ESTIMATING TOOLS FOR INFRASTRUCTURE PROJECTS

|

|

|

- Irene Stafford

- 5 years ago

- Views:

Transcription

1 ESTIMATING TOOLS FOR INFRASTRUCTURE PROJECTS 1 Saroop S and Allopi D 2 1 Kwezi V3 Engineers (Pty) Ltd, P O Box 299, Westville, 3630, Durban, South Africa 2 Department of Civil Engineering and Surveying, Durban Institute of Technology, P O Box 953, Durban, South Africa ABSTRACT Minimum cost has become a critical performance criteria for most engineers in infrastructure projects where developers need to maximise the number of the property units. Today it is widely acknowledged that the complexity of infrastructure planning and realisation is growing, and on many levels: technical, legal, political, socially and financially. At present the control exercised over forecasting is limited. There is a growing need to manage actively the cost efficiency and forecasting for the wider interest of society. Government needs to effectively monitor the design process from beginning to end instead of just allocating money and that a different approach is needed to infrastructure projects. While there are numerous political, social and economical aspects of the infrastructure problem, there is a great need for appropriate technical solutions. This research contributes to the underdeveloped area of cost planning and forecasting on infrastructure projects. There has to be a greater effort at improving cost-benefit analysis and integrating infrastructure design options and costs consequences. There is a need for generating ideas for new projects and alternative solutions. In general, the increased efficiency of existing and new infrastructure has to be promoted. The purpose of the paper is to present the standard outputs of the cost planning model that was discussed in its subsequent paper. The output generated by the model will compare the cost of various design options and is expected to reduce the cost of projects The cost planning model and its outputs is a disciplined effort to produce fundamental decisions in shaping the project cost. The process must be seen as an integrated whole in order to maximise the opportunities for improving quality and reducing project costs. This will place a heavy burden on the consultants to use client s money in the most efficient way possible. The economic analysis involves undertaking a cost-analysis of the various project options to assess their economic viability. The economic analysis guides the decision-makers by altering key design factors and assessing how and what costs should be increased. 1. INTRODUCTION Early design decisions are made when too much data are unavailable. The cost model makes cost effective options just one of the criteria relevant to the project approval, which must be balanced against other criteria such as price and quality and ensures that social benefits are obtained with the minimum possible costs to the government. 1 ssaroop@kv3.co.za and 2 allopid@dit.ac.za Proceedings of the 25 th Southern African Transport Conference (SATC 2006) July 2006 ISBN Number: Pretoria, South Africa Produced by: Document Transformation Technologies cc Conference organised by: Conference Planners

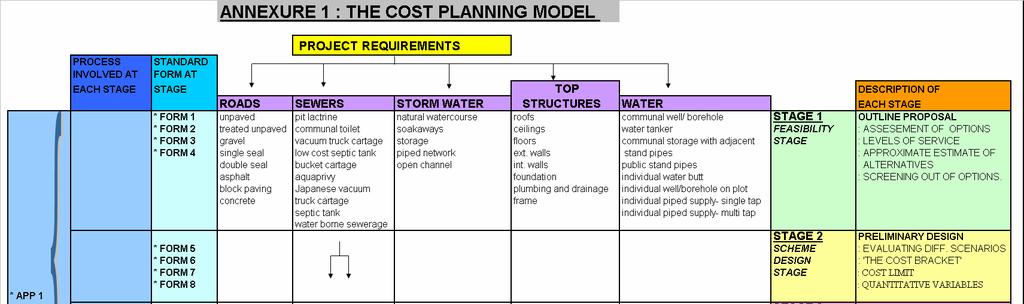

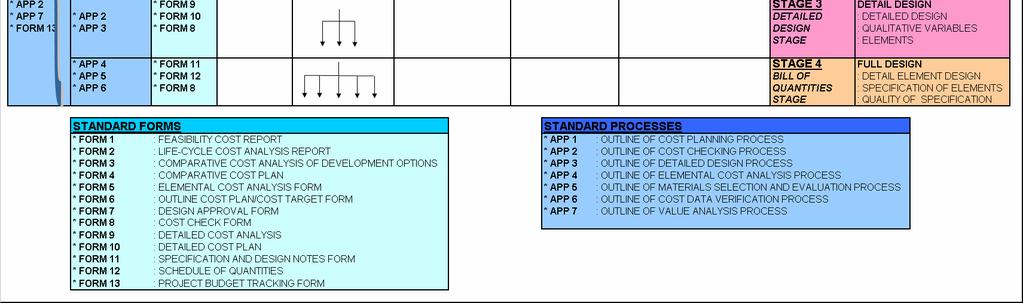

2 The essence of the cost model is to enable the engineer to control the cost of a project (within the target) while he is still designing. The earlier this process is introduced the greater the measure of control that can be exercised over ultimate cost, quality and design. This paper shows how different levels of cost estimate can be prepared in parallel with design development. The system allows for the various components of the costs to be estimated at their own discrete level, depending on the level of design information available. 2. OBJECTIVES OF THE COST FORMS The underlying purpose of this paper is to present the standard output forms of the cost planning model as shown in annexure 1. The standardised cost forms were developed to: Ensure that the work is carried out in a professional, competent and cost effective manner. Set out the methods by which deliverables may be obtained and verified. Determine the means by which goals can be quantified at early design stages. Measure, quantify and verify cost at any stage of design. Provide a basis for planning and budgeting. Develop a system of comparing a range of possible design alternatives at any stage in the design evolution and the forecasting of the economic effects upon the change of different variables or elements. Achieve the required balance of expenditure between the various elements of the project. Keep the expenditure within the amount allowed by the client 3. THE COST PLANNING MODEL METHODOLOGY Annexure 1 illustrates the conceptual model for cost forecasting at the different stages of design as well as standard forms for the analysis of the various options. (Saroop and Allopi, 2005a) The model was developed to provide clients and consultants with more control over the economic decisions taken in each design stage. It enables a rapid comparison of the options under consideration and assesses the cost of various engineering solutions as well as cost implications of certain parameters. This paper shows how different levels of cost estimate can be prepared in parallel with design development. The system allows for the various components of the costs to be estimated at their own discrete level, depending on the level of design information available. 4. COST REPORTS A cost report is a document that defines in a comprehensive, precise and verifiable manner, the essential characteristics of a deliverable. The standard forms shown in table 1 are not only concerned with what is specified, but also forms the foundation for an effective cost evaluation, which is laid down in these precise reports. It is used to measure, quantify, verify and audit the different design options on infrastructure projects. (Saroop and Allopi, 2005b)

3 A critical role identified for designers is that of optimal interaction with clients, particularly at the design brief stage. This is the most crucial phase for the successful completion of any project.. Design cost planning is particularly crucial as decisions made during the early stages of the development process carry more far reaching economic consequences than the relatively limited decisions which can be made later in the process. (Flanagan and Tate, 1997) Table 1. Standard forms for each stage. Stage Form No. Form Name FEASIBILITY STAGE SCHEME DESIGN STAGE DETAILED STAGE BILL OF QUANTITIES STAGE FORM 1 FORM 2 FORM 3 FORM 4 FORM 5 FORM 6 FORM 7 FORM 8 FORM 9 FORM 10 FORM 8 FORM 11 FORM 12 FORM 13 FORM 8 FEASIBILITY COST REPORT LIFE CYCLE COST ANALYSIS FORM COMPARATIVE DEVELOPMENT SCENARIO OPTIONS COMPARATIVE COST PLAN ELEMENTAL COST ANALYSIS COST TARGET FORM DESIGN REVIEW FORM COST CHECK FORM DETAILED COST ANALYSIS DETAILED COST PLAN COST CHECK FORM SPECIFICATION AND DESIGN NOTES FORM SCHEDULE OF QUANTITIES PROJECT BUDGET TRACKING FORM COST CHECK FORM (FINAL PRODUCTION) Form 1- Feasibility cost report During the first stage, as the brief is considered and developed, some idea of cost has to be established quickly. There may already be a budget limit but if not the client will need to know what order of cost is likely to be involved. The client may have a very firmly fixed budget and want to know what kind of level of services can be expected for the money Although there is bound to be much rethinking in the early stages, it is critically important to get as much as possible settled before it becomes increasingly expensive and unrealistic to make changes in design. The estimate is to be prepared on an elemental basis or unit method by comparisons of cost data available from previous similar projects. The cost of the desired alternative is computed and may be tabulated along with other cost combinations in a standard form called the feasibility cost report form. Form 2 Life cycle cost analysis form Most Civil Works projects represent major infrastructure investments for the nation, and are likely to remain in use indefinitely. Therefore, in addition to cost considerations, planning and design decisions need to be based on a consideration of the long-term performance of the project. Benefits and cost should be quantified and monetized to the maximum extent practicable. Benefits and costs should be measured and appropriately discounted over the full life cycle

4 of the project. Such analysis will enable informed tradeoffs among capital outlays, operating and maintenance costs, and non monetary costs borne by the public. These benefits are translated into measurable items in the life cycle cost form. Form 3 - Comparative development scenario options The basic method for identifying the costs of a project is to compare the costs and benefits that are likely to arise if a specific alternative is implemented, to the situation that would prevail if alternative design decisions were implemented. The alternative designs that were considered, are compared in this standard form. This method estimates the net savings on costs that are likely to be generated by the project alternatives and quantities. This form allows a comparative analysis of the different scenarios available to the client and their cost implications. Functions carried out at this stage include the following: Generation of options - For a comparison of reasonableness with other design alternatives, e.g. if stormwater pipes are costing far more than stormwater open channels, it is important in investigating the results of the different design options. A comparative evaluation of preferred options and major alternatives in the early stages of design should be done. Devising alternatives in response to the projects goals, objectives & constraints Evaluating options and impacts relative to its goals and objective Form 4 Comparative cost plan The Comparative cost plan involves presenting the refined cost-analysis of the various project options. The economic analysis guides the decision-makers by altering key design factors and assessing how and what costs should be increased. The comparative cost plan does not seek to enforce rigid cost limits for the design of particular elements, but rather to maintain flexibility of choice of a combination of possible design solutions, that will serve the purpose to be achieved. (Seeley, 1996) The comparative cost plan serves two important purposes: To confirm the budget already set; To allow the distribution of costs within the various functional elements to be made and to ensure that the distribution is appropriate for the needs of the project. Form 5 Elemental cost analysis form This form enables the user to evaluate different scenarios and change the value of a number of key variables, such as length of elements and number of elements, and go through the costing again. By setting out the budget based on these elements, budgetary control procedures can be adopted that will allow monitoring and correction of the design should it go outside the cost constrain (Cited by Ferry et al, 1999). The functions of the elemental cost analysis form are:

5 To compare the reasonableness of other design options, if stormwater pipes (for instance) are costing far more per metre than stormwater open channels or proportioning it over the project cost, it is worthwhile investigating the results of the different design options To determine the probable cost of each element of the project To show the distribution of cost of a project amongst its elements Form 6 - Cost target/limit form Once the sketch design has been completed and approved by the client, the task of allocating sums to the various elements can take place. The cost target is a statement of how the design team proposes to distribute the available money among the major elements of the project. A sum will eventually be agreed that will form the cost target for the whole scheme. Alternatively, a cost limit, once in operation, will become the cost target. This is largely the extent of the consultant s work at this stage, other than to advise on the cost of alternative methods of construction or matters, which have a contractual implication. There is no real point at this stage in formulating elemental targets, since design decisions still have to be made and the whole process could be a rather pointless exercise. If however, the proposed scheme is of a similar type to one already constructed, and a previous analysis is available and going to be followed in principle by the engineer, then these cost targets can be utilized, and they must be updated for inflation or regional factors Cost limits Definition-the sum of money, which the client considers, is the maximum that he is able and/or willing to pay for the building based on the amount that can be raised by grants, loans or other sources. The system of cost limits gives value for money in the public sector: Cost limits have been used for a large number of public construction projects. Their object is to establish a system limiting the expenditure on initial construction costs, but at the same time requiring a minimum standard of accommodation and specification. Housing cost yardsticks were first introduced in 1963 to keep down the costs of infrastructure services. In the absence of cost limits, housing standards and expenditure could reach high and unacceptable proportions. Form 7 - Design review form The design review is a coherent and systematic study of the design documents with the purpose of identifying problems and assessing the project s ability to fulfill specified and stipulated requirements. It is necessary to fix the time in the design stage when the design review is to be held. Usually, reviews are affected upon completion of the different steps of the design stage. Project details are gathered together under this form with considerable specification detail. It will also include a non-conformity section with reasons. Ashford describes design approval as a formal documented, comprehensive and systematic examination of a design to evaluate the design requirements and the capability

6 of the design to meet the requirements as well as to identify problems and proposed solution (Ashford, 1992). Having asked the necessary questions and recorded the responses, it is useful to assemble the design basis on a standard format. This enforces control in design stage. Design professionals should carry out one or more design reviews during the design stage. Form 8 - Cost check form. A process of checking the estimated cost of each section or element of the project as the detailed designs are developed, against the cost target set against it in the cost plan. The model makes provision for checking on a comprehensive basis whether costs are accurate by cost check forms. The check makes an adjustment of the design details, followed by a further feasibility. An analysis is then carried out to determine whether the performance requirements are satisfied. If not, a trial adjustment has to be made to the design details and a new analysis carried out in the search for a feasible solution. Analysis plays a comparable role in a planning problem. During the process of the consultants design, it is necessary that the total cost is not to be exceeded. Since the consultants will design in elements, it is convenient for the cost checks to be carried out on this basis and compared with the cost targets in the agreed cost plan. Form 9 - Detailed cost analysis The detailed cost analysis is the process of breaking down a complex product into its component parts before identifying different and hopefully more effective methods of achieving the desired result. It enables the designer to determine how much has been spent on each element and to show where reductions could be most beneficially made, should the estimate prove to be too high leading to more effective cost control. It is a systematic breakdown of cost data, to assist in the estimating of cost and in the cost planning of projects. It is essential for the planning team to take into consideration a range of possible variations in the values of project variables and test how such variations will affect the cost of the project. Apart from the quantitative variables there are also qualitative variables that affect the viability of the project. The reason for this is that a detailed cost analysis attempts to achieve a balanced design; so increasing the quality of the specification of the element is more likely to give the client good value for money than returning the savings to the client or distributing them among the other elements. This financial analysis translates the financial costs and benefits into economic costs and benefits by adjusting the project inputs and outputs for price distortions.

7 Form 10 Detailed cost plan The detailed cost plan involves presenting the refined detailed cost-analysis of the various items options of each element. The economic analysis guides the decision-makers by altering key design factors and assessing how and what costs should be increased. Definition- it is a statement of the proposed expenditure of each section or element to definite standard of quantity. Each item can be regarded as a cost target and is prepared in parallel with the detailed working drawings, and giving an itemized breakdown and outline specification of the cost allocation to design elements. It is more concerned with the comparison of each element s cost within a total sum, rather than attempting to control the design in relation to targets for sections of the work. Its objective is not necessarily to show how cheaply a project can be produced but to show the spread of costs over various parts of the project and what economies are feasible. This enables the engineer, within his cost terms of reference, to use the money to the best advantage in interpreting his design. This should lead to economy in design. This strategy will attempt to spend money in accordance with the client s requirements, by allocating sums of money to the various major components of the project. Form 11 Specification and design notes form The technical specifications form is required to ensure that the projects proposed are appropriate and feasible with respect to technical considerations and specifications. Technical specifications are used to define the product and to set out the acceptance criteria and resource specifications are used to define quality. These specifications not only define the deliverables which are to be realized in the process of delivery, but also set out the manner in which they can be achieved, measured and monitored. The function of this form is to check that the project elements will meet with the specified project requirements. The verification of compliance with specifications commences when materials are chosen for the design. This Procedure ensures that non-conforming materials are quarantined or otherwise prevented from being used. The cost analysis and estimate is supplemented with specification notes. 5. CONCLUSION The cost planning model and its outputs is a disciplined effort to produce fundamental decisions in shaping the project cost. The process must be seen as an integrated whole in order to maximise the opportunities for improving quality and reducing project costs. This will place a heavy burden on the consultants to use client s money in the most efficient way possible. Cost planning should be a continuous process, with progressive checks being made from time to time in relatively more detail on perhaps smaller sections of the project as the design is finalized. Another merit of cost planning is that it introduces a positive checking procedure into the design stage where previously nothing systematic had existed. This paper shows how different levels of cost estimate can be prepared in parallel with design development. The system allows for the various components of the costs to be

8 estimated at their own discrete level, depending on the level of design information available. Each of the standard forms has a measurable component, which enables the cost of each design component to be quantified. The cost model not only promotes cost effective options but extends into accelerated service provision sustainable infrastructure. The output reports referred to, in the cost-planning model serve to support decisionmaking and management functions. They are distinguished from textbook definitions in that they are more practical in application. By the complementary role of preliminary cost reporting in overall project performance, it is sure to enhance cost, productivity, quality and time The goal for continuous improvement in the infrastructure sector can be achieved through the proposed framework. This, together with basic principles of cost planning and construction economics can contribute to the concept of affordable township infrastructure and will result in a delivery system that becomes more efficient and effective. 6. REFERENCES [1] Ashford, J. L., 1992, The Management of Quality in Construction, E & F N Spon, London.pp [2] Ferry, D J, Brandon, P S, and Ferry, J (1999) Cost Planning of Buildings. 7ed. Blackwell science Ltd. [3] Flanagan, R. and Tate, B., 1997, Cost control in building design, Blackwell science LTD, London. pp. 285 [4] Saroop, S H and Allopi D A cost model for the evaluation of different options in township infrastructure projects, Proceedings of the 24 th Annual Southern African Transport Conference (SATC 2005), Pretoria, South Africa, 2005a, p [5] Saroop, S H and Allopi D A costing methodology for the evaluating infrastructure design, Journal of the Institution of Municipal Engineering of Southern Africa (IMESA), Volume 30, Number 11, December 2005b, p33-37 [6] Seeley, I. H., 1996, Building Economics (4 th ed.), Macmillan Press LTD, Malaysia. pp.190

9

A. Risk Management Framework

1 August 2002 - Page 1 A. Risk Management Framework A.1. Risk Management Process Definition of Risk Management Banking risk management includes all the activities and systems that contribute to: # Assessing

1 August 2002 - Page 1 A. Risk Management Framework A.1. Risk Management Process Definition of Risk Management Banking risk management includes all the activities and systems that contribute to: # Assessing

june 07 tpp 07-3 Service Costing in General Government Sector Agencies OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper

june 07 Service Costing in General Government Sector Agencies OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper Contents: Page Preface Executive Summary 1 2 1 Service Costing in the General Government

june 07 Service Costing in General Government Sector Agencies OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper Contents: Page Preface Executive Summary 1 2 1 Service Costing in the General Government

Investing in Hedge Funds

The aim of investing in hedge funds is to gain exposure to some actively managed strategies that delivers exceptional returns uncorrelated to other investment strategies. An investment in hedge funds could

The aim of investing in hedge funds is to gain exposure to some actively managed strategies that delivers exceptional returns uncorrelated to other investment strategies. An investment in hedge funds could

Terms of Reference for an Individual National Consultant to conduct the testing of the TrackFin Methodology in Uganda.

Terms of Reference for an Individual National Consultant to conduct the testing of the TrackFin Methodology in Uganda 21 July, 2017 Introduction: The Ministry of Water and Environment (MWE) is implementing

Terms of Reference for an Individual National Consultant to conduct the testing of the TrackFin Methodology in Uganda 21 July, 2017 Introduction: The Ministry of Water and Environment (MWE) is implementing

IMESA. Johan van den Berg (Strategic and Integrated Planning) Dr Danie Wium (Industry Leader, Government) Aurecon

Dr Danie Wium (Industry Leader, Government) Aurecon") Johan van den Berg (Strategic and Integrated Planning) Dr Danie Wium (Industry Leader, Government) Aurecon ABSTRACT The Consolidated Infrastructure Plan (CIP) is an initiative of the City growth needs.

Johan van den Berg (Strategic and Integrated Planning) Dr Danie Wium (Industry Leader, Government) Aurecon ABSTRACT The Consolidated Infrastructure Plan (CIP) is an initiative of the City growth needs.

ST/SGB/2018/3 1 June United Nations

1 June 2018 United Nations Regulations and Rules Governing Programme Planning, the Programme Aspects of the Budget, the Monitoring of Implementation and the Methods of Evaluation Secretary-General s bulletin

1 June 2018 United Nations Regulations and Rules Governing Programme Planning, the Programme Aspects of the Budget, the Monitoring of Implementation and the Methods of Evaluation Secretary-General s bulletin

Braindumps.PRINCE2-Foundation.150.QA

Braindumps.PRINCE2-Foundation.150.QA Number: PRINCE2-Foundation Passing Score: 800 Time Limit: 120 min File Version: 29.1 http://www.gratisexam.com/ I was a little apprehensive at first about an online

Braindumps.PRINCE2-Foundation.150.QA Number: PRINCE2-Foundation Passing Score: 800 Time Limit: 120 min File Version: 29.1 http://www.gratisexam.com/ I was a little apprehensive at first about an online

Investing in the future

Investing in the future Using value creation and value capture to fund the infrastructure our cities need Submission responding to the Discussion Paper issued by Department of Infrastructure and Regional

Investing in the future Using value creation and value capture to fund the infrastructure our cities need Submission responding to the Discussion Paper issued by Department of Infrastructure and Regional

Joint Venture on Managing for Development Results

Joint Venture on Managing for Development Results Managing for Development Results - Draft Policy Brief - I. Introduction Managing for Development Results (MfDR) Draft Policy Brief 1 Managing for Development

Joint Venture on Managing for Development Results Managing for Development Results - Draft Policy Brief - I. Introduction Managing for Development Results (MfDR) Draft Policy Brief 1 Managing for Development

Actualtests.PRINCE2Foundation.120questions

Actualtests.PRINCE2Foundation.120questions Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version: 4.8 http://www.gratisexam.com/ PRINCE2 Foundation PRINCE2 Foundation written Exam 1. Dump

Actualtests.PRINCE2Foundation.120questions Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version: 4.8 http://www.gratisexam.com/ PRINCE2 Foundation PRINCE2 Foundation written Exam 1. Dump

Risk management as an element of processes continuity assurance

Available online at www.sciencedirect.com ScienceDirect Procedia Engineering 63 ( 2013 ) 873 877 The Manufacturing Engineering Society International Conference, MESIC 2013 Risk management as an element

Available online at www.sciencedirect.com ScienceDirect Procedia Engineering 63 ( 2013 ) 873 877 The Manufacturing Engineering Society International Conference, MESIC 2013 Risk management as an element

VOLTA RIVER AUTHORITY

VOLTA RIVER AUTHORITY Capital Expenditure Guidelines November 2012 TABLE OF CONTENTS PAGE 1.0 Purpose and Scope of Guidelines...3 2.0 Projects Guidelines Apply To....4 3.0 Exemptions from Guidelines...4

VOLTA RIVER AUTHORITY Capital Expenditure Guidelines November 2012 TABLE OF CONTENTS PAGE 1.0 Purpose and Scope of Guidelines...3 2.0 Projects Guidelines Apply To....4 3.0 Exemptions from Guidelines...4

VALUE FOR MONEY AND FACILITIES PERFORMANCE: A SYSTEMS APPROACH

VALUE FOR MONEY AND FACILITIES PERFORMANCE: A SYSTEMS APPROACH David Rutter and Kassim Gidado School of the Environment, University of Brighton, Brighton, BN25GJ One of the central arguments for procuring

VALUE FOR MONEY AND FACILITIES PERFORMANCE: A SYSTEMS APPROACH David Rutter and Kassim Gidado School of the Environment, University of Brighton, Brighton, BN25GJ One of the central arguments for procuring

FRAMEWORK FOR SUPERVISORY INFORMATION

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

Working Paper #1. Optimizing New York s Reforming the Energy Vision

Center for Energy, Economic & Environmental Policy Rutgers, The State University of New Jersey 33 Livingston Avenue, First Floor New Brunswick, NJ 08901 http://ceeep.rutgers.edu/ 732-789-2750 Fax: 732-932-0394

Center for Energy, Economic & Environmental Policy Rutgers, The State University of New Jersey 33 Livingston Avenue, First Floor New Brunswick, NJ 08901 http://ceeep.rutgers.edu/ 732-789-2750 Fax: 732-932-0394

Learning Objectives. Learning Objectives 17/03/2016. Chapter 7 Establishing Objectives and Budgeting for the Promotional Program

Chapter 7 Establishing Objectives and Budgeting for the Promotional Program Copyright 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

Chapter 7 Establishing Objectives and Budgeting for the Promotional Program Copyright 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

ANNEX 4 REPORT OF THE STANDING COMMITTEE ON ADMINISTRATION AND FINANCE (SCAF)

") ANNEX 4 REPORT OF THE STANDING COMMITTEE ON ADMINISTRATION AND FINANCE (SCAF) REPORT OF THE STANDING COMMITTEE ON ADMINISTRATION AND FINANCE (SCAF) The following agenda items were considered by the Standing

ANNEX 4 REPORT OF THE STANDING COMMITTEE ON ADMINISTRATION AND FINANCE (SCAF) REPORT OF THE STANDING COMMITTEE ON ADMINISTRATION AND FINANCE (SCAF) The following agenda items were considered by the Standing

Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test

Use Test") Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document

Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document

Recommendation of the Council on Good Practices for Public Environmental Expenditure Management

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

Recommendation of the Council on for Public Environmental Expenditure Management ENVIRONMENT 8 June 2006 - C(2006)84 THE COUNCIL, Having regard to Article 5 b) of the Convention on the Organisation for

KEY GUIDE The key stages of financial planning

Kelvin Financial Planning Ltd KEY GUIDE The key stages of financial planning Financial planning is a relatively new profession, so it is not surprising that most people are vague about what financial planners

Kelvin Financial Planning Ltd KEY GUIDE The key stages of financial planning Financial planning is a relatively new profession, so it is not surprising that most people are vague about what financial planners

City Prosperity Initiative Conceptualization and Application

City Prosperity Initiative Conceptualization and Application Antony Abilla ; UN-Habitat Bangkok, Thailand The Origin of the Initiative In 2012, UN-Habitat created the City Prosperity Index - a tool to

City Prosperity Initiative Conceptualization and Application Antony Abilla ; UN-Habitat Bangkok, Thailand The Origin of the Initiative In 2012, UN-Habitat created the City Prosperity Index - a tool to

EFFICIENCY OF REPRODUCTION OF FIXED ASSETS IN POLISH AGRICULTURE

182 Bulgarian Journal of Agricultural Science, 22 (No 2) 2016, 182 187 Agricultural Academy EFFICIENCY OF REPRODUCTION OF FIXED ASSETS IN POLISH AGRICULTURE J. ZWOLAK 1 and M. KULYNYCH 2 1 University of

182 Bulgarian Journal of Agricultural Science, 22 (No 2) 2016, 182 187 Agricultural Academy EFFICIENCY OF REPRODUCTION OF FIXED ASSETS IN POLISH AGRICULTURE J. ZWOLAK 1 and M. KULYNYCH 2 1 University of

Comment Letter on the Discussion Paper: A Review of the Conceptual Framework for Financial Reporting

Verband der Industrie- und Dienstleistungskonzerne in der Schweiz Fédération des groupes industriels et de services en Suisse Federation of Industrial and Service Groups in Switzerland 14 January 2014

Verband der Industrie- und Dienstleistungskonzerne in der Schweiz Fédération des groupes industriels et de services en Suisse Federation of Industrial and Service Groups in Switzerland 14 January 2014

Sheila Belayutham CHAPTER 6 CONTROL

CHAPTER 6 CONTROL LEARNING OUTCOME Students will be able to: Understand monitoring and control in construction. Understand the monitoring and control methods in construction. MONITORING & CONTROL It s

CHAPTER 6 CONTROL LEARNING OUTCOME Students will be able to: Understand monitoring and control in construction. Understand the monitoring and control methods in construction. MONITORING & CONTROL It s

PRINCE2-PRINCE2-Foundation.150q

PRINCE2-PRINCE2-Foundation.150q Number: PRINCE2-Foundation Passing Score: 800 Time Limit: 120 min File Version: 6.0 Exam PRINCE2-Foundation Version: 6.0 Exam A QUESTION 1 What process ensures focus on

PRINCE2-PRINCE2-Foundation.150q Number: PRINCE2-Foundation Passing Score: 800 Time Limit: 120 min File Version: 6.0 Exam PRINCE2-Foundation Version: 6.0 Exam A QUESTION 1 What process ensures focus on

TSHWANE BRT: Development of a Traffic Model for the BRT Corridor Phase 1A Lines 1 and 2

TSHWANE BRT: Development of a Traffic Model for the BRT Corridor Phase 1A Lines 1 and 2 L RETIEF, B LORIO, C CAO* and H VAN DER MERWE** TECHSO, P O Box 35, Innovation Hub, 0087 *Mouchel Group, 307-317,

TSHWANE BRT: Development of a Traffic Model for the BRT Corridor Phase 1A Lines 1 and 2 L RETIEF, B LORIO, C CAO* and H VAN DER MERWE** TECHSO, P O Box 35, Innovation Hub, 0087 *Mouchel Group, 307-317,

Solvency II: Orientation debate Design of a future prudential supervisory system in the EU

MARKT/2503/03 EN Orig. Solvency II: Orientation debate Design of a future prudential supervisory system in the EU (Recommendations by the Commission Services) Commission européenne, B-1049 Bruxelles /

MARKT/2503/03 EN Orig. Solvency II: Orientation debate Design of a future prudential supervisory system in the EU (Recommendations by the Commission Services) Commission européenne, B-1049 Bruxelles /

European Railway Agency Recommendation on the 1 st set of Common Safety Methods (ERA-REC SAF)

") European Railway Agency Recommendation on the 1 st set of Common Safety Methods (ERA-REC-02-2007-SAF) The Director, Having regard to the Directive 2004/49/EC 1 of the European Parliament, Having regard

European Railway Agency Recommendation on the 1 st set of Common Safety Methods (ERA-REC-02-2007-SAF) The Director, Having regard to the Directive 2004/49/EC 1 of the European Parliament, Having regard

The 7 th International Scientific Conference DEFENSE RESOURCES MANAGEMENT IN THE 21st CENTURY Braşov, November 15 th 2012

The 7 th International Scientific Conference DEFENSE RESOURCES MANAGEMENT IN THE 21st CENTURY Braşov, November 15 th 2012 THE PLANNING-PROGRAMMING-BUDGETING SYSTEM LTC Valentin PÎRVUŢ Land Forces Academy

The 7 th International Scientific Conference DEFENSE RESOURCES MANAGEMENT IN THE 21st CENTURY Braşov, November 15 th 2012 THE PLANNING-PROGRAMMING-BUDGETING SYSTEM LTC Valentin PÎRVUŢ Land Forces Academy

PROJECT CYCLE MANAGEMENT & LOGICAL FRAMEWORK MATRIX TRAINING CYPRIOT CIVIL SOCIETY IN ACTION V INNOVATION AND CHANGES IN EDUCATION VI

PROJECT CYCLE MANAGEMENT & LOGICAL FRAMEWORK MATRIX TRAINING CYPRIOT CIVIL SOCIETY IN ACTION V INNOVATION AND CHANGES IN EDUCATION VI Objectives of the training Understand the definition of project and

PROJECT CYCLE MANAGEMENT & LOGICAL FRAMEWORK MATRIX TRAINING CYPRIOT CIVIL SOCIETY IN ACTION V INNOVATION AND CHANGES IN EDUCATION VI Objectives of the training Understand the definition of project and

A guide to reviewing the. recommendations of the Retirement. Options Task Force. J. Daniel Hare *

A guide to reviewing the recommendations of the Retirement Options Task Force J. Daniel Hare * James A. Chalfant ** January 15, 2016 The report from the Retirement Options Task Force is lengthy and complex.

A guide to reviewing the recommendations of the Retirement Options Task Force J. Daniel Hare * James A. Chalfant ** January 15, 2016 The report from the Retirement Options Task Force is lengthy and complex.

KEY GUIDE. The key stages of financial planning

KEY GUIDE The key stages of financial planning What can financial planning do for you? Financial planning has witnessed significant change, so it is not surprising that most people are unclear about what

KEY GUIDE The key stages of financial planning What can financial planning do for you? Financial planning has witnessed significant change, so it is not surprising that most people are unclear about what

STOCHASTIC COST ESTIMATION AND RISK ANALYSIS IN MANAGING SOFTWARE PROJECTS

Full citation: Connor, A.M., & MacDonell, S.G. (25) Stochastic cost estimation and risk analysis in managing software projects, in Proceedings of the ISCA 14th International Conference on Intelligent and

Full citation: Connor, A.M., & MacDonell, S.G. (25) Stochastic cost estimation and risk analysis in managing software projects, in Proceedings of the ISCA 14th International Conference on Intelligent and

Project Title: INFRASTRUCTURE AND INTEGRATED TOOLS FOR PERSONALIZED LEARNING OF READING SKILL

Project Title: INFRASTRUCTURE AND INTEGRATED TOOLS FOR PERSONALIZED LEARNING OF READING SKILL Project Acronym: Grant Agreement number: 731724 iread H2020-ICT-2016-2017/H2020-ICT-2016-1 Subject: Dissemination

Project Title: INFRASTRUCTURE AND INTEGRATED TOOLS FOR PERSONALIZED LEARNING OF READING SKILL Project Acronym: Grant Agreement number: 731724 iread H2020-ICT-2016-2017/H2020-ICT-2016-1 Subject: Dissemination

User-tailored fuzzy relations between intervals

User-tailored fuzzy relations between intervals Dorota Kuchta Institute of Industrial Engineering and Management Wroclaw University of Technology ul. Smoluchowskiego 5 e-mail: Dorota.Kuchta@pwr.wroc.pl

User-tailored fuzzy relations between intervals Dorota Kuchta Institute of Industrial Engineering and Management Wroclaw University of Technology ul. Smoluchowskiego 5 e-mail: Dorota.Kuchta@pwr.wroc.pl

Paper P2 PERFORMANCE MANAGEMENT. Acorn Chapters

Paper P2 PERFORMANCE MANAGEMENT Acorn Chapters 1 Relevant costing 2 Learning curve theory 3 Pricing 4 Budgeting 5 Break-even analysis (CVP analysis) 6 Activity based costing 7 Modern manufacturing techniques

Paper P2 PERFORMANCE MANAGEMENT Acorn Chapters 1 Relevant costing 2 Learning curve theory 3 Pricing 4 Budgeting 5 Break-even analysis (CVP analysis) 6 Activity based costing 7 Modern manufacturing techniques

Sustainability of Earnings: A Framework for Quantitative Modeling of Strategy, Risk, and Value

Sustainability of Earnings: A Framework for Quantitative Modeling of Strategy, Risk, and Value Neil M. Bodoff, FCAS, MAAA Abstract The value of a firm derives from its future cash flows, adjusted for risk,

Sustainability of Earnings: A Framework for Quantitative Modeling of Strategy, Risk, and Value Neil M. Bodoff, FCAS, MAAA Abstract The value of a firm derives from its future cash flows, adjusted for risk,

PENSION MATHEMATICS with Numerical Illustrations

PENSION MATHEMATICS with Numerical Illustrations Second Edition Howard E. Winklevoss, Ph.D., MAAA, EA President Winklevoss Consultants, Inc. Published by Pension Research Council Wharton School of the

PENSION MATHEMATICS with Numerical Illustrations Second Edition Howard E. Winklevoss, Ph.D., MAAA, EA President Winklevoss Consultants, Inc. Published by Pension Research Council Wharton School of the

Prince2 Foundation.exam.160q

Prince2 Foundation.exam.160q Number: Prince2 Foundation Passing Score: 800 Time Limit: 120 min PRINCE2 Foundation PRINCE2 Foundation written Exam Sections 1. Volume A 2. Volume B Exam A QUESTION 1 Which

Prince2 Foundation.exam.160q Number: Prince2 Foundation Passing Score: 800 Time Limit: 120 min PRINCE2 Foundation PRINCE2 Foundation written Exam Sections 1. Volume A 2. Volume B Exam A QUESTION 1 Which

executive summary ExEcuTivE SuMMAry

executive summary 1 British Energy was privatised in 1996. In 2002, the price of electricity fell and on 5 September 2002, the Company applied to the Department of Trade and Industry (the Department) for

executive summary 1 British Energy was privatised in 1996. In 2002, the price of electricity fell and on 5 September 2002, the Company applied to the Department of Trade and Industry (the Department) for

INTEGRATING RISK AND EARNED VALUE MANAGEMENT

INTEGRATING RISK AND EARNED VALUE MANAGEMENT A White Paper Contents Introduction... 3 Integrating Risk and Earned Value Management Processes... 3 Using Risk Mitigation to Improve Value... 4 An Integrated

INTEGRATING RISK AND EARNED VALUE MANAGEMENT A White Paper Contents Introduction... 3 Integrating Risk and Earned Value Management Processes... 3 Using Risk Mitigation to Improve Value... 4 An Integrated

machine design, Vol.7(2015) No.4, ISSN pp

No.4, ISSN pp") machine design, Vol.7(205) No.4, ISSN 82-259 pp. 9-24 Research paper ANALYSIS AND RISK ASSESSMENT OF IMPLEMENTATION OF THE AUTOMATED CAR PARKING SYSTEM PROJECT Radoslav TOMOVIĆ, * - Rade GRUJIČIĆ University

machine design, Vol.7(205) No.4, ISSN 82-259 pp. 9-24 Research paper ANALYSIS AND RISK ASSESSMENT OF IMPLEMENTATION OF THE AUTOMATED CAR PARKING SYSTEM PROJECT Radoslav TOMOVIĆ, * - Rade GRUJIČIĆ University

A Simple Model of Bank Employee Compensation

Federal Reserve Bank of Minneapolis Research Department A Simple Model of Bank Employee Compensation Christopher Phelan Working Paper 676 December 2009 Phelan: University of Minnesota and Federal Reserve

Federal Reserve Bank of Minneapolis Research Department A Simple Model of Bank Employee Compensation Christopher Phelan Working Paper 676 December 2009 Phelan: University of Minnesota and Federal Reserve

PFI PROJECTS: THEIR SCOPE FOR DELIVERING VFM

PFI PROJECTS: THEIR SCOPE FOR DELIVERING VFM David Rutter and Kassim Gidado School of The Environment, University of Brighton, Brighton, BN24GJ One of the key initial requirements for Private Finance Initiative

PFI PROJECTS: THEIR SCOPE FOR DELIVERING VFM David Rutter and Kassim Gidado School of The Environment, University of Brighton, Brighton, BN24GJ One of the key initial requirements for Private Finance Initiative

Reading notes. Determine client s financial needs and risk. A client's needs. Introduction. 'Fact finder'

Reading notes Determine client s financial needs and risk Introduction This learning resource examines how to meet a client s specific financial needs. Specifically, it addresses: the six steps that need

Reading notes Determine client s financial needs and risk Introduction This learning resource examines how to meet a client s specific financial needs. Specifically, it addresses: the six steps that need

UNIT 11: STANDARD COSTING

UNIT 11: STANDARD COSTING Introduction One of the prime functions of management accounting is to facilitate managerial control and the important aspect of managerial control is cost control. The efficiency

UNIT 11: STANDARD COSTING Introduction One of the prime functions of management accounting is to facilitate managerial control and the important aspect of managerial control is cost control. The efficiency

STOCHASTIC COST ESTIMATION AND RISK ANALYSIS IN MANAGING SOFTWARE PROJECTS

STOCHASTIC COST ESTIMATION AND RISK ANALYSIS IN MANAGING SOFTWARE PROJECTS Dr A.M. Connor Software Engineering Research Lab Auckland University of Technology Auckland, New Zealand andrew.connor@aut.ac.nz

STOCHASTIC COST ESTIMATION AND RISK ANALYSIS IN MANAGING SOFTWARE PROJECTS Dr A.M. Connor Software Engineering Research Lab Auckland University of Technology Auckland, New Zealand andrew.connor@aut.ac.nz

What can be learned from ImPRovEfor Horizon 2020?

What can be learned from ImPRovEfor Horizon 2020? RETHINKING THE ROLE OF SOCIAL SCIENCES (SSH) IN H2020 Tim Goedemé, PhD University of Antwerp Herman Deleeck Centre for Social Policy (CSB) 26-02-2015 Brussels

What can be learned from ImPRovEfor Horizon 2020? RETHINKING THE ROLE OF SOCIAL SCIENCES (SSH) IN H2020 Tim Goedemé, PhD University of Antwerp Herman Deleeck Centre for Social Policy (CSB) 26-02-2015 Brussels

RETURN ON RISK MANAGEMENT. Financial Services

RETURN ON RISK MANAGEMENT Financial Services RETURN ON RISK MANAGEMENT The global financial crisis revealed major risk management deficiencies across the banking industry. Governments and regulators have

RETURN ON RISK MANAGEMENT Financial Services RETURN ON RISK MANAGEMENT The global financial crisis revealed major risk management deficiencies across the banking industry. Governments and regulators have

MAXIMISE THE LEVEL OF SERVICE USING CROSS ASSET PORTFOLIO RENEWALS MANAGEMENT

Mason, Rangamuwa, Henning Page 1 of 15 MAXIMISE THE LEVEL OF SERVICE USING CROSS ASSET PORTFOLIO RENEWALS MANAGEMENT Michael Mason 1, Siri Rangamuwa 1, Theunis F. P Henning 2 Corresponding Author: Michael

Mason, Rangamuwa, Henning Page 1 of 15 MAXIMISE THE LEVEL OF SERVICE USING CROSS ASSET PORTFOLIO RENEWALS MANAGEMENT Michael Mason 1, Siri Rangamuwa 1, Theunis F. P Henning 2 Corresponding Author: Michael

3 rd FT-YES BANK International Banking Summit

3 rd FT-YES BANK International Banking Summit The Transformation of Global Banking: Gearing up for Renewed Growth? 24-25 October 2013 Taj Mahal Palace, Mumbai, India Overview Global banking is undergoing

3 rd FT-YES BANK International Banking Summit The Transformation of Global Banking: Gearing up for Renewed Growth? 24-25 October 2013 Taj Mahal Palace, Mumbai, India Overview Global banking is undergoing

Research on Financial Budget Performance Audit Platform Construction By Information System. Fangjie Wei 1, a

International Conference on Education, Management and Computing Technology (ICEMCT 2015) Research on Financial Budget Performance Audit Platform Construction By Information System Fangjie Wei 1, a 1 Shanghai

International Conference on Education, Management and Computing Technology (ICEMCT 2015) Research on Financial Budget Performance Audit Platform Construction By Information System Fangjie Wei 1, a 1 Shanghai

Inform Practice Note #8

Inform Practice Note #8 August 2008 (Version 2 - October 2008) Remunerating Professional Service Providers cidb s Inform Practice notes provide guidance and clarity in achieving client objectives in construction

Inform Practice Note #8 August 2008 (Version 2 - October 2008) Remunerating Professional Service Providers cidb s Inform Practice notes provide guidance and clarity in achieving client objectives in construction

NEPAD/Spanish Fund for African Women s empowerment

NEPAD/Spanish Fund for African Women s empowerment Project Proposal Format Annex 0 1 P age Proposal Format Proposal Cover Page: PROPOSAL TO THE NEPAD- SPANISH FUND FOR AFRICAN WOMEN s EMPOWERMENT Organization

NEPAD/Spanish Fund for African Women s empowerment Project Proposal Format Annex 0 1 P age Proposal Format Proposal Cover Page: PROPOSAL TO THE NEPAD- SPANISH FUND FOR AFRICAN WOMEN s EMPOWERMENT Organization

PROGRESS WITH THE NATIONAL INFRASTRUCTURE MAINTENANCE STRATEGY

PROGRESS WITH THE NATIONAL INFRASTRUCTURE MAINTENANCE STRATEGY Kevin Wall CSIR, P.O. Box 395, Pretoria, 0001; Cell: 082-4593618, Email: kwall@csir.co.za ABSTRACT The National Infrastructure Maintenance

PROGRESS WITH THE NATIONAL INFRASTRUCTURE MAINTENANCE STRATEGY Kevin Wall CSIR, P.O. Box 395, Pretoria, 0001; Cell: 082-4593618, Email: kwall@csir.co.za ABSTRACT The National Infrastructure Maintenance

Performance Budgeting in Australia

ISSN 1608-7143 OECD Journal on Budgeting Volume 7 No. 3 OECD 2007 Chapter 1 Performance Budgeting in Australia by Lewis Hawke* This article describes how the principles of management for results have worked

ISSN 1608-7143 OECD Journal on Budgeting Volume 7 No. 3 OECD 2007 Chapter 1 Performance Budgeting in Australia by Lewis Hawke* This article describes how the principles of management for results have worked

Small and Medium Sized Business (Finance Platforms) Regulations ABFA Policy Guidance

Regulations ABFA Policy Guidance") Small and Medium Sized Business (Finance Platforms) Regulations 2016 1. INTRODUCTION ABFA Policy Guidance 1.1. The Small and Medium Sized Business (Finance Platforms) Regulations (laid under the Small

Small and Medium Sized Business (Finance Platforms) Regulations 2016 1. INTRODUCTION ABFA Policy Guidance 1.1. The Small and Medium Sized Business (Finance Platforms) Regulations (laid under the Small

Available online at ScienceDirect. Procedia Economics and Finance 34 ( 2015 )

") Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 34 ( 2015 ) 187 193 Business Economics and Management 2015 Conference, BEM2015 The Importance of Investment Audit

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 34 ( 2015 ) 187 193 Business Economics and Management 2015 Conference, BEM2015 The Importance of Investment Audit

DECISION 22/2016/GB OF THE GOVERNING BOARD OF THE EUROPEAN POLICE COLLEGE ADOPTING CEPOL S EXTERNAL RELATIONS SUB-STRATEGY

DECISION 22/2016/GB OF THE GOVERNING BOARD OF THE EUROPEAN POLICE COLLEGE ADOPTING CEPOL S EXTERNAL RELATIONS SUB-STRATEGY Adopted by the Governing Board by written procedure on 12 July 2016 CEPOL CEPOL

DECISION 22/2016/GB OF THE GOVERNING BOARD OF THE EUROPEAN POLICE COLLEGE ADOPTING CEPOL S EXTERNAL RELATIONS SUB-STRATEGY Adopted by the Governing Board by written procedure on 12 July 2016 CEPOL CEPOL

Time boxing planning: Buffered Moscow rules

Time boxing planning: ed Moscow rules Eduardo Miranda Institute for Software Research Carnegie Mellon University ABSTRACT Time boxing is a management technique which prioritizes schedule over deliverables

Time boxing planning: ed Moscow rules Eduardo Miranda Institute for Software Research Carnegie Mellon University ABSTRACT Time boxing is a management technique which prioritizes schedule over deliverables

Decision Support Methods for Climate Change Adaption

Decision Support Methods for Climate Change Adaption 5 Summary of Methods and Case Study Examples from the MEDIATION Project Key Messages There is increasing interest in the appraisal of options, as adaptation

Decision Support Methods for Climate Change Adaption 5 Summary of Methods and Case Study Examples from the MEDIATION Project Key Messages There is increasing interest in the appraisal of options, as adaptation

STRATEGIC PLANNING PROCESS (2017) 1.1 The Association s strategic planning framework consists of the preparation of the following documents;

1.1 The Association s strategic planning framework consists of the preparation of the following documents;") 1.0 INTRODUCTION STRATEGIC PLANNING PROCESS (2017) 1.1 The Association s strategic planning framework consists of the preparation of the following documents; Corporate Management Plan Departmental Service

1.0 INTRODUCTION STRATEGIC PLANNING PROCESS (2017) 1.1 The Association s strategic planning framework consists of the preparation of the following documents; Corporate Management Plan Departmental Service

ECONOMIC PROCESSES IN PUBLIC SECTOR

Advanced Logistic Systems Vol. 8, No. 2 (2014) pp. 51-62 ECONOMIC PROCESSES IN PUBLIC SECTOR ZOLTÁN MEZEI 1 ÁKOS GUBÁN 2 Abstract: The research team called LOST (Logistification and Standardization Techniques)

Advanced Logistic Systems Vol. 8, No. 2 (2014) pp. 51-62 ECONOMIC PROCESSES IN PUBLIC SECTOR ZOLTÁN MEZEI 1 ÁKOS GUBÁN 2 Abstract: The research team called LOST (Logistification and Standardization Techniques)

Turkey: Credit Shock & the Economy

Turkey: Credit Shock & the Economy The effects of Credit Guarantee Fund (KGF) on the Turkish economy Alvaro Ortiz October 10 th 2017 The Credit Guarantee Fund (KGF) was implemented in March 2017 as a countercyclical

Turkey: Credit Shock & the Economy The effects of Credit Guarantee Fund (KGF) on the Turkish economy Alvaro Ortiz October 10 th 2017 The Credit Guarantee Fund (KGF) was implemented in March 2017 as a countercyclical

Appendix C: Economic Analysis of Natural Hazard Mitigation Projects

Appendix C: Economic Analysis of Natural Hazard Mitigation Projects This appendix was developed by the Oregon Partnership for Disaster Resilience at the University of Oregon s Community Service Center.

Appendix C: Economic Analysis of Natural Hazard Mitigation Projects This appendix was developed by the Oregon Partnership for Disaster Resilience at the University of Oregon s Community Service Center.

Plan PURPOSE OF THE PRACTICE NOTE

Practice note number 6: Compilation of the Business Rescue Plan PURPOSE OF THE PRACTICE NOTE To provide guidelines to Business Rescue Practitioners ( BRP ) in drawing up Business Rescue Plans ( BR Plan

Practice note number 6: Compilation of the Business Rescue Plan PURPOSE OF THE PRACTICE NOTE To provide guidelines to Business Rescue Practitioners ( BRP ) in drawing up Business Rescue Plans ( BR Plan

Risk Concentrations Principles

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Possibility of Using Value Engineering in Highway Projects

Creative Construction Conference 2016 Possibility of Using Value Engineering in Highway Projects Renata Schneiderova Heralova Czech Technical University in Prague, Faculty of Civil Engineering, Thakurova

Creative Construction Conference 2016 Possibility of Using Value Engineering in Highway Projects Renata Schneiderova Heralova Czech Technical University in Prague, Faculty of Civil Engineering, Thakurova

FUNCTIONS AND STRUCTURE OF THE PLANNING COMMISSION ( IN BRIEF )

") FUNCTIONS AND STRUCTURE OF THE PLANNING COMMISSION ( IN BRIEF ) Planning Commission was set up in March, 1950. A copy of the Resolution of Government of India has been given in Unit I of this document.

FUNCTIONS AND STRUCTURE OF THE PLANNING COMMISSION ( IN BRIEF ) Planning Commission was set up in March, 1950. A copy of the Resolution of Government of India has been given in Unit I of this document.

INVESTMENT AND FINANCING DECISION MAKING IN THE INDUSTRIAL COMPANY

INVESTMENT AND FINANCING DECISION MAKING IN THE INDUSTRIAL COMPANY Abstract doc. Ing. Jaroslava Kádárová, PhD. Technical Universityof Košice, Faculty of Mechanical Engineering, Department of Industrial

INVESTMENT AND FINANCING DECISION MAKING IN THE INDUSTRIAL COMPANY Abstract doc. Ing. Jaroslava Kádárová, PhD. Technical Universityof Košice, Faculty of Mechanical Engineering, Department of Industrial

Project Cycle Management and How To Write A Good Proposal. Eng. Suhail and Ayman Sultan Palestine Polytechnic University Ramallah April

Project Cycle Management and How To Write A Good Proposal Eng. Suhail and Ayman Sultan Palestine Polytechnic University Ramallah April 9 2006 Project Cycle Management Programming phase: Analyzing the situation

Project Cycle Management and How To Write A Good Proposal Eng. Suhail and Ayman Sultan Palestine Polytechnic University Ramallah April 9 2006 Project Cycle Management Programming phase: Analyzing the situation

Uzbekistan Towards 2030:

Uzbekistan Towards 23: A New Social Protection Model for a Changing Economy and Society Uzbekistan Towards 23: A New Social Protection Model for a Changing Economy and Society The study is financed by

Uzbekistan Towards 23: A New Social Protection Model for a Changing Economy and Society Uzbekistan Towards 23: A New Social Protection Model for a Changing Economy and Society The study is financed by

ARCH response to consultation on the options for reforming the rules around the use of Right to Buy receipts

ARCH response to consultation on the options for reforming the rules around the use of Right to Buy receipts Timeframe for spending Right to Buy receipts Question 1: Views on extending the time limit for

ARCH response to consultation on the options for reforming the rules around the use of Right to Buy receipts Timeframe for spending Right to Buy receipts Question 1: Views on extending the time limit for

Improving the home buying and selling process: UK Finance response to the DCLG call for evidence

Improving the home buying and selling process: UK Finance response to the DCLG call for evidence 15 December 2017 Introduction UK Finance represents around 300 firms in the UK providing credit, banking,

Improving the home buying and selling process: UK Finance response to the DCLG call for evidence 15 December 2017 Introduction UK Finance represents around 300 firms in the UK providing credit, banking,

ECONOMIC POLICY COMMITTEE EPC REPORT ON POTENTIAL OUTPUT AND OUTPUT GAPS

ECONOMIC POLICY COMMITTEE 1. Introduction Brussels, 23 March 2004 EPC/ECFIN/056/04-final EPC REPORT ON POTENTIAL OUTPUT AND OUTPUT GAPS The concepts of potential output and output gaps are important tools

ECONOMIC POLICY COMMITTEE 1. Introduction Brussels, 23 March 2004 EPC/ECFIN/056/04-final EPC REPORT ON POTENTIAL OUTPUT AND OUTPUT GAPS The concepts of potential output and output gaps are important tools

IPP TRANSACTION ADVISOR TERMS OF REFERENCE

IPP TRANSACTION ADVISOR TERMS OF REFERENCE Terms of reference for transaction advisor services to the Government of [ ] for the [insert description of the project] (the Project ). Contents 1. Introduction

IPP TRANSACTION ADVISOR TERMS OF REFERENCE Terms of reference for transaction advisor services to the Government of [ ] for the [insert description of the project] (the Project ). Contents 1. Introduction

Economic Assessment of a hypothetical interconnector RO-BG

Economic Assessment of a hypothetical interconnector RO-BG László Szabó REKK SEERMAP Electricity Network Assessment workshop Tirana, 14-16 December. 2016 1 Outline Introduction Economic vs financial focused

Economic Assessment of a hypothetical interconnector RO-BG László Szabó REKK SEERMAP Electricity Network Assessment workshop Tirana, 14-16 December. 2016 1 Outline Introduction Economic vs financial focused

IFRS Explained - supplement. Chapter 1 The IASB and the regulatory framework. Chapter 2 Conceptual framework for financial reporting

IFRS Explained - supplement Chapter 1 The IASB and the regulatory framework The organisations mentioned in this chapter were renamed in July 2010 as follows: The IASC Foundation became the IFRS Foundation

IFRS Explained - supplement Chapter 1 The IASB and the regulatory framework The organisations mentioned in this chapter were renamed in July 2010 as follows: The IASC Foundation became the IFRS Foundation

PROPOSED STRATEGIES FOR ATTAINING HEALTH FOR ALL BY THE YEAR Report of the Programme Committee of the Executive

WORLD HEALTH ORGANIZATION ЕВбз/42 ORGANISATION MONDIALE DE LA SANTÉ 22 November 1978 EXECUTIVE BOARD INDEXED Sixty-third Session Supplementary agenda item 1 d О ^ PROPOSED STRATEGIES FOR ATTAINING HEALTH

WORLD HEALTH ORGANIZATION ЕВбз/42 ORGANISATION MONDIALE DE LA SANTÉ 22 November 1978 EXECUTIVE BOARD INDEXED Sixty-third Session Supplementary agenda item 1 d О ^ PROPOSED STRATEGIES FOR ATTAINING HEALTH

Learning Objectives = = where X i is the i t h outcome of a decision, p i is the probability of the i t h

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

AUDIT CERTIFICATE GUIDANCE NOTES 6 TH FRAMEWORK PROGRAMME

AUDIT CERTIFICATE GUIDANCE NOTES 6 TH FRAMEWORK PROGRAMME WORKING NOTES FOR CONTRACTORS AND CERTIFYING ENTITIES MATERIALS PREPARED BY INTERDEPARTMENTAL AUDIT CERTIFICATE WORKING GROUP/ COORDINATION GROUP

AUDIT CERTIFICATE GUIDANCE NOTES 6 TH FRAMEWORK PROGRAMME WORKING NOTES FOR CONTRACTORS AND CERTIFYING ENTITIES MATERIALS PREPARED BY INTERDEPARTMENTAL AUDIT CERTIFICATE WORKING GROUP/ COORDINATION GROUP

Response to the QCA approach to setting the risk-free rate

Response to the QCA approach to setting the risk-free rate Report for Aurizon Ltd. 25 March 2013 Level 1, South Bank House Cnr. Ernest and Little Stanley St South Bank, QLD 4101 PO Box 29 South Bank, QLD

Response to the QCA approach to setting the risk-free rate Report for Aurizon Ltd. 25 March 2013 Level 1, South Bank House Cnr. Ernest and Little Stanley St South Bank, QLD 4101 PO Box 29 South Bank, QLD

Analysis of PPP Project Risk

Abstract Analysis of PPP Project Risk Jing Zhang 1, a, Jiefang Tian 1, b 1 School of North China University of Science and Technology, Tangshan 063210, China. a HappydeZhangJing@163.com, b 550341056@qq.com

Abstract Analysis of PPP Project Risk Jing Zhang 1, a, Jiefang Tian 1, b 1 School of North China University of Science and Technology, Tangshan 063210, China. a HappydeZhangJing@163.com, b 550341056@qq.com

THE NAMIBIAN ROAD SECTOR REFORM: AN EVALUATION

THE NAMIBIAN ROAD SECTOR REFORM: AN EVALUATION NILS BRUZELIUS Nils Bruzelius AB, Mätaregränden 6, 226 47 Lund, Sweden ABSTRACT In 2000 Namibia implemented a road sector reform, which at that time was one

THE NAMIBIAN ROAD SECTOR REFORM: AN EVALUATION NILS BRUZELIUS Nils Bruzelius AB, Mätaregränden 6, 226 47 Lund, Sweden ABSTRACT In 2000 Namibia implemented a road sector reform, which at that time was one

LIFE CYCLE ASSET MANAGEMENT. Project Management Overview. Good Practice Guide GPG-FM-001. March 1996

LIFE YLE Good Practice Guide ASSET MANAGEMENT Project Management Overview March 1996 Department of Energy Office of Field Management Office of Project and Fixed Asset Management ontents 1. INTRODUTION...1

LIFE YLE Good Practice Guide ASSET MANAGEMENT Project Management Overview March 1996 Department of Energy Office of Field Management Office of Project and Fixed Asset Management ontents 1. INTRODUTION...1

Principles of Financial Feasibility ARCH 738: REAL ESTATE PROJECT MANAGEMENT. Morgan State University

Principles of Financial Feasibility ARCH 738: REAL ESTATE PROJECT MANAGEMENT Morgan State University Jason E. Charalambides, PhD, MASCE, AIA, ENV_SP (This material has been prepared for educational purposes)

Principles of Financial Feasibility ARCH 738: REAL ESTATE PROJECT MANAGEMENT Morgan State University Jason E. Charalambides, PhD, MASCE, AIA, ENV_SP (This material has been prepared for educational purposes)

The Latest Progress of the Conceptual Framework

Modern Economy, 2015, 6, 694-699 Published Online June 2015 in SciRes. http://www.scirp.org/journal/me http://dx.doi.org/10.4236/me.2015.66065 The Latest Progress of the Conceptual Framework Ting Shang

Modern Economy, 2015, 6, 694-699 Published Online June 2015 in SciRes. http://www.scirp.org/journal/me http://dx.doi.org/10.4236/me.2015.66065 The Latest Progress of the Conceptual Framework Ting Shang

Delineating hazardous flood conditions to people and property

Delineating hazardous flood conditions to people and property G Smith 1, D McLuckie 2 1 UNSW Water Research Laboratory 2 NSW Office of Environment and Heritage, NSW Abstract Floods create hazardous conditions

Delineating hazardous flood conditions to people and property G Smith 1, D McLuckie 2 1 UNSW Water Research Laboratory 2 NSW Office of Environment and Heritage, NSW Abstract Floods create hazardous conditions

The Central Bank of Ireland Risk Appetite: A Discussion Paper

CONTRIBUTION FROM THE CREDIT UNION DEVELOPMENT ASSOCIATION IN RESPONSE TO The Central Bank of Ireland Risk Appetite: A Discussion Paper 1 st September 2014 Introduction CUDA (Credit Union Development Association)

CONTRIBUTION FROM THE CREDIT UNION DEVELOPMENT ASSOCIATION IN RESPONSE TO The Central Bank of Ireland Risk Appetite: A Discussion Paper 1 st September 2014 Introduction CUDA (Credit Union Development Association)

Publication date: 12-Nov-2001 Reprinted from RatingsDirect

Publication date: 12-Nov-2001 Reprinted from RatingsDirect Commentary CDO Evaluator Applies Correlation and Monte Carlo Simulation to the Art of Determining Portfolio Quality Analyst: Sten Bergman, New

Publication date: 12-Nov-2001 Reprinted from RatingsDirect Commentary CDO Evaluator Applies Correlation and Monte Carlo Simulation to the Art of Determining Portfolio Quality Analyst: Sten Bergman, New

MFE8825 Quantitative Management of Bond Portfolios

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

B.29[17d] Medium-term planning in government departments: Four-year plans

![B.29[17d] Medium-term planning in government departments: Four-year plans](/thumbs/77/76271875.jpg "B.29[17d] Medium-term planning in government departments: Four-year plans") B.29[17d] Medium-term planning in government departments: Four-year plans Photo acknowledgement: mychillybin.co.nz Phil Armitage B.29[17d] Medium-term planning in government departments: Four-year plans

B.29[17d] Medium-term planning in government departments: Four-year plans Photo acknowledgement: mychillybin.co.nz Phil Armitage B.29[17d] Medium-term planning in government departments: Four-year plans

THE INSTITUTE OF ACTUARIES OF AUSTRALIA A.B.N

THE INSTITUTE OF ACTUARIES OF AUSTRALIA A.B.N. 69 000 423 656 PROFESSIONAL STANDARD 200 ACTUARIAL REPORTS AND ADVICE TO A LIFE INSURANCE COMPANY APPLICATION Appointed Actuaries of life insurance companies

THE INSTITUTE OF ACTUARIES OF AUSTRALIA A.B.N. 69 000 423 656 PROFESSIONAL STANDARD 200 ACTUARIAL REPORTS AND ADVICE TO A LIFE INSURANCE COMPANY APPLICATION Appointed Actuaries of life insurance companies

Transparency Interpretation of the notion of individual aid award

Transparency Interpretation of the notion of individual aid award Interpretation The transparency provisions were introduced into State aids law by the State Aid Modernization. They require that Member

Transparency Interpretation of the notion of individual aid award Interpretation The transparency provisions were introduced into State aids law by the State Aid Modernization. They require that Member

BUDGETING. After studying this unit you will be able to know: different approaches for the preparation of budgets; 10.

UNIT 10 Structure APPROACHES TO BUDGETING 10.0 Objectives 10.1 Introduction 10.2 Fixed Budgeting 10.3 Flexible Budgeting 10.4 Difference between Fixed and Flexible Budgeting 10.5 Appropriation Budgeting

UNIT 10 Structure APPROACHES TO BUDGETING 10.0 Objectives 10.1 Introduction 10.2 Fixed Budgeting 10.3 Flexible Budgeting 10.4 Difference between Fixed and Flexible Budgeting 10.5 Appropriation Budgeting

Planning, Budgeting and Control

page 42 MAIN PROGRAM 04 Planning, Budgeting and Control 04.1 Strategic Planning and Policy Development 04.2 Program Budget and Financial Control Summary 78. The Office of Strategic Planning and Policy

page 42 MAIN PROGRAM 04 Planning, Budgeting and Control 04.1 Strategic Planning and Policy Development 04.2 Program Budget and Financial Control Summary 78. The Office of Strategic Planning and Policy

LEGAL OPINION REGARDING THE USE OF GREEN DOT MARK

www.ecopartners.bg office@ecopartners.bg LEGAL OPINION REGARDING THE USE OF GREEN DOT MARK This Opinion is prepared solely and specifically for own use, and should not be disseminated without the consent,

www.ecopartners.bg office@ecopartners.bg LEGAL OPINION REGARDING THE USE OF GREEN DOT MARK This Opinion is prepared solely and specifically for own use, and should not be disseminated without the consent,

Fundamentals of Risk Management

Fundamentals of Risk Management EWF-644-08 FUNDAMENTALS OF RISK MANAGEMENT Fundamentals of Risk Management 2 INDEX 1. INTRODUCTION...4 2. RISK MANAGEMENT PROCESS PHASES...5 2.1 Context definition...5 2.2

Fundamentals of Risk Management EWF-644-08 FUNDAMENTALS OF RISK MANAGEMENT Fundamentals of Risk Management 2 INDEX 1. INTRODUCTION...4 2. RISK MANAGEMENT PROCESS PHASES...5 2.1 Context definition...5 2.2

Chapter 19 Optimal Fiscal Policy

Chapter 19 Optimal Fiscal Policy We now proceed to study optimal fiscal policy. We should make clear at the outset what we mean by this. In general, fiscal policy entails the government choosing its spending

Chapter 19 Optimal Fiscal Policy We now proceed to study optimal fiscal policy. We should make clear at the outset what we mean by this. In general, fiscal policy entails the government choosing its spending

Committee on Payments and Market Infrastructures. Board of the International Organization of Securities Commissions

Committee on Payments and Market Infrastructures Board of the International Organization of Securities Commissions Recovery of financial market infrastructures October 2014 (Revised July 2017) This publication

Committee on Payments and Market Infrastructures Board of the International Organization of Securities Commissions Recovery of financial market infrastructures October 2014 (Revised July 2017) This publication