Service Models: Tools for Improving Outcomes. Diana Jordan, AIFA Director, Client Experience Unified Trust Company, N.A.

|

|

|

- Adelia Lucas

- 5 years ago

- Views:

Transcription

1 Service Models: Tools for Improving Outcomes Diana Jordan, AIFA Director, Client Experience Unified Trust Company, N.A. 1

2 Welcome! Hello I am Diana Jordan! Diana Jordan is the Director of Client Experience for Unified Trust. With 18 years experience in the industry, Mrs. Jordan joined Unified Trust in 2015 from Sikich LLP, where she was Partner in Charge of Wealth Management and Retirement Plan Services. Prior to that Jordan was a Financial Advisor with Morgan Stanley. 2

3 Presentation Agenda 1. Building a Consultative Practice 2. Developing an Annual Plan Calendar 3. Driving Participant Outcomes 2018 Unified Trust Company, N.A. All Rights Reserved Products and services offered by Unified Trust Company, N.A. are not insured by the FDIC, are not a deposit or other obligation of, or guaranteed by, Unified Trust Company, N.A., and are subject to investment risks, including possible loss of the principal amount invested. 3

4 Building a Consultative Practice

5 Sample Advisory Firm Combination of wealth management and retirement plan services Retirement plan practice Utilizing multiple vendor platforms Plans of various size AUM, participant count and/or number of locations More knowledgeable plan sponsors Focus on outcomes and wellness for participants Industry progression - Funds, Fiduciary and Fee Compression 5

6 Today s Plan Sponsor Advisors need to deliver tangible benefits to plan sponsors and participants. Review and understand your plan sponsor s goals and objectives for the plan Identify potential areas of risk or opportunities for improvement Offer creative and thoughtful solutions Demonstrate your value as a Retirement Plan Services Specialist 6

7 Annual Service Model Team focus on retirement plan services Establish an annual Plan Calendar 1. Fiduciary Review and Oversight 2. Plan Administration 3. Employee Communication Review the Plan Calendar every meeting 7

8 Sample Plan Rural Hospital, Small Community Plan Assets $20,000, Employees One Location Quarterly Retirement Plan Committee Meetings Quarterly Employee Education Group and One-on-One Meetings Advisor Fee Tiered Fee Schedule 0.23% or $46,000 Annually 8

9 First Steps Establish formal retirement plan committee o Beyond management/locations Provide fiduciary training o Initial training for new committee members o Refresher training for committee annually o Fi360 Resources Prudent Investment Practices handbook Develop presentation based on practices which includes your consultative role in oversight of the plan 9

Advisor led/powerpoint")

10 First Steps o Fi360 Resources (continued) Fiduciary Essentials for Defined Contribution Plans (FEDC) Advisor led/powerpoint deck Marketing resources Online training for committee members Certificate of Completion Continuing education for HRCI/SHRM/CFP/CPA 10

11 First Steps Develop Committee Charter and Fiduciary Acknowledgement Fi360 Resources ERISA Counsel Provides indemnification for plan committee members 11

12 Developing an Annual Plan Calendar

13 First Quarter Sample Plan Calendar 13

14 Sample Agenda Follows the same outline as the Plan Calendar. 1. Approve Minutes 2. Fiduciary Review and Oversight a) Key Acceptance Rates Report b) Fiduciary Monitoring Report (FMR) c) Fi360 Investment Review d) Board Year in Review 3. Plan Administration a) SSAE 16 Review 4. Employee Communication a) One-on-One Meetings 5. Meeting Schedule 6. Other Business 14

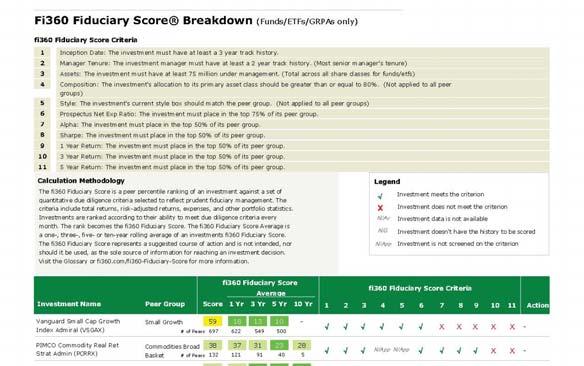

15 Fiduciary Monitoring Report 15

16 Board Year in Review Committee Charter delegates oversight of the plan from the Board of Directors to a defined committee. The Board Year in Review summarizes the activity of the plan during the past year and is presented to the board by a member of the committee on an annual basis. 16

17 Fi360 Investment Review 17

18 SSAE16 Review Statement on Auditing Standards (SSAE) No. 16, Service Organizations, is a widely recognized auditing standard developed by the American Institute of Certified Public Accountants (AICPA). A service auditor's examination performed in accordance with SSAE No. 16 ("SSAE 16 Audit") is widely recognized, because it represents that a service organization has been through an in-depth audit of their control objectives and control activities, which often include controls over information technology and related processes. A Type II report not only includes the service organization's description of controls, but also includes detailed testing of the service organization's controls over a minimum six month period. Include CPA audit firm peer review from 18

19 Minutes Follows the same outline as the Plan Calendar: 1. Fiduciary Review and Oversight 2. Plan Administration 3. Employee Communication 19

20 Second Quarter Sample Plan Calendar 20

21 ERISA 408(b)(2) Notices A Covered Service Provider (CSP) must provide to a responsible plan fiduciary (RPF) a description of the services provided, disclose their status (as a fiduciary or non-fiduciary), describe the compensation expected to be received (direct and indirect), describe any termination fees and how the compensation will be paid. 21

22 ERISA 404(a)(5) Notices The disclosure must include a description of when and how a participant may give investment instructions, the plan s designated investment alternative, the plan s designated investment manager, any changes in the listed information must be provided at least 30 days prior but no more than 90 days before the change becomes effective. 22

23 ERISA 404(a)(5) Notices The vendor must provide all plan related administrative expenses and fee information that may be charged to participant s accounts, all investment related information including the name and type of each designated investment alternative available under the plan, along with performance data, expenses, contact information and comparative data, and a glossary of terms. There is a DOL model comparative chart that should be followed. 23

24 Review Annual Disclosures Identify Covered Service Providers that need to comply with the ERISA 408(b)(2) Fee Disclosure Require receipt of ERISA 408(b)(2) Fee Disclosure in advance of any new plan service arrangements Review both ERISA 408(b)(2) and 404(a)(5) Fee Disclosures to confirm compliance and reasonableness Establish a process to benchmark fees and document the assessment Retain Fee Disclosures in Plan s permanent folder to document ongoing compliance and for future reference 24

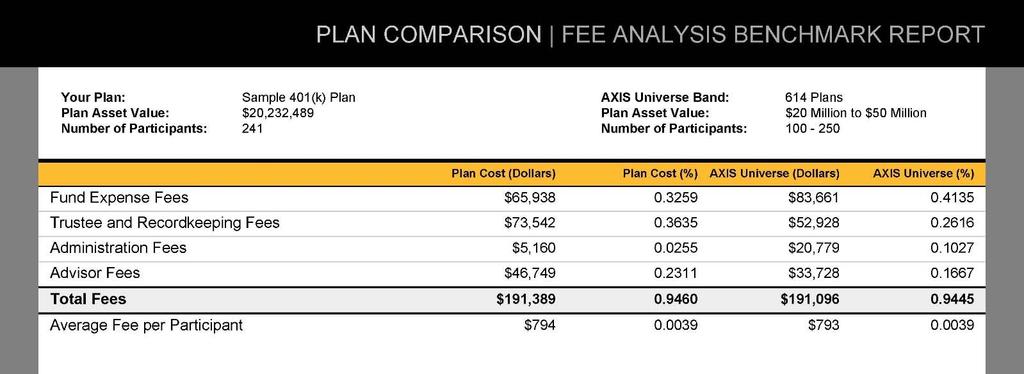

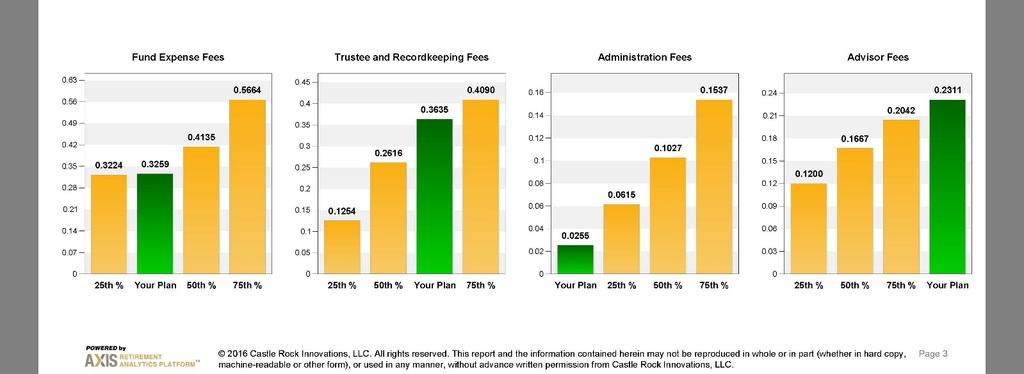

25 Fee Services and Benchmarking

26

27

28

29

30 Loan Policy and Interest Rate Review 30

31 Loan Policy and Interest Rate Review 31

32 Third Quarter Sample Plan Calendar 32

33 Plan Administration Compliance and Administration Testing IRS Form 5500 Plan Audit Plan Design Review and Recommendations 33

34 Plan Design Recommendations Entry Dates Current Document First day of quarter following eligibility requirements Recommendation First day of the month following eligibility requirements Deferral Changes Quarterly With each payroll Automatic Enrollment Auto Escalation Not available Not available Full plan re-enrollment, 6% deferral rate for all employees or continue with current deferral rate, if greater than 6% Full plan re-enrollment to a ceiling of 14%, 2% Automatic escalation April 1, Coincides with Annual Performance Reviews Roth 401(k) Deferrals Not available Add Roth 401(k) deferrals Rollovers Distributions only allowed at separation of service Distributions allowed at any time 34

35 Fourth Quarter Sample Plan Calendar 35

36 Discretionary Trustee Responsibilities Unified Trust Company, serving as the discretionary trustee, provides the highest level of fiduciary protection. 36

37 Discretionary Trustee Responsibilities Unified Trust Company, serving as the discretionary trustee, provides the highest level of fiduciary protection. 37

38 Investment Policy Statement Qualified Default Investment Alternative (QDIA) The QDIA safe harbor protects the plan sponsor from liability for defaulting the participant into the QDIA. ERISA 404(c) The 404(c) safe harbor protects the fiduciary from liability for the actions of the participants. 38

39 Investment Policy Statement Investment Policy Statement Fi360 Prudent Practices Fi360 ERISA Section 404(c) Checklist 39

40 Driving Participant Outcomes

41 The Average 31% Full Funded Percentage of participants on track to retire Kasten, G. The UnifiedPlan Dramatically Increases Retirement Success, 2016 Unified Trust Company 41

42 Annual Education Plan Defines the plan sponsor s goals and objectives for employee communication and education How many of your employees are on track for a successful retirement? What is your target participation rate? What is your target deferral rate? Do you offer Group and/or One on One Meetings? Measure results and update Education Plan annually! 42

43 Employee Education Resource for Participant Questions Targeted Group Meetings o o o Newly Eligible Pre-Retirees Customizing Your Retirement Projection One on One Meetings o Focus on Customizing Retirement Projection with Additional Retirement Information 43

44 Employee Education Targeted Campaigns: o o o Participants with Shortfalls Eligible Not Participating Not Maxing Out Employer Matching Contribution 44

45 Sample Plan Rural Hospital, Small Community Plan Assets $20,000, Employees One Location Quarterly Retirement Plan Committee Meetings Quarterly Employee Education Group and One-on-One Meetings Advisor Fee Tiered Fee Schedule 0.23% or $46,000 Annually 45

46 Key Acceptance Rates 401(k) Plans Success Rate 85% o Success Rate = Number of Participants on Track to Replace Default of 70% of Income in Retirement or Preferred Replacement Percentage Additional Retirement Information provided by 35% of Participants Participation Rate 95% Average Deferral Rate: % vs % Progressive Savings Rate Acceptance 44% 46

47 Key Acceptance Rates Investment Options and Risk Profile o QDIA Managed Account Solution 85% o Risk Based Portfolios 10% o Custom Allocation 5% 47

48 How do you drive these outcomes?

49 Plan Design Driving participant success begins with Intelligent Defaults. Recommend a FULL Plan Re-Enrollment vs. Newly Eligible Employees o Implement Automatic Enrollment at 6% o Implement Auto Escalation at 2% all Employees below Ceiling 49

50 The UnifiedPlan Platform The Pension-like Answer Set a Goal Determine a personal goal for each participant. Replace 70% of current income at Social Security Normal Retirement Age (SSNRA) Measure Measure participant progress each quarter. Provide the ability to customize the retirement projection. Manage Manage the investment. Automatically select investments with the lowest possible risk required to achieve the goal. 50

51 Sample Projected Benefit Statement 51

52 It is much easier for participants to say, Yes to the answer. 52

53 Participants don t want to know how to build a watch.

54 They just want to know the time!

55 Scalable Service Model Team focus on retirement plan services Establish an annual Plan Calendar 1. Fiduciary Review and Oversight 2. Plan Administration 3. Employee Communication Review the Plan Calendar every meeting 55

56 Thanks for attending the session today! If you would like a handout of sample service model handouts for retirement plan committee meetings please me at the address below! Diana Jordan 2353 Alexandria Drive, Suite 100, Lexington, KY (217) Diana.Jordan@unifiedtrust.com

57 Disclosures 1. The UnifiedPlan reporting tool helps investors understand whether they are on course to achieve a successful retirement. The UnifiedPlan uses asset liability matching. The asset is the money forecast to be accumulated and the liability is the amount of money needed to pay for the retirement. For investors who are planning for retirement, the tool estimates the amount of funds required to meet their retirement spending goals and provides alternatives such as delaying retirement or lowering retirement spending for those who may not be able to save the required amount. 2. For investors who are already retired, the tool estimates the confidence that their portfolio will be able to sustain their desired spending throughout retirement. The tool uses a combination of deterministic methods and Monte Carlo simulation that consider factors that include saving and spending levels, long-term market expectations associated with the risk profile selected, pre- and inretirement time horizons, and other sources of outside income. 3. The UnifiedPlan limitations relate to the large number of assumptions used in the analysis. The accuracy of these assumptions directly impacts the quality of the tool's assessment. Potential problems may include, but are not limited to, the use of inaccurate financial data by the investor, the selection of a risk tolerance by the investor that does not represent how their portfolio is actually invested, long term market expectations of risk, return, and inflation that are not achieved in the modeled time frame, the inclusion future income that is never received, and unforeseen life emergencies that require decreased saving before retirement, force an earlier retirement, or increase spending needs during retirement. 4. The UnifiedPlan is highly dependent upon assumptions of annual income and annual savings. Any variances or changes in the figures used should be reported immediately by the plan participant. Unified Trust is not responsible for any discrepancies in the data, or output from the UnifiedPlan tool. 5. All mutual fund and collective investment fund data was gathered from publicly available sources of information such as Standard & Poor s, Morningstar, Zephyr or vendors own websites. We take reasonable care in collecting the data, and believe the data are accurate, but reserve the right to correct any errors. Individual mutual fund or collective fund performance data throughout the document are net of underlying fund expense ratios but gross of addon expenses such as Trustee fees, administration fees, or advisory fees. The performance histories reported are simply dollar-weighted historical returns for the proposed funds and do not reflect the effects of rebalancing or fund replacements. 6. Any past performance information for the illustrated investment selections is not indicative of future returns but is merely a snapshot of historical performance. Past performance is not a guarantee of future performance. The investments are not FDIC insured. 7. Differences will probably exist between prospective and your actual results because events and circumstances frequently do not occur as expected, and those differences may be material, especially when making estimates over extended time periods. All figures are shown in current (inflation adjusted) dollars. The estimated inflation rate used in this analysis may vary over time. 57

58 Disclosures 8. The UnifiedPlan portfolio changes and time line changes for each participant are governed by the Plan Document, the Investment Policy Statement and the Benefit Policy Statement for their Plan. 9. The calculated 70% income replacement goal includes the estimated Social Security benefit. The actual Social Security benefit may be different from the estimated value. 10. Compensation in excess of the IRC 415 limit is excluded. All figures reported in current (inflation-adjusted) real dollars. retirement. For investors who are planning for retirement, the tool estimates the amount of funds required to meet their retirement spending goals and provides alternatives such as delaying retirement or lowering retirement spending for those who may not be able to save the required amount. 13. Projections are made based upon expected asset transfers. Actual transfer amounts may be different and may require a new retirement solution. 11. The projections or other information generated by the tool regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Projected growth of assets is based Unified Trust Company's Projected Future Modeled Returns and the asset allocation of your portfolio for this goal. The graphical representations are an approximation taken from the direct path between the pertinent events tied to your goal. Indices are unmanaged, do not incur management fees or expenses, and cannot be invested in directly. 12. Neither the Plan Sponsor nor Unified Trust can guarantee that any participant will achieve a successful retirement. The UnifiedPlan reporting tool helps investors understand whether they are on course to achieve a successful retirement. The UnifiedPlan uses asset liability matching. The asset is the money forecast to be accumulated and the liability is the amount of money needed to pay for the 58

The UnifiedPlan Dramatically Increases Retirement Success & Improves Plan Cost/Benefit Structure

The UnifiedPlan Dramatically Increases Retirement Success & Improves Plan Cost/Benefit Structure 1 2 DR. GREGORY W. KASTEN UNIFIED TRUST COMPANY, NA The UnifiedPlan Dramatically Increases Retirement Success

The UnifiedPlan Dramatically Increases Retirement Success & Improves Plan Cost/Benefit Structure 1 2 DR. GREGORY W. KASTEN UNIFIED TRUST COMPANY, NA The UnifiedPlan Dramatically Increases Retirement Success

Checklist for Employee Benefit Plan Sponsors

Checklist for Employee Benefit Plan Sponsors 999 Third Avenue, Suite 2800 Seattle WA, 98104 (206) 302-6800 The material appearing in this presentation is for informational purposes only and should not

Checklist for Employee Benefit Plan Sponsors 999 Third Avenue, Suite 2800 Seattle WA, 98104 (206) 302-6800 The material appearing in this presentation is for informational purposes only and should not

401(k)omplete. Offering a 401(k) Has Never Been Easier

omplete. Offering a 401(k) Has Never Been Easier") 401(k)omplete The Small Market Solution from Paychex Retirement Services and LPL Financial Offering a 401(k) Has Never Been Easier The Small Market Solution Preparing for retirement is complex. Paychex

401(k)omplete The Small Market Solution from Paychex Retirement Services and LPL Financial Offering a 401(k) Has Never Been Easier The Small Market Solution Preparing for retirement is complex. Paychex

3(38) Fiduciary Versus 3(21) Fiduciary: What Are the Real Duties and Risks?

Fiduciary Versus 3(21) Fiduciary: What Are the Real Duties and Risks?") 3(38) Fiduciary Versus 3(21) Fiduciary: What Are the Real Duties and Risks? Ary Rosenbaum, Esq. The Rosenbaum Law Firm, P.C. Dr. Gregory W. Kasten Chief Executive Officer Unified Trust Company, NA Most

3(38) Fiduciary Versus 3(21) Fiduciary: What Are the Real Duties and Risks? Ary Rosenbaum, Esq. The Rosenbaum Law Firm, P.C. Dr. Gregory W. Kasten Chief Executive Officer Unified Trust Company, NA Most

ERISA 403(b) Compliance & Administration Plan Data Form

Compliance & Administration Plan Data Form") ERISA 403(b) Compliance & Administration Plan Data Form Page 1 of 4 NewBus-814 (10-2013) ERISA 403 (b) Compliance & Administration Plan Data Form 1 Plan Sponsor Employer Legal Name Employer Mailing Address,

ERISA 403(b) Compliance & Administration Plan Data Form Page 1 of 4 NewBus-814 (10-2013) ERISA 403 (b) Compliance & Administration Plan Data Form 1 Plan Sponsor Employer Legal Name Employer Mailing Address,

Employee benefit plan large filers: Meeting your compliance and fiduciary requirements. April 20, 2016

Employee benefit plan large filers: Meeting your compliance and fiduciary requirements April 20, 2016 1 Your presenters Rose Ann Abraham, CPA Partner Baker Tilly 312 729 8086 roseann.abraham@bakertilly.com

Employee benefit plan large filers: Meeting your compliance and fiduciary requirements April 20, 2016 1 Your presenters Rose Ann Abraham, CPA Partner Baker Tilly 312 729 8086 roseann.abraham@bakertilly.com

Fiduciary Guide. Vested Interest Defined Contribution Plan Services

Vested Interest Defined Contribution Plan Services Fiduciary Guide Your guide to what you should know as a plan fiduciary, understanding Vested Interest services and the value these services provide to

Vested Interest Defined Contribution Plan Services Fiduciary Guide Your guide to what you should know as a plan fiduciary, understanding Vested Interest services and the value these services provide to

4/8/2010. Overview of the New 403(b) Regulations. Overview of 403(b) Issues

Regulations. Overview of 403(b) Issues") The New Regulatory Environment for Sponsors of 403(b) Plans 2003-2010 Multnomah Group, Inc. All rights reserved. Overview of 403(b) Issues Overview of the New Regulations Plan Operations: Universal Availability

The New Regulatory Environment for Sponsors of 403(b) Plans 2003-2010 Multnomah Group, Inc. All rights reserved. Overview of 403(b) Issues Overview of the New Regulations Plan Operations: Universal Availability

Background. 401(k) Plans Automatic Enrollment & Safe Harbor after PPA

Plans Automatic Enrollment & Safe Harbor after PPA") 401(k) Plans Automatic Enrollment & Safe Harbor after PPA Pam Thein Partner, Oppenheimer Wolff & Donnelly LLP Kim Wright - Vice President, Regional Director, Wachovia Retirement Services September 10,

401(k) Plans Automatic Enrollment & Safe Harbor after PPA Pam Thein Partner, Oppenheimer Wolff & Donnelly LLP Kim Wright - Vice President, Regional Director, Wachovia Retirement Services September 10,

FIDUCIARY RESPONSIBILITY AND DEFERRED COMPENSATION PLANS

FIDUCIARY RESPONSIBILITY AND DEFERRED COMPENSATION PLANS November 2017 June 9, 2017 Presented by: Frank Wan Senior Vice President Presented by: Frank Wan, Senior Vice President Burgess Chambers & Associates,

FIDUCIARY RESPONSIBILITY AND DEFERRED COMPENSATION PLANS November 2017 June 9, 2017 Presented by: Frank Wan Senior Vice President Presented by: Frank Wan, Senior Vice President Burgess Chambers & Associates,

PLANavigator. Presented by: Joel Shapiro, J.D., LL.M. ERISA Compliance

PLANavigator Presented by: Joel Shapiro, J.D., LL.M. ERISA Compliance Shifting the Paradigm of Creating Successful Participant Outcomes The goal of a retirement plan is to create successful retirement

PLANavigator Presented by: Joel Shapiro, J.D., LL.M. ERISA Compliance Shifting the Paradigm of Creating Successful Participant Outcomes The goal of a retirement plan is to create successful retirement

Why the UnifiedPlan Is So Effective in Improving Outcomes

Why the UnifiedPlan Is So Effective in Improving Outcomes Dr. Gregory W. Kasten Unified Trust Company, NA Objective outcome data show retirement success is greatly improved with the UnifiedPlan 1. The

Why the UnifiedPlan Is So Effective in Improving Outcomes Dr. Gregory W. Kasten Unified Trust Company, NA Objective outcome data show retirement success is greatly improved with the UnifiedPlan 1. The

Fiduciary Compliance Checklist

Employee Benefit Services Fiduciary Compliance Checklist Plan Fiduciaries are responsible for a variety of notices and duties as part of their responsibilities under ERISA. Fiduciaries must take every

Employee Benefit Services Fiduciary Compliance Checklist Plan Fiduciaries are responsible for a variety of notices and duties as part of their responsibilities under ERISA. Fiduciaries must take every

Fiduciary Guide. Vested Interest Defined Contribution Plan Services

Vested Interest Defined Contribution Plan Services [ ] Fiduciary Guide Your guide to what you should know as plan fiduciary, understanding Vested Interest services and the value of what these services

Vested Interest Defined Contribution Plan Services [ ] Fiduciary Guide Your guide to what you should know as plan fiduciary, understanding Vested Interest services and the value of what these services

Plan Design Guide. A new framework to help benchmark and enhance defined contribution plan effectiveness

Plan Design Guide A new framework to help benchmark and enhance defined contribution plan effectiveness What is your plan s profile? Based on an extensive research study on how plan sponsors make plan

Plan Design Guide A new framework to help benchmark and enhance defined contribution plan effectiveness What is your plan s profile? Based on an extensive research study on how plan sponsors make plan

QDIAs under the Pension Protection Act

QDIAs under the Pension Protection Act RETIREMENT MANAGEMENT SERVICES, LLC 9/14/2015 Rhonda Henry, CPA, APA When Congress passed the Pension Protection Act of 2006 ( PPA ), they addressed a major problem

QDIAs under the Pension Protection Act RETIREMENT MANAGEMENT SERVICES, LLC 9/14/2015 Rhonda Henry, CPA, APA When Congress passed the Pension Protection Act of 2006 ( PPA ), they addressed a major problem

Fiduciary Compliance Checklist Essential Points

Fiduciary Compliance Checklist Essential Points Who are the fiduciaries named under the plan? Defining the Fiduciary Structure Who are the fiduciaries not named under the plan but are performing duties

Fiduciary Compliance Checklist Essential Points Who are the fiduciaries named under the plan? Defining the Fiduciary Structure Who are the fiduciaries not named under the plan but are performing duties

Contents. Introduction to PSCA s 58th Annual Survey Respondent Demographics Employee Eligibility Participant Contributions...

Introduction to PSCA s 58th Annual Survey... 1 Respondent Demographics... 2 Table 1 Respondents by plan size and plan type... 2 Table 2 Respondents by total plan assets and plan type... 4 Table 3 Respondents

Introduction to PSCA s 58th Annual Survey... 1 Respondent Demographics... 2 Table 1 Respondents by plan size and plan type... 2 Table 2 Respondents by total plan assets and plan type... 4 Table 3 Respondents

EMPLOYEE BENEFIT PLANS FOR NFPs. Bertha Minnihan, Partner, Moss Adams LLP Brad Wall, Partner, Moss Adams LLP

EMPLOYEE BENEFIT PLANS FOR NFPs Bertha Minnihan, Partner, Moss Adams LLP Brad Wall, Partner, Moss Adams LLP 1 BERTHA MINNIHAN Bertha has nearly 20 years of experience in public accounting and serves as

EMPLOYEE BENEFIT PLANS FOR NFPs Bertha Minnihan, Partner, Moss Adams LLP Brad Wall, Partner, Moss Adams LLP 1 BERTHA MINNIHAN Bertha has nearly 20 years of experience in public accounting and serves as

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES 1 Today s Agenda Understand where ERISA applies to retirement

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES 1 Today s Agenda Understand where ERISA applies to retirement

Launching a New Line of Business to Serve Plan Sponsors and Their Participants

PROFILES IN EVOLVING BUSINESS MODELS Launching a New Line of Business to Serve Plan Sponsors and Their Participants An advisory firm formalizes its support for retirement plans to diversify its revenue

PROFILES IN EVOLVING BUSINESS MODELS Launching a New Line of Business to Serve Plan Sponsors and Their Participants An advisory firm formalizes its support for retirement plans to diversify its revenue

PLAN DESIGN STRATEGIES FOR SUCCESS

PLAN DESIGN STRATEGIES FOR SUCCESS PLAN DESIGN STRATEGIES FOR SUCCESS EXECUTIVE SUMMARY In the past, many financial advisors centered their retirement plan service model around their investment expertise.

PLAN DESIGN STRATEGIES FOR SUCCESS PLAN DESIGN STRATEGIES FOR SUCCESS EXECUTIVE SUMMARY In the past, many financial advisors centered their retirement plan service model around their investment expertise.

The Economics of Plan Profitability

The Economics of Plan Profitability Anders D. Smith, CIMA, CFP, AIFA Senior Vice President, National Sales Manager DCIO & Strategic Platforms Nuveen Investments www.nuveen.com Agenda 1) Defining profitability

The Economics of Plan Profitability Anders D. Smith, CIMA, CFP, AIFA Senior Vice President, National Sales Manager DCIO & Strategic Platforms Nuveen Investments www.nuveen.com Agenda 1) Defining profitability

A World of Change and Opportunity in 401(k) Plans

Plans") A World of Change and Opportunity in 401(k) Plans Steven Kaye, CFP, ChFC, CLU, CEBS, RHU, AAMS, CRC, AIF President AEPG Wealth Strategies 25 Independence Blvd. Suite 102, Warren, NJ 07059 Phone: 908-757-5600

A World of Change and Opportunity in 401(k) Plans Steven Kaye, CFP, ChFC, CLU, CEBS, RHU, AAMS, CRC, AIF President AEPG Wealth Strategies 25 Independence Blvd. Suite 102, Warren, NJ 07059 Phone: 908-757-5600

Fiduciary Fundamentals

Fiduciary Fundamentals Basics and Best Practices RETIREMENT & BENEFIT PLAN SERVICES At Bank of America Merrill Lynch, we understand the important role that you, the plan fiduciary, serve in maintaining

Fiduciary Fundamentals Basics and Best Practices RETIREMENT & BENEFIT PLAN SERVICES At Bank of America Merrill Lynch, we understand the important role that you, the plan fiduciary, serve in maintaining

ERISA Fiduciary Responsibilities for 403(b) Plans: Keys to Implementation

Plans: Keys to Implementation") ERISA Fiduciary Responsibilities for 403(b) Plans: Keys to Implementation ERISA Fiduciary Responsibilities for 403(b) Plans: Issues and Implementation Table of Contents Description Page I. Introduction...1

ERISA Fiduciary Responsibilities for 403(b) Plans: Keys to Implementation ERISA Fiduciary Responsibilities for 403(b) Plans: Issues and Implementation Table of Contents Description Page I. Introduction...1

DOL EXAMINATIONS OF RETIREMENT PLANS & FIDUCIARY BEST PRACTICES

We Design, Build and Manage Employee Benefit Programs DOL EXAMINATIONS OF RETIREMENT PLANS & FIDUCIARY BEST PRACTICES Presented by: John Higgins, CFP, AIF, CFS Patterson Smith Associates, LLC Securities

We Design, Build and Manage Employee Benefit Programs DOL EXAMINATIONS OF RETIREMENT PLANS & FIDUCIARY BEST PRACTICES Presented by: John Higgins, CFP, AIF, CFS Patterson Smith Associates, LLC Securities

Establishing a New Retirement Plan from A to Z

Establishing a New Retirement Plan from A to Z Virginia K. Sutton, QKA VKS Consulting/Johnson & Dugan Virginia K. Sutton, QKA Consultant; Account Executive, VKS Consulting; Johnson & Dugan Virginia K.

Establishing a New Retirement Plan from A to Z Virginia K. Sutton, QKA VKS Consulting/Johnson & Dugan Virginia K. Sutton, QKA Consultant; Account Executive, VKS Consulting; Johnson & Dugan Virginia K.

Benefit from a new fiduciary approach

RUSSELL INVESTMENTS DEFINED CONTRIBUTION FIDUCIARY OUTSOURCING SERVICES Benefit from a new fiduciary approach INVESTED. TOGETHER. New challenges require new solutions In a world where many employees will

RUSSELL INVESTMENTS DEFINED CONTRIBUTION FIDUCIARY OUTSOURCING SERVICES Benefit from a new fiduciary approach INVESTED. TOGETHER. New challenges require new solutions In a world where many employees will

ADP Retirement Services. New Plan Implementation Guide FOR PLAN SPONSOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC.

ADP Retirement Services New Plan Implementation Guide FOR PLAN SPONSOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC. Welcome to ADP We are excited to get your new 401(k) plan started. At ADP, we consistently

ADP Retirement Services New Plan Implementation Guide FOR PLAN SPONSOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC. Welcome to ADP We are excited to get your new 401(k) plan started. At ADP, we consistently

Plan Health Pro SM Workbook A guide to the information used in the evaluation process.

Plan Health Pro SM Workbook A guide to the information used in the evaluation process. Non-FDIC Insured May Lose Value No Bank Guarantee Thoughtful Retirement Plan Review Plan Health Pro SM was developed

Plan Health Pro SM Workbook A guide to the information used in the evaluation process. Non-FDIC Insured May Lose Value No Bank Guarantee Thoughtful Retirement Plan Review Plan Health Pro SM was developed

The New World of 403(b) Retirement Plans

Retirement Plans") LPL FINANCIAL RETIREMENT PARTNERS The New World of 403(b) Retirement Plans Retirement Strategies A Guide to Best Practices for Plan Fiduciaries Introduction Today, nonprofit plan sponsors need to have

LPL FINANCIAL RETIREMENT PARTNERS The New World of 403(b) Retirement Plans Retirement Strategies A Guide to Best Practices for Plan Fiduciaries Introduction Today, nonprofit plan sponsors need to have

Employee Retirement and Deferred Compensation Plans & Fiduciary Responsibilities of Retirement Plan Administrators

Presented by: Jeffery A. Acheson, QPFC, AIF Partner Employee Retirement and Deferred Compensation Plans & Fiduciary Responsibilities of Retirement Plan Administrators Schneider Downs Wealth Management

Presented by: Jeffery A. Acheson, QPFC, AIF Partner Employee Retirement and Deferred Compensation Plans & Fiduciary Responsibilities of Retirement Plan Administrators Schneider Downs Wealth Management

FIDUCIARY RESPONSIBILITIES/ PLAN GOVERNANCE

Nevada Public Employees Deferred Compensation Program FIDUCIARY RESPONSIBILITIES/ PLAN GOVERNANCE Presented by: Frank Picarelli Senior Vice President January 18, 2018 Copyright 2017 by The Segal Group,

Nevada Public Employees Deferred Compensation Program FIDUCIARY RESPONSIBILITIES/ PLAN GOVERNANCE Presented by: Frank Picarelli Senior Vice President January 18, 2018 Copyright 2017 by The Segal Group,

Building Your. Retirement Roadmap

Building Your Retirement Roadmap Today s Agenda Discuss a roadmap for saving to help you meet your retirement goals Look at key financial principles to follow Review action steps to consider How Fidelity

Building Your Retirement Roadmap Today s Agenda Discuss a roadmap for saving to help you meet your retirement goals Look at key financial principles to follow Review action steps to consider How Fidelity

Measuring Retirement Plan Effectiveness

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

Introducing the Latest Update to Fi360 s Prudent Practices fi360 Inc. All Rights Reserved.

Introducing the Latest Update to Fi360 s Prudent Practices Rich Lynch, AIFA Director, Fi360 & CEFEX Bennett Aikin, AIF Fi360, VP, Designations & Fiduciary Content Agenda History & Purpose of the Prudent

Introducing the Latest Update to Fi360 s Prudent Practices Rich Lynch, AIFA Director, Fi360 & CEFEX Bennett Aikin, AIF Fi360, VP, Designations & Fiduciary Content Agenda History & Purpose of the Prudent

Preparing for your first 401(k) plan audit

plan audit") Preparing for your first 401(k) plan audit 2017 2018 CONTENTS 02 INTRODUCTION 03 04 06 08 DOCUMENT GATHERING AND ORGANIZATION FIDUCIARY RESPONSIBILITY OPERATIONAL COMPLIANCE INTERNAL CONTROLS 11 FINANCIAL

Preparing for your first 401(k) plan audit 2017 2018 CONTENTS 02 INTRODUCTION 03 04 06 08 DOCUMENT GATHERING AND ORGANIZATION FIDUCIARY RESPONSIBILITY OPERATIONAL COMPLIANCE INTERNAL CONTROLS 11 FINANCIAL

Target Date Funds. TDFs: Due diligence is more than set and forget for plan sponsors

Target Date Funds TDFs: Due diligence is more than set and forget for plan sponsors TDFs: Due diligence is more than set and forget for plan sponsors The recent DOL fact sheet on Target Date Funds ( Tips

Target Date Funds TDFs: Due diligence is more than set and forget for plan sponsors TDFs: Due diligence is more than set and forget for plan sponsors The recent DOL fact sheet on Target Date Funds ( Tips

INVESTMARK 3(21) FIDUCIARY SERVICES PROGRAM

FIDUCIARY SERVICES PROGRAM") INVESTMARK 3(21) FIDUCIARY SERVICES PROGRAM The Investmark 3(21) Service is a Co Fiduciary solution which provides plan fiduciaries with a proven partner to assist in fulfilling the fiduciary obligations

INVESTMARK 3(21) FIDUCIARY SERVICES PROGRAM The Investmark 3(21) Service is a Co Fiduciary solution which provides plan fiduciaries with a proven partner to assist in fulfilling the fiduciary obligations

DOL Survival Guide and Top Ten 401(k) Pitfalls

Pitfalls") DOL Survival Guide and Top Ten 401(k) Pitfalls Presented by CohnReznick s Government Contracting Industry Practice Sandy Wendler, Manager and Travis Dutton, Principal, Lockton Retirement Services PLEASE

DOL Survival Guide and Top Ten 401(k) Pitfalls Presented by CohnReznick s Government Contracting Industry Practice Sandy Wendler, Manager and Travis Dutton, Principal, Lockton Retirement Services PLEASE

Overcome the Increased Scrutiny of Your Organization s Retirement Plan

Overcome the Increased Scrutiny of Your Organization s Retirement Plan Finance, HR & Business Operations Conference Washington, DC April 30 - May 1, 2013 4/30/2013 Goals for Today s Presentation Understand

Overcome the Increased Scrutiny of Your Organization s Retirement Plan Finance, HR & Business Operations Conference Washington, DC April 30 - May 1, 2013 4/30/2013 Goals for Today s Presentation Understand

Learn More About: Glass Jacobson Financial Group 401(k) Plan Services

Plan Services") Learn More About: Glass Jacobson Financial Group 401(k) Plan Services NAVIGATING THE PATH TO FINANCIAL SUCCESS Glass Jacobson has played a proactive role in creating financial success for businesses and

Learn More About: Glass Jacobson Financial Group 401(k) Plan Services NAVIGATING THE PATH TO FINANCIAL SUCCESS Glass Jacobson has played a proactive role in creating financial success for businesses and

Fiduciary Checklist. Fiduciary Source troweprice.com/centuryplan. Century Retirement Solutions

Fiduciary Checklist The following are areas of review that retirement plan fiduciaries may want to consider in fulfilling their fiduciary responsibilities. Plan sponsors and plan officials are encouraged

Fiduciary Checklist The following are areas of review that retirement plan fiduciaries may want to consider in fulfilling their fiduciary responsibilities. Plan sponsors and plan officials are encouraged

Retirement Document. Agenda. 403(b) Requirements. 403(b) Documents Webinar. (c) 2008 DATAIR 1. New Documents for 403(b) Plan Sponsors

Requirements. 403(b) Documents Webinar. (c) 2008 DATAIR 1. New Documents for 403(b) Plan Sponsors") Retirement Document New Documents for 403(b) Plan Sponsors Presented by Ethel Myles-Henderson, Esq. DATAIR Employee Benefit Systems, Inc. DATAIR 2008 1 Agenda 403(b) Regulations, Controls & Requirements

Retirement Document New Documents for 403(b) Plan Sponsors Presented by Ethel Myles-Henderson, Esq. DATAIR Employee Benefit Systems, Inc. DATAIR 2008 1 Agenda 403(b) Regulations, Controls & Requirements

Developing and Implementing Investment Policy for Trusts, Sub- Trusts and Endowments

Developing and Implementing Investment Policy for Trusts, Sub- Trusts and Endowments fi360 - global fiduciary insights National Conference May 4-6, 2011 San Antonio, Texas Liza Horvath, CTFA, AIF Copyright

Developing and Implementing Investment Policy for Trusts, Sub- Trusts and Endowments fi360 - global fiduciary insights National Conference May 4-6, 2011 San Antonio, Texas Liza Horvath, CTFA, AIF Copyright

LIFT RETIREMENT NEWS AND INFORMATION FOR EMPLOYERS Q Chuck Furr, CFP, AIF 1201 Battleground Avenue Suite 200 Greensboro, NC 27408

Q2 2017 LIFT RETIREMENT NEWS AND INFORMATION FOR EMPLOYERS Chuck Furr, CFP, AIF 1201 Battleground Avenue Suite 200 Greensboro, NC 27408 Email: info@midtownfa.com Phone: (336) 852-4554 Website: www.midtownfa.com

Q2 2017 LIFT RETIREMENT NEWS AND INFORMATION FOR EMPLOYERS Chuck Furr, CFP, AIF 1201 Battleground Avenue Suite 200 Greensboro, NC 27408 Email: info@midtownfa.com Phone: (336) 852-4554 Website: www.midtownfa.com

Fiduciary compliance reviews: For your defined-contribution plan

Fiduciary compliance reviews: For your defined-contribution plan A fiduciary compliance review is not the same as the annual ERISA audit. We will explore some of the aspects of the review and some areas

Fiduciary compliance reviews: For your defined-contribution plan A fiduciary compliance review is not the same as the annual ERISA audit. We will explore some of the aspects of the review and some areas

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C FORM 11-K COMMISSION FILE NUMBER:

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K /X/ ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31,

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 11-K /X/ ANNUAL REPORT PURSUANT TO SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31,

Session will advise advisers on marketing their services as a 3(38) fiduciary including legal and insurance considerations.

fiduciary including legal and insurance considerations.") Session will advise advisers on marketing their services as a 3(38) fiduciary including legal and insurance considerations. Gary Sutherland, CIC Jason C. Roberts, Esq., AIFA Katie Umile AIFA, www.naplia.com

Session will advise advisers on marketing their services as a 3(38) fiduciary including legal and insurance considerations. Gary Sutherland, CIC Jason C. Roberts, Esq., AIFA Katie Umile AIFA, www.naplia.com

Asset Management Programs, Retirement Plan Services and other Advisory Services Form ADV, Part 2A

Lincoln Financial Advisors Corporation Asset Management Programs, Retirement Plan Services and other Advisory Services Form ADV, Part 2A March 31, 2018 Lincoln Financial Advisors Corporation 1300 South

Lincoln Financial Advisors Corporation Asset Management Programs, Retirement Plan Services and other Advisory Services Form ADV, Part 2A March 31, 2018 Lincoln Financial Advisors Corporation 1300 South

two thousand eight ISSUE BROCHURE 403(b) Plans Frequently Asked Questions

Plans Frequently Asked Questions") Brochure 2-403bFAQs 11x17 - FINAL:Fact Sheet 2008.qxd 10/29/2008 11:04 AM Page 1 National Association of Government Defined Contribution Administrators, Inc. two thousand eight ISSUE BROCHURE 403(b) Plans

Brochure 2-403bFAQs 11x17 - FINAL:Fact Sheet 2008.qxd 10/29/2008 11:04 AM Page 1 National Association of Government Defined Contribution Administrators, Inc. two thousand eight ISSUE BROCHURE 403(b) Plans

Test Your Knowledge of Plan Operation Best Practices

Test Your Knowledge of Plan Operation Best Practices 1 Which Is The Primary Fiduciary Duty? A. Duty of Loyalty B. Duty of Self Governance C. Duty to Maintain Plan Documents on file for auditors and plan

Test Your Knowledge of Plan Operation Best Practices 1 Which Is The Primary Fiduciary Duty? A. Duty of Loyalty B. Duty of Self Governance C. Duty to Maintain Plan Documents on file for auditors and plan

Fiduciary Responsibility in the Age of Technology

Fiduciary Responsibility in the Age of Technology By: Lisa L. Jones, Esq., CPC, QPA VP ERISA Consulting Group, Sentinel Ryan M. Ransford, AIF, QPFC Retirement Plan Advisory Rep, Sentinel Overview This

Fiduciary Responsibility in the Age of Technology By: Lisa L. Jones, Esq., CPC, QPA VP ERISA Consulting Group, Sentinel Ryan M. Ransford, AIF, QPFC Retirement Plan Advisory Rep, Sentinel Overview This

DOL ISSUES FINAL QDIA GUIDANCE October 26, 2007

THE PROFIT SHARING AND 401(k) ADVOCATE SHARING THE COMMITMENT SINCE 1947 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863 7272 ferrigno@401k.org Edward Ferrigno Vice President, Washington

THE PROFIT SHARING AND 401(k) ADVOCATE SHARING THE COMMITMENT SINCE 1947 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863 7272 ferrigno@401k.org Edward Ferrigno Vice President, Washington

Contents. Executive Summary Full Data Tables Respondent Demographics Employee Eligibility Participation...

Executive Summary... 1 Full Data Tables... 14 Respondent Demographics... 15 Table 1 Respondents by plan size and plan type... 15 Table 2 Respondents by total plan assets and plan type... 15 Table 3 Respondents

Executive Summary... 1 Full Data Tables... 14 Respondent Demographics... 15 Table 1 Respondents by plan size and plan type... 15 Table 2 Respondents by total plan assets and plan type... 15 Table 3 Respondents

Presenters. James Jaramillo. Rose Ann Abraham, CPA. Todd Solomon, JD. Partner, McDermott Will & Emery LLP. Partner, Baker Tilly Virchow Krause, LLP

Presenters Rose Ann Abraham, CPA Partner, Baker Tilly Virchow Krause, LLP Todd Solomon, JD Partner, McDermott Will & Emery LLP James Jaramillo Vice President, Sheridan Road Financial 4 Trends in Corporate

Presenters Rose Ann Abraham, CPA Partner, Baker Tilly Virchow Krause, LLP Todd Solomon, JD Partner, McDermott Will & Emery LLP James Jaramillo Vice President, Sheridan Road Financial 4 Trends in Corporate

Contents. Executive Summary Full Data Tables Respondent Demographics Employee Eligibility Participation...

Executive Summary... 1 Full Data Tables... 14 Respondent Demographics... 15 Table 1 Respondents by plan size and plan type... 15 Table 2 Respondents by total plan assets and plan type... 15 Table 3 Respondents

Executive Summary... 1 Full Data Tables... 14 Respondent Demographics... 15 Table 1 Respondents by plan size and plan type... 15 Table 2 Respondents by total plan assets and plan type... 15 Table 3 Respondents

Improving the Target Date Fund Selection

Improving the Target Date Fund Selection INSIDE: By Chris Karam Executive Summary The target date selection process has dramatically changed over the last five years, aided by government regulations, an

Improving the Target Date Fund Selection INSIDE: By Chris Karam Executive Summary The target date selection process has dramatically changed over the last five years, aided by government regulations, an

Boosting 401(k) Retirement Readiness

Retirement Readiness") Boosting 401(k) Retirement Readiness With retirement savings taking a back seat to more immediate financial concerns, and the percentage of workers confident that they ll have enough money for a comfortable

Boosting 401(k) Retirement Readiness With retirement savings taking a back seat to more immediate financial concerns, and the percentage of workers confident that they ll have enough money for a comfortable

Questions to Ask a Plan Recordkeeper

Questions to Ask a Plan Recordkeeper RETIREMENT MANAGEMENT SERVICES, LLC 3/25/2015 Annemarie Keehn, ERPA, QPA, QKA This is Part I in a series on issues to consider when contemplating a change in plan vendors

Questions to Ask a Plan Recordkeeper RETIREMENT MANAGEMENT SERVICES, LLC 3/25/2015 Annemarie Keehn, ERPA, QPA, QKA This is Part I in a series on issues to consider when contemplating a change in plan vendors

Employee Benefits and Qualified Plan Update

Employee Benefits and Qualified Plan Update Sonya D. Wright, CFP, CEBS, QKA First, a Quiz... There will be prizes! Getting to Know You! Percentage of your business in qualified retirement plans? Securities

Employee Benefits and Qualified Plan Update Sonya D. Wright, CFP, CEBS, QKA First, a Quiz... There will be prizes! Getting to Know You! Percentage of your business in qualified retirement plans? Securities

Keeping Your Organization s Retirement Plan in Shape: A Two-Part CAPLAW Webinar Series. Webinar One: Ins and Outs of Retirement Plan Audits

Keeping Your Organization s Retirement Plan in Shape: A Two-Part CAPLAW Webinar Series Webinar One: Ins and Outs of Retirement Plan Audits Trainer: Angie Whiteside, CPA, AIF, Senior Manager 1 Materials/Disclaimer

Keeping Your Organization s Retirement Plan in Shape: A Two-Part CAPLAW Webinar Series Webinar One: Ins and Outs of Retirement Plan Audits Trainer: Angie Whiteside, CPA, AIF, Senior Manager 1 Materials/Disclaimer

The Employers Perspective on Retirement Benefits and Planning

The Employers Perspective on Retirement Benefits and Planning th Annual Transamerica Retirement Survey TCRS 0-0 Transamerica Center for Retirement Studies, 0 Table of Contents PAGE Introduction to the

The Employers Perspective on Retirement Benefits and Planning th Annual Transamerica Retirement Survey TCRS 0-0 Transamerica Center for Retirement Studies, 0 Table of Contents PAGE Introduction to the

Understanding the Roles and Responsibilities of a Fiduciary

Understanding the Roles and Responsibilities of a Fiduciary The retirement plan fiduciary has significant responsibilities. This paper outlines a fiduciary s responsibilities and offers strategies that

Understanding the Roles and Responsibilities of a Fiduciary The retirement plan fiduciary has significant responsibilities. This paper outlines a fiduciary s responsibilities and offers strategies that

Empowering employees with Advice Access

RETIREMENT & BENEFIT PLAN SERVICES Workplace Insights Empowering employees with Advice Access According to a report, employees who enroll in 401(k) managed accounts are more likely to have greater success

RETIREMENT & BENEFIT PLAN SERVICES Workplace Insights Empowering employees with Advice Access According to a report, employees who enroll in 401(k) managed accounts are more likely to have greater success

403(b) Bulletin for Advisors and Consultants

Bulletin for Advisors and Consultants") 403(b) Bulletin for Advisors and Consultants Tools and resources for assessing 403(b) plans Standard Retirement Services Introduction In 2009, significant changes were made to the 403(b) landscape. Plan

403(b) Bulletin for Advisors and Consultants Tools and resources for assessing 403(b) plans Standard Retirement Services Introduction In 2009, significant changes were made to the 403(b) landscape. Plan

Fiduciary Update and Best Practices for Retirement Plan Committee Members April 7, 2017

Fiduciary Update and Best Practices for Retirement Plan Committee Members April 7, 2017 Presented by: Nicole Berlowski ProHealth Care, Inc. 725 American Drive 191 N. Wacker Drive POB Suite 305 Suite 3700

Fiduciary Update and Best Practices for Retirement Plan Committee Members April 7, 2017 Presented by: Nicole Berlowski ProHealth Care, Inc. 725 American Drive 191 N. Wacker Drive POB Suite 305 Suite 3700

for public school employers retirement plan solutions 403(b) plan compliance guide

plan compliance guide") for public school employers retirement plan solutions 403(b) plan compliance guide AXA Equitable Life Insurance Company (NY, NY) Table of Contents About This Guide 1 AXA Equitable Experience, Knowledge,

for public school employers retirement plan solutions 403(b) plan compliance guide AXA Equitable Life Insurance Company (NY, NY) Table of Contents About This Guide 1 AXA Equitable Experience, Knowledge,

Retirement Plan Design Opportunities for Law Firms

Professional Education Series Retirement Plan Services 1 TRUST COMPANY OF ILLINOIS Continuing Legal Education Seminar Retirement Plan Design Opportunities for Law Firms and Their Small Business Clients

Professional Education Series Retirement Plan Services 1 TRUST COMPANY OF ILLINOIS Continuing Legal Education Seminar Retirement Plan Design Opportunities for Law Firms and Their Small Business Clients

401(k)ollaborate. Helping You Expand Your Retirement Plan Business. For financial advisor or plan sponsor use only. Not for use with the public.

ollaborate. Helping You Expand Your Retirement Plan Business. For financial advisor or plan sponsor use only. Not for use with the public.") 401(k)ollaborate Helping You Expand Your Retirement Plan Business For financial advisor or plan sponsor use only. Not for use with the public. Paychex Working Beside You For over 20 years, advisors have

401(k)ollaborate Helping You Expand Your Retirement Plan Business For financial advisor or plan sponsor use only. Not for use with the public. Paychex Working Beside You For over 20 years, advisors have

ADP Retirement Services. Conversion Implementation Guide FOR PLAN SPONSOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC.

ADP Retirement Services Conversion Implementation Guide FOR PLAN SPONSOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC. Thank you for choosing ADP Retirement Services Welcome to ADP Retirement Services.

ADP Retirement Services Conversion Implementation Guide FOR PLAN SPONSOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC. Thank you for choosing ADP Retirement Services Welcome to ADP Retirement Services.

Important Approaching Deadlines

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: November 15, 2016: 45 days prior to 12 month deadline to complete testing: Deadline for

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: November 15, 2016: 45 days prior to 12 month deadline to complete testing: Deadline for

Financial Intelligence. Produced Exclusively for Members of the Senior Executives Association

Financial Intelligence Produced Exclusively for Members of the Senior Executives Association Mike Miles Founder and Principal Advisor, Variplan, LLC Certified Financial Planner Registered Investment Advisor

Financial Intelligence Produced Exclusively for Members of the Senior Executives Association Mike Miles Founder and Principal Advisor, Variplan, LLC Certified Financial Planner Registered Investment Advisor

Fiduciary Issues for Retirement

Plan Sponsor Basics Webinar 6 of 6 Fiduciary Issues for Retirement Plan Sponsors October 15, 2013 Presenters: Julie K. Stapel Daniel R. Kleinman www.morganlewis.com Overview of Today s Webinar ERISA Overview

Plan Sponsor Basics Webinar 6 of 6 Fiduciary Issues for Retirement Plan Sponsors October 15, 2013 Presenters: Julie K. Stapel Daniel R. Kleinman www.morganlewis.com Overview of Today s Webinar ERISA Overview

EMPLOYER. Helping you fulfill your fiduciary duties. MassMutual s Regulatory Advisory Services 2019 Calendar for non-calendar year DC and DB plans

EMPLOYER Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2019 Calendar for non-calendar year DC and DB plans TABLE OF CONTENTS Defined Contribution Plans... 2 January

EMPLOYER Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2019 Calendar for non-calendar year DC and DB plans TABLE OF CONTENTS Defined Contribution Plans... 2 January

Plan Administration Manual

Plan Administration Manual P a g e 1 Thank you for choosing American United Life Insurance Company (AUL), a OneAmerica company, as the funding vehicle and administrative services provider for your retirement

Plan Administration Manual P a g e 1 Thank you for choosing American United Life Insurance Company (AUL), a OneAmerica company, as the funding vehicle and administrative services provider for your retirement

Helping you fulfill your fiduciary duties

A Fiduciary Planning Guide for Plan Sponsors Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2016 Calendar Contents Defined Contribution Plans 2 January March 4 April

A Fiduciary Planning Guide for Plan Sponsors Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2016 Calendar Contents Defined Contribution Plans 2 January March 4 April

A DEEPER DIVE THE WYOMING RETIREMENT SYSTEM 457 PLAN IS A POWERFUL SAVINGS TOOL THAT CAN MAKE HAVING A COMFORTABLE RETIREMENT A WHOLE LOT EASIER.

A DEEPER DIVE THE WYOMING RETIREMENT SYSTEM 457 PLAN IS A POWERFUL SAVINGS TOOL THAT CAN MAKE HAVING A COMFORTABLE RETIREMENT A WHOLE LOT EASIER. A Guided Tour Through Your WRS 457 Deferred Compensation

A DEEPER DIVE THE WYOMING RETIREMENT SYSTEM 457 PLAN IS A POWERFUL SAVINGS TOOL THAT CAN MAKE HAVING A COMFORTABLE RETIREMENT A WHOLE LOT EASIER. A Guided Tour Through Your WRS 457 Deferred Compensation

Target date funds: Translating Department of Labor guidance into action

RETIREMENT INSIGHTS Target date funds: Translating Department of Labor guidance into action IN BRIEF In February 2013, the U.S. Department of Labor (DOL) issued eight tips to help plan fiduciaries with

RETIREMENT INSIGHTS Target date funds: Translating Department of Labor guidance into action IN BRIEF In February 2013, the U.S. Department of Labor (DOL) issued eight tips to help plan fiduciaries with

Establishing a Due Diligence File

resource edge TM Establishing a Due Diligence File investment insights practice building solutions retirement resources RESOURCE EDGE TM Table of Contents 3 Introduction 4 401(k) fiduciary documentation

resource edge TM Establishing a Due Diligence File investment insights practice building solutions retirement resources RESOURCE EDGE TM Table of Contents 3 Introduction 4 401(k) fiduciary documentation

Defined Contribution and Defined Benefit Plans: Have you considered everything?

Defined Contribution and Defined Benefit Plans: Have you considered everything? Amy Henselin Partner, Audit Appleton Debbie Smith Partner, National Professional Standards Group Chicago Objectives Identify

Defined Contribution and Defined Benefit Plans: Have you considered everything? Amy Henselin Partner, Audit Appleton Debbie Smith Partner, National Professional Standards Group Chicago Objectives Identify

QDIA PRACTICES CHECKLIST

QDIA PRACTICES CHECKLIST PLAN SPONSOR: PLAN NAME(S): RECORDKEEPER: ADVISOR: ADVISOR GUIDELINES FOR RECOMMENDING QDIAS OVERVIEW: A common question asked by plan sponsors is: How do I select a qualified

QDIA PRACTICES CHECKLIST PLAN SPONSOR: PLAN NAME(S): RECORDKEEPER: ADVISOR: ADVISOR GUIDELINES FOR RECOMMENDING QDIAS OVERVIEW: A common question asked by plan sponsors is: How do I select a qualified

FINRA SAVINGS PLUS 401(K) PLAN SUMMARY PLAN DESCRIPTION 2017

PLAN SUMMARY PLAN DESCRIPTION 2017") FINRA SAVINGS PLUS 401(K) PLAN SUMMARY PLAN DESCRIPTION 2017 TABLE OF CONTENTS INTRODUCTION: THE FINRA SAVINGS PLUS PLAN... 1 This Booklet is Only a Summary... 1 Administrative Information... 1 Not a Contract

FINRA SAVINGS PLUS 401(K) PLAN SUMMARY PLAN DESCRIPTION 2017 TABLE OF CONTENTS INTRODUCTION: THE FINRA SAVINGS PLUS PLAN... 1 This Booklet is Only a Summary... 1 Administrative Information... 1 Not a Contract

401(k)ollaborate. Retirement Services. Helping You Expand Your Retirement Plan Business. For financial advisor use only. Not for use with the public.

ollaborate. Retirement Services. Helping You Expand Your Retirement Plan Business. For financial advisor use only. Not for use with the public.") 401(k)ollaborate Helping You Expand Your Retirement Plan Business Retirement Services For financial advisor use only. Not for use with the public. Paychex Makes It Simple Working Beside You For more than

401(k)ollaborate Helping You Expand Your Retirement Plan Business Retirement Services For financial advisor use only. Not for use with the public. Paychex Makes It Simple Working Beside You For more than

Auto Enrollment in 401(k) and 403(b) Plans: Can one solution fit every plan s needs?

and 403(b) Plans: Can one solution fit every plan s needs?") Auto Enrollment in 401(k) and 403(b) Plans: Can one solution fit every plan s needs? Executive summary: Automatic enrollment and automatic deferral escalation continue to get a lot of attention in the

Auto Enrollment in 401(k) and 403(b) Plans: Can one solution fit every plan s needs? Executive summary: Automatic enrollment and automatic deferral escalation continue to get a lot of attention in the

The Five Pillars of a Retirement Plan

The Five Pillars of a Retirement Plan An employee retirement plan can help: Recruit and retain valuable employees Bridge the gap between Social Security and retirement income needs, which are estimated

The Five Pillars of a Retirement Plan An employee retirement plan can help: Recruit and retain valuable employees Bridge the gap between Social Security and retirement income needs, which are estimated

The Seven Core Principles Every Fiduciary Should Know and Follow

The Seven Core Principles Every Fiduciary Should Know and Follow J. Richard Lynch, AIFA President, fi360 Mission: fi360 will help our clients gather, grow, and protect assets through better investment

The Seven Core Principles Every Fiduciary Should Know and Follow J. Richard Lynch, AIFA President, fi360 Mission: fi360 will help our clients gather, grow, and protect assets through better investment

Bickling Financial Services

Defined Contribution 401(k) 403(b) 457 Fiduciary Investment Services Defined Benefit Cash Balance ESOP Non-qualified Buy-sell Agreements Executive Bonus Key-Man Insurance Bickling Financial Services THE

Defined Contribution 401(k) 403(b) 457 Fiduciary Investment Services Defined Benefit Cash Balance ESOP Non-qualified Buy-sell Agreements Executive Bonus Key-Man Insurance Bickling Financial Services THE

UNDERSTANDING 401(K) AND PROFIT SHARING PLANS. Choosing an option that benefits your business and your employees.

AND PROFIT SHARING PLANS. Choosing an option that benefits your business and your employees.") UNDERSTANDING 401(K) AND PROFIT SHARING PLANS Choosing an option that benefits your business and your employees. UNDERSTANDING 401(K) AND PROFIT SHARING PLANS As a business owner, you re likely concerned

UNDERSTANDING 401(K) AND PROFIT SHARING PLANS Choosing an option that benefits your business and your employees. UNDERSTANDING 401(K) AND PROFIT SHARING PLANS As a business owner, you re likely concerned

Windstream 401(k) Plan. Summary Plan Description

Plan. Summary Plan Description") Summary Plan Description TABLE OF CONTENTS THE PLAN AT A GLANCE... 4 WINDSTREAM 401(k) PLAN SUMMARY PLAN DESCRIPTION AND PROSPECTUS... 6 ELECTIONS AND ACCOUNT INFORMATION... 7 ELIGIBILITY... 7 ENROLLMENT...

Summary Plan Description TABLE OF CONTENTS THE PLAN AT A GLANCE... 4 WINDSTREAM 401(k) PLAN SUMMARY PLAN DESCRIPTION AND PROSPECTUS... 6 ELECTIONS AND ACCOUNT INFORMATION... 7 ELIGIBILITY... 7 ENROLLMENT...

Roadmap to Understanding Retirement Plan Fees. The only guide you need

Roadmap to Understanding Retirement Plan Fees The only guide you need Executive Summary Retirement plan fees under the spotlight You know there are costs associated with offering a retirement plan, but

Roadmap to Understanding Retirement Plan Fees The only guide you need Executive Summary Retirement plan fees under the spotlight You know there are costs associated with offering a retirement plan, but

Part 2A of Form ADV: Firm Brochure

Financial Engines Advisors L.L.C. 1050 Enterprise Way, 3rd Floor Sunnyvale, California 94089 Chief Compliance Officer: Dexter Buck www.financialengines.com March 31, 2017 Part 2A of Form ADV: Firm Brochure

Financial Engines Advisors L.L.C. 1050 Enterprise Way, 3rd Floor Sunnyvale, California 94089 Chief Compliance Officer: Dexter Buck www.financialengines.com March 31, 2017 Part 2A of Form ADV: Firm Brochure

Plan Sponsor Webcast Series

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

A New Paradigm DELIVERING RETIREMENT BENEFITS TO HEALTHCARE AND HIGHER EDUCATION EMPLOYEES

Q&A PANEL January 2019 Retirement benefits insights to inform your decision-making. A New Paradigm DELIVERING RETIREMENT BENEFITS TO HEALTHCARE AND HIGHER EDUCATION EMPLOYEES The retirement benefits environment

Q&A PANEL January 2019 Retirement benefits insights to inform your decision-making. A New Paradigm DELIVERING RETIREMENT BENEFITS TO HEALTHCARE AND HIGHER EDUCATION EMPLOYEES The retirement benefits environment

The Case for Rethinking TDFs as QDIAs

The Case for Rethinking TDFs as QDIAs Presenters: Jake Adamczyk, Associate Vice President of Aurum Advisory Services and Mike McKeown, Director of Research at Aurum Advisory Services 6685 Beta Drive, Mayfield

The Case for Rethinking TDFs as QDIAs Presenters: Jake Adamczyk, Associate Vice President of Aurum Advisory Services and Mike McKeown, Director of Research at Aurum Advisory Services 6685 Beta Drive, Mayfield

Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS

PRICE PERSPECTIVE June 2015 In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced

PRICE PERSPECTIVE June 2015 In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced

Retirement reset. How re-enrollment can help strengthen U.S. retirement security IN BRIEF

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Retirement reset How re-enrollment can help strengthen U.S. retirement security AUTHORS Anne Lester Portfolio Manager and Head of Retirement Solutions

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Retirement reset How re-enrollment can help strengthen U.S. retirement security AUTHORS Anne Lester Portfolio Manager and Head of Retirement Solutions

Managing fiduciary responsibility for plan sponsors

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

MECH JOB INFORMATION SPECIFICATIONS NOTES

Portfolio Management A B Welcome to the Portfolio Management program. There comes a point when managing your assets can easily become a full-time job. As your life evolves, not only can your financial

Portfolio Management A B Welcome to the Portfolio Management program. There comes a point when managing your assets can easily become a full-time job. As your life evolves, not only can your financial