Calibration and Parameter Risk Analysis for Gas Storage Models

|

|

|

- Lesley Stone

- 6 years ago

- Views:

Transcription

1 Calibration and Parameter Risk Analysis for Gas Storage Models Greg Kiely (Gazprom) Mark Cummins (Dublin City University) Bernard Murphy (University of Limerick)

2 New Abstract

3

4 Model Risk Management: Regulatory Context Fed OCC (2000): Risk Bulletin on Model Validation Fed OCC (2011): Supervisory Guidance on Model Risk Management Basel Committee on Banking Supervision

5 Fed OCC: Risk Bulleting on Model Validation Independent Review Defined Responsibility Model Documentation Ongoing Validation Audit Oversight

6 Fed OCC: Supervisory Guidance on Model Risk Management Model development, implementation and use Governance and control mechanisms Policies and procedures Controls and compliance Appropriate incentives and organisational structure

7 Model Risk Definition Derman (1996) Model inapplicability Incorrect model use Incorrect solution to a correct model Incorrect use of a correct model Use of poorly specified model approximations Software and hardware errors Unstable or poor quality data input

8 Model Risk v Model Uncertainty Model Risk Exposure to future possible outcomes but with a unique defined probability measure Model Uncertainty Exposure to future possible outcomes for which there is no one unique defined probability measure Knight (1921)

9

Theory of convex risk measures Cont (2006) Theory of model risk")

10 Model Risk Measurement Artzner (1999) Theory of coherent risk measures Follmer and Schied (2000) Theory of convex risk measures Cont (2006) Theory of model risk measurement

11

12 Bannor and Scherer (2013) Propose calibration risk functional concept Incorporate calibration risk into bid-offer levels Theoretical framework consistent with convex risk measure concept Derive push-forward distributions for asset values based on calibration error from stochastic models

13 Bannor et al (2015) Examine parameter risk inherent in a real options modelbased approach to valuing power plant infrastructure Draw on innovative risk capturing approach of Bannor and Scherer (2013) Authors use sophisticated multi-factor setting to model emissions, gas and power prices Multidimensional search problem that poses considerable parameter risk Given unavailability of joint estimator s distribution in closed form, parameter risks are separately studied Bid-ask spreads from AVaR risk capturing price functional show spike risk is the most important parametric risk!

14 Motivation for Current Work Paucity of academic literature on model risk and model uncertainty Growing importance of industry practice of model risk management and model validation activity Regulatory impetus Bannor et al (2015) pave the way for further research into model risk issues in energy markets Perfect context given the range of OTC products and structures Extensive use of models for valuation and hedging activity

15 Motivation for Work Gas storage capacity presents a prime candidate for model risk analysis given: Ever increasing importance of gas storage capacity in Europe, and globally Difficulty in deriving competitive prices for this capacity Growing secondary market for capacity allowing market players to adjust seasonal flexibility to match portfolio growth Dependency on models for valuation and hedging No industry- or academic-consensus in circulation

16 Contributions Derive holistic approach to evaluating the uncertainty associated with parameter calibration and estimation Calibration to market derivative instruments Estimation to historical data Consider an innovative suite of mean-reverting Levy-driven models that offer market consistency Developed in first two papers of three-paper series Suggest method for ranking models based on their robustness to calibration errors Relevance to trading, risk and regulatory stakeholders

17 Henaff et al (2013) Examine historically estimated parameter risk associated with storage valuation Employ coherent model risk measure of Cont (2006) But deviate from this by replacing the set of benchmark instruments with a test which determines whether a set of model parameters returns likelihood value close to the ML value Use two proposed spot price models with price spikes We differ from Henaff et al (2013) in two ways: Unified approach to evaluating calibration and estimation risk Use of market consistent model framework that incorporates wider market information and is more in line with practical trading considerations

18 Bannor and Scherer (2013): Risk capturing functionals Risk functional Γ giving bid-ask spread Γ has certain desirable properties

19 Bannor and Scherer (2013): Risk capturing functionals Q is one of a family of potential models Q generally unknown distribution R In many cases the estimators of the model Q will possess asymptotic normality We can exploit this to note that

20 Bannor and Scherer (2013): Risk capturing functionals With this in place

21 Bannor and Scherer (2013): Risk capturing functionals Finally

22 Energy Model Risk Analysis Wish to consider parameter calibration risk and estimation risk jointly. But why? Realistic models of natural gas forward curve cannot be calibrated to benchmark instruments alone Due to lack of liquid time-spread options market Correlation structure is typically estimated from historical data and then approximated by a suitable model specification Storage valuation models are particularly sensitive to the model implied correlation structure Hence exposed to parameter estimation risk! Overall level of volatility implied by model constrained to be calibrated to the market To obtain consistency with the products used to hedge volatility risk Hence exposed to calibration risk!

23 Energy Model Risk Analysis We propose the following transformation function form Transformation function decomposed into Error term density conditional upon the historically estimated parameters Sampling error density associated with the historically estimated parameters From Bannor et al (2015), it is know that asymptotically Gaussian density suitable specification for sampling error density

24 Energy Model Risk Analysis Steps follow closely those of Bannor et al (2015) We apply the delta method described by the authors in conjunction with the sampling error density Construct a joint market and historical parameter risk induced value density

25 Energy Model Risk Analysis

26 Energy Model Risk Analysis

27 Energy Model Risk Analysis Last result gives the storage value variance induced by uncertainty over the estimate of the forward curve covariance matrix The relationship can be understood as First, weighting the matrix by the sensitivity of the model parameters to the sensitivity of the forward curve covariance matrix Second, weighting the result by the sensitivity of the storage value to the model parameters

28 Model Specifications Mean-Reverting Variance Gamma (MRVG) Kiely et al (2015a) Mean-Reverting Jump Diffusion (MRJD) Second model variant of first specified by Deng (2000) and used by Kjaer (2008) Choice of stochastic driver is different Jump-diffusion process with compound Poisson jump process driven by a double exponential distribution

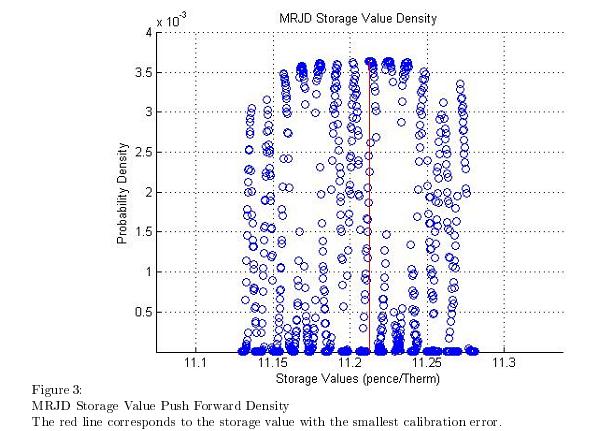

29 Model Specifications MRVG-3x Kiely et al (2015b) First factor accounts for majority of forward curve variability Composition of MRVG and MR Diffusion Parameter b... proportion of total variance attributed to first factor Second factor approximates the typical shape of the sensitivity of the forward curve to the second PC of forward curve returns covariance matrix

30 Storage Contract and Data Simple 20in / 20out storage deal Deal commences immediately on options quote date Lasts for 1 year All values in pence / therm Options data 6-month and 1-year monthly options on NBP Strike prices ranging from moneyness 14 option prices in total Quote date 19 th December 2012 Sourced from Bloomberg

31 Storage Contract and Data Data used to estimate historical covariance matrix 3 years ending 19 th December 2012 Contains relative maturity returns with a day-ahead quote and month-ahead quotes spanning 11-months First two models calibrated using FFT-based swaption pricing method Kiely et al (2015a) Third model calibrated using moment matching method with FFT-based option pricing Kiely et al (2015b)

32 Mark-Based Calibration Risk Consider 2808 parameter combinations Retain 807 based on 3% limit around minimum RMSE

33

34 Model-Based Calibration Risk Consider 2548 parameter combinations Retain 795 based on 3% limit around minimum RMSE

35

36 Model-Based Calibration Risk Conclusion MRVG and MRJD models carry comparable levels of calibration risk MRVG returns higher expected value than MRJD But MRVG also has higher variability than MRJD

37 Joint Calibration and Parameter Estimation Risk Consider 2548 parameter combinations Retain 838 based on 3% limit around minimum RMSE

38

39 Joint Calibration and Parameter Estimation Risk Comparing to MRVG and MRJD Value is much higher Coefficient of variation is almost double Confidence in calibrated value is lower Clustering of storage value at distinct levels Relate to different combinations of α and σ These combinations appear to fully determine storage value The impact of ν is minimal

40 Joint Calibration and Parameter Estimation Risk We now proceed to deriving the parameter risk density associated with the historically estimated parameters We can derive a sampling error covariance matrix for each of the volatility parameters Which is turn can be used to derive a parameter risk covariance matrix We must first estimate the Jacobian of our storage value with respect to our model parameters

41

42 Joint Calibration and Parameter Estimation Risk Variability has increased dramatically from inclusion of risk associated with the historically estimated parameters

43 Deriving Risk-Adjusted Price Levels

44 Deriving Risk-Adjusted Price Levels MRVG Bid-offer price levels Spread of 1.06% of mean value MRJD Bid-offer prices levels Spread of 1.02% of mean value MRVG-3x Bid-offer price levels Spread of 7.66% of mean value

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

Managing the Newest Derivatives Risks

Managing the Newest Derivatives Risks Michel Crouhy IXIS Corporate and Investment Bank / A subsidiary of NATIXIS Derivatives 2007: New Ideas, New Instruments, New markets NYU Stern School of Business,

Managing the Newest Derivatives Risks Michel Crouhy IXIS Corporate and Investment Bank / A subsidiary of NATIXIS Derivatives 2007: New Ideas, New Instruments, New markets NYU Stern School of Business,

FX Smile Modelling. 9 September September 9, 2008

FX Smile Modelling 9 September 008 September 9, 008 Contents 1 FX Implied Volatility 1 Interpolation.1 Parametrisation............................. Pure Interpolation.......................... Abstract

FX Smile Modelling 9 September 008 September 9, 008 Contents 1 FX Implied Volatility 1 Interpolation.1 Parametrisation............................. Pure Interpolation.......................... Abstract

Two and Three factor models for Spread Options Pricing

Two and Three factor models for Spread Options Pricing COMMIDITIES 2007, Birkbeck College, University of London January 17-19, 2007 Sebastian Jaimungal, Associate Director, Mathematical Finance Program,

Two and Three factor models for Spread Options Pricing COMMIDITIES 2007, Birkbeck College, University of London January 17-19, 2007 Sebastian Jaimungal, Associate Director, Mathematical Finance Program,

A Market Consistent Gas Storage Modelling Framework: Valuation, Calibration, & Model Risk

A Market Consistent Gas Storage Modelling Framework: Valuation, Calibration, & Model Risk by Greg Kiely B.Sc, National University of Ireland, Galway, 1st Hons. M.Sc University of Limerick, 1st Hons. Submitted

A Market Consistent Gas Storage Modelling Framework: Valuation, Calibration, & Model Risk by Greg Kiely B.Sc, National University of Ireland, Galway, 1st Hons. M.Sc University of Limerick, 1st Hons. Submitted

UPDATED IAA EDUCATION SYLLABUS

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

From Financial Engineering to Risk Management. Radu Tunaru University of Kent, UK

Model Risk in Financial Markets From Financial Engineering to Risk Management Radu Tunaru University of Kent, UK \Yp World Scientific NEW JERSEY LONDON SINGAPORE BEIJING SHANGHAI HONG KONG TAIPEI CHENNAI

Model Risk in Financial Markets From Financial Engineering to Risk Management Radu Tunaru University of Kent, UK \Yp World Scientific NEW JERSEY LONDON SINGAPORE BEIJING SHANGHAI HONG KONG TAIPEI CHENNAI

1. What is Implied Volatility?

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Stochastic Analysis Of Long Term Multiple-Decrement Contracts

Stochastic Analysis Of Long Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA and Chad Runchey, FSA, MAAA Ernst & Young LLP January 2008 Table of Contents Executive Summary...3 Introduction...6

Stochastic Analysis Of Long Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA and Chad Runchey, FSA, MAAA Ernst & Young LLP January 2008 Table of Contents Executive Summary...3 Introduction...6

Exploring Volatility Derivatives: New Advances in Modelling. Bruno Dupire Bloomberg L.P. NY

Exploring Volatility Derivatives: New Advances in Modelling Bruno Dupire Bloomberg L.P. NY bdupire@bloomberg.net Global Derivatives 2005, Paris May 25, 2005 1. Volatility Products Historical Volatility

Exploring Volatility Derivatives: New Advances in Modelling Bruno Dupire Bloomberg L.P. NY bdupire@bloomberg.net Global Derivatives 2005, Paris May 25, 2005 1. Volatility Products Historical Volatility

(FRED ESPEN BENTH, JAN KALLSEN, AND THILO MEYER-BRANDIS) UFITIMANA Jacqueline. Lappeenranta University Of Technology.

UFITIMANA Jacqueline. Lappeenranta University Of Technology.") (FRED ESPEN BENTH, JAN KALLSEN, AND THILO MEYER-BRANDIS) UFITIMANA Jacqueline Lappeenranta University Of Technology. 16,April 2009 OUTLINE Introduction Definitions Aim Electricity price Modelling Approaches

(FRED ESPEN BENTH, JAN KALLSEN, AND THILO MEYER-BRANDIS) UFITIMANA Jacqueline Lappeenranta University Of Technology. 16,April 2009 OUTLINE Introduction Definitions Aim Electricity price Modelling Approaches

(Text with EEA relevance)

") 20.5.2014 L 148/29 COMMISSION DELEGATED REGULATION (EU) No 528/2014 of 12 March 2014 supplementing Regulation (EU) No 575/2013 of the European Parliament and of the Council with regard to regulatory technical

20.5.2014 L 148/29 COMMISSION DELEGATED REGULATION (EU) No 528/2014 of 12 March 2014 supplementing Regulation (EU) No 575/2013 of the European Parliament and of the Council with regard to regulatory technical

Principal Component Analysis of the Volatility Smiles and Skews. Motivation

Principal Component Analysis of the Volatility Smiles and Skews Professor Carol Alexander Chair of Risk Management ISMA Centre University of Reading www.ismacentre.rdg.ac.uk 1 Motivation Implied volatilities

Principal Component Analysis of the Volatility Smiles and Skews Professor Carol Alexander Chair of Risk Management ISMA Centre University of Reading www.ismacentre.rdg.ac.uk 1 Motivation Implied volatilities

Dynamic Replication of Non-Maturing Assets and Liabilities

Dynamic Replication of Non-Maturing Assets and Liabilities Michael Schürle Institute for Operations Research and Computational Finance, University of St. Gallen, Bodanstr. 6, CH-9000 St. Gallen, Switzerland

Dynamic Replication of Non-Maturing Assets and Liabilities Michael Schürle Institute for Operations Research and Computational Finance, University of St. Gallen, Bodanstr. 6, CH-9000 St. Gallen, Switzerland

On modelling of electricity spot price

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

Financial Risk Management

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #3 1 Maximum likelihood of the exponential distribution 1. We assume

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #3 1 Maximum likelihood of the exponential distribution 1. We assume

Probability Weighted Moments. Andrew Smith

Probability Weighted Moments Andrew Smith andrewdsmith8@deloitte.co.uk 28 November 2014 Introduction If I asked you to summarise a data set, or fit a distribution You d probably calculate the mean and

Probability Weighted Moments Andrew Smith andrewdsmith8@deloitte.co.uk 28 November 2014 Introduction If I asked you to summarise a data set, or fit a distribution You d probably calculate the mean and

Market Risk Analysis Volume IV. Value-at-Risk Models

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

Financial Models with Levy Processes and Volatility Clustering

Financial Models with Levy Processes and Volatility Clustering SVETLOZAR T. RACHEV # YOUNG SHIN ICIM MICHELE LEONARDO BIANCHI* FRANK J. FABOZZI WILEY John Wiley & Sons, Inc. Contents Preface About the

Financial Models with Levy Processes and Volatility Clustering SVETLOZAR T. RACHEV # YOUNG SHIN ICIM MICHELE LEONARDO BIANCHI* FRANK J. FABOZZI WILEY John Wiley & Sons, Inc. Contents Preface About the

Equity correlations implied by index options: estimation and model uncertainty analysis

1/18 : estimation and model analysis, EDHEC Business School (joint work with Rama COT) Modeling and managing financial risks Paris, 10 13 January 2011 2/18 Outline 1 2 of multi-asset models Solution to

1/18 : estimation and model analysis, EDHEC Business School (joint work with Rama COT) Modeling and managing financial risks Paris, 10 13 January 2011 2/18 Outline 1 2 of multi-asset models Solution to

Interest rate models and Solvency II

www.nr.no Outline Desired properties of interest rate models in a Solvency II setting. A review of three well-known interest rate models A real example from a Norwegian insurance company 2 Interest rate

www.nr.no Outline Desired properties of interest rate models in a Solvency II setting. A review of three well-known interest rate models A real example from a Norwegian insurance company 2 Interest rate

Lecture 9: Practicalities in Using Black-Scholes. Sunday, September 23, 12

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Hedging the Smirk. David S. Bates. University of Iowa and the National Bureau of Economic Research. October 31, 2005

Hedging the Smirk David S. Bates University of Iowa and the National Bureau of Economic Research October 31, 2005 Associate Professor of Finance Department of Finance Henry B. Tippie College of Business

Hedging the Smirk David S. Bates University of Iowa and the National Bureau of Economic Research October 31, 2005 Associate Professor of Finance Department of Finance Henry B. Tippie College of Business

Model Risk for Energy Markets

Seite 1 Model Risk for Energy Markets Rüdiger Kiesel, Karl Bannör, Anna Nazarova, Matthias Scherer R. Kiesel Centre of Mathematics for Applications, Oslo University Chair for Energy Trading, University

Seite 1 Model Risk for Energy Markets Rüdiger Kiesel, Karl Bannör, Anna Nazarova, Matthias Scherer R. Kiesel Centre of Mathematics for Applications, Oslo University Chair for Energy Trading, University

Market Risk Analysis Volume II. Practical Financial Econometrics

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Challenges in developing internal models for Solvency II

NFT 2/2008 Challenges in developing internal models for Solvency II by Vesa Ronkainen, Lasse Koskinen and Laura Koskela Vesa Ronkainen vesa.ronkainen@vakuutusvalvonta.fi In the EU the supervision of the

NFT 2/2008 Challenges in developing internal models for Solvency II by Vesa Ronkainen, Lasse Koskinen and Laura Koskela Vesa Ronkainen vesa.ronkainen@vakuutusvalvonta.fi In the EU the supervision of the

Gas storage: overview and static valuation

In this first article of the new gas storage segment of the Masterclass series, John Breslin, Les Clewlow, Tobias Elbert, Calvin Kwok and Chris Strickland provide an illustration of how the four most common

In this first article of the new gas storage segment of the Masterclass series, John Breslin, Les Clewlow, Tobias Elbert, Calvin Kwok and Chris Strickland provide an illustration of how the four most common

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios Axioma, Inc. by Kartik Sivaramakrishnan, PhD, and Robert Stamicar, PhD August 2016 In this

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios Axioma, Inc. by Kartik Sivaramakrishnan, PhD, and Robert Stamicar, PhD August 2016 In this

Bloomberg. Portfolio Value-at-Risk. Sridhar Gollamudi & Bryan Weber. September 22, Version 1.0

Portfolio Value-at-Risk Sridhar Gollamudi & Bryan Weber September 22, 2011 Version 1.0 Table of Contents 1 Portfolio Value-at-Risk 2 2 Fundamental Factor Models 3 3 Valuation methodology 5 3.1 Linear factor

Portfolio Value-at-Risk Sridhar Gollamudi & Bryan Weber September 22, 2011 Version 1.0 Table of Contents 1 Portfolio Value-at-Risk 2 2 Fundamental Factor Models 3 3 Valuation methodology 5 3.1 Linear factor

A Quantitative Metric to Validate Risk Models

2013 A Quantitative Metric to Validate Risk Models William Rearden 1 M.A., M.Sc. Chih-Kai, Chang 2 Ph.D., CERA, FSA Abstract The paper applies a back-testing validation methodology of economic scenario

2013 A Quantitative Metric to Validate Risk Models William Rearden 1 M.A., M.Sc. Chih-Kai, Chang 2 Ph.D., CERA, FSA Abstract The paper applies a back-testing validation methodology of economic scenario

Survival of Hedge Funds : Frailty vs Contagion

Survival of Hedge Funds : Frailty vs Contagion February, 2015 1. Economic motivation Financial entities exposed to liquidity risk(s)... on the asset component of the balance sheet (market liquidity) on

Survival of Hedge Funds : Frailty vs Contagion February, 2015 1. Economic motivation Financial entities exposed to liquidity risk(s)... on the asset component of the balance sheet (market liquidity) on

European option pricing under parameter uncertainty

European option pricing under parameter uncertainty Martin Jönsson (joint work with Samuel Cohen) University of Oxford Workshop on BSDEs, SPDEs and their Applications July 4, 2017 Introduction 2/29 Introduction

European option pricing under parameter uncertainty Martin Jönsson (joint work with Samuel Cohen) University of Oxford Workshop on BSDEs, SPDEs and their Applications July 4, 2017 Introduction 2/29 Introduction

Vega Maps: Predicting Premium Change from Movements of the Whole Volatility Surface

Vega Maps: Predicting Premium Change from Movements of the Whole Volatility Surface Ignacio Hoyos Senior Quantitative Analyst Equity Model Validation Group Risk Methodology Santander Alberto Elices Head

Vega Maps: Predicting Premium Change from Movements of the Whole Volatility Surface Ignacio Hoyos Senior Quantitative Analyst Equity Model Validation Group Risk Methodology Santander Alberto Elices Head

Subject CS1 Actuarial Statistics 1 Core Principles. Syllabus. for the 2019 exams. 1 June 2018

` Subject CS1 Actuarial Statistics 1 Core Principles Syllabus for the 2019 exams 1 June 2018 Copyright in this Core Reading is the property of the Institute and Faculty of Actuaries who are the sole distributors.

` Subject CS1 Actuarial Statistics 1 Core Principles Syllabus for the 2019 exams 1 June 2018 Copyright in this Core Reading is the property of the Institute and Faculty of Actuaries who are the sole distributors.

Practical application of Liquidity Premium to the valuation of insurance liabilities and determination of capital requirements

28 April 2011 Practical application of Liquidity Premium to the valuation of insurance liabilities and determination of capital requirements 1. Introduction CRO Forum Position on Liquidity Premium The

28 April 2011 Practical application of Liquidity Premium to the valuation of insurance liabilities and determination of capital requirements 1. Introduction CRO Forum Position on Liquidity Premium The

SOLUTIONS 913,

Illinois State University, Mathematics 483, Fall 2014 Test No. 3, Tuesday, December 2, 2014 SOLUTIONS 1. Spring 2013 Casualty Actuarial Society Course 9 Examination, Problem No. 7 Given the following information

Illinois State University, Mathematics 483, Fall 2014 Test No. 3, Tuesday, December 2, 2014 SOLUTIONS 1. Spring 2013 Casualty Actuarial Society Course 9 Examination, Problem No. 7 Given the following information

INV2601 SELF ASSESSMENT QUESTIONS

INV2601 SELF ASSESSMENT QUESTIONS 1. The annual holding period return of an investment that was held for four years is 5.74%. The ending value of this investment was R1 000. Calculate the beginning value

INV2601 SELF ASSESSMENT QUESTIONS 1. The annual holding period return of an investment that was held for four years is 5.74%. The ending value of this investment was R1 000. Calculate the beginning value

A market risk model for asymmetric distributed series of return

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

Sensex Realized Volatility Index (REALVOL)

") Sensex Realized Volatility Index (REALVOL) Introduction Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility.

Sensex Realized Volatility Index (REALVOL) Introduction Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility.

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib. Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015 d-fine d-fine All rights All rights reserved reserved 0 Swaption

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015 d-fine d-fine All rights All rights reserved reserved 0 Swaption

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

Lecture 8: Markov and Regime

Lecture 8: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2016 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Lecture 8: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2016 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

FRAMEWORK FOR SUPERVISORY INFORMATION

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

IMPLEMENTING THE SPECTRAL CALIBRATION OF EXPONENTIAL LÉVY MODELS

IMPLEMENTING THE SPECTRAL CALIBRATION OF EXPONENTIAL LÉVY MODELS DENIS BELOMESTNY AND MARKUS REISS 1. Introduction The aim of this report is to describe more precisely how the spectral calibration method

IMPLEMENTING THE SPECTRAL CALIBRATION OF EXPONENTIAL LÉVY MODELS DENIS BELOMESTNY AND MARKUS REISS 1. Introduction The aim of this report is to describe more precisely how the spectral calibration method

HANDBOOK OF. Market Risk CHRISTIAN SZYLAR WILEY

HANDBOOK OF Market Risk CHRISTIAN SZYLAR WILEY Contents FOREWORD ACKNOWLEDGMENTS ABOUT THE AUTHOR INTRODUCTION XV XVII XIX XXI 1 INTRODUCTION TO FINANCIAL MARKETS t 1.1 The Money Market 4 1.2 The Capital

HANDBOOK OF Market Risk CHRISTIAN SZYLAR WILEY Contents FOREWORD ACKNOWLEDGMENTS ABOUT THE AUTHOR INTRODUCTION XV XVII XIX XXI 1 INTRODUCTION TO FINANCIAL MARKETS t 1.1 The Money Market 4 1.2 The Capital

P&L Attribution and Risk Management

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 7. Risk Management Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 8, 2012 2 Interest Rates & FX Models Contents 1 Introduction

INTEREST RATES AND FX MODELS 7. Risk Management Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 8, 2012 2 Interest Rates & FX Models Contents 1 Introduction

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

Contents Part I Descriptive Statistics 1 Introduction and Framework Population, Sample, and Observations Variables Quali

Part I Descriptive Statistics 1 Introduction and Framework... 3 1.1 Population, Sample, and Observations... 3 1.2 Variables.... 4 1.2.1 Qualitative and Quantitative Variables.... 5 1.2.2 Discrete and Continuous

Part I Descriptive Statistics 1 Introduction and Framework... 3 1.1 Population, Sample, and Observations... 3 1.2 Variables.... 4 1.2.1 Qualitative and Quantitative Variables.... 5 1.2.2 Discrete and Continuous

Model Risk Assessment

Model Risk Assessment Case Study Based on Hedging Simulations Drona Kandhai (PhD) Head of Interest Rates, Inflation and Credit Quantitative Analytics Team CMRM Trading Risk - ING Bank Assistant Professor

Model Risk Assessment Case Study Based on Hedging Simulations Drona Kandhai (PhD) Head of Interest Rates, Inflation and Credit Quantitative Analytics Team CMRM Trading Risk - ING Bank Assistant Professor

Near-expiration behavior of implied volatility for exponential Lévy models

Near-expiration behavior of implied volatility for exponential Lévy models José E. Figueroa-López 1 1 Department of Statistics Purdue University Financial Mathematics Seminar The Stevanovich Center for

Near-expiration behavior of implied volatility for exponential Lévy models José E. Figueroa-López 1 1 Department of Statistics Purdue University Financial Mathematics Seminar The Stevanovich Center for

COMMISSION DELEGATED REGULATION (EU) No /.. of

No /.. of") EUROPEAN COMMISSION Brussels, 12.3.2014 C(2014) 1556 final COMMISSION DELEGATED REGULATION (EU) No /.. of 12.3.2014 supplementing Regulation (EU) No 575/2013 of the European Parliament and of the Council

EUROPEAN COMMISSION Brussels, 12.3.2014 C(2014) 1556 final COMMISSION DELEGATED REGULATION (EU) No /.. of 12.3.2014 supplementing Regulation (EU) No 575/2013 of the European Parliament and of the Council

High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]

![High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]](/thumbs/79/79153367.jpg "High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]") 1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

Financial Engineering. Craig Pirrong Spring, 2006

Financial Engineering Craig Pirrong Spring, 2006 March 8, 2006 1 Levy Processes Geometric Brownian Motion is very tractible, and captures some salient features of speculative price dynamics, but it is

Financial Engineering Craig Pirrong Spring, 2006 March 8, 2006 1 Levy Processes Geometric Brownian Motion is very tractible, and captures some salient features of speculative price dynamics, but it is

Economic Scenario Generators

Economic Scenario Generators A regulator s perspective Falk Tschirschnitz, FINMA Bahnhofskolloquium Motivation FINMA has observed: Calibrating the interest rate model of choice has become increasingly

Economic Scenario Generators A regulator s perspective Falk Tschirschnitz, FINMA Bahnhofskolloquium Motivation FINMA has observed: Calibrating the interest rate model of choice has become increasingly

Can Rare Events Explain the Equity Premium Puzzle?

Can Rare Events Explain the Equity Premium Puzzle? Christian Julliard and Anisha Ghosh Working Paper 2008 P t d b J L i f NYU A t P i i Presented by Jason Levine for NYU Asset Pricing Seminar, Fall 2009

Can Rare Events Explain the Equity Premium Puzzle? Christian Julliard and Anisha Ghosh Working Paper 2008 P t d b J L i f NYU A t P i i Presented by Jason Levine for NYU Asset Pricing Seminar, Fall 2009

Market Risk Analysis Volume I

Market Risk Analysis Volume I Quantitative Methods in Finance Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume I xiii xvi xvii xix xxiii

Market Risk Analysis Volume I Quantitative Methods in Finance Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume I xiii xvi xvii xix xxiii

2.1 Random variable, density function, enumerative density function and distribution function

Risk Theory I Prof. Dr. Christian Hipp Chair for Science of Insurance, University of Karlsruhe (TH Karlsruhe) Contents 1 Introduction 1.1 Overview on the insurance industry 1.1.1 Insurance in Benin 1.1.2

Risk Theory I Prof. Dr. Christian Hipp Chair for Science of Insurance, University of Karlsruhe (TH Karlsruhe) Contents 1 Introduction 1.1 Overview on the insurance industry 1.1.1 Insurance in Benin 1.1.2

Factors in Implied Volatility Skew in Corn Futures Options

1 Factors in Implied Volatility Skew in Corn Futures Options Weiyu Guo* University of Nebraska Omaha 6001 Dodge Street, Omaha, NE 68182 Phone 402-554-2655 Email: wguo@unomaha.edu and Tie Su University

1 Factors in Implied Volatility Skew in Corn Futures Options Weiyu Guo* University of Nebraska Omaha 6001 Dodge Street, Omaha, NE 68182 Phone 402-554-2655 Email: wguo@unomaha.edu and Tie Su University

Extended Libor Models and Their Calibration

Extended Libor Models and Their Calibration Denis Belomestny Weierstraß Institute Berlin Vienna, 16 November 2007 Denis Belomestny (WIAS) Extended Libor Models and Their Calibration Vienna, 16 November

Extended Libor Models and Their Calibration Denis Belomestny Weierstraß Institute Berlin Vienna, 16 November 2007 Denis Belomestny (WIAS) Extended Libor Models and Their Calibration Vienna, 16 November

Fitting financial time series returns distributions: a mixture normality approach

Fitting financial time series returns distributions: a mixture normality approach Riccardo Bramante and Diego Zappa * Abstract Value at Risk has emerged as a useful tool to risk management. A relevant

Fitting financial time series returns distributions: a mixture normality approach Riccardo Bramante and Diego Zappa * Abstract Value at Risk has emerged as a useful tool to risk management. A relevant

Random Variables and Probability Distributions

Chapter 3 Random Variables and Probability Distributions Chapter Three Random Variables and Probability Distributions 3. Introduction An event is defined as the possible outcome of an experiment. In engineering

Chapter 3 Random Variables and Probability Distributions Chapter Three Random Variables and Probability Distributions 3. Introduction An event is defined as the possible outcome of an experiment. In engineering

Investment is one of the most important and volatile components of macroeconomic activity. In the short-run, the relationship between uncertainty and

Investment is one of the most important and volatile components of macroeconomic activity. In the short-run, the relationship between uncertainty and investment is central to understanding the business

Investment is one of the most important and volatile components of macroeconomic activity. In the short-run, the relationship between uncertainty and investment is central to understanding the business

Option Pricing Modeling Overview

Option Pricing Modeling Overview Liuren Wu Zicklin School of Business, Baruch College Options Markets Liuren Wu (Baruch) Stochastic time changes Options Markets 1 / 11 What is the purpose of building a

Option Pricing Modeling Overview Liuren Wu Zicklin School of Business, Baruch College Options Markets Liuren Wu (Baruch) Stochastic time changes Options Markets 1 / 11 What is the purpose of building a

Estimation of dynamic term structure models

Estimation of dynamic term structure models Greg Duffee Haas School of Business, UC-Berkeley Joint with Richard Stanton, Haas School Presentation at IMA Workshop, May 2004 (full paper at http://faculty.haas.berkeley.edu/duffee)

Estimation of dynamic term structure models Greg Duffee Haas School of Business, UC-Berkeley Joint with Richard Stanton, Haas School Presentation at IMA Workshop, May 2004 (full paper at http://faculty.haas.berkeley.edu/duffee)

EXAMINATION II: Fixed Income Valuation and Analysis. Derivatives Valuation and Analysis. Portfolio Management

EXAMINATION II: Fixed Income Valuation and Analysis Derivatives Valuation and Analysis Portfolio Management Questions Final Examination March 2011 Question 1: Fixed Income Valuation and Analysis (43 points)

EXAMINATION II: Fixed Income Valuation and Analysis Derivatives Valuation and Analysis Portfolio Management Questions Final Examination March 2011 Question 1: Fixed Income Valuation and Analysis (43 points)

Pricing of a European Call Option Under a Local Volatility Interbank Offered Rate Model

American Journal of Theoretical and Applied Statistics 2018; 7(2): 80-84 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20180702.14 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2018; 7(2): 80-84 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20180702.14 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Leverage Effect, Volatility Feedback, and Self-Exciting MarketAFA, Disruptions 1/7/ / 14

Leverage Effect, Volatility Feedback, and Self-Exciting Market Disruptions Liuren Wu, Baruch College Joint work with Peter Carr, New York University The American Finance Association meetings January 7,

Leverage Effect, Volatility Feedback, and Self-Exciting Market Disruptions Liuren Wu, Baruch College Joint work with Peter Carr, New York University The American Finance Association meetings January 7,

MFE8825 Quantitative Management of Bond Portfolios

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

Lecture notes on risk management, public policy, and the financial system. Credit portfolios. Allan M. Malz. Columbia University

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: June 8, 2018 2 / 23 Outline Overview of credit portfolio risk

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: June 8, 2018 2 / 23 Outline Overview of credit portfolio risk

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 3. The Volatility Cube Andrew Lesniewski Courant Institute of Mathematics New York University New York February 17, 2011 2 Interest Rates & FX Models Contents 1 Dynamics of

INTEREST RATES AND FX MODELS 3. The Volatility Cube Andrew Lesniewski Courant Institute of Mathematics New York University New York February 17, 2011 2 Interest Rates & FX Models Contents 1 Dynamics of

Developing a reserve range, from theory to practice. CAS Spring Meeting 22 May 2013 Vancouver, British Columbia

Developing a reserve range, from theory to practice CAS Spring Meeting 22 May 2013 Vancouver, British Columbia Disclaimer The views expressed by presenter(s) are not necessarily those of Ernst & Young

Developing a reserve range, from theory to practice CAS Spring Meeting 22 May 2013 Vancouver, British Columbia Disclaimer The views expressed by presenter(s) are not necessarily those of Ernst & Young

Robust Portfolio Optimization SOCP Formulations

1 Robust Portfolio Optimization SOCP Formulations There has been a wealth of literature published in the last 1 years explaining and elaborating on what has become known as Robust portfolio optimization.

1 Robust Portfolio Optimization SOCP Formulations There has been a wealth of literature published in the last 1 years explaining and elaborating on what has become known as Robust portfolio optimization.

IMPA Commodities Course: Introduction

IMPA Commodities Course: Introduction Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Department of Statistics and Mathematical Finance Program, University of Toronto, Toronto, Canada http://www.utstat.utoronto.ca/sjaimung

IMPA Commodities Course: Introduction Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Department of Statistics and Mathematical Finance Program, University of Toronto, Toronto, Canada http://www.utstat.utoronto.ca/sjaimung

Risk and Return of Short Duration Equity Investments

Risk and Return of Short Duration Equity Investments Georg Cejnek and Otto Randl, WU Vienna, Frontiers of Finance 2014 Conference Warwick, April 25, 2014 Outline Motivation Research Questions Preview of

Risk and Return of Short Duration Equity Investments Georg Cejnek and Otto Randl, WU Vienna, Frontiers of Finance 2014 Conference Warwick, April 25, 2014 Outline Motivation Research Questions Preview of

Stochastic modeling of electricity prices

Stochastic modeling of electricity prices a survey Fred Espen Benth Centre of Mathematics for Applications (CMA) University of Oslo, Norway In collaboration with Ole E. Barndorff-Nielsen and Almut Veraart

Stochastic modeling of electricity prices a survey Fred Espen Benth Centre of Mathematics for Applications (CMA) University of Oslo, Norway In collaboration with Ole E. Barndorff-Nielsen and Almut Veraart

Optimal Investment for Generalized Utility Functions

Optimal Investment for Generalized Utility Functions Thijs Kamma Maastricht University July 05, 2018 Overview Introduction Terminal Wealth Problem Utility Specifications Economic Scenarios Results Black-Scholes

Optimal Investment for Generalized Utility Functions Thijs Kamma Maastricht University July 05, 2018 Overview Introduction Terminal Wealth Problem Utility Specifications Economic Scenarios Results Black-Scholes

Bayesian Finance. Christa Cuchiero, Irene Klein, Josef Teichmann. Obergurgl 2017

Bayesian Finance Christa Cuchiero, Irene Klein, Josef Teichmann Obergurgl 2017 C. Cuchiero, I. Klein, and J. Teichmann Bayesian Finance Obergurgl 2017 1 / 23 1 Calibrating a Bayesian model: a first trial

Bayesian Finance Christa Cuchiero, Irene Klein, Josef Teichmann Obergurgl 2017 C. Cuchiero, I. Klein, and J. Teichmann Bayesian Finance Obergurgl 2017 1 / 23 1 Calibrating a Bayesian model: a first trial

Option P&L Attribution and Pricing

Option P&L Attribution and Pricing Liuren Wu joint with Peter Carr Baruch College March 23, 2018 Stony Brook University Carr and Wu (NYU & Baruch) P&L Attribution and Option Pricing March 23, 2018 1 /

Option P&L Attribution and Pricing Liuren Wu joint with Peter Carr Baruch College March 23, 2018 Stony Brook University Carr and Wu (NYU & Baruch) P&L Attribution and Option Pricing March 23, 2018 1 /

Validation of Nasdaq Clearing Models

Model Validation Validation of Nasdaq Clearing Models Summary of findings swissquant Group Kuttelgasse 7 CH-8001 Zürich Classification: Public Distribution: swissquant Group, Nasdaq Clearing October 20,

Model Validation Validation of Nasdaq Clearing Models Summary of findings swissquant Group Kuttelgasse 7 CH-8001 Zürich Classification: Public Distribution: swissquant Group, Nasdaq Clearing October 20,

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS001) p approach

p approach") Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS001) p.5901 What drives short rate dynamics? approach A functional gradient descent Audrino, Francesco University

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS001) p.5901 What drives short rate dynamics? approach A functional gradient descent Audrino, Francesco University

Hedging Default Risks of CDOs in Markovian Contagion Models

Hedging Default Risks of CDOs in Markovian Contagion Models Second Princeton Credit Risk Conference 24 May 28 Jean-Paul LAURENT ISFA Actuarial School, University of Lyon, http://laurent.jeanpaul.free.fr

Hedging Default Risks of CDOs in Markovian Contagion Models Second Princeton Credit Risk Conference 24 May 28 Jean-Paul LAURENT ISFA Actuarial School, University of Lyon, http://laurent.jeanpaul.free.fr

palgrave Shipping Derivatives and Risk Management macmiuan Amir H. Alizadeh & Nikos K. Nomikos

Shipping Derivatives and Risk Management Amir H. Alizadeh & Nikos K. Nomikos Faculty of Finance, Cass Business School, City University, London palgrave macmiuan Contents About the Authors. xv Preface and

Shipping Derivatives and Risk Management Amir H. Alizadeh & Nikos K. Nomikos Faculty of Finance, Cass Business School, City University, London palgrave macmiuan Contents About the Authors. xv Preface and

2017 IAA EDUCATION SYLLABUS

2017 IAA EDUCATION SYLLABUS 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging areas of actuarial practice. 1.1 RANDOM

2017 IAA EDUCATION SYLLABUS 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging areas of actuarial practice. 1.1 RANDOM

Portfolio Management

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Commodity and Energy Markets

Lecture 3 - Spread Options p. 1/19 Commodity and Energy Markets (Princeton RTG summer school in financial mathematics) Lecture 3 - Spread Option Pricing Michael Coulon and Glen Swindle June 17th - 28th,

Lecture 3 - Spread Options p. 1/19 Commodity and Energy Markets (Princeton RTG summer school in financial mathematics) Lecture 3 - Spread Option Pricing Michael Coulon and Glen Swindle June 17th - 28th,

Northern Trust Corporation

Northern Trust Corporation Market Risk Disclosures June 30, 2015 Market Risk Disclosures Effective January 1, 2013, Northern Trust Corporation (Northern Trust) adopted revised risk based capital guidelines

Northern Trust Corporation Market Risk Disclosures June 30, 2015 Market Risk Disclosures Effective January 1, 2013, Northern Trust Corporation (Northern Trust) adopted revised risk based capital guidelines

On the Relative Pricing of Long Maturity S&P 500 Index Options and CDX Tranches

On the Relative Pricing of Long Maturity S&P 500 Index Options and CDX Tranches by Pierre Collin-Dufresne Discussion by Markus Leippold Swissquote Conference Ecole Polytechnique Fédérale de Lausanne October,

On the Relative Pricing of Long Maturity S&P 500 Index Options and CDX Tranches by Pierre Collin-Dufresne Discussion by Markus Leippold Swissquote Conference Ecole Polytechnique Fédérale de Lausanne October,

STOCHASTIC MODELLING OF ELECTRICITY AND RELATED MARKETS

Advanced Series on Statistical Science & Applied Probability Vol. I I STOCHASTIC MODELLING OF ELECTRICITY AND RELATED MARKETS Fred Espen Benth JGrate Saltyte Benth University of Oslo, Norway Steen Koekebakker

Advanced Series on Statistical Science & Applied Probability Vol. I I STOCHASTIC MODELLING OF ELECTRICITY AND RELATED MARKETS Fred Espen Benth JGrate Saltyte Benth University of Oslo, Norway Steen Koekebakker

Lecture 9: Markov and Regime

Lecture 9: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2017 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Lecture 9: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2017 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Pricing with a Smile. Bruno Dupire. Bloomberg

CP-Bruno Dupire.qxd 10/08/04 6:38 PM Page 1 11 Pricing with a Smile Bruno Dupire Bloomberg The Black Scholes model (see Black and Scholes, 1973) gives options prices as a function of volatility. If an

CP-Bruno Dupire.qxd 10/08/04 6:38 PM Page 1 11 Pricing with a Smile Bruno Dupire Bloomberg The Black Scholes model (see Black and Scholes, 1973) gives options prices as a function of volatility. If an

Risk managing long-dated smile risk with SABR formula

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Risk Measurement: An Introduction to Value at Risk

Risk Measurement: An Introduction to Value at Risk Thomas J. Linsmeier and Neil D. Pearson * University of Illinois at Urbana-Champaign July 1996 Abstract This paper is a self-contained introduction to

Risk Measurement: An Introduction to Value at Risk Thomas J. Linsmeier and Neil D. Pearson * University of Illinois at Urbana-Champaign July 1996 Abstract This paper is a self-contained introduction to

Practical example of an Economic Scenario Generator

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Master of Science in Finance (MSF) Curriculum

Curriculum") Master of Science in Finance (MSF) Curriculum Courses By Semester Foundations Course Work During August (assigned as needed; these are in addition to required credits) FIN 510 Introduction to Finance (2)

Master of Science in Finance (MSF) Curriculum Courses By Semester Foundations Course Work During August (assigned as needed; these are in addition to required credits) FIN 510 Introduction to Finance (2)

Pension Funds Active Management Based on Risk Budgeting

Funds and Pensions Pension Funds Active Management Based on Risk Budgeting Chae Woo Nam, Research Fellow* When we look at changes in asset managers risk management systems including pension funds, we observe

Funds and Pensions Pension Funds Active Management Based on Risk Budgeting Chae Woo Nam, Research Fellow* When we look at changes in asset managers risk management systems including pension funds, we observe

Data Revisions and Macroecomics DR. ANA BEATRIZ GALVAO WARWICK BUSINESS SCHOOL UNIVERSITY OF WARWICK SEP, 2016

Data Revisions and Macroecomics DR. ANA BEATRIZ GALVAO WARWICK BUSINESS SCHOOL UNIVERSITY OF WARWICK SEP, 2016 National Account Data Macroeconomic aggregates: consumption, investment, GDP, trade balance.

Data Revisions and Macroecomics DR. ANA BEATRIZ GALVAO WARWICK BUSINESS SCHOOL UNIVERSITY OF WARWICK SEP, 2016 National Account Data Macroeconomic aggregates: consumption, investment, GDP, trade balance.

Structural credit risk models and systemic capital

Structural credit risk models and systemic capital Somnath Chatterjee CCBS, Bank of England November 7, 2013 Structural credit risk model Structural credit risk models are based on the notion that both

Structural credit risk models and systemic capital Somnath Chatterjee CCBS, Bank of England November 7, 2013 Structural credit risk model Structural credit risk models are based on the notion that both

Risk Measurement in Credit Portfolio Models

9 th DGVFM Scientific Day 30 April 2010 1 Risk Measurement in Credit Portfolio Models 9 th DGVFM Scientific Day 30 April 2010 9 th DGVFM Scientific Day 30 April 2010 2 Quantitative Risk Management Profit

9 th DGVFM Scientific Day 30 April 2010 1 Risk Measurement in Credit Portfolio Models 9 th DGVFM Scientific Day 30 April 2010 9 th DGVFM Scientific Day 30 April 2010 2 Quantitative Risk Management Profit

Valuation of Volatility Derivatives. Jim Gatheral Global Derivatives & Risk Management 2005 Paris May 24, 2005

Valuation of Volatility Derivatives Jim Gatheral Global Derivatives & Risk Management 005 Paris May 4, 005 he opinions expressed in this presentation are those of the author alone, and do not necessarily

Valuation of Volatility Derivatives Jim Gatheral Global Derivatives & Risk Management 005 Paris May 4, 005 he opinions expressed in this presentation are those of the author alone, and do not necessarily