Professional Standards and Ethics for Accountants

|

|

|

- Barnard Barber

- 6 years ago

- Views:

Transcription

1 Professional Standards and Ethics for Accountants CPA Australia IPP Program August 2009 Channa Wijesinghe ACMA (UK), CPA, CA Technical Director APESB

2 Overview History and structure of the APESB APESB and its pronouncements Issued Standards APES 110 Code of Ethics Section 290 Independence Future developments to the Code Why accounting ethics matter?

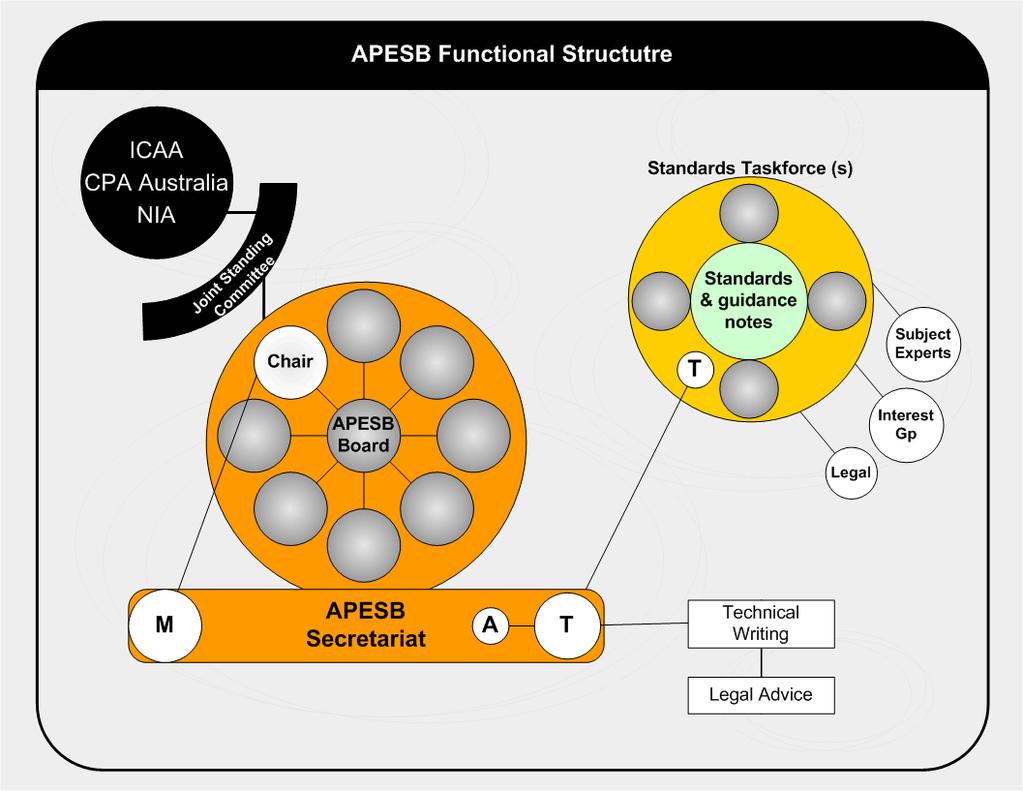

3 APESB History Established in Feb 2006 as an initiative of ICAA & CPA Australia NIA became a Member in Dec 2006 Previously professional/ethical pronouncements were developed by the professional bodies Members of the three bodies are required to comply and subject to disciplinary procedures of the relevant professional body

4 APESB Vision To be recognised by our stakeholders for our leading contribution in achieving the highest level of professional and ethical behaviour in the accounting profession

5 Board Composition Independent Chair Two Directors CPA Australia Two Directors ICAA One Director NIA

6

7

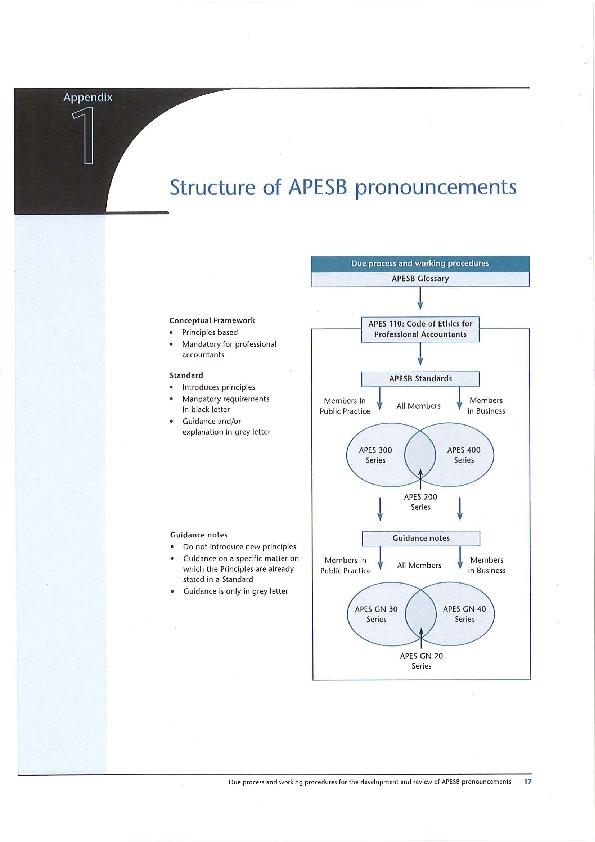

8 APESB Pronouncements to date All members APES 110 Code of Ethics APES 205 Conformity with Accounting Standards APES 210 Conformity with Auditing Standards APES 215 Forensic Accounting Services APES 220 Taxation Services APES 225 Valuation Services

9 APESB Pronouncements to date Members in Public Practice APES 305 Terms of Engagement APES 315 Compilation of Financial Information APES 320 Quality Control for Firms APES 330 ED Insolvency Services APES 345 Reporting on Prospective Financial Information

10 APES 110 Code of Ethics Part A: General Application Fundamental Principles Part B: Members in Public Practice Section 290 Independence Assurance Engagements Part C: Members in Business

11 APES 110 Code of Ethics Fundamental Principles - Integrity - Objectivity - Professional competence and due care - Confidentiality - Professional behaviour

12 APES 110 Code of Ethics Part B - Members in Public Practice Section 210 Professional Appointment Section 220 Conflicts of Interest Section 230 Second opinions Section 240 Fees and Other Types of Remuneration Section 250 Marketing Professional Services Section 260 Gifts and Hospitality Section 270 Custody of Client Assets Section 280 Objectivity All Services Section 290 Independence Assurance Engagements

13 APES 110 Code of Ethics Part C - Members in Business Section 300 Introduction Section 310 Potential conflicts Section 320 Preparation and Reporting of Information Section 330 Acting with Sufficient Expertise Section 340 Financial Interests Section 350 Inducements

14 Section 290 Independence Independence requires: Independence of Mind Independence of Appearance (S and definitions)

15 Section 290 Independence Threats to Independence - Self interest threat - Self review threat - Advocacy threat - Familiarity threat - Intimidation threat (S to )

16 Section 290 Independence Safeguards - created by the profession, legislation or regulation - within the Assurance client - within the firms own systems and procedures (S to )

17 Section 290 Independence Auditor s responsibility - Identify threats to independence - Evaluate whether these threats are clearly insignificant - If not identify and apply appropriate safeguards When safeguards are not available - Eliminate activity or interest creating the threat - Refuse to accept or continue the Assurance Engagement

18 Future developments that impact the Code International - Revised Code issued in July Impact of clarity project (Should/Shall) Australian - Taskforce working on revised Code

19 Accountability of Members Regulators such as ASIC and APRA Professional bodies Clients Shareholders

20 Why accounting ethics matter? Collapse of Arthur Anderson Arthur Anderson s problem clients (refer table 1) Increased regulations such as CLERP 9 in Australia and Sarbanes & Oxley in the US Recent corporate collapses brought on by the global credit crunch (refer table 2)

21 Table 1: Arthur Anderson s Audit Clients and their problems AA Client Problem Losses to shareholders WorldCom US $ 4.3 billion overstatement of earnings Job losses $ billion 17,000 Enron Waste Management Inflation of income, assets, bankrupt 2001 Overstatement of income by US $ 1.1 billion, ( ) $ 66.4 billion 6,100 $ 20.5 billion 11,000 Sunbeam Overstatement of 1997 income by US $ 71 million then bankruptcy $ 4.4 billion 1,700 Source: Fall from grace, Business Week, 2002

22 Table 2: Recent Corporate collapses due to the Global Credit Crunch Company Problems Business/Social impact Lehman Brothers Bear Stearns ABC Learning - Derivatives : MBS and ABS - Downgrading of credit ratings - Toxic commercial real estate assets - High leverage ratios - Derivatives : MBS and ABS - High leverage ratios - Unrealistic fair value accounting of assets - Revenue recognition - Gearing - Weak corporate governance - Majority of the 26,000 worldwide staff may be made redundant? - Approximately 9,000 employees lost their jobs - Shareholder lawsuits? unprofitable day care sites for sale - Unemployment - Child care services at risk? Opes Prime - Cash and share movement irregularities - Failed margin calls - Losses of AUD 600 million? Source:

23 The Seven Signs of Ethical Collapse Pressure to maintain those numbers Fear and silence Young uns and a bigger than life CEO Weak Board Conflicts Innovation like no other Goodness in some areas atoning for evil in others Jennings, M M 2006, The seven signs of ethical collapse: how to spot moral meltdown in companies before it s too late

24 For more information visit

Ethics and Professional Standards for the Professional Accountant: The Changing Landscape

Ethics and Professional Standards for the Professional Accountant: The Changing Landscape IPA Public Practice Symposium Sydney, 2 June 2011 Channa Wijesinghe MBA, CPA, CA Technical Director Overview History

Ethics and Professional Standards for the Professional Accountant: The Changing Landscape IPA Public Practice Symposium Sydney, 2 June 2011 Channa Wijesinghe MBA, CPA, CA Technical Director Overview History

The evolution of Accounting Professional Standards in Australia

The evolution of Accounting Professional Standards in Australia RMIT University Melbourne, 29 September 2016 Channa Wijesinghe FCMA (UK), FCPA, FCA Chief Executive Officer Overview History and structure

The evolution of Accounting Professional Standards in Australia RMIT University Melbourne, 29 September 2016 Channa Wijesinghe FCMA (UK), FCPA, FCA Chief Executive Officer Overview History and structure

Forensic Expertise and Corporate Collapses

Forensic Expertise and Corporate Collapses CPA Australia Melbourne, 26 November 2015 Channa Wijesinghe FCMA (UK), FCPA, FCA Technical Director Overview Turn of the century corporate collapses The development

Forensic Expertise and Corporate Collapses CPA Australia Melbourne, 26 November 2015 Channa Wijesinghe FCMA (UK), FCPA, FCA Technical Director Overview Turn of the century corporate collapses The development

APESB Professional and Ethical Standards

APESB Professional and Ethical Standards IPA Hebei Certified Tax Agents Association (HBCTAA) Melbourne, 9 December 2013 Channa Wijesinghe MBA, FCPA, FCA Technical Director Overview History and structure

APESB Professional and Ethical Standards IPA Hebei Certified Tax Agents Association (HBCTAA) Melbourne, 9 December 2013 Channa Wijesinghe MBA, FCPA, FCA Technical Director Overview History and structure

APESB and Auditor Independence

APESB and Auditor Independence Financial Reporting Council Audit Quality Committee 14 May 2014 Channa Wijesinghe MBA, FCPA, FCA Technical Director Overview Role of the Accounting Professional & Ethical

APESB and Auditor Independence Financial Reporting Council Audit Quality Committee 14 May 2014 Channa Wijesinghe MBA, FCPA, FCA Technical Director Overview Role of the Accounting Professional & Ethical

Australian Developments and APESB Agenda IESBA Meeting New York March 2013

Australian Developments and APESB Agenda IESBA Meeting New York March 2013 Kate Spargo LL.B. (Hons), B.A., FAICD Chairman Overview Australian Framework and Regulatory Regime APES 110 Code of Ethics for

Australian Developments and APESB Agenda IESBA Meeting New York March 2013 Kate Spargo LL.B. (Hons), B.A., FAICD Chairman Overview Australian Framework and Regulatory Regime APES 110 Code of Ethics for

APES 100 Code of Ethics

Professional Practice Program Module 2 Professional Practice Program APES 100 Code of Ethics DISCLAIMER AND COPYRIGHT NOTICE Institute of Public Accountants February 2018 all rights reserved. This written

Professional Practice Program Module 2 Professional Practice Program APES 100 Code of Ethics DISCLAIMER AND COPYRIGHT NOTICE Institute of Public Accountants February 2018 all rights reserved. This written

APES 345 Reporting on Prospective Financial Information prepared in connection with a Public Document

APES 210 Conformity with Auditing and Assurance Standards APES 345 Reporting on Prospective Financial Information prepared in connection with a Public Document [Supersedes APES 345 Reporting on Prospective

APES 210 Conformity with Auditing and Assurance Standards APES 345 Reporting on Prospective Financial Information prepared in connection with a Public Document [Supersedes APES 345 Reporting on Prospective

Accounting Professional & Ethical Standards Board Limited ACN

Accounting Professional & Ethical Standards Board Limited ACN 118 227 259 Annual report for the 17 months ended 30 June 2007 Vision: Our vision is: To be recognised by our stakeholders for our leading

Accounting Professional & Ethical Standards Board Limited ACN 118 227 259 Annual report for the 17 months ended 30 June 2007 Vision: Our vision is: To be recognised by our stakeholders for our leading

Proposed Standard: APES 310 Members Trust Accounts (Formerly APS 10)

") EXPOSURE DRAFT ED XX/08 (December 2008) Proposed Standard: APES 310 Members Trust Accounts (Formerly APS 10) Prepared and issued by Accounting Professional & Ethical Standards Board Limited Commenting

EXPOSURE DRAFT ED XX/08 (December 2008) Proposed Standard: APES 310 Members Trust Accounts (Formerly APS 10) Prepared and issued by Accounting Professional & Ethical Standards Board Limited Commenting

FINANCIAL ADVICE AND REGULATIONS

FINANCIAL ADVICE AND REGULATIONS GUIDANCE FOR THE ACCOUNTING PROFESSION FINANCIAL ADVICE AND REGULATIONS 2 DEVELOPED EXCLUSIVELY FOR THE MEMBERS IN PUBLIC PRACTICE OF CPA AUSTRALIA AND CHARTERED ACCOUNTANTS

FINANCIAL ADVICE AND REGULATIONS GUIDANCE FOR THE ACCOUNTING PROFESSION FINANCIAL ADVICE AND REGULATIONS 2 DEVELOPED EXCLUSIVELY FOR THE MEMBERS IN PUBLIC PRACTICE OF CPA AUSTRALIA AND CHARTERED ACCOUNTANTS

02-Dec What is an audit? Audit objective. An Overview of Auditing

An Overview of Auditing What is an audit? A systematic process of objectively obtaining and evaluating evidence regarding assertions made about economic actions and events to ascertain the degree of correspondence

An Overview of Auditing What is an audit? A systematic process of objectively obtaining and evaluating evidence regarding assertions made about economic actions and events to ascertain the degree of correspondence

November 2018 Basis for Conclusions: APES 110 Code of Ethics for Professional Accountants (including Independence Standards)

") November 2018 Basis for Conclusions: APES 110 Code of Ethics for Professional Accountants (including Independence Standards) Prepared by the Technical Staff of the Accounting Professional & Ethical Standards

November 2018 Basis for Conclusions: APES 110 Code of Ethics for Professional Accountants (including Independence Standards) Prepared by the Technical Staff of the Accounting Professional & Ethical Standards

May 2018 Basis for Conclusions: APES 310 Client Monies

May 2018 Basis for Conclusions: APES 310 Client Monies Prepared by the Technical Staff of the Accounting Professional & Ethical Standards Board BASIS FOR CONCLUSIONS: Revised APES 310 Client Monies (2018)

May 2018 Basis for Conclusions: APES 310 Client Monies Prepared by the Technical Staff of the Accounting Professional & Ethical Standards Board BASIS FOR CONCLUSIONS: Revised APES 310 Client Monies (2018)

July 2012 Explanatory Memorandum: Exposure Draft 03/12 APES 230 Financial Planning Services

July 2012 Explanatory Memorandum: Exposure Draft 03/12 APES 230 Financial Planning Services Copyright 2012 Accounting Professional & Ethical Standards Board Limited ( APESB ). All rights reserved. Apart

July 2012 Explanatory Memorandum: Exposure Draft 03/12 APES 230 Financial Planning Services Copyright 2012 Accounting Professional & Ethical Standards Board Limited ( APESB ). All rights reserved. Apart

Audit Partner rotation requirements in Australia Technical Staff Q&As. Issued: XXXXX 2017

Audit Partner rotation requirements in Australia Technical Staff Q&As Issued: XXXXX 2017 Purpose Australian professional and ethical requirements relating to audit partner rotation will change for periods

Audit Partner rotation requirements in Australia Technical Staff Q&As Issued: XXXXX 2017 Purpose Australian professional and ethical requirements relating to audit partner rotation will change for periods

Audit Partner rotation requirements in Australia Technical Staff Questions & Answers. December 2017

Audit Partner rotation requirements in Australia Technical Staff Questions & Answers December 2017 Purpose Australian professional and ethical requirements relating to audit partner rotation will change

Audit Partner rotation requirements in Australia Technical Staff Questions & Answers December 2017 Purpose Australian professional and ethical requirements relating to audit partner rotation will change

CPA Code of Ethics. June The Institute of Certified Public Accountants in Ireland

CPA Code of Ethics June 2016 The Institute of Certified Public Accountants in Ireland CONTENTS Definitions 2 PART A: GENERAL APPLICATION OF THE CODE ALL MEMBERS 100 Introduction and Fundamental Principles...

CPA Code of Ethics June 2016 The Institute of Certified Public Accountants in Ireland CONTENTS Definitions 2 PART A: GENERAL APPLICATION OF THE CODE ALL MEMBERS 100 Introduction and Fundamental Principles...

Accountancy Profession Act 1979 Cap 281

2015 Code of Ethics for Warrant Holders Accountancy Profession Act 1979 Cap 281 Directive Number 2 issued in terms of the Accountancy Profession Act (Cap 281) and of the Accountancy Profession Regulations

2015 Code of Ethics for Warrant Holders Accountancy Profession Act 1979 Cap 281 Directive Number 2 issued in terms of the Accountancy Profession Act (Cap 281) and of the Accountancy Profession Regulations

Joint Accounting Bodies CPA Australia Ltd, The Institute of Chartered Accountants in Australia & The Institute of Public Accountants

Joint Accounting Bodies CPA Australia Ltd, The Institute of Chartered Accountants in Australia & The Institute of Public Accountants Independence guide Fourth edition, February 2013 The Joint Accounting

Joint Accounting Bodies CPA Australia Ltd, The Institute of Chartered Accountants in Australia & The Institute of Public Accountants Independence guide Fourth edition, February 2013 The Joint Accounting

Financial Advice and Regulations: Guidance for the accounting profession

Financial Advice and Regulations: Guidance for the accounting profession Version 2.2 1 September 2017 Developed exclusively for the members in public practice of Chartered Accountants Australia and New

Financial Advice and Regulations: Guidance for the accounting profession Version 2.2 1 September 2017 Developed exclusively for the members in public practice of Chartered Accountants Australia and New

June 2015 Exposure Draft 02/15 Revision of APESB pronouncements

June 2015 Exposure Draft 02/15 Revision of APESB pronouncements Copyright 2015 Accounting Professional & Ethical Standards Board Limited ( APESB ). All rights reserved. Apart from fair dealing for the

June 2015 Exposure Draft 02/15 Revision of APESB pronouncements Copyright 2015 Accounting Professional & Ethical Standards Board Limited ( APESB ). All rights reserved. Apart from fair dealing for the

EXTERNAL AUDITOR INDEPENDENCE BRD 315

EXTERNAL AUDITOR INDEPENDENCE BRD 315 PURPOSE Policy BRD 310, Terms of Reference for the Audit & Finance Committee (the Committee ), assigns to the Committee the responsibility of reviewing the planning

EXTERNAL AUDITOR INDEPENDENCE BRD 315 PURPOSE Policy BRD 310, Terms of Reference for the Audit & Finance Committee (the Committee ), assigns to the Committee the responsibility of reviewing the planning

Independence Australia

Independence Australia Fact sheet internal use only Issued: July 2011 Independence requirements for new hires Introduction This fact sheet provides a brief summary of the main personal independence requirements

Independence Australia Fact sheet internal use only Issued: July 2011 Independence requirements for new hires Introduction This fact sheet provides a brief summary of the main personal independence requirements

INSOLVENCY CODE OF ETHICS

LIST OF CONTENTS INSOLVENCY CODE OF ETHICS Paragraphs Page No. Definitions 2 PART 1 GENERAL APPLICATION OF THE CODE 1-3 Introduction 3 4 Fundamental Principles 3 5-6 Framework Approach 3 7-16 Identification

LIST OF CONTENTS INSOLVENCY CODE OF ETHICS Paragraphs Page No. Definitions 2 PART 1 GENERAL APPLICATION OF THE CODE 1-3 Introduction 3 4 Fundamental Principles 3 5-6 Framework Approach 3 7-16 Identification

Board Audit Committee Charter

Board Audit Charter 5 May 2014 PURPOSE 1) The purpose of the Westpac Banking Corporation (Westpac) Board Audit () is to assist the Board to discharge its responsibilities by having oversight of the: a)

Board Audit Charter 5 May 2014 PURPOSE 1) The purpose of the Westpac Banking Corporation (Westpac) Board Audit () is to assist the Board to discharge its responsibilities by having oversight of the: a)

BAFS Elective Part Accounting Module Financial Accounting

BAFS Elective Part Accounting Module Financial Accounting Technology Education Section Curriculum Development Institute Education Bureau, HKSARG April 2009 Lesson One Learning Objectives Understand the

BAFS Elective Part Accounting Module Financial Accounting Technology Education Section Curriculum Development Institute Education Bureau, HKSARG April 2009 Lesson One Learning Objectives Understand the

Code of Professional Conduct

Code of Professional Conduct (Issued November 2010) Application of the Code This Code applies to every Member and Associate of the Institute or of any successor in title to the Institute. The Code of Professional

Code of Professional Conduct (Issued November 2010) Application of the Code This Code applies to every Member and Associate of the Institute or of any successor in title to the Institute. The Code of Professional

QUALITY REVIEW PROGRAM REVIEW OF INSOLVENCY ENGAGEMENTS QUESTIONNAIRE

QUALITY REVIEW PROGRAM REVIEW OF INSOLVENCY ENGAGEMENTS QUESTIONNAIRE 2 Quality Review Program Review Of Insolvency Engagements Questionnaire Review Code(s) Reviewer Review Date INTRODUCTION This questionnaire

QUALITY REVIEW PROGRAM REVIEW OF INSOLVENCY ENGAGEMENTS QUESTIONNAIRE 2 Quality Review Program Review Of Insolvency Engagements Questionnaire Review Code(s) Reviewer Review Date INTRODUCTION This questionnaire

Regulatory Compliance

Professional Practice Program Module 6 Professional Practice Program Regulatory Compliance DISCLAIMER AND COPYRIGHT NOTICE Institute of Public Accountants February 2018 all rights reserved. This written

Professional Practice Program Module 6 Professional Practice Program Regulatory Compliance DISCLAIMER AND COPYRIGHT NOTICE Institute of Public Accountants February 2018 all rights reserved. This written

Example Accounts Only

CaseWare Partnership (Special Purpose) Financial Statements Disclaimer: These financials include illustrative disclosures for a Partnership that is a non-reporting entity and is not intended to be and

CaseWare Partnership (Special Purpose) Financial Statements Disclaimer: These financials include illustrative disclosures for a Partnership that is a non-reporting entity and is not intended to be and

Code of Professional Ethics

Code of Professional Ethics AAT is a registered charity. No. 1050724 Contents Foreword... 3 Introduction... 4 Glossary of Terms... 6 Part A. General Application of the Code... 11 Section 100. Introduction

Code of Professional Ethics AAT is a registered charity. No. 1050724 Contents Foreword... 3 Introduction... 4 Glossary of Terms... 6 Part A. General Application of the Code... 11 Section 100. Introduction

Ethics Pronouncement EP 100

Ethics Pronouncement EP 100 Code of Professional Conduct and Ethics This Pronouncement was issued by the Council of the Institute of Singapore Chartered Accountants (ISCA) on 25 November 2015. This Pronouncement

Ethics Pronouncement EP 100 Code of Professional Conduct and Ethics This Pronouncement was issued by the Council of the Institute of Singapore Chartered Accountants (ISCA) on 25 November 2015. This Pronouncement

APES 220 Taxation Services

APES 220 Taxation Services [Supersedes APES 220 Taxation Services Issued in October 2007] Revised March 2011 Copyright 2011 Accounting Professional & Ethical Standards Board Limited ( APESB ). All rights

APES 220 Taxation Services [Supersedes APES 220 Taxation Services Issued in October 2007] Revised March 2011 Copyright 2011 Accounting Professional & Ethical Standards Board Limited ( APESB ). All rights

Chapter 01. The Role of the Public Accountant in the American Economy. McGraw-Hill/Irwin

Chapter 01 The Role of the Public Accountant in the American Economy McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Assurance services The broad range of information

Chapter 01 The Role of the Public Accountant in the American Economy McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Assurance services The broad range of information

IFAC Ethics Committee Agenda Item 2-C May 2004 Vienna, Austria Section 8 Mark-up Preferred Option

Section 8 Mark-up Preferred Option Please note that while a mark-up of this document is provided for convenience, at the May meeting the discussion will focus on this document. Therefore, Committee members

Section 8 Mark-up Preferred Option Please note that while a mark-up of this document is provided for convenience, at the May meeting the discussion will focus on this document. Therefore, Committee members

Revised Ethical Standard 2016

Standard Audit and Assurance Financial Reporting Council June 2016 Revised Ethical Standard 2016 The FRC s mission is to promote transparency and integrity in business. The FRC sets the UK Corporate Governance

Standard Audit and Assurance Financial Reporting Council June 2016 Revised Ethical Standard 2016 The FRC s mission is to promote transparency and integrity in business. The FRC sets the UK Corporate Governance

Code of Professional Ethics: independence provisions relating to review and assurance engagements

Code of Professional Ethics: independence provisions relating to review and assurance engagements AAT is a registered charity. No. 1050724 Contents Foreword... 4 Introduction... 5 Glossary of Terms...

Code of Professional Ethics: independence provisions relating to review and assurance engagements AAT is a registered charity. No. 1050724 Contents Foreword... 4 Introduction... 5 Glossary of Terms...

GUIDE TO CANADIAN INDEPENDENCE STANDARD

GUIDE TO CANADIAN INDEPENDENCE STANDARD This ( Guide ) has been prepared to assist members, firms, students, candidates, and applicants 1 in understanding and applying the independence standard. This version

GUIDE TO CANADIAN INDEPENDENCE STANDARD This ( Guide ) has been prepared to assist members, firms, students, candidates, and applicants 1 in understanding and applying the independence standard. This version

IFAC Ethics Committee Meeting Agenda Item 3-B September 2004 Helsinki, Finland

Definitions [Please note only definitions relating to independence are presented below] Financial aaudit client statementan entity in respect of which a firm conducts an financial statement audit engagement.

Definitions [Please note only definitions relating to independence are presented below] Financial aaudit client statementan entity in respect of which a firm conducts an financial statement audit engagement.

INTRODUCTION TO ACCOUNTING THEORY AND PRINCIPLES

SECTION 1 INTRODUCTION TO ACCOUNTING CHAPTER 1 THEORY AND PRINCIPLES Note in many cases with theory based questions, alternative answers or additional information may be appropriate. Solution 1.1 Directors,

SECTION 1 INTRODUCTION TO ACCOUNTING CHAPTER 1 THEORY AND PRINCIPLES Note in many cases with theory based questions, alternative answers or additional information may be appropriate. Solution 1.1 Directors,

Public Consultation. EP Code of Professional Conduct and Ethics

Public Consultation EP 100 - Code of Professional Conduct and Ethics October 2015 REQUEST FOR COMMENTS This proposed Pronouncement of ISCA was approved for publication in October 2015. This proposed Pronouncement

Public Consultation EP 100 - Code of Professional Conduct and Ethics October 2015 REQUEST FOR COMMENTS This proposed Pronouncement of ISCA was approved for publication in October 2015. This proposed Pronouncement

Code of Professional Ethics

Code of Professional Ethics The AAT Code of Professional Ethics is based on the Code of Ethics for Professional Accountants of the International Ethics Standards Board for Accountants, published by the

Code of Professional Ethics The AAT Code of Professional Ethics is based on the Code of Ethics for Professional Accountants of the International Ethics Standards Board for Accountants, published by the

KPMG comments on the Auditing Profession Bill, September 2005 This report contains 13 pages KPMG comments on the Auditing Profession Bill

KPMG comments on the Auditing Profession Bill, 2005 This report contains 13 pages KPMG comments on the Auditing Profession Bill 2005 KPMG International. KPMG International is a Swiss cooperative of which

KPMG comments on the Auditing Profession Bill, 2005 This report contains 13 pages KPMG comments on the Auditing Profession Bill 2005 KPMG International. KPMG International is a Swiss cooperative of which

Finally, the expected impacts on tax compliance behaviour of a large corporation adopting a tax risk management system are identified and discussed.

Article Summary Managing tax risk and compliance Focus and scope The identification of tax risk management, as part of good corporate governance practices, requires directors to consider the tax risk profile

Article Summary Managing tax risk and compliance Focus and scope The identification of tax risk management, as part of good corporate governance practices, requires directors to consider the tax risk profile

FEES QUESTIONNAIRE. IESBA Seeks Your View about the Level of Fees Charged by Audit Firms

FEES QUESTIONNAIRE IESBA Seeks Your View about the Level of Fees Charged by Audit Firms The level of fees charged by audit firms is considered by some stakeholders as an element that may affect auditor

FEES QUESTIONNAIRE IESBA Seeks Your View about the Level of Fees Charged by Audit Firms The level of fees charged by audit firms is considered by some stakeholders as an element that may affect auditor

The Role of the Public Accountant in the American Economy

CHAPTER 1 The Role of the Public Accountant in the American Economy Review Questions 1 1 The crisis of credibility largely arose from the number of companies that restated their previously issued financial

CHAPTER 1 The Role of the Public Accountant in the American Economy Review Questions 1 1 The crisis of credibility largely arose from the number of companies that restated their previously issued financial

AUDIT COMMITTEES AND AUDITOR INDEPENDENCE

AUDIT COMMITTEES AND AUDITOR INDEPENDENCE Presentation to: Oakland Unified School District Audit Committee December 12, 2007 Ann-Marie Hogan, CIA, CGAP City Auditor, Berkeley, CA ahogan@ci.berkeley.ca.us

AUDIT COMMITTEES AND AUDITOR INDEPENDENCE Presentation to: Oakland Unified School District Audit Committee December 12, 2007 Ann-Marie Hogan, CIA, CGAP City Auditor, Berkeley, CA ahogan@ci.berkeley.ca.us

F8 Audit & Assurance[INT] Sample Note

![F8 Audit & Assurance[INT] Sample Note](/thumbs/80/81950405.jpg "F8 Audit & Assurance[INT] Sample Note") F8 Audit & Assurance[INT] Sample Note For Exams in June2015 1 Content CORPORATE GOVERNANCE:... 9 AUDIT COMMITTEE:... 9 Corporate governance... 9 ISA 260... 12 PILOT PAPER Q3 CG and audit committee:...

F8 Audit & Assurance[INT] Sample Note For Exams in June2015 1 Content CORPORATE GOVERNANCE:... 9 AUDIT COMMITTEE:... 9 Corporate governance... 9 ISA 260... 12 PILOT PAPER Q3 CG and audit committee:...

The Audit Committee Roles and Responsibilities

AUDITOR GENERAL S REPORT ACTION REQUIRED The Audit Committee Roles and Responsibilities Date: January 12, 2011 To: From: Wards: Audit Committee Auditor General All Reference Number: SUMMARY The Audit Committee

AUDITOR GENERAL S REPORT ACTION REQUIRED The Audit Committee Roles and Responsibilities Date: January 12, 2011 To: From: Wards: Audit Committee Auditor General All Reference Number: SUMMARY The Audit Committee

ANZ Board Charter. 1.2 ANZ places great importance on the values of honesty, integrity, quality and trust.

ANZ Board Charter Contents 1. Introduction 2. Purpose and Role 3. Powers 4. Specific Responsibilities 5. Board Membership 6. Independence 7. Meetings 8. Board Committees 9. Board Renewal, Performance Evaluation

ANZ Board Charter Contents 1. Introduction 2. Purpose and Role 3. Powers 4. Specific Responsibilities 5. Board Membership 6. Independence 7. Meetings 8. Board Committees 9. Board Renewal, Performance Evaluation

Amendments to Long Association of Personnel with an Audit or Assurance Client requirements in APES 110 Code of Ethics for Professional Accountants

Amendments to Long Association of Personnel with an Audit or Assurance Client requirements in APES 110 Code of Ethics for Professional Accountants April 2018 Copyright 2018 Accounting Professional & Ethical

Amendments to Long Association of Personnel with an Audit or Assurance Client requirements in APES 110 Code of Ethics for Professional Accountants April 2018 Copyright 2018 Accounting Professional & Ethical

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

CBA Board Audit Committee Charter

Commonwealth Bank of Australia ACN 123 123 124 CBA Board Audit Committee Charter 1. Purpose and Duties of the Audit Committee 1.1. It is the policy of the Group to have an Audit Committee of the Board

Commonwealth Bank of Australia ACN 123 123 124 CBA Board Audit Committee Charter 1. Purpose and Duties of the Audit Committee 1.1. It is the policy of the Group to have an Audit Committee of the Board

The Audit Committee Roles and Responsibilities

STAFF REPORT INFORMATION ONLY The Audit Committee Roles and Responsibilities Date: January 12, 2007 To: From: Wards: Audit Committee Jeff Griffiths, Auditor General, Auditor General s Office All Reference

STAFF REPORT INFORMATION ONLY The Audit Committee Roles and Responsibilities Date: January 12, 2007 To: From: Wards: Audit Committee Jeff Griffiths, Auditor General, Auditor General s Office All Reference

Issued: December 2017

Close-Off Document: Amendments to Long Association of Personnel with an Audit or Assurance Client requirements in APES 110 Code of Ethics for Professional Accountants Issued: December 2017 Copyright 2017

Close-Off Document: Amendments to Long Association of Personnel with an Audit or Assurance Client requirements in APES 110 Code of Ethics for Professional Accountants Issued: December 2017 Copyright 2017

Survey of Standard Setters Work Plans and Existing Standards

Survey of Standard Setters Work Plans and Existing Standards This paper outlines matters are on the work plans of selected IFAC member bodies or other ethical standard setters. It also outlines matters

Survey of Standard Setters Work Plans and Existing Standards This paper outlines matters are on the work plans of selected IFAC member bodies or other ethical standard setters. It also outlines matters

Summary of July 2018 Content Updates

Summary of July 2018 Content Updates July 2018 Hello Future CPAs, With a new exam interface and significant test-taking improvements rolled out in April 2018, you can look forward to your next exam experience

Summary of July 2018 Content Updates July 2018 Hello Future CPAs, With a new exam interface and significant test-taking improvements rolled out in April 2018, you can look forward to your next exam experience

CIMA CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

CIMA CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS JANUARY 2015 02 CIMA code of ethics for professional accountants CIMA PREFACEl As chartered management accountants CIMA members (and registered students)

CIMA CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS JANUARY 2015 02 CIMA code of ethics for professional accountants CIMA PREFACEl As chartered management accountants CIMA members (and registered students)

PART B PROFESSIONAL ACCOUNTANTS IN PUBLIC PRACTICE

PART B PROFESSIONAL ACCOUNTANTS IN PUBLIC PRACTICE 200 Introduction 210 Professional Appointment Appendix to 210 220 Conflicts of Interest 221 Corporate Finance Advice 230 Second Opinions 240 Fees and

PART B PROFESSIONAL ACCOUNTANTS IN PUBLIC PRACTICE 200 Introduction 210 Professional Appointment Appendix to 210 220 Conflicts of Interest 221 Corporate Finance Advice 230 Second Opinions 240 Fees and

International Federation of Accountants 529 Fifth Avenue, 6th Floor New York, New York USA

International Federation of Accountants 529 Fifth Avenue, 6th Floor New York, New York 10017 USA This publication was published by the International Federation of Accountants (IFAC). Its mission is to

International Federation of Accountants 529 Fifth Avenue, 6th Floor New York, New York 10017 USA This publication was published by the International Federation of Accountants (IFAC). Its mission is to

T3 Auditing: The working client's story

T3 Auditing: The working client's story Sharlene Anderson CA Director Veritas Corp AUDITING STANDARDS COMPLIANCE When auditing SMSFs it is essential that the auditor comply with the applicable auditing

T3 Auditing: The working client's story Sharlene Anderson CA Director Veritas Corp AUDITING STANDARDS COMPLIANCE When auditing SMSFs it is essential that the auditor comply with the applicable auditing

Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Exposure Draft January 2017 Comments due: April 25, 2017 International Ethics Standards Board for Accountants Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Exposure Draft January 2017 Comments due: April 25, 2017 International Ethics Standards Board for Accountants Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Proposed Revisions to the Code Pertaining to the Offering and Accepting of Inducements

Exposure Draft September 2017 Comments due: December 8, 2017 International Ethics Standards Board for Accountants Proposed Revisions to the Code Pertaining to the Offering and Accepting of Inducements

Exposure Draft September 2017 Comments due: December 8, 2017 International Ethics Standards Board for Accountants Proposed Revisions to the Code Pertaining to the Offering and Accepting of Inducements

The Institute of Chartered Accountants of Sri Lanka. Code of Ethics

The Institute of Chartered Accountants of Sri Lanka Code of Ethics 2016 i The Institute of Chartered Accountants of Sri Lanka Code of Ethic 2016 is based on the Handbook of the Code of Ethic for Professional

The Institute of Chartered Accountants of Sri Lanka Code of Ethics 2016 i The Institute of Chartered Accountants of Sri Lanka Code of Ethic 2016 is based on the Handbook of the Code of Ethic for Professional

Code of Ethics for Warrant Holders

2009 Code of Ethics for Warrant Holders Accountancy Profession Act 1979 Cap 281 Directive Number 2 issued in terms of the Accountancy Profession Act (Cap 281) and of the Accountancy Profession Regulations

2009 Code of Ethics for Warrant Holders Accountancy Profession Act 1979 Cap 281 Directive Number 2 issued in terms of the Accountancy Profession Act (Cap 281) and of the Accountancy Profession Regulations

2 4 Generally accepted auditing standards are the Statements on Auditing Standards issued by the Auditing Standards Board.

CHAPTER 2 Professional Standards Review Questions 2 1 The Sarbanes-Oxley Act of 2002 created the PCAOB and gave this body authority to develop auditing standards for the audits of public companies. The

CHAPTER 2 Professional Standards Review Questions 2 1 The Sarbanes-Oxley Act of 2002 created the PCAOB and gave this body authority to develop auditing standards for the audits of public companies. The

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Module B Professional Ethics Auditors must approach their jobs with independence and skepticism. How do we instill

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Module B Professional Ethics Auditors must approach their jobs with independence and skepticism. How do we instill

FRA NEWS. No.7/2012. In this FRA News, your attention is drawn to the following developments:

FRA NEWS No.7/2012 Welcome to this issue of TNR FRA News. Financial Reporting and Auditing (FRA) News ( FRA News ) provides partners, staff and clients with a heads up of contemporary financial reporting,

FRA NEWS No.7/2012 Welcome to this issue of TNR FRA News. Financial Reporting and Auditing (FRA) News ( FRA News ) provides partners, staff and clients with a heads up of contemporary financial reporting,

Our Vision is: Values:

Our Vision is: To be recognised by our stakeholders for our leading contribution in achieving the highest level of professional and ethical behaviour in the accounting profession. We Achieve this Vision

Our Vision is: To be recognised by our stakeholders for our leading contribution in achieving the highest level of professional and ethical behaviour in the accounting profession. We Achieve this Vision

Accounting ACN Annual Report. 30 June 2014 ENGAGEMENT INFLUENCE

Accounting Professional Accounting& Ethical Professional Standards & Board Ethical Limited Standards ACN Board 118 227 259Limited ACN 118 227 259 Annual Report for Annual the year ended Report 30 for June

Accounting Professional Accounting& Ethical Professional Standards & Board Ethical Limited Standards ACN Board 118 227 259Limited ACN 118 227 259 Annual Report for Annual the year ended Report 30 for June

INSTITUTE OF CHARTERED PROFESSIONAL ACCOUNTANTS OF SASKATCHEWAN RULES

INTRODUCTION Registrants are subject to a regime of regulation defined as Rules which, means and includes any right, requirement, obligation of a registrant or duty or power of the Institute that is set

INTRODUCTION Registrants are subject to a regime of regulation defined as Rules which, means and includes any right, requirement, obligation of a registrant or duty or power of the Institute that is set

Guide to Accounting Officer Reporting Engagements

Guide to Accounting Officer Reporting Engagements EXPRESSI ON OF INTERE FOR TRAINING PROVIDERS TO PROVIDE TRAINING PROGRAMMES TO SAICA MEMBER SOUTHERN AFRICAN INSTITUTE FOR BUSINESS ACCOUNTANTS APPROVED

Guide to Accounting Officer Reporting Engagements EXPRESSI ON OF INTERE FOR TRAINING PROVIDERS TO PROVIDE TRAINING PROGRAMMES TO SAICA MEMBER SOUTHERN AFRICAN INSTITUTE FOR BUSINESS ACCOUNTANTS APPROVED

Audit Oversight Board (AOB)

") Audit Oversight Board (AOB) 6 th April 2010 Securities Commission Malaysia Establishment of AOB : In line with global trend United States: PCAOB Register auditors and firms, set auditing and ethical standards,

Audit Oversight Board (AOB) 6 th April 2010 Securities Commission Malaysia Establishment of AOB : In line with global trend United States: PCAOB Register auditors and firms, set auditing and ethical standards,

A GUIDE FOR SUPERANNUATION TRUSTEES to monitor listed Australian companies

A C S I G O V E R N A N C E G U I D E L I N E S May 2009 May 2009 A GUIDE FOR SUPERANNUATION TRUSTEES to monitor listed Australian companies J U L Y 2 0 1 1 A guide for superannuation trustees to monitor

A C S I G O V E R N A N C E G U I D E L I N E S May 2009 May 2009 A GUIDE FOR SUPERANNUATION TRUSTEES to monitor listed Australian companies J U L Y 2 0 1 1 A guide for superannuation trustees to monitor

Oversight Committee Mandate: Audit and Finance Committee

Oversight Committee Mandate: Audit and Finance Committee 1 1. PURPOSE The Audit and Finance Committee (the AFC) assists the Board of Directors (the BOD) in fulfilling its responsibilities with respect

Oversight Committee Mandate: Audit and Finance Committee 1 1. PURPOSE The Audit and Finance Committee (the AFC) assists the Board of Directors (the BOD) in fulfilling its responsibilities with respect

SAIBA MEMBER GUIDE TO ACCOUNTING OFFICER REPORTING ENGAGEMENTS

SAIBA MEMBER GUIDE TO ACCOUNTING OFFICER REPORTING ENGAGEMENTS The Southern African Institute for Business Accountants No. 5 Cecil Knight Office Park 46 Cecil Knight Street Rant en Dal KRUGERSDORP 1739

SAIBA MEMBER GUIDE TO ACCOUNTING OFFICER REPORTING ENGAGEMENTS The Southern African Institute for Business Accountants No. 5 Cecil Knight Office Park 46 Cecil Knight Street Rant en Dal KRUGERSDORP 1739

Richard M. Scrushy

Ethics Wins Richard M. Scrushy $100,000 Coffee Mug SUCCESS In 1806 Webster s Dictionary defined success as being generous, prosperous, healthy and kind. Today, Webster s defines success as the

Ethics Wins Richard M. Scrushy $100,000 Coffee Mug SUCCESS In 1806 Webster s Dictionary defined success as being generous, prosperous, healthy and kind. Today, Webster s defines success as the

Accounting for Business Combinations (ABC)

") Accounting for Business Combinations (ABC) Lecture 1;; Corporate Financial Reporting & Revision Nature of companies A company is a type of organisation established under the Corporations Act 2001. Companies

Accounting for Business Combinations (ABC) Lecture 1;; Corporate Financial Reporting & Revision Nature of companies A company is a type of organisation established under the Corporations Act 2001. Companies

February 14-15, 2005 New York, United States ASSOCIATION OF ACCOUNTING TECHNICIANS

IFAC Ethics Committee Meeting February 14-15, 2005 New York, United States Agenda Item 2-C Part I ASSOCIATION OF ACCOUNTING TECHNICIANS Response to the International Federation of Accountants (IFAC) exposure

IFAC Ethics Committee Meeting February 14-15, 2005 New York, United States Agenda Item 2-C Part I ASSOCIATION OF ACCOUNTING TECHNICIANS Response to the International Federation of Accountants (IFAC) exposure

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES CORPORATIONS AMENDMENT (PHOENIXING AND OTHER MEASURES) BILL 2012

BILL 2012") 2012 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES CORPORATIONS AMENDMENT (PHOENIXING AND OTHER MEASURES) BILL 2012 EXPLANATORY MEMORANDUM (Circulated by the authority of the

2012 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES CORPORATIONS AMENDMENT (PHOENIXING AND OTHER MEASURES) BILL 2012 EXPLANATORY MEMORANDUM (Circulated by the authority of the

Complaint Procedures for Accounting and Auditing Matters

Complaint Procedures for Accounting and Auditing Matters Corporate Secretariat Service August 7, 2014 V1.0 August 2016 V11 For Internal Use Table of contents 1. POLICY OVERVIEW... 3 1.1 SCOPE... 3 1.2

Complaint Procedures for Accounting and Auditing Matters Corporate Secretariat Service August 7, 2014 V1.0 August 2016 V11 For Internal Use Table of contents 1. POLICY OVERVIEW... 3 1.1 SCOPE... 3 1.2

AIST GOVERNANCE CODE. AIST Governance Code

AIST GOVERNANCE CODE AIST Governance Code 2017 Foreword The profit-to-member superannuation sector stands proudly by our record of achieving superior net returns on the retirement savings of our members.

AIST GOVERNANCE CODE AIST Governance Code 2017 Foreword The profit-to-member superannuation sector stands proudly by our record of achieving superior net returns on the retirement savings of our members.

AUDIT COMMITTEE CHARTER

Page 1 of 7 A. GENERAL 1. PURPOSE The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of Teck Resources Limited ( the Corporation ) is to provide an open avenue of

Page 1 of 7 A. GENERAL 1. PURPOSE The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of Teck Resources Limited ( the Corporation ) is to provide an open avenue of

ICP 7 Corporate Governance. Yoshi Kawai, Secretary General ASSAL, April 2015

ICP 7 Corporate Governance Yoshi Kawai, Secretary General ASSAL, April 2015 Corporate Governance Refers to systems (such as strategies, policies, processes and controls) through which an entity is managed

ICP 7 Corporate Governance Yoshi Kawai, Secretary General ASSAL, April 2015 Corporate Governance Refers to systems (such as strategies, policies, processes and controls) through which an entity is managed

International Accounting Education Standards Board

International Accounting Education Standards Board Corporate Collapses and the Need to Restore Credibility and Trust Sample Course 2 - Ethical Issues in Accountancy - These sample course materials have

International Accounting Education Standards Board Corporate Collapses and the Need to Restore Credibility and Trust Sample Course 2 - Ethical Issues in Accountancy - These sample course materials have

Annual Financial Report

Westpac TPS Trust ARSN 119 504 380 Annual Financial Report FOR THE YEAR ENDED 30 SEPTEMBER 2015 Westpac RE Limited as Responsible Entity for the Westpac TPS Trust ABN 80 000 742 478 / AFS Licence No 233717

Westpac TPS Trust ARSN 119 504 380 Annual Financial Report FOR THE YEAR ENDED 30 SEPTEMBER 2015 Westpac RE Limited as Responsible Entity for the Westpac TPS Trust ABN 80 000 742 478 / AFS Licence No 233717

Chapter Four. AICPA Code of Professional Conduct. McGraw-Hill/Irwin. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Four AICPA Code of Professional Conduct McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Investigations of the Profession High profile frauds in the 1970s,

Chapter Four AICPA Code of Professional Conduct McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Investigations of the Profession High profile frauds in the 1970s,

for Tax Preparers Part I

for Tax Preparers Part I Table of Contents 1. Introduction... 1 2. Training Objectives... 2 3. Resources... 3 4. Ethics Overview... 4 a. Ethical Behavior... 4 i. Applied Ethics... 4 b. Business Ethics...

for Tax Preparers Part I Table of Contents 1. Introduction... 1 2. Training Objectives... 2 3. Resources... 3 4. Ethics Overview... 4 a. Ethical Behavior... 4 i. Applied Ethics... 4 b. Business Ethics...

EMBRACING CORPORATE GOVERNANCE PRACTICES AMONG LISTED ENTITIES. Presentation by: CPA Tom Kimaru

EMBRACING CORPORATE GOVERNANCE PRACTICES AMONG LISTED ENTITIES Presentation by: CPA Tom Kimaru Director, Regulatory Affairs, Nairobi Securities Exchange Limited Wednesday, 22 nd March 2017 Uphold public

EMBRACING CORPORATE GOVERNANCE PRACTICES AMONG LISTED ENTITIES Presentation by: CPA Tom Kimaru Director, Regulatory Affairs, Nairobi Securities Exchange Limited Wednesday, 22 nd March 2017 Uphold public

NEED TO REGULATE & OUTLINE THE QUALIFICATION OF COMPANY LIQUIDATORS

NEED TO REGULATE & OUTLINE THE QUALIFICATION OF COMPANY LIQUIDATORS February 16, 2010 Under the Companies Act, 1956, Company Liquidators (professionals and private practitioners as Liquidators) can be

NEED TO REGULATE & OUTLINE THE QUALIFICATION OF COMPANY LIQUIDATORS February 16, 2010 Under the Companies Act, 1956, Company Liquidators (professionals and private practitioners as Liquidators) can be

TIME FOR KIDS SPECIAL PURPOSE FINANCIAL STATEMENT 2016/2017 FINANCIAL YEAR

TIME FOR KIDS SPECIAL PURPOSE FINANCIAL STATEMENT /2017 FINANCIAL YEAR Statement of profit or loss and other comprehensive income Page 1 Statement of financial position in the balance sheet Page 2 Statement

TIME FOR KIDS SPECIAL PURPOSE FINANCIAL STATEMENT /2017 FINANCIAL YEAR Statement of profit or loss and other comprehensive income Page 1 Statement of financial position in the balance sheet Page 2 Statement

CHAPTER 8: Accounting

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

ETHICAL STANDARD FOR AUDITORS (IRELAND) APRIL 2017

APRIL 2017") ETHICAL STANDARD FOR AUDITORS (IRELAND) APRIL 2017 MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality financial reporting,

ETHICAL STANDARD FOR AUDITORS (IRELAND) APRIL 2017 MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality financial reporting,

Regulation and Competition in Professional Services: Accounting Services

2008/SOM3/GOS/CONF/002 Regulation and Competition in Professional Services: Accounting Services Submitted by: Australia APEC-IDRC Conference on Competition Policy Issues in Services Sectors Lima, Peru

2008/SOM3/GOS/CONF/002 Regulation and Competition in Professional Services: Accounting Services Submitted by: Australia APEC-IDRC Conference on Competition Policy Issues in Services Sectors Lima, Peru

Wellington Management Portfolios (Australia) - Special Strategies Portfolio

- Special Strategies Portfolio") Wellington Management Portfolios (Australia) - Special Strategies Portfolio ARSN 130 381 887 Annual report - 30 June 2015 ARSN 130 381 887 Annual report - 30 June 2015 Contents Page Directors' Report 1

Wellington Management Portfolios (Australia) - Special Strategies Portfolio ARSN 130 381 887 Annual report - 30 June 2015 ARSN 130 381 887 Annual report - 30 June 2015 Contents Page Directors' Report 1

Australian Unity Office Fund

Australian Unity Office Fund 18 September 2018 Corporate Governance Statement Issued by: Australian Unity Investment Real Estate Limited ( Responsible Entity ) ABN 86 606 414 368, AFS Licence No. 477434

Australian Unity Office Fund 18 September 2018 Corporate Governance Statement Issued by: Australian Unity Investment Real Estate Limited ( Responsible Entity ) ABN 86 606 414 368, AFS Licence No. 477434

Review of Part C of the Code, Phase 2 Update

Agenda Item 4-A Review of Part C of the Code, Phase 2 Update How the Project Serves the Public Interest Over half of the world s professional accountants are professional accountants in business (PAIBs)

Agenda Item 4-A Review of Part C of the Code, Phase 2 Update How the Project Serves the Public Interest Over half of the world s professional accountants are professional accountants in business (PAIBs)

SESSION 1 INTRODUCTION TO AUDITING

SESSION 1 INTRODUCTION TO AUDITING Learning objectives: State the objectives and principal activities of statutory audit. Discuss the philosophy of audit. Discuss the concept of accountability. Discuss

SESSION 1 INTRODUCTION TO AUDITING Learning objectives: State the objectives and principal activities of statutory audit. Discuss the philosophy of audit. Discuss the concept of accountability. Discuss

Neil Cherry Chairman New Zealand Auditing and Assurance Standards Board

28 February 2014 Mr Ken Siong Technical Director International Ethics Standards Board for Accountants International Federation of Accountants 545 Fifth Avenue, 14th Floor New York, NY 10017 USA Dear Ken,

28 February 2014 Mr Ken Siong Technical Director International Ethics Standards Board for Accountants International Federation of Accountants 545 Fifth Avenue, 14th Floor New York, NY 10017 USA Dear Ken,