Presenters. James Jaramillo. Rose Ann Abraham, CPA. Todd Solomon, JD. Partner, McDermott Will & Emery LLP. Partner, Baker Tilly Virchow Krause, LLP

|

|

|

- Earl Richardson

- 6 years ago

- Views:

Transcription

1

2

3

4 Presenters Rose Ann Abraham, CPA Partner, Baker Tilly Virchow Krause, LLP Todd Solomon, JD Partner, McDermott Will & Emery LLP James Jaramillo Vice President, Sheridan Road Financial 4

5

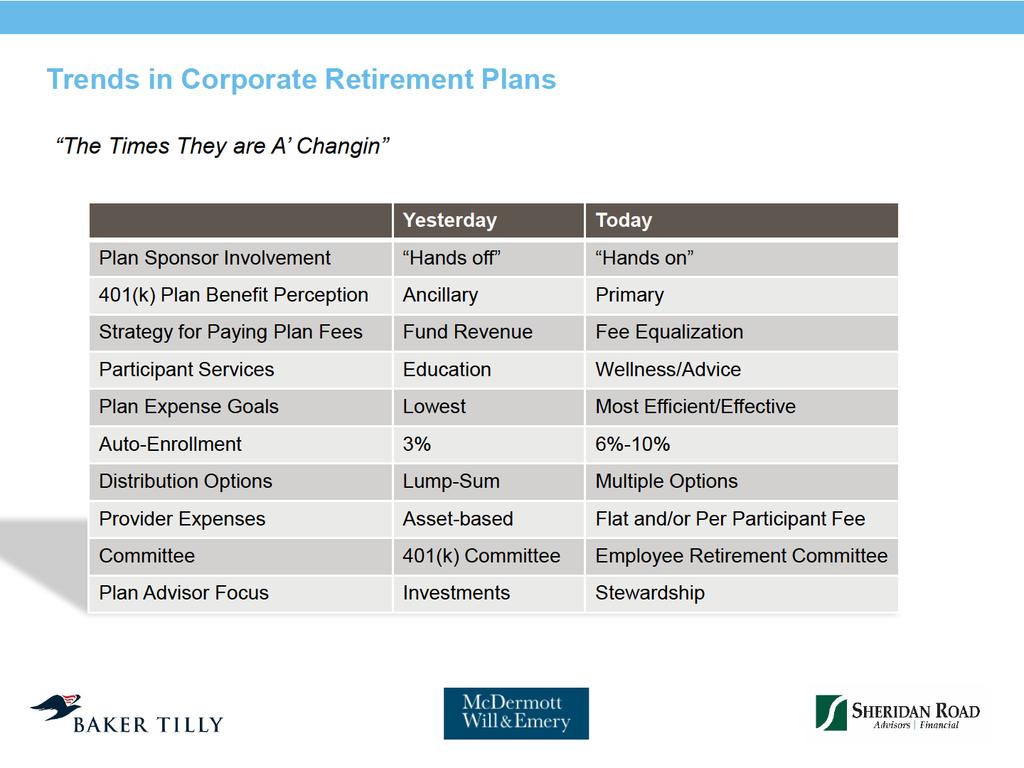

6 Trends in Corporate Retirement Plans Industry Trends Rapidly Changing Regulatory Environment Increased Costs of Employee Benefits Consolidation of Retirement Plan Providers Employees Increasingly looking to Employers for Financial Guidance Companies Required to Take More Active Role in Managing Fiduciary Obligations

7

8

9

10

11 Best Practices Action Steps Understand Roles and Responsibilities Hire Prudent Experts Identify, Quantify and Benchmark Plan Expenses Eliminate Conflicts of Interest Maximize Impact of Plan Design Help Your Employees

12

13

14 Pension Plan De-Risking Trends Continued trend to stabilizing liabilities and liability driven investing Prevalence of lump sum windows Be aware of IRS guidance regarding offering to retirees Be mindful of not making the lump sum a permanent feature / don t approach the same group multiple times Be clear in participant communications / be ready for claims / use ERISA discretion language Plan terminations becoming more prevalent 14

15 Pension Plan De-Risking Trends Most, but not all, terminating plans file for determination letter and wait for that before making distributions Annuity selection is a fiduciary function (95-1 safest available annuity standard) Some sponsors do a spin-off / termination PBGC premium reduction example Participant survey example Permanence issue Pre-62 in-service withdrawal concern Age 62 in-service withdrawal options are becoming more common 15

16 Fiduciary Best Practices / Litigation Update Make sure delegations to plan fiduciaries are clear Examine fiduciary insurance coverage and indemnification obligations Committees should meet regularly and keep good minutes (detailed enough, but not excessive) Vendor RFPs and fee benchmarking should be done periodically Lawsuits regarding stale vendor relationships Don t forget 403(b) plans Recent university litigation 16

17 Fiduciary Best Practices / Litigation Update Stable value litigation Against both providers and plan fiduciaries Cases alleging breach on both sides of the stable value / money market issue Excessive fee cases / settlements Make sure funds are in the cheapest possible share class Benchmark fees periodically Engage an outside advisor Unique company stock fund challenges / prevalence of independent fiduciary 17

18 Fiduciary Best Practices / Litigation Update Impact of New DOL Fiduciary Rule Effective April 2017 Limited impact on large plan sponsors / investment committees Limited impact on plan investment advisors / managers More impact on plan recordkeepers and small plans (under $50M) IRA rollover advice issue 18

19

20

21 Highlights of Accounting, Audit & Regulatory Updates Accounting Standards Update (ASU) ASU No Fair Value Measurement (Topic 820): Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent). ASU No Technical Corrections and Improvements ASU , Plan Accounting

22 ASU No Fair Value Measurement (Topic 820): Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent Removes the requirement to include investments in the fair value hierarchy for which fair value is measured using the net asset value practical expedient. Requires retrospective application. Effective for fiscal years beginning after December 15, 2015 (nonpublic for fiscal years beginning after December 15, 2016) with early adoption permitted. Sufficient information must be provided to permit reconciliation of the fair value of the assets categorized within the FV hierarchy table to amounts presented in the statement of net assets Continue to disclose investment strategy, future investment commitments and redemption requirements ASU removes the disclosure of investment strategy for funds that file Form 5500 as a Direct Filing Entity (DFE). 22

23 FASB Issued ASU No Technical Corrections and Improvements FASB Issued ASU No Technical Corrections and Improvements Make minor amendments to FASB Accounting Standards Codification. Changes to the FASB definition of readily determinable fair value. (paragraph 30) The fair value of an equity security is readily determinable if sales prices or bid-and-asked quotations are currently available on a securities exchange registered with the U.S. Securities and Exchange Commission (SEC) or in the over-the-counter market, provided that those prices or quotations for the over-the-counter market are publicly reported by the National Association of Securities Dealers Automated Quotations systems or by OTC Markets Group Inc. Restricted stock meets that definition if the restriction terminates within one year. 23

24 FASB Issued ASU No Technical Corrections and Improvements FASB Issued ASU No Technical Corrections and Improvements Changes to the FASB definition of readily determinable fair value. (cont d) The fair value of an equity securities traded only in a foreign market is readily determinable if that foreign market is of a breadth and scope comparable to one of the U.S. markets referred to above. The fair value of an equity security that is an investment in a mutual fund or in a structure similar to a mutual fund (that is, a limited partnership or a venture capital entity) is readily determinable if the fair value per share (unit) is determined and published and is the basis for current transactions. 24

25

26 ASU , Plan Accounting FASB issued a three-part ASU to simplify financial reporting for benefit plans. Part I: Fully Benefit-Responsive Investment Contracts Part II: Plan Investment Disclosures Part III: Measurement Date Practical Expedient Developed by FASB Emerging Issues Task Force (EITF) Responded to advocacy efforts by the AICPA s Employee Benefit Plans Expert Panel. Identified the issues affecting a large number of plans with the goal of completing a project within a short period of time. Effective for fiscal years beginning after December 15, 2015 Early application is permitted Plans can early adopt any of the ASU s three parts without early adopting the other parts 26

27 ASU , Plan Accounting Part I: Fully Benefit-Responsive Investment Contracts (FBRIC) Affects defined contribution, pension and health and welfare plans. Definition of FBRIC in master glossary did not change. Clarifies that contract value is the relevant measure for FBRICs because that is the amount participants would receive in a transaction. Eliminates requirements to measure fair value and present related fair value measurement disclosures. Responds to concerns about the cost and effort required to measure the fair value of FBRICs when fair value is not the relevant measure. 27

28 ASU , Plan Accounting Part I: Fully Benefit-Responsive Investment Contracts (FBRIC) Instead, plans will present FBRICs at contract value in the statement of net assets available for benefits, either as, Investments at contract value. Fully benefit-responsive investment contracts at contract value. Investment contracts that do not meet the definition of a FBRIC continue to be presented at fair value. Apply new guidance retrospectively. Requires FBRIC to be measured, presented, and disclosed only at contract value. 28

29 ASU , Plan Accounting Challenges: Stable Value Common or Collective Trusts (CCTs) or Similar Investment Funds Guidance clarifies that indirect investments in FBRICs through investment companies (e.g., stable value CCTs) are not in the scope of the FBRIC guidance. Plans should report these investments as fair value. These funds typically qualify for measuring fair value using the net asset value (NAV) practical expedient. These funds calculate NAV per share (or its equivalent) in a manner consistent with the measurement principles of ASC

30 ASU , Plan Accounting Stable Value Common or Collective Trusts (CCTs) or Similar Investment Funds Guidance clarifies that indirect investments in FBRICs through investment companies (e.g., stable value CCTs) are not in the scope of the FBRIC guidance. (cont d) As required by ASC 946, the NAV calculated by the fund is based on net assets which includes FBRICs at contract value. This NAV represents the plan s fair value since this is the NAV at which the plan transacts with the fund. 30

31 ASU , Plan Accounting Part II: Plan Investment Disclosures Requires that investments that are measured using fair value (both participant-directed and nonparticipant-directed investments) be grouped only by general type, eliminating the need to disaggregate the investments by nature, characteristics, and risks. Eliminates the disclosure of individual investments that represent 5 percent or more of net assets available for benefits (evaluation for concentration). Disclosure of net appreciation or depreciation for investments by general type, requiring only presentation of net appreciation or depreciation in investments in the aggregate. If an investment is measured using the net asset value per share as a practical expedient and that investment is a fund that files a U.S. Department of Labor Form 5500, as a direct filing entity, disclosure of that investment s strategy is no longer required. 31

32 ASU , Plan Accounting Part III: Measurement Date Practical Expedient Permits plans to measure investments and investment-related accounts (e.g., a liability for a pending trade with a broker) as of a month-end date that is closest to the plan s fiscal year-end, when the fiscal period does not coincide with month-end. 32

33 Regulatory Update Internal Revenue Service ( IRS ) Announcement (reflected in update Rev. Proc , C.B. 54, and in successor to Rev. Proc , I.R.B. 194) This announcement provides the detail of the changes in the IRS determination letter program and also provides a transition rule with respect to the remedial amendment period for certain plans currently on a 5-year cycle. In addition this announcement formally provides notification that effective July 21, 2015, the IRS will no longer accept determination letter applications that are submitted offcycle with certain exceptions. 33

34 Regulatory Update The cessation of this IRS determination program is based on the need of the agency to more efficiently direct its limited resources and is effective January 1, will include the elimination of the staggered 5-year determination letter remedial amendment cycles for individually designed plans. will limit the scope of this program for these plans to initial plan qualification and qualification for termination. will leave unchanged the current remedial amendment period (Cycle E, ending January 31,2016) and the next remedial amendment period (Cycle A, February 1, 2016 through January 1, 2017). 34

35 Regulatory Update Potential impact of the change in the determination program: Plan sponsors may consider obtaining expert opinions of compliance with the Code. Plan sponsors may consider transitioning their individually designed plans to a pre-approved format (Master and Prototype, of Volume Submitter) as this program remains unchanged. 35

36 Common Compliance Errors Elective deferrals timely remittance When the DOL considers deferrals as late 29 CFR Definition of plan assets participant contributions. Maximum time period for pension benefit plans. in no event shall the date occur later than the 15th business day of the month following the month in which the participant contribution amounts are received by the employer. (not a safe harbor) Reg. Rule is outside maximum, not a safe harbor. Late deposits - safe harbors For small plans (< 100 participants) proposed regulations include 7 business day safe harbor. When the DOL considers deferrals as late DOL view If employer can deposit within 1 business day, that will be the standard used by the DOL. If employer can deposit within 5 business days, then 5 business days would be the standard. Policy, procedures and consistency throughout the year. 36

37 Common Compliance Errors Correction Lost earnings must be funded to the plan and allocated to participant accounts for the time period between the administratively feasible date and the date actually remitted. Late deposits are a prohibited transaction subject to 15% excise tax (on the earnings, not the deposit) under the Internal Revenue Code ( IRC ) 4975 report and pay via Form Alternate: use DOL s correction program (see DOL s Voluntary Fiduciary Correction Program ( VFCP )). Prevention Written policy and procedures for adhering to DOL timeliness requirement Emphasis on the importance of timeliness with HR and Payroll personnel Assign back up personnel for transmitting contributions 37

38 Common Compliance Errors Eligible plan compensation using incorrect definition of compensation Definition of compensation is as defined in your plan document Plan amendment and restatements unintentionally changed plan provisions Change in, update of plan document or adoption agreements with unintended consequences Results in Improper compensation used to calculate deferrals, employer match, and profit-sharing contributions Corrective action Match the Plan definition of compensation and ensure payroll has properly flagged the appropriate types of compensation for deferral Educate payroll personnel on Plan compensation definition Have all additions of earnings codes be run through a review for Plan deferral and matching eligibility Prevention Verify that eligible compensation is calculated using the plan document definition Noncash fringe benefits should be included in the final payroll for the year, instead of as a W-2 adjustment Verify proper coding of all payroll-related items 38

39 Common Compliance Errors Hardship Distribution unsupported IRS has stringent guidelines for Hardship distributions. Your Plan might have limitations as well, and if these guidelines are not met the distribution could be deemed an unqualified distribution Outsourced to third party service providers or record keeper No source documents maintained by third party or service provider other than e-certify hardship Correction Plan should request documentation from participant to substantiate the hardship If participant does not have documentation, employer should request repayment Prevention Educate HR/Payroll on IRS Guidelines for hardship Ensure Hardship withdrawals are allowed by the Plan Request and maintain documentation from participant to substantiate the hardship Deferrals should be suspended for six months and reinstated at the rate of the last deferral election on file 39

40 Looking Forward to 2017 Form 5500 Modernization Initiative Targeted for 2019 plan year filings Goals Increase disclosure of financial information Update service provider fee and expense information Require reporting of all group health plans covered by ERISA Improve compliance through new questions on plan operations and financial management of plan 40

41 Looking Forward to 2017 Regulatory oversight IRS and DOL Range from desk audits to investigations Focus of IRS is on plan documentation and compliance with regulations Late contributions and VFCP filings Using data analytics to audit plans, plan sponsors and auditors Being prepared is important Review plan documents Document controls Retain documentation to support fiduciary oversight 41

42

43 Questions? 43

44 Disclosure The content in this presentation is a resource for Baker Tilly Virchow Krause, LLP clients and prospective clients. The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.

ACCOUNTING & AUDITING UPDATE

Session 4 ACCOUNTING & AUDITING UPDATE Eric Ernest, CPA Partner Page 104 Objective To provide Accounting and Auditing updates covering: What s new and effective this year Reminders for the EBP season What

Session 4 ACCOUNTING & AUDITING UPDATE Eric Ernest, CPA Partner Page 104 Objective To provide Accounting and Auditing updates covering: What s new and effective this year Reminders for the EBP season What

EBP ACCOUNTING, AUDITING AND REGULATORY UPDATE

EBP ACCOUNTING, AUDITING AND REGULATORY UPDATE Michelle Brumfield, CPA Director Page 135 Objective At the end of this session, participants will: Receive a debrief of the new accounting and auditing standards

EBP ACCOUNTING, AUDITING AND REGULATORY UPDATE Michelle Brumfield, CPA Director Page 135 Objective At the end of this session, participants will: Receive a debrief of the new accounting and auditing standards

Accounting Standards Update (ASU)

") Accounting Standards Update (ASU) 2015-12 Plan Accounting: Defined Benefit Pension Plans (Topic 960) Defined Contribution Pension Plans (Topic 962) Health and Welfare Benefit Plans (Topic 965) Presenters

Accounting Standards Update (ASU) 2015-12 Plan Accounting: Defined Benefit Pension Plans (Topic 960) Defined Contribution Pension Plans (Topic 962) Health and Welfare Benefit Plans (Topic 965) Presenters

Employee benefit plan large filers: Meeting your compliance and fiduciary requirements. April 20, 2016

Employee benefit plan large filers: Meeting your compliance and fiduciary requirements April 20, 2016 1 Your presenters Rose Ann Abraham, CPA Partner Baker Tilly 312 729 8086 roseann.abraham@bakertilly.com

Employee benefit plan large filers: Meeting your compliance and fiduciary requirements April 20, 2016 1 Your presenters Rose Ann Abraham, CPA Partner Baker Tilly 312 729 8086 roseann.abraham@bakertilly.com

ST. OLAF COLLEGE 403(b) RETIREMENT PLAN Northfield, Minnesota

RETIREMENT PLAN Northfield, Minnesota") Plan Number - 001 EIN - 41-0693979 ST. OLAF COLLEGE 403(b) RETIREMENT PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2015 and 2014 and for the

Plan Number - 001 EIN - 41-0693979 ST. OLAF COLLEGE 403(b) RETIREMENT PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2015 and 2014 and for the

{Benefit plan technical update.}

{Benefit plan technical update.} December 2015 Employee Benefit Plan Financial Reporting Simplification A 30,000-Foot View In an effort to simplify financial reporting for employee benefit plans, the Financial

{Benefit plan technical update.} December 2015 Employee Benefit Plan Financial Reporting Simplification A 30,000-Foot View In an effort to simplify financial reporting for employee benefit plans, the Financial

The Peterson Company Retirement Savings Plan

The Peterson Company Retirement Savings Plan Financial Statements and Supplemental Schedule For the Years Ended December 31, 2015 and 2014 The report accompanying these financial statements was issued

The Peterson Company Retirement Savings Plan Financial Statements and Supplemental Schedule For the Years Ended December 31, 2015 and 2014 The report accompanying these financial statements was issued

Board Meeting Handout Agenda Priority Definition of Readily Determinable Fair Value March 1, 2017

Board Meeting Handout Agenda Priority Definition of Readily Determinable Fair Value March 1, 2017 PURPOSE OF THIS MEETING 1. The March 1, 2017 Board meeting is a decision-making meeting. The staff will

Board Meeting Handout Agenda Priority Definition of Readily Determinable Fair Value March 1, 2017 PURPOSE OF THIS MEETING 1. The March 1, 2017 Board meeting is a decision-making meeting. The staff will

Plan sponsors (and plan advisors)

") WINTER 2016 www.bdo.com GET TO KNOW BDO EXECUTIVE AND HR SERVICES FASB S ASU 2015-12 SIMPLIFIES FINANCIAL REPORTING FOR EBPs Plan sponsors (and plan advisors) often struggle with the appropriate application

WINTER 2016 www.bdo.com GET TO KNOW BDO EXECUTIVE AND HR SERVICES FASB S ASU 2015-12 SIMPLIFIES FINANCIAL REPORTING FOR EBPs Plan sponsors (and plan advisors) often struggle with the appropriate application

ST. OLAF COLLEGE EMERITI RETIREE HEALTH PLAN Northfield, Minnesota

Plan Number - 513 EIN - 41-0693979 ST. OLAF COLLEGE EMERITI RETIREE HEALTH PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2015 and 2014 and for

Plan Number - 513 EIN - 41-0693979 ST. OLAF COLLEGE EMERITI RETIREE HEALTH PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2015 and 2014 and for

Keeping Your Organization s Retirement Plan in Shape: A Two-Part CAPLAW Webinar Series. Webinar One: Ins and Outs of Retirement Plan Audits

Keeping Your Organization s Retirement Plan in Shape: A Two-Part CAPLAW Webinar Series Webinar One: Ins and Outs of Retirement Plan Audits Trainer: Angie Whiteside, CPA, AIF, Senior Manager 1 Materials/Disclaimer

Keeping Your Organization s Retirement Plan in Shape: A Two-Part CAPLAW Webinar Series Webinar One: Ins and Outs of Retirement Plan Audits Trainer: Angie Whiteside, CPA, AIF, Senior Manager 1 Materials/Disclaimer

W. R. Berkley Corporation Profit Sharing Plan

United States Securities and Exchange Commission Washington, D.C. 20549 Form 11-K/A Annual Report Pursuant to Section 15(d) of the Securities Exchange Act of 1934 (Mark One) þ Annual Report Pursuant to

United States Securities and Exchange Commission Washington, D.C. 20549 Form 11-K/A Annual Report Pursuant to Section 15(d) of the Securities Exchange Act of 1934 (Mark One) þ Annual Report Pursuant to

DOL & IRS CORRECTION PROGRAMS

Session 2 DOL & IRS CORRECTION PROGRAMS Eric Ernest, CPA Partner Page 26 Objectives This session will provide an overview of the regulatory environment for employee benefit plans and cover: Plan Regulatory

Session 2 DOL & IRS CORRECTION PROGRAMS Eric Ernest, CPA Partner Page 26 Objectives This session will provide an overview of the regulatory environment for employee benefit plans and cover: Plan Regulatory

Checklist for Employee Benefit Plan Sponsors

Checklist for Employee Benefit Plan Sponsors 999 Third Avenue, Suite 2800 Seattle WA, 98104 (206) 302-6800 The material appearing in this presentation is for informational purposes only and should not

Checklist for Employee Benefit Plan Sponsors 999 Third Avenue, Suite 2800 Seattle WA, 98104 (206) 302-6800 The material appearing in this presentation is for informational purposes only and should not

Updates to Peer Reviews of EBP Audits, including 403(b) Plan Considerations

Plan Considerations") Updates to Peer Reviews of EBP Audits, including 403(b) Plan Considerations June 22, 2011 Presenters Moderator Marilee Lau, retired partner KPMG LLP; Marilee Lau, CPA Part 1 Bob Lavenberg, Chair, AICPA

Updates to Peer Reviews of EBP Audits, including 403(b) Plan Considerations June 22, 2011 Presenters Moderator Marilee Lau, retired partner KPMG LLP; Marilee Lau, CPA Part 1 Bob Lavenberg, Chair, AICPA

two thousand eight ISSUE BROCHURE 403(b) Plans Frequently Asked Questions

Plans Frequently Asked Questions") Brochure 2-403bFAQs 11x17 - FINAL:Fact Sheet 2008.qxd 10/29/2008 11:04 AM Page 1 National Association of Government Defined Contribution Administrators, Inc. two thousand eight ISSUE BROCHURE 403(b) Plans

Brochure 2-403bFAQs 11x17 - FINAL:Fact Sheet 2008.qxd 10/29/2008 11:04 AM Page 1 National Association of Government Defined Contribution Administrators, Inc. two thousand eight ISSUE BROCHURE 403(b) Plans

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 11-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K [ ü] Annual Report Pursuant to Section 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K [ ü] Annual Report Pursuant to Section 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December

Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013

and 403(b) Plan Sponsors in 2013") Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013 Presented by: Rose Panico-Marino, AIF, ERPA, QPA Senior Vice President January 30, 2013 Learning Objectives Review specific

Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013 Presented by: Rose Panico-Marino, AIF, ERPA, QPA Senior Vice President January 30, 2013 Learning Objectives Review specific

THE TIMKEN COMPANY SAVINGS AND INVESTMENT PENSION PLAN (Full title of the Plan)

") Section 1: 11-K (11-K) UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K ý o ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal

Section 1: 11-K (11-K) UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K ý o ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal

American Chamber of Commerce Executives Profit Sharing Plan EIN PN 001 Auditor s Report and Financial Statements

EIN 54-6487038 PN 001 Auditor s Report and Financial Statements Contents Independent Auditor s Report... 1 Financial Statements Statements of Net Assets Available for Benefits... 3 Statements of Changes

EIN 54-6487038 PN 001 Auditor s Report and Financial Statements Contents Independent Auditor s Report... 1 Financial Statements Statements of Net Assets Available for Benefits... 3 Statements of Changes

American Chamber of Commerce Executives Profit Sharing Plan EIN PN 001. Independent Auditor s Report and Financial Statements

American Chamber of Commerce Executives EIN 54-6487038 PN 001 Independent Auditor s Report and Financial Statements Contents Independent Auditor s Report... 1 Financial Statements Statements of Net Assets

American Chamber of Commerce Executives EIN 54-6487038 PN 001 Independent Auditor s Report and Financial Statements Contents Independent Auditor s Report... 1 Financial Statements Statements of Net Assets

TIMKENSTEEL CORPORATION VOLUNTARY INVESTMENT PENSION PLAN

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31,

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31,

Memo No. Issue Summary, Supplement No. 1. Issue Date June 4, Meeting Date EITF June 18, 2015

Memo No. Issue Summary, Supplement No. 1 Memo Issue Date June 4, 2015 Meeting Date EITF June 18, 2015 Contact(s) Lisa Muehlbauer Lead Author Ext. (203) 956-5258 Peter Proestakes Assistant Director Ext.

Memo No. Issue Summary, Supplement No. 1 Memo Issue Date June 4, 2015 Meeting Date EITF June 18, 2015 Contact(s) Lisa Muehlbauer Lead Author Ext. (203) 956-5258 Peter Proestakes Assistant Director Ext.

EMPLOYEE BENEFIT PLANS FOR NFPs. Bertha Minnihan, Partner, Moss Adams LLP Brad Wall, Partner, Moss Adams LLP

EMPLOYEE BENEFIT PLANS FOR NFPs Bertha Minnihan, Partner, Moss Adams LLP Brad Wall, Partner, Moss Adams LLP 1 BERTHA MINNIHAN Bertha has nearly 20 years of experience in public accounting and serves as

EMPLOYEE BENEFIT PLANS FOR NFPs Bertha Minnihan, Partner, Moss Adams LLP Brad Wall, Partner, Moss Adams LLP 1 BERTHA MINNIHAN Bertha has nearly 20 years of experience in public accounting and serves as

Protecting Yourself from ERISA Fiduciary Liability

Protecting Yourself from ERISA Fiduciary Liability Tax Executives Institute Cincinnati-Columbus Chapter February 9-10, 2015 Jodi H. Epstein (202) 662-3468 JEpstein@ipbtax.com Benjamin L. Grosz (202) 662-3422

Protecting Yourself from ERISA Fiduciary Liability Tax Executives Institute Cincinnati-Columbus Chapter February 9-10, 2015 Jodi H. Epstein (202) 662-3468 JEpstein@ipbtax.com Benjamin L. Grosz (202) 662-3422

United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 11-K

United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31,

United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31,

The views in this summary are not Generally Accepted Accounting Principles until a consensus is reached and it is ratified by the Board.

Memo No. Issue Summary No. 1 Memo Issue Date March 5, 2015 Meeting Date(s) BM March 19, 2015 Contact(s) Lisa Muehlbauer Lead Author, Project Lead (203) 956-5258 Peter Proestakes Assistant Director (203)

Memo No. Issue Summary No. 1 Memo Issue Date March 5, 2015 Meeting Date(s) BM March 19, 2015 Contact(s) Lisa Muehlbauer Lead Author, Project Lead (203) 956-5258 Peter Proestakes Assistant Director (203)

ST. OLAF COLLEGE MATCHED SAVINGS PLAN Northfield, Minnesota

ST. OLAF COLLEGE MATCHED SAVINGS PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2012 and 2011 and for the Year Ended December 31, 2012 TABLE OF

ST. OLAF COLLEGE MATCHED SAVINGS PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2012 and 2011 and for the Year Ended December 31, 2012 TABLE OF

Inside This Issue. Summer What Data Do You Have? Utilizing Data Analytics for Employee Benefit Plans

Summer 2017 Employee Benefit News Critical to Your Business Inside This Issue Utilizing Data Analytics for Employee Benefit Plans AICPA ASB Proposes Standard on Auditor Reporting on ERISA Financial Statements

Summer 2017 Employee Benefit News Critical to Your Business Inside This Issue Utilizing Data Analytics for Employee Benefit Plans AICPA ASB Proposes Standard on Auditor Reporting on ERISA Financial Statements

Is Your Health Plan Ready for a HIPAA Audit?

WINTER 2017 Employee Benefit News Critical to Your Business Inside This Issue Changes to the Determination Letter Program Significant Proposed Form 5500 Changes Current Trends in Employee Stock Ownership

WINTER 2017 Employee Benefit News Critical to Your Business Inside This Issue Changes to the Determination Letter Program Significant Proposed Form 5500 Changes Current Trends in Employee Stock Ownership

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans:

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: June 30, 2016: 6 months after plan year-end: Deadline for completion of corrective distributions

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: June 30, 2016: 6 months after plan year-end: Deadline for completion of corrective distributions

Fiduciary compliance reviews: For your defined-contribution plan

Fiduciary compliance reviews: For your defined-contribution plan A fiduciary compliance review is not the same as the annual ERISA audit. We will explore some of the aspects of the review and some areas

Fiduciary compliance reviews: For your defined-contribution plan A fiduciary compliance review is not the same as the annual ERISA audit. We will explore some of the aspects of the review and some areas

ST. OLAF COLLEGE SALARY REDUCTION SAVINGS PLAN Northfield, Minnesota

Plan Number - 002 EIN - 41-0693979 ST. OLAF COLLEGE SALARY REDUCTION SAVINGS PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31,2013 and 2012 and for

Plan Number - 002 EIN - 41-0693979 ST. OLAF COLLEGE SALARY REDUCTION SAVINGS PLAN Northfield, Minnesota FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31,2013 and 2012 and for

Fiduciary Compliance Checklist Essential Points

Fiduciary Compliance Checklist Essential Points Who are the fiduciaries named under the plan? Defining the Fiduciary Structure Who are the fiduciaries not named under the plan but are performing duties

Fiduciary Compliance Checklist Essential Points Who are the fiduciaries named under the plan? Defining the Fiduciary Structure Who are the fiduciaries not named under the plan but are performing duties

4/8/2010. Overview of the New 403(b) Regulations. Overview of 403(b) Issues

Regulations. Overview of 403(b) Issues") The New Regulatory Environment for Sponsors of 403(b) Plans 2003-2010 Multnomah Group, Inc. All rights reserved. Overview of 403(b) Issues Overview of the New Regulations Plan Operations: Universal Availability

The New Regulatory Environment for Sponsors of 403(b) Plans 2003-2010 Multnomah Group, Inc. All rights reserved. Overview of 403(b) Issues Overview of the New Regulations Plan Operations: Universal Availability

Important Approaching Deadlines

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: September 15, 2016: 8 ½ months after plan year-end: For employers who filed corporate

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: September 15, 2016: 8 ½ months after plan year-end: For employers who filed corporate

Fiduciary Compliance Checklist

Employee Benefit Services Fiduciary Compliance Checklist Plan Fiduciaries are responsible for a variety of notices and duties as part of their responsibilities under ERISA. Fiduciaries must take every

Employee Benefit Services Fiduciary Compliance Checklist Plan Fiduciaries are responsible for a variety of notices and duties as part of their responsibilities under ERISA. Fiduciaries must take every

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 11-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

Community Action Program Legal Services (CAPLAW) Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors

Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors") Community Action Program Legal Services (CAPLAW) Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors March 1, 2017 Michele Berman Golkow golkow@ballardspahr.com 215.864.8403 Retirement

Community Action Program Legal Services (CAPLAW) Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors March 1, 2017 Michele Berman Golkow golkow@ballardspahr.com 215.864.8403 Retirement

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES 1 Today s Agenda Understand where ERISA applies to retirement

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES 1 Today s Agenda Understand where ERISA applies to retirement

Preparing for your first 401(k) plan audit

plan audit") Preparing for your first 401(k) plan audit 2017 2018 CONTENTS 02 INTRODUCTION 03 04 06 08 DOCUMENT GATHERING AND ORGANIZATION FIDUCIARY RESPONSIBILITY OPERATIONAL COMPLIANCE INTERNAL CONTROLS 11 FINANCIAL

Preparing for your first 401(k) plan audit 2017 2018 CONTENTS 02 INTRODUCTION 03 04 06 08 DOCUMENT GATHERING AND ORGANIZATION FIDUCIARY RESPONSIBILITY OPERATIONAL COMPLIANCE INTERNAL CONTROLS 11 FINANCIAL

The American Institute of Certified Public Accountants (AICPA) held its HIGHLIGHTS FROM THE AICPA S DECEMBER 2012 EBP CONFERENCE CONTACT:

held its HIGHLIGHTS FROM THE AICPA S DECEMBER 2012 EBP CONFERENCE CONTACT:") WINTER 2013 WWW.BDO.COM CONTACT: BOB LAVENBERG Assurance Partner National Partner In Charge of Employee Benefit Plan Audit Quality 215-636-5576 rlavenberg@bdo.com www.bdo.com HIGHLIGHTS FROM THE AICPA

WINTER 2013 WWW.BDO.COM CONTACT: BOB LAVENBERG Assurance Partner National Partner In Charge of Employee Benefit Plan Audit Quality 215-636-5576 rlavenberg@bdo.com www.bdo.com HIGHLIGHTS FROM THE AICPA

Pacific Institute for Research and Evaluation, Inc. Profit Sharing Plan and Trust

Pacific Institute for Research and Evaluation, Inc. Financial Statements and Supplemental Schedule Years Ended December 31, 2016 and 2015 The report accompanying these financial statements was issued by

Pacific Institute for Research and Evaluation, Inc. Financial Statements and Supplemental Schedule Years Ended December 31, 2016 and 2015 The report accompanying these financial statements was issued by

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C Form 11-K. For the transition period from to

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Form 11-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2015

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Form 11-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2015

Defined Contribution and Defined Benefit Plans: Have you considered everything?

Defined Contribution and Defined Benefit Plans: Have you considered everything? Amy Henselin Partner, Audit Appleton Debbie Smith Partner, National Professional Standards Group Chicago Objectives Identify

Defined Contribution and Defined Benefit Plans: Have you considered everything? Amy Henselin Partner, Audit Appleton Debbie Smith Partner, National Professional Standards Group Chicago Objectives Identify

THE UPSIDE OF AUDITS: STREAMLINING YOUR RETIREMENT PLAN

THE UPSIDE OF AUDITS: STREAMLINING YOUR RETIREMENT PLAN Solutions that can help reduce costs, improve operations, limit fiduciary exposure, and better prepare your company for the future. It is possible

THE UPSIDE OF AUDITS: STREAMLINING YOUR RETIREMENT PLAN Solutions that can help reduce costs, improve operations, limit fiduciary exposure, and better prepare your company for the future. It is possible

IRS. 401(k) Plan Checklist. If you answered No to any of the above questions, you may have made a mistake in the

Plan Checklist. If you answered No to any of the above questions, you may have made a mistake in the") 401(k) Plan Checklist This checklist is not a complete description of all For Business Owner s Use plan requirements, and should not be used as a (do not send this worksheet to the IRS) substitute for

401(k) Plan Checklist This checklist is not a complete description of all For Business Owner s Use plan requirements, and should not be used as a (do not send this worksheet to the IRS) substitute for

Establishing a Due Diligence File

resource edge TM Establishing a Due Diligence File investment insights practice building solutions retirement resources RESOURCE EDGE TM Table of Contents 3 Introduction 4 401(k) fiduciary documentation

resource edge TM Establishing a Due Diligence File investment insights practice building solutions retirement resources RESOURCE EDGE TM Table of Contents 3 Introduction 4 401(k) fiduciary documentation

UNITED STATES SECURITIES AND EXCHANGE COMMISSION. Washington, D.C FORM 11-K. Commission File Number

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One) x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One) x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

LOUISIANA-PACIFIC 401(k) AND PROFIT SHARING PLAN

AND PROFIT SHARING PLAN") United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K [X] ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For fiscal year ended: December 31,

United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K [X] ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For fiscal year ended: December 31,

for public school employers retirement plan solutions 403(b) plan compliance guide

plan compliance guide") for public school employers retirement plan solutions 403(b) plan compliance guide AXA Equitable Life Insurance Company (NY, NY) Table of Contents About This Guide 1 AXA Equitable Experience, Knowledge,

for public school employers retirement plan solutions 403(b) plan compliance guide AXA Equitable Life Insurance Company (NY, NY) Table of Contents About This Guide 1 AXA Equitable Experience, Knowledge,

TRISTAR PENSION CONSULTING

TRISTAR PENSION CONSULTING 2/1/2006 Responsibilities of a Plan Sponsor Introduction Allocation of Duties Employee Notifications Plan Summaries Beneficiary Forms Deferral Elections Plan Contributions Safe

TRISTAR PENSION CONSULTING 2/1/2006 Responsibilities of a Plan Sponsor Introduction Allocation of Duties Employee Notifications Plan Summaries Beneficiary Forms Deferral Elections Plan Contributions Safe

TIMKENSTEEL CORPORATION SAVINGS AND INVESTMENT PENSION PLAN (Full title of the Plan)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31,

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31,

NIKE, Inc. (Full title of the plan)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended May 31, 2016

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended May 31, 2016

Farm Credit Foundations Defined Contribution / 401(k) Plan. Financial Statements December 31, 2015 and 2014

Plan. Financial Statements December 31, 2015 and 2014") Farm Credit Foundations Defined Contribution / 401(k) Plan Financial Statements December 31, 2015 and 2014 CliftonLarsonAllen LLP CLAconnect.com INDEPENDENT AUDITORS' REPORT Participants and Farm Credit

Farm Credit Foundations Defined Contribution / 401(k) Plan Financial Statements December 31, 2015 and 2014 CliftonLarsonAllen LLP CLAconnect.com INDEPENDENT AUDITORS' REPORT Participants and Farm Credit

SM SERVICE AGREEMENT. . The Plan Year in which Client engages MVP to begin providing services

SERVICE AGREEMENT This Service Agreement ( Agreement ) is entered into on the Effective Date set forth below between MVP Plan Administrators, Inc. ( MVP ), and the Plan Sponsor or Client. Except where

SERVICE AGREEMENT This Service Agreement ( Agreement ) is entered into on the Effective Date set forth below between MVP Plan Administrators, Inc. ( MVP ), and the Plan Sponsor or Client. Except where

TIMKENSTEEL CORP FORM 11-K. (Annual Report of Employee Stock Plans) Filed 06/26/15 for the Period Ending 12/31/14

Filed 06/26/15 for the Period Ending 12/31/14") TIMKENSTEEL CORP FORM 11-K (Annual Report of Employee Stock Plans) Filed 06/26/15 for the Period Ending 12/31/14 Address 1835 DUEBER AVENUE SW CANTON, OH 44706-0928 Telephone 330-471-7000 CIK 0001598428

TIMKENSTEEL CORP FORM 11-K (Annual Report of Employee Stock Plans) Filed 06/26/15 for the Period Ending 12/31/14 Address 1835 DUEBER AVENUE SW CANTON, OH 44706-0928 Telephone 330-471-7000 CIK 0001598428

FORM 11-K. STARWOOD HOTELS & RESORTS WORLDWIDE SAVINGS AND RETIREMENT PLAN (Full title of the plan)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K ý Annual Report Pursuant to Section 15(d) of the Securities Exchange Act of 1934 (Fee Required) For the Fiscal Year Ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K ý Annual Report Pursuant to Section 15(d) of the Securities Exchange Act of 1934 (Fee Required) For the Fiscal Year Ended

EBPFAQ Introduction. Indiana Society of CPAs September 17, 2013 Concurrent Session 2: The EBP Market 2013 Address Common Questions

Indiana Society of CPAs September 17, 2013 Concurrent Session 2: Loscalzo s Frequently Asked Questions In Employee Benefit Plan Loscalzo s 2012 Accounting And Auditing Template for PowerPoint Slides A

Indiana Society of CPAs September 17, 2013 Concurrent Session 2: Loscalzo s Frequently Asked Questions In Employee Benefit Plan Loscalzo s 2012 Accounting And Auditing Template for PowerPoint Slides A

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 11-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One): x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One): x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

403(B) THRIFT PLAN OF COMMUNITY INVOLVEMENT PROGRAMS FINANCIAL STATEMENTS. December 31, 2016 and 2015

THRIFT PLAN OF COMMUNITY INVOLVEMENT PROGRAMS FINANCIAL STATEMENTS. December 31, 2016 and 2015") 403(B) THRIFT PLAN OF COMMUNITY INVOLVEMENT PROGRAMS FINANCIAL STATEMENTS TABLE OF CONTENTS Independent Auditor's Report 1 Page Number FINANCIAL STATEMENTS Statements of Net Assets Available for Benefits

403(B) THRIFT PLAN OF COMMUNITY INVOLVEMENT PROGRAMS FINANCIAL STATEMENTS TABLE OF CONTENTS Independent Auditor's Report 1 Page Number FINANCIAL STATEMENTS Statements of Net Assets Available for Benefits

CPE. Advanced Auditing for Defined Contribution Retirement Plans

CPE Advanced Auditing for Defined Contribution Retirement Plans 1 Advanced Auditing for Defined Contribution Retirement Plans Chapter I/O Title Introduction and Overview 1 Defined Contribution Retirement

CPE Advanced Auditing for Defined Contribution Retirement Plans 1 Advanced Auditing for Defined Contribution Retirement Plans Chapter I/O Title Introduction and Overview 1 Defined Contribution Retirement

Common Compliance Issues and Remedies

Common Compliance Issues and Remedies Ilene H. Ferenczy, Esq. Ferenczy + Paul LLP Tricia A. Van Vliet, CPA Elliott Group CPAs, PLLC Today s Lineup Overview of plan compliance errors knowing how to recognize

Common Compliance Issues and Remedies Ilene H. Ferenczy, Esq. Ferenczy + Paul LLP Tricia A. Van Vliet, CPA Elliott Group CPAs, PLLC Today s Lineup Overview of plan compliance errors knowing how to recognize

Employee Benefit Plan Voluntary Correction Programs: Fixing Costly Errors and Preserving Tax Benefits

FOR LIVE PROGRAM ONLY Employee Benefit Plan Voluntary Correction Programs: Fixing Costly Errors and Preserving Tax Benefits WEDNESDAY, MARCH 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Employee Benefit Plan Voluntary Correction Programs: Fixing Costly Errors and Preserving Tax Benefits WEDNESDAY, MARCH 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

American States Water Company

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11 K (Mark One) x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 30, 2016

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11 K (Mark One) x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 30, 2016

Farm Credit Foundations Pre-409A Frozen Nonqualified Deferred Compensation Plan. Financial Statements December 31, 2015 and 2014

Farm Credit Foundations Pre-409A Frozen Nonqualified Deferred Compensation Plan Financial Statements December 31, 2015 and 2014 CliftonLarsonAllen LLP CLAconnect.com INDEPENDENT AUDITORS' REPORT Participants

Farm Credit Foundations Pre-409A Frozen Nonqualified Deferred Compensation Plan Financial Statements December 31, 2015 and 2014 CliftonLarsonAllen LLP CLAconnect.com INDEPENDENT AUDITORS' REPORT Participants

ERISA FIDUCIARY BASICS AND BEST PRACTICES

Presents ERISA FIDUCIARY BASICS AND BEST PRACTICES November 5, 2015 Misty A. Leon mleon@wifilawgroup.com COMPLIANCE 101 General Roles and Responsibilities Who's Involved? Plan Administrator Responsibilities

Presents ERISA FIDUCIARY BASICS AND BEST PRACTICES November 5, 2015 Misty A. Leon mleon@wifilawgroup.com COMPLIANCE 101 General Roles and Responsibilities Who's Involved? Plan Administrator Responsibilities

Equity method investments and joint ventures

Financial reporting developments A comprehensive guide Equity method investments and joint ventures October 2017 To our clients and other friends Investors frequently enter into transactions in which they

Financial reporting developments A comprehensive guide Equity method investments and joint ventures October 2017 To our clients and other friends Investors frequently enter into transactions in which they

Employee Benefits and Qualified Plan Update

Employee Benefits and Qualified Plan Update Sonya D. Wright, CFP, CEBS, QKA First, a Quiz... There will be prizes! Getting to Know You! Percentage of your business in qualified retirement plans? Securities

Employee Benefits and Qualified Plan Update Sonya D. Wright, CFP, CEBS, QKA First, a Quiz... There will be prizes! Getting to Know You! Percentage of your business in qualified retirement plans? Securities

BRISTOL-MYERS SQUIBB COMPANY 345 PARK AVENUE NEW YORK, NY (212)

") SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 TRANSITION

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 11-K x ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 TRANSITION

FIDUCIARY INSIGHTS & UPDATES

FIDUCIARY INSIGHTS & UPDATES Did You Know? The section of the Internal Revenue Code that made 401(k) plans possible was enacted into law in 1978. It was intended to allow taxpayers a break on taxes on

FIDUCIARY INSIGHTS & UPDATES Did You Know? The section of the Internal Revenue Code that made 401(k) plans possible was enacted into law in 1978. It was intended to allow taxpayers a break on taxes on

Fiduciary Responsibility in the Age of Technology

Fiduciary Responsibility in the Age of Technology By: Lisa L. Jones, Esq., CPC, QPA VP ERISA Consulting Group, Sentinel Ryan M. Ransford, AIF, QPFC Retirement Plan Advisory Rep, Sentinel Overview This

Fiduciary Responsibility in the Age of Technology By: Lisa L. Jones, Esq., CPC, QPA VP ERISA Consulting Group, Sentinel Ryan M. Ransford, AIF, QPFC Retirement Plan Advisory Rep, Sentinel Overview This

2016 Planning for ERISA Single-Employer Defined Contribution Plan Operations

2016 Planning for ERISA Single-Employer Defined Contribution Plan Operations Volume 38 Issue 146 November 10, 2015 The calendar provided in this FYI In-Depth will help you set up your own schedule of activities

2016 Planning for ERISA Single-Employer Defined Contribution Plan Operations Volume 38 Issue 146 November 10, 2015 The calendar provided in this FYI In-Depth will help you set up your own schedule of activities

Hot Topics IN PLAN AUDITS

Hot Topics IN PLAN AUDITS . A. Ted Hotz, CPA Audit Vice President Pugh CPAs Who Audits the Auditor? Department of Labor AICPA Peer Review program Review by another firm every 3 years Review requirement

Hot Topics IN PLAN AUDITS . A. Ted Hotz, CPA Audit Vice President Pugh CPAs Who Audits the Auditor? Department of Labor AICPA Peer Review program Review by another firm every 3 years Review requirement

Employee Benefit Plan Voluntary Correction Programs: Fixing Costly Errors and Preserving Tax Benefits

Employee Benefit Plan Voluntary Correction Programs: Fixing Costly Errors and Preserving Tax Benefits Leveraging Available IRS and DOL Programs to Proactively Address Plan Mistakes and Minimize Penalties

Employee Benefit Plan Voluntary Correction Programs: Fixing Costly Errors and Preserving Tax Benefits Leveraging Available IRS and DOL Programs to Proactively Address Plan Mistakes and Minimize Penalties

Correcting Qualified Plan Errors under EPCRS

Correcting Qualified Plan Errors under EPCRS This is just one example of the many online resources Practical Law Company offers. Andy Wang and Jennifer Kobayashi, Wang Kobayashi Austin, LLC with PLC Employee

Correcting Qualified Plan Errors under EPCRS This is just one example of the many online resources Practical Law Company offers. Andy Wang and Jennifer Kobayashi, Wang Kobayashi Austin, LLC with PLC Employee

UPS 401(k) Savings Plan

Savings Plan") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One) ý ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 11-K (Mark One) ý ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 11-K

(Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 For the fiscal year ended December 31, 2009 FORM 11-K ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE

(Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 For the fiscal year ended December 31, 2009 FORM 11-K ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE

2015 Employee Benefit Plan Audit Conference Basic Audit Workshop Maryland Association of CPA s Columbia, Maryland April 27, 2015

2015 Employee Benefit Plan Audit Conference Basic Audit Workshop Maryland Association of CPA s Columbia, Maryland April 27, 2015 1 Discussion Leaders Michael Auerbach Marilee P. Lau 2 1 Overview and Introduction

2015 Employee Benefit Plan Audit Conference Basic Audit Workshop Maryland Association of CPA s Columbia, Maryland April 27, 2015 1 Discussion Leaders Michael Auerbach Marilee P. Lau 2 1 Overview and Introduction

Accounting and Financial Reporting Developments for Private Companies

Accounting and Financial Reporting Developments for Private Companies THIRD QUARTER 2018 In this update, we highlight some of the more important 2018 third-quarter accounting and financial reporting activities

Accounting and Financial Reporting Developments for Private Companies THIRD QUARTER 2018 In this update, we highlight some of the more important 2018 third-quarter accounting and financial reporting activities

Hiding in Plain View: Impact of Recent Tax Legislation on Retirement Plans

Hiding in Plain View: Impact of Recent Tax Legislation on Retirement Plans Presented by Eric Paley and Claire Rowland March 14, 2018 Tax Cut and Jobs Act ( TCJA ) signed December 22, 2017 TCJA included

Hiding in Plain View: Impact of Recent Tax Legislation on Retirement Plans Presented by Eric Paley and Claire Rowland March 14, 2018 Tax Cut and Jobs Act ( TCJA ) signed December 22, 2017 TCJA included

Summary Plan Description. Handbook and. For Employees of Southwest Research Institute PLAN RETIREMENT

RETIREMENT PLAN Handbook and Summary Plan Description For Employees of Southwest Research Institute Issued July 1, 2014 INTRODUCTION This Summary Plan Description (SPD) summarizes the important features

RETIREMENT PLAN Handbook and Summary Plan Description For Employees of Southwest Research Institute Issued July 1, 2014 INTRODUCTION This Summary Plan Description (SPD) summarizes the important features

THE BUSH FOUNDATION. Financial Statements. December 31, 2015 and (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) KPMG LLP 4200 Wells Fargo Center 90 South Seventh Street Minneapolis, MN 55402 Independent Auditors Report The Board of Directors The Bush

Financial Statements (With Independent Auditors Report Thereon) KPMG LLP 4200 Wells Fargo Center 90 South Seventh Street Minneapolis, MN 55402 Independent Auditors Report The Board of Directors The Bush

Agenda. Agency Oversight Types of correction programs. Documentation of Corrections

Agenda Agency Oversight Types of correction programs IRS - Employee Plans Compliance Resolution System (EPCRS) DOL - Voluntary Fiduciary Correction Program (VFCP) DOL - Delinquent Filers Voluntary Compliance

Agenda Agency Oversight Types of correction programs IRS - Employee Plans Compliance Resolution System (EPCRS) DOL - Voluntary Fiduciary Correction Program (VFCP) DOL - Delinquent Filers Voluntary Compliance

Overview and Introduction. Basic Audit Workshop. Discussion Leaders. Michael E. Auerbach Marilee P. Lau Employee Benefit Plan Audit Conference

2011 Employee Benefit Plan Audit Conference Basic Audit Workshop Maryland Association of CPAs Columbia, Maryland May 110, 2011 Discussion Leaders Michael E. Auerbach Marilee P. Lau 2 Overview and Introduction

2011 Employee Benefit Plan Audit Conference Basic Audit Workshop Maryland Association of CPAs Columbia, Maryland May 110, 2011 Discussion Leaders Michael E. Auerbach Marilee P. Lau 2 Overview and Introduction

Qualified Plan Terminations and Partial Plan Terminations

Qualified Plan Terminations and Partial Plan Terminations John P. Griffin, JD, LLM ASC Institute, LLC Introduction Recent IRS Guidance Agenda The Decision to Terminate a Plan Consequences of Plan Termination

Qualified Plan Terminations and Partial Plan Terminations John P. Griffin, JD, LLM ASC Institute, LLC Introduction Recent IRS Guidance Agenda The Decision to Terminate a Plan Consequences of Plan Termination

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans:

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: April 1, 2019 Deadline to notify us of deferrals over the 2018 calendar deferral limit.

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: April 1, 2019 Deadline to notify us of deferrals over the 2018 calendar deferral limit.

Overview of Defined Contribution Plan Design

Overview of Defined Contribution Plan Design September 6, 2016 Mutual of America Your Retirement Company Chris Conway Sr. Regional Vice President & Abbas Moloo Vice President MUTUAL OF AMERICA California

Overview of Defined Contribution Plan Design September 6, 2016 Mutual of America Your Retirement Company Chris Conway Sr. Regional Vice President & Abbas Moloo Vice President MUTUAL OF AMERICA California

DOL Survival Guide and Top Ten 401(k) Pitfalls

Pitfalls") DOL Survival Guide and Top Ten 401(k) Pitfalls Presented by CohnReznick s Government Contracting Industry Practice Sandy Wendler, Manager and Travis Dutton, Principal, Lockton Retirement Services PLEASE

DOL Survival Guide and Top Ten 401(k) Pitfalls Presented by CohnReznick s Government Contracting Industry Practice Sandy Wendler, Manager and Travis Dutton, Principal, Lockton Retirement Services PLEASE

Fair value measurement

Financial reporting developments A comprehensive guide Fair value measurement Revised October 2017 To our clients and other friends Fair value measurements and disclosures continue to be topics of interest

Financial reporting developments A comprehensive guide Fair value measurement Revised October 2017 To our clients and other friends Fair value measurements and disclosures continue to be topics of interest

TAG Frequently Asked Questions. Presented By: Susan M. Wright, CPA, APM

TAG Frequently Asked Questions Presented By: Susan M. Wright, CPA, APM About TAG Ability to ask retirement plan questions our TAG specialists have, on average, over 25 years of experience Searchable FAQ

TAG Frequently Asked Questions Presented By: Susan M. Wright, CPA, APM About TAG Ability to ask retirement plan questions our TAG specialists have, on average, over 25 years of experience Searchable FAQ

Test it, Find it, Fix it!

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Introductions Session format Questions 2 The Plan Document What We Test.

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Introductions Session format Questions 2 The Plan Document What We Test.

Introductions. Test it, Find it, Fix it! Session format Questions 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Session format Questions Introductions 2 1 The Plan Document What We

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Session format Questions Introductions 2 1 The Plan Document What We

The DOL and ESOPs. Best Practices for a DOL Audit

The DOL and ESOPs Best Practices for a DOL Audit 61152401 1 Patti J. Hedgpeth, Esq. Shareholder Polsinelli 2950 N Harwood Street Suite 2100 Dallas, TX 75201 Phone: (214) 661-5556 Mobile: (214) 923-0251

The DOL and ESOPs Best Practices for a DOL Audit 61152401 1 Patti J. Hedgpeth, Esq. Shareholder Polsinelli 2950 N Harwood Street Suite 2100 Dallas, TX 75201 Phone: (214) 661-5556 Mobile: (214) 923-0251

FORM 11-K. FIRST CASH 401(k) PROFIT SHARING PLAN

PROFIT SHARING PLAN") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K (Mark One): [ X ] ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K (Mark One): [ X ] ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

Learning from Recent Litigation and Enforcement Actions

Learning from Recent Litigation and Enforcement Actions Discussion and Worksheet for Retirement Advisors PlanAdvisorTools.com Learning from Recent Litigation and Enforcement Actions No employer wants to

Learning from Recent Litigation and Enforcement Actions Discussion and Worksheet for Retirement Advisors PlanAdvisorTools.com Learning from Recent Litigation and Enforcement Actions No employer wants to

YOU ARE AN ERISA FIDUCIARY, NOW WHAT?

YOU ARE AN ERISA FIDUCIARY, NOW WHAT? November 16, 2016 Rebecca E. Greene 414-298-8244 rgreene@reinhartlaw.com 1000 North Water Street, Suite 1700, Milwaukee, WI 53202 www.reinhartlaw.com Rebecca E. Greene

YOU ARE AN ERISA FIDUCIARY, NOW WHAT? November 16, 2016 Rebecca E. Greene 414-298-8244 rgreene@reinhartlaw.com 1000 North Water Street, Suite 1700, Milwaukee, WI 53202 www.reinhartlaw.com Rebecca E. Greene

Section 403(b): Final Regulations and Subsequent Guidance Update Overview and Action Plan. Healthcare Practice Retirement Plan Consulting

: Final Regulations and Subsequent Guidance Update Overview and Action Plan. Healthcare Practice Retirement Plan Consulting") Subsequent Guidance Update Healthcare Practice Retirement Plan Consulting Background On July 23, 2007, the Internal Revenue Service ( IRS ) issued final regulations regarding 403(b) plans. 1 These final

Subsequent Guidance Update Healthcare Practice Retirement Plan Consulting Background On July 23, 2007, the Internal Revenue Service ( IRS ) issued final regulations regarding 403(b) plans. 1 These final

ROSS STORES, INC. 401(K) SAVINGS PLAN SUMMARY PLAN DESCRIPTION

SAVINGS PLAN SUMMARY PLAN DESCRIPTION") ROSS STORES, INC. 401(K) SAVINGS PLAN SUMMARY PLAN DESCRIPTION January 2015 ROSS STORES, INC. 401(k) SAVINGS PLAN SUMMARY PLAN DESCRIPTION Section I. Introduction... 1 Section II. Questions and Answers

ROSS STORES, INC. 401(K) SAVINGS PLAN SUMMARY PLAN DESCRIPTION January 2015 ROSS STORES, INC. 401(k) SAVINGS PLAN SUMMARY PLAN DESCRIPTION Section I. Introduction... 1 Section II. Questions and Answers

401(k) PLANS. for Small Businesses

PLANS. for Small Businesses") 401(k) PLANS for Small Businesses 401(k) Plans for Small Businesses is a joint project of the U.S. Department of Labor s Employee Benefits Security Administration (EBSA) and the Internal Revenue Service.

401(k) PLANS for Small Businesses 401(k) Plans for Small Businesses is a joint project of the U.S. Department of Labor s Employee Benefits Security Administration (EBSA) and the Internal Revenue Service.