Part-II H Individual Income Tax Return 2016

|

|

|

- Solomon Reynold Dawson

- 5 years ago

- Views:

Transcription

1

2 Part-II H Individual Income Tax Return 2016

3

4

5

6

7

8

9

10

11 Part-II H AOP Income Tax Return 2016

12

13

14

15

16

17

18

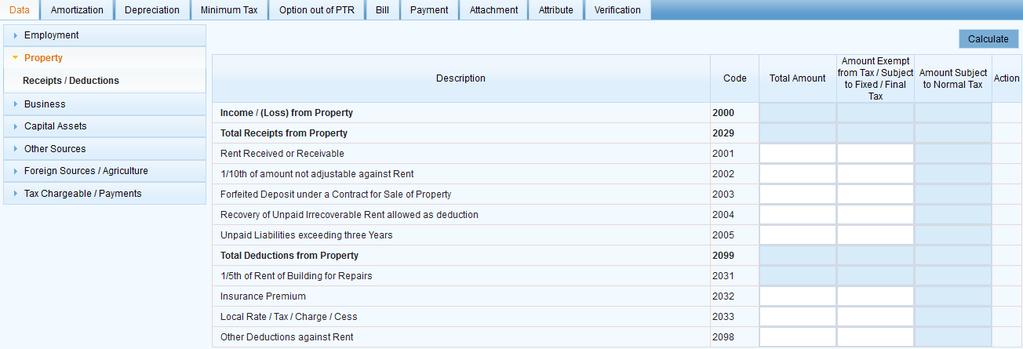

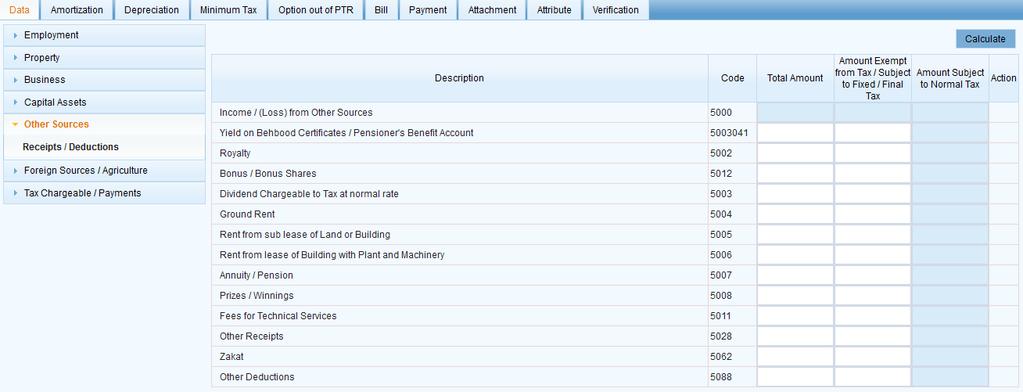

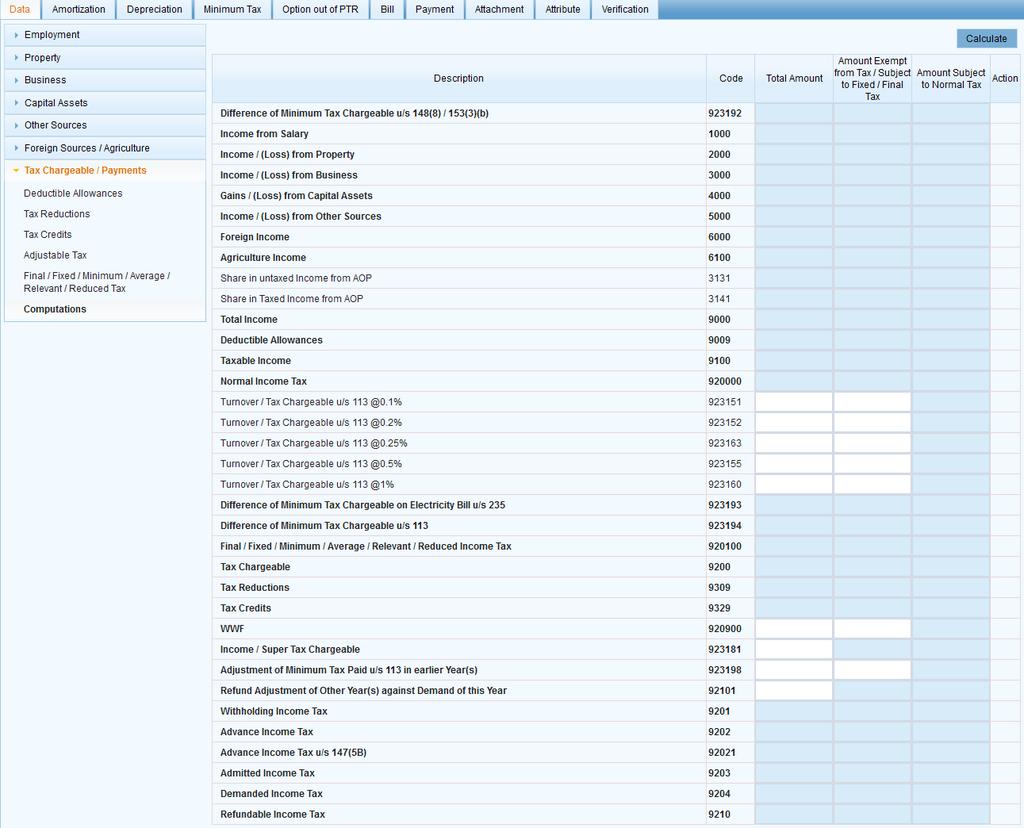

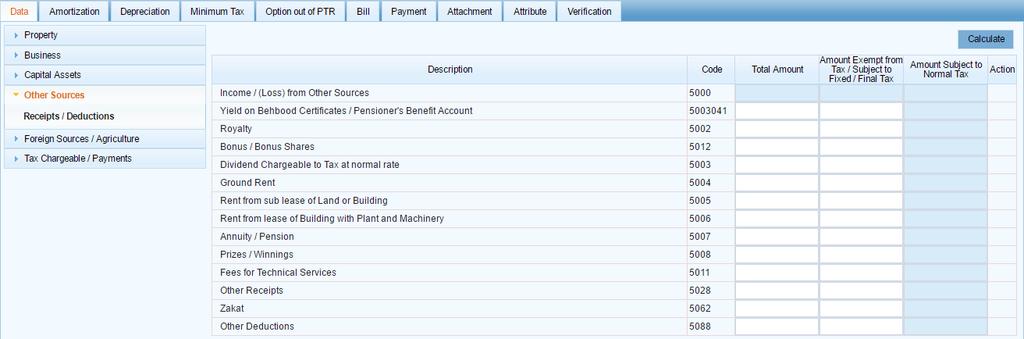

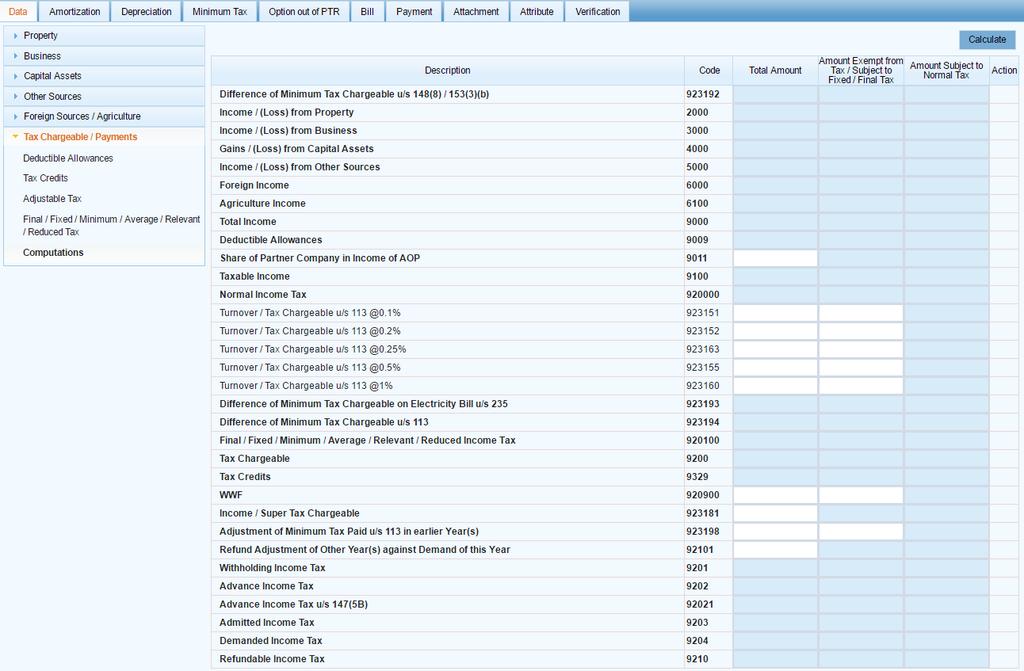

19 Name* Other Sources Deductible Allowances Computations CNIC* Address* Property Final / Fixed / Average / Relevant / Reduced Rate Regime Verification Sr. Code 1 Income / (Loss) from Property [Sum of 2 to 6] - [Sum of 7 to 10] Rent Received or Receivable /10th of amount not adjustable against Rent Forfeited Deposit under a Contract for Sale of Property Recovery of Unpaid Irrecoverable Rent allowed as deduction Unpaid Liabilities exceeding three years /5th of Rent of Building for Repairs [(2+3+4)*20%] Insurance Premium Local Rate / Tax / Charge / Cess Other Deductions against Rent Gains / (Loss) from Capital Assets Income / (Loss) from Other Sources Yield on Behbood Certificates / Pensioner''s Benefit Account Receipts from Other Sources Royalty Profit on Debt (Interest, Yield, etc) Ground Rent Rent from sub lease of Land or Building Rent from lease of Building with Plant and Machinery Bonus / Bonus Shares Loan, Advance, Deposit or Gift received in Cash Other Receipts Deductions from Other Sources Accounting Depreciation Other Deductions Foreign Income Share in untaxed Income from AOP Share in Taxed Income from AOP Total Income* Deductible Allowances [18+19] Zakat u/s Charitable Donations u/c 61, Part I, 2nd Schedule Taxable Income [16-17]* Tax Chargeable [Col.C ] Normal Income Tax Tax Reduction for Senior Taxpayer Tax Reduction for Disabled Taxpayer Tax Credits Tax Credit for Deductable Allowance for Profit on Debt u/s 64A Tax Credit for Employment Generation by Manufacturers u/s 64B Super Tax Signature: RETURN OF TOTAL INCOME / STATEMENT OF FINAL TAXATION UNDER THE INCOME TAX ORDINANCE, 2001 (IT-1B) (FOR INDIVIDUAL, DERIVING INCOME UNDER ANY HEAD OTHER THAN SALARY / BUSINESS) Description Tax Paid [Sr.28 Col. B+Sr.29 Col. B+Sr.35 Col. B+Sr.1 Col.B Annex-A] 43 Advance Income Tax Admitted Income Tax Refundable Income Tax [21-27 if <0] Demanded Income Tax [21-27 if >0] Refund Adjustment of Other Year(s) against Demand of this Year [=30] Agriculture Income Agriculture Income Tax 9291 Final / Fixed / Minimum / Average / Relevant / Reduced Income Tax [Sum of to 56] Dividend u/s Dividend u/s Dividend u/s 12.50% Profit on Debt u/s 151 from NSC / PO Deposits Profit on Debt u/s 151 from Bank Accounts / Deposits Profit on Debt u/s 151 from Government Securities Profit on Debt u/s 151 from Others Prize on Prize Bond u/s Winnings from Crossword Puzzle u/s Winnings from Raffle u/s Winnings from Lottery u/s Winnings from Quiz u/s Winnings from Sale Promotion u/s Dividend in specie u/s 236S Issuance of Bonus Shares by Companies not quoted on Stock Exchange u/s 236N Capital Gains on Immovable Property u/s Capital Gains on Immovable Property u/s Capital Gains on Immovable Property u/s Capital Gains on Securities u/s Capital Gains on Securities u/s Capital Gains on Securities u/s Capital Gains on Securities u/s I,, CNIC No. Total Amount Tax Year 2016 NTN Amount Exempt from Tax / Subject to Fixed / Final Tax Amount Subject to Normal Tax A B C Total Inadmissible Admissible Receipts / Value Tax Collected/ Deducted/Paid, in my capacity as Self / Date: Tax Chargeable Representative (as defined in section 172 of the Income Tax Ordinance, 2001) of the Taxpayer named above, do solemnly declare that to the best of my knowledge & belief the information given in this Return / Statement u/s 115(4) is correct & complete in accordance with the provisions of the Income Tax Ordinance, 2001 & Income Tax Rules, 2002.

20 RETURN OF TOTAL INCOME / STATEMENT OF FINAL TAXATION UNDER THE INCOME TAX ORDINANCE, 2001 (IT-2) 1/2 Name* CNIC* Address* FOR INDIVIDUAL DERIVING INCOME UNDER THE HEAD BUSINESS & ANY OTHER HEAD EXCEPT SALARY Tax Year 2016 NTN* Sr. Description Code Total Amount Amount Exempt from Tax / Subject to Fixed / Final Tax Amount Subject to Normal Tax A B C Property Other Sources Deductible Allowances 1 Income from Business Income / (Loss) from Property [Sum of 3 to 7] -[Sum of 8 to 11] Rent Received or Receivable /10th of amount not adjustable against Rent Forfeited Deposit under a Contract for Sale of Property Recovery of Unpaid Irrecoverable Rent allowed as deduction Unpaid Liabilities exceeding three years /5th of Rent of Building for Repairs [(3+4+5)*20%] Insurance Premium Local Rate / Tax / Charge / Cess Other Deductions against Rent Gains / (Loss) from Capital Assets Income / (Loss) from Other Sources Yield on Behbood Certificates / Pensioner''s Benefit Account Receipts from Other Sources Royalty Profit on Debt (Interest, Yield, etc) Ground Rent Rent from sub lease of Land or Building Rent from lease of Building with Plant and Machinery Bonus / Bonus Shares Loan, Advance, Deposit or Gift received in Cash Other Receipts Deductions from Other Sources Accounting Depreciation Other Deductions Foreign Income Share in untaxed Income from AOP Share in Taxed Income from AOP Total Income* Deductible Allowances [ ] Zakat u/s Workers Welfare Fund u/s 60A Charitable Donations u/c 61, Part I, 2nd Schedule Taxable Income [17-18]* Tax Chargeable Normal Income Tax Tax Reduction for Senior Taxpayer Tax Reduction for Disabled Taxpayer 9304 Total Inadmissible Admissible Computations Verification 40 Tax Credits Tax Credit for Deductable Allowance for Profit on Debt u/s 64A Tax Credit for Employment Generation by Manufacturers u/s 64B Difference of Minimum Tax Chargeable u/s 148(8) / 153(3)(b) Adjustment of Minimum Tax Paid u/s 113 in earlier Year(s) [<= ( )] Difference of Minimum Tax Chargeable on Electricity Bill u/s Difference of Minimum Tax Chargeable u/s Turnover / Tax Chargeable u/s Turnover / Tax Chargeable u/s Turnover / Tax Chargeable u/s Turnover / Tax Chargeable u/s Super Tax Tax Paid [Sr.38 Col. B+Sr.39 Col. B+Sr.46 Col. B+Sr.1 Col.B Annex-A] - 53 Advance Income Tax Admitted Income Tax Refundable Income Tax [23-37 if <0] Demanded Income Tax [23-37 if >0] Refund Adjustment of Other Year(s) against Demand of this Year [= 41] WWF Agriculture Income Agriculture Income Tax 9291 I,, CNIC No., in my capacity as Self / Representative (as defined in section 172 of the Income Tax Ordinance, 2001) of the Taxpayer named above, do solemnly declare that to the best of my knowledge & belief the information given in this Return / Statement u/s 115(4) are correct & complete in accordance with the provisions of the Income Tax Ordinance, 2001 & Income Tax Rules, Signature: Date:

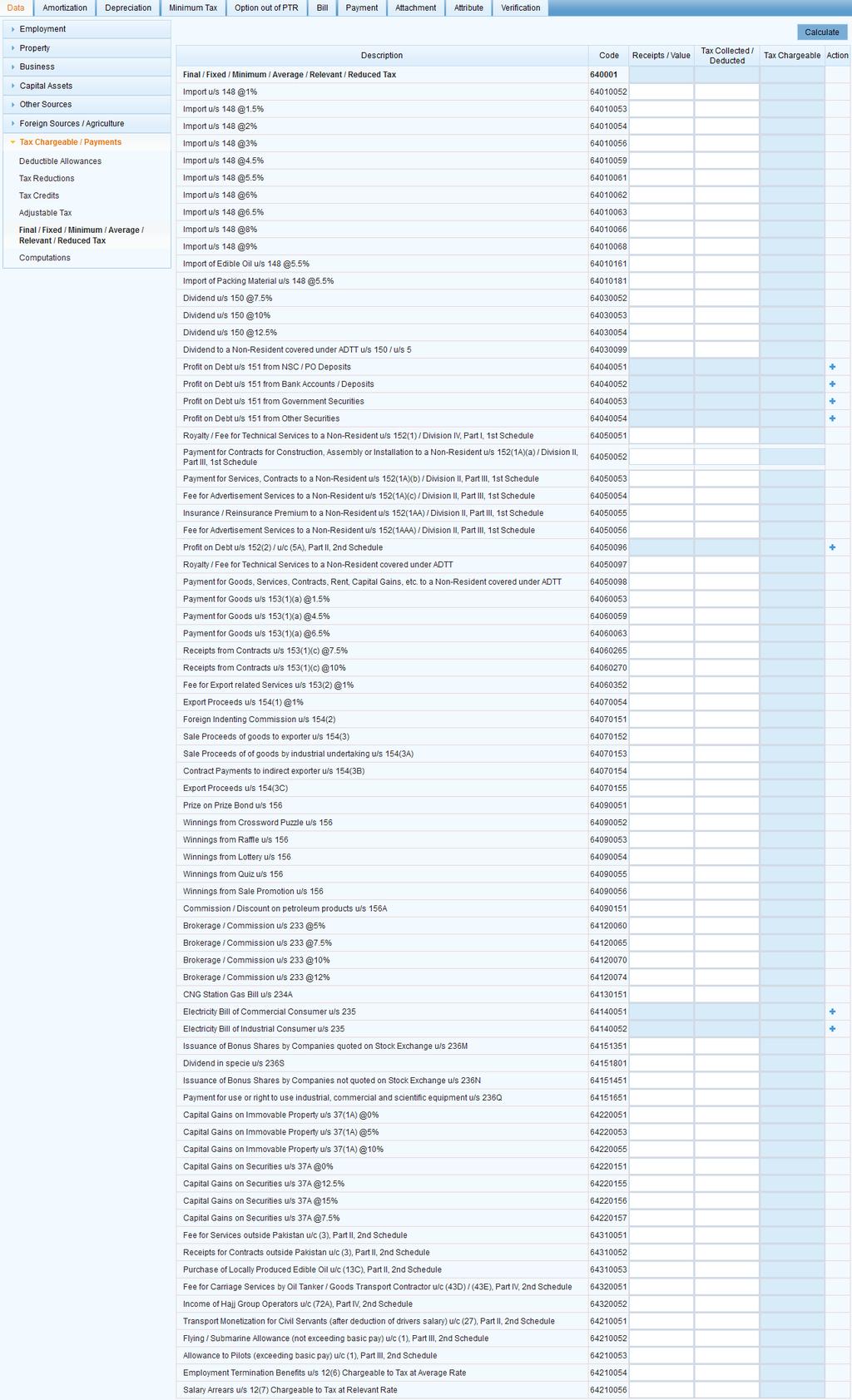

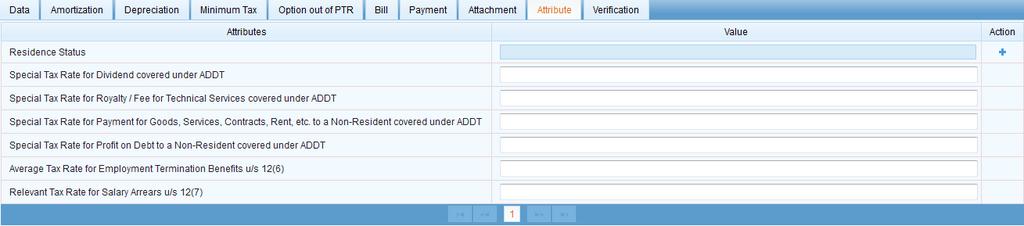

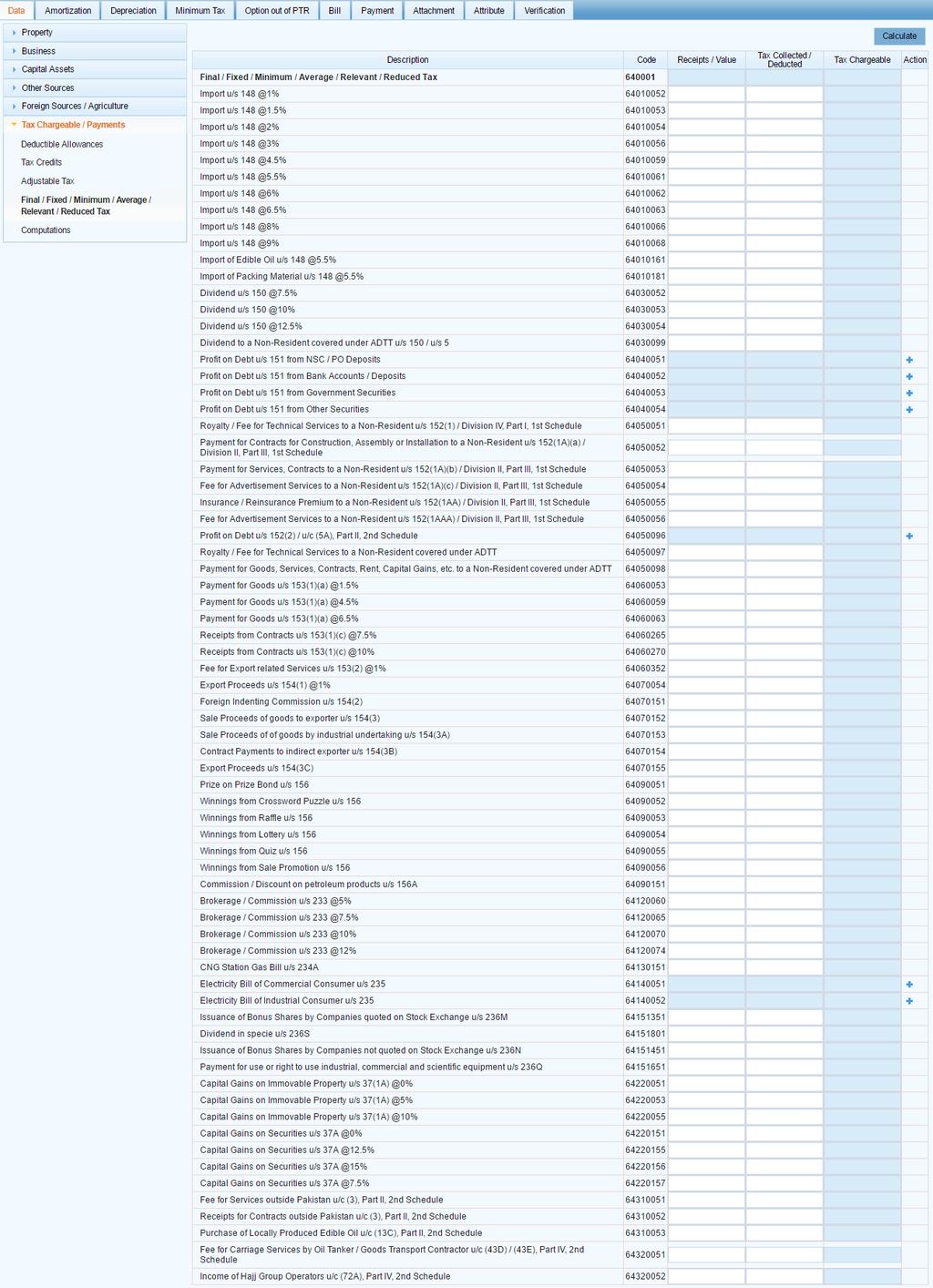

21 Name* CNIC* Final / Fixed / Average / Relevant / Reduced Rate Regime Sr. RETURN OF TOTAL INCOME / STATEMENT OF FINAL TAXATION UNDER THE INCOME TAX ORDINANCE, 2001 (IT-2) FOR INDIVIDUAL/AOP DERIVING INCOME UNDER THE HEAD BUSINESS & ANY OTHER HEAD Tax Year 2016 Description Code Final / Fixed / Minimum / Average / Relevant / Reduced Income Tax [Sum of to 107] Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import of Edible Oil u/s Import of Packing Material u/s Dividend u/s Dividend u/s Dividend u/s 12.50% Dividend to a Non-Resident covered under ADDT u/s 150 / u/s Profit on Debt u/s 151 from NSC / PO Deposits Profit on Debt u/s 151 from Bank Accounts / Deposits Profit on Debt u/s 151 from Government Securities Profit on Debt u/s 151 from Others Royalty / Fee for Technical Services to a Non-Resident u/s 152(1) / Division IV, 82 Part I, 1st Schedule Payment for Contracts for Construction, Assembly or Installation to a Non- 83 Resident u/s 152(1A)(a) / Division II, Part III, 1st Schedule Payment for Services, Contracts to a Non-Resident u/s 152(1A)(b) / Division II, 84 Part III, 1st Schedule Fee for Advertisement Services to a Non-Resident u/s 152(1A)(c) / Division II, Part 85 III, 1st Schedule Insurance / Reinsurance Premium to a Non-Resident u/s 152(1AA) / Division II, 86 Part III, 1st Schedule Fee for Advertisement Services to a Non-Resident u/s 152(1AAA) / Division II, 87 Part III, 1st Schedule Profit on Debt u/s 152(2) / u/c (5A), Part II, 2nd Schedule Royalty / Fee for Technical Services to a Non-Resident covered under ADDT Payment for Goods, Services, Contracts, Rent, etc. to a Non-Resident covered 90 under ADDT Payment for Goods u/s Payment for Goods u/s Payment for Goods u/s Receipts from Contracts u/s Receipts from Contracts u/s Fee for Export related Services u/s Export Proceeds u/s Foreign Indenting Commission u/s Prize on Prize Bond u/s Winnings from Crossword Puzzle u/s Winnings from Raffle u/s Winnings from Lottery u/s Winnings from Quiz u/s Winnings from Sale Promotion u/s Commission / Discount on petroleum products u/s 156A Brokerage / Commission u/s Brokerage / Commission u/s CNG Station Gas Bill u/s 234A Electricity Bill of Commercial Consumer u/s Electricity Bill of Industrial Consumer u/s Issuance of Bonus Shares by Companies quoted on Stock Exchange u/s 236M Dividend in specie u/s 236S Issuance of Bonus Shares by Companies not quoted on Stock Exchange u/s 236N Receipts / Value / Number NTN Tax Collected/ Deducted/Paid 2/2 Tax Chargeable A B C 114 Payment for use or right to use industrial, commercial and scientific equipment u/s 236Q Capital Gains on Immovable Property u/s Capital Gains on Immovable Property u/s Capital Gains on Immovable Property u/s Capital Gains on Securities u/s Capital Gains on Securities u/s Capital Gains on Securities u/s Capital Gains on Securities u/s Fee for Services outside Pakistan u/c (3), Part II, 2nd Receipts for Contracts outside Pakistan u/c (3), Part II, 2nd Purchase of Locally Produced Edible Oil u/c (13C), Part II, 2nd Fee for Carriage Services by Oil Tanker/Goods Transport Contractor u/c (43D) and 125 (43E), Part IV, 2nd Income of Hajj Group Operators u/c (72A), Part IV, 2nd Signature: Date:

22 Name* CNIC* Signature: Annex-A Adjustable Tax Collected / Deducted Sr. Description Code Receipts / Value 1 Adjustable Tax [Sum of 2 to 42] [Col.B Add to Col.B Sr.37 of Return] Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Import u/s Payment for Goods, Services, Contracts, Rent, etc. to a Non-Resident u/s 152(2) Profit on Debt to a Non-Resident u/s 152(2) Payment for Goods to a PE of a Non-Resident u/s 152(2A)(a) / Division II, Part III, 1st 14 Schedule Payment for Transport Services to a PE of a Non-Resident u/s 152(2A)(b) / Division II, 15 Part III, 1st Schedule Payment for Other Services to a PE of a Non-Resident u/s 152(2A)(b) / Division II, Part 16 III, 1st Schedule Payment for Contracts to a PE of a Non-Resident u/s 152(2A)(c) / Division II, Part III, 17 1st Schedule Payment for Goods u/s 153(1)(a) (ADJUSTABLE TAX ONLY) Rent of Property u/s Withdrawal from Pension Fund u/s 156B Cash Withdrawal from Bank u/s 231A Certain Banking Transactions u/s 231AA Motor Vehicle Registration Fee u/s 231B(1) Motor Vehicle Transfer Fee u/s 231B(2) Motor Vehicle Sale u/s 231B(3) Value of Shares traded through a member of a Stock exchange u/s 233A (1)(a) Value of Shares traded through a member of a Stock exchange u/s 233A (1)(b) Value of Shares traded by a member of a Stock exchange u/s 233A (1)(c) Margin Financing, Margin Trading or Securities Lending u/s 233AA Goods Transport Public Vehicle Tax u/s Passenger Transport Public Vehicle Tax u/s Private Vehicle Tax u/s Electricity Bill of Domestic Consumer u/s 235A Telephone Bill u/s 236(1)(a) Cellphone Bill u/s 236(1)(a) Prepaid Telephone Card u/s 236(1)(b) Phone Unit u/s 236(1)(c) Internet Bill u/s 236(1)(d) Prepaid Internet Card u/s 236(1)(e) Purchase by Auction u/s 236A Domestic Air Ticket Charges u/s 236B Sale / Transfer of Immovable Property u/s 236C Functions / Gatherings Charges u/s 236D Certification of Foreign-Produced TV Plays / Serials u/s 236E Issuance / Renewal of License to Cable Opeartors / Electronic Media u/s 236F Purchase of other commodities by Distributors / Dealers / Wholesalers u/s 236G Purchase of Fertilizer by Distributors / Dealers / Wholesalers u/s 236G Purchase by Retailers u/s 236H Educational Institution Fee u/s 236I Issuance / Renewal of License to Dealers / Commission Agents / Arhatis u/s 236J Purchase / Transfer of Immovable Property u/s 236K Purchase of International Air Ticket u/s 236L Banking transactions otherwise than through cash u/s 236P Education related expenses remitted abroad u/s 236R Purchase of future commodity contracts u/s 236T Date: Tax Year 2016 NTN Tax Collected / Deducted / Paid A B

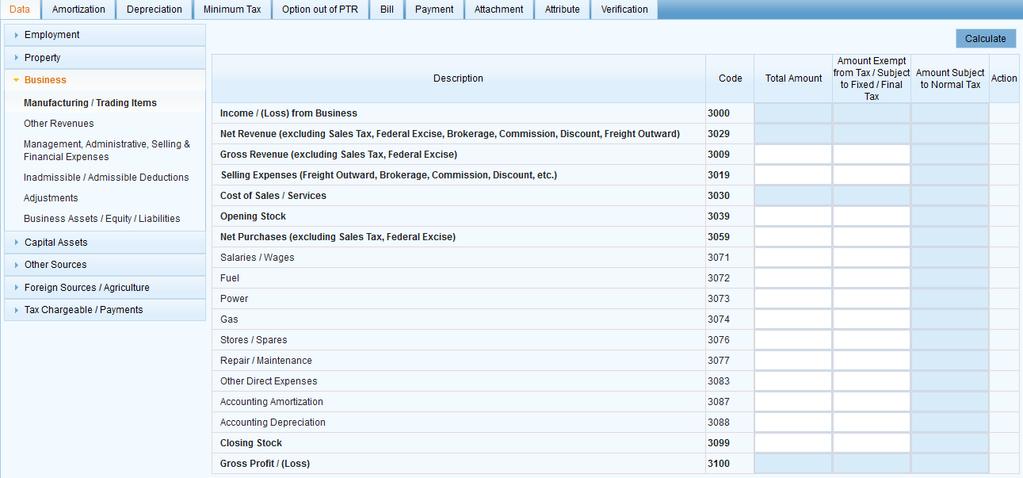

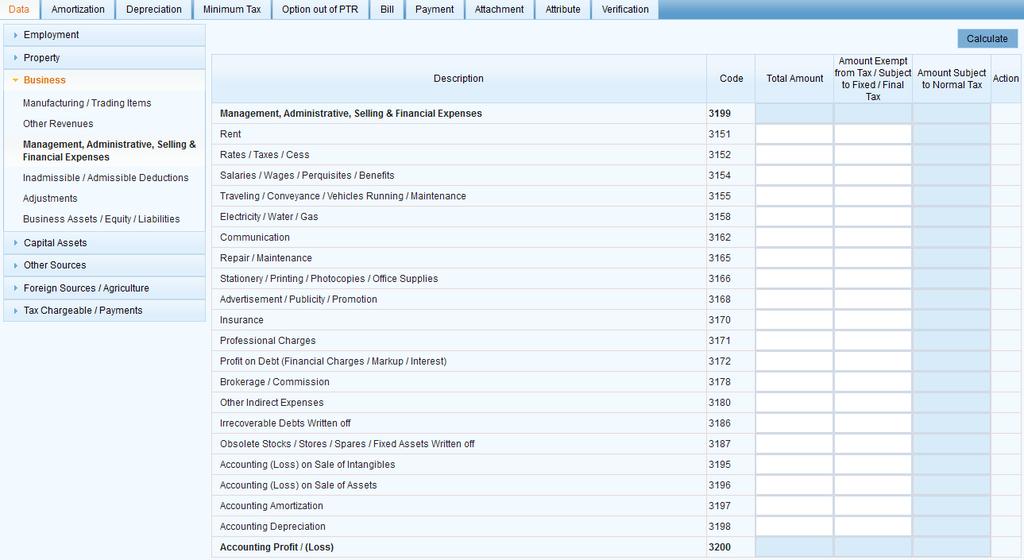

23 Name* Tax Year 2016 CNIC* Business Name* Revenue Cost of Sales / Services Indirect Expenses Sr. Description Code 1 Signature: Net Revenue (excluding Sales Tax, Federal Excise, Brokerage, Commission, Discount, Freight Outward) [2-3] Gross Revenue (excluding Sales Tax, Federal Excise) 3009 Selling Expenses (Freight Outward, Brokerage, Commission, Discount, 3 etc.) Cost of Sales / Services [(sum of 5 to 15)-16] Opening Stock Net Purchases (excluding Sales Tax, Federal Excise) Salaries / Wages Fuel Power Gas Stores / Spares Repair / Maintenance Annex-B Manufacturing / Trading / Profit & Loss Account ( including Revenues subject to Final / Fixed Tax) (Separate form should be filled for each business) 13 Other Direct Expenses Accounting Amortization Accounting Depreciation Closing Stock Gross Profit / (Loss) [1-4] Other Revenues [Sum of 19 to 21] Accounting Gain on Sale of Intangibles Accounting Gain on Sale of Assets Others 3128 Management, Administrative, Selling & Financial Expenses [Sum of to 42] Rent Rates / Taxes / Cess Salaries / Wages / Perquisites / Benefits Traveling / Conveyance / Vehicles Running / Maintenance Electricity / Water / Gas Communication Repair / Maintenance Stationery / Printing / Photocopies / Office Supplies Advertisement / Publicity / Promotion Insurance Professional Charges Profit on Debt (Financial Charges / Markup / Interest) Brokerage / Commission Irrecoverable Debts written off Obsolete Stocks / Stores / Spares / Fixed Assets written off Other Indirect Expenses Accounting (Loss) on Sale of Intangibles Accounting (Loss) on Sale of Assets Accounting Amortization Accounting Depreciation Accounting Profit / (Loss) [ ] 3200 Total Amount NTN Amount Subject to Final Tax 1/2 Amount Subject to Normal Tax A B C Date:

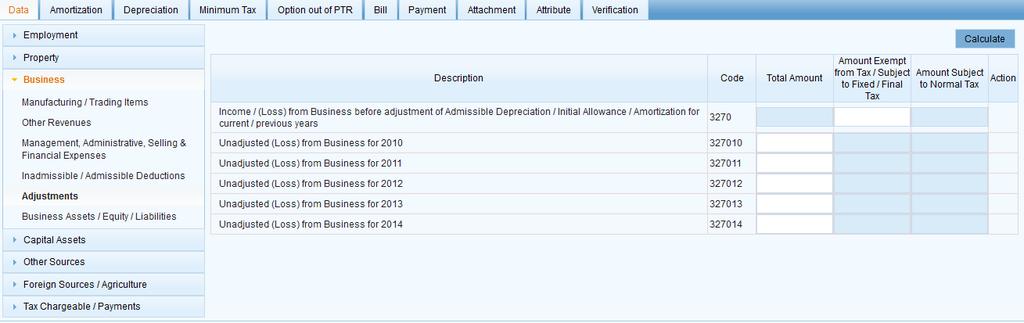

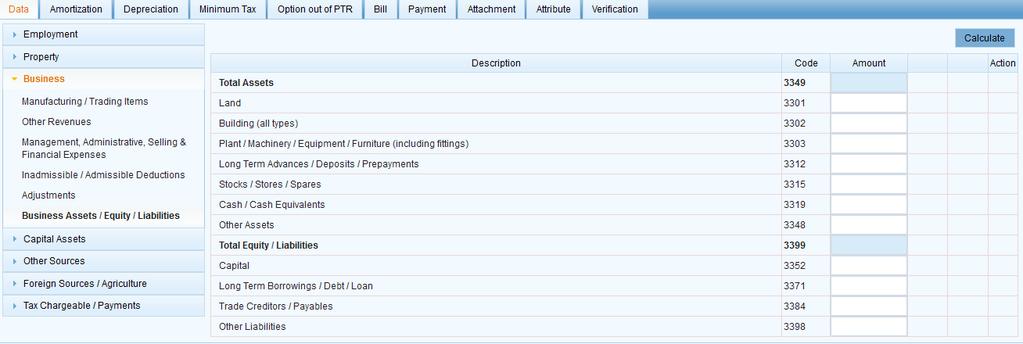

24 Name* Tax Year 2016 CNIC* Assets Liabilities Signature: Annex-B Manufacturing / Trading / Profit & Loss Account ( including Revenues subject to Final / Fixed Tax) (Separate form should be filled for each business) Sr. Description Code Total Amount NTN* Amount Subject to Final Taxation 2/2 Amount Subject to Normal Taxation A B C 44 Income / (Loss) from Business before adjustment of Admissible Depreciation / Initial Allowance / Amortization for current / previous years Unadjusted (Loss) from Business for Unadjusted (Loss) from Business for Unadjusted (Loss) from Business for Unadjusted (Loss) from Business for Unadjusted (Loss) from Business for Unadjusted (Loss) from Business for Unadjusted (Loss) from Business for Statement of Affairs / Balance Sheet 51 Total Assets [Sum of 52 to 57] Land Building (all types) Plant / Machinery / Equipment / Furniture (including fittings) Advances / Deposits / Prepayments/ Trade Debtors / Receivables Stocks / Stores / Spares Cash / Cash Equivalents Total Equity / Liabilities [Sum of 59 to 61] Capital Borrowings / Debt / Loan Advances / Deposits / Accrued Expenses/ Trade Creditors / Payables 3384 Date:

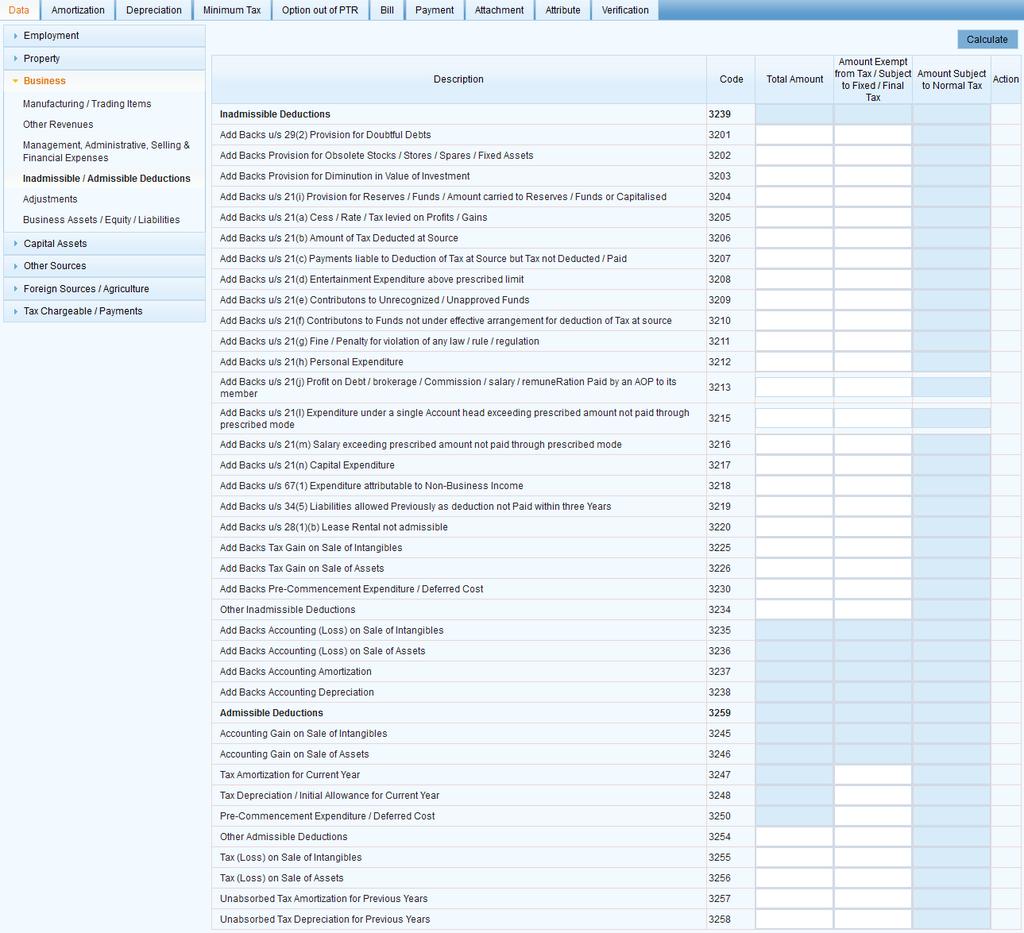

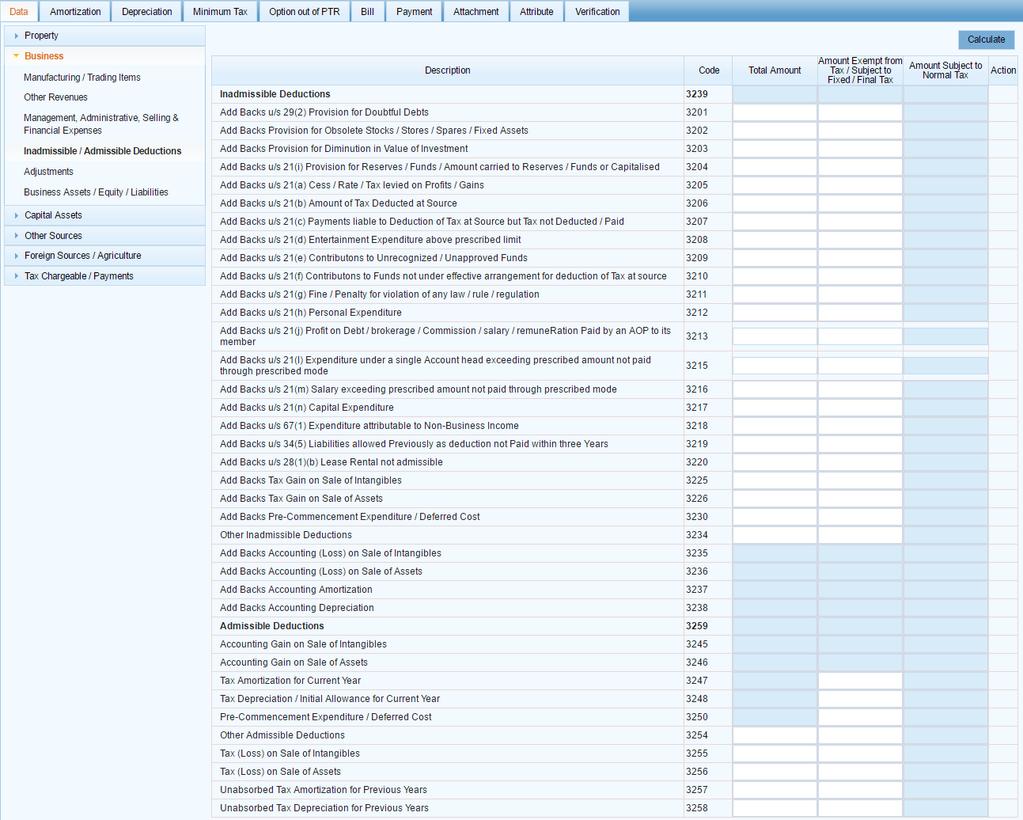

25 Name* CNIC* Admissible Deductions Inadmissible Deductions Signature: Annex-C Inadmissible / Admissible Deductions Tax Year 2016 Sr. Description Code Amount 1 Inadmissible Deductions [Sum of 2 to 28] Add Backs u/s 29(2) Provision for Doubtful Debts Add Backs Provision for Obsolete Stocks / Stores / Spares / Fixed Assets Add Backs Provision for Diminution in Value of Investment 3203 Add Backs u/s 21(i) Provision for Reserves / Funds / Amount carried to Reserves / Funds or 5 Capitalised Add Backs u/s 21(a) Cess / Rate / Tax levied on Profits / Gains Add Backs u/s 21(b) Amount of Tax Deducted at Source Add Backs u/s 21(c) Payments liable to deduction of tax at source but tax not deducted / paid Add Backs u/s 21(d) Entertainment Expenditure above prescribed limit Add Backs u/s 21(e) Contributons to Unrecognized / Unapproved Funds Add Backs u/s 21(f) Contributons to Funds not under effective arrangement for deduction of tax at source Add Backs u/s 21(g) Fine / penalty for violation of any law / rule / regulation Add Backs u/s 21(h) Personal Expenditure Add Backs u/s 21(j) Profit on Debt / Brokerage / Commission / Salary / Remuneration paid by an AOP to its Member Add Backs u/s 21(l) Expenditure under a single account head exceeding prescribed amount not paid through prescribed mode Add Backs u/s 21(m) Salary exceeding prescribed amount not paid through prescribed mode Add Backs u/s 21(n) Capital Expenditure Add Backs u/s 67(1) Expenditure attributable to Non-Business Income Add Backs u/s 34(5) Liabilities allowed Previously as deduction not Paid within three Years Add Backs u/s 28(1)(b) Lease Rental not admissible Add Backs Tax Gain on Sale of Intangibles Add Backs Tax Gain on Sale of Assets Add Backs Pre-Commencement Expenditure / Deferred Cost Add Backs Accounting (Loss) on Sale of Intangibles Add Backs Accounting (Loss) on Sale of Assets Add Backs Accounting Amortization Add Backs Accounting Depreciation Other Inadmissible Deductions Admissible Deductions [Sum of 30 to 39] Accounting Gain on Sale of Intangibles Accounting Gain on Sale of Assets Tax Amortization for Current Year Tax Depreciation / Initial Allowance for Current Year Pre-Commencement Expenditure / Deferred Cost Other Admissible Deductions Tax (Loss) on Sale of Intangibles Tax (Loss) on Sale of Assets Unabsorbed Tax Amortization for Previous Years Unabsorbed Tax Depreciation for Previous Years 3258 NTN Date:

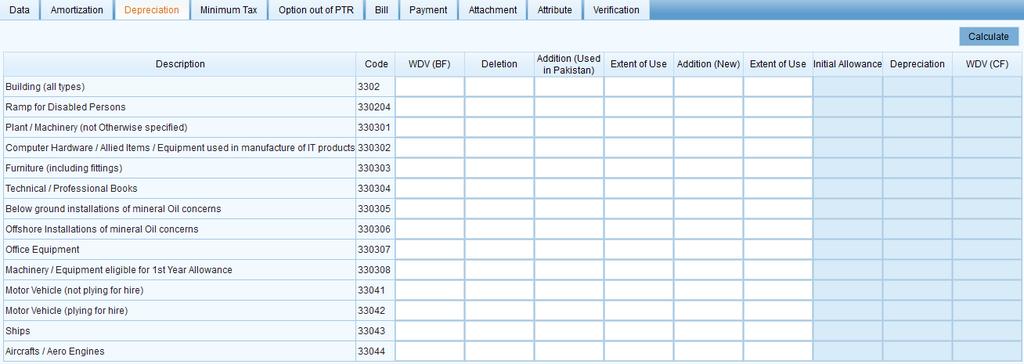

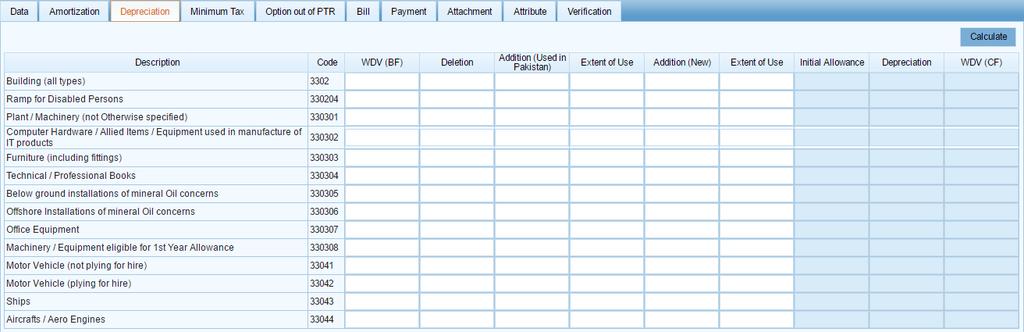

26 Name* CNIC* Sr. Description Code WDV (BF) Deletion Addition (Used Previously in Pakistan) Extent of Use Addition (New) Extent of Use Rate Tax Year 2016 NTN Initial Allowance Rate Depreciation WDV (CF) A B C D E F G H I 1 Building (all types) % 100% 15% 10% 2 Ramp for Disabled Persons % 100% 100% 100% Annex-D Depreciation, Initial Allowance, Amortization Depreciation 3 Plant / Machinery (not otherwise specified) % 100% 25% 15% Computer Hardware / Allied Items / Equipment 4 used in manufacture of IT products % 100% 25% 30% 5 Furniture (including fittings) % 100% 0% 15% 6 Technical / Professional Books % 100% 25% 15% 7 Below ground installations of mineral oil concerns % 100% 25% 100% 8 Offshore Installations of mineral oil concerns % 100% 25% 20% 9 Office Equipment % 100% 25% 15% Machinery / Equipment eligible for 1st year 10 Allowance % 100% 90% 15% 11 Motor Vehicle (not plying for hire) % 100% 0% 15% 12 Motor Vehicle (plying for hire) % 100% 25% 15% 13 Ships % 100% 25% 15% 14 Aircrafts / Aero Engines % 100% 25% 30% Tax Depreciation / Initial Allowance for Current 15 Year % 100% Amortization Signature: Description Code WDV (BF) 16 Intangible Intangible Intangible Expenditure providing Long Term Advantage / Benefit Tax Amortization for Current Year Pre-Commencement Expenditure 3306 Remaining Useful Life Extent of Use Amortizati on A B C D Date:

27 Name* CNIC* Minimum Tax Chargeable Sr. Description Code Receipts / Value 1 Minimum Tax Chargeable [Col.E Sum of 2 to 6 Transfer to Sr.28 of Return] 2 Import of Edible Oil u/s Import of Packing Material u/s Payment for Services u/s Payment for Services u/s Payment for Services u/s Payment for Services u/s Sr. Description Code Receipts / Value 7 Import u/s Import u/s Import u/s Import u/s Import u/s Annex-E Tax Collectible / Deductible Attributable Taxable Income Tax Year 2016 NTN Tax on Attributable Taxable Income Minimum Tax Chargeable A B C D E Final Tax Chargeable Attributable Taxable Income Tax on Attributable Taxable Income Difference (Option Valid if <=0) A B C D E Option out of PTR 12 Payment for Goods u/s Payment for Goods u/s Receipts from Contracts u/s Receipts from Contracts u/s Fee for Export related Services u/s Export Proceeds u/s Foreign Indenting Commission u/s Commission / Discount on petroleum products u/s 156A Brokerage / Commission u/s Brokerage / Commission u/s Signature: Date:

28 Annex-F Personal Expenses Name* CNIC* Tax Year 2016 NTN Sr. Description Code Amount 1 Personal Expenses [Sum of 2 to 16 minus 17] Rent Rates / Taxes / Charge / Cess Vehicle Running / Maintenence Travelling Electricity Water Gas 7060 Personal Expenses 9 Telephone Asset Insurance / Security Medical Educational Club Functions / Gatherings Donation, Zakat, Annuity, Profit on Debt, Life Insurance Premium, etc Other Personal / Household Expenses Contribution in Expenses by Family Members [Sum of 18 to 21] 7088 CNIC No. Name* Signature: Date:

29 WEALTH STATEMENT UNDER SECTION 116 OF THE INCOME TAX ORDINANCE, /4 Name* CNIC* Residence Address* Business Address* Tax Year 2016 NTN 1 Agricultural Property [Sum of 1 i to 1 x] Form (Irrigated / Unirrigated / Uncultivable) Mauza / Village / Chak No. Tehsil District Area (Acre) Share % Code Value at Cost Agricultural Property i 7001 ii 7001 iii 7001 iv 7001 v 7001 vi 7001 vii 7001 viii 7001 ix 7001 x 7001 Residential, Commercial, Industrial Property 2 Commercial, Industrial, Residential Property (Non-Business) [Sum of 2 i to 2 x] Form (House, Flat, Shop, Plaza, Factory, Workshop, etc.) Unit No. / Complex / Street / Block / Sector Area / Locality / Road City Area (Marla / sq. yd.) Share % Code Value at Cost i 7002 ii 7002 iii 7002 iv 7002 v 7002 vi 7002 vii 7002 viii 7002 ix 7002 x 7002 Business Capital 3 Business Capital Enter name, share percentage & capital amount in each AOP Share % Code Value at Cost i 7003 ii 7003 iii 7003 i Enter consolidated capital amount of all Sole Proprietorships 100% Equipment, etc. (Non-Business) [Sum of 4 i to 4 iv] Equipment Description Code i 7004 ii 7004 iii 7004 iv 7004 Value at Cost Signatures: Date:

30 WEALTH STATEMENT UNDER SECTION 116 OF THE INCOME TAX ORDINANCE, /4 Name* CNIC* Tax Year 2016 NTN 5 Animal (Non-Business) [Sum of 5 i to 5 iv] Description Code Value at Cost Animal i Livestock 7005 ii Pet 7005 iii Unspecified 7005 iv Unspecified Investment (Non-Business) [Sum of 6 i to 6 xiii] Account / Form Instrument No. Institution Name / Individual CNIC Share % Code Value at Cost i Account 7006 Current 7006 Current 7006 Fixed Deposit 7006 Fixed Deposit 7006 Profit / Loss Sharing 7006 Profit / Loss Sharing 7006 Saving 7006 Saving 7006 ii Annuity 7006 iii Bond 7006 iv Certificate 7006 v Debenture 7006 Investment vi Deposit 7006 Term Deposit 7006 Term Deposit 7006 vii Fund 7006 viii Instrument 7006 ix Insurance Policy 7006 x Security 7006 xi Stock / Share 7006 xii Unit 7006 xiii Others Debt (Non-Business) [Sum of 7 i to 7 vii] Form No. Institution Name / Individual CNIC Share % Code Value at Cost i Advance 7007 ii Debt 7007 iii Deposit 7007 iv Prepayment 7007 v Receivable 7007 vi Security 7007 vii Others Motor Vehicle (Non-Business) [Sum of 8 i to 8 viii] Form (Car,Jeep,Motor Cycle,Scooter,Van) E&TD Registration No. Maker Capacity Code Value at Cost Motor Vehicle i 7008 ii 7008 iii 7008 iv 7008 v 7008 vi 7008 vii 7008 viii 7008 Signatures: Date:

31 WEALTH STATEMENT UNDER SECTION 116 OF THE INCOME TAX ORDINANCE, /4 Name* CNIC* Tax Year 2016 NTN Precious Posession Household Effect 9 Precious Possession [Sum of 9 i to 9 iii] Description Code Value at Cost i Antique / Artifact 7009 ii Jewelry / Ornament / Metal / Stone 7009 iii Others (Specify) Household Effect [Sum of 10 i to 10 iv] Description Code Value at Cost i Unspecified 7010 ii Unspecified 7010 iii Unspecified 7010 iv Unspecified Personal Item [Sum of 11 i to 11 iv] * Personal Item Description Code i Unspecified 7011 ii Unspecified 7011 iii Unspecified 7011 iv Unspecified 7011 Value at Cost Cash Any Other Asset 12 Cash (Non-business) [Sum of 12 i to 12 x] Notes & Coins Any Other Asset [Sum of 13 i to 13 iv] Description Code Value at Cost i 7013 ii 7013 iii 7013 iv 7013 Assets in Others' Name Assets outside Pakistan 14 Assets in Others' Name [Sum of 14 i to 14 iv] Description Code Value at Cost i 7014 ii 7014 iii 7014 iv Assets outside Pakistan [Sum of 15 i to 15 iv] Description Code Value at Cost i 7015 ii 7015 iii 7015 iv Total Assets [Sum of 1 to 15] Signatures: Date:

32 Verification Disposed Asse Reconciliation of Net Assets Loan Name* CNIC* WEALTH STATEMENT UNDER SECTION 116 OF THE INCOME TAX ORDINANCE, 2001 Tax Year Credit (Non-Business) [Sum of 16 i to 16 viii] Form Creditor's NTN / CNIC Creditor's Name Code Value at Cost i Advance 7021 ii Borrowing 7021 iii Credit 7021 iv Loan 7021 v Mortgage 7021 vi Overdraft 7021 vii Payable 7021 viii Others Total Liabilities [=16] Net Assets Current Year [15-17] Net Assets Previous Year Increase / Decrease in Assets [18-19] Inflows [Sum of 21 i to 21 x] i Income declared as per Return for the year subject to normal tax 7031 ii Income declared as per Return for the year exempt from tax 7032 iii Income Attributable to Receipts, etc. Declared as per Return for the year subject to Final / Fixed Tax 7033 iv Adjustments in Income Declared as per Return for the year 7034 vi Foreign Remittance 7035 vii Inheritance 7036 viii Gift 7037 ix Gain on Disposal of Assets, excluding Capital Gain on Immovable Property 7038 x Others Personal Expenses [Transfer from Sr.1 Annex-F] Outflows [Sum of 23 i to 23 iii] i Gift 7091 ii Loss on Disposal of Assets 7092 iii Others Unreconciled Amount [ ] Assets Transferred / Sold / Gifted / Donated during the year [Sum of 25 i to 25 ii] Description i ii NTN Code 4/4 Value at Cost I,, CNIC No., in my capacity as Self / Representative (as defined in section 172 of the Income Tax Ordinance, 2001) of Taxpayer named above, do hereby solemnly declare that to the best of my knowledge & belief the information given in this statement of the assets & liabilities of myself, my spouse(s), minor children & other dependents as on & of my personal expenditure for the year ended are correct & complete in accordance with the provisions of the Income Tax Ordinance, 2001, Income Tax Rules, 2002.

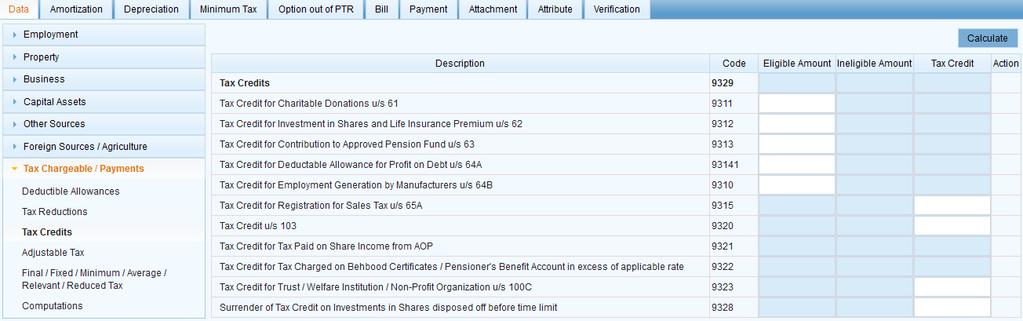

33 Form General Sr. IT-1B 13 IT-2 14 IT-1B 48 IT-2 45 IT-1B 26 IT-2 28 Annex-E Annex-F Annex-F 18 Statement Statement Wealth Statement Statement Wealth Statement 4 Wealth Statement 14 Wealth 21 Statement iv INSTRUCTIONS Instructions for Filling in Return Form & Wealth Statement The following persons are required to furnish a return of income for a tax year: (a) Every company; (b) Every person (other than a company) whose taxable income for the year exceeds PKR 400,000; (c) Every non-profit organization as defined in clause (36) of section 2; (d) Every welfare institution approved under clause (58) of Part I of the Second Schedule; (e) Every person who has been charged to tax in respect of any of the two preceding tax years; (f) Every person who claims a loss carried forward under this Ordinance for a tax year; (g) Every person who owns immovable property with a land area of two hundred and fifty square yards or more or owns any flat located in areas falling within the municipal limits existing immediately before the commencement of Local Government laws in the provinces; or areas in a Cantonment; or the Islamabad Capital Territory; (h) Every person who owns immoveable property with a land area of five hundred square yards or more located in a rating area; (i) Every person who owns a flat having covered area of two thousand square feet or more located in a rating area; (j) Every person who owns a motor vehicle having engine capacity above 1000 CC; (k) Every person who has obtained National Tax Number; (l) Every person who is the holder of commercial or industrial connection of electricity where the amount of annual bill exceeds rupees five hundred thousand; (m) Every person who is registered with any chamber of commerce and industry or any trade or business association or any market committee or any professional body including Pakistan Engineering Council, Pakistan Medical and Dental Council, Pakistan Bar Council or any Provincial Bar Council, Institute of Chartered Accountants of Pakistan or Institute of Cost and Management Accountants of Pakistan; (n) Every individual whose income under the head Business exceeds PKR 300,000 but does not exceed PKR 400,000 in a tax year. The following errors / omissions shall render a Return invalid & make the taxpayer a non-filer & liable to penalty under section 182(1): (a) Return on which CNIC is missing or incorrect or invalid; (b) Return on which mandatory fields marked by * are empty; (c) Return which is not signed by the Taxpayer or his Representative (as defined in section 172 of the Income Tax Ordinance, 2001); (d) Return which is not filed in the prescribed Form; (e) Return which is not filed in the prescribed mode. Individuals deriving income under the head Property, Capital Gains & Other Sources (excluding Salary / Business) & Income subject to fixed / final tax have to file one page Return in IT-1B Form with Annex-A, Annex-F & Wealth Statement if required to be filed. Individuals deriving income under the head business or falling under Final Tax Regime (FTR) such as Commercial Importers, Exporters, Contractors, etc. have to file two page Return in IT-2 Form with Annex-A, Annex-B, Annex-F & Wealth Statement if required to be filed. Annex- C, Annex-D & Annex-E are required only where Depreciation / Amortization, Admissible / Inadmissible Deductions & Minimum Tax Chargeable / Option out of Presumptive Tax Regime are involved. Individuals, including members of AOPs or directors of Companies must file Wealth Statement. Taxpayers may file Return of Total Income / Statement of Final Taxation & Wealth Statement through the following modes: Electronically at FBR Portal ( which is mandatory for all Companies, AOPs, Sales Tax Registered Persons, Refund Claimants & Individuals having income under the head Salary. However, all others are also encouraged to electronically file Return; Manually on paper at Taxpayer Facilitation Counter of the respective Regional Tax Office. Paper Return Form can be downloaded from FBR Website Taxpayers may seek guidance through the following modes: By calling Helpline , By visiting the nearest Taxpayer Facilitation Centre (TFC), list of which can be downloaded from FBR website at Tax can be paid in any authorized branch of NBP & SBP at any time before filing of return. List of authorized braches of NBP & SBP can be downloaded from Only Foreign Income (Not Loss) should be declared. Only Agriculture Income (Not Loss) should be declared. Tax Credits include Tax Credits for the following: Share in Taxed Income from AOP; Charitable Donations u/s 61; Investment in Shares of Public Companies listed on a Stock Exchange in Pakistan (only for Original Allottee other than a Company) u/s 62; Life Insurance Premim (only for Resident Individual deriving income from Salary / Business) u/s 62; 63; Profit or Share in Rent or Share in Appreciation of Value of Property paid on loan invested in property u/s 64. Taxpayers wanting to opt out of Presumptive Tax Regime (PTR) u/c (56B), (56C), (56D), (56E), (56F), (56G), Part IV, Second Schedule, must file Annex-E. Only Personal / Household (Non-Business) expenses should be declared. Expenses borne by more than one person must be declared in total by each person. For example, if in one family more than one member is contibuting to expenses or if more than one family is living jointly & within each family more than one member is contributing to expenses, total expenses under each head must be declared by each member of each family filing his wealth statement & then contribution by other family members be deducted to arrive at own contribution. If rows provided in any segment are inadequate, additional rows may be inserted. All assets must be delared at cost, including ancillary expenses. If an asset is acquired under a Hire Purchase Agreement, total price should be declared as asset under the appropriate head & balance payable amount should be declared as liability. If Wealth Statement is filed for the first time, separate Reconciliation Statement must be filed for each previous year. Equipment, Plant, Machinery (Non-Business) must be declared with description, for example, Generator, Tubewell, Harvestor, Tractor, Trolley, etc. Assets created in the name of spouse(s), children & other dependents should be declared only if acquired by them with funds provided by you (Benami Assets). value of perquisites, 1/10 of goodwill from tenant, 1/10 of goodwill on vacating possession of property, repairs allowance, admissible / inadmissible deductions, brought forward losses, unabsorbed depreciation / amortization

34

Instructions for Filling in Return Form & Wealth Statement Form General Sr. Instruction The following persons are required to furnish a return of income for a tax year: (a) Every company; (b) Every person

Instructions for Filling in Return Form & Wealth Statement Form General Sr. Instruction The following persons are required to furnish a return of income for a tax year: (a) Every company; (b) Every person

GOVERNMENT OF PAKISTAN REVENUE DIVISION FEDERAL BOARD OF REVENUE **** NOTIFICATION (Income Tax)

") GOVERNMENT OF PAKISTAN REVENUE DIVISION FEDERAL BOARD OF REVENUE **** Islamabad, the 17 th August, 2018. NOTIFICATION (Income Tax) S.R.O. 1012 (I)/2018.- In exercise of the powers conferred by sub-section

GOVERNMENT OF PAKISTAN REVENUE DIVISION FEDERAL BOARD OF REVENUE **** Islamabad, the 17 th August, 2018. NOTIFICATION (Income Tax) S.R.O. 1012 (I)/2018.- In exercise of the powers conferred by sub-section

Basic Concepts of Tax on Income

Basic Concepts of Tax on Income (Taxpayer s Facilitation Guide) September 2011 Revenue Division Federal Board of Revenue Government of Pakistan helpline@fbr.gov.pk 0800-00-227, 051-111-227-227 www.fbr.gov.pk

Basic Concepts of Tax on Income (Taxpayer s Facilitation Guide) September 2011 Revenue Division Federal Board of Revenue Government of Pakistan helpline@fbr.gov.pk 0800-00-227, 051-111-227-227 www.fbr.gov.pk

CHART OF WITHHOLDING TAX UNDER THE INCOME TAX ORDINANCE, 2001

148 Part II Imports Collector of Customs 5% of the value of goods Rate reduced of 1% for 149 Division I of Part I 150 Division III items mentioned in clause (9), 13(E), (13G), (23), 3% for items mentioned

148 Part II Imports Collector of Customs 5% of the value of goods Rate reduced of 1% for 149 Division I of Part I 150 Division III items mentioned in clause (9), 13(E), (13G), (23), 3% for items mentioned

Final Discharge of Tax Liability

Final Discharge of Tax Liability Index 1. Section 8. General provisions relating to taxes imposed under sections 5, 6 and 7...424 2. Section 169. Tax collected or deducted as a final tax...426 3. Commercial

Final Discharge of Tax Liability Index 1. Section 8. General provisions relating to taxes imposed under sections 5, 6 and 7...424 2. Section 169. Tax collected or deducted as a final tax...426 3. Commercial

FINAL TAX REGIME & MINIMUM TAX

Chapter 22 FINAL TAX REGIME & MINIMUM TAX Section Topic covered For CA Mod F & ICMAP students Section Rule 169 General provisions regarding income under final tax regime 153 Minimum tax on services & goods

Chapter 22 FINAL TAX REGIME & MINIMUM TAX Section Topic covered For CA Mod F & ICMAP students Section Rule 169 General provisions regarding income under final tax regime 153 Minimum tax on services & goods

Finance Act, 2014 Explanation regarding Important amendments made in the Income Tax Ordinance, Amendments in Mutual Funds Taxation Regime.

INCOME TAX Finance Act, 2014 Explanation regarding Important amendments made in the Income Tax Ordinance, 2001. Clause (61A) of sec 2, clause (99) of Part I of2nd Schedule, DIV I of Part III of first Schedule.

INCOME TAX Finance Act, 2014 Explanation regarding Important amendments made in the Income Tax Ordinance, 2001. Clause (61A) of sec 2, clause (99) of Part I of2nd Schedule, DIV I of Part III of first Schedule.

Income from Other Sources

Income from Other Sources Index 1. Section 11. Heads of income...262 2. Section.101. Geographical source of income...262 3. Section 15. Income from property...262 4. Section 112. Liability in respect of

Income from Other Sources Index 1. Section 11. Heads of income...262 2. Section.101. Geographical source of income...262 3. Section 15. Income from property...262 4. Section 112. Liability in respect of

Filing of Income Tax Return and Wealth Statement for salaried individual

Filing of Income Tax Return and Wealth Statement for salaried individual MR. SHARIF UDDIN KHILJI, FCA Tax Year 2018 AUGUST 30, 2018 6:00 PM TO 9:00 PM ICAP, AUDITORIUM, G-10/4 ISLAMABAD Persons liable

Filing of Income Tax Return and Wealth Statement for salaried individual MR. SHARIF UDDIN KHILJI, FCA Tax Year 2018 AUGUST 30, 2018 6:00 PM TO 9:00 PM ICAP, AUDITORIUM, G-10/4 ISLAMABAD Persons liable

TAXATION OF INCOME FROM SALARY TAX YEAR 2018 (JULY 01, 2017 TO JUNE 30, 2018)

") CIRCULAR NO. 9 OF (INCOME TAX) TAXATION OF INCOME FROM SALARY TAX YEAR 2018 (JULY 01, 2017 TO JUNE 30, 2018) The Circular on taxation of Income Salary is being updated as under:- The Computation of Tax

CIRCULAR NO. 9 OF (INCOME TAX) TAXATION OF INCOME FROM SALARY TAX YEAR 2018 (JULY 01, 2017 TO JUNE 30, 2018) The Circular on taxation of Income Salary is being updated as under:- The Computation of Tax

This guideline has been prepared in the light of;

With compliments from: Key Solutions, Chief Executive, Afzaal Ansari Tax, Software and Website Consultants Cell: 0333-4211086, Website: www.key-sol.com, Email: afzaal68@gmail.com Bsc, CA(Int) Life Member,

With compliments from: Key Solutions, Chief Executive, Afzaal Ansari Tax, Software and Website Consultants Cell: 0333-4211086, Website: www.key-sol.com, Email: afzaal68@gmail.com Bsc, CA(Int) Life Member,

Business Income and. related concepts. Karachi Tax Bar Association Professional Development Program November 2017

KPMG Taseer Hadi & Co. Chartered Accountants Business Income and related concepts 09 November 2017 Presenter: Zeeshan Zafar Khan Director KPMG Karachi Tax Bar Association Professional Development Program-2017

KPMG Taseer Hadi & Co. Chartered Accountants Business Income and related concepts 09 November 2017 Presenter: Zeeshan Zafar Khan Director KPMG Karachi Tax Bar Association Professional Development Program-2017

INCOME TAX WITHHOLDING CHART (Income Tax Ordinance, 2001)

") INCOME TAX WITHHOLDING CHART (Income Tax Ordinance, 2001) IMPORTS SALARY TAX YEAR 2019 w.e.f. July 01, 2018 WITHDRAWALS FROM BANK PURCHASE OF MOTOR VEHICLES DIVIDEND INTEREST 236 233 BROKERAGE AND COMMISSION

INCOME TAX WITHHOLDING CHART (Income Tax Ordinance, 2001) IMPORTS SALARY TAX YEAR 2019 w.e.f. July 01, 2018 WITHDRAWALS FROM BANK PURCHASE OF MOTOR VEHICLES DIVIDEND INTEREST 236 233 BROKERAGE AND COMMISSION

Pre-Budget Seminar

CHARTERED ACCOUNTANTS Institute of Cost & Management Accountants of Pakistan Pre-Budget Seminar 2013-14 Contact Address: 4 th Floor, Central Hotel Building Civil Lines, Mereweather Road Karachi - Pakistan

CHARTERED ACCOUNTANTS Institute of Cost & Management Accountants of Pakistan Pre-Budget Seminar 2013-14 Contact Address: 4 th Floor, Central Hotel Building Civil Lines, Mereweather Road Karachi - Pakistan

TAX DIGEST J.A.S.B. & Associates PREAMBLE. Chartered Accountants

PREAMBLE The purpose of this digest is to facilitate the readers about changes made by the Finance Act 2012 including rectification/additions in changes proposed in Finance Bill 2012. This document also

PREAMBLE The purpose of this digest is to facilitate the readers about changes made by the Finance Act 2012 including rectification/additions in changes proposed in Finance Bill 2012. This document also

INCOME TAX RULES, 2002

GOVERNMENT OF PAKISTAN CENTRAL BOARD OF REVENUE (REVENUE DIVISION) INCOME TAX MANUAL PART II INCOME TAX RULES, 2002 AMENDED UPTO NOVEMBER, 2004 Rules Income Tax Rules, 2002 Arrangement of Rules Page CHAPTER

GOVERNMENT OF PAKISTAN CENTRAL BOARD OF REVENUE (REVENUE DIVISION) INCOME TAX MANUAL PART II INCOME TAX RULES, 2002 AMENDED UPTO NOVEMBER, 2004 Rules Income Tax Rules, 2002 Arrangement of Rules Page CHAPTER

Income From Business. Index

Income From Business Index 1. Section 2. Definitions...128 2. Section 6. Tax on certain payments to non-residents...129 3. Section 101. Geographical source of income...129 4. Section 105. Taxation of a

Income From Business Index 1. Section 2. Definitions...128 2. Section 6. Tax on certain payments to non-residents...129 3. Section 101. Geographical source of income...129 4. Section 105. Taxation of a

INCOME TAX ORDINANCE, 2001

S.No INCOME TAX ORDINANCE, 2001 Important points Finance Act 2017-18 update 1 2 3 3a 4 5 6 Definition Clause 22A fast moving consumer goods Excluding durable goods Clause 30C Liaison office means a place

S.No INCOME TAX ORDINANCE, 2001 Important points Finance Act 2017-18 update 1 2 3 3a 4 5 6 Definition Clause 22A fast moving consumer goods Excluding durable goods Clause 30C Liaison office means a place

INDIAN INCOME TAX RETURN. Assessment Year FORM

INDIAN INCOME TAX RETURN Assessment Year FORM ITR-7 For persons including companies required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) (Please see

INDIAN INCOME TAX RETURN Assessment Year FORM ITR-7 For persons including companies required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) (Please see

Nadeem Butt (FCA) Chartered Accountant

Chartered Accountant") Prepared By Nadeem Butt (FCA) Principal Taj Arcade, 3 rd Floor, Office # 06, Opposite Services Hospital, 73-Main Jail Road, Lahore Pakistan Nadeem & Co. s AMENDMENTS THROUGH FINANCE ACT, AND AFTER THAT

Prepared By Nadeem Butt (FCA) Principal Taj Arcade, 3 rd Floor, Office # 06, Opposite Services Hospital, 73-Main Jail Road, Lahore Pakistan Nadeem & Co. s AMENDMENTS THROUGH FINANCE ACT, AND AFTER THAT

Circular No. 1 of 2007 (Income Tax)

") GOVERNMENT OF PAKISTAN REVENUE DIVISION CENTRAL BOARD OF REVENUE ****** No.F.4(1)ITP/2007-EC Islamabad, July 2, 2007 Circular No. 1 of 2007 (Income Tax) Subject: FINANCE ACT, 2007 EXPLANATION OF IMPORTANT

GOVERNMENT OF PAKISTAN REVENUE DIVISION CENTRAL BOARD OF REVENUE ****** No.F.4(1)ITP/2007-EC Islamabad, July 2, 2007 Circular No. 1 of 2007 (Income Tax) Subject: FINANCE ACT, 2007 EXPLANATION OF IMPORTANT

Withholding Tax Regime(Rates Card) Guidelines for the Taxpayers, Tax Collectors & Withholding Agents (Updated Up to 1 st July, 2014)

Guidelines for the Taxpayers, Tax Collectors & Withholding Agents (Updated Up to 1 st July, 2014)") Withholding Tax Regime(Rates Card) Guidelines for the Taxpayers, Tax Collectors & Withholding Agents (Updated Up to 1 st July, 2014) Section Provision of the Section Tax Rate deduct / collect / agent 148

Withholding Tax Regime(Rates Card) Guidelines for the Taxpayers, Tax Collectors & Withholding Agents (Updated Up to 1 st July, 2014) Section Provision of the Section Tax Rate deduct / collect / agent 148

Paper F6 (PKN) Taxation (Pakistan) Specimen questions for June Fundamentals Level Skills Module

Taxation (Pakistan) Specimen questions for June Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (Pakistan) Specimen questions for June 2015 Time allowed This Reading is and not planning: a full specimen 15 minutes paper, it is a selection of specimen Writing:

Fundamentals Level Skills Module Taxation (Pakistan) Specimen questions for June 2015 Time allowed This Reading is and not planning: a full specimen 15 minutes paper, it is a selection of specimen Writing:

AFGHANISTAN INCOME TAX LAW

AFGHANISTAN INCOME TAX LAW 2009 An unofficial translation of the Income Tax Law 2009 as published in Official Gazette number 976 dated 18 th March 2009. This translation has been prepared by the Afghanistan

AFGHANISTAN INCOME TAX LAW 2009 An unofficial translation of the Income Tax Law 2009 as published in Official Gazette number 976 dated 18 th March 2009. This translation has been prepared by the Afghanistan

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 8 BUSINESS TAXATION SEMESTER-4

Q. 2 (a) Tax Credit for Investment: SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 8 (1) Where a taxpayer being a company invests any amount in the purchase of plant and machinery, for the purposes of

Q. 2 (a) Tax Credit for Investment: SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 8 (1) Where a taxpayer being a company invests any amount in the purchase of plant and machinery, for the purposes of

Tax in Budget Finance Bill Income Tax Changes only! For the use of Clients & Staff Only.

Tax in Budget 2015 Finance Bill 2015 Income Tax Changes only! For the use of Clients & Staff Only. 2015 A. Salam Jan & Co. Chartered Accountants Member of AFFILICA International-UK. TABLE OF CONTENTS Foreword.

Tax in Budget 2015 Finance Bill 2015 Income Tax Changes only! For the use of Clients & Staff Only. 2015 A. Salam Jan & Co. Chartered Accountants Member of AFFILICA International-UK. TABLE OF CONTENTS Foreword.

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Income Tax Rules, 2002 Table of Contents

2009 2010 Income Tax Rules, 2002 Table of Contents CHAPTER I Rule Subject Page No. No. 1 Short title and commencement. 1 2 Definition. 1 CHAPTER II Determination Of Income - Heads of Income Part I Salary

2009 2010 Income Tax Rules, 2002 Table of Contents CHAPTER I Rule Subject Page No. No. 1 Short title and commencement. 1 2 Definition. 1 CHAPTER II Determination Of Income - Heads of Income Part I Salary

FORM NO. 2 [See rule 12(1)(b)(i) of Income-tax Rules,1962]

![FORM NO. 2 [See rule 12(1)(b)(i) of Income-tax Rules,1962]](/thumbs/75/72089576.jpg "FORM NO. 2 [See rule 12(1)(b)(i) of Income-tax Rules,1962]") FORM NO. 2 [See rule 12(1)(i) of Income-tax Rules,1962] RETURN OF INCOME SARAL ITS-2 For Non-Corporate assessees not claiming exemption u/s 11 and having income from ACKNOWLEDGEMENT business or profession)

FORM NO. 2 [See rule 12(1)(i) of Income-tax Rules,1962] RETURN OF INCOME SARAL ITS-2 For Non-Corporate assessees not claiming exemption u/s 11 and having income from ACKNOWLEDGEMENT business or profession)

A23 A24 A25 A26 B1 B2 B3 B5 In response to notice under section In response to notice under section 153A/ 153C 7 In pursuance of an order of the

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

April 9, 2018 Memorandum on Tax Reforms Package

April 9, 2018 Memorandum on Tax Reforms Package Chartered Accountants a member firm of the PwC network MEMORANDUM ON TAX REFORMS PACKAGE Preamble The Prime Minister of Pakistan announced salient features

April 9, 2018 Memorandum on Tax Reforms Package Chartered Accountants a member firm of the PwC network MEMORANDUM ON TAX REFORMS PACKAGE Preamble The Prime Minister of Pakistan announced salient features

CHAPTER 9 WITHHOLDING TAX RATES

CHPTER 9 WITHHOLDING TX RTES Section Nature of Payment/Transaction 148 Imports 5.00% Import of Items mentioned in Cl 9, P II, 2nd Sch, Cl 13E, P II, 2nd Sch, Cl 13G P II, 2nd Sch (Gold, Silver & Mobile

CHPTER 9 WITHHOLDING TX RTES Section Nature of Payment/Transaction 148 Imports 5.00% Import of Items mentioned in Cl 9, P II, 2nd Sch, Cl 13E, P II, 2nd Sch, Cl 13G P II, 2nd Sch (Gold, Silver & Mobile

Tax in Budget A. Salam Jan & Co. Chartered Accountants a member of AFFILICA International - UK

ASC Tax in Budget - 2017 A. Salam Jan & Co. Chartered Accountants a member of AFFILICA International - UK TABLE OF CONTENTS Foreword 1 Summary of Significant changes in Income tax law 2 Tax Rate Card for

ASC Tax in Budget - 2017 A. Salam Jan & Co. Chartered Accountants a member of AFFILICA International - UK TABLE OF CONTENTS Foreword 1 Summary of Significant changes in Income tax law 2 Tax Rate Card for

FA Fakhri Associates. Accounts, Income Tax & Sales Tax Consultant

4B Super tax for rehabilitation of temporarily displaced persons. 1 A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax year 2015 and 2016, at the rates specified

4B Super tax for rehabilitation of temporarily displaced persons. 1 A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax year 2015 and 2016, at the rates specified

THE BALOCHISTAN GAZETTE PUBLISHED BY THE AUTHORITY NO... QUETTA... GOVERNMENT OF BALOCHISTAN BALOCHISTAN REVENUE AUTHORITY

1 EXTRAORDINARY REGISTERED NO.. THE BALOCHISTAN GAZETTE PUBLISHED BY THE AUTHORITY NO... QUETTA... GOVERNMENT OF BALOCHISTAN BALOCHISTAN REVENUE AUTHORITY THE BALOCHISTAN SALES TAX SPECIAL PROCEDURE (WITHHOLDING)

1 EXTRAORDINARY REGISTERED NO.. THE BALOCHISTAN GAZETTE PUBLISHED BY THE AUTHORITY NO... QUETTA... GOVERNMENT OF BALOCHISTAN BALOCHISTAN REVENUE AUTHORITY THE BALOCHISTAN SALES TAX SPECIAL PROCEDURE (WITHHOLDING)

Paper F6 (PKN) Taxation (Pakistan) Thursday 10 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Pakistan) Thursday 10 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Pakistan) Thursday 10 December 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section A

Fundamentals Level Skills Module Taxation (Pakistan) Thursday 10 December 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section A

Composed & Solved Askari Team Vu Askari Team FIN623 Online Quiz#5 Lecture#1 to 42.. Solved By Askari Team..

Vu FIN623 Online Quiz#5 Lecture#1 to 42.. Solved By.. Question # 1 of 15 ( Start time: 02:32:45 AM ) Total Marks: 1 If an employee s taxable income is Rs.715, 000 and he paid donations amounting Rs. 10,000

Vu FIN623 Online Quiz#5 Lecture#1 to 42.. Solved By.. Question # 1 of 15 ( Start time: 02:32:45 AM ) Total Marks: 1 If an employee s taxable income is Rs.715, 000 and he paid donations amounting Rs. 10,000

Accredited Accounting Technician Examination

Accredited Accounting Technician Examination Pilot Examination Paper Paper 5 Principles of Taxation Questions & Answers Booklet The Suggested Answers given in this booklet are purposely made to give more

Accredited Accounting Technician Examination Pilot Examination Paper Paper 5 Principles of Taxation Questions & Answers Booklet The Suggested Answers given in this booklet are purposely made to give more

EUS EXECUTIVE UPDATING SERVICE Updating Acts, Ordinances, Statutory Rules & Orders (SROs.) etc.

etc.") EUS EXECUTIVE UPDATING SERVICE Updating Acts, Ordinances, Statutory Rules & Orders (SROs.) etc. III-H 11/21 NAZIMABAD Ph: (92-21) 3662 0242-3 For EUS Clients Use Only EUS UPDATE ADVANCE TAX PAID BY THE

EUS EXECUTIVE UPDATING SERVICE Updating Acts, Ordinances, Statutory Rules & Orders (SROs.) etc. III-H 11/21 NAZIMABAD Ph: (92-21) 3662 0242-3 For EUS Clients Use Only EUS UPDATE ADVANCE TAX PAID BY THE

Instructions for SUGAM Income Tax Return AY

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-4 SUGAM A.Y

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Tax Index of Financial Data

Tax Index of Financial Data Please input: Year of Assessment Reference number: Company Name:. of Trading Activities: Balance Sheet Income Statement Validations All mandatory fields present and correct?

Tax Index of Financial Data Please input: Year of Assessment Reference number: Company Name:. of Trading Activities: Balance Sheet Income Statement Validations All mandatory fields present and correct?

FORM NO. 3A RETURN OF INCOME

FORM NO. 3A RETURN OF INCOME INCOME-TAX ACT, 1961 [See RULE 12(1)(C)] [For assessees including companies claiming exemption under section 11. All Parts and Annexures must be filled in. If any Part or Annexure

FORM NO. 3A RETURN OF INCOME INCOME-TAX ACT, 1961 [See RULE 12(1)(C)] [For assessees including companies claiming exemption under section 11. All Parts and Annexures must be filled in. If any Part or Annexure

Elgi Compressors Italy S.r.l. Balance Sheet As At 31st March 2017

Balance Sheet As At 31st March 2017 Particulars Note March 31, 2017 March 31, 2016 Non Current Assets Property, Plant and Equipment 3 127,486,695 145,048,621 Capital work-in-progress 3 - Investment Property

Balance Sheet As At 31st March 2017 Particulars Note March 31, 2017 March 31, 2016 Non Current Assets Property, Plant and Equipment 3 127,486,695 145,048,621 Capital work-in-progress 3 - Investment Property

I. EQUITY AND LIABILITIES EQUITY Equity Share Capital , ,000 Other Equity 19 1,492,255 26,719

ERGO DESIGN PRIVATE LIMITED Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 639,731 58,912 Capital work-in-progress 3 Investment Property 4 Goodwill 5 Other Intangible

ERGO DESIGN PRIVATE LIMITED Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 639,731 58,912 Capital work-in-progress 3 Investment Property 4 Goodwill 5 Other Intangible

Fundamentals Level Skills Module, Paper F6 (PKN)

") Answers Fundamentals Level Skills Module, Paper F6 (PKN) Taxation (Pakistan) June 2012 Answers and Marking Scheme Notes: 1. The suggested answers provide detailed guidance on the subject for use as a study

Answers Fundamentals Level Skills Module, Paper F6 (PKN) Taxation (Pakistan) June 2012 Answers and Marking Scheme Notes: 1. The suggested answers provide detailed guidance on the subject for use as a study

Notes on clauses.

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

KPMG Taseer Hadi & Co. Chartered Accountants. Commentary on Finance Act, 2016

KPMG Taseer Hadi & Co. Chartered Accountants Commentary on Finance Act, 2016 The Budget Brief 2016 contained a review of economic scenario and highlights of Finance Bill 2016 as related to direct and indirect

KPMG Taseer Hadi & Co. Chartered Accountants Commentary on Finance Act, 2016 The Budget Brief 2016 contained a review of economic scenario and highlights of Finance Bill 2016 as related to direct and indirect

SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 7 BUSINESS TAXATION [G5] GRADUATION LEVEL

![SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 7 BUSINESS TAXATION [G5] GRADUATION LEVEL](/thumbs/79/80010862.jpg "SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 7 BUSINESS TAXATION [G5] GRADUATION LEVEL") + Question No. 2 SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 7 (a) Association of Persons (AOPs): 05 Association of persons includes a firm, a Hindu undivided family, any artificial juridical

+ Question No. 2 SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 7 (a) Association of Persons (AOPs): 05 Association of persons includes a firm, a Hindu undivided family, any artificial juridical

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION 1. NATURE OF INCOME :- Such Income Includes income from: - Business, Vocation and Profession carried on by the

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION 1. NATURE OF INCOME :- Such Income Includes income from: - Business, Vocation and Profession carried on by the

Articles Orientation Programme. The Chamber of Tax Consultants. By CA Amit Purohit. Coverage. Overview of Section 44 AB and its applicability

Articles Orientation Programme The Chamber of Tax Consultants By CA Amit Purohit Purpose of Tax audit Coverage Approaching Tax Audit Overview of Section 44 AB and its applicability Audit report applicability

Articles Orientation Programme The Chamber of Tax Consultants By CA Amit Purohit Purpose of Tax audit Coverage Approaching Tax Audit Overview of Section 44 AB and its applicability Audit report applicability

MTP_ Inter _Syllabus 2016_ June 2018_Set 1 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Fundamentals Level Skills Module, Paper F6 (PKN)

") Answers Fundamentals Level Skills Module, Paper F6 (PKN) Taxation (Pakistan) December 2013 Answers and Marking Scheme Notes: 1. The suggested answers provide detailed guidance on the subject for use as

Answers Fundamentals Level Skills Module, Paper F6 (PKN) Taxation (Pakistan) December 2013 Answers and Marking Scheme Notes: 1. The suggested answers provide detailed guidance on the subject for use as

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

ALBANIA TAX CARD 2017

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

Rates for Withholding (Income) Tax, Updated to the Effect of Proposed Changes vide the Finance Bill, 2016 APPLICABLE FOR TAX YEAR 2017

Tax, Updated to the Effect of Proposed Changes vide the Finance Bill, 2016 APPLICABLE FOR TAX YEAR 2017") DIVIDEND, INCLUDING DIVIDEND IN SPECIE [Section 150, 236S, Division I Part III First Schedule & Clause 11B Part IV Second Schedule] Dividends from privatized power projects or companies set up for power

DIVIDEND, INCLUDING DIVIDEND IN SPECIE [Section 150, 236S, Division I Part III First Schedule & Clause 11B Part IV Second Schedule] Dividends from privatized power projects or companies set up for power

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

1. In this Act "the Principal Act" means the Value-Added Tax Act, Section 1 of the Principal Act is hereby amended by

VALUE-ADDED TAX (AMENDMENT) ACT 1978 VALUE-ADDED TAX (AMENDMENT) ACT 1978 - LONG TITLE AN ACT TO AMEND THE VALUE-ADDED TAX ACT, 1972, AND THE ACTS AMENDING THAT ACT AND TO PROVIDE FOR RELATED MATTERS.

VALUE-ADDED TAX (AMENDMENT) ACT 1978 VALUE-ADDED TAX (AMENDMENT) ACT 1978 - LONG TITLE AN ACT TO AMEND THE VALUE-ADDED TAX ACT, 1972, AND THE ACTS AMENDING THAT ACT AND TO PROVIDE FOR RELATED MATTERS.

ITS-2F [See rule 12] RETURN OF INCOME ASSESSMENT YEAR FORM No. 2F. Printed from Taxmann s Income-tax Rules on CD Page 1 of 8

![ITS-2F [See rule 12] RETURN OF INCOME ASSESSMENT YEAR FORM No. 2F. Printed from Taxmann s Income-tax Rules on CD Page 1 of 8](/thumbs/90/102199847.jpg "ITS-2F [See rule 12] RETURN OF INCOME ASSESSMENT YEAR FORM No. 2F. Printed from Taxmann s Income-tax Rules on CD Page 1 of 8") ,,,,,,,, This Form may be used only by assessees being resident individual/hindu undivided family (HUF) (a) not having income from business or profession or agricultural income or capital gains (except

,,,,,,,, This Form may be used only by assessees being resident individual/hindu undivided family (HUF) (a) not having income from business or profession or agricultural income or capital gains (except

FINANCE BILL HIGHLIGHTS- 2017

1 FEDERAL BUDGET 2017 This memorandum has drafted to portray the significant changes which have been proposed to be incorporated in Finance Bill 2017. These changes are mainly relating to Income Tax, Sales

1 FEDERAL BUDGET 2017 This memorandum has drafted to portray the significant changes which have been proposed to be incorporated in Finance Bill 2017. These changes are mainly relating to Income Tax, Sales

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962]

![FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962]](/thumbs/89/98100419.jpg "FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962]") FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962] RETURN OF INCOME SARAL ITS-3 (For Non-Corporate assessees not claiming exemption u/s 11 and not having income from ACKNOWLEDGEMENT business

FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962] RETURN OF INCOME SARAL ITS-3 (For Non-Corporate assessees not claiming exemption u/s 11 and not having income from ACKNOWLEDGEMENT business

KPMG Taseer Hadi & Co. Chartered Accountants. Amendments through Finance Act 2017

KPMG Taseer Hadi & Co. Chartered Accountants Amendments through Finance Act 2017 The amendments proposed by Finance Bill, 2017 have now been enacted through Finance Act, 2017 with changes made in some

KPMG Taseer Hadi & Co. Chartered Accountants Amendments through Finance Act 2017 The amendments proposed by Finance Bill, 2017 have now been enacted through Finance Act, 2017 with changes made in some

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

FINANCIAL STATEMENT (Long Form)

") Division Commonwealth of Massachusetts The Trial Court Probate and Family Court Department FINANCIAL STATEMENT (Long Form) INSTRUCTIONS: If your income is less than 75,000.00 annually, you must complete

Division Commonwealth of Massachusetts The Trial Court Probate and Family Court Department FINANCIAL STATEMENT (Long Form) INSTRUCTIONS: If your income is less than 75,000.00 annually, you must complete

BILL. to give effect to the financial proposals of the Federal Government for the year

Finance Bill 2009 A BILL to give effect to the financial proposals of the Federal Government for the year beginning on the first day of July, 2009, and to amend certain laws WHEREAS it is expedient to

Finance Bill 2009 A BILL to give effect to the financial proposals of the Federal Government for the year beginning on the first day of July, 2009, and to amend certain laws WHEREAS it is expedient to

Syllabus CAF-6 OF ICAP

Syllabus CAF-6 OF ICAP Objective The aim of this paper is to develop basic knowledge and understanding in the core areas of Income Tax and its chargeability as envisaged in the Income Tax Ordinance 2001

Syllabus CAF-6 OF ICAP Objective The aim of this paper is to develop basic knowledge and understanding in the core areas of Income Tax and its chargeability as envisaged in the Income Tax Ordinance 2001

I. EQUITY AND LIABILITIES EQUITY Equity Share Capital ,061, ,061,139 Other Equity 19 (223,428,513) (199,234,465)

(199,234,465)") ELGI COMPRESSORES DO BRASIL IMPORTADORA E EXPORTADORA LTDA. Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 3,985,033 4,560,869 Capital work-in-progress 3 Investment Property

ELGI COMPRESSORES DO BRASIL IMPORTADORA E EXPORTADORA LTDA. Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 3,985,033 4,560,869 Capital work-in-progress 3 Investment Property

Instructions for filling out FORM ITR-3

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Circular The Schedule of dates for filing income-tax returns is given below:

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Fundamentals Level Skills Module, Paper F6 (PKN)

") Answers Fundamentals Level Skills Module, Paper F6 (PKN) Taxation (Pakistan) December 2016 Answers and Marking Scheme Note: All references to legislation shown in square brackets are for information only

Answers Fundamentals Level Skills Module, Paper F6 (PKN) Taxation (Pakistan) December 2016 Answers and Marking Scheme Note: All references to legislation shown in square brackets are for information only

PAYMENT OF ADVANCE TAX U/S 147 AND SAIDUDDIN & CO. TAXABILITY OF PROPERTY INCOME UNDER THE INCOME TAX ORDINANCE, 2001

PAYMENT OF ADVANCE TAX U/S 147 AND TAXABILITY OF PROPERTY INCOME UNDER THE INCOME TAX ORDINANCE, 2001 SAIDUDDIN & CO. ADVOCATES TAXATION, MANAGEMENT & COMPANY LAW CONSULTANTS PRESENTATION OVERVIEW The

PAYMENT OF ADVANCE TAX U/S 147 AND TAXABILITY OF PROPERTY INCOME UNDER THE INCOME TAX ORDINANCE, 2001 SAIDUDDIN & CO. ADVOCATES TAXATION, MANAGEMENT & COMPANY LAW CONSULTANTS PRESENTATION OVERVIEW The

KPMG Taseer Hadi & Co. Chartered Accountants. Amendments through Finance Act 2018

KPMG Taseer Hadi & Co. Chartered Accountants Amendments through Finance Act 2018 The amendments proposed by Finance Bill, 2018 have now been enacted through Finance Act, 2018 with changes made in some

KPMG Taseer Hadi & Co. Chartered Accountants Amendments through Finance Act 2018 The amendments proposed by Finance Bill, 2018 have now been enacted through Finance Act, 2018 with changes made in some

FORM NO. 3CD. Statement of particulars required to be furnished under section 44AB of the Income-tax Act, 1961 PART B.

FORM NO. 3CD [See rule 6G(2)] Statement of particulars required to be furnished under section 44AB of the Income-tax Act, 1961 PART A 1. Name of the assessee : 2. Address : 3. Permanent Account Number

FORM NO. 3CD [See rule 6G(2)] Statement of particulars required to be furnished under section 44AB of the Income-tax Act, 1961 PART A 1. Name of the assessee : 2. Address : 3. Permanent Account Number

Elgi Compressors Europe S.r.l. Balance Sheet As At 31st March, 2018 Particulars Note March 31, 2018 March 31, 2017

Balance Sheet As At 31st March, 2018 Particulars Note March 31, 2018 March 31, 2017 Non Current Assets Property, Plant and Equipment 3 144,494,837 127,486,695 Capital workinprogress 3 Investment Property

Balance Sheet As At 31st March, 2018 Particulars Note March 31, 2018 March 31, 2017 Non Current Assets Property, Plant and Equipment 3 144,494,837 127,486,695 Capital workinprogress 3 Investment Property

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

Paper F6 (PKN) Taxation (Pakistan) Tuesday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Pakistan) Tuesday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Pakistan) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (Pakistan) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Hong Kong. Investment basics. Currency Hong Kong Dollar (HKD) Foreign exchange control

Foreign exchange control") Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

Self FORM OF RETURN OF INCOME UNDER THE INCOME TAX ORDINANCE, 1984 (XXXVI OF 1984) PART-I

PART-I") Submit return in due time Avoid penalty Put the tick ( ) mark wherever applicable Self FORM OF RETURN OF INCOME UNDER THE INCOME TAX ORDINANCE, 1984 (XXXVI OF 1984) IT-11GA Normal Photograph of the Assessee

Submit return in due time Avoid penalty Put the tick ( ) mark wherever applicable Self FORM OF RETURN OF INCOME UNDER THE INCOME TAX ORDINANCE, 1984 (XXXVI OF 1984) IT-11GA Normal Photograph of the Assessee

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

Tax on. Salary. Income Tax Law & Calculation

Tax on 2018 Salary This tax guide is for the use of CLIENTS and STAFF only and covers the taxability aspects of the salary as per Pakistani income tax laws applicable to Tax Year 2018 Income Tax Law &

Tax on 2018 Salary This tax guide is for the use of CLIENTS and STAFF only and covers the taxability aspects of the salary as per Pakistani income tax laws applicable to Tax Year 2018 Income Tax Law &

PROFESSIONAL DEVELOPMENT PROGRAM 2015 (PDP) By:

By:") PROFESSIONAL DEVELOPMENT PROGRAM 2015 (PDP) By: MUHAMMAD ZEESHAN MERCHANT M. M. MERCHANT & COMPANY (Advocate High Court & Former Honorary General Secretary, Karachi Tax Bar Association) Suite No No..4,

PROFESSIONAL DEVELOPMENT PROGRAM 2015 (PDP) By: MUHAMMAD ZEESHAN MERCHANT M. M. MERCHANT & COMPANY (Advocate High Court & Former Honorary General Secretary, Karachi Tax Bar Association) Suite No No..4,

GREECE Agreement for avoidance of double taxation with Greece Whereas the annexed Agreement between the Government of India and the Government of

GREECE Agreement for avoidance of double taxation with Greece Whereas the annexed Agreement between the Government of India and the Government of Greece for the avoidance of double taxation of income has

GREECE Agreement for avoidance of double taxation with Greece Whereas the annexed Agreement between the Government of India and the Government of Greece for the avoidance of double taxation of income has

ILYAS SAEED & Co Chartered Accountants

Chartered Accountants CONTENTS Page SRO 487(I)/2006, dated June 30, 2016... 3 Exemption from Further Tax... 3 SRO 488(I)/2006, dated June 30, 2016... 3 Amendment in Special Procedure Rules... 3 Sales Tax

Chartered Accountants CONTENTS Page SRO 487(I)/2006, dated June 30, 2016... 3 Exemption from Further Tax... 3 SRO 488(I)/2006, dated June 30, 2016... 3 Amendment in Special Procedure Rules... 3 Sales Tax

GOVERNMENT OF PAKISTAN CENTRAL BOARD OF REVENUE. C.No.1-167(I) ITP/97 Islamabad, the 15th July, 1997 CIRCULAR NO. 6 OF 1997 (INCOME TAX)

ITP/97 Islamabad, the 15th July, 1997 CIRCULAR NO. 6 OF 1997 (INCOME TAX)") GOVERNMENT OF PAKISTAN CENTRAL BOARD OF REVENUE C.No.1-167(I) ITP/97 Islamabad, the 15th July, 1997 CIRCULAR NO. 6 OF 1997 (INCOME TAX) SUBJECT: FINANCE SUPPLEMENTARY (AMENDMENT) ACT, 1997 AND FINANCE

GOVERNMENT OF PAKISTAN CENTRAL BOARD OF REVENUE C.No.1-167(I) ITP/97 Islamabad, the 15th July, 1997 CIRCULAR NO. 6 OF 1997 (INCOME TAX) SUBJECT: FINANCE SUPPLEMENTARY (AMENDMENT) ACT, 1997 AND FINANCE

Question 1. The Institute of Chartered Accountants of India

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

SUGGESTED SOLUTIONS/ ANSWERS FALL 2017 EXAMINATIONS 1 of 8 BUSINESS TAXATION [G5] GRADUATION LEVEL

![SUGGESTED SOLUTIONS/ ANSWERS FALL 2017 EXAMINATIONS 1 of 8 BUSINESS TAXATION [G5] GRADUATION LEVEL](/thumbs/91/106390495.jpg "SUGGESTED SOLUTIONS/ ANSWERS FALL 2017 EXAMINATIONS 1 of 8 BUSINESS TAXATION [G5] GRADUATION LEVEL") Question No. 2 (a) (i) Definite Information: SUGGESTED SOLUTIONS/ ANSWERS FALL 2017 EXAMINATIONS 1 of 8 Definite information includes information on sales or purchases of any goods made by the taxpayer,

Question No. 2 (a) (i) Definite Information: SUGGESTED SOLUTIONS/ ANSWERS FALL 2017 EXAMINATIONS 1 of 8 Definite information includes information on sales or purchases of any goods made by the taxpayer,

Chapter 16 Indirect Taxation

Chapter 16 Indirect Taxation www.pwc.com/mt/doingbusiness Doing Business in Malta INDIRECT TAXES IN MALTA Value added tax (VAT) is charged on supplies of goods and services made in Malta, on intra-community

Chapter 16 Indirect Taxation www.pwc.com/mt/doingbusiness Doing Business in Malta INDIRECT TAXES IN MALTA Value added tax (VAT) is charged on supplies of goods and services made in Malta, on intra-community

Federal Budget Seminar

Federal Budget Seminar 2013-14 Pakistan Society of Human Resource Management Saqib Masood Partner / Head of Tax Services KPMG Taseer Hadi & Co. Karachi 05 July 2013 Salary Taxation Tax rate slabs enhanced