Exploring Islamic Banking Solutions for SMEs. Ahmed Ali Siddiqui & Mr. Suleman Muhammad Ali

|

|

|

- Jonas Richard

- 6 years ago

- Views:

Transcription

1 Exploring Islamic Banking Solutions for SMEs Ahmed Ali Siddiqui & Mr. Suleman Muhammad Ali

2 Presentation Outline Introduction to Islamic banking Overview of SME sector Financing needs of SMEs Islamic retail banking solutions for SME Short term Financing Needs Long term Financing Needs Trade Finance solutions Investment and liquidity management solutions SME focus approach

3 Strategic Direction for Islamic Banking Objectives of Islamic Banking Product Equitable Distribution & Circulation of Wealth in the society Avoid all Impermissible transactions Riba (Riba Al Nase ah / Riba Al Fadhl) Maysir / Gambling Gharar (Al Jahalah, Bai Qablal Qubz etc). Uqood-e-Fasida Promote participation based & asset Backed Financing Fulfilling halal Customer Needs Ensuring Shari a Compliance in all transactions

4 Islamic Banking What to offer NO Compromise on Shariah Compliance Products to fit all type of halal Customers need Easy of use Innovative & Value added Products Halal Returns for investment Halal & Riba Free Business solutions Create Awareness and educate

5 Shariah Framework Basic Permissibility & Prohibition: A solid foundation for a stable economic system

6 Guidelines for Commercial Dealings Allah (SWT) has ordained in Holy Quran Allah has permitted trade and prohibited Riba

Bai Qablal Qubz, Short sale, Future sale, Bai Dain /Sale of debt,sale of artificial instruments like derivatives/options etc Thus, Islamic banking system has a")

7 Prohibitions in Commercial Dealings 1. All type of Riba Riba Al Nase ah Riba Al Fadl 2. Maysir / Gambling 3. Gharar (transaction with uncertainty) Bai Qablal Qubz, Short sale, Future sale, Bai Dain /Sale of debt,sale of artificial instruments like derivatives/options etc Thus, Islamic banking system has a clear mandate to promote real economic activity by refraining from all prohibited transactions

8 Sources of Shariah 1. The Holy Qur an 2. The Sunnah of the Holy Prophet (SAW) 3. Ijma (consensus of the Ummah) 4. Qiyas (Anology)

9 Al Baqarah 275 Prohibition of Riba in the Qur an Those who devour Riba shall rise up before Allah like men whom Shaitan has demented by his touch; for they claim that trading is like Riba. But Allah has permitted trading and forbidden Riba. He that receives an admonition from his Rabb and mends his ways may keep what he has already earned; his faith is in the hand of Allah. But he that pays no heed shall be among the people of fire and shall remain in it forever. 9

10 Al Baqarah Prohibition of Riba in the Qur an O you who believe, Fear Allah and give up what remains of your demand for Interest, if you are indeed a believer. If you do not, then you are warned of the declaration of war from Allah and His Messenger; But if you turn back you shall have your principal: Deal not unjustly and you shall not be dealt with unjustly. 10

11 Prohibition of Riba in Ahadith From Hazrat Jabir Ibn-e-Abdullah (RA): The Prophet, peace be on him, cursed : The receiver and the payer of interest, The one who records it and The witnesses to the transaction And said: "They are all alike [in guilt]. (Muslim, Tirmidhi and Musnad Ahmad) 11

12 Definition of Riba Any debt that pull any kind of profit, that increase is Riba 12

13 Distinguishing Features We find the differences are on three levels: 1. Conceptual & Socio-religious level - not money lenders - cannot deal with interest & non permissible industries 2. Business model & Governing framework - IB actively participates in trade and production process - Governing framework in terms of Shariah Advisor &/or SSB 13

14 Distinguishing Features 3. Product Level Implementation - usually asset backed & involve trading/renting of asset & participation on profit & loss basis - Implementation is not just a mere change of paper work and terms but it involves - having the right intention, - the correct sequence of steps and timing of execution - clarity of roles 14

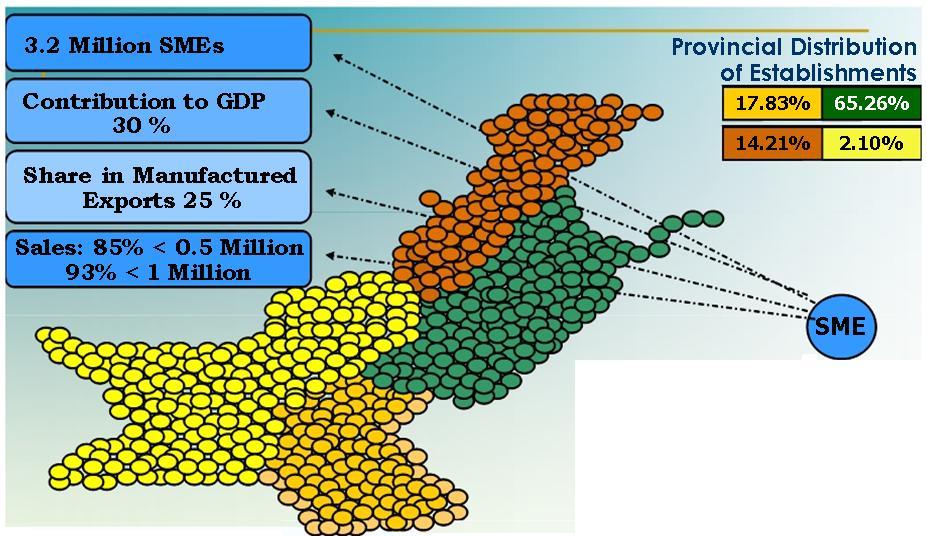

15 WHAT SME IS? In Pakistan, definition of SME varies from institution to institution. As per Prudential Regulations of SBP, SME is an entity which fulfills all the following characteristics. Total assets excluding land & building TRADING MANUFACTURING SERVICES Total no. of employees Sales 300 M 300 M 300 M

16 SMEs Contribution in Global Economy SME Contribution to Economic Development (%) Korea Japan China Pakistan Total Business GDP Employment Exports

17

18 Significance of SME Sector Growth For The Economy: Backbone of Economies: Significant contribution towards GDP (30%), Exports (25%), Improving the Balance of Payment situation, Boosting Industrialization Process Employment Generation, Poverty Alleviation, Reducing Income Inequality For The Banks: Diversification of Assets Portfolio Better Margins Potential Business Opportunity; Huge Target Market Low Loan Loss Ratio on Deposits.

19 IMPORTANCE OF SME (An untapped & misunderstood sector) Large Co s SME/COMM (Mass-market)

20 Challenges in SME Financing No Documentation- Free Style working behavior No Recording of transactions-verbal commitments No succession planning Less educated Avoid paying taxes No sharing of information Highly reliant on informal financing sources Informal financing cost is high but willing to bear to avoid documentation

21 Continued.. Not able to address their own process hindrances Limited exposure of broader spectrum of business Cursing External factors as the cause of their stagnant situation Non availability of problem solving skills No awareness of growth prospects (Local & International) No knowledge of SME products & services as it is a new concept

22 Financing Needs of SMEs Long Term Financing Needs Short Term Financing Needs Trade Finance Needs Investment and fund management needs

23 Islamic Banking Products Islamic banking now offers a complete range of Retail banking solutions for SME to cater their Financing & banking needs Financing Side modes - Murabaha Salam Istisna Tijarah Diminishing Musharakah Ijarah Mudarabah Musharakah

24 Focus on SME needs For Islamic Banking solution the center of focus is: Need of the Customer Business Cycle / Purchase Process of the customer Tenure of Financing required (Long or Short term) Rate of Financing (Fixed or Variable) Payment Flexibility (e.g. early termination)

25 Application of Mode Based on the criteria for selection of modes, the appropriate mode(s) is/(are) applied to fulfill the customer s need. Need Mode Selection Mode Application Example Murabaha Need: Raw material Tenure: 6 month Rate: Fixed Payment: At maturity

26 SMEs Sector Key points Over 230,000 entities Total revenue of over $1.2 billion Involved in wholesale trading, retailing, manufacturing, processing and services 30 per cent of the UAE's GDP, including the contribution from the oil sector. 70 to 80 per cent of UAE's non-oil GDP Still underserved by banking Higher demand for Islamic retail banking solutions

27 Short Term Financing Needs 1. Raw Material 2. Overheads / Utilities 3. Finished Goods 4. Trade receivable financing 5. Rental financing Islamic Banking solutions Murabaha - for working capital financing Salam/Istisna - for overheads, utilities & receivable Tijarah - for finished goods & receivables Lease & Sub Lease for rental financing

28 Long Term Financing Needs Acquisition/replacement/expansion of fixed assets, plant & machinery New Project Securitization Islamic Banking Solutions offered Ijarah Diminishing Musharakah Sukuk & syndicated project financing

29 Trade Finance Needs - Import Documentary Credits Sight LC / Usance LC Forward Cover Shipping Guarantees Islamic Banking Solutions offered Murabaha/Ijarah for retirement of sight LC Musawamah for Usance LC Wa ad for forward cover Kafalah for Shipping Guarantee

30 MURABAHA 30

31 Murabaha Murabaha is a particular kind of sale where the transaction is done on a cost plus profit basis i.e. the seller discloses the cost to the buyer and adds a certain profit to it to arrive at the final selling price. Payment of Murabaha price may be: 1) At spot 2) In installments 3) In lump sum after a certain time 31

32 Murabaha Do NOTs for Murabaha financing: Re-negotiation of price and roll over of Murabaha are not permitted. Discounting of Murabaha instrument is not permitted. 32

33 Murabaha Key features Underlying principle Tenure Rate Prepayment Discount Rescheduling of Price Uses Cost plus sales Short term - upto 1 year Fixed No No Purchase of Raw material/ Fixed asset 1. Payment of Cost 3. Payment of Murabaha price Supplier Bank Client 2. Delivery of goods

34 Step by step Murabaha financing 34

35 Murabaha 1. Client and bank sign an agreement to enter into Murabaha (MMFA). Bank Agreement to Murabaha Client 35

36 Murabaha 2. Client appointed as agent to purchase goods on bank s behalf Bank Agreement to Murabaha Agency Agreement Client 36

37 Murabaha 3. Bank gives money to agent/supplier for purchase of goods. Bank Agreement to Murabaha Agency Agreement Client Disbursement to the agent or supplier Supplier 37

38 Murabaha 4. The agent takes possession of goods on bank s behalf and provides Declaration. Transfer of Risk Vendor Delivery of goods Bank Agent 38

39 Murabaha 5(a). Client makes an offer to purchase the goods from bank through a Murabaha Contract Bank Client Offer to purchase 39

40 Murabaha 5(b). Bank accepts the offer and sale is concluded. Murabaha Contract + Transfer of Title Bank Client 40

41 Murabaha 6. Client pays agreed price to bank according to an agreed schedule. Usually on a deferred payment basis (Bai Muajjal) Bank Payment of Price Client 41

42 Murabaha Documentation There are a number of documents involved in a Murabaha financing transaction. The most essential of these documents are: Master Murabaha Financing Agreement Agency Agreement Order Form Declaration & Murabaha Contract Purchase Evidences Demand Promissory Note Payment Schedule 42

43 Issues in Murabaha 1. Timing of Offer & Acceptance 2. Rollover in Murabaha 3. Rebate on Early payment 4. Penalty in Late payment 5. Subject Matter 6. Purchase Evidence 7. Direct Payment 8. Profit recognition 9. Training of Customer & Bank staff 10. Process of Murabaha differ from product to products 43

44 ISTISNA 44

45 Istisna This product is an order to manufacture wherein; Customer will commit to manufacture/ provide specified items at a tentative date for IB. For this purpose IB will disburse the required financing amount in Customer s account. Funds may be used at the Customer s discretion. 45

46 Istisna Upon delivery of the specified items (Constructive possession through physical inspection), IB will appoint the Customer as its agent to sell the goods to its buyers. Customer will adjust the financing through the sale proceeds of the specified items. The Customer will ensure that in case of Credit Sales, goods are sold to Credible Buyers and will guarantee payments on due dates. 46

47 Istisna - features Underlying principle Tenure Rate Rescheduling of Price Uses Made to order Short Term Fixed Possible in some cases Order to manufacture goods/assets 1. Istisna a Agreement & payment 4. Sale Proceeds Customer Bank Buyer 2. Ultimate Delivery buyer of Goods as per schedule 3. Sale of Goods

48 Tijarah - features Underlying principle Tenure Rate Rescheduling of Price Uses Finished Good Purchase Short Term Fixed Agency incentive possible Finished good & receivable financing 1. Sale Agreement & payment 4. Sale Proceeds Customer Bank Buyer Ultimate 2. Immediate buyer Delivery of Goods 3. Sale of Goods

49 Salam - features Underlying principle Tenure Rate Rescheduling of Price Uses Advance payment purchase Short Term Fixed No Purchase of Agricultural/ Homogenous Comodities Customer 1. Payment of price 2. Goods delivery Bank 3. Goods delivery 3. Payment of price Market

50 Lease & Sub lease - features Underlying principle Tenure Rate Uses Operating Lease Short Term Fixed / variable Rental financing 1. Lease Agreement & upfront payment 4. Periodic Rental payments Landlord Bank Customer Ultimate 2. buyer Possession 3. Sub Lease

51 Long Term Financing Needs Acquisition/replacement/expansion of fixed assets, plant & machinery Islamic Banking solutions 1. Ijarah 2. Diminishing Musharakah

52 Long term Financing Needs Acquisition/replacement/expansion of fixed assets, plant & machinery Islamic Banking solutions: 1. Ijarah 2. Diminishing Musharakah 3. Sukuk

53 IJARAH

54 Ijarah Ijarah is a term of Islamic Fiqh Literally, it means To give something on rent The term Ijarah is used in two situations: 1. It means To employ the services of a person on wages e.g. A hires a porter at the airport to carry his luggage 2. Another type of Ijarah relates to paying rent for use of an asset or property defined as LAND in Islamic Economics

55 Ijarah as a mode of financing Ijarah is an Islamic alternative of Leasing. Leasing backed by an acceptable contract is an acceptable transaction under Shariah. The question of whether or not the transaction of leasing is Shariah compliant depends on the terms and conditions of the contract. Several characteristics of conventional agreements may not conform to Shariah thus making the transaction un-islamic and thereby invoking a prohibition.

56 Ijarah-Key Difference Risk and rewards of ownership lies with the owner i.e. any loss to the asset beyond the control of the lessee should be borne by the Lessor. Late payment penalty cannot be charged to the income of the Lessor. Rentals start after delivery of asset in workable/usable condition. Lease and Sale agreement should be separate and non contingent.

57 Process of Ijarah

58 Ijarah MECHANICS VENDOR ISLAMIC.. BANK Agreement-1 CUSTOMER The customer approaches the Bank with the request for financing and enters into a promise to lease agreement. The Bank purchases the item required for leasing and receives title of ownership from the vendor The Bank makes payment to the vendor

59 MECHANICS VENDOR Ijarah as a mode of financing ISLAMIC BANK Agreement-2.. CUSTOMER The Bank leases the asset to the customer after execution of lease agreement. The customer makes periodic payments as per the contract At the end the Title can be transferred to the customer via separate Sale agreement.

60 IJARAH Tenure Rate Early Termination Uses Long Term Fixed / Variable Yes Fixed Assets Financing VENDOR ISLAMIC BANK CUSTOMER

61 Ijarah Documentation

62 Ijarah Documentation Undertaking to Ijarah Ijarah Agreement Description of the Ijarah Asset Schedule of of Ijarah Rentals Receipt of Asset Demand Promissory Note Undertaking to Purchase Ijarah Asset Sale Deed

63 Ijarah Documentation Letter of Agency Undertaking to Lease Lease Agreement Undertaking to Purchase Sale Deed

64 Diminishing Musharakah-Introduction

65 Diminishing Musharakah- In Diminishing Musharakah the financier and the client participate either in joint ownership of a property or an equipment, or in a joint commercial enterprise The share of the financier will be divided into a number of units The client will purchase these units one by one periodically until he is the sole owner of the property

66 Diminishing Musharakah- However generally Diminishing Musharakah is used in cases of Shirkat-ul-Milk It involves taking share in the ownership of a specific asset and then gradually transferring complete ownership to the other partner. This concept is based on Declining ownership of the financier Three components Joint ownership of the Bank and customer Customer as a lessee uses the share of the bank Redemption of the share of the Bank by the customer

67 Diminishing Musharakah- Concept of Musha Musha means undivided ownership of the asset Lease of Musha It is allowed to lease Musha to other joint owner.

68 Basic Structure

69 BANK Joint Ownership Rent Musharaka CUSTOMER The customer approaches the Bank with the request for Project/Machinery/House financing The Bank enters into a Musharakah (Joint Ownership) agreement with the customer and both of them pay their respective shares to the seller of the asset. Customer pays rent for the use of banks share in the property

70 BANK Joint Ownership Gradual Transfer of Ownership Musharaka CUSTOMER The customer approaches the Bank with the request for Project/Machinery financing The Bank enters into a Musharakah (Joint Ownership) agreement with the customer and both of them pay their respective shares to the seller of the asset. Customer pays rent for the use of banks share in the property Ownership of the asset is gradually transferred to the customer upon payment of asset price. (with the help of a Sale transaction between bank & customer at the end of each period)

71 Shariah Principles

72 Shariah Principles To create joint ownership in property is called is Shirkat-ul-Milk and is expressly allowed by all schools of Islamic Jurisprudence. All Muslim Jurists agree on the permissibility of the Financier leasing his share in property to client and charging him rent i.e. the permissibility of leasing one s share to his partner. There is difference of opinion among leasing one s share to a third part But there is no difference on permissibility on leasing to a partner.

73 Shariah Principles Promise of client to purchase units of share of financier is also allowed. The Transactions cannot be combined in a single arrangements and they have to be executed independently. This is because it is a well settled rule of Islamic Jurisprudence that one transaction cannot be made a condition for another. Instead of making the transactions a precondition for one another there can be one-sided promises from one party to another

74 Shariah Principles Argument: In the case of promise to sell units of share by financier one might argue that if the promise to sale has been done before entering into actual sale This is practically putting a condition on the sale itself Answer: There is a difference between: Putting a condition on a sale and making a separate promise, without making it a condition. In case of condition, the sale will be valid only if the condition is fulfilled.

75 Diminishing Assets Musharakah Tenure Rate Early Termination Uses Long Term Fixed / Variable Yes Fixed Assets Financing BANK Joint Ownership Rent Gradual Transfer of Ownership Musharaka CUSTOMER

76 Trade Finance Needs - Import 1. Documentary Credits a. Sight LC / Usance LC 2. Forward Cover 3. Shipping Guarantees Possible Solutions Murabaha/Ijarah for retirement of sight LC Musawamah for Usance LC Wa ad for forward cover Kafalah for Shipping Guarantee

77 Trade Finance Needs - Export 1. Alternative to Export Bill Discounting 2. Islamic Export Refinance Scheme Possible Solutions Murabaha/Istisna Islamic Export Refinance Murabaha/Tijara for Alternate to Export Bill Discounting

78 SME focused banking Fast track services & Special service counters Score card & program based approach for fast approval of financing Cash Collection service from customers locations Extended online services. e.g, issuance of PO from online services Dedicated Shariah Advisory Desks at Islamic Banks Key challenges (documentation, security)

79 Thank you

Exploring Islamic Retail Banking Solutions for SMEs

Exploring Islamic Retail Banking Solutions for SMEs Ahmed Ali Siddiqui Executive Vice President Product Development, Shariah Compliance & Financial Advisory International Islamic Finance Forum May 19,

Exploring Islamic Retail Banking Solutions for SMEs Ahmed Ali Siddiqui Executive Vice President Product Development, Shariah Compliance & Financial Advisory International Islamic Finance Forum May 19,

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES. MEHOL K. SADAIN Commissioner NCMF February 9, 2015

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES MEHOL K. SADAIN Commissioner NCMF February 9, 2015 Definition of Terms Finance is the science or study of management of funds; the system that includes

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES MEHOL K. SADAIN Commissioner NCMF February 9, 2015 Definition of Terms Finance is the science or study of management of funds; the system that includes

Murabaha is one of the most commonly used modes of financing by Islamic banks and financial institutions.

16. MURABAHA Murabaha is one of the most commonly used modes of financing by Islamic banks and financial institutions. Definition Murabaha is a particular kind of sale where the seller expressly mentions

16. MURABAHA Murabaha is one of the most commonly used modes of financing by Islamic banks and financial institutions. Definition Murabaha is a particular kind of sale where the seller expressly mentions

This is the 3 rd of 4 series on the topic Islamic Banking Interest-Free Banking. Read the 1 st, 2 nd and 4 th of the series

This is the 3 rd of 4 series on the topic Islamic Banking Interest-Free Banking Read the 1 st, 2 nd and 4 th of the series 1 / 10 The universal functions of all financial systems are the same, differences

This is the 3 rd of 4 series on the topic Islamic Banking Interest-Free Banking Read the 1 st, 2 nd and 4 th of the series 1 / 10 The universal functions of all financial systems are the same, differences

MURABAHA Definition Of Murabaha What is a Murabaha? A Murabaha is a sale transaction where the cost of acquiring the asset and the profit to be added are disclosed to the client. The buying client typically

MURABAHA Definition Of Murabaha What is a Murabaha? A Murabaha is a sale transaction where the cost of acquiring the asset and the profit to be added are disclosed to the client. The buying client typically

Glossary of Islamic Capital Market Terms

Glossary of Islamic Capital Market Terms Terms Definition Bai` Bithaman Ajil (BBA) Bai` al-`inah Bai` al-istijrar A contract that refers to the sale and purchase transaction for the financing of assets

Glossary of Islamic Capital Market Terms Terms Definition Bai` Bithaman Ajil (BBA) Bai` al-`inah Bai` al-istijrar A contract that refers to the sale and purchase transaction for the financing of assets

Fixed Income Securities Shari a Perspective

SBP Research Bulletin Volume 3, Number 1, 2007 Fixed Income Securities Shari a Perspective Muhammad Imran Usmani 1. Introduction Fixed income securities have been popular around the world in raising finance

SBP Research Bulletin Volume 3, Number 1, 2007 Fixed Income Securities Shari a Perspective Muhammad Imran Usmani 1. Introduction Fixed income securities have been popular around the world in raising finance

Shari ah Standard No. (44) Obtaining and Deploying Liquidity

Obtaining and Deploying Liquidity") Shari ah Standard No. (44) Obtaining and Deploying Liquidity Contents Subject Page Preface... 1087 Statement of the Standard... 1088 1. Scope of the Standard... 1088... 1088 3. Need to Utilise Liquidity

Shari ah Standard No. (44) Obtaining and Deploying Liquidity Contents Subject Page Preface... 1087 Statement of the Standard... 1088 1. Scope of the Standard... 1088... 1088 3. Need to Utilise Liquidity

Presentation Outline Copyright Bank Nizwa. All Rights Reserved. 2

Presentation Outline Real Economy VS Capitalism PREAMBLE Overview of Islamic Finance Section 1 Islamic Banks VS Conventional Banks Section 2 A Glimpse Into Islamic Finance Products and Services Section

Presentation Outline Real Economy VS Capitalism PREAMBLE Overview of Islamic Finance Section 1 Islamic Banks VS Conventional Banks Section 2 A Glimpse Into Islamic Finance Products and Services Section

Islamic Project Finance and Infrastructure Funding in Thailand Key Concepts and Structures. Stephen Jaggs 23 November 2012

Islamic Project Finance and Infrastructure Funding in Thailand Key Concepts and Structures Stephen Jaggs 23 November 2012 Allen & Overy 2012 BN:1932301.1 1 Religious Principles and Background Body of Islamic

Islamic Project Finance and Infrastructure Funding in Thailand Key Concepts and Structures Stephen Jaggs 23 November 2012 Allen & Overy 2012 BN:1932301.1 1 Religious Principles and Background Body of Islamic

Introduction to Islamic Banking. Salman Ahmed Shaikh

Introduction to Islamic Banking Salman Ahmed Shaikh islamiceconomicsproject@gmail.com www.islamiceconomicsproject.wordpress.com HISTORY OF ISLAMIC BANKING Islamic banking and the field of Islamic finance

Introduction to Islamic Banking Salman Ahmed Shaikh islamiceconomicsproject@gmail.com www.islamiceconomicsproject.wordpress.com HISTORY OF ISLAMIC BANKING Islamic banking and the field of Islamic finance

Islamic Finance: Hedging Instruments and Structured Products. Dr Ken Baldwin Islamic Development Bank 27 th January 2014

Islamic Finance: Hedging Instruments and Structured Products Dr Ken Baldwin Islamic Development Bank 27 th January 2014 Religious Context Islamic financial institutions offer products consistent with Islamic

Islamic Finance: Hedging Instruments and Structured Products Dr Ken Baldwin Islamic Development Bank 27 th January 2014 Religious Context Islamic financial institutions offer products consistent with Islamic

Q: What types of Financial Institutions and transactions are involved in Islamic finance?

Q: What is Islamic Finance Islamic finance is an interest free finance system. There is therefore, no charge for its use. Islamic finance is asset based as opposed to being currency based. A deal is structured

Q: What is Islamic Finance Islamic finance is an interest free finance system. There is therefore, no charge for its use. Islamic finance is asset based as opposed to being currency based. A deal is structured

Basic Islamic Finance and Islamic Contracts

BASIC ISLAMIC FINANCE AND ISLAMIC CONTRACTS Basic Islamic Finance and Islamic Contracts PUBLISHED BY: AL ALAWI & CO., ADVOCATES & LEGAL CONSULTANTS BANKING & FINANCE GROUP In today s day and age, banking

BASIC ISLAMIC FINANCE AND ISLAMIC CONTRACTS Basic Islamic Finance and Islamic Contracts PUBLISHED BY: AL ALAWI & CO., ADVOCATES & LEGAL CONSULTANTS BANKING & FINANCE GROUP In today s day and age, banking

Primer on Shariah Finance

INTERNATIONAL INSOLVENCY INSTITUTE 7 th Annual Conference Primer on Shariah Finance New York, NY June 11-12, 2007 Jonathan D. Strum, Esq. Primer on Shariah Finance Shariah is the legal framework that regulates

INTERNATIONAL INSOLVENCY INSTITUTE 7 th Annual Conference Primer on Shariah Finance New York, NY June 11-12, 2007 Jonathan D. Strum, Esq. Primer on Shariah Finance Shariah is the legal framework that regulates

SME FINANCING INTRODUCTION

SME FINANCING INTRODUCTION Small & Medium Enterprises (SMEs) sector contributes significantly towards national GDP, employment generation and export earnings. Hence, the impact of financial inclusion of

SME FINANCING INTRODUCTION Small & Medium Enterprises (SMEs) sector contributes significantly towards national GDP, employment generation and export earnings. Hence, the impact of financial inclusion of

Musharaka. The term Musharaka has been derived from the Islamic fiqh concept of Shirkah which means sharing or partnership.

Musharaka The term Musharaka has been derived from the Islamic fiqh concept of Shirkah which means sharing or partnership. 1.Shirkat-ul-Milk: means joint ownership between two or more persons or parties

Musharaka The term Musharaka has been derived from the Islamic fiqh concept of Shirkah which means sharing or partnership. 1.Shirkat-ul-Milk: means joint ownership between two or more persons or parties

Risk Management in Islamic Financial Institutions

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY TWO Risk in Sharia Jurisprudence and Sharia Mechanism in Risk Management RISK IN SHARIA

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY TWO Risk in Sharia Jurisprudence and Sharia Mechanism in Risk Management RISK IN SHARIA

Whereas, Murabaha is considered as one of the acceptable financing modes under precepts of Islam.

Regulations Governing Shari ah Compliant Trading Platform For Murabaha These Regulations may be called the Regulations Governing Shari ah Compliant Trading Platform for Murabaha (the Regulations ) at Pakistan

Regulations Governing Shari ah Compliant Trading Platform For Murabaha These Regulations may be called the Regulations Governing Shari ah Compliant Trading Platform for Murabaha (the Regulations ) at Pakistan

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

Shariah Guidelines for Sukuk. Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

Islamic Finance More Than Window Dressing?

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Financing Products and Concepts, Current Market Trends and Opportunities. Nadim Khan, Partner, Herbert Smith LLP July 2010

Islamic Financing Products and Concepts, Current Market Trends and Opportunities Nadim Khan, Partner, Herbert Smith LLP July 2010 1 Overview Introduction to Islamic Finance The Key Products The Compliance

Islamic Financing Products and Concepts, Current Market Trends and Opportunities Nadim Khan, Partner, Herbert Smith LLP July 2010 1 Overview Introduction to Islamic Finance The Key Products The Compliance

Demystifying the Enigma of Commodity & Equity Swaps. November 2018 SHARIA ADVISOR LICENSED BY THE CENTRAL BANK OF BAHRAIN

Demystifying the Enigma of Commodity & Equity Swaps November 2018 SHARIA ADVISOR LICENSED BY THE CENTRAL BANK OF BAHRAIN 2 Introduction A financial swap takes place when two parties exchange financial

Demystifying the Enigma of Commodity & Equity Swaps November 2018 SHARIA ADVISOR LICENSED BY THE CENTRAL BANK OF BAHRAIN 2 Introduction A financial swap takes place when two parties exchange financial

Introduction to Islamic Investing. For professional clients only

Introduction to Islamic Investing For professional clients only 2 Overview Assets of Islamic financial institutions have grown by an average of 15% per annum* over the past five years to reach over $1trillion

Introduction to Islamic Investing For professional clients only 2 Overview Assets of Islamic financial institutions have grown by an average of 15% per annum* over the past five years to reach over $1trillion

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view 1 O M A R M U S T A F A A N S A R I A S S I S T A N T S E C R E T A R Y G E N E R A L A C C O U N T I N

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view 1 O M A R M U S T A F A A N S A R I A S S I S T A N T S E C R E T A R Y G E N E R A L A C C O U N T I N

Developing Islamic Finance Secondary Markets

Developing Islamic Finance Secondary Markets By Ahmed Ali Siddiqui Vice President & Manager, Product Development & Shariah Compliance (PDSC) Meezan Bank Limited 2 nd IIFM Conference - June 18, 2007 Islamic

Developing Islamic Finance Secondary Markets By Ahmed Ali Siddiqui Vice President & Manager, Product Development & Shariah Compliance (PDSC) Meezan Bank Limited 2 nd IIFM Conference - June 18, 2007 Islamic

The Guide to Islamic Economics, Banking, and Finance

MPRA Munich Personal RePEc Archive The Guide to Islamic Economics, Banking, and Finance Nidal Alsayyed INCEIF the Global University in Islamic Finance, International Islamic University Malaysia 11. December

MPRA Munich Personal RePEc Archive The Guide to Islamic Economics, Banking, and Finance Nidal Alsayyed INCEIF the Global University in Islamic Finance, International Islamic University Malaysia 11. December

CIFE STUDY NOTES

CIFE STUDY NOTES ABOUT ETHICA DOWNLOAD BROCHURE HERE >> About Ethica Institute of Islamic Finance About Ethica Institute of Islamic Finance About the Certified Islamic Finance Executive (CIFE ) About

CIFE STUDY NOTES ABOUT ETHICA DOWNLOAD BROCHURE HERE >> About Ethica Institute of Islamic Finance About Ethica Institute of Islamic Finance About the Certified Islamic Finance Executive (CIFE ) About

Economic and Social Council

United Nations E/C.18/2007/9 Economic and Social Council Distr.: General 21 August 2007 Original: English Committee of Experts on International Cooperation in Tax Matters Third session Geneva, 29 October-2

United Nations E/C.18/2007/9 Economic and Social Council Distr.: General 21 August 2007 Original: English Committee of Experts on International Cooperation in Tax Matters Third session Geneva, 29 October-2

SA ADAT BAI SALAM. (Islamic Alternate for Export Sight Bill Discounting) PRODUCT MANUAL MARCH, 2014

PRODUCT MANUAL MARCH, 2014") SA ADAT BAI SALAM (Islamic Alternate for Export Sight Bill Discounting) PRODUCT MANUAL MARCH, 2014 ISLAMIC BANKING DIVISION SINDH BANK LIMITED HEAD OFFICE Page 1 of 20 Table of Contents I. Bai Salam (Islamic

SA ADAT BAI SALAM (Islamic Alternate for Export Sight Bill Discounting) PRODUCT MANUAL MARCH, 2014 ISLAMIC BANKING DIVISION SINDH BANK LIMITED HEAD OFFICE Page 1 of 20 Table of Contents I. Bai Salam (Islamic

Fiqh or Fiction By Atif Khan Islamica Magazine - Summer / Fall 2004

Fiqh or Fiction By Atif Khan Islamica Magazine - Summer / Fall 2004 Is Islamic Banking Truly Islamic, or is it just cosmetically enhanced conventional banking? Islamic bankers, caught between scholars

Fiqh or Fiction By Atif Khan Islamica Magazine - Summer / Fall 2004 Is Islamic Banking Truly Islamic, or is it just cosmetically enhanced conventional banking? Islamic bankers, caught between scholars

This Structure Memorandum has been approved by IIFM Shari'ah Board on 25 October 2018.

STRUCTURE MEMORANDUM IIFM-BAFT MASTER UNFUNDED & FUNDED PARTICIPATION AGREEMENTS FOR TRADE FINANCE TRANSACTIONS مذرة هيكل اتفاق'ة م شاركة ري #سة م م و و ير م م و لمعاملات اتمويل التاري This Structure Memorandum

STRUCTURE MEMORANDUM IIFM-BAFT MASTER UNFUNDED & FUNDED PARTICIPATION AGREEMENTS FOR TRADE FINANCE TRANSACTIONS مذرة هيكل اتفاق'ة م شاركة ري #سة م م و و ير م م و لمعاملات اتمويل التاري This Structure Memorandum

SHARIAH COMPLIANCE MECHANISM

Sindh Bank Ltd SHARIAH COMPLIANCE MECHANISM March 2014 ISLAMIC BANKING DIVISION Page 0 of 60 A-POLICY FRAMEWORK OVERVIEW Sindh Bank Ltd (SNDBL)-Islamic Banking (IB) is committed towards Shariah Compliance

Sindh Bank Ltd SHARIAH COMPLIANCE MECHANISM March 2014 ISLAMIC BANKING DIVISION Page 0 of 60 A-POLICY FRAMEWORK OVERVIEW Sindh Bank Ltd (SNDBL)-Islamic Banking (IB) is committed towards Shariah Compliance

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

Tax Treatment of Islamic Financial Transactions

Tax Treatment of Islamic Financial Transactions This document should be read in conjunction with Part 8A Taxes Consolidation Act 1997 Document created November 2018. 1 Table of Contents 1 Introduction

Tax Treatment of Islamic Financial Transactions This document should be read in conjunction with Part 8A Taxes Consolidation Act 1997 Document created November 2018. 1 Table of Contents 1 Introduction

Islamic Finance and Banking: Modes of Finance

Islamic Finance and Banking: Modes of Finance Power point and Assessments Khalifa M Ali Hassanain Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this

Islamic Finance and Banking: Modes of Finance Power point and Assessments Khalifa M Ali Hassanain Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this

Sukuks. Bin Shabib & Associates (BSA) LLP. 1. Legal and Regulatory Issues: a. Introduction. Overview of the Sukuk Market

LLP. 1. Legal and Regulatory Issues: a. Introduction. Overview of the Sukuk Market") Bin Shabib & Associates (BSA) LLP Sukuks 1. Legal and Regulatory Issues: a. Introduction Overview of the Sukuk Market In a growing Islamic Finance market, it is essential to continually strengthen the

Bin Shabib & Associates (BSA) LLP Sukuks 1. Legal and Regulatory Issues: a. Introduction Overview of the Sukuk Market In a growing Islamic Finance market, it is essential to continually strengthen the

The Third Annual Conference of Islamic Economics & Islamic Finance. Venue: Chestnut Conference Center Date: October 29 th, 2016

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center Date: October 29 th, 2016 Organized by: ECO-ENA, Inc., Canada Presenter Ahmad Wais Popalyar VP Business

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center Date: October 29 th, 2016 Organized by: ECO-ENA, Inc., Canada Presenter Ahmad Wais Popalyar VP Business

EXCEPTIONAL SALES: SALAM AND ISTISNA'

EXCEPTIONAL SALES: SALAM AND ISTISNA' Murabaha and ijara constitute the core financing activities of Islamic banks. They are easily understood because of their proximity to conventional financing techniques,

EXCEPTIONAL SALES: SALAM AND ISTISNA' Murabaha and ijara constitute the core financing activities of Islamic banks. They are easily understood because of their proximity to conventional financing techniques,

Musharakah Mutanaqisah Home Financing: Shari ah Issues, Financial Implications and Accounting Considerations. INCEIF, Kuala Lumpur, Malaysia.

Musharakah Mutanaqisah Home Financing: Shari ah Issues, Financial Implications and Accounting Considerations Alam Asadov, Zaheer Anwer, Shinaj V. Shamsudheen 1 & Zulkarnain Muhamad Sori (PhD) 2 INCEIF,

Musharakah Mutanaqisah Home Financing: Shari ah Issues, Financial Implications and Accounting Considerations Alam Asadov, Zaheer Anwer, Shinaj V. Shamsudheen 1 & Zulkarnain Muhamad Sori (PhD) 2 INCEIF,

Alternative financing structures for the aviation industry

Alternative financing structures for the aviation industry Gregory Man Partner and Head of Debt Capital Markets (Middle East) Norton Rose Fulbright (Middle East) LLP October 4, 2016 Agenda Introduction

Alternative financing structures for the aviation industry Gregory Man Partner and Head of Debt Capital Markets (Middle East) Norton Rose Fulbright (Middle East) LLP October 4, 2016 Agenda Introduction

Takaful. Dr. Muhammad Imran Usmani. SECP Takaful Conference March 14, 2007

Takaful Dr. Muhammad Imran Usmani SECP Takaful Conference March 14, 2007 Presentation Outline Conventional Insurance How Qimar & Riba exist in Conventional Insurance Definition of Takaful Mudarabah Model

Takaful Dr. Muhammad Imran Usmani SECP Takaful Conference March 14, 2007 Presentation Outline Conventional Insurance How Qimar & Riba exist in Conventional Insurance Definition of Takaful Mudarabah Model

DUBAI ISLAMIC BANK PAKISTAN LIMITED BALANCE SHEET AS AT DECEMBER 31, 2009

BALANCE SHEET AS AT DECEMBER 31, 2009 Note ASSETS Cash and balances with treasury banks 8 2,932,264 2,691,572 Balances with other banks 9 2,430,437 3,273,878 Due from financial institutions 10 2,591,905

BALANCE SHEET AS AT DECEMBER 31, 2009 Note ASSETS Cash and balances with treasury banks 8 2,932,264 2,691,572 Balances with other banks 9 2,430,437 3,273,878 Due from financial institutions 10 2,591,905

Islamic Banking vs. Conventional Banking

Islamic Banking vs. Conventional Banking [Client Name] [Institute Name] ISLAMIC BANKING VS. CONVENTIONAL BANKING 2 Table of Contents Executive Summary... 5 Importance of the Research... 6 Introduction

Islamic Banking vs. Conventional Banking [Client Name] [Institute Name] ISLAMIC BANKING VS. CONVENTIONAL BANKING 2 Table of Contents Executive Summary... 5 Importance of the Research... 6 Introduction

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

INTEREST FREE BANKING-COMPLEMENT FOR INDIAN ECONOMY

INTEREST FREE BANKING-COMPLEMENT FOR INDIAN ECONOMY Author Name: Sameera Afroze Affiliation: Assistant Professor, Aristotle PG College Paper Title: Interest Free banking, complement for Indian Economy

INTEREST FREE BANKING-COMPLEMENT FOR INDIAN ECONOMY Author Name: Sameera Afroze Affiliation: Assistant Professor, Aristotle PG College Paper Title: Interest Free banking, complement for Indian Economy

Running Musharakah Product of Islamic Banks: An Alternative of Running Finance

Al-Idah 33 (Dec.,. 2016) Running Musharakah Product of Islamic Banks: 8 Running Musharakah Product of Islamic Banks: An Alternative of Running Finance Dr. Muhammad Mushtaq Ahmed Dr. Muhammad Farooq Muhammad

Al-Idah 33 (Dec.,. 2016) Running Musharakah Product of Islamic Banks: 8 Running Musharakah Product of Islamic Banks: An Alternative of Running Finance Dr. Muhammad Mushtaq Ahmed Dr. Muhammad Farooq Muhammad

Content. n Why? n Objectives. n Shariah Standards issued by BNM. n AAOIFI Shariah Standards

Shariah Standards 1 Content n Why? n Objectives n Shariah Standards issued by BNM n AAOIFI Shariah Standards Why? n Differences in interpreting Shari ah has led to a diverse legal and regulatory landscape

Shariah Standards 1 Content n Why? n Objectives n Shariah Standards issued by BNM n AAOIFI Shariah Standards Why? n Differences in interpreting Shari ah has led to a diverse legal and regulatory landscape

Tatagroprombank. Talk on Islamic Finance. Kazan -17 June Alberto G. Brugnoni - ASSAIF

Tatagroprombank Talk on Islamic Finance Kazan -17 June 2013 Alberto G. Brugnoni - ASSAIF CONTENTS OF THE TALK WHAT IS ISLAMIC FINANCE ISLAMIC MODES OF FINANCE AVAILABLE TO SMEs ISLAMIC TRADE FINANCE ISLAMIC

Tatagroprombank Talk on Islamic Finance Kazan -17 June 2013 Alberto G. Brugnoni - ASSAIF CONTENTS OF THE TALK WHAT IS ISLAMIC FINANCE ISLAMIC MODES OF FINANCE AVAILABLE TO SMEs ISLAMIC TRADE FINANCE ISLAMIC

Accounting, Auditing & Corporate Governance Standards for Islamic Banks & Islamic Financial Institutions with reference to AAOIFI

Accounting, Auditing & Corporate Governance Standards for Islamic Banks & Islamic Financial Institutions with reference to AAOIFI About AAOIFI The Accounting and Auditing Organization for Islamic Financial

Accounting, Auditing & Corporate Governance Standards for Islamic Banks & Islamic Financial Institutions with reference to AAOIFI About AAOIFI The Accounting and Auditing Organization for Islamic Financial

Operational models for Ijarah, Istisna, and Murabaha sukuk from Islamic point of view 1 Syed abbas musavian 2

Operational models for Ijarah, Istisna, and Murabaha sukuk from Islamic point of view 1 Syed abbas musavian 2 Mostafa Zehtabian 3 Abstract The absence of bonds in the capital market and the capability

Operational models for Ijarah, Istisna, and Murabaha sukuk from Islamic point of view 1 Syed abbas musavian 2 Mostafa Zehtabian 3 Abstract The absence of bonds in the capital market and the capability

Read the following and answer questions 2 and 3.

1. Which of the following is true? a) The credit balance of Hamish Jiddiyyah is presented in the asset side of the statement of financial position. b) Istisna receivables are presented within the investments.

1. Which of the following is true? a) The credit balance of Hamish Jiddiyyah is presented in the asset side of the statement of financial position. b) Istisna receivables are presented within the investments.

As economies continue to seek private sector participation for developing infrastructure projects,

United Arab Emirates A promising future Masood Khan Afridi of Afridi & Angell compares Islamic and conventional project financing, and explains why careful documentation is so important As economies continue

United Arab Emirates A promising future Masood Khan Afridi of Afridi & Angell compares Islamic and conventional project financing, and explains why careful documentation is so important As economies continue

Tax Planning Retirement Planning Wills & Inheritance Tax Mortgage Advice Investments & Savings Zakat

PROVIDING SOUND FINANCIAL ADVICE FOR YOU AND YOUR FAMILIES FUTURE Tax Planning Retirement Planning Wills & Inheritance Tax Mortgage Advice Investments & Savings Zakat THE UK S PREMIER PROVIDER OF HALAL

PROVIDING SOUND FINANCIAL ADVICE FOR YOU AND YOUR FAMILIES FUTURE Tax Planning Retirement Planning Wills & Inheritance Tax Mortgage Advice Investments & Savings Zakat THE UK S PREMIER PROVIDER OF HALAL

Glossary Of Islamic Finance Terms

January 7, 2008 Glossary Of Islamic Finance Terms Primary Credit Analyst: Mohamed Damak, Paris (33) 1-4420-7322; mohamed_damak@standardandpoors.com Table Of Contents The Five Pillars Of Islamic Finance

January 7, 2008 Glossary Of Islamic Finance Terms Primary Credit Analyst: Mohamed Damak, Paris (33) 1-4420-7322; mohamed_damak@standardandpoors.com Table Of Contents The Five Pillars Of Islamic Finance

Session IV. Other Islamic Finance Instruments

Session IV Other Islamic Finance Instruments Islamic Derivatives Derivatives have invoked mixed response from the Shariah scholars whose tendency in holding them as prohibited due to the violation of basic

Session IV Other Islamic Finance Instruments Islamic Derivatives Derivatives have invoked mixed response from the Shariah scholars whose tendency in holding them as prohibited due to the violation of basic

International Trade under Islamic Banking

International Trade under Islamic Banking Muhammad Bilal University of Sargodha Sub-campus Mianwali, Pakistan Abstract The crucial area of this study is to identify the international trade under Islamic

International Trade under Islamic Banking Muhammad Bilal University of Sargodha Sub-campus Mianwali, Pakistan Abstract The crucial area of this study is to identify the international trade under Islamic

Financial Inclusiveness in Islamic Banking: Comparison of Ideals and Practices Based on Maqasid-e-Shari ah

Financial Inclusiveness in Islamic Banking: Comparison of Ideals and Practices Based on Maqasid-e-Shari ah A B D U L G H A F A R I S M A I L M O H D A D I B I S M A I L S H A H I D A S H A H I M I S A

Financial Inclusiveness in Islamic Banking: Comparison of Ideals and Practices Based on Maqasid-e-Shari ah A B D U L G H A F A R I S M A I L M O H D A D I B I S M A I L S H A H I D A S H A H I M I S A

Murabaha Accounting. Murabaha is a dominant source of retail banking under Islamic financial system. Muhammad Hanif

Murabaha Accounting Murabaha is a dominant source of retail banking under Islamic financial system Muhammad Hanif Assistant Professor FAST School of Management National University of Computer & Emerging

Murabaha Accounting Murabaha is a dominant source of retail banking under Islamic financial system Muhammad Hanif Assistant Professor FAST School of Management National University of Computer & Emerging

ISLAMIC HEDGING MECHANISM: EMERGING TREND

ISLAMIC HEDGING MECHANISM: EMERGING TREND Dr. Mohd Daud Bakar President/CEO International Institute of Islamic Finance (IIIF) Inc. mdaud@iiif-inc.com www.iiif-inc.com Shariah Perspective on Economics of

ISLAMIC HEDGING MECHANISM: EMERGING TREND Dr. Mohd Daud Bakar President/CEO International Institute of Islamic Finance (IIIF) Inc. mdaud@iiif-inc.com www.iiif-inc.com Shariah Perspective on Economics of

SALAM. Chapter 14. Purpose of use:

Chapter 14 SALAM In Salam, the seller undertakes to supply specific goods to the buyer at a future date in exchange of an advanced price fully paid at spot. The payment is at spot but the supply of purchased

Chapter 14 SALAM In Salam, the seller undertakes to supply specific goods to the buyer at a future date in exchange of an advanced price fully paid at spot. The payment is at spot but the supply of purchased

Islamic Finance and Capital Markets: Sukuk Structure and Trading. Power point and Assessments

Islamic Finance and Capital Markets: Sukuk Structure and Trading Power point and Assessments Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work

Islamic Finance and Capital Markets: Sukuk Structure and Trading Power point and Assessments Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work

Sukuk Structures, Profiles and Risks

Sukuk Structures, Profiles and Risks Mona R. El Shazly, Columbia College Pragya Tripathy, Columbia College ABSTRACT Sukuk are financial instruments similar to bonds that are compliant with Islamic Shari

Sukuk Structures, Profiles and Risks Mona R. El Shazly, Columbia College Pragya Tripathy, Columbia College ABSTRACT Sukuk are financial instruments similar to bonds that are compliant with Islamic Shari

PRINCIPLES OF TAKAFUL

PRINCIPLES OF TAKAFUL PRESENTED BY: IIU PRINCIPLES OF TAKAFUL Introduction to Takaful Comparison between conventional and Islamic Insurance Main elements of Takaful Insurance Types of Takaful contracts

PRINCIPLES OF TAKAFUL PRESENTED BY: IIU PRINCIPLES OF TAKAFUL Introduction to Takaful Comparison between conventional and Islamic Insurance Main elements of Takaful Insurance Types of Takaful contracts

J. P. M O R G A N I S L A M I C F I N A N C E

Islamic Finance Overview May 2014 S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L English_General 2013 JPMorgan Chase & Co. All rights reserved. These materials herein are provided for informational

Islamic Finance Overview May 2014 S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L English_General 2013 JPMorgan Chase & Co. All rights reserved. These materials herein are provided for informational

Prof. Umar Qudoos Date of Submission

Assignment on: HABIBMETRO ISLAMIC INVESTMENT CERTIFICATES (HIIC) Bank: HABIBMETRO ISLAMIC BANK Submitted To: Prof. Umar Qudoos Date of Submission 02-12-2015 Submitted By: Syed Hani Hasnain M.S.C. A&F 2014-16

Assignment on: HABIBMETRO ISLAMIC INVESTMENT CERTIFICATES (HIIC) Bank: HABIBMETRO ISLAMIC BANK Submitted To: Prof. Umar Qudoos Date of Submission 02-12-2015 Submitted By: Syed Hani Hasnain M.S.C. A&F 2014-16

Mawarid Finance P.J.S.C. Consolidated Financial Statements

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-7 Consolidated statement of financial position 8 Consolidated statement of

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-7 Consolidated statement of financial position 8 Consolidated statement of

Mawarid Finance P.J.S.C. Consolidated Financial Statements for the year ended 31 December 2015

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-4 Consolidated statement of financial position 5 Consolidated statement of

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-4 Consolidated statement of financial position 5 Consolidated statement of

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

1 ISLAMIC LAW OF TRADE (Fiqh-Al-Muamlaat) O you who believe! Fulfill your obligations (Holy Quraan) Copyright Reserved 2010

O you who believe! Fulfill your obligations (Holy Quraan) Copyright Reserved 2010") 1 ISLAMIC LAW OF TRADE (Fiqh-Al-Muamlaat) O you who believe! Fulfill your obligations (Holy Quraan) 2 ISLAMIC LAW OF TRADE (Fiqh-Al-Muamlaat) INDEX Sr. Particulars Page 1 FIQH OF TRADE 3 2 MUDARABAH AND

1 ISLAMIC LAW OF TRADE (Fiqh-Al-Muamlaat) O you who believe! Fulfill your obligations (Holy Quraan) 2 ISLAMIC LAW OF TRADE (Fiqh-Al-Muamlaat) INDEX Sr. Particulars Page 1 FIQH OF TRADE 3 2 MUDARABAH AND

US SHARE FUND Financial Services

US SHARE FUND Financial Services US SHARE FUND; With the partner funds and Banks is focused on profitable growth through niche financial services provided locally, nationally and via the Internet. These

US SHARE FUND Financial Services US SHARE FUND; With the partner funds and Banks is focused on profitable growth through niche financial services provided locally, nationally and via the Internet. These

University of Cape Town

The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source. The thesis is to be used for private

The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source. The thesis is to be used for private

Luxembourg A prime location for Sukuk issuance

Luxembourg A prime location for issuance Contents Islamic finance in Luxembourg listed in Luxembourg 5 Structuring transactions 6 al-ijara 8 Mixed-asset 9 al-musharaka 0 al-murabaha al-istisna al-salam

Luxembourg A prime location for issuance Contents Islamic finance in Luxembourg listed in Luxembourg 5 Structuring transactions 6 al-ijara 8 Mixed-asset 9 al-musharaka 0 al-murabaha al-istisna al-salam

Independent Shari'a Auditor s Report

Raqaba Shari'a Audit & Islamic Financial Consultations 912 Maynard Creek Cary, NC 27513 NC, USA Tel: Website: E-mail: +1 919 917 6595 +1 919 300 0012 www.raqaba.co.uk info@raqaba.co.uk Independent Shari'a

Raqaba Shari'a Audit & Islamic Financial Consultations 912 Maynard Creek Cary, NC 27513 NC, USA Tel: Website: E-mail: +1 919 917 6595 +1 919 300 0012 www.raqaba.co.uk info@raqaba.co.uk Independent Shari'a

Sharing of Risks in Islamic Finance

IBSU Scientific Journal, 5(2): 13-20, 2011 ISSN: 1512-3731 print / 2233-3002 online Sharing of Risks in Islamic Finance Ahmet SEKRETER Abstract For most of the people the prohibition on interest is the

IBSU Scientific Journal, 5(2): 13-20, 2011 ISSN: 1512-3731 print / 2233-3002 online Sharing of Risks in Islamic Finance Ahmet SEKRETER Abstract For most of the people the prohibition on interest is the

Banking & Financial Services Practice Capability Overview

Corporate website: www.accelfrontline.com CAC Holdings website: www.cac-holdings.com Banking & Financial Services Practice Capability Overview A subsidiary of CAC Holdings Corporation RESTRICTIONS The

Corporate website: www.accelfrontline.com CAC Holdings website: www.cac-holdings.com Banking & Financial Services Practice Capability Overview A subsidiary of CAC Holdings Corporation RESTRICTIONS The

Mr. D.A.N. EKE DEPUTY DIRECTOR

AN OVER-VIEW OF CBN NON-INTEREST (ISLAMIC) BANKING FRAMEWORK Mr. D.A.N. EKE DEPUTY DIRECTOR BANKING SUPERVISION DEPARTMENT 29 TH JULY, 2009 Central Bank of Nigeria 1 Outline Central Bank of Nigeria 1.

AN OVER-VIEW OF CBN NON-INTEREST (ISLAMIC) BANKING FRAMEWORK Mr. D.A.N. EKE DEPUTY DIRECTOR BANKING SUPERVISION DEPARTMENT 29 TH JULY, 2009 Central Bank of Nigeria 1 Outline Central Bank of Nigeria 1.

Islamic Finance and Capital Markets: Structure and Trading of Sukuk. Khalifa M Ali Hassanain

Islamic Finance and Capital Markets: Structure and Trading of Sukuk Khalifa M Ali Hassanain Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work are

Islamic Finance and Capital Markets: Structure and Trading of Sukuk Khalifa M Ali Hassanain Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work are

Contribution of Islamic Finance to the 2030 Agenda for Sustainable Development (with special reference to infrastructure finance)

") Contribution of Islamic Finance to the 2030 Agenda for Sustainable Development (with special reference to infrastructure finance) Habib Ahmed Durham University Business School, UK 1 Infrastructure Investment

Contribution of Islamic Finance to the 2030 Agenda for Sustainable Development (with special reference to infrastructure finance) Habib Ahmed Durham University Business School, UK 1 Infrastructure Investment

Valuation and Accounting for Redeemable Corporate Capital: An Islamic Perspective

Valuation and Accounting for Redeemable Corporate Capital: An Islamic Perspective Dr Safdar Ali Butt 1 Dr. Arshad Hassan 2 Abstract Development of new Islamic financial products like Islamic bonds (Sukuk),

Valuation and Accounting for Redeemable Corporate Capital: An Islamic Perspective Dr Safdar Ali Butt 1 Dr. Arshad Hassan 2 Abstract Development of new Islamic financial products like Islamic bonds (Sukuk),

An Islamic Perspective of Business Finance (A Comparative Study with Conventional and Capitalistic Financing)

") DOI : 10.18843/ijms/v5i1(4)/16 DOIURL :http://dx.doi.org/10.18843/ijms/v5i1(4)/16 An Islamic Perspective of Business Finance (A Comparative Study with Conventional and Capitalistic Financing) Syed Mahmood

DOI : 10.18843/ijms/v5i1(4)/16 DOIURL :http://dx.doi.org/10.18843/ijms/v5i1(4)/16 An Islamic Perspective of Business Finance (A Comparative Study with Conventional and Capitalistic Financing) Syed Mahmood

Measuring Shariah compliance in Senior & Subordinated Bonds. May 2018 SHARIAH ADVISOR LICENSED BY THE CENTRAL BANK OF BAHRAIN

Measuring Shariah compliance in Senior & Subordinated Bonds May 2018 SHARIAH ADVISOR LICENSED BY THE CENTRAL BANK OF BAHRAIN 2 Summary Bond investments are common, conventional fixed income instruments.

Measuring Shariah compliance in Senior & Subordinated Bonds May 2018 SHARIAH ADVISOR LICENSED BY THE CENTRAL BANK OF BAHRAIN 2 Summary Bond investments are common, conventional fixed income instruments.

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

Dubai Islamic Bank P.J.S.C. Consolidated financial statements for the year ended 31 December 2015

Consolidated financial statements These audited financial statements are subject to the Central Bank of the UAE approval and adoption by shareholders at the annual general meeting. Report and consolidated

Consolidated financial statements These audited financial statements are subject to the Central Bank of the UAE approval and adoption by shareholders at the annual general meeting. Report and consolidated

CONTINGENCIES AND COMMITMENTS 24. The annexed notes 1 to 48 and Annexures I to IV form an integral part of these financial statements.

FAYSAL BANK LIMITED STATEMENT OF FINANCIAL POSITION AS AT DECEMBER 31, 2014 Note 2014 2013 -------------- Rupees '000 ------------- ASSETS Cash and balances with treasury banks 8 20,285,851 28,422,497

FAYSAL BANK LIMITED STATEMENT OF FINANCIAL POSITION AS AT DECEMBER 31, 2014 Note 2014 2013 -------------- Rupees '000 ------------- ASSETS Cash and balances with treasury banks 8 20,285,851 28,422,497

IIFM-BAFT Master Participation Agreements - Key legal aspects

IIFM-BAFT Master Participation Agreements - Key legal aspects M. Delwar Hossain Senior Associate - Bahrain office What is a Participation? An arrangement between two banks/financial institutions whereby:

IIFM-BAFT Master Participation Agreements - Key legal aspects M. Delwar Hossain Senior Associate - Bahrain office What is a Participation? An arrangement between two banks/financial institutions whereby:

Islamic Banking Two steps forward and four steps backward?

Islamic Banking Two steps forward and four steps backward? Under Islamic Banking (IB) the sharia laws or Islamic laws of banking are followed. It is also referred to Sharia Banking or Interest Free Banking.

Islamic Banking Two steps forward and four steps backward? Under Islamic Banking (IB) the sharia laws or Islamic laws of banking are followed. It is also referred to Sharia Banking or Interest Free Banking.

New Sukuk Products A Case for Microfinance Sector. Salman Syed Ali

New Sukuk Products A Case for Microfinance Sector Salman Syed Ali 1 Achievements of Current Global Islamic Finance Pluses Grew from small and gaining in size and coverage Entered into financing of large-scale

New Sukuk Products A Case for Microfinance Sector Salman Syed Ali 1 Achievements of Current Global Islamic Finance Pluses Grew from small and gaining in size and coverage Entered into financing of large-scale

The Bank of Khyber Islamic Banking Group

BASIS OF DEPOSITS : NAME OF POOL : DECLARATION DATE : APPLICABLE PERIODS : MUSHARAKAH GENERAL POOL 24TH APRIL, 217 1ST MAY 217 ONWARD Product Name 1.9.214 1.5.217 Interest Free PLS Saving Account Monthly

BASIS OF DEPOSITS : NAME OF POOL : DECLARATION DATE : APPLICABLE PERIODS : MUSHARAKAH GENERAL POOL 24TH APRIL, 217 1ST MAY 217 ONWARD Product Name 1.9.214 1.5.217 Interest Free PLS Saving Account Monthly

SYARIAH CONCEPTS AND PRINCIPLES THAT CAN BE ADOPTED FOR THE PURPOSE OF STRUCTURING, DOCUMENTING AND TRADING OF ISLAMIC PRIVATE DEBT SECURITIES (IPDS)

") SYARIAH CONCEPTS AND PRINCIPLES THAT CAN BE ADOPTED FOR THE PURPOSE OF STRUCTURING, DOCUMENTING AND TRADING OF ISLAMIC PRIVATE DEBT SECURITIES (IPDS) The following are acceptable Syariah concepts and principles

SYARIAH CONCEPTS AND PRINCIPLES THAT CAN BE ADOPTED FOR THE PURPOSE OF STRUCTURING, DOCUMENTING AND TRADING OF ISLAMIC PRIVATE DEBT SECURITIES (IPDS) The following are acceptable Syariah concepts and principles

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

Analysis of the Sukuk Market. Dubai, April 25, 2007

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Dubai Financial Market Standards on Shari a Compliance l Standard No. 1 l Issuing, Acquiring and Trading Shares

1 CONTENTS INTRODUCTION... 4 1. THE SCOPE OF THE STANDARD... 6 2. SHARI'A PARAMETERS FOR ACQUIRING SHARES OF COMPANIES... 6 3. ACQUIRING AND SUBSCRIBING TO SHARES OF COMPANIES OF MIXED ACTIVITIES:... 7

1 CONTENTS INTRODUCTION... 4 1. THE SCOPE OF THE STANDARD... 6 2. SHARI'A PARAMETERS FOR ACQUIRING SHARES OF COMPANIES... 6 3. ACQUIRING AND SUBSCRIBING TO SHARES OF COMPANIES OF MIXED ACTIVITIES:... 7

Securitization and Structuring Sukuk

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Chapter 8: Takaful. Chapter Objectives. Students must be able to: Understand the Sources of Islamic Law. Understand the Concept of Takaful

Chapter 8 Takaful Chapter Objectives Students must be able to: Understand the Sources of Islamic Law Understand the Concept of Takaful Define and Relate to the 3 Principles of Syariah Relating to a Contract

Chapter 8 Takaful Chapter Objectives Students must be able to: Understand the Sources of Islamic Law Understand the Concept of Takaful Define and Relate to the 3 Principles of Syariah Relating to a Contract

ISLAMIC DEVELOPMENT BANK

ISLAMIC DEVELOPMENT BANK ORDINARY CAPITAL RESOURCES Financial Statements and Independent Joint Auditors Report (24 October 2014) Financial Statements 30 Dhul Hijjah (24 October 2014) Page Independent joint

ISLAMIC DEVELOPMENT BANK ORDINARY CAPITAL RESOURCES Financial Statements and Independent Joint Auditors Report (24 October 2014) Financial Statements 30 Dhul Hijjah (24 October 2014) Page Independent joint

Alternative Financing Wafiq Fannoun 11/21/2002

The Federal Reserve Bank Of New York Alternative Financing By Wafiq Fannoun 11/21/2002 1 Islamic Financing Alternative financing for Muslims and all those who are averse to interest. 2 Islam & Muslims

The Federal Reserve Bank Of New York Alternative Financing By Wafiq Fannoun 11/21/2002 1 Islamic Financing Alternative financing for Muslims and all those who are averse to interest. 2 Islam & Muslims

Rahn Services Offered by Contemporary Islamic Financial Institutions: Challenges and Prospects

Rahn Services Offered by Contemporary Islamic Financial Institutions: Challenges and Prospects Rahn Services Offered by Contemporary Islamic Financial Institutions: Challenges and Prospects *Tahira Ifraq

Rahn Services Offered by Contemporary Islamic Financial Institutions: Challenges and Prospects Rahn Services Offered by Contemporary Islamic Financial Institutions: Challenges and Prospects *Tahira Ifraq

Islamic Transactions September 2008

Islamic Transactions September 2008 TABLE OF CONTENTS TABLE OF CONTENTS 2 INTRODUCTION 3 BASIC PRINCIPLES 5 FINANCE STRUCTURES 7 Partnership Structures 7 Sale and Purchase Structures 8 Leasing Structures

Islamic Transactions September 2008 TABLE OF CONTENTS TABLE OF CONTENTS 2 INTRODUCTION 3 BASIC PRINCIPLES 5 FINANCE STRUCTURES 7 Partnership Structures 7 Sale and Purchase Structures 8 Leasing Structures