Mortgage Lender Sentiment Survey

|

|

|

- Shonda McCoy

- 5 years ago

- Views:

Transcription

1 Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations 2015 Published: March 18, Fannie Mae. Trademarks of Fannie Mae Fannie Mae. Trademarks of Fannie Mae. 1

2 Table of Contents Summary of Key Findings... 4 Research Objectives Respondent Sample and Groups Key Findings Economic and Housing Sentiment... 8 Consumer Demand (Purchase Mortgages). 12 Credit Standards.. 19 Mortgage Execution Outlook 26 Mortgage Servicing Rights (MSR) Execution Outlook. 29 Profit Margin Outlook.. 31 Appendix 33 Survey Methodology Details.. 34 Consumer Demand (Purchase Mortgages). 42 Consumer Demand (Refinance Mortgages) Credit Standards.. 54 Mortgage Execution Mortgage Servicing Rights (MSR) Execution. 61 Profit Margin Outlook.. 66 Survey Question Text. 68 2

3 Disclaimer Opinions, analyses, estimates, forecasts, and other views of Fannie Mae's Economic & Strategic Research (ESR) group or survey respondents included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts, and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current, or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, and other views published by the ESR group represent the views of that group or survey respondents as of the date indicated and do not necessarily represent the views of Fannie Mae or its management. 3

4 Summary of Key Findings Housing Sentiment Consumer Demand Credit Standards Mortgage Execution Mortgage Servicing Rights (MSR) Compared with the general population of consumers, senior mortgage executives continue to be more optimistic about the overall economy and more pessimistic about consumers ability to get a mortgage today. After gradually trending down throughout, lenders purchase mortgage demand expectations across all loan types (GSE eligible, non-gse eligible, and government loans) increased this quarter across all institution sizes and types, although we recognize that there might be seasonal influences. This quarter, across all loan types, the share of lenders reporting credit easing is higher than the share of lenders reporting credit tightening. Mortgage banks continue to be more likely than depository institutions to report credit easing. Most institutions reported that they expect to maintain their strategy in relation to secondary market outlets over the next year. Among larger institutions and mortgage banks, more lenders reported expectations to decrease rather than to increase the share sold to GSEs. The majority of institutions reported that they expect to maintain their current Mortgage Servicing Rights (MSR) execution strategies over the next year. Among mortgage banks, more lenders reported plans to retain rather than to sell their MSRs. Profit Margin Outlook Lenders profit margin outlook has significantly improved from last year, in particular, among larger lenders, with the share of lenders expecting profit margin to go up over the next three months increasing significantly this quarter. Consumer demand and operational efficiency are the most cited reasons for increased profit margin expectations over the next three months. 4

5 Research Objectives Previously, there was no broad-based industry survey to track lenders expectations for the mortgage industry. The Mortgage Lender Sentiment Survey, which debuted in March, is a quarterly online survey among senior executives in the mortgage industry, designed to: Track insights and provide benchmarks into current and future mortgage lending activities and practices. Quarterly Regular Questions Consumer Mortgage Demand Credit Standards Mortgage Execution Mortgage Servicing Rights (MSR) Execution Featured Specific-Topic Questions FHA s Mortgage Insurance Premium Reduction by 0.5% 97% LTV Product Homeownership Education/Counseling Profit Margin Outlook 30-Year Fixed Mortgage Interest Rate Methodology A quarterly minute online survey of senior executives, such as CEOs and CFOs, of Fannie Mae s lending institution customers. The results are reported at the lending institution parent-company level. If more than one individual from the same institution completes the survey, their responses are averaged to represent their parent company. 5

Sample Size 197 58 Loan Origination Volume Groups Mid-sized Fannie Mae s")

6 2015 Respondent Sample and Groups For 2015, a total of 208 senior executives completed the survey from February 4-16, representing 197 lending institutions.* Loan Origination Volume Groups** HIGHER loan origination volume Larger Top 15% Mid-sized Top 16% - 35% 100% 85% 65% Sample Total Lending The Total data throughout this report is an average of the means of the three loan origination volume groups listed below. Larger Fannie Mae s customers whose 2013 total industry loan origination volume was in the top 15% (above $965 million) Sample Size Loan Origination Volume Groups Mid-sized Fannie Mae s customers whose 2013 total industry loan origination volume was in the next 20% (16%- 35%) (between $269 million to $965 million) 50 Smaller Bottom 65% Smaller Fannie Mae s customers whose 2013 total industry loan origination volume was in the bottom 65% (less than $269 million) 89 LOWER loan origination volume Institution Type*** Mortgage Banks (non-depository) 53 Depository 95 Credit Unions 40 * The results of the Mortgage Lender Sentiment Survey are reported at the lending institutional parent-company level. If more than one individual from the same institution completes the survey, their responses are averaged to represent their parent institution. ** The 2013 total loan volume per lender used here includes the best available annual origination information from sources such as Home Mortgage Disclosure Act (HMDA), Fannie Mae, Freddie Mac, and Marketrac. The most recent loan volume data available when the survey was conducted was *** Lenders that are not classified into mortgage banks or depository institutions or credit unions are mostly housing finance agencies. 6

7 Loan Type Definition Questions about consumer mortgage demand and credit standards are asked across three loan types: GSE eligible, Non-GSE eligible, and Government loans. Loan Type Definition Used in the Survey Loan Type Definition GSE Eligible Loans GSE Eligible Mortgages are defined as mortgages meeting the underwriting guidelines, including loan limit amounts, of the Government-Sponsored Enterprises (GSEs) (Fannie Mae and Freddie Mac). Government loans are excluded from this category. Non-GSE Eligible Loans Non-GSE Eligible Mortgages are defined as mortgages that do not meet the GSE guidelines for purchase. These loans typically require larger down payments and typically carry higher interest rates than GSE loans. Government loans are excluded from this category. Government Loans Government Mortgages primarily include Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA) insured loans but also includes other programs such as Rural Housing Guaranteed and Direct loans. 7

8 ECONOMIC AND HOUSING SENTIMENT Senior mortgage executives are significantly more optimistic about the overall economy and consumers ability to get a mortgage this quarter compared with this time last year. Compared with the general population of consumers, senior mortgage executives continue to be more optimistic about the economy and more pessimistic about consumers ability to get a mortgage today. 8

9 U.S. Economy Overall Senior mortgage executives are significantly more optimistic about the overall economy this quarter compared with last year, and continue to be more optimistic than the general population of consumers about the economy. In general, do you, as a senior mortgage executive, think the U.S. economy overall is on the right track or the wrong track? Right Track Don t know Wrong Track Total Larger Mid-sized Smaller N=197 N=192 N=196 N=186 N=247 N=58 N=49 N=50 N=47 N=46 N=50 N=56 N=55 N=50 N= 51 N=89 N=87 N=91 N=89 N=150 National Housing Survey TM Among the General Population (consumers) * Denotes a statistically significant change since Q4 ; Rows may not sum up to 100% because of rounding and don t know responses. National Housing Survey: 9

2.7% (Mar) 2.4% (Jun) 2.1% (Aug) 2.6% (Nov) 2.")

10 Home Prices Next 12 Months Senior mortgage executives are becoming more optimistic than the general population of consumers about future home prices. Total Larger Mid-sized Smaller N=197 N=192 N=196 N=186 N=247 N=58 N=49 N=50 N=47 N=46 N=50 N=56 N=55 N=50 N= 51 Nationally, during the next 12 months, do you, as a senior mortgage executive, think home prices in general will go up, go down, or stay the same as where they are now? N=89 N=87 N=91 N=89 N=150 Go Up Stay the Same Go Down By about what percent do you, as a senior mortgage executive, think home prices nationally will go up/down on average over the next 12 months? 3.2% 3.0% 3.2% 3.4% Q2 2.6% 3.3% 1.8% 2.7% Q3 1.9% 1.6% 1.8% 2.3% Q4 1.7% 1.1% 2.0% 2.1% % 2.5% 2.3% 2.6% National Housing Survey TM Among the General Population (consumers) 2.7% (Mar) 2.4% (Jun) 2.1% (Aug) 2.6% (Nov) 2.5% (Feb) * Denotes a statistically significant change since Q4 ; Rows may not sum up to 100% because of rounding and don t know responses. National Housing Survey: 10

Total Larger Mid-sized Smaller N=247")

11 Difficulty of Getting a Mortgage Senior mortgage executives are significantly more optimistic when it comes to the ease of getting a mortgage today this quarter compared with last year, but they are still less optimistic than the general population of consumers about the ease of getting a mortgage. Do you think it is very difficult, somewhat difficult, somewhat easy, or very easy for consumers to get a home mortgage today? Easy Difficult National Housing Survey TM Among the General Population (consumers) Total Larger Mid-sized Smaller N=247 N=186 N=196 N=192 N=197 N=46 N=47 N=50 N=49 N=58 N= 51 N=50 N=55 N=56 N=50 N=150 N=89 N=91 N=87 N=89 * Denotes a statistically significant change since Q4 Rows may not sum up to 100% because of rounding and don t know responses that are not included in the chart. Easy = Very easy + Somewhat easy; Difficult = Very difficult + Somewhat difficult National Housing Survey: 11

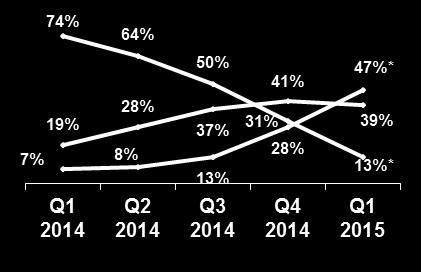

12 CONSUMER DEMAND (PURCHASE MORTGAGES) After gradually trending down throughout, lenders purchase mortgage demand expectations for all types of loans increased this quarter, with the share of lenders expecting demand to go up over the next three months increasing significantly across all institution sizes and types. Although the mortgage demand questions in the survey ask survey respondents to account for seasonal variation, we believe that some seasonal influence remains and contributed to the forecasted demand increase. Lenders also reported significant upward demand expectations for refinance mortgages (please see the Appendix). 12

13 Purchase Mortgage Demand: GSE Eligible Lenders purchase mortgage demand expectations for GSE eligible loans increased this quarter, across all institution sizes, after gradually declining in. Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family purchase mortgages go up, go down, or stay the same? Up = Went up significantly + Went up somewhat, Down = Went down significantly + Went down somewhat Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? Up = Go up significantly + Go up somewhat, Down = Go down significantly + Go down somewhat * Denotes a statistically significant change since Q4 13

14 Purchase Mortgage Demand: GSE Eligible (by institution type) Lenders purchase mortgage demand expectations for GSE eligible loans are higher now than a year ago, across all institution types. Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family purchase mortgages go up, go down, or stay the same? Up = Went up significantly + Went up somewhat, Down = Went down significantly + Went down somewhat Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? Up = Go up significantly + Go up somewhat, Down = Go down significantly + Go down somewhat * Denotes a statistically significant change since Q4 14

15 Purchase Mortgage Demand: Non-GSE Eligible Lenders purchase mortgage demand expectations for Non-GSE eligible loans increased this quarter across all institution sizes. Expectations are now more in line with expectations in. Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family purchase mortgages go up, go down, or stay the same? Up = Went up significantly + Went up somewhat, Down = Went down significantly + Went down somewhat Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? Up = Go up significantly + Go up somewhat, Down = Go down significantly + Go down somewhat * Denotes a statistically significant change since Q4 15

16 Purchase Mortgage Demand: Non-GSE Eligible (by institution type) Lenders purchase mortgage demand expectations for Non-GSE eligible loans increased this quarter for all institution types. Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family purchase mortgages go up, go down, or stay the same? Up = Went up significantly + Went up somewhat, Down = Went down significantly + Went down somewhat Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? Up = Go up significantly + Go up somewhat, Down = Go down significantly + Go down somewhat * Denotes a statistically significant change since Q4 16

17 Purchase Mortgage Demand: Government Lenders purchase mortgage demand expectations for government loans increased this quarter, across all institution sizes, after gradually declining in. Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family purchase mortgages go up, go down, or stay the same? Up = Went up significantly + Went up somewhat, Down = Went down significantly + Went down somewhat Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? Up = Go up significantly + Go up somewhat, Down = Go down significantly + Go down somewhat * Denotes a statistically significant change since Q4 17

18 Purchase Mortgage Demand: Government (by institution type) After gradually trending down throughout, lenders purchase mortgage demand expectations for government loans increased this quarter across all institution types. Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family purchase mortgages go up, go down, or stay the same? Up = Went up significantly + Went up somewhat, Down = Went down significantly + Went down somewhat Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? Up = Go up significantly + Go up somewhat, Down = Go down significantly + Go down somewhat * Denotes a statistically significant change since Q4 18

19 CREDIT STANDARDS Credit tightening observed last year has continued to gradually trend down into 2015, with fewer lenders reporting credit tightening over the prior three months. In particular, this quarter, across all loan types (GSE eligible, non-gse eligible, and government loans), the share of lenders reporting credit easing is higher than the share of lenders reporting credit tightening. Among larger institutions, more lenders continue to report credit easing than tightening across all loan types. Mortgage banks continue to be more likely than depository institutions to report credit easing. 19

?")

20 Credit Standards: GSE Eligible Credit tightening reported for GSE eligible loans over the prior three months has gradually trended down across all lender sizes. Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Ease Remain Unchanged Tighten Q: Over the past three months, how did your firm s credit standards for approving consumer applications for mortgage loans change (across both purchase mortgages and refinance mortgages)? Ease = Eased considerably + Eased somewhat, Tighten = Tightened somewhat + Tightened considerably Q: Over the next three months, how do you expect your firm s credit standards for approving applications from individuals for mortgage loans to change (across purchase mortgages and refinance mortgages)? Ease = Ease considerably + Ease somewhat, Tighten = Tighten somewhat + Tighten considerably 20

?")

21 Credit Standards: GSE Eligible (by institution type) Credit tightening reported for GSE eligible loans over the prior three months has gradually trended down. Mortgage banks continue to be more likely than depository institutions to report credit easing. Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Ease Remain Unchanged Tighten Q: Over the past three months, how did your firm s credit standards for approving consumer applications for mortgage loans change (across both purchase mortgages and refinance mortgages)? Ease = Eased considerably + Eased somewhat, Tighten = Tightened somewhat + Tightened considerably Q: Over the next three months, how do you expect your firm s credit standards for approving applications from individuals for mortgage loans to change (across purchase mortgages and refinance mortgages)? Ease = Ease considerably + Ease somewhat, Tighten = Tighten somewhat + Tighten considerably 21

22 Credit Standards: Non-GSE Eligible Reported credit tightening for non-gse eligible loans over the prior three months has gradually trended down while more lenders among mid-sized and smaller institutions say credit standards have remained unchanged. Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Ease Remain Unchanged Tighten Q: Over the past three months, how did your firm s credit standards for approving consumer applications for mortgage loans change (across both purchase mortgages and refinance mortgages)? Ease = Eased considerably + Eased somewhat, Tighten = Tightened somewhat + Tightened considerably Q: Over the next three months, how do you expect your firm s credit standards for approving applications from individuals for mortgage loans to change (across purchase mortgages and refinance mortgages)? Ease = Ease considerably + Ease somewhat, Tighten = Tighten somewhat + Tighten considerably 22

?")

23 Credit Standards: Non-GSE Eligible (by institution type) Reported credit tightening for non-gse eligible loans over the prior three months has gradually trended down while more lenders across mortgage banks and depository institutions say their credit standards have remained unchanged. Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Ease Remain Unchanged Tighten Q: Over the past three months, how did your firm s credit standards for approving consumer applications for mortgage loans change (across both purchase mortgages and refinance mortgages)? Ease = Eased considerably + Eased somewhat, Tighten = Tightened somewhat + Tightened considerably Q: Over the next three months, how do you expect your firm s credit standards for approving applications from individuals for mortgage loans to change (across purchase mortgages and refinance mortgages)? Ease = Ease considerably + Ease somewhat, Tighten = Tighten somewhat + Tighten considerably 23

24 Credit Standards: Government Reported credit tightening for government loans over the prior three months has gradually trended down. Among larger institutions, more lenders continue to report credit easing than tightening. Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Ease Remain Unchanged Tighten Q: Over the past three months, how did your firm s credit standards for approving consumer applications for mortgage loans change (across both purchase mortgages and refinance mortgages)? Ease = Eased considerably + Eased somewhat, Tighten = Tightened somewhat + Tightened considerably Q: Over the next three months, how do you expect your firm s credit standards for approving applications from individuals for mortgage loans to change (across purchase mortgages and refinance mortgages)? Ease = Ease considerably + Ease somewhat, Tighten = Tighten somewhat + Tighten considerably 24

?")

25 Credit Standards: Government (by institution type) Reported credit tightening for government loans over the prior three months has gradually trended down while mortgage banks are more likely than deposit institutions to report credit easing. Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Ease Remain Unchanged Tighten Q: Over the past three months, how did your firm s credit standards for approving consumer applications for mortgage loans change (across both purchase mortgages and refinance mortgages)? Ease = Eased considerably + Eased somewhat, Tighten = Tightened somewhat + Tightened considerably Q: Over the next three months, how do you expect your firm s credit standards for approving applications from individuals for mortgage loans to change (across purchase mortgages and refinance mortgages)? Ease = Ease considerably + Ease somewhat, Tighten = Tighten somewhat + Tighten considerably 25

26 MORTGAGE EXECUTION OUTLOOK Most institutions reported that they expect to maintain their strategy in relation to secondary market outlets over the next year. Moreover, Among larger institutions, more lenders reported expectations to decrease rather than to increase the share sold to GSEs. Among credit unions, more lenders reported expectations to decrease rather than to increase portfolioretention shares. Among mortgage banks, more lenders reported expectations to decrease rather than to increase the share sold to GSEs and correspondents (whole-loan sales to non-gses). 26

27 Mortgage Execution Outlook Next Year Most institutions reported that they expect to maintain their strategy in relation to secondary market outlets over the next year. Among larger institutions, more lenders reported expectations to decrease rather than to increase the share sold to GSEs. Total Larger Increase About the same Decrease Mid-sized Smaller Whether an institution reported increase/decrease/stay the same was based on the difference to their responses to the following 2 questions: Q: Approximately, what percent of your firm s total mortgage originations goes to each of the following categories? Q: Looking forward, what percent of your firm s total mortgage originations over the next year will go to each of the following categories? 27

28 Mortgage Execution Outlook Next Year (by institution type) Most institutions reported that they expect to maintain their strategy in relation to secondary market outlets over the next year. Among credit unions, more lenders reported expectations to decrease rather than to increase portfolio-retention shares. Among mortgage banks, more lenders reported expectations to decrease rather than to increase the share sold to GSEs and correspondents (whole loan sales to non-gses). Increase About the same Decrease Mortgage Banks Depository Credit Unions Portfolio Retention GSE (Fannie Mae and Freddie Mac) Ginnie Mae (FHA/VA) Private Label Securities / Non- Agency Securities Whole Loan Sales to NON-GSE (Correspo ndent) Portfolio Retention GSE (Fannie Mae and Freddie Mac) Ginnie Mae (FHA/VA) Private Label Securities / Non- Agency Securities Whole Loan Sales to NON-GSE (Correspo ndent) Portfolio Retention GSE (Fannie Mae and Freddie Mac) Ginnie Mae (FHA/VA) Private Label Securities / Non- Agency Securities Whole Loan Sales to NON-GSE (Correspo ndent) Whether an institution reported increase/decrease/stay the same was based on the difference to their responses to the following 2 questions: Q: Approximately, what percent of your firm s total mortgage originations goes to each of the following categories? Q: Looking forward, what percent of your firm s total mortgage originations over the next year will go to each of the following categories? 28

29 MORTGAGE SERVICING RIGHTS (MSR) EXECUTION OUTLOOK The majority of institutions reported that they expect their current MSR execution strategies to stay about the same over the next year. Moreover, Among mortgage banks, more lenders reported plans to retain rather than to sell their MSRs. Among credit unions, more lenders reported plans to sell rather than to retain their MSRs. 29

goes to each of the following categories?")

30 Mortgage Servicing Rights Execution Outlook The majority of institutions reported that they expect to maintain their current MSR execution strategies over the next year. Among mortgage banks, more lenders reported plans to retain rather than to sell their MSRs. Among credit unions, more lenders reported plans to sell rather than to retain their MSRs. Increase About the same Total Larger Mid-sized Smaller Decrease Mortgage Banks Depository Credit Unions Whether an institution reported increase/decrease/stay the same was based on the difference to their responses to the following 2 questions: Q: Approximately, what percent of your mortgage servicing rights (MSR) goes to each of the following categories? Q: Looking forward, what percent of your firm s mortgage servicing rights (MSR) over the next year will go to each of the following categories? 30

31 PROFIT MARGIN OUTLOOK The share of lenders reporting increased profit margin outlook over the next three months has increased significantly this quarter, in particular among larger lenders. Consumer demand and operational efficiency are the most cited reasons for increased profit margin expectations over the next three months. Government regulatory compliance and competition from other lenders are the most popular reasons given in driving the expectation of a decrease in profit margin over the next three months. 31

32 Profit Margin Outlook Next 3 Months The share of lenders reporting increased profit margin outlook over the next three months has increased significantly this quarter, in particular among larger lenders. Total Larger Mid-sized Smaller N=241 N=175 N=185 N=182 N=180 N=44 N=44 N=50 N=48 N=56 N=50 N=48 N=52 N=54 N=47 N=147 N=83 N=82 N=80 N=77 Q2 Q3 Q Q2 Q3 Q Q2 Q3 Q Q2 Q3 Q Top 2 Reasons for Expected Increase: (N=70) 1. Consumer demand 2. Operational efficiency (i.e., technology) Top 2 Reasons for Expected Increase: (N=29) 1. Consumer demand 2. Operational efficiency (i.e., technology) Top 2 Reasons for Expected Increase: (N=19) 1. Operational efficiency (i.e., technology) 2. Consumer demand Top 2 Reasons for Expected Increase: (N=22) 1. Consumer demand 2. Market trend changes (i.e. shift from refinance to purchase) Increase About the same Decrease Top 2 Reasons for Expected Decrease: (N=16) 1. Government regulatory compliance 2. Competition from other lenders Top 2 Reasons for Expected Decrease: (N=7) 1. Competition from other lenders 2. Government regulatory compliance Top 2 Reasons for Expected Decrease: (N=4) 1. Government regulatory compliance 2. GSE pricing and policies Top 2 Reasons for Expected Decrease: (N=5) 1. Government regulatory compliance 2. Competition from other lenders Q: Over the next three months, how much do you expect your firm's profit margin to change for its single-family mortgage production? [Showing: (Substantially Increase (25+ basis points) + Moderately Increase (5-25 basis points)), About the same (0-5 basis points), (Moderately Decrease (5-25 basis points) + Substantially Decrease (25+ basis points))] Q: What do you think will drive the increase (decrease) in your firm s profit margin over the next three months? Please select up to two of the most important reasons. * Denotes a statistically significant change since Q4 32

33 Appendix Survey Methodology Details.. 34 Consumer Demand (Purchase Mortgages). 42 Consumer Demand (Refinance Mortgages) Credit Standards.. 54 Mortgage Execution Mortgage Servicing Rights (MSR) Execution. 61 Profit Margin Outlook.. 66 Survey Question Text

34 Appendix Survey Methodology Details 34

35 Mortgage Lender Sentiment Survey Background The Fannie Mae Mortgage Lender Sentiment Survey is a quarterly online survey of senior executives of Fannie Mae s lending institution partners to provides insights and benchmarks that help mortgage industry professionals understand industry and market trends and assess their own business practices. Survey Methodology To ensure that the survey results represent the behavior and output of organizations rather than individuals, the Fannie Mae Mortgage Lender Sentiment Survey is structured and conducted as an establishment survey. The results are reported at the lending institutional level. If more than one individual from the same institution complete the survey, their responses are averaged to represent their institution. Each respondent is asked questions. Sample Design Each quarter a random selection of approximately 2,000 senior executives among Fannie Mae s approved lenders are invited to participate in the study. 35

36 Lending Institution Characteristics Fannie Mae s customers invited to participate in the Mortgage Lender Sentiment Survey represent a broad base of different lending institutions that conducted business with Fannie Mae in were divided into three groups based on their 2013 total industry loan volume - Larger (top 15%), Mid-sized (top 16%-35%), and Smaller (bottom 65%). The data below further describe the compositions and loan characteristics of the three groups of institutions. Institution Type Loan Types Loan Purposes 36

37 Sample Sizes Q2 Q3 Q Sample Size Margin of Error Sample Size Margin of Error Sample Size Margin of Error Sample Size Margin of Error Sample Size Margin of Error Total Lending 247 ±5.65% 186 ±6.69% 196 ±6.48% 192 ±6.56% 197 ±6.51% Loan Origination Volume Groups Larger Mid-sized Smaller 46 ±12.77% 47 ±12.60% 50 ±12.10% 49 ±12.11% 58 ±11.11% 51 ±12.41% 50 ±12.56% 55 ±11.84% 56 ±11.70% 50 ±12.68% 150 ±7.31% 89 ±9.86% 91 ±9.74% 87 ±9.98% 89 ±9.91 Mortgage Banks 38 ±14.61% 47 ±12.84% 57 ±11.34% 48 ±12.66% 53 ±12.07% Institution Type Depository 121 ±8.14% 84 ±10.07% 75 ±10.73% 83 ±10.13% 95 ±9.43% Credit Unions 72 ±10.39% 50 ±12.91% 52 ±12.62% 49 ±13.07% 40 ±14.77% was fielded between March 4, and March 18, Q2 was fielded between May 28, and June 8, Q3 was fielded between August 6, and August 23, Q4 was fielded between November 5, and November 24, 2015 was fielded between February 4, 2015 and February 16,

38 2015 Cross-Subgroup Sample Sizes Total Larger Lenders Mid-Sized Lenders Smaller Lenders Total Mortgage Banks (non-depository) Depository Credit Unions

39 2015 Sample Sizes: Consumer Demand Purchase Mortgages: GSE Eligible Past 3 Months Non-GSE Eligible Government GSE Eligible Next 3 Months Non-GSE Eligible Government Total Lending Larger Mid-sized Smaller Refinance Mortgages: GSE Eligible Past 3 Months Non-GSE Eligible Government GSE Eligible Next 3 Months Non-GSE Eligible Government Total Lending Larger Mid-sized Smaller

40 2015 Sample Sizes: Credit Standards GSE Eligible Past 3 Months Non-GSE Eligible Government GSE Eligible Next 3 Months Non-GSE Eligible Government Total Lending Larger Mid-sized Smaller

41 Calculation of the Total The Total data presented in this report are an average of the means of the three loan origination volume groups (Table below illustrates the Total calculation). Please note that percentages are based on the number of financial institutions that gave responses other than Not Applicable. Percentages may add to under or over 100% due to rounding. Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family purchase mortgages to go up, go down, or stay the same? GSE Eligible ( 2015) Larger Mid-sized Smaller Total Go up 73% 69% 72% 71% [(73% + 69% + 72%)/3] Stayed the same 27% 27% 25% 26% Go down 0% 5% 3% 3% 41

42 Appendix Consumer Demand (Purchase Mortgages) 42

43 Purchase Mortgage Demand: Drivers of Change (selected verbatim) Low Interest Rates Improving Economy FHA Premium Reductions Pent Up Demand Past 3 Months N=120 Drivers of Demand Up Drivers of Demand Down Q: What do you think drove the change in your firm s consumer demand for single-family purchase mortgages over the past three months? Please be as specific as possible. (Optional) Mortgage rates, improved consumer confidence, increased rental rates. Larger Institution Mainly increased consumer sentiment. Positive media attention around expansion of FNMA-FHLMC guidelines (97 LTV) and FHA MIP reductions have also contributed.. Mid-sized Institution Lower fuel prices allowed more confidence in the economy which in turn made the decision easier. Smaller Institution Increased competition who are reducing credit standards. Larger Institution Uncertainty in employment outlook. Mid-sized Institution Mortgage reform, increased underwriting requirements implemented by the CFPB, job loss, FICO scores. Smaller Institution 43

44 Purchase Mortgage Demand: Drivers of Change (GSE Eligible) You mentioned that you expect your firm s consumer demand for GSE eligible loans will go up over the next three months. Which of the following housing marketplace factors do you think will drive the demand to go up? Please select up to two of the most important reasons and rank them in order of importance. (Showing % rank 1 ) Total Larger Mid-sized Smaller N= National Housing Survey Among the General Population (consumers)* Mortgage rates are favorable 48% 58% 42% 43% 40% Economic conditions (e.g., employment) overall are favorable 41% 39% 45% 41% 12% Home prices are low 3% 0% 6% 5% 18% There are many homes available on the market 2% 0% 0% 5% 15% It is easy to qualify for a mortgage 0% 1% 0% 0% 4% You mentioned that you expect your firm s consumer demand for GSE eligible loans will go down over the next three months. Which of the following housing marketplace factors do you think will drive the demand down? Please select up to two of the most important reasons and rank them in order of importance. (Showing % rank 1) Total Larger Mid-sized Smaller N= National Housing Survey Among the General Population (consumers)** It is difficult to qualify for a mortgage 22% 0% 14% 33% 16% Economic conditions (e.g., employment) overall are not favorable 14% 0% 0% 33% 37% Home prices are high 14% 0% 0% 33% 19% Mortgage rates are not favorable 0% 0% 0% 0% 12% There are not many homes available on the market 0% 0% 0% 0% 3% *Q: Please tell me the primary reason why you think this is a good time to buy a house. **Q: Please tell me the primary reason why you think this is a bad time to buy a house. 44

45 Purchase Mortgage Demand: Drivers of Change (Non-GSE Eligible) You mentioned that you expect your firm s consumer demand for Non-GSE eligible loans will go up over the next three months. Which of the following housing marketplace factors do you think will drive the demand to go up? Please select up to two of the most important reasons and rank them in order of importance. (Showing % rank 1) Total Larger Mid-sized Smaller N= National Housing Survey Among the General Population (consumers)* Mortgage rates are favorable 43% 54% 38% 37% 40% Economic conditions (e.g., employment) overall are favorable 34% 29% 38% 37% 12% Home prices are low 6% 3% 11% 6% 18% There are many homes available on the market 2% 0% 4% 2% 15% It is easy to qualify for a mortgage 4% 3% 4% 6% 4% You mentioned that you expect your firm s consumer demand for Non-GSE eligible loans will go down over the next three months. Which of the following housing marketplace factors do you think will drive the demand down? Please select up to two of the most important reasons and rank them in order of importance. (Showing % rank 1) Total Larger Mid-sized Smaller N= National Housing Survey Among the General Population (consumers)** It is difficult to qualify for a mortgage 0% 0% 0% 0% 16% Economic conditions (e.g., employment) overall are not favorable 0% 0% 0% 0% 37% Home prices are high 75% 100% 0% 60% 19% Mortgage rates are not favorable 0% 0% 0% 0% 12% There are not many homes available on the market 0% 0% 0% 0% 3% *Q: Please tell me the primary reason why you think this is a good time to buy a house. **Q: Please tell me the primary reason why you think this is a bad time to buy a house. 45

46 Purchase Mortgage Demand: Drivers of Change (Government) You mentioned that you expect your firm s consumer demand for government loans will go up over the next three months. Which of the following housing marketplace factors do you think will drive the demand to go up? Please select up to two of the most important reasons and rank them in order of importance. (Showing % rank 1) Total Larger Mid-sized Smaller N= National Housing Survey Among the General Population (consumers)* Mortgage rates are favorable 49% 60% 43% 38% 40% Economic conditions (e.g., employment) overall are favorable 33% 24% 33% 46% 12% Home prices are low 1% 0% 0% 4% 18% There are many homes available on the market 1% 0% 0% 3% 15% It is easy to qualify for a mortgage 8% 7% 10% 6% 4% You mentioned that you expect your firm s consumer demand for government loans will go down over the next three months. Which of the following housing marketplace factors do you think will drive the demand down? Please select up to two of the most important reasons and rank them in order of importance. (Showing % rank 1) Total Larger Mid-sized Smaller N= National Housing Survey Among the General Population (consumers)** It is difficult to qualify for a mortgage 39% 0% 50% 50% 16% Economic conditions (e.g., employment) overall are not favorable 25% 0% 50% 0% 37% Home prices are high 0% 0% 0% 0% 19% Mortgage rates are not favorable 14% 0% 0% 50% 12% There are not many homes available on the market 21% 100% 0% 0% 3% *Q: Please tell me the primary reason why you think this is a good time to buy a house. **Q: Please tell me the primary reason why you think this is a bad time to buy a house. 46

47 Appendix Consumer Demand (Refinance Mortgages) 47

48 Refinance Mortgage Demand: GSE Eligible Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family refinance mortgages go up, go down, or stay the same? A: Went up, Stayed the same, or Went Down Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family refinance mortgages to go up, go down, or stay the same? A: Go up, Stay the same, or Go Down * Denotes a statistically significant change since Q4 48

49 Refinance Mortgage Demand: GSE Eligible (by institution type) Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family refinance mortgages go up, go down, or stay the same? A: Went up, Stayed the same, or Went Down Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family refinance mortgages to go up, go down, or stay the same? A: Go up, Stay the same, or Go Down * Denotes a statistically significant change since Q4 49

50 Refinance Mortgage Demand: Non-GSE Eligible Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family refinance mortgages go up, go down, or stay the same? A: Went up, Stayed the same, or Went Down Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family refinance mortgages to go up, go down, or stay the same? A: Go up, Stay the same, or Go Down * Denotes a statistically significant change since Q4 50

Mortgage Banks Depository Credit")

51 Refinance Mortgage Demand: Non-GSE Eligible (by institution type) Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family refinance mortgages go up, go down, or stay the same? A: Went up, Stayed the same, or Went Down Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family refinance mortgages to go up, go down, or stay the same? A: Go up, Stay the same, or Go Down * Denotes a statistically significant change since Q4 51

52 Refinance Mortgage Demand: Government Total Larger Mid-sized Smaller Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family refinance mortgages go up, go down, or stay the same? A: Went up, Stayed the same, or Went Down Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family refinance mortgages to go up, go down, or stay the same? A: Go up, Stay the same, or Go Down * Denotes a statistically significant change since Q4 52

53 Refinance Mortgage Demand: Government (by institution type) Mortgage Banks Depository Credit Unions Past 3 Months Next 3 Months Up The same Down Q: Over the past three months, apart from normal seasonal variation, did your firm s consumer demand for single-family refinance mortgages go up, go down, or stay the same? A: Went up, Stayed the same, or Went Down Q: Over the next three months, apart from normal seasonal variation, do you expect your firm s consumer demand for single-family refinance mortgages to go up, go down, or stay the same? A: Go up, Stay the same, or Go Down * Denotes a statistically significant change since Q4 53

54 Appendix Credit Standards 54

55 Credit Standards: Drivers of Change (selected verbatim) Drivers of Loosening Change Drivers of Tightening Change Regulations Rollback of Overlays New 97% LTV Past 3 Months N=49 Regulations Rollback of Overlays New 97% LTV Next 3 Months N=25 Q: What do you think drove the change in your firm s credit standards for approving consumer applications for purchase mortgage loans over the last three months? Please be as specific as possible. (Optional) Q: What do you think will drive the change in your firm s credit standards for approving consumer applications for purchase mortgage loans over the next three months? Please be as specific as possible. (Optional) Simple - higher compliance standards. Larger Institution DU Collateral Underwriter will impact appraisal standards. Larger Institution Investor overlays. Mid-sized Institution Compliance, compliance, compliance. Larger Institution We have always underwritten loans to Fannie Mae guidelines... We have always tried to be more conservative than those guidelines and have been rewarded.. Smaller Institution Government regulations. Smaller Institution Better clarity from Fannie Mae has allowed aggregators to reduce overlays and allows us to follow suit. Larger Institution Reduced aggregator overlays and improved guidance from Fannie Mae.. Larger Institution We relaxed our overlay to be more consistent with Fannie Mae. Mid-sized Institution Easier qualifications. Smaller Institution Allowing lower FICO scores on FHA and VA Loans. Mid-sized Institution New lending management, better understanding of compliance concerns. Smaller Institution 55

56 Appendix Mortgage Execution 56

57 Mortgage Execution Share Current What is your firm s approximate total mortgage business share for each of the following post mortgage-origination execution categories? Please enter a percent in each box below. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Q2 Total Q3 Q Q2 Larger Q3 Q Q2 Mid-sized Q3 Q Q2 Smaller Q3 Q N= GSE (Fannie Mae and Freddie Mac) 49% 49% 51% 49% 47% 51% 48% 52% 50% 48% 47% 51% 47% 47% 42% 49% 48% 53% 49% 51% Portfolio Retention 24% 22% 20% 23% 21% 19% 13% 8% 14% 13% 21% 18% 18% 19% 16% 32% 37% 34% 36% 34% Whole Loan Sales to NON-GSE (Correspondent) 13% 13% 12% 12% 17% 12% 16% 18% 15% 17% 19% 14% 14% 13% 25% 9% 8% 5% 8% 8% Ginnie Mae (FHA/VA) 11% 14% 14% 13% 12% 15% 20% 19% 19% 20% 11% 16% 15% 16% 13% 6% 5% 7% 5% 5% Private Label Securities / Non-Agency Securities 1% 1% 2% 1% 1% 3% 2% 2% 1% 2% 1% 1% 4% 1% 1% 1% 0% 0% 0% 1% Other 1% 1% 1% 1% 2% 0% 2% 0% 0% 0% 1% 1% 2% 3% 2% 2% 2% 1% 1% 2% 57

58 Mortgage Execution Share Next Year Looking forward, what percent of your firm s mortgage servicing rights (MSR) over the next year will go to each of the following categories? Please enter a percent for each category. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Total Larger Mid-sized Smaller N= GSE (Fannie Mae and Freddie Mac) 47% 47% 43% 50% Portfolio Retention 21% 13% 15% 33% Whole Loan Sales to NON-GSE (Correspondent) 16% 16% 24% 8% Ginnie Mae (FHA/VA) 13% 21% 14% 5% Private Label Securities / Non-Agency Securities 2% 3% 2% 1% 58

59 Mortgage Execution Share Current (by institution type) What is your firm s approximate total mortgage business share for each of the following post mortgageorigination execution categories? Please enter a percent in each box below. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Q2 Mortgage Banks Q3 Q Q2 Depository Q3 Q Q2 Credit Unions Q3 Q N= GSE (Fannie Mae and Freddie Mac) 43% 48% 50% 46% 40% 49% 50% 52% 49% 54% 52% 46% 50% 53% 47% Portfolio Retention 3% 1% 0% 1% 4% 29% 29% 28% 32% 25% 42% 44% 45% 42% 46% Whole Loan Sales to NON-GSE (Correspondent) 30% 23% 21% 26% 30% 11% 10% 10% 9% 11% 3% 4% 1% 1% 2% Ginnie Mae (FHA/VA) 22% 22% 25% 24% 22% 7% 9% 8% 8% 8% 2% 4% 2% 3% 3% Private Label Securities / Non-Agency Securities 2% 2% 2% 1% 2% 2% 1% 2% 0% 1% 1% 0% 1% 0% 1% Other 1% 3% 2% 1% 2% 3% 1% 1% 2% 1% 1% 1% 1% 1% 1% 59

60 Mortgage Execution Share Next Year (by institution type) Looking forward, what percent of your firm s mortgage servicing rights (MSR) over the next year will go to each of the following categories? Please enter a percent for each category. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Mortgage Banks Depository Credit Unions N= GSE (Fannie Mae and Freddie Mac) 39% 54% 47% Portfolio Retention 6% 24% 44% Whole Loan Sales to NON-GSE (Correspondent) 26% 11% 3% Ginnie Mae (FHA/VA) 24% 8% 4% Private Label Securities / Non-Agency Securities 4% 1% 1% Other 24% 18% 8% 60

61 Appendix MORTGAGE SERVICING RIGHTS (MSR) EXECUTION 61

62 Mortgage Servicing Rights (MSR) Execution Share Current Approximately what percent of your mortgage servicing rights (MSR) goes to each of the following categories? Please enter a percent in each box below. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Q2 Total Q3 Q Q2 Larger Q3 Q Q2 Mid-sized Q3 Q Q2 Smaller Q3 Q N= MSR retained, serviced inhouse 54% 51% 46% 54% 48% 47% 40% 30% 42% 39% 48% 42% 40% 45% 35% 67% 72% 69% 75% 71% MSR retained, serviced by a subservicer 23% 21% 22% 18% 17% 24% 23% 29% 28% 21% 30% 25% 23% 21% 22% 15% 13% 14% 7% 10% MSR sold 23% 28% 32% 27% 34% 29% 37% 41% 30% 40% 21% 33% 37% 34% 44% 18% 15% 17% 18% 19% 62

63 Mortgage Servicing Rights (MSR) Execution Share Next Year Looking forward, what percent of your firm s mortgage servicing rights (MSR) over the next year will go to each of the following categories? Please enter a percent for each category. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Total Larger Mid-sized Smaller N= MSR retained, serviced in-house 48% 40% 35% 70% MSR retained, serviced by a subservicer 17% 19% 21% 10% MSR sold 35% 41% 44% 20% 63

64 Mortgage Servicing Rights (MSR) Execution Share Current (by institution type) Approximately what percent of your mortgage servicing rights (MSR) goes to each of the following categories? Please enter a percent in each box below. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Q2 Mortgage Banks Q3 Q Q2 Depository Q3 Q Q2 Credit Unions Q3 Q N= MSR retained, serviced in-house 18% 17% 15% 18% 12% 64% 65% 63% 70% 65% 74% 80% 77% 85% 80% MSR retained, serviced by a subservicer 43% 33% 30% 27% 29% 12% 15% 16% 11% 9% 20% 15% 18% 10% 14% MSR sold 39% 50% 55% 55% 59% 24% 21% 21% 18% 27% 6% 6% 5% 5% 6% 64

65 Mortgage Servicing Rights (MSR) Execution Share Next Year (by institution type) Looking forward, what percent of your firm s mortgage servicing rights (MSR) over the next year will go to each of the following categories? Please enter a percent for each category. If a category is not applicable to your firm, please enter 0. The percentages below must add up to 100%. Showing Mean % Larger Mid-sized Smaller N= MSR retained, serviced in-house 14% 64% 79% MSR retained, serviced by a subservicer 28% 9% 13% MSR sold 59% 27% 8% 65

66 Appendix Profit Margin Outlook 66

67 Profit Margin Outlook Next 3 Months (by institution type) The share of lenders reporting increased profit margin outlook over the next three months has increased significantly this quarter, in particular among mortgage banks. Mortgage Banks Depository Credit Unions N=37 N=45 N=53 N=48 N=48 N=118 N=78 N=71 N=76 N=84 N=72 N=48 N=49 N=47 N=39 Q2 Q3 Q Q2 Q3 Q Q2 Q3 Q Top 2 Reasons for Expected Increase: 1. Consumer demand 2. Operational efficiency (i.e., technology) Top 2 Reasons for Expected Increase: 1. Consumer demand 2. Market trend changes (i.e. shift from refinance to purchase) Top 2 Reasons for Expected Increase: 1. Consumer demand 2. Operational efficiency (i.e., technology) Increase About the same Decrease Top 2 Reasons for Expected Decrease: 1. Competition from other lenders 2. Government regulatory compliance Top 2 Reasons for Expected Decrease: 1. Competition from other lenders 2. Government regulatory compliance Top 2 Reasons for Expected Decrease: 1. Government regulatory compliance 2. GSE pricing and policies Q: Over the next three months, how much do you expect your firm's profit margin to change for its single-family mortgage production? [Showing: (Substantially Increase (25+ basis points) + Moderately Increase (5-25 basis points)), About the same (0-5 basis points), (Moderately Decrease (5-25 basis points) + Substantially Decrease (25+ basis points))] Q: What do you think will drive the increase/decrease in your firm s profit margin over the next three months? Please select up to two of the most important reasons. * Denotes a statistically significant change since Q4 67

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations Full Report Published September 15, Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations Full Report Published September 15, Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations Full Report published December 26, Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations Full Report published December 26, Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations Summary Report Published March 24, 2011 Fannie Mae. Trademarks Fannie Mae. Fannie Mae. Trademarks

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations Summary Report Published March 24, 2011 Fannie Mae. Trademarks Fannie Mae. Fannie Mae. Trademarks

Mortgage Lender Sentiment Survey TM

Mortgage Lender Sentiment Survey TM Q1 2015 Data Summary The Mortgage Lender Sentiment Survey conducted by Fannie Mae polls senior executives, such as CEOs and CFOs, at Fannie Mae s lending institution

Mortgage Lender Sentiment Survey TM Q1 2015 Data Summary The Mortgage Lender Sentiment Survey conducted by Fannie Mae polls senior executives, such as CEOs and CFOs, at Fannie Mae s lending institution

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Q4 2014 Data Summary The Mortgage Lender Sentiment Survey conducted by Fannie Mae polls senior executives, such as CEOs and CFOs, at Fannie Mae s lending institution partners

Mortgage Lender Sentiment Survey Q4 2014 Data Summary The Mortgage Lender Sentiment Survey conducted by Fannie Mae polls senior executives, such as CEOs and CFOs, at Fannie Mae s lending institution partners

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Q1 2018 Topic Analysis Published May 16, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents Executive Summary..... 3 Business Context and Research Questions..

Mortgage Lender Sentiment Survey Q1 2018 Topic Analysis Published May 16, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents Executive Summary..... 3 Business Context and Research Questions..

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Q4 2018 Topic Analysis Published January 30, 2019 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents Executive Summary..... 3 Business Context and Research

Mortgage Lender Sentiment Survey Q4 2018 Topic Analysis Published January 30, 2019 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents Executive Summary..... 3 Business Context and Research

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey How Will Artificial Intelligence Shape Mortgage Lending? Q3 2018 Topic Analysis Published October 4, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey How Will Artificial Intelligence Shape Mortgage Lending? Q3 2018 Topic Analysis Published October 4, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Consumers Still Value the Human Touch Lenders channel strategies vs. consumer preferences Q3 2017 Topic Analysis Published October 30, 2017 2017 Fannie Mae. Trademarks

Mortgage Lender Sentiment Survey Consumers Still Value the Human Touch Lenders channel strategies vs. consumer preferences Q3 2017 Topic Analysis Published October 30, 2017 2017 Fannie Mae. Trademarks

Cost Cutting Has Emerged as a Focus of Lender Competitiveness

Cost Cutting Has Emerged as a Focus of Lender Competitiveness Economic and Strategic Research (ESR) Published June 21, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Disclaimer Opinions, analyses, estimates,

Cost Cutting Has Emerged as a Focus of Lender Competitiveness Economic and Strategic Research (ESR) Published June 21, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Disclaimer Opinions, analyses, estimates,

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

5 Common Types of Home Loans

5 Common Types of Home Loans Copyright 2016 Platinum Home Mortgage Corporation All Rights Reserved Feel free to email, tweet, blog, and pass this ebook around the web, but please don t alter any of its

5 Common Types of Home Loans Copyright 2016 Platinum Home Mortgage Corporation All Rights Reserved Feel free to email, tweet, blog, and pass this ebook around the web, but please don t alter any of its

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Older Homeowners: Accessing Home Equity in Retirement

Older : Accessing Home Equity in Retirement National Housing Survey Topic Analysis Q2 2016 2016 Fannie Mae. Trademarks of Fannie Mae. 1 Research Methodology: Q2 2016 Each month, beginning in June, 2010,

Older : Accessing Home Equity in Retirement National Housing Survey Topic Analysis Q2 2016 2016 Fannie Mae. Trademarks of Fannie Mae. 1 Research Methodology: Q2 2016 Each month, beginning in June, 2010,

May 17, Housing Sector Overview

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

June 2018 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

October 2018 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Sanford C. Bernstein Investor Presentation

NMI Holdings, Inc. (NMIH) Sanford C. Bernstein Investor Presentation May 14, 2014 2014 Copyright. National MI Cautionary Note Regarding Forward- Looking Statements This presentation contains forward-looking

NMI Holdings, Inc. (NMIH) Sanford C. Bernstein Investor Presentation May 14, 2014 2014 Copyright. National MI Cautionary Note Regarding Forward- Looking Statements This presentation contains forward-looking

March 29, Federal Housing Finance Agency Office of Housing and Regulatory Policy th St., SW, 9 th Floor Washington, D.C.

Federal Housing Finance Agency Office of Housing and Regulatory Policy 400 7 th St., SW, 9 th Floor Washington, D.C. 20219 RE: Credit Score Request for Input Dear Sir or Madam: On behalf of the National

Federal Housing Finance Agency Office of Housing and Regulatory Policy 400 7 th St., SW, 9 th Floor Washington, D.C. 20219 RE: Credit Score Request for Input Dear Sir or Madam: On behalf of the National

April 2018 Data Release

April 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the National

April 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the National

The Way to Greater Efficiency. Correspondent Lending

The Way to Greater Efficiency Correspondent Lending High-level service and partnership that uniquely leverages technology, processes and people to ensure effi cient and timely loan purchases Meeting the

The Way to Greater Efficiency Correspondent Lending High-level service and partnership that uniquely leverages technology, processes and people to ensure effi cient and timely loan purchases Meeting the

January 2018 Data Release

January 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the

January 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the

Lunchtime Data Talk. Housing Finance Policy Center. Mortgage Origination Pricing and Volume: More than You Ever Wanted to Know

Housing Finance Policy Center Lunchtime Data Talk Mortgage Origination Pricing and Volume: More than You Ever Wanted to Know Frank Nothaft, Freddie Mac Mike Fratantoni, Mortgage Bankers Association October

Housing Finance Policy Center Lunchtime Data Talk Mortgage Origination Pricing and Volume: More than You Ever Wanted to Know Frank Nothaft, Freddie Mac Mike Fratantoni, Mortgage Bankers Association October

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

Principles of Mortgage Lending Secondary Marketing MICHAEL WILBERTON VP CAPITAL MARKETS OFFICER, HARBORONE BANK

Principles of Mortgage Lending Secondary Marketing MICHAEL WILBERTON VP CAPITAL MARKETS OFFICER, HARBORONE BANK Executive Summary History of Secondary Marketing Key Participants in the Secondary Market

Principles of Mortgage Lending Secondary Marketing MICHAEL WILBERTON VP CAPITAL MARKETS OFFICER, HARBORONE BANK Executive Summary History of Secondary Marketing Key Participants in the Secondary Market

January 2019 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data

Data") September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

THC Asset-Liability Management (ALM) Insight Issue 5

Insight Issue 5") , WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

, WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-01 HUD: FHA has announced

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-01 HUD: FHA has announced

Principles of Mortgage Lending Secondary Marketing

Principles of Mortgage Lending Secondary Marketing DAN MCKENNEY PRESIDENT/CEO, MERRIMACK MORTGAGE COMPANY MARIO A. GOMEZ VP SECONDARY OFFICER, HARBORONE BANK Agenda History of Secondary Marketing Key Participants

Principles of Mortgage Lending Secondary Marketing DAN MCKENNEY PRESIDENT/CEO, MERRIMACK MORTGAGE COMPANY MARIO A. GOMEZ VP SECONDARY OFFICER, HARBORONE BANK Agenda History of Secondary Marketing Key Participants

What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from Recent Fannie Mae Acquisitions

What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from Recent Fannie Mae Acquisitions Qiang Cai and Sarah Shahdad, Economic & Strategic Research Published 4/13/2015 Prospective homebuyers

What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from Recent Fannie Mae Acquisitions Qiang Cai and Sarah Shahdad, Economic & Strategic Research Published 4/13/2015 Prospective homebuyers

Welcome to our Mortgage Fundamentals CE Class!

Welcome to our Mortgage Fundamentals CE Class! 1 Mortgage Fundamentals CE Course, brought to you by: Mike Porter, President Red Diamond Home Loans mporter@rdhloans.com 817-832-8452 Justin Rogers Mortgage

Welcome to our Mortgage Fundamentals CE Class! 1 Mortgage Fundamentals CE Course, brought to you by: Mike Porter, President Red Diamond Home Loans mporter@rdhloans.com 817-832-8452 Justin Rogers Mortgage

An Update on the Evolution of the Mortgage Origination Process 9

Mikhail Teytel (212) 816-8465 mikhail.teytel@ssmb.com An Update on the Evolution of the Mortgage Origination Process 9 One of the reasons for the rise in refinancing efficiency in 2001 is a continuing

Mikhail Teytel (212) 816-8465 mikhail.teytel@ssmb.com An Update on the Evolution of the Mortgage Origination Process 9 One of the reasons for the rise in refinancing efficiency in 2001 is a continuing

The Return of Private Capital

The Return of Private Capital October 14, 2014 Private investor share of the U.S. mortgage market has declined since the financial crisis; however, private investors hold market risk on more than 75 percent

The Return of Private Capital October 14, 2014 Private investor share of the U.S. mortgage market has declined since the financial crisis; however, private investors hold market risk on more than 75 percent

The Office of Economic Policy HOUSING DASHBOARD. March 16, 2016

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

October 2016 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Credit Underwriting Practices

Comptroller of the Currency Administrator of National Banks US Department of the Treasury 2011 Survey of OF THE R C LE UR R EN C Y CO M P T R O L Credit Underwriting Practices 186 3 Contents Introduction...

Comptroller of the Currency Administrator of National Banks US Department of the Treasury 2011 Survey of OF THE R C LE UR R EN C Y CO M P T R O L Credit Underwriting Practices 186 3 Contents Introduction...

PennyMac Correspondent Group Overlays, February 25, 2019 X Indicates Overlay

PennyMac Correspondent Group Overlays, February 25, 2019 Indicates Overlay GOVERNMENT FHA Full doc FHA Streamline VA Full Doc VA IRRRL Rural Housing Topic Overlay/Modification 203(k) Specific PennyMac

PennyMac Correspondent Group Overlays, February 25, 2019 Indicates Overlay GOVERNMENT FHA Full doc FHA Streamline VA Full Doc VA IRRRL Rural Housing Topic Overlay/Modification 203(k) Specific PennyMac

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Issue Date 12/10/18 Effective Date As Noted GA

updates and Conforming Product Suite Purpose This announcement includes the following topic: Federal Housing Finance Agency (FHFA) new loan limits Pricing and Funding FHLMC Rental Income Amendments FHLMC

updates and Conforming Product Suite Purpose This announcement includes the following topic: Federal Housing Finance Agency (FHFA) new loan limits Pricing and Funding FHLMC Rental Income Amendments FHLMC

7.1 Genworth-Insured Refinance Program (04/03/09)

") Genworth Mortgage Insurance 7.1 Genworth-Insured Refinance Program (04/03/09) The Genworth-Insured Refinance Program provides expanded underwriting guidelines for rate/term refinances of Genworth-insured

Genworth Mortgage Insurance 7.1 Genworth-Insured Refinance Program (04/03/09) The Genworth-Insured Refinance Program provides expanded underwriting guidelines for rate/term refinances of Genworth-insured

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Survey of Credit Underwriting Practices 2010

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1 SLIDE 1 COVER PAGE SLIDE 2 TOPICS In this section we will cover the following topics: I. Conventional mortgages II. III.

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1 SLIDE 1 COVER PAGE SLIDE 2 TOPICS In this section we will cover the following topics: I. Conventional mortgages II. III.

Prospects for Housing Finance Reform and A Plan for Eliminating Fannie Mae and Freddie Mac without Legislation. March 5, 2018

Prospects for Housing Finance Reform and A Plan for Eliminating Fannie Mae and Freddie Mac without Legislation March 5, 2018 Edward Pinto pintoedward1@gmail.com Co-director, Center on Housing Markets and

Prospects for Housing Finance Reform and A Plan for Eliminating Fannie Mae and Freddie Mac without Legislation March 5, 2018 Edward Pinto pintoedward1@gmail.com Co-director, Center on Housing Markets and

What Do Consumers Know About The Mortgage Qualification Criteria?

Fannie Mae 2015 Mortgage Qualification Research What Do Consumers Know About The Mortgage Qualification Criteria? Economic & Strategic Research Group December 2015 Disclaimer The analyses, opinions, estimates,

Fannie Mae 2015 Mortgage Qualification Research What Do Consumers Know About The Mortgage Qualification Criteria? Economic & Strategic Research Group December 2015 Disclaimer The analyses, opinions, estimates,

What To Digitize First, According To Recent Homebuyers

What To Digitize First, According To Recent Homebuyers National Housing Survey Topic Analysis Q1 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Borrowers Want Less Paperwork! Recent homebuyers are most

What To Digitize First, According To Recent Homebuyers National Housing Survey Topic Analysis Q1 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Borrowers Want Less Paperwork! Recent homebuyers are most

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Unders

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Understanding Credit Programs Impact of TRID (TILA Respa

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Understanding Credit Programs Impact of TRID (TILA Respa

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.3 Oct. 23, 2018 Updated Oct. 31, 2018 During the weekend of Dec. 8, 2018, Fannie Mae will implement Desktop Underwriter (DU ) Version

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.3 Oct. 23, 2018 Updated Oct. 31, 2018 During the weekend of Dec. 8, 2018, Fannie Mae will implement Desktop Underwriter (DU ) Version

Overview of Types of Mortgages Available

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18 Jerry Flach (973) 305-8800 x 4252 gflach@valleynationalbank.com Sofi Cordero (973) 305-8800 x 8884 scordero@valleynationalbank.com

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18 Jerry Flach (973) 305-8800 x 4252 gflach@valleynationalbank.com Sofi Cordero (973) 305-8800 x 8884 scordero@valleynationalbank.com

With all the borrowing that we do today, it is hard to believe that prior to the 1930s,

Hit the Books Instructions: As you read, trace over the words that are shaded and underlined. This will help you to understand and retain important information. With all the borrowing that we do today,

Hit the Books Instructions: As you read, trace over the words that are shaded and underlined. This will help you to understand and retain important information. With all the borrowing that we do today,

September 2015 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13