mhaven.net EXPATRIATION TAX PRESENTED BY MONICA HAVEN, EA, JD, LLM

|

|

|

- Curtis Walsh

- 6 years ago

- Views:

Transcription

1 EXPATRIATION TAX 2016 PRESENTED BY MONICA HAVEN, EA, JD, LLM

2 LEARNING OBJECTIVES Identify covered expatriates & exempt individuals Determine the basis on which the exit tax is computed Apply & correctly allocate the lifetime exclusion Know how to report & when to pay the tax 2

; moved to father s native country after pardon")

; was Brazilian first but moved to US when")

; to avoid")

; to accept a post as representative of the")

3 FAMOUS FORMER CITIZENS Tina Turner Switzerland (2013); lived 20 years in-country and married to German music executive Denise Rich Austria (2011); moved to father s native country after pardon by President Clinton Jet Li Singapore (2009); school system for daughters but Singapore does not allow dual citizenship Eduardo Savarin Singapore (2009); was Brazilian first but moved to US when targeted for kidnapping Bobby Fisher Iceland (2005); arrested and jailed for 8 months in Japan when US passport revoked for anti-american activities John Templeton Bahamas (1968); to avoid estate tax Yul Brynner Switzerland (1965); renounced when IRS sought to tax dual citizen who over-stayed in US President John Tyler Virginia (1862); to accept a post as representative of the Confederacy

4 AND THE NOT-SO FAMOUS Donna-Lane Nelson Switzerland (2011); Swiss bank threatened to close Americans accounts due to FATCA reporting requirements Laurie Lautman New Zealand (2013); can t afford annual tax prep fee of $3,360 to have US returns prepared Christina Amman Switzerland; burdensome FBAR reporting for joint accounts with Swiss husband Corine Mauch Switzerland; born to Swiss parents and feels at home in Zurich Norman Heinrich-Gale Austria; moved to the Alps when overwhelmed by pace of American life Quincy Davis III Taiwan; joined national basketball team Carol Tapanila Canada; wants to protect retirement savings earned in Canada from US tax

5 AND THE EXODUS CONTINUES

6 WHY LEAVE? High federal (& state) tax rates US taxes on worldwide income Burdensome reporting requirements under Bank Secrecy Act (1970) & Foreign Account Compliance Act (2010) Obtain or retain citizenship in a country that does allow dual citizenship In protest of US politics and policies: Creole entertainer & civil rights activist Josephine Baker angered by racism & discrimination Running for political office abroad: Andreas Papandreou became Prime Minister of Greece To obtain release from detention: Yasser Hamdi captured in Afghanistan & declared an enemy combatant

and does not return to the US to satisfy immigration rules Some are asked to leave Americans wishing to leave need not")

7 REASONS DON T MATTER The list of reasons is varied and long Some are accidental Americans Inadvertent forfeiture - Green Card holder who works & lives abroad claims Foreign Earned Income Exclusion (subject to residency tests) and does not return to the US to satisfy immigration rules Some are asked to leave Americans wishing to leave need not explain

8 WHATEVER THE REASON US will assess a departure tax to discourage tax avoidance by forfeiting US citizenship or residency Assessed on unrealized gains Known as the Exit or Expatriation Tax

9

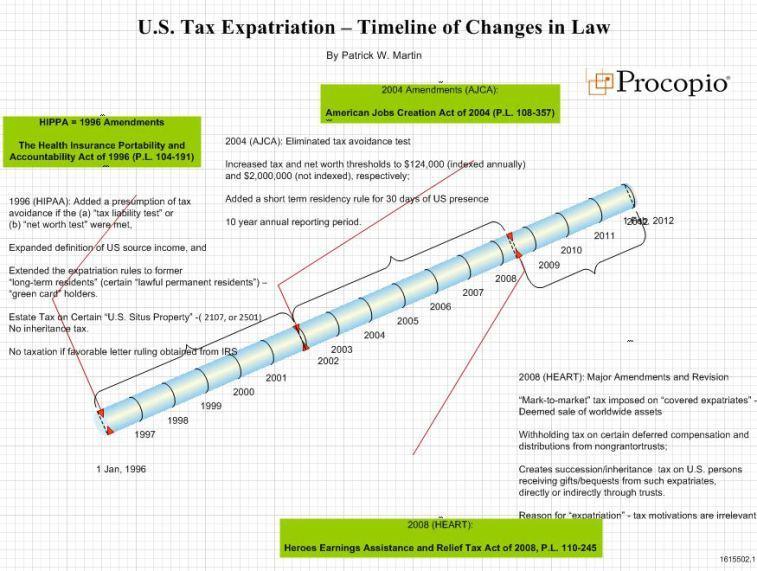

10 BACKGROUND 1913: 16 th Amendment created a tax regime that was citizenship-based Applied to every citizen of the US, whether residing at home or abroad 1918: Foreign Tax Credit introduced 1926: Foreign Earned Income Exclusion - No income limitations until : maximum exclusion = $101, : maximum exclusion = $102,100

11

12 COVERED EXPATRIATES Heroes Earnings Assistance and Relief Tax Act ( HEART ) of 2008 Reason for departure irrelevant presumption of tax avoidance now mute Covered if expatriate satisfies any one of the following three tests Income Tax Liability Net Worth (Non-)compliance

13 INCOME TEST Average annual income tax for 5 most recent years ending before expatriation > $161K [in 2016] Adjusted annually for inflation Effective June 18, 2008

14 NET WORTH TEST Must be > $2 million on date of expatriation No inflation adjustment Effective June 18, 2008

15 COMPLIANCE TEST Must certify compliance with all federal tax obligations for 5 most recent years ending before expatriation Use Form 8854 Initial and Annual Expatriation Statement Effective June 18, 2008

16 EXEMPT INDIVIDUALS Not covered if: Dual citizenship since birth, AND Have not lived in US more than 10 of most recent 15 years Individuals under age 18½ who have not lived in US more than 10 years

17 HOW TO EXPATRIATE Renunciation voluntary forfeiture of citizenship Requires formal process before a US diplomatic or consular officer in a foreign state Relinquishment involuntary forfeiture of citizenship Renounce in time of war with US Attorney General s approval Commit an act of treason [will lose citizenship but not tax status] Pledge an oath of allegiance to a foreign country Join the armed services of another country engaged in war against the US or join another country s army as an officer even if that country is not at war with the US Work for a foreign government while also a citizen of that country Accept employment by a foreign government in a job for which an oath of allegiance is required Abandonment voluntary forfeiture of residency

18 EXPATRIATION: US CITIZENS On the earliest date of: When renunciation before US diplomatic or consular officer is approved & certificate issued by US Dept. of State When person submits signed statement of voluntary relinquishment & certificate issued by US Dept. of State When US Dept. of State issues certificate of loss of nationality When US court cancels certificate of naturalization

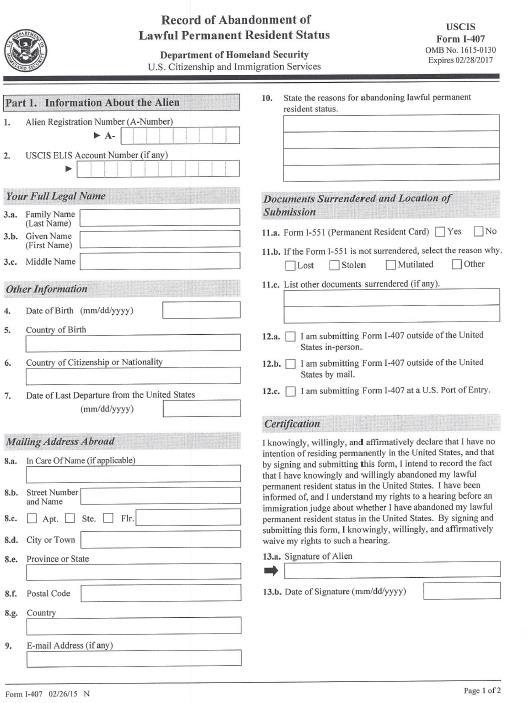

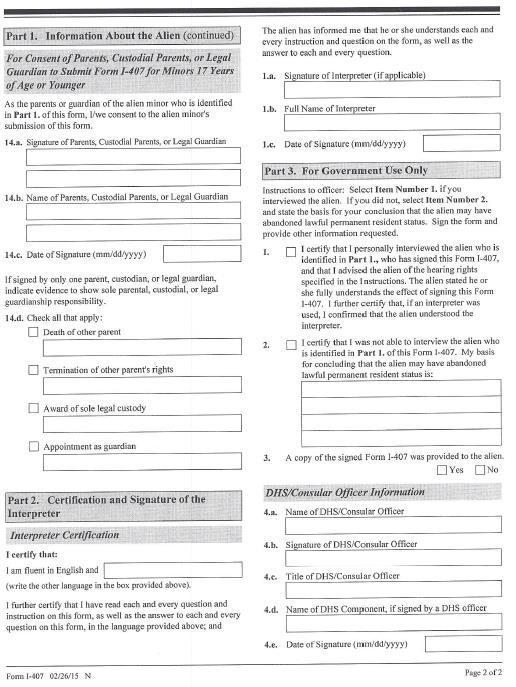

19 EXPATRIATION: US RESIDENTS Lawful permanent residency ceases when: Immigration & residency status revoked or administratively determined to have been abandoned, OR Inadvertent abandonment: Individual treated as resident of foreign country as per prevailing tax treaty & does not waive treaty provisions via Form 8333 Treaty-Based Return Position Disclosure and Form 8854 Initial and Annual Expatriation Statement (Part 1, Line 5), OR Formal abandonment: Individual submits Form I-407 Abandonment of Lawful Permanent Resident Status to US consular officer Green Card Holder subject to expatriation rules only if long-term resident (at least 8 of most recent 15 years)

20

21

22

23 BASIS FOR TAX Asset-based tax uses a mark-to-market regime Assessed on unrealized gains as if all assets sold 1 day before expatriation date Applied to all of expatriate s worldwide assets & future gifts/bequests Phantom gains (& losses) are subject to income tax Subject to capital gains & ordinary income tax rates Gifts & bequests taxed at highest estate tax rate Reported on Form 8854

24 EXEMPT ASSETS Certain deferred compensation plans & retirement accounts Non-grantor trusts (expatriate is not the owner on day before expatriation) Subject to automatic 30% withholding upon distribution Example Company granted restricted stock units to employee in 2015, receivable in 2017 if he continues to work for company. Taxpayer quits job and expatriates in 2016 units will be treated as vested on day before expatriation & subject to exit tax If instead taxpayer continues to work & notifies company of status as covered expatriate no exit tax inclusion but distributions subject to 30% withholding

25 EXCLUSION AMOUNT Tax basis may be reduced by applicable exclusion amount (indexed for inflation) $693,000 [in 2016] Each individual eligible for one lifetime exclusion amount Must be allocated on pro-rata basis to all gain properties Gains & losses actually realized upon later disposition may be adjusted for phantom gains and losses which were subject to exit tax

26 ALLOCATION OF EXCLUSION AMT. Covered Expatriate relinquished gain in He owned the following: Step 1: Step 2: Step 3: Asset FMV on date of expatriation ($) Basis = FMV at Purchase ($) Multiply total exclusion amount [$693K in 2016] by ratio of individual gain over aggregate gain on all assets. NOTE: Exclusion amount is not allocated to asset with built-in loss. Asset X: (1.8 million 2 million) X 693,000 = $623,700 Asset Y: (200,000 2 million) X 693,000 = $69,300 Subtract allocated exclusion amount from deemed gain Asset X: 1.8 million 623,700 = $1,176,300 reportable gain Asset Y: 200,000 62,600 = $130,700 reportable gain Built-in Gain or Loss ($) X 2,000, ,000 1,800,000 Y 1,000, , ,000 Z 500, ,000 (300,000) Aggregate Gain = $2 million Report includible gains of Assets X and Y, as well as loss of Asset Z on Form 1040 for the portion of the taxable year that includes day before expatriation. File Form 1040NR for the remainder of taxable year.

Expat is entitled to annual gift exclusion [$14K in 2016] but not lifetime exclusion [$5.")

27 GIFTS & BEQUESTS Expatriates are forever subject to gift and estate taxes on property transferred to US citizen or resident beneficiaries NOTE: Transfers to citizen spouse & non-citizen beneficiaries are exempt Property is valued at FMV on date of gift (death) Expat is entitled to annual gift exclusion [$14K in 2016] but not lifetime exclusion [$5.45 million in 2016] Example US citizen has only cash assets on date of expatriation no exit tax Expat later bequeaths net worth to his citizen children entire net worth subject to estate tax Same rules apply to expat s foreign trust if beneficiary is US citizen or resident

28 WHO IS LIABLE? Gifts and estates from expats are taxed at highest marginal rate in effect [40% in 2016] Tax becomes liability of US citizen or resident donee Forever taint can live on for multiple generations if beneficiaries include grandchildren & great-grandchildren Example High net worth taxpayer renounces citizenship & bequests $10 million to each of her US citizen children Each beneficiary will owe $4 million of federal tax in lieu of the estate taxes that expat will not pay

29 REPORTING THE TAX Gain or loss from deemed sales are included on Form 1040 (Forms 8949 & 4797, and Schedule D) Character of gain is preserved as capital or ordinary, short- or long-term Due 90 days after expatriation May make irrevocable election to defer payment until gain is realized on individual assets [must submit bond to guarantee payment of tax]

30 PAYING THE TAX Exit tax is due 90 days after expatriation Taxpayer may make irrevocable election to defer payment on asset by asset basis Must file Form 8854, Schedule C Must submit bond to Secretary of the Treasury to guarantee payment of tax If deferral agreement accepted by IRS, payment must be made by the earlier of: Due date of return for year in which asset is actually sold, OR Due date of the return for the year of expat s death, OR Date that posted bond is considered insufficient IRS will provide 30-day notice to taxpayer to increase bond or pay tax

31

32 FILING REQUIREMENTS Form 8854 must be filed with US consulate or federal court at time of expatriation NOTE: Failure to file penalty = $10,000 Expatriates must file even if no exit tax due Taxpayer must certify that he has complied with all federal tax filing requirements for most recent 5- year period before expatriation Must file Form 8854 annually for 10 years due April 15 th Must also file Form 1040NR for 10 years

33 FORM 8854 PART I GENERAL TAXPAYER INFO & GUIDANCE WHICH PARTS TO COMPLETE BASED ON DATE OF EXPATRIATI ON

34 FORM 8854 PART III PROVIDE MARK-TO- MARKET VALUATIO NS OF ALL ASSETS

35 FORM 8854 PART IV VERIFY THAT TAX RETURNS FOR 5 PRIOR YEARS HAVE BEEN FILED & THAT TAXPAYER IS NOT AN EXEMPT INDIVIDUA L

36 FORM 8854 PART IV USE TO ELECT DEFERRA L OF TAX PAYMENT

37 FORM 8854 PART V TAXPAYER MUST PROVIDE BALANCE SHEET & INCOME STATEMENT

38 PAY TO LEAVE

39 Monica Haven, E.A., J.D., L.L.M. PHONE: (310) FAX: (310) WEBSITE: www. Student Text to accompany this presentation is available on the Publications page of my website. The information contained herein is for educational use only and should not be construed as tax, financial, or legal advice. Each individual s situation is unique and may require specialized treatment. It is, therefore, imperative that you consult with tax and legal professionals prior to implementation of any strategies discussed.

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

TECHNICAL EXPLANATION OF H.R

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

Expatriation from the United States

Expatriation from the United States Hal J. Webb November 15, 2012 Bahamas Discussion Points Tax Rules Applicable to Expatriations on or After June 17, 2008 Reporting Requirements Planning for Expatriation

Expatriation from the United States Hal J. Webb November 15, 2012 Bahamas Discussion Points Tax Rules Applicable to Expatriations on or After June 17, 2008 Reporting Requirements Planning for Expatriation

"US recipients of gifts and bequests from Covered Expatriates will now incur gift and estate tax"

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

U.S. Adopts Exit Tax Upon Expatriation*

Originally published in: BNA Tax Planning International Review December 16, 2008 U.S. Adopts Exit Tax Upon Expatriation* By: Ellen S. Brody and Jason K. Binder With the passage of the Heroes Earnings Assistance

Originally published in: BNA Tax Planning International Review December 16, 2008 U.S. Adopts Exit Tax Upon Expatriation* By: Ellen S. Brody and Jason K. Binder With the passage of the Heroes Earnings Assistance

Filing Requirements U.S. citizens residing in Canada must file both Canadian and U.S. income tax returns every year.

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

Tax Planning for U.S. Citizen Residents in Canada. Maximize your wealth by utilizing tax planning ideas and understanding the tax issues

The Navigator RBC WEALTH MANAGEMENT SERVICES Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

The Navigator RBC WEALTH MANAGEMENT SERVICES Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

The Wolfe Law Group Gary S. Wolfe, A Professional Law Corporation. March 18, Expatriation and the Ten Year Rule

The Wolfe Law Group Gary S. Wolfe, A Professional Law Corporation 6303 WILSHIRE BOULEVARD TELEPHONE (323) 782-9139 SUITE 201 FACSIMILE (323) 782-9289 LOS ANGELES, CA 90048 E-MAIL gsw@gswlaw.com March 18,

The Wolfe Law Group Gary S. Wolfe, A Professional Law Corporation 6303 WILSHIRE BOULEVARD TELEPHONE (323) 782-9139 SUITE 201 FACSIMILE (323) 782-9289 LOS ANGELES, CA 90048 E-MAIL gsw@gswlaw.com March 18,

Expatriation. IRS Proposes New Regulations on Gifts. Abrahm W. Smith. Tax Section of the Florida Bar Wednesday, February 10, 2016

Expatriation IRS Proposes New Regulations on Gifts Tax Section of the Florida Bar Wednesday, February 10, 2016 Abrahm W. Smith Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a

Expatriation IRS Proposes New Regulations on Gifts Tax Section of the Florida Bar Wednesday, February 10, 2016 Abrahm W. Smith Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a

State of Expatriation 2012 TTN Conference New York 2013

State of Expatriation 2012 TTN Conference New York 2013 Michael G. Pfeifer, Esq. Caplin & Drysdale, Chartered May 6, 2013 Session Overview HISTORY OF EXPATRIATION RULES ( Alternative Tax Regime to Mark-to-Market

State of Expatriation 2012 TTN Conference New York 2013 Michael G. Pfeifer, Esq. Caplin & Drysdale, Chartered May 6, 2013 Session Overview HISTORY OF EXPATRIATION RULES ( Alternative Tax Regime to Mark-to-Market

Good Bye U.S.A. Emigration and Expatriation of U.S. Persons and Dual Nationals International Wealth Planners December 8, 2011 London

Good Bye U.S.A. Emigration and Expatriation of U.S. Persons and Dual Nationals International Wealth Planners December 8, 2011 London US citizens and lawful permanent residents US citizen At birth Born

Good Bye U.S.A. Emigration and Expatriation of U.S. Persons and Dual Nationals International Wealth Planners December 8, 2011 London US citizens and lawful permanent residents US citizen At birth Born

ALIYAH FROM THE USA. STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017

Washington, DC New York, NY New Haven, CT Chicago, IL ALIYAH FROM THE USA STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017 Stanley A. Barg Kozusko Harris Duncan Email: sbarg@kozlaw.com

Washington, DC New York, NY New Haven, CT Chicago, IL ALIYAH FROM THE USA STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017 Stanley A. Barg Kozusko Harris Duncan Email: sbarg@kozlaw.com

A Comparison of the New U.S. Expatriation Tax and the Canadian Departure Tax

University of St. Thomas, Minnesota UST Research Online Accounting Faculty Publications Accounting 2009 A Comparison of the New U.S. Expatriation Tax and the Canadian Departure Tax Alexander M. Gelardi

University of St. Thomas, Minnesota UST Research Online Accounting Faculty Publications Accounting 2009 A Comparison of the New U.S. Expatriation Tax and the Canadian Departure Tax Alexander M. Gelardi

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

Should Retirees Still Consider Expatriating?

Originally published in: Journal of Retirement Planning May 1, 2009 Should Retirees Still Consider Expatriating? By: Ellen S. Brody and Jason K. Binder* Introduction With the passage of the Heroes Earnings

Originally published in: Journal of Retirement Planning May 1, 2009 Should Retirees Still Consider Expatriating? By: Ellen S. Brody and Jason K. Binder* Introduction With the passage of the Heroes Earnings

Expatriation Tax. Monica Haven Summary

Expatriation Tax Monica Haven 013115 Summary Leaving so soon, my little pretty? Why my little party s just beginning. So says the Wicked Witch of the West to Dorothy. Apparently the little girl from Kansas

Expatriation Tax Monica Haven 013115 Summary Leaving so soon, my little pretty? Why my little party s just beginning. So says the Wicked Witch of the West to Dorothy. Apparently the little girl from Kansas

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons Matthew R. Hillery, Director September 27, 2016 Speaker Matthew R. Hillery Director in the Private Client Department. Concentrates

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons Matthew R. Hillery, Director September 27, 2016 Speaker Matthew R. Hillery Director in the Private Client Department. Concentrates

Top 10 Tax Issues facing U.S. Citizens living in Canada

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

EXPATRIATION: STILL THE ULTIMATE ESTATE PLAN

EXPATRIATION: STILL THE ULTIMATE ESTATE PLAN What is expatriation? Why expatriate? The mechanics of expatriation Are you a covered expatriate? Exit tax is only on UNREALIZED gains How to minimize or eliminate

EXPATRIATION: STILL THE ULTIMATE ESTATE PLAN What is expatriation? Why expatriate? The mechanics of expatriation Are you a covered expatriate? Exit tax is only on UNREALIZED gains How to minimize or eliminate

Aliens & Citizens: Foreign and Domestic Tax Issues

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

EXPATRIATION TAX AND PLANNING

New Haven New York Geneva EXPATRIATION TAX AND PLANNING Greenwich London Speaker: Ivan A. Sacks, Esq. Chairman, Withersworldwide Partner, Withers Bergman LLP Milan May 1, 2014 Miami, Florida Hong Kong

New Haven New York Geneva EXPATRIATION TAX AND PLANNING Greenwich London Speaker: Ivan A. Sacks, Esq. Chairman, Withersworldwide Partner, Withers Bergman LLP Milan May 1, 2014 Miami, Florida Hong Kong

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION September 27, 2017 Congress and the Administration are expected to consider changes in US

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION September 27, 2017 Congress and the Administration are expected to consider changes in US

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION February 7, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION February 7, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

Estate Planning for Foreign Nationals

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

If you have foreign accounts, entities, or assets, chances are that you

International Tax Form Filing Guide If you have foreign accounts, entities, or assets, chances are that you will be required to file various forms disclosing them. Some of these forms are filed with your

International Tax Form Filing Guide If you have foreign accounts, entities, or assets, chances are that you will be required to file various forms disclosing them. Some of these forms are filed with your

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

An Introduction to the US Estate and Gift Tax Regime

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

Expatriation Pursuant to the Heroes Act

August 2008 Expatriation Pursuant to the Heroes Act BY MICHAEL D. HAUN AND ERIC W. ENSMINGER Introduction On May 20, 2008 and May 22, 2008, the House of Representatives and the Senate, respectively, unanimously

August 2008 Expatriation Pursuant to the Heroes Act BY MICHAEL D. HAUN AND ERIC W. ENSMINGER Introduction On May 20, 2008 and May 22, 2008, the House of Representatives and the Senate, respectively, unanimously

Selected US Tax Developments

canadian tax journal / revue fiscale canadienne (2008) vol. 56, n o 2, 559-70 Selected US Tax Developments Co-Editors: Sanford H. Goldberg* and Peter A. Glicklich** New Expatriation Rules Under Sections

canadian tax journal / revue fiscale canadienne (2008) vol. 56, n o 2, 559-70 Selected US Tax Developments Co-Editors: Sanford H. Goldberg* and Peter A. Glicklich** New Expatriation Rules Under Sections

Domestic Tax Issues for Non-resident Aliens

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

International Journal TM

International Journal TM Reproduced with permission from Tax Management International Journal, 47 TM International Journal 439, 7/13/18. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033)

International Journal TM Reproduced with permission from Tax Management International Journal, 47 TM International Journal 439, 7/13/18. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033)

INSIGHT: EXIT TAX: Through the Maze of Expatriation Part 1

Reproduced with permission from Daily Tax Report, 18 DTR 61, 03/29/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Expatriation INSIGHT: EXIT TAX: Through

Reproduced with permission from Daily Tax Report, 18 DTR 61, 03/29/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Expatriation INSIGHT: EXIT TAX: Through

U.S. Citizens Living in Canada

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

A comparison of the Form filing requirements and the Form 8938 filing requirements follows:

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

International Trade and/or Investment Affords Opportunities

Overview of International Estate Planning Issues Affecting U.S. Persons or Non-U.S. Persons with U.S. Sitused Assets 2010 Advanced Tax Institute November 3, 2010 Baltimore, Maryland Elizabeth M. Schurig

Overview of International Estate Planning Issues Affecting U.S. Persons or Non-U.S. Persons with U.S. Sitused Assets 2010 Advanced Tax Institute November 3, 2010 Baltimore, Maryland Elizabeth M. Schurig

Foreign Tax Issues REBECCA DONEHEW

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

The Interaction of Immigration and Tax

The Interaction of Immigration and Tax A Discussion of Visa Options, Green Cards, and US Citizenship and the Corresponding Tax Consequences Florida Bar Tax Section Presentation November 2, 2016 Abrahm

The Interaction of Immigration and Tax A Discussion of Visa Options, Green Cards, and US Citizenship and the Corresponding Tax Consequences Florida Bar Tax Section Presentation November 2, 2016 Abrahm

Presentation to: The 1818 Society on The U.S. Exit Tax

Presentation to: The 1818 Society on The U.S. Exit Tax Dale Mason, CPA The Wolf Group The Wolf Group, PC 4401 Fair Lakes Court, Suite 310, Fairfax, VA 22033 Tel: (703) 502-9500 Disclaimer Any U.S. tax

Presentation to: The 1818 Society on The U.S. Exit Tax Dale Mason, CPA The Wolf Group The Wolf Group, PC 4401 Fair Lakes Court, Suite 310, Fairfax, VA 22033 Tel: (703) 502-9500 Disclaimer Any U.S. tax

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

U.S. Issues for U.S. Citizens Living in Canada

U.S. Issues for U.S. Citizens Living in Canada March 26, 2009 Angela Zarn, CA, CPA, CAFA Presented to Scotia Bank Table of Contents! Filing Requirements & Due Dates! Difference in Taxation between countries!

U.S. Issues for U.S. Citizens Living in Canada March 26, 2009 Angela Zarn, CA, CPA, CAFA Presented to Scotia Bank Table of Contents! Filing Requirements & Due Dates! Difference in Taxation between countries!

Tax Planning for U.S. persons in Europe Residency in Europe, Disclosure, Expatriation. Thierry Boitelle Stanley C. Ruchelman Beate Erwin

Tax Planning for U.S. persons in Europe Residency in Europe, Disclosure, Expatriation Thierry Boitelle Stanley C. Ruchelman Beate Erwin Agenda Issues U.S. Persons Encounter in Europe Disclosure Procedures

Tax Planning for U.S. persons in Europe Residency in Europe, Disclosure, Expatriation Thierry Boitelle Stanley C. Ruchelman Beate Erwin Agenda Issues U.S. Persons Encounter in Europe Disclosure Procedures

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

US and Canadian tax considerations for withdrawals and transfers to RRSP

Reference Paper for Vancity US and Canadian tax considerations for withdrawals and transfers to RRSP Introduction This paper will discuss the tax implications for Canadian resident who has participated

Reference Paper for Vancity US and Canadian tax considerations for withdrawals and transfers to RRSP Introduction This paper will discuss the tax implications for Canadian resident who has participated

9/20/2017. USA the dream destination. EB5 visa allows dream to be a reality. Tax regulations in USA affecting NRIs Resident Indians

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

Did You Say You Have a U.S. Passport?

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

Tax Information for Americans and Green Card Holders Living in Switzerland

Who must file Non-compliance What income needs to be declared? Double taxation Foreign Tax Credit Foreign Earned Income Exclusion Domiciliary states FBAR All U.S. citizens and green card (GC) holders abroad.

Who must file Non-compliance What income needs to be declared? Double taxation Foreign Tax Credit Foreign Earned Income Exclusion Domiciliary states FBAR All U.S. citizens and green card (GC) holders abroad.

American Bar Association. Expatriation and the New Section 2801 Proposed Regulations

American Bar Association Expatriation and the New Section 2801 Proposed Regulations The International Tax Planning Committee of the Income and Transfer Tax Planning Group of the Real Property, Trust &

American Bar Association Expatriation and the New Section 2801 Proposed Regulations The International Tax Planning Committee of the Income and Transfer Tax Planning Group of the Real Property, Trust &

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

The HIRE Act contains several provisions of interest to clients with foreign accounts and foreign trusts including the FATCA provisions.

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

T he relatively strong U.S. economy continues to attract

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

Tax Issues for U.S. Citizens Living Abroad

LifeMark Partners, Inc. 1306 Concourse Drive Suite 350 Linthicum, MD 21090 410-837-3022 marketing@lifemarkpartners.com www.lifemarkpartners.com Tax Issues for U.S. Citizens Living Abroad Page 1 of 5, see

LifeMark Partners, Inc. 1306 Concourse Drive Suite 350 Linthicum, MD 21090 410-837-3022 marketing@lifemarkpartners.com www.lifemarkpartners.com Tax Issues for U.S. Citizens Living Abroad Page 1 of 5, see

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

Agenda. US Taxation for Expatriates, US Passport/ Green Card Holders and Recent Tax Law Changes American Chamber of Commerce Bahrain 3/7/16

US Taxation for Expatriates, US Passport/ Green Card Holders and Recent Tax Law Changes American Chamber of Commerce Bahrain Alex P Jones 23 February 2016 Agenda Deloitte US High Net Worth Team US Approach

US Taxation for Expatriates, US Passport/ Green Card Holders and Recent Tax Law Changes American Chamber of Commerce Bahrain Alex P Jones 23 February 2016 Agenda Deloitte US High Net Worth Team US Approach

What You Don t Know Will Hurt You

What You Don t Know Will Hurt You Avoiding International Tax and Estate Planning Traps STEP Silicon Valley April 19, 2017 Richard S. Kinyon, Partner, Shartsis Friese, LLP E.J. Hong, Esq., Law Offices of

What You Don t Know Will Hurt You Avoiding International Tax and Estate Planning Traps STEP Silicon Valley April 19, 2017 Richard S. Kinyon, Partner, Shartsis Friese, LLP E.J. Hong, Esq., Law Offices of

California Society of CPAs 20 th Annual Tax and Accounting Institute. Taking Your Tax Practice International

California Society of CPAs 20 th Annual Tax and Accounting Institute Taking Your Tax Practice International November 18, 2016 Handlery Hotel 8:20 a.m. 10:00 a.m. Jon P. Schimmer, J.D., LL.M., CPA Procopio,

California Society of CPAs 20 th Annual Tax and Accounting Institute Taking Your Tax Practice International November 18, 2016 Handlery Hotel 8:20 a.m. 10:00 a.m. Jon P. Schimmer, J.D., LL.M., CPA Procopio,

Form 8854 Exit Tax Calculations and Reporting: Minimizing the IRC 877A Expatriation Tax

FOR LIVE PROGRAM ONLY Form 8854 Exit Tax Calculations and Reporting: Minimizing the IRC 877A Expatriation Tax THURSDAY, OCTOBER 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Form 8854 Exit Tax Calculations and Reporting: Minimizing the IRC 877A Expatriation Tax THURSDAY, OCTOBER 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

U.S. taxation of foreign citizens

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

Tax Planning for High Net Worth Individuals Immigrating to the United States

The Tax Adviser Tax Planning for High Net Worth Individuals Immigrating to the United States By Rolando Garcia, CPA, J.D., Houston 7 hours 42 minutes ago Editor: Mindy Tyson Weber, CPA, M.Tax. For generations,

The Tax Adviser Tax Planning for High Net Worth Individuals Immigrating to the United States By Rolando Garcia, CPA, J.D., Houston 7 hours 42 minutes ago Editor: Mindy Tyson Weber, CPA, M.Tax. For generations,

NRIs Resident Indians. By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR

Tax regulations in USAaffecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA thedream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USAaffecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA thedream destination USA has always been and will be a dream destination Getting a job Sending

ACA Town Hall Meeting. 21 September 2015 Zurich. We Understand London Geneva Zurich

ACA Town Hall Meeting 21 September 2015 Zurich A story Max & Alice go to see their US tax advisor Max was born in Switzerland and became a US citizen in 1987. Alice was born in the US. They married in

ACA Town Hall Meeting 21 September 2015 Zurich A story Max & Alice go to see their US tax advisor Max was born in Switzerland and became a US citizen in 1987. Alice was born in the US. They married in

U.S. TAX UPDATE: ISSUES THAT CANADIAN ADVISORS SHOULD BE AWARE OF FOR THEIR CLIENTS

STEP LONDON & SOUTHWESTERN ONTARIO CHAPTER LAUNCH EVENT THURSDAY, October 17, 2013 @ 4:30 p.m. U.S. TAX UPDATE: ISSUES THAT CANADIAN ADVISORS SHOULD BE AWARE OF FOR THEIR CLIENTS Speaker : Edward Northwood,

STEP LONDON & SOUTHWESTERN ONTARIO CHAPTER LAUNCH EVENT THURSDAY, October 17, 2013 @ 4:30 p.m. U.S. TAX UPDATE: ISSUES THAT CANADIAN ADVISORS SHOULD BE AWARE OF FOR THEIR CLIENTS Speaker : Edward Northwood,

Estate Planning Council of Toronto: Estate Tax Update

www.pwc.com/ca Estate Planning Council of Toronto: Ian Macdonald November 5, 2013 Agenda US Estate and Gift Tax Update 1. New Rules 2. Implications for US Citizens Living in Canada 3. Implications for

www.pwc.com/ca Estate Planning Council of Toronto: Ian Macdonald November 5, 2013 Agenda US Estate and Gift Tax Update 1. New Rules 2. Implications for US Citizens Living in Canada 3. Implications for

Initial and Annual Expatriation Statement

Form 8854 Department of the Treasury Internal Revenue Service Name Initial and Annual Expatriation Statement OMB No. 1545-0074 For calendar year 2010 or other tax year beginning, 2010, and ending, 20 2010

Form 8854 Department of the Treasury Internal Revenue Service Name Initial and Annual Expatriation Statement OMB No. 1545-0074 For calendar year 2010 or other tax year beginning, 2010, and ending, 20 2010

Introduction: recent trends... CROSS BORDER ESTATE PLANNING. Advocis Breakfast Meeting. Are you American? Is your child? Who should consider U.S. tax?

Introduction: recent trends.... CROSS BORDER ESTATE PLANNING Advocis Breakfast Meeting Will Todd Taxation / Wills, Estates & Trusts Practice Group April 4, 2013... Why pay attention now. More Canadian

Introduction: recent trends.... CROSS BORDER ESTATE PLANNING Advocis Breakfast Meeting Will Todd Taxation / Wills, Estates & Trusts Practice Group April 4, 2013... Why pay attention now. More Canadian

The Grandparent Tax Monica Haven, EA, JD, LLM 2015

The Grandparent Tax Monica Haven, EA, JD, LLM 2015 The Grandparent Tax Plan A Grandpa gifts $10 million to Dad $4 million tax Dad gifts $6 million to Grandson $2.4 million tax Net Gift to Grandson = $3.6

The Grandparent Tax Monica Haven, EA, JD, LLM 2015 The Grandparent Tax Plan A Grandpa gifts $10 million to Dad $4 million tax Dad gifts $6 million to Grandson $2.4 million tax Net Gift to Grandson = $3.6

E/C.18/2016/CRP.7. Note by the Secretariat. Summary. Distr.: General 4 October Original: English

E/C.18/2016/CRP.7 Distr.: General 4 October 2016 Original: English Committee of Experts on International Cooperation in Tax Matters Eleventh session Geneva, 11-14 October 2016 Item 3 (a) (i) of the provisional

E/C.18/2016/CRP.7 Distr.: General 4 October 2016 Original: English Committee of Experts on International Cooperation in Tax Matters Eleventh session Geneva, 11-14 October 2016 Item 3 (a) (i) of the provisional

Henry P. Bubel pbwt.com

Who is a U.S. Person? And the ramifications of being one Henry P. Bubel pbwt.com Why do we care? Income tax Information reporting, including Foreign Bank Account Reports (FBARs) Gift and Estate tax Exit

Who is a U.S. Person? And the ramifications of being one Henry P. Bubel pbwt.com Why do we care? Income tax Information reporting, including Foreign Bank Account Reports (FBARs) Gift and Estate tax Exit

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING. Jenny Coates Law, PLLC, International Tax Lawyer

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

EXPAT TAX.A TO Z. ASSETS Anything you own that has value is considered an asset. Bank accounts,

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

2014 WORLD CONFERENCE: FOREIGN GRANTOR TRUST

r u c h e l m a n 1 2014 WORLD CONFERENCE: FOREIGN GRANTOR TRUST A Foreign Grantor Trust is a Great Solution to Benefit U.S. Persons: A Look at How This is Done Thomas Lee, Chair Thomas Lee & Partners

r u c h e l m a n 1 2014 WORLD CONFERENCE: FOREIGN GRANTOR TRUST A Foreign Grantor Trust is a Great Solution to Benefit U.S. Persons: A Look at How This is Done Thomas Lee, Chair Thomas Lee & Partners

Private Company Services. U.S. Estate and Gift taxation of resident aliens and nonresident aliens

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

FBAR OVDP FATCA You won t find these terms in the Korean-English dictionary!

Your Korean passport may not get you out of the United States (for tax purposes) FBAR OVDP FATCA You won t find these terms in the Korean-English dictionary! But, if the answer to any of the following

Your Korean passport may not get you out of the United States (for tax purposes) FBAR OVDP FATCA You won t find these terms in the Korean-English dictionary! But, if the answer to any of the following

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

U.S. APPROACH TO APPLICATION OF INCOME TAX TREATIES TO PAYMENTS THROUGH HYBRID ENTITIES. Note by Mr. Henry Louie

Distr.: General 18 October 2013 Original: English Committee of Experts on International Cooperation in Tax Matters Ninth session Geneva, 21-25 October 2013 Agenda Item 6(a)i) Article 4 (Resident): Hybrid

Distr.: General 18 October 2013 Original: English Committee of Experts on International Cooperation in Tax Matters Ninth session Geneva, 21-25 October 2013 Agenda Item 6(a)i) Article 4 (Resident): Hybrid

THE BOVE & LANGA REPORT: ELECTION EDITION

Ten Tremont Street, Suite 600 Boston, MA 02108 www.bovelanga.com p 617.720.6040 f 617.720.1919 THE BOVE & LANGA REPORT: ELECTION EDITION March 2016 Once again, we are in the midst of the presidential primary

Ten Tremont Street, Suite 600 Boston, MA 02108 www.bovelanga.com p 617.720.6040 f 617.720.1919 THE BOVE & LANGA REPORT: ELECTION EDITION March 2016 Once again, we are in the midst of the presidential primary

Tax Planning for US Bound Clients

Tax Planning for US Bound Clients International Wealth Planners Geneva, 15 June 2011 Michael Parets Withers LLP, Zurich Office +41 44 488 8803 direct michael.parets@withersworldwide.com US-Bound Clients

Tax Planning for US Bound Clients International Wealth Planners Geneva, 15 June 2011 Michael Parets Withers LLP, Zurich Office +41 44 488 8803 direct michael.parets@withersworldwide.com US-Bound Clients

U.S. TAX PRINCIPLES THAT AFFECT U.S. PERSONS LIVING ABROAD. By Pamela Perez-Cuvit LL.M Madrid, May 26th 2016

U.S. TAX PRINCIPLES THAT AFFECT U.S. PERSONS LIVING ABROAD By Pamela Perez-Cuvit LL.M Madrid, May 26th 2016 UNIQUENESS OF U.S. TAX SYSTEM CITIZENSHIP BASED TAXATION (U.S citizens and Green Card Holders=U.S.

U.S. TAX PRINCIPLES THAT AFFECT U.S. PERSONS LIVING ABROAD By Pamela Perez-Cuvit LL.M Madrid, May 26th 2016 UNIQUENESS OF U.S. TAX SYSTEM CITIZENSHIP BASED TAXATION (U.S citizens and Green Card Holders=U.S.

Estate Tax Conflicts Resulting from a Change in Residence

Originally published in: International Fiscal Association 56 th Congress August 25, 2002 Estate Tax Conflicts Resulting from a Change in Residence By: Sanford H. Goldberg The focus in my presentation is

Originally published in: International Fiscal Association 56 th Congress August 25, 2002 Estate Tax Conflicts Resulting from a Change in Residence By: Sanford H. Goldberg The focus in my presentation is

REQUEST FOR DETERMINATION OF POSSIBLE LOSS OF UNITED STATES CITIZENSHIP PART I

1. Name (Last, First, MI) U. S. Department of State BUREAU OF CONSULAR AFFAIRS REQUEST FOR DETERMINATION OF POSSIBLE LOSS OF UNITED STATES CITIZENSHIP PART I 3. Place of Birth OMB NO. 1405-0178 EXPIRES:

1. Name (Last, First, MI) U. S. Department of State BUREAU OF CONSULAR AFFAIRS REQUEST FOR DETERMINATION OF POSSIBLE LOSS OF UNITED STATES CITIZENSHIP PART I 3. Place of Birth OMB NO. 1405-0178 EXPIRES:

U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2016 (2015 Tax Year)

") 02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2016 (2015 Tax Year) The 2015 U.S.

02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2016 (2015 Tax Year) The 2015 U.S.

Self-Certification Controlling Person AEOI / FATCA

Self-Certification Controlling Person AEOI / FATCA Policy / Application Number(s) In the following text Quantum refers to Quantum Leben AG. Key terms are explained in the glossary. Neither this document

Self-Certification Controlling Person AEOI / FATCA Policy / Application Number(s) In the following text Quantum refers to Quantum Leben AG. Key terms are explained in the glossary. Neither this document

Financial Planning for US Expatriates living in Ireland. White Paper Series

Financial Planning for US Expatriates living in Ireland White Paper Series Given the close historical and economic relations between Ireland and the U.S. it is not uncommon to find U.S. citizens living

Financial Planning for US Expatriates living in Ireland White Paper Series Given the close historical and economic relations between Ireland and the U.S. it is not uncommon to find U.S. citizens living

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

2016 FOREIGN NATIONAL QUESTIONNAIRE

PLEASE COMPLETE EACH ITEM INCLUDED IN THE FOREIGN NATIONAL QUESTIONNAIRE FOR EACH MEMBER OF YOUR HOUSEHOLD. TAXPAYER SPOUSE NAME: NAME: 100) PERSONAL INFORMATION 101) Country (countries) of citizenship:

PLEASE COMPLETE EACH ITEM INCLUDED IN THE FOREIGN NATIONAL QUESTIONNAIRE FOR EACH MEMBER OF YOUR HOUSEHOLD. TAXPAYER SPOUSE NAME: NAME: 100) PERSONAL INFORMATION 101) Country (countries) of citizenship:

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

PRESENTATION FOR VAELA

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

I. Basic Rules. Planning for the Non- Citizen Spouse: Tips and Traps 2/25/2016. Zena M. Tamler. March 11, 2016 New York, New York

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

AMT: Always More Tax. Presented by Monica Haven, EA, JD, LLM

AMT: Always More Tax Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net Life isn t fair! Us Them Wages & Taxable Investment Income ($) 59,350 0 AMT Taxable Tax-Free Income ($) 0 59,350

AMT: Always More Tax Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net Life isn t fair! Us Them Wages & Taxable Investment Income ($) 59,350 0 AMT Taxable Tax-Free Income ($) 0 59,350

Presented by: Dale Mason, CPA The Wolf Group

1818 Society Easing International Tax Complexity Presented by: Dale Mason, CPA The Wolf Group The Wolf Group, PC Fairfax, VA Washington, DC New York, NY (703) 502-9500 Disclaimer Any U.S. tax issues addressed

1818 Society Easing International Tax Complexity Presented by: Dale Mason, CPA The Wolf Group The Wolf Group, PC Fairfax, VA Washington, DC New York, NY (703) 502-9500 Disclaimer Any U.S. tax issues addressed

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

Planning for Mobile Executives and Business Owners Relocating to the U.S.

American Bar Association Section of Taxation Committee on U.S. Activities of Foreigners and Tax Treaties Planning for Mobile Executives and Business Owners Relocating to the U.S. Boca Raton, FL January

American Bar Association Section of Taxation Committee on U.S. Activities of Foreigners and Tax Treaties Planning for Mobile Executives and Business Owners Relocating to the U.S. Boca Raton, FL January

Toronto Young Practitioners Group

US Tax 2.0 January 27, 2016 LL.B, BCL SKL Tax Overview: Identifying the problem FATCA exacerbates the problem Solution 1 Rely on the firewall Solution 2 Catch up and comply Solution 3 Renouncing US citizenship

US Tax 2.0 January 27, 2016 LL.B, BCL SKL Tax Overview: Identifying the problem FATCA exacerbates the problem Solution 1 Rely on the firewall Solution 2 Catch up and comply Solution 3 Renouncing US citizenship

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

SOUTH DAKOTA DEPARTMENT OF LABOR, JOB SERVICE, UNEMPLOYMENT DIVISION, AND OFFICE OF ADMINISTRATIVE SERVICES RETIREMENT PLAN A Summary Plan Description

SOUTH DAKOTA DEPARTMENT OF LABOR, JOB SERVICE, UNEMPLOYMENT DIVISION, AND OFFICE OF ADMINISTRATIVE SERVICES RETIREMENT PLAN A Summary Plan Description (11/2013) PLAN HIGHLIGHTS 4-15193 (CL2012) Plan Highlights

SOUTH DAKOTA DEPARTMENT OF LABOR, JOB SERVICE, UNEMPLOYMENT DIVISION, AND OFFICE OF ADMINISTRATIVE SERVICES RETIREMENT PLAN A Summary Plan Description (11/2013) PLAN HIGHLIGHTS 4-15193 (CL2012) Plan Highlights

DEPARTMENT OF STATE. Decided by the Board February 22, 1985

DEPARTMENT OF STATE BOARD OF APPELLATE REVIEW IN THE LYATTER OF: F. D. C.' In Loss of Nationality Proceedings Decided by the Board February 22, 1985 Appellant, a veteran of World War 11, was transferred

DEPARTMENT OF STATE BOARD OF APPELLATE REVIEW IN THE LYATTER OF: F. D. C.' In Loss of Nationality Proceedings Decided by the Board February 22, 1985 Appellant, a veteran of World War 11, was transferred

GENERAL EFFECTIVE DATE UNDER ARTICLE 30: 1 JANUARY 1986 INTRODUCTION

TREASURY DEPARTMENT TECHNICAL EXPLANATION OF THE CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE REPUBLIC OF CYPRUS FOR THE AVOIDANCE OF DOUBLE TAXATION AND

TREASURY DEPARTMENT TECHNICAL EXPLANATION OF THE CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE REPUBLIC OF CYPRUS FOR THE AVOIDANCE OF DOUBLE TAXATION AND

MANAGING INTERNATIONAL TAX ISSUES

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel