Open economy macroeconomics and exchange rates Part I

|

|

|

- Phoebe Woods

- 5 years ago

- Views:

Transcription

1 Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr

2 Lecture 10 : Open economy macroeconomics and exchange rates Part I 1. Balance of payments (BOP) 2.Exchangerateinthelongrun:PPP 3. BOP Theory of Exchange Rates

3 Open economy national income identities National Accounting Y= C + I + G + EX -IM Y: GDP C: Consumption I: Investment G: public spending EX: Exports of goods and services IM: Imports Current account (sometimes net exports): CA= EX-IM

4 The Fundamental Balance of Payments Identity National Revenue = National Output National output (Y) is: Y I + C + G + [EX IM] with EX IMP = CA = Current Account Balance The use of national revenues : Y C + S P + T Then: (I S P ) + (G T) + (EX IMP) 0 Introducing Public Savings (Fiscal Surplus): S G =T-G CA S P + S G - I S-I

5 The Fundamental Balance of Payments Identity CA S P + S G - I S-I Accounting identity (no behaviour, no explanation, no theory here) A country whose savings exceed national investment tends to run a current account surplus : the country is lending to the rest oftheworld A current account deficit can reflect: - Small saving rate (high consumption) (US from 2000) - High investment(us ) - Budget deficit(us since 2001)

6 A bit more of accounting Balance of Payments (BOP) - Registers all transactions with foreign economic agents - 3 main sorts of transactions: - exports and imports of goods and services current account (CA) -sale and purchase of financial assets financial account (FA) - certain transfers of wealth (small) capital account (KA)

7 The Balance of Payments The Balance of Payments (BOP) = Current Account + Financial Account + Capital Account The Balance of Payments has to balance: BOP = 0 (abstracting from errors and omissions)

8 Why does the balance of payments have to balance? Essentially an accounting trick - every credit needs to be matched by a debit: double entry book keeping principle! The current account shows overall situation in transactions of goods and services. The capital and financial account shows how this is financed. Consider the case of the U.K running a current account deficit, in otherwordstheu.kcannotpayitsimportbillfromexportsalone. One solution is for the U.K to sell any overseas assets and use the money to pay the import bill. Another option would be to sell some U.K companies which would count as Inward Direct Investment. This would create a financial account surplus equal to the current account deficit.

9 The Current Account Trade Balance= Exports of Goods and Services -Imports of Goods and Services = (X-M) Current Account=Balance on Goods and Services + Net Foreign Workers Remittances + Net International Aid+ Net Royalties + Net Investment Income = (X-M+NFI)

10 The Financial & Capital Accounts Financial account (FA): records flow of financial assets. These are Foreign Direct Investment, Net Portfolio Flows and Net Other(mainly bank loans and trade credits) Capital account (KA): records flow of non-financial assets between countries debt forgiveness, purchase of royalty rights However because of measurement error also a category called errors and omissions

11 French Balance of Payments (EUR, millions, 2013) Current Account Balance of Trade Balance of Services Capital Account Financial Account Net FDI Net Portfolio Primary & secondary income bal Net Other (incl. derivatives) Errors and Omissions

12 China Balance of Payments ($bn H1 2009) Balance of Trade 118 Net FDI, Private and Official Assets Balance of Services -19 Reserves -186 NFI 31 Statistical Discrepancies Current Account 130 Financial Account -129 Capital Account -1 Total Balance (CA+FA+KA) 0

13 Lecture 10 : Open economy macroeconomics and exchange rates Part I 1. Balance of payments(bop) 2. Exchange rate in the long run: PPP 3. BOP Theory of Exchange Rates

14 The nominal exchange rate Two types of quotation: E is the exchange rate of the euro/dollar: price of the foreign currency (dollar) in units of the domestic currency (euro) 1 $ = E E increases means euro depreciates (it takes more euros to buy one dollar) E is the price of the domestic currency (euro) in units of the foreign currency (dollar) 1 = E $ In the following, we use the first(more standard, although not most intuitive) convention: E increases means the euro depreciates

15 Price conversion P i $ : price of good iin dollar E is the exchange rate (nbof euros to make one $) P i price of good iconverted in euro P i = E. P i $ Remark: A depreciation of the euro (E ) increases the price in euro of an American good (if the producer price P i $ does not react). Decreases the price in $ of a European good (if the producer price in euro does not change).

16 Floating and fixed exchange rate regimes Floating: The exchange rate is determined on exchange rate markets without interventions of central banks(euro/dollar) Fixed : Central banks intervene on markets to maintain the exchange rate at an announced level or around such a level (Gold standard at the end of 19th century, FF/DM, Bretton Woods system until 1971, certain developing and emerging countries) Many intermediate situations Mostly focus on floating for now.

17 The Yen and Euro Nominal Exchange Rate Nominal Exchange Rate = number of yen or euros that could be purchased with one dollar

18 31/01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ /09/ /01/ /05/ The Argentine Peso Nominal Exchange Rate Devaluation of the Peso Fixed Exchange rate Regime: 1 peso =1 $ An example of fixed exchange-rate: the Currency Board in Argentina in the nineties

19 The law of one price (LOP) Long term perspective on exchange rates = when prices are flexible On competitive markets, in absence of transport costs and tariffs twoidenticalgoodsmustbesoldatthesameprice (expressed in the same currency) Consideragoodindexedbyi. LawofonePrice=longtermarbitragemechanism P i = E. P i $ IfP i >E.P i$ :buytheusproducedgood,sellitineurope; increase demand in US, increase supply in Europe: price converge

20 Purchasing power parity (PPP) Idea developed initially by Ricardo ( ) The price levels of different countries are equalized when measured in the same currency: P = E x P $ where P and P $ are price indices of US and euro zone. E = P / P $ : Absolute version of PPP An increase in the general level of prices reduces purchasing power of domestic currency and leads to a depreciation. PPP (nominal) exchange rate: E PPP = P / P $

21 The PPP exchange rate: E PPP ( /$) = P / P $ P / P $ $ undervalued, overvalued $overvalued, undervalued 45 Nominal Exchange rate ( /$)

22 Relative PPP The variation of the exchange rate is equal to the difference in the variation in prices, the difference in inflation rates (approximation) E t = P t / P $t (E t E t-1 )/E t-1 π t -π $t π t and π $t : inflation in zone and US π t = (P t P t-1 )/ P t-1

23 Empirical validity of the LOP LOP fails in short run : not puzzling for non traded goods (haircuts); but also for traded goods. Transport costs, trade barriers (tariffs and regulations): make arbitrage more difficult. Imperfect competition: firms segment markets (to have high prices where price elasticity of demand is low) : pricing to market. Branding. Many goods considered to be highly traded contain nontraded components. Retail and wholesale costs (distribution costs) account for around 50% of final consumer price.

24 Empirical validity of PPP Studies overwhelmingly reject PPP as a short-run relationship, better as long term. The variance of floating nominal exchange rates is an order of magnitude greater than the variance of relative price indices. The failure of short-run PPP can be attributed partly to the stickiness in nominal prices(short run). Worksmuchbetterinthelongterm.

25 What is the exchange rate of country i consistent with LOP for the Big Mac? Required appreciation or depreciation to satisfy LOP? E Big Mac = P US /P i The Economist - Oct. 2010

26 Long term real exchange rate Real exchange rate (RER) defined as the relative price index of goods and services between two countries: q = E x P $ / P A real depreciation of vis-à-vis the $ (q )can come from nominal depreciation (E ), an increase in P $ or a fall in P Relative PPP RER is constant! PPP: (E t E t-1 )/E t-1 = π t -π $t (q t q t-1 )/q t-1 = (E t E t-1 )/E t-1 + π $t -π t = 0

27 Long Run PPP: $/ real exchange rate (in logs) 0.5 The mean reversion of real exchange rates overvalued relative to PPP undervalued relative to PPP Note: Higher values means a (real) dollar depreciation (or a appreciation)

28 The Yen/$ exchange rate and the relative priceratio over the long term

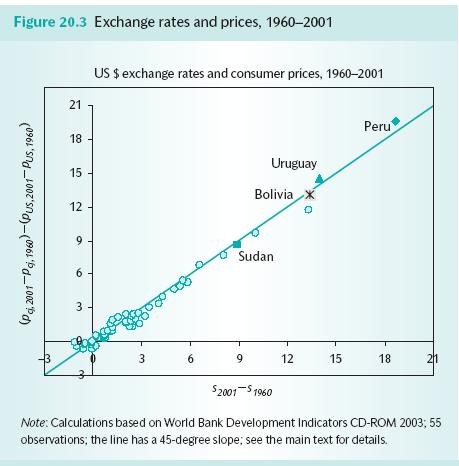

29 Empiricaltest of relative PPP in the long-run Looking across countries over a long time period [1960;2001], run the following regression where(i) is a country: log S S i/ us 2001 i/ us 1960 log P P i 2001 i 1960 log P P us 2001 us 1960 t 1 RelativePPPassumption:βisexpecttobe=1(andα=zero). Can inflation differentials over 41 years explain exchange rate variations over the same period? βisfairlyclosetooneforthissampleofcountries. Convergence towards PPP: slow reversion towards PPP(from 3 to 5yearstoeliminatehalfofthegap).

30

31 Relative PPP prevails in the very long-run but fails in the short-run %Depreciation 60 1 Year Window %Depreciation Inflation differential %Depreciation Inflation Differential Inflation Differential 20 Year Window Remember relative PPP: (E t E t-1 )/E t-1 = π t -π $t 5 Year Window

32 Why are prices higher in rich countries? Same question as: why E x P rich > P poor? Obvious deviation from PPP. Relatedquestion:whydoes the realexchange rate of countries that grow relative to rest of world appreciate?(q=exp world /P ) Examples: Japan, South Korea, Ireland, today China? One theory relies on the presence of non-traded goods together with productivity differences between rich and poor in the traded(manufacturing) sector = Balassa Samuelson effect

33

34 Balassa-Samuelson effect Key distinction: Tradable goods (manufactured goods) and non tradable(services) Around 75% of the consumption basket in industrialized countries is non tradable (health, education, most services ) even if definition of a tradable good/service becomes blurred (internet) Productivity differences between rich and poor countries is much larger for tradables than for non tradables: it is very large for example in manufacturing (of an order of 10 or more), but much smaller in services (think of haircuts: technology is not hugely different across countries).

35 Understanding the Balassa-Samuelson effect Workers can be hairdressers (non-traded) or work in the textile industry (traded). Workers can produce haircuts or T-shirts. T-shirts sold 1$ in international markets. US worker produces 50 T-shirts/hour, Indian worker only 10. Both US and Indian hairdressers make 5 haircuts/ hour. Question: what is the price of an haircut in India and in the US? Implications?

36 Income convergence and exchange rate appreciation(here appreciation is up!) Source: Reisen, 2009

37 Lecture 10 : Open economy macroeconomics and exchange rates Part I 1. Balance of payments(bop) 2.Exchangerateinthelongrun:PPP 3. BOP Theory of Exchange Rates

38 BOP theory of exchange rates Develop a simple framework to examine how the current account and exchange rate of a country is affected by various macroeconomic events to explain some of the medium term deviations from PPP documented in the section.

39 The role of exchange rate But while the National Accounts show that: How does this happen? CA = S-I Variations in the real exchange rate ensure that current account equals net savings.

40 The Current Account Focus on flexible exchange rates Two country model: Europe-US. CA = CA(q, Y d, Y $d ) q = E P $ /P : real exchange rate; relative priceof US goods with respect to European goods q : real depreciationof euro

41 The Current Account CA = EX -IM in euros = Net exports in euros Suppose E (or equivalently q ): How do exports (foreign demand for European goods) and imports (European demand for foreign goods) react? Depends on two main factors: 1) In which currency exporters fix their prices? How much pass-through of exchange rates to consumer prices? 2) How large is the elasticity of substitution between domestic and foreign goods?

42 The Current Account If q volume of imports, exports : substitution But if slow response of volumes(empirically 6 months-1 year): valueofimports volume versus value effect. In short term, the value effect can dominate NeteffectontheCAofq? J-curve--- in the short-term, a real exchange rate depreciation worsens the current account but in the medium-term (under some conditions), the substitution effect dominates and the current account improves.

43 The J-Curve volume effect dominates value effect Immediate effect of real depreciation on the CA J-curve: value effect dominates volume effect

44 The Current Account We assume from now on: nominal or real depreciabon (E or q ) generates an in demand via an in net exports : CA (q)= (EX -IM ) +

45 The Current Account q High real exchange rate means European goods cheaper so Europe export more and import less -net exports increases with q 0 CA=Net Exports

46 BOP Theory of Exchange Rates q S-I CA=Net Exports Real Exchange Rate determined by equality of net savings with net exports

47 BOP Theory of Exchange Rates A depreciation of real exchange rate means domestic goods are more competitive on international markets. Real exchange rate adjusts to ensure net exports equals net savings. If net savings > net exports, then real exchange rate depreciates which decreases imports and boosts exports. Eventually net exports equal net savings.

48 Increase in fiscal deficits (fall in public savings) q S-I CA=Net Exports Appreciation of the currency and deterioration of the current account

49 Reagan and Bush I Deficits 6 5 % of GDP Current Account deficit Fiscal deficit 5 % of GDP Source : Bureau of Economic Analysis

50 Drop in investment q S-I CA=Net Exports Depreciation of the currency and improvement of the current account

51 Argentina Financial Crisis Current Account (% of GDP) Investment rate % of GDP Real GDP Growth

52 Increase in demand for European goods q S-I CA=Net Exports

53 Summary In the long-term, changes in nominal exchange rates reflect differences in inflation as predicted by relative purchasing power parity. Failures of PPP are due to price rigidities, barriers to international trade, pricingto-market. Due to the Balassa Samuelson effect, poor countries have lower prices and face appreciating real exchange rates when catching-up in terms of productivity. In the medium to long-term, the real exchange rate will adjust to a level where the current account surplus/deficit matches longer term capital flows.

Open economy macroeconomics and exchange rates Part I

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Long term exchange rate and inflation

International Finance Master in International Economic Policy Long term exchange rate and inflation Lectures 5 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Motivation and roadmap What are the

International Finance Master in International Economic Policy Long term exchange rate and inflation Lectures 5 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Motivation and roadmap What are the

International Finance

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

LECTURE 10: Purchasing Power Parity

LECTURE 10: Purchasing Power Parity Primary Motivation: How realistic is the assumption P = P? Secondary motivation: How integrated are global goods markets? (1) Definition(s) of PPP (Absolute vs. Relative

LECTURE 10: Purchasing Power Parity Primary Motivation: How realistic is the assumption P = P? Secondary motivation: How integrated are global goods markets? (1) Definition(s) of PPP (Absolute vs. Relative

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

6 The Open Economy. This chapter:

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

10/14/2011. EXCHANGE RATES I: PPP and THE MONETARY APPROACH IN THE LONG RUN. Introduction to Exchange Rates and Prices

EXCHANGE RATES I: PPP and THE MONETARY APPROACH IN THE LONG RUN 14 1 Exchange Rates and Prices in the Long Run 2 Money, Prices, and Exchange Rates in the Long Run 3 The Monetary Approach 4 Money, Interest,

EXCHANGE RATES I: PPP and THE MONETARY APPROACH IN THE LONG RUN 14 1 Exchange Rates and Prices in the Long Run 2 Money, Prices, and Exchange Rates in the Long Run 3 The Monetary Approach 4 Money, Interest,

The Open Economy. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

Consumption expenditure The five most important variables that determine the level of consumption are:

The aggregate expenditure model: A macroeconomic model that focuses on the relationship between total spending and real GDP, assuming the price level is constant. Macroeconomic equilibrium: AE = GDP Consumption

The aggregate expenditure model: A macroeconomic model that focuses on the relationship between total spending and real GDP, assuming the price level is constant. Macroeconomic equilibrium: AE = GDP Consumption

Lecture 5: Intermediate macroeconomics, autumn 2014

Lecture 5: Intermediate macroeconomics, autumn 2014 Lars Calmfors Literature: Krugman Obstfeld Melitz, chapters 16 and 17. 1 1 Topics Absolute and relative purchasing power parity (PPP) The Balassa-Samuelson

Lecture 5: Intermediate macroeconomics, autumn 2014 Lars Calmfors Literature: Krugman Obstfeld Melitz, chapters 16 and 17. 1 1 Topics Absolute and relative purchasing power parity (PPP) The Balassa-Samuelson

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom The final exam is comprehensive. The best way to prepare is to review tests 1 and 2, the reviews for Test 1 and Test 2, and the Aplia

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom The final exam is comprehensive. The best way to prepare is to review tests 1 and 2, the reviews for Test 1 and Test 2, and the Aplia

Chapter 19 MONEY SUPPLIES, PRICE LEVELS, AND THE BALANCE OF PAYMENTS

Chapter 19 MONEY SUPPLIES, PRICE LEVELS, AND THE BALANCE OF PAYMENTS In the Keynesian model, the international transmission of shocks took place via the trade balance, with changes in national income or

Chapter 19 MONEY SUPPLIES, PRICE LEVELS, AND THE BALANCE OF PAYMENTS In the Keynesian model, the international transmission of shocks took place via the trade balance, with changes in national income or

Chapter 6. The Open Economy

Chapter 6 0 IN THIS CHAPTER, YOU WILL LEARN: accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies

Chapter 6 0 IN THIS CHAPTER, YOU WILL LEARN: accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies

Final exam Non-detailed correction 3 hours

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

Chapter 16. Price Levels and the Exchange Rate in the Long Run

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Economic Policy in PNG:

Economic Policy in PNG: 2010-2020 Institute of National Affairs 30 June 2016 Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National

Economic Policy in PNG: 2010-2020 Institute of National Affairs 30 June 2016 Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

Macroeconomics I International Group Course

Macroeconomics I International Group Course 2004-2005 Topic 7: SAVINGS AND INVESTMENT IN THE OPEN ECONOMY Learning objectives We now start the study of the open economy. This brings into the analysis of

Macroeconomics I International Group Course 2004-2005 Topic 7: SAVINGS AND INVESTMENT IN THE OPEN ECONOMY Learning objectives We now start the study of the open economy. This brings into the analysis of

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

EconS 327 Review for Test 2

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

The Open Economy. Inflation Worth Publishers, all rights reserved CHAPTER 5

6 The Open Economy Inflation CHAPTER 5 Modified by Ming Yi 2016 Worth Publishers, all rights reserved 5 IN THIS CHAPTER, YOU WILL LEARN: Accounting identities for the open economy The small open economy

6 The Open Economy Inflation CHAPTER 5 Modified by Ming Yi 2016 Worth Publishers, all rights reserved 5 IN THIS CHAPTER, YOU WILL LEARN: Accounting identities for the open economy The small open economy

internationa macroeconomics

internationa macroeconomics ROBERT C. FEENSTRA ALAN M.TAYLOR University WORTH PUBLISHERS Contents Preface XVII CHAPTER 1 The Globai Macroeconomy 1 PART 1 1 Foreign Exchange: Of Currencies and Crises 2,.

internationa macroeconomics ROBERT C. FEENSTRA ALAN M.TAYLOR University WORTH PUBLISHERS Contents Preface XVII CHAPTER 1 The Globai Macroeconomy 1 PART 1 1 Foreign Exchange: Of Currencies and Crises 2,.

01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date

Turkish Lira Example British Pound 0 1.0e+06 2.0e+06 3.0e+06 4.0e+06 5.0e+06 01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date British Pound British Pound Ozan Hatipoglu (Department

Turkish Lira Example British Pound 0 1.0e+06 2.0e+06 3.0e+06 4.0e+06 5.0e+06 01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date British Pound British Pound Ozan Hatipoglu (Department

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Exchange Rate Fluctuations Revised: January 7, 2012

The Global Economy Class Notes Exchange Rate Fluctuations Revised: January 7, 2012 Exchange rates (prices of foreign currency) are a central element of most international transactions. When Heineken sells

The Global Economy Class Notes Exchange Rate Fluctuations Revised: January 7, 2012 Exchange rates (prices of foreign currency) are a central element of most international transactions. When Heineken sells

Associate reading: Krugman-Obstfeld chapter 15 p , p

3 Lecture 3: The determinants of the real exchange rate Associate reading: Krugman-Obstfeld chapter 15 p. 369-373, p. 379-393 Intertemporal theory of the current account: what determines international

3 Lecture 3: The determinants of the real exchange rate Associate reading: Krugman-Obstfeld chapter 15 p. 369-373, p. 379-393 Intertemporal theory of the current account: what determines international

International Macroeconomics

Slides for Chapter 9: Determinants of the Real Exchange Rate International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University April 8, 2018 1 The LOOP LOOP stands for the Law of One Price.

Slides for Chapter 9: Determinants of the Real Exchange Rate International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University April 8, 2018 1 The LOOP LOOP stands for the Law of One Price.

Macroeconomics II. The Open Economy

Macroeconomics II The Open Economy Vahagn Jerbashian Ch. 5 from Mankiw (2010, 2003) Spring 2018 Where we are and where we are heading to So far we have considered closed economy no trade with other countries

Macroeconomics II The Open Economy Vahagn Jerbashian Ch. 5 from Mankiw (2010, 2003) Spring 2018 Where we are and where we are heading to So far we have considered closed economy no trade with other countries

Economics of International Financial Policy: ITF 220

Economics of International Financial Policy: ITF 220 Staff -- Professor: Jeffrey Frankel, Littauer 217 Office hours: Mon.& Tues., 3:00-4:00. Faculty Asst.: Minoo Ghoreishi, Belfer 505 (617) 384-7329 Teaching

Economics of International Financial Policy: ITF 220 Staff -- Professor: Jeffrey Frankel, Littauer 217 Office hours: Mon.& Tues., 3:00-4:00. Faculty Asst.: Minoo Ghoreishi, Belfer 505 (617) 384-7329 Teaching

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 2. Deadline: March 1st.

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Chapter 11 An Introduction to International Finance Adapted by H. Dellas

Chapter 11 An Introduction to International Finance Adapted by H. Dellas Topics to be Covered Foreign accounts-balance of payments Exchange rates-exchange rate markets Prices and exchange rates Interest

Chapter 11 An Introduction to International Finance Adapted by H. Dellas Topics to be Covered Foreign accounts-balance of payments Exchange rates-exchange rate markets Prices and exchange rates Interest

The Balance of Payments. Balance of Payments. Balance of Payments Accounts. Balance of Payments Accounts. They are composed of the following:

The Balance of Payments Chapter Objective: This chapter serves to introduce the student to the balance of payments, how it is constructed and how balance of payments data may be interpreted. Chapter Outline

The Balance of Payments Chapter Objective: This chapter serves to introduce the student to the balance of payments, how it is constructed and how balance of payments data may be interpreted. Chapter Outline

International Finance

Terminology International Finance Chris Edmond NYU Stern Spring 2008 Trade balance balance on merchandise trade ( goods ) balance on goods and services ( net exports ) Current account balance current account

Terminology International Finance Chris Edmond NYU Stern Spring 2008 Trade balance balance on merchandise trade ( goods ) balance on goods and services ( net exports ) Current account balance current account

Global Business Economics. Mark Crosby SEMBA International Economics

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Policy Discussion Assignment 1

Management 495 Spring 2016 Topics in Finance: International Macroeconomics Policy Discussion Assignment 1 April 6, 2016 Due: Instructor: E-mail: Wed, April 27, before 9:30am Marc-Andreas Muendler muendler@ucsd.edu

Management 495 Spring 2016 Topics in Finance: International Macroeconomics Policy Discussion Assignment 1 April 6, 2016 Due: Instructor: E-mail: Wed, April 27, before 9:30am Marc-Andreas Muendler muendler@ucsd.edu

Global Environment. The Real Exchange Rate. Francesco Franco. October 22, Nova SBE. Francesco Franco Global Environment 1/28

Global Environment The Real Exchange Rate Francesco Franco Nova SBE October 22, 2014 Francesco Franco Global Environment 1/28 Long Run What explains the long run behavior of exchange rates? Figure : Yen-Dollar

Global Environment The Real Exchange Rate Francesco Franco Nova SBE October 22, 2014 Francesco Franco Global Environment 1/28 Long Run What explains the long run behavior of exchange rates? Figure : Yen-Dollar

Objectives of the lecture

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

Period 3 MBA Program January February MACROECONOMICS IN THE GLOBAL ECONOMY Core Course. Professor Ilian Mihov

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Effects of CNY Revaluation on Mongolian Economy

PUBPOL542 International Financial Policy April 10, 2006 Prof. Kathryn Dominguez Course Group Project Effects of CNY Revaluation on Mongolian Economy Jinho Choi (UMID # 82989456, irobot@umich.edu) Ariunkhishig

PUBPOL542 International Financial Policy April 10, 2006 Prof. Kathryn Dominguez Course Group Project Effects of CNY Revaluation on Mongolian Economy Jinho Choi (UMID # 82989456, irobot@umich.edu) Ariunkhishig

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY

ECO41 FALL 2015 UDAYAN ROY") HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Purchasing Power Parity dr Bartłomiej Rokicki Purchasing power parity is derived from law of one

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Purchasing Power Parity dr Bartłomiej Rokicki Purchasing power parity is derived from law of one

Chapter 18 Exchange Rate Theories (modified version)

") Chapter 18 Exchange Rate Theories (modified version) Topics to be covered Exchange Rate Determination 1. The Elasticities Approach 2. The Asset Approach 2a. The Monetary Approach to the Exchange Rate 2b.

Chapter 18 Exchange Rate Theories (modified version) Topics to be covered Exchange Rate Determination 1. The Elasticities Approach 2. The Asset Approach 2a. The Monetary Approach to the Exchange Rate 2b.

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Answers to Questions: Chapter 7

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

Money, interest rates and nominal exchange rates

International Finance Master in International Economic Policy Money, interest rates and nominal exchange rates Lectures 3-4 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 3 and 4 Money,

International Finance Master in International Economic Policy Money, interest rates and nominal exchange rates Lectures 3-4 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 3 and 4 Money,

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity y( (also called the Law of

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al)

") Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Chapter 1: The Balance of Payments (BoP)

") Chapter 1: The Balance of Payments (BoP) 2: Definition and Rules 2.1 Overview 2.2 Current Account 2.3 Capital Account 2.4 Financial Account 2.5 Balance-of-Payments Equilibrium 2.6 Net Errors and Omissions

Chapter 1: The Balance of Payments (BoP) 2: Definition and Rules 2.1 Overview 2.2 Current Account 2.3 Capital Account 2.4 Financial Account 2.5 Balance-of-Payments Equilibrium 2.6 Net Errors and Omissions

Introduction to Exchange Rates and the Foreign Exchange Market

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

LECTURE XIV. 31 July Tuesday, July 31, 12

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

Chapter 16: Payments among Nations

Chapter 16: Payments among Nations Accounting Principles The balance of payments (BOP) is an accounting of a country's international transactions for a particular time period Double-entry accounting. Each

Chapter 16: Payments among Nations Accounting Principles The balance of payments (BOP) is an accounting of a country's international transactions for a particular time period Double-entry accounting. Each

INTERNATIONAL FINANCE TOPIC

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

Econ 340. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Outline: Exchange Rates

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

ECO 209Y MACROECONOMIC THEORY AND POLICY. Term Test #2. December 13, 2017

ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 December 13, 2017 U of T E-MAIL: @MAIL.UTORONTO.CA SURNAME (LAST NAME): GIVEN NAME (FIRST NAME): UTORID (e.g., LIHAO118): INSTRUCTIONS: The total time

ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 December 13, 2017 U of T E-MAIL: @MAIL.UTORONTO.CA SURNAME (LAST NAME): GIVEN NAME (FIRST NAME): UTORID (e.g., LIHAO118): INSTRUCTIONS: The total time

THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

Open economy macroeconomics and exchange rates Part II

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part II Lecture 11 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 11 : Open

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part II Lecture 11 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 11 : Open

Open Economy Macroeconomics Lecture Notes

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

18 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

18 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

INTERNATIONAL FINANCE. Objectives. Financing International Trade. Financing International Trade. Financing International Trade CHAPTER

INTERNATIONAL 34 FINANCE CHAPTER Objectives After studying this chapter, you will able to Explain how international trade is financed Describe a country s balance of payments accounts Explain what determines

INTERNATIONAL 34 FINANCE CHAPTER Objectives After studying this chapter, you will able to Explain how international trade is financed Describe a country s balance of payments accounts Explain what determines

Money and Exchange rates

Macroeconomic policy Class Notes Money and Exchange rates Revised: December 13, 2011 Latest version available at www.fperri.net/teaching/macropolicyf11.htm So far we have learned that monetary policy can

Macroeconomic policy Class Notes Money and Exchange rates Revised: December 13, 2011 Latest version available at www.fperri.net/teaching/macropolicyf11.htm So far we have learned that monetary policy can

Money, prices and exchange rates in the long run

Money, prices and exchange rates in the long run Outline Part I: Money and inflation 1. Definition of money 2. Money supply and money demand 3. The neutrality of money 4. The dichotomy principle and its

Money, prices and exchange rates in the long run Outline Part I: Money and inflation 1. Definition of money 2. Money supply and money demand 3. The neutrality of money 4. The dichotomy principle and its

(welly, 2018)

") a) Use the hypothetical information provided below to record the South African balance of payments transactions, using the double entry bookkeeping procedure. [12] Background information provided in the

a) Use the hypothetical information provided below to record the South African balance of payments transactions, using the double entry bookkeeping procedure. [12] Background information provided in the

International Trade. International Trade, Exchange Rates, and Macroeconomic Policy. International Trade. International Trade. International Trade

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

National Income & Business Cycles

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

Economics 302 Intermediate Macroeconomic

Economics 302 Intermediate Macroeconomic Theory and Policy (Spring 2010) Lecture 22-25 Apr. 12-Apr. 21, 2010 Foreign Trade and the Exchange Rate Chapter 12 Outline Foreign trade and aggregate demand The

Economics 302 Intermediate Macroeconomic Theory and Policy (Spring 2010) Lecture 22-25 Apr. 12-Apr. 21, 2010 Foreign Trade and the Exchange Rate Chapter 12 Outline Foreign trade and aggregate demand The

Exchange Rates and International Finance

Exchange Rates and International Finance Week 12 Vivaldo Mendes Dep. of Economics Instituto Universitário de Lisboa 8 December 2017 (Vivaldo Mendes ISCTE-IUL ) Macroeconomics I (L0271) 8 December 2014

Exchange Rates and International Finance Week 12 Vivaldo Mendes Dep. of Economics Instituto Universitário de Lisboa 8 December 2017 (Vivaldo Mendes ISCTE-IUL ) Macroeconomics I (L0271) 8 December 2014

Economics 3422 Sample Midterm examination. Part A: Multiple-choice questions. Choose the best alternative. The total for Part A is 25 points.

Economics 3422 Sample Midterm examination Instruction: Put your name and PeopleSoft ID on the question sheets and the blue book. Put your answers in the blue book only. Turn in both at the end of the examination.

Economics 3422 Sample Midterm examination Instruction: Put your name and PeopleSoft ID on the question sheets and the blue book. Put your answers in the blue book only. Turn in both at the end of the examination.

TOPIC 9. International Economics

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Micro versus Macro PP542. National Income Accounts. Micro versus Macro (cont.) National Income Accounts: GNP. National Income Accounts: GNP (cont.

National Income Accounts: GNP. National Income Accounts: GNP (cont.") PP542 Accounting Issues the Balance of Payments (BOP) Micro versus Macro MICROECONOMICS examines how individuals, by pursuing their own interests, collectively determine how resources are used. The key

PP542 Accounting Issues the Balance of Payments (BOP) Micro versus Macro MICROECONOMICS examines how individuals, by pursuing their own interests, collectively determine how resources are used. The key

ECO 209Y MACROECONOMIC THEORY AND POLICY. Term Test #2. December 13, 2017

ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 December 13, 2017 U of T E-MAIL: @MAIL.UTORONTO.CA SURNAME (LAST NAME): GIVEN NAME (FIRST NAME): UTORID (e.g., LIHAO118): INSTRUCTIONS: The total time

ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 December 13, 2017 U of T E-MAIL: @MAIL.UTORONTO.CA SURNAME (LAST NAME): GIVEN NAME (FIRST NAME): UTORID (e.g., LIHAO118): INSTRUCTIONS: The total time

Chapter 13 Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy

Chapter 13 Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy 1 Goals of Chapter 13 Two primary aspects of interdependence between economies of different nations International

Chapter 13 Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy 1 Goals of Chapter 13 Two primary aspects of interdependence between economies of different nations International

University of Toronto July 21, 2010 ECO 209Y L0101 MACROECONOMIC THEORY. Term Test #2

Department of Economics Prof. Gustavo Indart University of Toronto July 21, 2010 SOLUTIONS ECO 209Y L0101 MACROECONOMIC THEORY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Department of Economics Prof. Gustavo Indart University of Toronto July 21, 2010 SOLUTIONS ECO 209Y L0101 MACROECONOMIC THEORY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Traded and non-traded goods

Traded and non-traded goods ECON4330 Spring 2013 Lecture 12A Asbjørn Rødseth University of Oslo April 22, 2013 Traded and non-traded goods April 22, 2013 1 / 16 Different market structures Mundell-Fleming

Traded and non-traded goods ECON4330 Spring 2013 Lecture 12A Asbjørn Rødseth University of Oslo April 22, 2013 Traded and non-traded goods April 22, 2013 1 / 16 Different market structures Mundell-Fleming

7) What is the money demand function when the utility of money for the representative household is M M

What is the money demand function when the utility of money for the representative household is M M") 1) The savings curve is upward sloping, because (a) high interest rates increase the future returns that households obtain from their savings. (b) high interest rates increase the opportunity cost of consuming

1) The savings curve is upward sloping, because (a) high interest rates increase the future returns that households obtain from their savings. (b) high interest rates increase the opportunity cost of consuming

Introduction to Macroeconomics M Problem set 4

T1 T2 Introduction to Macroeconomics M5 2015-16 Problem set 4 dollar appreciate from T1 to T2? 1. Nominal rate. Consider tables T1 and T2, taken from http://www.x-rates.com/. In T1, for instance, 1 can

T1 T2 Introduction to Macroeconomics M5 2015-16 Problem set 4 dollar appreciate from T1 to T2? 1. Nominal rate. Consider tables T1 and T2, taken from http://www.x-rates.com/. In T1, for instance, 1 can

David Youngberg ECON 201 Montgomery College LECTURE 08: TRADE I

David Youngberg ECON 201 Montgomery College LECTURE 08: TRADE I I. A trading game a. Trade increases aggregate utility. b. The Fundamental Theorem of Exchange voluntary trade with complete information

David Youngberg ECON 201 Montgomery College LECTURE 08: TRADE I I. A trading game a. Trade increases aggregate utility. b. The Fundamental Theorem of Exchange voluntary trade with complete information

What Are Equilibrium Real Exchange Rates?

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

Chapter 25 The Exchange Rate and the Balance of Payments The Foreign Exchange Market

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

Slides for International Finance Purchasing Power Parity

Purchasing Power Parity American University 2017-10-01 Preview Absolute vs. Relative Purchasing power parity Commodity price parity Absolute PPP vs. Relative PPP Classical model of price determination

Purchasing Power Parity American University 2017-10-01 Preview Absolute vs. Relative Purchasing power parity Commodity price parity Absolute PPP vs. Relative PPP Classical model of price determination

ECON Intermediate Macroeconomic Theory

ECON 322 - Intermediate Macroeconomic Theory Fall 2018 Mankiw, Macroeconomics, 8th ed., Chapter 6 Chapter 6: Open Economy Macroeconomics Key points: Know both sides of the trade balance - the current account

ECON 322 - Intermediate Macroeconomic Theory Fall 2018 Mankiw, Macroeconomics, 8th ed., Chapter 6 Chapter 6: Open Economy Macroeconomics Key points: Know both sides of the trade balance - the current account

Macro for SCS Nov. 29, International Trade & Finance

Macro for SCS Nov. 29, 2017 International Trade & Finance The Gains from Trade Do you believe in magic The Gains from Trade Leave the England-Portugal rivalry for the soccer field Criticism of the free

Macro for SCS Nov. 29, 2017 International Trade & Finance The Gains from Trade Do you believe in magic The Gains from Trade Leave the England-Portugal rivalry for the soccer field Criticism of the free

In this chapter, we study a theory of how exchange rates are determined "in the long run." The theory we will develop has two parts:

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 1. Name:

Rutgers University Spring 2013 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 1 Name: 1. When the exchange value of the euro rises in terms of the U.S. dollar, U.S. residents

Rutgers University Spring 2013 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 1 Name: 1. When the exchange value of the euro rises in terms of the U.S. dollar, U.S. residents

Homework Assignment #2: Answer Sheet

Econ 434 Professor Ickes Fall 2008 Homework Assignment #2: Answer Sheet. Suppose that the price level in the home country is given by P = Pn α Pt α,wherep t is the price of traded goods, and α is the share

Econ 434 Professor Ickes Fall 2008 Homework Assignment #2: Answer Sheet. Suppose that the price level in the home country is given by P = Pn α Pt α,wherep t is the price of traded goods, and α is the share

University of Karachi

International Economics INTERNATOINAL ECONOMICS (PAPER - II) M.A (FINAL) EXTERNAL ANNUAL EXAMINATION 1997 University of Karachi Time: 3 Hours Maximum Marks: 100 1) Attempt any five questions. 2) All questions

International Economics INTERNATOINAL ECONOMICS (PAPER - II) M.A (FINAL) EXTERNAL ANNUAL EXAMINATION 1997 University of Karachi Time: 3 Hours Maximum Marks: 100 1) Attempt any five questions. 2) All questions

ECON0302 International Finance Midterm Exam Fall 2004

ECON0302 International Finance Midterm Exam Fall 2004 Short Questions (60 points each) 1. If in ation in the US is projected at 2:5% annually for the next 3 years and at 0:9% annually in Switzerland for

ECON0302 International Finance Midterm Exam Fall 2004 Short Questions (60 points each) 1. If in ation in the US is projected at 2:5% annually for the next 3 years and at 0:9% annually in Switzerland for

Goals of Topic 8. NX back!! What is the link between the exchange rate and net exports? How do different policies affect the trade deficit?

TOPIC 8 International Economics Goals of Topic 8 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 8 International Economics Goals of Topic 8 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

4. SOME KEYNESIAN ANALYSIS

4. SOME KEYNESIAN ANALYSIS Fiscal and Monetary Policy... 2 Some Basic Relationships... 2 Floating Exchange Rates and the United States... 7 Fixed Exchange Rates and France... 11 The J-Curve Pattern of

4. SOME KEYNESIAN ANALYSIS Fiscal and Monetary Policy... 2 Some Basic Relationships... 2 Floating Exchange Rates and the United States... 7 Fixed Exchange Rates and France... 11 The J-Curve Pattern of

Intermediate Macroeconomics, EC2201. L4: National income in the open economy

Intermediate Macroeconomics, EC2201 L4: National income in the open economy Anna Seim Department of Economics, Stockholm University Spring 2017 1 / 50 Contents and literature The balance of payments. National

Intermediate Macroeconomics, EC2201 L4: National income in the open economy Anna Seim Department of Economics, Stockholm University Spring 2017 1 / 50 Contents and literature The balance of payments. National

45% Imports Exports 40% 35% 30% 25% 20% 15% 10% 0% Canada France Germany Italy Japan U.K. U.S.

45% 40% 35% Imports Exports 30% 25% 20% 15% 10% 5% 0% Canada France Germany Italy Japan U.K. U.S. spending need not equal output spending need not equal output saving need not equal investment A country

45% 40% 35% Imports Exports 30% 25% 20% 15% 10% 5% 0% Canada France Germany Italy Japan U.K. U.S. spending need not equal output spending need not equal output saving need not equal investment A country

Aggregate real exchange rate persistence through the lens of sectoral data

Aggregate real exchange rate persistence through the lens of sectoral data Laura Mayoral and Lola Gadea Nashville, September 24 2010 Microeconomic Sources of Real Exchange Rate Behavior Motivation and

Aggregate real exchange rate persistence through the lens of sectoral data Laura Mayoral and Lola Gadea Nashville, September 24 2010 Microeconomic Sources of Real Exchange Rate Behavior Motivation and