New UK GAAP Insights and solutions. Julia Penny and Paul Brace

|

|

|

- Marilyn Young

- 5 years ago

- Views:

Transcription

1 New UK GAAP Insights and solutions Julia Penny and Paul Brace

2 Introduction Julia Penny Content Manager (Audit and Accounting) Paul Brace -Head of Business Development Audit and Accounts Agenda New UK GAAP Insight Information solutions Technology solutions

3 New UK GAAP Insight - Contents What will new UK GAAP mean for you? Listed companies Small companies Micro companies Impact of the new Company Regulations implementing the EU directive Early adoption Impacts on audit What about LLPs?

4 What will new UK GAAP mean for you? 2015 regime Microregime within FRSSE onwards regime Available for LLPs Available for charities Micro Small Nonsmall FRS 105 No No Listed/AIM FRSSE 2015 FRS 102 IFRS (FRS 101 or FRS 102 option for parent/subs ) FRS 102 with section 1A for presentation Yes but not for early adoption of new limits Yes, but currently no SORP for FRS 102 1A FRS 102 IFRS (FRS 101 or FRS 102 option for parent/subs ) Yes Yes Yes No

5 Limits from 2016 (does not exceed) Micro-entity Small Company Turnover 632, m (was 6.5m) Balance sheet total 316,000 Average number of employees m (was 3.26m) A plc in the group no longer makes the whole group ineligible but a traded company does. The new small company limits can be adopted early, for periods beginning on or after 1 January 2015, but this is not available as an option for LLPs.

6 Audit exemption At present audit exemption is available to companies that qualify as small (with the exception of charities which have different rules) The small company limits are rising in 2016, but are available for early adoption in 2015 but only for accounting purposes This means the audit exemption limit will not rise until at least 1 January 2016 and there is a possibility that it will be further postponed

7 So what is new UK GAAP? New UK GAAP therefore consists of: The new draft FRS 105 for micro-entities The current (August 2014) version of FRS 102 The draft (expected to be July 2015) version of FRS 102 including section 1A containing reduced disclosure requirements for small entities There are also reduced disclosure frameworks for those applying either FRS 102 or FRS 101. FRS 101 the reduced disclosure framework (based on IFRS) FRS 102 section 1.12

8 FRS 102 MAJOR IMPACTS

9 Major Impacts in accounts Financial instruments, on balance sheet and often at fair value through profit and loss (FVTPL) Loans need to be recognised at amortised cost, so if interest rate less than market rate then notional interest must be recognised More fair values in business combinations to recognise separate intangibles Presumed maximum life of goodwill and intangibles, where life cannot be determined will be 10 years (rather than 20)

10 Major impacts in accounts Options to fair value biological assets, PPE (property, plant and equipment) and associates/jvs Requirement to fair value investment property with changes through profit and loss Options to capitalise interest/development costs as in current UK GAAP but originally proposed to be removed Transition exemptions and disclosure requirements

11 Tax impacts There are no specific rules relating just to the move to FRS 102 but there may be important impacts in the following areas: Trading profits Loan relationships Intangible assets When accounting policies are changed there are already rules to ensure that tax is still charged/relief given once and only once. These will apply to changes to FRS 102 as well.

12 Tax impact Overall the timing for payment to HMRC might be impacted due to the change to either IFRS or FRS 102 HMRC have issued guidance regarding tax impact on FRS 101 and FRS

13 Possible problem areas Financial instruments Any financial instruments, such as derivatives and certain equities, that need to be fair valued in the balance sheet, require a value as at the date of transition For entities with a December year-end this was as at 1 January 2014 (as long as there aren t short accounting periods) This means that fair values will have to established retrospectively.

14 Possible problem areas Bank covenants These might be based on audited accounts or annual financial statements, for example and so a change in GAAP could impact whether they are breached or not; If GAAP used is changed a covenant may either: a) be based on frozen GAAP or b) be breached, as the rules have changed

15 Intra-group or director loans Loans between group companies at zero or below market rates of interest are common Under FRS 102 they will need to be recognised at fair value with notional interest being created. The amortised cost method then calculates the interest to be charged each year in the profit and loss

16 Profit related pay/bonuses/earnouts Care will be needed where remuneration or payment for another company based on figures calculated under old UK GAAP If contract isn t clear it might mean that bonuses get paid on unrealised earnings or on figures not anticipated as being included Review all profit related contracts and amend as appropriate.

17 Possible problem areas Acquisitions that take place over the next couple of years There are exemptions from retrospectively restating business combinations occurring before the date of transition to FRS 102 This means, for example, that business combinations after 31/12/13 will need to be recognised and measured in accordance with FRS 102, but also potentially under current GAAP This might require valuation of separable intangibles, certain financial assets etc. at the acquisition date.

18 SMALL ENTITIES

19 FRS 102 section 1A for small entities The new regime for small entities is contained in an amended draft of FRS 102 Recognition and measurement exactly the same as for larger companies Section 1A of this contains the required disclosures for small entities, which are limited, but These accounts still need to give a true and fair view, so consideration will be needed of all FRS 102 or other relevant disclosures

20 Abbreviated vs abridged Abbreviated accounts are not available under the new regime Abridged accounts are available (not for charities) these can be prepared for members and are shortened versions of full accounts with only main headings and starting with gross profit but Shareholder approval needed each year Accounts still need to show a true and fair view, so might need to include turnover?

21 Filing requirements If company with members permission choose to prepare abridged accounts then these are used for filing, but No requirement for small entity to file the profit and loss account So only need balance sheet and notes and information regarding members consent for abridgement and whether audit report qualified or not, if accounts audited.

22 MICRO ENTITIES FRS 105

23 Overview FRS 105 is available for micro-entities (less than 632,000 turnover ) It has simpler requirements for recognition and measurement It has very limited disclosure requirements Micro-entity accounts are deemed to give a true and fair view

24 Key simplifications for micros No fair values/revaluations No capitalisation of borrowing or development costs No accounting for equity settled share-based payments No deferred tax Grants to be recognised using performance method Contracted/forward rate must be used for forex No related party disclosures

25 INFORMATION SOLUTIONS

26 Guidance and tools to help Requirement Learn about the basics of new UK GAAP and when it applies Understand in detail the requirements of FRS 102 Get to grips with the financial instruments requirements when I have no prior knowledge Deal with transition to FRS 102 in a step by step way including seeing an illustrated case study Model accounts to follow Solution Our free website Applying new UK GAAP Financial instruments guide The Transition Guide Model accounts online

27 Guidance and tools to help Requirement Understand the differences between FRS 102; old UK GAAP and IFRS. Understand how to prepare accounts under FRSSE 2015 Understand the presentation and disclosure requirements of FRS 102 and FRS 102 Section 1A Understand how to prepare charity accounts under the new SORPs Solution New UK GAAP: an at a glance comparison Preparing company accounts: FRSSE and Micro 2015 Preparing FRS 102 accounts Preparing Charity Accounts

28 Guidance and tools to help Requirement Understand the impact of legal and regulatory changes on charities, including tax, audit and accounting Understand pension schemes, tax and accounting and auditing under new UK GAAP Big 4 guidance on applying new UK GAAP Explain to clients what is required and what the impact of new UK GAAP is Solution Charity IAAG Pensions IAAG Deloitte GAAP manuals on FRS 102 and FRS 102 model accounts New Accounting Regime SME guide

29 TECHNOLOGY SOLUTIONS

30 Technology Solutions from Wolters Kluwer Requirement Financial Statement Production Financial Statement Review ixbrl tagging of Word and Excel Accounts Solution CCH Accounts Production Interactive Accounts Disclosure Checklist CCH ixbrl Review & Tag Audit and Assurance Services CCH Audit Automation

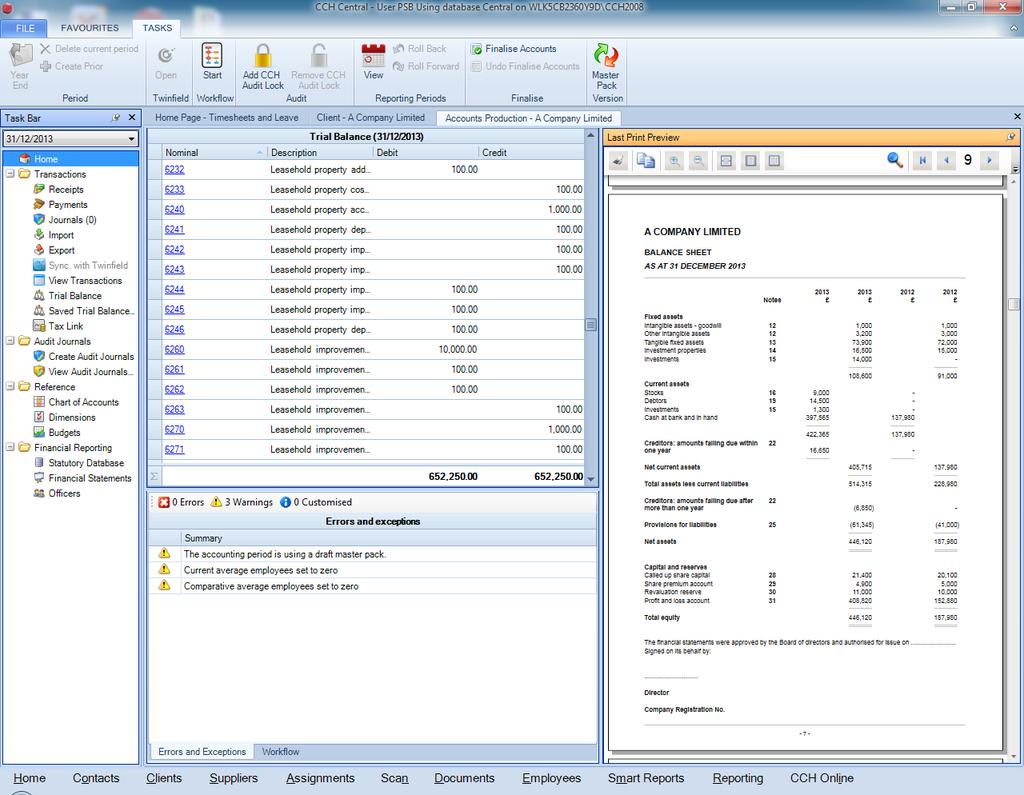

31 CCH Accounts Production Flexible easy to use system Forms part of our integrated solution and is also used as best of breed. Standard formats covering: Incorporated entities Micro entities Unincorporated entities Farms Charities Academies Pension funds Trusts Medical Practices

32

33 New UK GAAP Master Formats Caters for full and reduced disclosure Options to select IFRS or Companies Act terminology Guidance when entering details to the statutory database Straightforward input of information for the first year transition disclosures

34 IFRS or Companies Act Terminology

35 Reduced Disclosure Framework

36 Guidance notes

37 Transition disclosures 2 easy steps. First enter restatement journals

38 Transition disclosures Then analyse the restatements and describe

39 Transition disclosures

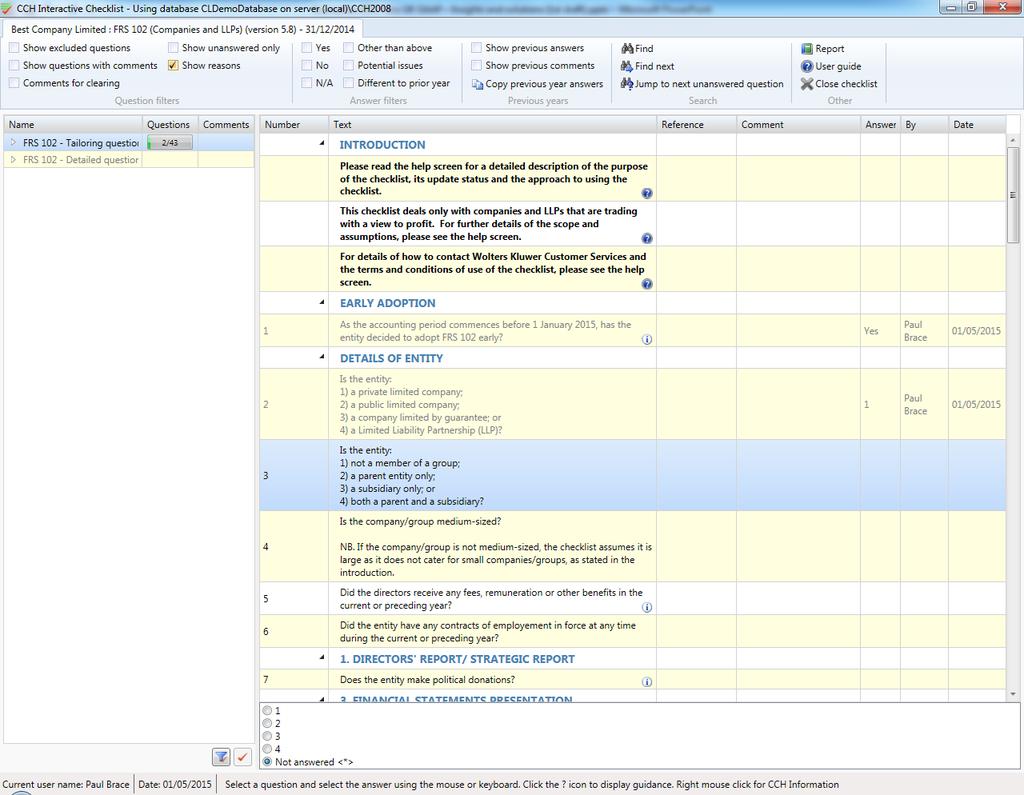

40 Interactive Accounts Disclosure Checklist Quick and efficient check of compliance Checklists cover both existing and New UK GAAP: Private and Public Companies Small Companies FRSSE LLPs Groups Listed Companies Charities and Scottish charities Community interest companies.

41

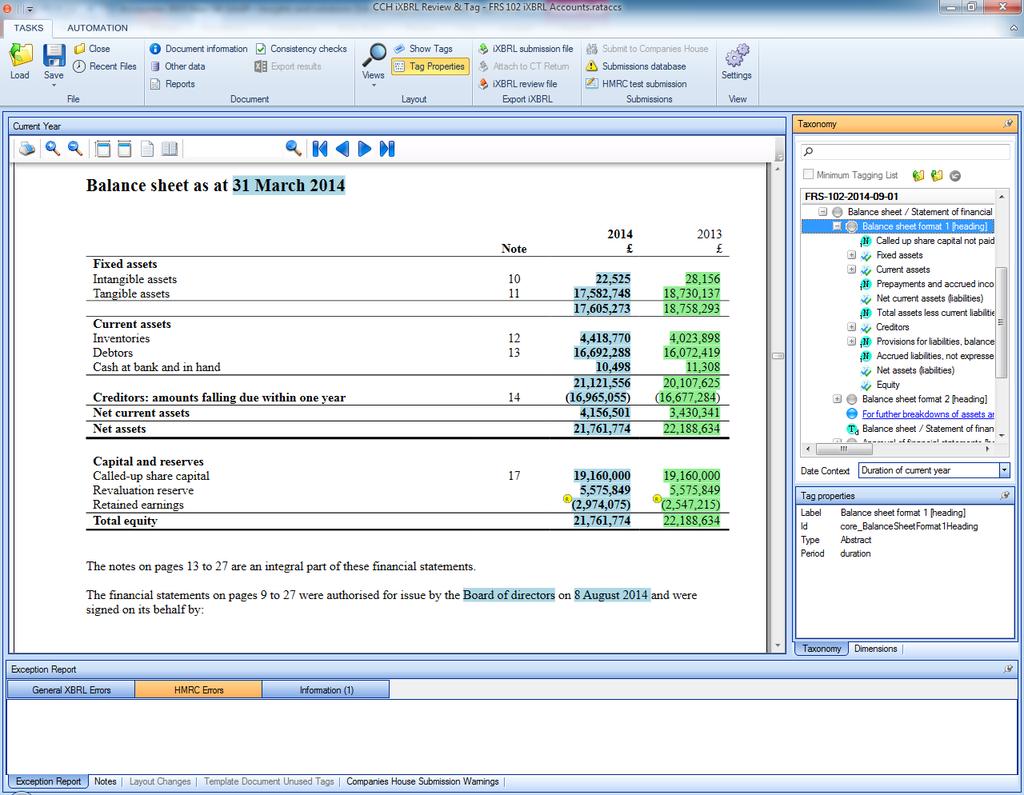

42 CCH ixbrl Review & Tag New ixbrl taxonomies for: IFRS FRS 101 FRS 102 Use of new ixbrl taxonomies mandatory from 1 April 2015 Automated tagging for accounts converted from Word or Excel

43

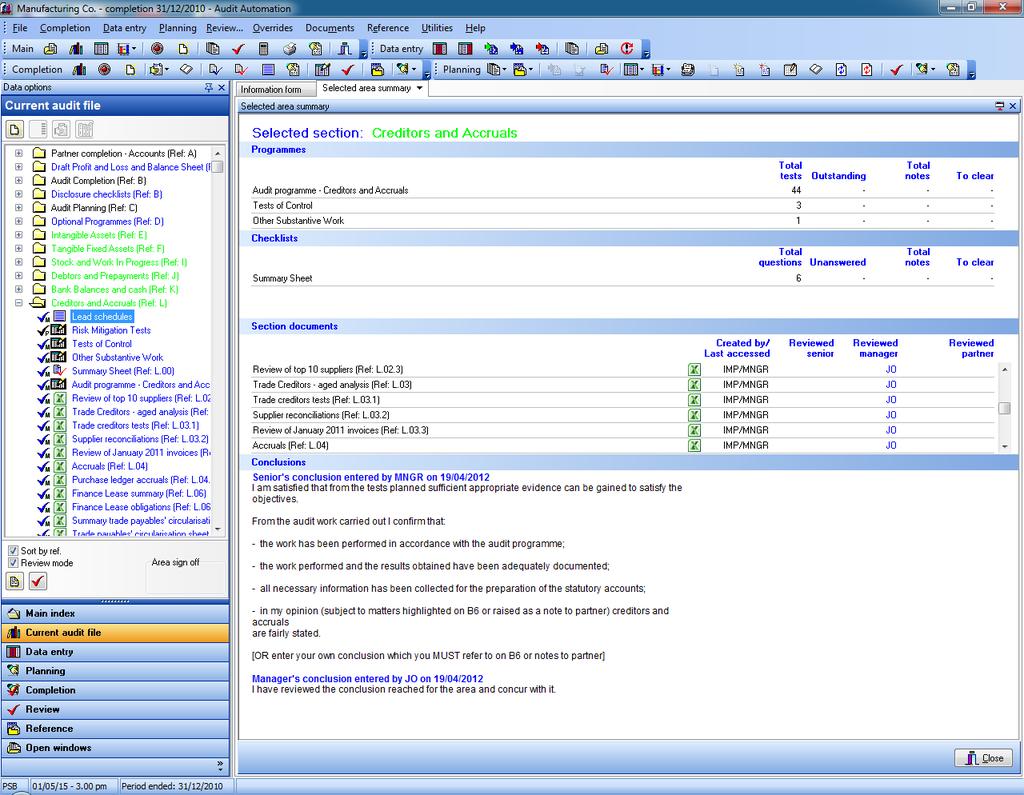

44 CCH Audit Automation Paperless environment covering the entire audit or assurance engagement Methodology enhanced to cover FRS 102 Integrated disclosure checklists extended to cover FRS 102

45

46 Wolters Kluwer Whether you need guidance or software to help you implement UK GAAP, Wolters Kluwer have the information and technology solutions you need to achieve a smooth transition to the new standards.

CCH Transition Guide. FRS 102 and FRS 105. Anne Cowley ACA and Paul Davies ACA, Wolters Kluwer

CCH Transition Guide FRS 102 and FRS 105 2017 18 Anne Cowley ACA and Paul Davies ACA, Wolters Kluwer 2017 18 Preface FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland

CCH Transition Guide FRS 102 and FRS 105 2017 18 Anne Cowley ACA and Paul Davies ACA, Wolters Kluwer 2017 18 Preface FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland

New UK GAAP- FRS102 (Section 1A) for Small Companies And FRS105 for Micro Entity

for Small Companies And FRS105 for Micro Entity") New UK GAAP- FRS102 (Section 1A) for Small Companies And FRS105 for Micro Entity Changes to small and micro company accounting regimes The new UK financial reporting framework which is already mandatory

New UK GAAP- FRS102 (Section 1A) for Small Companies And FRS105 for Micro Entity Changes to small and micro company accounting regimes The new UK financial reporting framework which is already mandatory

The changing accounting and reporting landscape FRS 101/102

The changing accounting and reporting landscape FRS 101/102 Contents Introduction 2 When will the changes take effect? 2 What will the key business implications be? 3 What are the key differences between

The changing accounting and reporting landscape FRS 101/102 Contents Introduction 2 When will the changes take effect? 2 What will the key business implications be? 3 What are the key differences between

CCH ixbrl Review & Tag. Version Release Notes

CCH ixbrl Review & Tag Version 2016.2 Release Notes Legal Notice Disclaimer Wolters Kluwer (UK) Limited has made every effort to ensure the accuracy and completeness of these Release Notes. However, Wolters

CCH ixbrl Review & Tag Version 2016.2 Release Notes Legal Notice Disclaimer Wolters Kluwer (UK) Limited has made every effort to ensure the accuracy and completeness of these Release Notes. However, Wolters

CCH Preparing FRS 102 Company Accounts Anne Cowley ACA

CCH Preparing FRS 102 Company Accounts 2017 18 Anne Cowley ACA Preface Welcome to the 2017 18 edition of Preparing FRS 102 Company Accounts, a practical guide to preparing company accounts under the UK

CCH Preparing FRS 102 Company Accounts 2017 18 Anne Cowley ACA Preface Welcome to the 2017 18 edition of Preparing FRS 102 Company Accounts, a practical guide to preparing company accounts under the UK

Tax Accounting under FRS 102. Introduction. What s the Same?

80 Introduction On 14 March 2013, the Financial Reporting Council issued FRS 102, The Financial Reporting Standard Applicable in the UK and Republic of Ireland. This is the third standard in the complete

80 Introduction On 14 March 2013, the Financial Reporting Council issued FRS 102, The Financial Reporting Standard Applicable in the UK and Republic of Ireland. This is the third standard in the complete

Technical Bulletin TR 170/15. The new Micro-entity regime. The new Micro-entity regime. Overview - Introduction and purpose of the bulletin

Suitable for internal and external use Technical Bulletin TR 170/15 December 2015 The new Micro-entity regime For further advice please contact the UHY technical team on +44 (0)20 7216 4632 technical@uhy-uk.com

Suitable for internal and external use Technical Bulletin TR 170/15 December 2015 The new Micro-entity regime For further advice please contact the UHY technical team on +44 (0)20 7216 4632 technical@uhy-uk.com

Whitepaper Are you FRS-ready? An overview of how the introduction of FRS 101 and 102 is set to affect accountants in business and in practice.

Whitepaper Are you FRS-ready? An overview of how the introduction of FRS 101 and 102 is set to affect accountants in business and in practice. Contents Introduction 1.0 IFRS - the background 2.0 The new

Whitepaper Are you FRS-ready? An overview of how the introduction of FRS 101 and 102 is set to affect accountants in business and in practice. Contents Introduction 1.0 IFRS - the background 2.0 The new

Changing your GAAP Planning your conversion to the new Irish reporting regime. March 2015

Changing your GAAP Planning your conversion to the new Irish reporting regime March 2015 Contents Introduction 1 What s changed? 2 What are my options? 6 Frequently asked questions 9 What about tax? 15

Changing your GAAP Planning your conversion to the new Irish reporting regime March 2015 Contents Introduction 1 What s changed? 2 What are my options? 6 Frequently asked questions 9 What about tax? 15

New UK GAAP. A guide to the largest change in UK accounting standards and financial reporting for a generation

New UK GAAP A guide to the largest change in UK accounting standards and financial reporting for a generation Introduction On 1 January 2015 the Financial Reporting Council ( FRC ) replaced the accounting

New UK GAAP A guide to the largest change in UK accounting standards and financial reporting for a generation Introduction On 1 January 2015 the Financial Reporting Council ( FRC ) replaced the accounting

CCH New UK GAAP: An at a glance comparison between new and old UK GAAP and IFRS. Anne Cowley ACA

CCH New UK GAAP: An at a glance comparison between new and old UK GAAP and IFRS 2017 18 Anne Cowley ACA 2017 18 What s new in New UK GAAP an at a glance comparison between new and old UK GAAP and IFRS

CCH New UK GAAP: An at a glance comparison between new and old UK GAAP and IFRS 2017 18 Anne Cowley ACA 2017 18 What s new in New UK GAAP an at a glance comparison between new and old UK GAAP and IFRS

Association of Accounting Technicians response to FRED 59 Draft amendments to FRS 102 The Financial Reporting Standard applicable in the UK and

Association of Accounting Technicians response to FRED 59 Draft amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland 1 Association of Accounting Technicians

Association of Accounting Technicians response to FRED 59 Draft amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland 1 Association of Accounting Technicians

Proposed changes to UK accounting standards FREDs 58 to 60

A new accounting regime for small and micro-entities: FRC proposals 27 April 2015 Proposed changes to UK accounting standards FREDs 58 to 60 27 April 2015 Background Why amend standards now? New EU Accounting

A new accounting regime for small and micro-entities: FRC proposals 27 April 2015 Proposed changes to UK accounting standards FREDs 58 to 60 27 April 2015 Background Why amend standards now? New EU Accounting

International Financial Reporting Standards Analyst Briefing March 2005

Aggreko plc International Financial Reporting Standards Analyst Briefing March 2005-1- Briefing Structure IFRS impact summary Time-line for communication with the market IFRS implementation project Key

Aggreko plc International Financial Reporting Standards Analyst Briefing March 2005-1- Briefing Structure IFRS impact summary Time-line for communication with the market IFRS implementation project Key

New UK GAAP. Preparing your organisation for change

New UK GAAP Preparing your organisation for change Background to the change in UK GAAP Accounting standards - the UK history 1971 - SSAP 1 Accounting for the results of associated companies 1991 - FRS

New UK GAAP Preparing your organisation for change Background to the change in UK GAAP Accounting standards - the UK history 1971 - SSAP 1 Accounting for the results of associated companies 1991 - FRS

The new UK GAAP -- a major change in financial reporting

The new UK GAAP -- a major change in financial reporting A Wolters Kluwer review for accountants and finance professionals August 2013 Introduction Major change will soon be upon us. The new UK GAAP in

The new UK GAAP -- a major change in financial reporting A Wolters Kluwer review for accountants and finance professionals August 2013 Introduction Major change will soon be upon us. The new UK GAAP in

Financial Reporting Update. 19 September 2014

Financial Reporting Update 19 September 2014 Welcome Seminar overview The current UK financial reporting regime Changes to UK GAAP Impact on charity financial reporting Introduction of new SORPs Transition

Financial Reporting Update 19 September 2014 Welcome Seminar overview The current UK financial reporting regime Changes to UK GAAP Impact on charity financial reporting Introduction of new SORPs Transition

CCH Accounts Production. FRS 105 Micro Entities User Guide. Master Pack 11.00

CCH Accounts Production FRS 105 Micro Entities User Guide Master Pack 11.00 Legal Notice Disclaimer Wolters Kluwer (UK) Limited has made every effort to ensure the accuracy and completeness of these Release

CCH Accounts Production FRS 105 Micro Entities User Guide Master Pack 11.00 Legal Notice Disclaimer Wolters Kluwer (UK) Limited has made every effort to ensure the accuracy and completeness of these Release

Association of Accounting Technicians response to FRED 58 Draft FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

Association of Accounting Technicians response to FRED 58 Draft FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime 1 Association of Accounting Technicians response to FRED

Association of Accounting Technicians response to FRED 58 Draft FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime 1 Association of Accounting Technicians response to FRED

30/09/2015. The new regime for small and micro entities. The new regime for small and micro entities. Introduction

The new regime for small and micro entities 30 September 2015 Download the slides to accompany the webinar /FRFwebinarresources The new regime for small and micro entities 30 September 2015 Introduction

The new regime for small and micro entities 30 September 2015 Download the slides to accompany the webinar /FRFwebinarresources The new regime for small and micro entities 30 September 2015 Introduction

A STEP BY STEP GUIDE TO IMPLEMENTING FRS 102

A STEP BY STEP GUIDE TO IMPLEMENTING FRS 102 This book is published by UK Training (Worldwide) Limited and is designed to help people complete a smooth transition from existing UK GAAP to FRS 102. The

A STEP BY STEP GUIDE TO IMPLEMENTING FRS 102 This book is published by UK Training (Worldwide) Limited and is designed to help people complete a smooth transition from existing UK GAAP to FRS 102. The

The New UK Accounting Standard FRS 102

The New UK Accounting Standard FRS 102 FRS 102 is here The new standard, which applies for accounting periods beginning on or after 1 January 2015, replaces all the present UK accounting standards. A number

The New UK Accounting Standard FRS 102 FRS 102 is here The new standard, which applies for accounting periods beginning on or after 1 January 2015, replaces all the present UK accounting standards. A number

The New UK GAAP - FRS January 2014

The New UK GAAP - FRS 102 21 January 2014 Setting the scene Brief overview of new regime What is FRS 102 & what will it mean? Next steps What is happening? FRS 100 and FRS 101 published in November 2012

The New UK GAAP - FRS 102 21 January 2014 Setting the scene Brief overview of new regime What is FRS 102 & what will it mean? Next steps What is happening? FRS 100 and FRS 101 published in November 2012

December 2013 Category Course title Author Accounting Transition to the new UK GAAP, FRS 102 Paul Gee. Disclaimer and Copyright

December 2013 Category Course title Author Accounting Transition to the new UK GAAP, FRS 102 Paul Gee Disclaimer and Copyright Whilst every care has been taken in the preparation of this learning material

December 2013 Category Course title Author Accounting Transition to the new UK GAAP, FRS 102 Paul Gee Disclaimer and Copyright Whilst every care has been taken in the preparation of this learning material

Changes to the small companies regime. Steve Collings FMAAT FCCA Audit and Technical Director Leavitt Walmsley Associates Ltd

Changes to the small companies regime Steve Collings FMAAT FCCA Audit and Technical Director Leavitt Walmsley Associates Ltd Webinar overview Overview of why the changes have occurred The new small companies

Changes to the small companies regime Steve Collings FMAAT FCCA Audit and Technical Director Leavitt Walmsley Associates Ltd Webinar overview Overview of why the changes have occurred The new small companies

Guide to FRS 102 & Relate Accounts Production

Guide to FRS 102 & Relate Accounts Production www.relate-software.com info@relate-software.com UK +44 871 284 3446 ROI +353 1 4597800 UK R008 April 2015 CONTENTS Relate Accounts Production Guide to FRS

Guide to FRS 102 & Relate Accounts Production www.relate-software.com info@relate-software.com UK +44 871 284 3446 ROI +353 1 4597800 UK R008 April 2015 CONTENTS Relate Accounts Production Guide to FRS

New GAAP is here: It s time to change. The introduction of New GAAP

New GAAP is here: It s time to change The introduction of New GAAP CONTENT 01 Highlights 1 02 Managing conversion effectively 2 03 What are my options? 3 04 How should I evaluate my options? 4 05 What

New GAAP is here: It s time to change The introduction of New GAAP CONTENT 01 Highlights 1 02 Managing conversion effectively 2 03 What are my options? 3 04 How should I evaluate my options? 4 05 What

FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland The FRC's mission is to promote transparency

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland The FRC's mission is to promote transparency

DISCLOSURE SOLUTIONS LIMITED The Old Smithy,Radwinter Road, Ashdon, CB10 2ET Telephone

DISCLOSURE SOLUTIONS LIMITED The Old Smithy,Radwinter Road, Ashdon, CB10 2ET Telephone 01799 584053 Jenny Carter FRC 8 th Floor 125 London Wall LONDON EC2Y 5AS 28 November 2014 ACCOUNTING STANDARDS FOR

DISCLOSURE SOLUTIONS LIMITED The Old Smithy,Radwinter Road, Ashdon, CB10 2ET Telephone 01799 584053 Jenny Carter FRC 8 th Floor 125 London Wall LONDON EC2Y 5AS 28 November 2014 ACCOUNTING STANDARDS FOR

The Future of UK GAAP Your questions answered

www.pwc.co.uk The Future of UK GAAP Your questions answered December 2012 Contents Introduction 3 Nature and scope of the changes 4 FRS for UK and RoI the standard and its adoption 6 Adopting IFRS or IFRS

www.pwc.co.uk The Future of UK GAAP Your questions answered December 2012 Contents Introduction 3 Nature and scope of the changes 4 FRS for UK and RoI the standard and its adoption 6 Adopting IFRS or IFRS

Accounts Production Advanced Release Notes 2016

Accounts Production Advanced Release Notes 2016 Sage (UK) Limited Copyright Statement Sage (UK) Limited, 2016. All rights reserved. If this documentation includes advice or information relating to any

Accounts Production Advanced Release Notes 2016 Sage (UK) Limited Copyright Statement Sage (UK) Limited, 2016. All rights reserved. If this documentation includes advice or information relating to any

Technical factsheet FRS 102 small company reporting

Technical factsheet FRS 102 small company reporting Contents Page Introduction 2 Standards in issue and amendments to the Companies Act 2006 3 Reduced disclosure requirements and the true and fair concept

Technical factsheet FRS 102 small company reporting Contents Page Introduction 2 Standards in issue and amendments to the Companies Act 2006 3 Reduced disclosure requirements and the true and fair concept

FRS 102 One year on Practical problems

2020 Innovation FRS 102 One year on Practical problems Bill Telford, Telford Financial Training Ltd No responsibility for loss occasioned to any person acting or refraining from action as a result of the

2020 Innovation FRS 102 One year on Practical problems Bill Telford, Telford Financial Training Ltd No responsibility for loss occasioned to any person acting or refraining from action as a result of the

igaap 2005 in your pocket

igaap 2005 in your pocket A summary of international financial reporting from a UK perspective July 2005 Contents Deloitte guidance 1 Abbreviations used in this publication 2 Current international standards

igaap 2005 in your pocket A summary of international financial reporting from a UK perspective July 2005 Contents Deloitte guidance 1 Abbreviations used in this publication 2 Current international standards

UK COMPANY ACCOUNTS The New Reporting Regime FACTSHEET 02 SIZE REALLY DOES MATTER

UK COMPANY ACCOUNTS The New Reporting Regime FACTSHEET 02 SIZE REALLY DOES MATTER Contents Introduction... 2 Scope... 2 Effective date... 2 What the changes mean... 3 Eligibility criteria... 4 More on

UK COMPANY ACCOUNTS The New Reporting Regime FACTSHEET 02 SIZE REALLY DOES MATTER Contents Introduction... 2 Scope... 2 Effective date... 2 What the changes mean... 3 Eligibility criteria... 4 More on

IFRS and UK GAAP Update. Lisa Weaver BA FCA

IFRS and UK GAAP Update Lisa Weaver BA FCA Overview of the session IFRS update covering all recent major changes in international reporting UK GAAP update including FRSs 100 to 102 the latest position

IFRS and UK GAAP Update Lisa Weaver BA FCA Overview of the session IFRS update covering all recent major changes in international reporting UK GAAP update including FRSs 100 to 102 the latest position

A New Era for UK & Irish GAAP

A New Era for UK & Irish GAAP The New Financial Reporting Standards in Ireland & the UK Presented By: Maureen Kelly CPA Technical Services Executive New Standards FRS 100 Application of Financial Reporting

A New Era for UK & Irish GAAP The New Financial Reporting Standards in Ireland & the UK Presented By: Maureen Kelly CPA Technical Services Executive New Standards FRS 100 Application of Financial Reporting

Preparing for SORP 2015: an essential overview for charities

Charity Finance Group Preparing for SORP 2015: an essential overview for charities Ray Jones - Training consultant to CFG and member of Charities SORP Committee Preparing for SORP 2015 Background and overview

Charity Finance Group Preparing for SORP 2015: an essential overview for charities Ray Jones - Training consultant to CFG and member of Charities SORP Committee Preparing for SORP 2015 Background and overview

FRS 102 PROFESSIONAL SERVICES. The main new Irish GAAP standard

FRS 102 PROFESSIONAL SERVICES The main new Irish GAAP standard November 2014 2 PROFESSIONAL SERVICES PROFESSIONAL SERVICES 3 The long awaited replacement for Irish GAAP has finally arrived in the form

FRS 102 PROFESSIONAL SERVICES The main new Irish GAAP standard November 2014 2 PROFESSIONAL SERVICES PROFESSIONAL SERVICES 3 The long awaited replacement for Irish GAAP has finally arrived in the form

Draft FRS The Financial Reporting Standard applicable to the Micro-entities Regime

Draft FRS 105 - The Financial Reporting Standard applicable to the Micro-entities Regime FRED 58, issued by the Financial Reporting Council in February 2015 Comments from ACCA 30 April 2015 ACCA (the Association

Draft FRS 105 - The Financial Reporting Standard applicable to the Micro-entities Regime FRED 58, issued by the Financial Reporting Council in February 2015 Comments from ACCA 30 April 2015 ACCA (the Association

FRS One Year On - a practical review

FRS 102 - One Year On - a practical review Bill Telford Telford Financial Training Ltd Introduction Chapter 1 Telford Financial Training Ltd Are you on the right webinar?? o FRS 102 One Year on o It is

FRS 102 - One Year On - a practical review Bill Telford Telford Financial Training Ltd Introduction Chapter 1 Telford Financial Training Ltd Are you on the right webinar?? o FRS 102 One Year on o It is

The European Context. Distinct elements. Implementation of the EU Accounting Directive in the UK

Implementation of the EU Accounting Directive in the UK Vickie Wood Assistant Director, Accounting Policy Business Environment Directorate 2 The European Context Smart Regulation in the European Union

Implementation of the EU Accounting Directive in the UK Vickie Wood Assistant Director, Accounting Policy Business Environment Directorate 2 The European Context Smart Regulation in the European Union

Changing tack. A new financial reporting framework for public benefit entities. January 2017

Changing tack A new financial reporting framework for public benefit entities January 2017 Introduction Public benefit entities (PBEs) have experienced significant changes to their financial reporting

Changing tack A new financial reporting framework for public benefit entities January 2017 Introduction Public benefit entities (PBEs) have experienced significant changes to their financial reporting

Audit and Assurance Faculty Roadshow Autumn 2015

Audit and Assurance Faculty Roadshow Autumn 2015 Presented by John Selwood Deloitte began investing heavily in automation, analytics and technological innovation four years ago, explains Kakoullis. The

Audit and Assurance Faculty Roadshow Autumn 2015 Presented by John Selwood Deloitte began investing heavily in automation, analytics and technological innovation four years ago, explains Kakoullis. The

New UK GAAP. Radical changes for small and micro-entities. A new financial reporting regime for the UK s smallest entities A BRAVE NEW WORLD

New UK GAAP SUMMER 2016 ICAEW.COM/FRF Radical changes for small and micro-entities A BRAVE NEW WORLD A new financial reporting regime for the UK s smallest entities A FACULTY TECHNICAL PUBLICATION FOREWORD

New UK GAAP SUMMER 2016 ICAEW.COM/FRF Radical changes for small and micro-entities A BRAVE NEW WORLD A new financial reporting regime for the UK s smallest entities A FACULTY TECHNICAL PUBLICATION FOREWORD

UK GAAP Preparing for the change. Breakfast Briefing 5 February 2015

UK GAAP Preparing for the change Breakfast Briefing 5 February 2015 Topics Overview of new UK GAAP FRS 102 and differences with current UK GAAP Tax implications of FRS 102 Next steps Summary Overview of

UK GAAP Preparing for the change Breakfast Briefing 5 February 2015 Topics Overview of new UK GAAP FRS 102 and differences with current UK GAAP Tax implications of FRS 102 Next steps Summary Overview of

Interim Managers Update

Interim Managers Update Simone Taylor-Allkins Technical Advisory Services, ICAEW Content Technical advisory services who are we, and how we can help you; Just arrived and just around the corner Audit exemption

Interim Managers Update Simone Taylor-Allkins Technical Advisory Services, ICAEW Content Technical advisory services who are we, and how we can help you; Just arrived and just around the corner Audit exemption

Yes, we agree that the latest proposals achieve the ASB s project objective.

Appendix 1 Responses to specific questions raised in the FREDs Q 1 The ASB is setting out the proposals in this revised FRED following a prolonged period of consultation. The ASB considers that the proposals

Appendix 1 Responses to specific questions raised in the FREDs Q 1 The ASB is setting out the proposals in this revised FRED following a prolonged period of consultation. The ASB considers that the proposals

SCR Reporting. Bulletin 2015 / 2. An apology

Winter 2015 SCR Reporting Bulletin 2015/2 SCR Reporting Bulletin 2015 / 2 An apology In our last bulletin I promised that the small company module would be available in September / October following the

Winter 2015 SCR Reporting Bulletin 2015/2 SCR Reporting Bulletin 2015 / 2 An apology In our last bulletin I promised that the small company module would be available in September / October following the

International Accounting Standards Board 30 Cannon Street London EC4M 6XH UK. Cc: EFRAG. Oslo, November 29, Dear Sir/Madam

International Accounting Standards Board 30 Cannon Street London EC4M 6XH UK Cc: EFRAG Oslo, November 29, 2012 Dear Sir/Madam Request for Information: Comprehensive Review of the IFRS for SMEs We appreciate

International Accounting Standards Board 30 Cannon Street London EC4M 6XH UK Cc: EFRAG Oslo, November 29, 2012 Dear Sir/Madam Request for Information: Comprehensive Review of the IFRS for SMEs We appreciate

NEW UK GAAP ONE YEAR IN: PRACTICAL DEVELOPMENTS AND EMERGING ISSUES

NEW UK GAAP ONE YEAR IN: PRACTICAL DEVELOPMENTS AND EMERGING ISSUES February 2017 TABLE OF CONTENTS TABLE OF CONTENTS... 1 1. NEW UK GAAP ONE YEAR IN... 2 1.1 Summary of new UK GAAP... 2 1.2 Increased

NEW UK GAAP ONE YEAR IN: PRACTICAL DEVELOPMENTS AND EMERGING ISSUES February 2017 TABLE OF CONTENTS TABLE OF CONTENTS... 1 1. NEW UK GAAP ONE YEAR IN... 2 1.1 Summary of new UK GAAP... 2 1.2 Increased

Amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland

Amendment to Standard Accounting and Reporting Financial Reporting Council July 2015 Amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland Small entities and

Amendment to Standard Accounting and Reporting Financial Reporting Council July 2015 Amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland Small entities and

Amendments to FRS 102. Updating the Charities SORP (FRS 102) issued in July 2014 for:

issued in July 2014 for:") Accounting and Reporting by Charities: Statement of Recommended Practice applicable to charities preparing their accounts in accordance with the Financial Reporting Standard applicable in the UK and Republic

Accounting and Reporting by Charities: Statement of Recommended Practice applicable to charities preparing their accounts in accordance with the Financial Reporting Standard applicable in the UK and Republic

ixbrl 7 September 2017 Paul Braden - KPMG

ixbrl 7 September 2017 Paul Braden - KPMG Overview What is ixbrl? Why do Revenue want ixbrl financials? When is an ixbrl filing required for Revenue? What does a Revenue ixbrl filing consist of? What needs

ixbrl 7 September 2017 Paul Braden - KPMG Overview What is ixbrl? Why do Revenue want ixbrl financials? When is an ixbrl filing required for Revenue? What does a Revenue ixbrl filing consist of? What needs

01/06/2015. FRS 102 practical issues. FRS 102 practical issues. Introduction

24 February 2015 Download the slides to accompany the webinar /FRFwebinarresources 24 February 2015 Introduction Sarah Dunn Technical Manager, Financial Reporting Faculty 1 Introduction Stephanie Henshaw

24 February 2015 Download the slides to accompany the webinar /FRFwebinarresources 24 February 2015 Introduction Sarah Dunn Technical Manager, Financial Reporting Faculty 1 Introduction Stephanie Henshaw

CCH Accounts Production. FRS 102 Master Pack User Guide

CCH Accounts Production FRS 102 Master Pack 14.00 User Guide Legal Notice Disclaimer Wolters Kluwer (UK) Limited has made every effort to ensure the accuracy and completeness of these Release Notes. However,

CCH Accounts Production FRS 102 Master Pack 14.00 User Guide Legal Notice Disclaimer Wolters Kluwer (UK) Limited has made every effort to ensure the accuracy and completeness of these Release Notes. However,

Understanding the New UK GAAP for Small and Micro-Entities

Understanding the New UK GAAP for Small and Micro-Entities Shashwat Tulsian I am a Quali ed Chartered Accountant, Lawyer and Company Secretary. As a result, I have a unique ability to manage multi-disciplinary

Understanding the New UK GAAP for Small and Micro-Entities Shashwat Tulsian I am a Quali ed Chartered Accountant, Lawyer and Company Secretary. As a result, I have a unique ability to manage multi-disciplinary

Relate Accounts Production FRS 102 DISCLOSURE. Using Relate Accounts Production to produce FRS 102 Compliant Financial Statements.

FRS 102 DISCLOSURE Using Relate Accounts Production to produce FRS 102 Compliant Financial Statements Laurence Pyzer BSc FCA CEng MBCS CITP MIET Compliance Officer of Relate Software ACCOUNTING REGIMES

FRS 102 DISCLOSURE Using Relate Accounts Production to produce FRS 102 Compliant Financial Statements Laurence Pyzer BSc FCA CEng MBCS CITP MIET Compliance Officer of Relate Software ACCOUNTING REGIMES

Financial reporting standards and amendments to financial reporting standards

Financial reporting standards and amendments to financial reporting standards FRS 100 Application of Financial Reporting Requirements FRS 101 Reduced Disclosure Framework These new standards were issued

Financial reporting standards and amendments to financial reporting standards FRS 100 Application of Financial Reporting Requirements FRS 101 Reduced Disclosure Framework These new standards were issued

Need to know. FRC publishes Triennial review 2017 Incremental improvements and clarifications (Amendments to FRS 102) Contents

Contents") FRC publishes Triennial review 2017 Incremental improvements and clarifications (Amendments to FRS 102) Contents Background What are the main areas of improvement or clarification? Effective date and early

FRC publishes Triennial review 2017 Incremental improvements and clarifications (Amendments to FRS 102) Contents Background What are the main areas of improvement or clarification? Effective date and early

Policy Proposal: The Future of UK GAAP

Policy Proposal: The Future of UK GAAP The ABI s response to the ASB s consultation paper Introduction 1. The ABI is the voice of the insurance and investment industry in the UK. Its members constitute

Policy Proposal: The Future of UK GAAP The ABI s response to the ASB s consultation paper Introduction 1. The ABI is the voice of the insurance and investment industry in the UK. Its members constitute

SMALL COMPANY REPORTING ISSUES

John Selwood 9 March 2018 No responsibility for loss occasioned to any person acting or refraining from action as a result of the material in this document can be accepted by the author or 2020 Innovation

John Selwood 9 March 2018 No responsibility for loss occasioned to any person acting or refraining from action as a result of the material in this document can be accepted by the author or 2020 Innovation

Re: IASB Request for information: Comprehensive review of the IFRS for SMEs

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street GB LONDON EC4M 6XH E-mail: commentletters@ifrs.org 14 December 2012 Ref.: FRP/PRJ/TSI/IDS Dear Chairman, Re: IASB

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street GB LONDON EC4M 6XH E-mail: commentletters@ifrs.org 14 December 2012 Ref.: FRP/PRJ/TSI/IDS Dear Chairman, Re: IASB

Small Company Accounting

Small Company Accounting Small Company Accounting The required format of statutory accounts that small companies have to prepare and send to Companies House has changed. This factsheet sets out the choices

Small Company Accounting Small Company Accounting The required format of statutory accounts that small companies have to prepare and send to Companies House has changed. This factsheet sets out the choices

Small company filing options 20 February 2017

Small company filing options 20 February 2017 Download the slides to accompany the webinar from resources panel ICAEW 2017 Small company filing options 20 February 2017 ICAEW 2017 Introduction Eddy James

Small company filing options 20 February 2017 Download the slides to accompany the webinar from resources panel ICAEW 2017 Small company filing options 20 February 2017 ICAEW 2017 Introduction Eddy James

All change for accounting standards FRS 102

All change for accounting standards FRS 102 Effective: 1 January 2015 FRS102 is one of the biggest changes to UK medium and large company reporting for many years. The first changes affect balance sheets

All change for accounting standards FRS 102 Effective: 1 January 2015 FRS102 is one of the biggest changes to UK medium and large company reporting for many years. The first changes affect balance sheets

Hello and welcome to this CPD webinar on New UK GAAP FRS 101/102 Update

AAT Webinar Hello and welcome to this CPD webinar on New UK GAAP FRS 101/102 Update We are due to start at 19:00. You should not have any sound at this stage. We will be doing a sound check at 18:55 Please

AAT Webinar Hello and welcome to this CPD webinar on New UK GAAP FRS 101/102 Update We are due to start at 19:00. You should not have any sound at this stage. We will be doing a sound check at 18:55 Please

FRS102. Within the first set of statutory accounts prepared under FRS102 the following disclosures will have to be made:

FRS102 What and when? The Financial Reporting Council has replaced the existing UK GAAP with The Financial Reporting Standard 102 (FRS102), which is applicable in the UK and Republic of Ireland. The new

FRS102 What and when? The Financial Reporting Council has replaced the existing UK GAAP with The Financial Reporting Standard 102 (FRS102), which is applicable in the UK and Republic of Ireland. The new

IFRS/UK differences Paper P2 Dec 2014 and June 2015

IFRS/UK differences Paper P2 Dec 2014 and June 2015 Introduction This supplement provides the additonal material examinable in the UK and Irish Paper. It comprises the main areas of differnece between

IFRS/UK differences Paper P2 Dec 2014 and June 2015 Introduction This supplement provides the additonal material examinable in the UK and Irish Paper. It comprises the main areas of differnece between

May 2014 Category Course title Author Accounting Income tax under FRS 102 Paul Gee. Disclaimer and Copyright

May 2014 Category Course title Author Accounting Income tax under FRS 102 Paul Gee Disclaimer and Copyright Whilst every care has been taken in the preparation of this learning material we do not accept

May 2014 Category Course title Author Accounting Income tax under FRS 102 Paul Gee Disclaimer and Copyright Whilst every care has been taken in the preparation of this learning material we do not accept

Pearson plc IFRS Technical Analysis

Pearson plc IFRS Technical Analysis Contents A. Introduction B. Basis of presentation C. UK GAAP to IFRS adjustments D. Performance measures Schedules 1. Income statement Reconciliation UK GAAP to IFRS

Pearson plc IFRS Technical Analysis Contents A. Introduction B. Basis of presentation C. UK GAAP to IFRS adjustments D. Performance measures Schedules 1. Income statement Reconciliation UK GAAP to IFRS

financial services frs 102 The main new IRISH GaaP standard: implications for The financial services sector

financial services frs 102 The main new IRISH GaaP standard: implications for The financial services sector 1 financial services The long awaited replacement for Irish GAAP has finally arrived in the form

financial services frs 102 The main new IRISH GaaP standard: implications for The financial services sector 1 financial services The long awaited replacement for Irish GAAP has finally arrived in the form

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2005 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS ADOPTED BY THE EUROPEAN

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2005 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS ADOPTED BY THE EUROPEAN

International Financial Reporting Standard. Small and Medium-sized Entities

A Staff Overview This overview of the IASB s exposure draft of a proposed International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) was prepared by Paul Pacter, IASB

A Staff Overview This overview of the IASB s exposure draft of a proposed International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) was prepared by Paul Pacter, IASB

Accounting Technical Workshop New Irish GAAP- FRS 102/ November 2015

Accounting Technical Workshop New Irish GAAP- FRS 102/103 13 November 2015 Agenda Welcome & Introduction Recap Where we are now and how we got here Key differences between Old and New Irish GAAP Steps

Accounting Technical Workshop New Irish GAAP- FRS 102/103 13 November 2015 Agenda Welcome & Introduction Recap Where we are now and how we got here Key differences between Old and New Irish GAAP Steps

An essential charity update. Are you. ready for the Big Change? Alliotts guide to how the new 2015 SORPs will affect your charity.

Are you An essential charity update ready for the Big Change? Alliotts guide to how the new 2015 SORPs will affect your charity www.alliotts.com Contents Page 3: What changes have been made? Page 3: What

Are you An essential charity update ready for the Big Change? Alliotts guide to how the new 2015 SORPs will affect your charity www.alliotts.com Contents Page 3: What changes have been made? Page 3: What

Accounting Update. Kelly Martin. Spring 2014

Accounting Update Kelly Martin Spring 2014 Agenda IASB update IASB timetable & new for 2014 Revenue Leasing UK GAAP update Reminder & proposed changes War stories 32 IASB update IASB timetable & new for

Accounting Update Kelly Martin Spring 2014 Agenda IASB update IASB timetable & new for 2014 Revenue Leasing UK GAAP update Reminder & proposed changes War stories 32 IASB update IASB timetable & new for

Financial reporting standards and amendments to financial reporting standards

Financial reporting standards and amendments to financial reporting standards FRS 100 Application of Financial Reporting Requirements FRS 101 Reduced Disclosure Framework These new standards were issued

Financial reporting standards and amendments to financial reporting standards FRS 100 Application of Financial Reporting Requirements FRS 101 Reduced Disclosure Framework These new standards were issued

UK Company Accounts The New Reporting Regime. Factsheet 06 Accounting for Investment Property. Peter Edwards

UK Company Accounts The New Reporting Regime Factsheet 06 Accounting for Investment Property Peter Edwards Contents Introduction... 2 New UK GAAP v. Old UK GAAP... 3 Small companies... 9 Micro-entities...

UK Company Accounts The New Reporting Regime Factsheet 06 Accounting for Investment Property Peter Edwards Contents Introduction... 2 New UK GAAP v. Old UK GAAP... 3 Small companies... 9 Micro-entities...

IFRS Project Insights Financial Instruments: Classification and Measurement

IFRS Project Insights Financial Instruments: Classification and Measurement 2 October 2012 The IASB s financial instrument project will replace IAS 39 Financial Instruments: Recognition and Measurement.

IFRS Project Insights Financial Instruments: Classification and Measurement 2 October 2012 The IASB s financial instrument project will replace IAS 39 Financial Instruments: Recognition and Measurement.

PREPARING FOR FRS 102 THE NEW UK GAAP

PREPARING FOR FRS 102 THE NEW UK GAAP market leaders for financial training This document represents the text of the PowerPoint displays that are used during the presentation of the seminar: Preparing

PREPARING FOR FRS 102 THE NEW UK GAAP market leaders for financial training This document represents the text of the PowerPoint displays that are used during the presentation of the seminar: Preparing

MITCHELLS & BUTLERS PLC. Adoption of International Financial Reporting Standards

7 December 2005 MITCHELLS & BUTLERS PLC Adoption of International Financial Reporting Standards Mitchells & Butlers plc ( the Group ) today releases its financial results for the 53 weeks to 1 October

7 December 2005 MITCHELLS & BUTLERS PLC Adoption of International Financial Reporting Standards Mitchells & Butlers plc ( the Group ) today releases its financial results for the 53 weeks to 1 October

Welcome. FRS 102 CIMA Webinar December Contents. Contents

Welcome FRS 102 CIMA Webinar December 2014 Presented by: Adrian Gibbons BSc ACA 0845 450 5555 www.swat.co.uk Making your practice compliant, efficient and profitable Contents The Reporting Framework 2015

Welcome FRS 102 CIMA Webinar December 2014 Presented by: Adrian Gibbons BSc ACA 0845 450 5555 www.swat.co.uk Making your practice compliant, efficient and profitable Contents The Reporting Framework 2015

NHF Finance Forums 2012

www.pwc.com NHF Finance Forums 2012 SORP and IFRS (or new UK GAAP) Alphabet Soup! Plans for the session Part 1 Part 2 Part 3 Introduction, background, taking stock Implications for housing sector Where

www.pwc.com NHF Finance Forums 2012 SORP and IFRS (or new UK GAAP) Alphabet Soup! Plans for the session Part 1 Part 2 Part 3 Introduction, background, taking stock Implications for housing sector Where

FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime The FRC's mission is to promote transparency and

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime The FRC's mission is to promote transparency and

November Changes to the financial reporting framework in Singapore.

November 2008 Changes to the financial reporting framework in Singapore. The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

November 2008 Changes to the financial reporting framework in Singapore. The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

Meridian Petroleum plc RESTATED INTERIM RESULTS FOLLOWING ADOPTION OF IFRS for the Six Month period ended 30 June 2006 (Unaudited)

") Meridian Petroleum plc Meridian Petroleum plc RESTATED INTERIM RESULTS FOLLOWING ADOPTION OF IFRS for the Six Month period ended 30 June 2006 (Unaudited) The results for the year ended December 2006 have

Meridian Petroleum plc Meridian Petroleum plc RESTATED INTERIM RESULTS FOLLOWING ADOPTION OF IFRS for the Six Month period ended 30 June 2006 (Unaudited) The results for the year ended December 2006 have

SORP information sheet 4: the adoption of FRS 102 by charities reporting under the SORP

SORP information sheet 4: the adoption of FRS 102 by charities reporting under the SORP 1. Background 1.1. The Charity Commission and the Office of the Scottish Charity Regulator are the joint SORP-making

SORP information sheet 4: the adoption of FRS 102 by charities reporting under the SORP 1. Background 1.1. The Charity Commission and the Office of the Scottish Charity Regulator are the joint SORP-making

Supporting Older People Conference

Supporting Older People Conference Speakers: Active chair: SP1: The housing SORP but not as we know it! Mei Ashelford Project Director, Accounting and Reporting Policy Team, Financial Reporting Council

Supporting Older People Conference Speakers: Active chair: SP1: The housing SORP but not as we know it! Mei Ashelford Project Director, Accounting and Reporting Policy Team, Financial Reporting Council

ACCOUNTS AND AUDIT UPDATE SPRING 2017 FOR. Guy Loveday

ACCOUNTS AND AUDIT UPDATE SPRING 2017 FOR Guy Loveday 1 WHAT IS COMING UP? TRIENNIAL REVIEW OF FRS 102 REGIME REMINDER SMALL COMPANY FILING OPTIONS UNDER FRS 102 S1A - WHAT MIGHT BE REQUIRED FOR TRUTH

ACCOUNTS AND AUDIT UPDATE SPRING 2017 FOR Guy Loveday 1 WHAT IS COMING UP? TRIENNIAL REVIEW OF FRS 102 REGIME REMINDER SMALL COMPANY FILING OPTIONS UNDER FRS 102 S1A - WHAT MIGHT BE REQUIRED FOR TRUTH

24. Accounting for groups and the preparation of consolidated accounts

24. Accounting for groups and the preparation of consolidated accounts 24.1. All charities using the FRSSE that prepare consolidated accounts, whether as a requirement of charity law or on a voluntary

24. Accounting for groups and the preparation of consolidated accounts 24.1. All charities using the FRSSE that prepare consolidated accounts, whether as a requirement of charity law or on a voluntary

To: IASB. From: Herman Molenaar, Chief Financial Officer Vanderlande Industries

To: IASB From: Herman Molenaar, Chief Financial Officer Vanderlande Industries Name of Submitter: Herman Molenaar, CFO Organisation: Vanderlande Industries Holding BV Country / jurisdiction: the Netherlands

To: IASB From: Herman Molenaar, Chief Financial Officer Vanderlande Industries Name of Submitter: Herman Molenaar, CFO Organisation: Vanderlande Industries Holding BV Country / jurisdiction: the Netherlands

29 June SAVILLS PLC (Savills or 'The Group') ADOPTION OF INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS)

ADOPTION OF INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS)") 29 June 2005 SAVILLS PLC (Savills or 'The Group') ADOPTION OF INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) Introduction From 1 January 2005, the Group is required to prepare its consolidated financial

29 June 2005 SAVILLS PLC (Savills or 'The Group') ADOPTION OF INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) Introduction From 1 January 2005, the Group is required to prepare its consolidated financial

FRS 100 Application of Financial Reporting Requirements

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 100 Application of Financial Reporting Requirements The FRC's mission is to promote transparency and integrity in business.

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 100 Application of Financial Reporting Requirements The FRC's mission is to promote transparency and integrity in business.

HIGHER EDUCATION INSTITUTIONS AND THE NEW UK GAAP. A comparison of current and future accounting

HIGHER EDUCATION INSTITUTIONS AND THE NEW UK GAAP A comparison of current and future accounting SESSION 1 - INTRODUCTION AND OVERVIEW FRS 100 Application of Financial Reporting Requirements May voluntarily

HIGHER EDUCATION INSTITUTIONS AND THE NEW UK GAAP A comparison of current and future accounting SESSION 1 - INTRODUCTION AND OVERVIEW FRS 100 Application of Financial Reporting Requirements May voluntarily

SESSION 36 IFRS 1 FIRST-TIME ADOPTION

SESSION 36 IFRS 1 FIRST-TIME ADOPTION Overview Objective To explain how an entity s first-time IFRS financial statements should be prepared and presented in accordance with IFRS 1 First-Time Adoption of

SESSION 36 IFRS 1 FIRST-TIME ADOPTION Overview Objective To explain how an entity s first-time IFRS financial statements should be prepared and presented in accordance with IFRS 1 First-Time Adoption of

INTERNATIONAL FINANCIAL REPORTING STANDARDS AND CHARITIES

INTERNATIONAL FINANCIAL REPORTING STANDARDS AND CHARITIES A review of the potential impact of recent proposals Spring 2010 A review of the potential impact of recent proposals Spring 2010 03 IFRS FOR

INTERNATIONAL FINANCIAL REPORTING STANDARDS AND CHARITIES A review of the potential impact of recent proposals Spring 2010 A review of the potential impact of recent proposals Spring 2010 03 IFRS FOR

Accounting and reporting by charities: the statement of recommended practice (SORP) scope and application

scope and application") Accounting and reporting by charities: the statement of recommended practice (SORP) scope and application Introduction 1. The Statement of Recommended Practice applicable to charities preparing their accounts

Accounting and reporting by charities: the statement of recommended practice (SORP) scope and application Introduction 1. The Statement of Recommended Practice applicable to charities preparing their accounts

Changes to Dutch Accounting Standards for micro-sized and small legal entities Changes to annual edition 2017

Changes to Dutch Accounting Standards for micro-sized and small legal entities Changes to annual edition 2017 Professional Practice Department October 2017 Changes to Dutch Accounting Standards for micro-sized

Changes to Dutch Accounting Standards for micro-sized and small legal entities Changes to annual edition 2017 Professional Practice Department October 2017 Changes to Dutch Accounting Standards for micro-sized

United Kingdom case study

United Kingdom case study Richard Martin Head of Financial Reporting ACCA Global body for professional accountants 140,000 members and 404,000 students 80,000 members in Europe 170 countries Implementing

United Kingdom case study Richard Martin Head of Financial Reporting ACCA Global body for professional accountants 140,000 members and 404,000 students 80,000 members in Europe 170 countries Implementing