Volume II. Chapter 1. Study Iq Education

|

|

|

- Russell Owens

- 5 years ago

- Views:

Transcription

1

2

3 Volume II Chapter 1

4 Chapter 1 Introduction Section A. Analytical review of recent development The Goods & Services Tax Paradigm Shift to Low Inflation Wedge between asset price & real economy Farm Loan Wavers- Macro Economic Impact Demonetization: Long Term Benefits & Short Term Cost Section B. Outlook & policies for Section C:Review of Development in

5 Outlook & Policies for

6 Outlook for Real Activity for For some time now, India has been in the throes of what Carmen Reinhart and Kenneth Rogoff have called balance sheet recessions ("weaker than potential growth" rather than "recessions" is a more appropriate characterization for India).

7 Outlook for Real Activity for Para 1: Credit & Investment Legacy General Scenario In most countries, booms are accompanied by rapid increases in credit growth, followed by deleveraging (or credit decline) after which credit growth can not necessarily will pick up. China has followed a different path: it has chosen to re-leverage with a vengeance in order to stave off a growth slowdown. This works in the short run, although at the expense of decreasing capital efficiency and building up financial sector vulnerabilities that could lead to dramatic growth slowdowns in the future.

8 Outlook for Real Activity for Indian Scenario Indian boom of mid 2000 is not followed by serious deleveraging. Slowdown in bank credit is the source of concern. If deleveraging is necessary condition for resuming growth than India needs more debt resolution and reduction in the short run.

9

10 Outlook for Real Activity for Para 2: Current Situation of Indian Economy A number of indicators GDP, core GVA (GVA excluding agriculture and Government), IIP, credit, investment and capacity utilization point to a deceleration in real activity. Real GVA growth for Q was 5.6 per cent. Unless potential output growth is much lower than is commonly assumed (around 7 percent or more), output gaps are expected to widen.

11 Outlook for Real Activity for Para 3: Expectation in Volume I of Economic Survey Volume I range for GDP growth of between 6.75 and 7.5 percent factoring in More buoyant exports Post demonetization catch up in consumption Relaxation of monetary conditions which prevailed during demonetization.

12 Outlook for Real Activity for Para 4: Present factors affecting the expectations Deflationary bias is expected in economy reason beingü Real exchange rate appreciation. ü Farm loan waivers ü Increased stress to balance sheet in power, telecommunication and agricultural sector. ü Transitional Changes implementing the GST

13 Outlook for Real Activity for Para 6- Effect of farm loan waiver The deflationary impact of farm loan waiver will depend upon how many states imitate the same action as UP, Mahrashtra, MP & Karnataka. Deflationary impact is expected to be 0.35% due to the farm loan waiving.

14 Outlook for Real Activity for Para 7- Monetary Policy and it s effect Real policy rate is tighter than what was expected in Volume I. It is expected that if current monetary policy will continue then forecasted GDP will show a downside risk.

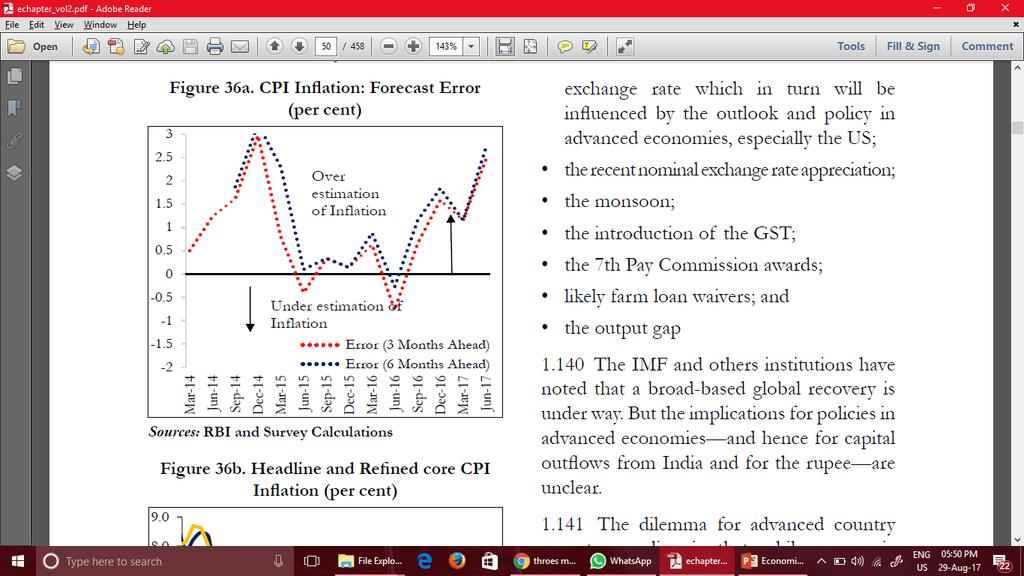

15 Outlook for Real Activity for Para 8- TBS and Prospects Since the Volume I Government & RBI has taken various steps to resolve the TBS problem. Market Confidence has boosted. Deleveraging the corporate balance sheets will be necessary to restore investment & credit demand. Deleveraging of bank balance sheets will be essential to unblock the choked channels of the supply of credit. However, the substantive growth impact of the steps taken will depend on the scope, effectiveness, and timeliness of resolution of stressed assets.

16 Outlook for Real Activity for Para 9- GST Effects There is also some upside from the GST. The removal of check posts and the consequent easing of transport constraints can provide some short-term fillip to economic activity.

17 Outlook for Real Activity for Para 10- Conclusion In Volume I growth in GDP was expected to be 7% from 6.75%. But the preceding discussion indicates that the balance of risks seem to have shifted to the downside. The balance of probabilities has changed accordingly, with outcomes closer to the upper end having much less weight than previous.

18

19 Outlook for Price & Inflation for Para 1 Anticipated Inflationary Trend The section on Paradigm Shift to Low Inflation argued that India might already be in the throes of a structural disinflationary shift, driven by more permanent developments in both the international oil market and domestic agriculture reflected in unanticipated inflation developments.

20

21 Outlook for Price & Inflation for RBI s newly adopted Flexible Inflation Targeting framework: Headline CPI- Measures target rate of inflation indicating price of essential consumotion goods and goods having highly volatile prices. Inflation in these prices hurts the lower income group. Core CPI- Represents long tern inflation trend of economy. It ignores food products and all such product of which prices are volatile like oil. This is done to separate permanent and temporary inflation movements. Para 2 Headline & Core CPI

22 Outlook for Price & Inflation for Para 3 Determiners of Inflation in Near Term Capital flows and exchange rates which are dependent upon the outlook & policies of advanced economies specially of US. Recent exchange rate appreciation The monsoon The GST impacts The 7 th Pay Commission Awards Likely Farm Loan Waivers The output gap

23 Outlook for Price & Inflation for Other Important Issues Food prices are expected to be on higher side and very encouraging due to the anticipated better rainfall than previous years. The GST is expected, on balance, to reduce prices because of the lower incidence of taxation compared to the combined incidence of central and state taxes previously. The 7th Pay Commission housing award is expected to increase inflation on average by between 0.4 and 1.2 percentage points, depending on whether just the Centre or the Centre and all the states implement the award.

24 Outlook for Price & Inflation for Other Important Issues Farm loan waivers are more likely to be deflationary than inflationary and hence impart a downward not upward bias to prices. Output gaps are important for inflation and the earlier discussion points to a weakening economy and widening output gaps.

25 Policy Instances

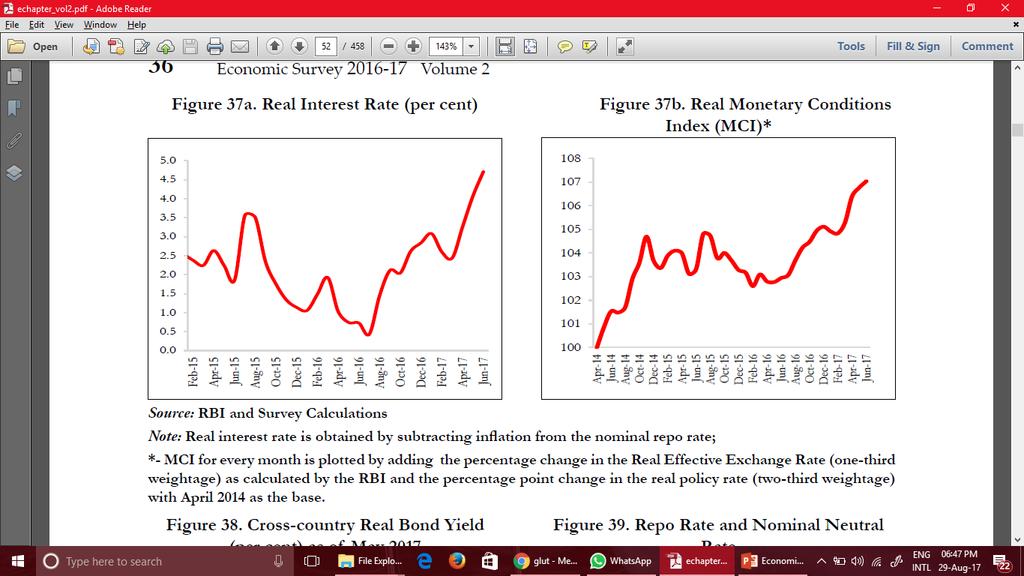

26 Monetary Policy Three main features have characterized the Monetary Policy since release of Volume I: 1. Real Interest rates are currently high. 2. Unusual volatility in G-Sec Rates of Bonds. (Chapter 3) 3. Glut of liquidity in banks has persisted for about 9 months. (Chapter 3)

27

28 Rates are also substantially higher than in comparable emerging market countries.

29

30 Nominal Neutral Rate & Repo Rate Normal or neutral interest rates are those that prevail when inflation is close to target and real GDP close to potential. At targeted inflation rate of 4%; neutral interest rate must be between % but the present rate is 6% which shows a deflation of Basis points. Current inflation, at 1.5 percent, is running well below the 4 percent target, with the domestic economy lacking the dynamism to push this back toward the target. Example: Capacity utilization in Q3 of is 72.7%. It is suggest that the policy rate should actually be below not basis points or so above the neutral rate.

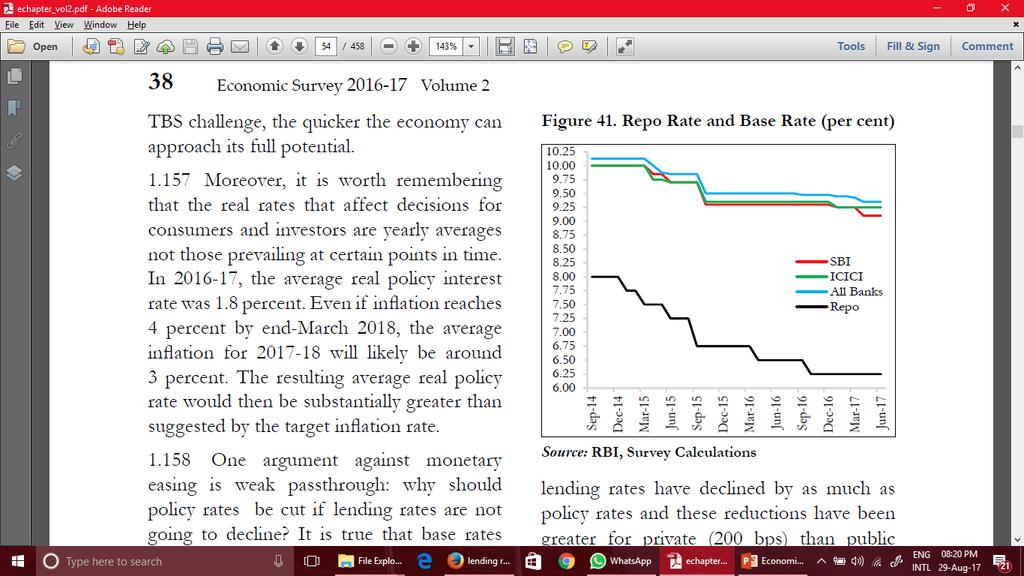

31 Conclusion: The scope for monetary easing is considerable, more than that suggested by comparison with neutral interest rates. The earlier the easing, complemented with other reform actions especially to address the TBS challenge, the quicker the economy can approach its full potential. Real Rates which affect the decision of consumer and investors are yearly average not what is at the certain point of time. In the average inflation rate was 1.8%, even if in we reach the targeted 4% the average will be 3%. Still the policy interest rate is substantially higher than targeted inflation rate.

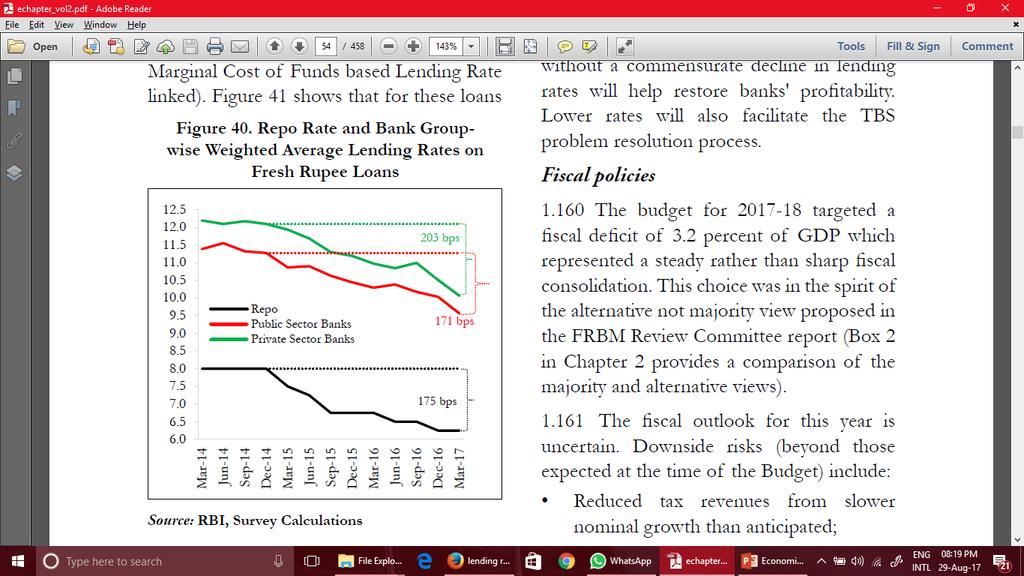

32 Lending Rate, Base Rate & Policy Rates (Repo Rates): Argument against easing repo rate: Why repo rate should be reduced if base rate does not reduce accordingly. Base rate declines by 80 bp in comparison with 175 bp of policy rates. Answer: There are financial stability benefits from cutting policy rates The reduction in the cost of funds without a commensurate decline in lending rates will help restore banks' profitability. Lower rates will also facilitate the TBS problem resolution process. These reductions in lending rates benefit all borrowers, including small and medium enterprises (SMEs).

33

34 Fiscal Policy The fiscal outlook for this year is uncertain. Downside risk other than those discussed in budget previously include: Reduced tax revenues from slower nominal growth than anticipated. Reduced GST collections on account of the lower GST rates compared with the pre- GST taxes, and transitional challenges from GST implementation. Reduced spectrum receipts on account of the structural jolt to the viability of incumbent firms. Higher expenditures from the 7th Pay Commission estimated at Rs.30,000 crore. A Slight upside trend may also be seen by positive aspect of GST implementation and tax compliance policies by the demonetization process.

35 Other Policies Agricultural stress will need appropriate policy responses. Given that 2017 will also be a year of surplus rather than scarcity, and to the extent that firming up prices will be essential to boost agricultural incomes. Situation of cobweb cycle may arise if agriculture issues not seen properly. Proper remuneration policy, stable MSP and easy access to export market will protect both producers and consumers from production & price swings.

36 Cobweb Cycle Cobweb Cycle is featured by market in which supply by producer depends upon the prices in the previous period. It is the basic characteristic of the market in which time gap between production and selling is large. What to produce in next year is dependent on previous years experience. For example, if pulses prices are particularly high in a given year, more farmers will choose to plant pulses the next year to take advantage of the high price. This increased supply, however, will lead to lower prices.

37 Other Policies All the impediments that come in the way of realizing better prices for farmers stock limits imposed under the Essential Commodities Act, export restrictions, impediments to the implementation of e-nam need to be removed. The time is also ripe to consider whether direct support to farmers can be a more effective way to boost farm incomes over current indirect, Ineffective, and inefficient forms of support. National Agriculture Market (NAM) is a pan-india electronic trading portal which networks the existing APMC (Agriculture Produce & Market Committee) mandis to create a unified national market for agricultural commodities.

38

RBI Q1 FY11 Monetary Policy Review

RBI Q1 FY11 Monetary Policy Review The Policy Measures In Brief In its First Quarter Review of the Annual Monetary Policy for 2010-11, the Reserve Bank of India increased its policy rates with immediate

RBI Q1 FY11 Monetary Policy Review The Policy Measures In Brief In its First Quarter Review of the Annual Monetary Policy for 2010-11, the Reserve Bank of India increased its policy rates with immediate

Reviewing Macro-economic Developments and Understanding Macro-Economic Policy

MINISTRY OF FINANCE GOVERNMENT OF INDIA Reviewing Macro-economic Developments and Understanding Macro-Economic Policy Module 5 Contemporary Themes in India s Economic Development and the Economic Survey

MINISTRY OF FINANCE GOVERNMENT OF INDIA Reviewing Macro-economic Developments and Understanding Macro-Economic Policy Module 5 Contemporary Themes in India s Economic Development and the Economic Survey

Macroeconomic Context and Budget Priorities Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013

Macroeconomic Context and Budget Priorities 2013-14 by Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013 * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India,

Macroeconomic Context and Budget Priorities 2013-14 by Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013 * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India,

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

FIXED INCOME OUTLOOK August 2017

FIXED INCOME OUTLOOK August 2017 Key trends that drive our strategy Significant fall in headline & core CPI Inflation; Headline CPI expected to meet RBI long term target of slightly above 4% Slowdown in

FIXED INCOME OUTLOOK August 2017 Key trends that drive our strategy Significant fall in headline & core CPI Inflation; Headline CPI expected to meet RBI long term target of slightly above 4% Slowdown in

Monetary Policy Review Premature end to the easing cycle?

The monetary policy committee (MPC) maintained status quo for the second policy review running, keeping Repo rate at 6.25%, contrary to market expectations of 25bps cut. Consequently, the reverse repo/msf

The monetary policy committee (MPC) maintained status quo for the second policy review running, keeping Repo rate at 6.25%, contrary to market expectations of 25bps cut. Consequently, the reverse repo/msf

India and the Global Crisis

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

Prepared by Basanta K Pradhan & Sangeeta Chakravarty August 2010

Prepared by Basanta K Pradhan & Sangeeta Chakravarty August 21 Highlights Industrial growth cools down WPI inflation falls marginally. Rupee appreciates marginally The annual growth of Index of Industrial

Prepared by Basanta K Pradhan & Sangeeta Chakravarty August 21 Highlights Industrial growth cools down WPI inflation falls marginally. Rupee appreciates marginally The annual growth of Index of Industrial

India s Economic Outlook

India s Economic Outlook Draft Report 2017-18 & 2018-19 India-LINK Team* September 2017 *These forecasts, developed as part of World Project Link, are based on the India-LINK (earlier known as CDE- DSE

India s Economic Outlook Draft Report 2017-18 & 2018-19 India-LINK Team* September 2017 *These forecasts, developed as part of World Project Link, are based on the India-LINK (earlier known as CDE- DSE

RBI Monetary Policy Update - RBI maintains the neutral stance with cautious outlook on inflation and growth

RBI Monetary Policy Update - RBI maintains the neutral stance with cautious outlook on inflation and growth In the latest policy meeting, the RBI kept the key policy rate unchanged at 6% and maintained

RBI Monetary Policy Update - RBI maintains the neutral stance with cautious outlook on inflation and growth In the latest policy meeting, the RBI kept the key policy rate unchanged at 6% and maintained

MONETARY POLICY OUTLOOK- THE FIFTH BI-MONTHLY MONETARY POLICY REVIEW OF THE CURRENT FINANCIAL YEAR DECEMBER-MARCH

MONETARY POLICY OUTLOOK- THE FIFTH BI-MONTHLY MONETARY POLICY REVIEW OF THE CURRENT FINANCIAL YEAR DECEMBER-MARCH 2018-19 Dr. Arun Kumar Misra, Associate Professor, Finance & Accounts, VGSOM, IIT Kharagpur

MONETARY POLICY OUTLOOK- THE FIFTH BI-MONTHLY MONETARY POLICY REVIEW OF THE CURRENT FINANCIAL YEAR DECEMBER-MARCH 2018-19 Dr. Arun Kumar Misra, Associate Professor, Finance & Accounts, VGSOM, IIT Kharagpur

RBI Monetary Policy Update Status Quo on Rates

RBI Monetary Policy Update Status Quo on Rates After the cutting the rate by 25 bps in August policy, the RBI kept the key policy rate unchanged at 6% and maintained the neutral stance of monetary policy

RBI Monetary Policy Update Status Quo on Rates After the cutting the rate by 25 bps in August policy, the RBI kept the key policy rate unchanged at 6% and maintained the neutral stance of monetary policy

Meeting with Analysts

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

Economic Outlook Survey. January 2017

January 2017 GDP growth estimated at 6.8% in 2016-17: FICCI s Economic Outlook Survey HIGHLIGHTS GDP growth for FY 17 estimated at 6.8% The latest round of FICCI s Economic Outlook Survey puts forth an

January 2017 GDP growth estimated at 6.8% in 2016-17: FICCI s Economic Outlook Survey HIGHLIGHTS GDP growth for FY 17 estimated at 6.8% The latest round of FICCI s Economic Outlook Survey puts forth an

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 20 November 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 20 November 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

Fixed Income Update October 2015

Month Overview Average Liquidity Support by RBI Rs -5,527 Cr. Includes: LAF, MSF, SLF & Term Repo Bank Credit Growth Money Market Bank Deposit Growth 9.6% 11.6% Change in basis points Tenure CD Change

Month Overview Average Liquidity Support by RBI Rs -5,527 Cr. Includes: LAF, MSF, SLF & Term Repo Bank Credit Growth Money Market Bank Deposit Growth 9.6% 11.6% Change in basis points Tenure CD Change

The Czech Economy and Monetary Policy: Deflationary Risks and the Exchange Rate as a Monetary Policy Instrument Luboš Komárek

The Czech Economy and Monetary Policy: Deflationary Risks and the Exchange Rate as a Monetary Policy Instrument Luboš Komárek 75th East Jour Fixe - 10 Years of EU Enlargement Vienna, 25th April 2014 I.

The Czech Economy and Monetary Policy: Deflationary Risks and the Exchange Rate as a Monetary Policy Instrument Luboš Komárek 75th East Jour Fixe - 10 Years of EU Enlargement Vienna, 25th April 2014 I.

Meeting with Analysts

CNB s New Forecast (Inflation Report I/2018) Meeting with Analysts Tomáš Holub Prague, 2 February 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report I/2018) Meeting with Analysts Tomáš Holub Prague, 2 February 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

18th Year of Publication. A monthly publication from South Indian Bank.

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 18th Year of Publication SIB STUDENTS

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 18th Year of Publication SIB STUDENTS

India s Economic Outlook

India s Economic Outlook Draft Report 2016-17 India-LINK Team* September 2016 Comments and queries may be addressed to: Pami Dua 1, N.R. Bhanumurthy 2 and Lokendra Kumawat 3 *These forecasts, developed

India s Economic Outlook Draft Report 2016-17 India-LINK Team* September 2016 Comments and queries may be addressed to: Pami Dua 1, N.R. Bhanumurthy 2 and Lokendra Kumawat 3 *These forecasts, developed

GDP to grow at 7% in fiscal CRISIL Outlook September 2017

GDP to grow at 7% in fiscal 2018 CRISIL Outlook September 2017 CRISIL has trimmed its fiscal 2018 growth forecast for India by 40 basis points to 7% from 7.4% earlier, after data for the first quarter

GDP to grow at 7% in fiscal 2018 CRISIL Outlook September 2017 CRISIL has trimmed its fiscal 2018 growth forecast for India by 40 basis points to 7% from 7.4% earlier, after data for the first quarter

Economic Outlook Survey September 2015

FICCI s Economic Outlook Survey: GDP growth at 7.6% for 2015-16 Results of FICCI s latest Economic Outlook Survey indicate moderation in GDP growth estimates. Based on the responses received, the median

FICCI s Economic Outlook Survey: GDP growth at 7.6% for 2015-16 Results of FICCI s latest Economic Outlook Survey indicate moderation in GDP growth estimates. Based on the responses received, the median

Prepared by Basanta K Pradhan & Sangeeta Chakravarty January and February 2013

Prepared by Basanta K Pradhan & Sangeeta Chakravarty January and February 2013 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally Marginal rise in CPI inflation Rupee

Prepared by Basanta K Pradhan & Sangeeta Chakravarty January and February 2013 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally Marginal rise in CPI inflation Rupee

Economic projections

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

FICCI Economic Outlook Survey

FICCI Economic Outlook Survey January 2010 FICCI, Federation House, 1, Tansen Marg, New Delhi About the Survey The Economic Outlook Survey was conducted during the period January 1 to January 15, 2010.

FICCI Economic Outlook Survey January 2010 FICCI, Federation House, 1, Tansen Marg, New Delhi About the Survey The Economic Outlook Survey was conducted during the period January 1 to January 15, 2010.

August 1, 2017 I Economics EXPECTATIONS FROM CREDIT POLICY: AUGUST 2017

EXPECTATIONS FROM CREDIT POLICY: AUGUST 2017 August 1, 2017 I Economics The third bi-monthly monetary policy review for this fiscal year is to be announced by the RBI on 2nd August 2017. It will be sixth

EXPECTATIONS FROM CREDIT POLICY: AUGUST 2017 August 1, 2017 I Economics The third bi-monthly monetary policy review for this fiscal year is to be announced by the RBI on 2nd August 2017. It will be sixth

Monetary Policy Review : April 16

April 5, 2016 Monetary Policy Review : April 16 On expected lines, the RBI in its first bi-monthly Monetary Policy announced 25 bps cut in repo rate from 6.75 % to 6.5%. It also announced measures to address

April 5, 2016 Monetary Policy Review : April 16 On expected lines, the RBI in its first bi-monthly Monetary Policy announced 25 bps cut in repo rate from 6.75 % to 6.5%. It also announced measures to address

Mid-Quarter Monetary Policy Review

18 December, 2013 Mid-Quarter Monetary Policy Review RBI maintained status quo in the mid-quarter monetary policy meeting held today preferring to wait and watch for more forthcoming macro-economic data

18 December, 2013 Mid-Quarter Monetary Policy Review RBI maintained status quo in the mid-quarter monetary policy meeting held today preferring to wait and watch for more forthcoming macro-economic data

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 18 January 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank In recent weeks,

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 18 January 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank In recent weeks,

Key Insights. China Macro Pulse

MACRO REPORT China Economy Update March 2015 Key Insights Monica Defend Head of Global Asset Allocation Research Qinwei Wang Economist Global Asset Allocation Research Economic Conditions: China s macro

MACRO REPORT China Economy Update March 2015 Key Insights Monica Defend Head of Global Asset Allocation Research Qinwei Wang Economist Global Asset Allocation Research Economic Conditions: China s macro

Economic Outlook and Forecast

Economic Outlook and Forecast Stefano Eusepi Research & Statistics Group January 2017 All views expressed are those of the author only and not necessarily those of the Federal Reserve Bank of New York

Economic Outlook and Forecast Stefano Eusepi Research & Statistics Group January 2017 All views expressed are those of the author only and not necessarily those of the Federal Reserve Bank of New York

Prepared by Basanta K Pradhan & Sangeeta Chakravarty December 2012

Prepared by Basanta K Pradhan & Sangeeta Chakravarty December 2012 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally CPI inflation fell very marginally Rupee stabilizing

Prepared by Basanta K Pradhan & Sangeeta Chakravarty December 2012 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally CPI inflation fell very marginally Rupee stabilizing

Deepak Mohanty: Inflation dynamics in India issues and concerns

Deepak Mohanty: Inflation dynamics in India issues and concerns Speech by Mr Deepak Mohanty, Executive Director of the Reserve Bank of India, to the Bombay Chamber of Commerce and Industry, Mumbai, 4 March

Deepak Mohanty: Inflation dynamics in India issues and concerns Speech by Mr Deepak Mohanty, Executive Director of the Reserve Bank of India, to the Bombay Chamber of Commerce and Industry, Mumbai, 4 March

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

STCI Primary Dealer Ltd

Macroeconomic Update: GDP Q3 FY18 Beating expectations, India s Real GDP noted a sharp rebound, coming in at 7.2% for Q3 FY18, higher than the revised estimate of 6.5% witnessed in the previous quarter.

Macroeconomic Update: GDP Q3 FY18 Beating expectations, India s Real GDP noted a sharp rebound, coming in at 7.2% for Q3 FY18, higher than the revised estimate of 6.5% witnessed in the previous quarter.

Summary of Opinions at the Monetary Policy Meeting 1,2 on December 19 and 20, 2018

Not to be released until 8:50 a.m. Japan Standard Time on Friday, December 28, 2018. December 28, 2018 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on December 19 and 20, 2018 I.

Not to be released until 8:50 a.m. Japan Standard Time on Friday, December 28, 2018. December 28, 2018 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on December 19 and 20, 2018 I.

Indian Economy. GDP growth slowed down but remained above the comfortable 7% Manufacturing GVAbp

Indian Economy Economic Growth GDP growth slowed down but remained above the comfortable 7% Domestic economy witnessed 7.1% GDP growth during the first quarter (Apr - Jun) of fiscal 2016-17 (Q1FY17) as

Indian Economy Economic Growth GDP growth slowed down but remained above the comfortable 7% Domestic economy witnessed 7.1% GDP growth during the first quarter (Apr - Jun) of fiscal 2016-17 (Q1FY17) as

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

Chapter 4: A First Look at Macroeconomics

Chapter 4: A First Look at Macroeconomics Principles of Macroeconomics I. Economics as a Social Science A. Economics is the social science that studies the choices that individuals, businesses, governments,

Chapter 4: A First Look at Macroeconomics Principles of Macroeconomics I. Economics as a Social Science A. Economics is the social science that studies the choices that individuals, businesses, governments,

Economic Projections :2

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 2006

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 1. Introduction 1.1 There are three objectives to undertake a mid-term review of the Monetary Policy Statement (MPS). First, it is intended to review progress

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 1. Introduction 1.1 There are three objectives to undertake a mid-term review of the Monetary Policy Statement (MPS). First, it is intended to review progress

MONTHLY UPDATE SEPTEMBER 2017

MONTHLY UPDATE SEPTEMBER 2017 September 2017 "I am a better investor because I am a businessman and a better businessman because I am an investor. - Warren Buffett Equity Markets Indices 31 st Aug 2017

MONTHLY UPDATE SEPTEMBER 2017 September 2017 "I am a better investor because I am a businessman and a better businessman because I am an investor. - Warren Buffett Equity Markets Indices 31 st Aug 2017

Second Hike with Neutral Stance

Second Hike with Neutral Stance RBI hiked the key policy rate by 25 bps to 6.50%, while retaining the neutral stance of monetary policy. This is second consecutive hike since June 2018. Highlight of the

Second Hike with Neutral Stance RBI hiked the key policy rate by 25 bps to 6.50%, while retaining the neutral stance of monetary policy. This is second consecutive hike since June 2018. Highlight of the

Economic Projections :3

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Second Bi-Monthly Monetary Policy Review

June 3, 2014 Second Bi-Monthly Monetary Policy Review RBI kept key policy rates unchanged in line with consensus expectations. RBI reduced statutory liquidity ratio (SLR) by 50 bps to 22.50% with effect

June 3, 2014 Second Bi-Monthly Monetary Policy Review RBI kept key policy rates unchanged in line with consensus expectations. RBI reduced statutory liquidity ratio (SLR) by 50 bps to 22.50% with effect

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Gill Marcus, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 27 March 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Gill Marcus, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 27 March 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Gill Marcus, Governor of the South African Reserve Bank Since the previous

CARE Ratings Survey on the Indian Economy: FY16

July 16, 2015 Economics CARE Ratings Survey on the Indian Economy: FY16 Expectations ran high for the Indian economy since early 2014 on hopes that the domestic economy would be recharged and investments

July 16, 2015 Economics CARE Ratings Survey on the Indian Economy: FY16 Expectations ran high for the Indian economy since early 2014 on hopes that the domestic economy would be recharged and investments

Prepared by Basanta K Pradhan & Sangeeta Chakravarty November 2009

Prepared by Basanta K Pradhan & Sangeeta Chakravarty November 2009 Index of industrial production shows sign of economic recovery IIP increased by 9.1 percent Inflation now turning positive High food prices

Prepared by Basanta K Pradhan & Sangeeta Chakravarty November 2009 Index of industrial production shows sign of economic recovery IIP increased by 9.1 percent Inflation now turning positive High food prices

First Quarter Review of Monetary Policy

RESERVE BANK OF INDIA First Quarter Review of Monetary Policy 2012-13 Dr. D. Subbarao Governor July 31, 2012 Mumbai i ii CONTENTS Page No. I. The State of the Economy Global Economy...2 Domestic Economy...3

RESERVE BANK OF INDIA First Quarter Review of Monetary Policy 2012-13 Dr. D. Subbarao Governor July 31, 2012 Mumbai i ii CONTENTS Page No. I. The State of the Economy Global Economy...2 Domestic Economy...3

ECONOMIC OUTLOOK UNIVERSITY OF CYPRUS ECONOMICS RESEARCH CENTRE. January 2017 SUMMARY. Issue 17/1

SUMMARY UNIVERSITY OF CYPRUS The expansion of real economic activity in Cyprus is expected to continue in 2017 at rates similar to those registered in 2016. Real GDP is forecasted to have increased by

SUMMARY UNIVERSITY OF CYPRUS The expansion of real economic activity in Cyprus is expected to continue in 2017 at rates similar to those registered in 2016. Real GDP is forecasted to have increased by

RBI hikes by 25 bps to 6.25% - First time since Jan 2014

RBI hikes by 25 bps to 6.25% - First time since Jan 2014 RBI hiked the key policy rate by 25 bps to 6.25%, while maintaining the neutral stance of monetary policy. This is first hike since January 2014.

RBI hikes by 25 bps to 6.25% - First time since Jan 2014 RBI hiked the key policy rate by 25 bps to 6.25%, while maintaining the neutral stance of monetary policy. This is first hike since January 2014.

RBI s Sixth Bi-Monthly Monetary Policy Review ( ) Maintains status quo...neutral Stance

Maintains status quo...neutral Stance") 7h February 2018 RBI s Sixth Bi-Monthly Monetary Policy Review (2017-18) Maintains status quo...neutral Stance Repo Rate unchanged at Reverse Repo Rate stands at 5.75% Marginal Standing Facility and Bank

7h February 2018 RBI s Sixth Bi-Monthly Monetary Policy Review (2017-18) Maintains status quo...neutral Stance Repo Rate unchanged at Reverse Repo Rate stands at 5.75% Marginal Standing Facility and Bank

REFERENCE NOTE. No. 28/RN/Ref./November /2013

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 28/RN/Ref./November /2013 For the use of

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 28/RN/Ref./November /2013 For the use of

Growth and Inflation Prospects and Monetary Policy

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Inflation Unit V[ Part1/2]

![Inflation Unit V[ Part1/2]](/thumbs/86/93637821.jpg "Inflation Unit V[ Part1/2]") Inflation Unit V[ Part1/2] CPT General Economics Chapter - 6 Select Aspects of Indian Economy CA. Dipti Lunawat Learning Objectives Meaning & Types of Inflation Price Trends in India Causes of Inflation

Inflation Unit V[ Part1/2] CPT General Economics Chapter - 6 Select Aspects of Indian Economy CA. Dipti Lunawat Learning Objectives Meaning & Types of Inflation Price Trends in India Causes of Inflation

Outlook for Economic Activity and Prices

Not to be released until : p.m. Japan Standard Time on Saturday, October 31, 15. October 31, 15 Bank of Japan Outlook for Economic Activity and Prices October 15 (English translation prepared by the Bank's

Not to be released until : p.m. Japan Standard Time on Saturday, October 31, 15. October 31, 15 Bank of Japan Outlook for Economic Activity and Prices October 15 (English translation prepared by the Bank's

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2018) Meeting with Analysts Petr Král Prague, 4 May 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report II/2018) Meeting with Analysts Petr Král Prague, 4 May 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

Globalisation and monetary policy

Globalisation and monetary policy José Manuel González-Páramo European Central Bank Frankfurt, 1 March 2007 08/03/07 1 Introduction Globalisation process accelerated in the last two decades, mainly for

Globalisation and monetary policy José Manuel González-Páramo European Central Bank Frankfurt, 1 March 2007 08/03/07 1 Introduction Globalisation process accelerated in the last two decades, mainly for

Latest Macroeconomic Projections - May Vice-Governor Anita Angelovska-Bezhoska

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Fixed Income Markets & Strategy of Duration Funds

Fixed Income Markets & Strategy of Duration Funds Market Update: July 2017 Positive bias on favorable macro data releases, awaiting further cues from RBI policy in August. At the start of the month, bond

Fixed Income Markets & Strategy of Duration Funds Market Update: July 2017 Positive bias on favorable macro data releases, awaiting further cues from RBI policy in August. At the start of the month, bond

Outlook for Economic Activity and Prices (April 2017) Summary

Summary") April 27, 2017 Bank of Japan The Bank's View 1 Outlook for Economic Activity and Prices (April 2017) Summary Japan's economy is likely to continue expanding and maintain growth at a pace above its potential,

April 27, 2017 Bank of Japan The Bank's View 1 Outlook for Economic Activity and Prices (April 2017) Summary Japan's economy is likely to continue expanding and maintain growth at a pace above its potential,

Summary of Opinions at the Monetary Policy Meeting 1,2 on March 14 and 15, 2019

Not to be released until 8:50 a.m. Japan Standard Time on Tuesday, March 26, 2019. March 26, 2019 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on March 14 and 15, 2019 I. Opinions

Not to be released until 8:50 a.m. Japan Standard Time on Tuesday, March 26, 2019. March 26, 2019 Bank of Japan Summary of Opinions at the Monetary Policy Meeting 1,2 on March 14 and 15, 2019 I. Opinions

Outlook for Economic Activity and Prices (April 2014)

") April 30, 2014 Bank of Japan Outlook for Economic Activity and Prices (April 2014) The Bank's View 1 Summary From fiscal 2014 through fiscal 2016, Japan's economy is likely to continue growing at a pace

April 30, 2014 Bank of Japan Outlook for Economic Activity and Prices (April 2014) The Bank's View 1 Summary From fiscal 2014 through fiscal 2016, Japan's economy is likely to continue growing at a pace

Results of the Survey of Professional Forecasters on Macroeconomic Indicators Round 44 1

Results of the Survey of Professional Forecasters on Macroeconomic Indicators Round 44 1 In the 44 th round of the Survey of Professional Forecasters, output growth for 2016-17 measured by gross value

Results of the Survey of Professional Forecasters on Macroeconomic Indicators Round 44 1 In the 44 th round of the Survey of Professional Forecasters, output growth for 2016-17 measured by gross value

Global economic issues and the impact on Shipping

1st Annual Marine Money Cyprus Forum Global economic issues and the impact on Shipping Andreas Assiotis, PhD 26 April 2017 Table of contents 1 2 3 4 5 Economic Fundamentals and Global Drivers 3 Global

1st Annual Marine Money Cyprus Forum Global economic issues and the impact on Shipping Andreas Assiotis, PhD 26 April 2017 Table of contents 1 2 3 4 5 Economic Fundamentals and Global Drivers 3 Global

Indian Economy. Industrial output grew highest in four months in June 2015 but volatility continued

Indian Economy Industrial Production Industrial output grew highest in four months in June 2015 but volatility continued After a slowdown in May 2015, industrial production grew by 3.8% during the month

Indian Economy Industrial Production Industrial output grew highest in four months in June 2015 but volatility continued After a slowdown in May 2015, industrial production grew by 3.8% during the month

INFLATION REPORT / I 015 2

INFLATION REPORT / I 5 INFLATION REPORT / I FOREWORD In 998, the Czech National Bank switched to inflation targeting. In the inflation targeting regime, the central bank s communication with the public

INFLATION REPORT / I 5 INFLATION REPORT / I FOREWORD In 998, the Czech National Bank switched to inflation targeting. In the inflation targeting regime, the central bank s communication with the public

Ryuzo Miyao: Economic activity and prices in Japan and monetary policy

Ryuzo Miyao: Economic activity and prices in Japan and monetary policy Summary of a speech by Mr Ryuzo Miyao, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Tokushima,

Ryuzo Miyao: Economic activity and prices in Japan and monetary policy Summary of a speech by Mr Ryuzo Miyao, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Tokushima,

The global economy: so far so good? 1

Presentation at the Belgian Financial Forum, Brussels, 8 July 5 The global economy: so far so good? Malcolm D Knight, General Manager Bank for International Settlements 4 was one of the best years for

Presentation at the Belgian Financial Forum, Brussels, 8 July 5 The global economy: so far so good? Malcolm D Knight, General Manager Bank for International Settlements 4 was one of the best years for

With an eventful year 2015 coming to an end, at the very outset, we wish everyone a very happy and prosperous New Year

Equity View With an eventful year 2015 coming to an end, at the very outset, we wish everyone a very happy and prosperous New Year- 2016. Key highlights: We believe that 2016 can be a year of immense possibilities

Equity View With an eventful year 2015 coming to an end, at the very outset, we wish everyone a very happy and prosperous New Year- 2016. Key highlights: We believe that 2016 can be a year of immense possibilities

Czech Economy and Monetary Policy

Lunch with the Czech National Bank Czech Economy and Monetary Policy Vojtěch Benda CNB Board Member London, 21 May 2018 Outline and main messages Czech economy: robust growth, tight labour market. Inflation:

Lunch with the Czech National Bank Czech Economy and Monetary Policy Vojtěch Benda CNB Board Member London, 21 May 2018 Outline and main messages Czech economy: robust growth, tight labour market. Inflation:

MONTHLY REPORT. USDINR Gone By. 2 nd March 2015

USDINR Gone By 2 nd March 2015 Rupee opened the month at 61.99 levels and initially remained on weaker note owing to negative sentiments in Global equities. According to the latest data, US GDP faltered

USDINR Gone By 2 nd March 2015 Rupee opened the month at 61.99 levels and initially remained on weaker note owing to negative sentiments in Global equities. According to the latest data, US GDP faltered

Survey of Professional Forecasters on Macroeconomic Indicators Results of the 45 th Round 1

Survey of Professional Forecasters on Macroeconomic Indicators Results of the 45 th Round 1 ----------------------------------------------------------------------------------------------------------------------

Survey of Professional Forecasters on Macroeconomic Indicators Results of the 45 th Round 1 ----------------------------------------------------------------------------------------------------------------------

Viet Nam GDP growth by sector Crude oil output Million metric tons 20

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

ECONOMIC RECOVERY AT CRUISE SPEED

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

Vajiram & Ravi (A Unit of Vajiram and Ravi IAS Study Centre LLP)

") Economic Survey 2014-15 (SV) Economic Outlook, Prospects and Policy Challenges Macroeconomic fundamentals in 2014-15 have dramatically improved. Highlights are: Inflation has declined by over 6 percentage

Economic Survey 2014-15 (SV) Economic Outlook, Prospects and Policy Challenges Macroeconomic fundamentals in 2014-15 have dramatically improved. Highlights are: Inflation has declined by over 6 percentage

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Gill Marcus, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 18 September 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Gill Marcus, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 18 September 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Gill Marcus, Governor of the South African Reserve Bank Since the previous

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS DEBT SUSTAINABILITY ANALYSIS Directorate of Debt Management and Economic Cooperation

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS A S D DEBT SUSTAINABILITY ANALYSIS 2015 Directorate of Debt Management and Economic Cooperation Table of Contents LIST OF TABLES... 2 LIST OF FIGURES... 2 LIST

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS A S D DEBT SUSTAINABILITY ANALYSIS 2015 Directorate of Debt Management and Economic Cooperation Table of Contents LIST OF TABLES... 2 LIST OF FIGURES... 2 LIST

Update. Regulatory. What after FIPB?

Regulatory Update What after FIPB? India has become a favored investment destination in light of its large domestic consumption based economy, favorable demographics, skilled workforce and the continuing

Regulatory Update What after FIPB? India has become a favored investment destination in light of its large domestic consumption based economy, favorable demographics, skilled workforce and the continuing

Inflation Report. January March 2013

January March 2013 May 8, 2013 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants 4 Forecasts and Balance of Risks 2 External Conditions Global Environment

January March 2013 May 8, 2013 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants 4 Forecasts and Balance of Risks 2 External Conditions Global Environment

Demonetization Drive: Biggest Economic Reform by the MODI Government

Demonetization Drive: Biggest Economic Reform by the MODI Government The historic demonetization move by the government is seen as a war on parallel economy, corruption, money laundering and to stop financing

Demonetization Drive: Biggest Economic Reform by the MODI Government The historic demonetization move by the government is seen as a war on parallel economy, corruption, money laundering and to stop financing

MONTHLY UPDATE NOVEMBER 2018

MONTHLY UPDATE NOVEMBER 2018 November 2018 A champion is defined not by their wins but by how they can recover when they fall. Equity markets - Serena Williams Indices 31 st Oct 2018 30 th Nov 2018 1 Month

MONTHLY UPDATE NOVEMBER 2018 November 2018 A champion is defined not by their wins but by how they can recover when they fall. Equity markets - Serena Williams Indices 31 st Oct 2018 30 th Nov 2018 1 Month

Outlook for Economic Activity and Prices (January 2018)

") Outlook for Economic Activity and Prices (January 2018) January 23, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue expanding on the back of highly accommodative financial

Outlook for Economic Activity and Prices (January 2018) January 23, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue expanding on the back of highly accommodative financial

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

APPENDIX: Country analyses

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

Koji Ishida: Japan s economy, price developments and monetary policy

Koji Ishida: Japan s economy, price developments and monetary policy Speech by Mr Koji Ishida, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Fukuoka, 18 February

Koji Ishida: Japan s economy, price developments and monetary policy Speech by Mr Koji Ishida, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Fukuoka, 18 February

Czech Monetary Policy and Economic Outlook

IMF/WB Annual Meetings 17 Czech Monetary Policy and Economic Outlook Vladimir TOMSIK Vice-Governor Czech National Bank Bank of America Merril Lynch Symposium and JPMorgan Investor Seminar 13 1 October

IMF/WB Annual Meetings 17 Czech Monetary Policy and Economic Outlook Vladimir TOMSIK Vice-Governor Czech National Bank Bank of America Merril Lynch Symposium and JPMorgan Investor Seminar 13 1 October

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Outlook for Economic Activity and Prices (July 2018)

") Outlook for Economic Activity and Prices (July 2018) July 31, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue growing at a pace above its potential in fiscal 2018, mainly

Outlook for Economic Activity and Prices (July 2018) July 31, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue growing at a pace above its potential in fiscal 2018, mainly

Survey of Professional Forecasters on Macroeconomic Indicators Results of the 47 th Round 1

Survey of Professional Forecasters on Macroeconomic Indicators Results of the 47 th Round 1 ----------------------------------------------------------------------------------------------------------------------

Survey of Professional Forecasters on Macroeconomic Indicators Results of the 47 th Round 1 ----------------------------------------------------------------------------------------------------------------------

Transcending from Recovery to Growth

India and the Global Financial Crisis Transcending from Recovery to Growth Peterson Institute for International Economics Washington DC April 26, 2010 Dr. D. Subbarao Governor, Reserve Bank of India India

India and the Global Financial Crisis Transcending from Recovery to Growth Peterson Institute for International Economics Washington DC April 26, 2010 Dr. D. Subbarao Governor, Reserve Bank of India India

World Economic outlook

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Czech monetary policy: On a way to neutral interest rates

Czech monetary policy: On a way to neutral interest rates Petr Král Deputy Executive Director Monetary Department Czech & Hungary Investor Day London, 14 November 2018 Current economic situation 2 Structure

Czech monetary policy: On a way to neutral interest rates Petr Král Deputy Executive Director Monetary Department Czech & Hungary Investor Day London, 14 November 2018 Current economic situation 2 Structure

MONETARY AND FINANCIAL TRENDS IN THE FIRST NINE MONTHS OF 2013

MONETARY AND FINANCIAL TRENDS IN THE FIRST NINE MONTHS OF 2013 Introduction This note is to analyze the main financial and monetary trends in the first nine months of this year, with a particular focus

MONETARY AND FINANCIAL TRENDS IN THE FIRST NINE MONTHS OF 2013 Introduction This note is to analyze the main financial and monetary trends in the first nine months of this year, with a particular focus

Model Question Paper Economics - II (MSF1A4)

") Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

Economic Projections For 2014 And 2015

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Meeting with Analysts

CNB s New Forecast (Inflation Report III/3) Meeting with Analysts Tibor Hlédik Prague, 9 August, 3 Summary of the Inflation Forecast (i) The recovery of GDP in the effective euro area is postponed again

CNB s New Forecast (Inflation Report III/3) Meeting with Analysts Tibor Hlédik Prague, 9 August, 3 Summary of the Inflation Forecast (i) The recovery of GDP in the effective euro area is postponed again

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover