ACCA Paper P2. Financial Management. theexpgroup.com

|

|

|

- Reynold Clarke

- 6 years ago

- Views:

Transcription

1 Thank you for downloading this extract from our ExPedite notes to accompany your free online Course in a Coffee Break. To download a free complete set of our ExPress notes please visit Good luck with your P2 studies. ACCA Paper P2 Financial Management For exams in 2010

2 Chapter 5 Financial Instruments START The Big Picture Although financial instruments appear frequently in the P2 exam, they are only at level 2 knowledge within the syllabus. This means that the scenarios in which they are tested are likely to be relatively straightforward. It s easy to spend too much time preparing for these accounting standards, since they cover a huge array of different possible transactions, from regular trade receivables to exotic currency and interest rate swaps. Page 5.1

3 The best way to approach study is to know: The four different classifications of all financial instruments The difference in fair value and amortised cost accounting The possible ways in which any gain or loss (whether on a financial instrument or not) may be reported in financial statements. If you are keen to take this as far as you can, then move on to study hedging, though this has generally only been worth a couple of marks in the exam. When used... Example... Example that can t be categorised this way Initial recognised value Year-end valuation method Gains or losses reported in... Held-to-maturity financial assets When have the ability and positive intention to hold a security to its stated maturity date. Investment in corporate bonds or government bonds. Ordinary shares, as no maturity date. Nothing can be HTMFA if the entity has reclassified any investment out of HTMFA in the preceding two years. Cost paid, including transaction costs. Amortised cost, less impairments. Impaired value estimated using revised cash flows, discounted at the original discount rate when the investment was purchased. Profit or loss Loans and receivables When have loaned a third party money (to a maturity date) or have an amount receivable (e.g. trade receivables). Originated loan to a third party (e.g. a bank lending a loan to a homebuyer). - Initial cash advanced, plus transaction costs. Amortised cost, less impairments. Impaired value estimated using revised cash flows, discounted at the original discount rate when the investment was purchased. Profit or loss Page 5.2

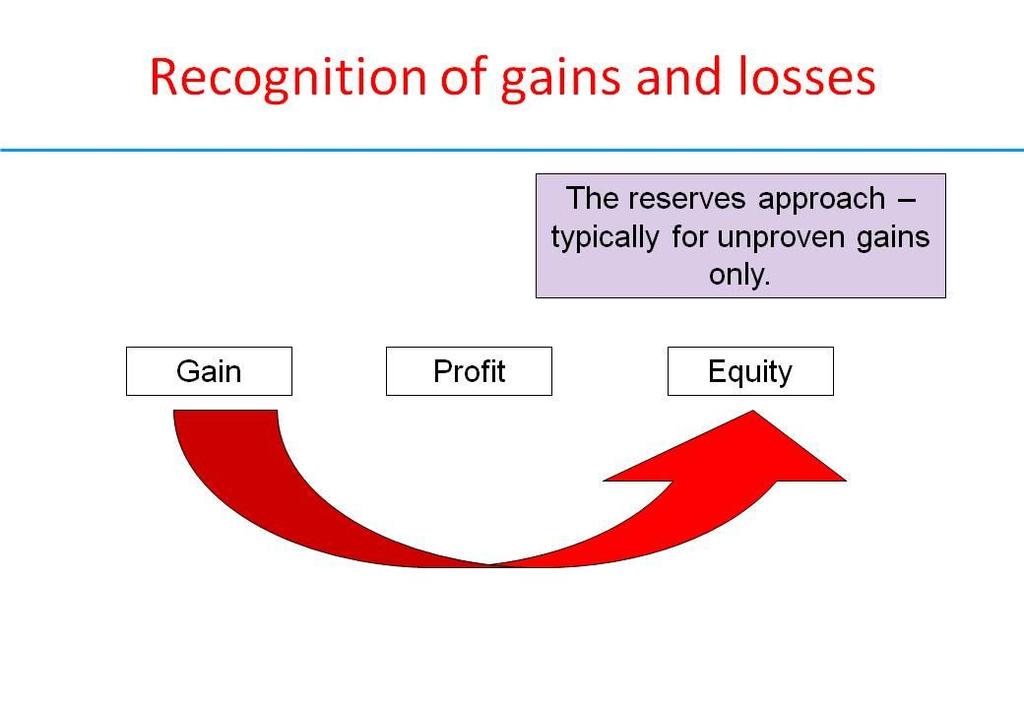

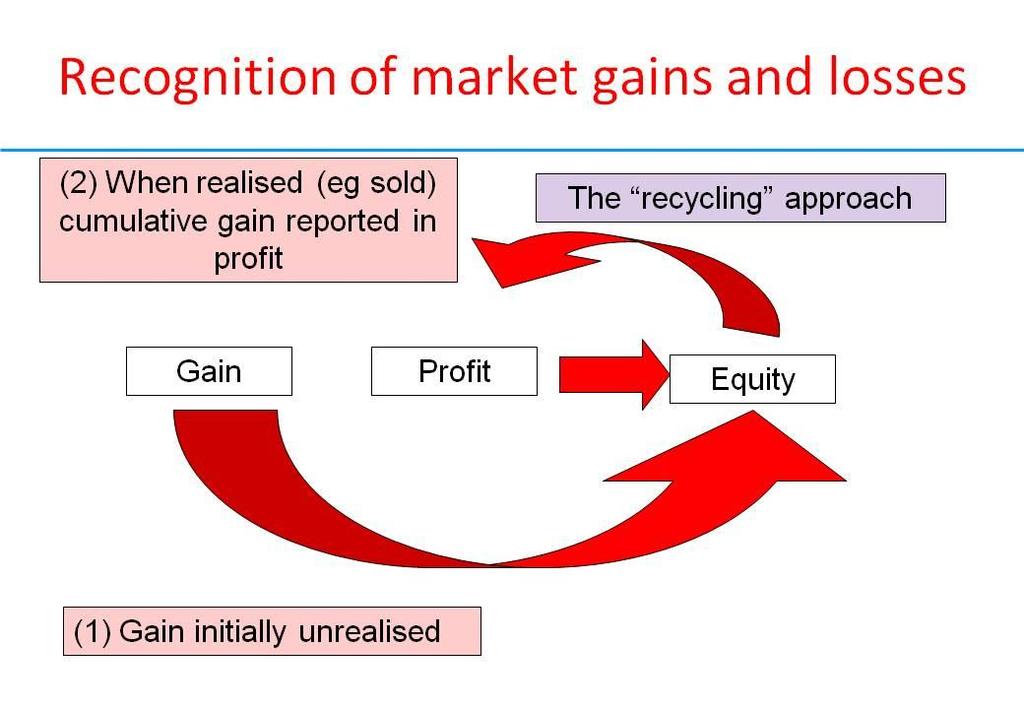

4 When used... Example... Financial asset or liability held at fair value through profit or loss Almost anything can be categorised as FVPL at its initial recognition (notably not debt issued by the entity itself). Securities held for trading will be classified as FVPL. Shares held for trading. Available-for-sale financial assets A catch-all category. Anything not in either of the other categories will be AFSFA. Typically, where investor stands ready to sell the security but has no immediate plans to. Shares held for intermediate term investment. Example that can t be categorised this way - - Initial recognised value Year-end valuation method Gains or losses reported in... Cash paid to acquire. Transaction costs immediately written off to profit or loss. Fair value. Best achievable market price, not deducting anticipated selling costs (though at the lower end of the bid ask spread). Profit or loss Cash paid to acquire. Transaction costs added to initial value of investment. Fair value. Best achievable market price, not deducting anticipated selling costs (though at the lower end of the bid ask spread). Initially gain or loss reported in equity until sold, when the gain or loss is recycled (ie reported again) in profit. Page 5.3

5 Page 5.4

6 KEY WORKING METHODS Recognition and derecognition The recognition criteria for financial instruments are slightly different to the recognition criteria in many other IASs/ IFRSs. The intention is to ensure that as many as recognised as possible, for as long as possible. They are recognised when the entity becomes party to the contract rather than when control is obtained. They are derecognised only when it s virtually certain that all the risks of a financial instrument have expired or have been transferred to another party. Fair value accounting Fair value essentially means market value. So if the market is acting irrationally, then fair value may lead to dysfunctional financial reporting. This is a recent criticism of fair value accounting techniques. Fair values are determined as: Best achievable market value (but not deducting expected transaction costs), or Valuation using discounted cash flows that consider all matters relevant (e.g. expected cash flows, timing of cash flows, credit risk, market interest rates, or Exceptionally if no reliable DCF valuation is possible, historical cost. Amortised cost For held-to-maturity financial assets, both the issuer and the holder of the financial instrument (e.g. bond) know all the cash flows and the timing of those cash flows. The market value at its issue is known, as is its market value at maturity, since a bond that pays $1,000 on a known date is worth $1,000 on that date! Any changes in market value in between the date of issue and the maturity date is therefore irrelevant as that gain or loss will not be realised. The easiest treatment is therefore to spread the total return over the bond over its total life. This is done using the effective rate, which is the total return on the bond. Page 5.5

of 4% of nominal value.")

7 This is the internal rate of return of all the cash flows. In the exam, you would be given the effective rate and be asked to calculate the figures in the financial statements. EXAMPLE On 1 January 20x1, Cordelia Co issued a bond with a nominal value of $200,000, a coupon rate (ie cash paid) of 4% of nominal value. The bond is due for redemption on 31 December 20x5 for $200,000 (plus the coupon payable on that date). In reality, it s likely that the effective rate would be worked out using a spreadsheet and the IRR function, which is illustrated below. This means that by the end of the five year life of the bond, it has been transformed ( amortised ) from its initially recognised value to its redemption value of $200,000. Page 5.6

8 So the charge or credit to profit for finance costs/ finance income is determined using the effective rate. The difference between interest calculated using the effective rate and the coupon paid/ received is the rolled up interest, which is added to the value of the bond each year. Reclassication To prevent creative accounting, reclassifying from one category of financial instruments to another is strongly discouraged by IAS 39. If a material held-to-maturity financial asset is reclassified out of held-to-maturity financial assets, then: All other held-to-maturity financial assets must be immediately reclassified as available for sale, with immediate recognition of all gain or loss (paragraph 52, IAS 39). For that year and the two years thereafter, it is barred from classifying anything as held-tomaturity financial assets (paragraph 9, IAS 39). Impairments All financial assets held at fair value are automatically revalued for impairments. If a heldto-maturity asset appears to be impaired (e.g. if the credit risk increases a great deal), then the new impaired value must be calculated using: The revised expected cash flows and expected timing At the original discount rate. Note that discounting the revised cash flows at the new rate (which would be higher, as the risk has increased) would double count the risk factor and result in undervaluation of the asset. Page 5.7

9 Hedging Hedging has only occasionally been tested in paper P2 and then normally as a relatively minor adjustment in question 1. It is common in practice and useful knowledge. Becoming expert in hedging should not be a top priority for most students studying for paper P2, since it can take a lot of time to master for a relatively low profile in the exam itself. KEY WORKING METHODS Hedged item: The thing the enterprise is worried about changing in value, e.g.: Foreign currency investment Foreign currency payable Variable interest rate loan resulting in higher than expected cash outflows Forecast future major purchase in a foreign currency becoming unaffordable due to changes in the exchange rate. To remove or reduce this risk, the entity may buy something that is expected to move in value in the opposite direction to the hedged item. This counterweight is the hedging instrument and may be an almost infinite number of different financial instruments, though derivatives are common. Understanding the intricacies of how hedging relationships may be set up is not important for paper P2. It s useful to know how to account for movements in the hedged item and the hedging instrument. Page 5.8

10 Though three types of hedge are mentioned in IAS 39, there are only two accounting treatments for hedges, so there are basically two types of hedge: Fair value hedge The hedging instrument was taken out in order to protect against value changes of an item recognised in the SOFP. E.g. a foreign currency loan to protect against a foreign exchange change in value of a foreign currency receivable that is being shown in the SOFP. Cash flow hedge A hedge that is not a fair value hedge, broadly! This might be to protect against adverse movements in an item not in the SOFP yet. E.g. an entity may structure its business plan around buying a ship from a foreign ship builder, but it has not yet placed a binding order. As there is no binding order, there is no obligation, so there is no liability. The forecast/ intended transaction is not yet a liability, though the company will want to ensure that they can afford the expected future cash outflow. To protect against adverse exchange movements making the ship unaffordable, the entity may hedge the foreign currency exposure, e.g. buy buying a foreign currency forward contract. Accounting for hedges A fair value hedge is simple. Both the hedged item and hedging instrument will be in the SOFP and will record a gain and a loss. The accounting rules simply offset the gain on the hedged item with the loss on the hedging instrument, or vice versa. A cash flow hedge is a bigger challenge for the writers of the IAS! The hedging instrument will be a contract, so will be in the SOFP, but the hedged item will be an intention, so is not in the SOFP. Since the hedging instrument exists only because of the expected existence of the hedged item, the gain or loss on the hedging instrument is hidden in equity until the hedged transaction takes place. Page 5.9

Chapter 4 to 6 extract from our ExPress notes for use with the current video.

Chapter 4 to 6 extract from our ExPress notes for use with the current video. A full set of F2 ExPress notes can be downloaded free of charge at www.. Notes CIMA Paper F2 Financial Management Contents

Chapter 4 to 6 extract from our ExPress notes for use with the current video. A full set of F2 ExPress notes can be downloaded free of charge at www.. Notes CIMA Paper F2 Financial Management Contents

RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 What is a financial instrument? Let us start by looking at the definition of a financial instrument, which is that a financial instrument is a contract that

RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 What is a financial instrument? Let us start by looking at the definition of a financial instrument, which is that a financial instrument is a contract that

FINANCIAL INSTRUMENTS

page 48 student accountant NOVEMBER/DECEMBER 2008 FINANCIAL INSTRUMENTS understanding the basics RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 This article aims to help students better understand accounting

page 48 student accountant NOVEMBER/DECEMBER 2008 FINANCIAL INSTRUMENTS understanding the basics RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 This article aims to help students better understand accounting

Understanding IFRS 9 (2014) for Directors By Tan Liong Tong

for Directors By Tan Liong Tong") Understanding IFRS 9 (2014) for Directors By Tan Liong Tong 1. Introduction Many preparers and users of financial statements and other interested parties have expressed concerns that the requirements of

Understanding IFRS 9 (2014) for Directors By Tan Liong Tong 1. Introduction Many preparers and users of financial statements and other interested parties have expressed concerns that the requirements of

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS Financial instruments FRS 102 significantly changed the accounting for financial instruments in comparison to the requirements applicable to most UK and Ireland

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS Financial instruments FRS 102 significantly changed the accounting for financial instruments in comparison to the requirements applicable to most UK and Ireland

ACCA Paper F7. Financial Management. theexpgroup.com

Thank you for downloading this extract from our ExPedite notes to accompany your free online Course in a Coffee Break. To download a free complete set of our ExPress notes please visit www.. Good luck

Thank you for downloading this extract from our ExPedite notes to accompany your free online Course in a Coffee Break. To download a free complete set of our ExPress notes please visit www.. Good luck

MITCHELLS & BUTLERS PLC. Adoption of International Financial Reporting Standards

7 December 2005 MITCHELLS & BUTLERS PLC Adoption of International Financial Reporting Standards Mitchells & Butlers plc ( the Group ) today releases its financial results for the 53 weeks to 1 October

7 December 2005 MITCHELLS & BUTLERS PLC Adoption of International Financial Reporting Standards Mitchells & Butlers plc ( the Group ) today releases its financial results for the 53 weeks to 1 October

1 Summary of significant accounting policies (continued)

") (g) (g) Impairment of financial assets (continued) '()*+, Financial assets carried at amortised cost (continued) If there is objective evidence that an impairment loss on financial assets carried at amortised

(g) (g) Impairment of financial assets (continued) '()*+, Financial assets carried at amortised cost (continued) If there is objective evidence that an impairment loss on financial assets carried at amortised

OJSC Kapital Bank Financial Statements. Year ended 31 December 2012 Together with Independent Auditors Report

Financial Statements Year ended 31 December Together with Independent Auditors Report financial statements CONTENTS Independent auditors report Statement of financial position... 1 Income statement...

Financial Statements Year ended 31 December Together with Independent Auditors Report financial statements CONTENTS Independent auditors report Statement of financial position... 1 Income statement...

HSBC Bank Middle East Limited - UAE Operations Financial statements As at and for the year ended 31 December 2010

Financial statements As at and for the year ended 31 December 2010 Financial statements As at and for the year ended 31 December 2010 Contents Independent auditors' report Page 1 Statement of income 2

Financial statements As at and for the year ended 31 December 2010 Financial statements As at and for the year ended 31 December 2010 Contents Independent auditors' report Page 1 Statement of income 2

ACCOUNTING POLICIES. for the year ended 30 June MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

Anesu Daka CA(SA) - CAA

- CAA") FAC4863 4 August 2015 Tut 105/106 1. IAS 21- The effects of changes in foreign exchange rates 2. IAS32/39/IFRS9&7-Financial instruments 3. IAS 39-Hedging 4. IAS 33-Earnings per share 5. IAS 17- Leases

FAC4863 4 August 2015 Tut 105/106 1. IAS 21- The effects of changes in foreign exchange rates 2. IAS32/39/IFRS9&7-Financial instruments 3. IAS 39-Hedging 4. IAS 33-Earnings per share 5. IAS 17- Leases

IAS 32 & IFRS 9 Financial Instruments

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

Financial Instruments: Disclosures

International Financial Reporting Standard 7 Financial Instruments: Disclosures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 30 Disclosures in the Financial Statements

International Financial Reporting Standard 7 Financial Instruments: Disclosures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 30 Disclosures in the Financial Statements

Commercial Bank International P.S.C. Reports and the consolidated financial statements for the year ended 31 December 2017

Commercial Bank International P.S.C. Reports and the consolidated financial statements for the year ended 31 December 2017 These audited consolidated financial statements are subject to approval of the

Commercial Bank International P.S.C. Reports and the consolidated financial statements for the year ended 31 December 2017 These audited consolidated financial statements are subject to approval of the

FINANCIAL REPORTING FOR GROUP ENTITIES UNDER IFRS

FINANCIAL REPORTING FOR GROUP ENTITIES UNDER IFRS IAS 28 Investments in Associates and Joint Ventures Conf.univ.dr. Victor-Octavian Müller victor.muller@econ.ubbcluj.ro www.econ.ubbcluj.ro/~victor.muller

FINANCIAL REPORTING FOR GROUP ENTITIES UNDER IFRS IAS 28 Investments in Associates and Joint Ventures Conf.univ.dr. Victor-Octavian Müller victor.muller@econ.ubbcluj.ro www.econ.ubbcluj.ro/~victor.muller

Unaudited Quarterly Accounts of the National Asset Management Agency and its Group Entities. For the period ended 31 December 2010

Unaudited Quarterly Accounts of the Agency and its Group Entities For the period ended 31 December 2010 Agency Contents Page Board and other information 3 Introduction and general information 4-6 Agency

Unaudited Quarterly Accounts of the Agency and its Group Entities For the period ended 31 December 2010 Agency Contents Page Board and other information 3 Introduction and general information 4-6 Agency

IFRS 7 and IFRS 13 disclosures

www.pwc.ie In depth IFRS 7 and IFRS 13 disclosures A In depth to the disclosure requirements of IFRS 7 and IFRS 13 for investment funds, private equity funds, real estate funds and investment managers

www.pwc.ie In depth IFRS 7 and IFRS 13 disclosures A In depth to the disclosure requirements of IFRS 7 and IFRS 13 for investment funds, private equity funds, real estate funds and investment managers

Deutsche Post Finance B.V. Annual Report 2016

Deutsche Post Finance B.V. Annual Report 2016!III m INI Table of contents Page 1. Management Report 4 1.1 Introduction 4 1.2 Business activities 4 1.3 Legal relationships 4 1.4 Main business developments

Deutsche Post Finance B.V. Annual Report 2016!III m INI Table of contents Page 1. Management Report 4 1.1 Introduction 4 1.2 Business activities 4 1.3 Legal relationships 4 1.4 Main business developments

Anesu Daka CA(SA)- CAA

- CAA") FAC4861 4 August 2015 Tut 105/106 1. IAS32/39/IFRS9&7-Financial instruments 2. IAS 33-Earnings per share 3. IAS 17- Leases Forex Transactions: IAS 21 Effects in foreign exchange rates transactions IAS

FAC4861 4 August 2015 Tut 105/106 1. IAS32/39/IFRS9&7-Financial instruments 2. IAS 33-Earnings per share 3. IAS 17- Leases Forex Transactions: IAS 21 Effects in foreign exchange rates transactions IAS

INVESTMENT HOLDING GROUP Q.P.S.C. DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2017

DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2017 INVESTMENT HOLDING GROUP Q.P.S.C. DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT

DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2017 INVESTMENT HOLDING GROUP Q.P.S.C. DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT

Consolidated financial statements for the year ended December 31 st, In accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2009 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2009 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1. Corporate information DP World PLC ( the Company ) formerly known as DP World Limited, was incorporated on 9 August 2006 as a Company Limited by Shares with the Registrar of Companies of the Dubai International

1. Corporate information DP World PLC ( the Company ) formerly known as DP World Limited, was incorporated on 9 August 2006 as a Company Limited by Shares with the Registrar of Companies of the Dubai International

Arab Banking Corporation (B.S.C.) CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS") CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2014 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Year ended Note PROFIT FOR THE YEAR 318 297 Other comprehensive income: Other comprehensive income

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2014 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Year ended Note PROFIT FOR THE YEAR 318 297 Other comprehensive income: Other comprehensive income

Principal Accounting Policies

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

ACCOUNTING POLICIES 1 PRESENTATION OF FINANCIAL STATEMENTS. for the year ended 30 June BASIS OF PREPARATION 1.2 STATEMENT OF COMPLIANCE

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

Corporate Information 1. Directors' Report. Independent Auditors' Report. Statement of Financial Position 4

TABLE OF CONTENTS - DECEMBER 31, 2013 Corporate Information 1 Pages Directors' Report Independent Auditors' Report 2-2(a) 3-3(a) Statement of Financial Position 4 Statement of Profit or Loss and Other

TABLE OF CONTENTS - DECEMBER 31, 2013 Corporate Information 1 Pages Directors' Report Independent Auditors' Report 2-2(a) 3-3(a) Statement of Financial Position 4 Statement of Profit or Loss and Other

The IFRS for SMEs Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity This PowerPoint presentation was prepared by IFRS Foundation education

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity This PowerPoint presentation was prepared by IFRS Foundation education

Kereskedelmi és Hitelbank Zártkörűen Működő Részvénytársaság CONSOLIDATED ANNUAL REPORT

ildiko.gasparek@kh.hu Digitally signed by ildiko.gasparek@kh.hu DN: cn=ildiko.gasparek@kh.hu Date: 2017.04.28 14:26:06 +02'00' Kereskedelmi és Hitelbank Zártkörűen Működő Részvénytársaság CONSOLIDATED

ildiko.gasparek@kh.hu Digitally signed by ildiko.gasparek@kh.hu DN: cn=ildiko.gasparek@kh.hu Date: 2017.04.28 14:26:06 +02'00' Kereskedelmi és Hitelbank Zártkörűen Működő Részvénytársaság CONSOLIDATED

IFRS Interim Results. 25 weeks to 24 July November 2005

IFRS Interim Results 25 weeks to 24 July 2005 17 November 2005 Overview 2 UK GAAP trading update of 20 October remains unchanged Operating profit before exceptionals unchanged at 50.7m Conversion to IFRS

IFRS Interim Results 25 weeks to 24 July 2005 17 November 2005 Overview 2 UK GAAP trading update of 20 October remains unchanged Operating profit before exceptionals unchanged at 50.7m Conversion to IFRS

ST. KITTS-NEVIS-ANGUILLA NATIONAL BANK LIMITED

Consolidated balance sheet As of June 30, 2013 ASSETS Notes Cash and balances with Central Bank 6 355,574 254,466 Treasury bills 7 137,962 99,179 Deposits with other financial institutions 8 526,884 418,865

Consolidated balance sheet As of June 30, 2013 ASSETS Notes Cash and balances with Central Bank 6 355,574 254,466 Treasury bills 7 137,962 99,179 Deposits with other financial institutions 8 526,884 418,865

JSC MICROFINANCE ORGANIZATION FINCA GEORGIA. Financial statements. Together with the Auditor s Report. Year ended 31 December 2010

JSC MICROFINANCE ORGANIZATION FINCA GEORGIA Financial statements Together with the Auditor s Report Year ended 31 December 2010 JSC MICROFINANCE ORGANIZATION FINCA Georgia FINANCIAL STATEMENTS Contents:

JSC MICROFINANCE ORGANIZATION FINCA GEORGIA Financial statements Together with the Auditor s Report Year ended 31 December 2010 JSC MICROFINANCE ORGANIZATION FINCA Georgia FINANCIAL STATEMENTS Contents:

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IFRS 9 Financial Instruments (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International

FACT SHEET September 2011 IFRS 9 Financial Instruments (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International

Consolidated Financial Statements

Consolidated Financial Statements 2015 PROCREDIT BANK (BULGARIA) EAD CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 Financial statements in English are translation from the original in Bulgarian. This

Consolidated Financial Statements 2015 PROCREDIT BANK (BULGARIA) EAD CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 Financial statements in English are translation from the original in Bulgarian. This

AHLI UNITED BANK K.S.C.P. KUWAIT INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION 30 JUNE 2018 (UNAUDITED)

") AHLI UNITED BANK K.S.C.P. KUWAIT INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION 30 JUNE 2018 (UNAUDITED) Kuwait Interim Condensed Consolidated Financial Information 30 June 2018 C o n t e n t s Page

AHLI UNITED BANK K.S.C.P. KUWAIT INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION 30 JUNE 2018 (UNAUDITED) Kuwait Interim Condensed Consolidated Financial Information 30 June 2018 C o n t e n t s Page

VOLUME III. Accounting Policies

VOLUME III Accounting Policies 2016 002 CONTENT Accounting Policies 1 Basis of accounting... 4 2 Changes in accounting policies... 5 3 Accounting estimates... 7 4 Events after the reporting period... 8

VOLUME III Accounting Policies 2016 002 CONTENT Accounting Policies 1 Basis of accounting... 4 2 Changes in accounting policies... 5 3 Accounting estimates... 7 4 Events after the reporting period... 8

HSBC Bank Armenia cjsc

The HSBC Group HSBC Bank Armenia is a member of HSBC Group, one of the largest banking and financial services organizations in the world. HSBC Group international network comprises around 6,600 offices

The HSBC Group HSBC Bank Armenia is a member of HSBC Group, one of the largest banking and financial services organizations in the world. HSBC Group international network comprises around 6,600 offices

The IFRS for SMEs Topic 2.1 Section 11 Basic Financial Instruments Michael Wells

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Michael Wells Sections 11-12 Introduction 2 Financial instruments split into two sections: Sec. 11 Basic Financial Instruments Sec.

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Michael Wells Sections 11-12 Introduction 2 Financial instruments split into two sections: Sec. 11 Basic Financial Instruments Sec.

AHLI UNITED BANK K.S.C.P. KUWAIT INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION 31 MARCH 2018 (UNAUDITED)

") AHLI UNITED BANK K.S.C.P. KUWAIT INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION 31 MARCH 2018 (UNAUDITED) Kuwait Interim Condensed Consolidated Financial Information 31 March 2018 C o n t e n t s

AHLI UNITED BANK K.S.C.P. KUWAIT INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION 31 MARCH 2018 (UNAUDITED) Kuwait Interim Condensed Consolidated Financial Information 31 March 2018 C o n t e n t s

EMIRATES NBD BANK PJSC

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

Artsakhbank cjsc. Financial Statements for the year ended 31 December 2013

Financial Statements for the year ended 31 December Artslllcllbllllk cjsc Stateml!nt ofprofit or Loss Clnd Other Comprehensive income for the year ended 31 December 20 13 Notes AMD'OOO AMD'OOO Interest

Financial Statements for the year ended 31 December Artslllcllbllllk cjsc Stateml!nt ofprofit or Loss Clnd Other Comprehensive income for the year ended 31 December 20 13 Notes AMD'OOO AMD'OOO Interest

Financial Instruments Standards 11 November Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA Nelson 1

MBA MSc BBA CPA(US) ACA Nelson 1") Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement

Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement

Kereskedelmi és Hitelbank Zártkörűen Működő Részvénytársaság ANNUAL REPORT

ildiko.gasparek @kh.hu Digitally signed by ildiko.gasparek@kh.hu DN: cn=ildiko.gasparek@kh.hu Date: 2018.04.18 18:19:11 +02'00' Kereskedelmi és Hitelbank Zártkörűen Működő Részvénytársaság ANNUAL REPORT

ildiko.gasparek @kh.hu Digitally signed by ildiko.gasparek@kh.hu DN: cn=ildiko.gasparek@kh.hu Date: 2018.04.18 18:19:11 +02'00' Kereskedelmi és Hitelbank Zártkörűen Működő Részvénytársaság ANNUAL REPORT

Open Joint Stock Company Raiffeisen Bank Aval Consolidated Financial Statements

Open Joint Stock Company Raiffeisen Bank Aval Consolidated Financial Statements For the year ended 31 December Together with Independent Auditors Report Consolidated Financial Statements CONTENTS INDEPENDENT

Open Joint Stock Company Raiffeisen Bank Aval Consolidated Financial Statements For the year ended 31 December Together with Independent Auditors Report Consolidated Financial Statements CONTENTS INDEPENDENT

FInAnCIAl StAteMentS

Financial STATEMENTS The University of Newcastle ABN 157 365 767 35 Contents 106 Income statement 107 Statement of comprehensive income 108 Statement of financial position 109 Statement of changes in equity

Financial STATEMENTS The University of Newcastle ABN 157 365 767 35 Contents 106 Income statement 107 Statement of comprehensive income 108 Statement of financial position 109 Statement of changes in equity

UBA CAPITAL PLC. Un-audited results for half year ended 30 June 2014

Un-audited results for half year ended 30 June 2014 Consolidated and Separate Statement of Comprehensive Income Half year ended 30 June 2014 Notes 30th June 2014 30th June 2013 Gross Earnings 2,258,102

Un-audited results for half year ended 30 June 2014 Consolidated and Separate Statement of Comprehensive Income Half year ended 30 June 2014 Notes 30th June 2014 30th June 2013 Gross Earnings 2,258,102

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA Asset Impairment Workshop 16 th July to 17 th July Session Five: Financial Assets

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA Asset Impairment Workshop 16 th July to 17 th July Session Five: Financial Assets Credibility. Professionalism. AccountAbility Content 1. Recognition

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA Asset Impairment Workshop 16 th July to 17 th July Session Five: Financial Assets Credibility. Professionalism. AccountAbility Content 1. Recognition

NOTES TO THE FINANCIAL STATEMENTS For the year ended 31st December, 2013

1. GENERAL Cosmos Machinery Enterprises Limited (the Company ) is a public limited company domiciled and incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the

1. GENERAL Cosmos Machinery Enterprises Limited (the Company ) is a public limited company domiciled and incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the

STRUCTURED CONNECTIVITY SOLUTIONS (PTY) LTD (Registration number 2002/001640/07) Historical FInancial Information for the year ended 31 August 2012

LTD (Registration number 2002/001640/07) Historical FInancial Information for the year ended 31 August 2012") STRUCTURED CONNECTIVITY SOLUTIONS (PTY) LTD Historical FInancial Information for the year ended 31 August 2012 Index The reports and statements set out below comprise the historical financial information

STRUCTURED CONNECTIVITY SOLUTIONS (PTY) LTD Historical FInancial Information for the year ended 31 August 2012 Index The reports and statements set out below comprise the historical financial information

Financial Reporting, Topic Area 3 Financial Instruments

www.acasimplified.com Sample Q&A Financial Reporting, Topic Area 3 69 short questions and answers to drill the narrative and numerical aspects of the topic The Q&A will work best if you cover the answer

www.acasimplified.com Sample Q&A Financial Reporting, Topic Area 3 69 short questions and answers to drill the narrative and numerical aspects of the topic The Q&A will work best if you cover the answer

EQUITY INSTRUMENTS - IMPAIRMENT AND RECYCLING EFRAG DISCUSSION PAPER MARCH 2018

EQUITY INSTRUMENTS - IMPAIRMENT AND RECYCLING EFRAG DISCUSSION PAPER MARCH 2018 2018 European Financial Reporting Advisory Group. European Financial Reporting Advisory Group ( EFRAG ) issued this Discussion

EQUITY INSTRUMENTS - IMPAIRMENT AND RECYCLING EFRAG DISCUSSION PAPER MARCH 2018 2018 European Financial Reporting Advisory Group. European Financial Reporting Advisory Group ( EFRAG ) issued this Discussion

pwc.com/ifrs A practical guide to new IFRSs for 2014

pwc.com/ifrs A practical guide to new IFRSs for 2014 February 2014 February 2014 pwc.com/ifrs inform.pwc.com inform.pwc.com for 2013 year ends www.pwc.com/ifrs inform.pwc.com PwC s IFRS, corporate reporting

pwc.com/ifrs A practical guide to new IFRSs for 2014 February 2014 February 2014 pwc.com/ifrs inform.pwc.com inform.pwc.com for 2013 year ends www.pwc.com/ifrs inform.pwc.com PwC s IFRS, corporate reporting

1.3 IFRS AND THE TREASURER

1.3 IFRS AND THE TREASURER Study Unit: Study Unit 3 Corporate Financial Management Section: Section 1 Financial Accounting and Reporting Date: 15 August 2008 Summary: An introduction to the impact of International

1.3 IFRS AND THE TREASURER Study Unit: Study Unit 3 Corporate Financial Management Section: Section 1 Financial Accounting and Reporting Date: 15 August 2008 Summary: An introduction to the impact of International

IFRS for SMEs IFRS Foundation-World Bank

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

Risk and Accounting. IFRS 9 Financial Instruments. Marco Venuti 2018

Risk and Accounting IFRS 9 Financial Instruments Marco Venuti 2018 Agenda Reasons for issuing IFRS 9 Classification approach by IFRS 9 Classification and Measurement of financial assets Contractual cash

Risk and Accounting IFRS 9 Financial Instruments Marco Venuti 2018 Agenda Reasons for issuing IFRS 9 Classification approach by IFRS 9 Classification and Measurement of financial assets Contractual cash

Annual report 2011 DNB BOLIGKREDITT AS. - a company in the DNB Group

Annual report 2011 DNB BOLIGKREDITT AS - a company in the DNB Group Annual report Directors' report... 2 Statement pursuant to the Securities Trading Act... 5 Annual accounts... 6 Statement of Comprehensive

Annual report 2011 DNB BOLIGKREDITT AS - a company in the DNB Group Annual report Directors' report... 2 Statement pursuant to the Securities Trading Act... 5 Annual accounts... 6 Statement of Comprehensive

BANK DHOFAR SAOG FINANCIAL STATEMENTS 31 DECEMBER Registered and principal place of business:

FINANCIAL STATEMENTS 31 DECEMBER 2017 Registered and principal place of business: Bank Dhofar SAOG Central Business District P.O. Box 1507 Ruwi 112 Sultanate of Oman STATEMENT OF FINANCIAL POSITION 2017

FINANCIAL STATEMENTS 31 DECEMBER 2017 Registered and principal place of business: Bank Dhofar SAOG Central Business District P.O. Box 1507 Ruwi 112 Sultanate of Oman STATEMENT OF FINANCIAL POSITION 2017

Translation from Bulgarian

FIRST INVESTMENT BANK AD Unconsolidated statement of comprehensive income for the year ended 31 December 2013 unaudited in BGN 000 2013 2012 Interest income 446,451 454,979 Interest expense and similar

FIRST INVESTMENT BANK AD Unconsolidated statement of comprehensive income for the year ended 31 December 2013 unaudited in BGN 000 2013 2012 Interest income 446,451 454,979 Interest expense and similar

STUDENTS TRUST INTERNATIONAL PLANS Canadian $ Students Trust International Plan

STUDENTS TRUST INTERNATIONAL PLANS Canadian $ Students Trust International Plan Financial Statements as of and for the year ended September 30, 2015 and Independent Auditors Report TABLE OF CONTENTS Page

STUDENTS TRUST INTERNATIONAL PLANS Canadian $ Students Trust International Plan Financial Statements as of and for the year ended September 30, 2015 and Independent Auditors Report TABLE OF CONTENTS Page

NOTES TO THE FINANCIAL STATEMENTS

1 GENERAL INFORMATION Kerry Properties Limited (the Company ) is a limited liability company incorporated in Bermuda. The address of its registered office is Canon s Court, 22 Victoria Street, Hamilton

1 GENERAL INFORMATION Kerry Properties Limited (the Company ) is a limited liability company incorporated in Bermuda. The address of its registered office is Canon s Court, 22 Victoria Street, Hamilton

SD Finance pie. Unaudited Financial Statements 31 March 2017

Unaudited Financial Statements 31 March Statement of financial position Income statement Statement of changes in equity Notes to the financial statements 2 3 4-8 Statement of financial position As at 31

Unaudited Financial Statements 31 March Statement of financial position Income statement Statement of changes in equity Notes to the financial statements 2 3 4-8 Statement of financial position As at 31

STUDENTS TRUST INTERNATIONAL PLANS US $ Students Trust International Plan

STUDENTS TRUST INTERNATIONAL PLANS US $ Students Trust International Plan Financial Statements as of and for the year ended September 30, 2015 and Independent Auditors Report TABLE OF CONTENTS Page INDEPENDENT

STUDENTS TRUST INTERNATIONAL PLANS US $ Students Trust International Plan Financial Statements as of and for the year ended September 30, 2015 and Independent Auditors Report TABLE OF CONTENTS Page INDEPENDENT

ANSWERS TO THE MOST FREQUENTLY ASKED QUESTIONS CONCERNING THE FIRST APPLICATION OF IFRS 9

ANSWERS TO THE MOST FREQUENTLY ASKED QUESTIONS CONCERNING THE FIRST APPLICATION OF THE INTERNATIONAL FINANCIAL REPORTING STANDARD 9 FINANCIAL INSTRUMENTS IFRS 9 Last updated: March 2018 1. Measurement

ANSWERS TO THE MOST FREQUENTLY ASKED QUESTIONS CONCERNING THE FIRST APPLICATION OF THE INTERNATIONAL FINANCIAL REPORTING STANDARD 9 FINANCIAL INSTRUMENTS IFRS 9 Last updated: March 2018 1. Measurement

Agenda. 5. Looking ahead. 1. NPLs in IFRS terms. 2. Practical considerations. 3. Harmonisation of IFRS with Banking regulations

0 Agenda 1. NPLs in IFRS terms 2. Practical considerations 3. Harmonisation of IFRS with Banking regulations 4. Important disclosures 5. Looking ahead 6. Conclusion NPLs in IFRS terms Financial instruments

0 Agenda 1. NPLs in IFRS terms 2. Practical considerations 3. Harmonisation of IFRS with Banking regulations 4. Important disclosures 5. Looking ahead 6. Conclusion NPLs in IFRS terms Financial instruments

Notes to the consolidated financial statements

Notes to the consolidated financial statements As at 31 December 1 ACTIVITIES BBK B.S.C. (the Bank ), a public shareholding company, was incorporated in the Kingdom of Bahrain by an Amiri Decree in March

Notes to the consolidated financial statements As at 31 December 1 ACTIVITIES BBK B.S.C. (the Bank ), a public shareholding company, was incorporated in the Kingdom of Bahrain by an Amiri Decree in March

Accounting policies for the year ended 30 June 2016

Accounting policies for the year ended 30 June 2016 The principal accounting policies adopted in preparation of these financial statements are set out below: Group accounting Subsidiaries Subsidiaries

Accounting policies for the year ended 30 June 2016 The principal accounting policies adopted in preparation of these financial statements are set out below: Group accounting Subsidiaries Subsidiaries

16/01/2015. FRS 102 & financial instruments basic and other debt instruments. FRS 102 & financial instruments basic and other debt instruments

FRS 102 & financial instruments basic and other debt instruments 20 January 2015 Download the slides to accompany the webinar /FRFwebinarresources FRS 102 & financial instruments basic and other debt instruments

FRS 102 & financial instruments basic and other debt instruments 20 January 2015 Download the slides to accompany the webinar /FRFwebinarresources FRS 102 & financial instruments basic and other debt instruments

ANZ Bank New Zealand Limited Annual Report and Registered Bank Disclosure Statement

ANZ Bank New Zealand Limited Annual Report and Registered Bank Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2015 NUMBER 79 ISSUED NOVEMBER 2015 ANZ Bank New Zealand Limited Annual Report and Registered

ANZ Bank New Zealand Limited Annual Report and Registered Bank Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2015 NUMBER 79 ISSUED NOVEMBER 2015 ANZ Bank New Zealand Limited Annual Report and Registered

Nordea Bank Polska S.A. Annual Report 2011

Nordea Bank Polska S.A. Annual Report 2011 This document is a free translation of the Polish original. Terminology current in Anglo-Saxon countries has been used where practicable for the purposes of this

Nordea Bank Polska S.A. Annual Report 2011 This document is a free translation of the Polish original. Terminology current in Anglo-Saxon countries has been used where practicable for the purposes of this

REVIEW OF THE CONCEPTUAL FRAMEWORK IASB DISCUSSION PAPER INTERNATIONAL FINANCIAL REPORTING BULLETIN 2013/18

REVIEW OF THE CONCEPTUAL FRAMEWORK IASB DISCUSSION PAPER INTERNATIONAL FINANCIAL REPORTING BULLETIN 2013/18 Summary In July 2013 the International Accounting Standards Board (IASB) released a new Discussion

REVIEW OF THE CONCEPTUAL FRAMEWORK IASB DISCUSSION PAPER INTERNATIONAL FINANCIAL REPORTING BULLETIN 2013/18 Summary In July 2013 the International Accounting Standards Board (IASB) released a new Discussion

Explanation of balance sheet items

Decree No 8 of the Governor of Eesti Pank of 15 June 2016 Amendment of Decree No 6 of the Governor of Eesti Pank of 23 May 2014 Establishment of substantive and formal requirements for the balance sheet

Decree No 8 of the Governor of Eesti Pank of 15 June 2016 Amendment of Decree No 6 of the Governor of Eesti Pank of 23 May 2014 Establishment of substantive and formal requirements for the balance sheet

IFRS 1 - First-Time Adoption of IFRS

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

Open Joint Stock Company Raiffeisen Bank Aval Consolidated Financial Statements

Open Joint Stock Company Raiffeisen Bank Aval Consolidated Financial Statements Year ended 31 December Together with Independent Auditors Report Consolidated Financial Statements CONTENTS INDEPENDENT AUDITORS

Open Joint Stock Company Raiffeisen Bank Aval Consolidated Financial Statements Year ended 31 December Together with Independent Auditors Report Consolidated Financial Statements CONTENTS INDEPENDENT AUDITORS

NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 SEPTEMBER 2014

14 NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES The financial statements are presented in South African Rand, unless otherwise stated, rounded to the nearest million, which is

14 NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES The financial statements are presented in South African Rand, unless otherwise stated, rounded to the nearest million, which is

SUGGESTED ANSWERS AND EXAMINER S COMMENTARY. Question 1. Final exam Diploma in IFRSs 2 July 2012

SUGGESTED ANSWERS AND EXAMINER S COMMENTARY Final exam Diploma in IFRSs 2 July 2012 The suggested answers set out below were used to mark this question. Markers were encouraged to use discretion and to

SUGGESTED ANSWERS AND EXAMINER S COMMENTARY Final exam Diploma in IFRSs 2 July 2012 The suggested answers set out below were used to mark this question. Markers were encouraged to use discretion and to

Consolidated Financial Statements

Alliance Boots GmbH Consolidated Financial Statements for the period ended 31 March 2008 Alliance Boots GmbH 2007/08 Consolidated Financial Statements Contents Independent auditor s report 1 Group income

Alliance Boots GmbH Consolidated Financial Statements for the period ended 31 March 2008 Alliance Boots GmbH 2007/08 Consolidated Financial Statements Contents Independent auditor s report 1 Group income

IFRS amendments after financial crisis

IFRS amendments after financial crisis international financial reporting standards, and int. valuation stand. Supervised by: Yrd.Doç.Dr.:Müge Saltoğlu PhD program of Accounting and finance Prepared by:

IFRS amendments after financial crisis international financial reporting standards, and int. valuation stand. Supervised by: Yrd.Doç.Dr.:Müge Saltoğlu PhD program of Accounting and finance Prepared by:

SMP Bank (OJSC) Consolidated Financial Statements for the year ended 31 December 2011

Consolidated Financial Statements for the year ended 31 December 2011") Consolidated Financial Statements for the year ended 31 December 2011 Contents Independent Auditors Report... 3 Consolidated statement of comprehensive income... 4 Consolidated statement of financial position...

Consolidated Financial Statements for the year ended 31 December 2011 Contents Independent Auditors Report... 3 Consolidated statement of comprehensive income... 4 Consolidated statement of financial position...

Ameriabank cjsc. Financial Statements For the second quarter of 2016

Financial Statements For the second quarter of Contents Statement of profit or loss and other comprehensive income... 3 Statement of financial position... 4 Statement of cash flows... 5 Statement of changes

Financial Statements For the second quarter of Contents Statement of profit or loss and other comprehensive income... 3 Statement of financial position... 4 Statement of cash flows... 5 Statement of changes

Professional Level Essentials Module, Paper P2 (IRL)

") Answers Professional Level Essentials Module, Paper P2 (IRL) Corporate Reporting (Irish) June 2012 Answers 1 (a) Robby Consolidated Statement of Financial Position at 31 May 2012 Assets Non-current assets:

Answers Professional Level Essentials Module, Paper P2 (IRL) Corporate Reporting (Irish) June 2012 Answers 1 (a) Robby Consolidated Statement of Financial Position at 31 May 2012 Assets Non-current assets:

Interim Financial Reporting

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

In depth IFRS 9 Impact on the Pharmaceutical Industry December 2017 No. INT

www.pwc.co.uk In depth IFRS 9 Impact on the Pharmaceutical Industry December 2017 No. INT2017-10 Contents Application of IFRS 9 in the pharmaceutical and life sciences industry 1 Introduction a snapshot

www.pwc.co.uk In depth IFRS 9 Impact on the Pharmaceutical Industry December 2017 No. INT2017-10 Contents Application of IFRS 9 in the pharmaceutical and life sciences industry 1 Introduction a snapshot

KUWAIT BUSINESS TOWN REAL ESTATE COMPANY K.S.C. (CLOSED) AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2012

AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2012") KUWAIT BUSINESS TOWN REAL ESTATE COMPANY K.S.C. (CLOSED) AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2012 Ernst & Young Al Aiban, Al Osaimi & Partners P.O. Box 74 Safat 13001 Safat,

KUWAIT BUSINESS TOWN REAL ESTATE COMPANY K.S.C. (CLOSED) AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2012 Ernst & Young Al Aiban, Al Osaimi & Partners P.O. Box 74 Safat 13001 Safat,

GOODMAN PROPERTY TRUST

GOODMAN PROPERTY TRUST Audited annual results for announcement to the market Reporting Period 12 months to 31 March Previous Reporting Period 12 months to 31 March Amount Percentage Change Revenue from

GOODMAN PROPERTY TRUST Audited annual results for announcement to the market Reporting Period 12 months to 31 March Previous Reporting Period 12 months to 31 March Amount Percentage Change Revenue from

Al-Mubarak IPO Fund (Managed By Arab National Investment Company)

") Al-Mubarak IPO Fund (Managed By Arab National Investment Company) INTERIM CONDENSED FINANCIAL STATEMENTS (UNAUDITED) 30 JUNE 2018 INTERIM CONDENSED STATEMENT OF FINANCIAL POSITION (UNAUDITED) As at 30

Al-Mubarak IPO Fund (Managed By Arab National Investment Company) INTERIM CONDENSED FINANCIAL STATEMENTS (UNAUDITED) 30 JUNE 2018 INTERIM CONDENSED STATEMENT OF FINANCIAL POSITION (UNAUDITED) As at 30

Accounting policies extracted from the 2016 annual consolidated financial statements

Steinhoff International Holdings N.V. (Steinhoff N.V.) is a Netherlands registered company with tax residency in South Africa. The consolidated annual financial statements of Steinhoff N.V. for the period

Steinhoff International Holdings N.V. (Steinhoff N.V.) is a Netherlands registered company with tax residency in South Africa. The consolidated annual financial statements of Steinhoff N.V. for the period

QNB FINANCE LTD. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017

QNB FINANCE LTD. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017 QNB Finance Ltd. Statement of Comprehensive Income 2017 2016 Income Interest Income 260,389 196,027 Expense Interest Expense

QNB FINANCE LTD. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017 QNB Finance Ltd. Statement of Comprehensive Income 2017 2016 Income Interest Income 260,389 196,027 Expense Interest Expense

Notes to the consolidated financial statements (forming part of the financial statements)

") Annual Report and Accounts Notes to the consolidated financial statements 1. Corporate information DP World Limited ( the Company ) was incorporated on 9 August 2006 as a Company Limited by Shares with

Annual Report and Accounts Notes to the consolidated financial statements 1. Corporate information DP World Limited ( the Company ) was incorporated on 9 August 2006 as a Company Limited by Shares with

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION (UNAUDITED) 30 SEPTEMBER 2018

30 SEPTEMBER 2018") AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 2018

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 2018

Consolidated Financial Statements For the Year Ended 31 December 2018

Consolidated Financial Statements For the Year Ended 31 December 2018 Consolidated Income Statement 2018 2017 Notes QR000 QR000 Interest Income 25 50,744,709 41,958,662 Interest Expense 26 (31,711,804)

Consolidated Financial Statements For the Year Ended 31 December 2018 Consolidated Income Statement 2018 2017 Notes QR000 QR000 Interest Income 25 50,744,709 41,958,662 Interest Expense 26 (31,711,804)

The St. Vincent Co-operative Bank Limited Financial Statements Year Ended January 31, 2014

The St. Vincent Co-operative Bank Limited Financial Statements Year Ended January 31, 2014 Contents Page 1 Pages 2-3 Page 4 Page 5 Page 6 Page 7 Pages 8-35 Corporate Information Independent Auditors Report

The St. Vincent Co-operative Bank Limited Financial Statements Year Ended January 31, 2014 Contents Page 1 Pages 2-3 Page 4 Page 5 Page 6 Page 7 Pages 8-35 Corporate Information Independent Auditors Report

Oman Arab Bank (SAOC)

") Oman Arab Bank (SAOC) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Summary of Results 1 Statement of Financial Position 2 Statement

Oman Arab Bank (SAOC) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Summary of Results 1 Statement of Financial Position 2 Statement

QATARI GERMAN COMPANY FOR MEDICAL DEVICES Q.S.C. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2013

FINANCIAL STATEMENTS FINANCIAL STATEMENTS CONTENTS Page(s) Independent auditors report 1-2 Financial statements Statement of financial position 3 Statement of comprehensive income 4 Statement of changes

FINANCIAL STATEMENTS FINANCIAL STATEMENTS CONTENTS Page(s) Independent auditors report 1-2 Financial statements Statement of financial position 3 Statement of comprehensive income 4 Statement of changes

Capital Adequacy Framework (Internal Models Based Approach)

") Capital Adequacy Framework (Internal Models Based Approach) Prudential Supervision Department Document BS2B Issued: December 2012 Ref #4174150 TABLE OF CONTENTS 2 PART 1 INTRODUCTION... 3 PART 2 CAPITAL

Capital Adequacy Framework (Internal Models Based Approach) Prudential Supervision Department Document BS2B Issued: December 2012 Ref #4174150 TABLE OF CONTENTS 2 PART 1 INTRODUCTION... 3 PART 2 CAPITAL

SB JSC HSBC Bank Kazakhstan. Financial Statements for the year ended 31 December 2013

Financial Statements for the year ended 31 December Contents Independent Auditors Report Statement of Profit or Loss and Other Comprehensive Income 5 Statement of Financial Position 6 Statement of Cash

Financial Statements for the year ended 31 December Contents Independent Auditors Report Statement of Profit or Loss and Other Comprehensive Income 5 Statement of Financial Position 6 Statement of Cash

ACCOUNTING POLICIES 1 PRESENTATION OF FINANCIAL STATEMENTS MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 17

20 ACCOUNTING POLICIES FOR THE YEAR ENDED 30 JUNE 2017 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 Basis of preparation These consolidated and separate financial statements have been prepared under the

20 ACCOUNTING POLICIES FOR THE YEAR ENDED 30 JUNE 2017 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 Basis of preparation These consolidated and separate financial statements have been prepared under the

15 August 2005 International Financial Reporting Standards

15 August 2005 International Financial Reporting Standards Overview Bendigo Bank has transitioned its accounting policies and financial reporting from existing Australian standards to Australian equivalents

15 August 2005 International Financial Reporting Standards Overview Bendigo Bank has transitioned its accounting policies and financial reporting from existing Australian standards to Australian equivalents

Good Bank (International) Limited. Illustrative consolidated financial statements for the year ended 31 December 2016

Limited. Illustrative consolidated financial statements for the year ended 31 December 2016") Good Bank (International) Limited Illustrative consolidated financial statements for the year ended 31 December 2016 Contents Abbreviations and key... 2 Introduction... 3 Basis of preparation and presentation...

Good Bank (International) Limited Illustrative consolidated financial statements for the year ended 31 December 2016 Contents Abbreviations and key... 2 Introduction... 3 Basis of preparation and presentation...

Saudi Riyal Money Market Fund (Managed by Alawwal Invest Company)

") Saudi Riyal Money Market Fund (Managed by Alawwal Invest Company) INTERIM CONDENSED FINANCIAL STATEMENTS (UNAUDITED) FOR THE SIX-MONTH PERIOD ENDED 30 JUNE INTERIM CONDENSED STATEMENT OF FINANCIAL POSITION

Saudi Riyal Money Market Fund (Managed by Alawwal Invest Company) INTERIM CONDENSED FINANCIAL STATEMENTS (UNAUDITED) FOR THE SIX-MONTH PERIOD ENDED 30 JUNE INTERIM CONDENSED STATEMENT OF FINANCIAL POSITION

IFRS pocket guide inform.pwc.com

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)