City and County of Denver. General Tax Information Booklet

|

|

|

- Abigayle Carter

- 5 years ago

- Views:

Transcription

1 City and County of Denver General Tax Information Booklet

2 Table of Contents Contents INTRODUCTION... 5 TYPES OF TAX & CHARGES... 6 DENVER SALES TAX... 6 DENVER USE TAX... 6 DENVER OCCUPATIONAL PRIVILEGETAX (OPT)... 7 LODGER S TAX... 7 FACILITIES DEVELOPMENT ADMISSION TAX (FDA)... 8 TELECOMMUNICATIONS BUSINESS TAX (TBT)... 8 EMERGENCY TELEPHONE CHARGE (E911)... 8 WHO MUST HAVE A LICENSE/REGISTER... 9 GENERAL GUIDELINES... 9 TYPES OF LICENSES... 9 LICENSE FEES BUYING OR SELLING A BUSINESS RELATEDINFORMATION CONSTRUCTION VENDINGMACHINE SALES OBTAINING A SALES, USE, LODGER S OR OCCUPATIONAL PRIVILEGE TAX LICENSE RECORD KEEPING TAKINGGOODS OUT OF INVENTORY BURDEN OF PROOF FILINGFREQUENCY SALES, USE AND LODGER S OCCUPATIONAL PRIVILEGETAX (OPT) FACILITIES DEVELOPMENT ADMISSIONS (FDA) TELECOMMUNICATIONS BUSINESS TAX (TBT) EMERGENCY TELEPHONE CHARGE (E911) PENALTIES / INTEREST FOR LATE FILINGS FILING TIPS NO NEGATIVE RETURNS NO TAXES OR CHARGES DUE? BUSINESS PERSONAL PROPERTY TAXATION GENERALINFORMATION PERSONALPROPERTY THE ASSESSOR S RESPONSIBILITY THE BUSINESS OWNER SRESPONSIBILITY THE TREASURER S RESPONSIBILITIES FILING DECLARATIONS LEASED, LOANED, OR RENTED PERSONAL PROPERTY DECLARATION FILING OPTIONS A MESSAGE TO SMALL BUSINESS OWNERS EXEMPTIONS FROM ASSESSMENT PERSONAL PROPERTY ASSESSMENT CALENDAR PAYMENT AND COLLECTION OF PERSONAL PROPERTY TAX REAL PROPERTY TAX DUE DATES SALES TAX, LODGER S TAX, USE TAX OCCUPATIONAL PRIVILEGE TAX FACILITIES DEVELOPMENT ADMISSION (FDA) TAX TELECOMMUNICATIONS BUSINESS TAX EMERGENCY TELEPHONE CHARGE (E911) PERSONAL PROPERTY TAX REAL PROPERTY TAX WHERE TO GET HELP EXAMPLE RETURNS AND DECLARATIONS EXAMPLE SALES TAX RETURN P a g e

3 EXAMPLE CONSUMER S USE TAX RETURN P a g e

4 EXAMPLE LODGER S TAX RETURN EXAMPLE OCCUPATIONAL PRIVILEGE TAX RETURN EXAMPLE SPECIAL EVENT APPLICATION AND SALES TAX RETURN EXAMPLE TELECOMMUNICATIONS BUSINESS TAX RETURN EXAMPLE FACILITIES DEVELOPMENT ADMISSIONS TAX RETURN EXAMPLE EMERGENCY TELEPHONE CHARGE FILING FORM EXAMPLE BUSINESS PERSONAL PROPERTY TAX DECLARATION P a g e

5 This page intentionally left blank 5 P a g e

6 INTRODUCTION This booklet is intended to provide general tax and charge information for anyone conducting business in The City and County of Denver. It provides information for collecting and filing sales, use, lodger s, occupational privilege (OPT), facilities development (FDA), telecommunications (TBT), Emergency Telephone Charge (E911), and property taxes. The Denver Treasury Division of the Department of Finance collects all of the taxes and charges governed by the Denver Revised Municipal Code (DRMC) Chapter 53 and Chapter 16. The Treasury Division also collects the real estate and personal property taxes governed by the Colorado Revised Statutes (CRS). For further information, please visit the Treasury Division website at where you will find the DRMC, Denver Tax Guides and Denver Tax Rules. You can also call the Treasury Division s Taxpayer Service staff at The Denver Assessment Division of the Department of Finance determines the actual value of all real and personal property located in the City and County of Denver. These values are used to determine the property taxes that will be billed and collected by the Denver Treasury Division. Information regarding business personal property and real property assessment can be obtained at the Assessor s website at or by calling or NOTE: This booklet is not all inclusive; it is not intended for legal purposes to be substituted for the full text of the DRMC or CRS and applicable rules and regulations. 6 P a g e

7 TYPES OF TAX & CHARGES DENVER SALES TAX The Denver Revised Municipal Code (DRMC) imposes a 3.65% sales tax on the purchase price paid or charged on retail sales, leases, or rentals of tangible personal property, taxable products and taxable services. Taxable services include, but are not limited to, the sale or furnishing of telephone and certain telecommunications services, electricity, steam and natural gas for energy producing purposes, internet subscription services, software as a service, sound system services, informational, and entertainment services. In addition, tax is imposed on digital products including but not limited to digital images, digital audio works, and digital books. Taxes collected are used to pay for the operations of the City including the payment of principal and interest due on certain municipal bonds. The DRMC imposes special tax rates for the following sales at retail: A four percent (4.0%) tax is imposed on the sale of food and beverages not exempt by ordinance. A limited exemption is provided for the sale of food for domestic household use. Some examples of taxable sales include prepared food and beverages sold by restaurants and grocery stores, catered food, coffee services, and liquor purchases. A four cent ($0.04) per gallon tax is imposed on the sale of aviation fuel. A seven and one quarter percent (7.25%) tax is imposed on the rental of automotive vehicles for a period of thirty (30) days or less. A combined seven and one fifteenth percent (7.15%) tax is imposed on the sale of all retail marijuana and retail marijuana products. DENVER USE TAX There are two types of use tax: 1. Consumer Use Tax is imposed on tangible personal property (generally furniture, fixtures, equipment, and supplies (not inventory),taxable products, and taxable services, that are used, stored or consumed within Denver upon which local sales tax equal to or greater than Denver s rate has not been paid. Example: ABC Company which is located in Denver buys a machine from a manufacturer in Chicago, which is shipped into Denver. ABC will use the machine to make belts. The Chicago firm does not collect sales tax. ABC is required to pay Denver the 3.65% consumer use tax. ABC will include this amount on line 8 of its Denver sales tax return. 2. Retailer s Use Tax is collected on retail sales by non-resident vendors on sales delivered into Denver. Retailer s use tax rate is the same as the sales tax rate and is reported in the same manner. 7 P a g e

8 Example: XYZ Corporation (a licensed Denver vendor) is located in Greeley, Colorado and makes retail sales of appliances which are delivered into Denver. Since XYZ does not have a Denver outlet, it collects 3.65% retailer s use tax on the purchase price and reports the tax on its Denver sales tax return. For further information, please refer to our Tax Guide, Topic 83, Use Tax, which can be found on our website at: NOTE: Use tax rates are the same as the sales tax rates explained above. DENVER OCCUPATIONAL PRIVILEGE TAX (OPT) Denver occupational privilege tax is also known as OPT or head tax. The occupational privilege tax consists of two distinct parts: the employee occupational privilege tax and the business occupational privilege tax. The tax is imposed on businesses operating in the City and on individuals who perform sufficient services within Denver to receive as compensation from an employer at least five hundred dollars ($500) for a calendar month. Each taxable employee is liable for the employee OPT, which is withheld by the employer at a rate of $5.75 per month. The employer is also required to pay the business OPT at a rate of $4.00 per month for each taxable employee. Employees need not live in Denver nor the business be based within Denver to be liable for the OPT. Additionally, the employer is required to pay the business OPT at a rate of $4.00 per month for each owner, partner, or manager engaged in business in Denver regardless of how much they earn. Any entity that performs any business, trade, occupation, or profession of any kind, is liable for a minimum of $4.00 per month for each month in which that entity has any activity in Denver. The purpose of both the employee and the business occupational privilege tax is to generate funds for the planning or design for, and the replacement, expansion, acquisition, construction, installation, repair or improvement of City facilities, as well as the provision of municipal services to Denver citizens and businesses. LODGER S TAX Denver imposes a tax on the sale of lodging of 10.75%. The entire amount charged to any person for overnight accommodations or rooms (defined as sleeping accommodations in a hotel, apartment hotel, lodging house, motor house, motor hotel, guest house, guest ranch, resort, mobile home, auto camp, trailer court or park), who is not a permanent resident and who has not entered into a written agreement for occupancy of a room or rooms or sleeping accommodations for a period of at least thirty (30) consecutive days, is taxable. The purpose of the tax is to raise funds for the payment of expenses of operating and improving the City and its facilities, for the payment of principal and interest due on the bonds issued to finance construction and expansion of the Colorado Convention Center, and 8 P a g e

9 to finance the operation of the Denver Metro Convention and Visitors Bureau. FACILITIES DEVELOPMENT ADMISSION TAX (FDA) Denver imposes a ten percent (10%) facilities development admissions tax upon the purchase price of each admission to any entertainment, amusement, or athletic event or other production or assembly staged, produced, convened or held in or on any City-owned or leased property. This tax is commonly referred to as the seat tax. TELECOMMUNICATIONS BUSINESS TAX (TBT) Denver imposes a tax upon telecommunications businesses authorized by the Colorado Public Utilities Commission (PUC) to provide local exchange service to general public customers in Denver. The TBT is imposed at the rate of $1.12 per month for each of the telecommunications company s accounts within the City to which a basic dial-tone line is provided. It is imposed directly upon the business, as opposed to being collected from its customers and held in trust; however, the telecommunications companies are allowed by State statute and PUC authorization to show the charge separately on their billings to customers. This tax is separate from, and in addition to, the City s general sales tax on telecommunications, which is imposed on the customer, collected by the provider, and applies to certain telecommunications services that originate and are charged to a telephone number or account located within the City. EMERGENCY TELEPHONE CHARGE (E911) Denver imposes a charge upon each phone number or service user within the City and County of Denver. The E911 Charge is imposed at the rate of $0.70 per month per exchange access facility, per wireless communications access, and per interconnected voiceover-internet-protocol access. The E911 charge is not subject to sales or use tax and shall be reported separately from taxes and fees charged. All E911 charges, except for prepaid telecommunications, are reported directly to the City on the prescribed monthly filing form. E911 charges for prepaid telecommunications are reported directly to the Colorado Department of Revenue; they are not reported to the City. 9 P a g e

10 WHO MUST HAVE A LICENSE/REGISTER GENERAL GUIDELINES A Denver sales tax license is required for any retailer or vendor who is selling, leasing, or granting a license to use tangible personal property or selling taxable services to the user at retail within the City and County of Denver. The Denver sales tax license gives the retailer or vendor the authority to collect the sales tax on behalf of the City. If you have more than one location where sales are made, a separate license is required for each location. If a business makes retail sales at special events within the City and County of Denver and does not possess a regular sales tax license, a special event sales tax license is required for each event. All businesses engaged in business within the City shall file an occupational privilege tax registration. TYPES OF LICENSES Four types of tax licenses are issued by the Denver Treasury Division: 1. Sales Tax License A sales tax license is required for any retailer or vendor who is selling, leasing, or granting a license to use tangible personal property or taxable services to the user at retail within the City and County of Denver. Fee: $50.00 for each location per two-year period. 2. Retailer s Use Tax License This license is required for non-resident retailers/vendors that do not have a Denver location and are selling, leasing, or granting a license to use tangible personal property or providing a taxable service to purchasers at retail in Denver. Fee: $50.00 per two-year period. 3. Special Event Sales Tax License Businesses making retail sales at special events must apply for a special event sales tax license, which is good for that event only. Special events are defined as being less than two weeks in duration. (Note: The license fee payment will be recorded but no paper license will be issued.) Participants in special events who hold regular retail sales licenses do not need to p a y this fee. They will report these sales on their regular sales tax return. Fee: $5.00 for each special event license. 10 P a g

11 4. Lodger s Tax License A lodger s tax license is required for any vendor who provides overnight lodging or accommodations in the City and County of Denver for a period of less than thirty (30) consecutive days. Fee: $50.00 for each location per two-year period. NOTE: The above licenses are not licenses to engage in business within the City. A separate business license must be obtained from the Department of Excise and Licenses, if applicable. Go to for more information. LICENSE FEES License fees help recover the administrative cost of establishing and maintaining tax accounts and are non-refundable. All licenses, with the exception of the special event license, are effective for a two-year period. Two-year licenses are renewed at the beginning of each even-numbered year, and expire at the end of each odd-numbered year. The fee for a license purchased after the start of an even-numbered year will be prorated in six-month increments, as follows: Date purchased: Jan 1 June 30, even numbered year.$50.00 July 1 Dec 31, even numbered year.$37.50 Jan 1 June 30, odd numbered year...$25.00 July 1 Dec 31, odd numbered ear... $12.50 For example, if you open your business July 20, of an even numbered year, the first six months of the license period have already elapsed. Therefore, you would pay $37.50 for a license for the remaining 18 months of the remaining two-year period. TAX LICENSE TYPES Jan. 1 to Jun 30, even # year PRO-RATED FEES IF BUSINESS BEGINS July 1 to Dec 31, even # year Jan 1 to Jun 30, odd # year Jul 1 to Dec 31, odd # year SALES TAX $50.00 $37.50 $25.00 $12.50 SALES & LODGER S TAX $50.00 $37.50 $25.00 $12.50 LODGER S TAX $50.00 $37.50 $25.00 $12.50 RETAILER S USE TAX $50.00 $37.50 $25.00 $ P a g e

, Emergency Telephone Charge (E911) or facilities development admissions (FDA) tax")

12 Prior to the license expiring at the end of the two-year period, a renewal form will be mailed to you. If you do not receive a renewal form, you may request one by calling NOTES: No fee is required for consumer use tax, occupational privilege tax, telecommunications business tax (TBT), Emergency Telephone Charge (E911) or facilities development admissions (FDA) tax registration. The special event license fee is $5.00 for each event. OBTAINING A SALES, USE, LODGER S OR OCCUPATIONAL PRIVILEGE TAX LICENSE The easiest way to file to complete an application for Denver Sales, Use, Lodger s Tax License and/or Occupational Privilege Tax Registration is online through Denver s ebiz Tax Center. Go to and a click the Register a New Business hyperlink. You will pay any applicable license fees when you submit your application. You can obtain a hard copy of the Application for Denver Sales, Use, Lodger s Tax License and/or Occupational Privilege Tax Registration form in the following ways: Online: Click here to download the form. Submit the completed form via regular mail or hand delivery as listed below. By Mail: Call Taxpayer Service at to request one be mailed to you In Person: Visit our office at 201 W. Colfax Ave., Denver, CO Monday through Friday between 8:00 a.m. and 5:00 p.m. 11 P a g e

13 Pay the appropriate fee when you turn in your application form. Paper applications can be submitted in the following ways: Mail: Treasury Division, 201 W. Colfax Ave., Dept 403, Denver, CO NOTES: You can contact us at for assistance in completing the form. Please allow three weeks from receipt of application for processing and mailing your license. Your license will be mailed to your location address. BUYING OR SELLING A BUSINESS Refer to Denver Tax Guide 69, Sale and Purchase of a Business for the Denver sales/use tax implications of buying or selling a business. If you are buying a business, you should: 1. Obtain a Certificate of Taxes Due. You will need the current owner s signature in order for us to release the tax information. This is important because the new owner takes the property subject to delinquent taxes owed by the former owner. The fee is $10.00 per t a x type. Click here to obtain a Request for Certificate of Taxes Due form online: Submit a completed form by or regular mail. o Treasury.Information@denvergov.org o Mail: 201 W. Colfax Ave., Dept 403, Denver, CO Pay sales/use tax on the tangible personal property (furniture, fixtures, equipment and supplies), included in the purchase of the business. Do not pay sales/use tax on items purchased for resale. 3. Register with the Denver Treasury Division for all the required tax accounts. 4. Register with the Business Personal Property section of the Assessor s Office. If you are selling a business, you should: 1. Pay all taxes current through the date of the sale, including the current year s personal property taxes. 2. Collect and remit sales tax on the purchase price of taxable tangible personal property sold in the transaction. 3. Close your account number with the Treasury Division. Click here to obtain an Acc ount Change/Cancellation form online. Submit a completed form by or regular mail. o Treasury.Information@denvergov.org o Mail: 201 W. Colfax Ave., Dept 403, Denver, CO P a g e

14 RELATED INFORMATION CONSTRUCTION General Contractors and Subcontractors The City and County of Denver imposes a 3.65% consumer use tax on all construction materials and supplies used on a Denver job. The use tax is due unless vendors have charged the 3.65% Denver sales tax. Tools and equipment are subject to the 3.65% use tax on the cost or fair market value at the occasion of first use in Denver. Exceptions are: Automotive vehicles required by law to be registered outside Denver are exempt. If equipment will be used or stored in Denver for 30 consecutive days or less, a declaration completed prior to the equipment being brought into Denver may result in a smaller tax liability. Credit is allowed for any legally imposed sales and use taxes previously paid on materials, supplies, tools and equipment to any municipal corporation (city), county and/or state, to the extent the rate does not exceed the total combined rate. In addition to the above, it is important to note the following: Denver does not provide an exemption from sales or use tax for construction or building materials used on any construction project located in Denver, including government, or charitable. Denver does not collect use tax at the time a building permit is issued. Tax is paid to retailers at the time of purchase or directly to the City of Denver on the consumer use tax return. Denver does not provide an exemption from sales or use tax for energy (natural gas, electricity, etc.) used in building construction. Denver sales or use tax applies to diesel fuel used off-highway, including that used for the operation of construction equipment. Contractors that manufacture materials or other items of tangible personal property that are to be incorporated into a structure are liable for use tax on the manufactured cost of these items, which, in addition to materials, includes labor and services used in the manufacturing process. All contractors are required to have an occupational privilege tax registration. In addition, construction contractors may be issued a consumer use tax account; contractorretailers are issued either a sales tax license, if the business is located in Denver, or a retailer s use tax license for business locations outside Denver. A license fee is required for both sales and retailer s use tax licensure. 13 P a g e

15 For more information on construction, please see Denver Tax Rule 5, Rules Regarding the Assessment and Collection of Sales and Use Tax on Sales and Use of Tangible Personal Property Acquired by Construction Companies. VENDING MACHINE SALES Items sold through vending machines may include the sales tax in the sales price of the item vended. This is an exception, specifically allowed by ordinance, to the general requirement that sales tax be added to the selling price as a separate amount. The vended price includes the Denver sales tax plus the sales tax collected by the State of Colorado. "Honor box" sales are treated the same as vending machine sales. Non-food items sold through vending machines, such as toys, DVDs, or valet items (as often found in hotels/motels), are taxed by Denver at the general rate of 3.65% of the purchase price. Sales of food and beverages vended through machines are taxed by Denver at the rate of 4.0% of the sales price, as are all other sales of taxable food and drink. For more information on vending machine sales, please see Denver Tax Guide 84, Vending Machine Sales and Equipment. RECORD KEEPING You must keep records of all of your business transactions to enable you and the City and County of Denver to determine the correct amount of sales, use, and occupational privilege taxes for which your business is liable. These records must include: Detailed general ledgers Depreciation schedules Purchase invoices and receipts Sales invoices and receipts Sales and purchase journals Bank statements and cancelled checks Delivery documents Payroll records Copies of City and County of Denver tax returns and back-up detail supporting information reported All other accounting records and documents that pertain to the activities of the business 14 P a g e

16 If you make nontaxable sales such as resale sales to other retailers or wholesalers, or exempt sales to tax exempt organization, obtain copies of current sales tax licenses and /or Denver letters of exemption, and maintain these documents in your customer files. You must keep and preserve all records related to business activity for a period of four (4) years following the due date of the return or payment of the tax. These records must be available for review by the City and County of Denver. TAKING GOODS OUT OF INVENTORY If your business withdraws inventory goods that were purchased tax-free for resale and uses the goods for personal or business purposes, it is liable for consumer use tax on those items. Report the use tax on the Schedule B of the Denver Sales Tax Return or on the appropriate line of your Use Tax Return. BURDEN OF PROOF If you make a tax-exempt sale, records must be kept that sufficiently demonstrate the purchaser s tax exemption by the City and County of Denver. The exempt status of each transaction must be determined on its own merits. You, as the retailer or vendor, bear the ultimate responsibility of proving that the purchaser is entitled to exemption from sales tax. Therefore, you should know the nature of your customer's business before allowing any form of exemption, and should have the purchaser complete an Affidavit of Exempt Sale 15 P a g e

17 FILING FREQUENCY Also see the Due Dates section. The filing frequency of sales, use and lodger s, OPT, TBT tax returns are as follows: SALES, USE AND LODGER S Monthly - filing is required if the average monthly tax liability exceeds $300. The return is due on the 20th day of the month following the taxable month. Quarterly - filing is allowed if the monthly tax liability averages $300 or less. Due dates are April 20, July 20, October 20 and January 20. Annual - filing is allowed if the monthly tax liability averages $15 or less. The return is due on the 20th day of January following the taxable year. All marijuana businesses, bars, liquor stores, restaurants, caterers and street vendors are required to file monthly tax returns, regardless of sales volume. OCCUPATIONAL PRIVILEGE TAX (OPT) Monthly - filing is required if the business has 10 or more employees. The return is due on the last day of the month following the taxable month. Quarterly - filing is allowed if the business has fewer than 10 employees. The return is due on the last day of the month following the taxable month. Due dates are April 30, July 31, October 31 and January 31. Annual - annual filing is allowed for individuals, sole proprietors, and partnerships without employees. The return is due by January 31st. FACILITIES DEVELOPMENT ADMISSIONS (FDA) Monthly - filing is required for the purchase of each admission to any entertainment, amusement, or athletic event or other production or assembly staged, produced, convened, or held in or on any city-owned property. The return is due on the 15th day of the month following the month of sale/date of event. TELECOMMUNICATIONS BUSINESS TAX (TBT) Monthly - filing is required for landline within Denver City limits. The return is due on the 20th day of the month following the taxable month. 16 P a g e

18 The filing frequency of Emergency Telephone Charge (E911) filing forms are as follows: EMERGENCY TELEPHONE CHARGE (E911) Monthly - filing is required for every phone line within Denver City limits. The filing form is due on the last day of the month following the chargeable month. PENALTIES / INTEREST FOR LATE FILINGS If your filing form is filed AFTER the due date, you must pay a penalty of 15% of the tax due or $25.00, whichever is greater. NOTE: Mailed filing forms MUST be postmarked on or before the due date. (Only bonafide Post Office postmarks are acceptable. Postal meter dates are not accepted as proof of timely filing.) If your filing form is filed after the due date, interest is due at the rate of 1% for each month the filing form is past due. 17 P a g e

19 FILING TIPS For accurate and fast filing, file online using Denver s ebiz Tax Center at Follow the filing form instructions carefully. The instructions are included on each form. Report any excess tax collected on line 6 of the sales or lodger s tax return. It is illegal for you to keep excess tax collected. If you have a tax credit, enter the credit amount on the following lines of the specified return: RETURN LINE NO. Sales 12 OPT 6 Lodger s 10 Use 9 Be sure to attach back-up documentation to support your credit. The tax return must still be filed on time to avoid penalty and interest charges. Send your signed and dated tax return, along with your check made payable to Manager of Finance, to the address on the return. Do not send cash in the mail. Keep a copy of your return for your records. NO NEGATIVE RETURNS Entries on lines 1, 2B, and 4 of the Sales Tax Return and Lodger s Tax Return cannot be less than zero ($0.00). However, in those instances where deductions for bad debt and/or returned goods would result in a negative entry on line 4 or tax credits exceed $3,000.00, you are advised to apply for a refund of taxes paid. Total deductions reported cannot exceed gross sales and services on your return. NO TAXES OR CHARGES DUE? You MUST file a form for every period, even if no tax was collected or due. Complete the appropriate form with zero ($0.00) in all columns that apply. Failure to file will result in a late penalty of $ The form must be signed. 18 P a g e

20 BUSINESS PERSONAL PROPERTY TAXATION GENERAL INFORMATION The assessment process is the basis for generating property tax revenues that pay for schools, roads, fire protection, police protection, and other local services. Each year, millions of dollars in tax revenues are raised through the personal property tax, yet many taxpayers are often unaware of important personal property tax procedures and deadlines. All of the revenue generated by property taxes stays within your county. Property taxes DO NOT support any state services. PERSONAL PROPERTY Personal property is defined in (11) of the Colorado Revised Statutes (C.R.S.). The definition may be paraphrased as everything which is subject to ownership and which is not included in the category of real property. Personal property includes but is not l i m i t e d to furniture, machinery, equipment, and other articles related to the business of a commercial or industrial operation and can include certain leasehold improvements such as shelving, signs, counters, power wiring/cabling, etc. All of the laws concerning personal property taxation are set by the Colorado legislature and interpreted by the Colorado Division of Property Taxation, not by the City and County of Denver. The Assessor s office in the City and County of Denver is simply carrying out tax procedures which have been written by the Colorado legislature. These tax laws are the same in all Colorado counties. Each January, you will receive a declaration form (also called a schedule or a return) from the Assessor s office. On this form you will declare the assets which are used by your business. Be sure to send in your completed declaration by April 15, so that the assessment placed on your assets can be based on your own information, rather than on an estimate b y the Assessor which may be too high. You also have the option of filing your return online at and by with an Excel attachment to assessor@denvergov.org. After you submit your declaration, the Personal Property Section of the Assessor s office will calculate a value for your assets. In June, you will be sent a Notice of Valuation which will contain your new proposed value and instructions on how you can submit a protest if you disagree with that value. Be sure to follow the protest instructions if you think the value is wrong. Most personal property value protests are approved. Personal property tax bills are mailed in January for the prior year s taxes. Per C.R.S., you have the option to pay the tax in full, on or before April 30, or in two equal installments, with the first installment due by the last day of February and the second installment due June 15. Whenever there is a major change in your business, such as a new address or a closure, etc., be sure to promptly notify the Personal Property Section of the Assessor s Office at or at assessor@denvergov.org. 21 P a g e

21 THE ASSESSOR S RESPONSIBILITY The County Assessor is responsible for valuing all property in the county, as directed by state laws. The Assessor s goal is equalization of property values to ensure that the tax burden is distributed fairly and equitably among property owners, as defined in section (2) C.R.S. THE BUSINESS OWNER S RESPONSIBILITY As the property owner and taxpayer, you have specific rights and responsibilities in the assessment process. You have the right to examine the assessor s property records and to participate in the budget hearings held by school boards, cities and towns, and special districts that levy taxes on your property. You also have the right to protest your property s value if you disagree with the assessor s valuation. Additionally, you have the responsibility to provide accurate information to the assessor about property you own, as defined in section C.R.S. THE TREASURER S RESPONSIBILITIES The Treasurer is responsible for collection of property tax as directed by state law. The Treasurer s goal is the timely and efficient collection of property tax. FILING DECLARATIONS As stipulated at C.R.S., as soon after the assessment date as may be practicable, the Assessor shall mail or deliver two copies of the personal property schedule to the place of business or to the residence of each person known or believed to own taxable personal property located in his county, or to the agent of such person. Such person or his agent shall list in such schedule all taxable personal property owned by him, or in his possession, or under his control located in said county on the assessment date, attaching such exhibits or statements thereto as may be necessary, and shall sign and return the original copy thereof to the assessor no later than the April 15 next following. A sample personal property declaration schedule is included at the back of this booklet. The declaration schedule and filing instructions can also be obtained from the City and County of Denver Assessor's website along with other important property assessment information and forms. The website address is 22 P a g e

22 LEASED, LOANED, OR RENTED PERSONAL PROPERTY As stated in C.R.S., it is the responsibility of the owner of business personal property to provide accurate information about property they own. The owner or title holder of leased, loaned or rented personal property has the responsibility to accurately report that property to the assessor, including property which may be under a capital lease contract (or similar financing agreement). Additionally, the lessee of business personal property should report leased, loaned or rented property in section H of the declaration schedule. DECLARATION FILING OPTIONS Denver businesses may file their personal property declarations in the following ways: Online: Go to Note: automated filing meets the legal filing requirement and ensures greater accuracy because your data is loaded directly into our valuation software, reducing the chance of errors or omissions. By Mail: Denver County Assessor Personal Property 201 W. Colfax Ave., Dept 403 Denver, CO By - Using an Attachment: 1. Create or generate your asset data spreadsheet (using Excel is the most common) listing the following for each asset: o acquisition date o cost o brief description of the property 2. Attach your asset data spreadsheet to an 3. Send your to assessor@denvergov.org IMPORTANT NOTES: Filing deadline is April 15 If you elect to file online or by then DO NOT file a paper declaration. If you do your assessment may be too high! File by only one of the methods listed above. 23 P a g e

23 A MESSAGE TO SMALL BUSINESS OWNERS If your business is a small business in Denver County you may be exempt from business personal property tax, in accordance with Colorado Revised Statutes (C.R.S.). You are not required to file a personal property declaration if the total actual value (market value) of your personal property is under a specific threshold (go to the Assessor s website at to obtain the current threshold). However, if your business is new to Denver County, and you have never filed a declaration schedule, to ensure that the exemption (if applicable) is properly recorded for your business, please provide a complete listing of all machinery, equipment, and other personal property at your business location. This listing will help to ensure that the Assessor s office will properly set up your business as exempt if you have indicated that the total actual value (market value) of your business property is under the threshold. If you have questions regarding the actual value of your property, please call (720) Please note, if you file a personal property declaration and, based on the information you submit, it is determined that the actual value of your property is under the threshold you will automatically be exempted from business personal property tax. EXEMPTIONS FROM ASSESSMENT Organizations that have non-profit status for federal (Internal Revenue Service) purposes are not automatically exempt from local personal property assessments. To obtain such exempt status, organizations that are charitable, educational, or religious in nature, must apply to the State Division of Property Taxation. Exemption applications can be obtained by calling the Division of Property Taxation at (303) Other exemptions include but are not limited to inventory, intangible assets (such as software), and consumable supplies having a life of one year or less. Additional information on exemptions can be found in the Assessor s Reference Library Volume 5. To view the Assessor s Reference Library, please click here. PERSONAL PROPERTY ASSESSMENT CALENDAR January 1, 12 Noon: Assessment date for all taxable property. As soon after January 1 as possible: Assessor mails two Personal Property Declaration Schedules to each taxpayer. Not later than April 15 Taxpayers must return Personal Property Declaration Schedules to Assessor. Subsequent to April 15: Assessor determines personal property values. By June 15: Assessor sends property values and protest instructions. 24 P a g e

24 June 30: Taxpayer deadline for mailing protest of values. July 5: Taxpayer deadline for in-person/walk-in protest of values. By July 10 in even years and August 31 in odd years: Assessor must mail Notices of Determination of protests. By July 20 in even years and September 15 in odd years: Taxpayer may appeal Assessor s determination to County Board of Equalization. In January of the following year, personal property tax bills are mailed. If you have Business Personal Property assessment questions that are not covered in this booklet, you may obtain assistance by telephone, through the mail, in person or online. By Phone: By Mail or in Person: Denver Assessment Division Business Personal Property 201 W. Colfax Ave., Dept 406 Denver, CO By assessor@denvergov.org Online at the Denver Assessor s Website: Online Colorado Division of Property Taxation Website: PAYMENT AND COLLECTION OF PERSONAL PROPERTY TAX Bills for personal property tax are mailed in January, with the following payment options: 1) Pay the tax in full by April 30, or 2) Pay in halves - first half is due the last day of February, and the second half is due June 15. NOTE: Personal property taxes are paid one year in arrears. If the tax is not paid on time, then state law directs that delinquent interest will be charged (at the rate of 1% per month) on the unpaid tax amount. Collection of delinquent personal property tax will occur shortly after the due date(s) have passed without full payment. If the taxes and delinquent interest remain unpaid by the end of August, then state law directs that the delinquency be advertised in September in a 25 P a g e

25 newspaper published within the county. As a final step in the collection process, if full payment is not received by September 30, then the personal property is subject to seizure and sale beginning October 1. REAL PROPERTY TAX Questions regarding commercial or industrial real estate tax should be directed to or visit the Assessor s website at For information regarding the collection of real property tax contact the Treasury Division at or visit the Treasurer s website at 26 P a g e

26 DUE DATES SALES TAX, LODGER S TAX, USE TAX Monthly Returns: Due the 20th day of the month following the reporting month. For example, a January return is due February 20. Quarterly Returns: January March..due April 20 April June due July 20 July September.due October 20 October December..due January 20 Annual Returns: Due January 20 OCCUPATIONAL PRIVILEGE TAX Monthly Returns: Due the last day of the month following the reporting period. For example, a February return is due March 31. Quarterly Returns: January March....due April 30 April June..due July 31 July September.. due October 31 October December....due January 31 Annual Returns: Due January 31 and is available for individuals, sole proprietors, and partnerships without employees. FACILITIES DEVELOPMENT ADMISSION (FDA) TAX Due the 15 th day of the month following the month of the sale. TELECOMMUNICATIONS BUSINESS TAX Due the 20 th day of the month following the month for which the tax is levied. EMERGENCY TELEPHONE CHARGE (E911) Due the last day of the month following the month for which the tax is levied. 27 P a g e

27 PERSONAL PROPERTY TAX February 28 (February 29 in leap year): First half tax due (if paid in halves) April 15: Taxpayers must return Personal Property Declaration Schedules to Assessor April 30: Full tax amount due (if not paid in halves) June 15: Second half tax due (if paid in halves) June 30: Taxpayer deadline for mailing protest of values July 5: Taxpayer deadline for in-person/walk-in protest of values July 20: Taxpayer may appeal Assessor s determination to County Board of Equalization REAL PROPERTY TAX February 28 (February 29 in leap year): First half of taxes due (if paid in halves); Maintenance District fees due in full April 30: Full tax amount due (if not paid in halves) June 15: Second half of taxes due (if paid in halves) 28 P a g e

28 WHERE TO GET HELP The following contacts can provide assistance and answer any questions that you and your company might have: City and County of Denver: City and County of Denver Information Desk 311 Business Assistance Center Treasury Division (all City of Denver tax issues) Assessor Excise and License Zoning Office of Economic Development Division of Workforce Development Division of Business Development Division of Contract Compliance Division of Housing and Neighborhood Development Building Department Quick Permits Permits and Regulatory Issues Building Department Assistance Desk ebiz Tax Center Help Line State of Colorado: Colorado Department of Revenue Colorado Secretary of State Colorado Department of Regulatory Agencies Colorado Division of Property Taxation Colorado Small Business Hotline Federal: U.S. Internal Revenue Service OR P a g e

29 EXAMPLE RETURNS AND DECLARATIONS EXAMPLE SALES TAX RETURN

30

31 EXAMPLE CONSUMER S USE TAX RETURN

32 EXAMPLE LODGER S TA X RETURN

33 EXAMPLE OCCUPATIONAL PRIVILEGE TAX RETURN

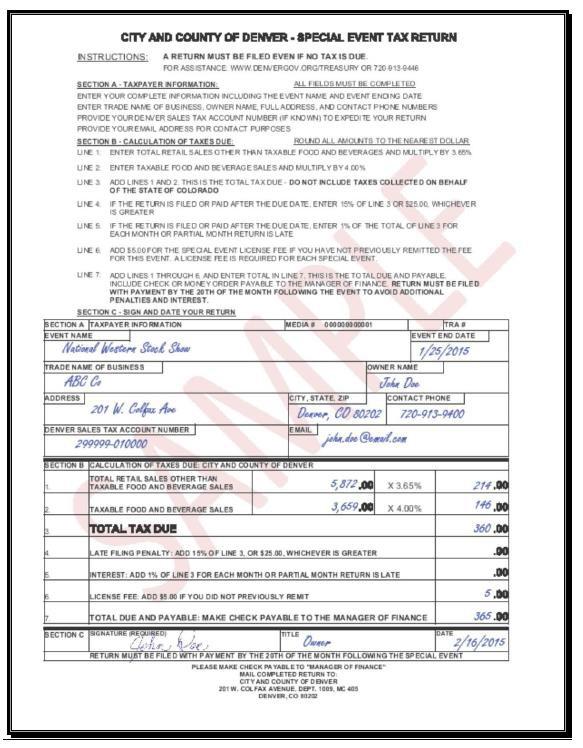

34 EXAMPLE SPECIAL EVENT APPLICATION AND SALES TAX RETURN

35

36 EXAMPLE TELECOMMUNICATIONS BUSINESS TAX RETURN

37 EXAMPLE FACILITIES DEVELOPMENT ADMISSIONS TAX RETURN

38 EXAMPLE EMERGENCY TELEPHONE CHARGE FILING FORM

39 EXAMPLE BUSINESS PERSONAL PROPERTY TAX DECLARATION

40

January 1, If you have any questions please don t hesitate to contact Taxpayer Service at or by at

Department of Finance Treasury Division Tax Compliance Audit Unit 201 W Colfax Ave MC 1001, Dept #1009 Denver, CO 80202 www.denvergov.org/treasury January 1, 2019 The City and County of Denver imposes

Department of Finance Treasury Division Tax Compliance Audit Unit 201 W Colfax Ave MC 1001, Dept #1009 Denver, CO 80202 www.denvergov.org/treasury January 1, 2019 The City and County of Denver imposes

Chapter 4.12 LODGERS' TAX 1

Page 1 of 13 Chapter 4.12 LODGERS' TAX 1 4.12.010: SHORT TITLE: This chapter shall be known as and may be cited as THE LODGERS' TAX ORDINANCE. (Ord. 97-32 1, 1997: prior code 19-48) 4.12.020: PURPOSE:

Page 1 of 13 Chapter 4.12 LODGERS' TAX 1 4.12.010: SHORT TITLE: This chapter shall be known as and may be cited as THE LODGERS' TAX ORDINANCE. (Ord. 97-32 1, 1997: prior code 19-48) 4.12.020: PURPOSE:

Greenwood. Village UNDERSTANDING TAXES IN INSIDE: Licensing and Permits Occupational Privilege Tax Sales Tax

UNDERSTANDING TAXES IN Greenwood Village INSIDE: Licensing and Permits Occupational Privilege Tax Sales Tax Use Tax Building Materials Use Tax Accommodations Tax Property Tax Tax Filing Requirements Other

UNDERSTANDING TAXES IN Greenwood Village INSIDE: Licensing and Permits Occupational Privilege Tax Sales Tax Use Tax Building Materials Use Tax Accommodations Tax Property Tax Tax Filing Requirements Other

Subd. 5. "Health and Inspections Department" means the City of St. Cloud Health and

Section 441 - Lodging Establishments Section 441:00. Regulation of Lodging Establishments, Hotels, Motels, Bed and Breakfast and Board and Lodging Establishments. Subd. 1. Purpose. The purpose of this

Section 441 - Lodging Establishments Section 441:00. Regulation of Lodging Establishments, Hotels, Motels, Bed and Breakfast and Board and Lodging Establishments. Subd. 1. Purpose. The purpose of this

City and County of Denver Department of Finance Treasury Division. Short Term Rental Taxation Information

City and County of Denver Department of Finance Treasury Division Short Term Rental Taxation Information Individuals or businesses offering short-term lodging (less than 30 days) at a private residence

City and County of Denver Department of Finance Treasury Division Short Term Rental Taxation Information Individuals or businesses offering short-term lodging (less than 30 days) at a private residence

This chapter shall be known as and may be cited as "the lodgers' tax ordinance."

Chapter 3.08 LODGERS' TAX 3.08.010 Short title. This chapter shall be known as and may be cited as "the lodgers' tax ordinance." (Ord. 854 (part), 1999: prior code 14-45) 3.08.020 Purpose. The purpose

Chapter 3.08 LODGERS' TAX 3.08.010 Short title. This chapter shall be known as and may be cited as "the lodgers' tax ordinance." (Ord. 854 (part), 1999: prior code 14-45) 3.08.020 Purpose. The purpose

SALES TAX INFORMATION GUIDE. Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO (970)

") SALES TA INFORMATION GUIDE Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO 81615 www.tosv.com (970) 923-3796 Table of Contents *You will be taken directly to any section in this document by

SALES TA INFORMATION GUIDE Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO 81615 www.tosv.com (970) 923-3796 Table of Contents *You will be taken directly to any section in this document by

CODE OF REGULATIONS. CUYAHOGA COUNTY -Division of Lodging Bed Tax -

CODE OF REGULATIONS CUYAHOGA COUNTY -Division of Lodging Bed Tax - REVISED September 12, 2000 Table of Contents Title..1 Definitions 1-2 Levy of the Tax, When Collectable; Exemptions; Presumption..2-3

CODE OF REGULATIONS CUYAHOGA COUNTY -Division of Lodging Bed Tax - REVISED September 12, 2000 Table of Contents Title..1 Definitions 1-2 Levy of the Tax, When Collectable; Exemptions; Presumption..2-3

COUNTY OF MONTEREY CHAPTER 5.40 UNIFORM TRANSIENT OCCUPANCY TAX

5.40.010 TITLE COUNTY OF MONTEREY CHAPTER 5.40 UNIFORM TRANSIENT OCCUPANCY TAX As amended June 19, 2007 The ordinance codified in this chapter shall be known as the Uniform Transient Occupancy Tax Ordinance

5.40.010 TITLE COUNTY OF MONTEREY CHAPTER 5.40 UNIFORM TRANSIENT OCCUPANCY TAX As amended June 19, 2007 The ordinance codified in this chapter shall be known as the Uniform Transient Occupancy Tax Ordinance

This is not a current year tax form and cannot be used to file a 2009 return. If you use this form for a tax year other than is intended, it will not

This is not a current year tax form and cannot be used to file a 2009 return If you use this form for a tax year other than is intended, it will not be processed Instead, it will be returned to you with

This is not a current year tax form and cannot be used to file a 2009 return If you use this form for a tax year other than is intended, it will not be processed Instead, it will be returned to you with

FYI For Your Information

TAXPAYER SERVICE DIVISION FYI For Your Information How to Document Sales to Retailers, Tax-Exempt Organizations and Direct Pay Permit Holders GENERAL INFORMATION The information contained in this FYI is

TAXPAYER SERVICE DIVISION FYI For Your Information How to Document Sales to Retailers, Tax-Exempt Organizations and Direct Pay Permit Holders GENERAL INFORMATION The information contained in this FYI is

Chapter 14 MUNICIPALLY IMPOSED TAXES AND FEES

Chapter 14 MUNICIPALLY IMPOSED TAXES AND FEES Some locally-imposed taxes and fees are optional, and a given municipality may have imposed all or portions of their taxing authority under that item. Other

Chapter 14 MUNICIPALLY IMPOSED TAXES AND FEES Some locally-imposed taxes and fees are optional, and a given municipality may have imposed all or portions of their taxing authority under that item. Other

CHAPTER 34 OCCUPATION AND OTHER TAXES

34.01 Municipal Retailers Occupation Tax 34.02 Municipal Service Occupation Tax 34.03 Municipal Use Tax 34.04 Police Protection Tax 34.05 Hotel Tax 34.06 Taxation of Occupations or Privileges CHAPTER 34

34.01 Municipal Retailers Occupation Tax 34.02 Municipal Service Occupation Tax 34.03 Municipal Use Tax 34.04 Police Protection Tax 34.05 Hotel Tax 34.06 Taxation of Occupations or Privileges CHAPTER 34

New Jersey Sales and Use Tax EZ Telefile System

New Jersey Sales and Use Tax EZ Telefile System (Forms ST-51 Monthly Return and ST-50 Quarterly Return) Instructions Filing Forms ST-50/51 by Phone Complete the EZ Telefile Worksheet, call the Business

New Jersey Sales and Use Tax EZ Telefile System (Forms ST-51 Monthly Return and ST-50 Quarterly Return) Instructions Filing Forms ST-50/51 by Phone Complete the EZ Telefile Worksheet, call the Business

Sales and Use Tax Returns. Sales and Use Tax Return HD/PM Date: / / DR-15 R. 08/18 Florida 1. Gross Sales 2. Exempt Sales 3. Taxable Amount 4.

Instructions for DR-15 Sales and Use Tax Returns Rule 12AER18-07, F.A.C. Effective 08/18 Page 1 of 8 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos and estimated tax

Instructions for DR-15 Sales and Use Tax Returns Rule 12AER18-07, F.A.C. Effective 08/18 Page 1 of 8 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos and estimated tax

2011 KANSAS Privilege Tax

2011 KANSAS Privilege Tax ON THE INSIDE General Information 2 Form K-130 4 Form K-130AS 8 Instructions for K-130 10 Instructions for K-130AS 13 Form K-131 16 ImproveProcessing Back Cover Tax Assistance

2011 KANSAS Privilege Tax ON THE INSIDE General Information 2 Form K-130 4 Form K-130AS 8 Instructions for K-130 10 Instructions for K-130AS 13 Form K-131 16 ImproveProcessing Back Cover Tax Assistance

CHAPTER 193 Transient Occupancy Excise Tax

179 CHAPTER 193 Transient Occupancy Excise Tax 193.01 DefInitions. 193.02 Rate of tax. 193.03 Exemptions. 193.04 Separately stated and charged. 193.05 Registration. 193.06 Reporting and remitting. 193.07

179 CHAPTER 193 Transient Occupancy Excise Tax 193.01 DefInitions. 193.02 Rate of tax. 193.03 Exemptions. 193.04 Separately stated and charged. 193.05 Registration. 193.06 Reporting and remitting. 193.07

Florida. Sales Tax Tales:

Sales Tax Tales: Objectives Registration and Account Maintenance Sales Tax Transactions Use Tax Tax Rates How to File and Pay Fact or Fiction New businesses must register at their nearest service center.

Sales Tax Tales: Objectives Registration and Account Maintenance Sales Tax Transactions Use Tax Tax Rates How to File and Pay Fact or Fiction New businesses must register at their nearest service center.

Title 3. Revenue and Finance

Title 3 Revenue and Finance Chapters: 3.04 Sales Tax 3.04.010 Definitions. 3.04.020 Schedules of Sales Tax. 3.04.030 General Provisions and Exemptions From Taxation. 3.04.040 Right of Retailer to Retain

Title 3 Revenue and Finance Chapters: 3.04 Sales Tax 3.04.010 Definitions. 3.04.020 Schedules of Sales Tax. 3.04.030 General Provisions and Exemptions From Taxation. 3.04.040 Right of Retailer to Retain

Dear New Business Owner,

Dear New Business Owner, The City of Beckley would like to take this opportunity to welcome you! The city believes that all business is important not only to our city but to the overall economy. I would

Dear New Business Owner, The City of Beckley would like to take this opportunity to welcome you! The city believes that all business is important not only to our city but to the overall economy. I would

Revenue Chapter ALABAMA DEPARTMENT OF REVENUE SALES, USE & BUSINESS TAX DIVISION ADMINISTRATIVE CODE

Revenue Chapter 810-6-5 ALABAMA DEPARTMENT OF REVENUE SALES, USE & BUSINESS TAX DIVISION ADMINISTRATIVE CODE CHAPTER 810-6-5 USE TAX LAW; CONTRACTORS GROSS RECEIPTS TAX; LODGINGS TAX; RENTAL TAX; UTILITY

Revenue Chapter 810-6-5 ALABAMA DEPARTMENT OF REVENUE SALES, USE & BUSINESS TAX DIVISION ADMINISTRATIVE CODE CHAPTER 810-6-5 USE TAX LAW; CONTRACTORS GROSS RECEIPTS TAX; LODGINGS TAX; RENTAL TAX; UTILITY

Office of the Madison City Clerk

Office of the Madison City Clerk 210 Martin Luther King, Jr., Boulevard, Room 103, Madison, Wisconsin 53703-3342 Phone: 608 266 4601 TDD: 608 266 6573 FAX: 608 266 4666 To: From: All City of Madison Hotel

Office of the Madison City Clerk 210 Martin Luther King, Jr., Boulevard, Room 103, Madison, Wisconsin 53703-3342 Phone: 608 266 4601 TDD: 608 266 6573 FAX: 608 266 4666 To: From: All City of Madison Hotel

Invest in Denver! FOR ILLUSTRATIVE PURPOSES ONLY; APPLICATION AVAILABLE SPRING 2017 THE 2017 DENVER BUSINESS INVESTMENT PROGRAM

Invest in Denver! City & County of Denver THE 2017 DENVER BUSINESS INVESTMENT PROGRAM For investments made in 2016, Denver s business owners can get a business personal property tax credit offered through

Invest in Denver! City & County of Denver THE 2017 DENVER BUSINESS INVESTMENT PROGRAM For investments made in 2016, Denver s business owners can get a business personal property tax credit offered through

City of Scottsbluff, Nebraska Monday, September 19, 2016 Regular Meeting

City of Scottsbluff, Nebraska Monday, September 19, 2016 Regular Meeting Item Resolut.2 Council to consider an Ordinance providing for a new 1 ½% restaurant occupation tax, effective January 1, 2017 (second

City of Scottsbluff, Nebraska Monday, September 19, 2016 Regular Meeting Item Resolut.2 Council to consider an Ordinance providing for a new 1 ½% restaurant occupation tax, effective January 1, 2017 (second

Sales and Use Tax Returns. File and pay electronically and on time to receive a collection allowance.

Instructions for DR-15 Sales and Use Tax Returns DR-15N R. 01/18 Rule 12A-1.097 Florida Administrative Code Effective 01/18 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos

Instructions for DR-15 Sales and Use Tax Returns DR-15N R. 01/18 Rule 12A-1.097 Florida Administrative Code Effective 01/18 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos

CHAPTER 21 TAXATION ARTICLE I. FIRE PROTECTION TAX ARTICLE II. FOREIGN FIRE INSURANCE COMPANY TAX

CHAPTER 21 TAXATION ART. I Fire Protection Tax, 21-1-1 21-1-2 ART. II Foreign Fire Insurance Company Tax, 21-2-1 21-2-5 ART. III Municipal Retailers Occupation Tax, 21-3-1 21-3-3 ART. IV. Municipal Service

CHAPTER 21 TAXATION ART. I Fire Protection Tax, 21-1-1 21-1-2 ART. II Foreign Fire Insurance Company Tax, 21-2-1 21-2-5 ART. III Municipal Retailers Occupation Tax, 21-3-1 21-3-3 ART. IV. Municipal Service

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54 RESALE CERTIFICATES This Bulletin is intended solely as advice to assist persons in determining, exercising

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54 RESALE CERTIFICATES This Bulletin is intended solely as advice to assist persons in determining, exercising

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 594 HOUSE BILL 703

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 594 HOUSE BILL 703 AN ACT TO AUTHORIZE WAKE COUNTY TO LEVY A ROOM OCCUPANCY TAX AND A PREPARED FOOD AND BEVERAGE TAX. The General Assembly of North

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 594 HOUSE BILL 703 AN ACT TO AUTHORIZE WAKE COUNTY TO LEVY A ROOM OCCUPANCY TAX AND A PREPARED FOOD AND BEVERAGE TAX. The General Assembly of North

Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers

New York State Department of Taxation and Finance Publication 774 (1/10) Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers About this publication

New York State Department of Taxation and Finance Publication 774 (1/10) Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers About this publication

Sales and Use Tax Return Filing Guide

Sales and Use Tax Return Filing Guide GENERAL QUESTIONS How often must I file? Depending on your filing schedule, your business will receive a sales and use tax form on a regular basis. Average tax due

Sales and Use Tax Return Filing Guide GENERAL QUESTIONS How often must I file? Depending on your filing schedule, your business will receive a sales and use tax form on a regular basis. Average tax due

Chapter TRANSIENT ROOM TAX

TITLE 8-4 Chapter 8.02 8.02 TRANSIENT ROOM TAX 8.02.010 Definitions Except where the context otherwise requires, the definitions given in this section govern the construction of this chapter. A. ACCRUAL

TITLE 8-4 Chapter 8.02 8.02 TRANSIENT ROOM TAX 8.02.010 Definitions Except where the context otherwise requires, the definitions given in this section govern the construction of this chapter. A. ACCRUAL

DECISION OF MUNICIPAL TAX HEARING OFFICER

DECISION OF MUNICIPAL TAX HEARING OFFICER Decision Date: August 13, 2004 Decision: MTHO #151 Tax Collector: Cities of Peoria, Tempe, and Scottsdale Hearing Date: April 5, 2004 Introduction DISCUSSION On

DECISION OF MUNICIPAL TAX HEARING OFFICER Decision Date: August 13, 2004 Decision: MTHO #151 Tax Collector: Cities of Peoria, Tempe, and Scottsdale Hearing Date: April 5, 2004 Introduction DISCUSSION On

CHAPTER FOUR: BUSINESS ACTIVITIES. Subchapter 4.01: Business Registration and Registration Tax

4.01.010 Purpose. CHAPTER FOUR: BUSINESS ACTIVITIES Subchapter 4.01: Business Registration and Registration Tax The purpose of this ordinance is to provide for the establishment and levying of registration

4.01.010 Purpose. CHAPTER FOUR: BUSINESS ACTIVITIES Subchapter 4.01: Business Registration and Registration Tax The purpose of this ordinance is to provide for the establishment and levying of registration

H 5209 S T A T E O F R H O D E I S L A N D

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

3rd Quarter 2006 ONLY

FOR PHONE Business Paperless Telefiling System Worksheet New Jersey Sales and Use Tax EZ Telefile System (Forms ST-51 Monthly Remittance Statement and ST-50 Quarterly Return) 3rd Quarter 26 ONLY Note:

FOR PHONE Business Paperless Telefiling System Worksheet New Jersey Sales and Use Tax EZ Telefile System (Forms ST-51 Monthly Remittance Statement and ST-50 Quarterly Return) 3rd Quarter 26 ONLY Note:

Florida Department of Revenue Tax Information Publication. TIP 03A01-20 Date Issued: Dec 17, 2003

Florida Department of Revenue Tax Information Publication TIP 03A01-20 Date Issued: Dec 17, 2003 COUPONS, DISCOUNTS, REBATES, FREE MERCHANDISE, AND OTHER PROMOTIONAL GIFTS Florida law provides that "discounts

Florida Department of Revenue Tax Information Publication TIP 03A01-20 Date Issued: Dec 17, 2003 COUPONS, DISCOUNTS, REBATES, FREE MERCHANDISE, AND OTHER PROMOTIONAL GIFTS Florida law provides that "discounts

Office of the City Clerk Maribeth Witzel-Behl, City Clerk

Office of the City Clerk Maribeth Witzel-Behl, City Clerk City-County Building, Room 103 210 Martin Luther King, Jr. Boulevard Madison, Wisconsin 53703 Phone: (608) 266-4601 Fax: (608) 266-4666 clerk@cityofmadison.com

Office of the City Clerk Maribeth Witzel-Behl, City Clerk City-County Building, Room 103 210 Martin Luther King, Jr. Boulevard Madison, Wisconsin 53703 Phone: (608) 266-4601 Fax: (608) 266-4666 clerk@cityofmadison.com

2008 KANSAS. Fiduciary Income Tax. Forms and Instructions. Page 1

2008 KANSAS Fiduciary Income Tax Forms and Instructions www.ksrevenue.org Page 1 What s New... The following changes are effective for the 2008 tax year: WHAT S IN THIS BOOKLET? What s New Tips to Improve

2008 KANSAS Fiduciary Income Tax Forms and Instructions www.ksrevenue.org Page 1 What s New... The following changes are effective for the 2008 tax year: WHAT S IN THIS BOOKLET? What s New Tips to Improve

ORDINANCE BE IT AND IT IS HEREBY ORDAINED by the Mayor and Council of the City of Hapeville and under the authority thereof that:

STATE OF GEORGIA CITY OF HAPEVILLE ORDINANCE 2013-03 AN ORDINANCE TO AMEND THE CODE OF ORDINANCES OF THE CITY OF HAPEVILLE, GEORGIA; TO AMEND CHAPTER 17, ARTICLE 7 HOTEL OCCUPANY TAX FOR THE PURPOSES OF

STATE OF GEORGIA CITY OF HAPEVILLE ORDINANCE 2013-03 AN ORDINANCE TO AMEND THE CODE OF ORDINANCES OF THE CITY OF HAPEVILLE, GEORGIA; TO AMEND CHAPTER 17, ARTICLE 7 HOTEL OCCUPANY TAX FOR THE PURPOSES OF

South Carolina Department of Revenue

SMALL BUSINESS TAX WORKSHOP South Carolina Department of Revenue Topics To Be Covered Today Checklist for New Businesses in South Carolina Purchasing the Assets of a Business The Retail License Sales &

SMALL BUSINESS TAX WORKSHOP South Carolina Department of Revenue Topics To Be Covered Today Checklist for New Businesses in South Carolina Purchasing the Assets of a Business The Retail License Sales &

FY Property Taxes

FY 2012-2013 Office of the Tax Collector Mecklenburg County, NC Mecklenburg Charlotte Cornelius Davidson Huntersville Matthews Mint Hill Pineville What do property taxes pay for? When you call the police

FY 2012-2013 Office of the Tax Collector Mecklenburg County, NC Mecklenburg Charlotte Cornelius Davidson Huntersville Matthews Mint Hill Pineville What do property taxes pay for? When you call the police

TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1 REAL PROPERTY TAXES

5-1 TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1. REAL PROPERTY TAXES. 2. SALES AND USE TAX 3. PRIVILEGE TAXES. 4. WHOLESALE BEER TAX. 5. COMPETITIVE BIDDING. 6. HOTEL/MOTEL PRIVILEGE TAXES. 5-101.

5-1 TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1. REAL PROPERTY TAXES. 2. SALES AND USE TAX 3. PRIVILEGE TAXES. 4. WHOLESALE BEER TAX. 5. COMPETITIVE BIDDING. 6. HOTEL/MOTEL PRIVILEGE TAXES. 5-101.

DR-15EZ. Sales and Use Tax Returns

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 07/12 Rule 12A-1.097 Florida Administrative Code Are you Eligible to Use a DR-15EZ Return? Collection Allowance Our records indicate you are

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 07/12 Rule 12A-1.097 Florida Administrative Code Are you Eligible to Use a DR-15EZ Return? Collection Allowance Our records indicate you are

Sales Tax Guidelines for the Construction Industry Originally issued March 26, 2003/Revised August 1, 2014 Wyoming Department of Revenue

Sales Tax Guidelines for the Construction Industry Originally issued March 26, 2003/Revised August 1, 2014 Wyoming Department of Revenue This publication is intended for those in the construction industry.

Sales Tax Guidelines for the Construction Industry Originally issued March 26, 2003/Revised August 1, 2014 Wyoming Department of Revenue This publication is intended for those in the construction industry.

State Tax Return. Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

New Jersey Sales and Use Tax EZ Telefile System Instructions

New Jersey Sales and Use Tax EZ Telefile System Instructions (Forms ST-50 Quarterly Return and ST-51 Monthly Remittance Statement) Do NOT Use for 3rd Quarter 2006 Rate Change The New Jersey Sales and Use

New Jersey Sales and Use Tax EZ Telefile System Instructions (Forms ST-50 Quarterly Return and ST-51 Monthly Remittance Statement) Do NOT Use for 3rd Quarter 2006 Rate Change The New Jersey Sales and Use

Oneida Indian Nation Tax Rules Effective as of March 5, 2014

Oneida Indian Nation Tax Rules Effective as of March 5, 2014 I. RULES OF THE NATION DEPARTMENT OF TAXATION A. The Oneida Nation has authorized the creation of the Nation Department of Taxation with responsibility

Oneida Indian Nation Tax Rules Effective as of March 5, 2014 I. RULES OF THE NATION DEPARTMENT OF TAXATION A. The Oneida Nation has authorized the creation of the Nation Department of Taxation with responsibility

Table of Contents FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

Important Information About This Summary This document briefly summarizes recent substantive changes to Arizona's tax laws. The bills addressed herein were approved by Arizona's Legislature and signed

Important Information About This Summary This document briefly summarizes recent substantive changes to Arizona's tax laws. The bills addressed herein were approved by Arizona's Legislature and signed

Operating a Restaurant in Conway or Operating a Private Club Serving Alcohol in Conway

Michael O. Garrett Clerk-Treasurer cityclerk@cityofconway.org City of Conway 1201 Oak Street Conway, Arkansas 72032 501-450-6100 501-450-6109 FAX Operating a Restaurant in Conway or Operating a Private

Michael O. Garrett Clerk-Treasurer cityclerk@cityofconway.org City of Conway 1201 Oak Street Conway, Arkansas 72032 501-450-6100 501-450-6109 FAX Operating a Restaurant in Conway or Operating a Private

CBJ SALES TAX OFFICE GENERAL GUIDELINES FOR CBJ SALES TAX EXEMPTIONS Procedure 400

CBJ SALES TAX OFFICE GENERAL GUIDELINES FOR CBJ SALES TAX EXEMPTIONS Procedure 400 The following guideline provides a brief, general description of the CBJ sales tax exemptions. It does not provide specific

CBJ SALES TAX OFFICE GENERAL GUIDELINES FOR CBJ SALES TAX EXEMPTIONS Procedure 400 The following guideline provides a brief, general description of the CBJ sales tax exemptions. It does not provide specific

Uniform Transient Occupancy Tax. (a) DEFINITIONS AND GENERAL PROVISIONS. ( 1 ) Reference to Ordinance or Statute. Whenever any reference is

DEFINITIONS AND GENERAL PROVISIONS. ( 1 ) Reference to Ordinance or Statute. Whenever any reference is") 14.023 Uniform Transient Occupancy Tax. (a) DEFINITIONS AND GENERAL PROVISIONS. ( 1 ) Reference to Ordinance or Statute. Whenever any reference is made to any portion of this, or of any other ordinance,

14.023 Uniform Transient Occupancy Tax. (a) DEFINITIONS AND GENERAL PROVISIONS. ( 1 ) Reference to Ordinance or Statute. Whenever any reference is made to any portion of this, or of any other ordinance,

PORTAGE TOWNSHIP OTTAWA COUNTY, OHIO

PORTAGE TOWNSHIP OTTAWA COUNTY, OHIO LODGING EXCISE TAX REGULATIONS EFFECTIVE JANUARY 1, 2009 1 PORTAGE TOWNSHIP LODGING EXCISE TAX REGULATIONS INDEX Section 1. Title 3 Page Section 2. Definitions 3-4

PORTAGE TOWNSHIP OTTAWA COUNTY, OHIO LODGING EXCISE TAX REGULATIONS EFFECTIVE JANUARY 1, 2009 1 PORTAGE TOWNSHIP LODGING EXCISE TAX REGULATIONS INDEX Section 1. Title 3 Page Section 2. Definitions 3-4

Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages

212.05 Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages in the business of selling tangible personal property

212.05 Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages in the business of selling tangible personal property

RELATED ACTS. Priv. Acts 1999, ch. 39, "Relative to the levy of a privilege tax on hotels, inns, tourist camps, tourist cabins, motels, etc."...

C-41 RELATED ACTS Priv. Acts 1999, ch. 39, "Relative to the levy of a privilege tax on hotels, inns, tourist camps, tourist cabins, motels, etc."... C-42 C-42 PRIVATE ACTS 1999 CHAPTER NO. 39 HOUSE BILL

C-41 RELATED ACTS Priv. Acts 1999, ch. 39, "Relative to the levy of a privilege tax on hotels, inns, tourist camps, tourist cabins, motels, etc."... C-42 C-42 PRIVATE ACTS 1999 CHAPTER NO. 39 HOUSE BILL

Small Business Tax Organizer

EIN Name Date Started Street Address City State Zip Code Please utilize this Tax Organizer to help you gather and organize information relating to preparation of your business income tax returns. Where

EIN Name Date Started Street Address City State Zip Code Please utilize this Tax Organizer to help you gather and organize information relating to preparation of your business income tax returns. Where

Booklet Includes: Instructions DR 0112 Related Forms. Colorado C Corporation Income Tax Filing Guide This book includes:

(10/11/18) Booklet Includes: Instructions DR 0112 Related Forms 112 Book C Corporation 2018 Colorado C Corporation Income Tax Filing Guide This book includes: DR 0112 2018 Colorado C Corporation Income

(10/11/18) Booklet Includes: Instructions DR 0112 Related Forms 112 Book C Corporation 2018 Colorado C Corporation Income Tax Filing Guide This book includes: DR 0112 2018 Colorado C Corporation Income

STREAMLINED SALES TAX PROJECT TAXES AFFECTED BY SSTP ACT AND AGREEMENT (7/3/02)

") The Project approved moving this paper to the Implementing States on June 14, 2002. Draft Document Not For Publication But For Discussion Purposes Only Nothing contained herein represents a final position

The Project approved moving this paper to the Implementing States on June 14, 2002. Draft Document Not For Publication But For Discussion Purposes Only Nothing contained herein represents a final position

DR-15EZ Sales and Use Tax Returns

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 01/16 TC Rule 12A-1.097 Florida Administrative Code Effective 01/16 Are you Eligible to Use a DR-15EZ Return? Collection Allowance Our records

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 01/16 TC Rule 12A-1.097 Florida Administrative Code Effective 01/16 Are you Eligible to Use a DR-15EZ Return? Collection Allowance Our records

Allegheny County Alcoholic Beverage Tax Official Rules and Regulations

Allegheny County Alcoholic Beverage Tax Official Rules and Regulations Table of Contents Preface... 1 Section 101. Definitions.... 2 Section 102. Imposition and Rate of Tax.... 3 Section 103. Taxable Transactions....

Allegheny County Alcoholic Beverage Tax Official Rules and Regulations Table of Contents Preface... 1 Section 101. Definitions.... 2 Section 102. Imposition and Rate of Tax.... 3 Section 103. Taxable Transactions....

KANSAS LIQUOR DRINK TAX ACT AND REGULATIONS

KANSAS LIQUOR DRINK TAX ACT AND REGULATIONS K.S.A. Chapter 79, Article 41a Last amended in 2013 K.A.R. Agency 92, Article 24 Last amended in March 2010 Without Annotations - For Public Distribution Division

KANSAS LIQUOR DRINK TAX ACT AND REGULATIONS K.S.A. Chapter 79, Article 41a Last amended in 2013 K.A.R. Agency 92, Article 24 Last amended in March 2010 Without Annotations - For Public Distribution Division

Florida Senate SB 1320

By Senator Stargel 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 A bill to be entitled An act relating to tax administration; amending s. 198.30, F.S.; deleting a requirement

By Senator Stargel 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 A bill to be entitled An act relating to tax administration; amending s. 198.30, F.S.; deleting a requirement

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION HOUSE BILL DRH40552-MCx-164 (04/05)

") H GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 HOUSE BILL DRH0-MCx- (0/0) H.B. 00 Apr, 0 HOUSE PRINCIPAL CLERK D Short Title: Safe Infrastructure & Low Property Tax Act. (Public) Sponsors: Referred to:

H GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 HOUSE BILL DRH0-MCx- (0/0) H.B. 00 Apr, 0 HOUSE PRINCIPAL CLERK D Short Title: Safe Infrastructure & Low Property Tax Act. (Public) Sponsors: Referred to:

BUTLER COUNTY HOTEL ROOM RENTAL TAX TRAINING JULY 12, 2016 PRESENTED BY DIANE R. MARBURGER, CTP MICHAEL H. PEULER, CPA, CFP INDEPENDENT AUDITOR

BUTLER COUNTY HOTEL ROOM RENTAL TAX TRAINING JULY 12, 2016 PRESENTED BY DIANE R. MARBURGER, CTP COUNTY TREASURER MICHAEL H. PEULER, CPA, CFP INDEPENDENT AUDITOR History OVERVIEW Rules & Regulations Latest

BUTLER COUNTY HOTEL ROOM RENTAL TAX TRAINING JULY 12, 2016 PRESENTED BY DIANE R. MARBURGER, CTP COUNTY TREASURER MICHAEL H. PEULER, CPA, CFP INDEPENDENT AUDITOR History OVERVIEW Rules & Regulations Latest

CHAPTER 545 LODGING TAX

CHAPTER 545 Section 545 LODGING TAX Section 545.01 Definitions 545.02 Imposition of Tax 545.03 Collections 545.04 Exceptions and Exemptions 545.05 Advertising No Tax 545.06 Payment and Returns 545.07 Records

CHAPTER 545 Section 545 LODGING TAX Section 545.01 Definitions 545.02 Imposition of Tax 545.03 Collections 545.04 Exceptions and Exemptions 545.05 Advertising No Tax 545.06 Payment and Returns 545.07 Records

Self Employment Income & Single Member LLC Organizer This Organizer belongs to:

This self-employment organizer will assist you with organization of your business information and records. The IRS imposes reporting and record-keeping rules, some of which are described in this Organizer.

This self-employment organizer will assist you with organization of your business information and records. The IRS imposes reporting and record-keeping rules, some of which are described in this Organizer.

Hotel Occupancies and New Jersey Taxes

Tax Topic Bulletin S&U-13 Introduction This bulletin explains the application of the New Jersey Sales and Use Tax Act to the sale of hotel occupancies and related property, services, and fees. It also

Tax Topic Bulletin S&U-13 Introduction This bulletin explains the application of the New Jersey Sales and Use Tax Act to the sale of hotel occupancies and related property, services, and fees. It also

Self Employment Income & Single Member LLC Organizer This Organizer belongs to:

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

ACCOMMODATION ORDINANCE COUNTY OF GENESEE STATE OF MICHIGAN

ACCOMMODATION ORDINANCE COUNTY OF GENESEE STATE OF MICHIGAN AN ORDINANCE PROVIDING FOR THE ASSESSMENT AND COLLECTION OF AN EXCISE TAX ON PERSONS ENGAGE IN THE BUSINESS OF PROVIDING ROOMS FOR DWELLING,

ACCOMMODATION ORDINANCE COUNTY OF GENESEE STATE OF MICHIGAN AN ORDINANCE PROVIDING FOR THE ASSESSMENT AND COLLECTION OF AN EXCISE TAX ON PERSONS ENGAGE IN THE BUSINESS OF PROVIDING ROOMS FOR DWELLING,

TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1 MISCELLANEOUS

5-1 CHAPTER 1. MISCELLANEOUS. 2. REAL PROPERTY TAXES. 3. PRIVILEGE TAXES. 4. WHOLESALE BEER TAX. 5. HOTEL/MOTEL TAX. TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 5-101. Fiscal year. 5-102. Depositories for

5-1 CHAPTER 1. MISCELLANEOUS. 2. REAL PROPERTY TAXES. 3. PRIVILEGE TAXES. 4. WHOLESALE BEER TAX. 5. HOTEL/MOTEL TAX. TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 5-101. Fiscal year. 5-102. Depositories for

CHAPTER 21 COUNTY PERMISSIVE LODGING TAX

CHAPTER 21 COUNTY PERMISSIVE LODGING TAX 21.01 INTRODUCTION Latest Revision July, 2013 In l967 municipalities and townships were given authority to levy a 3% lodging tax which could be used for any lawful

CHAPTER 21 COUNTY PERMISSIVE LODGING TAX 21.01 INTRODUCTION Latest Revision July, 2013 In l967 municipalities and townships were given authority to levy a 3% lodging tax which could be used for any lawful

FRIDLEY CITY CODE CHAPTER 608. LODGING TAX (Ref. 859)

") FRIDLEY CITY CODE CHAPTER 608. LODGING TAX (Ref. 859) 608.01 PURPOSE The legislature has authorized the imposition of a tax upon lodging at a hotel, motel, rooming house, tourist court or other use of

FRIDLEY CITY CODE CHAPTER 608. LODGING TAX (Ref. 859) 608.01 PURPOSE The legislature has authorized the imposition of a tax upon lodging at a hotel, motel, rooming house, tourist court or other use of

RELATED ACTS 1. Priv. Acts 1981, ch. 51, "Privilege tax on the occupancy of hotels and motels, etc."... C-42

C-41 RELATED ACTS 1 PAGE Priv. Acts 1981, ch. 51, "Privilege tax on the occupancy of hotels and motels, etc."... C-42 1 The validity of this act is questionable since the town operates under the general

C-41 RELATED ACTS 1 PAGE Priv. Acts 1981, ch. 51, "Privilege tax on the occupancy of hotels and motels, etc."... C-42 1 The validity of this act is questionable since the town operates under the general

Application for Refund. Application. Have Questions? Inside. Use the enclosed form to request a refund for: Call

Application for Refund Use the enclosed form to request a refund for: Have Questions? Call 850-488-8937 Inside Frequently Asked Questions... p. 2-3 For Information, Forms, and Online Filing... p. 3 Application

Application for Refund Use the enclosed form to request a refund for: Have Questions? Call 850-488-8937 Inside Frequently Asked Questions... p. 2-3 For Information, Forms, and Online Filing... p. 3 Application

DR-15EZ Sales and Use Tax Returns

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 01/18 Rule 12A-1.097 Florida Administrative Code Effective 01/18 Are you Eligible to Use a DR-15EZ Return? Businesses that: Pay $200,000 or

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 01/18 Rule 12A-1.097 Florida Administrative Code Effective 01/18 Are you Eligible to Use a DR-15EZ Return? Businesses that: Pay $200,000 or

CHAPTER 118: LODGING TAX

CHAPTER 118: LODGING TAX Section 118.01 Definitions 118.02 Imposition of lodging tax 118.03 Exceptions and exemptions 118.04 Advertising no lodging tax 118.05 Collections 118.06 Payment and returns 118.07

CHAPTER 118: LODGING TAX Section 118.01 Definitions 118.02 Imposition of lodging tax 118.03 Exceptions and exemptions 118.04 Advertising no lodging tax 118.05 Collections 118.06 Payment and returns 118.07