Bo Singh, TGA President

|

|

|

- Ethel Stokes

- 5 years ago

- Views:

Transcription

1 Bo Singh, TGA President 1

2 ABOUT US T. Gschwender & Associates, Inc. is a diversified consulting company that has been providing services to financial institutions and businesses in the Northeast United States since Our financial institutional clients include small community banks and credit unions with less than $100 million in assets to much larger regional institutions with over $7 billion in assets. Our business clients include small sole proprietorships to middle market privately held corporations. T. Gschwender & Associates, Inc. is best known for our loan review services. But we do more than just loan reviews. Credit analysis, field audits, TDRs, ALLL, equipment evaluations, appraisal reviews, business valuations, environmental remediation, and problem loan management are just some of the services we provide. We can also assist clients to meet all components of a regulatory enforcement action. Our Consultants have extensive banking and corporate management experience. Some of our Associates have been with us since the company was started, and our current staff provides a wide depth of experience, having held high level positions within banking, accounting, and regulatory institutions. With expertise spanning both sides of the street the company s Associates provide a well balanced and thorough approach to all that we do. 2

3 OUR FOCUS Not just a Loan Review Company.a Credit Risk Management Company We like to describe ourselves as a highly sophisticated Credit Department, able to handle all functions from initial borrower due diligence to collateral liquidation and everything in between. Supplement in house personnel; bring independence and expertise to an institution s credit function in a cost effective manner. Growth (12 to 100 clients; 5 to 30 consultants) Expansion of services Expansion of market area Federal Home Loan Bank of Pittsburgh (collateral exam reviews/large banks) Provide our clients with realistic solutions that will save time and enhance their credit risk management processes SBA Veteran Owned Business Achievement Award for 2014 Personnel the real key to our success Our success is based on the expertise of our staff which includes Bank Presidents, Chief Credit Officers, Senior Loan Officers, and OCC Assistant Deputy Comptroller. 3

4 4

5 GOAL Avoiding mistakes that caused many banks to fail during the last recession. Know how much risk you are carrying in the portfolio at all times. What is the impact of the loan you are approving on your overall loan portfolio risk level? How are your Loan Officers performing? Helping the Board set proper risk tolerances. 5

6 MONITORING THE NET OPERATING INCOME It has been TGA s experience that most banks will realize the greatest losses from commercial real estate (CRE) loans where the collateral value has significantly declined. These are primarily associated with investor owned properties where value is based on income approach using market rents at stabilization. Banks should monitor current Net Operating Income (NOI) for investment owned properties with the NOI used in the appraisals. NOI significantly less than those used by the appraiser can result in dramatic devaluation of the collateral property in case the loan becomes impaired, requiring large ALLL allocation. Reserve should be increased periodically if NOI of a particular loan is not achieving stabilization and the loan is showing credit quality concerns. NOI, and the LTV, should be stress tested based on changing interest rates, cap rates, and vacancy factors. 6

7 MONITORING THE NET OPERATING INCOME Borrower Name Loan Number Original Loan Amount Origination Date Maturity Date Interest Rate Interest Rate Variable or Fixed Current Balance Overall Appraisal Market Value Date of Appraisal Appraiser Name Property Type Property Street Address Property City Property State Property ZIP Cap Rate Appraisal NOI Appraisal Income Approach Value Date of Most Recent Financial Statements Annual P&I Payments Current NOI Value Based on Current NOI Current Collateral Property DSCR Global DSCR 7

8 WHY USE THE WEIGHTED AVERAGE RISK RATING? If determined properly, the risk rating takes into account the risk the loan poses to the bank: Capacity DSCRs Capital Profitability, Liquidity, Leverage Collateral Secondary Protection Character Delinquencies Conditions Environmental factors Credit Administration Financial statements/loan structure Easy to calculate, understand and explain. 8

9 RISK RATINGS RISK RATING DESCRIPTOR 1 Secured by Liquid Collateral /Government Guaranteed 2 Excellent 3 Satisfactory 4 Pass/Watch 5 Special Mention 6 Substandard 7 Doubtful 8 Loss 9

10 AVERAGE RATING vs. WEIGHTED AVERAGE RISK RATING AVERAGE RISK RATING Loan # Exposure Risk Rating 1 $ 100, $ 1,000, $ 250, $ 3,500, $ 4,850, WEIGHTED AVERAGE RISK RATING Loan # Exposure Risk Rating Weighted Dollars 1 $ 100, $ 100, $ 1,000, $ 4,000, $ 250, $ 750, $ 3,500, $ 21,000, $ 4,850, $ 25,850,

11 ACCEPTABLE WARR RISK RATING DESCRIPTOR 1 Secured by Liquid Collateral /Government Guaranteed 2 Excellent 3 Satisfactory 4 Pass/Watch 5 Special Mention 6 Substandard 7 Doubtful 8 Loss basis points Below the Pass/Watch Risk Rating (4 Pass Ratings) 5 Pass Ratings: Pass Ratings:

12 USING THE WARR RISK TOLERANCE STATEMENT Key Ratios: Classified Loans to Tier 1 Capital + ALLL not to exceed 25% Special Mention to Tier 1 Capital + ALLL not to exceed 25% Weighted Average Risk Rating (WARR) of all commercial loans not to exceed 3.50 No policy exceptions if WARR exceeds 3.50 Loans Approved with Policy Exceptions to Total Loans not to exceed 10% (measured in dollars) Net Loans to Average Assets not to exceed 75% Net Loans to Equity not to exceed 8.00x Loan Growth not to exceed more than 20% from previous year Losses, Non-Accrual Loans, and Loans Days Past Due to Total Loans Ratios below national peer group average 12

13 THE PASS/WATCH RISK RATING The following should result in loans being risk rated as Pass/Watch: Loans lacking current financial statements but paying as agreed and adequately protected by collateral. Usually done when Borrower will not provide current financials despite repeated requests and financial statements become more than 24 months old. Loans approved based on projections. New entity/no historical cash flow performance. Existing entity that did not cash flow most recent FYE, but have in the past, and have provided realistic projections that will cash flow in the upcoming year. Loans dependent on secondary source of repayment (i.e., owners/guarantors). Collateral property does not cash flow on its own. Business entity does not cash flow on its own. 13

14 MONITORING CREDIT RISK 14

15 MONITORING CREDIT RISK 15

16 MONITORING CREDIT RISK 16

17 MONITORING CREDIT RISK 17

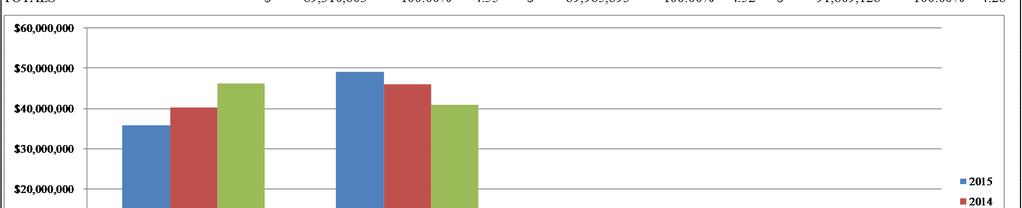

18 MONITORING CREDIT RISK Year Originated Total Weighted Average Risk Rating YTD 2016 $ 18,991, $ 66,909, $ 41,610, $ 30,830, $ 23,617, $ 20,778, $ 4,648, & Before $ 35,720,

19 POLICY EXCEPTIONS POLICY EXCEPTIONS TOTAL EXPOSURE WEIGHTED AVERAGE RISK RATING (WARR) Total Loans Reviewed $ 89,310, Loans Approved With Policy Exceptions $ 40,574, Percent Approved with Policy Exceptions 45.43% 19

20 POLICY EXCEPTIONS Origination Date POLICY EXCEPTIONS BY ORIGINATION DATE TOTAL EXPOSURE WEIGHTED AVERAGE RISK RATING (WARR) 2014 Total Loans Reviewed $ 22,758, Loans Approved With Policy Exceptions $ 11,336, Percent Approved with Policy Exceptions 49.81% 2013 Total Loans Reviewed $ 23,949, Loans Approved With Policy Exceptions $ 15,060, Percent Approved with Policy Exceptions 62.89% 2012 Total Loans Reviewed $ 19,547, Loans Approved With Policy Exceptions $ 6,279, Percent Approved with Policy Exceptions 32.12% 20

21 POLICY EXCEPTIONS Loan Type POLICY EXCEPTIONS BY LOAN TYPE TOTAL EXPOSURE WEIGHTED AVERAGE RISK RATING (WARR) Commercial Real Estate Mortgages (CREMs) Total Loans Reviewed $ 49,186, Loans Approved With Policy Exceptions $ 24,037, Percent Approved with Policy Exceptions 48.87% Commercial & Industrial (C&I) Total Loans Reviewed $ 35,787, Loans Approved With Policy Exceptions $ 13,598, Percent Approved with Policy Exceptions 38.00% 21

22 POLICY EXCEPTIONS By Industry POLICY EXCEPTIONS BY INDUSTRY TOTAL EXPOSURE WEIGHTED AVERAGE RISK RATING (WARR) Retail Trade Total Loans Reviewed $ 11,882, Loans Approved With Policy Exceptions $ 5,278, Percent Approved with Policy Exceptions 44.42% Real Estate and Rental and Leasing Total Loans Reviewed $ 31,428, Loans Approved With Policy Exceptions $ 18,324, Percent Approved with Policy Exceptions 58.31% Accommodation and Food Services Total Loans Reviewed $ 10,780, Loans Approved With Policy Exceptions $ 3,516, Percent Approved with Policy Exceptions 32.62% 22

23 SUMMARY Have a good risk rating methodology in place to properly risk rate your pass loans. It can t be all subjective, you must build some objectivity into it. It has to ensure consistency and transparency in your risk rating process. Just having definitions of risk ratings in your policy is not going to cut it. Use the WARR to monitor and control risk in the portfolio. By using the WARR, you will know how much risk you are carrying in the portfolio at all times. You will know what the impact is of the loan you are approving on your overall loan portfolio risk level. Set risk tolerance limits using the WARR. Board of Directors understand the concept of the WARR better than just showing them metrics on portfolio (volume, risk ratings, delinquencies, non performing loans, etc.). Monitor the NOI of your non owner occupied CREMs. Stress test the NOI and LTV continually and know which loans show high probability of default (weak DSCR) and high probability of loss (weak LTV). 23

24 QUESTIONS? T. GSCHWENDER & ASSOCIATES, INC. 311 MONTGOMERY STREET, SUITE 1 SYRACUSE, NY assoc.com 24

CRE Concentrations: Practical Management Techniques

CRE Concentrations: Practical Management Techniques Tuesday, 6/27/2017 11:00:00 AM - 12:00:00 PM Presented by: Adam Mustafa Co-founder and Managing Partner Invictus Consulting Group 275 Madison Avenue,

CRE Concentrations: Practical Management Techniques Tuesday, 6/27/2017 11:00:00 AM - 12:00:00 PM Presented by: Adam Mustafa Co-founder and Managing Partner Invictus Consulting Group 275 Madison Avenue,

California Credit Union SECTION IV LENDING

SECTION IV LENDING Policy California Credit Union will provide loans to its members in accordance with the laws and regulations of the State of California, the laws and regulations of the United States

SECTION IV LENDING Policy California Credit Union will provide loans to its members in accordance with the laws and regulations of the State of California, the laws and regulations of the United States

CRE Lending Best Practices

CRE Lending Best Practices Understanding the risk and rewards P R E S E N T E D B Y Rob Ashbaugh Executive Risk Management Consultant Sageworks Disclaimer This presentation may include statements that

CRE Lending Best Practices Understanding the risk and rewards P R E S E N T E D B Y Rob Ashbaugh Executive Risk Management Consultant Sageworks Disclaimer This presentation may include statements that

All of the Method None of the Madness

CECL Simplified Current Expected Credit Losses ASU 2016-13 All of the Method None of the Madness The ProBank Austin 2017 Webinar Series November 9, 2017 11:00 AM ESDT Live Case Study - CECL I. Example

CECL Simplified Current Expected Credit Losses ASU 2016-13 All of the Method None of the Madness The ProBank Austin 2017 Webinar Series November 9, 2017 11:00 AM ESDT Live Case Study - CECL I. Example

TABLE OF CONTENTS. President's Letter to Shareholders Selected Consolidated Financial and Other Data... 2

3 TABLE OF CONTENTS Page President's Letter to Shareholders... 1 Selected Consolidated Financial and Other Data... 2 Management's Discussion and Analysis of Financial Condition and Results of Operations...

3 TABLE OF CONTENTS Page President's Letter to Shareholders... 1 Selected Consolidated Financial and Other Data... 2 Management's Discussion and Analysis of Financial Condition and Results of Operations...

KEY UNDERWRITING AND MONITORING CRITERIA FOR BUSINESS LOANS

KEY UNDERWRITING AND MONITORING CRITERIA FOR BUSINESS LOANS April 12, 2016 Today s Presenter Bruce Hull, Team Resources Bruce Hull has more than 30 years lending experience. His knowledge and ability to

KEY UNDERWRITING AND MONITORING CRITERIA FOR BUSINESS LOANS April 12, 2016 Today s Presenter Bruce Hull, Team Resources Bruce Hull has more than 30 years lending experience. His knowledge and ability to

CECL: Current Expected Credit Loss

CECL: Current Expected Credit Loss Business Issues Forum May 1, 2018 Counselors of Real Estate Mid-Year Meeting Copyright 2017, Trepp LLC CECL What is it? Accounting Standard Update 2016-13, issued by

CECL: Current Expected Credit Loss Business Issues Forum May 1, 2018 Counselors of Real Estate Mid-Year Meeting Copyright 2017, Trepp LLC CECL What is it? Accounting Standard Update 2016-13, issued by

114 North Grand Avenue Fiscal Year Beginning January 2019

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $825,000 $16,500 $577,500 $5,775 $269,775 MORTGAGE

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $825,000 $16,500 $577,500 $5,775 $269,775 MORTGAGE

Beyond the Simplicity of DSC and LTV

Beyond the Simplicity of DSC and LTV November 2013 Introduction The credit risk of a Commercial Real Estate (CRE) deal is associated with a highly complex and non-linear deal structure. Historically the

Beyond the Simplicity of DSC and LTV November 2013 Introduction The credit risk of a Commercial Real Estate (CRE) deal is associated with a highly complex and non-linear deal structure. Historically the

Understanding Business Borrowers $150 COURSE DESCRIPTIONS

ABA SELF-PACED BUSINESS BANKING AND COMMERCIAL LENDING PROGRAMS A $10.00 shipping, recordkeeping and administrative fee will be added to all self-paced enrollments. Course Descriptions Below Register Now!

ABA SELF-PACED BUSINESS BANKING AND COMMERCIAL LENDING PROGRAMS A $10.00 shipping, recordkeeping and administrative fee will be added to all self-paced enrollments. Course Descriptions Below Register Now!

9550 Deering Dr. Fiscal Year Beginning October 2018

5-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment 5-YEAR CASH FLOW SUMMARY $160,000 $0 $120,000 $1,200

5-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment 5-YEAR CASH FLOW SUMMARY $160,000 $0 $120,000 $1,200

California Credit Union COMMERCIAL LOANS

COMMERCIAL LOANS General Statement California Credit Union will make sound business loans as a means to meet changing member financial needs within its field of membership. Commercial loans will be priced

COMMERCIAL LOANS General Statement California Credit Union will make sound business loans as a means to meet changing member financial needs within its field of membership. Commercial loans will be priced

Pledging & Underwriting Guidelines (Commercial Real Estate and Multifamily Loan Collateral)

") Pledging & Underwriting Guidelines (Commercial Real Estate and Multifamily Loan Collateral) I. Collateral Eligibility: The Federal Home Loan Bank of Boston s ( the Bank ) Products and Solutions Guide defines

Pledging & Underwriting Guidelines (Commercial Real Estate and Multifamily Loan Collateral) I. Collateral Eligibility: The Federal Home Loan Bank of Boston s ( the Bank ) Products and Solutions Guide defines

805 California St, Tallahassee, Fl Fiscal Year Beginning February 2018

5-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment 5-YEAR CASH FLOW SUMMARY $235,000 $4,700 $176,250

5-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment 5-YEAR CASH FLOW SUMMARY $235,000 $4,700 $176,250

TRENDS IN ASSET QUALITY AVERAGE LEVEL OF ADVERSELY GRADED ASSETS

Trends in Asset Quality Average Levels Based on Steve H. Powell & Company client data, during the Fourth Quarter 2016, the average level of adversely graded assets decreased as a percentage of total assets

Trends in Asset Quality Average Levels Based on Steve H. Powell & Company client data, during the Fourth Quarter 2016, the average level of adversely graded assets decreased as a percentage of total assets

Certified Enterprise Risk Professional (CERP) Test Content Outline

Test Content Outline") Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Preparing the Financial Statement Credit Quality Disclosure

Preparing the Financial Statement Credit Quality Disclosure Twenty Twenty Analytics is the Exclusive CUNA Strategic Service provider for your Loan Portfolio Analytics and Regulatory Compliance Objective

Preparing the Financial Statement Credit Quality Disclosure Twenty Twenty Analytics is the Exclusive CUNA Strategic Service provider for your Loan Portfolio Analytics and Regulatory Compliance Objective

1337 East 61st Street Tulsa OK Fiscal Year Beginning August 2018

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $11,000,000 $220,000 $8,250,000 $82,500 $3,052,500

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $11,000,000 $220,000 $8,250,000 $82,500 $3,052,500

National Risk Committee (NRC) Semiannual Risk Perspective. Fall 2015

Semiannual Risk Perspective. Fall 2015") National Risk Committee (NRC) Semiannual Risk Perspective Fall 2015 NRC Risk Priorities and Actions Underwriting Strategic Risk Interest Rate Risk Cybersecurity Compliance Easing confirmed in examinations

National Risk Committee (NRC) Semiannual Risk Perspective Fall 2015 NRC Risk Priorities and Actions Underwriting Strategic Risk Interest Rate Risk Cybersecurity Compliance Easing confirmed in examinations

Commercial. Real Estate Stress Testing. by Mike Newett and Don Gilliam. The Loan

Commercial Real Estate Commercial Real Estate Stress Testing Stress testing of commercial real estate portfolios has become an even more important risk management tool, especially since interest rates

Commercial Real Estate Commercial Real Estate Stress Testing Stress testing of commercial real estate portfolios has become an even more important risk management tool, especially since interest rates

BAR HARBOR SAVINGS AND LOAN ASSOCIATION

BAR HARBOR SAVINGS AND LOAN ASSOCIATION FINANCIAL STATEMENTS With Independent Auditor's Report INDEPENDENT AUDITOR'S REPORT Board of Directors Bar Harbor Savings and Loan Association We have audited the

BAR HARBOR SAVINGS AND LOAN ASSOCIATION FINANCIAL STATEMENTS With Independent Auditor's Report INDEPENDENT AUDITOR'S REPORT Board of Directors Bar Harbor Savings and Loan Association We have audited the

Cherry, Bekaert & Holland, L.L.P. The Allowance for Loan Losses and Current Credit Trends

Cherry, Bekaert & Holl, L.L.P. The Allowance for Loan Losses Current Cid Hickman, Partner, Industry Leader Services Group chickman@cbh.com www.cbh.com 919.782.1040 Agenda Current Bank Performance Framework,

Cherry, Bekaert & Holl, L.L.P. The Allowance for Loan Losses Current Cid Hickman, Partner, Industry Leader Services Group chickman@cbh.com www.cbh.com 919.782.1040 Agenda Current Bank Performance Framework,

Loan Portfolio Management

Loan Portfolio Management Michael Wear 2016 1 2 ALLL Activity - Summary ($000) 2013 2014 2015 6/2016 Beginning 2,456 3,471 4,343 6,513 Balance Provisions 2,000 2,000 8,000 6,000 Net Charge-offs Ending

Loan Portfolio Management Michael Wear 2016 1 2 ALLL Activity - Summary ($000) 2013 2014 2015 6/2016 Beginning 2,456 3,471 4,343 6,513 Balance Provisions 2,000 2,000 8,000 6,000 Net Charge-offs Ending

LOAN REGISTRATION Type In Form Note: Partial Packages Will NOT Be Reviewed!

LOAN REGISTRATION Type In Form Note: Partial Packages Will NOT Be Reviewed! (Check One) Borrower Broker/Banker Contact Name Date Company Phone Cell Address Fax City, State, Zip: E-Mail Borrower Information

LOAN REGISTRATION Type In Form Note: Partial Packages Will NOT Be Reviewed! (Check One) Borrower Broker/Banker Contact Name Date Company Phone Cell Address Fax City, State, Zip: E-Mail Borrower Information

Asset Quality. Contents

Asset quality is a critical part of your financial analysis of an institution because it directly impacts the evaluation of other component areas such as capital, earnings, and liquidity. The assessment

Asset quality is a critical part of your financial analysis of an institution because it directly impacts the evaluation of other component areas such as capital, earnings, and liquidity. The assessment

Office of Material Loss Reviews Report No. MLR Material Loss Review of Great Basin Bank of Nevada, Elko, Nevada

Office of Material Loss Reviews Report No. MLR-10-008 Material Loss Review of Great Basin Bank of Nevada, Elko, Nevada December 2009 Executive Summary Why We Did The Audit Material Loss Review of Great

Office of Material Loss Reviews Report No. MLR-10-008 Material Loss Review of Great Basin Bank of Nevada, Elko, Nevada December 2009 Executive Summary Why We Did The Audit Material Loss Review of Great

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics. Key Lending Issues from an Examiner Perspective

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

President s Letter to Shareholders Independent Auditor s Report Consolidated Balance Sheets as of June 30, 2016 and

2016 ANNUAL REPORT TABLE OF CONTENTS Page President s Letter to Shareholders... 1 Independent Auditor s Report... 2 Consolidated Balance Sheets as of... 3 Consolidated Statements of Income for the years

2016 ANNUAL REPORT TABLE OF CONTENTS Page President s Letter to Shareholders... 1 Independent Auditor s Report... 2 Consolidated Balance Sheets as of... 3 Consolidated Statements of Income for the years

Lehman Brothers. Global Financial Services Conference. 8 September 2008 New York, NY

Page 1 of 41 EX-99.1 2 LEHMAN BROTHERS PRESENTATION Lehman Brothers Global Financial Services Conference 8 September 2008 New York, NY Page 2 of 41 Forward-Looking Statements This presentation contains

Page 1 of 41 EX-99.1 2 LEHMAN BROTHERS PRESENTATION Lehman Brothers Global Financial Services Conference 8 September 2008 New York, NY Page 2 of 41 Forward-Looking Statements This presentation contains

U.S. Federal Banking Agencies Issue a Policy Statement on Commercial Real Estate Loan Workouts

Financial Institutions Advisory, Financial Regulatory Group & Property Group November 13, 2009 U.S. Federal Banking Agencies Issue a Policy Statement on Commercial Real Estate Loan Workouts There is a

Financial Institutions Advisory, Financial Regulatory Group & Property Group November 13, 2009 U.S. Federal Banking Agencies Issue a Policy Statement on Commercial Real Estate Loan Workouts There is a

CREFC Standardized Annex A - December 2010 Primary Securitized Debt. = Proposed Added Fields to Common, Pre 2010 Annex A's

General Loan Information Mortgage Asset Number Footnotes Mortgage Loan Seller Related Group Sponsor Name Loan Purpose Acquisition / Refinance Cross Collateralized (Y/N) Yes / No Loan Type Fixed Floating

General Loan Information Mortgage Asset Number Footnotes Mortgage Loan Seller Related Group Sponsor Name Loan Purpose Acquisition / Refinance Cross Collateralized (Y/N) Yes / No Loan Type Fixed Floating

Description: Sound Risk Management Practices. Subject: Leveraged Financing PURPOSE

Subject: Leveraged Financing Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision Description: Sound

Subject: Leveraged Financing Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision Description: Sound

2018 ICBA Regulator Panel Agricultural Lending

2018 ICBA Regulator Panel Agricultural Lending March 15, 2018 Keith Osborne ADC Wichita Field Office 1 Agenda Agricultural Lending Risk Management Practices Risk Rating Agricultural Loans References Questions

2018 ICBA Regulator Panel Agricultural Lending March 15, 2018 Keith Osborne ADC Wichita Field Office 1 Agenda Agricultural Lending Risk Management Practices Risk Rating Agricultural Loans References Questions

Southeast Bankers Outreach Forum

Southeast Bankers Outreach Forum CRE Exposures and Sound Risk Management Practices Date: September 28, 2017 Presented by: Trey Wheeler Assistant Vice President Office - 404.498.7152 trey.wheeler@atl.frb.org

Southeast Bankers Outreach Forum CRE Exposures and Sound Risk Management Practices Date: September 28, 2017 Presented by: Trey Wheeler Assistant Vice President Office - 404.498.7152 trey.wheeler@atl.frb.org

Commercial Real. Estate. CMBS Conduit. Loan. Program. Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

CECL SUMMER GAMES Part 5: Key Disclosures & Reports 6/29/2017

CECL SUMMER GAMES Part 5: Key Disclosures & Reports 6/29/2017 1 CPE Credits Visible Equity and the content of this webinar is officially approved with the NASBA (National Association of State Boards of

CECL SUMMER GAMES Part 5: Key Disclosures & Reports 6/29/2017 1 CPE Credits Visible Equity and the content of this webinar is officially approved with the NASBA (National Association of State Boards of

COMMERCIAL CREDIT APPLICATION PAGE 1 of 5. Business Name: Street Address: City: State: Zip:

CRE C&I Bridge DATE: / / APP. NO.: www.cfsb.com COMMERCIAL CREDIT APPLICATION PAGE 1 of 5 PRINCIPLES / GUARANTORS APPLICANT INFORMATION BUSINESS ADDRESS: Fax Number: Tax Payer ID # : Email Address: BUSINESS

CRE C&I Bridge DATE: / / APP. NO.: www.cfsb.com COMMERCIAL CREDIT APPLICATION PAGE 1 of 5 PRINCIPLES / GUARANTORS APPLICANT INFORMATION BUSINESS ADDRESS: Fax Number: Tax Payer ID # : Email Address: BUSINESS

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C.

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. STATE OF OREGON DEPARTMENT OF CONSUMER AND BUSINESS SERVICES SALEM, OREGON Written Agreement by and

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. STATE OF OREGON DEPARTMENT OF CONSUMER AND BUSINESS SERVICES SALEM, OREGON Written Agreement by and

CREDIT RISK MANAGEMENT GUIDANCE FOR HOME EQUITY LENDING

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

FY 2018 Q3 Investor Call

FY 2018 Q3 Investor Call Forward-Looking Statement Statements in this presentation that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of

FY 2018 Q3 Investor Call Forward-Looking Statement Statements in this presentation that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of

Member Business Lending

MOTIVATE. BUILD. LEAD. Member Business Lending Foremost provider of Commerical lending services WHO WE ARE Member Business Lending (MBL) is a credit union service organization (CUSO) established in 2004

MOTIVATE. BUILD. LEAD. Member Business Lending Foremost provider of Commerical lending services WHO WE ARE Member Business Lending (MBL) is a credit union service organization (CUSO) established in 2004

Credit Analysis Solutions COMMERCIAL

Credit Analysis Solutions COMMERCIAL FINPACK 130 Ruttan Hall 1994 Buford Avenue St. Paul, Minnesota 55108 Phone: (612) 625-1964 Toll-Free: (800) 234-1111 Fax: (612) 625-3105 Email: FINPACK@umn.edu Online:

Credit Analysis Solutions COMMERCIAL FINPACK 130 Ruttan Hall 1994 Buford Avenue St. Paul, Minnesota 55108 Phone: (612) 625-1964 Toll-Free: (800) 234-1111 Fax: (612) 625-3105 Email: FINPACK@umn.edu Online:

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

How to Finance (Almost) Any Multifamily Property

Any Multifamily Property") How to Finance (Almost) Any Multifamily Property Disclaimer This is not a solicitation or offer Nothing in this presentation is meant to be legal, Tax or financial advice Consult you lawyer for legal advice

How to Finance (Almost) Any Multifamily Property Disclaimer This is not a solicitation or offer Nothing in this presentation is meant to be legal, Tax or financial advice Consult you lawyer for legal advice

CHART 4.1 THE SEVEN BASIC FUNCTIONS FOR EXTENDING CREDIT

CHART 4.1 THE SEVEN BASIC FUNCTIONS FOR EXTENDING CREDIT What are the seven essential functions in the extension of credit that all lenders must perform or cause to have performed? The configuration of

CHART 4.1 THE SEVEN BASIC FUNCTIONS FOR EXTENDING CREDIT What are the seven essential functions in the extension of credit that all lenders must perform or cause to have performed? The configuration of

Asset Management / Portfolio Management

Asset Management / Portfolio Management Asset / Portfolio Management Brian Miller, CHFA Director of Asset Management Kristi Budish, CHFA Manager Asset Quality Steve Boice, CHFA Loan Analyst Erik Robinson,

Asset Management / Portfolio Management Asset / Portfolio Management Brian Miller, CHFA Director of Asset Management Kristi Budish, CHFA Manager Asset Quality Steve Boice, CHFA Loan Analyst Erik Robinson,

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington D.C. 20549 FORM 10-Q (Mark One) [X] QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington D.C. 20549 FORM 10-Q (Mark One) [X] QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

Ben Franklin Financial, Inc. 830 E. Kensington Road Arlington Heights, IL (847)

") Ben Franklin Financial, Inc. 830 E. Kensington Road Arlington Heights, IL 60004 (847) 398-0990 Financial Report For the Six Months Ended June 30, 2014 Note: This report is intended to be read in conjunction

Ben Franklin Financial, Inc. 830 E. Kensington Road Arlington Heights, IL 60004 (847) 398-0990 Financial Report For the Six Months Ended June 30, 2014 Note: This report is intended to be read in conjunction

FORM 10-Q. Commission File No New Bancorp, Inc. (Exact name of registrant as specified in its charter)

") 10-Q 1 nwbb20170630_10q.htm FORM 10-Q SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [X] Quarterly Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934 For

10-Q 1 nwbb20170630_10q.htm FORM 10-Q SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [X] Quarterly Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934 For

3Q18 Financial Update

3Q18 Update 3Q18 Financial Update Quarterly loss of $5.7 million, $0.34 per diluted share Operating loss was $0.09 per share excluding pre-tax gain on transfer of loans to held for sale of $4,000 and pre-tax

3Q18 Update 3Q18 Financial Update Quarterly loss of $5.7 million, $0.34 per diluted share Operating loss was $0.09 per share excluding pre-tax gain on transfer of loans to held for sale of $4,000 and pre-tax

Banking Regulatory Update

Banking Regulatory Update Joint OCC/Fed/FDIC Release (FIL-51-2013): October 29, 2013 Revision of the 2004 "Uniform Agreement on the Classification of Assets" Oct. 30 th 2013 Attached for your review is

Banking Regulatory Update Joint OCC/Fed/FDIC Release (FIL-51-2013): October 29, 2013 Revision of the 2004 "Uniform Agreement on the Classification of Assets" Oct. 30 th 2013 Attached for your review is

FIRST COMMUNITY CORPORATION AND FIRST COMMUNITY BANK OF EAST TENNESSEE. Rogersville, Tennessee CONSOLIDATED FINANCIAL STATEMENTS

FIRST COMMUNITY CORPORATION AND FIRST COMMUNITY BANK OF EAST TENNESSEE Rogersville, Tennessee CONSOLIDATED FINANCIAL STATEMENTS Rogersville, Tennessee AUDITED CONSOLIDATED FINANCIAL STATEMENTS TABLE OF

FIRST COMMUNITY CORPORATION AND FIRST COMMUNITY BANK OF EAST TENNESSEE Rogersville, Tennessee CONSOLIDATED FINANCIAL STATEMENTS Rogersville, Tennessee AUDITED CONSOLIDATED FINANCIAL STATEMENTS TABLE OF

Survey of Credit Underwriting Practices 2010

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

BNCCORP, INC. (OTCQX: BNCC)

") Quarterly Report For the quarter ended September 30, 2018 BNCCORP, INC. (OTCQX: BNCC) 322 East Main Bismarck, North Dakota 58501 (701) 250-3040 BNCCORP, INC. INDEX TO QUARTERLY REPORT September 30, 2018

Quarterly Report For the quarter ended September 30, 2018 BNCCORP, INC. (OTCQX: BNCC) 322 East Main Bismarck, North Dakota 58501 (701) 250-3040 BNCCORP, INC. INDEX TO QUARTERLY REPORT September 30, 2018

Case Study: Exploring FedChoice Federal Credit Union s Effective MBL Program

Veronese 2401 Friday, July 25, 2014 10:00 11:00 a.m.; 11:15 a.m. 12:15 p.m. Case Study: Exploring FedChoice Federal Credit Union s Effective MBL Program Bill Keilholtz, Director Lending Services, FedChoice

Veronese 2401 Friday, July 25, 2014 10:00 11:00 a.m.; 11:15 a.m. 12:15 p.m. Case Study: Exploring FedChoice Federal Credit Union s Effective MBL Program Bill Keilholtz, Director Lending Services, FedChoice

Delta Agricultural Credit Association

Quarterly Report June 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries,

Quarterly Report June 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries,

BERMUDA MONETARY AUTHORITY GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

Maspeth Federal Savings and Loan Association and Subsidiaries

Maspeth Federal Savings and Loan Association and Subsidiaries Consolidated Financial Statements Table of Contents Page Independent Auditor s Report 1 Consolidated Financial Statements Consolidated Statements

Maspeth Federal Savings and Loan Association and Subsidiaries Consolidated Financial Statements Table of Contents Page Independent Auditor s Report 1 Consolidated Financial Statements Consolidated Statements

REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS FOR MOUNTAIN PACIFIC BANK

REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS FOR MOUNTAIN PACIFIC BANK December 31, 2017 and 2016 Table of Contents Report of Independent Auditors 1 PAGE Financial Statements Balance sheets

REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS FOR MOUNTAIN PACIFIC BANK December 31, 2017 and 2016 Table of Contents Report of Independent Auditors 1 PAGE Financial Statements Balance sheets

Loan Policy. Including Loan Program Parameters & Underwriting Guidelines. Last Updated 11/30/18

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

Credit Administration and Documentation Standards

Credit Administration and Documentation Standards OVERVIEW: It is the objective of this Organization to extend adequate and constructive credit, in accordance with regulations, under the definition of

Credit Administration and Documentation Standards OVERVIEW: It is the objective of this Organization to extend adequate and constructive credit, in accordance with regulations, under the definition of

FedLinks. Connecting Policy with Practice. Expectations for Banks. How Examiners Assess the ALLL

FedLinks Connecting Policy with Practice ALLOWANCE FOR LOAN AND LEASE LOSSES JANUARY 2013 During periods of unstable financial conditions, meeting the supervisory expectations for maintaining an appropriate

FedLinks Connecting Policy with Practice ALLOWANCE FOR LOAN AND LEASE LOSSES JANUARY 2013 During periods of unstable financial conditions, meeting the supervisory expectations for maintaining an appropriate

Securities and Exchange Commission Washington, DC FORM 10-Q

Securities and Exchange Commission Washington, DC 20549 FORM 10-Q [X] Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the period ended March 31, 2011 or [ ]

Securities and Exchange Commission Washington, DC 20549 FORM 10-Q [X] Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the period ended March 31, 2011 or [ ]

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. and STATE OF NORTH CAROLINA NORTH CAROLINA COMMISSIONER OF BANKS RALEIGH, NORTH CAROLINA

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. and STATE OF NORTH CAROLINA NORTH CAROLINA COMMISSIONER OF BANKS RALEIGH, NORTH CAROLINA ) In the Matter of ) ) MACON BANK, INC. ) CONSENT ORDER FRANKLIN,

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. and STATE OF NORTH CAROLINA NORTH CAROLINA COMMISSIONER OF BANKS RALEIGH, NORTH CAROLINA ) In the Matter of ) ) MACON BANK, INC. ) CONSENT ORDER FRANKLIN,

A Real Stress Test for CRE Portfolios

ProMS A Real Stress Test for CRE Portfolios Radley & Associates Radley & Associates is an independent firm dedicated to the development of advanced simulation based analytics for the Commercial Real Estate

ProMS A Real Stress Test for CRE Portfolios Radley & Associates Radley & Associates is an independent firm dedicated to the development of advanced simulation based analytics for the Commercial Real Estate

ALLL About Disclosure Reports. Key issues to know

ALLL About Disclosure Reports Key issues to know About Sageworks Lending, Credit Risk and Portfolio Risk Solutions More than 1,100 financial institution clients Thought leader for institutions and examiners

ALLL About Disclosure Reports Key issues to know About Sageworks Lending, Credit Risk and Portfolio Risk Solutions More than 1,100 financial institution clients Thought leader for institutions and examiners

Orbisonia Community Bancorp, Inc.

Audited Financial Statements December 31 2017 Orbisonia Community Bancorp, Inc. CONTENTS INDEPENDENT AUDITOR'S REPORT 1 2 Page CONSOLIDATED FINANCIAL STATEMENTS Consolidated balance sheets 3 Consolidated

Audited Financial Statements December 31 2017 Orbisonia Community Bancorp, Inc. CONTENTS INDEPENDENT AUDITOR'S REPORT 1 2 Page CONSOLIDATED FINANCIAL STATEMENTS Consolidated balance sheets 3 Consolidated

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. OFFICE OF STATE BANK COMMISSIONER TOPEKA, KANSAS

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. OFFICE OF STATE BANK COMMISSIONER TOPEKA, KANSAS Written Agreement by and among SOLUTIONSBANK CORPORATION

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. OFFICE OF STATE BANK COMMISSIONER TOPEKA, KANSAS Written Agreement by and among SOLUTIONSBANK CORPORATION

Residential Mortgage. Underwriting Policy. Sound Business & Financial Practices

Residential Mortgage 2019 Underwriting Policy Three Point Capital Corp. ( TPC ) has published this Residential Mortgage Underwriting Policy ( TPC Policy ), which was adapted from and based on the November

Residential Mortgage 2019 Underwriting Policy Three Point Capital Corp. ( TPC ) has published this Residential Mortgage Underwriting Policy ( TPC Policy ), which was adapted from and based on the November

Multifamily Securities Locator Service Glossary

Multifamily Securities Locator Service Glossary Term 30/360 Actual/360 Additional Disclosure Additional Liens Adjustable Rate Term Affordable Housing Type Method of computing interest on a mortgage loan

Multifamily Securities Locator Service Glossary Term 30/360 Actual/360 Additional Disclosure Additional Liens Adjustable Rate Term Affordable Housing Type Method of computing interest on a mortgage loan

The Real Price of Risk in Lending

The Real Price of Risk in Lending IBA, NBA & OBA 2018 Convention June 21, 2018 Today s Agenda Why we care about risk How we can (and should) use risk s What makes a strong risk system How to develop and

The Real Price of Risk in Lending IBA, NBA & OBA 2018 Convention June 21, 2018 Today s Agenda Why we care about risk How we can (and should) use risk s What makes a strong risk system How to develop and

REGULATORY DISCUSSION TOPICS

REGULATORY DISCUSSION TOPICS COMPLIANCE THE ISSUE Community banks play a critical role in the health and growth of communities across the country by providing access to credit where it otherwise may not

REGULATORY DISCUSSION TOPICS COMPLIANCE THE ISSUE Community banks play a critical role in the health and growth of communities across the country by providing access to credit where it otherwise may not

Freddie Mac Multifamily Securitization Small Balance Loan (FRESB) as of June 30, 2016

as of June 30, 2016") Freddie Mac Multifamily Securitization Small Balance Loan (FRESB) as of June 30, 2016 Table of Contents Freddie Mac Multifamily Business Key Facts 2016 YTD Multifamily Review Small Balance Loan (SBL) Business

Freddie Mac Multifamily Securitization Small Balance Loan (FRESB) as of June 30, 2016 Table of Contents Freddie Mac Multifamily Business Key Facts 2016 YTD Multifamily Review Small Balance Loan (SBL) Business

Maspeth Federal Savings and Loan Association and Subsidiaries

Maspeth Federal Savings and Loan Association and Subsidiaries Consolidated Financial Statements Table of Contents Page Independent Auditor s Report 1 Consolidated Financial Statements Consolidated Statements

Maspeth Federal Savings and Loan Association and Subsidiaries Consolidated Financial Statements Table of Contents Page Independent Auditor s Report 1 Consolidated Financial Statements Consolidated Statements

on Delaware Banks Prepared for Delaware Bankers Association

The Impact of Standardized di d Basel II on Delaware Banks Prepared for Delaware Bankers Association Executive Summary Basel II bank capital regulations are in the news We estimate that Standardized Basel

The Impact of Standardized di d Basel II on Delaware Banks Prepared for Delaware Bankers Association Executive Summary Basel II bank capital regulations are in the news We estimate that Standardized Basel

Making the Business Case for the CECL Approach Part II

ADVICE TO STRENGTHEN FINANCIAL INSTITUTIONS Making the Business Case for the CECL Approach Part II Released January 2017 This white paper is the second part of a three part series that presents the numerous

ADVICE TO STRENGTHEN FINANCIAL INSTITUTIONS Making the Business Case for the CECL Approach Part II Released January 2017 This white paper is the second part of a three part series that presents the numerous

Challenges in the. Mike Lubansky, Senior Analyst Sageworks, Inc Centerview Drive Raleigh, NC

Challenges in the Estimation of the ALLL Mike Lubansky, Senior Analyst Sageworks, Inc. The estimation of the Allowance for Loan and Lease Losses (ALLL) has been a part of the financial institution s accounting

Challenges in the Estimation of the ALLL Mike Lubansky, Senior Analyst Sageworks, Inc. The estimation of the Allowance for Loan and Lease Losses (ALLL) has been a part of the financial institution s accounting

July 21, Wells Fargo & Company. All rights reserved.

2Q10 Quarterly Supplement July 21, 2010 2010 Wells Fargo & Company. All rights reserved. Forward-looking statements and additional information Forward-looking statements: This Quarterly Supplement contains

2Q10 Quarterly Supplement July 21, 2010 2010 Wells Fargo & Company. All rights reserved. Forward-looking statements and additional information Forward-looking statements: This Quarterly Supplement contains

Farm Credit Southeast Missouri, ACA

Quarterly Report September 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Quarterly Report September 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Guidance from Bank Regulators on Managing Commercial Real Estate Concentrations

GLOBAL BANKING & MARKETS Guidance from Bank Regulators on Managing Commercial Real Estate Concentrations Richard Daingerfield Chief Legal Officer, The Royal Bank of Scotland plc NY Branch Chair, Banking

GLOBAL BANKING & MARKETS Guidance from Bank Regulators on Managing Commercial Real Estate Concentrations Richard Daingerfield Chief Legal Officer, The Royal Bank of Scotland plc NY Branch Chair, Banking

Credit Risk Benchmarks

2ND Quarter 2015 Credit Risk Benchmarks We are pleased to provide second-quarter 2015 metrics for this Journal feature, which provides an up-to-date view of C&I and Commercial Real Estate credit quality

2ND Quarter 2015 Credit Risk Benchmarks We are pleased to provide second-quarter 2015 metrics for this Journal feature, which provides an up-to-date view of C&I and Commercial Real Estate credit quality

Interpretation of Regulatory Guidance on Dodd Frank Investment Grade Due Diligence

Interpretation of Regulatory Guidance on Dodd Frank Investment Grade Due Diligence JC Brew, Senior Municipal Bond Analyst, Seifried & Brew LLC January 8, 2015 (Updated January 5, 2016) Seifried & Brew

Interpretation of Regulatory Guidance on Dodd Frank Investment Grade Due Diligence JC Brew, Senior Municipal Bond Analyst, Seifried & Brew LLC January 8, 2015 (Updated January 5, 2016) Seifried & Brew

Effective MBL Reviews

2014 CliftonLarsonAllen LLP Effective MBL Reviews Dean Rohne, CPA, CIA 800-657-4477 Dean.rohne@claconnect.com Objectives Review key considerations related to a member business loan Discuss key operational

2014 CliftonLarsonAllen LLP Effective MBL Reviews Dean Rohne, CPA, CIA 800-657-4477 Dean.rohne@claconnect.com Objectives Review key considerations related to a member business loan Discuss key operational

How to Justify a Change in Your ALLL

How to Justify a Change in Your ALLL Ed Bayer, Managing Director Tim McPeak, Senior Risk Management Consultant Sageworks O - (919) 851-7474 F - (919) 851-6718 info@sageworks.com www.sageworksanalyst.com

How to Justify a Change in Your ALLL Ed Bayer, Managing Director Tim McPeak, Senior Risk Management Consultant Sageworks O - (919) 851-7474 F - (919) 851-6718 info@sageworks.com www.sageworksanalyst.com

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY COMPTROLLER OF THE CURRENCY ) ) ) CONSENT ORDER

) ) CONSENT ORDER") UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY COMPTROLLER OF THE CURRENCY #2009-010 In the Matter of: Corus Bank, National Association Chicago, Illinois ) ) ) CONSENT ORDER AA-EC-2009-13 WHEREAS,

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY COMPTROLLER OF THE CURRENCY #2009-010 In the Matter of: Corus Bank, National Association Chicago, Illinois ) ) ) CONSENT ORDER AA-EC-2009-13 WHEREAS,

GE Capital. Overview / Strategy first quarter

GE Capital Overview / Strategy This document contains forward-looking statements - that is, statements related to future, not past, events. In this context, forward-looking statements often address our

GE Capital Overview / Strategy This document contains forward-looking statements - that is, statements related to future, not past, events. In this context, forward-looking statements often address our

2018 Commercial Lending School

2018 Commercial Lending School 2018 Commercial Lending School June 11-15, 2018 IBA Center for Professional Development Indianapolis, IN 2018 COMMERCIAL LENDING SCHOOL GENERAL INFORMATION ROE: Return on

2018 Commercial Lending School 2018 Commercial Lending School June 11-15, 2018 IBA Center for Professional Development Indianapolis, IN 2018 COMMERCIAL LENDING SCHOOL GENERAL INFORMATION ROE: Return on

Bangor Bancorp, MHC and its Subsidiary, Bangor Savings Bank Consolidated Financial Statements March 31, 2017 and 2016

Bangor Bancorp, MHC and its Subsidiary, Bangor Savings Bank Consolidated Financial Statements Page 1 Table of Contents Page(s) Independent Auditor s Report... 1 Consolidated Financial Statements Balance

Bangor Bancorp, MHC and its Subsidiary, Bangor Savings Bank Consolidated Financial Statements Page 1 Table of Contents Page(s) Independent Auditor s Report... 1 Consolidated Financial Statements Balance

ORANGE COUNTY S CREDIT UNION AND SUBSIDIARY Santa Ana, California. CONSOLIDATED FINANCIAL STATEMENTS December 31, 2011 and 2010

ORANGE COUNTY S CREDIT UNION AND SUBSIDIARY Santa Ana, California CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED FINANCIAL STATEMENTS Consolidated

ORANGE COUNTY S CREDIT UNION AND SUBSIDIARY Santa Ana, California CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED FINANCIAL STATEMENTS Consolidated

FPB FINANCIAL CORP. AND SUBSIDIARIES

FPB FINANCIAL CORP. AND SUBSIDIARIES Audits of Consolidated Financial Statements December 31, 2015 and 2014 Contents Independent Auditor s Report 1-2 Basic Consolidated Financial Statements Consolidated

FPB FINANCIAL CORP. AND SUBSIDIARIES Audits of Consolidated Financial Statements December 31, 2015 and 2014 Contents Independent Auditor s Report 1-2 Basic Consolidated Financial Statements Consolidated

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C FORM ABS-15G

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM ABS-15G ASSET-BACKED SECURITIZER REPORT PURSUANT TO SECTION 15G OF THE SECURITIES EXCHANGE ACT OF 1934 Check the appropriate

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM ABS-15G ASSET-BACKED SECURITIZER REPORT PURSUANT TO SECTION 15G OF THE SECURITIES EXCHANGE ACT OF 1934 Check the appropriate

Making the Business Case for the CECL Approach

Making the Business Case for the CECL Approach Attend any recent or upcoming financial institution conference and you will find considerable discussion and debate about the new accounting guidance related

Making the Business Case for the CECL Approach Attend any recent or upcoming financial institution conference and you will find considerable discussion and debate about the new accounting guidance related

Survey of Credit Underwriting Practices 2005 Office of the Comptroller of the Currency National Credit Committee

Survey of Credit Underwriting Practices 25 Office of the Comptroller of the Currency National Credit Committee June 25 1 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4 Commentary...6

Survey of Credit Underwriting Practices 25 Office of the Comptroller of the Currency National Credit Committee June 25 1 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4 Commentary...6

ABA SELF-PACED LENDING PROGRAMS

ABA SELF-PACED LENDING PROGRAMS A $10.00 shipping, recordkeeping and administrative fee will be added to all self-paced enrollments. Course Descriptions Below Certificate in Business & Commercial Lending

ABA SELF-PACED LENDING PROGRAMS A $10.00 shipping, recordkeeping and administrative fee will be added to all self-paced enrollments. Course Descriptions Below Certificate in Business & Commercial Lending

Ownership Goals and Objectives Financing and Loan Analysis Types of Loans Calculating Loans Loan to Value (LTV%) Debt Coverage Ratio (DCR) Leverage

Debt Coverage Ratio (DCR) Leverage") REVIEW CONTENT: FINANCIAL OPERATIONS AND ASSET ANALYSIS The outline below serves as a guide to understanding the main topic areas that you could be tested on in the CPM certification exam: Ownership Goals

REVIEW CONTENT: FINANCIAL OPERATIONS AND ASSET ANALYSIS The outline below serves as a guide to understanding the main topic areas that you could be tested on in the CPM certification exam: Ownership Goals

FPB FINANCIAL CORP. AND SUBSIDIARIES FINANCIAL STATEMENTS DECEMBER 31, 2017

FINANCIAL STATEMENTS DECEMBER 31, 2017 Postlethwaite & Netterville A Professional Accounting Corporation www.pncpa.com FINANCIAL STATEMENTS DECEMBER 31, 2017 TABLE OF CONTENTS Page Independent Auditors'

FINANCIAL STATEMENTS DECEMBER 31, 2017 Postlethwaite & Netterville A Professional Accounting Corporation www.pncpa.com FINANCIAL STATEMENTS DECEMBER 31, 2017 TABLE OF CONTENTS Page Independent Auditors'

The Unintended Consequences of Basel III for Community Banks in the United States

FINANCIAL PERFORMANCE The Unintended Consequences of Basel III for Community Banks in the United States sales@profitstars.com 877.827.7101 Contents Introduction 2 Consequences of Changing Status of AFS

FINANCIAL PERFORMANCE The Unintended Consequences of Basel III for Community Banks in the United States sales@profitstars.com 877.827.7101 Contents Introduction 2 Consequences of Changing Status of AFS

Farm Credit Southeast Missouri, ACA

Quarterly Report June 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Quarterly Report June 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

The Top 10 Things to Note from the New MAP Underwriting Guidelines Tracy W. Peters

The Top 10 Things to Note from the New MAP Underwriting Guidelines Tracy W. Peters 10. Better Loan Parameters OLD NEW 223(f) Loan to Value DSCR 223(f) Loan to Value DSCR Market Rate 83% 1.20x Market Rate

The Top 10 Things to Note from the New MAP Underwriting Guidelines Tracy W. Peters 10. Better Loan Parameters OLD NEW 223(f) Loan to Value DSCR 223(f) Loan to Value DSCR Market Rate 83% 1.20x Market Rate