Ch.4 The Accounting Cycle for a Service Business (cont )

|

|

|

- Clarence Parks

- 5 years ago

- Views:

Transcription

1 Ch.4 The Accounting Cycle for a Service Business (cont ) Adjusting entries using T-accounts Work with a Worksheet for a service business Prepare Financial Statements Journalizing and posting adjusting entries 1

2 The Accounting Cycle: Steps 5 Through 8 Step 5 Determine needed adjustments. Step 6 Prepare a work sheet. Step 7 Prepare financial statements from a completed work sheet. Step 8 Journalize and post adjusting entries. 2

3 Determine Needed Adjustments An adjusting entry is an entry made at the end of an accounting period to bring up to date the balance of an account that has become out of date. Adjusting entries are referred to as internal transactions because they do not involve parties outside the business. Adjusting entries never affect the cash account. 3

4 Example Supplies Used Assume the Office Supplies account has a balance before adjustment of $275. An inventory account on December 31 shows $230 of supplies still on hand. Therefore $45 of supplies have been used during the accounting period. 4

5 Example Adjusting Entry for Supplies Used Office Supplies Debit Credit + - Office Supplies Expense Debit Credit + - Balance Amount used Transferred to The amount of supplies used is debited to an expense account (Office Supplies Expense) and credited to an asset account (Office Supplies). 5

6 Example Insurance Expired Assume the Prepaid Insurance account has a balance before adjustment of $240, representing a one-year insurance policy, purchased on Dec. 1. The amount of insurance will be $240 per year 12 months = $20 per month. 6

7 Example Adjusting Entry for Insurance Expired Prepaid Insurance Debit Credit + - Insurance Expense Debit Credit + - Balance Amount of coverage expired Transferred to 7 The amount of insurance expired is debited to an expense account (Insurance Expense) and credited to an asset account (Prepaid Insurance).

8 Depreciation of Office Equipment and Office Furniture Depreciation describes the expense that results from the loss in usefulness of an asset due to age, wear and tear, and obsolescence. The purpose of depreciation accounting is to spread the cost of an asset over its useful life rather than treating the asset s cost as an expense in the year it was purchased. 8

9 Depreciation Calculations Straight-Line Method One of the most popular depreciation methods Yields the same amount of depreciation for each full period an asset is used Formula: Cost of asset Trade-in value Estimated years of usefulness = Annual depreciation expense 9

10 Example Depreciation Calculations Assume office furniture costs $2,000 and has a $200 trade-in value. The office furniture has a useful life of 5 years. The annual depreciation will therefore be $1,800 5 years or $360 per year. The monthly depreciation will be $360 per year 12 months or $30 per month. 10

11 Example The Depreciation Entry Depreciation is always recorded by Debiting an expense account entitled Depreciation Expense Crediting an account entitled Accumulated Depreciation 11

12 Example The Depreciation Entry Accumulated Depreciation A contra asset account Always has a credit balance 12

13 Example Adjusting Entry for Depreciation Depreciation Expense Debit Credit Accumulated Depreciation Debit Credit The Estimated depreciation is always debited to an expense account (Depreciation Expense) and credited to a contra asset account (Accumulated Depreciation) 13

14 Book Value The difference between the cost of an asset and its accumulated depreciation Shown on the balance sheet Example: Office equipment and office furniture accounts for Walker and Associates 14

15 Example Book Value 15

16 Example Unpaid Salaries 16 Assume A business has 3 employees each earning $150 per day. Employees are paid every Friday for a 5-day week ending on Friday. December 31 falls on a Wednesday. An adjusting entry must be prepared On Wednesday, December 31 for salaries owed to employees for Monday, Tuesday, and Wednesday. For 3 employees $150 per day 3 days = $1,350.

17 Example Unpaid Salaries The adjusting entry for unpaid salaries includes A debit to Salaries Expense A credit to Salaries Payable 17

18 Matching Principle Revenue and expenses are recorded in the accounting period in which they occurred. Adjusting entries are needed to properly match expenses and revenue. Although adjusting entries may be made any time, they are normally adjusted at the end of a month or the end of the year. 18

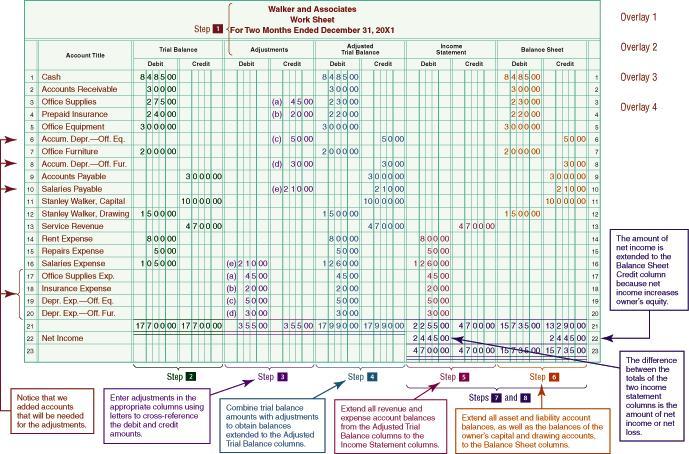

19 The Work Sheet Informal working paper Used in preparing the financial statements and completing the work of the accounting cycle The work sheet is used to Organize data Lessen the possibility of overlooking an adjustment Provide an arithmetical check on the accuracy of work Arrange data in logical form for the preparation of financial statements 19

20 Steps in Completing the Work Sheet 1. Enter the heading. 2. Enter the current trial balance in the Trial Balance columns. 3. Enter the adjustments in the Adjustments Debit and Credit columns. 4. Complete the Adjusted Trial Balance columns. 20

21 Steps in Completing the Work Sheet 5. Complete the Income Statements columns. 6. Complete the Balance Sheet columns. 7. Total the Income Statement and Balance Sheet columns. 8. Determine the amount of net income or net loss, and balance the statement columns. 21

22 Placement of Items on a Work Sheet 22

23 23

24 24 The Income Statement Summary of revenue and expenses showing net income or net loss for an accounting period Prepared directly from data in the Income Statements columns of the work sheet Typically prepared at the end of each month, quarter, or year; however, can be prepared for any period of time Dated to cover a period of time The revenue and expenses shown occurred over the entire period, not just the last date

25 The Statement of Owner s Equity Summarizes the changes that have occurred in owner s equity during an accounting period, such as a month or a year. Prepared from the information on the work sheet: The owner s capital account balance in the Balance Sheet Credit column The owner s drawing account balance in the Balance Sheet Debit column The amount of net income or net loss, shown at the bottom of the Income Statement section 25

26 The Balance Sheet Shows that assets = liabilities + owner s equity Data come from the Balance Sheet columns of the work sheet The up-to-date amount for owner s equity on the balance sheet is taken from the statement of owner s equity 26

27 27 Preparing the Financial Statements 1. Prepare the income statement The net income or net loss calculated on the income statement is shown on the statement of owner s equity. 2. Prepare the statement of owner's equity The ending equity is shown on the balance sheet. 3. Prepare the balance sheet using the ending equity calculated on the statement of owner s equity.

28 Financial Statements The dates of the income statement and the statement of owner s equity cover a period of time. On the income statement, expenses are usually arranged in order of highest to lowest. 28

29 Financial Statements The date of the balance sheet is the last day of the accounting period. 29

30 Example Assume a company uses $45 of office supplies during the current accounting period. Prepare the adjusting entry as follows: General Journal Date Account Title P.R. Debit Credit 20X1 Dec. 31 Office Supplies Expense 45 Office Supplies 45 30

31 Example Assume expired insurance for the current period is $20. Prepare the adjusting entry as follows: General Journal Date Account Title P.R. Debit Credit 20X1 Dec. 31 Insurance Expense 20 Prepaid Insurance 20 31

32 Example Assume depreciation on office furniture for the current period is $30. Prepare the adjusting entry as follows: General Journal Date Account Title P.R. Debit Credit 20X1 Dec. 31 Depreciation Expense Office Furniture 30 Accumulated Depr. Office Furniture 30 32

33 Example Assume December 31 is a Wednesday and accrued salaries owed to employees for Monday through Wednesday amount to $1,350. Prepare the adjusting entry as follows: General Journal Date Account Title P.R. Debit Credit 20X1 Dec. 31 Salaries Expense 1,350 Salaries Payable 1,350 33

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

THE ACCOUNTING CYCLE: Accruals and Deferrals

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Chapter 17 Accounting for Accruals and Deferrals

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

October 20, 2004 Anderson ECON 136A Midterm #1 Name

October 20, 2004 Anderson ECON 136A Midterm #1 Name Please write your name, perm # and ECON 136A Fall 2004 on both your scantron and blue-book. You may take this exam with you. Answer the multiple choice

October 20, 2004 Anderson ECON 136A Midterm #1 Name Please write your name, perm # and ECON 136A Fall 2004 on both your scantron and blue-book. You may take this exam with you. Answer the multiple choice

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

ACCOUNTING I Chapter 10 Reading Guide. 1. What are the two major activities of merchandising businesses?

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM. MULTIPLE CHOICE Conceptual. Test Bank Chapter 3

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Trial Balance. Format of Trial Balance. The under mention points may be noted for preparing a trial balance.

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Week 3. Topic 3 Chapter 3. ACT102 Introduction to Accounting. Accounting for end of financial period adjustments 21/02/2018

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

Disco Dave s Dance Club Continuing the Accounting Cycle: Journal, Ledger, Trial Balance, Adjustments, Worksheet

Overview One of your friends, Disco Dave, just started a new club called. Chart of Accounts These are the account names and numbers that you should use throughout the problem. Some of these accounts will

Overview One of your friends, Disco Dave, just started a new club called. Chart of Accounts These are the account names and numbers that you should use throughout the problem. Some of these accounts will

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 3 The Adjusting Process 2 After studying

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 3 The Adjusting Process 2 After studying

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry.

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

In this module we look at how financial records are balanced and how financial reports are produced, incorporating Balance Day adjustments.

Introduction In this module we look at how financial records are balanced and how financial reports are produced, incorporating Balance Day adjustments. At the end of each accounting period an organisation

Introduction In this module we look at how financial records are balanced and how financial reports are produced, incorporating Balance Day adjustments. At the end of each accounting period an organisation

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

XI ACCOUNTING REGULAR / PRIVATE. S.Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Annie s Animal Care Practice with Adjusting Entries

Overview One of your friends, Annie, owns a local animal kennel called Annie s Animal Care. Refer to the Chart of Accounts and Business Transactions listed below and then complete the Journal and Ledger

Overview One of your friends, Annie, owns a local animal kennel called Annie s Animal Care. Refer to the Chart of Accounts and Business Transactions listed below and then complete the Journal and Ledger

Look at Chapter 2 of Horngren. Make sure that you understand and can describe the following:

Week 1 Revise the introduction to Financial Accounting from CMA100, Chapters 1 and 2, Horngren and then look at Week 1 s topic The Adjusting Process, Chapter 3. Look at Chapter 1 of Horngren. Make sure

Week 1 Revise the introduction to Financial Accounting from CMA100, Chapters 1 and 2, Horngren and then look at Week 1 s topic The Adjusting Process, Chapter 3. Look at Chapter 1 of Horngren. Make sure

2014 Mar. 31 Balance 30, Adjusting 26 22,500 7, Mar. 31 Balance 3, Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

XI ACCOUNTING PRIVATE. Sameer Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit 2014 XI ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit 2014 XI ACCOUNTING

FBLA Accounting I Practice Test 2004

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

4. A They increase retained earnings in the shareholders equity section. This is why we always credit revenues.

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

ACCOUNTING 201. PRACTICE MIDTERM - (Covering Chapters 1-5)

") Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

CHAPTER 8 REVIEW EXERCISES (continued) Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE

Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE") Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Chapter 13 Payroll Accounting, Taxes, and Reports

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

CHAPTER 3. The Adjusting Process. Chapter Overview

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

Accounting principle/ concept. 1 Change the depreciation methods for non-current assets Consistency

1 (a) Insurance account 1 April 2014 Balance b/d 500 31 March 2015 I/S 4350 31 March 2015 Bank 4000 Balance c/d 150 4500 4500 1 April 2015 Balance b/d 150 Commission receivable account 31 March 2015 Income

1 (a) Insurance account 1 April 2014 Balance b/d 500 31 March 2015 I/S 4350 31 March 2015 Bank 4000 Balance c/d 150 4500 4500 1 April 2015 Balance b/d 150 Commission receivable account 31 March 2015 Income

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts

Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts") Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

MATH WORK SHEET CHAPTER 4

Math Work Sheets and Solutions 1 Name Date Class CHAPTER 4 Calculating New Account Balances Calculate and record the new balance for each of the following accounts. ACCOUNT Cash ACCOUNT NO. 110.... 1,

Math Work Sheets and Solutions 1 Name Date Class CHAPTER 4 Calculating New Account Balances Calculate and record the new balance for each of the following accounts. ACCOUNT Cash ACCOUNT NO. 110.... 1,

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

THE UNITED REPUBLIC OF TANZANIA NATIONAL EXAMINATIONS COUNCIL CERTIFICATE OF SECONDARY EDUCATION EXAMINATION. Instructions

THE UNITED REPUBLIC OF TANZANIA NATIONAL EXAMINATIONS COUNCIL CERTIFICATE OF SECONDARY EDUCATION EXAMINATION 062 BOOK KEEPING (For Both School and Private Candidates) Time: 3 Hours Friday, 12 th October

THE UNITED REPUBLIC OF TANZANIA NATIONAL EXAMINATIONS COUNCIL CERTIFICATE OF SECONDARY EDUCATION EXAMINATION 062 BOOK KEEPING (For Both School and Private Candidates) Time: 3 Hours Friday, 12 th October

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

PART 4. Owners Equity in Business. Partnerships: Formation, operation and reporting Companies: Formation and operations

PART 4 Owners Equity in Business Partnerships: Formation, operation and reporting Companies: Formation and operations 15 16 CHAPTER 15 Partnerships: Formation, operation and reporting CONTENTS 15.1 Formation

PART 4 Owners Equity in Business Partnerships: Formation, operation and reporting Companies: Formation and operations 15 16 CHAPTER 15 Partnerships: Formation, operation and reporting CONTENTS 15.1 Formation

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PRINCIPLES OF ACCOUNTING b.com part I

PRINCIPLES OF ACCOUNTING b.com part I 2013 PRIVATE (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks. (3)

PRINCIPLES OF ACCOUNTING b.com part I 2013 PRIVATE (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks. (3)

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Shared By: Hira Ali. If u like me than raise your hand with me If not than raise ur standard That s about me! Time: 60 min Marks: 50

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Asslam O Alikum FIN621- Financial Statement Analysis mid term paper shared n rechecked by Hira Ali Remember Us In Your Prayers

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Asslam O Alikum FIN621- Financial Statement Analysis mid term paper shared n rechecked by Hira Ali Remember Us In Your Prayers

4 Adjustments for financial reporting

4 Adjustments for financial reporting 4.1 Learning objectives Describe the basic characteristics of the cash basis and the accrual basis of accounting. Identify the reasons why adjusting entries must be

4 Adjustments for financial reporting 4.1 Learning objectives Describe the basic characteristics of the cash basis and the accrual basis of accounting. Identify the reasons why adjusting entries must be

Full file at

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

Chapter 20 Notes Uncollectible Accounts Expense

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

3. Balance sheet accounts are referred to as temporary accounts because their balances are always changing.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

Statement of Cash Flows

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

Bookkeepers are the accountant s eyes and ears. Few accountants actually take the time

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

CHAPTER 2 QUESTIONS. revenue, and expense accounts of the

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

GOLDEN RULES. 1.) The following are elements of financial statements:

The following are elements of financial statements:") GOLDEN RULES 1.) The following are elements of financial statements: Elements by which the financial position (assets = equity + liabilities) is measured: (1) Assets (2) Liabilities (3) Equity Elements

GOLDEN RULES 1.) The following are elements of financial statements: Elements by which the financial position (assets = equity + liabilities) is measured: (1) Assets (2) Liabilities (3) Equity Elements

Review of a Company s Accounting System

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

Question No: 1 ( Marks: 1 ) - Please choose one Which of the following principle deals with the valuation and recording of the assets at cost?

- Please choose one Which of the following principle deals with the valuation and recording of the assets at cost?") Question No: 1 ( Marks: 1 ) - Please choose one Which of the following principle deals with the valuation and recording of the assets at cost? Entity Principle Matching Principle Cost Principle p--3 Stable

Question No: 1 ( Marks: 1 ) - Please choose one Which of the following principle deals with the valuation and recording of the assets at cost? Entity Principle Matching Principle Cost Principle p--3 Stable

ACC 211/212: Double Entry Logs

ACC 211/212: Double Entry Logs Journal Entries: o Credits are always indented (account name and value). o The sum of debits will always equal the sum of credits. o The month name is required only for the

ACC 211/212: Double Entry Logs Journal Entries: o Credits are always indented (account name and value). o The sum of debits will always equal the sum of credits. o The month name is required only for the

ACCOUNTS FROM INCOMPLETE RECORDS

CHAPTER-10 ACCOUNTS FROM INCOMPLETE RECORDS Learning Objectives After studying this lesson you will be able to : Define the concept of incomplete records. Distinguish between Double entry system and Accounts

CHAPTER-10 ACCOUNTS FROM INCOMPLETE RECORDS Learning Objectives After studying this lesson you will be able to : Define the concept of incomplete records. Distinguish between Double entry system and Accounts

Do not turn this page until the start signal is given!

UNIVERSITY INTERSCHOLASTIC LEAGUE ACCOUNTING EXAM Invitational 2015-A Contestant # Team # Do not turn this page until the start signal is given! All answers MUST be written on your answer sheet. Either

UNIVERSITY INTERSCHOLASTIC LEAGUE ACCOUNTING EXAM Invitational 2015-A Contestant # Team # Do not turn this page until the start signal is given! All answers MUST be written on your answer sheet. Either

Answer: b Rationale: Journalizing means to record a transaction in a general journal.

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Financial Statements

CH2404 Process Economics Unit IV Financial Statements Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

CH2404 Process Economics Unit IV Financial Statements Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

ACCT1115. Review Package - Quiz 2. Fall 2013

ACCT1115 Review Package - Quiz 2 Fall 2013 Page 1 of 16 Part I Multiple Choice 1) A company has a $48,000 loan to be paid off over 24 months. Principal payments are $2,000 per month. The current and non-current

ACCT1115 Review Package - Quiz 2 Fall 2013 Page 1 of 16 Part I Multiple Choice 1) A company has a $48,000 loan to be paid off over 24 months. Principal payments are $2,000 per month. The current and non-current

download from https://testbankgo.eu/p/

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3