored in a warehouse, especially agricultural products. A warehouse should be required to deliver a detailed monthly goods and value report to the Bank for comparison with the Bank s records. This report should summarize all transactions by individual item, by units and by dollar value. The report should make the borrower and the Bank aware of problems, (e.g., slow movers, possible shortages, etc.) Physical inspection of the warehoused goods by the Bank should be authorized by the storage agreement. If the storage agreement does not authorize inspections, the Bank should get consent from the warehouse. In addition, check Specific Property Description and describe the negotiable warehouse receipts or bills of lading with collateral descriptions such as: Warehouse receipt issued by [warehouseman] covering [quantity] of [goods] and dated and all goods covered thereby. Negotiable bill of lading issued by [carrier] covering [quantity] of [goods] and dated and all goods covered thereby. SPECIAL BANKRUPTCY CONSIDERATIONS: Section 522 of the Bankruptcy Code determines what property a debtor may exempt in a bankruptcy proceeding. Under 522(b), a debtor may choose between the federal exemptions set forth in 10-19

22 MEDIATION: REGULATION Z: 522(d) or the exemptions provided by state law. If a state s exempt property laws are significantly more favorable to debtors than the federal exemptions, bankruptcy debtors almost always choose the state exemptions. In addition to creating federal exemptions and preserving state exemptions, 522(f) permits a debtor to avoid certain non-possessory, non-purchase money liens to the extent that the lien impairs an exemption to which the debtor would have been entitled under state exempt property law. What constitutes exempt property is a matter of state law, but the dollar amount of the available exemption cannot exceed a certain statutory amount [$6,225 in 2014]. This effectively allows farmers to claim as exempt personal property their tractors, combines and other vehicles which are frequently used to collateralize operating lines of credit. Section 502 of the Agricultural Credit Act of 1987 authorized the U.S. Secretary of Agriculture to help states develop USDA Certified State Mediation Programs to resolve disputes between farmers and agricultural lenders. These programs are administered by the USDA Farm Service Agency and exist in more than 30 states, Banks should consider using a Certified Mediation Program as a dispute resolution option. Agricultural purpose loans are transactions exempted from the requirements of the Truth-in-Lending Act/Regulation Z. Under Regulation Z, the term agricultural purposes includes the production, harvest, exhibition, marketing, transportation, processing or manufacture of agricultural products by a natural person who cultivates, plants, propagates or nurtures those agricultural products, including but not limited to the acquisition of farmland, real property with a farm residence, and personal property and services used primarily in farming. For purposes of Regulation Z, the term agricultural products includes agricultural, horticultural, viticultural and dairy products, livestock, wildlife, poultry, bees, forest products, fish and shellfish and any products thereof, including processed and manufactured products, and any and all products raised or produced on farms and any processed or manufactured products thereof

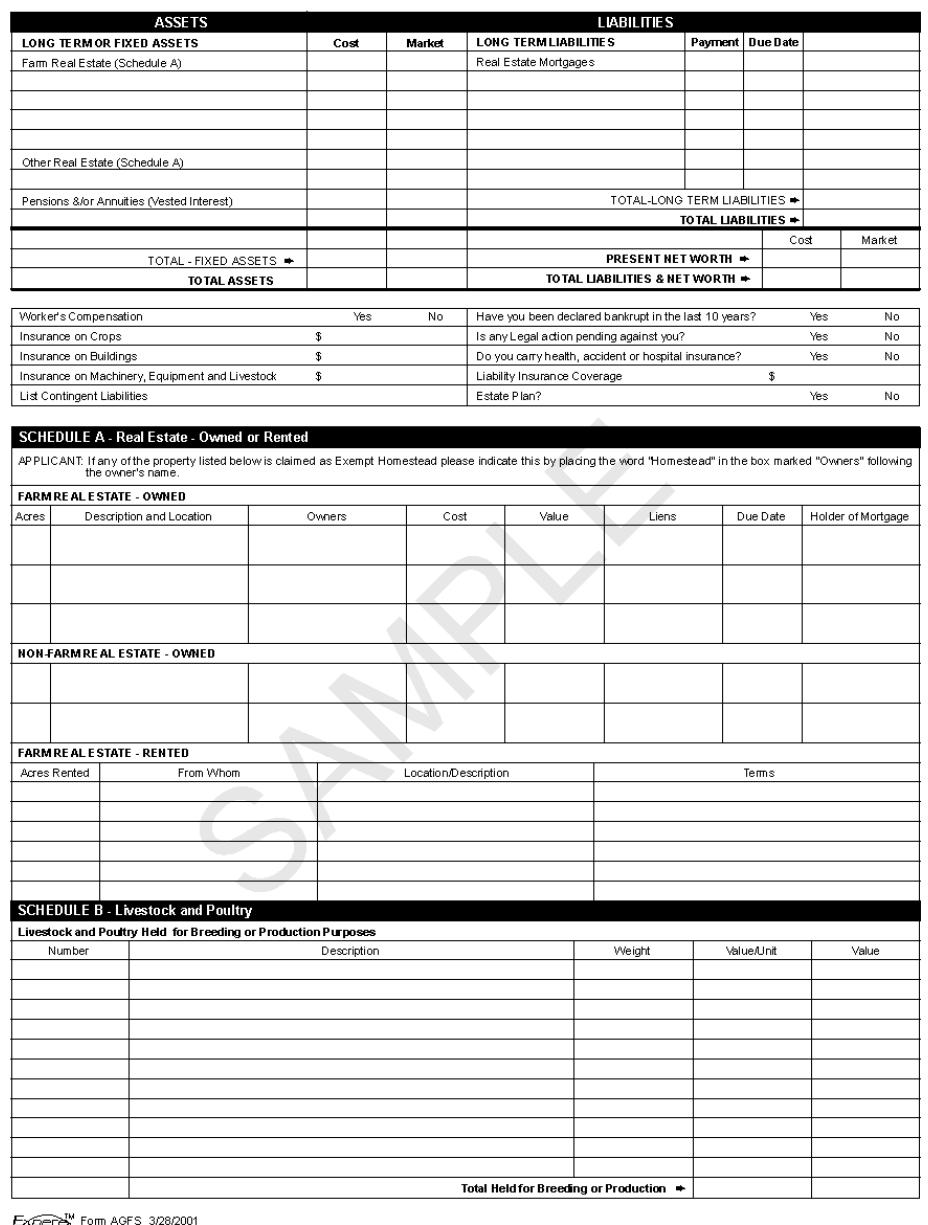

23 IV. DOCUMENT CHECKLIST DOCUMENTS REQUIRED FOR FARM PRODUCTS: Loan Application. Current Financial Statement of Borrower. See the form Agricultural Financial Statement at the end of this chapter. This form is produced and copyrighted by Bankers Systems, Inc. Authorization Documentation. Title Verification Documentation. Promissory Note. Security Agreement. See the form Commercial Security Agreement at the end of Chapter 4. This form includes an option box for Farm Products, Equipment, Accounts and documents and contains an excellent covenant requiring the Borrower to provide the Bank with a list of buyers for FSA prenotification purposes. Form UCC-1 Financing Statement. The Bank should file Form UCC-1 Financing Statement and should obtain a search reflecting such filing prior to funding the loan. As noted, the form used by the Bank should be the form authorized for use in the office in which the filing is made, in most states, the Office of the Secretary of State. As a general rule, the Form UCC-1 should reflect the language describing the collateral set forth in the security agreement. In completing Form UCC-1, the Bank should consider the following matters: If the Bank is taking a security interest in all items used in a farm operation, the general description may state: All of the following property of Debtor now owned, hereafter acquired or produced: all farm products including, but not limited to, all livestock and their products, feed, feed additives, feed supplements; all crops, whether annual or perennial, seed, fertilizer, chemicals and supplies; all equipment including, farm machinery, tools and other implements and all additions, accessions, parts and equipment now or hereafter incorporated into, affixed to or used in connection with said equipment; all inventory; all now existing or hereafter arising; all 10-21

24 documents, chattel paper and notes receivable; all investment property including all commodities futures contracts, margin deposits and any funds maintained by any broker for the benefit of Debtor; and all general intangibles including all government payments and payments-in-kind to which Debtor may now or hereafter be entitled; Supplements to be added when applicable: The aforementioned livestock will include, but not limited to livestock branded (sketch of brand) on (location on animal). All fixtures located on the property described as [legal description of the property] NOTE: A real property description is not required on crop filings but is required on fixture filings. If the Bank is taking a security interest in only certain items the description should be specific such as: * Crops: All of Debtor s crops, including, but not limited to, (describe here the specific type(s) of crops to be taken, e.g., cotton, corn, oranges, etc.), now growing or to be grown, together with all seed, fertilizer, chemicals and supplies, plus all products thereof, and any and all proceeds arising from the disposition thereof and all accounts and general intangibles. * Livestock: All livestock now owned or hereafter acquired by Debtor and the young conceived thereof, together with all increases thereof wherever located and all feed, feed additives, feed supplements, including any and all product and proceeds arising therefrom to be added when applicable. The aforementioned livestock will include, but not be limited to livestock branded (sketch of brand) on (location on animal)

25 Food Security Act List. A Listing of Potential Buyers, Selling Agents and Commission Merchants to or through whom the Borrower may sell the farm products covered by the security agreement should be obtained from the Borrower. This list should be verified and, if needed, amended annually through a Verification of List of Potential Buyers. Sample forms for the Borrower to complete are located at the end of this chapter. These forms are produced and copyrighted by Bankers Systems, Inc. Assignment of Federal Program Payments. If the Borrower has rights under one or more federal payment programs administered by the CCC or the Farm Service Agency, Forms CCC-36, CCC-251 and/or CCC-352 should be completed and filed. Food Security Act Prenotification. A Notice of Security Interest should be sent at least annually to every potential buyer of the Borrower s farm products. It is suggested that this be sent by certified mail. In the alternative, if the state is a CNS state, the Bank should (i) file an EFS in the form approved by that state and (ii) be a CNS subscriber and check the CNS master list annually to assure that all of the Borrower s potential buyers are on the master list. A Notice of Security Interest form and Notice of Termination of Security Interest form, both produced and copyrighted by Bankers Systems, Inc. are located at the end of this chapter. Landlord s Waiver. This should be considered if crops are grown on land under lease or mortgage (may take the form of right to go upon the land to maintain and harvest ) or farm equipment is or will be located on leased premises or on mortgaged premises and a UCC-1 fixture filing is made by the Bank. Consult Bank Counsel regarding preparation of an landlord s waiver with respect to equipment and crops. Insurance Policy with endorsement naming the Bank as loss payee. With respect to crops this should include: Fire insurance on grain crops; Hail insurance if crops are in an area with a history of hail damage; Frost insurance when appropriate and available; and 10-23

26 Flood insurance when appropriate and available. Federal All Risk Insurance, if available, may cover the above plus additional risks. A general liability policy is also recommended. ADDITIONAL DOCUMENTS FOR WAREHOUSE RECEIPTS: Security Agreement. Check Document. In addition, check Specific Property Description and describe the negotiable warehouse receipts with collateral descriptions such as: Warehouse receipt issued by [warehouseman] covering [quantity] of [goods] and dated and all goods covered thereby. Form UCC-1 Financing Statement for all nonnegotiable warehouse receipts and bills of lading. Describe both the warehouse receipts or bills of lading, and the items or types of stored or shipped goods as collateral. Title Verification Documentation: Warehouse Receipts or Bills of Lading. Negotiable or non-negotiable. Collateral Receipt. A sample form is located at the end of Chapter. Guaranties of the signatures of endorsers of negotiable receipts, if needed. Report verifying the financial condition of the warehouse, including proof of the existence and the amount of bonding. Copy of any Warehouse Lease. Copy of Warehouse Storage Agreement. Warehouse Waiver or Subordination. Goods Grading Certificate with respect to the stored goods. A memorandum from the loan officer, accompanying a warehouse receipt, stating the percentage of advance and the release value and, if no known market exists, the value of the collateral and the method by which it was determined. Hazard Insurance. Comprehensive casualty insurance, including 10-24

27 flood insurance, naming the Bank as loss payee. Formal verification by the warehouse of the validity of any outstanding receipts to be taken as collateral. Proof of authorization of Agent signing warehouse receipt in place of warehouseman, if needed. Formal consent by the warehouse to periodic inspection of the stored goods by the Bank if this formal consent does not appear in the storage agreement. Copies of all warehouse receiving records, which should be reconciled with the inventory reports mentioned above, which are received at regular time intervals. Regular, detailed, inventory reports from the warehouse, verifying quantities and value of the inventory on hand together with a monthly statement from the warehouse verifying that all accrued warehousing fees and charges have been paid by the borrower. Authorization for the release of merchandise, on behalf of the borrower and the Bank. If the receipts are negotiable, Security Agreement-Trust Receipts to be executed before a negotiable receipt is surrendered to the borrower. V. FORMS FORMS: The forms referenced in this chapter appear in the following order: * Verification of List of Potential Buyers * Notice of Security Interest * CCC-36 Assignment of Payment * Agricultural Financial Statement * Notice of Termination of Security Interest * Agricultural Lending Limits 10-25

28 10-26

29 10-27

30 10-28

31 10-29

32 10-30

33 10-31

34 10-32

35 10-33

36 10-34

37 10-35

38 10-36

39 10-37

40 10-38

Your State Association Presents. Program Materials

Your State Association Presents Lenders Learn TM Chapter 10 Agricultural Lending Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure

Your State Association Presents Lenders Learn TM Chapter 10 Agricultural Lending Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure

INTRODUCTION. While significant attention has recently been focused on production contracts with large,

June 2009 FARM LEGAL SERIES Agricultural Production Contracts Phillip L. Kunkel, Jeffrey A. Peterson, Jessica A. Mitchell Copyright 2009 Regents of the University of Minnesota. All rights reserved. INTRODUCTION

June 2009 FARM LEGAL SERIES Agricultural Production Contracts Phillip L. Kunkel, Jeffrey A. Peterson, Jessica A. Mitchell Copyright 2009 Regents of the University of Minnesota. All rights reserved. INTRODUCTION

Prepare, print, and e-file your federal tax return for free!

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

Risk Management Agency Dave Schumann

Risk Management Agency Dave Schumann History In 1938 the Federal Crop Insurance Corporation, or FCIC, was created. In 1980, the FCIC act was amended to expand to all states and primary field crops. This

Risk Management Agency Dave Schumann History In 1938 the Federal Crop Insurance Corporation, or FCIC, was created. In 1980, the FCIC act was amended to expand to all states and primary field crops. This

REVISED ARTICLE 9 AND IOWA CHAPTER 570 LANDLORD LIENS

REVISED ARTICLE 9 AND IOWA CHAPTER 570 LANDLORD LIENS By: Jason M Finch, M.B.A., J.D., LL.M. Norelius & Nelson, P.C. 1317 Broadway P.O. Box 278 Denison, Iowa 51442 (712) 263-4245 1-888-669-2942 Prepared

REVISED ARTICLE 9 AND IOWA CHAPTER 570 LANDLORD LIENS By: Jason M Finch, M.B.A., J.D., LL.M. Norelius & Nelson, P.C. 1317 Broadway P.O. Box 278 Denison, Iowa 51442 (712) 263-4245 1-888-669-2942 Prepared

CROP LOAN GUARANTEE PROGRAM

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

Basics of UCC Article 9 -- Your Guide to Security Interests

Basics of UCC Article 9 -- Your Guide to Security Interests June 28, 2018 Panelists: James C. Schulwolf (moderator), Shipman & Goodwin LLP, Hartford, CT R. Marshall Grodner, McGlinchey Stafford, Baton

Basics of UCC Article 9 -- Your Guide to Security Interests June 28, 2018 Panelists: James C. Schulwolf (moderator), Shipman & Goodwin LLP, Hartford, CT R. Marshall Grodner, McGlinchey Stafford, Baton

University of Arkansas. An Agricultural Law Research Project. Statutory Agricultural Lien Rapid Finder Chart. State of Washington

University of Arkansas An Agricultural Law Research Project Statutory Agricultural Lien Rapid Finder Chart State of Washington Originally published 1993 by Martha L. Noble Updated 2008 by Elizabeth R.

University of Arkansas An Agricultural Law Research Project Statutory Agricultural Lien Rapid Finder Chart State of Washington Originally published 1993 by Martha L. Noble Updated 2008 by Elizabeth R.

Policies Revenue Protection (RP) Yield Protection (YP) Group Risk Income Protection (GRIP) Group Risk Protection (GRP)

Yield Protection (YP) Group Risk Income Protection (GRIP) Group Risk Protection (GRP)") Policies Revenue Protection (RP) Yield Protection (YP) Group Risk Income Protection (GRIP) Group Risk Protection (GRP) RP What is Revenue Protection? A Revenue Protection (RP) policy protects a policyholder

Policies Revenue Protection (RP) Yield Protection (YP) Group Risk Income Protection (GRIP) Group Risk Protection (GRP) RP What is Revenue Protection? A Revenue Protection (RP) policy protects a policyholder

CITY OF DE PERE REVOLVING LOAN FUND MANUAL. Prepared by the: Planning and Economic Development Department

CITY OF DE PERE REVOLVING LOAN FUND MANUAL Prepared by the: Planning and Economic Development Department In conjunction with the Wisconsin Economic Development Corporation Adopted: January 15, 2013 TABLE

CITY OF DE PERE REVOLVING LOAN FUND MANUAL Prepared by the: Planning and Economic Development Department In conjunction with the Wisconsin Economic Development Corporation Adopted: January 15, 2013 TABLE

Monday, June 19, 2017 Ag Law Rooms: Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m.

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

FSA Direct Loans Loan Making

FSA Direct Loans Loan Making CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can

FSA Direct Loans Loan Making CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can

Personal Property Security Agreement

Personal Property Security Agreement (This form is intended for use in Washington State consumer transactions and for related personal property specified in Exhibit A; it is not intended for general use

Personal Property Security Agreement (This form is intended for use in Washington State consumer transactions and for related personal property specified in Exhibit A; it is not intended for general use

Minimizing Risk on Problematic Ag Loans

Minimizing Risk on Problematic Ag Loans November 3, 2015 Today s Presenters: Lynn W. Hartman (319) 896-4083 lhartman@simmonsperrine.com Eric W. Lam (319) 896-4018 elam@simmonsperrine.com Christopher K.

Minimizing Risk on Problematic Ag Loans November 3, 2015 Today s Presenters: Lynn W. Hartman (319) 896-4083 lhartman@simmonsperrine.com Eric W. Lam (319) 896-4018 elam@simmonsperrine.com Christopher K.

Balance Sheet and Schedules

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

Agricultural Disaster Assistance

Order Code RS21212 Updated July 3, 2008 Summary Agricultural Disaster Assistance Ralph M. Chite Specialist in Agricultural Policy Resources, Science, and Industry Division The U.S. Department of Agriculture

Order Code RS21212 Updated July 3, 2008 Summary Agricultural Disaster Assistance Ralph M. Chite Specialist in Agricultural Policy Resources, Science, and Industry Division The U.S. Department of Agriculture

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Fall Article 9 Priorities (Revised)

") Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Article 9 Priorities (Revised) I. The Concept: If the value of collateral is insufficient to

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Article 9 Priorities (Revised) I. The Concept: If the value of collateral is insufficient to

APPLICATION / MASTER NOTE / SECURITY AGREEMENT

(A) LOAN REQUEST (B) APPLICANT INFORMATION APPLICATION / MASTER NOTE / SECURITY AGREEMENT $ Individual Legal Name [must be the same as driver s license] Loan requires at least one Individual Social Security

(A) LOAN REQUEST (B) APPLICANT INFORMATION APPLICATION / MASTER NOTE / SECURITY AGREEMENT $ Individual Legal Name [must be the same as driver s license] Loan requires at least one Individual Social Security

LIENS OUTSIDE ARTICLES 9 AND 8 OF THE UNIFORM COMMERCIAL CODE

Conflicting security interests in property has been a major source of litigation in the lending industry since common law times. With respect to real estate, early recording statutes went a long way towards

Conflicting security interests in property has been a major source of litigation in the lending industry since common law times. With respect to real estate, early recording statutes went a long way towards

PRACTICE CHECKLISTS MANUAL

LAW SOCIETY OF BRITISH COLUMBIA SECURITY AGREEMENT INTRODUCTION Purpose and currency of checklist. This checklist is designed to be used with the CLIENT IDENTIFICATION AND VERIFICATION PROCEDURE (A-1)

LAW SOCIETY OF BRITISH COLUMBIA SECURITY AGREEMENT INTRODUCTION Purpose and currency of checklist. This checklist is designed to be used with the CLIENT IDENTIFICATION AND VERIFICATION PROCEDURE (A-1)

Chapter VII SECURED TRANSACTIONS IN PERSONAL PROPERTY CONDENSED OUTLINE

Chapter VII SECURED TRANSACTIONS IN PERSONAL PROPERTY CONDENSED OUTLINE I. METHODS USED BEFORE UNIFORM COMMERCIAL CODE A. In General. B. Pledge. C. Trust Receipt. D. Chattel Mortgage. E. Conditional Sale.

Chapter VII SECURED TRANSACTIONS IN PERSONAL PROPERTY CONDENSED OUTLINE I. METHODS USED BEFORE UNIFORM COMMERCIAL CODE A. In General. B. Pledge. C. Trust Receipt. D. Chattel Mortgage. E. Conditional Sale.

PROTECTING YOURSELF THROUGH CONTRACTS AND LIENS

PROTECTING YOURSELF THROUGH CONTRACTS AND LIENS 2012 IOWA PORK REGIONAL CONFERENCES Eldon McAfee Beving, Swanson & Forrest, P.C. Des Moines, Iowa SWINE CONTRACTS after 6/18/08 Packers & Stockyards requirements

PROTECTING YOURSELF THROUGH CONTRACTS AND LIENS 2012 IOWA PORK REGIONAL CONFERENCES Eldon McAfee Beving, Swanson & Forrest, P.C. Des Moines, Iowa SWINE CONTRACTS after 6/18/08 Packers & Stockyards requirements

Banking Webinar. April 25, Daniel A. Beckman Michael S. Dove Dean M. Zimmerli

Banking Webinar April 25, 2018 Daniel A. Beckman dbeckman@gislason.com Michael S. Dove mdove@gislason.com Dean M. Zimmerli dzimmerli@gislason.com April 2018 Banking Webinar Section I By: Daniel A. Beckman

Banking Webinar April 25, 2018 Daniel A. Beckman dbeckman@gislason.com Michael S. Dove mdove@gislason.com Dean M. Zimmerli dzimmerli@gislason.com April 2018 Banking Webinar Section I By: Daniel A. Beckman

UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills

For further information please contact: UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills Paul Hodnefield Associate General Counsel

For further information please contact: UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills Paul Hodnefield Associate General Counsel

ILLINOIS FINANCE AUTHORITY GUARANTEED LOAN PROGRAMS LENDER S AGREEMENT

ILLINOIS FINANCE AUTHORITY GUARANTEED LOAN PROGRAMS LENDER S AGREEMENT The purpose of this Lender s Agreement (the Agreement ) is to establish Lender as an approved participant in the guaranteed loan programs

ILLINOIS FINANCE AUTHORITY GUARANTEED LOAN PROGRAMS LENDER S AGREEMENT The purpose of this Lender s Agreement (the Agreement ) is to establish Lender as an approved participant in the guaranteed loan programs

Principles of Business Credit

Principles of Business Credit National Education Department 8840 Columbia 100 Parkway, Columbia, MD 21045-2158 Fax: 410-740-5574 Email: education_info@nacm.org Eighth Edition UCC ARTICLE 2 SALES OFFER

Principles of Business Credit National Education Department 8840 Columbia 100 Parkway, Columbia, MD 21045-2158 Fax: 410-740-5574 Email: education_info@nacm.org Eighth Edition UCC ARTICLE 2 SALES OFFER

CONTRACTS: LEARNING FROM THE EXPERIENCE OF DIFFICULT ECONOMIC TIMES IOWA PORK CONGRESS

CONTRACTS: LEARNING FROM THE EXPERIENCE OF DIFFICULT ECONOMIC TIMES IOWA PORK CONGRESS Jan. 28, 2010 Eldon McAfee Beving, Swanson & Forrest, P.C. Des Moines, Iowa CONTRACT DEFAULT Communicate with the

CONTRACTS: LEARNING FROM THE EXPERIENCE OF DIFFICULT ECONOMIC TIMES IOWA PORK CONGRESS Jan. 28, 2010 Eldon McAfee Beving, Swanson & Forrest, P.C. Des Moines, Iowa CONTRACT DEFAULT Communicate with the

Noninsured Crop Disaster Assistance Program

Program Intent The Noninsured Crop Disaster Assistance Program (NAP) is a risk management tool designed to reduce financial losses that occur when natural disasters cause a loss of production or prevented

Program Intent The Noninsured Crop Disaster Assistance Program (NAP) is a risk management tool designed to reduce financial losses that occur when natural disasters cause a loss of production or prevented

Credit Enhancements: Beyond the Personal Guaranty. Thomas R. Fawkes and Brian J. Jackiw Goldstein & McClintock LLLP

Credit Enhancements: Beyond the Personal Guaranty Thomas R. Fawkes and Brian J. Jackiw Goldstein & McClintock LLLP Warning Signs of Impending Default Deviations in the manner or timing of counterparty

Credit Enhancements: Beyond the Personal Guaranty Thomas R. Fawkes and Brian J. Jackiw Goldstein & McClintock LLLP Warning Signs of Impending Default Deviations in the manner or timing of counterparty

UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills

For further information please contact: UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills Paul Hodnefield Associate General Counsel

For further information please contact: UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills Paul Hodnefield Associate General Counsel

UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills

For further information please contact: UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills Paul Hodnefield Associate General Counsel

For further information please contact: UCC Article 9 & Other Lien-Related Legislation Includes Tax Lien, Judgment Lien, Real Estate Lien and Fraudulent Filing Bills Paul Hodnefield Associate General Counsel

United States Department of Agriculture Farm Service Agency. Risky Business. 27 th Women in Ag Conference Kearney, Nebraska - February 23/24, 2012

Risky Business 27 th Women in Ag Conference Kearney, Nebraska - February 23/24, 2012 Farming today takes more than a tractor & a plow. This workshop will explore different programs USDA offers that can

Risky Business 27 th Women in Ag Conference Kearney, Nebraska - February 23/24, 2012 Farming today takes more than a tractor & a plow. This workshop will explore different programs USDA offers that can

Loan Enforcement Improving the Odds of Recovery. By Michael A. Campbell Polsinelli Shughart PC

Loan Enforcement Improving the Odds of Recovery By Michael A. Campbell Polsinelli Shughart PC Copyright 2009 Contents 1. Good Underwriting 2. Speed and its Effect on Recoveries 3. Pre-Enforcement Asset

Loan Enforcement Improving the Odds of Recovery By Michael A. Campbell Polsinelli Shughart PC Copyright 2009 Contents 1. Good Underwriting 2. Speed and its Effect on Recoveries 3. Pre-Enforcement Asset

Today s Presenter. The SBA Authorization Wisconsin SBA Lenders Conference May 19, SBA Loan Closing: Proper Documentation & Pitfalls

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

THE RICHLAND ELECTRIC COOPERATIVE REVOLVING LOAN FUND MANUAL

THE RICHLAND ELECTRIC COOPERATIVE REVOLVING LOAN FUND MANUAL The Rural Business Enterprise Grant (RBEG) Program, administered by the Wisconsin USDA Rural Development, provided the Richland Electric Cooperative

THE RICHLAND ELECTRIC COOPERATIVE REVOLVING LOAN FUND MANUAL The Rural Business Enterprise Grant (RBEG) Program, administered by the Wisconsin USDA Rural Development, provided the Richland Electric Cooperative

Ag Lending: Top 10 Lender Mistakes Snell & Wilmer

Ag Lending: Top 10 Lender Mistakes 1 Snell & Wilmer Overview Full-service business law firm, representing corporations, small businesses, and individuals Founded in 1938 in Phoenix, Arizona More than 400

Ag Lending: Top 10 Lender Mistakes 1 Snell & Wilmer Overview Full-service business law firm, representing corporations, small businesses, and individuals Founded in 1938 in Phoenix, Arizona More than 400

Agricultural Business Management

Agricultural Business Management Farm Legal Series Phillip L. Kunkel, Jeffrey A. Peterson, P. Jason Thibodeaux, Dorraine Larison, Matthew Webster, Betsy Whitlatch, S. Scott Wick, Kathi J. Wright Attorneys,

Agricultural Business Management Farm Legal Series Phillip L. Kunkel, Jeffrey A. Peterson, P. Jason Thibodeaux, Dorraine Larison, Matthew Webster, Betsy Whitlatch, S. Scott Wick, Kathi J. Wright Attorneys,

Farm Service Agency Programs Overview. USDA is an equal opportunity provider, employer, and lender.

Farm Service Agency Programs Overview Farm Service Agency (FSA) Overview Part of U.S. Department of Agriculture (USDA), under Farm and Foreign Agriculture Services (FFAS) Farm programs, loans to help agricultural

Farm Service Agency Programs Overview Farm Service Agency (FSA) Overview Part of U.S. Department of Agriculture (USDA), under Farm and Foreign Agriculture Services (FFAS) Farm programs, loans to help agricultural

COLLEGE OF AGRICULTURE AND LIFE SCIENCES

COLLEGE OF AGRICULTURE AND LIFE SCIENCES COOPERATIVE EXTENSION AZ1587 January 2013 An Overview of Risk Management Agency Insurance Products and Farm Service Agency Programs Available for Arizona Agricultural

COLLEGE OF AGRICULTURE AND LIFE SCIENCES COOPERATIVE EXTENSION AZ1587 January 2013 An Overview of Risk Management Agency Insurance Products and Farm Service Agency Programs Available for Arizona Agricultural

FSA Guaranteed Loans

FSA Guaranteed Loans CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can change

FSA Guaranteed Loans CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can change

4. equipment: catch all ; goods other than inventory, farm products, and consumer goods; used or bought for use primarily in business

Secured Transactions Prof. Payne Chapter 1. Goods: all things that are movable when a security interest attaches 1. consumer goods: goods that are used or bought for use primarily for personal, family

Secured Transactions Prof. Payne Chapter 1. Goods: all things that are movable when a security interest attaches 1. consumer goods: goods that are used or bought for use primarily for personal, family

VILLAGE OF LITTLE CHUTE SMALL BUSINESS MICRO LOAN PROGRAM

VILLAGE OF LITTLE CHUTE SMALL BUSINESS MICRO LOAN PROGRAM CONTACT Charles P. Kell, Village Administrator 108 West Main Street Little Chute, Wisconsin 54140 Telephone: (920) 788-7380 Ext. 202 E-mail: chuck@littlechutewi.org

VILLAGE OF LITTLE CHUTE SMALL BUSINESS MICRO LOAN PROGRAM CONTACT Charles P. Kell, Village Administrator 108 West Main Street Little Chute, Wisconsin 54140 Telephone: (920) 788-7380 Ext. 202 E-mail: chuck@littlechutewi.org

Supplemental Revenue Assistance Payments Program (SURE): Montana

: Montana") Supplemental Revenue Assistance Payments Program (SURE): Montana Agricultural Marketing Policy Center Linfield Hall P.O. Box 172920 Montana State University Bozeman, MT 59717-2920 Tel: (406) 994-3511 Fax:

Supplemental Revenue Assistance Payments Program (SURE): Montana Agricultural Marketing Policy Center Linfield Hall P.O. Box 172920 Montana State University Bozeman, MT 59717-2920 Tel: (406) 994-3511 Fax:

Secured Transactions Law School Legends Professor Michael I. Spak

Secured Transactions Law School Legends Professor Michael I. Spak Introduction What Article 9 is NOT: 99.99% of all sales. E.g., I sell you my tie for $1 down and $1 a month for 9 months. You stop making

Secured Transactions Law School Legends Professor Michael I. Spak Introduction What Article 9 is NOT: 99.99% of all sales. E.g., I sell you my tie for $1 down and $1 a month for 9 months. You stop making

A Guide to the USDA Noninsured Crop Disaster Assistance Program (NAP)

") A Guide to the USDA Noninsured Crop Disaster Assistance Program (NAP) For Organic Production, 2018 crop year By Michael Stein & Diana Jerkins, Ph.D. Table of Contents Introduction...4 Overview...4 Crop

A Guide to the USDA Noninsured Crop Disaster Assistance Program (NAP) For Organic Production, 2018 crop year By Michael Stein & Diana Jerkins, Ph.D. Table of Contents Introduction...4 Overview...4 Crop

CITY OF WASHBURN REVOLVING LOAN FUND. POLICIES AND PROCEDURES MANUAL (Revised February 10, 2017)

") CITY OF WASHBURN REVOLVING LOAN FUND POLICIES AND PROCEDURES MANUAL (Revised February 10, 2017) 1 TABLE OF CONTENTS FOREWORD... 3 SECTION 1. GENERAL PROVISIONS... 4 1.1 PURPOSE... 4 1.2 OBJECTIVES... 4

CITY OF WASHBURN REVOLVING LOAN FUND POLICIES AND PROCEDURES MANUAL (Revised February 10, 2017) 1 TABLE OF CONTENTS FOREWORD... 3 SECTION 1. GENERAL PROVISIONS... 4 1.1 PURPOSE... 4 1.2 OBJECTIVES... 4

The Top 10 Loan Documentation Mistakes

Your State Association Presents Lenders Learn TM The Top 10 Loan Documentation Mistakes Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast.

Your State Association Presents Lenders Learn TM The Top 10 Loan Documentation Mistakes Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast.

COMMODITY CREDIT CORPORATION NOTE AND SECURITY AGREEMENT TERMS AND CONDITIONS

This form is available electronically. See Page 7 for Privacy Act and Paperwork Reduction Act Statements. CCC-601 U.S. DEPARTMENT OF AGRICULTURE (11-13-17) Commodity Credit Corporation COMMODITY CREDIT

This form is available electronically. See Page 7 for Privacy Act and Paperwork Reduction Act Statements. CCC-601 U.S. DEPARTMENT OF AGRICULTURE (11-13-17) Commodity Credit Corporation COMMODITY CREDIT

How to Structure and Manage Secured Transactions Under New Article 9 By Richard R. Gleissner Finkel & Altman, L.L.C.

Page 1 of 18 1.D. How to Structure and Manage Secured Transactions under New Article 9. Structuring and managing secured transactions is complicated and cannot be adequately addressed in this brief introduction

Page 1 of 18 1.D. How to Structure and Manage Secured Transactions under New Article 9. Structuring and managing secured transactions is complicated and cannot be adequately addressed in this brief introduction

A. The Relationship Between Article 9 and the Bankruptcy Code State Law v. Bankruptcy Law

Page 1 of 35 III. The Impact of Article 9 Changes on Bankruptcy A. The Relationship Between Article 9 and the Bankruptcy Code State Law v. Bankruptcy Law South Carolina s adoption of Article 9 of the Uniform

Page 1 of 35 III. The Impact of Article 9 Changes on Bankruptcy A. The Relationship Between Article 9 and the Bankruptcy Code State Law v. Bankruptcy Law South Carolina s adoption of Article 9 of the Uniform

Noninsured Crop Disaster Assistance Program (NAP)

") Noninsured Crop Disaster Assistance Program (NAP) Overview NAP provides financial assistance to producers of noninsurable crops to protect against natural disasters that result in lower yields or crop

Noninsured Crop Disaster Assistance Program (NAP) Overview NAP provides financial assistance to producers of noninsurable crops to protect against natural disasters that result in lower yields or crop

Agricultural Disaster Assistance

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Congressional Research Service Reports Congressional Research Service 2010 Agricultural Disaster Assistance Dennis A. Shields

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Congressional Research Service Reports Congressional Research Service 2010 Agricultural Disaster Assistance Dennis A. Shields

Federal Crop Insurance Primer. Crop Insurance is an important part of a general plan for managing any farm that is

This paper presents a general overview and is not intended as legal advice. For legal advice, consult a lawyer of your own choosing about your situation. Federal Crop Insurance Primer I. What is Crop Insurance

This paper presents a general overview and is not intended as legal advice. For legal advice, consult a lawyer of your own choosing about your situation. Federal Crop Insurance Primer I. What is Crop Insurance

Statutory Liens. Assignment 13 Priority: Secured Party vs. Statutory Lienholders. Problem 1. Common Statutory Liens (Personalty)

") Assignment 13 Priority: Secured Party vs. Statutory Lienholders Reference: Understanding Secured Transactions 13.01, 13.02 Statutory Liens State statutes other than Article 9 give certain kinds of creditors