Unconventional Monetary Policy Tools. Michelle Gleeck Patrick Higgins Barry Kelly Cian McDonnell

|

|

|

- Jeffry Ray

- 5 years ago

- Views:

Transcription

1 Unconventional Monetary Policy Tools Michelle Gleeck Patrick Higgins Barry Kelly Cian McDonnell

2 INTRO Quantitive Easing or Credit Easing

3 Conventional tools include: 1) Open Market Operations 2) The Discount Rate 3) Reserve Requirements

4 Why Unconventional? The conventional tools predominantly used have been exhausted, and the federal funds rate is now between 0 and.25%.

5

6 Beyond the Fed Funds Rate: The Fed s Policy Toolkit: These tools can be divided into three main groups: 1) Lending to financial institutions involves the provision of short-term liquidity to sound financial institutions. 2) Providing liquidity directly to key credit markets provision of liquidity directly to borrowers and investors in key credit markets. 3) Buying longer-term securities

7 Term Auction Facility TAF Through the TAF sound institutions can obtain longer term funding on a collateralized basis Single Price Auction of 28-day,84-day loans Eligibility of depository institutions CAMELS Rating, Primary Credit DW standards Terms and Conditions, Eligible Collateral Minimum/Maximum bids, degree of collateralization etc How much is available at each auction? Latest auction: 26 th January, $150bn worth of 84-day credit

8 TAF Objective - To alleviate liquidity pressures on financial institutions during market disruption.

9 Term Securities Lending Facility (TSLF) Allows primary dealers to swap illiquid assets for in-demand Treasury securities What is a primary dealer? - Bank or broker that may trade in U.S Govt securities directly with the Fed. - Fed lending up to $200billion of Treasury securities to primary dealers in exchange for less creditworthy collateral. Eligible collateral?

10 TSLF Subject to haircut? - Percentage that is subtracted from the par value of the assets that are being used as collateral. The size of the haircut reflects the perceived risk associated with holding the assets How are loans allocated? Terms and Conditions How do agents bid? Primary Aim of TSLF - Improve the ability of primary dealers to provide financing to participants in securitization markets.

11 TSLF Options Programme (TOP) Allows PD s to bid for options on TSLF loans Price of loan fixed; price of option determined by competitive auction. Offering liquidity over periods of heightened collateral market pressures e.g. Quarter end dates Additional $50billion on top of TSLF funds of $200bn Option Fee = Total Price of borrowed securities*stop-out rate*term of loan in days/360days...owed regardless of whether option is exercised.

12 Primary Dealers Credit Facility (PDCF) An overnight loan facility that provides funding to primary dealers for a range of eligible collateral. Eligible collateral Broad range of collateral eligible Again subject to haircut Rates and Frequency-based fee Rate of loan is primary credit rate Fee charged after certain amount of business day s of use

13 PDCF How much can be borrowed? Loan equivalent of margin-adjusted collateral pledged Aims of PDCF - Providing liquidity to key players in credit markets $150billion extended at peak use in October 2008

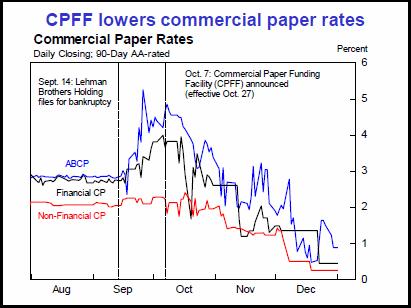

14 Commercial Paper Funding Facility Created to improve liquidity in the shortterm Supported by the Treasury Operational from Oct April

15 Purpose of the CPFF To enhance liquidity of CP market by increasing CP funding to issuers and providing assurance to investors. CPFF will improve liquidity through SPV SPV will purchase 3-month unsecured and ABCP directly from issuers. (financed by NY FED). SPV holds CP until maturity, uses proceeds to repay its loan from NY FED

16 Without short-term funding, institutions - tap credit lines or restrict spending - deepening recession. By eliminating risk that issuers will not be able to repay CP - should encourage investors into CP. Increased investor demand - lower CP rates. Improved CP market will enhance financial intermediaries ability to meet U.S. credit needs.

17

18 Terms and Conditions Only U.S. issuers, including U.S. issuers with foreign parent eligible. 10 b.p. facility fee on registration. Must register 2 business days in advance. Max amount - greatest amount of $ CP it had outstanding - Jan 1 - Aug (idea is to rollover existing CP) CP rated A1/F1/P1, 3-month maturity.

19 Price SPV will purchase at? CP discounted by rate equal to a spread over 3month OIS. Spread for unsecured CP -100 b.p. p.a. Credit Surcharge unsecured-100bp p.a. Spread for ABCP b.p. p.a.

20 ABCP MM LIQUIDITY FACILITY Program intended to help restore liquidity to the ABCP markets. Runs from Sep 19th Apr 30th 2009 Administered by the FRBB

21 ABCP - short-term investment vehicle - notes generally backed by assets such as trade receivables. MMFs - Link between investor return and business debt. Weak demand for CP, massive outflows from MMFs - forced CP sales in illiquid markets - leading to some losses. Compounding CP market issues was the reallocation of MMFs portfolios toward safer, more liquid Treasury securities. (see graph) MMF outflows slowed after Treasury announced temporary guarantee of MMFs and FED anounced AMLF on SEP 19.

22

23 AMLF provides nonrecourse loans at primary credit rate to eligible institutions. Can then use loans to purchase eligible ABCP at amortized cost from MMFs. Credit risk effectively transferred to FED. Institutions can earn profits through borrowing at the discount window and purchasing ABCP. (see graph) MMFs - experiencing redemption can sell its ABCP to banks with no loss. Bank can then make profit by earning the spread between discount window and ABCP. By increasing liquidity AMLF also provides incentives for MMFs to resume purchasing ABCP from issuers.

24

25 AMLF Eligibility- U.S. depository institutions, bank holding companies, U.S. branches and agencies of foreign banks. Only U.S. dollar denominated issues from a U.S. issuer and rated First-Tier securities are eligible. (A1,F1,P1 by two NRSRO s). Borrowers must have account with one of FRB s. Nonaccountholders may borrow through correspondant. Credit risk effectively transferred to the FED. No Fee. RATES - Loans made at rate equal to primary credit rate on initiation date that the loan is made. Fixed for term of loan. MATURITY - Non-depository - Max 270 days - Depository - Max 120 days

26 Price SPV will purchase at? CP discounted by rate equal to a spread over 3month OIS. Spread for unsecured CP -100 b.p. p.a. Credit Surcharge unsecured-100bp p.a. Spread for ABCP b.p. p.a.

27 INTEREST ON RESERVES AND EXCESS RESERVES Interest on required and excess reserves is 25 bps Prior rates had been set as the average target federal funds rate Paying interest on required reserve balances eliminates implicit tax

28 MMIFF MONEY MARKET INVESTOR FUNDING FACILITY. FOR THE PURCHASE OF COMMERCIAL PAPER AND CERTIFICATES OF DEPOSIT THAT WILL MATURE IN GREATER THAN 7 DAYS AND LESS THAT 90 DAYS. INTENDED TO RETURN LIQUITITY TO MONEY MARKETS & FACILITATE THE AVAILABILITY OF SHORT TERM CREDIT.

29 MMIFF SPECIAL PURPOSE VEHICLES (SPVS) Q: WHY NOT BORROW DIRECTLY FORM THE FED?... A: REGULATED BY THE U.S. SECURITIES AND EXCHANGE COMMISSION. 90% CASH, 10 % ASSET BACKED COMMERCIAL PAPER. RISK OF DEFAULT?

30 TALF TERM ASSET BACKED SECURITY LENDING FACILITY. ASSIST THE CREDIT MARKETS IN ACCOMODIATING THE CREDIT NEEDS OF CONSUMERS AND SMALL BUSINESSES $200 BILLION, $20 BILLION CREDIT PROTECTION FROM TREASURY DEPT. CONDITIONS: NON-RECOURSE, ONE-YEAR TERM, FULLY SECURED BY ELIGIBLE ABS.

31 TALF Q: WHO IS THE TALF DESIGNED TO HELP?..A: AUTO LOANS, CREDIT CARD LOANS, SMALL BUSINESS LOANS. WHO CAN BORROW? WHAT ABOUT THE RISK? HAIRCUTS!!!!!

32 CONCLUSION LATEST FOMC STATEMENT RISK THAT INFLATION COULD PERSIST FOR A TIME BELOW RATES THAT BEST FOSTER ECONOMIC GROWTH AND PRICE STABILITY IN THE LONGER TERM CONTINUED PURCHASE OF AGENCY DEBT AND MBS, LONGER TERMED TREASURY SECURITIES.

33 The great depression % UNEMPLOYED % UNEMPLOYED SOLVENCY VS LIQUIDITY INFLATION -25% 29-33

34 CREDIT VS MONETARY 11-1 VOTE FOR PROPOSALS JEFFERY M.LACKER VOTED AGAINST DUE TO PREFERENCE FOR EXPANDING MONETARY BASE BY PURCHASING U.S TREASURY SECURITIES AS OPPOSED TO TARGETED CREDIT PROGRAMS.

35 Thank You For Your Attention!

Financial Highlights

February 10, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Paper Issuance 3 Spreads over Treasuries 3 Broad Financial Market Indicators LIBOR Spreads

February 10, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Paper Issuance 3 Spreads over Treasuries 3 Broad Financial Market Indicators LIBOR Spreads

Financial Highlights

April 7, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Paper Issuance 3 Outstanding 3 Broad Financial Market Indicators LIBOR Spreads 4 Fed Funds

April 7, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Paper Issuance 3 Outstanding 3 Broad Financial Market Indicators LIBOR Spreads 4 Fed Funds

Credit and Liquidity Programs and the Balance Sheet

July 2009 Federal Reserve System Monthly Report on Credit and Liquidity Programs and the Balance Sheet Board of Governors of the Federal Reserve System 1 Purpose The Federal Reserve prepares this monthly

July 2009 Federal Reserve System Monthly Report on Credit and Liquidity Programs and the Balance Sheet Board of Governors of the Federal Reserve System 1 Purpose The Federal Reserve prepares this monthly

Financial Highlights

November 17, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Consumer Credit Consumer Credit: Revolving and Nonrevolving 2 ABS Yields and Issuance 3 Corporate Bonds Yield Spreads and Bond Issuance

November 17, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Consumer Credit Consumer Credit: Revolving and Nonrevolving 2 ABS Yields and Issuance 3 Corporate Bonds Yield Spreads and Bond Issuance

Lecture 5. Notes on the Current Crisis

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Financial Highlights

January 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Mortgage Backed Securities Issuance and Spreads 3 CMBS TALF Operations 4 Broad Financial

January 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Mortgage Backed Securities Issuance and Spreads 3 CMBS TALF Operations 4 Broad Financial

Shadow Maturity Transformation and Systemic Risk. Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York

Shadow Maturity Transformation and Systemic Risk Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York 8 March 2011 Overview of discussion What is shadow bank

Shadow Maturity Transformation and Systemic Risk Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York 8 March 2011 Overview of discussion What is shadow bank

Financial Highlights

January 20, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Consumer Credit Revolving and Nonrevolving 3 Compared with Past Recessions 4 Credit Card Delinquencies

January 20, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Consumer Credit Revolving and Nonrevolving 3 Compared with Past Recessions 4 Credit Card Delinquencies

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Central Bank collateral frameworks before and during the crisis

Central Bank collateral frameworks before and during the crisis The case of the Federal Reserve Central banking, liquidity crises and financial stability lecture Mai 20 th, 2011 Presentation by 1 Goals

Central Bank collateral frameworks before and during the crisis The case of the Federal Reserve Central banking, liquidity crises and financial stability lecture Mai 20 th, 2011 Presentation by 1 Goals

The Other Bailout: How the Fed is Financing the Financiers, and Related SEC Disclosure Mark S. Nelson, J.D. CCH Writer Analyst

The Other Bailout: How the Fed is Financing the Financiers, and Related SEC Disclosure Mark S. Nelson, J.D. CCH Writer Analyst 2 Introduction The legislative response to the ongoing economic crisis took

The Other Bailout: How the Fed is Financing the Financiers, and Related SEC Disclosure Mark S. Nelson, J.D. CCH Writer Analyst 2 Introduction The legislative response to the ongoing economic crisis took

The year 2008 marked a watershed for

Financial Turmoil and the Economy Economic Research Economic Research, the other areas contributing to this report, and the Legal department are part of an interdepartmental committee the Federal Reserve

Financial Turmoil and the Economy Economic Research Economic Research, the other areas contributing to this report, and the Legal department are part of an interdepartmental committee the Federal Reserve

Financial Highlights

October 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad Financial

October 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad Financial

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Banks as Liquidity Provider of Second to Last Resort

Banks as Liquidity Provider of Second to Last Resort Til Schuermann* Federal Reserve Bank of New York Q-Group, October 2008 * Any views expressed represent those of the author only and not necessarily

Banks as Liquidity Provider of Second to Last Resort Til Schuermann* Federal Reserve Bank of New York Q-Group, October 2008 * Any views expressed represent those of the author only and not necessarily

Three Lessons for Monetary Policy from the Panic of 2008

Three Lessons for Monetary Policy from the Panic of 2008 James Bullard President and CEO Federal Reserve Bank of St. Louis The Philadelphia Fed Policy Forum December 4, 2009 Any opinions expressed here

Three Lessons for Monetary Policy from the Panic of 2008 James Bullard President and CEO Federal Reserve Bank of St. Louis The Philadelphia Fed Policy Forum December 4, 2009 Any opinions expressed here

Financial Highlights

September 8, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad

September 8, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad

Implementation and Transmission of Monetary Policy

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 27, 2017 The views expressed in this presentation

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 27, 2017 The views expressed in this presentation

Who Gave It. How They Got It. It Takes A Pillage: Behind the Bailouts, Bonuses and Backroom Deals from Washington to Wall Street

Bailout and Subsidization Type Report by Nomi Prins and Krisztina Ugrin May 5, 2010 Supplemental Analysis for It Takes A Pillage: Behind the Bailouts, Bonuses and Backroom Deals from Washington to Wall

Bailout and Subsidization Type Report by Nomi Prins and Krisztina Ugrin May 5, 2010 Supplemental Analysis for It Takes A Pillage: Behind the Bailouts, Bonuses and Backroom Deals from Washington to Wall

The Fed s new front in the financial crisis

MPRA Munich Personal RePEc Archive The Fed s new front in the financial crisis Tatom, John Networks Financial institute at Indiana State University 31. October 2008 Online at http://mpra.ub.uni-muenchen.de/11803/

MPRA Munich Personal RePEc Archive The Fed s new front in the financial crisis Tatom, John Networks Financial institute at Indiana State University 31. October 2008 Online at http://mpra.ub.uni-muenchen.de/11803/

Financial Highlights

November 16, 2011 Financial Highlights Federal Reserve Balance Sheet 1 Europe European Bond Spreads 2 Mortgage Markets Mortgage Rates 3 Mortgage Applications Consumer Credit Revolving and Nonrevolving

November 16, 2011 Financial Highlights Federal Reserve Balance Sheet 1 Europe European Bond Spreads 2 Mortgage Markets Mortgage Rates 3 Mortgage Applications Consumer Credit Revolving and Nonrevolving

Financial Highlights

May 5, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Commercial Paper Issuance 2 Outstanding 2 Stocks and Bonds S&P and Dow Jones 3 VIX and MOVE volatility indices 3 European Debt Bond Spreads

May 5, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Commercial Paper Issuance 2 Outstanding 2 Stocks and Bonds S&P and Dow Jones 3 VIX and MOVE volatility indices 3 European Debt Bond Spreads

DOMESTIC OPEN MARKET OPERATIONS DURING 2009

DOMESTIC OPEN MARKET OPERATIONS DURING 29 A Report Prepared for the Federal Open Market Committee by the Markets Group of the Federal Reserve Bank of New York January 21 DOMESTIC OPEN MARKET OPERATIONS

DOMESTIC OPEN MARKET OPERATIONS DURING 29 A Report Prepared for the Federal Open Market Committee by the Markets Group of the Federal Reserve Bank of New York January 21 DOMESTIC OPEN MARKET OPERATIONS

Understanding the Policy Response to the Financial Crisis. Macroeconomic Theory Honors EC 204

Understanding the Policy Response to the Financial Crisis Macroeconomic Theory Honors EC 204 Key Problems in the Crisis Bank Solvency Declining home prices and rising mortgage defaults put banks in danger

Understanding the Policy Response to the Financial Crisis Macroeconomic Theory Honors EC 204 Key Problems in the Crisis Bank Solvency Declining home prices and rising mortgage defaults put banks in danger

Financial Highlights

November 3, 21 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad Financial

November 3, 21 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad Financial

How did Monetary Policy Implementation Change with the Financial Crisis?

How did Monetary Policy Implementation Change with the Financial Crisis? John McGowan Assistant Vice President Money Markets, Markets Group, FRBNY September 28, 2015 Internal FR I. FRS Mandate and Pre-

How did Monetary Policy Implementation Change with the Financial Crisis? John McGowan Assistant Vice President Money Markets, Markets Group, FRBNY September 28, 2015 Internal FR I. FRS Mandate and Pre-

Implementation and Transmission of Monetary Policy

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 21, 2016 The views expressed in this presentation

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 21, 2016 The views expressed in this presentation

Financial Highlights

June 2, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Consumer Credit ABS Issuance 3 ABS Spreads 3 Outstanding Amounts 4 Charge-Off Rates 4 Credit

June 2, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Consumer Credit ABS Issuance 3 ABS Spreads 3 Outstanding Amounts 4 Charge-Off Rates 4 Credit

Essential Learning for CTP Candidates NY Cash Exchange 2018 Session #CTP-06

NY Cash Exchange 2018: CTP Track Money Markets S/T Investing & Borrowing Session #6 (Thur. 11:00 am Noon) ETM5-Chapter 5: Money Markets ETM5-Chapter 13: Short-Term Investing and Borrowing Essentials of

NY Cash Exchange 2018: CTP Track Money Markets S/T Investing & Borrowing Session #6 (Thur. 11:00 am Noon) ETM5-Chapter 5: Money Markets ETM5-Chapter 13: Short-Term Investing and Borrowing Essentials of

Unconventional Monetary Policy

Unconventional Monetary Policy Mark Gertler (based on joint work with Peter Karadi) NYU October 29 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes pre versus post August 27 Post August

Unconventional Monetary Policy Mark Gertler (based on joint work with Peter Karadi) NYU October 29 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes pre versus post August 27 Post August

William C Dudley: The Federal Reserve's liquidity facilities

William C Dudley: The Federal Reserve's liquidity facilities Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, at the Vanderbilt University

William C Dudley: The Federal Reserve's liquidity facilities Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, at the Vanderbilt University

APPENDIX A: GLOSSARY

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

U.S. Monetary Policy Objectives in the Short and Long Run 1

Presentation to the Andrew Brimmer Policy Forum IBEFA/ASSA Meeting San Francisco, CA By Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco For delivery on January 4, 2009, 2:30 PM

Presentation to the Andrew Brimmer Policy Forum IBEFA/ASSA Meeting San Francisco, CA By Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco For delivery on January 4, 2009, 2:30 PM

Financial Highlights

May 12, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Broad Financial Market Indicators LIBOR OIS Spread 3 Fed Funds Futures 3 LIBOR and OIS Rates

May 12, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Broad Financial Market Indicators LIBOR OIS Spread 3 Fed Funds Futures 3 LIBOR and OIS Rates

The New Nontraditional Lending Facilities by the Federal Reserve, as Lender of Last Resort in the US, in Response to Financial Markets Turmoil **

The New Nontraditional Lending Facilities by the Federal Reserve, as Lender of Last Resort in the US, in Response to Financial Markets Turmoil ** Marwan El Nasser Professor of Economics School of Business

The New Nontraditional Lending Facilities by the Federal Reserve, as Lender of Last Resort in the US, in Response to Financial Markets Turmoil ** Marwan El Nasser Professor of Economics School of Business

Financial Highlights

December 1, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 CMBS Delinquency Rates 4 Senior Loan Officer

December 1, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 CMBS Delinquency Rates 4 Senior Loan Officer

Financial Highlights

July 21, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Bond and Equity Markets Stock Market Indices 3 Volatility (VIX and MOVE) 3 Broad Financial

July 21, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Bond and Equity Markets Stock Market Indices 3 Volatility (VIX and MOVE) 3 Broad Financial

Slow recovery from worst downturn since Great Depression. Monetary policy at the zero lower bound: Empirical evidence

Monetary policy at the zero lower bound: Empirical evidence A. Brief summary of 27-214 1. Emergency lending 2. Large-scale asset purchases 3. Forward guidance Slow recovery from worst downturn since Great

Monetary policy at the zero lower bound: Empirical evidence A. Brief summary of 27-214 1. Emergency lending 2. Large-scale asset purchases 3. Forward guidance Slow recovery from worst downturn since Great

Economic Outlook. Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis. NLB,LLC The Lodge, Des Peres, MO.

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT?

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT? L. Randall Wray Levy Economics Institute and University of Missouri - Kansas City www.levy.org; www.cfeps.org; wrayr@umkc.edu *Report of a Research Project

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT? L. Randall Wray Levy Economics Institute and University of Missouri - Kansas City www.levy.org; www.cfeps.org; wrayr@umkc.edu *Report of a Research Project

Financial Highlights

June 16, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Commercial Mortgage Backed Securities Yield Spreads 3 Issuance 3 Residential Mortgages Rates

June 16, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Commercial Mortgage Backed Securities Yield Spreads 3 Issuance 3 Residential Mortgages Rates

The Great Recession. ECON 43370: Financial Crises. Eric Sims. Spring University of Notre Dame

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

EconomicLetter. Insights from the. TALF: Jump-Starting the Securitization Markets. Federal Reserve Bank of Dallas

Vol. 4, No. 6 AUGUST 29 EconomicLetter Insights from the TALF: Jump-Starting the Securitization Markets by Kenneth J. Robinson Securitization was a major source of credit to the economy, and its resurgence

Vol. 4, No. 6 AUGUST 29 EconomicLetter Insights from the TALF: Jump-Starting the Securitization Markets by Kenneth J. Robinson Securitization was a major source of credit to the economy, and its resurgence

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi Executive Board member of the European Central Bank Conference The ECB and

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi Executive Board member of the European Central Bank Conference The ECB and

TARP, TALF, TGLP Help!!! Ever since

The Alphabet Soup of the Financial System Bailout By Carol Hempfling Pratt A glossary of programs administered by the Treasury, the FDIC and the Federal Reserve. TARP, TALF, TGLP Help!!! Ever since Congress

The Alphabet Soup of the Financial System Bailout By Carol Hempfling Pratt A glossary of programs administered by the Treasury, the FDIC and the Federal Reserve. TARP, TALF, TGLP Help!!! Ever since Congress

The Financial Crisis. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

Transparency in the U.S. Repo Market

Transparency in the U.S. Repo Market Antoine Martin Federal Reserve Bank of New York October 11, 2013 The views expressed in this presentation are my own and may not represent the views of the Federal

Transparency in the U.S. Repo Market Antoine Martin Federal Reserve Bank of New York October 11, 2013 The views expressed in this presentation are my own and may not represent the views of the Federal

Implementing Monetary Policy: Transition Tools

Implementing Monetary Policy: Transition Tools Julie Remache Central Banking Seminar Oct 6, 2015 The views expressed in this presentation reflect the author s and do not necessarily reflect that of the

Implementing Monetary Policy: Transition Tools Julie Remache Central Banking Seminar Oct 6, 2015 The views expressed in this presentation reflect the author s and do not necessarily reflect that of the

Discussion of The Great Escape? A Quantitative Evaluation of the Fed s Non- Standard Policies by Del Negro, Eggertsson, Ferrero, and Kiyotaki

Discussion of The Great Escape? A Quantitative Evaluation of the Fed s Non- Standard Policies by Del Negro, Eggertsson, Ferrero, and Kiyotaki Zheng Liu, FRB San Francisco March 5, 2010 The opinions expressed

Discussion of The Great Escape? A Quantitative Evaluation of the Fed s Non- Standard Policies by Del Negro, Eggertsson, Ferrero, and Kiyotaki Zheng Liu, FRB San Francisco March 5, 2010 The opinions expressed

Central banks as lenders of last resort: experiences during the crisis and lessons for the future 1

Central banks as lenders of last resort: experiences during the 2007 10 crisis and lessons for the future 1 Dietrich Domanski, 2 Richhild Moessner 3 and William Nelson 4 Abstract During the 2007 10 financial

Central banks as lenders of last resort: experiences during the 2007 10 crisis and lessons for the future 1 Dietrich Domanski, 2 Richhild Moessner 3 and William Nelson 4 Abstract During the 2007 10 financial

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Liquidity is Relevant Again

Liquidity is Relevant Again April 2019 Not FDIC Insured May Lose Value No Bank Guarantee Not NCUA or NCUSIF insured. May lose value. No credit union guarantee. For institutional use only. l 2019 FMR LLC.

Liquidity is Relevant Again April 2019 Not FDIC Insured May Lose Value No Bank Guarantee Not NCUA or NCUSIF insured. May lose value. No credit union guarantee. For institutional use only. l 2019 FMR LLC.

STATUS UPDATE ON TREASURY, FEDERAL RESERVE AND FDIC FINANCIAL MARKET INITIATIVES

CLIENT MEMORANDUM STATUS UPDATE ON TREASURY, FEDERAL RESERVE AND FDIC FINANCIAL MARKET INITIATIVES On November 18, 2008, Secretary Paulson, Chairman Bernanke and Chairman Bair outlined to the Committee

CLIENT MEMORANDUM STATUS UPDATE ON TREASURY, FEDERAL RESERVE AND FDIC FINANCIAL MARKET INITIATIVES On November 18, 2008, Secretary Paulson, Chairman Bernanke and Chairman Bair outlined to the Committee

The Impact of Liquidity, Securitization, and Banks on the Real Economy

The Impact of Liquidity, Securitization, and Banks on the Real Economy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Panel Discussion Conference on Financial Markets

The Impact of Liquidity, Securitization, and Banks on the Real Economy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Panel Discussion Conference on Financial Markets

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

Appendix 1: Materials used by Mr. Dudley

Presentation Materials (PDF) Pages 169 to 188 of the Transcript Appendix 1: Materials used by Mr. Dudley Class II FOMC - Restricted FR Page 1 (1) Title: Spread between Jumbo and Conforming Mortgage Rates

Presentation Materials (PDF) Pages 169 to 188 of the Transcript Appendix 1: Materials used by Mr. Dudley Class II FOMC - Restricted FR Page 1 (1) Title: Spread between Jumbo and Conforming Mortgage Rates

Update on Federal Programs in Response to the Financial Crisis

EESA, TARP, TALF, CaPP, TLGP, CpFF, MMIFF, AMLF, ABCP MMFLF, PDCF, TSLF, TOP OMG!! Update on Federal Programs in Response to the Financial Crisis April 29, 2009 2009 Morrison & Foerster LLP All Rights

EESA, TARP, TALF, CaPP, TLGP, CpFF, MMIFF, AMLF, ABCP MMFLF, PDCF, TSLF, TOP OMG!! Update on Federal Programs in Response to the Financial Crisis April 29, 2009 2009 Morrison & Foerster LLP All Rights

A Thought on Repo Market Haircuts

A Thought on Repo Market Haircuts Joo, Hyunsoo Repo is a money market instrument that works in a similar way to a secured loan where a cash borrower provides its securities as collateral to a cash lender.

A Thought on Repo Market Haircuts Joo, Hyunsoo Repo is a money market instrument that works in a similar way to a secured loan where a cash borrower provides its securities as collateral to a cash lender.

Today's FOMC statement: how the language changed from prior meeting

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Federal Reserve Wednesday, December 19, 2018 Today's FOMC

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Federal Reserve Wednesday, December 19, 2018 Today's FOMC

The recent financial crisis brought about dramatic changes in the way that the

Social Education 75(2), pp 76 81 2011 National Council for the Social Studies The Fed and Monetary Policy It s Not Your Mother and Father s Monetary Policy Anymore: The and Financial Crisis Relief Andrew

Social Education 75(2), pp 76 81 2011 National Council for the Social Studies The Fed and Monetary Policy It s Not Your Mother and Father s Monetary Policy Anymore: The and Financial Crisis Relief Andrew

Financial Turmoil and the Economy

Financial Turmoil and the Economy Federal Reserve Bank of San Francisco 2008 Annual Report The Federal Reserve Bank of San Francisco is one of twelve regional Federal Reserve Banks across the United States

Financial Turmoil and the Economy Federal Reserve Bank of San Francisco 2008 Annual Report The Federal Reserve Bank of San Francisco is one of twelve regional Federal Reserve Banks across the United States

The Flight from Maturity. Gary Gorton, Yale and NBER Andrew Metrick, Yale and NBER Lei Xie, AQR Investment Management

The Flight from Maturity Gary Gorton, Yale and NBER Andrew Metrick, Yale and NBER Lei Xie, AQR Investment Management Explaining the Crisis How can a small shock cause a large crisis? 24 bps of realized

The Flight from Maturity Gary Gorton, Yale and NBER Andrew Metrick, Yale and NBER Lei Xie, AQR Investment Management Explaining the Crisis How can a small shock cause a large crisis? 24 bps of realized

Markets: Fixed Income

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Government Cash Balances - Linkages with Liquidity

Amol Agrawal amol@stcipd.com +91-22-6622234 Government Cash Balances - Linkages with Liquidity We have been releasing reports in the nature of primers on RBI s operations and accounts (Refer Guide to Weekly

Amol Agrawal amol@stcipd.com +91-22-6622234 Government Cash Balances - Linkages with Liquidity We have been releasing reports in the nature of primers on RBI s operations and accounts (Refer Guide to Weekly

March 17 18, 2009 Authorized for Public Release. Appendix 1: Materials used by Ms. Mosser

March 17 18, 29 Authorized for Public Release 222 of 266 Appendix 1: Materials used by Ms. Mosser 11 March 17 18, 29 Authorized for Public Release 223 of 266 Index to 1=8/1/8 (1) Global Equities August

March 17 18, 29 Authorized for Public Release 222 of 266 Appendix 1: Materials used by Ms. Mosser 11 March 17 18, 29 Authorized for Public Release 223 of 266 Index to 1=8/1/8 (1) Global Equities August

Management s Report on Internal Control Over Financial Reporting

Management s Report on Internal Control Over Financial Reporting April 21, 2010 To the Board of Directors of the Federal Reserve Bank of Dallas: The management of the Federal Reserve Bank of Dallas ( FRBD

Management s Report on Internal Control Over Financial Reporting April 21, 2010 To the Board of Directors of the Federal Reserve Bank of Dallas: The management of the Federal Reserve Bank of Dallas ( FRBD

TERM ASSET-BACKED SECURITIES LOAN FACILITY (TALF): CAN WALL STREET HELP MAIN STREET?

: CAN WALL STREET HELP MAIN STREET?") SECTION 01 04 APPENDIX TERM ASSET-BACKED SECURITIES LOAN FACILITY (TALF): CAN WALL STREET HELP MAIN STREET? By Morrison & Foerster, LLP On November 25, 2008, the U.S. Department of the Treasury (Treasury)

SECTION 01 04 APPENDIX TERM ASSET-BACKED SECURITIES LOAN FACILITY (TALF): CAN WALL STREET HELP MAIN STREET? By Morrison & Foerster, LLP On November 25, 2008, the U.S. Department of the Treasury (Treasury)

Chapter 6 : Money Markets

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

Financial Turmoil: Federal Reserve Policy Responses

Order Code RL34427 Financial Turmoil: Federal Reserve Policy Responses Updated October 23, 2008 Marc Labonte Specialist in Macroeconomic Policy Government and Finance Division Financial Turmoil: Federal

Order Code RL34427 Financial Turmoil: Federal Reserve Policy Responses Updated October 23, 2008 Marc Labonte Specialist in Macroeconomic Policy Government and Finance Division Financial Turmoil: Federal

Federal Reserve Bank of Chicago

Federal Reserve Bank of Chicago Federal Reserve Policies and Financial Market Conditions during the Crisis Scott A. Brave and Hesna Genay REVISED July 2011 WP 2011-04 Federal Reserve Policies and Financial

Federal Reserve Bank of Chicago Federal Reserve Policies and Financial Market Conditions during the Crisis Scott A. Brave and Hesna Genay REVISED July 2011 WP 2011-04 Federal Reserve Policies and Financial

TALF Update: New Guidance Available, Program to Launch this Month

Economic Stabilization Advisory Group March 6, 2009 TALF Update: New Guidance Available, Program to Launch this Month On March 3, 2009, the Board of Governors of the U.S. Federal Reserve System (the Federal

Economic Stabilization Advisory Group March 6, 2009 TALF Update: New Guidance Available, Program to Launch this Month On March 3, 2009, the Board of Governors of the U.S. Federal Reserve System (the Federal

STATEMENT OF AUDITOR INDEPENDENCE

STATEMENT OF AUDITOR INDEPENDENCE In 2009, the Board of Governors engaged Deloitte & Touche LLP (D&T) for the audits of the individual and combined financial statements of the Reserve Banks and the consolidated

STATEMENT OF AUDITOR INDEPENDENCE In 2009, the Board of Governors engaged Deloitte & Touche LLP (D&T) for the audits of the individual and combined financial statements of the Reserve Banks and the consolidated

Investor Presentation. December 2017

Investor Presentation December 2017 This is not an offer to sell. FHLBank debt is not an obligation of or guaranteed by the United States and may not be offered or sold in any jurisdiction requiring its

Investor Presentation December 2017 This is not an offer to sell. FHLBank debt is not an obligation of or guaranteed by the United States and may not be offered or sold in any jurisdiction requiring its

Today's FOMC statement: how the language changed from prior meeting

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Federal Reserve Wednesday, January 30, 2019 Today's FOMC

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Federal Reserve Wednesday, January 30, 2019 Today's FOMC

Global Securities Lending Business and Market Update

NORTHERN TRUST 2009 INSTITUTIONAL CLIENT CONFERENCE GLOBAL REACH, LOCAL EXPERTISE Global Securities Lending Business and Market Update Michael A. Vardas, CFA Managing Director Quantitative Management and

NORTHERN TRUST 2009 INSTITUTIONAL CLIENT CONFERENCE GLOBAL REACH, LOCAL EXPERTISE Global Securities Lending Business and Market Update Michael A. Vardas, CFA Managing Director Quantitative Management and

Operation Twist: 1961 vs. 2011

Amol Agrawal amol@stcipd.com +91-22-66202234 Operation Twist: 1961 vs. 2011 Ever since the crisis, Federal Reserve (and other central banks following Fed) has introduced new innovative measures to stimulate

Amol Agrawal amol@stcipd.com +91-22-66202234 Operation Twist: 1961 vs. 2011 Ever since the crisis, Federal Reserve (and other central banks following Fed) has introduced new innovative measures to stimulate

Management s Report on Internal Control Over Financial Reporting

20 FEDERAL RESERVE BANK OF DALLAS 2008 Annual Report Management s Report on Internal Control Over Financial Reporting April 2, 2009 To the Board of Directors of the Federal Reserve Bank of Dallas: The

20 FEDERAL RESERVE BANK OF DALLAS 2008 Annual Report Management s Report on Internal Control Over Financial Reporting April 2, 2009 To the Board of Directors of the Federal Reserve Bank of Dallas: The

Third Quarter Report 2010

Third Quarter Report REPORT TO MEMBERS CENTRAL 1 REPORTS STRONG RESULTS FOR THIRD QUARTER OF Thirdquarter highlights compared to the same period last year: Central s Net income of $18.2 million, compared

Third Quarter Report REPORT TO MEMBERS CENTRAL 1 REPORTS STRONG RESULTS FOR THIRD QUARTER OF Thirdquarter highlights compared to the same period last year: Central s Net income of $18.2 million, compared

Term Asset-Backed Securities Loan Facility: Frequently Asked Questions

Term Asset-Backed Securities Loan Facility: Frequently Asked Questions Effective May 19, 2009 General Governance and Reporting Policy and Regulation Borrower Eligibility Investment Funds Collateral Eligibility

Term Asset-Backed Securities Loan Facility: Frequently Asked Questions Effective May 19, 2009 General Governance and Reporting Policy and Regulation Borrower Eligibility Investment Funds Collateral Eligibility

Lecture 23 Monetary Policy. Noah Williams

Lecture 23 Monetary Policy Noah Williams University of Wisconsin - Madison Economics 702 Fed Policy Instrument Main instrument of conventional policy is the Federal Funds rate. An extremely short-term

Lecture 23 Monetary Policy Noah Williams University of Wisconsin - Madison Economics 702 Fed Policy Instrument Main instrument of conventional policy is the Federal Funds rate. An extremely short-term

Recent developments in the euro money market. Money Market Contact Group Frankfurt, 18 September 2012

Recent developments in the euro money market Money Market Contact Group Frankfurt, 18 September 2012 ECB developments and announcements I 5 July 2012 The ECB reduced by 25 basis points the interest rate

Recent developments in the euro money market Money Market Contact Group Frankfurt, 18 September 2012 ECB developments and announcements I 5 July 2012 The ECB reduced by 25 basis points the interest rate

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1. Printer version Changes from October November 130 Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Financial Bubbling: from the Asian Crisis to the Subprime Mess

Financial Bubbling: from the Asian Crisis to the Subprime Mess University of Bari by Giovanni Ferri (University of Bari) Workshop The complexity of financial crisis in a long-period perspective: facts,

Financial Bubbling: from the Asian Crisis to the Subprime Mess University of Bari by Giovanni Ferri (University of Bari) Workshop The complexity of financial crisis in a long-period perspective: facts,

Prices and Quantities in the Monetary Policy Transmission Mechanism

Prices and Quantities in the Monetary Policy Transmission Mechanism Tobias Adrian a and Hyun Song Shin b a Federal Reserve Bank of New York b Princeton University Central banks have a variety of tools

Prices and Quantities in the Monetary Policy Transmission Mechanism Tobias Adrian a and Hyun Song Shin b a Federal Reserve Bank of New York b Princeton University Central banks have a variety of tools

An Update on Economic Conditions. January 5, 2010

An Update on Economic Conditions Raymond Owens January 5, 21 Real Gross Domestic Product 8 7 6 5 4 Percent change from previous quarter at annual rate 3 Q3 2.2% 2 1-1 -2-3 -4-5 -6-7 21 22 23 24 25 26 27

An Update on Economic Conditions Raymond Owens January 5, 21 Real Gross Domestic Product 8 7 6 5 4 Percent change from previous quarter at annual rate 3 Q3 2.2% 2 1-1 -2-3 -4-5 -6-7 21 22 23 24 25 26 27

Today's FOMC statement: how the language changed from prior meeting

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Federal Reserve Wednesday, August 1, 2018 Today's FOMC statement:

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Federal Reserve Wednesday, August 1, 2018 Today's FOMC statement:

The Bank of Japan s Eligible Collateral Framework and Recently Accepted Collateral

The s Eligible Collateral Framework and Recently Accepted Collateral 1 The s Eligible Collateral Framework and Recently Accepted Collateral I. Summary 1 The completely revised its eligible collateral framework

The s Eligible Collateral Framework and Recently Accepted Collateral 1 The s Eligible Collateral Framework and Recently Accepted Collateral I. Summary 1 The completely revised its eligible collateral framework

COMMENTARY. CREdit FOR CONsuMERs ANd BusiNEsses

March 2009 JONES DAY COMMENTARY The FedERAl ResERve s TERM AssET-BACked securities loan FACiliTY ( TALF ) ExpANding New CREdit FOR CONsuMERs ANd BusiNEsses In 2008, issuances of asset-backed securities

March 2009 JONES DAY COMMENTARY The FedERAl ResERve s TERM AssET-BACked securities loan FACiliTY ( TALF ) ExpANding New CREdit FOR CONsuMERs ANd BusiNEsses In 2008, issuances of asset-backed securities

FEDERAL RESERVE BANK of CLEVELAND

2 0 0 9 A N N U A L R E P O R T FEDERAL RESERVE BANK of CLEVELAND The Federal Reserve System is responsible for formulating and implementing U.S. monetary policy. It also supervises banks and bank holding

2 0 0 9 A N N U A L R E P O R T FEDERAL RESERVE BANK of CLEVELAND The Federal Reserve System is responsible for formulating and implementing U.S. monetary policy. It also supervises banks and bank holding

Arbitrage, liquidity and exit: The repo and federal funds market before, during, and after the financial crisis

Arbitrage, liquidity and exit: The repo and federal funds market before, during, and after the financial crisis Morten Bech (FRBNY), Elizabeth Klee (FRB), and Viktors Stebunovs (FRB) May 21, 2011 The views

Arbitrage, liquidity and exit: The repo and federal funds market before, during, and after the financial crisis Morten Bech (FRBNY), Elizabeth Klee (FRB), and Viktors Stebunovs (FRB) May 21, 2011 The views

Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

CENTRE DEBT MARKET IN INDIA KNOWLEDGE. Introduction. Which sectors are covered by the Index?

DEBT MARKET IN INDIA Introduction Indian debt markets, in the early nineties, were characterised by controls on pricing of assets, segmentation of markets and barriers to entry, low levels of liquidity,

DEBT MARKET IN INDIA Introduction Indian debt markets, in the early nineties, were characterised by controls on pricing of assets, segmentation of markets and barriers to entry, low levels of liquidity,

Auditor Independence. In 2009, the Board of Governors engaged. of the individual and combined financial statements

Auditor Independence In 2009, the Board of Governors engaged Deloitte & Touche LLP (D&T) for the audits of the individual and combined financial statements of the Reserve Banks and the consolidated financial

Auditor Independence In 2009, the Board of Governors engaged Deloitte & Touche LLP (D&T) for the audits of the individual and combined financial statements of the Reserve Banks and the consolidated financial

Lecture 22 Liquidity Trap Hyperinflation Monetary Policy. Noah Williams

Lecture 22 Liquidity Trap Hyperinflation Monetary Policy Noah Williams University of Wisconsin - Madison Economics 702 Limitations on Stabilization & Liquidity Traps Generally have monetary policy smooth

Lecture 22 Liquidity Trap Hyperinflation Monetary Policy Noah Williams University of Wisconsin - Madison Economics 702 Limitations on Stabilization & Liquidity Traps Generally have monetary policy smooth

Auction of DGB Opening auction of new 10Y DGB on Wednesday 25 January. Frederik Nordsborg. Maria Holm Rasmussen 20 January 2017

1 Auction of DGB 227 Opening auction of new 1Y DGB on Wednesday 2 January Frederik Nordsborg Maria Holm Rasmussen 2 January 217 DGB 227: Main arguments and pricing Pros (tight pricing) DKK callable covered

1 Auction of DGB 227 Opening auction of new 1Y DGB on Wednesday 2 January Frederik Nordsborg Maria Holm Rasmussen 2 January 217 DGB 227: Main arguments and pricing Pros (tight pricing) DKK callable covered

Public Policy Brief A DETAILED LOOK AT THE FED S CRISIS RESPONSE BY FUNDING FACILITY AND RECIPIENT. Levy Economics Institute of Bard College

Levy Economics Institute of Bard College Levy Economics Institute of Bard College Public Policy Brief No. 123, 2012 A DETAILED LOOK AT THE FED S CRISIS RESPONSE BY FUNDING FACILITY AND RECIPIENT JAMES

Levy Economics Institute of Bard College Levy Economics Institute of Bard College Public Policy Brief No. 123, 2012 A DETAILED LOOK AT THE FED S CRISIS RESPONSE BY FUNDING FACILITY AND RECIPIENT JAMES

The International Economy: Challenge and Opportunity

The International Economy: Challenge and Opportunity The Origins of the Financial Crisis Christopher J. Neely Assistant Vice President Federal Reserve Bank of St. Louis United Nations Association of St.

The International Economy: Challenge and Opportunity The Origins of the Financial Crisis Christopher J. Neely Assistant Vice President Federal Reserve Bank of St. Louis United Nations Association of St.

The Changed Landscape for Short-term Investing Post SEC Money Market Fund Reform

The Changed Landscape for Short-term Investing Post SEC Money Market Fund Reform April 4, 2017 1718920 CRC Exp. 02/23/2018 FOR INSTITUTIONAL USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC. A Challenging

The Changed Landscape for Short-term Investing Post SEC Money Market Fund Reform April 4, 2017 1718920 CRC Exp. 02/23/2018 FOR INSTITUTIONAL USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC. A Challenging

F INANCIAL S TATEMENTS AND S UPPLEMENTAL I NFORMATION

F INANCIAL S TATEMENTS AND S UPPLEMENTAL I NFORMATION SunTrust Robinson Humphrey, Inc. Year Ended December 31, 2008 With Reports of Independent Registered Public Accounting Firm (A wholly owned subsidiary

F INANCIAL S TATEMENTS AND S UPPLEMENTAL I NFORMATION SunTrust Robinson Humphrey, Inc. Year Ended December 31, 2008 With Reports of Independent Registered Public Accounting Firm (A wholly owned subsidiary

Proposed Credit Guarantee and Investment Mechanism (CGIM) Asian Development Bank

Asian Development Bank") Proposed Credit Guarantee and Investment Mechanism (CGIM) A. Noy Siackhachanh Advisor Office of Regional Economic Integration Asian Development Bank The opinion expressed in the presentation is that of

Proposed Credit Guarantee and Investment Mechanism (CGIM) A. Noy Siackhachanh Advisor Office of Regional Economic Integration Asian Development Bank The opinion expressed in the presentation is that of