Econ 338c. April 12, 2007

|

|

|

- Warren Atkins

- 5 years ago

- Views:

Transcription

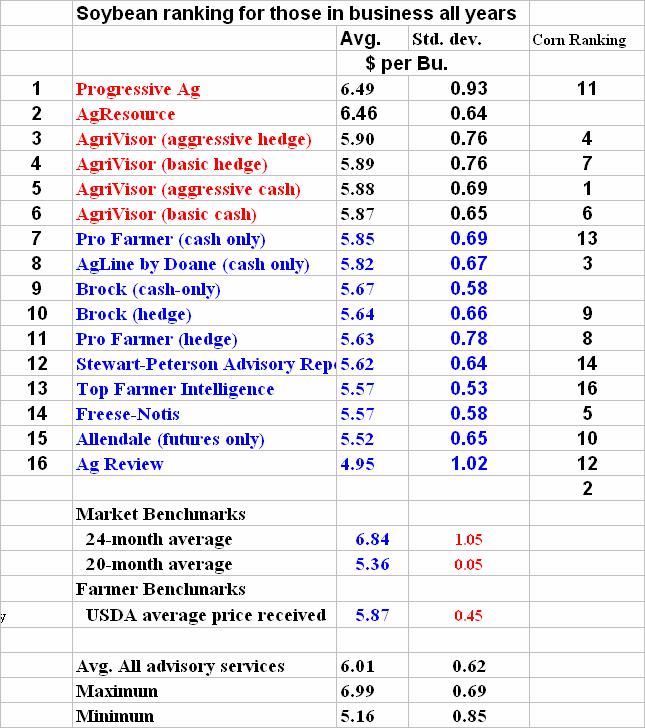

1 60 Econ 338c April 12, 2007

2 10 Traits of a Successful Grain Marketer Starts Early (before planting) Knows production, storage costs & risk bearing ability Understands basis & mkt. carry Follows several relevant markets daily Manages yield risk with revenue insurance Has discipline to price when goals are reached Knows various contracts & when to use them Relies on good sources of market information Has an exit plan Keeps marketing records & evaluates results 61

3 62

4 63

5 Profit Equation for Grain 64 Producers: What are the three key variables? Cost, Price & Yield

6 Cost Data, Francis Childs Avg. Farm Yield: 394 bu./a. 65 Land charge $199/A. Operating Expenses Total Cost $ Break-even price? $2.20 avg. price?

7 Cost Data, Francis Childs Avg. Farm 66 Yield: 394 bu./a. Land charge $199/A. Operating Expenses Total Cost $ Break-even price 1.68/Bu. Profit, $2.20 avg. price /A. On 400A.: $81,952 + $79,600 for owned land

8 Assignment: Working individually or in teams of 2 to 4 people, answer these questions: 1. How much better have advisory service recommendations as a group been over the study period, in average cents per bushel, than the average price received by farmers? corn soybeans 2. For the services as a group, how did their average price compare with the 20-month market benchmark? Corn, Soybeans. 3. For the services as a group, how did their average price compare with the 24-month market benchmark? Corn, Soybeans. Full Report: All Tables: AGMASS Excel Summary table: see class web site Univ. of Illinois does an annual evaluation of Ag Market Advisory Services. You can get the report at the above web address. See Especially the Excel summary table on our class web site. 67

9 Univ. of Illinois annual evaluation of Ag Market Advisory Services, continued Has any one advisory service been able to beat the 24 month market benchmark every year over the study period? 5. How much does the relative ranking of advisory services vary from year to year? 6. Brock is an advisory service used by Cargill in some of its new generation contracts. On average, how has Brock ranked among advisory Services? 7. Pro Farmer is headquartered in Cedar Falls, Iowa. How has it ranked among advisory services, on average? 8. Doane is a long-time farm management and advisory service. How has it ranked among advisory services?

10 69

11 70

12 New-Crop Pricing 71 When is the best chance for reaching price goals? What tools will best fit my needs? What are the risks? How much to sell? months to sell?

13 72

14 Gain vs. harvest cash sales 73

15 Average Annual Net Cash Flow, Alternative 74 Strategies, , 1200 Acres Corn/Soybeans (000 $) No Insur. Cash Renter Buyer-Renter Debt-Free Harvest Pre- Harvest Harvest Pre- Harvest Harvest Pre- Harvest MPCI CRC Pre-Harvest Denotes Pricing Before Harvest, * Primarily With Options

16 Marketing Tools 75 Futures markets Options markets Elevator contracts New-generation contracts Storage on & off the farm Basis as a tool for determining where to sell & a partial answer to When to sell? (Important for all of above + cash sales)

17 Basis: Key to Understanding 76 Regional Variations in Price Three Components of Price: Level = Futures Basis Spreads over Time Basis: Cash Price Minus a SpecificFutures Contract price Example: N.C. Iowa Cash $3.29 May $3.63 (4/05/07) Basis?

18 Ways of Using Basis 77 information for farmer marketing For evaluating forward contracts For pre-harvest & storage hedging decisions For market signals For decisions about ownership of grain or options

19 If harvest Basis is 78 strong Market says sell now If weak: Signals to store & hedge or use hta contract

20 Factors Affecting the Basis Local supply conditions 2. Transportation problems 3. Planting activity 4. Harvesting weather 5. Storage space availability 6. Regional & global supply & demand 7. Handling ability of elevators 8. Processing activity

21 Factors Affecting the Basis Anything slowing demand tends to weaken basis 2. Anything increasing movement into market channels tends to weaken the basis 3. Any problems in handling, storing, or transporting grain weakens the basis

22 How would these factors affect basis? 1. After long delays, farmers have a break in weather & are busy with spring fieldwork 2. Summer weather has turned quite dry and temperatures are 100s across the Corn Belt 3. A hurricane has halted shipments from the U.S. Gulf 4. Elevators are piling grain outside 5. A large local feedlot is out of business 6. Rain is delaying harvest 7. Local ethanol plants are short on corn 81

23 Using Basis to localize 82 futures price for hedging December futures $3.33/bu. Less expected harvest basis 0.45 Less transaction cost 0.01 Expected hedge price $2.87

24 Hedging Grain 83 Protects against price drop Can not follow the market up if Prices rise Pre-harvest corn: Procedure: sell Dec. futures for the amount you want to sell. CBOT futures are 5,000 bu. Contracts Mid-America: 1,000 bu. contracts

25 Risk premium in early new-crop forward corn contracts? 84

26 85

27 Past performance is not a quarantee of future price behavior 86

28 87

29 8-MonthStorage $2.90 Corn 88 Shrinkage below 15% Extra drying Extra handling Interest (8%) Storage charge Quality deterioration & storage shrink Total costs On-farm Off-farm $0.073 (to 13%) $ (Fixed cost) $0.331 $0.425

30 8-MonthStorage 89 $7.00 Soybeans Extra handling Interest (8%) Storage charge Quality deterioration & storage shrink Total costs On-farm Off-farm (Fixed cost) $0.425 $0.564

31 Variable Costs of Corn Storage 90 $2.00 $1.95 $1.90 $1.85 $ /2002 Corn Crop (through 04/03/02): Average Iowa Price and Cost of Ownership hdg. return Off-farm On Farm Interest + other costs Interest Only $1.75 $1.70 $1.65 $1.60 Example Costs of Ownership: 1 cent per bu. per month storage + 7.5% Interest. Costs start 10/24/01 O N D J F M A M J J

32 91

33 92

34 93

35 94

36 If harvest Basis is 95 strong Market says sell now Is it better to buy futures than store? Will cash & futures go up in sync.? Example: Harv. Cash 2.80, July fut.3.55 Next spring: cash 2.95, July fut Gain from cash storage: $0.15 Gain from July futures? Net storage return with $0.22 cost?

37 Keeping Basis Records for Farm Marketing Decide what markets are relevant Daily record of cash & futures prices ideal Once/week is adequate--thursday Get current cash & forward contract bids if available Update continually Keep charts Iowa district basis may be starting point Excel: good for basis analysis 96

38 PRICING DECISION CHART 97 ALTERNATIVES 1. Store and wait to price 2. Delayed price contract 3. Min. price contract variable basis Futures Price Up ALTERNATIVES 1. Basis contract 2. Sell cash and buy futures (long) 3. Buy call 4. Min. price contract set basis Strengthen Basis Expected Change Basis Weaken ALTERNATIVES 1. Hedge 2. Hedge to arrive Non-Roll, basis not set 3. Put option Futures Price Down ALTERNATIVES 1. Cash sales 2. Forward contract 3. Hedge to arrive fixed basis

39 Grain Contracts: Areas of 98 Risk Exposure Price Level Basis Spreads (Intra-and Inter-Year) Options volatility risk Production risk Counter-party risk Control risk Tax risk

40 Types of conventional grain contracts Forward contract: establishes price & basis Delayed price: neither is established Price later: same as above (credit sale) Hedge-to-arrive (non-roll): establishes futures, but not basis Delayed-payment: shifts income for tax purposes Basis contract: establishes basis, not futures Minimum-price: retains upward flexibility 99

41 Traditional Grain 100 Contracts Forward contract: locks in price level, basis, spreads Hedge to Arrive: does not lock in Basis Basis Contract: locks in basis but not price Price Later contract: doesn t lock in either one (You lose ownership cash out LDPs first)

42 Traditional Grain 101 Contracts Premium offer contract Typically involves sale of options & farmer potential sale commitment in next season

43 Minimum Price 102 Contract Establishes a floor price & lets you follow the market higher if it goes up Elevators add call option purchase to forward contract Locks in current price level & basis Farmer pays cost of buying the call option Typically used for retaining ownership into summer About 80% of time, corn calls will be worthless

44 Dec Corn 103 Dec. 05 high $ /04/04 Low: $ /18/05 & 2/09/05 Note strong incentive to monitor New crop pricing opportunities as much as months ahead of harvest, especially for high-cost producer. Price data from Don Rose, U.S. Commodities, Des Moines, IA

45 Dec Corn 104 Price data from Don Rose, U.S. Commodities, Des Moines, IA

46 Dec Corn 105

47 Dec Corn 106 Price data from Don Rose, U.S. Commodities, Des Moines, IA

48 Dec Corn 107 Price data from Don Rose, U.S. Commodities, Des Moines, IA

49 Dec Corn 108

50 Dec Corn 109

51 110 Nov. Soybeans 2003 Price data from Don Rose, U.S. Commodities, Des Moines, IA

52 Nov. Soybeans Price data from Don Rose, U.S. Commodities, Des Moines, IA

53 Nov. Soybeans Price data from Don Rose, U.S. Commodities, Des Moines, IA

54 Nov. Soybeans Price data from Don Rose, U.S. Commodities, Des Moines, IA

55 Nov. Soybeans Price data from Don Rose, U.S. Commodities, Des Moines, IA

56 Nov. Soybeans Price data from Don Rose, U.S. Commodities, Des Moines, IA

57 Nov. Soybeans Price data from Don Rose, U.S. Commodities, Des Moines, IA

58 Yield Deviation from Trend strongly Influences Price Deviation vs. Loan Rate % of time yields are 8% or more above trend 40% of years had yield 8% or more above trend 20% of years had yield 8% or more below trend

59 Corn yields, selected Iowa counties 118 IA. Avg. Obrien Story Taylor Scott Avg St.Dev

60 Refresher on Options Markets 119 Two Types: Puts & Calls (CBOT) Buying Puts: Insure against lower prices Buying Calls: lets you follow market higher after a cash sale No further market expense after buying Cost: premium plus brokerage charge Selling puts: you have an obligation to sell grain at strike price if market goes lower Maximum gain = initial premium

61 120 ricing 50% of yield with puts Declining price : put value tends to rise, adds value to half of crop Rising price:value of 100% of crop increases; only cost is options prm. + brokerage Unchanged price: Worst-case? Premium lost, price doesn t rise

62 Determining Minimum 121 Price With Put Purchase Select Strike Price: $3.50 Deduct: expected harv. basis premium transaction cost Expected Minimum Price $2.89

63 Corn Put Example, May 18, $2.60 put prem.: $.16/bu. Min. price:$ basis = $2.04 Sept. 30 put prem.=$.52, fut. =$2.08 Harvest Cash corn = $1.55 Corn priced with puts: added value: $ = +$.36 Upward price flexibility retained, can store, collect LDP, hedge for May 2001 Gain on 80% of 600 A. corn: $25,900 Hedge gain: $0.50/bu. or $36,000 on 600 A.

64 Difference on 600 A. corn, 80% yld.:$64,000 Corn Put Example, If prices had risen sharply: $2.60 put prem., May 18: $.16/bu. Min. price:$ basis= $2.04 Sept. prices for Dec. corn: $3.60 Sept. 30 put prem.= $0 Harvest Cash corn = $3.25 Corn priced with puts: Net price $ put prem. = $3.09/Bu. Corn Contracted in May: $2.20/bu.

65 Next Week (April 19) 124 Steve Johnson will teaching, with help from Ed Kordick, Iowa Farm Bureau Program: winning the game a simulated marketing year & you do the marketing April, 26 will be review session for the final Final will be take-home final, available on the class web site Final must be turned in to Cindy Pease, 460 Heady Hall by no later than May 4, 2007

GRAIN MARKETS SENSITIVE TO EXPORTS, SOUTH AMERICAN WEATHER

December 15, 1999 Ames, Iowa Econ. Info. 1779 GRAIN MARKETS SENSITIVE TO EXPORTS, SOUTH AMERICAN WEATHER October, November, and the first 10 days of December were unusually dry over a large part of southern

December 15, 1999 Ames, Iowa Econ. Info. 1779 GRAIN MARKETS SENSITIVE TO EXPORTS, SOUTH AMERICAN WEATHER October, November, and the first 10 days of December were unusually dry over a large part of southern

Pulling the Marketing Trigger

Pulling the Marketing Trigger Robert Wisner Iowa State University Why Marketing is Critical Typical Corn Net Profit Margin, Past Years: $.30/ bu. $.10 increase in Price = 33% increase in Net Returns Also

Pulling the Marketing Trigger Robert Wisner Iowa State University Why Marketing is Critical Typical Corn Net Profit Margin, Past Years: $.30/ bu. $.10 increase in Price = 33% increase in Net Returns Also

Section III Advanced Pricing Tools. Chapter 17: Selling grain and buying call options to establish a minimum price

Section III Chapter 17: Selling grain and buying call options to establish a minimum price Learning objectives Selling grain and buying call options to establish a minimum price Key terms Paper farming:

Section III Chapter 17: Selling grain and buying call options to establish a minimum price Learning objectives Selling grain and buying call options to establish a minimum price Key terms Paper farming:

Storing Unpriced Grain: Strategies & Tools

Storing Unpriced Grain: Strategies & Tools December 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Crop

Storing Unpriced Grain: Strategies & Tools December 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Crop

UK Grain Marketing Series January 19, Todd D. Davis Assistant Extension Professor. Economics

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

HEDGING WITH FUTURES AND BASIS

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

December 6-7, Steven D. Johnson. Farm & Ag Business Management Specialist

December 6-7, 2018 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management 1 Learning Objectives Highlight Current Corn

December 6-7, 2018 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management 1 Learning Objectives Highlight Current Corn

Suggested Schedule of Educational Material (cont.)

") Suggested Schedule of Educational Material (cont.) SECOND SESSION: Strategies to Get the Best Price Look at marketing tools Seasonality Basis Spreads Quality Differentials Developing a basic marketing

Suggested Schedule of Educational Material (cont.) SECOND SESSION: Strategies to Get the Best Price Look at marketing tools Seasonality Basis Spreads Quality Differentials Developing a basic marketing

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry Nathan Thompson & James Mintert Purdue Center for Commercial Agriculture Many Different Ways to Price Grain Today 1) Spot

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry Nathan Thompson & James Mintert Purdue Center for Commercial Agriculture Many Different Ways to Price Grain Today 1) Spot

Considerations When Using Grain Contracts

E-231 RM2-38.0 12-09 Risk Management Considerations When Using Grain Contracts Robert Wisner, Mark Welch and Dean McCorkle* The grain industry has developed several new tools to help farmers manage increasing

E-231 RM2-38.0 12-09 Risk Management Considerations When Using Grain Contracts Robert Wisner, Mark Welch and Dean McCorkle* The grain industry has developed several new tools to help farmers manage increasing

Econ 337 Spring 2015 Due 10am 100 points possible

Econ 337 Spring 2015 Final Due 5/4/2015 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Basis = price price 2. A bear thinks prices will. 3. A bull thinks prices will. 4. are willing to

Econ 337 Spring 2015 Final Due 5/4/2015 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Basis = price price 2. A bear thinks prices will. 3. A bull thinks prices will. 4. are willing to

Basis: The price difference between the cash price at a specific location and the price of a specific futures contract.

Section I Chapter 8: Basis Learning objectives The relationship between cash and futures prices Basis patterns Basis in different regions Speculators trade price, hedgers trade basis Key terms Basis: The

Section I Chapter 8: Basis Learning objectives The relationship between cash and futures prices Basis patterns Basis in different regions Speculators trade price, hedgers trade basis Key terms Basis: The

Table of Contents Activity Table

Table of Contents Chapter #1: Successful Market Planning... 1 Chapter #2: Futures Price Movements... 4 Chapter #3: Basis Movements... 10 Chapter #4: Using Crop Marketing Contracts... 13 Chapter #5: Carrying

Table of Contents Chapter #1: Successful Market Planning... 1 Chapter #2: Futures Price Movements... 4 Chapter #3: Basis Movements... 10 Chapter #4: Using Crop Marketing Contracts... 13 Chapter #5: Carrying

Considerations When Using Grain Contracts

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

2015 New Crop Marketing. Ed Kordick Iowa Farm Bureau Federation. February, Pre-harvest marketing with Revenue Protection Crop Insurance

2015 New Crop Marketing Ed Kordick Iowa Farm Bureau Federation February, 2015 Objectives Get back to the basics: Understand the tools, Have a revenue perspective And realistic goals Pre-harvest marketing

2015 New Crop Marketing Ed Kordick Iowa Farm Bureau Federation February, 2015 Objectives Get back to the basics: Understand the tools, Have a revenue perspective And realistic goals Pre-harvest marketing

ACE 427 Spring Lecture 6. by Professor Scott H. Irwin

ACE 427 Spring 2013 Lecture 6 Forecasting Crop Prices with Futures Prices by Professor Scott H. Irwin Required Reading: Schwager, J.D. Ch. 2: For Beginners Only. Schwager on Futures: Fundamental Analysis,

ACE 427 Spring 2013 Lecture 6 Forecasting Crop Prices with Futures Prices by Professor Scott H. Irwin Required Reading: Schwager, J.D. Ch. 2: For Beginners Only. Schwager on Futures: Fundamental Analysis,

Econ 337 Spring 2014 Due 10am 100 points possible

Econ 337 Spring 2014 Final Due 5/7/2014 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Price discovery is the process by which and arrive at a specific price for a given lot of produce

Econ 337 Spring 2014 Final Due 5/7/2014 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Price discovery is the process by which and arrive at a specific price for a given lot of produce

Crop Storage Analysis: Program Overview

Crop Storage Analysis: Program Overview The Crop Storage Analysis program aids farmers in making crop storage decisions. The program compares selling grain at harvest to selling grain one to twelve months

Crop Storage Analysis: Program Overview The Crop Storage Analysis program aids farmers in making crop storage decisions. The program compares selling grain at harvest to selling grain one to twelve months

Primary and Alternative Crop Budgets along with Marketing for Presented by: Josh Tjosaas, Northland College FBM

Primary and Alternative Crop Budgets along with Marketing for 2019 Presented by: Josh Tjosaas, Northland College FBM Quick Quiz Which farmer is the most profitable per acre with Spring Wheat at $6.00 per

Primary and Alternative Crop Budgets along with Marketing for 2019 Presented by: Josh Tjosaas, Northland College FBM Quick Quiz Which farmer is the most profitable per acre with Spring Wheat at $6.00 per

Price Trend Effects On Cash Sales & Forward Contracts. Grain Marketing Principles & Tools Cash Grain Basis, Forward Contracts, Futures & Options

Grain Marketing Principles & Tools Cash Grain Basis, Forward Contracts, Futures & Options Dr. Daniel M. O Brien Extension Agricultural Economist K-State Research and Extension Price Trend Effects On Cash

Grain Marketing Principles & Tools Cash Grain Basis, Forward Contracts, Futures & Options Dr. Daniel M. O Brien Extension Agricultural Economist K-State Research and Extension Price Trend Effects On Cash

New Generation Grain Contracts

New Generation Grain Contracts Econ 338c April 19, 2007 Steven D. Johnson Farm Management Field Specialist Presentation Objectives Highlight 7 Megatrends in the Grain Industry Identify Producer Challenges

New Generation Grain Contracts Econ 338c April 19, 2007 Steven D. Johnson Farm Management Field Specialist Presentation Objectives Highlight 7 Megatrends in the Grain Industry Identify Producer Challenges

Crops Marketing and Management Update

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2017 (2) February 16, 2017 Topics

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2017 (2) February 16, 2017 Topics

Steven D. Johnson. Presentation Objectives

January 30, 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Presentation Objectives Define Shallow Loss

January 30, 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Presentation Objectives Define Shallow Loss

New Generation Grain Contracts Decision Contracts

New Generation Grain Contracts Decision Contracts MARKET BASED RISK MANAGEMENT FOR AGRICULTURE September 2006 Iowa State University Regis Lefaucheur Decision Commodities, LLC 614 Billy Sunday Rd., Suite

New Generation Grain Contracts Decision Contracts MARKET BASED RISK MANAGEMENT FOR AGRICULTURE September 2006 Iowa State University Regis Lefaucheur Decision Commodities, LLC 614 Billy Sunday Rd., Suite

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Module 12. Alternative Yield and Price Risk Management Tools for Wheat

Topics Module 12 Alternative Yield and Price Risk Management Tools for Wheat George Flaskerud, North Dakota State University Bruce A. Babcock, Iowa State University Art Barnaby, Kansas State University

Topics Module 12 Alternative Yield and Price Risk Management Tools for Wheat George Flaskerud, North Dakota State University Bruce A. Babcock, Iowa State University Art Barnaby, Kansas State University

Price-Risk Management in Grain Marketing

Price-Risk Management in Grain Marketing for North Carolina, South Carolina, and Georgia Nicholas E. Piggott George A. Shumaker, Charles E. Curtis Jr. North Carolina State University University of Georgia

Price-Risk Management in Grain Marketing for North Carolina, South Carolina, and Georgia Nicholas E. Piggott George A. Shumaker, Charles E. Curtis Jr. North Carolina State University University of Georgia

1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures contract.

Econ 337 Name Midterm Spring 2017 100 points possible 3/28/2017 Fill in the blanks (2 points each) 1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures

Econ 337 Name Midterm Spring 2017 100 points possible 3/28/2017 Fill in the blanks (2 points each) 1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures

Basis for Grains. Why is basis predictable?

Basis for Grains Why is basis predictable? Average basis levels (expectations) are determined by transportation and storage costs associated with the commodity. Variations in basis levels (outcomes) are

Basis for Grains Why is basis predictable? Average basis levels (expectations) are determined by transportation and storage costs associated with the commodity. Variations in basis levels (outcomes) are

Grain Marketing. Innovative. Responsive. Trusted.

Grain Marketing Extension is a Division of the Institute of Agriculture and Natural Resources at the University of Nebraska Lincoln cooperating with the Counties and the United States Department of Agriculture.

Grain Marketing Extension is a Division of the Institute of Agriculture and Natural Resources at the University of Nebraska Lincoln cooperating with the Counties and the United States Department of Agriculture.

Crops Marketing and Management Update

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (2) February 14, 2018 Topics

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (2) February 14, 2018 Topics

Grain Market Prospects for 2017

Grain Market Prospects for 2017 A Test Drive of 2017 Grain Sales Strategies Jewell, Kansas January 10, 2017 DANIEL O BRIEN EXTENSION AGRICULTURAL ECONOMIST Probability of Corn Futures Trends Examining

Grain Market Prospects for 2017 A Test Drive of 2017 Grain Sales Strategies Jewell, Kansas January 10, 2017 DANIEL O BRIEN EXTENSION AGRICULTURAL ECONOMIST Probability of Corn Futures Trends Examining

Post-Harvest Marketing Alternatives

Curriculum Guide I. Goals and Objectives A. Understand the benefits of pricing grain prior to planting for post harvest sales. B. Learn and understand the mechanics of several post-harvest marketing strategies.

Curriculum Guide I. Goals and Objectives A. Understand the benefits of pricing grain prior to planting for post harvest sales. B. Learn and understand the mechanics of several post-harvest marketing strategies.

Commodity Programs in 2014 Farm Bill. Key Provisions

Commodity Programs in 2014 Farm Bill Gary Schnitkey, Jonathan Coppess, Nick Paulson, and Carl Zulauf University of Illinois The Ohio State University (February 13, 2014) 1 Key Provisions Eliminates direct,

Commodity Programs in 2014 Farm Bill Gary Schnitkey, Jonathan Coppess, Nick Paulson, and Carl Zulauf University of Illinois The Ohio State University (February 13, 2014) 1 Key Provisions Eliminates direct,

factors that affect marketing

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

The Minimum Price Contract

The Minimum Price Contract Purpose of a Minimum Price Contract Minimum price contracts are one of the marketing tools available to producers to help them cope with decreases in farm program support, price

The Minimum Price Contract Purpose of a Minimum Price Contract Minimum price contracts are one of the marketing tools available to producers to help them cope with decreases in farm program support, price

Informed Storage: Understanding the Risks and Opportunities

Art Informed Storage: Understanding the Risks and Opportunities Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The

Art Informed Storage: Understanding the Risks and Opportunities Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The

Post Harvest Marketing Tips

Post Harvest Marketing Tips (from my best friends) Edward Usset Grain Marketing Economist, University of Minnesota usset001@umn.edu Corn & Soybean Digest columnist Center for Farm Financial Management

Post Harvest Marketing Tips (from my best friends) Edward Usset Grain Marketing Economist, University of Minnesota usset001@umn.edu Corn & Soybean Digest columnist Center for Farm Financial Management

Using Hedging in a Marketing Program Hedging is a valuable tool to use in implementing

File A2-61 December 2006 www.extension.iastate.edu/agdm Using Hedging in a Marketing Program Hedging is a valuable tool to use in implementing a grain marketing program. Additional information on hedging

File A2-61 December 2006 www.extension.iastate.edu/agdm Using Hedging in a Marketing Program Hedging is a valuable tool to use in implementing a grain marketing program. Additional information on hedging

Don t get Caught with Your Marketing and Crop Insurance on the Wrong Side of the Basis When it Narrows 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Crops Marketing and Management Update

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (3) March 11, 2018 Topics in

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (3) March 11, 2018 Topics in

Introduction to Futures & Options Markets

Introduction to Futures & Options Markets Kevin McNew Montana State University Marketing Your Crop Marketing: knowing when and how to price your crop. When Planting Pre-Harvest Harvest Post-Harvest How

Introduction to Futures & Options Markets Kevin McNew Montana State University Marketing Your Crop Marketing: knowing when and how to price your crop. When Planting Pre-Harvest Harvest Post-Harvest How

Crop Risk Management

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Creating Your Marketing Plan

Creating Your Marketing Plan Jeff Peterson Heartland Farm Partners 402 366 4694 jeffpeterson@heartlandfarmpartners.com www.heartlandfarmpartners.com Topics Developing a marketing plan Answering the essential

Creating Your Marketing Plan Jeff Peterson Heartland Farm Partners 402 366 4694 jeffpeterson@heartlandfarmpartners.com www.heartlandfarmpartners.com Topics Developing a marketing plan Answering the essential

2013 Risk and Profit Conference Breakout Session Presenters. 4. Basics of Futures and Options: Part 1

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

1997 Pricing Performance of Market Advisory Services for Corn and Soybeans. Thomas E. Jackson, Scott H. Irwin, and Darrel L. Good

1997 Pricing Performance of Market Advisory Services for Corn and Soybeans by Thomas E. Jackson, Scott H. Irwin, and Darrel L. Good 1997 Pricing Performance of Market Advisory Services for Corn and Soybeans

1997 Pricing Performance of Market Advisory Services for Corn and Soybeans by Thomas E. Jackson, Scott H. Irwin, and Darrel L. Good 1997 Pricing Performance of Market Advisory Services for Corn and Soybeans

Turner s Take WASDE Expectations vs. Sept WASDE report:

Published by: Craig Turner 11/4/2013 4:02:09 PM In this issue 1) CORN: USDA Friday exected to be bearish. Looking to short Corn ahead of WASDE 2) SOYBEANS: Short Bean Ideas with Long Call Protection 3)

Published by: Craig Turner 11/4/2013 4:02:09 PM In this issue 1) CORN: USDA Friday exected to be bearish. Looking to short Corn ahead of WASDE 2) SOYBEANS: Short Bean Ideas with Long Call Protection 3)

Strike prices are listed at predetermined price levels for each commodity: every 25 cents for soybeans, and 10 cents for corn.

Types of Options If you buy an option to buy futures, you own a call option. If you buy an option to sell futures, you own a put option. Call and put options are separate and distinct options. Calls and

Types of Options If you buy an option to buy futures, you own a call option. If you buy an option to sell futures, you own a put option. Call and put options are separate and distinct options. Calls and

MARKETING ALTERNATIVES

2018 CONTRACT GUIDE MARKETING ALTERNATIVES We, at Crossroads Cooperative Association, would like to offer various marketing alternatives to our producer customers. Each alternative has its place and value

2018 CONTRACT GUIDE MARKETING ALTERNATIVES We, at Crossroads Cooperative Association, would like to offer various marketing alternatives to our producer customers. Each alternative has its place and value

Marketing 101: Knowing the tools in your marketing toolbox and when to use them

Marketing 101: Knowing the tools in your marketing toolbox and when to use them Brian Grete Sr. Market Analyst, Pro Farmer Hedger or Cash-Only Marketer? comparing the two Cash-only marketers Fewer tools

Marketing 101: Knowing the tools in your marketing toolbox and when to use them Brian Grete Sr. Market Analyst, Pro Farmer Hedger or Cash-Only Marketer? comparing the two Cash-only marketers Fewer tools

Fall 2017 Crop Outlook Webinar

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

HEDGING WITH FUTURES. Understanding Price Risk

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

Development of a Market Benchmark Price for AgMAS Performance Evaluations. Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson

Development of a Market Benchmark Price for AgMAS Performance Evaluations by Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson Development of a Market Benchmark Price for AgMAS Performance Evaluations

Development of a Market Benchmark Price for AgMAS Performance Evaluations by Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson Development of a Market Benchmark Price for AgMAS Performance Evaluations

Saturday, January 5, Notes from Al

Get This Newsletter Every Saturday from Al Kluis Commodities..."Your Markets, Right Now"...AlKluis.com Saturday, January 5, 2013 Notes from Al Happy New Year and welcome to a volatile 2013. It has been

Get This Newsletter Every Saturday from Al Kluis Commodities..."Your Markets, Right Now"...AlKluis.com Saturday, January 5, 2013 Notes from Al Happy New Year and welcome to a volatile 2013. It has been

CHS Pro Advantage Update- February Corn

CHS Pro Advantage Update- February 2018 Corn Recap and Outlook- The most important thing that happened in corn since our last update is the breakout of the 2 ½ month trading range that had existed prior

CHS Pro Advantage Update- February 2018 Corn Recap and Outlook- The most important thing that happened in corn since our last update is the breakout of the 2 ½ month trading range that had existed prior

Farmer for the day. Do you have what it takes? How did we do?

Farmer for the day Do you have what it takes? How did we do? NC State Farmers Situation: Grain farmer that grows corn and beans Expect to grow 100,000 bushels of corn this year Corn cost of production

Farmer for the day Do you have what it takes? How did we do? NC State Farmers Situation: Grain farmer that grows corn and beans Expect to grow 100,000 bushels of corn this year Corn cost of production

Managing Margins in 2017

Managing Margins in 2017 12 th Farming for the Future Conference Coalition to Support Iowa s Farmers Ames, Iowa Jan. 19, 2017 Alejandro Plastina Assistant Professor plastina@iastate.edu 515-294-6160 Chad

Managing Margins in 2017 12 th Farming for the Future Conference Coalition to Support Iowa s Farmers Ames, Iowa Jan. 19, 2017 Alejandro Plastina Assistant Professor plastina@iastate.edu 515-294-6160 Chad

DEVELOP THE RIGHT PLAN FOR YOU.

DEVELOP THE RIGHT PLAN FOR YOU. The Agricultural Risk Consulting Group LLC Developing and Implementing Sound Risk Management Solutions (866) 574-2724 agriskconsulting.net What should you look for in a

DEVELOP THE RIGHT PLAN FOR YOU. The Agricultural Risk Consulting Group LLC Developing and Implementing Sound Risk Management Solutions (866) 574-2724 agriskconsulting.net What should you look for in a

Developing a Grain Marketing Plan

Developing a Grain Marketing Plan T. Randall Fortenbery Dept. of Ag. And Applied Economics UW - Madison Introduction Most producers develop excellent crop production plans each year. They develop strategies

Developing a Grain Marketing Plan T. Randall Fortenbery Dept. of Ag. And Applied Economics UW - Madison Introduction Most producers develop excellent crop production plans each year. They develop strategies

Commodity products. Grain and Oilseed Hedger's Guide

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

Provide a brief review of futures. Carefully review alternative market

Provide a brief review of futures markets. Carefully review alternative market conditions i and which h marketing strategies work best under alternative conditions. Have an open and interactive discussion!!

Provide a brief review of futures markets. Carefully review alternative market conditions i and which h marketing strategies work best under alternative conditions. Have an open and interactive discussion!!

1. On Jan. 28, 2011, the February 2011 live cattle futures price was $ per hundredweight.

Econ 339X Spring 2011 Homework Due 2/8/2011 65 points possible Short answer (two points each): 1. On Jan. 28, 2011, the February 2011 live cattle futures price was $107.50 per hundredweight. If the cash

Econ 339X Spring 2011 Homework Due 2/8/2011 65 points possible Short answer (two points each): 1. On Jan. 28, 2011, the February 2011 live cattle futures price was $107.50 per hundredweight. If the cash

2002 FSRIA. Farm Security & Rural Investment Act. (2002 Farm Bill) How much money is spent with the United States Department of Agriculture (USDA)?

How much money is spent with the United States Department of Agriculture (USDA)?") 2002 FSRIA Farm Security & Rural Investment Act (2002 Farm Bill) Some general background: How much money is spent with the United States Department of Agriculture (USDA)? How much money is spent on farm

2002 FSRIA Farm Security & Rural Investment Act (2002 Farm Bill) Some general background: How much money is spent with the United States Department of Agriculture (USDA)? How much money is spent on farm

Understanding Markets and Marketing

Art Understanding Markets and Marketing Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The objective of marketing

Art Understanding Markets and Marketing Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The objective of marketing

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs. Gary Schnitkey and Dale Lattz. October 15, 2008 IFEU 08-05

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs Gary Schnitkey and Dale Lattz October 15, 2008 IFEU 08-05 Turmoil within the financial sector has caused concerns about the

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs Gary Schnitkey and Dale Lattz October 15, 2008 IFEU 08-05 Turmoil within the financial sector has caused concerns about the

Crops Marketing and Management Update

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (2) February

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (2) February

ARC vs. PLC Enrollment Decisions

ARC vs. PLC Enrollment Decisions April 2014 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management FSA Commodity Crop

ARC vs. PLC Enrollment Decisions April 2014 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management FSA Commodity Crop

b) (3 pts.) Based on this Balance Sheet, what is the Current Ratio on 12/31/2010? CR = current assets/current liabilities = 320,000 / 200,000 = 1.

(3 pts.) Based on this Balance Sheet, what is the Current Ratio on 12/31/2010? CR = current assets/current liabilities = 320,000 / 200,000 = 1.") AAE 320 Spring 2011 Exam #2 Name: KEY 1) (15 pts. total) Below is a simplified farm Balance Sheet. a) (5 pts.) Use the information given and your knowledge of the relationships among Balance Sheet entries

AAE 320 Spring 2011 Exam #2 Name: KEY 1) (15 pts. total) Below is a simplified farm Balance Sheet. a) (5 pts.) Use the information given and your knowledge of the relationships among Balance Sheet entries

Crop Insurance Strategies for

Crop Insurance Strategies for 2018 Why is Crop Insurance Important for Risk Management? Creates a Foundation to build upon Makes a big impact on marketing throughout the year Changes your Risk/Profitability

Crop Insurance Strategies for 2018 Why is Crop Insurance Important for Risk Management? Creates a Foundation to build upon Makes a big impact on marketing throughout the year Changes your Risk/Profitability

The Pricing Performance of Market Advisory Services in Corn and Soybeans Over : A Non-Technical Summary

The Pricing Performance of Market Advisory Services in Corn and Soybeans Over 1995-2001: A Non-Technical Summary by Scott H. Irwin, Joao Martines-Filho and Darrel L. Good The Pricing Performance of Market

The Pricing Performance of Market Advisory Services in Corn and Soybeans Over 1995-2001: A Non-Technical Summary by Scott H. Irwin, Joao Martines-Filho and Darrel L. Good The Pricing Performance of Market

(Lecture notes for the Week 1 Second session, Wednesday, 2/5/14) Introductory Pricing/Marketing Workshop for Grains, On-Line

Introductory Pricing/Marketing Workshop for Grains, On-Line") (Lecture notes for the Week 1 Second session, Wednesday, 2/5/14) Introductory Pricing/Marketing Workshop for Grains, On-Line Review Futures Market Prices Hilker s version to make some points Think of futures

(Lecture notes for the Week 1 Second session, Wednesday, 2/5/14) Introductory Pricing/Marketing Workshop for Grains, On-Line Review Futures Market Prices Hilker s version to make some points Think of futures

Third Quarter Earnings Call. November 8, 2016

Third Quarter Earnings Call November 8, 2016 Forward Looking Statements & Non-GAAP Measures Certain information discussed today constitutes forward-looking statements. Actual results could differ materially

Third Quarter Earnings Call November 8, 2016 Forward Looking Statements & Non-GAAP Measures Certain information discussed today constitutes forward-looking statements. Actual results could differ materially

Loan Deficiency Payments or the Loan Program?

Loan Deficiency Payments or the Loan Program? Dermot J. Hayes and Bruce A. Babcock Briefing Paper 98-BP 19 September 1998 Center for Agricultural and Rural Development Iowa State University Ames, Iowa

Loan Deficiency Payments or the Loan Program? Dermot J. Hayes and Bruce A. Babcock Briefing Paper 98-BP 19 September 1998 Center for Agricultural and Rural Development Iowa State University Ames, Iowa

Econ 337 Spring 2016 Midterm 3/8/ points possible

Econ 337 Spring 2016 Midterm 3/8/2016 100 points possible Fill in the blanks (2 points each) 1. A put option contains the right to sell a futures contract. 2. A call option contains the right to buy a

Econ 337 Spring 2016 Midterm 3/8/2016 100 points possible Fill in the blanks (2 points each) 1. A put option contains the right to sell a futures contract. 2. A call option contains the right to buy a

Performance of market advisory firms

Price risk management: What to expect? #3 out of 5 articles Performance of market advisory firms Kim B. Anderson & B. Wade Brorsen This is the third of a five part series on managing price (marketing)

Price risk management: What to expect? #3 out of 5 articles Performance of market advisory firms Kim B. Anderson & B. Wade Brorsen This is the third of a five part series on managing price (marketing)

Merchandisers Corner. By Diana Klemme, Vice President, Grain Service Corp., Atlanta, GA

Merchandisers Corner Photo courtesy of the Chicago Board of Trade By Diana Klemme, Vice President, Grain Service Corp., Atlanta, GA Most people hate buying insurance; it means paying premiums with little

Merchandisers Corner Photo courtesy of the Chicago Board of Trade By Diana Klemme, Vice President, Grain Service Corp., Atlanta, GA Most people hate buying insurance; it means paying premiums with little

Crop Marketing 101. Prairie Oat Growers Association Annual meeting Banff, Alberta December 4, 2014

Crop Marketing 101 Prairie Oat Growers Association Annual meeting Banff, Alberta December 4, 2014 Risk in Agriculture Production -weather -insects -disease -weeds Human -injury, illness, death, divorce

Crop Marketing 101 Prairie Oat Growers Association Annual meeting Banff, Alberta December 4, 2014 Risk in Agriculture Production -weather -insects -disease -weeds Human -injury, illness, death, divorce

BUSINESS AND MARKETING TOOLS FOR PROFITABLE FARMING. Summer Crossroads: Volatility and Opportunity. Bryce Knorr Farm Futures Magazine

Summer Crossroads: Volatility and Opportunity Bryce Knorr Farm Futures Magazine Don t Bury The Lead Why were soybeans up more than 50 cents despite higher acres? 2014 crop likely smaller Acreage up in

Summer Crossroads: Volatility and Opportunity Bryce Knorr Farm Futures Magazine Don t Bury The Lead Why were soybeans up more than 50 cents despite higher acres? 2014 crop likely smaller Acreage up in

Has the Presence of the LDP Created Marketing Havoc in Missouri? Joe Parcell, Assistant Professor & Extension Economist

Has the Presence of the LDP Created Marketing Havoc in Missouri? Joe Parcell, Assistant Professor & Extension Economist Beginning in the Fall of 1998 low corn and soybean prices triggered a government

Has the Presence of the LDP Created Marketing Havoc in Missouri? Joe Parcell, Assistant Professor & Extension Economist Beginning in the Fall of 1998 low corn and soybean prices triggered a government

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price By Linwood Hoffman and Michael Beachler 1 U.S. Department of Agriculture Economic Research Service Market and Trade Economics

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price By Linwood Hoffman and Michael Beachler 1 U.S. Department of Agriculture Economic Research Service Market and Trade Economics

Knowing and Managing Grain Basis

Curriculum Guide I. Goals and Objectives A. To learn the definition of basis and gain an understanding of the factors that determine basis. B. To gain an understanding of the seasonal trends in basis.

Curriculum Guide I. Goals and Objectives A. To learn the definition of basis and gain an understanding of the factors that determine basis. B. To gain an understanding of the seasonal trends in basis.

Econ 337 Spring 2019 Homework #3 Due 2/21/19 70 points

Econ 337 Spring 2019 Homework #3 Due 2/21/19 70 points For the following questions use the attached futures and options data. Assume historical expected basis of -$0.30 per bushel and a commission of $0.01

Econ 337 Spring 2019 Homework #3 Due 2/21/19 70 points For the following questions use the attached futures and options data. Assume historical expected basis of -$0.30 per bushel and a commission of $0.01

AGRICULTURAL PRODUCTS. Soybean Crush Reference Guide

AGRICULTURAL PRODUCTS Soybean Crush Reference Guide As the world s largest and most diverse derivatives marketplace, CME Group (cmegroup.com) is where the world comes to manage risk. CME Group exchanges

AGRICULTURAL PRODUCTS Soybean Crush Reference Guide As the world s largest and most diverse derivatives marketplace, CME Group (cmegroup.com) is where the world comes to manage risk. CME Group exchanges

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS. Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000 Larry D. Makus College of Agriculture University of Idaho

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000 Larry D. Makus College of Agriculture University of Idaho

Corn and Soybeans Basis Patterns for Selected Locations in South Dakota: 1999

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange Department of Economics Research Reports Economics 5-15-2000 Corn and Soybeans

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange Department of Economics Research Reports Economics 5-15-2000 Corn and Soybeans

New Generation Grain Marketing Contracts

New Generation Grain Marketing Contracts by Lewis A. Hagedorn, Scott H. Irwin, Darrel L. Good, Joao Martines-Filho, Bruce J. Sherrick, and Gary D. Schnitkey New Generation Grain Marketing Contracts by

New Generation Grain Marketing Contracts by Lewis A. Hagedorn, Scott H. Irwin, Darrel L. Good, Joao Martines-Filho, Bruce J. Sherrick, and Gary D. Schnitkey New Generation Grain Marketing Contracts by

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

How to Write a Pre-Harvest Marketing Plan

How to Write a Pre-Harvest Marketing Plan Edward Usset, Grain Marketing Economist University of Minnesota Columnist, Corn & Soybean Digest usset001@umn.edu www.cffm.umn.edu Three slides that explain the

How to Write a Pre-Harvest Marketing Plan Edward Usset, Grain Marketing Economist University of Minnesota Columnist, Corn & Soybean Digest usset001@umn.edu www.cffm.umn.edu Three slides that explain the

September futures traded to a new low for the move of 3.46 ¾ probing under the June 19 th low. Resistance is at the winter lows of 3.70, the 50% retra

Technical Overview Corn prices have continued to drop and are testing the lows on the nearby contracts from last winter near 3.35, completely retracing the winter/spring rally. The next support is the

Technical Overview Corn prices have continued to drop and are testing the lows on the nearby contracts from last winter near 3.35, completely retracing the winter/spring rally. The next support is the

It s time to book 2018 fertilizer Focus on nitrogen first, using right tool for each market By Bryce Knorr, grain market analyst

It s time to book 2018 fertilizer Focus on nitrogen first, using right tool for each market By Bryce Knorr, grain market analyst A slump in nitrogen costs this summer gives growers a chance to lock in

It s time to book 2018 fertilizer Focus on nitrogen first, using right tool for each market By Bryce Knorr, grain market analyst A slump in nitrogen costs this summer gives growers a chance to lock in

Daily Commentary. Corn (888) Monday, July 22, Today s Trade Action. Today s Closing Prices. Recommendations.

Monday, July 22, Today s Trade Action. Today s Closing Prices. Recommendations.") Corn The market finished lower but off it earlier lows as soybeans supplied support for the corn market today. The USDA cut the good to excellent rating by 3 points in crop condition report released after

Corn The market finished lower but off it earlier lows as soybeans supplied support for the corn market today. The USDA cut the good to excellent rating by 3 points in crop condition report released after

Reinsuring Group Revenue Insurance with. Exchange-Provided Revenue Contracts. Bruce A. Babcock, Dermot J. Hayes, and Steven Griffin

Reinsuring Group Revenue Insurance with Exchange-Provided Revenue Contracts Bruce A. Babcock, Dermot J. Hayes, and Steven Griffin CARD Working Paper 99-WP 212 Center for Agricultural and Rural Development

Reinsuring Group Revenue Insurance with Exchange-Provided Revenue Contracts Bruce A. Babcock, Dermot J. Hayes, and Steven Griffin CARD Working Paper 99-WP 212 Center for Agricultural and Rural Development

When Basis and Spreads Speak, We Listen Tregg Cronin

When Basis and Spreads Speak, We Listen Tregg Cronin Cronin Farms, Inc. Halo Commodities Background Fourth Generation, Century Farm in Gettysburg, SD 8,500 acres of corn, soybeans, spring and winter wheat,

When Basis and Spreads Speak, We Listen Tregg Cronin Cronin Farms, Inc. Halo Commodities Background Fourth Generation, Century Farm in Gettysburg, SD 8,500 acres of corn, soybeans, spring and winter wheat,

Price Risk. Management in December Corn Futures. Wayne D. Purcell Alumni Distinguished Professor Department of Agricultural and Applied Economics

Price Risk Management in December Corn Futures Wayne D. Purcell Alumni Distinguished Professor Department of Agricultural and Applied Economics Agricultural Competitiveness Virginia s Rural Economic Analysis

Price Risk Management in December Corn Futures Wayne D. Purcell Alumni Distinguished Professor Department of Agricultural and Applied Economics Agricultural Competitiveness Virginia s Rural Economic Analysis

VOLATILITY: FRIEND OR ENEMY? YOU DECIDE!

VOLATILITY: FRIEND OR ENEMY? YOU DECIDE! Jared Morgan INTL FCStone Financial Inc. FCM Division Kansas Farm Bureau -- Young Farmers & Ranchers Conference January 25-27, 2019 Manhattan, KS Part 1 DISCLOSURES

VOLATILITY: FRIEND OR ENEMY? YOU DECIDE! Jared Morgan INTL FCStone Financial Inc. FCM Division Kansas Farm Bureau -- Young Farmers & Ranchers Conference January 25-27, 2019 Manhattan, KS Part 1 DISCLOSURES

May 26, 2017 CORN. Planting Progress

May 26, 2017 CORN ENCOURAGING WEEK July corn was strong right out of the gate Monday as the market responded to some weather complications across the Corn Belt. Soybeans came under pressure late in the

May 26, 2017 CORN ENCOURAGING WEEK July corn was strong right out of the gate Monday as the market responded to some weather complications across the Corn Belt. Soybeans came under pressure late in the

Marketing Plans Development & Maintenance

Marketing Plans Development & Maintenance Kevin McNew MSU-Bozeman A Marketing Plan Should Remove emotion from the marketing decision and incorporate financial goals Be consistent with your approach to

Marketing Plans Development & Maintenance Kevin McNew MSU-Bozeman A Marketing Plan Should Remove emotion from the marketing decision and incorporate financial goals Be consistent with your approach to

1998 Income Management for Crop Farmers

1998 Income Management for Crop Farmers Gary Schnitkey and Scott Irwin 1 The fall of 1998 has brought a precipitous drop in grain prices, with harvest-time corn prices below $2.00 per bushel and soybean

1998 Income Management for Crop Farmers Gary Schnitkey and Scott Irwin 1 The fall of 1998 has brought a precipitous drop in grain prices, with harvest-time corn prices below $2.00 per bushel and soybean

Dependable Approved Insurance Providers. 34 full-time risk management professionals. N early $1 Billion in crop insurance coverage

Farm Credit I llinois Risk M anagement at a Glance M any regional offices now host vice presidents and assistant vice presidents of risk management, dedicated to providing the expertise you need. A ll

Farm Credit I llinois Risk M anagement at a Glance M any regional offices now host vice presidents and assistant vice presidents of risk management, dedicated to providing the expertise you need. A ll