Getting started as an investor. A guide for investors

|

|

|

- Jayson Johns

- 5 years ago

- Views:

Transcription

1 Getting started as an investor A guide for investors

2 MAKE A RETURN AND A DIFFERENCE You can earn attractive, stable returns by lending to businesses through Funding Circle. Set up your account in minutes, then use our simple lending tools to lend to hundreds of businesses automatically. You can also open an ISA account to earn returns tax-free. Your lending will help those businesses to grow and push the UK economy forward, and you ll earn a return as they pay you back with interest. We believe it s a better system for everyone.

3 About this guide In this guide you ll learn how to start lending, how to find your way around your account and other important information about lending through Funding Circle. If you have any questions, you can contact our Investor Support team by phone or Monday - Friday, 9am - 6pm (exc. Bank Holidays) If you re unsure whether lending is right for you, you should seek independent financial advice before you start. Remember by lending to businesses your capital is at risk, while tax rules and relief can change depending on your personal circumstances. Funding Circle is not covered by the Financial Services Compensation Scheme. Contents How lending works 4 Who am I lending to? 9 Your investor account 12 Your account summary Lending options Accessing your money ISA account 21 Interest, tax and fees 25 Further information 27

4 How lending works We connect established, creditworthy businesses looking for finance to investors with money to lend. Whether you have a Classic account or an ISA account, lending to businesses works in the same way. Investors Investors use their online account to easily lend to hundreds of businesses looking to borrow. Funding Circle We review applications and only approve creditworthy businesses. We then pay out your funds to the businesses you lend to, and process your repayments. Businesses Businesses make fixed monthly repayments with interest, which we distribute to all the investors who lent to them. The lending process 1. A business applies for a loan We assess their application and their creditworthiness. If successful, we assign them a risk band and make them an offer. The risk band and loan term helps determine the interest rate they will pay. 2. The loan is funded If accepted, the loan is funded by lots of investors each lending small amounts. These are called loan parts. Each loan part represents the loan contract you and the business have entered into. You ll be able to lend across lots of loan parts to build a diversified portfolio. 3. The business repays the loan with interest Loans are typically repaid in fixed monthly instalments. The business makes the payment to us, and we distribute it to all the investors who lent to them. That means you can start earning interest after your first month. 4

5 4. Repayments are reinvested As long as you keep lending active on your account, your repayments will be continuously lent out again on other loans. This helps your interest to compound, maximising your return. 5. Withdraw when you re ready You can sell your loan parts to other investors (subject to demand), and withdraw a lump sum, or turn reinvesting off and withdraw your payments as they come in. More on this on page 19. 5

6 How we manage risk Only established businesses who have passed our rigorous credit assessment process can borrow through Funding Circle. However, it s important to remember that some businesses will not be able to fully repay their loan. We call this a bad debt, and it s already accounted for in your projected return. We reduce the impact it has on your return in 3 important ways: Rigorous assessment with advanced technology There are 3 key pillars to our assessment process: 1. Policy criteria We receive thousands of applications from all types of small businesses. To help our team focus on the right type of application, we have criteria in place that filter out businesses who have a low likelihood of being approved. To be eligible for a loan a business must have: A minimum of 2 years trading history At least 1 year of filed or formally prepared accounts No County Court Judgements (CCJs) registered in the last 12 months, and no outstanding CCJs larger than 1000 UK ownership and resident directors: majority that are UK resident 2. Statistical credit models Our proprietary credit model uses thousands of data points to assess the creditworthiness of every business that applies. It uses publicly available information, credit bureau data and our own historical data of loan performance and applications. Successful applications are then given a risk band from A+ to E, which helps determine the interest rate they ll pay. 3. Expert judgement Alongside our statistical credit models, each business is manually assessed by a member of our credit assessment team, who combine decades of experience from some of the world s leading financial institutions. They use our credit model and financials relating to the business and company directors to manually assess each application. This allows the team to raise and clarify any potential questions before a loan is approved. 6

7 The combination of these 3 pillars gives us a full picture of a borrower s financial health, allowing us to make balanced credit decisions so that you can earn stable returns. Diversification Diversification, where you spread your lending across many businesses, is the best way to earn a stable return as it reduces the impact of businesses being unable to repay their loans. By using our automated lending tool, you can easily lend to hundreds of businesses to quickly build a diversified portfolio. As the minimum you can lend to each business is 10, lending at least 2000 will allow you to: Lend to at least 200 businesses Lend no more than 0.5% of your total to each one 93% of investors who have diversified like this for a year or more are earning 4% or more annually after fees and bad debt (correct as of 30th September 2018). Investors lending more than 2,000 will lend no more than 0.5% of their total portfolio to each business. Lending 2,000 or more will help you be fully diversified for a more stable return. If you d like to start with less, there is an initial minimum card transfer of 1,000 when opening a Classic or ISA account. 7

8 Collections and Recoveries team Funding Circle loans are typically supported by a personal guarantee from company directors (or members if the business is a LLP). We also sometimes take other forms of security, for example on property finance loans. If a business is unable to repay the loan, our team can look to recover the outstanding balance from the guarantors. Our Collections & Recoveries team pursue every single late or defaulted loan, arranging a new payment plan if possible, or exhausting every legal process available. The team has a range of methods and technologies in place to recover as much as possible for you. When a loan defaults, it will show the total loss on your account. However, our team are often able to recover a significant portion of that loss. Historically we have recovered approximately 40% of loans that have been defaulted for at least three years, so it s worth remembering that the amount lost on recent defaults may improve over time. Please note, a personal guarantee, or any form of security, does not ensure a full recovery of outstanding debts will be made if a loan defaults, and there may be instances where no recovery can be made. 8

9 Who am I lending to? You ll lend to hundreds of established, creditworthy businesses in different sectors and regions throughout the UK. They may use their loan for a wide range of purposes, including to hire staff, buy new stock or equipment, open new premises or boost cash flow. All businesses will have been trading for 2 years or more, but our average business is 8 years old. Debbie Leon from Fashionizer has won awards for her innovative uniform designs. She borrowed 195,000 for working capital. Debbie Leon from Fashionizer has won awards for her innovative uniformdesigns. She borrowed 195,000 for working capital. Average business 8 years old Employs 5-10 people Turnover of 420,000 Businesses from every region in the UK have borrowed, and an estimated 45,000 jobs were created and sustained in 2017 thanks to investors lending through Funding Circle. Oxford Economics estimates that for every 1 lent through Funding Circle, 2 is added to the UK economy, so your lending really will make a huge difference to British businesses and our economy. 9

10 Types of businesses There are two types of loans on our platform small business loans and property finance loans and there are slight differences to how these loans work. We expect to stop all new property finance lending by mid Small business loans Business owners may need finance for many reasons, for example to expand their premises or hire new staff. Their loans will be covered by a Personal Guarantee from the directors or shareholders of the business. They will pay back their loan in monthly instalments of both principal (the original loan amount) and interest. What are the risks of lending to small business loans? As part of lending to businesses, there will be instances where a business cannot continue to repay their loan, which becomes a bad debt. When this happens, our in-house collections team work to recover your money (see page 8) We provide bad debt rates by the year loans are made, and update these regularly. You can view our bad debt rates on our statistics page. You can read more about the key features and risks of lending to small businesses here. Property finance loans Lending through Funding Circle also helps experienced property professionals build new residential homes, refurbish existing properties and access short-term finance. All property finance loans are secured against an asset, which means if the borrower is unable to pay their loan, Funding Circle can enforce the security and use the sale of the asset to repay investors. Unlike small business loans, the interest payable by the borrower is typically funded by investors alongside the principal when the loan is first made. Investors will then typically receive monthly instalments of interest. The principal and interest is then repaid by the borrower at the end of the loan term when properties are sold. 10

11 How are property finance loans assessed? Property loans are assessed by our experienced property credit assessment team. Some of the key considerations when deciding whether a loan should be approved are: Funding ratios We ensure that the value of the property that is used as security is higher than the value of the loan requested by the borrower (i.e. an appropriate Loan-to-value ratio). The borrower also needs to commit an appropriate amount of equity to the project, in case market conditions change. Property fundamentals We assess whether the proposed property is the right fit for its location, has an appropriate sale price and the building costs/timings are suitable for the term of the loan. Borrower track record We want to be comfortable that the borrower has successfully delivered similar projects in the past. Like small business loans, property finance loans will be assigned a risk band, however the interest rate will be priced individually for each loan. What are the risks of lending to property finance loans? As property loans are secured against an asset, if the borrower is unable to repay, we can use the sale of the asset to pay investors back. Although we would often anticipate a significant recovery this can t be guaranteed, and could take a significant amount of time, for example if market conditions change. Most property loans repay on time, however delays can happen when building homes. These can be caused by bad weather, construction issues or the sales process taking longer than expected. You can read more on what happens when a property loan is late in our FAQs, and a list of the key features and risks can be found here. 11

12 Your investor account Account types At Funding Circle we offer two types of investor accounts; ISA and Classic. They work in the same way, however the ISA account allows you to earn interest tax-free. ISA account Classic account Earn interest tax-free Earnings subject to tax Annual subscription limit No annual limit Minimum initial investment of 1,000 Minimum initial investment of 1,000 You can use this section to guide you through operating both types of accounts, but you can find information specific to the Funding Circle ISA on page 21. Getting started You can set up your ISA or Classic account and start lending in a matter of minutes. Enter a few details about you on our simple form, pick your lending option and read and accept our terms and conditions. Then transfer money from your debit card and you re ready to start lending. 12

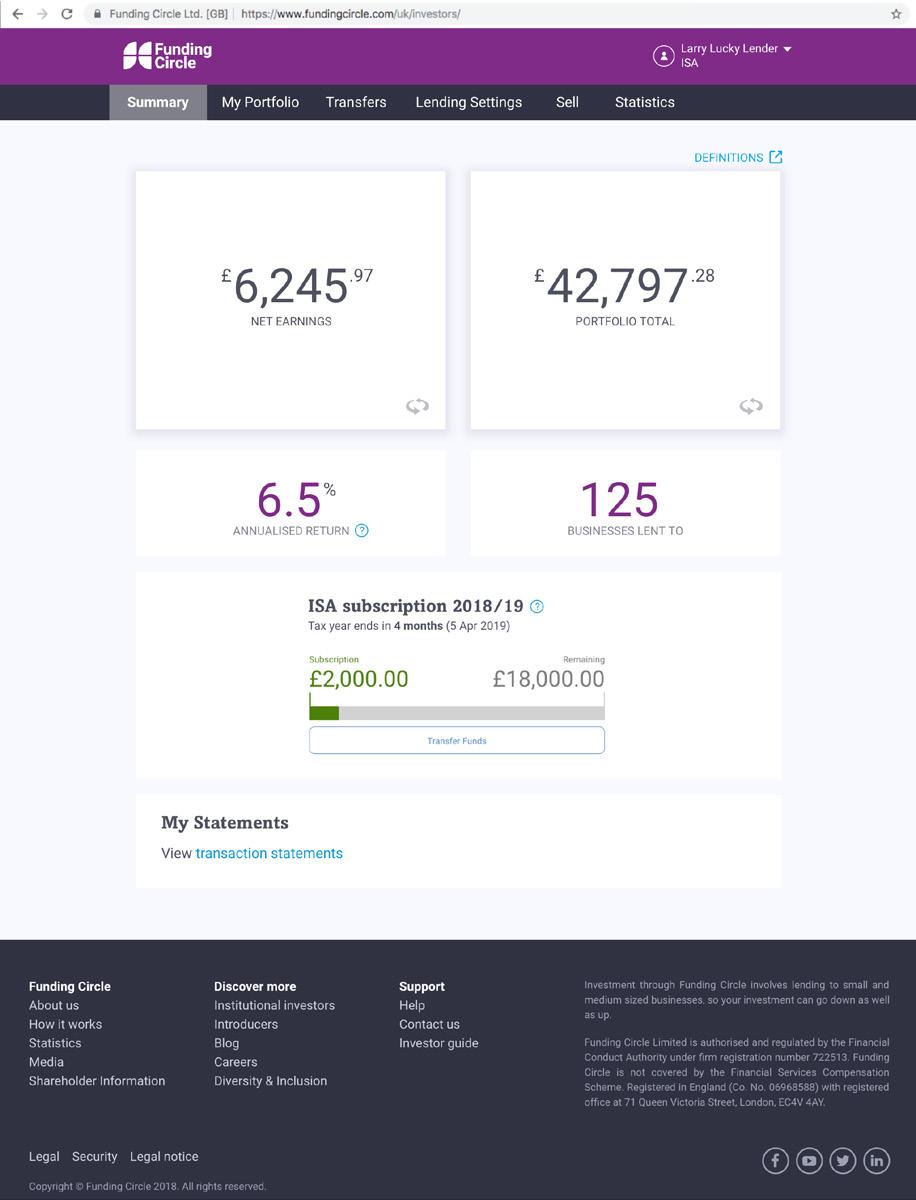

13 Account Summary Here you can keep track of your interest earned to date, the loans you re bidding on, the businesses you re lending to and much more. 13

14 Net earnings and earnings summary See your all time net earnings total, and flip the box over to view the full breakdown of your earnings and any losses (due to bad debt) Portfolio total See the real time status of your portfolio total and flip the box over to view your amount lent, amount ordered and what s still available to lend. Annualised return Click the? icon for information on how the return is calculated. Returns are shown before tax. Businesses lent to See the number of UK businesses you are currently lending to. My statements Download your transaction history and tax statement here. You can change the date range to the months you require. 14

15 Active lending Once you ve set up your Classic or ISA account, picked your lending option and transferred funds, you will automatically start lending your funds to businesses. Our lending tool will help you build a portfolio of loan parts, aiming for a projected return in line with that of your selected lending option. As loan applications are approved, the lending tool will order parts of those loans on your behalf. These show as Orders on your account summary page. When the loan is fully funded, your order will then become a loan part, and will show in My loan parts. It will also buy loan parts from other investors who are looking to sell. Our tool will also help you build a well diversified portfolio. New loan parts range from 10 to 100, and investors lending 2,000 or more will lend no more than 0.5% of their portfolio to any business. If you are lending 20,000 or more, you may have multiple loan parts (eg. 2 x 100) with one business, but you will still lend no more than 0.5% of your total to each one. Reinvesting You ll receive monthly repayments from the businesses you ve lent to. Typically the repayments will be both principal and interest, although property loans differ (see page 9). By keeping lending active, our lending tool will keep lending out your repayments and any available funds. This helps your interest to compound and maximise your return. If you would like to stop reinvesting, you can pause lending on your account at any time by going to the Lending settings tab in your account. 15

16 Your lending options To help you get the return you re looking for, you can choose between two lending options. You ll need to select an option when you set up your account, but you can change it at any time in your account (see page 17). Conservative Balanced You only lend to creditworthy You lend to the full range of businesses that have been creditworthy businesses to assessed as lower risk build a balanced portfolio This option has a lower This option has a higher projected return, with a lower projected return, with a higher estimated bad debt rate estimated bad debt rate What return can I expect to earn? The projected return for each lending option can change. You can see the current projected return for each option on the Lending Settings page of your Funding Circle account. When you lend to businesses, your funds will be matched to borrowers with the aim of meeting the projected return of your chosen lending option. However, it s important to remember: You are lending to your own individual portfolio of businesses, so your own projected return may be higher or lower than the projected return of your lending option. Your own individual loan parts may perform better or worse than expected, so your actual return may be higher or lower than your projected return. Important The projected return we provide is the annual return we expect you to earn, after fees and bad debt, over a typical investment period. Your return may be higher or lower than this in the short-term. Returns are likely to change over time as defaults tend to happen at certain points in a loan s life. You can read more about how your returns are likely to change over time in our blog. Remember, by lending to businesses your capital is at risk. 16

17 Changing your lending option You can change your lending option at any time by going to the Lending settings tab in your account. Simply select the option you d prefer and click save. Remember, this will only affect new lending on your account, so your projected return will change gradually as you begin to lend to businesses through your new lending option. 17

Important Please note you must use a bank")

18 Transfer funds from your bank Once your account is set up, go to the Transfer money tab to move funds in or out of your account. You can transfer money in using: UK debit card immediate transfer Bank transfer up to 5 working days (this option is not available for your first transfer) Important Please note you must use a bank account or debit card in your name, otherwise your payment will be rejected. When using a bank transfer, please ensure you enter the reference number provided, or your transfer won t go into your account. Unfortunately we can t accept cheques or credit cards. When transferring funds into an ISA account, it is important that you don t exceed your current tax year s subscription limit. It is your responsibility to keep a record of your total subscriptions across all of your ISA accounts for each tax year. To help you diversify and earn a more stable return, we suggest lending 2,000 or more. If you d like to start with less, there is a minimum initial transfer of 1,000 when opening a Classic or ISA account. This must be made by a debit card and only applies to your first transfer. 18

19 To transfer money out, you need to set up a nominated UK bank account. Again you need to use a bank account in your name. We recommend adding a nominated account before you need to make a withdrawal. If we are unable to automatically verify your bank details we may ask you to send us recent bank statements to verify your account. Accessing your money Your loan parts are typically repaid over 6 months to 5 years, but you have options to access your money at any stage. When you re ready to withdraw you have two options: 1. Withdraw as you go - Turn off reinvesting and withdraw your repayments as they come in. To turn off reinvesting, go to the Lending settings tab on your account. Scroll to the bottom and click Pause lending. With lending paused, the repayments you receive will stay as available funds for you to withdraw. 2. Withdraw a lump sum - Select the amount you d like to withdraw, and sell your active loans to other investors using our automatic selling tool. There is no fee to sell your loan parts to other investors. Go to the Sell tab in your account and enter the amount you d like to sell. Our tool will then automatically sell your loans to other investors. We ll notify you when the process is complete. 19

20 How much can I access early? Typically, you can get early access to approximately 85-95% of your funds. A loan can only be sold if it is active with no material credit issues, the business is still trading and not in the last month of its term. Often the remaining businesses will continue to make repayments, and their loans may become sellable again in the future. How long does it take to sell loan parts? Selling loans is not instant and depends on the supply of loans and demand from other investors looking to buy at that time. This can vary from a couple of hours to several weeks. If selling times are taking considerably longer than usual, a notification will be placed on your account. Statistics So you can see exactly how well we re doing, we publish all our performance data on our statistics page. You can also find in-depth articles and other resources on our blog. Quick tip Make sure you keep your profile section up to date in case we ever need to contact you about your account (to confirm a transfer for example). We ll either call you or send you an . How else will we contact you? We also send regular newsletters, which you can opt-out of at any time by clicking unsubscribe. 20

21 ISA Account Individual Savings Accounts (ISAs) are accounts for savings and investments that let you earn tax-free returns. The Funding Circle ISA is an Innovative Finance ISA, which allows you to earn tax-free returns by lending directly to businesses through Funding Circle. Every tax year you have a subscription limit which can be split between a Cash ISA, Stocks & Shares ISA, Lifetime ISA and an Innovative Finance ISA. You can only subscribe to one of each ISA type per year, so it s important to choose your ISA provider and product carefully. The Funding Circle ISA is also a flexi ISA, which means you can take money out of your account and put it back later in the same tax year, without losing your tax-free entitlement. Find out more about withdrawing funds in Accessing your money on page 19. ISA key facts and features All ISAs: You have a subscription limit of 20,000 for the 2017/18 tax year which can be split across all ISA types You must be 18+ years of age and a UK resident You need a National Insurance number to apply You can only subscribe to one Innovative Finance ISA per tax year, which can be opened through your chosen platform The Funding Circle ISA: The ISA account is a flexi ISA. Under ISA rules you can take your money out of your ISA and put it back later in the same tax year, without losing your tax-free entitlement The ISA account requires a minimum initial transfer of 1,000 You cannot transfer funds directly from a Classic account to an ISA account. You must first sell your loans, before withdrawing your funds to a nominated UK bank account and then transferring them to your ISA account You can transfer any existing ISAs you hold with other ISA providers (subject to any restrictions set by your current provider). 21

22 If you change your mind and would like to cancel your ISA account, you have 14 days from the date on which your ISA has started to cancel your agreement with us and close your ISA. If you wish to cancel your ISA, please us at or give us a call on After 14 days you must close your ISA account in the same way as you would close a Classic account. Opening an ISA account You can open an ISA account in a matter of minutes, subject to eligibility requirements. Simply follow the button from our main investor page, or on our ISA account page. Important As the Funding Circle ISA is an investment product and your returns are not guaranteed, it s important to understand the tax disadvantages which may arise if you make a loss on your investment. By putting money into your ISA account, you will use your tax-free subscription regardless of the earnings you make. If your loan parts do not earn interest or are not repaid, then you will not receive any tax benefit from them. If you are already lending through a Classic account, you can create an ISA account using the same address. Follow these steps to set yours up: 1. Login to your Funding Circle account 2. Select Open an ISA from the drop-down menu, located in the top right corner of your Summary page 3. Follow the instructions to create your ISA account Your ISA account On the Your Summary page you can see an overview of your ISA account. You can find your all-time earnings, your loan parts and download statements. The Transfer, Lending settings, Sell and Statistics sections work exactly like a Classic account. You can read about them on page

23 23

24 Transferring money to your ISA account You can transfer funds into your ISA account in the same way as a Classic account. When transferring funds, it is important that you don t exceed your current tax year s subscription limit. It is up to you to keep a record of your total ISA transfers for each tax year. When transferring funds into your ISA account, please remember: 1. The ISA account requires a minimum initial card transfer of 1, You cannot transfer funds directly from a Classic account to an ISA account. You must first sell your loans, then transfer the money raised into a nominated UK bank account before transferring them to your ISA account Transferring your existing ISAs to Funding Circle You can transfer any existing ISAs you hold over to your Funding Circle ISA, subject to any restrictions set by your current provider. This means that any funds you hold in a Cash, Stocks & Shares, or Innovative Finance ISA can be transferred to your Funding Circle ISA without affecting your current tax-year ISA subscription, unless you are transferring any funds you have used to subscribe to an ISA this tax year. Transferring an ISA is simple: 1. Navigate to the Transfers page in your account 2. Select the type of ISA you would like to transfer 3. Answer a few quick questions 4. Print, sign and date your transfer form 5. Send your transfer form to the freepost address provided More information on how to transfer an existing ISA can be found here. Transferring money to another ISA provider If you want to transfer your Funding Circle ISA to another ISA provider, you must first sell your loans (read more about selling loans on page 19). To transfer the funds raised please refer to your ISA provider. Any loans that cannot be sold will be transferred over to a new Classic account and will no longer be eligible for tax-free interest. Funding Circle does not charge a fee to transfer any available funds to another provider. 24

25 Switching between your ISA and Classic accounts Although you can manage both an ISA account and a Classic account using the same login, it s important to remember they are separate accounts that will lend to a separate portfolio of loans. You can navigate between your accounts using the drop-down menu in the top right corner. You ll then be able to transfer funds, access your money and adjust your lending settings in exactly the same way on both accounts. Interest, tax and fees Interest The interest you earn is paid by businesses on a monthly basis. Between monthly repayments you accrue interest daily, which is shown in the Summary page of your account as accrued interest. What is negative interest? When you buy loan parts from other investors, you pay them any accrued interest they ve earned since the last repayment, which shows as negative interest until that repayment comes in. This ensures that when you buy a loan part that is in-between repayments, the previous owner will earn the interest for the days before the sale, and you ll earn the interest for the days after the sale. It shows as negative interest because you ve paid out for interest that is owing, but hasn t yet been paid by the business. 25

26 Tax If you have an ISA account, any interest you earn from loans held within the ISA is tax-free. Each tax year you have a subscription limit which can be split across one of each type of ISA. If you are lending as an individual through a Classic account, the interest you earn is paid to you before tax and you may need to pay income tax on your earnings. You should declare any interest to HM Revenue & Customs on a self assessment tax return or inform your local tax office. For more tax information and how peer-to-peer loans are treated for tax purposes, please refer to our help centre or seek independent financial and tax advice. Fees Your projected return includes the 1% annual servicing fee. It is calculated monthly on the outstanding loan amount and taken directly from loan repayments. This means that by the time the interest reaches your account, the servicing fee has been applied. No servicing fee is taken from recoveries on defaulted loans. The servicing fee helps cover the cost of operating our platform and servicing the loans, for example collecting and distributing payments. There are no charges for opening an ISA or Classic account, selling loan parts or withdrawing your funds. There are also no fees on funds that aren t lent out. That s it no account fees, hidden charges or costs. What happens if Funding Circle goes out of business? In the unlikely event that Funding Circle goes out of business, you would continue to receive repayments for the loans originated on our platform and our back-up service provider would administer these payments for you. If you hold an ISA account, ISA regulations now provide for the ability for our backup servicer to become approved as an ISA manager to allow the maintenance of your ISA account. It s important to understand that if Funding Circle were to go out of business and our back-up servicer at the time was not an ISA manager, your investments may no longer benefit from tax-free earnings. Our current back-up servicer is authorised by HMRC as an ISA manager. Funding Circle is not covered by the Financial Services Compensation Scheme. 26

27 Further information Please visit our help centre for more details on a wide range of questions, including: What are the key features and risks of lending to small businesses? What are the key features and risks of lending to property professionals? What would happen in the unlikely event that Funding Circle goes out of business? What does it mean to be a Retail Client? How to make a complaint You can also visit our blog, where we post a range of articles on how to get the most from your investment and insight and analysis from across the platform: How our Collections and Recoveries process works How can your returns change over time? What could happen to your returns in an economic downturn? If you have any further questions or would like to speak to someone, our team are always happy to help Monday Friday, 9am 6pm (exc. Bank Holidays) contactus@fundingcircle.com Visit our help centre support.fundingcircle.com/home Here s a glossary of all the sections and what you can use them for: 27

28 28

Getting started as an investor. A guide for investors

Getting started as an investor A guide for investors MAKE A RETURN AND A DIFFERENCE You can earn attractive, stable returns by lending to businesses through Funding Circle. Set up your account in minutes,

Getting started as an investor A guide for investors MAKE A RETURN AND A DIFFERENCE You can earn attractive, stable returns by lending to businesses through Funding Circle. Set up your account in minutes,

Getting started as an investor. A guide for investors

Getting started as an investor A guide for investors MAKE A RETURN AND A DIFFERENCE You can earn attractive, stable returns by lending to businesses through Funding Circle. Set up your account in minutes,

Getting started as an investor A guide for investors MAKE A RETURN AND A DIFFERENCE You can earn attractive, stable returns by lending to businesses through Funding Circle. Set up your account in minutes,

Lending to small businesses

Lending to small businesses Key features and risks By lending through Funding Circle you are supporting the backbone of the UK economy, providing businesses with the finance they need to grow while earning

Lending to small businesses Key features and risks By lending through Funding Circle you are supporting the backbone of the UK economy, providing businesses with the finance they need to grow while earning

A step-by-step guide to borrowing.

A step-by-step guide to borrowing. Welcome to Funding Circle. Getting finance should be quick and easy, so you can get back to doing what you do best - running your business. That s why we ve cut out the

A step-by-step guide to borrowing. Welcome to Funding Circle. Getting finance should be quick and easy, so you can get back to doing what you do best - running your business. That s why we ve cut out the

Welcome to Lending Loop

A Guide to Lending Welcome to Lending Loop A Smarter Way to Lend This guide contains all the information you will need to start lending with Lending Loop. We ve designed our process with you in mind and

A Guide to Lending Welcome to Lending Loop A Smarter Way to Lend This guide contains all the information you will need to start lending with Lending Loop. We ve designed our process with you in mind and

INVESTOR PORTFOLIO SERVICE (IPS) ONLINE USER GUIDE

ONLINE USER GUIDE") INVESTOR PORTFOLIO SERVICE (IPS) ONLINE USER GUIDE HELPING HAND. It s important to keep a close eye on your investments, so we do all we can to lend a helping hand. That s why we ve put together this step-by-step

INVESTOR PORTFOLIO SERVICE (IPS) ONLINE USER GUIDE HELPING HAND. It s important to keep a close eye on your investments, so we do all we can to lend a helping hand. That s why we ve put together this step-by-step

Innovative Finance ISA Key Information

Innovative Finance ISA Key Information April 2018 The purpose of this ISA Investor Key Information document is to focus your attention on some of the important things you should know before deciding to

Innovative Finance ISA Key Information April 2018 The purpose of this ISA Investor Key Information document is to focus your attention on some of the important things you should know before deciding to

From application to pay-out.

An introducer s guide: From application to pay-out. Find out more W fundingcircle.com E introducer@fundingcircle.com T 0203 667 2208 Welcome to Funding Circle Business finance should be straight-forward,

An introducer s guide: From application to pay-out. Find out more W fundingcircle.com E introducer@fundingcircle.com T 0203 667 2208 Welcome to Funding Circle Business finance should be straight-forward,

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT FINANCIAL GUIDE Green Financial Advice is authorised and regulated by the Financial

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT FINANCIAL GUIDE Green Financial Advice is authorised and regulated by the Financial

Interest Rates, Charges & Important Information

Interest Rates, Charges & Important Information Guide To Changes We are making some changes to this brochure. The changes will come into effect on 6th April 2018 and will apply to all St. James s Place

Interest Rates, Charges & Important Information Guide To Changes We are making some changes to this brochure. The changes will come into effect on 6th April 2018 and will apply to all St. James s Place

Business loans at Funding Circle

Business loans at Funding Circle A step-by-step guide to borrowing Business finance tailored to you 94% of customers would come back to us first Getting finance to take the next step for your business

Business loans at Funding Circle A step-by-step guide to borrowing Business finance tailored to you 94% of customers would come back to us first Getting finance to take the next step for your business

Fixed Rate Cash ISA. Savings

Savings Fixed Rate Cash ISA The Financial Conduct Authority is the independent financial services regulator. It requires us, Britannia, to give you this important information to help you to decide whether

Savings Fixed Rate Cash ISA The Financial Conduct Authority is the independent financial services regulator. It requires us, Britannia, to give you this important information to help you to decide whether

Interest rates, charges and important information

Interest rates, charges and important information Guide to Changes: We are making some changes to this brochure. The changes will come into effect on 6 April 2018 and will apply to all Intelligent Finance

Interest rates, charges and important information Guide to Changes: We are making some changes to this brochure. The changes will come into effect on 6 April 2018 and will apply to all Intelligent Finance

Business loans at Funding Circle

Business loans at Funding Circle A guide for introducers Dedicated service for introducers Getting finance for your clients is now fast and hassle free. So you can help your clients get the fast access

Business loans at Funding Circle A guide for introducers Dedicated service for introducers Getting finance for your clients is now fast and hassle free. So you can help your clients get the fast access

GETTING THE MOST FROM YOUR PENSION SAVINGS

GETTING THE MOST FROM YOUR PENSION SAVINGS 2 Getting the most from your pension savings CONTENTS 04 Two types of pension 05 Tax and your pension An overview 05 Who can pay into a pension? 05 How does tax

GETTING THE MOST FROM YOUR PENSION SAVINGS 2 Getting the most from your pension savings CONTENTS 04 Two types of pension 05 Tax and your pension An overview 05 Who can pay into a pension? 05 How does tax

Retirement Investments Retirement Insurance Health Investments Insurance Health

Retirement Investments Insurance Health Investment Portfolio Investment Portfolio from Aviva Whatever your financial needs, Investment Portfolio offers you a wide range of investment options, giving you

Retirement Investments Insurance Health Investment Portfolio Investment Portfolio from Aviva Whatever your financial needs, Investment Portfolio offers you a wide range of investment options, giving you

WESLEYAN UNIT TRUST INDIVIDUAL SAVINGS ACCOUNT (ISA)

") IMPORTANT DOCUMENT PLEASE READ WESLEYAN UNIT TRUST INDIVIDUAL SAVINGS ACCOUNT (ISA) INCLUDING THE TERMS AND CONDITIONS 02 Individual Savings Account (ISA) KEY FEATURES OF THE INDIVIDUAL SAVINGS ACCOUNT

IMPORTANT DOCUMENT PLEASE READ WESLEYAN UNIT TRUST INDIVIDUAL SAVINGS ACCOUNT (ISA) INCLUDING THE TERMS AND CONDITIONS 02 Individual Savings Account (ISA) KEY FEATURES OF THE INDIVIDUAL SAVINGS ACCOUNT

Get connected. A how to guide to your Alliance Trust Savings platform

Get connected A how to guide to your Alliance Trust Savings platform 2 Get connected with Alliance Trust Savings As an Alliance Trust Savings customer, you have 24/7 secure online access to your Account(s).

Get connected A how to guide to your Alliance Trust Savings platform 2 Get connected with Alliance Trust Savings As an Alliance Trust Savings customer, you have 24/7 secure online access to your Account(s).

Essential Super. Reference Guide. MySuper

Essential Super Reference Guide MySuper MYSUPER AUTHORISATION IDENTIFIER 5 6 6 019 2 5 4 3 5 9 0 9 Issue No 2018/1, dated 17 March 2018 Investments in Essential Super are offered from Commonwealth Essential

Essential Super Reference Guide MySuper MYSUPER AUTHORISATION IDENTIFIER 5 6 6 019 2 5 4 3 5 9 0 9 Issue No 2018/1, dated 17 March 2018 Investments in Essential Super are offered from Commonwealth Essential

Santander Investment Hub Key Features Document (including Fees, Charges & Interest rates and Best Execution Policy)

") Santander Investment Hub Key Features Document (including Fees, Charges & Interest rates and Best Execution Policy) Effective from 6 April 2018 This document provides information about the Santander Investment

Santander Investment Hub Key Features Document (including Fees, Charges & Interest rates and Best Execution Policy) Effective from 6 April 2018 This document provides information about the Santander Investment

Retirement Account. Key Features of the

Key Features of the Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, ReAssure, to give you this important information to help you decide whether our

Key Features of the Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, ReAssure, to give you this important information to help you decide whether our

INVESTOR PORTFOLIO SERVICE (IPS) GUIDE TO FACILITATED ADVISER CHARGES.

GUIDE TO FACILITATED ADVISER CHARGES.") INVESTOR PORTFOLIO SERVICE (IPS) GUIDE TO FACILITATED ADVISER CHARGES. This is an important document. Please keep it safe for future reference. INVESTOR PORTFOLIO SERVICE (IPS) GUIDE TO FACILITATED ADVISER

INVESTOR PORTFOLIO SERVICE (IPS) GUIDE TO FACILITATED ADVISER CHARGES. This is an important document. Please keep it safe for future reference. INVESTOR PORTFOLIO SERVICE (IPS) GUIDE TO FACILITATED ADVISER

Further information about your mortgage

Further information about your mortgage This booklet explains how we now manage your mortgage. It also explains how we managed your account before we made changes. The booklet does not set out to explain

Further information about your mortgage This booklet explains how we now manage your mortgage. It also explains how we managed your account before we made changes. The booklet does not set out to explain

Key Features of the Options ISA. - Anytime Access option - Fixed Term option

Key Features of the Options ISA - option - option The Financial Conduct Authority is a financial services regulator. It requires us, Police Mutual, to give you this important information to help you decide

Key Features of the Options ISA - option - option The Financial Conduct Authority is a financial services regulator. It requires us, Police Mutual, to give you this important information to help you decide

SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS

INVESTMENTS") SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

Interest rates, charges and important information

Interest rates, charges and important information CONTENTS Savings 1 Current Accounts 9 International Payment Services 13 Mortgages 14 Important Information 15 Savings Intelligent Finance isaver Intelligent

Interest rates, charges and important information CONTENTS Savings 1 Current Accounts 9 International Payment Services 13 Mortgages 14 Important Information 15 Savings Intelligent Finance isaver Intelligent

Aegon Platform key information document

For customers Aegon Platform key information document Including the Aegon ISA and Aegon General Investment Account key features documents The information that follows is accurate to the best of our knowledge

For customers Aegon Platform key information document Including the Aegon ISA and Aegon General Investment Account key features documents The information that follows is accurate to the best of our knowledge

START INVESTING A STEP-BY-STEP GUIDE. A quick and easy guide to making your first investment on LendInvest

START INVESTING A STEP-BY-STEP GUIDE A quick and easy guide to making your first investment on LendInvest Summary How peer-to-peer (P2P) works at LendInvest 3 Funding your account 4 Selecting a property

START INVESTING A STEP-BY-STEP GUIDE A quick and easy guide to making your first investment on LendInvest Summary How peer-to-peer (P2P) works at LendInvest 3 Funding your account 4 Selecting a property

Getting started with Alliance Trust Savings How to guide

Getting started with Alliance Trust Savings How to guide Contents Getting started 05 How to... Log in 07 How to... Set up a Direct Debit 10 How to... Set up regular monthly dealing 12 How to... Change

Getting started with Alliance Trust Savings How to guide Contents Getting started 05 How to... Log in 07 How to... Set up a Direct Debit 10 How to... Set up regular monthly dealing 12 How to... Change

Your guide to lifetime mortgages

Your guide to lifetime mortgages What is a lifetime mortgage? 1 What difference could a lifetime mortgage make to you? 4 What is a lifetime mortgage? A way of releasing money from your home without having

Your guide to lifetime mortgages What is a lifetime mortgage? 1 What difference could a lifetime mortgage make to you? 4 What is a lifetime mortgage? A way of releasing money from your home without having

USING IPS. START. This document gives you information about using IPS to manage and make changes to your investment.

LEGAL & GENERAL INVESTOR PORTFOLIO SERVICE (IPS) USING IPS. This document gives you information about using IPS to manage and make changes to your investment. START USING THIS DOCUMENT. This document gives

LEGAL & GENERAL INVESTOR PORTFOLIO SERVICE (IPS) USING IPS. This document gives you information about using IPS to manage and make changes to your investment. START USING THIS DOCUMENT. This document gives

YOUR COMPANY PENSION GROUP PERSONAL PENSION. A guide to help you prepare for the retirement you want

YOUR COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want WELCOME TO YOUR SCOTTISH WIDOWS WORKPLACE PENSION Everyone needs a plan for their retirement. This guide

YOUR COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want WELCOME TO YOUR SCOTTISH WIDOWS WORKPLACE PENSION Everyone needs a plan for their retirement. This guide

THE MARIE CURIE COMPANY PENSION GROUP PERSONAL PENSION. A guide to help you prepare for the retirement you want

THE MARIE CURIE COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your Marie Curie company pension is provided by Scottish Widows. INTRODUCING ZAPPAR Welcome

THE MARIE CURIE COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your Marie Curie company pension is provided by Scottish Widows. INTRODUCING ZAPPAR Welcome

WELCOME TO ALLIANCE TRUST SAVINGS. Guide for Advised Clients

WELCOME TO ALLIANCE TRUST SAVINGS Guide for Advised Clients 2 Welcome to Alliance Trust Savings IN THIS GUIDE This guide is designed to provide helpful information and answer the questions we are most

WELCOME TO ALLIANCE TRUST SAVINGS Guide for Advised Clients 2 Welcome to Alliance Trust Savings IN THIS GUIDE This guide is designed to provide helpful information and answer the questions we are most

Retirement Investments Retirement Insurance Health Investments Insurance Health

Retirement Investments Insurance Health ISA Portfolio If you re investing for the medium to long term, then you should always consider a stocks and shares ISA with the significant tax advantages it offers.

Retirement Investments Insurance Health ISA Portfolio If you re investing for the medium to long term, then you should always consider a stocks and shares ISA with the significant tax advantages it offers.

Co-operative Bank Cash ISA

Key features of our Co-operative Bank Cash ISA The Financial Conduct Authority is the independent financial services regulator. It requires us, The Co-operative Bank, to give you this important information

Key features of our Co-operative Bank Cash ISA The Financial Conduct Authority is the independent financial services regulator. It requires us, The Co-operative Bank, to give you this important information

Terms and Conditions of the Cofunds Platform

SELF-DIRECTED Terms and Conditions of the Cofunds Platform You must take time to read through this booklet, as this is a legal contract between you and Cofunds. Version 0118SDE Issued and approved by Cofunds

SELF-DIRECTED Terms and Conditions of the Cofunds Platform You must take time to read through this booklet, as this is a legal contract between you and Cofunds. Version 0118SDE Issued and approved by Cofunds

An introduction to the Cofunds Pension Account

Product guide for self-directed investors An introduction to the Cofunds Pension Account provided by Suffolk Life A straightforward way to plan for your retirement Contents Introduction 1 The experts behind

Product guide for self-directed investors An introduction to the Cofunds Pension Account provided by Suffolk Life A straightforward way to plan for your retirement Contents Introduction 1 The experts behind

YOUR COMPANY PENSION GROUP STAKEHOLDER PENSION. A guide to help you prepare for the retirement you want

YOUR COMPANY PENSION GROUP STAKEHOLDER PENSION A guide to help you prepare for the retirement you want WELCOME TO YOUR SCOTTISH WIDOWS WORKPLACE PENSION Everyone needs a plan for their retirement. This

YOUR COMPANY PENSION GROUP STAKEHOLDER PENSION A guide to help you prepare for the retirement you want WELCOME TO YOUR SCOTTISH WIDOWS WORKPLACE PENSION Everyone needs a plan for their retirement. This

Key Features of the Stakeholder Pension. For plans started on or after 1 February Retirement Investments Insurance Health

Key Features of the Stakeholder Pension For plans started on or after 1 February 2008 Retirement Investments Insurance Health Key Features of the Stakeholder Pension The Financial Conduct Authority is

Key Features of the Stakeholder Pension For plans started on or after 1 February 2008 Retirement Investments Insurance Health Key Features of the Stakeholder Pension The Financial Conduct Authority is

product guide. This is an important document. Please keep it safe for future reference. Legal & General select portfolio bond

SELECT PORTFOLIO BOND (WEALTH MANAGERS) product guide. This is an important document. Please keep it safe for future reference. Legal & General select portfolio bond 2 SELECT PORTFOLIO BOND (wealth managers)

SELECT PORTFOLIO BOND (WEALTH MANAGERS) product guide. This is an important document. Please keep it safe for future reference. Legal & General select portfolio bond 2 SELECT PORTFOLIO BOND (wealth managers)

Stakeholder Pension. The simple way to start a pension plan. Retirement Investments Insurance Health

Stakeholder Pension The simple way to start a pension plan Retirement Investments Insurance Health Introduction Any decision you make about investing for your future retirement needs careful consideration

Stakeholder Pension The simple way to start a pension plan Retirement Investments Insurance Health Introduction Any decision you make about investing for your future retirement needs careful consideration

Key Features of the Stakeholder Pension Plan

Key Features of the Stakeholder Pension Plan The Financial Conduct Authority is a financial service regulator. It require us, Police Mutual, to give you this important information to help you to decide

Key Features of the Stakeholder Pension Plan The Financial Conduct Authority is a financial service regulator. It require us, Police Mutual, to give you this important information to help you to decide

GUIDE TO YOUR RETIREMENT. Your choices explained. Pensions

GUIDE TO YOUR RETIREMENT Your choices explained Pensions 2 Please read this guide in conjunction with the Money Advice Service guide Your pension: it s time to choose which is included with your Retirement

GUIDE TO YOUR RETIREMENT Your choices explained Pensions 2 Please read this guide in conjunction with the Money Advice Service guide Your pension: it s time to choose which is included with your Retirement

PENSION BENEFITS GUIDE HOW YOU CAN USE YOUR PENSION POT TO SUIT YOUR NEEDS

PENSION BENEFITS GUIDE HOW YOU CAN USE YOUR PENSION POT TO SUIT YOUR NEEDS With the flexibility you have to take benefits through your pension, it can be difficult to know what s best for you and your

PENSION BENEFITS GUIDE HOW YOU CAN USE YOUR PENSION POT TO SUIT YOUR NEEDS With the flexibility you have to take benefits through your pension, it can be difficult to know what s best for you and your

New Generation Personal Pension

To be used with Group Personal Pension Schemes that comply with Automatic Enrolment Regulations. Key Features of the New Generation Personal Pension Reference MPEN30/A 04.18 The Financial Conduct Authority

To be used with Group Personal Pension Schemes that comply with Automatic Enrolment Regulations. Key Features of the New Generation Personal Pension Reference MPEN30/A 04.18 The Financial Conduct Authority

Alliance Trust Savings Platform Products Key Facts for Advised Clients

Alliance Trust Savings Platform Products Key Facts for Advised Clients June 2018 2 Key Facts: Alliance Trust Savings Platform Products CONTENTS This is a Key Facts Document (KFD) giving you important information

Alliance Trust Savings Platform Products Key Facts for Advised Clients June 2018 2 Key Facts: Alliance Trust Savings Platform Products CONTENTS This is a Key Facts Document (KFD) giving you important information

Wrap ISA and. Wrap Personal Portfolio. Key Features. Helping you decide. 2. Your commitment. 1. Its aims

Wrap ISA and Wrap Personal Portfolio Key Features This key features document is for UK residents only. The Financial Conduct Authority is a financial services regulator. It requires us, Standard Life,

Wrap ISA and Wrap Personal Portfolio Key Features This key features document is for UK residents only. The Financial Conduct Authority is a financial services regulator. It requires us, Standard Life,

THE AURUM COMPANY PENSION GROUP PERSONAL PENSION. A guide to help you prepare for the retirement you want

THE AURUM COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your AURUM company pension is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS TO HELP

THE AURUM COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your AURUM company pension is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS TO HELP

smile cash ISA Key features of our

Key features of our smile cash ISA The Financial Conduct Authority is the independent financial services regulator. It requires us, smile, to give you this important information to help you decide whether

Key features of our smile cash ISA The Financial Conduct Authority is the independent financial services regulator. It requires us, smile, to give you this important information to help you decide whether

LENDER AND ISA GUIDE

LENDER AND ISA GUIDE Great investments. Brilliant feeling. Huge impact. As well as earning a great interest rate, your FOLK2FOLK investment will be doing great things. Why invest with FOLK2FOLK? Earn up

LENDER AND ISA GUIDE Great investments. Brilliant feeling. Huge impact. As well as earning a great interest rate, your FOLK2FOLK investment will be doing great things. Why invest with FOLK2FOLK? Earn up

Get great value now and in the years ahead. The Fidelity guide to pricing

Get great value now and in the years ahead The Fidelity guide to pricing Value and support throughout your investment journey Whenever you re thinking about buying something, from a phone or a car to a

Get great value now and in the years ahead The Fidelity guide to pricing Value and support throughout your investment journey Whenever you re thinking about buying something, from a phone or a car to a

Wrap ISA and Wrap Personal Portfolio

Wrap ISA and Wrap Personal Portfolio Key Features This key features document is for UK residents only. The Financial Conduct Authority is a financial services regulator. It requires us, Standard Life,

Wrap ISA and Wrap Personal Portfolio Key Features This key features document is for UK residents only. The Financial Conduct Authority is a financial services regulator. It requires us, Standard Life,

Wrap ISA and Wrap Personal Portfolio

Wrap ISA and Wrap Personal Portfolio Key Features This key features document is for UK residents only. The Financial Conduct Authority is a financial services regulator. It requires us, Standard Life,

Wrap ISA and Wrap Personal Portfolio Key Features This key features document is for UK residents only. The Financial Conduct Authority is a financial services regulator. It requires us, Standard Life,

Guide to buying an annuity

Guide to buying an annuity 2 Welcome to our guide to buying an annuity You now have more choice than ever before when it comes to using your pension savings. Of course having more options can make it difficult

Guide to buying an annuity 2 Welcome to our guide to buying an annuity You now have more choice than ever before when it comes to using your pension savings. Of course having more options can make it difficult

INVESTOR PORTFOLIO SERVICE (IPS) USING IPS.

USING IPS.") INVESTOR PORTFOLIO SERVICE (IPS) USING IPS. This document gives you information about using IPS to manage and make changes to your investment. USING THIS DOCUMENT. This document gives you important information

INVESTOR PORTFOLIO SERVICE (IPS) USING IPS. This document gives you information about using IPS to manage and make changes to your investment. USING THIS DOCUMENT. This document gives you important information

IMPORTANT DOCUMENT PLEASE READ WESLEYAN UNIT TRUST JUNIOR INDIVIDUAL SAVINGS ACCOUNT (JUNIOR ISA) (INCLUDING THE TERMS AND CONDITIONS)

(INCLUDING THE TERMS AND CONDITIONS)") IMPORTANT DOCUMENT PLEASE READ WESLEYAN UNIT TRUST JUNIOR INDIVIDUAL SAVINGS ACCOUNT (JUNIOR ISA) (INCLUDING THE TERMS AND CONDITIONS) 02 Junior Individual Savings Account (Junior ISA) KEY FEATURES OF

IMPORTANT DOCUMENT PLEASE READ WESLEYAN UNIT TRUST JUNIOR INDIVIDUAL SAVINGS ACCOUNT (JUNIOR ISA) (INCLUDING THE TERMS AND CONDITIONS) 02 Junior Individual Savings Account (Junior ISA) KEY FEATURES OF

IMPORTANT DOCUMENT PLEASE READ THE WITH PROFITS INDIVIDUAL SAVINGS ACCOUNT (ISA) (FOR NON ADVISED ISAs ISSUED ON OR BEFORE 30 DECEMBER 2012)

(FOR NON ADVISED ISAs ISSUED ON OR BEFORE 30 DECEMBER 2012)") IMPORTANT DOCUMENT PLEASE READ THE WITH PROFITS INDIVIDUAL SAVINGS ACCOUNT (ISA) (FOR NON ADVISED ISAs ISSUED ON OR BEFORE 30 DECEMBER 2012) 02 The With Proمحts Individual Savings Account (ISA) KEY FEATURES

IMPORTANT DOCUMENT PLEASE READ THE WITH PROFITS INDIVIDUAL SAVINGS ACCOUNT (ISA) (FOR NON ADVISED ISAs ISSUED ON OR BEFORE 30 DECEMBER 2012) 02 The With Proمحts Individual Savings Account (ISA) KEY FEATURES

GUIDE TO YOUR RETIREMENT. Your choices explained. Pensions

GUIDE TO YOUR RETIREMENT Your choices explained Pensions 2 Please read this guide in conjunction with the Money Advice Service guide Your pension: it s time to choose which is included with your Retirement

GUIDE TO YOUR RETIREMENT Your choices explained Pensions 2 Please read this guide in conjunction with the Money Advice Service guide Your pension: it s time to choose which is included with your Retirement

Key Features of the General Investment Account and ISA Account for the Global Investment Centre

Key Features of the General Investment Account and ISA Account for the Global Investment Centre This is an important document. You need to read this before you invest in the General Investment Account

Key Features of the General Investment Account and ISA Account for the Global Investment Centre This is an important document. You need to read this before you invest in the General Investment Account

MORTGAGE PRODUCT TRANSFER SERVICE

MORTGAGE PRODUCT TRANSFER SERVICE Everything you need to know about using our service WELCOME Thank you for choosing to use our product transfer service. When it comes to renewing a customer s mortgage,

MORTGAGE PRODUCT TRANSFER SERVICE Everything you need to know about using our service WELCOME Thank you for choosing to use our product transfer service. When it comes to renewing a customer s mortgage,

Living today while planning for tomorrow. UTC Employee Savings Plan Enrollment Guide TOTAL REWARDS

Living today while planning for tomorrow 2018 UTC Employee Savings Plan Enrollment Guide TOTAL REWARDS WHAT S INSIDE Why Save Now?...3 Steps To Getting Started STEP 1: Decide How Much To Save...4 STEP

Living today while planning for tomorrow 2018 UTC Employee Savings Plan Enrollment Guide TOTAL REWARDS WHAT S INSIDE Why Save Now?...3 Steps To Getting Started STEP 1: Decide How Much To Save...4 STEP

Key Features of the Group Personal Pension 2000 Plan. This is an important document which you should keep in a safe place.

Key Features of the Group Personal Pension 2000 Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Key Features of the Group Personal Pension 2000 Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Your Guide to the Personal Finance Portal (PFP)

") Your Guide to the Personal Finance Portal (PFP) Introduction to the Personal Finance Portal Access to the Personal Finance Portal (PFP) is provided as part of our Ongoing Service for investment customers.

Your Guide to the Personal Finance Portal (PFP) Introduction to the Personal Finance Portal Access to the Personal Finance Portal (PFP) is provided as part of our Ongoing Service for investment customers.

ISA and Investment Funds

ISA and Investment Funds Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator. It requires us, Standard

ISA and Investment Funds Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator. It requires us, Standard

Flexible Guarantee Bond Series 3

Flexible Guarantee Bond Series 3 Supplementary Information Document (SID) This document provides you with additional important information to help you to decide whether our Flexible Guarantee Bond is right

Flexible Guarantee Bond Series 3 Supplementary Information Document (SID) This document provides you with additional important information to help you to decide whether our Flexible Guarantee Bond is right

Self Invested Personal Pension. How it can work for you

Self Invested Personal Pension How it can work for you Contents 02 Combining your pensions 03 Maximising your tax efficiency 04 Your payment options 06 Your investment choices 07 Accessing your money 08

Self Invested Personal Pension How it can work for you Contents 02 Combining your pensions 03 Maximising your tax efficiency 04 Your payment options 06 Your investment choices 07 Accessing your money 08

New Generation Personal Pension

Key Features of the New Generation Personal Pension Reference MPEN1/A 04.18 The Financial Conduct Authority is a financial services regulator. It requires us, Aviva Life & Pensions UK Limited, to give

Key Features of the New Generation Personal Pension Reference MPEN1/A 04.18 The Financial Conduct Authority is a financial services regulator. It requires us, Aviva Life & Pensions UK Limited, to give

All you need to know Optional Payment Lifetime Mortgage

All you need to know Optional Payment Lifetime Mortgage Contents Section 1 All about our Lifetime Mortgages 3 Section 2 Applying for a lifetime mortgage 11 Section 3 What happens if your circumstances

All you need to know Optional Payment Lifetime Mortgage Contents Section 1 All about our Lifetime Mortgages 3 Section 2 Applying for a lifetime mortgage 11 Section 3 What happens if your circumstances

Flexible Pension Plan

Flexible Pension Plan Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator. It requires us, Standard

Flexible Pension Plan Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator. It requires us, Standard

Pension Portfolio J26372_LF10207_0318.indd 1 05/03/18 6:39 am

Pension Portfolio could be the perfect home for your pension. It allows you to take full advantage of the pension freedoms. Pension Portfolio has two options - Core and Choice - which are designed to meet

Pension Portfolio could be the perfect home for your pension. It allows you to take full advantage of the pension freedoms. Pension Portfolio has two options - Core and Choice - which are designed to meet

Collective Retirement Account

Key features of the Collective Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, Old Mutual Wealth, to give you this important information to help you

Key features of the Collective Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, Old Mutual Wealth, to give you this important information to help you

Key features of the Flexible Pension Plan

Key features of the Flexible Pension Plan Read on to find out the main points about your Flexible Pension Plan. You ll also get a personal illustration, so you can put figures to the benefits you may receive

Key features of the Flexible Pension Plan Read on to find out the main points about your Flexible Pension Plan. You ll also get a personal illustration, so you can put figures to the benefits you may receive

Accessing your pension savings

Accessing your pension savings 2 Accessing your pension savings CONTENTS 03 About this guide 04 An important note 06 A few basics to start 06 Your options in summary 07 Tax-free cash 10 Flexible retirement

Accessing your pension savings 2 Accessing your pension savings CONTENTS 03 About this guide 04 An important note 06 A few basics to start 06 Your options in summary 07 Tax-free cash 10 Flexible retirement

Key Features of the Stakeholder Pension

Key Features of the Stakeholder Pension For plans started on or after 1 February 2008 Key Features of the Stakeholder Pension The Financial Services Authority is the independent financial services regulator.

Key Features of the Stakeholder Pension For plans started on or after 1 February 2008 Key Features of the Stakeholder Pension The Financial Services Authority is the independent financial services regulator.

KEY FEATURES OF THE SAVE THE CHILDREN UK GROUP PERSONAL PENSION PLAN.

KEY FEATURES OF THE SAVE THE CHILDREN UK GROUP PERSONAL PENSION PLAN. This is an important document which you should keep in a safe place. Legal & General working in Association with: 2 SAVE THE CHILDREN

KEY FEATURES OF THE SAVE THE CHILDREN UK GROUP PERSONAL PENSION PLAN. This is an important document which you should keep in a safe place. Legal & General working in Association with: 2 SAVE THE CHILDREN

TAKE CHARGE OF YOUR RETIREMENT.

TAKE CHARGE OF YOUR RETIREMENT. Make it personal. And keep it on target. That s what Target Retirement s are designed to do make it easier to invest properly during your working years and help you achieve

TAKE CHARGE OF YOUR RETIREMENT. Make it personal. And keep it on target. That s what Target Retirement s are designed to do make it easier to invest properly during your working years and help you achieve

Cash ISAs. Important information and Key Facts

Cash ISAs Important information and Key Facts We d like to help your savings grow faster. Some of us are seasoned savers. Others just starting out. But one thing s for sure, it always makes good sense

Cash ISAs Important information and Key Facts We d like to help your savings grow faster. Some of us are seasoned savers. Others just starting out. But one thing s for sure, it always makes good sense

Bank of Montreal. Investing for you. Individual Savings Account General Investment Account ISA GIA

Bank of Montreal Investing for you. ISA GIA Individual Savings Account General Investment Account Investing for your future 3 Contents 1. Start with a BMO plan 4 Investing for you: Individual Savings Account

Bank of Montreal Investing for you. ISA GIA Individual Savings Account General Investment Account Investing for your future 3 Contents 1. Start with a BMO plan 4 Investing for you: Individual Savings Account

THE NTT EUROPE COMPANY PENSION GROUP PERSONAL PENSION. A guide to help you prepare for the retirement you want

THE NTT EUROPE COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your NTT Europe company pension is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS

THE NTT EUROPE COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your NTT Europe company pension is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS

An introduction to the Cofunds Pension Account

Product guide for self-directed investors An introduction to the Cofunds Pension Account provided by Suffolk Life A straightforward way to plan for your retirement Contents Introduction 1 The experts behind

Product guide for self-directed investors An introduction to the Cofunds Pension Account provided by Suffolk Life A straightforward way to plan for your retirement Contents Introduction 1 The experts behind

Customer Guide. Don t just be good with money, be MoneyBrilliant

Customer Guide Welcome to MoneyBrilliant. Your Financial Partner has invited you to use the MoneyBrilliant service and to share your MoneyBrilliant information with them. They can work with you and provide

Customer Guide Welcome to MoneyBrilliant. Your Financial Partner has invited you to use the MoneyBrilliant service and to share your MoneyBrilliant information with them. They can work with you and provide

Key Features of the Group Stakeholder Pension Scheme. This is an important document which you should keep in a safe place.

Key Features of the Group Stakeholder Pension Scheme This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Key Features of the Group Stakeholder Pension Scheme This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Flexible Transitions Account

Flexible Transitions Account Key features of the Flexible Transitions Account The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important information

Flexible Transitions Account Key features of the Flexible Transitions Account The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important information

KEY FEATURES OF CORE INVESTMENTS

KEY FEATURES OF CORE INVESTMENTS The Financial Conduct Authority is a financial services regulator. It requires us, Royal London, to give you this important information to help you to decide whether our

KEY FEATURES OF CORE INVESTMENTS The Financial Conduct Authority is a financial services regulator. It requires us, Royal London, to give you this important information to help you to decide whether our

Doing Business with FundsNetwork

Doing Business with FundsNetwork Including the Key Features of the Investment Fund Account and ISA Contents About FundsNetwork 1 About this document 1 Other documents to read 1 Communicating with you 2

Doing Business with FundsNetwork Including the Key Features of the Investment Fund Account and ISA Contents About FundsNetwork 1 About this document 1 Other documents to read 1 Communicating with you 2

INFORMATION ABOUT YOUR MORTGAGE.

INFORMATION ABOUT YOUR MORTGAGE. WELCOME TO YOUR GUIDE TO HALIFAX MORTGAGES. Please read this booklet alongside your mortgage conditions and offer letter. It explains our most often used policies and procedures.

INFORMATION ABOUT YOUR MORTGAGE. WELCOME TO YOUR GUIDE TO HALIFAX MORTGAGES. Please read this booklet alongside your mortgage conditions and offer letter. It explains our most often used policies and procedures.

Getting the retirement income you need RETIREMENT PLANNING

Getting the retirement income you need RETIREMENT PLANNING 01 It can be a big decision. But you don t have to make it on your own Whether your retirement is still a little way off or coming up quickly,

Getting the retirement income you need RETIREMENT PLANNING 01 It can be a big decision. But you don t have to make it on your own Whether your retirement is still a little way off or coming up quickly,

INVESTMENTS. The M&G guide to. bonds. Investing Bonds Property Equities Risk Multi-asset investing Income

INVESTMENTS The M&G guide to bonds Investing Bonds Property Equities Risk Multi-asset investing Income Contents Explaining the world of bonds 3 Understanding how bond prices can rise or fall 5 The different

INVESTMENTS The M&G guide to bonds Investing Bonds Property Equities Risk Multi-asset investing Income Contents Explaining the world of bonds 3 Understanding how bond prices can rise or fall 5 The different

FAQ. Jump to. How does one Finch? Signing Up. Pay and Request. Tabs. Bank Transfers. Bank Account and Cards. Account Settings and Security

FAQ How does one Finch? Jump to Signing Up Pay and Request Tabs Bank Transfers Bank Account and Cards Account Settings and Security Signing Up Having trouble getting started? Where can I sign up? You can

FAQ How does one Finch? Jump to Signing Up Pay and Request Tabs Bank Transfers Bank Account and Cards Account Settings and Security Signing Up Having trouble getting started? Where can I sign up? You can

Key Lender Information

Key Lender Information The purpose of this Key Lender Information document is to focus your attention on some of the important things you should know before deciding to lend your money on the Lending Works

Key Lender Information The purpose of this Key Lender Information document is to focus your attention on some of the important things you should know before deciding to lend your money on the Lending Works

Active Money Self Invested Personal Pension Key Features

Active Money Self Invested Personal Pension Key Features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is an independent financial services

Active Money Self Invested Personal Pension Key Features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is an independent financial services

Guide to. buying an annuity

Guide to buying an annuity 2 Guide to buying an annuity Welcome to our guide to buying an annuity You now have more flexibility than ever before when it comes to using your pension savings. Of course all

Guide to buying an annuity 2 Guide to buying an annuity Welcome to our guide to buying an annuity You now have more flexibility than ever before when it comes to using your pension savings. Of course all

Platform Key Information Document

SELF-DIRECTED Platform Key Information Document Including the ISA and Investment Funds Key Features documents The information that follows is accurate to the best of our knowledge and belief as at 06 April

SELF-DIRECTED Platform Key Information Document Including the ISA and Investment Funds Key Features documents The information that follows is accurate to the best of our knowledge and belief as at 06 April

Self Invested Personal Pension for Wrap

Self Invested Personal Pension for Wrap Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is an independent financial services regulator.

Self Invested Personal Pension for Wrap Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is an independent financial services regulator.

Your guide to retirement savings. Start

Your guide to retirement savings Start What is the Zurich Retirement Saver (the plan)? 3 Can I rely on the State alone? 4 What are my alternatives? 4 How do I join? 5 What are the payments? 5 How regular

Your guide to retirement savings Start What is the Zurich Retirement Saver (the plan)? 3 Can I rely on the State alone? 4 What are my alternatives? 4 How do I join? 5 What are the payments? 5 How regular

Postgraduate Loan guide to terms and conditions

Postgraduate Loan guide to terms and conditions 2016/17 www.gov.uk/postgraduateloan /SF_England /SFEFILM Contents 1 What this guide s about 02 2 Your loan contract 02 3 Who does what 03 4 Your responsibilities

Postgraduate Loan guide to terms and conditions 2016/17 www.gov.uk/postgraduateloan /SF_England /SFEFILM Contents 1 What this guide s about 02 2 Your loan contract 02 3 Who does what 03 4 Your responsibilities

KEY FEATURES OF THE PENSION SAVER FOR GE EMPLOYEES.

KEY FEATURES OF THE PENSION SAVER FOR GE EMPLOYEES. This is an important document which you should keep in a safe place. Legal & General working in association with: 2 PENSION SAVER KEY FEATURES CONTENTS

KEY FEATURES OF THE PENSION SAVER FOR GE EMPLOYEES. This is an important document which you should keep in a safe place. Legal & General working in association with: 2 PENSION SAVER KEY FEATURES CONTENTS

KEY FEATURES OF THE ELI LILLY SELF INVESTED PENSION PLAN (LILLY SIPP).

.") KEY FEATURES OF THE ELI LILLY SELF INVESTED PENSION PLAN (LILLY SIPP). This is an important document which you should keep in a safe place. Legal & General working in Association with: 2 ELI LILLY SELF

KEY FEATURES OF THE ELI LILLY SELF INVESTED PENSION PLAN (LILLY SIPP). This is an important document which you should keep in a safe place. Legal & General working in Association with: 2 ELI LILLY SELF

KEY FEATURES OF THE INDIVIDUAL STAKEHOLDER PENSION PLAN

KEY FEATURES OF THE INDIVIDUAL STAKEHOLDER PENSION PLAN The Financial Conduct Authority is a financial services regulator. It requires us, Royal London, to give you this important information to help you

KEY FEATURES OF THE INDIVIDUAL STAKEHOLDER PENSION PLAN The Financial Conduct Authority is a financial services regulator. It requires us, Royal London, to give you this important information to help you