IDF FINANCIAL SERVICES. Affordable microfinance to the underprivileged

|

|

|

- Owen Rafe Hill

- 5 years ago

- Views:

Transcription

1 IDF FINANCIAL SERVICES Affordable microfinance to the underprivileged

2 IDF FSPL OPERATIONAL FROM IDF FINANCIAL SERVICES PVT.LTD. A Private Limited Company, incorporated under the Companies Act, 1956 as a limited liability company For profit entity Licensed by RBI to carry on financing activities Initially acquired by the Trustees of IDF

3 MISSION Financial Empowerment of the Economically underprivileged through good quality and sustainable financial services

4 VISION Reaching 20 lakh families by 2020

5 CORE VALUES 1. Commitment 2. Transparency 3. Innovation 4. Exceptional team work 5. Ethics in business

6 OBJECTIVES Build a banking model with a social face that is commercially viable for the poor These include Assist organizing the poor into Self Help Groups (SHGs) Build the capacity of Self Help Groups through Training & Non training interventions. Help organize the SHGs into clusters and Federations Facilitate Federations of SHGs to organize trainings related to Livelihood, Health & Community Development Assist SHG Federations mobilize thrift from the SHGs Assist SHG Federations to provide Credit plus services. Provide Credit to SHGs Build the capacity of SHG Federations towards participation in Governance of the Federations as well as in IDF FSPL in which the federations are the share holders.

7 STRATEGIC PARTNERS Indian Institute of Management Bangalore Sa-Dhan Association of Karnataka Micro Finance Institute(AKMI) Indus Knowledgeware Private Limited Microsave Intellcap EDA Rural System

8 idf HELPS FORMING GROUPS FUNCTIONAL, TECHNICAL & DEVELOPMENTAL ADVOCACY SUPPORT Equity SHG Feds Promoters + Staff Devpt Bankers Social Investors Loans Com Banks FIs Devpt Bankers Shareholders CAPITAL IDF FSPL NBFC, for profit DIVIDEND LOAN DIRECTLY TO SHGS SHG FED GIVE BACK PROFITS ON CAPITAL SHG FED SHG FED SHG FED SHG FED PROVIDE CAPITAL CONTRIBUTION CLUSTERS SHGs

9

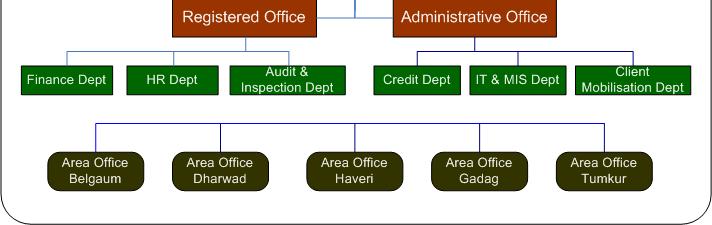

10 AREA OFFICE ORGANOGRAM Regional Manager Area Manager Credit Manager- 1 Credit Manager- 2 Credit Manager- 3 Credit Manager- 4 Credit Manager 5 Credit Manager 6 Credit officers (5) COs(5) Cluster (3-4) SHGs (8-20) Credit Officers(5) COs(5) Cluster (3-4) SHGs (8-20) Credit Officers(5) COs(5) Cluster (3-4) SHGs (8-20) Credit Officers(5) COs(5) Cluster (3-4) SHGs (8-20) Credit Officers(5) COs(5) Cluster (3-4) SHGs (8-20) Credit Officers(5) COs(5) Clusters (3-4) SHGs (8-20)

11 SHG FEDERATIONORGANOGRAM IDF SHG FEDERATION Board of Trustees Chair Person Vice Chair Person Elected Trustee Trustee (Finance) Trustee ( Operation) Advisory Committee CEO Clusters SHGs

12 SHAREHOLDERS As on 31 March 2010 Name of Shareholder No. of equity shares % of shareholding Subtotal % Acquirers 500, IDF SHG Federation Dharwad 274, IDF SHG Federation Haveri 125,480 8 IDF SHG Federation Tumkur 353, IDF SHG Federation Gadag 49,720 3 IDF SHG Federation Belgaum 243, Total 1,545,

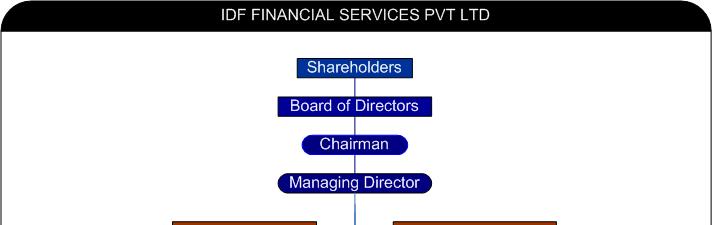

13 GOVERNANCE Board of Directors Salimath VN Patil N M Srikantha Shenoy TV Kulkarni G S Smt. Tajbi Nadaf - Chairman - Managing Director - Director -Director - Director

14 IDF SHG Federation IDF-SHG Federation Private for profit micro trusts Based on the principle of mutuality Owned by the SHG Members Managed by SHGs and closely monitored with technical & managerial help from other entities Registered in 5 locations Belgaum, Dharwad, Gadag, Haveri and Tunkur

15 IDF SHG FEDERATIONS

16 IDF SHG FEDERATIONS Governance All SHGthrough cluster leaders constitute the General Body. IDFto appoint the Chairman Trustee IDF/ IDFFSPL provide Financial and Operational Trustees Management Two trustees elected from Leaders and to be trained for future management, under the strict standards of management.

17 IDF SHG FEDERATIONS Collect capital contribution from SHGsto the extent of 10% of their borrowing and upload as capital into IDF FSPL. Savings will always be utilisedfor investment in approved investments IDFFSPLprovide emergency loans to the extent of SHG savings on recommendations of IDF SHG Federations Deal with their specific set of SHGsonly and will have no transactions with other Institutions or Federations or SHGs.

18 IDF SHG FEDERATIONS Since owned by member-shgs and receives the entire funds of SHGs in an accounts opened with it, the laws are not violated for public deposits / savings. Is managed by Trustees and the funds are in the hands of trust. Is capable of buying equity in IDF FSPL.

19 IDF SHG CLUSTERS-1 8 to 20 SHGs form a cluster, for the purposes of collection of loans repayments, savings and other cash transactions, including insurance premium and fee for health services etc. Two representatives of the SHGs assemble at the pre appointed date; time and place with the Cash collected at the SHG meetings and deliver the same. The venue of meeting of cluster is in a place where the radius of travel by the SHGrepresentatives would not exceed 15 Kmsapproximately.

20 IDF SHG CLUSTERS-2 The cluster is an informal congregation of SHGs to and for cash delivery to the MBT / Company. The cash is collected by the Credit Officers of IDFF and moved to the Branch office of IDFF and SHG FED office for further deposit into bank account. Recommend loan applications for its quantum, tenure and other terms etc for appraisal by the Credit Manager of IDF Financial services Private Limited.

21 IDF SHG CLUSTERS-3 Clusters attend to defaults at the SHG level and pursue for payment Attending the problems of SHG, strengthening member groups. Auxiliary support for group formation and motivation.

22 IDF SHGs - 1 SHGs are enrolled in to IDF SHG Federation through Inter Se agreements. Will have account with IDF SHG Federations to which they are affiliated and will financially deal with IDF SHG Federations only. Will be controlled through a common set of business rules and regulations of the IDF SHG Federations.

23 IDF SHGs -2 SHGare member of Clusters and send two representatives to it Being a General Body member of Federation will elect two trustees as per the Federation bye- laws Will conduct their financial business in cluster meeting in the presence of Federation officials All accounts are maintained by Federation, but outsourced to IDF FSPL Even the collection of the due are outsourced to IDF FSPL

24 COMMUNITY MOBILISATION PROCESS Months Area Survey and Potential assessment Seeding the concept of SHG 2-3 Formation of SHG Formation of Cluster Capacity Building through Training Savings with Federations Rating of SHG Credit Linkage

25 TRAININGS TO SHGS SHG Concept SHG Meetings/ Savings Leadership Book Keeping Bank / MFI Linkages Vision building

26 LENDING PROCESS PRE APPLICATION SHG FORMATION CAPACITY BUILDING ELIGIBILTY FOR LOAN REGISTRATION SHG ASSESSMENT SHG SUBMITS APPLICATION SHG Age > 4 months Internal lending commenced Repayment 100% SHG cluster recommends loan Credit Scoring Model: Out of 100 marks SHG scoring > 60 is eligible to get loans POST APPLICATION LOAN COMMITTEE SANCTIONS LOAN LOAN DISBURSEN\MENT THROUGH CHEQUE Loan sanctioned depending on appraisal MONTHLY RECOVERY FROM CREDIT OFFICER

27 LOAN PRODUCT -RETAIL Loan Terms Products I Cycle II Cycle III Cycle Max Loan Amount in Rs ,50,000 4,50,000 Repayment Period in months Rate of interest in %* Service Charge % upfront Penalty Rs for I visit Rs per II second visit In Bangalore ROI is 19%

28 LOAN PRODUCT BULK Loan Terms Max Loan Amount in Rs 25,00,000 Repayment Period in months Rate of interest in % 14 Service Charge in % of sanctioned amount Up front Overdue interest in % 2 2

29 LOAN PRODUCT- EMERGENCY LOAN

30 GEOGRAPHICAL SPREAD Dharwad, Haveri, Gadag, Belgaum, Koppal,Chitradurga Tumkur, and Bangalore urban districts. The RegedOffice at Bengaluru and Adm office at Dharwad. It will cover both Urban and Rural area at the ratio of 60:40

31 Districtwise SHGs and members as on 31 March 2010 District SHGs (Nos) Dharwad 3222 Bangalore 425 Belagam 3509 Haveri 1984 Gadag 710 Tumkur 3693 Chitradurga 1239 Koppal 102 Ballary 237 Davangere 83 Total Koppal; 1% Ballary; 2% Chitradurga; 8% Gadag; 5% Tumkur; 24% Haveri; 13% Davangere; 0% Dharwad; 21% Belagam; 23% Bangalore; 3%

32 Districtwise Loan Davanagere 1% Bellary 0% Gadag 3% Koppal 1% outstanding As on 31 March 2010 Bangalore 2% Chitradurga 7% Haveri 9% Belgaum 26% Tumkur 29% Dharwad 22%

33 Productwise Loan outstanding As on 31 March 2010 III Cycle 0.81% IV Cycle 0.06% II Cycle 62.01% NGO 0.64% I Cycle 36.21% Emergency 0.27%

34 Lakh Rs Am. Disbursed Am. Outstanding March 2008 March 2009 March 2010 March

35 Current Balance Sheet (1 of 2) Account FY FY FY FY ( Amt in Lakh Rs) Cash and Bank Current Account Short term Investments in market instruments Outstanding loan Portfolio Loan loss reserves Net loan outstanding portfolio (3-4) Other current assets Total current assets ( ) Long-term investments Gross fixed assets (at the beginning of FY+ additions - Deduction) Depreciation Net fixed asset (9-10) Total long-term assets (8+11) Total assets (7+12)

36 Current Balance Sheet (2 of 2) Liabilities FY FY FY FY Long term loan outstanding (commercial rate) Long term loan outstanding (concessional/ subsidized rate) Other long term liabilities (pl. specify) Total liabilities ( ) Equity Prior years retained earnings (losses) not Incl. cash donations Current years retained earnings Other capital accounts (16-17 of income statements) Total equity (18 to 23) Total Liabilities & equity (17+24) Average Portfolio Return on equity %

37 Portfolio related data as on 31 March Description Mar-07 Mar-08 Mar-09 Mar-10 Value of loans disbursed during period Number of loans disbursed during period Number of active borrowers (end of period) Avg. number of active borrowers Value of loan outstanding (end of period) Avg. outstanding balance of loans Value of payments in arrears (end of period) Value of outstanding balance of loans in arrears (end of period) Value of loans written off during period Avg. loans size Avg. loans term (months) to to to 36 Avg. number of loans officers during period Value of re-scheduled loans outstanding Value of re-financed loans outstanding Value of loan outstanding for which repayment is yet to begin

38 Ratios as on 31 March 2010 Actuals Projected FY FY FY FY FY FY FY FY FY Ratios in % Operating Cost Ratio Total Cost Ratio Operating Self Sufficiency Financial Self Sufficiency NA NA Yield on Portfolio Return on Assets % Return on Equity %

39 Ageing Analysis of Outstanding Loans as on 31 March 2010 Type of Loans Value of Loans (IV) as a % of Total Loan Out Standing Regular Loans % Less than 30 days past due % Between days past due % Between days past due % Between days past due % Between days past due % >365 days past due % Total %

40 Projected Balance Sheet Amount in Million Indian Rupees FY10/11 FY11/12 FY12/13 FY13/14 FY14/15 ASSETS * Cash in Bank and Near Cash ,1 6,2 Net Portfolio Outstanding 1, , , , ,803.5 Other current ass Net Fixed Assets Other LT assets TOTAL ASSETS 1, , , , ,833.2 LIABILITIES * Short-term Commercial Loans , , ,725.3 Other Current Liabilities Long-term Commercial Loans TOTAL LIABILITIES , , ,734.3 EQUITY * Shareholder equity , , ,815.6 Accumulated net surplus TOTAL EQUITY , , ,098.9 TOTAL LIABILITIES AND EQUITY 1, , , , ,833.2

41 Projected Income and Expenditure Statement Amount in Million Indian Rupees Income Statement FY10/11 FY11/12 FY12/13 FY13/14 FY14/15 Financial Income Financial Expense Net Financial Income Provision for loan losses Net Financial Margin Program Operating Exp Administrative Operating Exp Net Operating Income Net Non-Operating Income/(Exp) Net Income (before taxes) Amount of taxes paid Net income (after taxes)

Banking and Development : Observations in. Reforms Era

CMDR Monograph Series No. - 62 Banking and Development : Observations in Reforms Era Dr. Barik Prasanna Kumar Study Completed Under Dr. D. M. Nanjundappa Chair CENTRE FOR MULTI-DISCIPLINARY DEVELOPMENT

CMDR Monograph Series No. - 62 Banking and Development : Observations in Reforms Era Dr. Barik Prasanna Kumar Study Completed Under Dr. D. M. Nanjundappa Chair CENTRE FOR MULTI-DISCIPLINARY DEVELOPMENT

M2i s Experience in Microfinance

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]:

![Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]:](/thumbs/92/109840252.jpg "Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]:") Sector Bank Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]: Parameter A Premier Public Sector Bank As at 30 June 15[Q1]

Sector Bank Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]: Parameter A Premier Public Sector Bank As at 30 June 15[Q1]

ORIGIN AND PERFORMANCE OF MGNREGA IN INDIA A SPECIAL REFERENCE TO KARNATAKA

Pinnacle Research Journals 25 ORIGIN AND PERFORMANCE OF MGNREGA IN INDIA A SPECIAL REFERENCE TO KARNATAKA ABSTRACT T. P. SHASHIKUMAR* *Assistant Professor, Karnataka State Open University, Mukthagangothri,

Pinnacle Research Journals 25 ORIGIN AND PERFORMANCE OF MGNREGA IN INDIA A SPECIAL REFERENCE TO KARNATAKA ABSTRACT T. P. SHASHIKUMAR* *Assistant Professor, Karnataka State Open University, Mukthagangothri,

& Mohan Kumar. M.S [b]

![& Mohan Kumar. M.S [b]](/thumbs/86/94321625.jpg "& Mohan Kumar. M.S [b]") The Changing scenario of Micro Insurance in Karnataka with special reference to Yeshasvini Scheme by Safeer Pasha M [a] & Mohan Kumar. M.S [b] Abstract Human being is always prone risk which may be associated

The Changing scenario of Micro Insurance in Karnataka with special reference to Yeshasvini Scheme by Safeer Pasha M [a] & Mohan Kumar. M.S [b] Abstract Human being is always prone risk which may be associated

E- ISSN X ISSN MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD By A Ramanathan, Chief General Manager Micro Finance Innovations Department NABARD Mumbai What is

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD By A Ramanathan, Chief General Manager Micro Finance Innovations Department NABARD Mumbai What is

An Overview of Microfinance in AP

National Seminar on Women Empowerment through Microfinance and Small Enterprises (11 th &12 th November 2010) organized by Dept. of Commerce, Govt. College for Women, Begumpet, Hyderabad Presentation on

National Seminar on Women Empowerment through Microfinance and Small Enterprises (11 th &12 th November 2010) organized by Dept. of Commerce, Govt. College for Women, Begumpet, Hyderabad Presentation on

Draft ToR for Thematic study on Financial inclusion Interventions, Challenges and Lessons under NERLP

Draft ToR for Thematic study on Financial inclusion Interventions, Challenges and Lessons under NERLP 1. Background NERLP is a World Bank funded rural poverty reduction project of the Ministry of Development

Draft ToR for Thematic study on Financial inclusion Interventions, Challenges and Lessons under NERLP 1. Background NERLP is a World Bank funded rural poverty reduction project of the Ministry of Development

Chaitanya India Fin Credit Private Limited (CIFCPL) mfr4

mfr4") Chaitanya India Fin Credit Private Limited (CIFCPL) mfr4 Date Assigned October 1, 2013 Analytical Contacts: Mr. Yogesh Dixit Senior Director Phone: +91 22 3342 3037 Email: yogesh.dixit@crisil.com Mr.

Chaitanya India Fin Credit Private Limited (CIFCPL) mfr4 Date Assigned October 1, 2013 Analytical Contacts: Mr. Yogesh Dixit Senior Director Phone: +91 22 3342 3037 Email: yogesh.dixit@crisil.com Mr.

Chapter-VII Data Analysis and Interpretation

Chapter-VII Data Analysis and Interpretation 16 CHAPTER-VII DATA ANALYSIS AND INTERPRETATION In order to arrive at a logical and constructive analysis of micro financing by commercial banks in Rajasthan

Chapter-VII Data Analysis and Interpretation 16 CHAPTER-VII DATA ANALYSIS AND INTERPRETATION In order to arrive at a logical and constructive analysis of micro financing by commercial banks in Rajasthan

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE :: KADAPA. Circular No BC - CD Date:

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE :: KADAPA Circular No. 317 2011 - BC - CD Date: 31.12.2011 SHG - BANK LINKAGE PROGRAMME SANCTION OF CASH CREDIT LIMIT REVISED GUIDELINES Ref. Cir. No. 1) 145-2006-BC-CST,

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE :: KADAPA Circular No. 317 2011 - BC - CD Date: 31.12.2011 SHG - BANK LINKAGE PROGRAMME SANCTION OF CASH CREDIT LIMIT REVISED GUIDELINES Ref. Cir. No. 1) 145-2006-BC-CST,

Details of the loan products - 30 June 2012 Product Description Loan size* months for income to generation purposes.

Microfinance Methodology BFL primarily follows the SHG methodology, although it has Joint Liability Groups and individual loans too. As of 30 th June 2012, 62% of its loan portfolio was in SHGs, 11% in

Microfinance Methodology BFL primarily follows the SHG methodology, although it has Joint Liability Groups and individual loans too. As of 30 th June 2012, 62% of its loan portfolio was in SHGs, 11% in

GRAMEEN FINANCIAL SERVICES PVT. LTD. S CODE OF CONDUCT E-LEARNING MODULE

GRAMEEN FINANCIAL SERVICES PVT. LTD. S CODE OF CONDUCT E-LEARNING MODULE Meet Grameen Financial Services Pvt. Ltd. Grameen Financial Services Pvt. Ltd. (GFSL) is an Indian Non Banking Financial Company

GRAMEEN FINANCIAL SERVICES PVT. LTD. S CODE OF CONDUCT E-LEARNING MODULE Meet Grameen Financial Services Pvt. Ltd. Grameen Financial Services Pvt. Ltd. (GFSL) is an Indian Non Banking Financial Company

RBI/ /49 DNBS.(PD)CC.No. 347 / / July 1, 2013

CC.No. 347 / / July 1, 2013") RBI/2013-14/49 DNBS.(PD)CC.No. 347 /03.10.38/2013-14 July 1, 2013 To, All NBFCs(excluding RNBCs) Dear Sirs, Master Circular- Introduction of New Category of NBFCs - Non Banking Financial Company-Micro

RBI/2013-14/49 DNBS.(PD)CC.No. 347 /03.10.38/2013-14 July 1, 2013 To, All NBFCs(excluding RNBCs) Dear Sirs, Master Circular- Introduction of New Category of NBFCs - Non Banking Financial Company-Micro

GUIDELINES OF INDIA MICROFINANCE EQUITY FUND

GUIDELINES OF INDIA MICROFINANCE EQUITY FUND 1 CONTENTS 1. Objective - Page 3 2. Principal features - Page 3 3. Purpose - Page 3 4. Types of instruments - Page 3 5. Eligibility criteria - Page 4 6. Sanction

GUIDELINES OF INDIA MICROFINANCE EQUITY FUND 1 CONTENTS 1. Objective - Page 3 2. Principal features - Page 3 3. Purpose - Page 3 4. Types of instruments - Page 3 5. Eligibility criteria - Page 4 6. Sanction

Internal Audit of NBFCs

Internal Audit of NBFCs Introduction to NBFC Meaning of NBFC A company registered under the Companies Act, 2013 engaged in: the business of loans and advances, acquisition of shares/stocks/bonds/debentures/securities

Internal Audit of NBFCs Introduction to NBFC Meaning of NBFC A company registered under the Companies Act, 2013 engaged in: the business of loans and advances, acquisition of shares/stocks/bonds/debentures/securities

Building A Model Microfinance Institution: The Case of Sanghamithra Rural Financial Services 1

Building A Model Microfinance Institution: The Case of Sanghamithra Rural Financial Services 1 H.S. Shylendra 2 Institute of Rural Management Anand (IRMA) 1. MFI with a Difference The Sanghamithra Rural

Building A Model Microfinance Institution: The Case of Sanghamithra Rural Financial Services 1 H.S. Shylendra 2 Institute of Rural Management Anand (IRMA) 1. MFI with a Difference The Sanghamithra Rural

Asha for Education Fellowship Application Form

Asha for Education Fellowship Application Form SECTION I: Personal Contact Information Name : Sanju Kumar Address : H.No.144, 2 nd Cross, Behind Bus Stand C.I.B Colony, Gulbarga-585104 Karnataka State,

Asha for Education Fellowship Application Form SECTION I: Personal Contact Information Name : Sanju Kumar Address : H.No.144, 2 nd Cross, Behind Bus Stand C.I.B Colony, Gulbarga-585104 Karnataka State,

LIST OF TABLES Census wise Sex Ratio in India 100

LIST OF TABLES 1. 1.1 Progress of Microfinance as on 31 st March 2009. 05 2. 2.1 3. 2.2 Share of rural household debt by source of credit, All India, 1951-1991 Advances to Agriculture and Other Priority

LIST OF TABLES 1. 1.1 Progress of Microfinance as on 31 st March 2009. 05 2. 2.1 3. 2.2 Share of rural household debt by source of credit, All India, 1951-1991 Advances to Agriculture and Other Priority

Banking and Finance Indian Microfinance Sector: Entering a phase of moderate credit risk, three years post AP crisis

Indian Microfinance Sector: Entering a phase of moderate credit risk, three years post AP crisis March 7, 214 Summary Microfinance sector in India has gone through 3 broad risk phases in the past high

Indian Microfinance Sector: Entering a phase of moderate credit risk, three years post AP crisis March 7, 214 Summary Microfinance sector in India has gone through 3 broad risk phases in the past high

18th Year of Publication. A monthly publication from South Indian Bank.

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 18th Year of Publication Experience

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 18th Year of Publication Experience

SELF HELP GROUPS-BANK LINKAGE PROGRAMME : A RECURRENT STUDY IN ANDHRA PRADESH RESEARCH & ADVOCACY UNIT APMAS

SELF HELP GROUPS-BANK LINKAGE PROGRAMME : A RECURRENT STUDY IN ANDHRA PRADESH RESEARCH & ADVOCACY UNIT APMAS 1 BACKGROUND OF THE STUDY In 2003 APMAS conducted a study on SHG Bank Linkage More no. of SHGs

SELF HELP GROUPS-BANK LINKAGE PROGRAMME : A RECURRENT STUDY IN ANDHRA PRADESH RESEARCH & ADVOCACY UNIT APMAS 1 BACKGROUND OF THE STUDY In 2003 APMAS conducted a study on SHG Bank Linkage More no. of SHGs

BFIL s lowest interest rate benefits 55 lakh women in 1 lakh villages

BFIL UPDATE Sab se Sastha loan BFIL s lowest interest rate benefits 55 lakh women in 1 lakh villages MAR 2017 BHARAT FINANCIAL INCLUSION LIMITED (Formerly known as SKS Microfinance Limited ) BSE: 533228

BFIL UPDATE Sab se Sastha loan BFIL s lowest interest rate benefits 55 lakh women in 1 lakh villages MAR 2017 BHARAT FINANCIAL INCLUSION LIMITED (Formerly known as SKS Microfinance Limited ) BSE: 533228

Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012

Bill, 2012") Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012 The Bill was introduced in the Lok Sabha by the Minister of Finance on May 22, 2012. The Bill was referred to the

Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012 The Bill was introduced in the Lok Sabha by the Minister of Finance on May 22, 2012. The Bill was referred to the

Presentation Structure

Housing Finance in South Asia,,J Jakarta May 27-29, 29, 2009 Low Income Housing Finance R. V. Verma National Housing Bank India Presentation Structure I. General Economic Trends II. Trends in Housing Finance

Housing Finance in South Asia,,J Jakarta May 27-29, 29, 2009 Low Income Housing Finance R. V. Verma National Housing Bank India Presentation Structure I. General Economic Trends II. Trends in Housing Finance

Central Bank of Sudan Microfinance Unit

Central Bank of Sudan Microfinance Unit Role & Mission April 2007 Mutwakil Bakri Why Microfinance Matters? Poverty Map in Sudan: 76% Under Poverty Line,70% in Rural Deprived Areas Demand Gap:only 1-3%

Central Bank of Sudan Microfinance Unit Role & Mission April 2007 Mutwakil Bakri Why Microfinance Matters? Poverty Map in Sudan: 76% Under Poverty Line,70% in Rural Deprived Areas Demand Gap:only 1-3%

Financial Inclusion & Postal Banking The India Story

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

23 rd Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank

Experience Next Generation Banking To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank

SAMRUDHI Micro Fin Society (SMS) Brief Profile

Brief Profile") SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

Enabling Holistic Dignified Living. Fair Practice Code

Enabling Holistic Dignified Living Fair Practice Code Table of Contents 1. Mission... 2 2. Vision... 2 3. Policy Objective... 2 4. Client... 2 5. Policy... 2 5.1. General... 2 5.2. Applications for loans

Enabling Holistic Dignified Living Fair Practice Code Table of Contents 1. Mission... 2 2. Vision... 2 3. Policy Objective... 2 4. Client... 2 5. Policy... 2 5.1. General... 2 5.2. Applications for loans

State Bank of India

State Bank of India 24.01.2009 Disclaimer This presentation is made purely for information. We have tried to give relevant information which we believe will help in knowing the Bank. The viewers may use

State Bank of India 24.01.2009 Disclaimer This presentation is made purely for information. We have tried to give relevant information which we believe will help in knowing the Bank. The viewers may use

SAMRUDHI Micro Fin Society

SAMRUDHI Micro Fin Society Update & Renewal for Asha fellowship SAMRUDHI is a responsible civil society to work with the rural & urban poor women to reinforce their efforts to rise, remain, above the poverty

SAMRUDHI Micro Fin Society Update & Renewal for Asha fellowship SAMRUDHI is a responsible civil society to work with the rural & urban poor women to reinforce their efforts to rise, remain, above the poverty

Financial Inclusion: Meaning, Objective & Importance [Banking Awareness]

![Financial Inclusion: Meaning, Objective & Importance [Banking Awareness]](/thumbs/85/93030230.jpg "Financial Inclusion: Meaning, Objective & Importance [Banking Awareness]") Financial Inclusion: Meaning, Objective & Importance [Banking Awareness] Author : Oliveboard Date : July 14, 2017 Dear Aspirants, Financial Inclusion (FI) is a very important topic for Bank & Government

Financial Inclusion: Meaning, Objective & Importance [Banking Awareness] Author : Oliveboard Date : July 14, 2017 Dear Aspirants, Financial Inclusion (FI) is a very important topic for Bank & Government

A DESCRIPTIVE STUDY ON PRADHAN MANTHRI MUDRA YOJANA (PMMY)

") International Journal of Latest Trends in Engineering and Technology Special Issue SACAIM 2016, pp. 121-125 e-issn:2278-621x A DESCRIPTIVE STUDY ON PRADHAN MANTHRI MUDRA YOJANA (PMMY) Mahammad Shahid 1

International Journal of Latest Trends in Engineering and Technology Special Issue SACAIM 2016, pp. 121-125 e-issn:2278-621x A DESCRIPTIVE STUDY ON PRADHAN MANTHRI MUDRA YOJANA (PMMY) Mahammad Shahid 1

Equitas Holdings Limited Investor Presentation Q1FY19 Quarter ended 30 June 2018

Equitas Holdings Limited Investor Presentation Q1FY19 Quarter ended 30 June 2018 1 MISSION Empowering through Financial Inclusion VISION To Serve 5% of Indian Households by 2025 VALUES Fair and Transparent

Equitas Holdings Limited Investor Presentation Q1FY19 Quarter ended 30 June 2018 1 MISSION Empowering through Financial Inclusion VISION To Serve 5% of Indian Households by 2025 VALUES Fair and Transparent

27 th Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

1. Key development issues and rationale for Bank involvement

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized DRAFT PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB5278 Project Name

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized DRAFT PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB5278 Project Name

Regulation of Microfinance Institutions in India

Regulation of Microfinance Institutions in India Santadarshan Sadhu, Kenny Kline, Justin Oliver CMF-IFMR 20 th April 2011 Study Outline Microfinance sector - overview Analysis of the existing regulatory

Regulation of Microfinance Institutions in India Santadarshan Sadhu, Kenny Kline, Justin Oliver CMF-IFMR 20 th April 2011 Study Outline Microfinance sector - overview Analysis of the existing regulatory

IJEMR - May Vol.2 Issue 5 - Online - ISSN Print - ISSN

Role of Public Sector Banks in Microfinance - A Study of Public Sector Banks in the Southern Region of India * Dr. Sujatha Susanna Kumari. D Asst. Professor, Dept. of Commerce, School of Business Studies,

Role of Public Sector Banks in Microfinance - A Study of Public Sector Banks in the Southern Region of India * Dr. Sujatha Susanna Kumari. D Asst. Professor, Dept. of Commerce, School of Business Studies,

CHAPTER II THE KARNATAKA STATE CO-OPERATIVE AGRICULTURE AND RURAL DEVELOPMENT BANK LTD

CHAPTER II THE KARNATAKA STATE CO-OPERATIVE AGRICULTURE AND RURAL DEVELOPMENT BANK LTD INTRODUCTION In the year 1929 on 25 th November the Mysore State Co-operative Land Mortgage Bank was established in

CHAPTER II THE KARNATAKA STATE CO-OPERATIVE AGRICULTURE AND RURAL DEVELOPMENT BANK LTD INTRODUCTION In the year 1929 on 25 th November the Mysore State Co-operative Land Mortgage Bank was established in

Good and Bad Practices in Micro insurance

Good and Bad Practices in Micro insurance Munich October 19 th James Roth and Vijay Athreye Categories Life and General (Non Life). Before 2001 - Public monopoly 1Life Corporation and 4 General Corporations

Good and Bad Practices in Micro insurance Munich October 19 th James Roth and Vijay Athreye Categories Life and General (Non Life). Before 2001 - Public monopoly 1Life Corporation and 4 General Corporations

Microfinance in India: What do we know?

Presentation at ICRIER s Financial Sector Seminar 5th February 2008, 12.30pm Microfinance in India: What do we know? by Mathew Titus, Executive Director Sa-Dhan Presentation Outline 1 Microfinance Sector

Presentation at ICRIER s Financial Sector Seminar 5th February 2008, 12.30pm Microfinance in India: What do we know? by Mathew Titus, Executive Director Sa-Dhan Presentation Outline 1 Microfinance Sector

Financial Performance For the Quarter/ Nine Months Ended 31ST DEC. 2017

Financial Performance For the Quarter/ Nine Months Ended 31ST DEC. 2017 12th FEBRUARY 2018 1 Corporation Bank was founded in the Year 1906 in Udupi a small town in South India Nationalized in the year

Financial Performance For the Quarter/ Nine Months Ended 31ST DEC. 2017 12th FEBRUARY 2018 1 Corporation Bank was founded in the Year 1906 in Udupi a small town in South India Nationalized in the year

Annual Results FY 08. May 02, 2008

Annual Results May 02, 2008 1 BUSINESS HIGHLIGHTS SBI Group net profit crosses USD 2.24 Billion (Rs 8,960 crore) SBI Stand-alone Net Profit crosses Rs 6,700 crore Net Profit for at Rs 6,729 crore, up by

Annual Results May 02, 2008 1 BUSINESS HIGHLIGHTS SBI Group net profit crosses USD 2.24 Billion (Rs 8,960 crore) SBI Stand-alone Net Profit crosses Rs 6,700 crore Net Profit for at Rs 6,729 crore, up by

Content. Highlights. Financial Performance. Business Performance. Treasury Operations. Asset Quality. Capital. Digital Banking & Financial Inclusion

Q2 FY 2019 Content Highlights Financial Performance Business Performance Treasury Operations Asset Quality Capital Digital Banking & Financial Inclusion 2 Highlights 3 Highlights for Quarter September

Q2 FY 2019 Content Highlights Financial Performance Business Performance Treasury Operations Asset Quality Capital Digital Banking & Financial Inclusion 2 Highlights 3 Highlights for Quarter September

Case Study - Strategy to enable Green Micro-finance

Case Study - Strategy to enable Green Micro-finance Shakti Sustainable Energy Foundation (SSEF) is a not for profit organization committed to support India s developmental and energy security objectives.

Case Study - Strategy to enable Green Micro-finance Shakti Sustainable Energy Foundation (SSEF) is a not for profit organization committed to support India s developmental and energy security objectives.

BSE: NSE: SATIN CSE: Corporate Identity No. L65991DL1990PLC Familiarization Programme for Independent Directors

BSE: 539404 NSE: SATIN CSE: 30024 Corporate Identity No. L65991DL1990PLC041796 Familiarization Programme for Independent Directors Microfinance Through Window of Relevance Micro-finance is defined as financial

BSE: 539404 NSE: SATIN CSE: 30024 Corporate Identity No. L65991DL1990PLC041796 Familiarization Programme for Independent Directors Microfinance Through Window of Relevance Micro-finance is defined as financial

BWDA 1 to BFL 2 : Transformation of an NGO into an MFI. D.Yeswanth Institute of Rural Management Anand(IRMA) Abstract

Abstract") BWDA 1 to BFL 2 : Transformation of an NGO into an MFI D.Yeswanth Institute of Rural Management Anand(IRMA) Abstract Poverty is multi-dimensional in its nature. By providing access to financial services,

BWDA 1 to BFL 2 : Transformation of an NGO into an MFI D.Yeswanth Institute of Rural Management Anand(IRMA) Abstract Poverty is multi-dimensional in its nature. By providing access to financial services,

International Journal of Advancements in Research & Technology, Volume 3, Issue 1, January ISSN

International Journal of Advancements in Research & Technology, Volume 3, Issue, January-24 95 BANK PERFORMANCE TO HELP THE DEVELOPMENT OF SELF HELP GROUPS (SHGs) Dr. G.Kotreshwar M.Com., Ph.D., Guide,

International Journal of Advancements in Research & Technology, Volume 3, Issue, January-24 95 BANK PERFORMANCE TO HELP THE DEVELOPMENT OF SELF HELP GROUPS (SHGs) Dr. G.Kotreshwar M.Com., Ph.D., Guide,

GOVERNMENT OF KARNATAKA FINANCE DEPARTMENT CIRCULAR

GOVERNMENT OF KARNATAKA FINANCE DEPARTMENT No. FD 07 BPE 2018 Karnataka Government Secretariat Vidhana Soudha Bangalore, Dated:19-11-2018 CIRCULAR Subject: Budget 2019-20 General Guidelines and Preparation

GOVERNMENT OF KARNATAKA FINANCE DEPARTMENT No. FD 07 BPE 2018 Karnataka Government Secretariat Vidhana Soudha Bangalore, Dated:19-11-2018 CIRCULAR Subject: Budget 2019-20 General Guidelines and Preparation

FY First Quarter Results. Investor Presentation

FY 2009-10 First Quarter Results Investor Presentation 1 Performance Highlights Q1FY10 Net Profit Net Interest Income Fee Income Operating Revenue Operating Profit 70% YOY 29% YOY 17% YOY 40% YOY 47% YOY

FY 2009-10 First Quarter Results Investor Presentation 1 Performance Highlights Q1FY10 Net Profit Net Interest Income Fee Income Operating Revenue Operating Profit 70% YOY 29% YOY 17% YOY 40% YOY 47% YOY

Profile of the NBFC Sector based on RBI s study

Profile of the NBFC Sector based on RBI s study Madan Sabnavis Chief Economist madan.sabnavis@careratings.com 91-22-6754 3638 Author: Sushant Hede Associate Economist sushant.hede@careratings.com 91-22-6754

Profile of the NBFC Sector based on RBI s study Madan Sabnavis Chief Economist madan.sabnavis@careratings.com 91-22-6754 3638 Author: Sushant Hede Associate Economist sushant.hede@careratings.com 91-22-6754

Impact of Deprived Sector Credit Policy on Micro Financing Presented by Nepal Rastra Bank

Impact of Deprived Sector Credit Policy on Micro Financing Presented by Nepal Rastra Bank Introduction: The deprived sector credit policy is directed credit policy of Nepal Rastra Bank, which is designed

Impact of Deprived Sector Credit Policy on Micro Financing Presented by Nepal Rastra Bank Introduction: The deprived sector credit policy is directed credit policy of Nepal Rastra Bank, which is designed

Madura Micro Finance Limited

Madura Micro Finance Limited August 20, 2018 Summary of rated instruments Instrument* Previous Rated Amount Subordinated 50.00 50.00 - Loans from Banks 300.00 300.00 Non-convertible 36.60 36.60 Non-convertible

Madura Micro Finance Limited August 20, 2018 Summary of rated instruments Instrument* Previous Rated Amount Subordinated 50.00 50.00 - Loans from Banks 300.00 300.00 Non-convertible 36.60 36.60 Non-convertible

NABARD & microfinance

NABARD & microfinance 2001-2002 Ten years of SHG-Bank Linkage (1992-2002) Self Help Groups An SHG is a group of about 20 people from a homogeneous class, who come together for addressing their common problems.

NABARD & microfinance 2001-2002 Ten years of SHG-Bank Linkage (1992-2002) Self Help Groups An SHG is a group of about 20 people from a homogeneous class, who come together for addressing their common problems.

Sustainable Financial Services for a Developing Rural Economy: Establishing Needs and Prospects for Growth through Microfinance Institutions (MFIs)

") Kamla-Raj 2014 J Economics, 5(2): 231-237 (2014) Sustainable Financial Services for a Developing Rural Economy: Establishing Needs and Prospects for Growth through Microfinance Institutions (MFIs) K.C.

Kamla-Raj 2014 J Economics, 5(2): 231-237 (2014) Sustainable Financial Services for a Developing Rural Economy: Establishing Needs and Prospects for Growth through Microfinance Institutions (MFIs) K.C.

Segment -1 (Background)

") National Rural Livelihood Mission (NRLM): Segment -1 (Background) National Rural Livelihood Mission (NRLM) was launched by Ministry of Rural Development, GoI by restructuring Swaranjayanti Gram Swarozgar

National Rural Livelihood Mission (NRLM): Segment -1 (Background) National Rural Livelihood Mission (NRLM) was launched by Ministry of Rural Development, GoI by restructuring Swaranjayanti Gram Swarozgar

Microfinance Contribution towards the Savings & Borrowings of the Poor in India

29 Microfinance Contribution towards the Savings & Borrowings of the Poor in India Smrita Jain 1, Dr. Deepti Gupta 2 1 Assistant Professor, Department of Management, MIT, Moradabad 2 Director, SSIM, Moradabad

29 Microfinance Contribution towards the Savings & Borrowings of the Poor in India Smrita Jain 1, Dr. Deepti Gupta 2 1 Assistant Professor, Department of Management, MIT, Moradabad 2 Director, SSIM, Moradabad

State Bank of India Q2FY09 RESULTS ANALYSTS MEET

State Bank of India Q2FY09 RESULTS ANALYSTS MEET 27.10.2008 Operating and Net Profit 4193 Q2FY08 Q2FY09 Rs. In Crs 2714 28.43% 54.52% 1611 36.04% 2260 40.23% Operating Profit Net Profit 1 34454 Deposit

State Bank of India Q2FY09 RESULTS ANALYSTS MEET 27.10.2008 Operating and Net Profit 4193 Q2FY08 Q2FY09 Rs. In Crs 2714 28.43% 54.52% 1611 36.04% 2260 40.23% Operating Profit Net Profit 1 34454 Deposit

ROLE OF MICROFINANCE IN THE ECONOMIC GROWTH OF INDIA: STATUS AND CHALLENGES

ROLE OF MICROFINANCE IN THE ECONOMIC GROWTH OF INDIA: STATUS AND CHALLENGES **SHRUTI GUPTA & SOMA NAYAK Introduction According to CGAP, Microfinance is the provision of financial services to low-income

ROLE OF MICROFINANCE IN THE ECONOMIC GROWTH OF INDIA: STATUS AND CHALLENGES **SHRUTI GUPTA & SOMA NAYAK Introduction According to CGAP, Microfinance is the provision of financial services to low-income

Indiabulls Housing Finance Limited Unaudited Financial Results Q3 FY January 22, 2014

Indiabulls Housing Finance Limited Unaudited Financial Results Q3 FY 2013-14 January 22, 2014 Safe Harbour Statement This document contains certain forward-looking statements based on current expectations

Indiabulls Housing Finance Limited Unaudited Financial Results Q3 FY 2013-14 January 22, 2014 Safe Harbour Statement This document contains certain forward-looking statements based on current expectations

A Case Study: Micro Financial Institutions (MFI) - Loan Maintenance

- Loan Maintenance") A Case Study: Micro Financial Institutions (MFI) - Loan Maintenance Introduction Small time farmers find it very challenging to access loans for their farming activities. Though many financial institutions

A Case Study: Micro Financial Institutions (MFI) - Loan Maintenance Introduction Small time farmers find it very challenging to access loans for their farming activities. Though many financial institutions

A STUDY ON PROGRESS OF MICRO FINANCE INSTITUTIONS BANK LINKAGE PROGRAM IN INDIA *Dr. Krishna Banana, Research Supervisor, Dept.

A STUDY ON PROGRESS OF MICRO FINANCE INSTITUTIONS BANK LINKAGE PROGRAM IN INDIA *Dr. Krishna Banana, Research Supervisor, Dept. of Commerce & Business Administration Acharya Nagarjuna University Ongole

A STUDY ON PROGRESS OF MICRO FINANCE INSTITUTIONS BANK LINKAGE PROGRAM IN INDIA *Dr. Krishna Banana, Research Supervisor, Dept. of Commerce & Business Administration Acharya Nagarjuna University Ongole

M-CRIL Analytics 2009

M-CRIL Analytics 2009 A Celebration and a Lament Contents Introduction A celebration and a lament 1 1 The M-CRIL sample 4 2 Outreach 5 3 Portfolio growth and loan size 7 4 Operating efficiency and staff

M-CRIL Analytics 2009 A Celebration and a Lament Contents Introduction A celebration and a lament 1 1 The M-CRIL sample 4 2 Outreach 5 3 Portfolio growth and loan size 7 4 Operating efficiency and staff

Dairying as Livelihood Activity among SHGs - An overview. Dr. K. Natchimuthu RAGACOVAS, Puducherry.

Dairying as Livelihood Activity among SHGs - An overview Dr. K. Natchimuthu RAGACOVAS, Puducherry. Introduction Organised but unregistered groups involved primarily in savings and credit. Neighbourhood

Dairying as Livelihood Activity among SHGs - An overview Dr. K. Natchimuthu RAGACOVAS, Puducherry. Introduction Organised but unregistered groups involved primarily in savings and credit. Neighbourhood

Performance Analysis of Commercial Banks Providing Microfinance in Rural Areas of Maharashtra

Performance Analysis of Commercial Banks Providing Microfinance in Rural Areas of Maharashtra Ms. Mrinal Savyanavar, Dr. Pankaj Trivedi Assistant Professor, Bharati Vidyapeeth's Institute of Management

Performance Analysis of Commercial Banks Providing Microfinance in Rural Areas of Maharashtra Ms. Mrinal Savyanavar, Dr. Pankaj Trivedi Assistant Professor, Bharati Vidyapeeth's Institute of Management

2018/SMEWG/DIA/008 National Financial Inclusion Strategy

2018/SMEWG/DIA/008 National Financial Inclusion Strategy 2016-2020 Submitted by: Centre for Excellence in Financial Inclusion Policy Dialogue on Micro, Small and Medium Enterprises Internationalization

2018/SMEWG/DIA/008 National Financial Inclusion Strategy 2016-2020 Submitted by: Centre for Excellence in Financial Inclusion Policy Dialogue on Micro, Small and Medium Enterprises Internationalization

Draft Concept Note on the Social Audit Mechanism to be followed in Karnataka.

Draft Concept Note on the Social Audit Mechanism to be followed in Karnataka. (This note will be shared with the SIRD for further actions. The role of SIRD includes the following. (1) To prepare a job

Draft Concept Note on the Social Audit Mechanism to be followed in Karnataka. (This note will be shared with the SIRD for further actions. The role of SIRD includes the following. (1) To prepare a job

Dimensions rated Governance & strategy b b b+ Organization & Management systems. Financial performance b b b. Visit: August 2012

Below Investment Grade Above Gramalaya Urban and Rural Development Initiatives and Network () - Section 25 Company {second update} Trichy, Tamil Nadu, India October 2012 Microfinance Institutional Rating

Below Investment Grade Above Gramalaya Urban and Rural Development Initiatives and Network () - Section 25 Company {second update} Trichy, Tamil Nadu, India October 2012 Microfinance Institutional Rating

Board Presentation Quarter / Year ended 31 st March TH APRIL 2016

Board Presentation Quarter / Year ended 31 st March 2016 19 TH APRIL 2016 1 SUMMARY FINANCIAL STATEMENT Amounts In Rs. Lakhs Financial Snapshot * Figures are annualized Quarter Ended Q-o-Q Year Ended

Board Presentation Quarter / Year ended 31 st March 2016 19 TH APRIL 2016 1 SUMMARY FINANCIAL STATEMENT Amounts In Rs. Lakhs Financial Snapshot * Figures are annualized Quarter Ended Q-o-Q Year Ended

Role of Financial Institutions in Promoting Microfinance through SHG Bank Linkage Programme in India

Volume 10 Issue 4, October 2017 Role of Financial Institutions in Promoting Microfinance through Bank Linkage Programme in India Dr. Manpreet Arora Assistant Professor Department of Accounting and Finance

Volume 10 Issue 4, October 2017 Role of Financial Institutions in Promoting Microfinance through Bank Linkage Programme in India Dr. Manpreet Arora Assistant Professor Department of Accounting and Finance

Financial Inclusion after PMJDY: A Case Study of Gubbi Taluk, Tumkur

WORKING PAPER, NO: 568 Financial Inclusion after PMJDY: A Case Study of Gubbi Taluk, Tumkur Charan Singh Economics and Social Science Indian Institute of Management Bangalore Bannerghatta Road, Bangalore-560076

WORKING PAPER, NO: 568 Financial Inclusion after PMJDY: A Case Study of Gubbi Taluk, Tumkur Charan Singh Economics and Social Science Indian Institute of Management Bangalore Bannerghatta Road, Bangalore-560076

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble MBA - I, Finance What is Microfinance? Microfinance is the supply of loans, savings, and other basic financial services to the

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble MBA - I, Finance What is Microfinance? Microfinance is the supply of loans, savings, and other basic financial services to the

Adhikar Agora Annapurna Arohan Asirvad Belstar. BSS Chaitanya Fusion Grameen Koota Growing. Madura Margdarshak Midland MSM Muthoot Microfin

Adhikar Agora Annapurna Arohan Asirvad Belstar BFIL BSS Chaitanya Fusion Grameen Koota Growing Opportunity Hindusthan Fino Jagaran Light M Power Madura Margdarshak Midland MSM Muthoot Microfin Namra Navachetna

Adhikar Agora Annapurna Arohan Asirvad Belstar BFIL BSS Chaitanya Fusion Grameen Koota Growing Opportunity Hindusthan Fino Jagaran Light M Power Madura Margdarshak Midland MSM Muthoot Microfin Namra Navachetna

Investor Presentation

Make Life Easy MANAPPURAM FINANCE LIMITED Investor Presentation For the Quarter ended September 30, 2013 Result Highlights for Q2 FY14 Net profit up 32% q-q to Rs 697.2 Mn Interim dividend of Rs 0.45 per

Make Life Easy MANAPPURAM FINANCE LIMITED Investor Presentation For the Quarter ended September 30, 2013 Result Highlights for Q2 FY14 Net profit up 32% q-q to Rs 697.2 Mn Interim dividend of Rs 0.45 per

Client Protection Assessment Report

Client Protection Assessment Report Annapurna Microfinance Private Limited January / February - 2011 Conducted by: ACCESS ASSIST 28A Hauz Khas Village, First Floor, New Delhi, 110 016 www.accessdev.org

Client Protection Assessment Report Annapurna Microfinance Private Limited January / February - 2011 Conducted by: ACCESS ASSIST 28A Hauz Khas Village, First Floor, New Delhi, 110 016 www.accessdev.org

Indiabulls Housing Finance Limited Unaudited Financial Results Q1 FY July 18, 2013

Indiabulls Housing Finance Limited Unaudited Financial Results Q1 FY 2013-14 July 18, 2013 Safe Harbour Statement This document contains certain forward-looking statements based on current expectations

Indiabulls Housing Finance Limited Unaudited Financial Results Q1 FY 2013-14 July 18, 2013 Safe Harbour Statement This document contains certain forward-looking statements based on current expectations

CHAPTER 4 IMPACT OF PROMOTIONAL ACTIVITIES ON BANKS DEPOSITS

CHAPTER 4 IMPACT OF PROMOTIONAL ACTIVITIES ON BANKS DEPOSITS One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major

CHAPTER 4 IMPACT OF PROMOTIONAL ACTIVITIES ON BANKS DEPOSITS One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major

PROPOSALS FOR REGULATIONS

PROPOSALS FOR REGULATIONS Tier 4 Microfinance Institutions and Money Lenders Act (2016) Shared with Department of Microfinance MoFPED March 2017 PROPOSALS FOR REGULATIONS Tier 4 Microfinance Institutions

PROPOSALS FOR REGULATIONS Tier 4 Microfinance Institutions and Money Lenders Act (2016) Shared with Department of Microfinance MoFPED March 2017 PROPOSALS FOR REGULATIONS Tier 4 Microfinance Institutions

Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029) Audited Financial Results FY April 23, 2014

Audited Financial Results FY April 23, 2014") Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029) Audited Financial Results FY 2013-14 April 23, 2014 Safe Harbour Statement This document contains certain forward-looking statements based

Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029) Audited Financial Results FY 2013-14 April 23, 2014 Safe Harbour Statement This document contains certain forward-looking statements based

ON THE WEBSITE OUTSOURCING OF CONCURRENT AUDIT FUNCTIONS Notification No. Kvgb/INSP/ 01/ Dated 17/03/2017

APPLICATION TO BE SUBMITTED TO: THE GENERAL MANAGER, INSPECTION DIVISION, KARNATAKA VIKAS GRAMEENA BANK, HEAD OFFICE, BELGAUM ROAD, NEAR NEW BUS STAND, DHARWAD - 580008 ON THE WEBSITE OUTSOURCING OF CONCURRENT

APPLICATION TO BE SUBMITTED TO: THE GENERAL MANAGER, INSPECTION DIVISION, KARNATAKA VIKAS GRAMEENA BANK, HEAD OFFICE, BELGAUM ROAD, NEAR NEW BUS STAND, DHARWAD - 580008 ON THE WEBSITE OUTSOURCING OF CONCURRENT

Transaction Costs in Group Microcredit in India

Transaction Costs in Group Microcredit in India Savita Shankar Institute for Financial Management and Research, Chennai. India Email: savita@ifmr.ac.in Transaction Costs in Group Microcredit in India Existing

Transaction Costs in Group Microcredit in India Savita Shankar Institute for Financial Management and Research, Chennai. India Email: savita@ifmr.ac.in Transaction Costs in Group Microcredit in India Existing

RURAL ENTERPRISE DEVELOPMENT SECTOR

RURAL ENTERPRISE DEVELOPMENT SECTOR Final Documentation Report People Women Empowerment Program Report Generated by: Monitoring Evaluation & Research Section Rural Credit Enterprise Development Sector

RURAL ENTERPRISE DEVELOPMENT SECTOR Final Documentation Report People Women Empowerment Program Report Generated by: Monitoring Evaluation & Research Section Rural Credit Enterprise Development Sector

Aarhat Multidisciplinary International Education Research Journal (AMIERJ) ISSN

ISSN") Page18 MICRO-FINANCE IN INDIA PROGRESS OF SHG-BANK LINKAGE PROGRAMME RAVINDER KUMAR Deptt. Of Commerce Kurukshetra University Kurukshetra RITIKA Deptt. Of Commerce Kurukshetra University Kurukshetra Abstract

Page18 MICRO-FINANCE IN INDIA PROGRESS OF SHG-BANK LINKAGE PROGRAMME RAVINDER KUMAR Deptt. Of Commerce Kurukshetra University Kurukshetra RITIKA Deptt. Of Commerce Kurukshetra University Kurukshetra Abstract

Financial Inclusion Through Self Help Groups for Rural Livelihoods An Analysis

Financial Inclusion Through Self Help Groups for Rural Livelihoods An Analysis K.Somasekhar Department of Rural Development, Acharya Nagarjuna University, Guntur - 522 510, Andhra Pradesh, India ABSTRACT

Financial Inclusion Through Self Help Groups for Rural Livelihoods An Analysis K.Somasekhar Department of Rural Development, Acharya Nagarjuna University, Guntur - 522 510, Andhra Pradesh, India ABSTRACT

CHAPTER 7 MAJOR FINDINGS

Major findings CHAPTER 7 MAJOR FINDINGS Micro-finance is an essential tool for: Creating social capital and advancing human development Clearly supporting the poor, especially the women However it seems

Major findings CHAPTER 7 MAJOR FINDINGS Micro-finance is an essential tool for: Creating social capital and advancing human development Clearly supporting the poor, especially the women However it seems

Uninterrupted dividend payment track record since inception Declared Dividend of 190% Bank has crossed total Business of Rs.

Corporation Bank was incorporated in the Year 1906 in Udupi a small town in South India Nationalized in the year 1980 and went public in 1998 The Bank holds a unique record of posting profits right from

Corporation Bank was incorporated in the Year 1906 in Udupi a small town in South India Nationalized in the year 1980 and went public in 1998 The Bank holds a unique record of posting profits right from

Microfinance in Haryana: Evaluation of Self Help Group-Bank Linkage Programme of NABARD in Haryana

Microfinance in Haryana: Evaluation of Self Help Group-Bank Linkage Programme of NABARD in Haryana Sachin 1 and Sameesh Khunger 2 1,2 (Assistant Professor, Department of Business Administration, Chaudhary

Microfinance in Haryana: Evaluation of Self Help Group-Bank Linkage Programme of NABARD in Haryana Sachin 1 and Sameesh Khunger 2 1,2 (Assistant Professor, Department of Business Administration, Chaudhary

Kudumbashree Accounts & Audit Service Society

Kudumbashree Accounts & Audit Service Society Kudumbashree- State Poverty Eradication Mission, Govt of Kerala was launched in 1998. It has now 258336 NHGs (Neighbourhood groups synonymous with SHGs), 19311

Kudumbashree Accounts & Audit Service Society Kudumbashree- State Poverty Eradication Mission, Govt of Kerala was launched in 1998. It has now 258336 NHGs (Neighbourhood groups synonymous with SHGs), 19311

Management Information System (MIS): MIS Major Outcome Linkage Loan above equal or above 8lakhs Scope of the Study

: MIS Major Outcome Linkage Loan above equal or above 8lakhs Scope of the Study") Microfinance & MIS I. Micro Finance: Microfinance simply means the provision of thrift, credit and other financial services and products of very small amounts to the poor in rural, semi urban or urban

Microfinance & MIS I. Micro Finance: Microfinance simply means the provision of thrift, credit and other financial services and products of very small amounts to the poor in rural, semi urban or urban

Financial Inclusion and Employment Generation of Rural Women Empowerment Thorough Self Help Groups- A Case Study Of Satna District

Financial Inclusion and Employment Generation of Rural Women Empowerment Thorough Self Help Groups- A Case Study Of Satna District Ritwik Sahai Bisariya Introduction Financial inclusion is the delivery

Financial Inclusion and Employment Generation of Rural Women Empowerment Thorough Self Help Groups- A Case Study Of Satna District Ritwik Sahai Bisariya Introduction Financial inclusion is the delivery

CHAPTER 2 CONCEPTUAL FRAMEWORK

CHAPTER 2 CONCEPTUAL FRAMEWORK 2.1 Introduction Prahalad C. K. (2006) in his famous book Fortune at the bottom of the pyramid illustrated the assumption behind the dominant logic of commercial organizations.

CHAPTER 2 CONCEPTUAL FRAMEWORK 2.1 Introduction Prahalad C. K. (2006) in his famous book Fortune at the bottom of the pyramid illustrated the assumption behind the dominant logic of commercial organizations.

Cost of social banking

Cost of social banking The traditional self-centered, profit-oriented banking concept is fading, and a modern socio-economic role is emerging for the. The social control imposed over for the first time

Cost of social banking The traditional self-centered, profit-oriented banking concept is fading, and a modern socio-economic role is emerging for the. The social control imposed over for the first time

Rating Rationale Western India Transport Finance Company Pvt. Ltd. (WITFIN) Ratings

Ratings") Rating Rationale Western India Transport Finance Company Pvt. Ltd. (WITFIN) Ratings Instrument Amount (Rs. crore) Long Term Bank Facilities 35.00 (Rupees Thirty Five crore only) Rating 1 CARE BBB- (Triple

Rating Rationale Western India Transport Finance Company Pvt. Ltd. (WITFIN) Ratings Instrument Amount (Rs. crore) Long Term Bank Facilities 35.00 (Rupees Thirty Five crore only) Rating 1 CARE BBB- (Triple

Evaluation of SHG-Bank Linkage: A Case Study of Rural Andhra Pradesh Women

EUROPEAN ACADEMIC RESEARCH Vol. II, Issue 8/ November 2014 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.1 (UIF) DRJI Value: 5.9 (B+) Evaluation of SHG-Bank Linkage: A Case Study of Rural Andhra Pradesh

EUROPEAN ACADEMIC RESEARCH Vol. II, Issue 8/ November 2014 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.1 (UIF) DRJI Value: 5.9 (B+) Evaluation of SHG-Bank Linkage: A Case Study of Rural Andhra Pradesh

Micro Finance in the World and in India: Status, Problems and Prospects

Micro Finance in the World and in India: Status, Problems and Prospects By Vijay Mahajan Chair, CGAP ExCom Founder and CEO, BASIX Social Enterprise Group, India President, MFIN (MFI Network of India) March

Micro Finance in the World and in India: Status, Problems and Prospects By Vijay Mahajan Chair, CGAP ExCom Founder and CEO, BASIX Social Enterprise Group, India President, MFIN (MFI Network of India) March

SHG-Bank Linkage Programme: A Study on Loan Default and Recovery

National Seminar on Micro Finance Sector in India Issues & Challenges (10 th September 2011) Organized by Gitam School of International Business Gitam University, Visakhapatnam Presentation on SHG-Bank

National Seminar on Micro Finance Sector in India Issues & Challenges (10 th September 2011) Organized by Gitam School of International Business Gitam University, Visakhapatnam Presentation on SHG-Bank

Welcome to Analysts Meet

PERFORMANCE HIGHLIGHTS For the Quarter Ended 30 th JUNE, 2013 Welcome to Analysts Meet 31 st July- 2013 Mumbai INDEX Sl. No. Slide Details Slide No. 1 Financial Highlights 4 2 Earnings Cross Section 5

PERFORMANCE HIGHLIGHTS For the Quarter Ended 30 th JUNE, 2013 Welcome to Analysts Meet 31 st July- 2013 Mumbai INDEX Sl. No. Slide Details Slide No. 1 Financial Highlights 4 2 Earnings Cross Section 5

ACQUISITION OF OUR BANK BY STATE BANK OF INDIA

Reg. No. MAG(3)/NPP/391/2015-2016 JUNE - 2016 ISSUE-02 ACQUISITION OF OUR BANK BY STATE BANK OF INDIA Most of employees of our Bank, State Bank of Mysore, past and present were saying 'we have heard rumours

Reg. No. MAG(3)/NPP/391/2015-2016 JUNE - 2016 ISSUE-02 ACQUISITION OF OUR BANK BY STATE BANK OF INDIA Most of employees of our Bank, State Bank of Mysore, past and present were saying 'we have heard rumours